Embed Size (px)

Citation preview

1

2012 Massachusetts Investor

Conference

Thursday, December 13,

2012

2

Disclaimer This investor presentation is provided for your general information and convenience only and does not constitute an offer to sell or a

solicitation of an offer to buy securities. The information contained herein does not constitute a sufficient basis for making a decision with

respect to the purchase or sale of any security, and is not intended to constitute investment advice of any kind.

All information regarding or relating to bonds issued or to be issued by the Commonwealth of Massachusetts, the Massachusetts Bay

Transportation Authority, the Massachusetts Port Authority, the Massachusetts Water Pollution Abatement Trust, the Massachusetts

Water Resources Authority, the University of Massachusetts Building Authority, the Massachusetts State College Building Authority, the

Massachusetts Housing Finance Agency, Massachusetts Department of Transportation, the Massachusetts School Building Authority, the

Massachusetts Development Finance Agency, or the Massachusetts Educational Financing Authority (the “Issuers”) is qualified in its

entirety by the applicable Official Statement and any related primary and continuing disclosure documents and filings, all of which

documents and filings should be reviewed before any investment decision is made with respect to any such bonds.

With respect to each Issuer’s section of this investor presentation, such section has been furnished by such Issuer and includes

information obtained from other sources that are believed by such Issuer to be reliable, but is not guaranteed as to accuracy or

completeness. The information and expressions of opinion contained in this investor presentation are subject to change without notice.

The information contained in this investor presentation speaks only as of the date such information was prepared and has not been

updated since that date. Accordingly, such information may not address all factors which may be material to an investor and may contain

omissions of fact or statements that are not accurate because of the passage of time or changes in facts or circumstances subsequent to

the date of such information. The Issuers are under no obligation to update any of the information set forth in this investor presentation.

None of the Issuers or their respective representatives or agents, including any underwriters of bonds issued or to be issued by any of the

Issuers, shall have any liability whatsoever in negligence or otherwise for any loss however arising from any use of this investor

presentation or its contents or otherwise arising in connection with this investor presentation.

No dealer, broker, salesperson or any other person has been authorized by any of the Issuers to give any information or to make any

representation in connection with the Issuers or any bonds of any of the Issuers, and, if given or made, such other information or

representation must not be relied upon as having been authorized by any of the Issuers.

This investor presentation includes forward-looking statements based on current beliefs and expectations about future events. Forward-

looking statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives

and expectations with respect to future events. Forward-looking statements are not guarantees of future performance and are subject to

inherent risks, uncertainties and assumptions about the Issuers, changes in economic conditions globally, nationally or in Massachusetts,

and political and regulatory factors. Those events are uncertain; their outcome may differ from current expectations, which may in turn

significantly affect expected results. Actual results may differ materially from those projected or implied in these forward-looking

statements. Any forward-looking statement contained in this investor presentation speaks as of the date of this presentation. The Issuers

undertake no obligation to publicly revise or update any forward-looking statements in light of new information or future events.

2012 Massachusetts Investor Conference

3

Agenda

2012 Massachusetts Investor Conference

Time Presentation Presenter(s) 7:30 - 8:00 Registration & Breakfast --

8:00 - 8:30 Conference Welcome Honorable Deval L. Patrick, Governor of Massachusetts

8:30 - 9:00 Update on the Commonwealth Honorable Steven Grossman, State Treasurer

9:00 - 9:30 Presentation: “The Massachusetts Economy: A

Long-Term Perspective”

Alan Clayton-Matthews, MassBenchmarks & Northeastern

University

9:30 - 10:00 Credit Panel: Water: Mass. Water Resources

Authority, Mass. Water Pollution Abatement Trust

Fred Laskey & Rachel Madden, MWRA; Sue Perez, Steve

McCurdy & Drew Smith, MWPAT

10:00 - 10:15 Break / Coffee

10:15 - 11:00 Credit Panel: Education: Mass. School Building

Authority, Mass. State College Building Authority,

UMass Building Authority

Vin Alabiso, MSBA; Edward Adelman, MSCBA; Katherine

Craven, UMBA

11:00 - 11:45 Investor Roundtable Panel Chris Alwine, Vanguard

11:45 - 12:45 LUNCH & Presentation John Cross, Securities & Exchange Commission

12:45 - 1:30 Credit Panel: The Commonwealth of Massachusetts

Secretary of Administration & Finance, Jay Gonzalez;

Colin MacNaught, State Treasurer’s Office

1:30 - 2:15 2013 Market Outlook Tom Doe, Municipal Market Advisors

2:15 - 2:30 Break/Coffee

2:30 - 3:15 Credit Panel: Transportation: MassDOT & MassPort Dana Levenson, MassDOT;

John Pranckevicius & Betsy Taylor, MassPort

3:15 - 3:45 Updates to the EMMA System Justin Pica & Ritta McLauglin, MSRB

3:45 – 4:15 Credit Panel: Economic Development:

MassDevelopment, MassHousing

Steve Chilton, MDFA; Charles Karimbakas, MHFA

4

Table of Contents

2012 Massachusetts Investor Conference

Section Page

“The Massachusetts Economy: A Long-Term Perspective” 7

Massachusetts Water Resources Authority 18

Massachusetts Water Pollution Abatement Trust 46

Massachusetts School Building Authority 61

Massachusetts State College Building Authority 85

University of Massachusetts Building Authority 97

The Commonwealth of Massachusetts 111

2013 Market Outlook 144

Massachusetts Department of Transportation 169

Massachusetts Port Authority 180

Updates to the EMMA System 195

Massachusetts Development Finance Agency 229

Massachusetts Finance Housing Agency 238

5

2012 Massachusetts Investor Conference

Conference Welcome

Honorable Deval L. Patrick

Governor of Massachusetts

Presented by:

6

2012 Massachusetts Investor Conference

Update on the Commonwealth

Treasurer Steven Grossman

Presented by:

7

2012 Massachusetts Investor Conference

The Massachusetts Economy:

A Long-Term Perspective

Alan Clayton-Matthews

Northeastern University

December 13, 2012

Presented by:

8

Massachusetts has out-performed the nation in the recession

and the recovery to date.

4.3

1.9

3.7 3.6

-0.8

2.7

2.0

5.4

1.9

2.6

2.2

2.4 2.42.3 2.2

2.62.4

0.1

2.5

1.3

4.1

2.0

1.3

2.7

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2010 2011 2012 2013

Qu

arte

rly

Gro

wth

at

An

nu

al R

ate

s (%

)Growth in Real Product, Massachusetts vs. U.S.

Massachusetts U.S.

Source: U.S., Bureau of Economic Analysis; Massachusetts: MassBenchmarks

Projected

9

The state has a slower growing population than the U.S….

-1%

0%

1%

2%

1987 1991 1995 1999 2003 2007 2011 2015 2019

Population Growth, Massachusetts versus U.S., Annual Rate

Massachusetts U.S.

Source: Census Bureau History, Global Insight Forecast

10

…and slower-growing employment.

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

1987 1991 1995 1999 2003 2007 2011 2015 2019

Employment Growth, Massachusetts versus U.S., from Same Quarter Prior Year

Massachusetts U.S.

Source: BLS History, Global Insight Forecast

11

However, output growth often matches or exceeds that of the

U.S….

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

1987 1991 1995 1999 2003 2007 2011 2015 2019

Real GDP Growth, Massachusetts versus U.S., from Same Quarter Prior Year

Massachusetts U.S.

Source: BEA History, Global Insight Forecast

Massachusetts history interpolated from annual data by Global Insight

12

… and over the long-term, U.S. and state output growth has been virtually

identical; and is expected to equal that of the U.S. over the next 10 years.

50

60

70

80

90

100

110

120

130

140

150

1987 1991 1995 1999 2003 2007 2011 2015 2019

Real Gross Domestic Product, Massachusetts versus U.S., 2005=100

Massachusetts U.S.

Source: BEA History, Global Insight Forecast

Massachusetts history interpolated from annual data by Global Insight

13

How is this possible? Because of faster productivity growth.

0%

1%

2%

3%

4%

1993 1996 1999 2002 2005 2008 2011 2014 2017 2020

Productivity Growth, Massachusetts versus U.S., Annual Rate, Centered 5-Year Centered Moving Average

Massachusetts U.S.

Source: BEA and BLS History, Global Insight Forecast

Productivity is Real GDP per Non-Farm Payroll Job

14

Higher productivity means higher incomes.

$-

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

1987 1991 1995 1999 2003 2007 2011 2015 2019

Per Capita Personal Income, Massachusetts versus U.S.

Massachusetts U.S.

Source: BEA History, Global Insight Forecast

15

Faster productivity growth results in faster-growing incomes.

100%

105%

110%

115%

120%

125%

130%

135%

1987 1991 1995 1999 2003 2007 2011 2015 2019

Ratio of Massachusetts to U.S. Per Capita Personal Income

Source: BEA History, Global Insight Forecast

16

The basis of the state’s economic performance is its highly-

educated workforce…

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

25 30 35 40 45 50 55 60 65

Age

Percent of Persons 25 and Older with a BA or Higher Degree, by Age, 2009

Massachusetts U.S.

Source: American Community Survey, 2009 PUMS

17

...especially at the high end, which gives Massachusetts a

powerful comparative advantage in the global economy.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

25 30 35 40 45 50 55 60 65

Age

Percent of Persons 25 and Older with an Advanced Degree, by Age, 2009

Massachusetts U.S.

