Embed Size (px)

Citation preview

AJCIC100 Handout Page 1

4.1 D4.1 Deessccrriibe Commbe Commoon n PPiittfafalllsls iin Acn Acttiviivittyy BBaasseed Cod Cossttiinng ag annd Ways d Ways tto Avoido AvoidThTheemm

Learning Objective

Describe common pitfalls and ways to avoid them (TLO).

Tasks

Describe limits to precision Describe affordability, credibility and relevance constraints

Key Terms

Affordabiliy

Credibility

Relevance

In this lesson we will explore the inherent practical limits to precision in managerial

costing. Defining the precision requirements of a managerial costing system is

important for threereasons, which are closely related to the three dimensions discussed in the previous module. The most important is that managers need information, not data. Attempts to build highly precise systems may fall into the trap of producing a lot of precise data while failing to supply reasonably accurate, relevant information. Such a system falls short in the dimension of managerial usefulness.

The second reason to carefully consider a system’s requirement for precision is that precision is expensive. Attempts at great precision require greater dis-aggregation, increased detail and more direct costing. This will increase the cost of the system or decrease its functionality in other areas such as the frequency of update. It is always possible to measure to greater precision and easy to spend more on cost measurement than it is worth.

The third and final reason for examining the level of precision to be built into a cost measurement system is that there may be technical and physical limits to the precision of a measurement. A system that reports costs to the penny, while utilizing a cost measurement methodology that is inherently bound by physical or technical limits may give a false sense of precision.

AJCIC100 Handout Page 2

•Raw Accounting Data

Data

Translate

•Managerial Costing Translation

•Managerially Useful Information

Cost Object

Consideration of a managerial costing system’s requirement for precision is an important topic for managers and managerial cost accountants before building the system. There seems to be a facet of human nature that encourages excessive precision when starting cost measurement.

Consider the activity based cost accounting system found in a federal organization that used 275 activities to distribute annual overhead of $3.5 million. The burden of feeding raw accounting data and updating the distribution mechanisms resulted in the system only being updated once a year. It is not surprising that the manager of the organization found little use for the information in continuously improving his operation.

It should be noted that this approach was a good front end for a re-engineering effort. Such effort typically maps the process in great detail and scrutinizes each detail for value added to the process. The outcome from re-engineering is a re-designed organization. While certainly useful, continuous organization re-design is not a sustainable paradigm for continuous improvement in cost management.

The areas of physical or technical limits of precision, managerial relevancy requirement for precision, and cost of precision will be discussed in theoretical terms and illustrated with practical examples. The goal of a managerial costing system is to provide information of practical value to cost managers. The goal of this paper is to address the issue of “how much precision do cost managers need?”

PPhhyyssicicaall LLiimmiittss oof f PPrrececiissiionon:: WWeaeakkeestst LLiinnkk TTheoheorryy

Engineers and scientists use a term called “significant digits” to express the precision inherent in a physical measurement. In measuring the distance to a star, precision may only be possible within the nearest light year (roughly 6,000,000,000,000,000 miles). It makes no difference from what point on earth you are measuring or where in its trip around the sun the earth sits because these differences are small in comparison to the distance light travels in a year. In other words they are not within the significant digits.

A related way to think about this issue is remember that a chain is only as strong as its weakest link. Overall precision in costs to be aggregated can be no greater than that of the least precise: the “weakest link.” It makes little sense to measure

AJCIC100 Handout Page 3

some costs to the nearest penny when that measurement will be added to cost that can only be estimated to the nearest thousand dollars.

AJCIC100 Handout Page 4

It is crucial to recognize that any allocation process is depends heavily upon assumptions, and these assumptions have an impact on precision. As discussed in the previous article, the selection of a cost driver implicitly assumes that each unit of that cost driver is reasonably homogeneous. Allocation based on a cost driver is essentially an average cost per unit of cost driver. In reality, there is some varying range of cost per each individual unit of cost driver. Therefore, allocations inherently limit precision. The unavoidable assumptions required by the allocation process create a “weak link” in the overall costing process.

PPhhyyssicicaall LLiimmiittss oof f PPrrececiissiioonn IIlllluussttrraattiioonn

Consider the measurement process you would use in calculating the driving distance for a vacation. The trip can be visualized as the aggregation of several distance segments.

The first segment you might consider would be the distance from the town nearest your origin to the town nearest your destination. You could then also estimate the distance from your community to the nearest town, the distance from your street to your community, and the distance from the town nearest your destination to the destination itself.

