Embed Size (px)

Citation preview

Ambient Insight

Regional Report

The 2012-2017 Africa Mobile Learning Market

Africa has the Highest Mobile Learning Growth Rate in the

World with Consumers Driving the Market and Academic Segments Coming On Board at a Rapid Rate

“We Put Research into Practice”

www.ambientinsight.com

Market Analysis by: Sam S. Adkins, Chief Research Officer

Published: September 2013

To learn more about our research services, email:

Ambient Insight Copyright Policy: All rights reserved. All media and research data published by Ambient Insight are protected by copyright. Unauthorized use of Ambient Insight research without prior permission is prohibited. Ambient Insight research products provide valuable financial data only to the individual purchaser or the purchasing organization. Purchasers may not modify or repurpose the information and financial data in our research in any manner. Specific distribution rights are provided based on the license model granted at time of purchase. Quoting Ambient Insight Research: Permission is required to use quotes, tables, diagrams, or charts from Ambient Insight research in press releases, promotional material, external presentations, or commercial publications. Permission from Ambient Insight is required to reproduce or distribute in entirety any table, paragraph, section, or report.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 2

Table of Contents

List of Tables ...................................................................... 3

List of Figures ..................................................................... 3

Abstract ............................................................................. 4

The Major Catalysts in the Africa Mobile Learning Market ......................... 6

The Boom in Mobile Learning VAS .................................................................... 7

The Adoption of Tablets and Personal Learning Devices in the Schools .................. 8

Smarter Low-cost Devices and Faster Networks Pervade Africa .......................... 10

Direct Carrier Billing Energizes the App Ecosystem ........................................... 12

Leapfrogging the Digital Divide In Africa ......................................................... 13

What You Will Find in This Report ............................................... 15

Who is the Buyer? .............................................................................15

What Are They Buying? ......................................................................16

Related Research ...................................................................... 18

2012-2017 Africa Forecast and Analysis ............................... 19

Demand-side Analysis ............................................................... 19

Algeria .............................................................................................20

Angola .............................................................................................21

Ghana ..............................................................................................23

Kenya ..............................................................................................25

Mozambique .....................................................................................29

Nigeria .............................................................................................30

Rwanda ............................................................................................33

Senegal ............................................................................................36

South Africa ......................................................................................38

Tanzania...........................................................................................44

Tunisia .............................................................................................47

Uganda ............................................................................................49

Zambia.............................................................................................51

Zimbabwe .........................................................................................52

Supply-side Analysis ................................................................. 55

Index of Suppliers ............................................................. 57

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 3

List of Tables

Table 1 - 2012-2017 Revenue Forecasts for Mobile Learning by

Fourteen Countries in Africa (in $US Millions) ................................ 19

Table 2 - 2012-2017 Africa Revenue Forecasts for Mobile

Learning by Five Product Types (in $US Millions) ............................ 55

List of Figures

Figure 1 - 2012-2017 Top Africa Mobile Learning Five-year

Growth Rates by Country .............................................................. 4

Figure 2 – Primary Catalysts Driving the 2012-2017 Mobile

Learning Market in Africa .............................................................. 6

Figure 3 - 2012-2017 Africa Mobile Learning Five-year Growth

Rates by Five Product Types ........................................................ 56

“We Put Research into Practice”

www.ambientinsight.com

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 4

Abstract

"The future of education in Africa is mobile. Mobile learning,

either alone or in combination with existing education

approaches, is supporting and extending education in ways

not possible before."

