Embed Size (px)

Citation preview

THE IMPACT OF EXTERNAL AUDIT IN ACCOUNTABILITY AND

TRANSPARENCY OF NGOS IN THE BOLGATANGA MUNICIPALITY

By

Ali Baba Solomon (BSc. Accounting and Computing)

© 2015 Department of Accounting and Finance

A thesis submitted to Department of Accounting and Finance

Kwame Nkrumah University of Science and Technology School of Business

in partial fulfilment of the requirements

for the degree of

MASTER OF BUSINESS ADMINISTRATION (ACCOUNTING-OPTION)

School of Business, KNUST

College of Humanities and Social sciences

August, 2015

i

DECLARATION

I hereby declare that this submission is my own work towards the award of Masters

in Business Administration that, to the best of my knowledge, it contains no material

previously published by another person nor material which has been accepted for the

award of any other degree of any University or Professional Institution, except where

due acknowledgement has been made in the text.

Ali Baba Solomon ………………………. …………………

PG 9599613 Signature Date

Student Name

Certified by:

Mr. Richard Owusu Afriyie, …………………….. ………………..

Supervisor Name Signature Date

Certified by:

Dr. K. O. Appiah …………………….. ………………..

Head of Department Signature Date

ii

ABSTRACT

This study is to assess the impact of external audit in accountability and transparency

of NGOs in the Bolgatanga Municipality Both qualitative and quantitative approach

were used that included questionnaires, interviews, focus group discussions to collect

data. Purposive sampling technique was used in the selection of respondents. A

sample size of sixty four (108) respondent were selected from NGOs, stakeholders

and beneficiaries across board and SPSS was used in the analysis of the data. From

the findings, it is observed that the external audit report of NGOs are not utilised to

bring about compliance and that recommendations of the external auditors are not

enforced by management. This invariably calls for a case by case research on NGO

activities. It was established that external audit report does not have positive effect

on NGOs activities in relation to accountability and transparency. Project end

evaluation should not be only narrative as has been the case in most evaluations but

should include audited financial statement to be signed by the external auditor.

External Auditors should not be hired by management of NGOs but by the Board of

Directors or Donors so the external auditors will report to the Board or the donor or

funding agency and not management of NGOs. Beneficiary communities and

stakeholders should be educated to demand full disclosure of the entire package of

support or intervention such that they can hold NGOs implementing the projects

within their community accountable if they refused to render the agreed support

package.

iii

DEDICATION

I sincerely dedicate this work to the following:

My wife: Bernice Akolgo

Children: Racheal Kakpegre, Laura Kakpegre, and Lucretus Kakpegre

Who have given me the support, encouragement and permitted my long absence

from home most of the time to enable me complete this piece of work.

iv

ACKNOWLEDGEMENT

My first appreciation goes to the Lord Almighty for given me the wisdom, courage,

strength and ability to bring this work to a final stage

I am also grateful to Mr. Richard Owusu - Afriyie, my Supervisor who saw me

through the proposal writing. His useful comments and criticisms made me stay on

course through my presentation to the data collection stage.

I wish to acknowledge other researches, without their work this research would not

have come into completion, much was borrowed from them. Also this research

would not have come to a successful completion without the help of a number of

people.

My deepest appreciation and thanks particularly goes to Stephen G. Tobazaa (CA,

CFA) of Bolgatanga Polytechnic for his constructive suggestions, criticisms and

useful comments. Without his dedication, the work would not have become a reality.

v

TABLE OF CONTENTS

DECLARATION ......................................................................................................... i

ABSTRACT ................................................................................................................ ii

DEDICATION ........................................................................................................... iii

ACKNOWLEDGEMENT ........................................................................................ iv

TABLE OF CONTENTS .......................................................................................... v

LIST OF TABLES .................................................................................................. viii

ABBREVIATIONS AND ACRONYMS ................................................................. ix

CHAPTER ONE ........................................................................................................ 1

INTRODUCTION ...................................................................................................... 1

1.1 Background to the Study ........................................................................................ 1

1.2 Statement of the Problem ....................................................................................... 1

1.3 RESEARCH OBJECTIVE .................................................................................... 3

1.3.1General objective ................................................................................................. 5

1.3.2 Specific objectives .............................................................................................. 5

1.4 RESEARCH QUESTIONS ................................................................................... 6

1.6 SIGNIFICANCE OF THE STUDY ....................................................................... 6

1.7 SCOPE OF THE STUDY ...................................................................................... 7

1.8: LIMITATIONS OF THE STUDY ....................................................................... 7

1.9 ORGANISATION OF THE STUDY .................................................................... 8

CHAPTER TWO ....................................................................................................... 9

LITERATURE REVIEW ......................................................................................... 9

2.0 Introduction ............................................................................................................ 9

2.1 The context of NGO accountability and transparency ........................................... 9

2.2 Upward and downward accountability .................................................................. 9

2.3 Hierarchical and holistic accountability ............................................................... 13

2.5 Concept of Auditing ............................................................................................. 15

2.6 Independent Auditing Standards .......................................................................... 15

2.8 Working with External Auditors ...................................................................... 19

2.9 The External Auditing Process ......................................................................... 20

2.10 Audit planning .................................................................................................. 20

vi

2.11 Responsibilities of management and auditors for fraud and error ..................... 21

2.1.1.1 Responsibilities of management .................................................................... 21

2.11.2 Responsibilities of the auditor......................................................................... 21

2.12 Detecting Fraud .................................................................................................. 22

2.14 The Audit Report ............................................................................................... 24

2.15 Internal Audit ..................................................................................................... 26

2.16 Difference between Internal Audit and External Audit ..................................... 27

2.17 Control Procedures ............................................................................................. 28

2.19 Audit Committees .............................................................................................. 30

2.19.1 Characteristics of Audit Committees .............................................................. 31

2.19.2 Effectiveness ................................................................................................... 32

2.19.3 Role of Audit Committee ................................................................................ 32

CHAPTER THREE ................................................................................................. 36

RESEARCH METHODOLOGY ........................................................................... 36

3.0 Introduction .......................................................................................................... 36

3.1 Study Design ........................................................................................................ 36

3.3 Study Population .................................................................................................. 37

3.4 Sampling Techniques .......................................................................................... 37

3.4.1 Sample Size ....................................................................................................... 37

3.5. Sources of Data ................................................................................................... 38

3.6. Data Collection Procedure .................................................................................. 38

3.7. Data Analysis ...................................................................................................... 39

3.8. Ethical consideration ........................................................................................... 39

3.9 LIMITATIONS TO THE STUDY ...................................................................... 39

3.10 The Study Area .................................................................................................. 40

CHAPTER FOUR .................................................................................................... 43

PRESENTATION, ANALYSIS AND INTERPRETATION OF DATA ............ 43

4.1 Introduction .......................................................................................................... 43

CHAPTER FIVE ..................................................................................................... 55

SUMMARY OF FINDING, CONCLUSIONS AND RECOMMENDATIONS 55

5.0 Introduction .......................................................................................................... 55