Source: American Community Survey, 2009 PUMS

18

2012 Massachusetts Investor Conference

Massachusetts Water

Resources Authority

Massachusetts Water Resources Authority:

Frederick A. Laskey, Executive Director

Rachel Madden, Director of Administration and Finance

Thomas Durkin, Treasurer

Presented by:

19

MWRA Service Area

MWRA provides wholesale water and wastewater services to over 2.5 million customers in 61 communities

On average, MWRA delivers 200 million gallons per day to its water customers

MWRA collects and treats an average of 350 million gallons of wastewater per day, with a peak capacity of 1.2 billion gallons

2012 Massachusetts Investor Conference

20

MWRA Has Spent $7.1 Billion To Rebuild The Water And Sewer Systems

Boston Harbor Project

MetroWest Supply Tunnel Hultman Aqueduct Rehab Spot Pond Supply Mains

Braintree-Weymouth Relief Facilities

Norumbega Covered Storage

Weston Aqueduct Supply Mains

Carroll Water Treatment Plant UV Treatment

Union Park

East Boston Branch Sewer

North Dorchester Bay CSO

Community Managed CSO Projects

Deer Island Asset Protection

$0

$100

$200

$300

$400

$500

$600

$700

$ M

illio

ns

Actual Projected

2012 Massachusetts Investor Conference

21

Over 80% Of Spending Has Been For Mandated Projects

$0

$100

$200

$300

$400

$500

$600

$700

FY86 FY88 FY90 FY92 FY94 FY96 FY98 FY00 FY02 FY04 FY06 FY08 FY10 FY12

Mill

ions

Mandated(Court Orders, Consent Orders)

Non-Mandated(Pipeline Rehabilitation and Infrastructure Replacement)

2012 Massachusetts Investor Conference

22

MWRA’s Capital Finance Program

As of June 30, 2012, MWRA had approximately $5.94 billion in debt:

Senior Lien General $3.49 Multi-Modal

Subordinated $1.19

Mass WPAT$1.12

TECP$0.14

2012 Massachusetts Investor Conference

23

MWRA’s Capital Finance Program

MWRA’s Credit Ratings were most recently affirmed in November 2012:

Moody's Standard and Poor's FitchRatings

Senior – Aa1 Senior – AA+ Senior – AA+

Subordinate – Aa2 Subordinate - AA Subordinate – AA

2012 Massachusetts Investor Conference

24

An Environmental Success Story

In 2002, $3.8 billion Boston Harbor Project was completed

About 350 million gallons of wastewater is treated at the new Deer Island Treatment plant every day

Treated wastewater is discharged 9.5 miles out into the deeper waters of Massachusetts Bay

Sludge is transported to Quincy where it is recycled into fertilizer

2012 Massachusetts Investor Conference

25

Dramatic Improvements In Water Quality – Even In Wet Weather

Average Enterococcus counts in Boston Harbor in wet weather

The lighter the blue, the better

1987-1998 (Before Secondary Treatment

and South System transfer)

1999 - 2011 (After Secondary Treatment

and New Outfall)

1999 - 2011 1987 - 1991

2012 Massachusetts Investor Conference

26

Combined Sewer Overflow Control Program

Four communities - Boston,

Brookline, Cambridge,

Chelsea and Somerville -

have combined sewer

systems that connect to

MWRA's sewer system

Boston Harbor, the

Charles, the Mystic and the

Neponset Rivers are

subject to overflows of

combined stormwater and

sewage during heavy rains

2012 Massachusetts Investor Conference

27

Annual CSO Volume Has Been Reduced Dramatically

0

0.5

1

1.5

2

2.5

3

3.5

1988 1992 2011 2015

(Billio

n G

allo

ns)

Untreated Treated

• 29 of 35 projects have been completed to date

• Annual CSO volumes have already been reduced by 2.7 billion gallons

• By 2015, 93% of the remaining CSO flows will be treated

6 2012 Massachusetts Investor Conference

28

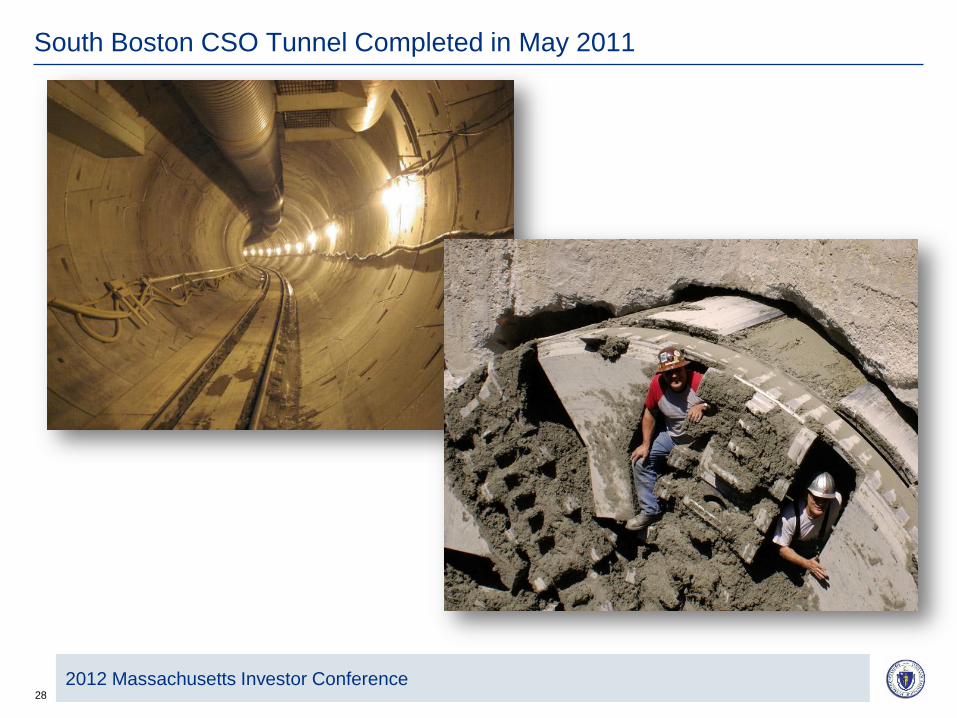

South Boston CSO Tunnel Completed in May 2011

2012 Massachusetts Investor Conference

29

Boston Now Has Some Of The Cleanest Urban Beaches In The Country

2012 Massachusetts Investor Conference

30

The MWRA Water System Has Been Modernized

MetroWest

Water Supply Tunnel

Nash Hill

Loring Road

Fells Spot Pond

Norumbega

CWTP Blue Hills

Pipeline Rehabilitation

Watershed Protection

John J. Carroll

Water Treatment Plant

Quabbin

Water Treatment Plant

2012 Massachusetts Investor Conference

31

John J. Carroll Water Treatment Plant

Complete in July 2005

Treatment Processes:

– Ozonation for primary disinfection

– Corrosion control

– Chloramination for secondary disinfection

– Fluoridation

2012 Massachusetts Investor Conference

32

Carroll Water Treatment Plant UV Disinfection

• Required to meet new federal regulations

• Work is 75% complete

2012 Massachusetts Investor Conference

33

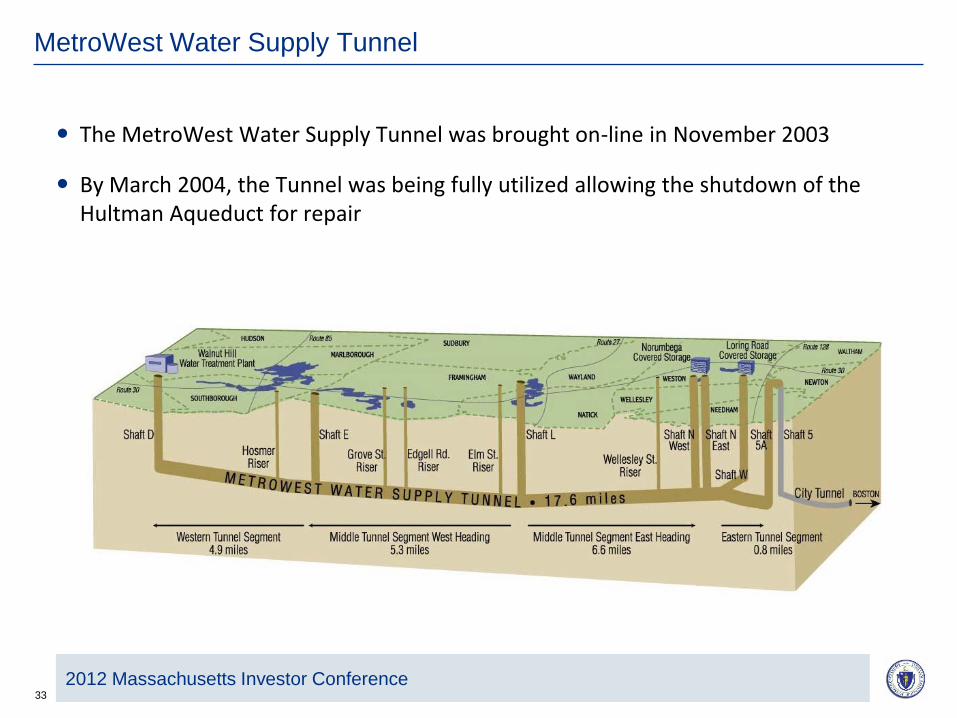

MetroWest Water Supply Tunnel

The MetroWest Water Supply Tunnel was brought on-line in November 2003

By March 2004, the Tunnel was being fully utilized allowing the shutdown of the Hultman Aqueduct for repair

2012 Massachusetts Investor Conference

34

May 1, 2010 Water Main Break

On May 1st, a break occurred on a 10-foot diameter water main in Weston

Use of the emergency water system also triggered a precautionary “boil water order” for 2 million residents in 30 affected communities