Steve Vosloo, Mobile Learning Specialist, UNESCO

BBC Future, August 2012

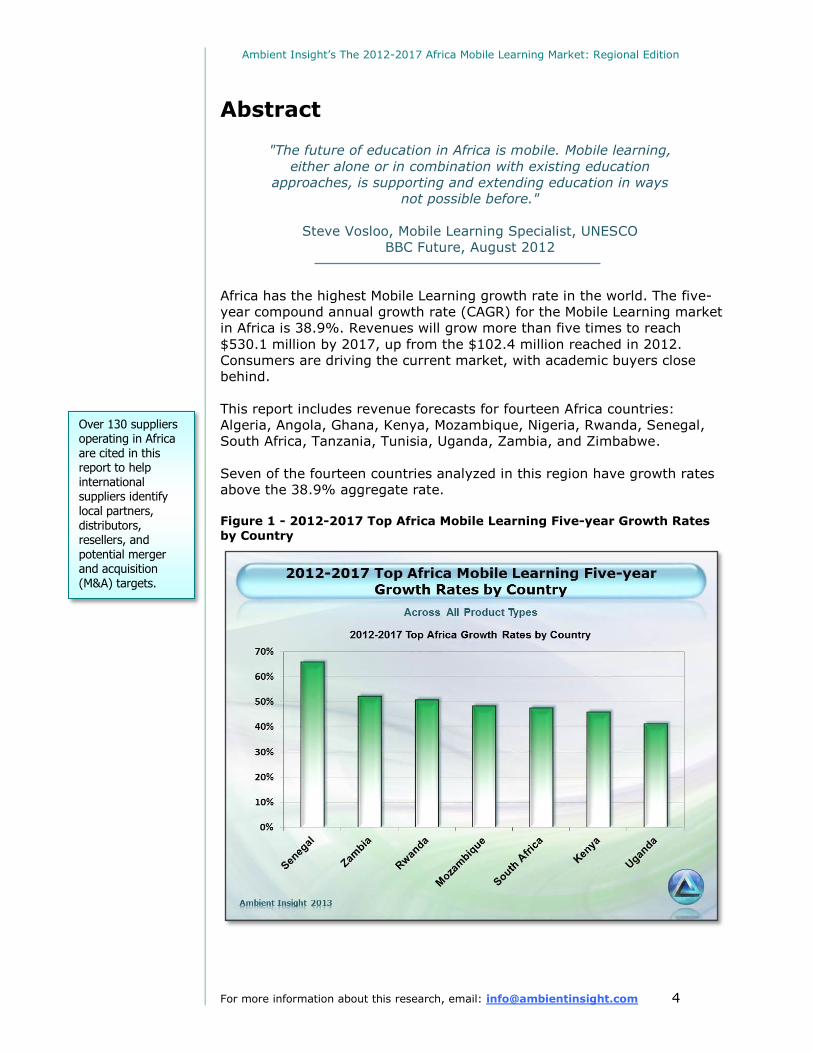

Africa has the highest Mobile Learning growth rate in the world. The five-

year compound annual growth rate (CAGR) for the Mobile Learning market

in Africa is 38.9%. Revenues will grow more than five times to reach

$530.1 million by 2017, up from the $102.4 million reached in 2012.

Consumers are driving the current market, with academic buyers close

behind.

This report includes revenue forecasts for fourteen Africa countries:

Algeria, Angola, Ghana, Kenya, Mozambique, Nigeria, Rwanda, Senegal,

South Africa, Tanzania, Tunisia, Uganda, Zambia, and Zimbabwe.

Seven of the fourteen countries analyzed in this region have growth rates

above the 38.9% aggregate rate.

Figure 1 - 2012-2017 Top Africa Mobile Learning Five-year Growth Rates

by Country

Over 130 suppliers operating in Africa are cited in this report to help international suppliers identify local partners, distributors, resellers, and

potential merger and acquisition (M&A) targets.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 5

Several countries in Africa have mobile penetration rates over 100%

including Algeria, Ghana, Morocco, Senegal, South Africa, and Tunisia.

Adoption rates are growing very fast in every African country analyzed in

this report.

The number of mobile subscribers in Zimbabwe grew from less than

2 million in 2009 to over 11 million subscribers by the end of 2012

The number of mobile subscribers in Ghana jumped from 23.2

million in 2011 to 27.5 million in 2012.

Ambient Insight has revised our forecasts significantly upward for most

African countries. In our syndicated reports, we only include revenue

forecasts for countries with over $1 million in revenue. We have added

nine more countries to our Mobile Learning analysis for Africa in

just the last year.

Africa is not a single cohesive market. There are 56 countries in Africa with

over 1,500 spoken languages. Suppliers that compete in the region must

market products to specific countries and to particular demographics inside

each country. This report provides suppliers with the competitive

intelligence to do this.

The app ecosystem across Africa is relatively new. The device makers and

the telecoms were first to market with app stores; they began launching

app stores in several countries starting in early 2011. Device makers and

telecoms are quite active in the Africa Mobile Learning market and offer

significant partnering opportunities for international suppliers. The device

makers are now expanding their app stores throughout Africa. This report

identifies the device makers and telecoms active in each country.

Unlike other regions of the world where many telecoms have closed down

their app stores, they are still opening new app stores in Africa—the most

recent being MTN's app store in Nigeria, which opened in July 2013.

Apple opened app stores in sixteen African countries in the last two

years including Algeria, Angola, Ghana, Mozambique, Nigeria,

Tanzania, and Zimbabwe.

In December 2012, Microsoft opened twenty app stores across

Africa including Angola, Kenya, Mozambique, Rwanda, Senegal,

Tanzania, Uganda, Zambia, and Zimbabwe.

Amazon opened their first app store in Africa in South Africa in late

2011. They opened app stores across the continent in May 2013.

The BlackBerry World app store is now available in 37 African

countries. BlackBerry has taken an active role in supporting the

local development of apps in Africa. As of January 2013, there were

over 80 universities and colleges participating in the BlackBerry

Academic Program (BAP).

Because of their own app stores, direct carrier billing agreements with device makers, and their Mobile Learning VAS offerings, the telecoms are major players in the Mobile Learning market in Africa.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 6

While app stores are new to the region, Mobile Learning Value Added

Services (VAS) products have been on the market in Africa since 2009

when Nokia launched Nokia Life in Uganda. Nokia Life launched in Nigeria

in 2010. Yet the majority of Mobile Learning VAS products came on the

market in 2012 and 2013.

