Embed Size (px)

DESCRIPTION

November 1, 2011 Bryan Clontz, CFP® President Charitable Solutions, LLC

Citation preview

▪

Estate Planning Council of Central New York

▪

▪

▪

▪

[Divider Page]

Tab: “Resources for Advisors”

Program Benefits This program offers a number of benefits for financials advisors and donors:

Asset Retention: Advisors can retain and manage client charitable assets at their financial institution on an ongoing basis on behalf of the Community Founda-tion.Non-managed Assets: Non-managed cli-ent assets, such as real estate, closely-held business interests, personal property and art can be converted into charitable funds that are managed through the program.Philanthropic Services: Financial advisors can offer philanthropic consulting ser-vices to their clients by connecting them to the Community Foundation – adding value to their investment services and client relationships. With more than 80 years of experience, we are able to bring significant community knowledge to bear in crafting creative approaches to clients’ charitable goals and objectives.

Program Policies and CriteriaThe Community Foundation’s Board of Di-rectors has approved a policy statement for the Financial Advisors Program. Program highlights include:

Fund Minimum: This program is open to funds with minimum balances of $500,000. Funds with balances less than $500,000 may be invested in one of sev-eral other investment options we main-tain listed on page 2.

a.

b.

c.

a.

Investment Allocations Strategies: We have adopted four model investment alloca-tion strategies reflecting a variety of risk tolerances, time durations and philan-thropic purposes. These include: Short Duration Fixed Income, Core Fixed In-come, Balanced and Growth strategies.Reporting and Benchmarking: Our Fi-nance Committee and investment con-sultant will periodically review invest-ment performance of funds managed through the program against applicable benchmarks.

Identifying Clients Who Qualify Some typical examples of clients appropriate for this program include those who:

Are planning to sell a private company or have high capital gains tax exposureAre contemplating life transitions—whether they are retired, have no chil-dren or are involved in estate planning decisionsWant a charitable tax deduction now with the flexibility to make grants over time Want to grow charitable contributions tax-free over timeDesire to create endowments benefitting multiple nonprofit organizationsDesire to give something back to Cen-tral New York communitiesAre involved in multiple charities, civic causes or issuesWant to engage their children or family members in philanthropy

b.

c.

a.

b.

c.

d.

e.

f.

g.

h.

The Financial Advisors Program allows donors to recommend a financial advisor or firm to invest charitable funds created at the Central New York Community Foundation. The investments for these charitable funds are managed by financial advisors or firms outside of our primary investment pools.

: Financial Advisors Program

CENTRAL NEW YORK COMMUNITY FOUNDATION

www.cnycf.org(315) 422-9538

Types of FundsA variety of client charitable goals and objec-tives can be achieved through the Commu-nity Foundation’s charitable fund options.

Community Fund: Grants from our un-restricted Community Fund support the broadest range of charitable needs and issues in our region, now and in the fu-ture.Designated Funds: Donors designate specified charities to receive support on an ongoing basis. This option is popular in cases involving small charities, multi-ple charities or where there is a desire to endow and monitor charitable programs funded by the donor.Donor Advised Funds: A popular alter-native to a Private Foundation, Donor Advised Funds allow a donor, family, business or group to recommend grants from a charitable fund administered by the Community Foundation.Field of Interest Funds: For donors look-ing to support a particular field of inter-est (e.g., arts, environment), geographic area (e.g., Madison County, Auburn) or population (e.g., single mothers, in-dividuals with disabilities), a Field of Interest fund is structured to support ef-fective charitable programs in particular fields that change over time.Scholarship Funds: Funds can be created to focus on a particular a high school, college, scholastic discipline or profes-sional field. We are the largest non-aca-demic manager of scholarships in Cen-tral New York.

Bequests and Planned GiftsClients can name a fund to benefit from a percentage of their estates, as the remainder beneficiary after other gifts are made or uti-lize other gift options.

Charitable Trusts: Clients can establish a Charitable Remainder Trust or Chari-

a.

b.

c.

d.

e.

a.

table Lead Trust and name the Com-munity Foundation as the beneficiary for the purpose of creating any type of charitable fund and purpose.Private Foundation Termination: A client might consider terminating an existing Private Foundation in order to simplify their giving or address succession plan-ning issues.Retirement Plans: Naming the Commu-nity Foundation through a retirement plan beneficiary designation can be a very tax-efficient way to make a chari-table gift.

Other Investment Options We maintain several investment pools and options.

CNYCF Permanent Investment Pool: The permanent investment pool is our pri-mary investment vehicle, representing about $100 million in commingled in-vested assets for most of our 500 com-ponent charitable funds. This pool’s current allocation is: 55% equities, 22% fixed income and 23% alternatives.CNYCF Short Term Liquidity Pool: This investment pool is appropriate for funds with short-term horizons for grantmak-ing purposes or donors desiring no mar-ket exposure for their funds.American Funds Mutual Funds: For funds with balances of less than $500,000, do-nors may request an allocation to a port-folio of American Funds mutual funds. A donor’s financial advisor is listed as the referral source of record with Ameri-can Funds.Socially Responsible Investments: For do-nors desiring particular social screens or investment approaches outside these options above, we can craft personalized investment structures reflecting their goals.

b.

c.

a.

b.

c.

d.

: Financial Advisors Program (cont.)

www.cnycf.org(315) 422-9538

What is a Community Foundation?

