Embed Size (px)

Citation preview

3/9/15Happy Monday!!

Class Needs:whiteboard, rag, marker, textbook, calculator, notes from front table and your homework..(math packet)

Class Objectives:Review:

1. What is a down payment and how is it calculated and applied?2. What is a closing cost and how is/are it/they applied in the purchase of a home?3. How do you calculate how much cash you need to bring with you to “close” on a house?4. Be able to use an amortization table

Chapter 6 Owning a Home or

Car

Chapter 6 (Owning a Home)

6-1 Home buying (usually)requires:

Down payment – usually a given % amount of cash….this shows the bank you really want this house and are willing to pay for it.

The bank will tell you how large a % of a down payment you need.

(Usually represented as a %)

The balance of the purchase price (after the down payment) is usually borrowed through a mortgage loan taken with a bank or other lender.

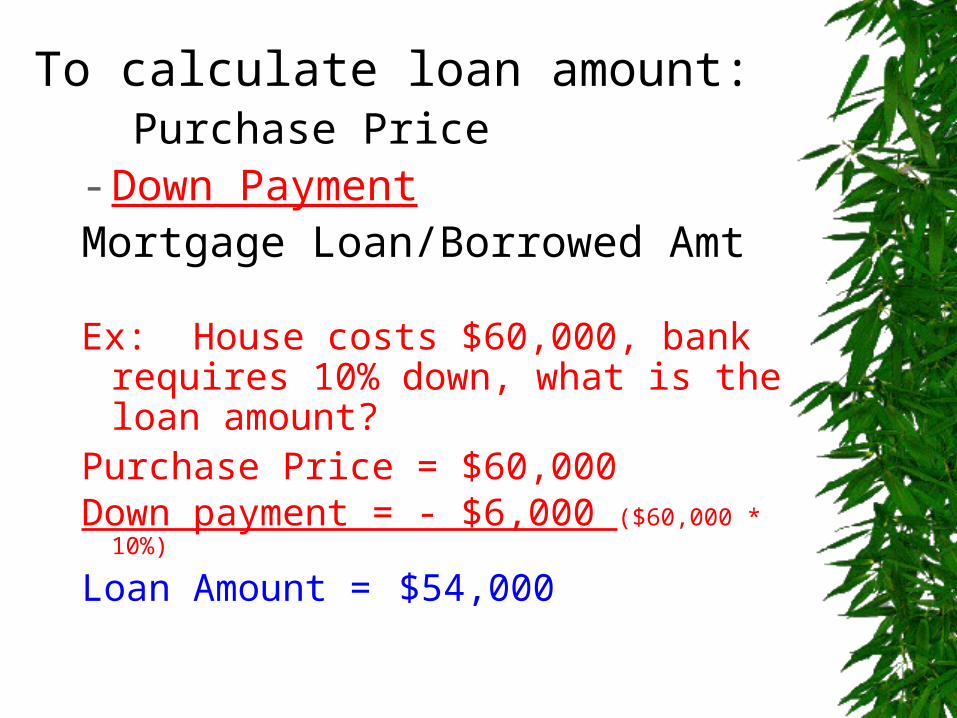

To calculate loan amount: Purchase Price- Down PaymentMortgage Loan/Borrowed Amt

To calculate loan amount: Purchase Price- Down PaymentMortgage Loan/Borrowed Amt

Ex: House costs $60,000, bank requires 10% down, what is the loan amount?

Purchase Price = $60,000Down payment = - $6,000 ($60,000 * 10%)

Loan Amount = $54,000

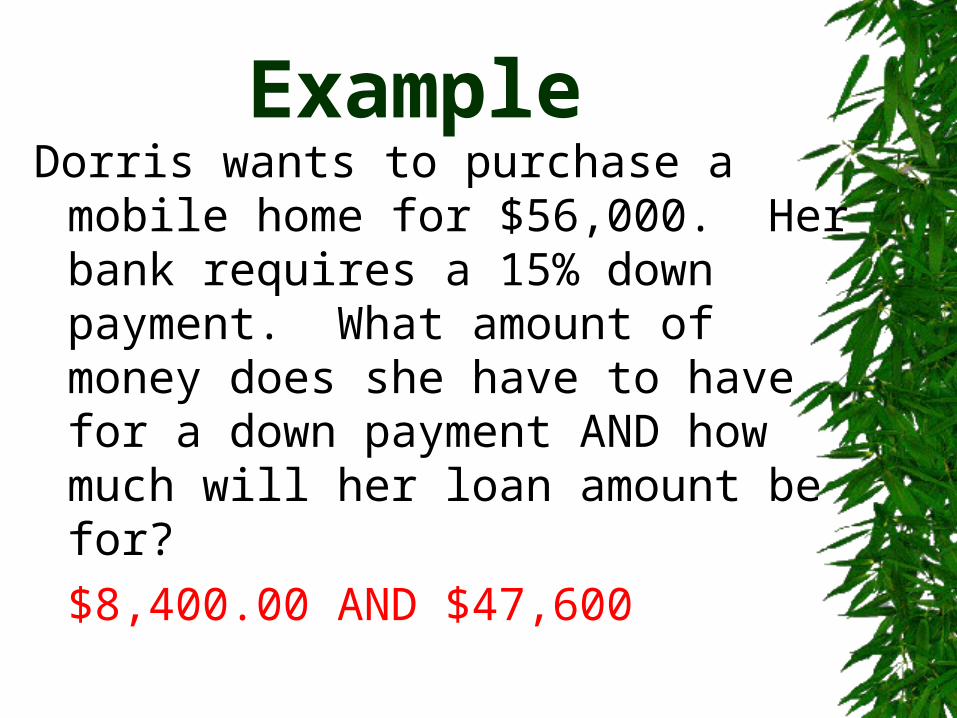

ExampleDorris wants to purchase a mobile

home for $56,000. Her bank requires a 15% down payment. What amount of money does she have to have for a down payment AND how much will her loan amount be for?

$8,400.00 AND $47,600

When you finish the last page of a book, what do you

usually do?The actual transaction to

purchase a house is called a Closing…however…

There are other costs involved than just paying

the down payment and getting the loan for the

balance.

These are called closing costs.

Please look at the situational questions in

your folders on your tables.

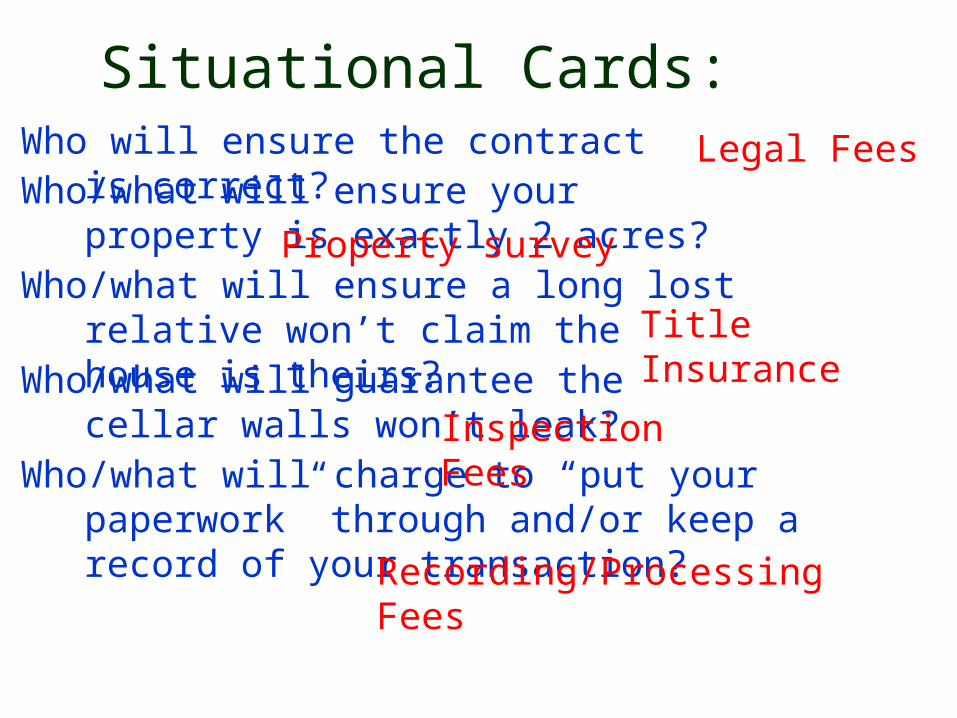

Situational Cards:Who will ensure the contract is correct?

Who/what will ensure a long lost relative won’t claim the house is theirs?

Who/what will ensure your property is exactly 2 acres?

Who/what will guarantee the cellar walls won’t leak?

Who/what will charge to “put your paperwork” through and/or keep a record of your transaction?

Legal Fees

Property survey

Title Insurance

Inspection Fees

Recording/Processing Fees

Closing Costs :these are fees and expenses paid to complete the transfer of ownership of a home. Closing costs range from 3% to 6% of the purchase price of the home and include:

legal fees title insurance appraisal fees inspection fees land surveys, …etc.