The leak was repaired quickly and the system was back to normal in under 72 hours

2012 Massachusetts Investor Conference

35

Hultman Aqueduct Rehabilitation

• Rehabilitation of the 15-mile Hultman Aqueduct is nearly complete

2012 Massachusetts Investor Conference

36

Norumbega Covered Storage Facility

The tank was completed in May 2004

It provides 115 million gallons of storage for metropolitan Boston

2012 Massachusetts Investor Conference

37

Covered Storage Projects

• MWRA is building seven new covered storage tanks to replace all open reservoirs

• Six are completed and on-line

Nash Hill

Loring Road

Fells Spot Pond

Norumbega

Walnut

Hill

Blue Hills

2012 Massachusetts Investor Conference

38

Spot Pond Storage Facility

20-million-gallon buried water tank currently under construction

Buried emergency pump station will provide redundancy 21 communities

2012 Massachusetts Investor Conference

39

Drinking Water Quality Is Excellent

2012 Massachusetts Investor Conference

40

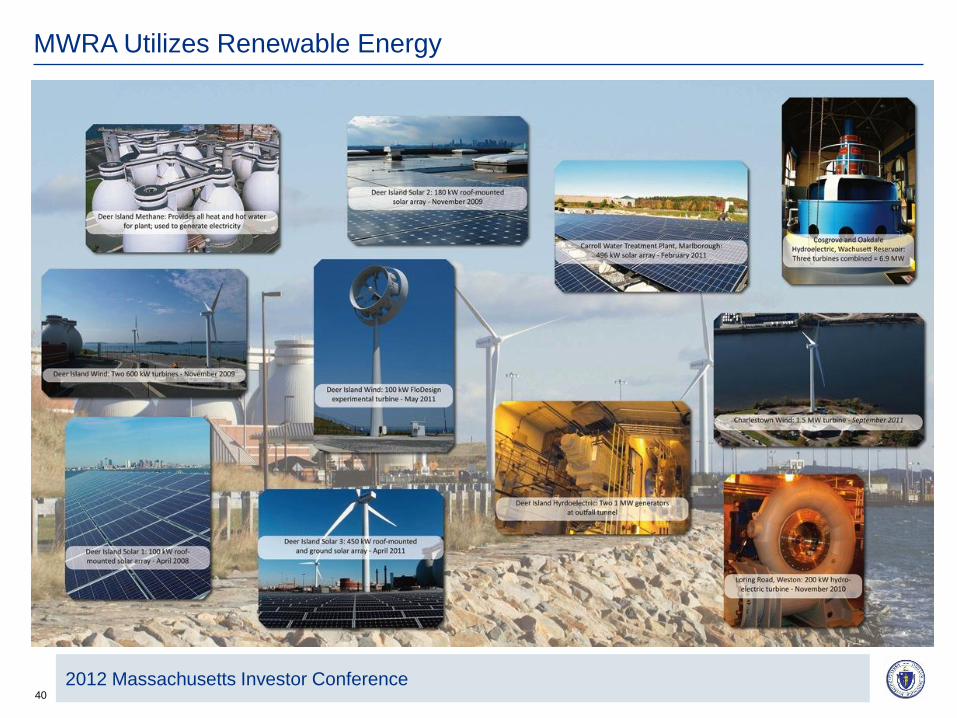

MWRA Utilizes Renewable Energy

2012 Massachusetts Investor Conference

41

Future Challenges: Maintenance

• Parts of the “new” Deer Island Treatment Plant have been on-line for almost 20 years

2012 Massachusetts Investor Conference

42

Future Challenges: Water System Redundancy

2012 Massachusetts Investor Conference

43

Future Challenges: Stormwater

2012 Massachusetts Investor Conference

44

Future Challenges: Aging Local Infrastructure

2012 Massachusetts Investor Conference

45

Future Challenges: Another Hurricane Sandy

2012 Massachusetts Investor Conference

46

2012 Massachusetts Investor Conference

Massachusetts Water Pollution

Abatement Trust

Massachusetts Water Pollution Abatement Trust:

Sue Perez, Executive Director

Presented by:

47

Massachusetts Water Pollution Abatement Trust (MWPAT) - Overview

2012 Massachusetts Investor Conference

Established in 1989 to improve the water quality in the Commonwealth through the provision of low-

cost capital financing to cities, towns and other eligible entities, and to maintain stewardship of public

funds with prudence, professionalism and integrity

Administered by a three-member board chaired by the Treasurer of the Commonwealth, and includes

the Secretary of the Executive Office for Administration and Finance, and the Commissioner of the

Department of Environmental Protection

Oversees financing for the clean water (“CW”) and drinking water (“DW”) state revolving funds (“SRFs”)

in partnership with DEP

– Trust receives significant federal and Commonwealth support – over $2.0 billion in federal

capitalization grants and state matching funds through FY 2012

Provides subsidized loans to local governmental units for CW and DW infrastructure development

– Projects financed are those ranked as a priority based on responses to a series of questions

intended to identify the most relevant public health and environmental related projects

Since its establishment, the Trust has provided approximately $5.7 billion in loans to nearly

300 borrowers to improve and maintain the quality of water in the Commonwealth – an

estimated 97% of Massachusetts citizens have benefited from these essential projects

48

Clean Water Projects Financed through SRF Program

2012 Massachusetts Investor Conference

Clean Water SRF

Maintenance and upgrade of municipal wastewater systems

is critical to protecting the Commonwealth’s environment,

meeting the public health needs of its citizens, and

promoting business development

The 2012 CWSRF Intended Use Plan (IUP) offered $302

million to finance clean water projects:

– Replacement of aged infrastructure components

– Installation of advance water treatment technologies

– Reduction to the carbon footprint of treatment facilities by

installing more energy efficient equipment

Additional subsidies provided for Renewable Energy

Generation and Environmental Justice Communities

$302 million of SRF Funded projects

estimated to create 1,800 construction

and engineering jobs

49

Drinking Water Projects Financed through SRF Program

2012 Massachusetts Investor Conference

Drinking Water SRF

Every citizen in the Commonwealth has the right to safe and

clean drinking water, and they depend on their federal, state

and local governments to protect this right

The 2012 DWSRF Intended Use Plan (IUP) offered $115

million to finance drinking water projects:

– Construction or upgrade of a municipal water treatment

facility

– Replacement or rehabilitation of water mains and pump

stations to address deficiencies in the water supply

distribution system

– Construction or rehabilitation of water storage tanks to

ensure a reliable water supply

– Additional subsidies provided for Renewable Energy

Generation and Environmental Justice Communities

$115 million of SRF Funded projects

estimated to create 690 construction and

engineering jobs

50

Leveraged State Revolving Fund Programs

2012 Massachusetts Investor Conference

Massachusetts is among the

largest SRF programs in the

country

– Historically, one of the top 5

states in dollars lent for

infrastructure investment

compared to each dollar

received from federal

government

– $2.0 billion in federal grants and

state matching funds leveraged

to $5.7 billion in project

financing

– 2009 ARRA Grants ($133.1

million for clean water and

$52.1 million for drinking water)

were committed by the Trust as

additional subsidization in the

form of principal forgiveness to

eligible borrowers

Federal Capitalization Grant and State Matching Funds

51

Financing Programs

2012 Massachusetts Investor Conference

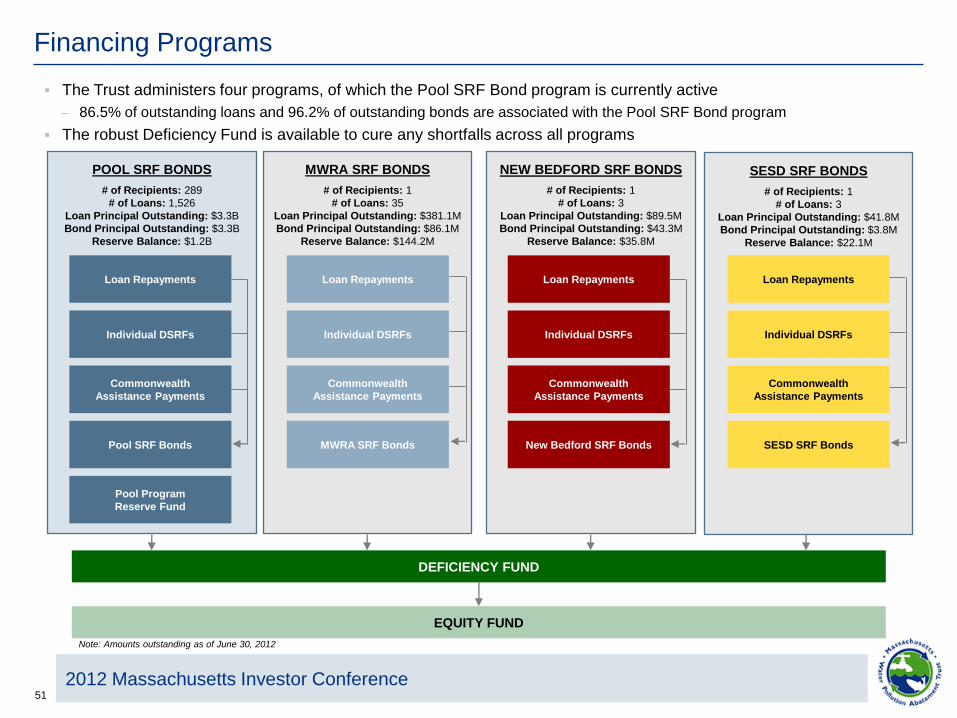

The Trust administers four programs, of which the Pool SRF Bond program is currently active

– 86.5% of outstanding loans and 96.2% of outstanding bonds are associated with the Pool SRF Bond program