Each of these segments has a different level of precision imbedded in its measurement process.The road atlas may be accurate to a mile or so, but your estimates of the other segments are likely to be less precise.

The estimate from town nearest destination to destination is likely to be the least precise and may be “wrong” by several miles. The “weakest link” theory says that the total distance can be no more accurate than this least accurate segment.

This is why we do not get our ruler and measure the distance from our garage to our street in order to get a more precise measurement. The distance to the street can be measured very precisely, perhaps to the nearest foot, but it makes no sense to do so. The precision limitations of the other measurements make driveway measurement an unnecessary waste of time. Just because we can measure that segment very accurately does not mean that we improve the overall measurement for our trip: the underlying management purpose of the measurement itself.

Similarly, in a cost measurement where one component of cost can be measured to the nearest cent, and another can only be measured to the nearest one hundred thousand dollars, the entire calculation can be no more precise than the nearest one hundred thousand dollars. Think about this the next time you see a “cost” measurement of millions of dollars that includes the number of pennies.

AJCIC100 Handout Page 5

MaMannaaggeeririaall ReRelleevvaanncycy RReequirquiremeemenntt ffor Pror Preecciissiioonn::

TThhee OOnnee PePerrccenent t TTheoheorryy

The issue to be addressed here is how much precision managers need. In the vacation planning illustration, how useful would it be to actually know the distance to the nearest foot? Would this information be relevant to any decision you might make. Would it improve your trip planning or budgeting to any meaningful degree?

It is proposed here that management generally needs precision to no greater than one percent.Management decisions rarely hinge on the tenths of percent differences found in numbers with three or more significant figures. Managers typically look only at the first two digits.

Precision in terms of dollars and cents is simply irrelevant in decisions involving thousands of dollars.

Making generalizations, however, is somewhat risky. As “beauty is in the eye of the beholder,” so is precision in the mind of the manager. There are some distance measurement applications (programming cruise missiles, for example) that need very precise measurement capability to be effective. Likewise, some managers feel comfortable with more detail and others with less. In general though, it seems clear that there is a practical limit of one percent to the precision needed and really required.

RelReleevvancancyy ReReququirireememenntt ffoorr PPrreecciissiioonn IIlllluuststrraattiioonn

Another way to think about the issue of practical relevancy for precision is to look at the clock in Figure 13-1 and determine “what time is it?” Is it 2:00 or 2:05? Or is it 2:03 or 2:02:47? Would you ever answer the question by saying that it is 2:02:46:35? It is illustrative to think about how and why you answer the way you answer.

AJCIC100 Handout Page 6

For most of us, there are physical limitations to our time keeping equipment. We know that ourwatches’ significant digits do not include hundredths of a second. But more importantly,

AJCIC100 Handout Page 7

we also know that for all conceivable uses, hundredths of a second simply do not make any difference. They are irrelevant and do not meet measurement’s relevancy requirement.

As mentioned earlier, the determination of relevancy is a function of the measurement’s management application. Radio station operations probably demand time measurement to greater precision that more individuals require. Furthermore, some highly time sensitive applications like synchronous data transmission can require extremely accurate time measurement.

CCoostst o of Prf Preecciissiioonn::

CCoostst BeBenenefitfit TTheoheoryry

Precision costs. The highly accurate distance measurement process for cruise missiles and the highly accurate time measurement clock for synchronous data transmission are expensive. Designers must use a cost-benefit logic to determine whether increasing precision in any area increases the overall value of the measurement.

Any costing methodology incurs costs of measuring, accumulating, storing, editing, manipulating, reporting, and explaining. These costs increase substantially as greater levels of precision are attempted.

Cost systems that attempt great precision require greater dis-aggregation. A hundred-activity cost system is likely to be more precise than a ten-activity cost system, but will cost substantially more. The hundred-activity cost system could certainly be done more precisely by using 1000 activities, again with an increase in the cost of the cost measurement process. It is proposed here that the incremental benefit of increased detail must exceed the incremental cost of measurement.

CCoostst oof f PPrrececiissiioonn IIlllluussttrraattiioonn

An Army installation recently developed an activity based cost accounting system that tracked1700 activities for its Maintenance Department. The size of the system and the burden of repopulating cost data and revisiting cost distributions meant that the system provided only annual data for the previous year some months after the end of the year. Management found the benefit of the presumably precise, but ancient, history unworthy of its subsequent updating and never repopulated. Unfortunately, the system was discontinued rather that simplified to the point where it would provide a positive cost- benefit.