Closing costs can be listed individually OR it can be estimated as a percentage.

Where do closing costs come in?When you need to calculate how

much cash you must bring with you to the “closing”

To calculate cash needed to buy a home: Down Payment + Closing Costs Cash Needed to Buy a Home

At this “closing” is when you sign the bank papers for the loan.

Look try these examples:Hilda is buying a home for $74,000. She

will make a 20% down payment and estimates closing costs as:

1. What amount of money will she need to borrow for her mortgage loan?

$74,000 * .20= $14,800

$74,000-$14,800 = $59,200

Look try these examples:Hilda is buying a home for $74,000. She

will make a 20% down payment and estimates closing costs as:

Legal fees $950

Title insurance $140

Property survey $250

Inspection $175

Loan processing fee $ 84

Recording fee $740

1. What amount of cash will she need when she buys the house?

$14,800 (down payment) +

$2,339 (closing costs) = $17,139.00

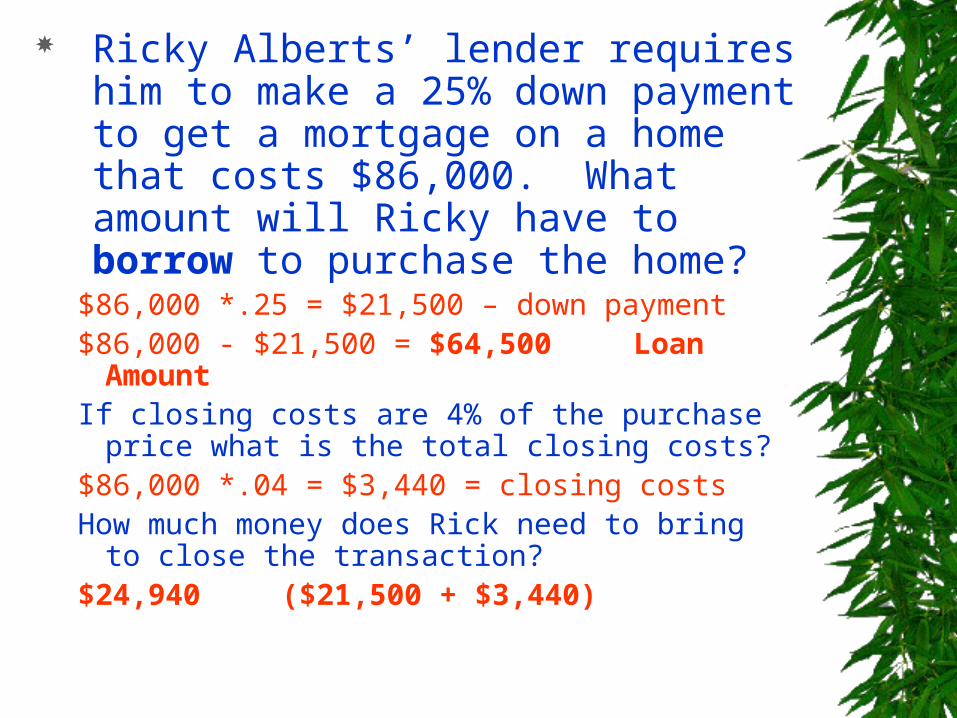

Ricky Alberts’ lender requires him to make a 25% down payment to get a mortgage on a home that costs $86,000. What amount will Ricky have to borrow to purchase the home?

$86,000 *.25 = $21,500 – down payment$86,000 - $21,500 = $64,500 Loan AmountIf closing costs are 4% of the purchase price what

is the total closing costs? $86,000 *.04 = $3,440 = closing costsHow much money does Rick need to bring to

close the transaction?$24,940 ($21,500 + $3,440)

Terri Wilburn will be able to purchase a condominium by making a 5% down payment on its $64,000 purchase price. She estimates her closing costs to be 3.5% of the purchase price. What amount of money will Terri need to pay the down payment and closing costs?

$64,000 * 5% = $3,200$64,000 * 3.5% = $2,240$6,425 + $2,240 = $5,440

Why do you think a bank would required a larger %

for down payment OR a higher interest rate?

Looking at the closing costs, what would make a

closing costs increase?

Can you explain?? How do you calculate a loan amount

with a down payment? What kind of items are included in

closing costs? How do you calculate how much cash

you need to bring with you to “close” on a house.

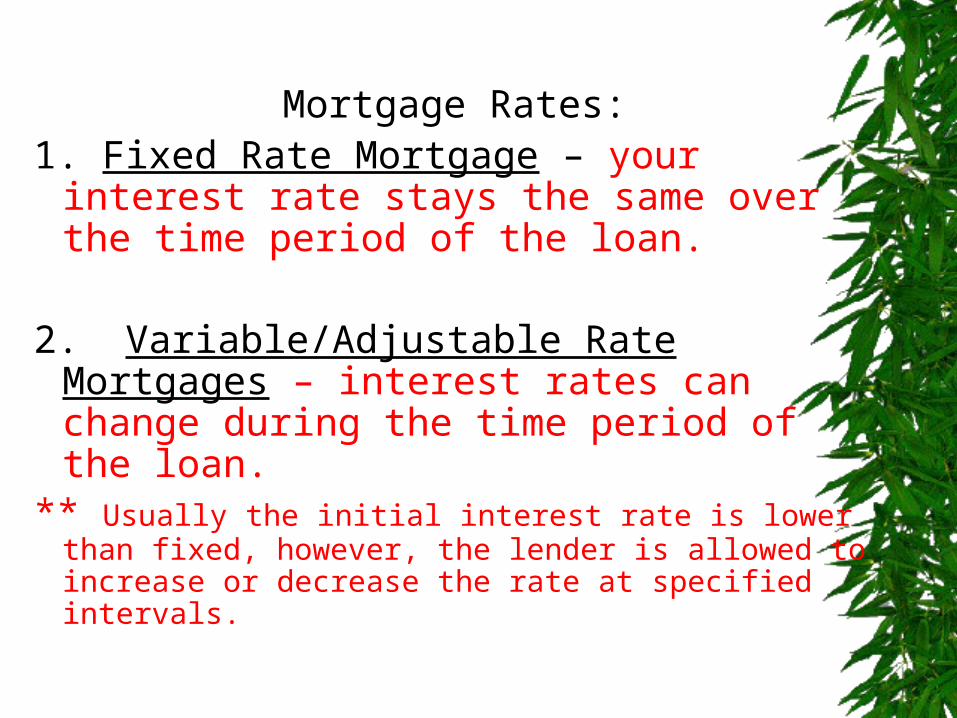

Mortgage Rates:1. Fixed Rate Mortgage – your interest

rate stays the same over the time period of the loan.

2. Variable/Adjustable Rate Mortgages –

interest rates can change during the time period of the loan.

** Usually the initial interest rate is lower than fixed, however, the lender is allowed to increase or decrease the rate at specified intervals.

Amortization TablesMost mortgages are repaid gradually,

or amortized, over the life of the mortgage in equal monthly payments. Each payment pays off part of the principal plus the interest due each month.

Look at the top of page 211..note how little principal is paid in the first few months compared to the last few.

Amortization TablesAt first, most of the monthly payment goes

to pay interest. As time passes, the amount that goes to repay the principal increases.

Most lenders allow customers to make additional payments toward the principal so the mortgage can be paid off earlier. These added payments reduce the total interest paid.

ExamplesUsing the table on page 211, what is my

monthly payment for a $45,000 mortgage taken out for 30 years at 6% interest?$ 269.80…how many times(months) did you make this payment?12 * 30 = 360How much did you pay for this $45,000 loan at the end of the term?269.80 * 360 = $97,128.00

3/18/14Class Needs:

whiteboard, rag, marker, textbook, calculator, workbook pg 71-72

ExampleOlivia wants to buy a home that costs

$83,000. She has $13,000 for the down payment and her bank will loan her $70,000 on a 25-year, 8% mortgage. Find Olivia’s monthly payments and the total amount of interest she would pay of the term of the mortgage.Monthly Payment = $540.27$540.27 * 25 years * 12 months per year = $162,081 (amount paid after 25 years)$162,081 - $70,000 = $92,081 (interest)

Review:Page 212 Letters C and D

C. $620.24; $68,857.60

D. $257.72; $37,316

3/19/14Class Needs:

Log into computerwhiteboard, rag, marker,

textbook, calculator, workbook pg 71-72

When interest rates go down, business firms and property owners may replace their fixed or variable rate mortgages with another mortgage at a lower interest rate….this is called refinancing.

Refinancing a Mortgage – when you take out a new mortgage and use that money to pay off the old mortgage. You must also pay new closing costs that are incurred.

Look at page 213 Example.. E and FE. $748

F. $71

Please open workbooks to page 72We will do together

3/13/15Happy Friday!!

