Embed Size (px)

Citation preview

2013 Global Survey of Financial AdvisorsFrance – Individual Country Report

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

3

Methodology

CoreData Research was commissioned by Natixis Global Asset Management to conduct an international study of financial advisors, with the aim of better understanding the contemporary attitudes and needs of this key collective of individuals to the financial services industry.

Financial advisors are the bridge between product manufacturers and retail investors and many small, medium and in some cases, large corporations and it is therefore imperative to assess the opportunities and challenges facing this group of professionals.

Specifically this study assesses at advisor attitudes to a range of topics such as business growth, portfolio construction (including volatility, risk and income), client service, advice proposition, time management and investment challenges.

Data was gathered over a five week period spanning August and September 2013.

The survey was delivered through an online quantitative survey of approximately 40 questions and was hosted by CoreData Research.

Globally, the study involved 1,300 financial advisors in nine countries and across four continents.

Individual country details can be found in the appendices section of the report.

A Global View

The opportunities for financial advisory businesses worldwide are strong. Ageing populations, a perpetually uncertain investment environment and ever increasing complexity (compounded by relentless sources of information being thrust upon investors) are combining to cement the need for professional, quality, informed and impartial financial advice.

A by-product of robust equity markets is 60% of financial advice businesses globally are growing – in part driven by varying degrees of asset-based fee remuneration structures.

However, despite the recent market buoyancy and implicit demand around the world for professional advice, the post-crisis turnaround for businesses is not a guarantee of future success.

Financial advisors face a multitude of challenges and pressures, and it is imperative product manufacturers in the investment industry strive to reduce – and ultimately help remove – some of the hurdles hampering advisors.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

4

One of the hardest tests for advisors is in seeking to achieve balance when making decisions against a backdrop of competing variables and sometimes contradictory variables.

Advisors must sometimes feel analogous to a performing artist – trying to juggle their own time and resource limitations, client investment objectives, market realities, client understanding, client emotions/psychology, investment strategies and commercial business dynamics

Ultimately, to grow a business for the long term advisors require satisfied clients today and prospective clients tomorrow.

One of the big questions is whether advisors have the product set to satisfy existing clients and also to attract and meet the need of prospective clients?

A big risk for advisor businesses globally is the energy spent trying to meet existing client needs - a real risk as many advisors are finding this difficult to achieve.

In a double whammy, the subsequent neglect of seeking new clients to drive future business growth will really hurt businesses.

Future Alarm

Time spent seeking new clients (currently limited to only 11% or 15.9 hours per month).

Only 40% of advisors globally are actively seeking younger clients to replace older clients or those in decumulation phase.

Present Alarm

53% of advisors globally admitted difficulty in accommodating draw-downs for clients in retirement, but keeping portfolios growing to transfer wealth.

46% found it difficult to generate sufficient income for clients in retirement.

40% cited difficulty in effectively managing volatility risk for those in retirement.

In search of investment solutions to meet their needs, advisors and their clients are typically forced to make compromises and in some cases the end solutions either fail to deliver, client expectations/needs are too great for their investment portfolios to deliver a successful outcome, or the bridge that needs to be crossed is a bridge too far, e.g. clients don’t have a sufficient time horizon to reach their goals.

Some common investment paradoxes - a question of compromise or education?

Clients may want enduring stable income but they loath the volatility of being exposed to market capriciousness.

Clients may want portfolio growth but they invariably misunderstand and shirk risk.

Clients may accept a need for broader diversification but continue to hold heavy exposures to a handful of asset classes via traditional investment techniques.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

5

In instances such as these, advisors are thrust into a scenario where they are forced to try and ‘tick all the boxes’.

Almost four in five advisors globally say they seek investment strategies/products that help to manage risk (81%), manage volatility (79%) and produce income for clients (82%).

It seems there is a need for new thinking and approaches. Advisors mostly accept this. Diversification and a move away from traditional approaches could be part of the solution.

59% of advisors internationally agree there is a need to replace traditional diversification and portfolio construction techniques with new approaches to achieve results, with only 31% in disagreement and the remainder neither agreeing nor disagreeing.

Underneath all of this is also an acceptance by financial advisors that they, as their clients do, also have a strong need for better understanding.

Three quarters of advisers (75%) admitted financial advisors require more education, with only 16% in disagreement, and the remainder neither agreeing nor disagreeing.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

6

Outlook for French financial advisers

There are difficult times ahead for the French economy after it was announced in late September that public debt will hit a record 95.1% of GDP in 2014. France, which is the Eurozone's second largest economy after Germany, recently revealed its Budget for 2014 which will look to save £12.6bn through a tightening of its public spending, while there will be some tax increases for households, albeit these will levelled off by some tax reductions to businesses. This budget is based around a growth forecast of 0.9% for 2014, lowered from 1.2%, while growth is forecast at a meagre 0.1% for 2013.

The pessimism around the economy is reflected in the financial advice market, where a quarter of French advisors (23%) have reported a decline in their business in the past few years (vs. 14% for other countries).

10% of French advisors said their business has ‘declined very strongly’ in the past few years - well above the average for the other countries (4%).