Similar efforts at Fort Huachuca, Arizona started in the same mode of striving for great precision. The activity-based cost accounting system developed for its Logistics Directorate originally had 350 activities and was updated annually. Fort Huachuca alsofound this reporting irrelevant, but chose to evolve its system towards greater usefulness.By the third iteration the entire directorate was comprised of 35 activities

AJCIC100 Handout Page 8

updated quarterly. Management reports that the system is an essential part of the garrison’s cost- based management effort that has yielded hundreds of thousands of dollars in productivity improvement in the last two years.

AJCIC100 Handout Page 9

DDiinniinngg HHaallll I Illlluuststrraattiionon:: A CA Comompprrehensehensivivee CaCassee StStududyy

The Dining Hall Department at Fort Huachuca was part of the Directorate of Logistics described above. In the first system it contained fifteen activities associated with providing its service, along with the costs associated with each activity. In rank order these costs in thousands of dollars were:

Cool Food $237

Clean $119

Serve $64

Collect Money $63

Prepare Food $36

Do Paperwork $22

Wash Dishes $20

Prepare Vegetables $20

Prepare Salads $20

Plan Meals $18

Drive Trucks $18

Unload Trucks $14

Stock Shelves $14

Replenish Line $14

Maintain Equipment $14

Total $693

An important question to consider is “how many activities should be considered in the system?” Let’s consider three approaches. One approach is to consider all 15 activities. The allocation of these activities to cost objects must then measure the cost for each activity, determine the distribution methodology for each activity, and then measure the distribution metric for each distribution methodology.

A second strategy would involve aggregating a number of the smaller activities into a single cost pool we could call “all other.” “All other” would then be distributed on a weighted average of the larger activities’ distribution results. Aggregating the smallest 12 activities into the “all other” activity decreases the effort (and the cost) of the cost distribution process by 80%.

A third strategy is to expand the number of activities by considering smaller value subsets of each of the 15 activities shown. Preparing vegetables could be divided by process into cutting, washing, cooking, etc.

Each of these activities could be further subdivided into activities by vegetable type: potatoes, beans, peas, carrots, cauliflower, etc. Cooking activities could also be

AJCIC100 Handout Page 10

subdivided into separate activities for different cooking processes: frying, baking, steaming, etc.

AJCIC100 Handout Page 11

Each of the three strategies can be used to distribute the dining hall costs to costs objects. Each represents a different level of accounting cost and accounting precision. The important tradeoff to be considered here is the marginal cost of increased detail versus the marginal benefit of increased detail. It should be clear that there is a diminishing return to the increased detail, since the maximum number of possible activities is theoretically infinite while the marginal benefit is undoubtedly limited.

Discussion:

CCoostst ManaManaggeememenntt oof thef the CCoostst MeaMeassuurreememenntt

Pareto Analysis can be a helpful tool to provide the best value in cost measurement. It also helps to avoid the likely diminishing return to accounting effort that occurs when an overly detailed system is attempted.

Pareto Analysis simply observes that any distribution has a few significant components, but many trivial ones. This is sometimes called the 80-20 rule since is often happens that 80% of an effect is represented by 20% of the causes.

This 80-20 rule holds true in the dining hall example. The largest four activities (actually 27% of the 15 activities) account for 78% of the cost. We would call these high-ticket items the “significant few.” They are the ones to target first in order to make an efficient impact on the overall cost measurement.

Evaluation of the “trivial many” will generally have little impact on the overall cost distribution.Considering them in detail will likely increase the cost of the measurement process without adding much benefit. Consider that a 10% measurement error in the largest activity, cooling food, is larger than the total cost involved in each of the smallest ten activities. (See the chart that follows)

AJCIC100 Handout Page 12

Evaluating the cost/benefit ratio of additional activities is difficult. While the benefit contribution of the small cost activities is likely to be small, the cost of measuring them is not. In the dining hall example, let’s assume that the cost of measuring an activity, determining a distribution methodology, and measuring the distribution metric is $180.