The robust Deficiency Fund is available to cure any shortfalls across all programs

EQUITY FUND

DEFICIENCY FUND

SESD SRF BONDS

# of Recipients: 1

# of Loans: 3

Loan Principal Outstanding: $41.8M

Bond Principal Outstanding: $3.8M

Reserve Balance: $22.1M

NEW BEDFORD SRF BONDS

# of Recipients: 1

# of Loans: 3

Loan Principal Outstanding: $89.5M

Bond Principal Outstanding: $43.3M

Reserve Balance: $35.8M

POOL SRF BONDS

# of Recipients: 289

# of Loans: 1,526

Loan Principal Outstanding: $3.3B

Bond Principal Outstanding: $3.3B

Reserve Balance: $1.2B

MWRA SRF BONDS

# of Recipients: 1

# of Loans: 35

Loan Principal Outstanding: $381.1M

Bond Principal Outstanding: $86.1M

Reserve Balance: $144.2M

SESD SRF Bonds

Commonwealth

Assistance Payments

Individual DSRFs

Loan Repayments

New Bedford SRF Bonds

Commonwealth

Assistance Payments

Individual DSRFs

Loan Repayments

MWRA SRF Bonds

Commonwealth

Assistance Payments

Individual DSRFs

Loan Repayments

Pool Program

Reserve Fund

Pool SRF Bonds

Commonwealth

Assistance Payments

Loan Repayments

Individual DSRFs

Note: Amounts outstanding as of June 30, 2012

52

MWPAT Debt Profile

2012 Massachusetts Investor Conference

MWPAT Debt Service by FY*

Total Debt Outstanding: $3.5 billion

Maximum Annual Debt Service: $359.7 million

Average Annual Debt Service: $157.9 million

Weighted Average Life of Debt: 16.2 years

Capital Structure:

— Fixed Rate Mode: 100%

— Unhedged Variable Rate Mode: 0%

— Derivatives Exposure: $77.3 million CPI Bonds, swapped to a fixed rate

Key Statistics

*As of June 30, 2012

53

Security and Structure

2012 Massachusetts Investor Conference

Contract

Assistance

Payments

Secures all Bonds issued by the Trust on a parity basis

Amounts released from DSRFs securing MWRA, SESD, and New

Bedford Bonds not already released are transferred to the

Deficiency Fund, together with funds released from the Pool

Program Reserve Fund

Deficiency

Fund

Each Debt Service Reserve Fund secures its respective Bonds –

as bonds amortize, proportional amounts of reserve funds “de-

allocate” and are available as security

42% of Reserve funds invested in laddered portfolios of U.S.

Treasuries and Agencies – remainder are invested in GICs, the

bulk of which carry at least “AA” category ratings

Reserve

Funds

Secures all Bonds issued by the Trust on a parity basis

Amounts released from DSRFs securing MWRA, SESD, and New

Bedford Bonds not already released are transferred to the

Deficiency Fund, together with funds released from the Pool

Program Reserve Fund

Deficiency

Fund

$495.8 million in current and future assistance payments have

been pledged by the Commonwealth to the Trust on behalf of

program borrowers

Secured by the full faith and credit of the Commonwealth, which is

rated “Aa1/AA+/AA+”

Secures all Bonds issued by the Trust on a parity basis

Amounts released from DSRFs securing MWRA, SESD, and New

Bedford Bonds not already released are transferred to the

Deficiency Fund, together with funds released from the Pool

Program Reserve Fund

Deficiency

Fund

Secures all Bonds issued by the Trust on a parity basis

Amounts released from DSRFs securing MWRA, SESD, and New

Bedford Bonds not already released are transferred to the

Deficiency Fund, together with funds released from the Pool

Program Reserve Fund

Deficiency

Fund

Secures all Bonds issued by the Trust on a parity basis

Amounts released from DSRFs securing MWRA, SESD, and New

Bedford Bonds not already released are transferred to the

Deficiency Fund, together with funds released from the Pool

Program Reserve Fund

Deficiency

Fund

Composed of multiple revenue streams from nearly 300 unique

borrowers

Payments are due to the Trust 15 days in advance of debt service

payments

Loan

Repayments

Bonds are secured by direct and cascading cashflows consisting of loan repayments, Commonwealth

contract assistance payments, reserve fund earnings, and balances in the Pool Program Reserve Fund

and Deficiency funds

Commonwealth

Assistance

Payments

11%

Loan Repayments

78%

Reserve

Earnings

11%

Pledged Sources Securing Bonds

54

Loan Portfolio

The Trust’s loan portfolio provides a stable and secure source of repayment for the Bonds

– 75% of Pool SRF Program loans are secured by a general obligation pledge of the borrowers

Strong legal protections for loan repayments are bolstered by a local aid intercept whereby, upon a

borrower’s default, the Trust is authorized to obtain Commonwealth financial assistance that would

otherwise be transferred to the borrower

The essentiality of water and wastewater service underlies the security of the loan repayment streams

Rank Recipient

Loan Principal

Outstanding % of Total

1 MWRA $1,086,783,383 28.04%

2 Upper Blackstone Water Poll. Abatement Dist. 154,667,222 3.99%

3 City of Fall River 141,884,950 3.66%

4 City of New Bedford 136,077,946 3.51%

5 City of Brockton 100,223,232 2.59%

6 City of Lowell 82,504,643 2.13%

7 City of Taunton 79,128,575 2.04%

8 City of Chicopee 61,471,288 1.59%

9 Town of Nantucket 56,681,014 1.46%

10 Springfield Water and Sewer Commission 56,085,524 1.45%

11 Lynn Water and Sewer Commission 55,104,004 1.42%

12 City of Framingham 52,098,546 1.34%

13 South Essex Sewerage District 51,743,443 1.33%

14 City of Gloucester 50,279,712 1.30%

15 Town of Westborough 49,220,633 1.27%

277 Total all others 1,662,522,456

42.89%

Top 15 Borrowers Across All Programs High Quality Financing Book

Large and diverse pool of borrowers with

sound credit quality

Based on loan principal outstanding,

roughly 97% of program borrowers are

rated “A3/A-” or better and 65% are rated

“Aa3/AA-” or better

No leveraged loans have ever defaulted

MWRA – which is the Trust’s largest

borrower and serves 61 member

communities in and around the metropolitan

Boston area – is rated “Aa1/AA+/AA+”

7

2012 Massachusetts Investor Conference

55

DSRF Investments

The Trust has approximately $1.3 billion in reserves outstanding

– As bonds amortize, proportional amounts of DSRFs “de-allocate” and are available as security

42% of outstanding DSRFs are invested in laddered portfolios of U.S. Treasuries and Agencies

The Trust continues to opportunistically manage away from exposure to third party investment providers

– Recently, the Trust had the opportunity to terminate $119.1 million of guaranteed investment contracts

(“GICs”)

Remaining DSRFs are invested in GICs, the bulk of which carry at least “AA” category ratings

The Series 16 Bonds did not fund a DSRF and will thus avoid exposure to today’s more challenging

reinvestment environment

DSRF Investment Breakdown

U.S.

Treasuries and

Agencies

42%

“AA”

Category

45%

“A”

Category

13%

Note: Based on the highest rating. Data as of 11/30/12

2012 Massachusetts Investor Conference

56

Flow of Funds

SRF Program Funds

Investment Earnings

State Matching

Funds

Federal Grants

As borrowers pay down the principal balances of

their loans and as the Trust pays debt service on

its bonds, proportional amounts are released from

reserves and/or loans pledged to secure related

bonds and are returned to the SRF program funds.

Revenue Fund

Reserve Fund

Earnings

Loan Repayments

Contract Assistance

Debt Service Fund

Rebate Fund

Pool Program Reserve Fund

Deficiency Fund

2012 Massachusetts Investor Conference

57

Security for the Trust Bonds

2012 Massachusetts Investor Conference

The Trust applies the federal grants and state matching funds and other moneys available to

the Trust (SRF Program Funds) to make loans or to provide security for its Bonds.

– In the past, the Trust has applied SRF Program Funds to establish reserve funds to

secure the bonds issued to fund such projects – earnings on these reserve funds were

used to pay debt service

– Beginning with Series 16, the Trust may apply its SRF Program Funds to fund loans to

borrowers that will be pledged as security to the bonds – interest payments on these

loans will be used to pay debt service

– The program reflects the combination of Reserve Fund and Cash Flow models, utilizing

loans and reserve funds to secure bonds

Trust’s Series 16 Bonds applied the Cash Flow Model - allowed for an additional $121 million in projects to

be funded rather than SRF Program Funds deposited into a reserve fund.

Reserve

Fund

Model

Bond Series Financings

Cash

Flow

Model

Hybrid

Model

58

Credit Highlights

2012 Massachusetts Investor Conference

Strong Borrower Fundamentals

No leveraged loans have ever defaulted

Strong default tolerances meeting the AAA criteria of all three rating agencies

Local aid intercept

Programmatic Strength

Highly rated and diverse loan pool with strong security provisions

Commonwealth Assistance Payments are a source of program subsidy

Additional security at a program level (Pool Program Reserve Fund and

Deficiency Fund)

Support and Management

Repeat borrowers and constant municipal contact ensure Trust awareness of

local considerations

Bonds trade actively in the secondary market.

Maturity of the Program

Essentiality of the water and wastewater infrastructure projects being funded

The Trust constitutes the single largest financing source of essential water

infrastructure projects in the Commonwealth

The Trust continues to be a strong “Aaa/AAA/AAA” rated credit by Moody’s, S&P and Fitch. Maintaining the

AAA bond rating reduces the cost of borrowing, thus reducing the cost incurred by the Commonwealth to

subsidize the loans.