Adviser Business Growth - Regionally

11%56%

26%

6%1%UK

8%

42%

31% 13%

6%Europe

9%67%

16%

7%1%US

27%

55%17%

1%Asia

40%

32%

15%8%5%Middle

East

Growing very strongly GrowingFlat/No changeDeclining Declining very strongly

GlobalGrowing = 60%Declining = 14%

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

7

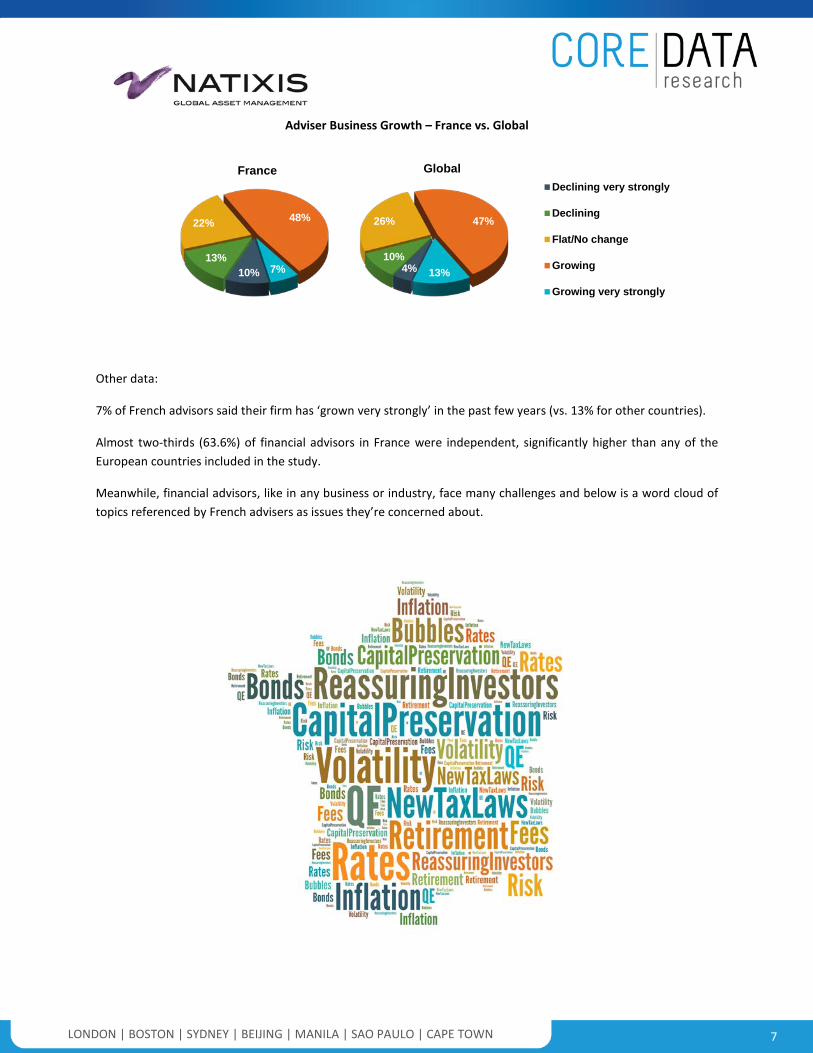

Adviser Business Growth – France vs. Global

10%13%

22% 48%

7%

France

4%10%

26% 47%

13%

GlobalDeclining very strongly

Declining

Flat/No change

Growing

Growing very strongly

Other data:

7% of French advisors said their firm has ‘grown very strongly’ in the past few years (vs. 13% for other countries).

Almost two-thirds (63.6%) of financial advisors in France were independent, significantly higher than any of the European countries included in the study.

Meanwhile, financial advisors, like in any business or industry, face many challenges and below is a word cloud of topics referenced by French advisers as issues they’re concerned about.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