vii

5.1 Summary of findings ............................................................................................ 55

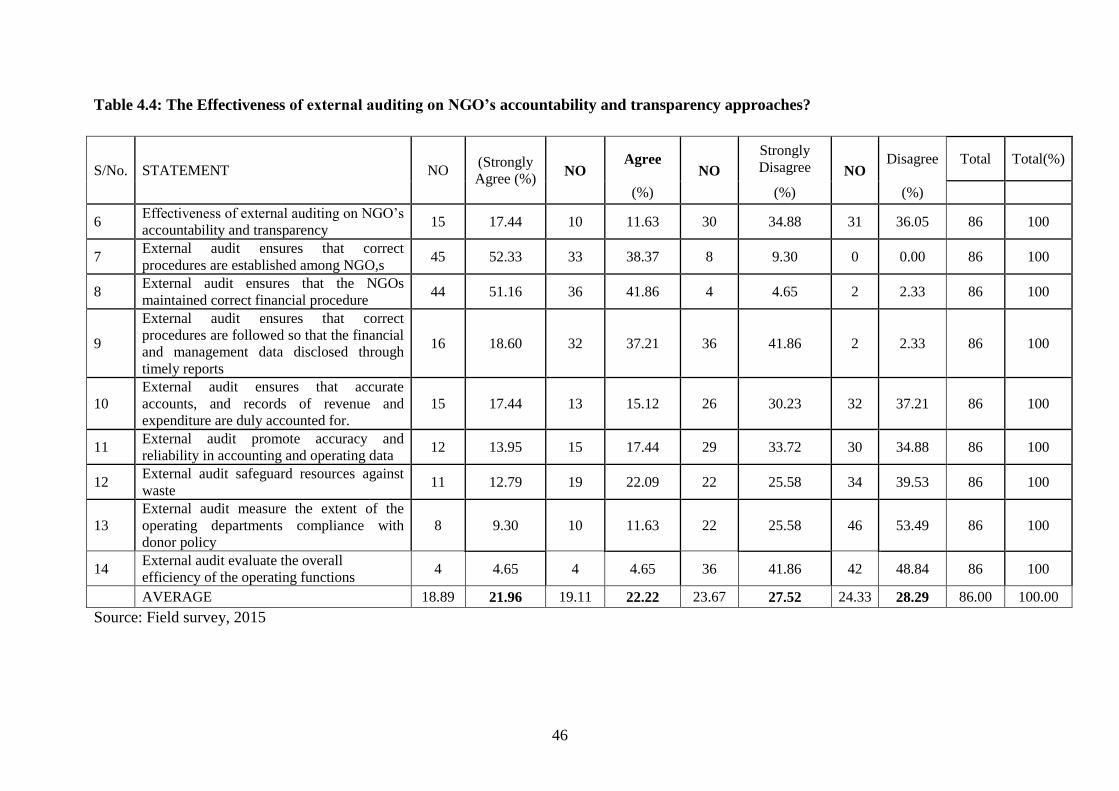

5.1.1 Assess how effective external audit is on NGO‘s in accountability and

transparency. ..................................................................................................... 55

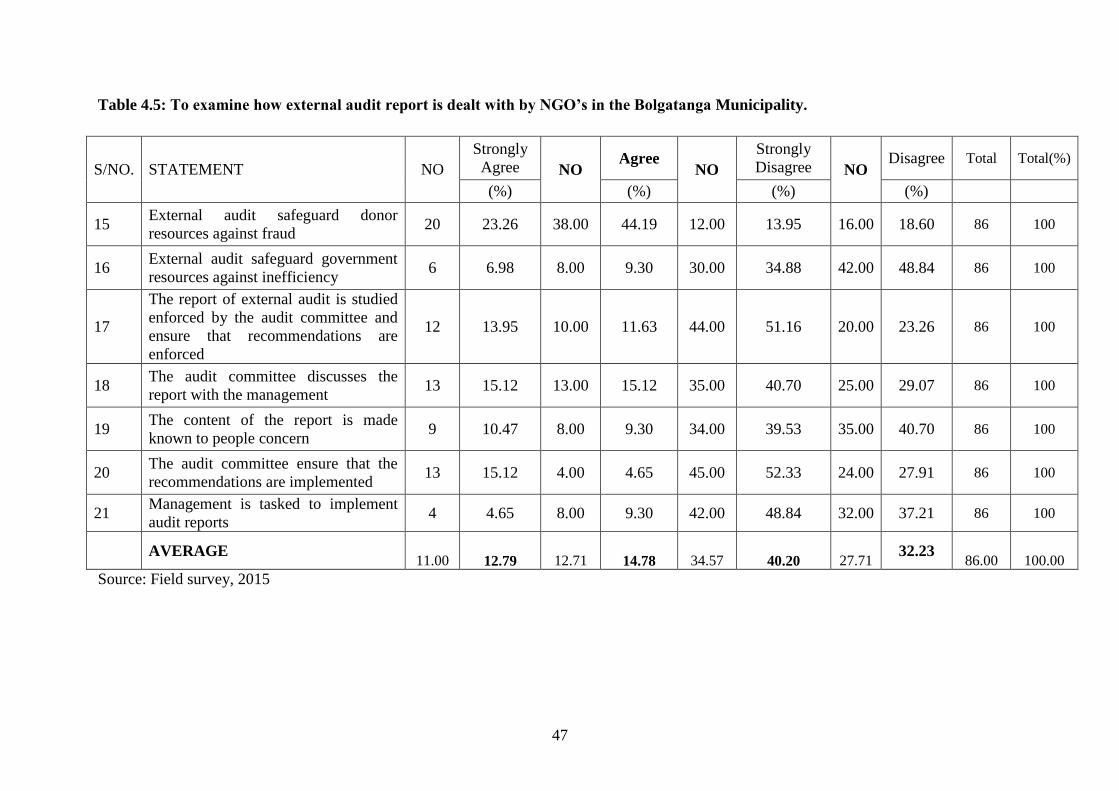

5.1.2 To examine how external audit report is dealt with by NGOs in the Bolgatanga

Municipality. ..................................................................................................... 56

5.1.3 Challenges that NGOs face in ensuring transparency and accountability. ....... 56

5.2 Conclusion ........................................................................................................... 56

5.3 Recommendations ................................................................................................ 57

REFERENCES ......................................................................................................... 59

APPENDICES .......................................................................................................... 62

Appendix 1: QUESTIONAIRE TO STAFF AND BENEFICIARY ......................... 62

viii

LIST OF TABLES

TABLE PAGE

Table 2.1 Comparison Chart ...................................................................................... 28

Table 4.1: Selection of the Sample Size .................................................................... 43

Table4.2 Distribution of Respondents by Gender ...................................................... 44

Table 4.3: Distribution of Respondents According to Age:....................................... 44

Table 4.4: The Effectiveness of external auditing on NGO‘s accountability and

transparency approaches? .......................................................................... 46

Table 4.5: To examine how external audit report is dealt with by NGO‘s in the

Bolgatanga Municipality. .......................................................................... 47

Table 4.6 Challenges that NGOs face in ensuring accountability and transparency . 51

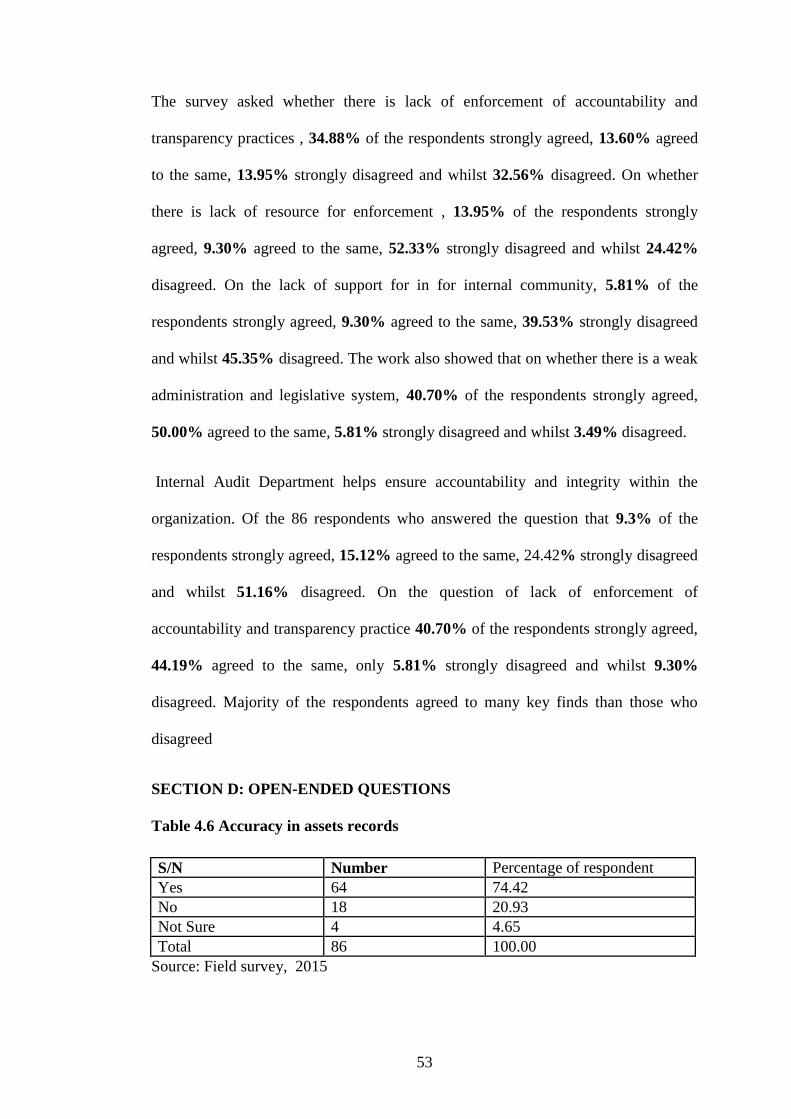

Table 4.6 Accuracy in assets records ......................................................................... 53

