Embed Size (px)

DESCRIPTION

bankin

Citation preview

Account Operations

Banker’s Quotient

Recap of Negotiable Instruments

Promissory Note

Bills of exchange

Cheques

Characteristics and features of NI

Endorsements

Crossings

Material alterations and Payment of cheque

Protection to paying & collecting Banker

List activities that you have seen

have heard@ branches

Stop PaymentCustomer can stop payment of a cheque ( single or multiple)

Written request – specify account number, cheque number and reason for stopping the payment

Verification of signature

Check whether it is already paid

If not, then accept & stop payment

Acknowledgement to customer

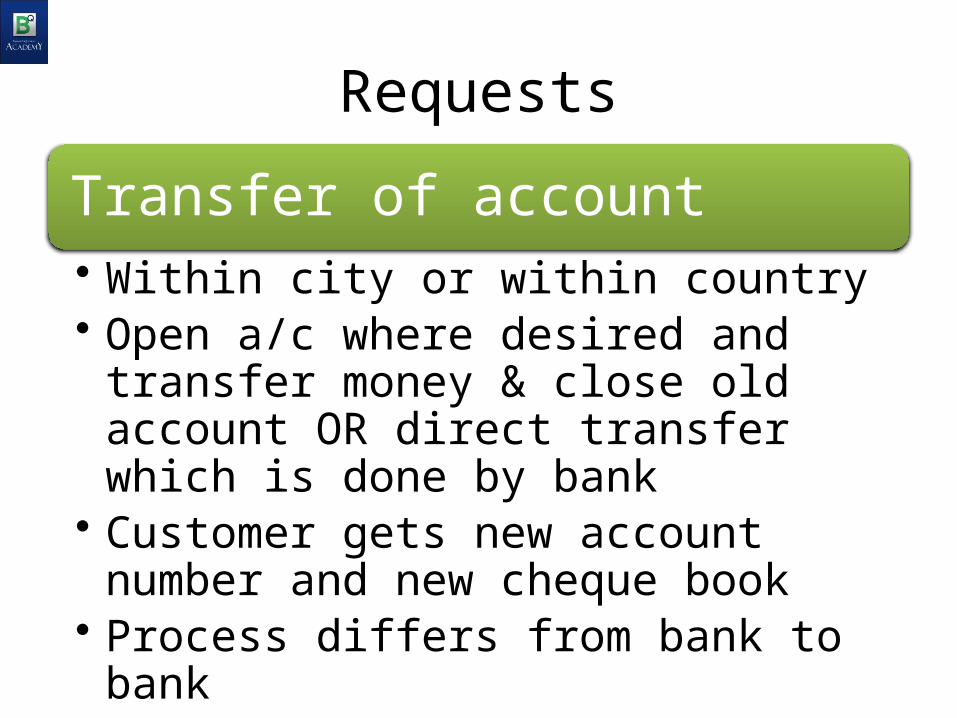

Requests

Transfer of account• Within city or within country• Open a/c where desired and transfer

money & close old account OR direct transfer which is done by bank

• Customer gets new account number and new cheque book

• Process differs from bank to bank

Requests

Addition of name Or deletion of name• Reconfiguration after death or one or more holders• Specific requests

Aspects of addition of names• Resident applicants cannot be added to non resident

accounts as holders (NRE,FCNR,RFC)• Can be added for NRO accounts as second holders• Cannot be added for loan accounts• No attachments or freeze should be there in existing

accounts

Process to add names Request letter from existing holders

Both new and existing holders need to fill a fresh form- order of holder must continue to be same

All relevant proof of new holder/s to be obtained

No objection/ letter acknowledging existence of ATM/Debit card of existing holder – from new holder