8

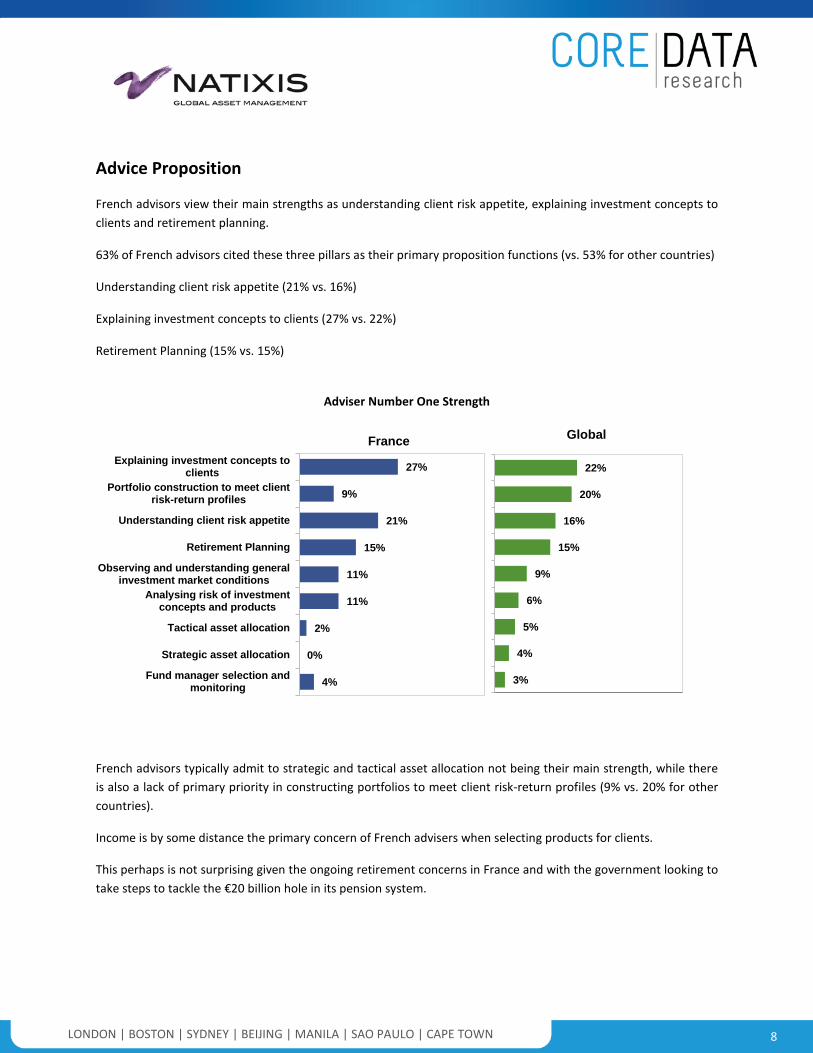

Advice Proposition

French advisors view their main strengths as understanding client risk appetite, explaining investment concepts to clients and retirement planning.

63% of French advisors cited these three pillars as their primary proposition functions (vs. 53% for other countries)

Understanding client risk appetite (21% vs. 16%)

Explaining investment concepts to clients (27% vs. 22%)

Retirement Planning (15% vs. 15%)

Adviser Number One Strength

27%

9%

21%

15%

11%

11%

2%

0%

4%

Explaining investment concepts toclients

Portfolio construction to meet clientrisk-return profiles

Understanding client risk appetite

Retirement Planning

Observing and understanding generalinvestment market conditions

Analysing risk of investmentconcepts and products

Tactical asset allocation

Strategic asset allocation

Fund manager selection andmonitoring

France

22%

20%

16%

15%

9%

6%

5%

4%

3%

Global

French advisors typically admit to strategic and tactical asset allocation not being their main strength, while there is also a lack of primary priority in constructing portfolios to meet client risk-return profiles (9% vs. 20% for other countries).

Income is by some distance the primary concern of French advisers when selecting products for clients.

This perhaps is not surprising given the ongoing retirement concerns in France and with the government looking to take steps to tackle the €20 billion hole in its pension system.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

9

Advisers Seeking Specific Strategies/Investment Products to Manage:

87% of French advisors look for income strategies/investments to manage their clients’ portfolio (vs. 82% for other countries). The search for strategies/investment products for risk (73% of French advisers) and volatility (69% of French advisers) are both well below the average for other countries.

Just over half (56%) of French advisors said their clients missed the late 2012 stock rally because they had too much invested in cash (vs. 70% for other countries).

56%70% 69% 78% 72% 80% 70%

55%

44%30% 31% 22% 28% 20% 30%

45%

0%

25%

50%

75%

100%

France Global France Global France Global France Global

Clients missed takingadvantage of the late2012 rally in stocks

because they had toomuch invested in cash.

I am confident clientportfolios can withstand

a market correction.

I am confident clientportfolios can withstandan increase in interest

rates.

Many clients believe theirown home is a better

investment than stocksor stock funds.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

10

Other data:

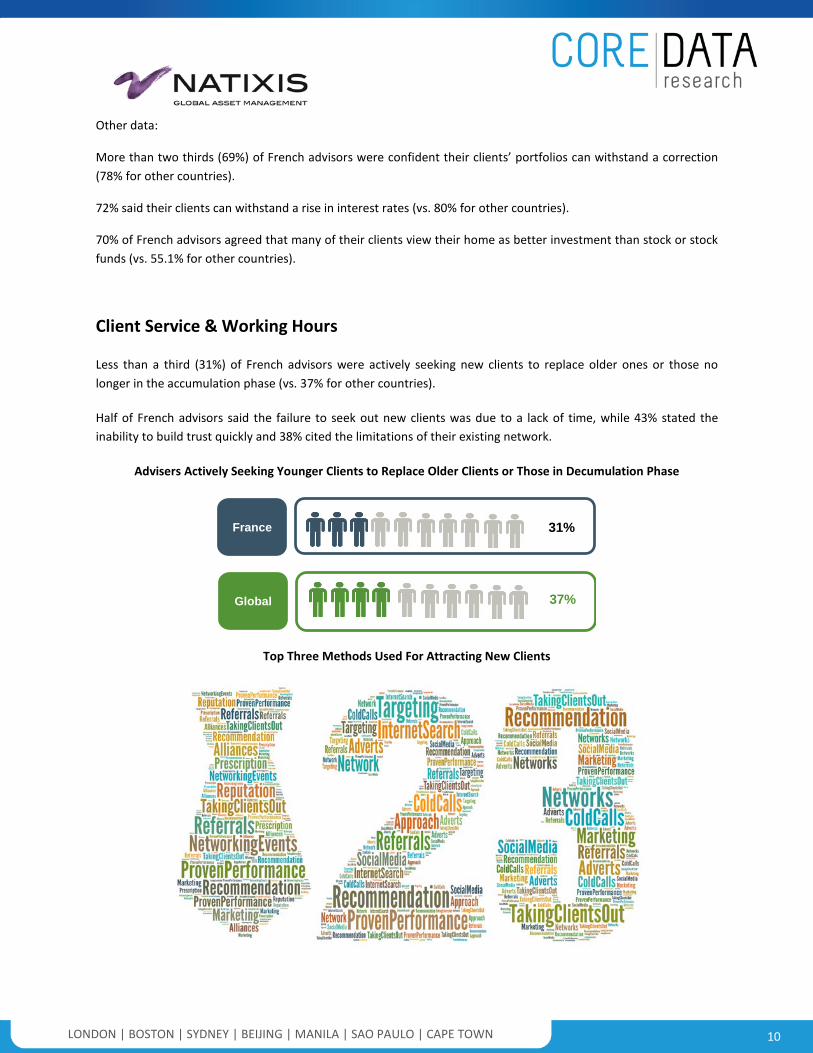

More than two thirds (69%) of French advisors were confident their clients’ portfolios can withstand a correction (78% for other countries).

72% said their clients can withstand a rise in interest rates (vs. 80% for other countries).

70% of French advisors agreed that many of their clients view their home as better investment than stock or stock funds (vs. 55.1% for other countries).

Client Service & Working Hours

Less than a third (31%) of French advisors were actively seeking new clients to replace older ones or those no longer in the accumulation phase (vs. 37% for other countries).

Half of French advisors said the failure to seek out new clients was due to a lack of time, while 43% stated the inability to build trust quickly and 38% cited the limitations of their existing network.

Advisers Actively Seeking Younger Clients to Replace Older Clients or Those in Decumulation Phase

31%France

Global 37%

Top Three Methods Used For Attracting New Clients

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

11

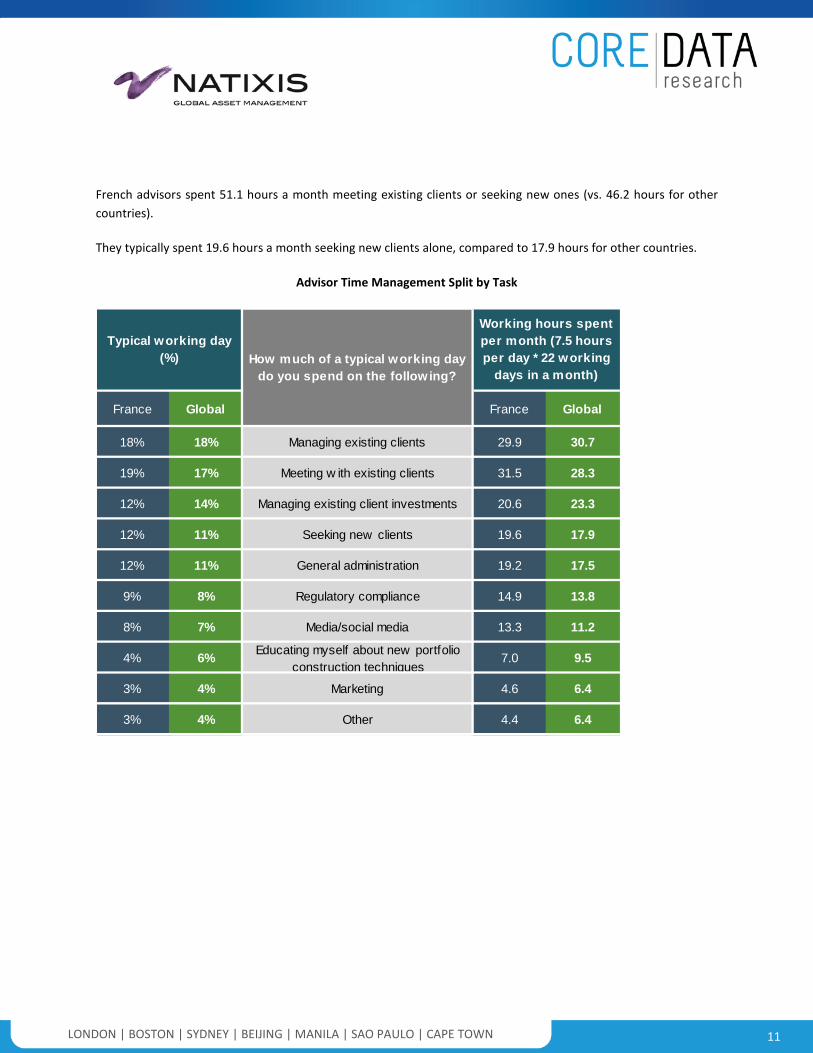

French advisors spent 51.1 hours a month meeting existing clients or seeking new ones (vs. 46.2 hours for other countries).

They typically spent 19.6 hours a month seeking new clients alone, compared to 17.9 hours for other countries.