Defining the benefit is more arbitrary, although it would seem reasonable that the incremental benefit is related to the incremental improvement in measurement. Arbitrarily valuing the benefit as one percent of the absolute value of all cost redistribution between cost objects yields the graph shown on the following page. While the cost and benefit parameters are arguable, the general shape of the lines is clear given the decreasing return to accuracy as more activities are evaluated to distribute a total cost that remains unchanged.

Generally then, it makes good sense to consolidate small activities into a single pool. Yet there are exceptions to the general rule. If one of the small activities was distributed to cost object in a unique way, it might make sense to not aggregate it with the others. For example, if one of the small activities was “dinner music” and dinner cost was one of our cost objects, it would make sense to allocate “dinner music” 100% to dinner cost and not aggregate it with activities that support breakfast and lunch. Keep in mind though, that “dinner music” cost of a very small amount will not affect the cost distribution in any relevant way and should be ignored.

It should be clear that the significant few must be determined and addressed in the managerial costing process. This is where effort will yield the best value in cost measurement. It may be useful for managerial costers to consider the Willie Sutton Law of Managerial Costing. When Mr. Sutton was asked why he robbed

AJCIC100 Handout Page 13

banks, he replied, “Because that’s where the money is.” Cost system designers should recognize that higher levels of effort are desirable in big-ticket items, because “that’s where the money is.”

AJCIC100 Handout Page 14

SumSummamarryy aanndd CCononcclluussiioonnss

Physical limits to precision bound the accuracy of measurement to that of the least accurate component or “weakest link.” Making assumptions concerning the homogeneity of cost drivers creates weak links in allocation based cost distributions. Managerial costing systems that are dependent on allocations or estimations cannot achieve a level of precision comparable to bookkeeping systems. Implying such precision is misleading. Great precision in managerial costing is NOT POSSIBLE.

Relevancy requirements for precision demand that management’s intended use of cost information drive the measurement process and its specified accuracy. Management use of information generally requires reasonable approximation rather than precise aggregation. Managerial costing systems should recognize that managers typically do not need or use a level of precision that may be technically possible. Great precision in managerial costing is NOT NEEDED.

Costs inherent in precision are theoretically infinite, as greater levels of detail are always possible in cost measurement. The benefit of precision is subject to a diminishing return that generally does not justify a highly detailed system. The requirement for system benefit to exceed system cost is a practical necessity. Great precision in managerial costing is NOT AFFORDABLE.

Consideration of the physical limits to precision, relevancy requirements for precision and costs of precision differentiates managerial costing from traditional bookkeeping and accounting processes. Ignorance of this difference will result in costing efforts that fail to provide the right kind of managerial information that justifies the effort. As a practical matter, in managerial costing it is better to be reasonably right than precisely wrong.

Battlefield commanders must have reconnaissance that is useful, credible, and affordable. No commander facing a battle would want to use someone else’s or a generic reconnaissance plan that did not fit the specific needs of the situation. No commander would want reconnaissance that was unreliable. Finally, no commander would want to put so many troops in reconnaissance functions that there weren’t enough left to actually fight the battle.

Cost Warriors face the same difficult task in defining managerial costing processes. Managerial costing must simultaneously be useful, credible, and affordable. The last chapter offers insight into these often-conflicting requirements and provides guidance on avoiding common pitfalls. The rest of the chapter is reprinted with the permission of the Government Accountants Journal. It was published under the title: Practical Issues in Avoiding Pitfalls in Managerial Costing Implementation.

AJCIC100 Handout Page 15

Next we address a number of key practical issues in the formulation of managerial costing systems in government organizations. These issues are presented as a series of articles. The first considered government’s increasing needs for cost management and differentiated the cost measurement process of managerial costing from the external reporting of cost. The second offered guidance on management’s role in selecting from alternative measurement methodologies and in choosing cost objects: the view of cost to be measured.

The third article discussed practical issues in defining and selecting cost drivers along three dimensions: managerial impact and usefulness, measurement credibility, and measurement cost. The fourth showed that measurement limitations and measurement costs restrict the level of precision possible in managerial costing systems. Fortunately, management’s need for precision is also considerably lower than that typically expected in bookkeeping or accounting systems driven by external reporting requirements.

Recent experience suggests a somewhat naïve expectation that simply hiring a good contractor and using good activity based cost accounting software automatically results in better cost management. Unfortunately, success is not guaranteed. This final installment in the series will build a general theory of managerial costing by considering pitfalls in the three dimensions of usefulness, truthfulness, and affordability.

