Embed Size (px)

Citation preview

An Empirical Note on the Independence of Technology and Financial StructureAuthor(s): Gordon AndersonSource: The Canadian Journal of Economics / Revue canadienne d'Economique, Vol. 23, No. 3(Aug., 1990), pp. 693-699Published by: Wiley on behalf of the Canadian Economics AssociationStable URL: http://www.jstor.org/stable/135655 .

Accessed: 16/06/2014 21:54

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

Wiley and Canadian Economics Association are collaborating with JSTOR to digitize, preserve and extendaccess to The Canadian Journal of Economics / Revue canadienne d'Economique.

http://www.jstor.org

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

An empirical note on the independence of technology and financial structure

GORDON ANDERS ON University of Toronto

I. INTRODUCTION

Rarely in the empirical literature on capital fornmation or finance is the possibility of a relationship between a firms financing structure and its technology admitted. In the former (see, e.g., Nickell 1978, chap. 11) financial structure is generally assumed exogenous with respect to the investment equation. In the latter, with few exceptions (see, e.g., Auerbach 1985; Gordon, Hines, and Summers 1986), firm technology is ignored in modelling financial structure. This is not surprising, given the array of theorems since Modigliani and Miller (1958) which, under suitable conditions (usually the existence of perfect capital markets, and the absence of tax wedges and bankruptcy), establish the separability of real and financial decisions.

Recently, alternative finance theories have suggested links between technology and financial structure (see, e.g., Summers 1986, Smith and Warner 1979, Scott 1976 for collateral-oriented arguments; Boadway, Bruce, and Mintz 1984, Daly et al. 1985, King 1974, Auerbach and King 1983, and Meyer 1983 for tax-related arguments; Easterbrook 1984 and Rozeff 1982 for agency cost arguments; and Bhattacharya 1979 and Lintner 1956 for signalling arguments), though this impli- cation has not been examined empirically. The matter is of concern, since corporate tax policy generally discriminates between finance sources (contradicting the no-tax wedge assumption), and a relationship between technology and financial structure would result in such policies' having distortionary effects on the choice of factor mix.

This note examines whether these issues can continue to be ignored in empirical models in this area. Anderson (1989) establishes the statistical dependence of the firm's capital stock and tax status on its (assumed exogenous) financial structure. Here the validity of the exogenous financial structure assumption is examined via simple reduced form tests. A structural model discriminating between the various

This work has been pursued as part of a contract with the Social and Economic Studies Division of Statistics Canada. Many thanks are due to two referees for their helpful comments and to Normand Lavoy for his dilligent research assistance. Helpful discussions with Brian Murphy and Michael Wolfson are much appreciated as are discussions with my colleagues in the research seminars at McMaster University and the Institute of Fiscal Studies, London, England. Naturally all opinions and errors herein are the sole responsibility of the author.

Canadian Journal of Economics Revue canadienne d'Economique, XXII, No. 3 August aoat 1990. Printed in Canada Imprime au Canada

0008-4085 / 90 / 693-699 $1.50 " Canadian Economics Association

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

694 Gordon Anderson

theories referred to above is not developed, since it is not clear that they are individually identifiable; rather, the issue addressed is whether their total impact is small enough to be ignored.

II. THE DATA, MODEL, AND RESULTS.

The hypothesis of interest is that, given firm-specific effects, financial structure is independent of factor inputs. The data are those recorded by fimis on Revenue Canada's Financial Analysis Data Card in 1982; a random sample of 4,917 firms was employed. Three basic financing sources are identified: short-term debt, long- term debt, and all other sources (predominantly equity), which are characterized by the respective ratios of short- and long-term debt to total liabilities and one minus their sum. These are an approximation, since the equity measure fails to accommodate market valuation, which tends to understate the equity component. Internal financing is represented by the retentions to revenue ratio, which was chosen over the retentions to after-tax profits ratio, since the denominator in the latter is zero for many observations.

Firm location, legal status, and industrial classification are assumed exogenous for this exercise. Including all tax parameters would yield no explanatory power, since they are constant across firms. On the other hand, firm-specific tax variables vary with tax status, which in turn depends upon technology and financial structure (see Anderson 1989), rendering them endogenous and hence inappropriate condi- tioning variables. Thus the null hypothesis for fj, the share in firm n's financing of the jth financing instrument (or its retention to revenue ratio) may be represented by the following reduced form equation:

T L R

fjn = 1jO + Z OIjtItn + E OjlIln + E OjrIrn + Ujn; 1, 2, 3, (1) t=1 1=1 r=1

where

tn = 1 if firm n is in industry t = 0 otherwise.

Iln = 1 if firm n is of legal entity type 1 = 0 otherwise.

Irn = 1 if firm n is in province r = 0 otherwise.

ujn is independent identically distributed white noise

Given the same explanatory variables in each equation, ordinary least squares is efficient. Since the three financing ratios sum to one, only two of them are inde- pendent; the third, and its associated parameters, may be deduced with probability one from the data and the adding-up conditions (see Anderson and Blundell 1982). Furthermore, for this sample, some firms had no short-term and others no long-term debt; hence Tobit regression techniques (see Maddala 1983) were employed.