Advisor Time Management Split by Task

France Global France Global

18% 18% Managing existing clients 29.9 30.7

19% 17% Meeting w ith existing clients 31.5 28.3

12% 14% Managing existing client investments 20.6 23.3

12% 11% Seeking new clients 19.6 17.9

12% 11% General administration 19.2 17.5

9% 8% Regulatory compliance 14.9 13.8

8% 7% Media/social media 13.3 11.2

4% 6% Educating myself about new portfolio construction techniques

7.0 9.5

3% 4% Marketing 4.6 6.4

3% 4% Other 4.4 6.4

Typical working day (%) How much of a typical working day

do you spend on the following?

Working hours spent per month (7.5 hours per day * 22 working

days in a month)

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

12

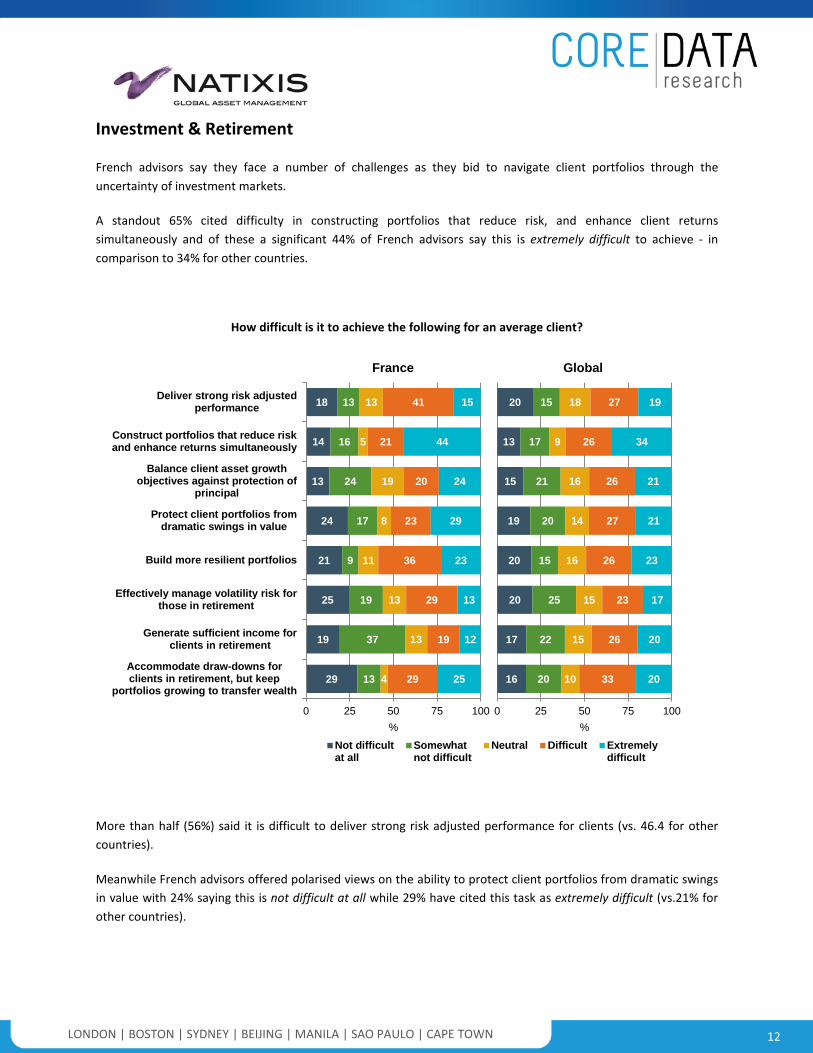

Investment & Retirement

French advisors say they face a number of challenges as they bid to navigate client portfolios through the uncertainty of investment markets.

A standout 65% cited difficulty in constructing portfolios that reduce risk, and enhance client returns simultaneously and of these a significant 44% of French advisors say this is extremely difficult to achieve - in comparison to 34% for other countries.

How difficult is it to achieve the following for an average client?

18

14

13

24

21

25

19

29

13

16

24

17

9

19

37

13

13

5

19

8

11

13

13

4

41

21

20

23

36

29

19

29

15

44

24

29

23

13

12

25

0 25 50 75 100

Deliver strong risk adjustedperformance

Construct portfolios that reduce riskand enhance returns simultaneously

Balance client asset growthobjectives against protection of

principal

Protect client portfolios fromdramatic swings in value

Build more resilient portfolios

Effectively manage volatility risk forthose in retirement

Generate sufficient income forclients in retirement

Accommodate draw-downs forclients in retirement, but keep

portfolios growing to transfer wealth

%

France

20

13

15

19

20

20

17

16

15

17

21

20

15

25

22

20

18

9

16

14

16

15

15

10

27

26

26

27

26

23

26

33

19

34

21

21

23

17

20

20

0 25 50 75 100%

Global

Not difficultat all

Somewhatnot difficult

Neutral Difficult Extremelydifficult

More than half (56%) said it is difficult to deliver strong risk adjusted performance for clients (vs. 46.4 for other countries).

Meanwhile French advisors offered polarised views on the ability to protect client portfolios from dramatic swings in value with 24% saying this is not difficult at all while 29% have cited this task as extremely difficult (vs.21% for other countries).