Class Needs:textbook, calculator, notes

and your homework

3/16/15Class Needs:

textbook, calculator and notes

6-2 Renting or Owning a Home

Cost of Ownership…Owning a home comes with expenses:

Property taxes Repairs Maintenance Utilities Insurance Trash pick up…etc

Two less obvious expenses:

1. Depreciation

2. Loss of Income on the money invested in the home.

Depreciation

1. The loss of value of property caused by aging and use….ex: roof, heating costs, not updating

Most housing depreciates slowly at about 1% to 4% of its original value per year.

Amount of depreciation can’t be calculated until a house is sold

Loss of Income on the money invested in the home.

1. Occurs because the money initially invested in buying the property (down payment and closing costs) could have been deposited in a savings account and earned interest.

Then why own? …people can include the interest they pay on their home mortgage and property taxes they pay on their tax return….this reduces taxable income…you pay less taxes and have equity in a house.

Equity - The difference between what is owed on a home and its value.

There is a net cost to owning a house…look on page 217 Ex 1.

The Krafts want to buy a home. Their estimated first-year expenses are: mortgage interest, $6,848; property taxes, $3,782; insurance, $560; depreciation, $1,790; utilities, $1,300; and maintenance and repairs, $2,050. They estimate lost interest income on savings to be $1,562. Income tax savings are estimated to be $1,320. Find their net cost of home ownership for the first year.

$ 16,572.00

Please do #B on page 218

B. $12,629

Costs of Property RentalSome people can’t afford to buy or don’t want

the hassle of maintenance…so they rentRenters:1. Usually pay a one time security deposit in

addition to their first month’s rent…this covers any damage done while living there…if there is no damage, the money is returned.

2. Sign a lease or rental agreement that they will be there for a stated period of time.

3. Insurance – renter’s insurance is optional, but recommended…it covers you for the lost of items due to theft or fire.

Joe wants to rent my apartment for $450 a month. Before he moves in he has to pay his first month’s rent and one month’s rent as a security deposit. He signs a lease for 12 months. After 1 year he moves out. After inspecting his apartment I find:

1.Hole in wall ($50 to fix)

2.Nails in wall from pictures hung ($25 to fix)

3.Cracked/broken back window($130 to replace)

4.How much of his security deposit should he get back? (reasonable versus damage)

5.$450 - $50 - $130 = $270

Sue rented an apartment for one year and paid $625 monthly rent. Her other apartment-related costs for the year were: security deposit of $625; insurance, $85; utilities, $1,210; replacement of lost mailbox key, $10. What was the cost of renting the apartment for one year?

$9,430

Page 218 #D

$19,286

Compare Renting and Owning Homes

When you rent, you consider the monthly rent as an expense, however when you pay your mortgage, that is not considered an expense, but the interest, utilities and everything else is.

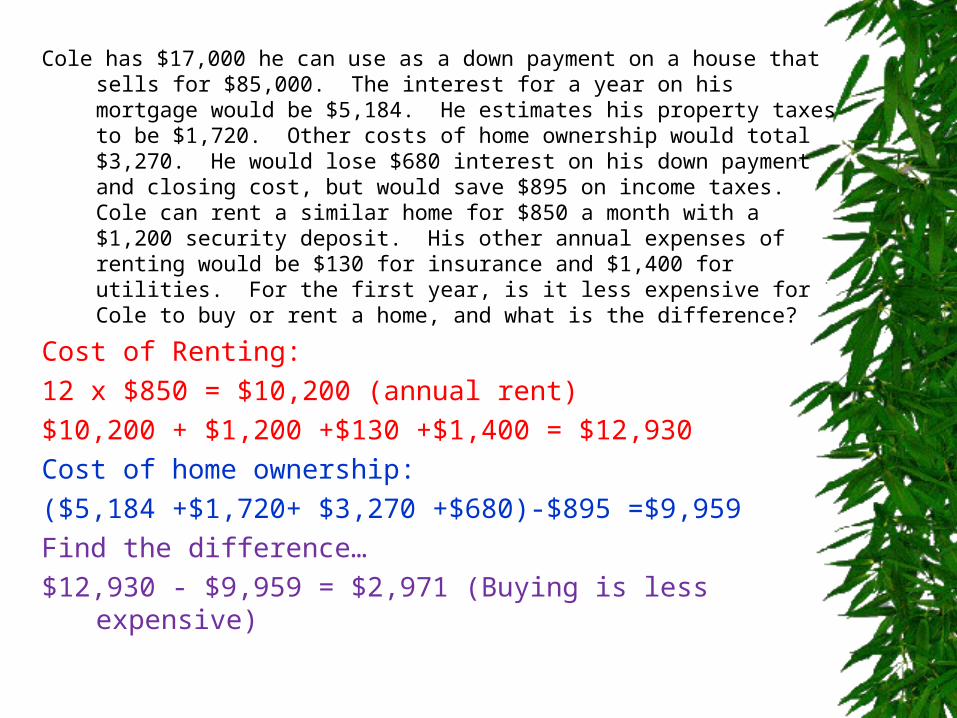

Cole has $17,000 he can use as a down payment on a house that sells for $85,000. The interest for a year on his mortgage would be $5,184. He estimates his property taxes to be $1,720. Other costs of home ownership would total $3,270. He would lose $680 interest on his down payment and closing cost, but would save $895 on income taxes. Cole can rent a similar home for $850 a month with a $1,200 security deposit. His other annual expenses of renting would be $130 for insurance and $1,400 for utilities. For the first year, is it less expensive for Cole to buy or rent a home, and what is the difference?

Cost of Renting:

12 x $850 = $10,200 (annual rent)

$10,200 + $1,200 +$130 +$1,400 = $12,930

Cost of home ownership:

($5,184 +$1,720+ $3,270 +$680)-$895 =$9,959

Find the difference…

$12,930 - $9,959 = $2,971 (Buying is less expensive)

Textbook Page 221 #9-13

9. $20,528

10. $12,062

11. $4,068

12. $18,910

13. Buying save $1,022

Homework – Workbook pages 73

Homework – Workbook pages 74

Workbook Page 74

6. $3,806

7. $15,914

8. $15,174; $1,426

9. Renting by $1,025

6-3 Property Taxes

Property taxes – taxes on the value of real estate such as homes, business property, or farm land.

Usually collected annually or semiannually by the tax department of the town or city you live in.

Services paid for by taxes: Schools Government operations Fire protection Police protection Parks Road maintenance

Taxes are paid based on the assessed value…

An assessed value is usually calculated by local tax assessors and is usually a percentage of the actual value of your house…

Ex:Bill Watson’s home is valued at $150,000.00. It is assessed at 40% of its market value or $60,000.00.

Taxes are then calculated on the assessed value of $60,000.00

Local tax districts determine the tax rate needed to pay for the services they provide.

They estimate their expenses for the coming year and prepare an expense budget. They also estimate income from sources other than property tax, such as licenses, fee, fines, rents, state aid and so on.

The difference between the total budget and the income from other sources is the amount that must be raised by the property tax.

Local tax districts then determine the decimal tax rate, which is the tax rate at which property is to be taxed.

Decimal tax rate = amount to be raised by property tax

Total assessed value

The Columbia School District’s total budgeted expenses last year were $6,000,000. Estimated income from other sources was $1,800,000. The total assessed value of all taxable property in Columbia last year was $39,999,000. Find the decimal tax rate needed to meet expenses, rounded to the nearest hundred thousandth.

$6,000,000 - $1,800,000 = $4,200,000 (property tax needed)

$39,999,000

= .107692

Fiber County’s budget for a year is $6,750,000. Of that, $650,000 is raised from other income, and the rest from property taxes. The total assessed value of the county’s property is $80,000,000. What is the decimal tax rated, rounded to the nearest thousandth?– $6,750,000 – $650,000 = $6,100,000– $6,100,000 / $80,000,000 = – 0.076

The Gayle Fire District must raise $1,950,000 from property taxes. The assessed value of property in the district is $48,200,000. What is the decimal tax rate needed, to the nearest ten thousandth?– $1,950,000 / $48,200,000 =