Nomination – fresh

If it is for companies, firms- fresh resolution

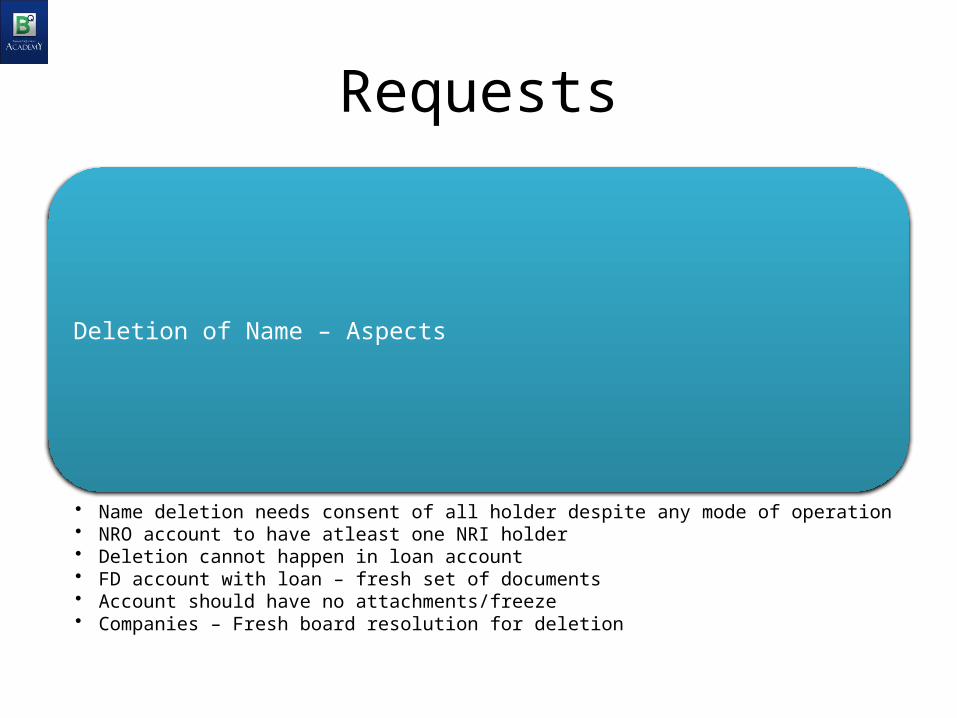

Requests

Deletion of Name – Aspects

• Name deletion needs consent of all holder despite any mode of operation• NRO account to have atleast one NRI holder• Deletion cannot happen in loan account• FD account with loan – fresh set of documents• Account should have no attachments/freeze• Companies – Fresh board resolution for deletion