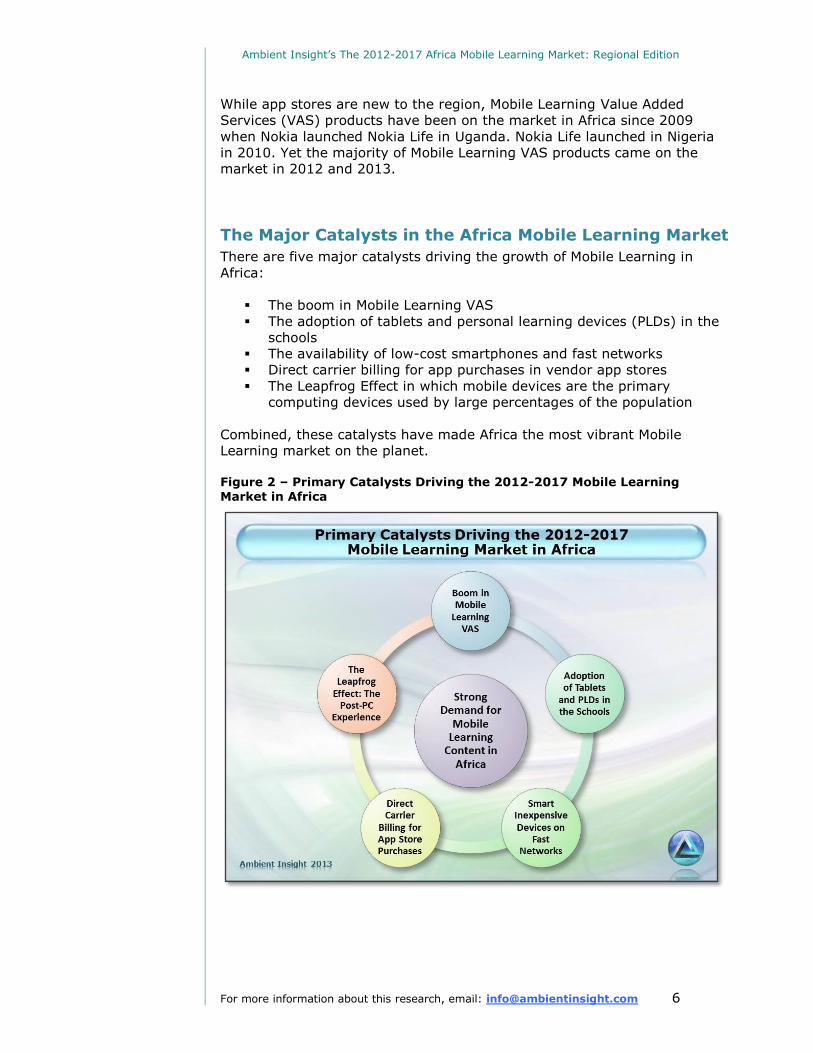

The Major Catalysts in the Africa Mobile Learning Market

There are five major catalysts driving the growth of Mobile Learning in

Africa:

The boom in Mobile Learning VAS

The adoption of tablets and personal learning devices (PLDs) in the

schools

The availability of low-cost smartphones and fast networks

Direct carrier billing for app purchases in vendor app stores

The Leapfrog Effect in which mobile devices are the primary

computing devices used by large percentages of the population

Combined, these catalysts have made Africa the most vibrant Mobile

Learning market on the planet.

Figure 2 – Primary Catalysts Driving the 2012-2017 Mobile Learning Market in Africa

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 7

The Boom in Mobile Learning VAS

“mLearning is powerful because it breaks through the

traditional barriers of time, location, and the cost of delivering

educational content. The power of the Internet in an

educational context has always been that it simplifies access

to content and the experts on that content. With Mxit we are

taking that power and making it easily accessible on the

average feature phone.”

Andrew Rudge, Chief of Insight and Reach at Mxit

October 2012

By July 2013, there were 44 Mobile Learning VAS products in Africa. Kenya

and South Africa led the region with eight and five Mobile Learning VAS

products, respectively. The African Mobile Learning VAS market is unique.

Language learning content dominates the Asia and Latin America Mobile

Learning VAS markets. Literacy, exam prep (also known as exam revision),

mHealth, and "agro" educational content are the top Mobile Learning VAS

products in Africa. Like Asia and Latin America, many Mobile Learning VAS

offerings in Africa have millions of subscribers.

Mxit is the largest social network in South Africa. Mxit is also a native

mobile platform. By October 2012, Mxit had over five million subscribers to

their new educational content catalog, with 600,000 subscribing to the

eight exam revision applications. Although smartphones are now

supported, most Mxit users still access the service via a feature phone.

Mxit executives reported in the press that "this provides ample evidence

that the average mobile phone can become a transformative education tool

for learners."

One successful Mobile Learning VAS on Mxit is QuizMax (developed by

Learning to the Max Foundation), which has over 200,000 subscribers.

QuizMax is an exam prep service for high school students and offers

practice exams that map to South Africa's National Examination Guidelines

on math, physical science, and life science exams.

