Embed Size (px)

Citation preview

A Top-Down Mean-Variance Frameworkfor Option Investment and Pricing

Liuren Wujoint with Peter Carr

Baruch College

May 10, 2019CUNY Macroeconomics and Finance Colloquium

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 1 / 13

The classic bottom-up apprach of derivative pricing

The approach is analogous to that in classic physics

Identify the smallest common denominator (particle)

Construct everything bottom up with the smallest common particle

The analogy in classic derivative pricing

The common denominatorThe risk-neutral dynamics (or the physical dynamics and pricing) of aset of common driving factor; the pricing of Arrow-Debreu securities

The bottom-up constructionTake expectation of future payoffs of all derivative securities on thesame dynamics; price the payoffs as a basket of Arrow-Debreu securities

The ambition of a classic quant: Build one model that prices everything!

Specify the dynamics of the short-rate (or pricing kernel) →Price bonds of all maturities

Specify the joint factor structure of pricing kernels of all countries →Price bonds of all maturities, all currencies and the exchange rates

Specify the stock price dynamics → Price all options on the stock

Specify the factor structure on stock dynamics → Price all options onall stocks and stock indexes, maybe even bonds...

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 2 / 13

Why the urge to go to the bottom of everything?

Human nature or animal instinct?

Just like a groundhog who cannot help but keep digging!

For derivative pricing, the approach offers cross-sectional consistency

The common denominator specification provides a single yardstick(pricing menu) for valuing all derivatives built on top of it.

The valuations on different contracts are consistent with one another,in the sense that they are all derived from the same yardstick.

Even if the yardstick is wrong, the valuations remain consistent withone another.

They are just consistently wrong.

A foolish consistency is the hobgoblin of little minds,adored by little statesmen and philosophers and divines.— Ralph Waldo Emerson

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 3 / 13

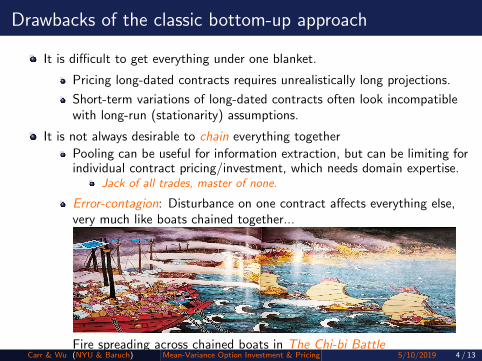

Drawbacks of the classic bottom-up approach

It is difficult to get everything under one blanket.

Pricing long-dated contracts requires unrealistically long projections.

Short-term variations of long-dated contracts often look incompatiblewith long-run (stationarity) assumptions.

It is not always desirable to chain everything together

Pooling can be useful for information extraction, but can be limiting forindividual contract pricing/investment, which needs domain expertise.

Jack of all trades, master of none.

Error-contagion: Disturbance on one contract affects everything else,very much like boats chained together...

Fire spreading across chained boats in The Chi-bi BattleCarr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 4 / 13

A new top-down decentralized perspective

What do investors want?

Different types of investors have different domain expertise and focuson different segments of the markets.

They need a model that can lever their domain expertise

Short-term investors do not care much about the terminal payoffs: Allshe worries about is the P&L on her particular investment over theshort investment horizon.

Short-term risk exposures are more of the focus than terminal payoffs

Long-term investors must also worry about their daily P&L fluctuationdue to marking to market and margin trading

We develop a new framework that generates decentralized pricingimplications based on short-term investment risk on a particular contract.

The short-term focus allows the investor to make near-term riskprojections without worrying about long-run dynamics.

The particular contract focus allows the investor to make top-downprojections without generating implications on other contracts.

Be right about what you do. Don’t worry about conformity with others.Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 5 / 13

Value representation of an option contract

We use an investment in a vanilla option contract as an illustrating example

We represent the option via the BMS pricing equation, B(t,St , It ;K ,T )

(K ,T ) capture the contract characteristics.

The value of the contract can vary with calendar time t, the underlyingsecurity price St , and the option’s BMS implied volatility It .

Appropriate representation/transformation is important for highlightinginformation/risk source, stabilizing quotation...

The at-the-money implied volatility term structure reflects the returnvariance expectation.

The implied volatility smile/skew shape across strike reveals thenon-normality of the underlying distribution.

As long as the option price does not allow arbitrage against theunderlying and cash, there existence of a positive It to match the price.(Hodges, 96)

Different transformation can highlight different insights

BMS is a common/nice choice, but one can explore others...Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 6 / 13

P&L attribution of a short-term option investment

With the BMS representation, we can perform a short-term P&L attributionanalysis on the option investment:

dB = [Btdt + BSdSt + BIdIt ]

+[

12BSS (dSt)

2 + 12BII (dIt)

2 + BIS (dStdIt)]

+ HigherOrderTerms,

The expansion can stop at second order for diffusive moves.