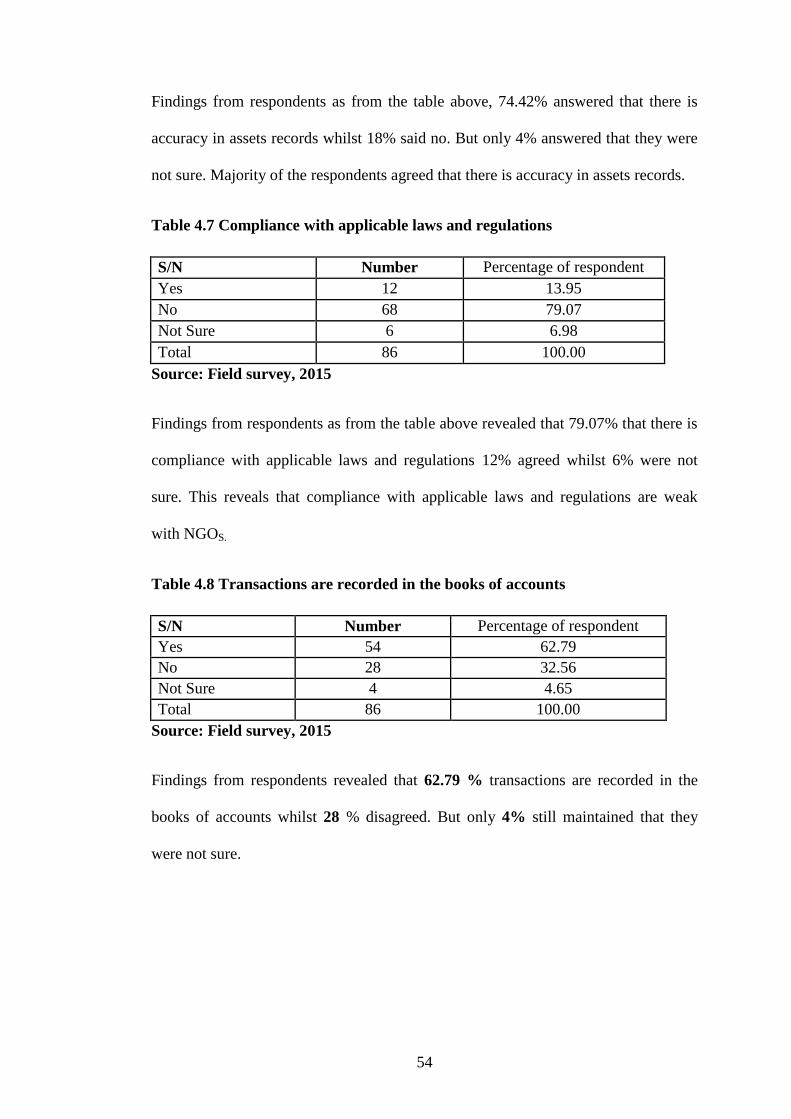

Table 4.7 Compliance with applicable laws and regulations ..................................... 54

Table 4.8 Transactions are recorded in the books of accounts .................................. 54

ix

ABBREVIATIONS AND ACRONYMS

IAU Internal Audit Unit

GoG Government of Ghana

IIA Institute of Internal Auditors

FAA Financial Administration Act

FAR Financial Administration Regulation

L.I Legislative Instrument

COSO Committee of Sponsoring Organization

ARIC Audit Report Implementation Committee

FMP Financial Management Practices

APR Annual Performance Report

BNI Bureau of National Investigations

IAA Internal Audit Agency

IIA Institute of Internal Auditors

MDAs Ministries Departments And Agencies

GOG Government of Ghana

PFM Public Financial Management

CEO Chief Executive Officer

SA Statutory audit

PV Private audit

IA Interim audit

MA Management audit

CA Continues audit

EA External audit

FRA Financial and Regularity audit

x

EA Effectiveness audit

VMA Value for money audit

BMA Bolgatanga Municipal Assembly

SSPS Statistical Package for Social Science

UER Upper East Region

IAS International Accounting Standards

ISA International, Standard in Auditing

1

CHAPTER ONE

INTRODUCTION

1.1 Background to the Study

Issues of transparency, honesty and accountability have in recent years been regarded

as significant in matter relating to businesses of NGOs business. According to the

Nepal News (2001), "only a few of these NGOs appear to be transparent and

accountable in their activities‖. The Director General of the World Trade

Organisation (WTO), Mike Moore in 2001 instituted a code of conduct which would

be ensure and require that NGOs are transparent and accountable in their activities.

Such demands mostly mandate NGOs to deliver what they demand of others:

transparency, honesty, and accountability.

Transparency is regarded as an essential part of accountability. Therefore, ―effective

accountability requires a statement of goals, transparent decision-making and

relationships, and honest reporting of resource use and achievements, which can

emphasize the honesty and efficiency with which resources are used or the impact

and effectiveness of the work‖ (Ramesh, 1996: 8). External auditors are mandated by

law to evaluate and publicly issue an opinion on the transparency and accountability

on NGOs activities. Its purpose, in part, is to ensure that the financial status and

operating performance of NGOs are fairly presented and disclosed."

2

Internal and external stakeholders need access to timely and adequate information

about the activities of NGOs since it plays significant roles to them performing

effectively. NGOs must thus not only be honest, but they ought to be regarded as

such. This is because, government bodies can politically isolate them, which would

render them incapable of going about their voluntary activities. The development of

NGOs has come up with issues not lonely relating to their task to perform but also on

accountability. There have been rise in the attentions for transparency and

accountability as a result of the increase and continual funding of projects by NGOs.

However the extent of NGOs balancing their effectiveness in performance and

accountability relies on the doing away with ambiguities of the concept of

accountability. Accountability, which basically refers to 'answerability', is a well

known concept to the Non-governmental sector. The extent to which one is

accountable is the standard requirement or expectation of the one whom the report is

given.

Rajesh Tandon, examines accountability in the context of stakeholder obligations,

including beneficiaries, donors, regulators and staff as well as other NGOs and

regard them as part of the system to ensure accountability. Rajesh further asserts that

since their stake is in relation to their performance and not in its governance, their

assessment of governance requires that NGOs perform effectively, thereby ensuring

accountability to stakeholders. This implies that if NGOs are to have the continued

3

access to the flow of funds from donors, then their ―desirable processes and

outcomes‖, and ―interest and concerns must be matched‖ by performance. To

buttress these views, Tandon further explains that accountability to donors should be

more related to output indicators than it is being practice now.

1.2 Statement of the Problem

Governments and intergovernmental agencies have recognised the need for

maximising the effectiveness with which NGOs are operating in the beneficiary

communities. Thus, making external audit an integral part of transparency and

accountability towards achieving the desired goals.

Much aid funding is channeled through the medium of non-governmental

organizations (NGOs), which are responsible for how effective the funding is

translated into aid delivery. At both the project (NGO) level and country

(governmental) level, accounting and accountability mechanisms have the potential

to increase or decrease the effectiveness with which development funding is

deployed.

Furthermore, there is a general lack of independent research into the impact and

perceptions of, beneficiaries of those attempts that some NGOs have made over the

years to expand their accountability and transparency drive. Those studies that have

addressed this issue have tended to be narrowly focused on particular NGOs, and

have therefore not been able to provide broader insights into issues at the

4

fundamental level associated with the development and implementation of new

forms of accountability and transparency mechanisms towards meeting beneficiary

needs among others.

It is argued that auditing as examination or review of various activities of the NGOs,

aims at ensuring internal controls, accountability and transparency. Such

organisations include both the government and non-governmental agencies.

In addition, few concerns have also been raised that most NGOs divert or misapply

funds allocated to them (Gaventa and McGee, 2008). Several attributes have been

given to the lack of external auditing in these organisations.

The global growth of NGOs has been a specific locus of discussions and initiatives to

achieve accountability that ensure effective and efficient performance of their

activities. Charitable codes of conduct, certification initiatives and other

accountability mechanisms have thrived in the sector in recent years, and

organisations have been established to support and promote accountability

improvement (Jordan, 2005; Lloyd, Oatham, & Hammer, 2007; Omelicheva, 2004).

A Survey conducted by Transparency International on How Corrupt NGOs in

Developing Nations are, by RICK Chohen, July 16th

, 2013, emphasis that NGOs in

Developing Nations are corrupt. September 26th

,2003 GNA Mr. Joseph Oji United

Nations Volunteer Program Officer in Ghana, on Friday has criticised Youth related

5

Non – Governmental Organisations (NGOs) in Africa that misapply donor funding

projects by hiking overheads cost.

Although NGOs are audited by external auditors, the public perceptions and the

publications kept pointing figures at NGOs misapplying donor funds.

In respect of these, the researcher intends to assess the impact of external audit on

NGO‘s activities in relation to accountability and transparency in Ghana by focusing

on NGOs in the Bolgatanga municipality.