AA G Geneenerraall TTheoheorryy oof f CCoonnvveergrgenentt ReRequiquirreememenntsts

Government organizations have long met their external accounting requirements without cost accounting systems. This situation can undoubtedly continue. Current motivation for cost information is coming from inside the organization as managers are more interested in productivity increases to accomplish organizational missions in an era of reduced resources. Reprogrammed cost efficiencies provide new budget resources for unfunded mission priorities. Enhancing the mission is the goal of “managerial costing.”

AJCIC100 Handout Page 16

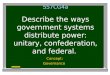

Managerial costing systems can be evaluated in three fundamental dimensions. Managerial costing is either useful to managers or it is not. Managerial costing is either credible in providing a reasonable view of the true cost of resources consumed or it is not. Managerial costing is either affordable or it is not.

Useful Credible Affordable

It is undoubtedly easier to miss the target for any of these dimensions than to hit it.Furthermore, it is proposed here that satisfying one or two of these dimensions is insufficient. The goal of mission enhancement will be met by the managerial costing effort only where there is a convergence of all three dimensions.

Much of the existing accounting in government is of limited usefulness to managers seeking continuous improvement in the productivity of their operations. Cost managers must find managerial costing information useful. If managers don’t use the system, the effort dies from lack of interest.

Costing inevitably requires the making of assumptions as to what cost elements to include and how to include them. It is relatively easy to make assumptions that fail to reasonably represent the “true” cost of resources consumed. Bad assumptions will do more harm than good by undercosting or overcosting cost objects with resultant undesired economic behavior. Cost measurements must credibly represent the true consumption of resources by cost object. If cost measurements do not reasonably represent underlying physical and economic realities, the system will die from lack of trust.

Finally, it should be recognized that the upper limit for the cost of cost measurement is infinity.Cost measurement can always be done in greater detail and more frequently. Even if we had a cost accountant for every employee we could still think of ways to measure cost that would cost more. If the cost of cost measurement is too high, the system will die from lack of affordability.

Each of these requirements dimensions represents a necessary condition for success. Each is also insufficient, on its own, to guarantee success. Truly successful

AJCIC100 Handout Page 17

managerial costing efforts must find a point of convergence in all three dimensions, while avoiding pitfalls. See the figure below.

AJCIC100 Handout Page 18

Designing a managerial costing system that meets one of the requirements is difficult. Meeting the usefulness requirement, for example, demands a good understanding of how cost measurement will be used in the cost management process. The probability of a randomly developed system hitting this target is small. The same difficulty exists in meeting the credibility and affordability requirements.

The convergency requirement that all three be simultaneously satisfied further drastically limits the space available for a truly successful system. System designers should carefully consider these requirements and the common pitfalls that threaten successful applications.

Usefulness Requirement and Standardization Pitfall

Managerial costing information must help managers manage cost. We covered the difference between managerial costing and external reporting in the first article in this series. The second further developed management’s essential role in the specification of cost objects. These articles emphasized the need for management to actively “pull” mana- gerial costing information rather than be the passive recipient of cost data. Here we will further explore the usefulness requirement by considering the “standardization” pitfall.

Some seem to think that simply installing a cost accounting system automatically creates a cost management process. If this were true, it would make great sense to standardize governmental cost accounting systems on some commercial off-the-shelf accounting package. However, this approach misses the point that the cost management process must drive or “pull” cost measurement. Standardized

AJCIC100 Handout Page 19

approaches often fail because they do not respond to the situation specific needs that exist in organizations with diverse missions, environments, personalities, and structures. If all situations, organizations, and managers were identical, perhaps standardization would work. Unfortunately, they are not and no one size is likely to “fit all.”

AJCIC100 Handout Page 20

SSttandaandarrddizizaattiioonn PPiitftfaallll IIlllluussttrraattiioonn

The Federal Accounting Standards Advisory Board’s “Statement #4/ Managerial Cost Accounting Concepts and Standards for the Federal Government,” offers federal departments great flexibility in developing cost measurement approaches. Footnote number 24 states:

“Costing Methodology-The costing methodology used (e.g., activity-based costing, job order costing, standard costing, etc.) should be appropriate for management’s needs and the operating environment.”

Yet, initial discussion by the Board considered a wide range of approaches. Some suggested that all federal agencies should use the same cost measurement system. Some even suggested using the same Cost Accounting Standards developed for defense contractors.