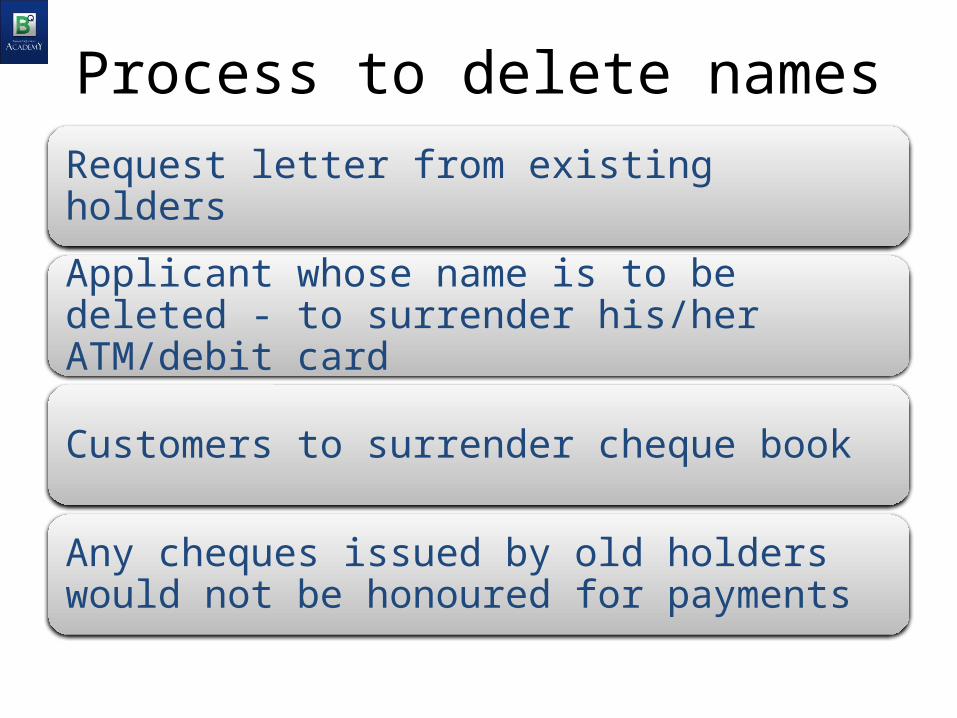

Process to delete names

Request letter from existing holders

Applicant whose name is to be deleted - to surrender his/her ATM/debit card

Customers to surrender cheque book

Any cheques issued by old holders would not be honoured for payments

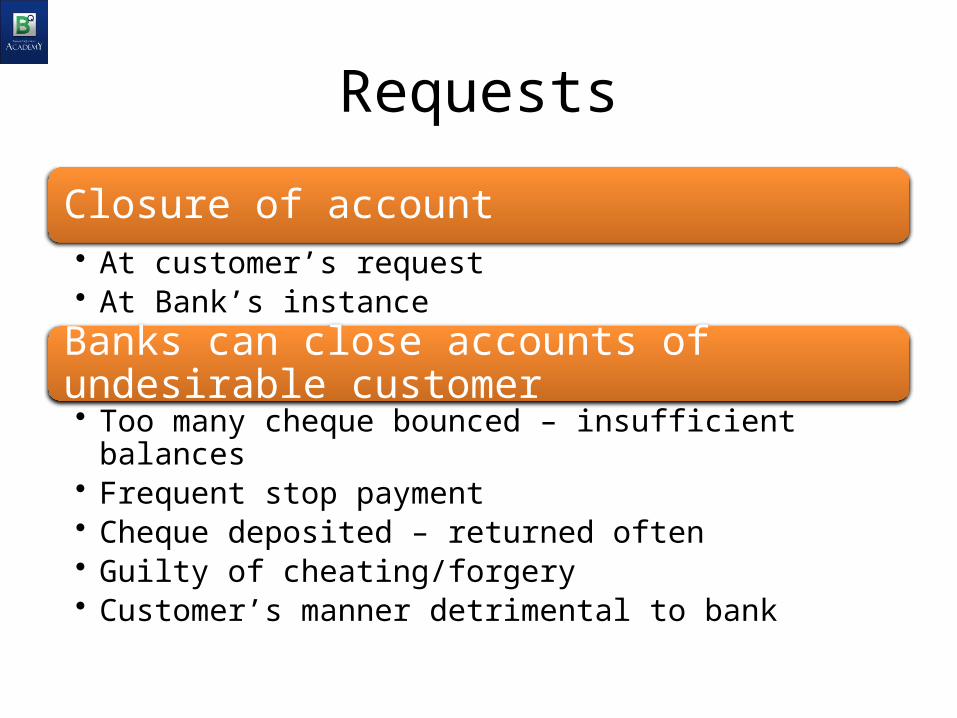

Requests

Closure of account• At customer’s request• At Bank’s instance

Banks can close accounts of undesirable customer • Too many cheque bounced – insufficient balances• Frequent stop payment• Cheque deposited – returned often• Guilty of cheating/forgery• Customer’s manner detrimental to bank