“Large and diverse pool of

underlying borrowers with sound

credit characteristics.” Moody’s

Investors Service – May 21, 2012

“The stable outlook reflects our

expectation that pledged revenues

will continue to provide strong debt

service coverage consistent with the

rating level, given historical trends.”

Standard & Poor’s Ratings Services

– May 18, 2012

“An extremely strong enterprise risk

profile, given that the pool has

ongoing support from multiple levels

of government and was established

by statute…” Standard & Poor’s

Ratings Services – May 18, 2012

59

MWPAT Anticipated Borrowings – Spring 2013

2012 Massachusetts Investor Conference

Pool 17 SRF Bonds

– ~ $150 - $200 million new money

– February/March 2013

– Structure as Hybrid – primarily cash flow model (little to no reserve fund)

Given current market rates, continue to evaluate refunding opportunities

– Over $100 million in potential refunding opportunities

60

2012 Massachusetts Investor Conference

15 Minute Break

61

2012 Massachusetts Investor Conference

Massachusetts School

Building Authority

Massachusetts School Building Authority:

Vin Alabiso, Chief Financial Officer

Presented by:

62

Massachusetts School Building Authority

1. Overview

3. Key Credit Strengths

4. Debt Profile

5. Ratings and Forward Calendar

2. Capital Pipeline and Program Initiatives

2012 Massachusetts Investor Conference

63

MSBA - Overview

1 Excludes taxes imposed on the sales of meals and certain other items. Please refer to the MSBA’s Official Statement

for a full definition of MSBA’s Dedicated Sales Tax Revenue Amount.

• The MSBA was created by Ch. 208 of the Acts of 2004 to effectively

manage, plan, and create a new, financially-sustainable school building

construction and renovation grant program

• 7-member Board chaired by State Treasurer Steven Grossman

• The Commonwealth irrevocably dedicated a 1% statewide sales tax to

the MSBA’s bond program1

• The MSBA instituted a number of changes to the Commonwealth’s

previous school building assistance program:

– Implemented programmatic oversight and controls to ensure efficiency

and solvency of the program

– Ended entitlement culture for school building grants

– Created competitive application process based on need and project

urgency

– Implemented regulations to focus on intensive pre-design scope,

schedule, and budget

• The MSBA has made more than $9.2 billion grant payments to districts

since 2004

2012 Massachusetts Investor Conference

64

MSBA - History

• In 2004, the MSBA was established to replace the Commonwealth’s

unsustainable school building assistance program, which had accumulated more

than $10 billion in liabilities and a multi-year funding and audit backlog for

hundreds of projects

• Chapter 208 of the Acts of 2004 ended the former school building assistance

program and created the MSBA, charged with:

– Succeeding to the powers of the Department of Education, inheriting

outstanding payments and audits for 1,156 previously authorized projects

– Achieving the effective management, planning and financial sustainability

of a new program for school building construction grants

– Revising regulations for a new program of grants for school construction

– Accepting applications for new grant program starting July 2007

2012 Massachusetts Investor Conference

65

Former Program - Inherited Commitments Update

• 94% of the total inherited Waiting

List liability/commitment retired to

date

• 74% of the total inherited Prior

Grant commitment retired to date

$5.1B Inherited Prior Grants Status

$1.3B , 26%

$3.8B , 74%

Payments and audit

savings to date

Remaining Prior Grant

commitments

* Includes payment and audit savings through 11/15/2012.

MSBA Inherited Programs

Grant Payments

$0

$500

$1,000

$1,500

$2,000

$2,500

FY2005

FY2006

FY2007

FY2008

FY2009

FY2010

FY2011

FY2012

FY2013

YTD

*

Fiscal Year

Gra

nt

Pa

ym

en

ts (

in m

illi

on

s)

Waiting List

Prior Grants

*Reflects payments made through 11/15/2012.

$5.5B Inherited Waiting List Status

$5,211.6* , 94%

$87.7* , 2%

$200.7* , 4%

Payments and audit

savings to date

Est. remaining annual

payments (FY14-FY24)

Est. remaining Progress

Payments

* Amounts in millions. Includes payment and audit savings through 11/15/2012.

2012 Massachusetts Investor Conference

66

New Program Solutions

The MSBA has implemented programmatic oversight and controls to ensure the grant program stays within available resources:

Focused New Program Spending

– Emphasis on core academic spaces, such as classrooms and science labs

– Adherence to educationally-sound MSBA space guidelines/standards

– “Pay as you build” Progress Payment system

Completed Two Capital Surveys of Approximately 1,800 School Facilities Across the Commonwealth

– Identified baseline public school inventory

Limited Grant Approvals to Available Funds

– Develop individual project budgets

– Require districts to design to agreed-upon budget/scope

– MSBA/local district financial commitment clearly documented

The MSBA has utilized taxpayers’ resources to support cost-effective and educationally appropriate programs:

Created “Model School” Program

– Adapts proven designs for reuse

Created Green and Accelerated Repair Programs

– Focus on preservation of existing assets by performing energy efficiency upgrades that will extend useful life of facilities

– Projects progress on accelerated schedule using streamlined procurement process

– Authorized nearly 170 Green Repair projects with estimated grants totaling approximately $223 million

– Authorized 14 Accelerated Repair projects to date with estimated grants of $12.6 million

Established Science Lab Initiative

– Enhances learning environments and facilitates delivery of 21st century science curriculum

– Funds up to $60 million in prototype designs for high school science labs

2012 Massachusetts Investor Conference

67

Massachusetts School Building Authority

1. Overview

3. Key Credit Strengths

4. Debt Profile

5. Ratings and Forward Calendar

2. Capital Pipeline and Program Initiatives

2012 Massachusetts Investor Conference

68

• Robust capital pipeline with more than 350 projects

• Project scopes range from energy efficiency repairs to new construction

Source: MSBA website, as of October 1, 2012.

MSBA projects across the Commonwealth

Partnering with school districts across the Commonwealth

2012 Massachusetts Investor Conference

69

MSBA Capital Pipeline Project Status - Capital Pipeline, All Projects (as of October Board of Directors’

Meeting)

2012 Massachusetts Investor Conference

70

Capital Pipeline - Grant Payments Update

More than $1.1 billion

reimbursement payments made

for New Program projects since

FY08

$226.1 million New Program

payments made FY13 YTD

FY13 YTD weekly average of

$24.8 million project costs

submitted for review through

Progress Payment

reimbursement system

FY13 YTD average of $11.6

million reimbursements paid

weekly for Capital Pipeline

project costs

MSBA New Program Grant Payments

$-

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

FY2008 FY2009 FY2010 FY2011 FY2012 FY2013

YTD*

Fiscal Year

Ne

w P

rog

ram

Gra

nt

Pa

ym

en

ts

*Reflects payments made through 11/15/2012.

FY13 Progress Payment System Activity

Total Weekly Project Costs Submitted

$0$10,000,000$20,000,000$30,000,000$40,000,000$50,000,000$60,000,000$70,000,000$80,000,000

7/2/

2012

- 7/8/2

012

7/16

/2012

- 7/22/

2012

7/30

/2012

- 8/5/2

012

8/13

/2012

- 8/19/

2012

8/27

/2012

- 9/2/2

012

9/10

/2012

- 9/16/

2012

9/24

/2012

- 9/30/

2012

10/8/2

012 -

10/1

4/20

12

10/22/2

012

- 10/

28/2

012

11/5/2

012 -

11/1

1/20

12

Week

To

tal S

ub

mit

ted

Co

sts

2012 Massachusetts Investor Conference

71

Capital Pipeline: Accelerated Repair Program

Utilizes best practices from the former Green Repair Program (172 projects) and is primarily for the repair and/or replacement of roofs, windows, and/or boilers with the potential to include additional systems as may be determined by the MSBA

Districts with repair needs in their facilities can apply through the Statement of Interest Process

Focuses on the preservation of existing assets by performing energy-efficient and cost-saving upgrades, which will result in direct operational savings for school districts

Districts invited into the Accelerated Repair Program are required to use pre-qualified Owner’s Project Managers (OPMs) and designers, and adhere to other requirements unique to this program, such as implementing an accelerated project schedule

2012 Massachusetts Investor Conference

72

Capital Pipeline: Model School Program

4

3

11

0

2

4

6

8

10

12

Elementary Middle/Middle High High

Elementary

Middle/Middle High

High

Seeks to effectively adapt and re-use the design of successful, recently constructed elementary, middle and high schools

18 districts currently participating

Up to five additional reimbursement percentage points for participation

Model School Program Task Force

– Input from design, construction and project management professionals

2012 Massachusetts Investor Conference

73 www.MassSchoolBuildings.org

Model School Chosen

(Whitman-Hanson Regional High School)

Rendering

of New

Hingham

Middle School

Capital Pipeline: Model School Program

New Norwood

High School

2012 Massachusetts Investor Conference

74

Capital Pipeline: Science Lab Initiative

• Program updates otherwise sound educational facilitates and enhances delivery of a 21st century science curriculum

• Six grants approved to date:

– Total project budgets: $26.1 million

– Estimated maximum total facilities grants: $15.3 million

A competitive grant program established through 2012 SOI process

www.MassSchoolBuildings.org/news_events/Science_Lab_Video

2012 Massachusetts Investor Conference

75

Program Initiative: Commissioning

• MSBA-commissioned buildings undergo an intensive quality

assurance process that begins during design and continues

through construction, occupancy, and operations

• Ensures facility operates efficiently, and as intended

• Prepares facility staff to operate and maintain building systems

and equipment

• Critical component in “green” building programs, including LEED

and MA-CHPS

• 100% Funded by the MSBA

MSBA fully-funded process involving independent third party testing a

building’s systems and materials and the operation of the building as a whole

$15.9 million commissioning contracts executed to date

191 contracts for 241 schools

2012 Massachusetts Investor Conference

76

Massachusetts School Building Authority

1. Overview

3. Key Credit Strengths

4. Debt Profile

5. Ratings and Forward Calendar

2. Capital Pipeline and Grant Initiatives

2012 Massachusetts Investor Conference

77

• Unconditional Gross Pledge of a 1% statewide sales tax1

– Sales tax supported by the strong, diverse Massachusetts economy

– Massachusetts is home to 11 Fortune 500 corporate headquarters

• Strong Coverage Levels on Senior & Subordinate Liens

– Dilution of pledged revenue is restricted by an Additional Bonds Test

of 1.40x maximum Adjusted Senior Bond Debt Service Requirement

on Senior Bonds, and 1.30x maximum Adjusted Bond Debt Service

Requirement on Subordinate Bonds

– Historic coverage ratios on Senior Lien Debt in excess of 2x

– Current Senior Lien MADS coverage ratio of 2.05x

• Fully Cash Funded Debt Service Reserve Funds

– $488 million in cash funded Debt Service Reserve Funds

• No Operational Risk

– MSBA does not pay for the operational costs of the infrastructure

projects it helps fund

• MSBA Tax Revenue is not Subject to Appropriation

• Statutory Non-Impairment Covenant

• Monthly funding of principal and interest on Senior Lien Bonds

MSBA - Key Credit Features

1 Excludes taxes imposed on the sales of meals and certain other items. Please refer to the MSBA’s

Official Statement for a full definition of MSBA’s Dedicated Sales Tax Revenue Amount.

Department of

Revenue

SMART Fund

Trustee

Bond Related

Costs Fund

(For Costs Related

to Senior Bonds)

Subordinated Debt

Service Fund

Subordinated Debt

Service Reserve Fund

Bond Related

Costs Fund

(For Costs Related to

Subordinated Bonds)

Senior Debt Service

Reserve Fund

Senior Debt

Service Fund

Revenue Fund

Dedicated

Payments

Additional

Revenues

Subordinated

Sinking Fund

Accounts

Sinking Fund

Deposits

Dedicated Sales Tax

Revenue Amount

Massachusetts School

Building Authority

2012 Massachusetts Investor Conference

78 Massachusetts School Building Authority

• Growth in all but 6 of the last 37 years

• Long history of favorable growth rates

• Strong performance across economic cycles

1 Total sales tax receipts after reimbursements and abatements, less the Statutorily Exempted Revenue. 2 These data are presented as an estimate of historical Dedicated Sales Tax Revenue Amount based on historical sales tax receipts, and represent a 1% sales tax. 3 In January 1998, the payment schedule for businesses with tax liabilities greater than $25,000 per year was changed to simpli fy the time period on which such

payments are based. While the timing change did not affect the amount of tax owed by the affected businesses, the new payment schedule caused a one-

time delay in receipt of tax revenues realized in FY 1998. According to DOR, approximately $105 million less in sales tax revenue was collected in FY 1998

as a result of this change.

4 A tax amnesty program was in effect for a portion of FY 2003 which, according to DOR, generated approximately $42 million of sales and use tax revenues. 5 Reflects additional revenue due to sales tax rate increase from 5.0% to 6.25% (estimated by DOR to be approximately $739 mill ion in FY 2010 and $918 million in FY 2011), and elimination of sales tax exemption for alcoholic beverages for the period between August

1, 2009 and January 1, 2011 (estimated by DOR to be $96.6 million in FY 2010 and $81.0 million in FY 2011, of which amounts $15.5 million and $13.0 million, respectively, are included in the Dedicated Sales Tax Revenue Amount for each respective year). 6 Amounts for FY 2012 are estimated by DOR and unaudited. 7 Amounts for FY 2013 are based on the Commonwealth’s revised FY 2013 tax revenue estimate as of December 4, 2012.

FY

Sales Tax

Receipts1

Applicable % of

Sales Tax

Receipts2

% Increase/

Decrease

1977 $441.8 $88.4 27.2%

1978 520.7 104.1 17.8%

1979 577.8 115.6 11.0%

1980 608.4 121.7 5.3%

1981 704.2 140.8 15.7%

1982 753.1 150.6 7.0%

1983 865.3 173.1 14.9%

1984 1,041.8 208.4 20.4%

1985 1,209.5 241.9 16.1%

1986 1,452.1 290.4 20.1%

1987 1,600.0 320.0 10.2%

1988 1,733.3 346.7 8.3%

1989 1,787.1 357.4 3.1%

1990 1,660.5 332.1 (7.1%)

1991 1,617.7 323.5 (2.6%)

1992 1,682.3 336.5 4.0%

1993 1,821.0 364.2 8.2%

1994 1,978.8 395.8 8.7%

1995 2,137.0 427.4 8.0%

1996 2,252.1 450.4 5.4%

1997 2,494.7 498.9 10.8%

1998 (3) 2,572.4 514.5 3.1%

1999 2,833.0 566.6 10.1%

2000 3,107.2 621.4 9.7%

2001 3,273.0 654.6 5.3%

2002 3,193.9 638.8 (2.4%)

2003 (4) 3,196.0 639.2 0.1%

2004 3,211.1 642.2 0.5%

2005 3,330.8 666.2 3.7%

2006 3,420.2 684.0 2.7%

2007 3,458.9 691.8 1.1%

2008 3,453.8 690.8 (0.1%)

2009 3,239.0 647.8 (6.2%)

2010 (5) 3,852.1 637.1 (1.7%)

2011 (5) 4,091.5 654.7 2.8%

2012 (6) 4,190.6 670.5 2.4%

2013 (7) 4,264.4 682.3 1.8%

Dedicated 1 Cent Statewide Sales Tax ($’s in Millions)

0

100

200

300

400

500

600

700

800

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

($’s

in

Millio

ns)

Strong History of Statewide Sales Tax Growth

2012 Massachusetts Investor Conference

79

FY13 SMART Sales Tax Collections

Total sales collections through October were $5M (2.3%) greater than collections through same period in FY12

Collections have exhibited growth each month over the same month in the previous year

Month Jul Aug Sep Oct YTD

FY12 Collections ($ in thousands) 59,646 54,111 52,414 56,434 222,606

FY13 Collections ($ in thousands) 60,514 56,214 53,253 57,667 227,648

Change ($ in thousands) 868 2,103 839 1,232 5,042

% Change 1.5% 3.9% 1.6% 2.2% 2.3%

Monthly SMART Collections

0

50,000

100,000

150,000

200,000

250,000

Jul Aug Sep Oct YTD

To

tal

Sale

s T

ax C

oll

ecti

on

s (

$ i

n t

ho

usan

ds)

FY12 Collections ($ in thousands)

FY13 Collections ($ in thousands)

2012 Massachusetts Investor Conference

80

Massachusetts School Building Authority

1. Overview

3. Key Credit Strengths

4. Debt Profile

5. Ratings and Forward Calendar

2. Capital Pipeline and Grant Initiatives

2012 Massachusetts Investor Conference

81 Massachusetts School Building Authority

1 Debt service reflects the impact of 2012 Series A and B refunding bonds. Debt service does not account for expected Debt Service Reserve Account earnings and the Federal BAB and QSCB subsidies; however, debt service is net of the amounts that are expected to be paid from Debt Service Reserve Account releases.

• $4.95 billion of Senior Lien debt outstanding as of November 15, 2012

• $293.38 million of Subordinate Lien debt outstanding as of November 15, 2012

– 100% comprised of Qualified School Construction Bond issuance

• Senior Lien MADS (net of Debt Service Reserve Account releases) totals approximately $367.62 million

• 100% of MSBA’s debt portfolio comprised of fixed rate debt

• FY13 refunding issuances (2012 Series A and 2012 Series B) generated more than $150.01 million net PV savings

MSBA Debt Service1 vs. Sales Tax Revenues

2

2

2

MSBA – Outstanding Debt

2012 Massachusetts Investor Conference

82

Massachusetts School Building Authority

1. Overview

3. Key Credit Strengths

4. Debt Profile

5. Ratings and Forward Calendar

2. Capital Pipeline and Grant Initiatives

2012 Massachusetts Investor Conference

83

Ratings

Recent affirmation of strong credit ratings as part of MSBA’s $916 million 2012

Series B refunding issuance

– Fitch: AA+

– Moody’s: Aa1

– S&P: AA+

Forward Calendar

New Money Issuance (~$500 million) – Q2 calendar 2013

Qualification of underwriters to be conducted Q1 calendar 2013

MSBA – Ratings and Forward Calendar

2012 Massachusetts Investor Conference

84

• Jack McCarthy, Executive Director

– (617) 720-4466, [email protected]

• Vin Alabiso, Chief Financial Officer

– (617) 720-4466, [email protected]

• Susan Flanagan-Cahill, General Counsel

– (617) 720-4466, [email protected]

• Ken Wissman, Chief Financial Advisor

– (617) 720-4466, [email protected]

Contact Information

Massachusetts School Building Authority

2012 Massachusetts Investor Conference

85

2012 Massachusetts Investor Conference

Massachusetts State College

Building Authority

Massachusetts State College Building Authority:

Edward H. Adelman, Executive Director

Presented by:

86

Massachusetts State College Building Authority

2012 Massachusetts Investor Conference

1. Overview

2. Demand for State University and Campus Facilities

3. Bond Security Features

4. Authority Debt Profile

5. Project Delivery and Management

6. Future Borrowing Needs

Weygand H

all B

ridgew

ate

r Sta

te U

niv

ers

ity

87

2012 Massachusetts Investor Conference

Massachusetts Maritime Academy

Fitchburg State University

Massachusetts College of Liberal Arts

Worcester State University

Bridgewater State University

Salem State University

Framingham State University

Westfield State University

The Massachusetts State University System

Massachusetts College of Art and Design

1. Overview:

MSCBA – Authority System Overview

The Authority finances, designs, constructs, and manages residential and student activity

facilities on the campuses of the nine State Universities

The Authority portfolio currently has capacity for approximately 15,000 students in 43

residential complexes. These facilities house approximately 42% of the undergraduate

student population

88

2012 Massachusetts Investor Conference

Demand

Full Occupancy; Increasing Enrollment

High Interest in Residential Campus Experience

Improved Facility Condition

Affordable Rent and Fees

Revenue and Reserves

Strong Project Revenues, Pledges, and Reserves

Multiple Years of Increases in Authority Reserves

No Variable Rate Debt; No Derivatives Exposure

All Revenue Available for All Debt

Statutory Appropriations Intercept (Pre-Default)

Strong Commonwealth Rating: Aa1 (Moody’s)

and AA+ (S&P)

Strong Intercept Mechanics

Improved Appropriations/Debt Service Coverage

Ratio

North Hall Framingham State University

1. Overview:

MSCBA – Key Credit Strengths

89

2012 Massachusetts Investor Conference

Undergraduate headcount has increased steadily from 34,748 in Fall 2002 to 42,127 in

Fall 2012, an increase of 21%

Fall 2011 to Fall 2012 undergraduate headcount rose by 1.2%

State University Undergraduate Headcount1

30,000

32,000

34,000

36,000

38,000

40,000

42,000

Fall

2002

Fall

2003

Fall

2004

Fall

2005

Fall

2006

Fall

2007

Fall

2008

Fall

2009

Fall

2010

Fall

2011

Fall

2012

(# o

f Stu

dents

)

Source: Baard of Higher Education 1 Early estimates for Fall 2012

2. Demand:

MSCBA – State University Enrollment

90

2012 Massachusetts Investor Conference

Residence hall design capacity (# of beds) has increased 48% from 10,065 in 2001 to

14,863 in 2012

Residence hall occupancy has remained stable at over 100% actual occupancy since

academic year 2003-2004, even as the number of beds has increased by nearly 4,800

All of the State Universities residence halls are fully occupied, with the majority having

Fall 2012 occupancy greater than 100%

Source: Authority

System Actual Occupancy versus Design Capacity

2. Demand:

MSCBA – State University Residence Hall Capacity and Occupancy

91

2012 Massachusetts Investor Conference

3. Bond Security Features:

MSCBA – Flow of Funds Established by Trust Agreement

92

2012 Massachusetts Investor Conference

3. Bond Security Features:

MSCBA – Total Revenue, Reserves and Pledges Available for Debt Service

93

2012 Massachusetts Investor Conference

3. Bond Security Features:

MSCBA – Projected Reserve Levels

94

2012 Massachusetts Investor Conference

4. Authority Debt Profile:

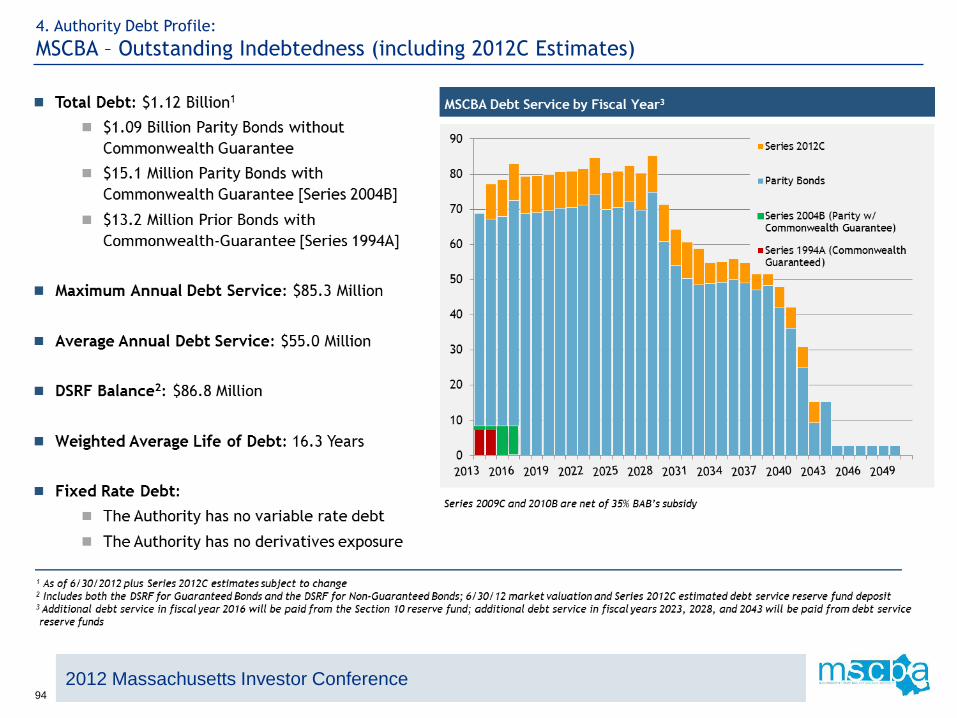

MSCBA – Outstanding Indebtedness (including 2012C Estimates)

95

2012 Massachusetts Investor Conference

Qualifications-based selection process

Completion bonus/penalties

Track record for on-time and-on budget

performance

Build and sustain quality facilities

Schedule and fund periodic

reinvestment

Bonding and insurance

“The new dorm tower at

Massachusetts College of Art and

Design is the most interesting

Boston high-rise in years.”

Robert Campbell

architecture critic

The Boston Globe

Sunday, May 13, 2012

Treehouse Residence Mass College of Art and Design

5. Project Delivery and Management:

MSCBA – Project Approach

96

2012 Massachusetts Investor Conference

For further information, please contact:

Edward Adelman

Executive Director

617/933-8337

Visit on the web:

www.mscba.org

Currently, the Authority expects to issue approximately $80 million in both 2014 and

2015 to fund two new residence halls and renovations to student activity facilities

Fitness & Recreation Center Salem State University

6. Future Borrowing Needs:

MSCBA – Upcoming Issuances

97

2012 Massachusetts Investor Conference

University of Massachusetts

Building Authority Presented by:

Katherine Craven

Executive Director

The University of Massachusetts Building Authority

98

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

History

Created by Mass. Legislature in 1960

Merged with Lowell University and Southeastern Mass University Authorities in 1995

First issuer in Mass. to use taxable Build America Bonds

Completed the Authority’s first competitive bond sale in 2011

Governance

11 Members

Appointed by the Governor

5 Members must be UMass Trustees

2 Non-Trustee Members must be alumni of the University

Non-Trustee Members serve 6 year terms

Trustee Members serve as long as they are Trustees

99

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

Debt Outstanding (in thousands) – June 30, 2012

100

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

75%

25%

0%

Debt Outstanding – June 30, 2012

Fixed Rate

Synthetic Fixed Rate

Variable Rate

101

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

58%17%

18%

7%

Debt Credit Support – June 30, 2012

University Credit

Insured

Credit Enhanced

CommonwealthGuaranteed

102

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

103

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

Projects

104

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

Albert Sherman Life Sciences Building

105

1

0

5

Capital Improvement Requirements:

Debt Financing

Five-year plan proposes $1.73 billion in debt funded spending

• $700 million already borrowed

• $1 billion to be borrowed during the five-year period (Next planned borrowing- Spring 2013)

• UMass maintains strong Aa2/AA ratings, providing market access for a variety of financing alternatives

and attractive borrowing costs

Fitch Ratings Report:

“Management continues to prudently

oversee an extensive capital improvement

program meant to enhance teaching and

research facilities, and elevate the

university’s academic standing.”

Debt Service – Existing plus $1

billion of new bonds

2012 Massachusetts Investor Conference

University of Massachusetts Building Authority

106

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

Credit Review

Rating Agencies:

Moody’s Aa2

Fitch AA

S&P AA (Commonwealth Guarantee Debt)

University of Massachusetts

69,600+ students over 5 campus system (Fall 2011)

Nearly 14,000 degrees conferred (2010 – 2011)

13,500+ admissions (Fall 2011)

$586+ million in research expenditures and continues to grow at an 8.1% increase over FY

2010

107

University of Massachusetts Building Authority

2012 Massachusetts Investor Conference

University of Massachusetts

In the Fall of 2011 the Times of London ranked UMass as the 64th best University in the

world.

Ranked behind only Harvard, MIT and Tufts in Massachusetts

The Times of London 2011 World Reputational Rankings ranked UMass 19th in the world in

reputation.

The 2012 U.S. News rankings of primary care medicine ranked UMass Worcester 7th out of

146 institutions.

In 2010, the most current ranking, UMass ranked 13th nationwide in terms of universities

generating revenues from licensing and technology transfer.

UMassOnline, which delivers 100+ programs to diverse and geographically dispersed

learners, increased by 11% in 2011 to over 50,000 enrollments.

UMass endowment assets grew by 15% in 2012 and exceeded $529 million.