– 0.045

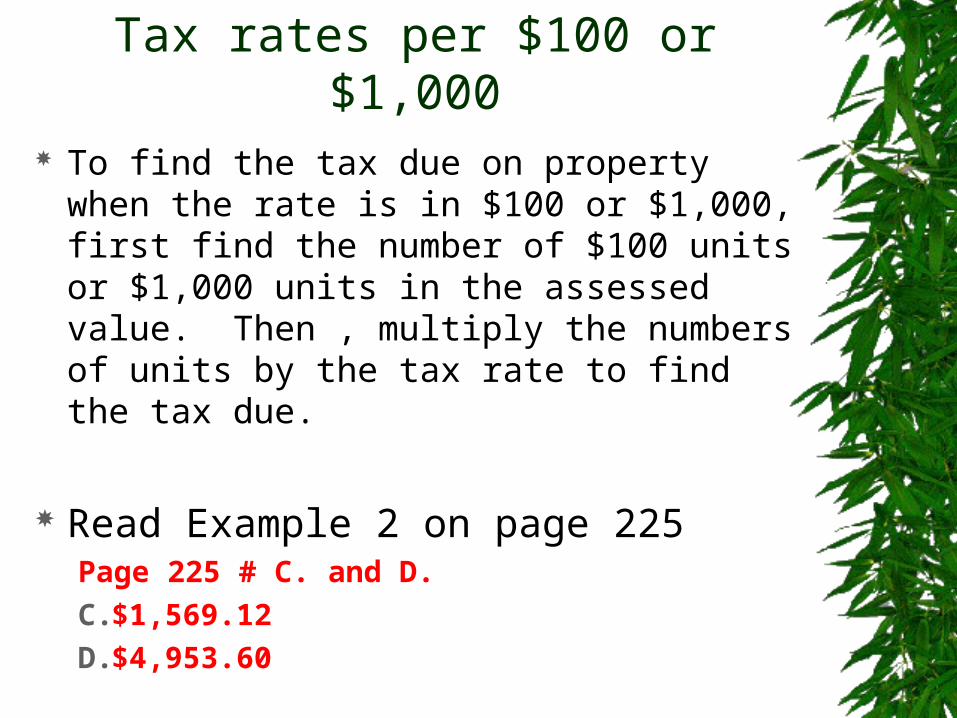

Tax rates per $100 or $1,000 To find the tax due on property when the

rate is in $100 or $1,000, first find the number of $100 units or $1,000 units in the assessed value. Then , multiply the numbers of units by the tax rate to find the tax due.

Read Example 2 on page 225Page 225 # C. and D.

C.$1,569.12

D.$4,953.60

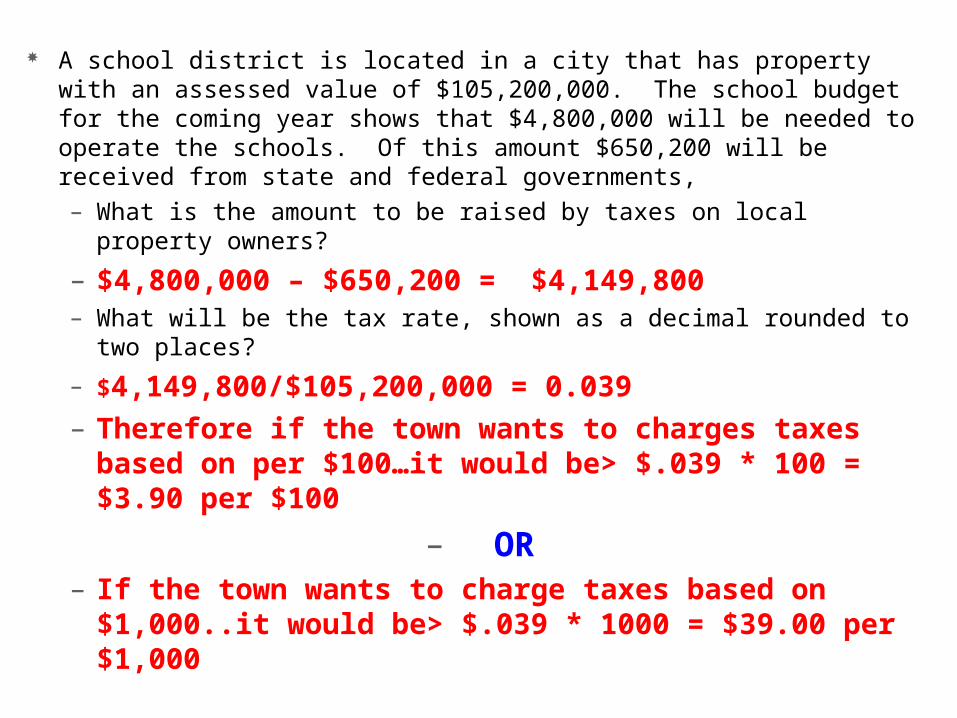

A school district is located in a city that has property with an assessed value of $105,200,000. The school budget for the coming year shows that $4,800,000 will be needed to operate the schools. Of this amount $650,200 will be received from state and federal governments, – What is the amount to be raised by taxes on local property owners?

– $4,800,000 – $650,200 = $4,149,800– What will be the tax rate, shown as a decimal rounded to two places?

– $4,149,800/$105,200,000 = 0.039– Therefore if the town wants to charges taxes based on

per $100…it would be> $.039 * 100 = $3.90 per $100

– OR– If the town wants to charge taxes based on $1,000..it

would be> $.039 * 1000 = $39.00 per $1,000

4/13/15Class Needs:

spring review math packets

whiteboard, rag, marker, textbook, notes, calculator,

workbooks

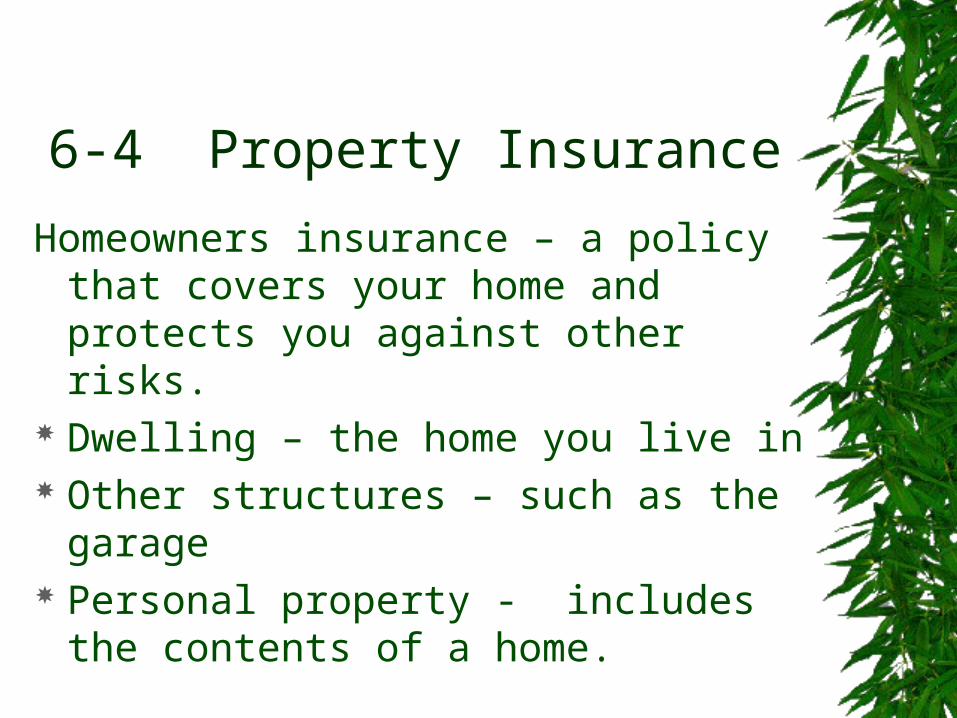

6-4 Property Insurance

Homeowners insurance – a policy that covers your home and protects you against other risks.

Dwelling – the home you live in Other structures – such as the garage Personal property - includes the

contents of a home.

6-4 Property InsuranceAdditional living expense – which pays

for the extra cost of living when you cannot use your own home because of damage.

Personal liability – which protects you in case of lawsuits by person injured on your property

Medical payments to others, but not to you or your family, for medical expenses in case of injury on your property.

Con’tFace value – the amount for which your

home is insured for.

Personal property is usually covered for 50% of the face value.

Additional living expense coverage is typically 20% of the face value.

Other options – off premises…covers property away…usually 10% of face value.

Con’tReplacement Cost Policy – the

insurance company will pay to replace an item at current prices.– Insurers usually require a survey and

inspection of the property and it must be insured for 100% of its current replacement value.

– Premiums are 10-15% higher for extra coverage.

Con’tInsurance premiums – the money paid to

an insurance company for property insurance….cost depends on many things…

kind of coverage, how house is built, location…

***Some items such as jewelry, computer, expensive stereos are not covered by a basic policy…it will cost more.

Con’tNolan insured his home for $61,000.

Find the annual premium, to the nearest dollar, he will pay for a policy that costs $.46 per $100.

$281.00

Mandy insures her home for $43,000. What annual premium will she pay if the policy cost is $0.74 per $100?

$318.20

Con’tRenters Insurance Premiums – provides

protection similarly as homeowner except for loss of the dwelling.

Page 232 C. and D.