1.3 RESEARCH OBJECTIVE

1.3.1General objective

The general objective of the study is to assess the impact of external audit in

Accountability and Transparency in the Bolgatanga Municipality

1.3.2 Specific objectives

In order to achieve this objective the following specific objectives are designed in

that direction.

1. To assess how effective external audit is on NGO‘s accountability and

transparency

2. To examine how external audit report is dealt with by NGO‘s in the

Bolgatanga Municipality.

3. To ascertain the challenges that NGOs face in ensuring accountability

and transparency.

6

1.4 RESEARCH QUESTIONS

The following are the research questions designed to achieve this objective;

1. •How effective is external auditing on NGO‘s accountability and

transparency approaches?

2. •How has external audit report on NGOs impacted on their performance in

the Bolgatanga Municipality?

3. •What challenges do NGOs face in ensuring accountability and transparency?

1.6 SIGNIFICANCE OF THE STUDY

It is known that every study play a major role in one way or the other. The findings

of the study are anticipated to be significant because of the primary role external

audit play in promoting the principles of good governance through accountability and

transparency.

The result of the study would identify the internal control practices that ensure

effective accountability and transparency in the NGOs, effectiveness of external

auditing on NGO‘s accountability and transparency and examine how external audit

report is dealt with by NGOs as well as ascertain the major challenges that hinder the

accomplishment of external audit by the NGOs.

These findings would help the researcher to make prudent recommendations to the

various NGOs and the beneficiaries to ensure efficient accountability. In addition, the

outcome of the study would enable NGOs to implement external audit report so as to

ensure effectiveness of external auditing on NGO‘s accountability and transparency.

It is again expected that after ascertaining those major challenges that hinder the

accomplishment of external audit by the NGOs would help the NGOs to apply best

strategies to that effect. The report will also be a source of reference for other

7

researchers on should more about the impact of external audit instead of only

transparency and accountability

1.7 SCOPE OF THE STUDY

The study would be conducted in the Bolgatanga Municipality in the Upper East.

The content scope covered the impact of external audit of NGO‘s in the light of

accountability and transparency in Ghana by focusing on NGOs. The study will

concentrate on the management staff of the NGOs, Audit firms and beneficiary

communities and individuals.

1.8: LIMITATIONS OF THE STUDY

The study is to be limited to the impact of external audit on NGO‘s activities in

relation to accountability and transparency in Ghana by focusing on NGOs in the

Bolgatanga Municipality.

Time: The time of the research is very short and this makes it very difficult if not

impossible for the researcher to design a great number of items of questionnaires to

be administered for the research work.

Cost: The cost of producing this study is substantial considering the fact that one has

to type the manuscript, produce photocopies and commute frequently within twenty

(20) commies in the Bolgatanga Municipality for the information the NGOs.

Co-operation: This research needs a lot of information from both management staff

of the NGOs and some beneficiaries. However, some farmer groups and individuals

were skeptical in providing information with the excuse that they have responded to

a lot of such questions in the past but have not seen any benefit. Never the less,

response to the required information was gathered upon further persuasion.

8

1.9 ORGANISATION OF THE STUDY

This study will be organized in five chapters as follows. Chapter One gives an

overview of the study including the background to the study, objectives of the study,

and significance of the study. The second chapter entails the review relevant

literature on the subject matter. Chapter Three provides an insight into the procedures

the researcher would use in carrying out the study. This includes the description of

the study type and design, population, sample and sampling technique to be used,

data collection methods and analysis among others. Chapter Four focuses on the

analysis of the results of the findings. This will consist of tables and charts to give

more meaning to the data that would be collected from the field. Chapter Five will

provide summary of the study findings and draw the final conclusions and

recommendations to ensure that possible improvement of accountability and

transparency in NGO operations in the Bolgatanga and Ghana as whole.

9

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

The chapter entails the review of literature which relates to the topic the impact of

External audit of NGO‘s in the light of accountability and transparency in Ghana by

focusing on NGOs in the Bolgatanga Municipality. Varied scholarly works and

research would be selected and relevant areas would be appraised, assessed and

evaluated. The chapter further gives relevant information about the aspects of earlier

works relating to the study.

2.1 The context of NGO accountability and transparency

NGO accountability and transparency issues are concepts that are regarded complex.

This is basically due to the ambiguous nature in which NGOs are known to operate.

According to Jordan and van Tuijl (2006) and O‘Dwyer (2007), intermediary

organisations essentially collaborate with multiple stakeholders who have diverse

demands. NGOs from developed nations and governments are further known to

provide funds and other resources as well as locally-based service delivery. There

exits numerous International NGOs (INGOs) from developed nations who also

mobilize resources (funds) and channel them to developing economies via local-

based operations. There are thus NGOs at the local level and local operations of

INGOs who serve as intermediary between international donors and the beneficiary

local communities.

Several research works have revealed that NGOs play important role when it comes

to health care delivery, education and other numerous welfare services in developing

countries. Such works include Dixon et al. (2006); Ebrahim (2003a); Edwards and

10

Fowler (2002); Goddard and Assad (2006); Gray et al. (2006); O‘Dwyer and

Unerman (2007); Porter (2003); and Unerman and O‘Dwyer (2006a).

The concept of transparency is mostly deemed a significant characteristic of good

governance. It is also regarded an important requirement for promoting

accountability among states and citizens. Transparent government primarily shows

At its most basic, transparent governance according to Suk et al (2005:649) signifies

― the openness of government systems to citizens and the public through clear-cut

and well defined procedures, loose access to information, that in the end promotes

and leads to accountability in the duties of organizations and individuals managing

the resources or been in public office‖. Furthermore, transparency is ―regarded a

significant feature of government systems, organisations, companies and individuals

having access to open information on plans, rules, actions and procedures‖ as

indicated by the Transparency International (2009: 44).

Goetz and Jenkins (2005) further assert that accountability realistically takes into

consideration both ―answerability‖, which is the mandate of duty-bearers to make

available the required information and justification about their actions; and

―enforceability‖ which is the possibility of penalties or consequences for failing to

answer accountability claims.

According to Nelson and Dorsey (2003:2014), development practices of INGOs have

been revealed that concentrate much on development as a need and a gift. There are

however other recent revelations that indicates development to be more as a right,

which has the aim of ensuring assistance that involves the duty to aid in the

achievement of the entitlements of individuals. This step (rights-based) has resulted

to the INGOs playing the key role in educating those affected by the projects and

11

activities of these INGOs. The educational actions are geared towards inculcating

higher levels of understanding or knowledge specifically on the rights of the

individual. Lastly Nelson and Dorsey (2003) indicate that the design of projects of

INGOs have happened in a more participatory manner, which have recognized the

needs to respect or consider the rights of the people who are affected by such

projects.

2.2 Concepts of Upward and downward accountability

A normal requirement attached to the funding provided to these NGOs is that the

locally based NGO has to account to the donor government or INGO for the manner

in which their funds have been used. Although this requirement can help to ensure

that funding is not being misappropriated or spent on undesignated projects, it has

also been shown to have problematic consequences. For example, there is some

evidence that the accountability mechanisms employed (or required) by INGOs to

address this need for so-called upward accountability to donors can prove

counterproductive by damaging the effectiveness of service delivery to the NGOs‘

beneficiaries (Dixon et al. 2006; Goddard and Assad 2006). To ensure that the

funding provided by donor governments and NGOs gives the greatest benefit to its

intended beneficiaries, it is clearly important for governments and other donors to be

aware of the potentially damaging and counterproductive impact of some of the

upward-accountability mechanisms they may be insisting that NGOs implement.

However, how information accessibility affects accountability and improves the

quality of governance is still poorly understood (Bellver and Kaufmann 2005).

Recent innovations in citizens‘ legal right to information and participatory budgeting

and community development processes have tested the extent to which ‗transparency

on decisions hand in hand with transparency on consequences‘ (Prat 2005: 869).

12

More judiciously stated, the relationship of transparency to accountability is as a

necessary but insufficient condition. Relatedly, while some take the ‘accountancy‘

approach of treating accountability as a set of rules and procedures which can be

monitored and audited (Newell & Wheeler 2006) , others see it as a set of

relationships, which necessarily involve power and contestation. Fox, for instance,

discusses ‗the arena of conflict over whether and how those in power are held

publicly responsible for their actions‘ (2007a: 12). This arena, which he terms

‗accountability politics‘, cannot be reduced to a set of institutional mechanism or a

checklist of procedures. It is mediated by formal institutions but not determined by

them; an arena of contestation, not a tool for efficiency and effectiveness.