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

13

French advisors also admitted they struggled to provide portfolios for retail clients that are correlated when markets go up but uncorrelated when they go down. Two-thirds (69%) said this is challenging (33% of which say it is very challenging).

Other stats:

Almost a quarter (25%) of French advisors said they would find it ‘extremely difficult’ to accommodate draw-downs for clients in retirement, but keep portfolios growing to transfer wealth for the average client (vs. 20% for other countries).

Interestingly, 41% of French advisors believed the majority of their clients know how much the need to save to meet their retirement goals/expectations (vs. 31% for other countries)

How challenging is it to deliver the following for your retail client?

16

11

15

29

14

16

10

22

20

15

19

30

17

23

17

23

18

16

16

14

18

16

13

12

25

32

27

16

24

24

24

18

21

26

23

11

26

21

36

24

0 25 50 75 100%

Global

Not challengingat all

Somewhatnot challenging

Neutral Challenging Verychallenging

13

13

15

20

15

19

11

23

29

19

26

37

17

24

12

31

20

18

9

10

17

13

8

7

23

33

35

23

33

26

36

21

15

17

16

10

19

19

33

19

0 25 50 75 100

Mitigate the impact of marketvolatility

Returns uncorrelated to broaderglobal markets

Positive investment returns in anenvironment of higher correlations

Strong performance returns whenmarkets rise

Strong performance returns whenmarkets are volatile

Strong performance in a low interestrate environment

Portfolios that are correlated whenmarkets go up but not correlated

when markets go downProvide suitable alternatives to

savings accounts or money marketproducts

%

France

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

14

Income is a big talking point when it comes to retirement in France, with advisers giving mixed views on the outlook.

One in six French advisors (15%) were not confident their client’s current investments are able to grow portfolios to meet retirement income needs (vs. 9% for other countries).

Despite the state of the country’s pension system, French advisors are remarkably confident in their ability to deliver sufficient income for clients in retirement - with only 9% suggesting they lack confidence.

How confident, generally speaking, are you that your client's current investments are able to?

31

20

2

8

13

15

9

61

61

39

61

57

64

53

8

19

59

31

31

21

38

0 25 50 75 100

Protect my portfolio fromdramatic swings in value

Preserve capital

Ensure appropriate portfoliodiversification

Take advantage of bull marketperiods

Protect client long-terminvestments from inflation

Grow portfolios to meetretirement income needs

Provide steady income forclients in retirement

%

France

18

13

3

11

6

9

8

61

61

39

53

63

68

65

21

27

58

36

31

23

28

0 25 50 75 100%

Global

Notconfident

Moderatelyconfident

Veryconfident

Other key points:

Less than one in five (19%) French advisors were very confident their client’s current investments can preserve capital (27% for other countries)

31% of French advisors were very confident their client’s current investments can take advantage of bull market periods (36% for other countries).

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

15

Portfolio Construction

Advisors in France were strongly receptive to the idea of introducing new methods to offer investors diversification in their portfolios.

Almost two-thirds (65%) of French advisors agreed that a traditional 60% equities/40% bonds split is no longer the best way to pursue returns and manage investment risk for most investors (vs. 49% for other countries).

68% of French advisors also agreed that financial advisers need to replace traditional diversification and portfolio construction techniques with new approaches to achieve results (vs. 59% for other countries).

Four in five (80%) of French advisors said financial advisers need more education, compared to 75% for other countries.

In terms of portfolio construction and management, to what extent do you agree with the following?

9

29

18

23

9

7

10

17

11

13

13

7

17

7

7

3

10

6

27

34

30

33

37

25

37

14

35

27

31

55

0 25 50 75 100

There are very few tools available toadequately remove the 'guesswork'

associated with managinginvestments in today's markets.

A traditional equities and fixedincome split is appropriate forinvestors with moderate risk

tolerance.

A traditional portfolio allocation is nolonger the best way to pursue returnand manage investment risk for most

investors.

Historical market data demonstratingthat longer holding periods decrease

the likelihood of a negativeannualized return is no longer valid.

Financial advisors need to replacetraditional diversification and

portfolio construction techniqueswith new approaches to achieve

results.

Financial advisors need moreeducation.

%

France

16

21

18

30

15

7

17

18

18

16

16

9

18

12

16

11

11

10

22

26

22

23

30

23

27

22

27

19

29

52

0 25 50 75 100%

Global

Stronglydisagree

Disagree Neither agreenor disagree

Agree Stronglyagree

Other data points on portfolio construction:

Historical market data demonstrating that longer holding periods decrease the likelihood of a negative annualized return is no longer valid – 60% of French advisors agreed (vs.42% for other countries).