C. $9,950

D. $64,500

Collecting on Insurance Claims…

- file paperwork, inspector…pay less deductible

Deductible – the amount you are responsible for paying

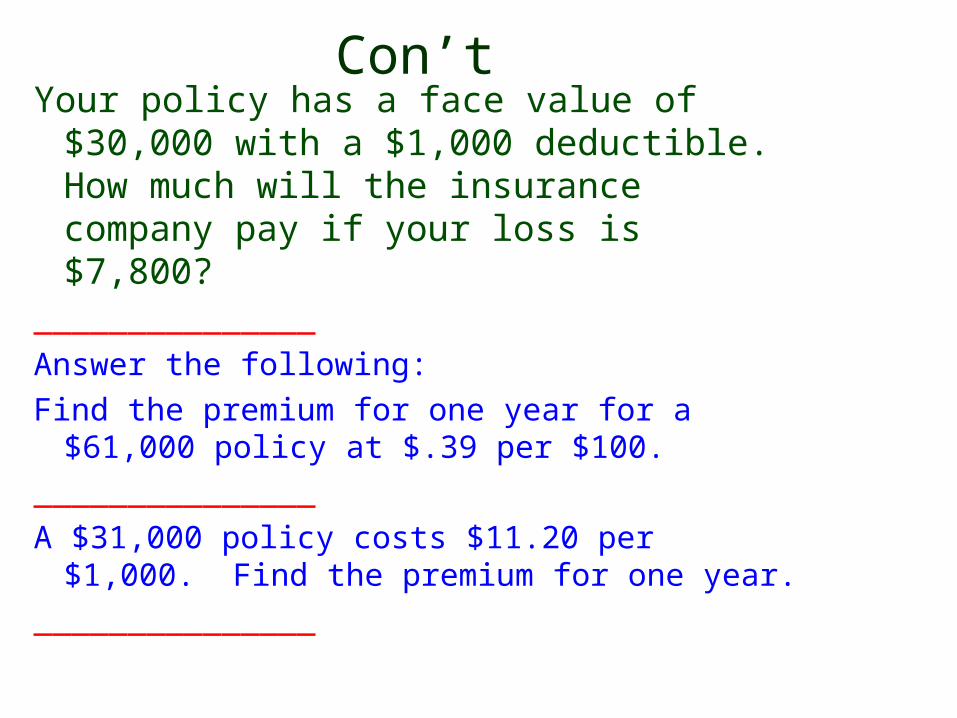

Con’tYour policy has a face value of $30,000

with a $1,000 deductible. How much will the insurance company pay if your loss is $7,800?

$6,800

Answer the following:

Find the premium for one year for a $61,000 policy at $.39 per $100.

$237.90

A $31,000 policy costs $11.20 per $1,000. Find the premium for one year.

$347.20

Homework:

Workbook pages 77-78

This will be graded tomorrow

6-5 Buying a Car

MSRP – Manufacturer’s Suggested Retail Price….also known as sticker price

Car buyers usually do not pay this price…they negotiate a price to pay based on trade in, rebates, and loan options.

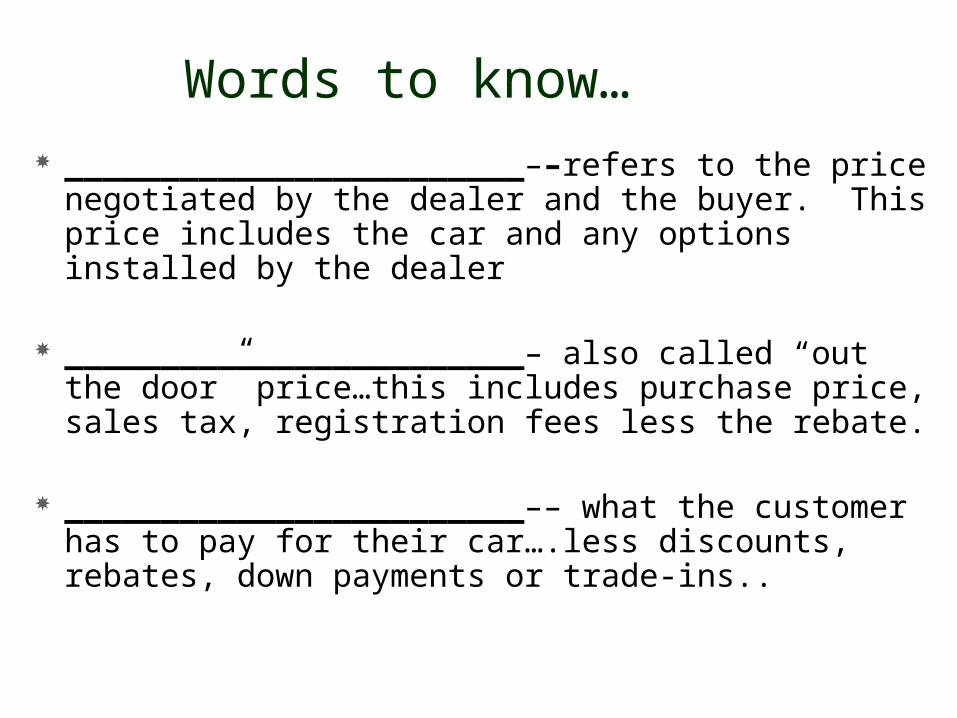

Purchase Price –refers to the price negotiated by the dealer and the buyer. This price includes the car and any options installed by the dealer

Delivered Price – also called “out the door”

price…this includes purchase price, sales tax, registration fees less the rebate.

Balance Due – what the customer has to pay for

their car….less discounts, rebates, down payments or trade-ins..

Words to know…

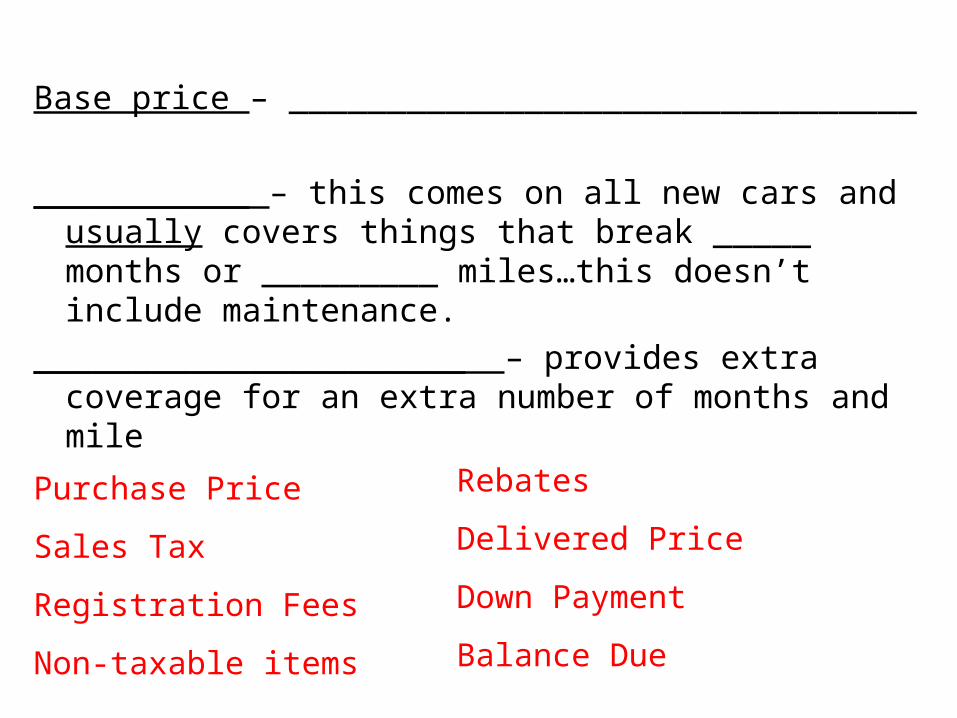

Base price – price for a model with just the standard features.

Warranty – this comes on all new cars and usually covers things that break 36 months or 36,000 miles…this doesn’t include maintenance.

Extended warranty – provides extra coverage for a number of months and mile

Purchase Price

Sales Tax

Registration Fees

Non-taxable items

Rebates

Delivered Price

Down Payment

Balance Due

6-6 Car Purchases and Leases

The delivered price of a car purchase may be paid in cash, however, most people make a down payment and take out installment loans.

6-6 Car Purchases and Leases

The delivered price of Sue’s car is $23,560. She makes a $2,000 down payment and pays the balance in 48 monthly payments of $560. What total amount did Sue pay for the car, AND what was the finance charge?