•

•

•

•

•

•

▪

▪

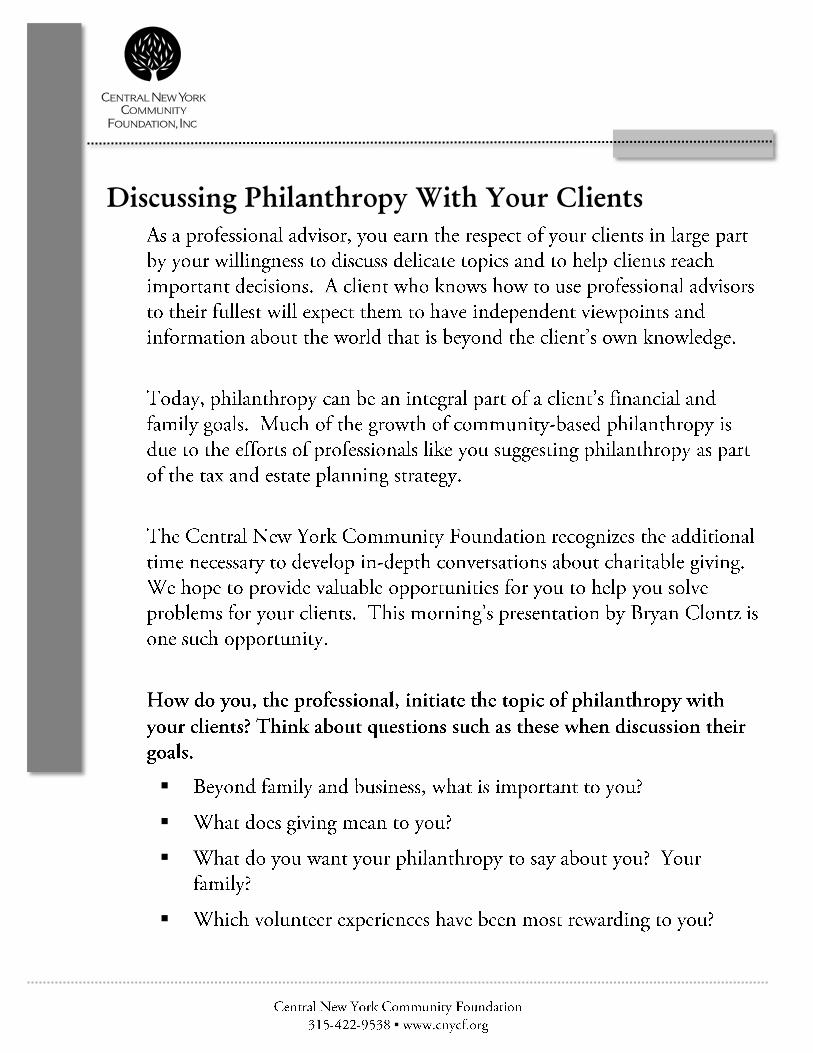

Discussing Philanthropy With Your Clients

▪

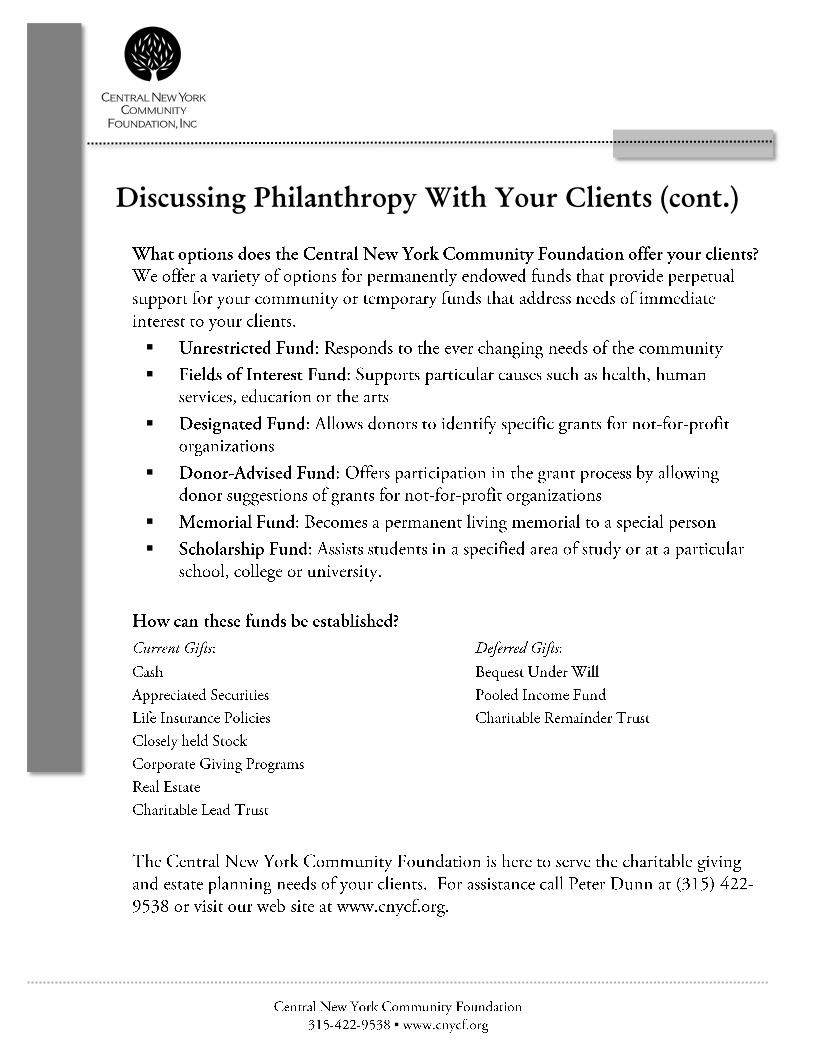

Discussing Philanthropy With Your Clients (cont.)

▪

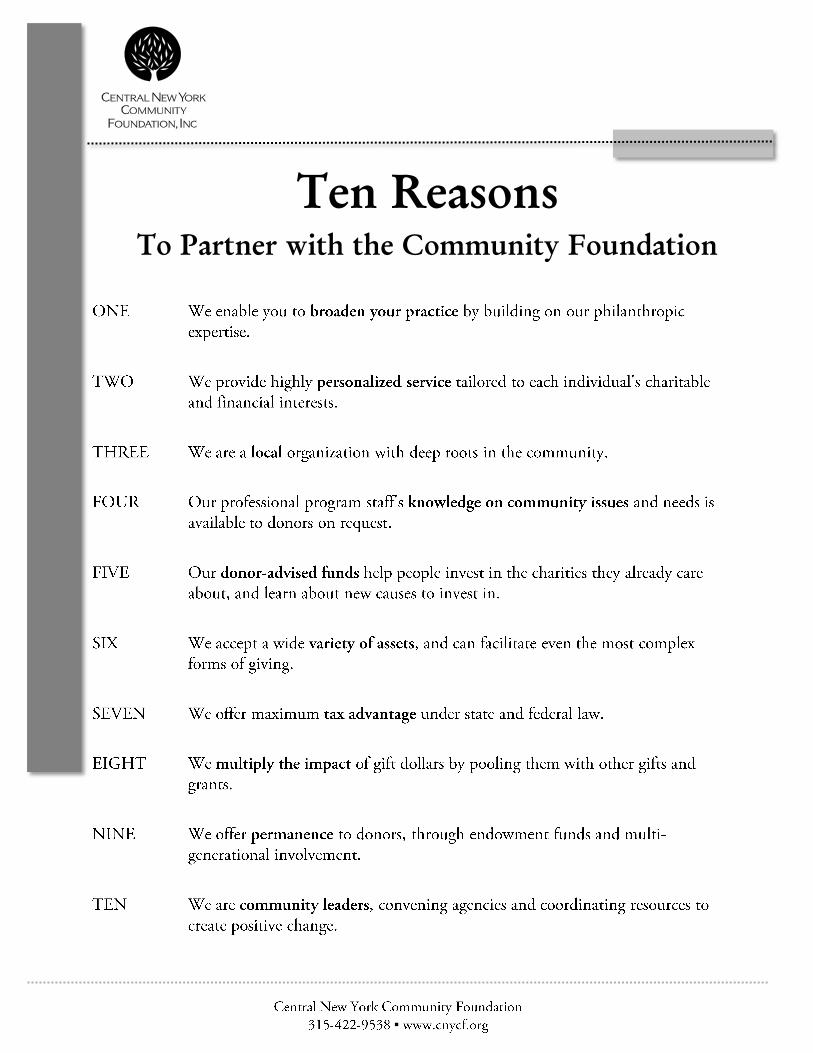

Ten Reasons

To Partner with the Community Foundation

▪

Typical Community Foundation Clients are:

[Divider Page]

Tab: “Presentation”

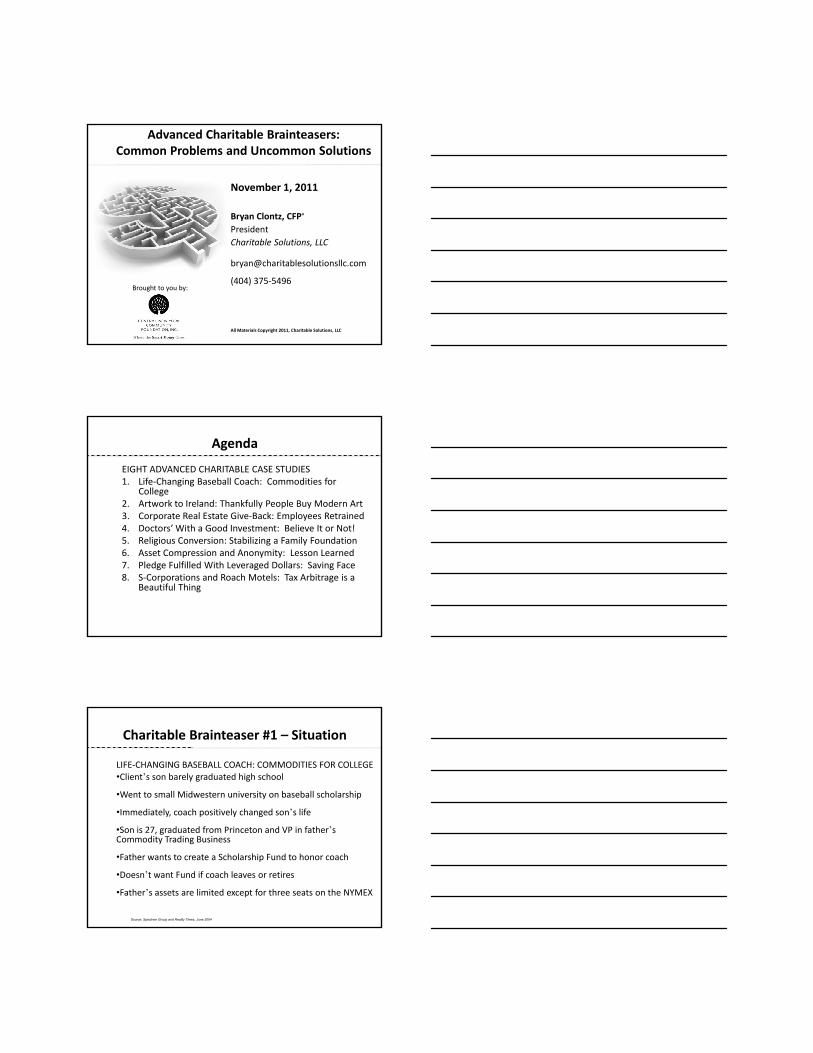

Advanced Charitable Brainteasers: Common Problems and Uncommon Solutions

November 1, 2011

Bryan Clontz, CFP®

President

Charitable Solutions, LLC

(404) 375‐5496

All Materials Copyright 2011, Charitable Solutions, LLC

Brought to you by:

Agenda

EIGHT ADVANCED CHARITABLE CASE STUDIES1. Life‐Changing Baseball Coach: Commodities for