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

16

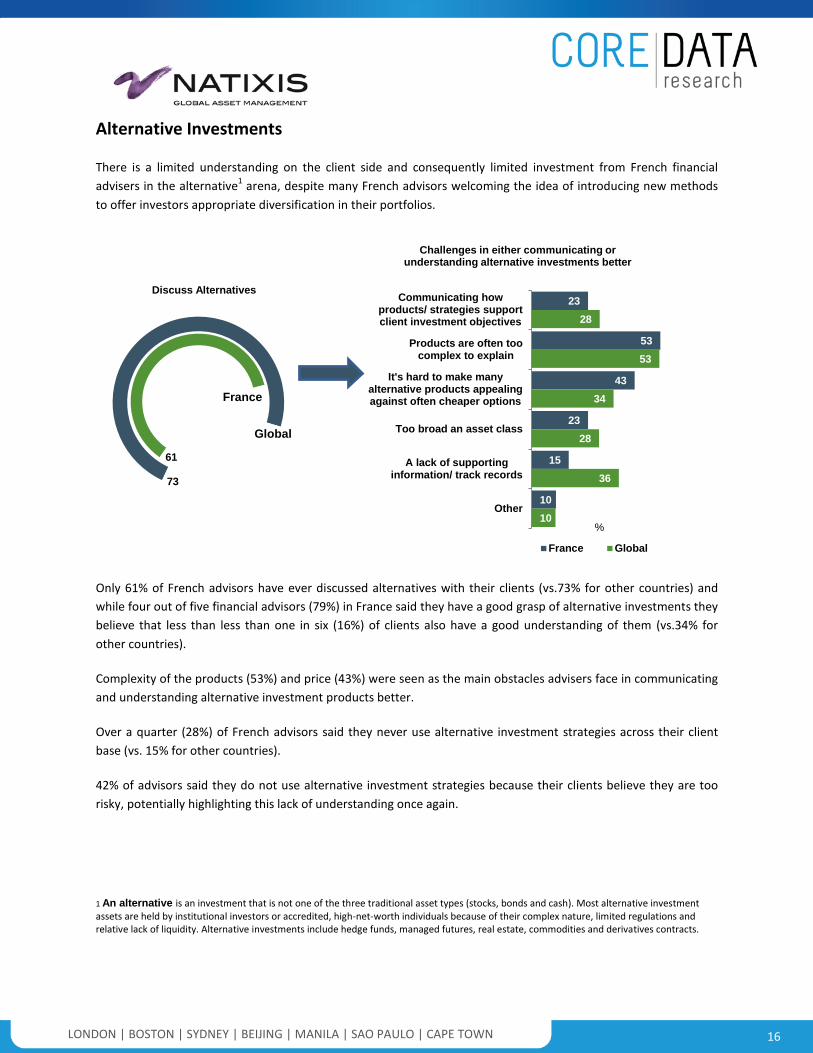

Alternative Investments

There is a limited understanding on the client side and consequently limited investment from French financial advisers in the alternative1 arena, despite many French advisors welcoming the idea of introducing new methods to offer investors appropriate diversification in their portfolios.

61

France

Global

73

23

53

43

23

15

10

28

53

34

28

36

10

Communicating howproducts/ strategies supportclient investment objectives

Products are often toocomplex to explain

It's hard to make manyalternative products appealingagainst often cheaper options

Too broad an asset class

A lack of supportinginformation/ track records

Other

%

France Global

Discuss Alternatives

Challenges in either communicating or understanding alternative investments better

Only 61% of French advisors have ever discussed alternatives with their clients (vs.73% for other countries) and while four out of five financial advisors (79%) in France said they have a good grasp of alternative investments they believe that less than less than one in six (16%) of clients also have a good understanding of them (vs.34% for other countries).

Complexity of the products (53%) and price (43%) were seen as the main obstacles advisers face in communicating and understanding alternative investment products better.

Over a quarter (28%) of French advisors said they never use alternative investment strategies across their client base (vs. 15% for other countries).

42% of advisors said they do not use alternative investment strategies because their clients believe they are too risky, potentially highlighting this lack of understanding once again.

1 An alternative is an investment that is not one of the three traditional asset types (stocks, bonds and cash). Most alternative investment assets are held by institutional investors or accredited, high-net-worth individuals because of their complex nature, limited regulations and relative lack of liquidity. Alternative investments include hedge funds, managed futures, real estate, commodities and derivatives contracts.

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

17

Usage of Alternative Investment Strategies Across Client Base

28

15

43

57

28

27

0 25 50 75 100

France

Global

%Never Infrequent Regular

Private equity (54%), shorting of shares (49%) and futures (46%) were the three main asset classes French advisers deem as alternative investments.

Which of the following would you consider to be Alternative Investment?

54

49

46

40

35

31

31

31

23

23

21

12

8

2

63

47

52

59

43

60

42

26

41

30

48

14

12

6

Private equity funds

Shorting of shares

Futures

Commodities

Currencies

Hedge funds

Options

ETFs

Real estate

Absolute return funds

Gold and other precious metals

Multi-Manager funds

International bonds

International shares

% France Global

The client segment French advisors believed is primarily suited to alternative strategies is the High Net Worth ($1m plus of assets) segment with 51.4% being inclined to offer these products (vs. 62.5% other countries).