Another successful Mobile Learning VAS on Mxit is CellSchool. CellSchool

provides short video lessons for 12th graders on math, science, English,

literacy, and accounting. Live tutors are available two hours a day. The

charges for CellSchool are the equivalent of forty cents for a ten-minute

lesson.

Nokia continues to roll out their Nokia Life Mobile Learning VAS across

Africa. Nokia Life, already available in Uganda and Nigeria, launched in

Kenya in early 2013. In April 2013, Bharti Airtel, the region's largest

telecom, announced that they would make Nokia Life available in fifteen

additional countries in Africa including Ghana, Rwanda, Tanzania, and

Zambia.

Nokia Life is "designed to meet customer needs in areas such as education,

agriculture, healthcare, livelihood, and even spirituality." Since its launch in

An interesting Mobile Learning VAS is Kytabu eTextbook rental service for tablets in Kenya. The content is designed for PreK-12 students and

streamed in real time to their tablets. Their parents "rent" the eTextbooks for three cents an hour.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 8

India, Nokia Life has expanded to over 30 countries, and as of June 2013,

had reached more than 100 million people with Mobile Learning content in

18 languages.

Africa has become the proving ground for Mobile Healthcare (mHealth)

services with over 95 active programs operating across the region by the

end of 2012, the most for any region in the world. The mHealth initiatives

are heavily concentrated in Kenya and Uganda, so far. All mHealth

initiatives employ educational content and many are designed solely for

healthcare education.

The telecoms partner with content providers and have become a

lucrative distribution channel for digital education content

publishers. Over 35 of these telecoms are identified in this report.

An example of an "agro" Mobile Learning VAS is iCow, officially launched by

Safaricom in Kenya in July 2013. The service offers a range of agricultural

education and advice and had been in a pilot stage prior to the formal

launch. At the formal launch, the service had over 6,000 active users that

pay the equivalent of four cents per SMS message.

Wikipedia Zero is a free Mobile Learning VAS that includes a text-only

version of the Wikipedia site. The Russia-based telecom VimpleCom

distributes Wikipedia Zero in Africa. As of September 2012, VimpelCom had

212 million mobile subscribers in 18 countries across Asia and Africa. "The

main target for Wikipedia Zero is people whose primary or only internet

access is via a mobile device."

The Adoption of Tablets and Personal Learning Devices in the Schools

"There is a not so quiet revolution playing out in the education

sector in Osun State, Nigeria. The Opon Imo initiative is a

unique and groundbreaking attempt at re-engineering how

students learn at the senior secondary level, by making

available to each one of them hand held digital tablets."

Gbenro Adegbola, Managing Director of Evans Publishers

May 2013

Both the PreK-12 and higher education segments across Africa are just

beginning to use mobile devices in the classroom. There were hundreds of

small-scale initiatives as of the end of 2012. The larger deployments have

just started. By the end of the forecast period, tablets will be a major

distribution channel for educational content suppliers competing in Africa.

In October 2012, Microsoft announced an agreement with the

Kenyan government and Indigo Telecom to supply 2,000 tablets

preloaded with educational content to rural Kenyan schools. This is

an example of a relatively small-scale deployment.

Vodafone's Healthline Mobile Learning VAS in Ghana is an SMS-based product that provides subscribers with a range of healthcare related educational content and advice. Vodafone charges five cents per message.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 9

In June 2013, the governor of Osun State in Nigeria announced the

Opon-imo (tablet of knowledge) program that will distribute tablets

to every secondary student in the state. The first phase will deploy

150,000 tablets preloaded with "an e-library of 63 eTextbooks, a

virtual classroom, and an integrated test zone."

In June 2013, the government in Gauteng, a highly urbanized

province in South Africa that includes the cities of Johannesburg and

Pretoria, announced that they would distribute 88,000 Huawei

tablets to 2,200 schools in the province by January 2014.

In June 2013, the Kenyan government announced a four-year $622

million project to provide computing devices to every primary

and secondary student in the country. There are just under 10

million school children in Kenya. In July 2013, the government

indicated that a "significant" amount of those devices would be

tablets.

IT School Innovation (ITSI) is a South African Mobile Learning supplier

serving the PreK-12 segment. ITSI has a deal with Samsung and the ITSI

MobiMath, MobiWord and MobiSpeed apps were preloaded on over three

million Samsung devices in 2012.

The NGO Worldreader distributes Kindle eReaders to schools in Africa

preloaded with over 1,200 eBooks localized for the various countries in

which they operate including Nigeria, Ethiopia, Ghana, Kenya, Uganda,

Rwanda, and Tanzania. Their goal is to reach over one million children

"across the world" by 2015.

Tablet adoption is also gaining traction in the higher education segments in

Africa. In November 2012, Ghana Technology University College (GTUC)

launched a new educational tablet called the Campus Companion. The

tablet was built in collaboration with UK-based Learning Nugget. The tablet

comes preloaded with Mobile Learning content from several educational

publishers and is sold to GTUC's 3,000 students at heavily discounted

prices. In May 2013, Microsoft launched a tablet-based initiative that

targets university students in Dar es Salaam, Tanzania. UhuruOne, a local

ISP, offers an inexpensive bundle that includes a Windows 8 tablet,

wireless broadband connectivity, and educational applications.