Goetz and Jenkins (2001) expand on horizontal and vertical notions of

accountability, identifying new ‗hybrid‘ forms they call ‗diagonal‘ accountability

relationships. Goetz and Jenkins (2005) also stress the important distinction between

de jure and de facto accountability. This review‘s focus on effectiveness and impact

points us towards de facto accountability – what occurs in practice, as opposed to

what is set out in law or intent.

Many NGOs and some donors now recognize that, in addition to ensuring that

upward-accountability mechanisms are not counterproductive, they can enhance the

effectiveness of NGO service delivery by ensuring that local NGOs, and the local

operations of INGOs, are downwardly accountable to their beneficiaries (O‘Dwyer

and Unerman 2007). This downward accountability should be designed and

implemented in such a way as to help the NGO identify the needs of its intended

beneficiaries and assess how well it is addressing these needs (Ebrahim 2003a).

13

2.3 Hierarchical and holistic accountability

The concepts used in this research to frame and analyse the evidence about how

different NGO accounting and accountability methods influence the effectiveness of

aid delivery, draw on these ideas of upward and downward accountability. Upward

accountability to donors is regarded as a form of hierarchical accountability (Fowler

1996; Najam 1996; Dillon 2004; Kilby 2004; O‘Dwyer and Unerman 2007;

O‘Dwyer and Unerman 2008), characterised by fairly rigid accounting and

accountability procedures. This form of accounting typically provides donors with a

written (usually quantified) account comprising information in a form they have

requested to help ensure that the funds they have donated have been used for the

purposes they have specified. This is usually in the form of a one-way flow of

information from the NGO to the donor, with the focus being on the efficiency with

which the donors‘ funds have been spent (in terms of spending the funds on the

particular projects as specified by the donors) (Edwards and Hulme 1996a, 1996b;

Fowler 1996; Dillon 2004).

The one-way flow of information in hierarchical accountability often does not,

however, provide either the NGO or the donor with information about how

effectively the funding has been, or can be, used to provide the maximum alleviation

of human suffering for each dollar of aid (Fowler 1996; Leen 2006; Najam 1996;

Dillon 2004). It seems to presume that in specifying details of the projects upon

which their funding must be spent, donors know the most effective way to alleviate

poverty at the local level. Where donors have common project requirements and

specifications across a number of locations, it also presumes that variable local

conditions do not affect the manner in which aid projects should be run to deliver the

maximum benefit.

14

In practice, there is a distance between the donors in more developed nations and the

localised aid projects, and differences exist in local conditions that affect the impact

of different aid delivery processes. This implies that to help maximize the

effectiveness of aid delivery, local knowledge needs to be used in deciding and

specifying the details of individual aid projects at the local level (Najam 1996;

Hilhorst 2002; Dillon 2004).

2.4 Obstacles that hinder the implementation of accountability systems

Lack of accountability, unethical behaviour and corrupt practices have apparently

become so pervasive, and even institutionalized norms of behaviour. Aside this,

outright bribery and corruption, nepotism, embezzlement, influence peddling, use of

one's position for self-enrichment, bestowing of favours on relatives and friends,

partiality, late coming to work, abuse of public property, leaking and/or abuse of

government information and the like are common manifestation of this plight.

Dealing successfully with this phenomenon requires a deeper understanding of its

underlying causes. Repeated attempts have been made over the years to combat

corrupt practices and unethical violations. A common feature of those is the

enactment of codes and establishment of institutional mechanisms to enforce ethical

behaviour (Rasheed, 1995). For example, Nigeria enacted a Code of Conduct in 1975

- which was subsequently incorporated into the 1979 and 1989 constitutions -

requiring public officials not to allow personal interests to conflict with their official

responsibilities; not to operate foreign bank accounts; not to ask for gifts; and to

declare their assets immediately after taking office, every four years and at the end of

their terms of office. In addition, the Economic and Financial Crimes Commission

(EFCC) and the Independent Corrupt Practices Commission (ICPC) and other bodies

have also been established to curb ethical violations.

15

In some cases, these initiatives were partially successful in achieving some of the

immediate objectives behind these measures. However, this has not been generally

the case. More crucial has been the fact that the incidence of ethical violation has

increased even where a number of violators have been investigated and/or punished

especially by the EFCC. Therefore, the crucial question here is: why have these

measures been generally unsuccessful? In an attempt to answer this question the

following reasons are given.

2.5 Concept of Auditing

Auditing refers to a systematic and independent examination of books, accounts,

documents and vouchers of an organization to ascertain how far the financial

statements present a true and fair view of the concern. It also attempts to ensure that

the books of accounts are properly maintained by the concern as required by law.

This is done with the sole aim of ensuring that funds, resources and valuable of

corporations, on-Governmental Organisation, and government institutions are not

misappropriated, abuse or use for personal gains

Auditing has become such an ubiquitous phenomenon in the corporate and the public

sector that academics started identifying an "Audit Society". According to Power

Michael. 1999. (The Audit Society: Rituals of Verification. Oxford: Oxford University Press) the

auditor perceives and recognizes the propositions before him/her for examination,

obtains evidence, evaluates the same and formulates an opinion on the basis of his

judgement which is communicated through his audit report.[2]

2.6 Independent Auditing Standards

The auditing process is based on standards, concepts, procedures, and reporting

practices that are primarily imposed by the Institute of Chartered Accountants (ICA

16

Gh). The auditing process relies on evidence, analysis, conventions, and informed

professional judgment. General standards are brief statements relating to such

matters as training, independence, and professional care. AICPA general standards

declare that:

External audits should be performed by a person or persons having adequate

technical training and proficiency as an auditor.

The auditor or auditors maintain complete independence in all matters

relating to the assignment.

The independent auditor or auditors should make sure that all aspects of the

examination and the preparation of the audit report are carried out with a high

standard of professionalism.

Standards of fieldwork provide basic planning standards to be followed during

audits. The AICPA's standards for fieldwork stipulate that:

The work is to be adequately planned and assisted, if any, are to be properly

supervised.

Independent auditors will carry out proper study and evaluation of the

existing internal controls to determine their reliability and suitability for

conducting all necessary auditing procedures.

External auditors will make certain that they are able to review all relevant

evidential materials, whether obtained through inspection, observation,

inquiries, or confirmation, so that they can form an informed and reasonable

opinion regarding the quality of the financial statements under examination.

17

Standards of reporting describe auditing standards relating to the audit report and its

requirements. AICPA standards of reporting stipulate that the auditor indicate

whether the financial statements examined were presented in accordance with

generally accepted accounting principles; whether such principles were consistently

observed in the current period in relation to the preceding period; and whether

informative disclosures to the financial statements were adequate. Finally, the

external auditor's report should include 1) an opinion about the financial

statements/records that were examined, or 2) a disclaimer of opinion, which typically

is included in instances where, for one reason or another, the auditor is unable to

render an opinion on the state of the business's records.

2.7 Related Terms: Audits, Internal; Accounting Methods

An audit is a systematic process of objectively obtaining and evaluating the accounts

or financial records of a governmental, business, or other entity. Whereas some

businesses rely on audits conducted by employees—these are called internal audits—

others utilize external or independent auditors to handle this task (some businesses

rely on both types of audits in some combination).

External auditors are authorized by law to examine and publicly issue an opinion on

the reliability of corporate financial reports. Dennis Applegate describes the history

of the external audits in an article appearing in the magazine Internal Auditor as

follows. "The U.S. Congress shaped the external auditing profession and created its

primary audit objective with the passage of the Securities Act of 1933 and the

Securities Exchange Act of 1934. This combined legislation requires independent

financial audits of all firms whose capital stock is bought and sold in open markets.

Its purpose, in part, is to ensure that the financial status and operating performance of

18

publicly traded companies are fairly presented and disclosed." Firms not obliged by

law to perform external audits often contract for such accounting services

nonetheless. Smaller businesses, for example, that do not have the resources or

inclination to maintain internal audit systems will often have external audits done on

a regular basis as a sort of safeguard against errors or fraud.

The primary goal of external auditing is to determine the extent to which the

organization adheres to managerial policies, procedures, and requirements. The

independent or external auditor is not an employee of the organization. He or she

performs an examination with the objective of issuing a report containing an opinion

on a client's financial statements. The attest function of external auditing refers to the

auditor's expression of an opinion on a company's financial statements. The typical

independent audit leads to an attestation regarding the fairness and dependability of

the statements. This is communicated to the officials of the audited entity in the form

of a written report accompanying the statements (an oral presentation of findings

may sometimes be requested as well). During the course of an audit study, the

external auditor also becomes well-acquainted with the virtues and flaws of the

client's accounting procedures. As a result, the auditor's final report to management

often includes recommendations on methodologies of improving internal controls

that are in place.