ListSome Special events which

happen@ home……

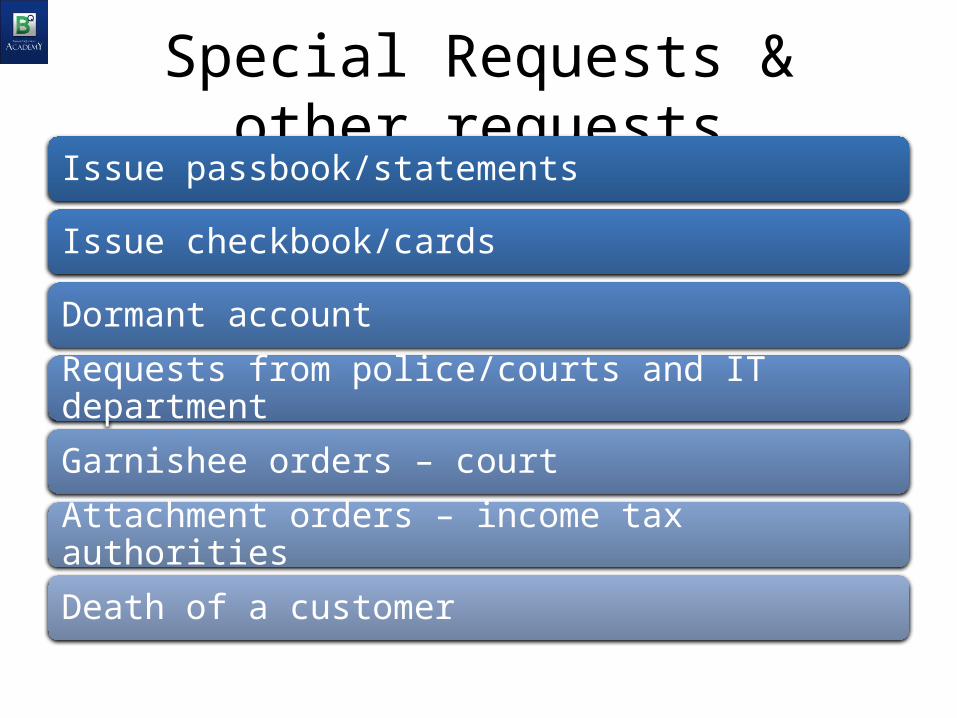

Special Requests & other requestsIssue passbook/statements

Issue checkbook/cards

Dormant account

Requests from police/courts and IT department

Garnishee orders – court

Attachment orders – income tax authorities

Death of a customer

Issue of cheque book, passbook, statement and other security items

Written request or the designated format from the bank – duly filled up by customer

Signature verified with the available records

Security items issued with additional verification of identity proof

Passbook updation is a regular request

Statement – sent by bank periodically – only additional requests need checking to ensure information is not provided to any one other than holder

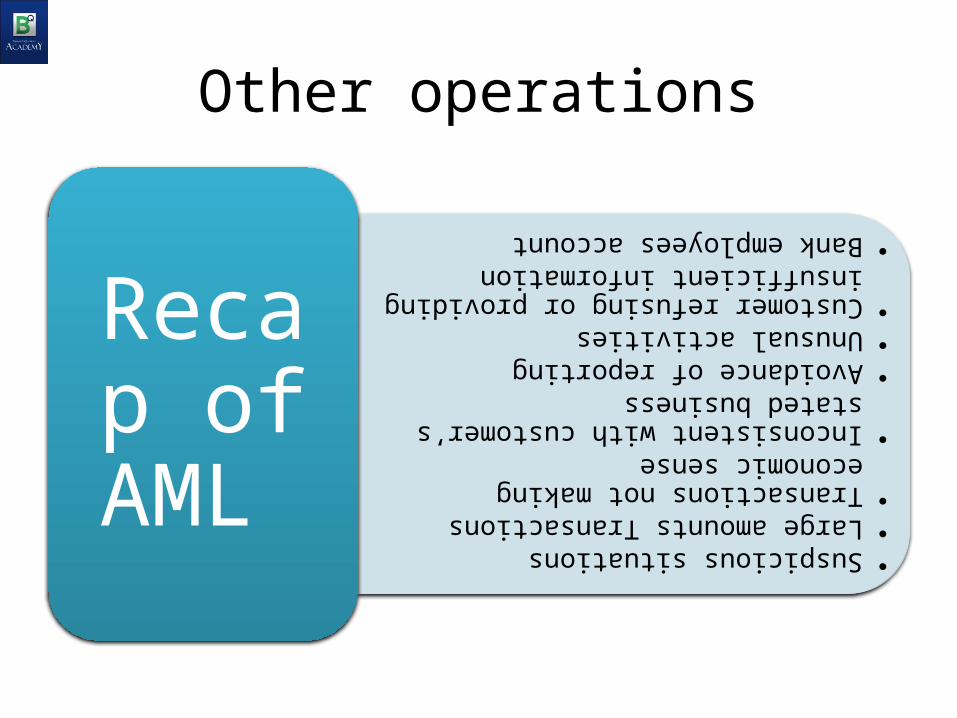

Other operations•Suspicious situations•Large amounts Transactions•Transactions not making

economic sense•Inconsistent with customer’s

stated business•Avoidance of reporting •Unusual activities •Customer refusing or providing