In August 2013, the University of South Africa, the largest online education

provider in Africa with over 310,000 students, launched a program to

provide students with 3G connectivity and a tablet at "massively discounted

prices." Students can buy subsidized tablets for as low as $125 and get 3G

access for the equivalent of $10 a month from any of the four major

telecoms.

Personal learning devices (PLDs) are becoming popular in Africa with

domestic suppliers selling PLDs preloaded with content designed for

particular countries.

There are four PLDs in South Africa alone including Phusion Media's

MobiPad, Esquire Technologies' Geeko Kids tablet, Wise Tablets' TAB4Kids,

Samsung launched their Smart School solution in Nigeria in May 2013. It was the first Samsung Smart School deployment in Africa.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 10

and Future Mobile Technology's TouchTutor tablet. A new Zambian

company called iSchool sells a personal learning device (to both schools

and parents) called the ZEduPad, which "is packed with primary school

lessons for Grade 1-7, in eight local languages, and has many other apps

for education, farming, and health."

There are 200,000 OLPC (One-Laptop-Per-Child) laptops used in the

schools in Rwanda. In October 2012, the Rwandan government announced

they would purchase one million more OLPCs by 2017. As of early 2013,

the latest OLPC specification is not a laptop, but a tablet. The additional

OLPCs purchased by Rwanda will be the new tablet OLPC.

Intel's Classmate is a low-cost educational laptop preloaded with

educational content, which many school systems in countries across Africa

including Kenya, Nigeria, and South Africa have purchased. Classmate is a

product specification and domestic manufacturers build the actual device.

In late 2012, the new Classmate specification became a tablet. In August

2013, Intel launched a new branded educational tablet simply called the

Intel Education Tablet, which is also sold pre-loaded with educational

content.

A major trend influencing the adoption of tablets and PLDs in the schools is

the recent availability of very low-cost tablets "flooding" the markets in

every country analyzed in this report. Domestic manufacturers are now

selling tablets priced under $200.

Smarter Low-cost Devices and Faster Networks Pervade

Africa

"Mobile devices are becoming smarter, faster, and more

affordable; smartphone adoption is growing by around 15%

year on year across the continent, and mobile bandwidth has

become better and more affordable."

Ayanda Dlamini, Business Development Manager, LGR

Telecommunications

March 2013

According to the trade organization GSMA, there are over 500 million

mobile subscriptions in Africa and they forecast that this number will grow

to over 750 million by 2017. While most of the phones in use are still

feature phones, most of those phones are now Internet enabled.

Samsung estimates that as of the end of 2012, over 50% of Internet

access in Africa was via mobile devices. In fact, this is often much higher in

certain countries. Over 90% of Internet access in Uganda is via a mobile

phone and over 70% of the Internet access in Senegal is via 3G wireless

networks.

In October 2012, a Samsung executive stated in the press that

smartphones were outselling PCs "at the ratio of 4 to 1 in the three key

Alltel Limited launched the first indigenous personal learning device in Ghana in January 2012. Alltel's K-pad tablet is designed to "provide e-learning and e-health solutions for the Ghanaian market."

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 11

African markets." In February 2013, Safaricom in Kenya announced that

they would phase out feature phones completely in favor of low-cost

smartphones. In May 2013, Vodacom reported it had six million

smartphones on its network in South Africa.

A major learning technology catalyst in Africa is the recent arrival of fiber

optic connectivity. Prior to this, satellite access was the primary

connectivity medium, which is very expensive. This was inhibiting the

uptake of Internet connectivity.

The telecom industries across Africa are undergoing a rapid expansion due

to the recent connections to international fiber optic cables. As of the end

of 2012, ten major undersea cables connect Africa to the global Internet.

This development ends the region's dependency on expensive satellite

connectivity and dramatically increases the bandwidth available to

customers.

The availability of fiber optic connectivity has created a price war with

telecoms and ISPs dropping prices to attract customers. It has also created

a boom in the adoption of Internet and mobile technologies.

3G and 4G wireless networks are rolling out all over Africa. By the end of

2012, all of the fourteen countries in this report had operational 3G

networks. Eleven of the fourteen had launched 4G networks.

In June 2013, the government of Rwanda announced a joint venture with

South Korea's KT Corporation to build a nationwide 4G network that will

provide wireless broadband to 95% of the population in three years. This is

the most comprehensive roll out of 4G in Africa. The new 4G network is

being defined as a "wholesale" network with the government planning to

resell connectivity to the telecoms.

The faster networks are the prerequisite for smartphones and the device

makers are flooding the market with cheap smartphones.

In February 2013, Samsung released their REX series of phones

priced for emerging markets starting as low as $68.

In June 2013, South Africa-based Vodacom launched a $70

smartphone.

In July 2013, Nokia launched their Asha 210 smartphone in Kenya,

Tanzania, and Uganda priced at $76, $85, and $87, respectively.