Major types of audits conducted by external auditors include the financial statements

audit, the operational audit, and the compliance audit. A financial statement audit (or

attest audit) examines financial statements, records, and related operations to

ascertain adherence to generally accepted accounting principles. An operational audit

examines an organization's activities in order to assess performances and develop

19

recommendations for improvements, or further action. Auditors perform statutory

audits which are performed to comply with the requirements of a governing body,

such as a federal, state, or city government or agency. A compliance audit has as its

objective the determination of whether an organization is following established

procedures or rules.

2.8 Working with External Auditors

Experts urge business owners to establish proactive working relationships with

external auditors. In order to accomplish this, companies should make sure that they:

Select an auditing firm with expertise in their industry and a proven track

record.

Establish and maintain efficient record keeping systems to ease the task of the

auditor.

Make sure that owners, executives, and managers know the basics of

financial reporting requirements.

Establish effective lines of communication and work processes between

external auditors and internal auditors (if any).

Recognize the value that external auditors can have as objective reviewers of

existing and proposed operational processes.

Focus on high-risk areas of operations, such as inventory levels.

Focus on periods of change and expansion, such as transitions to public

ownership or expansion into new markets.

Build an effective audit committee that can provide cogent financial and

operational analysis based on audit results.

20

2.9 The External Auditing Process

The independent auditor generally proceeds with an audit according to a set process

with three steps: planning, gathering evidence, and issuing a report.

In planning the audit, the auditor develops an audit program that identifies and

schedules audit procedures that are to be performed to obtain the evidence. Audit

evidence is proof obtained to support the audit's conclusions. Audit procedures

include those activities undertaken by the auditor to obtain the evidence. Evidence-

gathering procedures include observation, confirmation, calculations, analysis,

inquiry, inspection, and comparison. An audit trail is a chronological record of

economic events or transactions that have been experienced by an organization. The

audit trail enables an auditor to evaluate the strengths and weaknesses of internal

controls, system designs, and company policies and procedures.

2.10 Audit planning

International Standard on Auditing 300: Planning an Audit of Financial

Statements requires auditor to plan the audit engagement. This involves setting up

audit strategy and then devising a plan in the light of strategy. As the engagement

progress, auditor may feel the need to update, extend or change the planned

procedures. How this is done and what needs to be done. Also the Auditor is required

to plan the audit by developing an audit strategy to guide the plan itself. Audit plan is

necessary for number of reasons of which the foremost is to achieve audit efficiency

and effectiveness. Audit plan involves planning risk assessment procedures, further

audit procedures and other audit procedures to obtain sufficient appropriate audit

evidence. During the audit if auditor concludes that initial plan requires alteration

21

then auditor shall consider revising audit strategy as well if needed. Change in audit

plan involves change in the scope timing or extent of planned audit procedures.

Auditor shall document the audit plan and any changes thereto.

2.11 Responsibilities of management and auditors for fraud and error

2.1.1.1 Responsibilities of management

Management is responsible for preparing financial statements that show a 'true

and fair view'. This role is reinforced by principles of good corporate

governance, which require management to set up appropriate systems and

controls. Management is therefore responsible for the prevention and detection

of fraud and error.

2.11.2 Responsibilities of the auditor

The auditor is responsible for reporting on whether the financial statements show

a 'true and fair view'. He is therefore only concerned with fraud and error that has

a material effect on the true and fair view. The auditor's responsibility is to

obtain reasonable assurance that the financial statements, taken as a whole, are

free from material misstatement, whether caused by fraud or error. It is not the

primary responsibility of the auditor to prevent or detect fraud error or, although

the audit may act as a deterrent to fraud. Auditors may also discover error or

fraud during the course of their audit work, but they are by no means certain to

do so whenever error or fraud has occurred. It must be recognized that some

material misstatements caused by fraud or error may go undetected, because of

the inherent limitations in any audit and the fact that deliberate attempts may be

made to conceal fraud from the auditor.

ISA240 states the responsibilities of management and the auditor as follows:

22

'The primary responsibility for the prevention and detection of fraud

rests with both those charged with governance of the entity and

management.'

An auditor conducting an audit in accordance with ISAs is

responsible for obtaining reasonable assurance that the financial

statements as a whole are free from material misstatement, whether

caused by fraud or error.'

2.12 Detecting Fraud

Detection of potentially fraudulent financial record keeping and reporting is one of

the central charges of the external auditor. According to Fraudulent Financial

Reporting, 1987—1997, a study published by the Committee of Sponsoring

Organizations of the Treadway Commission, most companies charged with financial

fraud by the Securities and Exchange Commission (SEC) posted far less than $100

million in assets and revenues in the year preceding the fraud. Not surprisingly, fraud

cropped up most often in companies in the grips of financial stress, and it was

perpetrated most often by top-level executives or managers. According to the study,

more than 50 percent of fraudulent acts uncovered by the SEC involved

overstatements of revenue by recording revenues prematurely or fictitiously.

As the study's authors, Mark Beasley, Joseph Carcello, and Dana Hermanson, noted

in Strategic Finance, fraudulent techniques in this area included false sales,

recording revenues before all terms were satisfied, recording conditional sales,

improper cutoffs of transactions at period end, improper use of percentage of

completion, unauthorized shipments, and recording of consignment sales as

completed sales. In addition, many firms overstated asset values such as inventory,

23

accounts receivable, property, equipment, investments, and patent accounts. Other

types of fraud detailed in the study included misappropriation of assets (12 percent of

charged companies) and understatement of liabilities and expenses (18

percent).Accidental misstatements are almost always detected in audits. But these

errors should not be confused with fraudulent activity. Errors can occur at any time,

in any place with unpredictable financial statement effects. Fraud, on the other hand,

is intentional and is often more difficult to detect than are errors. Part of the job of an

external auditor is to recognize when conditions indicate potentially higher risks of

employee or management fraud and then increase the scrutiny of all records

accordingly.

2.13.The distinction between fraud and error

ISA 240 The auditor's responsibilities relating to fraud in an audit of financial statements

regulates this area. It makes the following distinction between fraud and error:

Fraud: may be defined as intentional acts which may involve:

fraudulent financial reporting (falsification of records or

documents, a deliberately incorrect application of accounting

policies)

misappropriation of assets.

Both types of fraud can result in material misstatements in the financial

statements.

Error may be defined as:

unintentional misapplication of accounting policies

oversights

24

unintentional clerical errors, or

Misinterpretation of facts.

The key distinction between fraud and error is therefore whether the effect on the

financial statements is deliberate (fraud) or unintentional (error). However, there

may be little or no difference between fraud and error as far as the impact on the

audit is concerned. In both cases the auditor will be concerned about the impact

on the 'true and fair view' presented by the financial statements.

The main difference between fraud and error may arise in relation to any national

reporting requirements. There may be requirements to report suspicions of fraud,

but not error.

2.14 The Audit Report

The independent audit report sets forth the independent auditor's findings about the

business's financial statements and their level of conformity with generally accepted

accounting principles. A check is made to verify that representations over a period of

years are consistent. A fair presentation of financial statements is generally

understood by accountants to refer to whether the accounting principles used in the

statements have general acceptability. This includes such things as 1) the accounting

principles are appropriate in the circumstances; 2) the financial statements are

prepared so they can be used, understood, and interpreted; 3) the information

presented in the financial statements is classified and summarized in a reasonable

manner; and 4) the financial statements reflect the underlying events and transactions

in a way that presents an accurate portrait of financial operations and cash flows

within reasonable and practical limits.

25

The auditor's unqualified report contains three paragraphs. The introductory

paragraph identifies the financial statements audited, states that management is

responsible for those statements, and asserts that the auditor is responsible for

expressing an opinion on them. The scope paragraph describes what the auditor has

done and specifically states that the auditor has examined the financial statements in

accordance with generally accepted auditing standards and has performed

appropriate tests. The opinion paragraph expresses the auditor's opinion (or formally

announces his or her lack of opinion and why) on whether the statements are in

accordance with generally accepted accounting principles.

Various audit opinions are defined by the AICPA's Auditing Standards Board as

follows:

Unqualified opinion — This opinion means that all materials were made

available, found to be in order, and met all auditing requirements. This is the

most favourable opinion that can be rendered by an external auditor about a

company's operations and records.

Explanatory language added—Circumstances may require that the auditor

add an explanatory paragraph (or other explanatory language) to his or her

report. When this is done the opinion is prefaced with the term, explanatory

language added.