1. $2,000 + $26,880 (560 x 48) =

2. $28,880 - $23,560 =

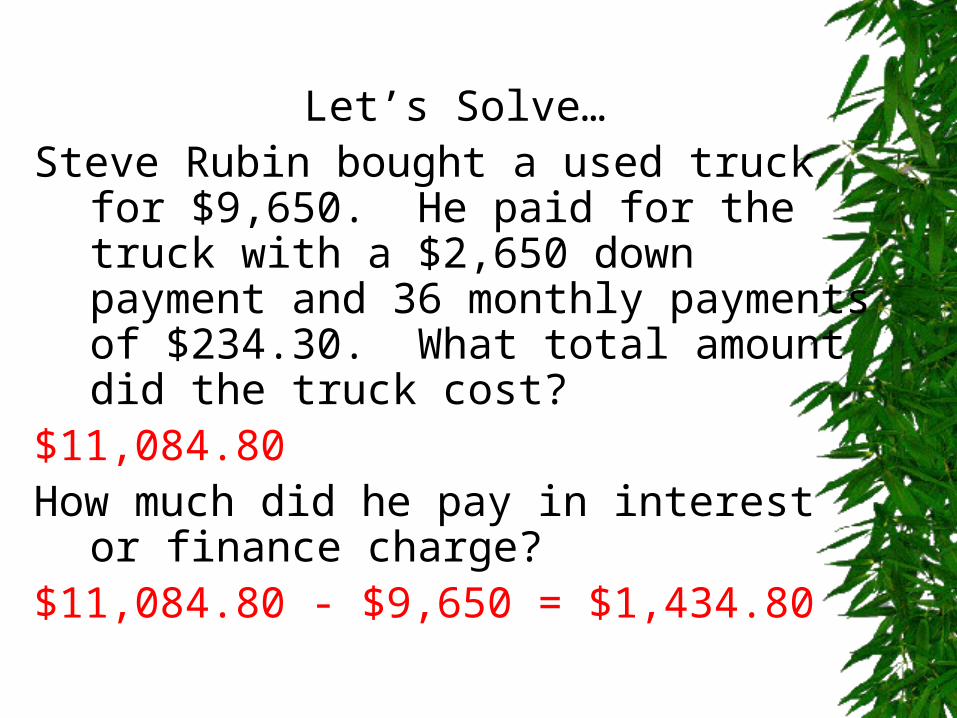

Let’s Solve…Steve Rubin bought a used truck for

$9,650. He paid for the truck with a $2,650 down payment and 36 monthly payments of $234.30. What total amount did the truck cost?

$11,084.80How much did he pay in interest or

finance charge?$11,084.80 - $9,650 = $1,434.80

Let’s Solve…Angie bought a luxury car for $47,850

and made a $4,500 down payment. She got a special loan rate of 2.1% for 60 months. Her monthly payments were $780.30. What was her finance charge on this car?

$780.30 * 60 = $46,818 + $4,500 = $51,318.00

$51,318 – $47,850 = $3,468

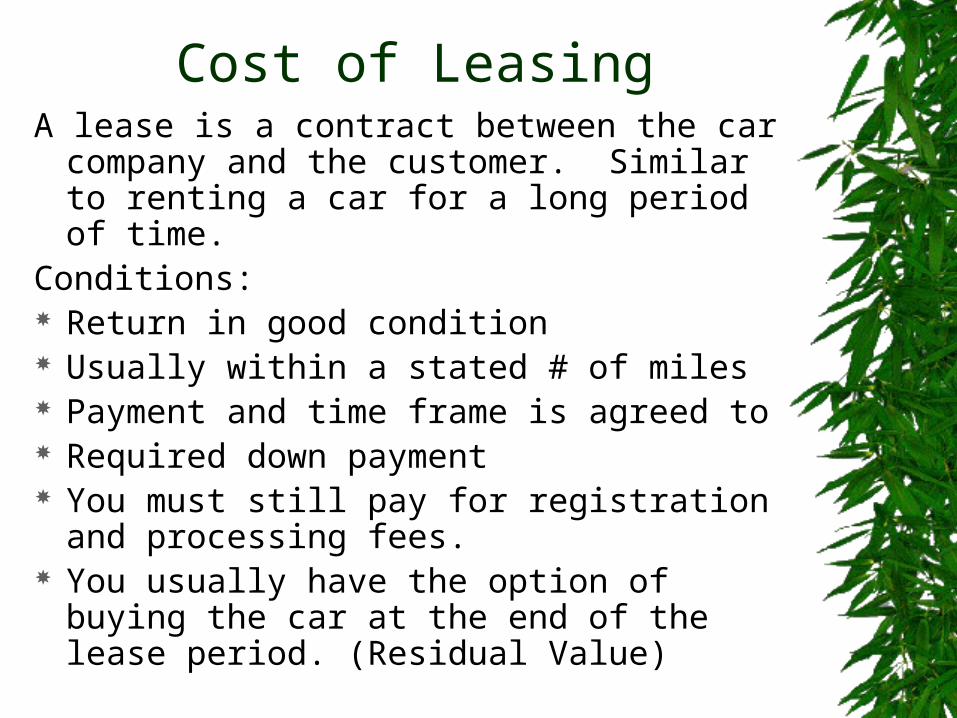

Cost of LeasingA lease is a contract between the car

company and the customer. Similar to renting a car for a long period of time.

Conditions: Return in good condition Usually within a stated # of miles Payment and time frame is agreed to Required down payment You must still pay for registration and

processing fees. You usually have the option of buying the

car at the end of the lease period. (Residual Value)

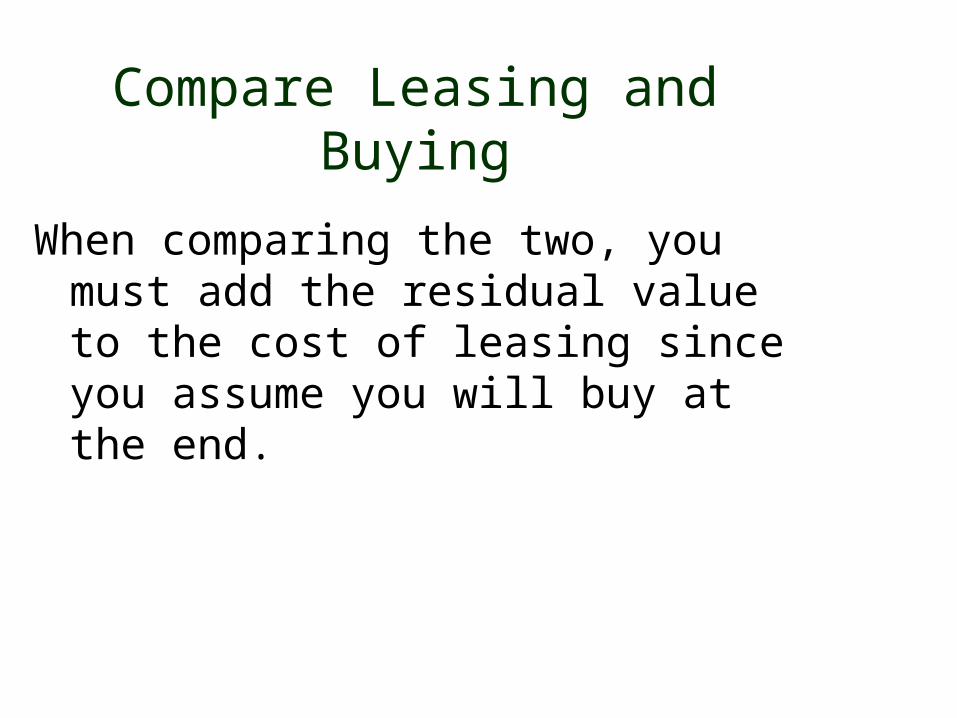

Compare Leasing and Buying

When comparing the two, you must add the residual value to the cost of leasing since you assume you will buy at the end.

Residual value is the amount of money you would get for your car after the lease is over….if you were to buy it.

Wilbur and his dealer negotiated a price of $27,400 for a new car. He can lease the car for $496 for 36 months and buy it at the end of the lease for its residual value of $16,200. If he buys the car now his month loan payment will be $822 for three years after making a $2,000 down payment . What is the total cost of purchasing the car under each plan? Which is less expensive?

Lease: $496 * 36 = $17,856$17,856 + $16,200 = $34,056

Buy: $822 * 36 = $29,592$29,592 + $2,000 = $31,592 Difference: $34,056 – $31,592 = $2,464

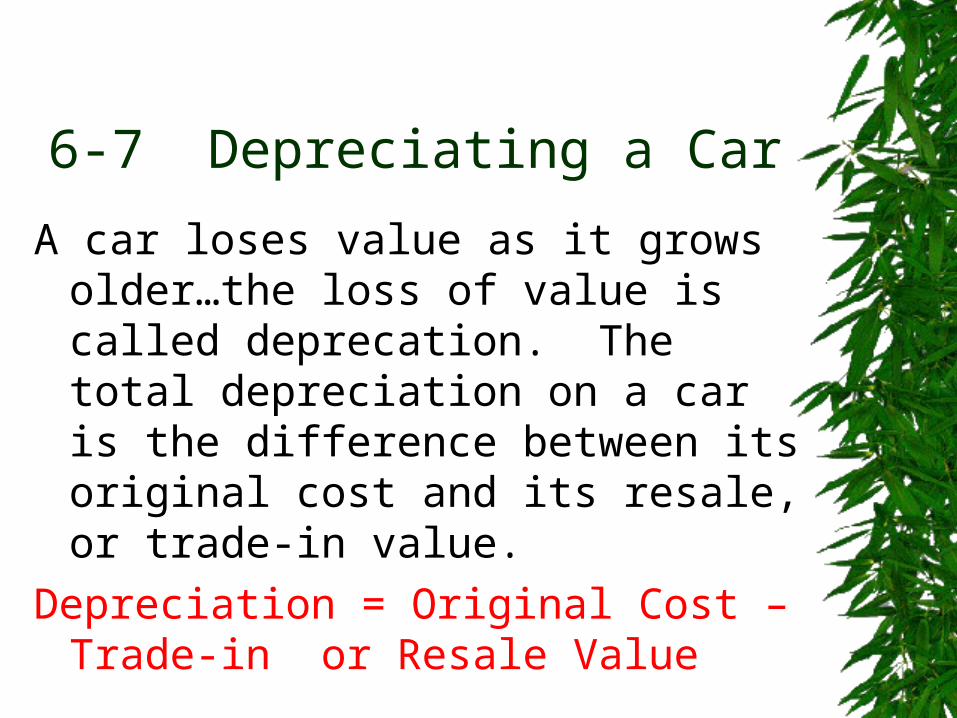

6-7 Depreciating a Car

A car loses value as it grows older…the loss of value is called deprecation. The total depreciation on a car is the difference between its original cost and its resale, or trade-in value.