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

18

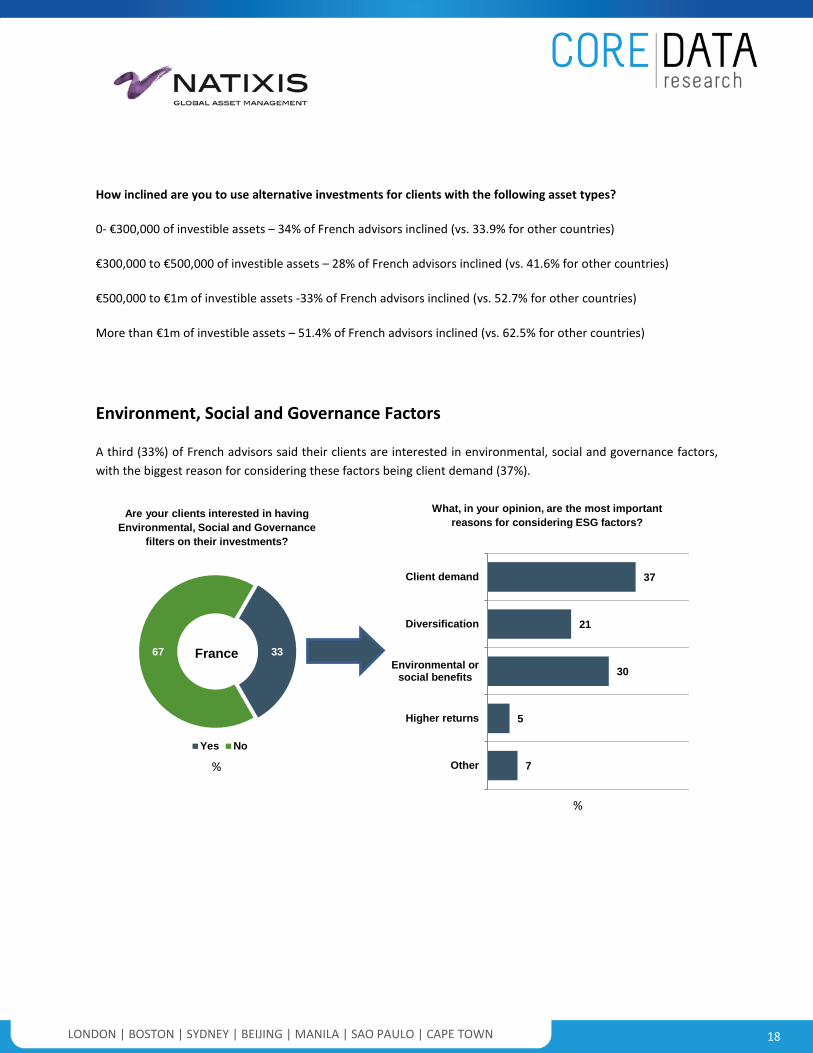

How inclined are you to use alternative investments for clients with the following asset types?

0- €300,000 of investible assets – 34% of French advisors inclined (vs. 33.9% for other countries)

€300,000 to €500,000 of investible assets – 28% of French advisors inclined (vs. 41.6% for other countries)

€500,000 to €1m of investible assets -33% of French advisors inclined (vs. 52.7% for other countries)

More than €1m of investible assets – 51.4% of French advisors inclined (vs. 62.5% for other countries)

Environment, Social and Governance Factors

A third (33%) of French advisors said their clients are interested in environmental, social and governance factors, with the biggest reason for considering these factors being client demand (37%).

3367 France

Yes No

37

21

30

5

7

Client demand

Diversification

Environmental orsocial benefits

Higher returns

Other

Are your clients interested in having Environmental, Social and Governance

filters on their investments?

What, in your opinion, are the most important reasons for considering ESG factors?

%

%

LONDON | BOSTON | SYDNEY | BEIJING | MANILA | SAO PAULO | CAPE TOWN

19

NOTES:

The study involved 1,300 financial advisors in nine countries and across four continents.

For France there were 150 participants.

Of these 95 were independent financial advisors, 14 were tied financial advisors, 34 were heads of an advice firm (practising advisors) and 7 were in other advisory roles.

The average client portfolio size was €712, 833. With regard to the firm’s asset level, the average firm represented by each advisor manages approximately €948.5 million.

The total level of assets of firms in France involved in the study amounted to €142.3 billion.

This communication is for information only. Analyses of the survey referenced herein are as of October 24, 2013. There can be no assurance that developments will transpire as may be forecasted in this material. This material may not be distributed, published or reproduced, in whole or in part. Although Natixis Global Asset Management believes the information provided in this material to be reliable, it does not guarantee the accuracy, adequacy or completeness of such information. In the EU (ex UK): Distributed by NGAM S.A., a Luxembourg management company authorized by the CSSF, or one of its branch offices. NGAM S.A., 51, avenue J.F. Kennedy, L-1855 Luxembourg, Grand Duchy of Luxembourg. Natixis Global Asset Management consists of Natixis Global Asset Management, S.A., NGAM Distribution, L.P., NGAM Advisors, L.P., NGAM S.A., and NGAM S.A.’s business development units across the globe, each of which is an affiliate of Natixis Global Asset Management, S.A. The affiliated investment managers and distribution companies are each an affiliate of Natixis Global Asset Management, S.A. • ngam.natixis.com This material should not be considered investment advice nor a solicitation to buy or an offer to sell any product or service to any person in any jurisdiction where such activity would be unlawful. Copyright © 2013 NGAM Advisors, L.P. – All rights reserved.