College2. Artwork to Ireland: Thankfully People Buy Modern Art 3. Corporate Real Estate Give‐Back: Employees Retrained 4 D t ’ With G d I t t B li It N t!4. Doctors’ With a Good Investment: Believe It or Not!5. Religious Conversion: Stabilizing a Family Foundation6. Asset Compression and Anonymity: Lesson Learned7. Pledge Fulfilled With Leveraged Dollars: Saving Face 8. S‐Corporations and Roach Motels: Tax Arbitrage is a

Beautiful Thing

Charitable Brainteaser #1 – Situation

LIFE‐CHANGING BASEBALL COACH: COMMODITIES FOR COLLEGE•Client’s son barely graduated high school

•Went to small Midwestern university on baseball scholarship

•Immediately, coach positively changed son’s life

•Son is 27, graduated from Princeton and VP in father’s Commodity Trading Business

•Father wants to create a Scholarship Fund to honor coach

•Doesn’t want Fund if coach leaves or retires

•Father’s assets are limited except for three seats on the NYMEX

Source: Spectrem Group and Reality Times, June 2004

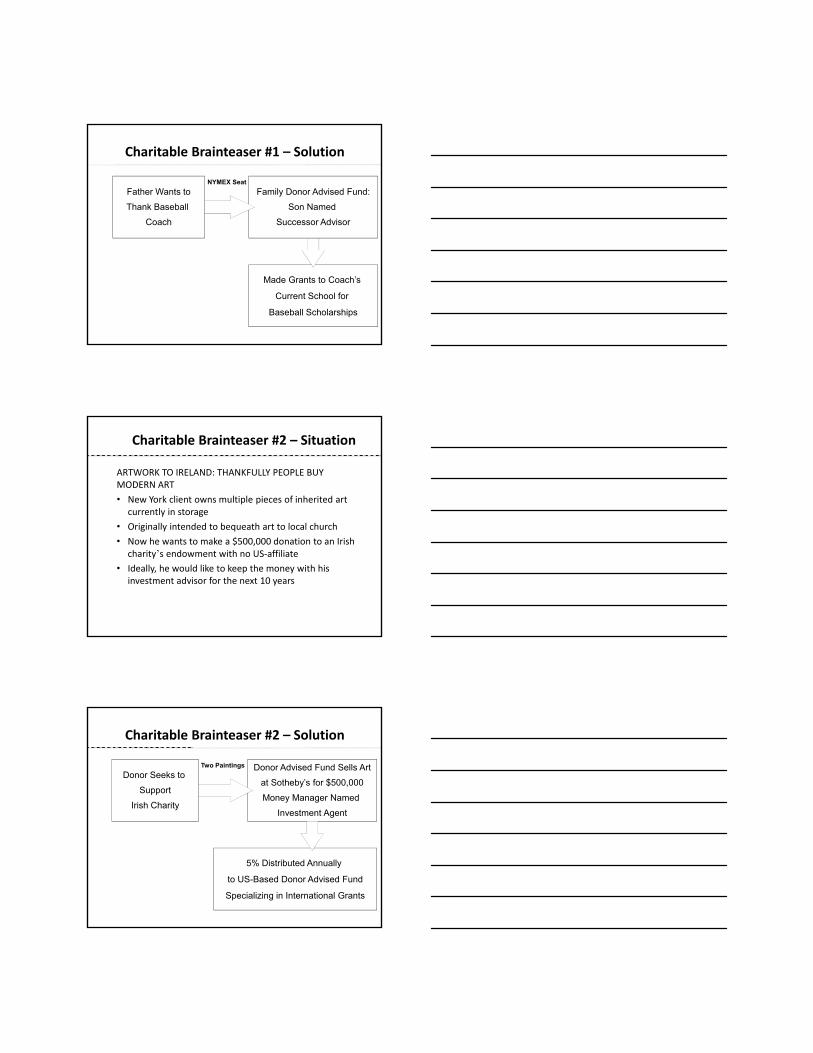

Charitable Brainteaser #1 – Solution

NYMEX Seat

Family Donor Advised Fund:

Son Named

Successor Advisor

Father Wants to

Thank Baseball

Coach

Made Grants to Coach’s

Current School for

Baseball Scholarships

Charitable Brainteaser #2 – Situation

ARTWORK TO IRELAND: THANKFULLY PEOPLE BUY MODERN ART

• New York client owns multiple pieces of inherited art currently in storage

• Originally intended to bequeath art to local church• Originally intended to bequeath art to local church

• Now he wants to make a $500,000 donation to an Irish charity’s endowment with no US‐affiliate

• Ideally, he would like to keep the money with his investment advisor for the next 10 years

Charitable Brainteaser #2 – Solution

Donor Advised Fund Sells Art

at Sotheby’s for $500,000

Money Manager Named

Investment Agent

Two Paintings

Donor Seeks to

Support

Irish Charity

5% Distributed Annually

to US-Based Donor Advised Fund

Specializing in International Grants

Charitable Brainteaser #3 – Situation

CORPORATE REAL ESTATE GIVE‐BACK: EMPLOYEES RETRAINED

• Fortune 500 corporation shut down domestic textile mill production and outsourced jobs

• Goal was to create a foundation to provide job‐retrainingGoal was to create a foundation to provide job retraining and social service grants to effected employees

• Critically important to maximize tax savings and minimize administrative burden

• Would consider funding with cash or shuttered mill property

Charitable Brainteaser #3 – Solution

Corporation Donor Advised Fund

VP/Community Affairs Named

Fund Advisor

Mill Real Estate

Public Corporations

Wants to Support

Displaced Employees

Grants to Multiple Southeastern Rural

Communities for Job Retraining and

Social Services

Charitable Brainteaser #4 – Situation

DOCTORS WITH A GOOD INVESTMENT: BELIEVE IT OR NOT!

• Four doctors owned their medical building with virtually zero cost‐basis

• A regional REIT offered to purchase it every year

D t t d t ti d ll ti t i j i• Doctors wanted to retire and sell practice to six junior doctors

• Junior doctors wanted long‐term lease

• Each doctor was charitably‐inclined but wanted to maximize tax savings and receive a life income

• Two were particularly concerned about disinheriting children/grandchildren with donations

Charitable Brainteaser #4 – Solution

$1 2 illi /20% I

Four Donor Advised Funds

Children Successor Advisors

$1.2 million/20% Interest Four 7 Percent

Charitable Remainder Trusts

for LifeFour Doctors

Owned $6.0 Million Medical Building

$1.2 million/20% Interest

Multiple Grants

to Multiple Charities

$1 Million

Insurance

Trust #1

$300K

Insurance

Trust #2

Charitable Brainteaser #5 – Situation

RELIGIOUS CONVERSION:STABILIZING A FAMILY FOUNDATION

• 5 years ago, grandfather wanted a 100% charitable estate tax deduction without irrevocably giving the assets to charity

h ld d f d h ld• Now, two children and four grandchildren are on foundation’s board – one grandchild married outside of faith and upset her brother

• She feels ostracized and can’t make grants to new church

• Family foundation had not met 5% payout requirement and also wanted to grant to an environmental charity but application expressly excluded environmental groups