My testimony to the Board asked them to consider the implications of standardizing all combat ships in the Navy on a single design. Take a moment to think about the advantages and disadvantages of such standardization. Would there be advantages?

Of course there would be advantages. There are always advantages of standardization.Efficiencies would be found in the training and staffing of sailors. Repair part inventorieswould be dramatically reduced. Purchases of ammunition and stores could probably be done at lower cost due to great quantities of fewer part numbers. Unit costs of building ships would probably improve as shipbuilders experienced greater learning curve effects through larger quantities. Perhaps most importantly, force deployment and evaluation of battle results could be done much more precisely: leading to increased effectiveness.

While it is true that there would be advantages, there would also be disadvantages. Ultimately, the decision maker must weigh the advantages and disadvantages in making a decision. To illustrate disadvantages, I offered the graphic shown in on the next page. (Geiger,1994)

AJCIC100 Handout Page 21

Some combat missions include the need for air operations, so every ship must meet this requirement and have a flight deck. All ships must be double hulled and have a conning tower since some of the user community needs to work underwater. Yes, this does interfere sometimes with flight operations, but the problem is consistent.

Other underwater missions require ballistic missiles and torpedoes. The submitted design suggests ballistic missiles in the middle of the flight deck (with the stipulation that only very careful landings will be permitted). Torpedo tubes in the bow conflict with the need for the ship to land on the beaches and disembark marines, but this could probably be worked out technically.

Edwin Land once said that any problem could be solved: “if you can define a problem and have enough resources.” This ship could undoubtedly be built. However, it would be expensive and, worse, it would not be a very good aircraft carrier, submarine, or landing craft. Trying to be all things results in being good at none. So it is with managerial costing.

CrCredediibibilliityty ReReququirireememenntt aanndd MiMiss--CCoossttiinngg PPiitftfaallll

As we have implied throughout this series, cost measurement is not simple. In fact, it is quite easy to do wrong. Let’s consider the pitfall of mis-measurement and the consequential resource consumption implications.

Economic theory has long recognized the relationship between cost of goods and the consumption of goods. The “demand curve” relates the two. Lower cost means higher demand and higher cost means lower demand. Economists, however, assume away the cost measurement issues that may be particularly important within government organiza- tions new to cost measurement.

An earlier article in this series already discussed the potential for “infinite demand” of apparently “free goods” in organizations that do not measure cost. Here we will consider the impact of mis-measured cost. Consider Figure 14-4. Cost X elicits consumption Y while similar rational economic response to cost X1 generates

demand of Y1.If X represents the “true cost” and X1 the “as measured cost,” it

should be apparent that the undercosting error in measurement will rationally stimulate greater consumption by the increment ofY1 less Y. Similarly it can be illustrated that overcosting will stimulate underconsumption.

AJCIC100 Handout Page 22

Cost measurement literature (Johnson and Kaplan, 1987) has recognized this phenomenon.They describe the common scenario of an organization that allocates large overhead pools on a direct labor cost driver. The fully burdened labor rate appears to be very expensive. Economic alternatives such as outsourcing, automation, or privatization look relatively more attractive. This overcosting phenomenon logically leads to underconsumption by encouraging excessive outsourcing, over-automation, and inappropriate privatization.

FASAB Standard #4 recognizes the importance of credibility by preferring direct measurement where practical and emphasizing cause and effect relationships and reasonability when allocating:

“The cost assignments should be performed by the following methods listed in the order of preference: (a) directly tracing costs wherever feasible and economically practicable, (b) assigning costs on a cause-and-effect basis, or (c) allocating costs on a reasonable and consistent basis.”

AJCIC100 Handout Page 23

MMisis--CCoossttiinngg PPiitftfaallll I Illlluussttrraattiioonn

Let’s consider a case to illustrate a managerial costing application where the management seeks to evaluate outsourcing against in house operation. Consider a situation where the Navy wishes to “compete” nuclear and non-nuclear ship refurbishment between its own shipyards and private sector shipyards.

Let’s inject a common flaw into the measurement process. Let’s assume that the Navy shipyards aggregate overhead for all refurbishment into a single pool and then allocates the pool to refurbishments based on the direct labor used.

Now, it would seem reasonable to assume that nuclear refurbishment overhead is actually higher than non-nuclear. Nuclear materials demand greater levels of security and safety. Nuclear reactors required greater technical sophistication than gas turbine engines. Therefore, it is likely that allocating the single overhead pool on the basis of direct labor will overcost non-nuclear refurbishment and undercost nuclear.