In August 2013, China-based Spreadtrum Communications released

two smartphone in the Africa market priced in the $40 range. An

executive stated in the press that "These devices are having a

massive effect on the African market, bringing Internet services in

reach for more people than ever before."

In March 2013, Vodacom reported that they sold 1.6 million smartphones

in 2012, a 30% increase from the year before. In May 2013, they reported

In January 2013, the Nigerian government began distributing over 10 million Internet-enabled phones to farmers in the country.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 12

that they had over 6 million smartphones on their network in South Africa,

which is 80% of all smartphones in use in that country.

In February 2013, Microsoft launched the three-year, $70 million Microsoft

4Afrika Initiative. According to Microsoft, "the 4Afrika Initiative plans to

help place tens of millions of smart devices in the hands of African youth."

As part of the initiative, Microsoft and Huawei launched the low-cost

Huawei 4Afrika smartphone. At launch, the phone was available in Angola,

Kenya, Morocco, Nigeria, and South Africa. The Huawei 4Afrika phone is

"targeted toward university students, developers, and first-time

smartphone users."

The availability of powerful inexpensive mobile devices and the recent

arrival of fiber optic and wireless broadband connectivity across the African

continent has created an explosion in the rate of mobile technology

adoption (and dramatic drops in prices.)

Direct Carrier Billing Energizes the App Ecosystem

"Interestingly enough, app stores that drove service providers’

content portals to extinction over the past few years are today

leading efforts to integrate their storefronts with carrier billing.

Carrier billing enables app stores to boost sales conversions by

up to 5-times."

Oded Israeli, Director, Mobile Payments, Amdocs

February 2013

As of the end of 2012, up to 70% of consumers in Africa did not have credit

cards. The advent of direct carrier billing across the continent removes a

major barrier that impeded the growth of the mobile app ecosystem.

By the end of 2012, Samsung, Nokia, Microsoft, Facebook, Sony,

BlackBerry, Mozilla, and Google have direct billing agreements in Latin

America, Africa, and Asia. Amazon joined the fray in August 2013

announcing a deal with third-party mobile billing provider Bango.

The telecoms have a significant advantage in the developing economies as

they are often the only electronic payment gateway.

Two of the largest app stores in Nigeria are branded by the telecoms, but

the stores are actually operated by third-party white-label store providers.

Globacom Nigeria launched their app store in May 2012. Globacom's

app store is built on Malaysia-based Infindo's white-label store

called the Polygon White Label Platform.

In July 2013, MTN Nigeria, the largest telecom in Nigeria, opened

their NextApps store, which is running on top of US-based neXva's

white-label store platform.

Telecoms with direct carrier billing agreements are now viable competitors to credit card companies across the globe, even in developed economies.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 13

In July 2012, VimpleCom's Telecel announced a direct billing agreement

with Google that will allow subscribers in Algeria and Zimbabwe to

purchase content in Google Play and get billed by the carrier. In February

2013, VimpelCom announced a similar direct billing agreement for Algeria

and Zimbabwe with Microsoft and Nokia.

Direct carrier billing is already integrated with Nokia's app store by 145

telecoms across 52 countries across the globe. In March 2013, Airtel and

Nokia announced a direct billing agreement starting with Airtel subscribers

in Nigeria and Kenya. Airtel reported that they would expand the service

"across Africa" starting with East Africa.

In June 2013, Nokia announced a direct billing arrangement with Vodacom

allowing Windows Phone users in South Africa to buy apps via the device

and have the charge applied to their monthly bill. Vodacom has a similar

agreement with BlackBerry and Google.

Leapfrogging the Digital Divide In Africa

"Operators are already reporting that they are shipping more

smartphones than feature phones. In the process, many

Africans are gaining access to services such as social

networking, the web, and email for the first time. Africa will

leapfrog the PC era to the mobile, post-PC world."

Aidan Baigrie, Head of Business Development at SEACOM

October 2012

Mobile devices are now the primary computing devices used by consumers

in many countries in Africa. At GSMA's Connected Living event in June

2013, Kristin Atkins, Senior Director at Qualcomm, said "For many, the first

and only computing experience will be mobile."

According to the Nigerian Communications Commission (NCC), over 32

million Nigerians were accessing the web via their mobile devices by

February 2013. What is more interesting is that the NCC reports that the

number of mobile web users is now growing by an average of 1.4 million

people every 60 days.

At the current growth rate, over 40 million Nigerians will be accessing the

web on their mobile devices by the end of 2013. By the end of the forecast

period, over 100 million people will access the web in Nigeria via a mobile

device, far outstripping PC access.

In Uganda, over 90% of the access to the Internet is via mobile devices,

making the web experience a quintessentially mobile experience for users

in that country.