Charitable Brainteaser #5 – Solution

Donor Advised Fund

for Daughter

26-Year Charitable

Lead Annuity Trust/

Family Foundation

2 Parents/4 Children

Daughter Made Grants on Her Terms

and Family Foundation Flowed Anonymous Grants Through Fund

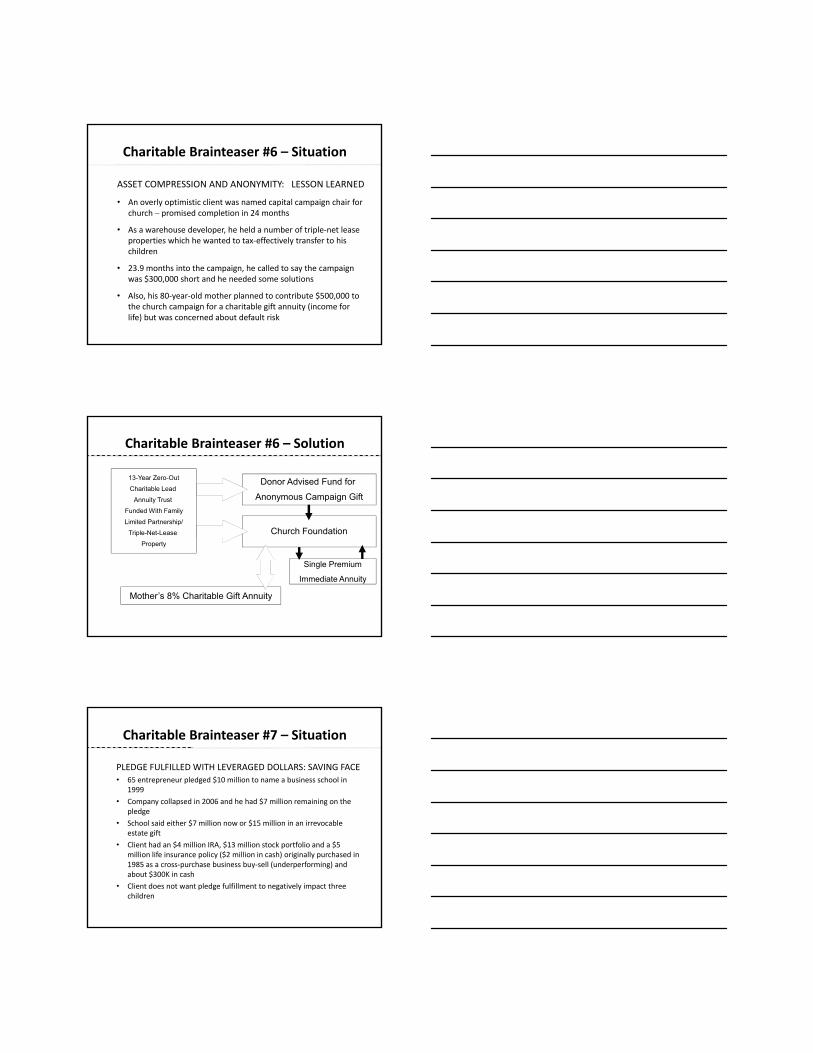

Charitable Brainteaser #6 – Situation

ASSET COMPRESSION AND ANONYMITY: LESSON LEARNED

• An overly optimistic client was named capital campaign chair for church – promised completion in 24 months

• As a warehouse developer, he held a number of triple‐net lease properties which he wanted to tax‐effectively transfer to his children

• 23.9 months into the campaign, he called to say the campaign was $300,000 short and he needed some solutions

• Also, his 80‐year‐old mother planned to contribute $500,000 to the church campaign for a charitable gift annuity (income for life) but was concerned about default risk

Charitable Brainteaser #6 – Solution

Donor Advised Fund for

Anonymous Campaign Gift

13-Year Zero-Out

Charitable Lead

Annuity Trust

Funded With Family

Limited Partnership/

Mother’s 8% Charitable Gift Annuity

Church Foundation

Single Premium

Immediate Annuity

Triple-Net-Lease

Property

Charitable Brainteaser #7 – Situation

PLEDGE FULFILLED WITH LEVERAGED DOLLARS: SAVING FACE

• 65 entrepreneur pledged $10 million to name a business school in 1999

• Company collapsed in 2006 and he had $7 million remaining on the pledge

• School said either $7 million now or $15 million in an irrevocable estate gift

• Client had an $4 million IRA, $13 million stock portfolio and a $5 million life insurance policy ($2 million in cash) originally purchased in 1985 as a cross‐purchase business buy‐sell (underperforming) and about $300K in cash

• Client does not want pledge fulfillment to negatively impact three children

Charitable Brainteaser #7 – Solution

Donor 1035-Exchanges Old

Policy For Better Performing

$15 Million Death Benefit/

$4 Million Cash Value

Donor Needs to

Complete School

Pledge

Donates Policy to University

Funds with IRA Contribution and

$2 million Appreciated Stock

$4 Million Cash Value

$2 Million

Life Insurance Trust

For Three Children

$100K from

IRA – Tax-Free

Charitable Brainteaser #8 – Situation

S‐CORPORATIONS AND ROACH MOTELS: TAX ARBITRAGE IS A BEAUTIFUL THING

• Investment advisor’s firm is a S‐Corp and he wants to sell $500,000 to new partner

• State income tax rate is 8%State income tax rate is 8%

• Investment advisor is charitably‐inclined

• Advisor wants to use the S‐Corp stock if possible to make a contribution to consumer credit counseling

• S‐Corp has zero cost‐basis and all gain is categorized as unrelated business taxable income to the charity (UBTI)

Charitable Brainteaser #8 – Solution

Public Charitable Trust

With a Donor Advised Fund

Sells to New Partner/15% Gains

Tax Reduced by 50% for Deduction

Advisor Contributes

S-Corp to Trust-Form

Public Charity in

Florida (Income for Deduction

Charity Receives Net 94% of Gift as Grant

Donor Receives a 100% FMV Deduction

Vs. Sale and Gift Netting 77% to Donor and Charity

Tax-Free State)

35 90%

41.20%

16.60%

16.40%

26.60%

16.10%

26.00%

27.80%

42.90%

44.30%

19.80%

24.10%

38.80%

40.80%

67.50%

Peers or Peer Networks

Fundraisers / Nonprofit staff

Financial and Wealth Advisors

Attorney

Accountant

HIGH NET WORTH HOUSEHOLDS CHARITABLE GIVING DECISIONS BY TYPE OF PERSON CONSULTED (%)

2010

3.70%

7.10%

12.30%

8.70%

15.20%

35.90%

4.00%

9.90%

3.30%

16.50%

15.10%18.10%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Coaching Program

Broker

Others

Bank or Trust Co. Staff

Community Foundation Staff2008

2006

The following slides were developed by Lee Hoffman, President/CEO, Planned Giving Design Center from data derived from "The 2010 Study of High Net Worth Philanthropy" Sponsored by Bank of America and researched and written by The Center on Philanthropy at Indiana University

20.90%

46.50%

3.10%

11.70%

D Ad i d F d t C Fd

Endowment Fund

Will with Charitable Provision

HIGH NET WORTH HOUSEHOLDS WHO HAVE OR WOULD CONSIDER ESTABLISHING IN THREE YEARS

12.00%

15.40%

17.50%

3.40%

8.00%

2.80%

0% 10% 20% 30% 40% 50% 60% 70%

Private Foundation

Charitable Remainder/ Lead Trust/ Gift Annuity

Donor‐Advised Fund at Comm. Fdn., Bank or Other Org.

Currently Have Would Consider Establishing in 3 Years

10%

WHO INITIATED THE CONVERSATION ABOUT PHILANTHROPY?

90%

Donor Advisor

Thank you for Coming!

Bryan Clontz, CFP®

President

Charitable Solutions, LLC

(404) 375‐5496

Peter A. Dunn

President & CEO

Central New York Community Foundation

(315) 422‐9538

[Divider Page]

Tab: “Resources”