Higher order terms can become significant when the security price/impliedvolatility can jump by a random amount.

It is difficult/messy to perform integrated analysis of both small andlarge moves.

Diffusive moves can be handled effectively via dynamic hedging(frequent updating of a few instruments)

Hedging random jumps need careful positioning of many derivativecontracts.

The effects of large jumps are better analyzed separately with scenarioanalysis/stress tests.

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 7 / 13

Risk-neutral valuation of the investment return

Take risk-neutral expectation on the investment P&L, and assume zero rate,

0 = Et

[dB

dt

]= Bt + BI Itµt +

1

2BSSS

2t σ

2t +

1

2BII I

2t ω

2t + BIS ItStγt (1)

(µt , σ2t , ω

2t , γt) are the time-t conditional mean and

variance/covariances:

µt ≡ Et

[dItIt

]/dt, σ2

t ≡ Et

[(dSt

St

)2]/dt,

ω2t ≡ Et

[(dItIt

)2]/dt, γt ≡ Et

[(dSt

St, dItIt

)]/dt.

(1) can be regarded as a pricing equation: The value of the optionmust satisfy this equality to exclude dynamic arbitrage.

Plug in the partial derivatives and rearrange, we obtain a simple valuationequation on the option implied volatility:

I 2t = σ2t + 2τµt I

2t + 2γtz+ + ω2

t z+z−.

z± ≡(lnK/Ft ± 1

2 I2t τ)

— convexity-adjusted moneyness

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 8 / 13

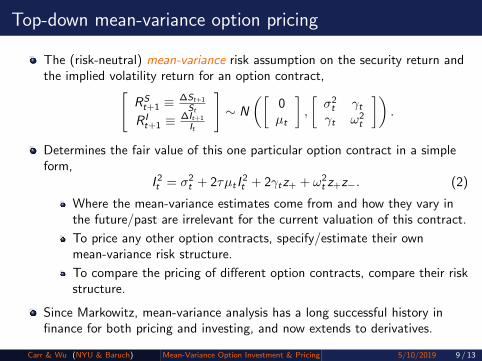

Top-down mean-variance option pricing

The (risk-neutral) mean-variance risk assumption on the security return andthe implied volatility return for an option contract,[

RSt+1 ≡

∆St+1

St

R It+1 ≡

∆It+1

It

]∼ N

([0µt

],

[σ2t γtγt ω2

t

]).

Determines the fair value of this one particular option contract in a simpleform,

I 2t = σ2

t + 2τµt I2t + 2γtz+ + ω2

t z+z−. (2)

Where the mean-variance estimates come from and how they vary inthe future/past are irrelevant for the current valuation of this contract.

To price any other option contracts, specify/estimate their ownmean-variance risk structure.

To compare the pricing of different option contracts, compare their riskstructure.

Since Markowitz, mean-variance analysis has a long successful history infinance for both pricing and investing, and now extends to derivatives.

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 9 / 13

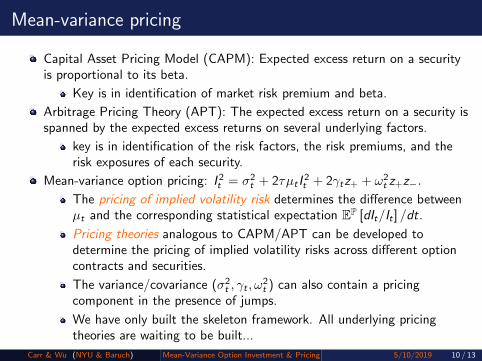

Mean-variance pricing

Capital Asset Pricing Model (CAPM): Expected excess return on a securityis proportional to its beta.

Key is in identification of market risk premium and beta.

Arbitrage Pricing Theory (APT): The expected excess return on a security isspanned by the expected excess returns on several underlying factors.

key is in identification of the risk factors, the risk premiums, and therisk exposures of each security.

Mean-variance option pricing: I 2t = σ2

t + 2τµt I2t + 2γtz+ + ω2

t z+z−.

The pricing of implied volatility risk determines the difference betweenµt and the corresponding statistical expectation EP [dIt/It ] /dt.

Pricing theories analogous to CAPM/APT can be developed todetermine the pricing of implied volatility risks across different optioncontracts and securities.

The variance/covariance (σ2t , γt , ω

2t ) can also contain a pricing

component in the presence of jumps.

We have only built the skeleton framework. All underlying pricingtheories are waiting to be built...