Figure 14-5 illustrates the difference between “true cost” and “measured cost” on a per labor hour basis. It should be clear that the Navy’s “as measured” cost for nuclear refurbishment was lower than the “true cost.” This process has been undercosted.

The consequences of undercosting can be illustrated with one additional, but likely, assumption: that the private shipyards know the “true cost” for their processes. It should then be obvious that private shipyards are likely to win the non-nuclear refurbishment business: perhaps at greater cost than what the Navy was actually incurring. Furthermore, it should be clear that the Navy will never realize projected savings based on the overcosted non- nuclear outsourcing.

Let’s use some hypothetical numbers to illustrate what is likely to happen. See Table 14-1. If the contractor adds 15% to true cost in making a bid, he will still show an

AJCIC100 Handout Page 24

apparent 10% savings on non-nuclear refurbishment since the Navy will compare the bid of 46 to the reported cost of 50. Accepting this bid wins somebody a purchasing award but in reality increases total cost for the government.

AJCIC100 Handout Page 25

True Reported Contractor Post Outsourcing

Cost Cost Bid Cost True Cost

Nuclear 60 50 69 60

Non-Nuclear 40 50 46 46

Total 100 100 115 106

Comparing contractor bid to Navy reported cost shows that the Navy is apparently proficient at nuclear work, but that the non-nuclear should be outsourced.

In this case the extra measurement cost incurred by having a two pool overhead system would be justified by the improved credibility or truthfulness in the measured cost per hour of the two refurbishment processes. The consequences of not improving measurement credibility far outweigh the increased costs of measurement.

AffAffoorrdabdabililiityty ReReququirireememenntt anandd ExcExceessssivivee CCoomplemplexixityty PPiitftfalalll

No organization exists for the sole purpose of measuring itself. The managerial costing process is therefore subject to affordability constraints. The pitfall, of course, is a measurement process that is excessively complex and overly detailed.

Unfortunately, when fiscal resources are readily available cost measurement and cost management are less important, and management attention seems to go elsewhere. When fiscal resources are constrained, management is more interested in cost management, but the fiscal resources available for cost measurement are constrained. The cost of the cost measurement process inevitably assumes the most importance when the measurement need is greatest.

FASAB Standard #4 on Managerial Costing recognizes the pitfall of excessive complexity and explicitly avoids its requirement:

“While each entity’s managerial cost accounting should meet the basics discussed above, this standard does not specify the degree of complexity or sophistication of any managerial cost accounting process. Each reporting identity should determine the appropriate detail for its cost accounting processes and procedures based on several factors. These include the:

nature of the entity’s operations;

precision desired and needed in cost information;

practicality of data collection and processing;

availability of electronic data handling facilities;

AJCIC100 Handout Page 26

cost of installing, operating, and maintaining the cost accounting processes; and

any specific information needs of management.”

AJCIC100 Handout Page 27

Excessive Complexity Pitfall Illustration

Perhaps in response to a natural instinct for self-preservation, it seems that initial attempts at cost measurement tend towards excessive complexity. Imagine that, due to resource constraints or budget cuts, you are asked to develop an activity based cost accounting initiative in your own organization.

You recognize the threat to your interests, but certainly want to cooperate with the effort. Your major concern is that something may be left out. Besides wanting everyone to see how complex your operation is, you suffer from “budget mentality.” If you leave something out in the budget process, it doesn’t get funded and it disappears. You certainly don’t want this to happen during the managerial costing process.

Therefore it seems that there is a natural bias in government organizations towards excessive complexity when they start a managerial costing effort. This tendency seems to occur so often that the fourth article in this series was addressed to the issue in its entirety. Let’s consider a short, but real, example to illustrate what can easily happen.

The Maintenance Department at the United States Army Installation at Fort Knox seemed to experience this phenomenon. An activity based costing system was developed to measure some 1700 activities to the penny once per year. Contractor charges totaled roughly $100K, and the effort probably required an equal expenditure of government employee cost.

However, Maintenance Department management was not satisfied with the system.Development of an even more complex system was briefly considered but rejected. The system died. It was not even “populated” a second time. The Garrison Commander said “the system just didn’t provide enough new information to justify the time and effort it took.”