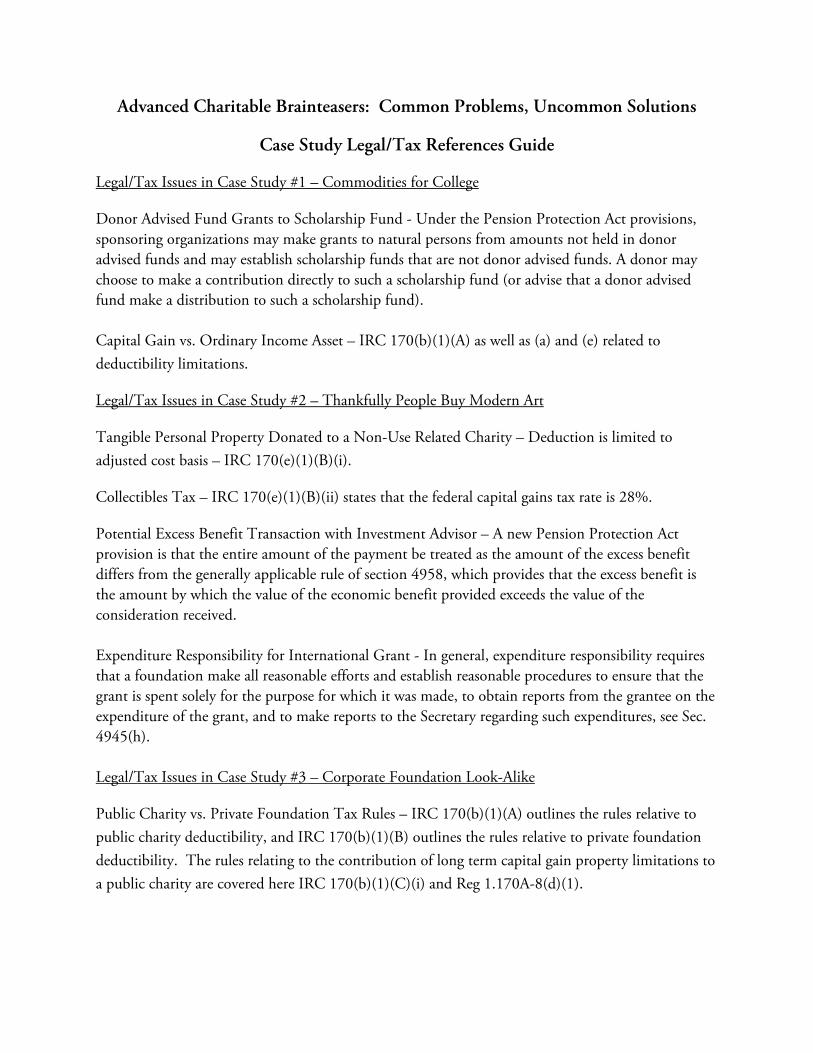

Advanced Charitable Brainteasers: Common Problems, Uncommon Solutions

Case Study Legal/Tax References Guide

Legal/Tax Issues in Case Study #1 – Commodities for College

Donor Advised Fund Grants to Scholarship Fund - Under the Pension Protection Act provisions, sponsoring organizations may make grants to natural persons from amounts not held in donor advised funds and may establish scholarship funds that are not donor advised funds. A donor may choose to make a contribution directly to such a scholarship fund (or advise that a donor advised fund make a distribution to such a scholarship fund). Capital Gain vs. Ordinary Income Asset – IRC 170(b)(1)(A) as well as (a) and (e) related to deductibility limitations.

Legal/Tax Issues in Case Study #2 – Thankfully People Buy Modern Art

Tangible Personal Property Donated to a Non-Use Related Charity – Deduction is limited to adjusted cost basis – IRC 170(e)(1)(B)(i).

Collectibles Tax – IRC 170(e)(1)(B)(ii) states that the federal capital gains tax rate is 28%.

Potential Excess Benefit Transaction with Investment Advisor – A new Pension Protection Act provision is that the entire amount of the payment be treated as the amount of the excess benefit differs from the generally applicable rule of section 4958, which provides that the excess benefit is the amount by which the value of the economic benefit provided exceeds the value of the consideration received. Expenditure Responsibility for International Grant - In general, expenditure responsibility requires that a foundation make all reasonable efforts and establish reasonable procedures to ensure that the grant is spent solely for the purpose for which it was made, to obtain reports from the grantee on the expenditure of the grant, and to make reports to the Secretary regarding such expenditures, see Sec. 4945(h). Legal/Tax Issues in Case Study #3 – Corporate Foundation Look-Alike

Public Charity vs. Private Foundation Tax Rules – IRC 170(b)(1)(A) outlines the rules relative to public charity deductibility, and IRC 170(b)(1)(B) outlines the rules relative to private foundation deductibility. The rules relating to the contribution of long term capital gain property limitations to a public charity are covered here IRC 170(b)(1)(C)(i) and Reg 1.170A-8(d)(1).

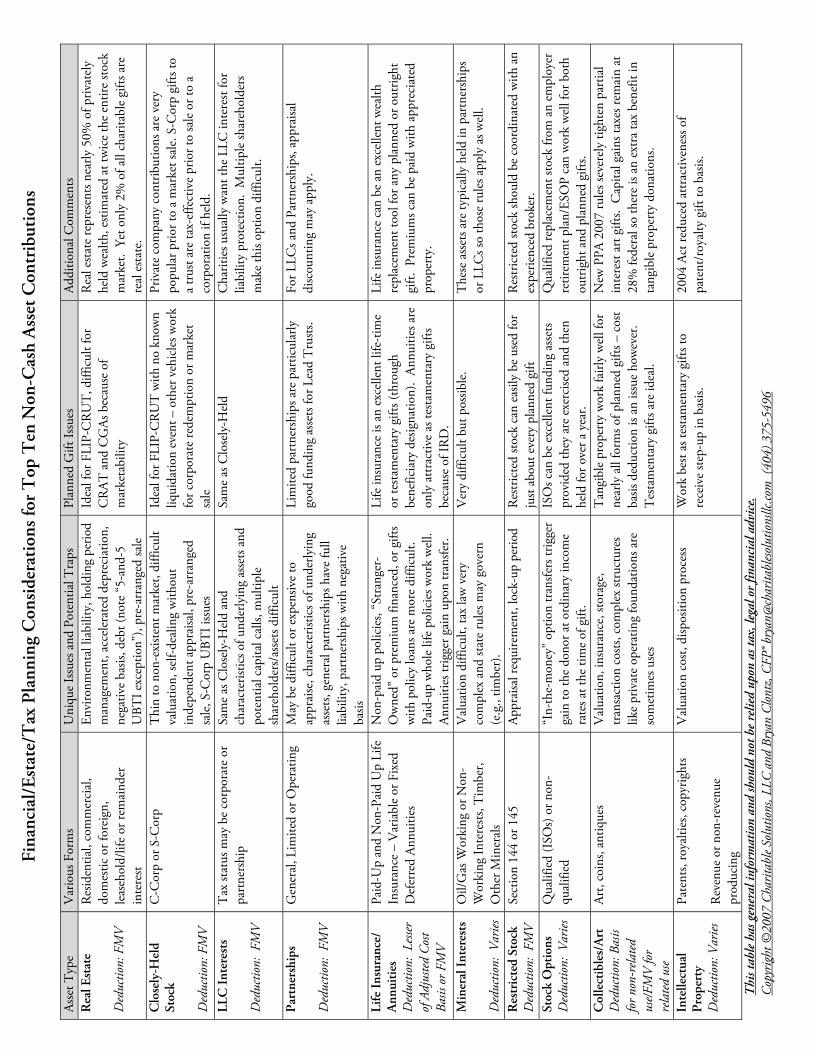

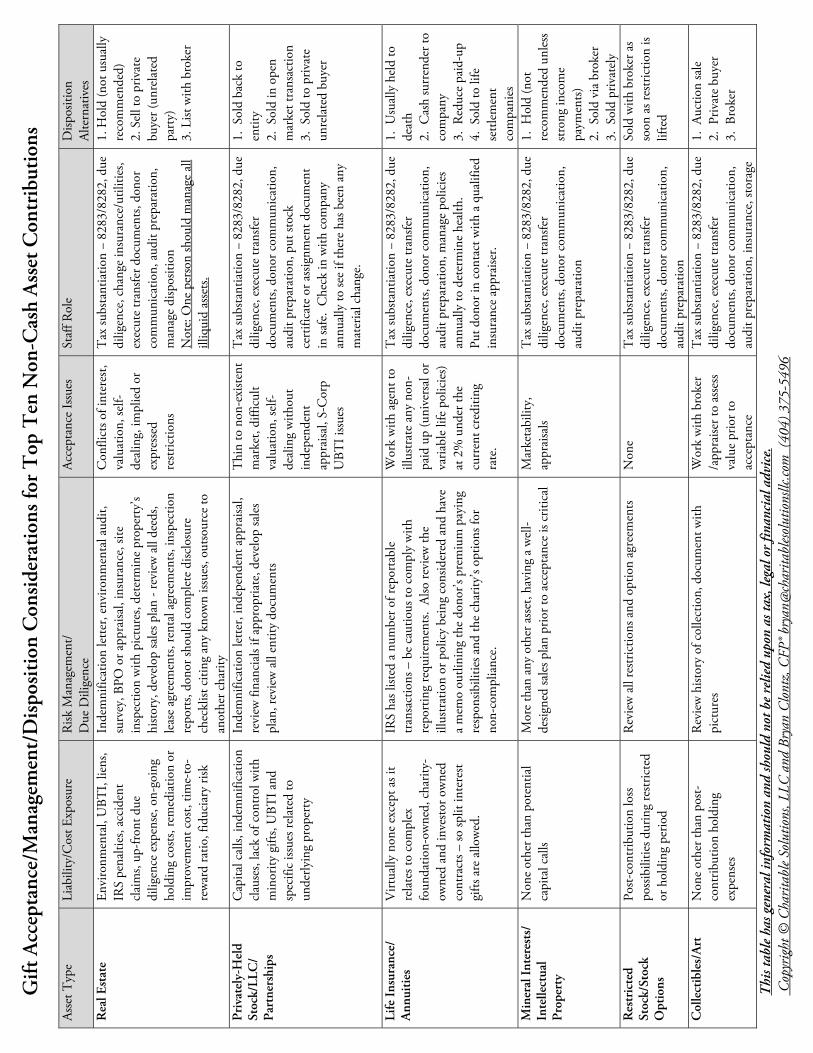

C-Corporation Deduction Rules - IRC 170(b)(2), IRC 170(d)(2) and Reg. 1.170A-11(c) cover the 10% of net income deduction limitation and the five year carry forward provisions for any unused deduction.