Qualified opinion—This type of opinion is used for instances in which most

of the company's financial materials were in order, with the exception of a

certain account or transaction.

Adverse opinion—An adverse opinion states that the financial statements do

not accurately or completely represent the company's financial position,

26

results of operations, or cash flows in conformity with generally accepted

accounting principles. Such an opinion is obviously not good news for the

business being audited.

Disclaimer of opinion—A disclaimer of opinion states that the auditor does

not express an opinion on the financial statements, generally because he or

she feels that the company did not present sufficient information. Again, this

opinion casts an unfavourable light on the business being audited.

The fair presentation of financial statements does not mean that the statements are

fraud-proof. The independent auditor has the responsibility to search for errors or

irregularities within the recognized limitations of the auditing process. Investors

should examine the auditor's report for citations of problems such as debt-agreement

violations or unresolved lawsuits. "Going-concern" references can suggest that the

company may not be able to survive as a functioning operation. If an "except for"

statement appears in the report, the investor should understand that there are certain

problems or departures from generally accepted accounting principles in the

statements, and that these problems may call into question whether the statements

fairly depict the company's financial situation. These statements typically require the

company to resolve the problem or somehow make the accounting treatment

acceptable.

2.15 Internal Audit

The Institute of Internal Auditors defines Internal Audit as “…an independent,

objective assurance and consulting activity designed to add value and improve an

organization’s operations. It helps an organization accomplish its objectives by

27

bringing a systematic, disciplined approach to evaluate and improve the

effectiveness of risk management, control, and governance processes.”

Internal audit function is also defined in ISA 610 as an appraisal or monitoring

activity established within an entity as a service to the entity. It functions by,

amongst other things, examining, evaluating and reporting to management and the

directors on the adequacy and effectiveness of components of the accounting and

internal control systems.

There are several parts to the definition of Internal Auditing which gives the core

role of the Internal Auditor as:

Independent and objective assurance and consulting activity;

Designed to add value and improve an organization‘s operations;

Helps an organization to accomplish its objectives by

bringing a systematic, disciplined approach to:

evaluate and

Improve the effectiveness of risk management, control, and

governance processes.‖

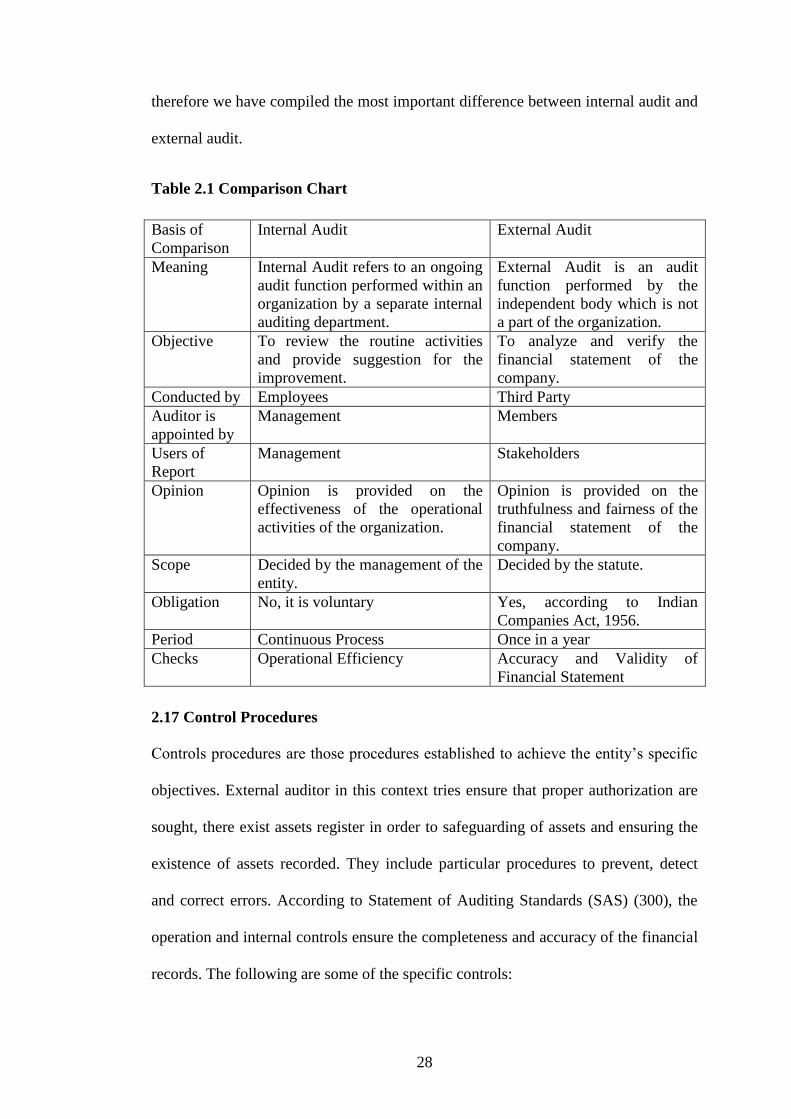

2.16 Difference between Internal Audit and External Audit

Internal Audit and External Audit are the two most important types of audit which

are performed in an organization. Internal Audit is not compulsory by nature, but

can be conducted to review the operational activities of the organization. Let‘s look

the other term External Audit which is obligatory for every separate legal entity,

where a third party is brought to the organization to perform the process of Audit and

give its opinion on the Financial Statements of the company. It happens many times

that we consider both as one, but they are thoroughly different from each other and

28

therefore we have compiled the most important difference between internal audit and

external audit.

Table 2.1 Comparison Chart

Basis of

Comparison

Internal Audit External Audit

Meaning Internal Audit refers to an ongoing

audit function performed within an

organization by a separate internal

auditing department.

External Audit is an audit

function performed by the

independent body which is not

a part of the organization.

Objective To review the routine activities

and provide suggestion for the

improvement.

To analyze and verify the

financial statement of the

company.

Conducted by Employees Third Party

Auditor is

appointed by

Management Members

Users of

Report

Management Stakeholders

Opinion Opinion is provided on the

effectiveness of the operational

activities of the organization.

Opinion is provided on the

truthfulness and fairness of the

financial statement of the

company.

Scope Decided by the management of the

entity.

Decided by the statute.

Obligation No, it is voluntary Yes, according to Indian

Companies Act, 1956.

Period Continuous Process Once in a year

Checks Operational Efficiency Accuracy and Validity of

Financial Statement

2.17 Control Procedures

Controls procedures are those procedures established to achieve the entity‘s specific

objectives. External auditor in this context tries ensure that proper authorization are

sought, there exist assets register in order to safeguarding of assets and ensuring the

existence of assets recorded. They include particular procedures to prevent, detect

and correct errors. According to Statement of Auditing Standards (SAS) (300), the

operation and internal controls ensure the completeness and accuracy of the financial

records. The following are some of the specific controls:

29

Request by user departments and for appropriate authorization by the head

Control over computerized applications and the information technology

environment.

Checking the arithmetical accuracy of the records.

Ensure that goods are receipted in stores before requisitions are made

Reconciliations

Comparing the results of cash, security and inventory with accounting records

Comparison with external source of information

Comparison of results with budget

Limiting direct physical access to assets and records

2.18 Assessing the effectiveness of the external audit process

It is important that the audit committee has an independent point of view on audit

quality.

These requirements are part of recent measures intended to increase the transparency

of the external audit process and the accountability of the auditor to the audit

committee and the audit committee to shareholders. The latest development which

calls for further strengthening in this area is the Competition Commission‘s report.

Amongst other things the report recommends that:

An advisory vote be introduced on the audit committee‘s report (within the

annual report and accounts).

Audit committees report the results of any external quality inspections of the

auditor during the period.

30

Only audit committees be permitted to negotiate and agree audit fees, the

scope of audit work, initiate tender processes, make recommendations for

appointment of auditors and authorize the external audit firm to carry out

non-audit services. Assessing the effectiveness of external audit process is not

new to audit committees.

Result in constructive and honest dialogue with the audit firm about its

performance, what went well and what could be improved.

Provide insights for the company into a broad range of areas including

governance, processes and controls and business improvement

Result in optimized assurance being derived from the audit

Help inform future audit tender processes that the audit committee will

undertake.

2.19 Audit Committees

There are a number of definitions for audit committees, each tailored to the

environment and structure in which they operate. According to Wong (2012) an audit

committee is defined as a subcommittee of the board of directors or its equivalent

structure. An audit committee is a committee of the board of directors responsible for

oversight of the financial reporting process, selection of the independent auditor, and

receipt of audit results‖ (AICPA, USA: 2009).