Discussion

The failure at Fort Knox was attributed to excessive complexity. The managerial costing effort also could have failed on the basis of usefulness due to the infrequency of the data and its potential delay in availability. Infrequent, annual cost information is unlikely to be extremely useful in cost management applications. Imagine if we sent the tanks at Fort Knox to the target range every day, but we didn’t tell them their score until the end of the year. Such a long feedback process is unlikely to produce the kind of armored force that won the Gulf War in 100 hours.

The usefulness of data will suffer if it is not fresh: available soon after the period being measured. Providing monthly data at yearend is probably little better than providing annual data once per year. Long lag time diminishes the effectiveness of a managerial costing process. In general, frequent data inherently offers greater relevance for cost management. Fresh, frequent data is better yet.

AJCIC100 Handout Page 28

However, increasing usefulness by providing monthly data will increase the cost of the cost measurement by an order of magnitude and threaten failure on the affordability requirement. Attempts to improve affordability by reducing system complexity may impact on credibility or usefulness.

AJCIC100 Handout Page 29

Consider, for example, the complexity pitfalls exposed in answering the apparently simple12request to measure the cost of the Blackhawk

Helicopter.There are so many

permutations of assumptions possible that an initial effort is almost doomed to excessive complexity.

Does cost of a helicopter include pilots and crew? Does it include their training? If so, does it include just flight training or does it include basic training? What about their quarters? What about the cost of meals and the cost of buying meals? The list of cost issues goes on and on as we consider R&D, ammunition, maintenance, higher headquarters, airfields,etc, etc, etc. Assumptions must be made in measuring cost and the credibility of the measurement rests on the reasonableness of those assumptions in light of the measurement’s intended use.

Perhaps it is simply too difficult for organizations, like many in government that have never measured cost, to initially determine a managerial costing specification in the convergence zone that balances usefulness, credibility, and affordability. It is more likely that good managerial costing systems will move towards this zone as they learn from experience and evolve towards increased usefulness and credibility at less cost as shown in Figure 14-6.

12 See FINANCIAL MANAGEMENT: Reliability of Weapon System Cost Reports Is HighlyQuestionable

(GAO/AIMD-94-10) released October 28, 1993 for an idea of how the Army was called to task on this issue.

This is what happened at Fort Huachuca in an area similar to the one that failed at Fort Knox.

AJCIC100 Handout Page 30

The initial activity based cost system for the Directorate of Logistics measured 350 activities annually. However, the Garrison Commander felt that this effort provided less benefit than the labor required. But unlike Fort Knox, Fort Huachuca evolved their man-

AJCIC100 Handout Page 31

agerial costing effort. The second activity based model had 125 activities. Two years later the third model tracked 35 activities quarterly and had helped management achieve significant levels of cost reduction.

Summary and Conclusions

There are three conflicting forces that shape managerial costing system design. These are usability, measurability, and affordability. Each of these forces places demands on the system that compromise the other two. Development of a system that doesn’t meet all three constraints is unlikely to be fully successful. Each is a necessary, but insufficient, consideration for success of a managerial costing system. Unless all three requirements are met, the system is likely to fail and the system development is best avoided.

Relevancy requirements demand that management’s intended use of cost information drive the cost measurement process. Ignoring this requirement results in the production of “gee whiz” numbers that have no practical use other than the knowledge of perhaps interesting, but useless, numbers. Systems that fail to address the usefulness requirement could be labeled as pointless managerial costing.

Credibility requirements demand that the measurement process determine the “true” cost specified by management. This can best be thought of as a range of reasonably accurate measurements where that accuracy is determined in the context of management’s intended use for the measurement. The greatest danger here is in systematically over or under-costing the measurement. Measurement processes that misstate costs systematically or imply great, but practically speaking, impossible levels of precision could be labeled as fraudulent managerial costing.

Affordability requirements require an equal or greater value than the cost of developing and maintaining a managerial costing process. The law of diminishing returns generally results in a cost-effective limit to system detail and attempted precision. Systems that cost more than their benefit will not survive in fiscally constrained organizations and could be labeled as consumptive managerial costing.

It is thus the case that managerial costing design must balance the effect of the three conflicting forces: usability, measurability, and affordability. If sensible compromises are made a convergence of conflicting constraints is possible. Within this intersection we can afford- ably measure true cost in ways useful to management.

In closing we must recognize that as difficult as managerial costing seems, it is the easy part in changing the way government organizations operate. Managing cost demands culturaland behavioral change and is difficult enough even when the pitfalls in managerial costing are avoided.