Legal/Tax Issues in Case Study #4 – Doctors with a Real Estate Investment

Partial Interest Gifts - IRC 170(f)(3) disallows any partial interest gifts. The exceptions can be an entire undivided interest (IRC 170(f)(B)(iii) or qualified split-interest contributions like charitable remainder trusts – see IRC 664(d)(2).

Qualified Appraisal Requirements and Substantiation – Pension Protection Act Definitions

Qualified Appraisers The provision defines a qualified appraiser as an individual who (1) has earned an appraisal designation from a recognized professional appraiser organization or has otherwise met minimum education and experience requirements to be determined by the IRS in regulations; (2) regularly performs appraisals for which he or she receives compensation; (3) can demonstrate verifiable education and experience in valuing the type of property for which the appraisal is being performed; (4) has not been prohibited from practicing before the IRS by the Secretary at any time during the three years preceding the conduct of the appraisal; and (5) is not excluded from being a qualified appraiser under applicable Treasury regulations. Qualified Appraisals The provision defines a qualified appraisal as an appraisal of property prepared by a qualified appraiser (as defined by the provision) in accordance with generally accepted appraisal standards and any regulations or other guidance prescribed by the Secretary.

See Reg. 1.170A-13(c)(1)(i) and Reg. 1.170A-13(c)(3)(i).

Charitable Remainder Trust Provisions – Charitable remainder trusts are discussed at length in Chapter 13. Flip unitrust provisions can be seen in Reg. 1.664-3(a)(1(i)(c)-1.6643(a)(1)(i)(f).

Irrevocable Life Insurance Trust – This trust, if designed properly, allows for the death benefit to be both income and estate tax free - IRC 2042(1) and(2).

Legal/Tax Issues in Case Study #5 – Stabilizing a Family Foundation

Charitable Lead Annuity Trust – For a comprehensive overview of charitable lead trusts, see IRC 170(f)(2)(B), 2055(e)(2)(B) and 2522(c)(2)(B).

Private Foundation Qualifying Grant – The 5 percent minimum distribution rule is covered here IRC 4942(e). Grants to public charities, like community foundations component funds, qualify as distributed income.

Anonymous Grants – Private foundations must disclose all grants on the 990-PF tax return. Community foundations also have to disclose the amount and organization of all grants, however, they are aggregated from all the sponsoring organizations component funds. The public charity 990 tax return does not require each grant to be “attached” to specific funds.

Legal/Tax Issues in Case Study #6 – Asset Compression and Anonymity

Charitable Lead Annuity Trust Valuation – The IRS approved a CLT funding with limited partnership interests, as the partnership’s income comprised solely of passive investment income. Thus it was not a business enterprise and the income was not unrelated business taxable income (UBTI) – see PLR 9810019.

Charitable Gift Annuity – Complete coverage of gift annuities can be found at Reg. 1.170A-1(d)(1), Rev. Rul. 55-388, 1955-1 CB 233; Rev. Rul. 80-281, 1980-2 CB 282 – in particular the tax deductibility of the qualified installment bargain sale transaction.

Charitable Gift Annuity Reinsurance Provisions – Qualifying reinsurance provisions can be found in 170(f)10 charitable reverse split dollar rules. There have also been two relatively recent PLRs 200847014 and 200852037 that allow for some flexibility in the reinsurance design. A number of additional articles can be found at http://charitablesolutionsllc.com/library.html and the American Council on Gift Annuities – www.acga-net.org.

Legal/Tax Issues in Case Study #7

IRA Rollover – A qualified charitable IRA rollover, outlined in IRC 408(d)(8)(A), allows an individual 70 ½ and older, to make a direct contribution of up to $100,000 of their retirement account to a public charity (excluding donor advised funds and supporting organizations). It was extended through December 31, 2011. The direct distribution is not included in income.

Charitable Gifts of Life Insurance – Since nearly all life insurance gain is ordinary income, the deduction is limited to the lesser of fair market value or adjusted cost basis – see IRC 170(e)(1)(A).

Legal/Tax Issues in Case Study #8

Charitable Gifts of S-Corp Stock – Chris Hoyt wrote an excellent article on S-Corp at http://lawprofessors.typepad.com/trusts_estates_prof/2011/09/donations-by-s-corporations-and-shareholders-.html . It is also covered in IRC 512(e).

Trust Tax Law for Charitable Contributions – IRC 512(B)(2) allows for a trust to take a charitable income tax deduction up to 50% of its Unrelated Business Taxable Income (UBTI). Further, a trust is taxed at individual rates for recognized long-term capital gains at the 15 percent federal rate.

Fina

ncia

l/Es

tate

/Tax

Pla

nnin

g C

onsi

dera

tion

s fo

r T

op T

en N

on-C

ash

Ass

et C

ontr

ibut

ions

Asse

t Typ

e V

ario

us F

orm

s U

niqu

e Is

sues

and

Pot

entia

l Tra

psPl

anne

d G

ift Is

sues

Ad

ditio

nal C

omm

ents

Rea

l Est

ate

Ded

uctio

n: F

MV

Res

iden

tial,

com

mer

cial

, do

mes

tic o

r for

eign

, le

aseh

old/

life

or re

mai

nder

in

tere

st

Envi

ronm

enta

l lia

bilit

y, h

oldi

ng p

erio

d m

anag

emen

t, ac

cele

rate

d de

prec

iatio

n,

nega

tive

basis

, deb

t (no

te “

5-an

d-5

UBT

I exc

eptio

n”),

pre-

arra

nged

sale

Idea

l for

FLI

P-C

RU

T, d

iffic

ult f

or

CR

AT a

nd C

GAs

bec

ause

of

mar

keta

bilit

y

Rea

l esta

te re

pres

ents

near

ly 5

0% o

f priv

atel

y he

ld w

ealth

, esti

mat

ed a

t tw

ice

the

entir

e sto

ck

mar

ket.

Yet

onl

y 2%

of a

ll ch

arita

ble

gifts

are

re

al e

state

. C

lose

ly-H

eld

Stoc

k D

educ

tion:

FM

V

C-C

orp

or S

-Cor

p T

hin

to n

on-e

xiste

nt m

arke

t, di

fficu

lt va

luat

ion,

self-

deal

ing

with

out

inde

pend

ent a

ppra

isal,

pre-

arra

nged

sa

le, S

-Cor

p U

BTI i

ssue

s

Idea

l for

FLI

P-C

RU

T w

ith n

o kn

own

liqui

datio

n ev

ent –

oth

er v

ehic

les w

ork

for c

orpo

rate

rede

mpt

ion

or m

arke

t sa

le

Priv

ate

com

pany

con

trib

utio

ns a

re v

ery

popu

lar p

rior t

o a

mar

ket s

ale.

S-C

orp

gifts

to

a tr

ust a

re ta

x-ef

fect

ive

prio

r to

sale

or t

o a

corp

orat

ion

if he

ld.

LLC

Int

eres

ts

Ded

uctio

n: F

MV

Tax

stat

us m

ay b

e co

rpor

ate

or

part

ners

hip

Sam

e as

Clo

sely

-Hel

dan

d ch

arac

teris

tics o

f und

erly

ing

asse

ts an

d po

tent

ial c

apita

l cal

ls, m

ultip

le

shar

ehol

ders

/ass

ets d

iffic

ult

Sam

e as

Clo

sely

-Hel

d C

harit

ies u

sual

ly w

ant t

he L

LC in

tere

st fo

r lia

bilit

y pr

otec

tion.

Mul

tiple

shar

ehol

ders

m

ake

this

optio

n di

fficu

lt.

Part

ners

hips

D

educ

tion:

FM

V

Gen

eral

, Lim

ited

or O

pera

ting

May

be

diffi

cult

or e

xpen

sive

to

appr

aise

, cha

ract

erist

ics o

f und

erly

ing

asse

ts, g

ener

al p

artn

ersh

ips h

ave

full

liabi

lity,

par

tner

ship

s with

neg

ativ

e ba

sis

Lim

ited

part

ners

hips

are

par

ticul

arly

go

od fu

ndin

g as

sets

for L

ead

Tru

sts.

For L

LCs a

nd P

artn

ersh

ips,

appr

aisa

l di

scou

ntin

g m

ay a

pply

.

Life

Ins

uran

ce/

Ann

uiti

es

Ded

uctio

n: L

esser

of

Adj

uste

d C

ost

Basis

or F

MV

Paid

-Up

and

Non

-Pai

d U

p Li

fe

Insu

ranc

e –

Var

iabl

e or

Fix

ed

Def

erre

d An

nuiti

es

Non

-pai

d up

pol

icie

s, “S

tran

ger-

Ow

ned”

or p

rem

ium

fina

nced

, or g

ifts

with

pol

icy

loan

s are

mor

e di

fficu

lt.