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

Independence of technology 695

To characterize firm technology with the available data the ratio of expenditure on materials to total revenue is utilized to reflect the materials and energy input; the ratio of salaries, wages, and benefits to total revenue reflects the labour input; and the ratio of repairs and maintenance expenditures to total revenue reflects the capital input. With the exception of capital, these ratios correspond to the dependent variables in a direct translog representation of factor demands (see Berndt and Christensen 1974). The correct capital variable, if it were available, would be open to concerns of spurious correlation, since the cost of capital is a function of the returns to various sources of finance; thus the measure employed here may be viewed as an instrument. This variable too is potentially endogenous, since, in the presence of credit rationing, firms may well cut back on repairs and maintenance disproportionately to other factors. However, relative to the marginal financing source, its correlation as a consequence of this effect is likely to be, and is assumed to be, very small. The corresponding reduced-form equations for the technology ratios Wmn is

T L R

Wmn = rmO + 1 'rmtltn + >rmlIln + > 'rmrlrn + Vmn; m - 1, 2, 3, (2) t=1 1=1 r=1

where Itn, Iln and Irn are defined as before and Vmn is independent identically distributed white noise.

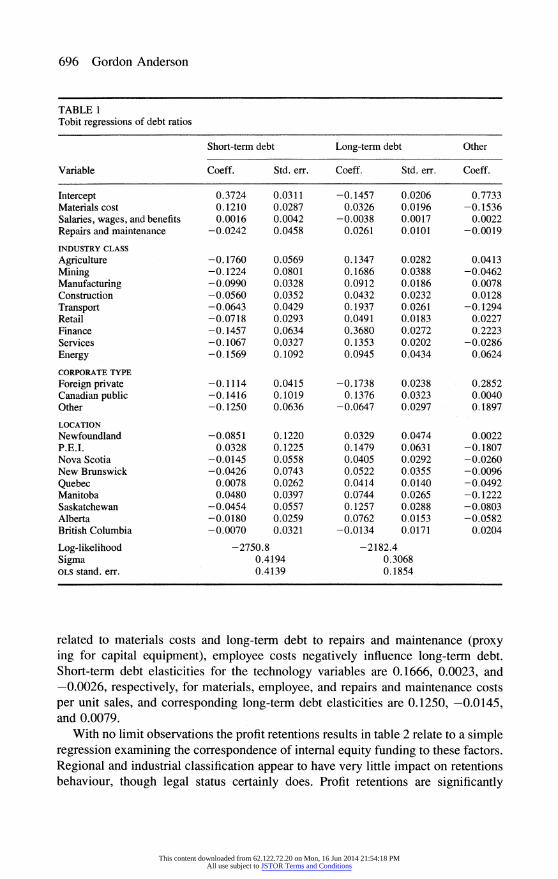

Including the residuals from (2) in (1) would present a standard test of the weak exogeneity of technology with respect to the financing structure (see Engle, Hendry and Richard 1983). That they are included implicitly by including only the dependent variables from (2) in (1) derives from least squares, theory and the fact that identical sets of instruments appear in both systems of equations. Table 1 records the parameter estimates for the corresponding Tobit regressions of (1), including as explanatory variables expenditure shares described in (2).

The base company, given the dummy variable structure, is a private Canadian wholesale company located in Ontario. The first four columns of table 1 relate to the coefficients and standard errors from Tobit regressions of the proportions to total liabilities of short-term and long-term debt, the fifth column represents the parameters implied by the adding-up conditions for the non-debt financing instruments. The difference between sigma (an estimate of the standard error of the equation) and the standard error of the ordinary least squares equation (used to start the iterative process) reflects the impact the zero observations have in the Tobit estimates. The few limit observations in the short-term debt equations had little effect, whereas the larger numbers in the long-term debt equation have considerable impact.

The results suggest that location has no impact on the relative level of short-term debt, while that of industrial and legal status is limited. Industrial classification, legal status, and location all affect long-term debt. Relative to the base, all corporate and industrial classifications carry less short-term debt and, apart from foreign private and public firms, carry more long-term debt. Short-term debt is positively

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

696 Gordon Anderson

TABLE 1 Tobit regressions of debt ratios

Short-term debt Long-term debt Other

Variable Coeff. Std. err. Coeff. Std. err. Coeff.