insufficient information•Bank employees account

Recap of AML

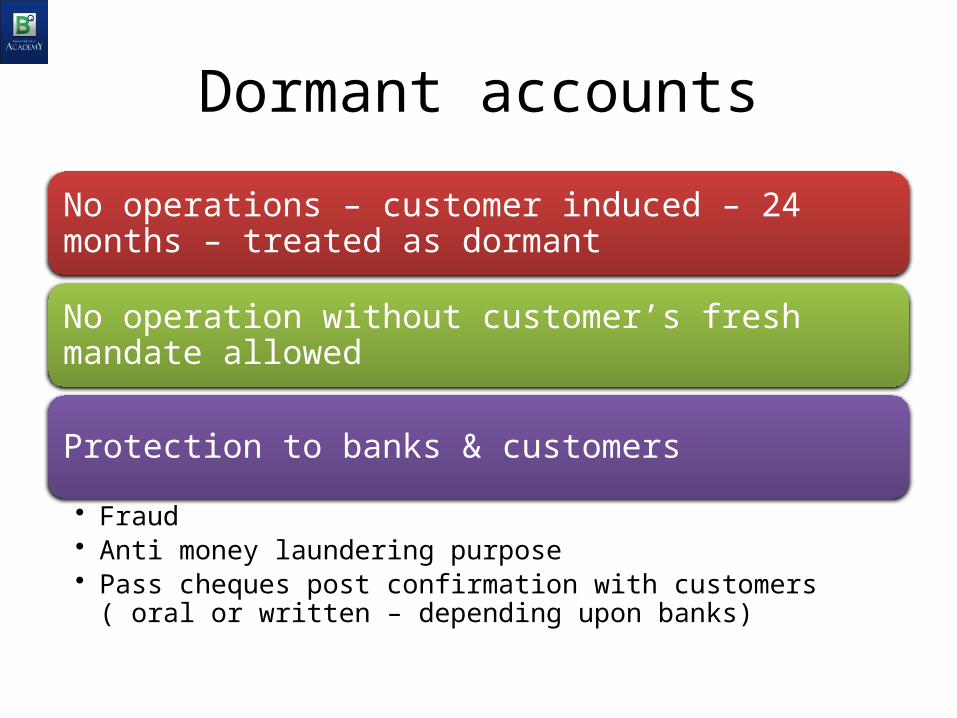

Dormant accounts

No operations – customer induced – 24 months – treated as dormant

No operation without customer’s fresh mandate allowed

Protection to banks & customers

• Fraud• Anti money laundering purpose• Pass cheques post confirmation with customers ( oral or written –

depending upon banks)

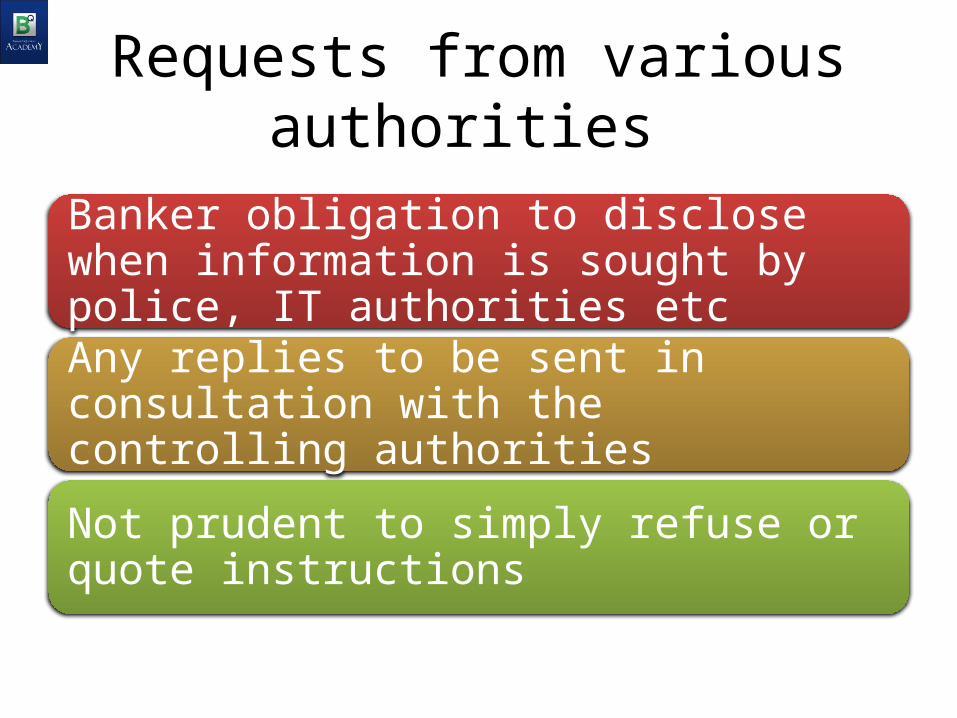

Requests from various authorities

Banker obligation to disclose when information is sought by police, IT authorities etc