Paid

-up

who

le li

fe p

olic

ies w

ork

wel

l. An

nuiti

es tr

igge

r gai

n up

on tr

ansfe

r.

Life

insu

ranc

e is

an e

xcel

lent

life

-tim

e or

testa

men

tary

gift

s (th

roug

h be

nefic

iary

des

igna

tion)

. An

nuiti

es a

re

only

attr

activ

e as

testa

men

tary

gift

s be

caus

e of

IRD

.

Life

insu

ranc

e ca

n be

an

exce

llent

wea

lth

repl

acem

ent t

ool f

or a

ny p

lann

ed o

r out

right

gi

ft. P

rem

ium

s can

be p

aid

with

app

reci

ated

pr

oper

ty.

Min

eral

Int

eres

ts

Ded

uctio

n: V

aries

Oil/

Gas

Wor

king

or N

on-

Wor

king

Inte

rests

, Tim

ber,

Oth

er M

iner

als

Val

uatio

n di

fficu

lt, ta

x la

w v

ery

com

plex

and

stat

e ru

les m

ay g

over

n (e

.g.,

timbe

r).

Ver

y di

fficu

lt bu

t pos

sible

.T

hese

ass

ets a

re ty

pica

lly h

eld

in p

artn

ersh

ips

or L

LCs s

o th

ose

rule

s app

ly a

s wel

l.

Res

tric

ted

Stoc

k D

educ

tion:

FM

V Se

ctio

n 14

4 or

145

Ap

prai

sal r

equi

rem

ent,

lock

-up

perio

dR

estr

icte

d sto

ck c

an e

asily

be

used

for

just

abou

t eve

ry p

lann

ed g

ift

Res

tric

ted

stock

shou

ld b

eco

ordi

nate

d w

ith a

n ex

perie

nced

bro

ker.

Stoc

k O

ptio

ns

Ded

uctio

n: V

aries

Q

ualif

ied

(ISO

s) o

r non

-qu

alifi

ed

“In-

the-

mon

ey”

optio

n tr

ansfe

rs tr

igge

r ga

in to

the

dono

r at o

rdin

ary

inco

me

rate

s at t

he ti

me

of g

ift.

ISO

s can

be

exce

llent

fund

ing

asse

ts pr

ovid

ed th

ey a

re e

xerc

ised

and

then

he

ld fo

r ove

r a y

ear.

Qua

lifie

d re

plac

emen

t sto

ck fr

om a

n em

ploy

er

retir

emen

t pla

n/ES

OP

can

wor

k w

ell f

or b

oth

outr

ight

and

pla

nned

gift

s. C

olle

ctib

les/

Art

D

educ

tion:

Bas

is fo

r non

-rela

ted

use/F

MV

for

rela

ted

use

Art,

coin

s, an

tique

s V

alua

tion,

insu

ranc

e, st

orag

e,

tran

sact

ion

costs

, com

plex

stru

ctur

es

like

priv

ate

oper

atin

g fo

unda

tions

are

so

met

imes

use

s

Tan

gibl

e pr

oper

ty w

ork

fairl

y w

ell f

or

near

ly a

ll fo

rms o

f pla

nned

gift

s – c

ost

basis

ded

uctio

n is

an is

sue

how

ever

. T

esta

men

tary

gift

s are

idea

l.

New

PPA

200

7 ru

les s

ever

ely

tight

en p

artia

l in

tere

st ar

t gift

s. C

apita

l gai

ns ta

xes r

emai

n at

28

% fe

dera

l so

ther

e is

an e

xtra

tax

bene

fit in

ta

ngib

le p

rope

rty d

onat

ions

.

Inte

llect

ual

Pro

pert

y D

educ

tion:

Var

ies

Pate

nts,

roya

lties

, cop

yrig

hts

Rev

enue

or n

on-r

even

ue

prod

ucin

g

Val

uatio

n co

st, d

ispos

ition

pro

cess

Wor

k be

st as

testa

men

tary

gift

s to

rece

ive

step-

up in

bas

is.

2004

Act r

educ

ed a

ttrac

tiven

ess o

f pa

tent

/roy

alty

gift

to b

asis.

Thi

s tab

le h

as g

ener

al in

form

atio

n an

d sh

ould

not

be

relie

d up

on a

s tax

, leg

al o

r fin

anci

al a

dvic

e.

Cop

yrig

ht ©

2007

Cha

ritab

le So

lutio

ns, L

LC a

nd B

ryan

Clo

ntz,

CFP

® bry

an@

char

itabl

esolu

tions

llc.co

m (

404)

375

-549

6

Gift

Acc

epta

nce/

Man

agem

ent/

Dis

posi

tion

Con

side

rati

ons

for

Top

Ten

Non

-Cas

h A

sset

Con

trib

utio

ns

Thi

s tab

le h

as g

ener

al in

form

atio

n an

d sh

ould

not

be r

elie

d up

on a

s tax

, leg

al o

r fin

anci

al a

dvic

e.

Cop

yrig

ht ©

Cha

ritab

le So

lutio

ns, L

LC a

nd B

ryan

Clo

ntz,

CFP

® bry

an@

char

itabl

esolu

tions

llc.co

m (

404)

375

-549

6

Asse

t Typ

e Li

abili

ty/C

ost E

xpos

ure

Risk

Man

agem

ent/

Due

Dili

genc

e Ac

cept

ance

Issu

esSt

aff R

ole

Disp

ositi

on

Alte

rnat

ives

R

eal E

stat

e

Envi

ronm

enta

l, U

BTI,

liens

, IR

S pe

nalti

es, a

ccid

ent

clai

ms,

up-fr

ont d

ue

dilig

ence

exp

ense

, on-

goin

g ho

ldin

g co

sts, r

emed

iatio

n or

im

prov

emen

t cos

t, tim

e-to

-re

war

d ra

tio, f

iduc

iary

risk

Inde

mni

ficat

ion

lette

r, en

viro

nmen

tal a

udit,

su

rvey

, BPO

or a

ppra

isal,

insu

ranc

e, si

te

insp

ectio

n w

ith p

ictu

res,

dete

rmin

e pr

oper

ty’s

histo

ry, d

evel

op sa

les p

lan

- rev

iew

all

deed

s, le

ase

agre

emen

ts, re

ntal

agr

eem

ents,

insp

ectio

n re

port

s, do

nor s

houl

d co

mpl

ete

disc

losu

re

chec

klist

citi

ng a

ny k

now

n iss

ues,

outso

urce

to

anot

her c

harit

y

Con

flict

s of i

nter

est,

valu

atio

n, se

lf-de

alin

g, im

plie

d or

ex

pres

sed

restr

ictio

ns

Tax

subs

tant

iatio

n –

8283

/828

2, d

ue

dilig

ence

, cha

nge

insu

ranc

e/ut

ilitie

s, ex

ecut

e tr

ansfe

r doc

umen

ts, d

onor

co

mm

unic

atio

n, a

udit

prep

arat

ion,

m

anag

e di

spos

ition

N

ote:

One

per

son

shou

ld m

anag

e al

l ill

iqui

d as

sets.

1. H

old

(not

usu

ally

re

com

men

ded)

2.

Sel

l to

priv

ate

buye

r (un

rela

ted

part

y)

3. L

ist w

ith b

roke

r

Priv

atel

y-H

eld

Stoc

k/LL

C/

Part

ners

hips

Cap

ital c

alls,

inde

mni

ficat

ion

clau

ses,

lack

of c

ontr

ol w

ith

min

ority

gift

s, U

BTI a

nd

spec

ific

issue

s rel

ated

to

unde

rlyin

g pr

oper

ty

Inde

mni

ficat

ion

lette

r, in

depe

nden

t app

raisa

l, re

view

fina

ncia

ls if

appr

opria

te, d

evel

op sa

les

plan

, rev

iew

all

entit

y do

cum

ents

Thi

n to

non

-exi

stent

m

arke

t, di

fficu

lt va

luat

ion,

self-

deal

ing

with

out

inde

pend

ent

appr

aisa

l, S-

Cor

p U

BTI i

ssue

s

Tax

subs

tant

iatio

n –

8283

/828

2, d

ue

dilig

ence

, exe

cute

tran

sfer

docu

men

ts, d

onor

com

mun

icat

ion,

au

dit p

repa

ratio

n, p

ut st

ock

cert

ifica

te o

r ass

ignm

ent d

ocum

ent

in sa

fe.

Che

ck in

with

com

pany

an

nual

ly to

see i

f the

re h

as b

een

any

mat

eria

l cha

nge.

1. S

old

back

to

entit

y 2.