(Source: The University of Massachusetts 2012 Annual Indicators Report and University personnel)

108

2012 Massachusetts Investor Conference

Investor Roundtable Panel

Colin MacNaught, Office of the State Treasurer

Moderated by:

Chris Alwine, Vanguard

109

2012 Massachusetts Investor Conference

Presentation By:

John J. Cross III

Securities and Exchange Commission

Director of the Municipal Securities Office

110

2012 Massachusetts Investor Conference

John J. Cross III, Securities and Exchange Commission, Director of the Municipal Securities Office

John Cross has a broad range of experience with municipal finance transactions in nearly every

state, including experience with some of largest and most complex municipal financings ever

undertaken. Mr. Cross has been a leader in the public policy area affecting municipal finance.

For the past several years, Mr. Cross has been serving as the Associate Tax Legislative Counsel in

the Office of Tax Policy at the U.S. Treasury Department, where he has had significant responsibility

for legislative, regulatory and budgetary tax matters affecting municipal bonds. Mr. Cross led the

agency’s implementation of the municipal bond provisions of the 2009 Recovery Act, which included

public guidance on Build America Bonds and other targeted municipal bond programs. He also

played a significant role in the Treasury Department’s efforts to address municipal bond market

challenges in the 2008 financial crisis.

Prior to working at the Treasury Department, Mr. Cross was a partner at national municipal bond

specialty law firm Hawkins Delafield & Wood LLP from 1994 to 2006. He previously served as a

counsel at the Internal Revenue Service in the Financial Institutions and Products division, where his

work involved derivative financial products that were used with municipal bonds.

Mr. Cross has been active in several professional organizations, including the National Association of

Bond Lawyers (NABL), where he’s a former board member. He’s also a member of the editorial

board for Municipal Finance Journal. Mr. Cross received his B.A. from Brown University in 1978, a

J.D. from Vanderbilt University School of Law in 1981, where he was a member of the Vanderbilt Law

Review, and a Masters of Laws in Taxation from Georgetown University Law Center in 1988. He is

married to Meredith Cross, who is Director of the SEC’s Division of Corporation Finance.

111

2012 Massachusetts Investor Conference

The Commonwealth of Massachusetts

Executive Office for Administration and Finance:

Jay Gonzalez, Secretary

Greg Mennis, Assistant Secretary for Fiscal Policy

Scott Jordan, Assistant Secretary for Capital Finance

Michael Esmond, Budget Director

State Treasurer’s Office:

Colin MacNaught, Assistant Treasurer for Debt Management

Delia Rissmiller, Investor Relations Manager

Presented by:

112

The Commonwealth of Massachusetts – Fiscal 2013 Update

2012 Massachusetts Investor Conference

• FY 2013 signed on-time, and in balance, totaling approximately $32.5 billion, an increase of

4.9%.

• As of the signing of the budget, the reliance on one-time resources was estimated to be

$616 million, down from $669 min fiscal 2012 and over $1.9 billion in fiscal 2011.

• As we will discuss further in the presentation, ANF continues its efforts to develop and

improve long-term fiscal planning models and policies. Based on ANF’s long-term models,

this level of non-recurring resources is safely within a sustainable level for the state’s

annual budget.

• The fiscal 2013 budget continues to reform, including such areas as, community colleges

governance, accountability and effectiveness; programs and services for homeless

families; state facilities managements; performance management and budget

transparency; and, efforts to control health care spending for the state and employers

across the Commonwealth.

• Spending controls continue. While the fiscal 2013 budget did not require the same level of

reductions and related spending control measures as some previous budgets, state

agencies must continue to find ways to limit growth in their costs and operate more

efficiently.

113

The Commonwealth of Massachusetts – Fiscal 2013 Update

2012 Massachusetts Investor Conference

On December 4, 2012, pursuant to Section 9C of Chapter 29 of the Massachusetts General

Laws, the Secretary of Administration and Finance advised the Governor of a budgetary

shortfall of revenues totaling $540 million with respect to the appropriations approved to

date for fiscal 2013.

On the same day, the Secretary revised the tax revenue estimate for fiscal 2013 to $21.496

billion, which represents a reduction of $515 million from the revenue estimate assumed in

the fiscal 2013 budget adjusted for subsequent tax law changes.

On December 4th the Governor announced a balanced set of solutions, and filed

accompanying legislation, that would close the gap.

The Administration and Legislature have established a number of prudent fiscal policies to

ensure structurally-balanced budgets and long-term fiscal sustainability. These have been

codified through changes in law and in the Administration’s Long-Term Fiscal Policy

Framework.

One of these fiscal policies is a commitment to solve no more than half of any mid-year tax

revenue shortfall with rainy day funds or other one-time, non-recurring resources. This

policy ensures a balanced set of budgetary solutions that will better position the state to

absorb the impact the tax revenue reduction may have in subsequent years as well.

114

The Commonwealth of Massachusetts – Fiscal 2013 Update

2012 Massachusetts Investor Conference

Overview of Budget Balancing Measures

Fiscal Action Plan

Change in Estimated FY 2013 Tax Receipts: (515)

Year-To-Date Dedicated One-Time Tax Settlements: (25)

Projected Budgetary Shortfall: (540)

Non-Recurring Solutions:

Increase Rainy Day Fund: 200

One-Time Medicaid Revenue: 49

One-Time Executive Branch Reductions: 10

Other Fund Surpluses: 11

sub-total: 270

Recurring Solutions:

Additional Federal Revenues: 49

Non-Executive Branch Reductions (1%): 25

Reduced Sales Tax Transfer to School Building Authority 20

Local Aid Reduction (1%) 9

Executive Branch Reductions (net)*: 147

Health Care and Debt Service Savings: 20

sub-total: 270

115

The Commonwealth of Massachusetts – Fiscal 2013 Update

2012 Massachusetts Investor Conference

Nationally, the rate of economic growth has been slower than in typical post-recession

periods and, over the last few months, economic growth has been slower across the

country than had been projected at this time last year when we developed the tax revenue

estimate for the fiscal 2013 budget.

The slow-down in economic growth is largely due to the uncertainty caused by the so-called

“fiscal cliff” and the federal fiscal condition generally.

Though we have proactively addressed the current projected shortfall, inaction by the

federal government to address the so-called “fiscal cliff” would have a significant impact to

state tax revenues. Some forecasts project a $300 million fiscal 2013 tax revenue hit as a

result of full sequestration and expiration of tax cuts.

116

The Commonwealth of Massachusetts – Reserves

2012 Massachusetts Investor Conference

The fiscal 2012 estimates released by the National Association of State Budget Officers

(NASBO) in June 2011, together with the results reported in the Commonwealth’s fiscal

2012 Statutory Basis Financial Report, indicate that Massachusetts’s Stabilization Fund

balance of $1.652 billion is estimated to be the third highest reserve fund balance in the

nation in absolute size

After accounting for the additional withdrawals from the Fund in fiscal 2013 the projected

ending balance would b $1.192 billion, one of the highest in the nation.

This is a direct of result of prudent budget management by the Administration and

Legislature, fiscal 2012 was the second year in a row that had a year-on-year increase.

In addition, two recently passed amendments to state finance law have also helped to

increase the balance of the state’s reserves

– A provision that requires the deposit of any one-time settlements greater than $10 million

to the Stabilization Fund resulted in a $375 million being added to the fund in fiscal 2012.

– A provision that requires any tax revenue from capital gains that exceeds $1 billion in a

fiscal year is to be deposited into the Stabilization Fund is projected to result in a $90

million deposit into the fund in fiscal 2013.

117

The Commonwealth of Massachusetts – Reserves

2012 Massachusetts Investor Conference

1,137

1,728

2,155

2,335

2,119

841

669

1,379

1,652

1,192

0

500

1,000

1,500

2,000

2,500

$s

in

mil

lio

ns

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Fiscal Year

Stabilization Fund Balances

by Fiscal Year

118

The Commonwealth of Massachusetts – Looking Forward – Fiscal 2014 Overview

2012 Massachusetts Investor Conference

House 1 Development. A&F is actively working with state agencies now to develop the

Governor’s budget for next year.

With a continued uncertain revenue picture, A&F developed competing scenarios of

potential impacts resulting from some or all of the fiscal cliff occurring on January 1,

2013.

The state FY 2014 tax consensus hearing process will begin on December 11 with the

joint A&F and legislative hearing at which economic forecasters will provide testimony

on likely revenues and related economic factors. Actual revenue forecasts for FY 2014

tax collections and related distributions of dedicated tax streams will not be finalized

until early to mid January 2013.

The Governor’s budget will be filed on Wednesday, January 23, 2013.

The impact of the “fiscal cliff” would be significant to the Commonwealth’s fiscal 2014

tax revenues, with some forecast’s projecting a revenue loss of $1 billion as a result of

full sequestration and expiration of tax cuts.

119

The Commonwealth of Massachusetts – Capital Investment Plan

2012 Massachusetts Investor Conference

Statewide, five-year capital plan. The plan coordinates capital expenditures by state

agencies and authorities that are funded primarily with Commonwealth debt, third party

payments and federal reimbursements.

Limit on Borrowing, from all sources. The Administration limits bond-funded capital

expenditures, known as the “bond cap.” fiscal 2013 bond cap is $1.875 billion with an

additional $93 million in unused capacity from the prior fiscal year.

Bond cap determination is based on the Debt Affordability Analysis and policies in which

A&F sets the annual borrowing limit at an amount sized to keep debt service within 8% of

budgeted revenues

The Administration has conservatively constrained the bond cap in FY16 and FY17 at the

fiscal 2015 level. Future debt affordability analysis may show sufficient revenue growth to

allow increased bond cap in future plans.

120

The Commonwealth of Massachusetts – Capital Investment Plan

2012 Massachusetts Investor Conference

-

500,000,000

1,000,000,000

1,500,000,000

2,000,000,000

2,500,000,000

FY12 FY13 FY14 FY15 FY16 FY17

Unused Capacity

State Bond Cap

121