Depreciation = Original Cost – Trade-in or Resale Value

6-7 Depreciating a Car

When you buy a car, you can only estimate what the depreciation will be. The actual amount of depreciation will be known only when the car is sold or traded in.

Lori bought a car for $14,800. She estimates her trade-in will be $5,800 after 4 years. Her depreciation will be…

$14,800- $5,800 = $9,000

Her annual depreciation will be…

$9,000/4 = $2,250

Rate of Depreciation = average annual depreciation divided by original cost.

Her rate of depreciation is…

$2,250 / $14,800 = .15 or 15%

6-8 Cost of Owning a Car

Look at pages 81-82

in your workbook

6-8 Cost of Owning a Car

Car Insurance:

There are 4 basic types of insurance or coverage for motor vehicles that protect you against the risk of financial loss:

6-8 Cost of Owning a Car1. Bodily Injury – covers your liability for injury

to others.2. Property damage – covers damage to other

people’s property including their vehicles.3. Collision – covers damage to your own motor

vehicle.4. Comprehensive damage – covers damage or

loss to your vehicle from fire, theft, vandalism, hail, and other causes.

$25/$50,000 – means a maximum of $25,000 per person, and $50,000per accident will be paid by the insurance company.

Costs of Operating Cars…

The total operating cost for a car is the sum of all the annual expenses of using the car.

These expenses include:•Insurance

•Gas

•Oil

•License

•Inspection fees

•Tires

•Repairs

•Garage rent

•Parking fees

•Taxes

•Depreciation

•Interest lost on down payment

Chapter 6 Owning a Home or

Car

Chapter 6 Owning a Home or

Car

Chapter 6 (Owning a Home)

6-1 Home buying (usually)requires:

Down payment – _________________

_______________________________

_______________________________ (Usually represented as a %)

The balance of the purchase price (after the down payment) is usually borrowed through a mortgage loan taken with a bank or other lender.

To calculate loan amount: ______________________- ______________________=______________________

To calculate loan amount: Purchase Price- Down PaymentMortgage Loan/Borrowed Amt

Ex: House costs $60,000, bank requires 10% down, what is the loan amount?

Purchase Price = _______________Down payment = _______________Loan Amount = _____________

ExampleDorris wants to purchase a mobile home

for $56,000. Her bank requires a 15% down payment. What amount of money does she have to have for a down payment AND how much will her loan amount be for?

_____________________________

Situational Cards:Who will ensure the contract is correct?

Who/what will ensure a long lost relative won’t claim the house is theirs?

Who/what will ensure your property is exactly 2 acres?

Who/what will guarantee the cellar walls won’t leak?

Who/what will charge to “put your paperwork” through and/or keep a record of your transaction?

____________

________________

___________

_______________

________________________

Closing Costs :these are fees and expenses paid to complete the transfer of ownership of a home. Closing costs range from _____ to ______of the purchase price of the home and include:

_____________ _____________ _____________ _____________ _____________

Closing costs can be listed individually OR it can be estimated as a percentage.

Where do closing costs come in?When you need to calculate how much

cash you must bring with you to the “closing”

To calculate cash needed to buy a home: ______________ + _____________________________________

At this “closing” is when you sign the bank papers for the loan.

Look try these examples:Hilda is buying a home for $74,000. She

will make a 20% down payment and estimates closing costs as:

1. What amount of money will she need to borrow for her mortgage loan?

_______________________________________

Look try these examples:Hilda is buying a home for $74,000. She

will make a 20% down payment and estimates closing costs as:

Legal fees $950

Title insurance $140

Property survey $250

Inspection $175

Loan processing fee $ 84

Recording fee $740

1. What amount of cash will she need when she buys the house?

________________

Ricky Alberts’ lender requires him to make a 25% down payment to get a mortgage on a home that costs $86,000. What amount will Ricky have to borrow to purchase the home?

______________________________________________________________________________If closing costs are 4% of the purchase price what

is the total closing costs? _______________________________________How much money does Rick need to bring to

close the transaction?________________________________________

Terri Wilburn will be able to purchase a condominium by making a 5% down payment on its $64,000 purchase price. She estimates her closing costs to be 3.5% of the purchase price. What amount of money will Terri need to pay the down payment and closing costs?

______________________________ ____________________________________________________________

Why do you think a bank would required a larger % for

down payment OR a higher interest rate?

Looking at the closing costs, what would make a

closing costs increase?

Can you explain?? How do you calculate a loan amount

with a down payment? What kind of items are included in

closing costs? How do you calculate how much cash

you need to bring with you to “close” on a house.

Mortgage Rates:1. Fixed Rate Mortgage – _________________________________________ 2. Variable/Adjustable Rate Mortgages

– ___________________________________________________________** Usually the initial interest rate is lower than

fixed, however, the lender is allowed to increase or decrease the rate at specified intervals.

Amortization TablesMost mortgages are repaid gradually, or

amortized, over the life of the mortgage in equal monthly payments. Each payment pays off part of the principal plus the interest due each month.

Amortization tables allow a person to easily calculate a monthly mortgage amount..

(we can also use them on the computer)

Look at the top of page 211..note how little principal is paid in the first few months compared to the last few.

Amortization TablesAt first, most of the monthly payment goes

to pay interest. As time passes, the amount that odes to repay the principal increases.

Most lenders allow customers to make additional payments toward the principal so the mortgage can be paid off earlier. These added payments reduce the total interest paid.

ExamplesUsing the table on page 211, what is

my monthly payment for a $45,000 mortgage taken out for 30 years at 6% interest?______________________________

_______________________________How much did you pay for this $45,000 loan at the end of the term? _____________________________

ExampleOlivia wants to buy a home that costs

$83,000. She has $13,000 for the down payment and her bank will loan her $70,000 on a 25-year, 8% mortgage. Find Olivia’s monthly payments and the total amount of interest she would pay of the term of the mortgage.Monthly Payment = ____________Amount paid after 25 years = __________$________ - $______ = $_____ (interest)

Review:Page 212 Letters C and D

C. ______________

D. ______________

When _____________________, business firms and property owners may replace their fixed or variable rate mortgages with _____________at a __________ interest rate….this is called _______________.

Refinancing a Mortgage – _____ ________________________________________________________________________________. You must also _______________ that are incurred.

Look at page 213 ExampleE. ___________

F. ___________

6-2 Renting or Owning a Home

Cost of Ownership…Owning a home comes with expenses:

____________________ ____________________ ____________________ ____________________ ____________________ ____________________

Two less obvious expenses:

1. Depreciation

2. Loss of Income on the money invested in the home.

Depreciation

1. The loss of value of property caused by aging and use….ex: roof, heating costs, not updating

Most housing depreciates slowly at about ___________ of its original value per year.

Amount of depreciation can’t be calculated until a house is sold.

Loss of Income on the money invested in the home.

1. Occurs because the money initially invested in buying the property (down payment and closing costs) could have been deposited in a savings account and earned interest.

Then why own? …people can include the interest they pay on their home mortgage and property taxes they pay on their tax return….this reduces taxable income…you pay less taxes and have equity in a house.

Equity - The difference between what is owed on a home and its value.

There is a net cost to owning a house…look on page 217 Ex 1.

The Krafts want to buy a home. Their estimated first-year expenses are: mortgage interest, $6,848; property taxes, $3,782; insurance, $560; depreciation, $1,790; utilities, $1,300; and maintenance and repairs, $2,050. Income tax savings are estimated to be$1,320. Find their net cost of home ownership for the first year.

$ ___________

Costs of Property RentalSome people can’t afford to buy or don’t want

the hassle of maintenance…so they rentRenters:1. Usually pay a one time security deposit in

addition to their first month’s rent…this covers _________________________,if there is ______________, the money is _________.