Any replies to be sent in consultation with the controlling authorities

Not prudent to simply refuse or quote instructions

Garnishee Orders

Recap – Order nisi and order absolute

Banker customer relationship – suspended

Directs bank to stop payment out of this account

On receipt – recover any dues and then freeze the remaining amount

Customer informed of receipt of order

Bank’s reply provided to court and post that order absolute is issued

Bank needs to remit the frozen amount in entirety

WHERE CAN GARNISHEE ORDERBE APPLICABLE AND WHERE NOT

Income Tax attachment orderSec 226 of IT Act 1961

Credit balance attached • Any deposits due and payable• Debts due but not payable ( FDs which are to

mature)• Any amount received subsequently• Balance of other joint accounts• Funds of deceased/insolvent customers

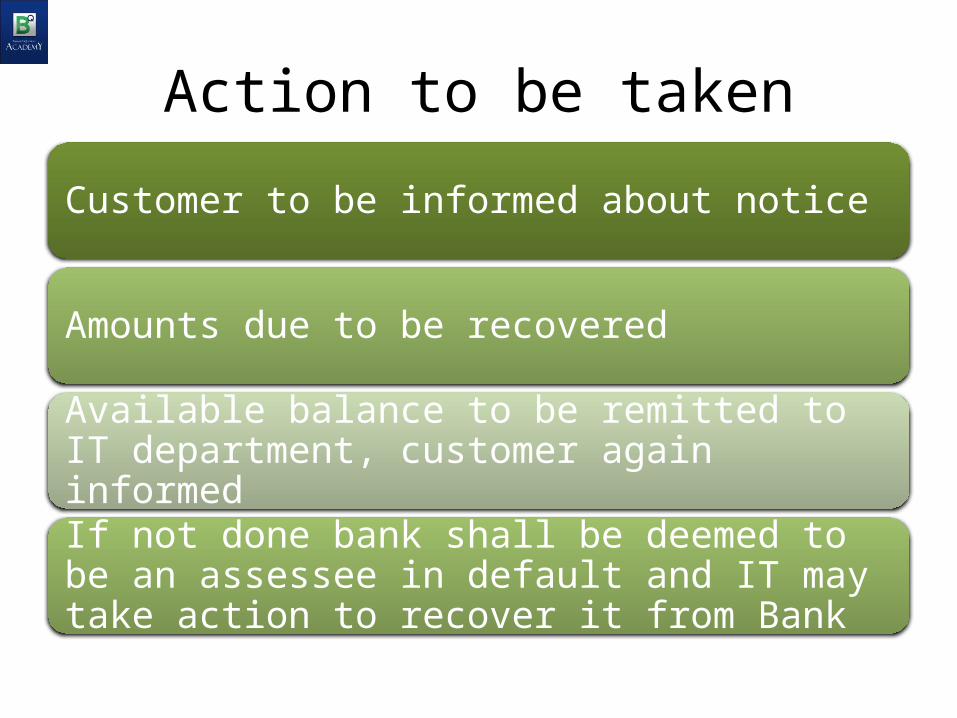

Action to be taken

Customer to be informed about notice

Amounts due to be recovered

Available balance to be remitted to IT department, customer again informed

If not done bank shall be deemed to be an assessee in default and IT may take action to recover it from Bank