AARF, IIA-Australia, and AICD - Joint Publication Audit Committees 2002: Best

Practice Guide (second edition) defined ―An audit committee is a subcommittee of

the Board of an organization. It provides a forum where directors, managers and

auditors together can deal with issues relating to the management of risk and with

other governance obligations (AARF, IIA-Australia, AICD, AARF Joint Publication

2002 :10).

31

An audit committee operates within a network of relationships. They are reliant on

management, internal audit and external audit to provide the information required to

meet their functions of assessment and exercise of control on behalf of their boards

(Wong, 2012). Typically an audit committee in the private sector is a committee of

the board of directors. Directors in the private sector are either executive or non-

executive independent members. Audit committee members in private sector

organisations are usually independent directors. The audit committee in the public

sector, where the governing body do not have a board audit committee, have

members appointed and selected by the organisation to provide advice to

Departmental Secretaries or boards of directors. In Ghana for example audit

committee report to Boards where it exists while in other countries audit committee

report to chairperson of the councils or the boards.

2.19.1 Characteristics of Audit Committees

The following are characteristics of audit committee according to Wong (2012) that

appear critical to enable audit committee performance include:

having clear authority and definition of its role, legal authority, charter, terms

of reference and organizational status;

having audit committee members with the right attributes qualifications and

experience; and

having the audit committee perform the required oversight functions,

processes, activities, procedures and compliance with professional standards.

The Blue Ribbon Committee (BRC 1999) regulating US corporate

environment also suggested that three important issues should be addressed in

order to successfully improve the performance of a Corporate Audit

Committee: (i) effectiveness, (ii) accountability, (iii) independence.

32

2.19.2 Effectiveness

DeZoort & Salterio (2001) found that, in the case of auditor-management disputes,

the independent members of an audit committee and the level of members‘ auditing

knowledge were positively associated with support for the auditor, thus assuring that

financial disclosure would be in compliance with standards. Effectiveness is also

associated with the appointment of audit committee members who are financially

literate. Regarding financial expertise, Davidson, Xie & Xu (2004) found that

auditing and audit firm experience is more important than corporate financial

management and financial statement experience because auditors are required to

verify what management has prepared. Verifying and evaluating presented financial

reports against accounting standards by applying procedures specified in auditing

standards provides that additional assurance.

2.19.3 Role of Audit Committee

To perform its role an audit committee must be established and be empowered with

the authority to perform its duties. That is government departments and agencies are

required to establish audit committees. Best practice governance (OECD 2004)

requires Boards to establish boards and audit committees that are independent from

management. Independence however is related to composition of the committee.

Wong (2012) summarized the role of an audit committee as to ensure that reliable

information about the processes and outcomes of management control and operations

and their accountability are conveyed to the board. Therefore, a major issue for audit

committees to address is their oversight role. Wong further asserted that audit

committee assists the board or a departmental head in fulfilling its oversight

responsibilities for the financial reporting process, the system of internal control over

financial reporting, the audit process, and the organization‘s process for monitoring

33

compliance with laws and regulations. Audit committees (―Audit Committee‖) are

recognized as the cornerstone of a successful and credible financial reporting system.

To many, the Audit Committee is the epitome of corporate governance. The role of

the Audit Committee is to lend creditability to the integrity of the internal control and

financial reporting system, and to boost confidence in the company‘s financial

reporting. The essence to an Audit Committee‘s function is its independence, given

that it needs to be made up of entirely non-executive directors, majority of which are

independent, which allows it to carry out its roles effectively.

The Victorian Department of Heath website (2010) cited in Wong (2012) states ―The

role of the Audit Committee is to provide independent assurance and assistance to

the Secretary on the Department‘s risk management and control and compliance

frameworks and its external accountability responsibilities‖

Audit committees are responsible for financial and risk management oversight and

are one of several internal governance mechanisms whose function is to assist a

board of directors to monitor management performance (ASX 2007). Adamu and

Yusoff (2012) summarized the role of the audit committee in the following

statements as most of the organisation‘s failed due to lack of risk exposure relating to

the organisation‘s governance in relation to; compliance with laws, regulations, &

contracts operation and information system effective and efficiency of operation,

reliability and integrity of financial and operation information and safeguarding the

assets. They further contend that, audit committee is established with the aim of

enhancing confidence in the integrity of an organisation's processes and procedures

relating to internal control and corporate reporting including financial reporting

(Adamu and Yusoff, 2012). Audit Committee provides an ‗independent‘ guarantee to

the board through its oversight and monitoring role. Among many responsibilities the

34

boards entrust the Audit Committee with the transparency and accuracy of financial

reporting and disclosures, effectiveness of external and internal audit functions,

robustness of the systems of internal audit and internal controls, effectiveness of anti-

fraud, ethics and compliance systems, review of the functioning of the whistleblower

mechanism. Audit Committee also plays a significant role in the oversight of the

company‘s risk management policies and programs (Adamu and Yusoff, 2012).

According to the State Queensland Treasury and Trade (2012) audit committee can

involve all or a combination of the following duties and responsibilities:

Obtain assurance from management that all financial and non-financial

internal control and risk management functions are operating effectively and

reliably.

Provide an independent review of an agency‘s reporting functions to ensure

the integrity of financial reports.

Monitor the effectiveness of the agency‘s performance management and

performance information.

Provide strong and effective oversight of an agency‘s internal audit function.

Provide effective liaison and facilitate communication between management

and external audit.

Provide oversight of the implementation of accepted audit recommendations

and

Ensure the agency effectively monitors compliance with legislative and

regulatory requirements and promotes a culture committed to lawful and

ethical behavior.

35

Adams, Grose and Donald (2004) listed a number of these functions which they

propose as generic functions that audit committee perform:

Approving the selection of the external auditor,

Reviewing the arrangements and scope of audit including reviewing the

emphasis of work so that areas considered in need of attention receive it,

Considering reports from the internal auditor and reviewing management

action on them,

Providing a forum for the board, management, or the auditor to raise matters

of concern,

Receiving the necessary information from the auditor as required under the

International Accounting Standards,

Reviewing the annual financial statements prior to their approval by the

board,

Coordinating the work of internal audit and external audit, Assessing the

effectiveness of management information systems, Reviewing significant

transactions of an extraordinary or abnormal nature and Assessing current

and potential risks.

36

CHAPTER THREE

RESEARCH METHODOLOGY

3.0 Introduction

This chapter will focus on the methodology the researcher will adopt to undertake the

study. The areas study will cover include the study design, the population, sample

size, sampling techniques; data collection and analysis as well sources of data for the

study.

3.1 Study Design

The researcher used mixed approaches which consist of both qualitative and

quantitative research methods. Qualitative analysis according to (Borrego et al.,

2009) is characterized by the collection and analysis of textual data which are

surveys, interviews, focus groups, conversational analysis, observation on the context

within which the study occurs. It allows the researcher to make connection between

the study and the situation. Due to this research being an explanatory research, both

quantitative and qualitative analysis was needed. The qualitative results served to

explain the quantitative results according to (Borrego et al., 2009).

The choice of the survey strategy allowed for the collection of large amount of data

from the population. The selection of survey design over other research methods

such as experimental, longitudinal, cross-sectional and others was determined by the

assertion of Saunders, Lewis, and Thornhill (2007) that survey is an appropriate and

a common strategy in business and management researches which is a highly

economical means of analyzing a large amount of data.

In addition, the research involves quantitative study. Miles and Huberman (1994)

indicated that quantitative research involves primary understanding in terms of

37

measurement of quantity, intensity or frequency. It is about asking people for their

opinions in structured way so that one can produce hard facts and statistics to guide

you. To get reliable statistical results, it is important to survey people in fairly large

numbers and make sure they are representative sample of the target. It is for this

reason that the researcher is selecting quantitative to gain deeper understanding of

the subject matter which is to assess the impact of external audit on NGOs in relation

to accountability and transparency.

3.3 Study Population

The study will focus on the impact of external audit of NGO‘s in the light of

accountability and transparency in Ghana by focusing on NGOs in the Bolgatanga.

The region has about twenty three (23) NGOs operating in various projects and

programmes. Out of the twenty three (23), sixteen (16) operate within the Bolgatanga

township and its environs.

The study focused on these 16 NGOs in addition to some selected beneficiaries. The

beneficiaries included heads of schools, opinion leaders and Assembly Men in

various areas.

3.4 Sampling Techniques

This study essentially targets Top management staff of these aforementioned offices

and personalities. The researcher therefore will use purposive sampling techniques to

selecting interview respondents. This will ensure that only people with relevant

information are sampled.

3.4.1 Sample Size

Staff of the NGOs will be contacted for all needed information in order to achieve