2. Sign a __________or ______________ that they will be there for a _______________

3. Insurance – renter’s insurance is _______, but __________________, it covers you for the lost of items due to theft or fire.

Sue rented an apartment for one year and paid $625 monthly rent. Her other apartment-related costs for the year were: security deposit of $625; insurance, $85; utilities, $1,210; replacement of lost mailbox key, $10. What was the cost of renting the apartment for one year?

___________________

Page 218 #D

___________________

Compare Renting and Owning Homes

When you rent, you consider the monthly rent as an expense, however when you pay your mortgage, that is not considered an expense, but the interest, utilities and everything else is.

Cole has $17,000 he can use as a down payment on a house that sells for $85,000. The interest for a year on his mortgage would be $5,184. He estimates his property taxes to be $1,720. Other costs of home ownership would total $3,270. He would lose $680 interest on his down payment and closing cost, but would save $895 on income taxes. Cole can rent a similar home for $850 a month with a $1,200 security deposit. His other annual expenses of renting would be $130 for insurance and $1,400 for utilities. For the first year, is it less expensive for Cole to buy or rent a home, and what is the difference?

Cost of Renting:

____________________________________________

____________________________________________

Cost of home ownership:

___________________________________________

Find the difference…

____________________________________________

Loss of Income on the money invested in the home.

1. Occurs because the money initially invested in buying the property (down payment and closing costs) could have been deposited in a savings account and earned interest.

Then why own? …people can include the interest they pay on their home mortgage and property taxes they pay on their tax return….this reduces taxable income…you pay less taxes and have equity in a house….(taxable income that we learned in chapter 3)

Compare Renting and Owning Homes

When you rent, you consider the monthly rent as an expense, however when you pay your mortgage, that is not considered an expense, but the interest, utilities and everything else is.

6-3 Property Taxes

Property taxes – taxes on the value of real estate such as homes, business property, or farm land.

Usually collected __________ or ______________ by the tax department of the town or city you live in.

Services paid for by taxes: ________________________ ________________________ ________________________ ________________________ ________________________ ________________________

Taxes are paid based on the assessed value…

An assessed value is usually calculated by _________________ and is usually a __________ of the actual value of your house…

Ex: Bill Watson’s home is valued at $150,000.00. It is assessed at 40% of its market value or _______________.

Taxes are then calculated on the assessed value of _______________.

_____________________ determine the tax rate needed to pay for the services they provide.

They estimate their __________ for the coming year and prepare an expense budget. They also estimate income from sources other than property tax, such as ________, _______, ______, _____, __________ aid and so on.

The difference between the total budget and the income from other sources is the amount that must be raised by the property tax.

Local tax districts then determine the decimal tax rate, which is the tax rate at which property is to be taxed.

Decimal tax rate = amount to be raised by property tax

Total assessed value

Example 1 from page 224:$6,000,000 - $1,800,000 = $4,200,000(property tax needed)

$39,999,000

= .107692

Tax rates per $100 or $1,000

To find the tax due on property when the rate is in $100 or $1,000, first find the number of $100 units or $1,000 units in the assessed value. Then , multiply the numbers of units by the tax rate to find the tax due.

Read Example 2 on page 225

6-4 Property Insurance

Homeowners insurance – a policy that covers your home and protects you against other risks.

___________ – the home you live in Other structures – such as the ______ _________________ - includes the

___________ of a home.

6-4 Property Insurance- Additional living expense – which pays for

the extra cost of living when you cannot _________________________________

_________________.

- Personal liability – which protects you in case of lawsuits _________________

______________________________.

- Medical payments to others, but not to you or your family, for medical expenses in case of injury on your property.

Con’t_____________ – the amount for which

your home is insured for.

Personal property is usually covered for _______ % of the face value.

Additional living expense coverage is typically _____ % of the face value.

Other options – ____________…covers property away…usually ______ % of face value.

Con’t_______________________ – the

insurance company will pay to replace an item at current prices.– Insurers usually require a __________

and ______________ of the property and it must be insured for 100% of its current replacement value.

– Premiums are _________ % higher for extra coverage.

Con’tInsurance ___________ – the money

paid to an insurance company for property insurance….cost depends on many things…

kind of coverage, how house is built, location…

***Some items such as _______, __________, expensive _________ are not covered by a basic policy…it will cost more.

Con’tNolan insured his home for $61,000.

Find the annual premium, to the nearest dollar, he will pay for a policy that costs $.46 per $100.

________________

Mandy insures her home for $43,000. What annual premium will she pay if the policy cost is $0.74 per $100?

________________

Con’tRenters Insurance Premiums – provides

protection similarly as homeowner except for loss of the dwelling.

Page 232 C. and D.

C. _____________

D. _____________

Collecting on Insurance Claims…

- file paperwork, inspector…pay less deductible

______________ – the amount you are responsible for paying

Con’tYour policy has a face value of $30,000

with a $1,000 deductible. How much will the insurance company pay if your loss is $7,800?

_______________

Answer the following:

Find the premium for one year for a $61,000 policy at $.39 per $100.

_______________

A $31,000 policy costs $11.20 per $1,000. Find the premium for one year.

_______________

6-5 Buying a Car

MSRP – _______________________________

….also known as ___________ price

Car buyers usually do not pay this price…they ____________ a price to pay based on _____________, _______________, and ____________ options.

________________________––refers to the price negotiated by the dealer and the buyer. This price includes the car and any options installed by the dealer

________________________– also called “out the door”

price…this includes purchase price, sales tax, registration fees less the rebate.

________________________–– what the customer has

to pay for their car….less discounts, rebates, down payments or trade-ins..

Words to know…

Base price – ________________________________

___________ – this comes on all new cars and usually covers things that break _____ months or _________ miles…this doesn’t include maintenance.

______________________ – provides extra coverage for an extra number of months and mile

Purchase Price

Sales Tax

Registration Fees

Non-taxable items

Rebates

Delivered Price

Down Payment

Balance Due

6-6 Car Purchases and LeasesThe delivered price of a car purchase may be

paid in cash, however, most people make a down payment and take out installment loans OR lease a vehicle.

Lease – _______________________________

6-6 Car Purchases and Leases

The delivered price of Sue’s car is $23,560. She makes a $2,000 down payment and pays the balance in 48 monthly payments of $560. What total amount did Sue pay for the car, AND what was the finance charge?

1. $2,000 + $26,880 (560 x 48) = $28,880

2. $28,880 - $23,560 = $5,320

Steve Rubin bought a used truck for $9,650. He paid for the truck with a $2,650 down payment and 36 monthly payments of $234.30. What total amount did the truck cost?

_________________________How much did he pay in interest or

finance charge?_________________________

Let’s Solve…Angie bought a luxury car for $47,850

and made a $4,500 down payment. She got a special loan rate of 2.1% for 60 months. Her monthly payments were $780.30. What was her finance charge on this car?

______________________________________________________________

Cost of LeasingA lease is a contract between the car company and

the customer. Similar to renting a car for a long period of time.

Conditions:

______________________________________

______________________________________

______________________________________

_____________________________________

______________________________________

______________________________________

Compare Leasing and Buying

When comparing the two, you must add the residual value to the cost of leasing since you assume you will buy at the end.

Wilbur and his dealer negotiated a price of $27,400 for a new car. He can lease the car for $496 for 36 months and buy it at the end of the lease for its residual value of $16,200. If he buys the car now his month loan payment will be $822 for three years after making a $2,000 down payment . What is the total cost of purchasing the car under each plan? Which is less expensive?

Lease: __________________________________________________________________

Buy: _____________________________________________________________________ Difference: ___________________________

6-7 Depreciating a Car

A car loses value as it grows older…the loss of value is called deprecation. The total depreciation on a car is the difference between its original cost and its resale, or trade-in value.

Depreciation = ______________ – _______________________________

6-7 Depreciating a Car

When you buy a car, you can only estimate what the depreciation will be. The actual amount of depreciation will be known only when the car is sold or traded in.

Lori bought a car for $14,800. She estimates her trade-in will be $5,800 after 4 years. Her depreciation will be… _________________.

Her annual depreciation will be…

____________________________.

Rate of Depreciation = average annual depreciation divided by original cost.

Her rate of depreciation is….

__________________________

6-8 Cost of Owning a Car

Car Insurance:

There are 4 basic types of insurance or coverage for motor vehicles that protect you against the risk of financial loss:

6-8 Cost of Owning a Car1. ________________ – covers your liability for

injury to others.2. ________________– covers damage to other

people’s property including their vehicles.3. ________________– covers damage to your own

motor vehicle.4. ________________– covers damage or loss to

your vehicle from fire, theft, vandalism, hail, and other causes.

Read page 256…and the example 1…___________Page 257 A. and B. A. __________________B. __________________

Costs of Operating Cars…

The total operating cost for a car is the sum of all the annual expenses of using the car.

These expenses include:•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________

•__________________