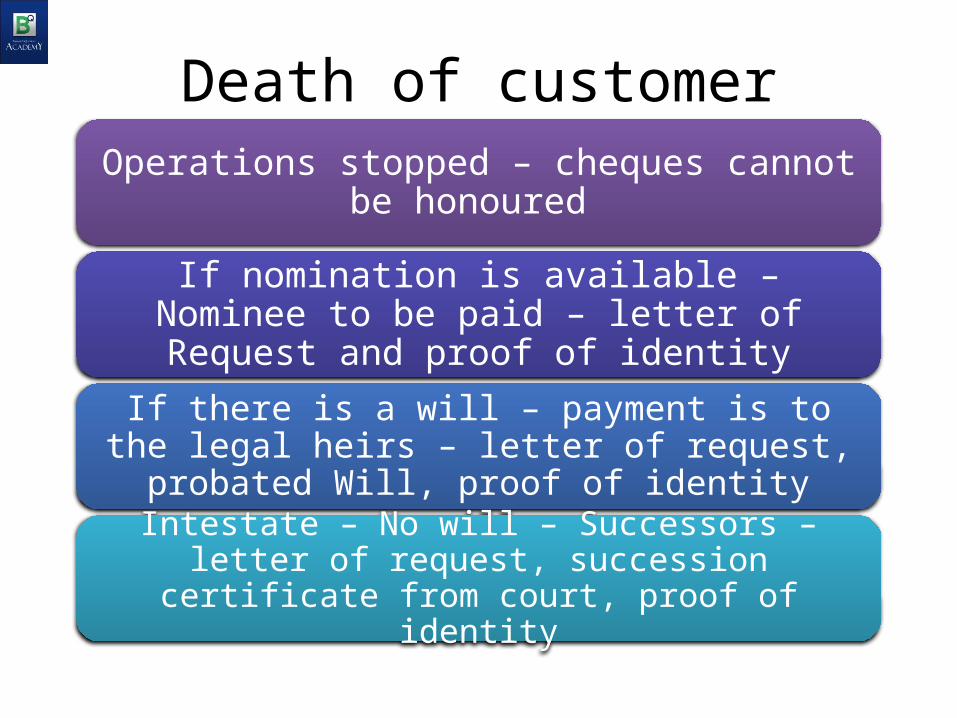

Death of customer

Operations stopped – cheques cannot be honoured

If nomination is available – Nominee to be paid – letter of Request and proof of identity

If there is a will – payment is to the legal heirs – letter of request, probated Will, proof of identity

Intestate – No will – Successors – letter of request, succession certificate from court, proof of identity

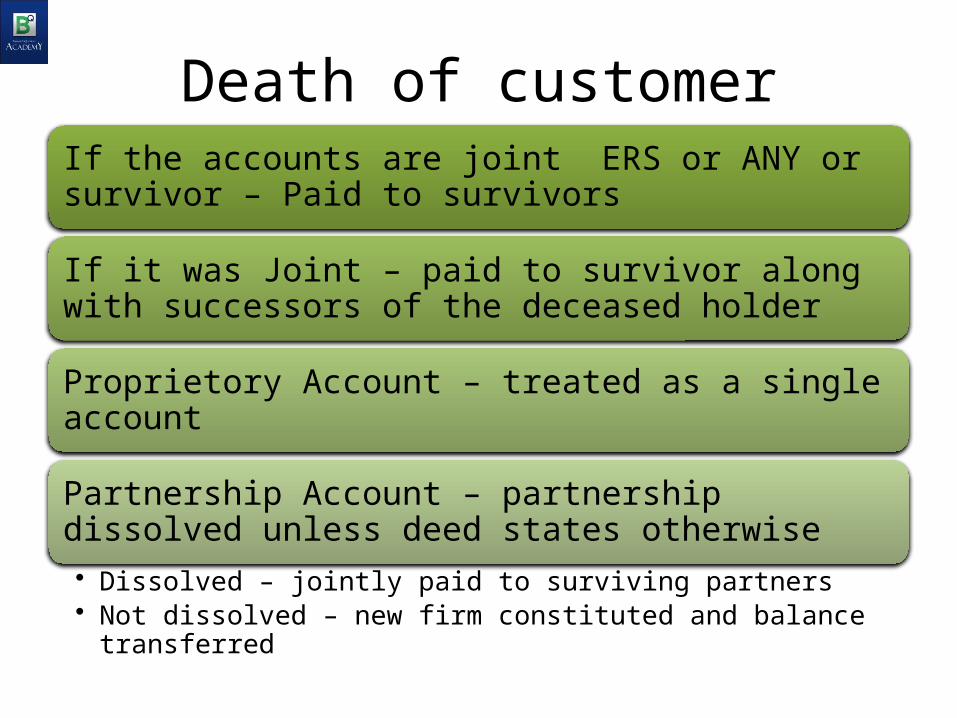

Death of customerIf the accounts are joint ERS or ANY or survivor – Paid to survivors

If it was Joint – paid to survivor along with successors of the deceased holder

Proprietory Account – treated as a single account

Partnership Account – partnership dissolved unless deed states otherwise • Dissolved – jointly paid to surviving partners• Not dissolved – new firm constituted and balance transferred

Death of customerFor entities – companies, HUF, Trust etc • Remaining members of board, company,

management can continue operation• Appoint new member and add him as authorized

signatory• Trusts- Trust deed reference to continue operations• HUF – next senior co-parcener will continue

operations• Executors administrators etc – appointed by court

and hence orders from court needed to operate

THANK YOU