Sol

d in

ope

n m

arke

t tra

nsac

tion

3. S

old

to p

rivat

e un

rela

ted

buye

r

Life

Ins

uran

ce/

Ann

uiti

es

Virt

ually

non

e exc

ept a

s it

rela

tes t

o co

mpl

ex

foun

datio

n-ow

ned,

cha

rity-

owne

d an

d in

vesto

r ow

ned

cont

ract

s – so

split

inte

rest

gifts

are

allo

wed

.

IRS

has l

isted

a n

umbe

r of r

epor

tabl

e tr

ansa

ctio

ns –

be

caut

ious

to c

ompl

y w

ith

repo

rtin

g re

quire

men

ts. A

lso re

view

the

illus

trat

ion

or p

olic

y be

ing

cons

ider

ed a

nd h

ave

a m

emo

outli

ning

the

dono

r’s p

rem

ium

pay

ing

resp

onsib

ilitie

s and

the

char

ity’s

optio

ns fo

r no

n-co

mpl

ianc

e.

Wor

k w

ith a

gent

to

illus

trat

e an

y no

n-pa

id u

p (u

nive

rsal

or

varia

ble

life

polic

ies)

at

2%

und

er th

e cu

rren

t cre

ditin

g ra

te.

Tax

subs

tant

iatio

n –

8283

/828

2, d

ue

dilig

ence

, exe

cute

tran

sfer

docu

men

ts, d

onor

com

mun

icat

ion,

au

dit p

repa

ratio

n, m

anag

e po

licie

s an

nual

ly to

det

erm

ine

heal

th.

Put d

onor

in c

onta

ct w

ith a

qua

lifie

d in

sura

nce

appr

aise

r.

1. U

sual

ly h

eld

to

deat

h 2.

Cas

h su

rren

der t

o co

mpa

ny

3. R

educ

e pa

id-u

p 4.

Sol

d to

life

se

ttlem

ent

com

pani

es

Min

eral

Int

eres

ts/

Inte

llect

ual

Pro

pert

y

Non

e ot

her t

han

pote

ntia

l ca

pita

l cal

ls M

ore

than

any

oth

er a

sset

, hav

ing

a w

ell-

desig

ned

sale

s pla

n pr

ior t

o ac

cept

ance

is c

ritic

al

Mar

keta

bilit

y,

appr

aisa

ls T

ax su

bsta

ntia

tion

–82

83/8

282,

due

di

ligen

ce, e

xecu

te tr

ansfe

r do

cum

ents,

don

or c

omm

unic

atio

n,

audi

t pre

para

tion

1. H

old

(not

re

com

men

ded

unle

ss

stron

g in

com

e pa

ymen

ts)

2. S

old

via

brok

er

3. S

old

priv

atel

y R

estr

icte

d St

ock/

Stoc

k O

ptio

ns

Post-

cont

ribut

ion

loss

po

ssib

ilitie

s dur

ing

restr

icte

d or

hol

ding

per

iod

Rev

iew

all

restr

ictio

ns a

nd o

ptio

n ag

reem

ents

Non

e T

ax su

bsta

ntia

tion

–82

83/8

282,

due

di

ligen

ce, e

xecu

te tr

ansfe

r do

cum

ents,

don

or c

omm

unic

atio

n,

audi

t pre

para

tion

Sold

with

bro

ker a

s so

on a

s res

tric

tion

is lif

ted

Col

lect

ible

s/A

rt

Non

e ot

her t

han

post-

cont

ribut

ion

hold

ing

expe

nses

Rev

iew

hist

ory

of c

olle

ctio

n, d

ocum

ent w

ith

pict

ures

W

ork

with

bro

ker

/app

raise

r to

asse

ss

valu

e pr

ior t

o ac

cept

ance

Tax

subs

tant

iatio

n–

8283

/828

2, d

ue

dilig

ence

, exe

cute

tran

sfer

docu

men

ts, d

onor

com

mun

icat

ion,

au

dit p

repa

ratio

n, in

sura

nce,

stor

age

1. A

uctio

n sa

le

2. P

rivat

e bu

yer

3. B

roke

r

A

ddit

iona

l Rea

ding

s fo

r N

on-C

ash

Ass

ets

Rea

l Est

ate

1.

Pl

anne

d G

ivin

g D

esig

n C

ente

r – T

echn

ical

Rep

ort o

n R

eal P

rope

rty

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=6

0165

) 2.

G

ifts o

f Rea

l Esta

te –

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=2

3747

) 3.

G

old

in th

e gr

ound

: A P

ract

ical

Gui

de to

Dev

elop

ing

and

Acce

ptin

g G

ifts o

f Rea

l Esta

te, M

yerb

erg,

Nea

l - Jo

urna

l of G

ift P

lann

ing,

Vol

ume

10, N

umbe

r 2,

June

200

6 , p

p. 1

1-43

(33)

4.

R

eal E

state

Gift

s--B

eyon

d th

e Ba

sics,

Car

ovan

o, J.

; Nas

h, A

nne

Jour

nal o

f Gift

Pla

nnin

g, V

olum

e 7,

Num

ber 3

, 1 S

epte

mbe

r 200

3 , p

p. 5

-41(

37)

5.

Con

trib

utin

g M

ortg

aged

Pro

pert

y to

Cha

rity,

Pee

bles

, Lau

ra –

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=2

7287

) C

lose

ly-h

eld

Stoc

k/LL

C/P

artn

ersh

ips

1.

Pl

anne

d G

ivin

g D

esig

n C

ente

r – T

echn

ical

Rep

ort o

n Pr

ivat

ely-

Hel

d In

tere

sts (h

ttp://

ww

w.p

gdc.

com

/usa

/item

/?ite

mID

=604

31)

2.

Gift

Par

tner

ing

with

Ent

repr

eneu

rial D

onor

s, T

icco

ni, P

eter

Jour

nal o

f Gift

Pla

nnin

g, V

olum

e 4,

Num

ber 3

, 1 S

epte

mbe

r 200

0 , p

p. 1

1-33

(23)

3.

C

harit

able

Gift

s of S

ubch

apte

r S S

tock

: H

ow to

Sol

ve th

e Pr

actic

al L

egal

Pro

blem

s, H

oyt,

Chr

is (h

ttp://

ww

w.p

gdc.

com

/usa

/item

/?ite

mID

=247

92)

4.

Tax

Sav

ing

Opp

ortu

nitie

s for

Cha

ritie

s Ow

ning

Sub

chap

ter S

Sto

ck, P

eebl

es, L

aura

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=2

5732

) 5.

Is

sues

to C

onsid

er W

hen

Mak

ing

and

Acce

ptin

g G

ifts o

f Res

tric

ted

Stoc

k, F

rank

lin, J

and

She

vlin

, D (h

ttp://

ww

w.p

gdc.

com

/usa

/item

/?ite

mID

=281

16)

Life

Ins

uran

ce/S

tock

Opt

ions

/Col

lect

ible

s/In

telle

ctua

l Pro

pert

y

1

. L

ife In

sura

nce:

The

Goo

d, T

he B

ad a

nd th

e U

gly,

Mac

Nab

, JJ J

ourn

al o

f Gift

Pla

nnin

g, V

olum

e 5,

Num

ber 1

, 1 M

arch

200

1 , p

p. 1

7-44

(28)

2.

C

harit

able

Gift

s of L

ife In

sura

nce,

Clo

ntz,

B an

d Br

ink,

M. (

http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=2

7962

) 3.

N

avig

atin

g St

ock

Opt

ions

and

Oth

er S

tock

Rig

hts,

Ott,

D. a

nd L

ew, R

. (ht

tp://

ww

w.p

gdc.

com

/usa

/item

/?ite

mID

=272

35)

4.

Plan

ned

Giv

ing

Des

ign

Cen

ter –

Tec

hnic

al R

epor

t on

Inta

ngib

le P

rope

rty

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=6

0379

) 5.

Pl

anne

d G

ivin

g D

esig

n C

ente

r – T

echn

ical

Rep

ort o

n T

angi

ble

Prop

erty

(http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=6

0229

) G

ift A

ccep

tanc

e/M

anag

emen

t/D

ispo

siti

on

1.

U

nder

stand

ing

and

Dra

fting

Non

-Pro

fit G

ift A

ccep

tanc

e Po

licie

s, M

iree,

Kat

hryn

(http

://w

ww

.pgd

c.co

m/u

sa/it

em?it

emID

=266

63)

2.

The

Haz

ards

of U

nman

aged

Life

Insu

ranc

e Po

licie

s, Ba

rney

, A. (

http

://w

ww

.pgd

c.co

m/u

sa/it

em/?

item

ID=2

7755

)