Mobile users in African countries are quite advanced in the use of mobile

technology for a variety of things that are still quite rare in developed

In South Africa, over 70% of all mobile users and 85% of high school and higher education students use their phones to access the web.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 14

economies. Africans now use their devices for banking, payrolls,

healthcare, everyday purchases (like bus fare), agriculture, and social

media (the largest social media network in Africa is the mobile Mxit

platform.) In December 2012, Riitta Vänskä, Senior Manager in Nokia's

Mobile Learning Group, said "Mobile phones are now the laptops of Africa."

Mobile banking is widespread in Africa on a scale that dwarfs usage in other

regions. The World Bank reports that 15 of the 20 countries with the

highest percentages of mobile banking usage are in Africa. By May 2013,

Uganda had over nine million mobile money users, triple from the year

before.

According to an August 2013 report by the GSMA, over 23 million mobile

subscribers (74% of the population) in Kenya use mobile banking. By far,

this is the highest usage of mobile banking in the world.

Africa has become the proving ground for Mobile Healthcare (mHealth)

initiatives with over 95 active programs operating across the region at the

end of 2012, more than anywhere else in the world. The mHealth

initiatives in Africa are concentrated in Kenya and Uganda.

Large rural populations across Africa are now avid users of Mobile Learning

technology, while relatively few have experienced Self-paced eLearning on

a PC. In developing economies, PC penetration is often low, yet mobile

subscriptions are quite high. Mobile Learning suppliers are targeting the

mobile device as the delivery platform of choice in those economies.

Six of the fourteen countries analyzed in this report had mobile penetration

rates over 100% by the end of 2012. By the end of 2013, three more

countries will also have over 100%.

In stark contrast, none of the fourteen countries analyzed in this report had

a PC-based Internet penetration rate above 50% as of August 2013. Half

had PC-based Internet penetration rates below 25%.

Africa has the highest mobile growth rate in the world and by the end of

the forecast period, all fourteen countries analyzed in this report

will have mobile penetration rates well above 100%. Virtually all of

those subscribers will be using smartphones and tablets.

In many countries in Africa, accessing the web on an Internet-enabled

feature phone or a smartphone is often a user's first Internet experience, in

what is often referred to as a Post-PC experience. In this scenario, Mobile

Learning is their primary learning technology and they may never be

exposed to other learning products.

By the end of 2012, four countries in Africa (Kenya, Uganda, Tanzania, and

Mozambique) were spending more on Mobile Learning than on Self-paced

Learning. By the end of 2013, six more countries will join the ranks with

Nigeria, Ghana, Rwanda, Zimbabwe, Zambia, and Senegal also spending

more on Mobile Learning than on eLearning.

Ten of the fourteen countries in Africa analyzed in this

report will be spending more on Mobile Learning than on eLearning by the end of 2013.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 15

In the developed economies, Mobile Learning is often seen as a disruptive

learning technology, particularly in the consumer and academic segments.

It is ostensibly disrupting the legacy PC-based Self-paced eLearning

industry. This is referred to as "product substitution" in market research.

Buyers in Africa are not substituting Mobile Learning for Self-paced

eLearning, they are leapfrogging eLearning altogether.

In light of the extraordinary adoption of mobile technology across all

sectors in Africa and the rapid growth of the middle class, African thought

leaders now bristle about the persistent myths of a digital divide in Africa,

still perpetuated by many outside the continent.

In July 2013, SEACOM's Suveer Ramdhani said, "Talk about ‘bridging the

digital divide’ has become clichéd and patronizing. Africans have access to

smart phones and know how to use them. Combine this with the rise of

new broadband communications technologies such as long term evolution

(LTE) for high-speed mobile connectivity and there is no reason that Africa

should not leap straight into the post-PC era.”

What You Will Find in This Report This report identifies the countries with the highest uptake of Mobile

Learning and identifies the major buying segments and the types of

products they buy. This will help suppliers compete in the right segment

with products in the highest demand.

There are two sections in this report: a demand-side analysis and a supply-

side analysis. In the demand-side analysis, a detailed breakout of revenue

forecasts is included for fourteen countries in Africa. The supply-side

section breaks out the addressable revenues for five Mobile Learning

product types across the region (for all countries combined).

All revenues in this report are in $US dollars based on the exchange rate

for each country's currency as of May 2013.

Who is the Buyer?

In the current market, the two major buying segments across Africa are

the consumer and academic segments. Mobile Learning adoption is just

starting to expand into the other buying segments, with the highest growth

rates in the healthcare and NGO segments.

Consumers in Africa will account for the majority of expenditures on Mobile

Learning throughout the forecast period. Consumers buy educational apps

and subscribe to Mobile Learning VAS products. Academic institutions are

just starting to adopt Mobile Learning. By 2017, the expenditures made by

the combined academic segments (PreK-12 and higher education) will be

on par with consumers spending.

The consumer buying behaviors in each of the countries analyzed in this report are quite different. This report identifies the

mobile educational apps in the highest demand in each country.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 16

In the 2012 market, private academic institutions were more likely than

public institutions to purchase Mobile Learning products. This will change

over the forecast period as major digitization and tablet adoption efforts

roll out across the public schools in the region. Public schools systems in

the region are administered by government agencies, and while the

government is the actual buyer, this report categorizes those expenditures

as PreK-12 spending.