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 10 / 13

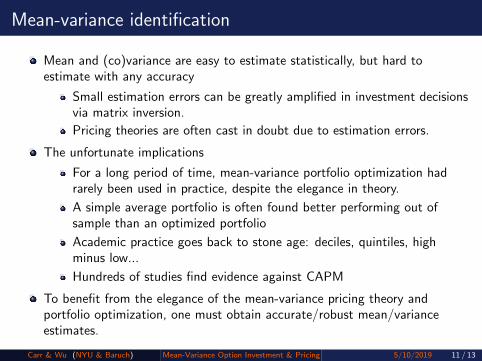

Mean-variance identification

Mean and (co)variance are easy to estimate statistically, but hard toestimate with any accuracy

Small estimation errors can be greatly amplified in investment decisionsvia matrix inversion.

Pricing theories are often cast in doubt due to estimation errors.

The unfortunate implications

For a long period of time, mean-variance portfolio optimization hadrarely been used in practice, despite the elegance in theory.

A simple average portfolio is often found better performing out ofsample than an optimized portfolio

Academic practice goes back to stone age: deciles, quintiles, highminus low...

Hundreds of studies find evidence against CAPM

To benefit from the elegance of the mean-variance pricing theory andportfolio optimization, one must obtain accurate/robust mean/varianceestimates.

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 11 / 13

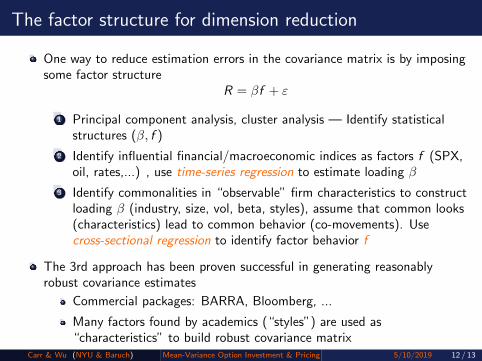

The factor structure for dimension reduction

One way to reduce estimation errors in the covariance matrix is by imposingsome factor structure

R = βf + ε

1 Principal component analysis, cluster analysis — Identify statisticalstructures (β, f )

2 Identify influential financial/macroeconomic indices as factors f (SPX,oil, rates,...) , use time-series regression to estimate loading β

3 Identify commonalities in “observable” firm characteristics to constructloading β (industry, size, vol, beta, styles), assume that common looks(characteristics) lead to common behavior (co-movements). Usecross-sectional regression to identify factor behavior f

The 3rd approach has been proven successful in generating reasonablyrobust covariance estimates

Commercial packages: BARRA, Bloomberg, ...

Many factors found by academics (“styles”) are used as“characteristics” to build robust covariance matrix

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 12 / 13

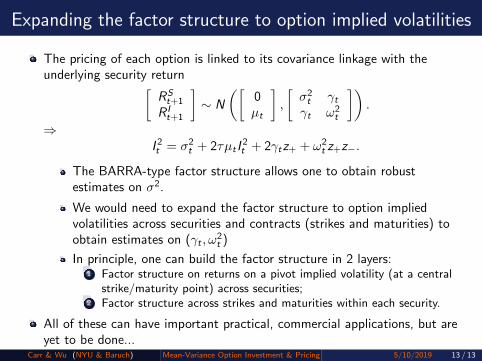

Expanding the factor structure to option implied volatilities

The pricing of each option is linked to its covariance linkage with theunderlying security return[

RSt+1

R It+1

]∼ N

([0µt

],

[σ2t γtγt ω2

t

]).

⇒I 2t = σ2

t + 2τµt I2t + 2γtz+ + ω2

t z+z−.

The BARRA-type factor structure allows one to obtain robustestimates on σ2.

We would need to expand the factor structure to option impliedvolatilities across securities and contracts (strikes and maturities) toobtain estimates on (γt , ω

2t )

In principle, one can build the factor structure in 2 layers:1 Factor structure on returns on a pivot implied volatility (at a central

strike/maturity point) across securities;2 Factor structure across strikes and maturities within each security.

All of these can have important practical, commercial applications, but areyet to be done...

Carr & Wu (NYU & Baruch) Mean-Variance Option Investment & Pricing 5/10/2019 13 / 13

![Mean-Variance Portfolio Rebalancing with Transaction · PDF fileMean-Variance Portfolio Rebalancing with Transaction Costs ... (Leland [2000] or Donohue and Yip [2003]). ... mean-variance](https://img.pdfslide.net/doc/110x75/5aa9b2147f8b9a81188d1c27/mean-variance-portfolio-rebalancing-with-transaction-portfolio-rebalancing-with.jpg)