Except for telecom companies and commercial language learning

companies that buy Mobile Learning products and services to meet the

needs of their customers, there is very little adoption of Mobile Learning for

corporate training across the region. This mirrors the weak corporate

adoption of the product type found in other regions.

Governments, NGOs, and non-profit foundations are starting to deploy

custom mobile content for literacy, human rights, cultural heritage, civics,

health and wellness, public safety, and agro-information. They hire content

suppliers to develop educational apps for their constituents.

What Are They Buying?

This report identifies the revenue opportunities across the region for five

product types. The supply-side section provides revenue forecasts for five

types of Mobile Learning products and services including:

Packaged content and educational apps

Value added services (VAS)

Custom content development services

Authoring tools and platforms

Personal learning devices

Mobile Learning VAS products will generate the highest revenues in Africa

throughout the forecast period. This is due in large part to the Leapfrog

Effect. Africa has the highest growth rate in the world for Mobile

Learning VAS.

Content suppliers competing in Africa have to know the primary languages

of education and training used in the schools, government, and business.

Consumer-facing suppliers also need to understand the language patterns

in each country. They are different in every country analyzed in this report.

This report identifies the official languages, the language of instruction in

the schools, and the major languages in use in terms of the percent of the

population that speak those languages.

There are two Lusophone (Portuguese-speaking) countries analyzed in this

report. English is the primary language of instruction in eight African

countries covered in this report. Yet, it is rarely that simple in Africa.

Many countries in Africa have several official languages. For example,

South Africa has eleven official languages and Zimbabwe has three official

All of the Mobile Learning product types have healthy growth rates in Africa. Four of the five products have growth rates above 30%.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 17

languages. Even in the presence of large populations that speak indigenous

languages, many countries have mandated the use of French or English as

the official language of instruction in the schools. In some African

countries, the official language of instruction is different in the PreK-12

schools and in the higher education institutions.

Even in countries that mandate French or English as the language of

instruction, the language used in the early grades is often an indigenous

language, depending on the location of the schools, with French or English

instruction starting in about fourth grade. This is one factor contributing to

the emergence of new domestic firms that are better suited (compared to

international suppliers) to develop digital content in the local languages.

This report identifies the language parameters for each of the countries

analyzed in this report.

In Tanzania, the government mandates that Swahili be used as the

language of instruction in public primary schools and government-

sponsored adult education centers. However, English is the official

language of instruction in Tanzanian public secondary schools and

universities.

In general, there is a strong consumer demand for early childhood learning

and language learning apps in most African countries. Brain training apps

are popular in several African countries analyzed in this report.

What is interesting is the unique app buying behaviors in each country. No

two countries analyzed in this report exhibit the same consumer buying

patterns. For example, the language learning apps in demand differ from

country to country.

This report identifies the specific types of education apps that

generate the highest revenues in each country.

There is a significant demand for custom content development services in

the region, particularly in the public and private academic segments.

This report includes the forecasts for Mobile Learning content developed for

several types of handheld devices including:

Dedicated handheld gaming devices

Mobile phones (feature phones and smartphones)

Personal media players (PMPs)

Tablets and slates

Mobile clinical assistants

eReaders

Personal learning devices (PLDs) designed solely for learning

and performance support

Personal learning devices are a new distribution channel for

educational publishers and packaged content suppliers. All of the

African personal learning device suppliers are identified in this

report.

There are 31 Francophone (French-speaking) countries in Africa; over 115 million people speak French on the continent.

Ambient Insight’s The 2012-2017 Africa Mobile Learning Market: Regional Edition

For more information about this research, email: [email protected] 18

In essence, these are dedicated educational tablets. The devices are

attractive to consumers (parents) and academic buyers because they are:

Designed solely for education

Preloaded with vetted educational content

Priced significantly lower than general-purpose tablets

Personal learning devices (PLDs) are increasingly popular in Africa. There is

a burgeoning middle class across Africa and consumer demand for the

PLDS is beginning to mirror other regions around the world with large

middle class populations where consumers are avid buyers.

Over 130 suppliers operating in specific countries in Africa are cited in this

report. This will help international suppliers identify local partners,

distributors, resellers, and potential merger and acquisition (M&A) targets.

Targeting specific buyers in particular countries with particular product

types is the key to generating revenues in Africa. Ambient Insight provides

a description of how we categorize product types in Ambient Insight’s 2013

Learning Technology Research Taxonomy.

Related Research Buyers of this report may also benefit by the following Ambient Insight

market research:

The Africa Market for Self-paced Learning Products and Services: 2012-

2017 Forecast and Analysis (Regional Edition)

The Africa Market for Digital English Language Learning Products and

Services: 2011-2016 Forecast and Analysis (Regional Edition)

Ambient Insight’s 2013 Learning Technology Research Taxonomy

“We Put Research into Practice”

www.ambientinsight.com

Very few PLD suppliers develop their own digital content. Most of the personal learning device suppliers collaborate with third-party

education publishers for content.