Intercept 0.3724 0.0311 -0.1457 0.0206 0.7733 Materials cost 0.1210 0.0287 0.0326 0.0196 -0.1536 Salaries, wages, and benefits 0.0016 0.0042 -0.0038 0.0017 0.0022 Repairs and maintenance -0.0242 0.0458 0.0261 0.0101 -0.0019

INDUSTRY CLASS

Agriculture -0.1760 0.0569 0.1347 0.0282 0.0413 Mining -0.1224 0.0801 0.1686 0.0388 -0.0462 Manufacturing -0.0990 0.0328 0.0912 0.0186 0.0078 Construction -0.0560 0.0352 0.0432 0.0232 0.0128 Transport -0.0643 0.0429 0.1937 0.0261 -0.1294 Retail -0.0718 0.0293 0.0491 0.0183 0.0227 Finance -0.1457 0.0634 0.3680 0.0272 0.2223 Services -0.1067 0.0327 0.1353 0.0202 -0.0286 Energy -0.1569 0.1092 0.0945 0.0434 0.0624

CORPORATE TYPE

Foreign private -0.1114 0.0415 -0.1738 0.0238 0.2852 Canadian public -0.1416 0.1019 0.1376 0.0323 0.0040 Other -0.1250 0.0636 -0.0647 0.0297 0.1897

LOCATION

Newfoundland -0.0851 0.1220 0.0329 0.0474 0.0022 P.E.I. 0.0328 0.1225 0.1479 0.0631 -0.1807 Nova Scotia -0.0145 0.0558 0.0405 0.0292 -0.0260 New Brunswick -0.0426 0.0743 0.0522 0.0355 -0.0096 Quebec 0.0078 0.0262 0.0414 0.0140 -0.0492 Manitoba 0.0480 0.0397 0.0744 0.0265 -0.1222 Saskatchewan -0.0454 0.0557 0.1257 0.0288 -0.0803 Alberta -0.0180 0.0259 0.0762 0.0153 -0.0582 British Columbia -0.0070 0.0321 -0.0134 0.0171 0.0204

Log-likelihood -2750.8 -2182.4 Sigma 0.4194 0.3068 OLS stand. err. 0.4139 0.1854

related to materials costs and long-term debt to repairs and maintenance (proxy ing for capital equipment), employee costs negatively influence long-term debt. Short-term debt elasticities for the technology variables are 0.1666, 0.0023, and -0.0026, respectively, for materials, employee, and repairs and maintenance costs per unit sales, and corresponding long-term debt elasticities are 0.1250, -0.0145, and 0.0079.

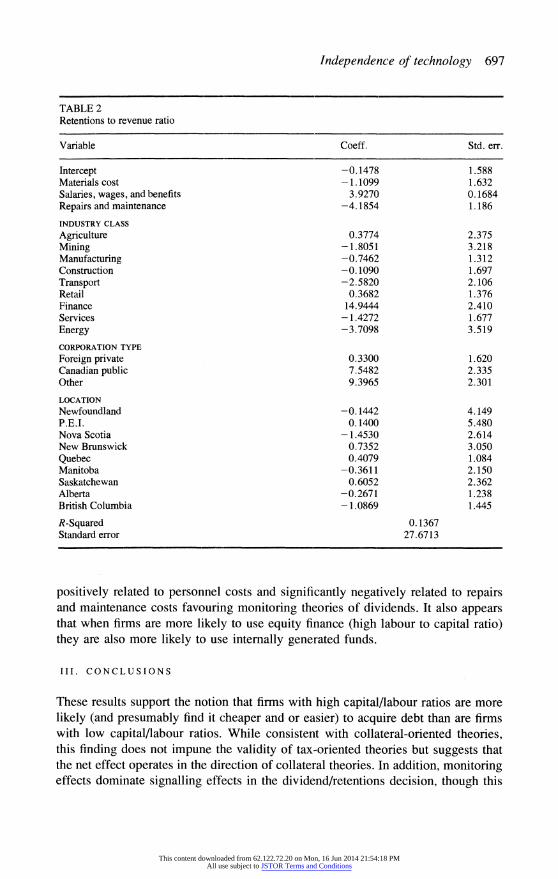

With no limit observations the profit retentions results in table 2 relate to a simple regression examining the correspondence of internal equity funding to these factors. Regional and industrial classification appear to have very little impact on retentions behaviour, though legal status certainly does. Profit retentions are significantly

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

Independence of technology 697

TABLE 2 Retentions to revenue ratio

Variable Coeff. Std. err.

Intercept -0.1478 1.588 Materials cost -1.1099 1.632 Salaries, wages, and benefits 3.9270 0.1684 Repairs and maintenance -4.1854 1.186

INDUSTRY CLASS

Agriculture 0.3774 2.375 Mining -1.8051 3.218 Manufacturing -0.7462 1.312 Construction -0.1090 1.697 Transport -2.5820 2.106 Retail 0.3682 1.376 Finance 14.9444 2.410 Services -1.4272 1.677 Energy -3.7098 3.519

CORPORATION TYPE

Foreign private 0.3300 1.620 Canadian public 7.5482 2.335 Other 9.3965 2.301

LOCATION

Newfoundland -0.1442 4.149 P.E.I. 0.1400 5.480 Nova Scotia -1.4530 2.614 New Brunswick 0.7352 3.050 Quebec 0.4079 1.084 Manitoba -0.3611 2.150 Saskatchewan 0.6052 2.362 Alberta -0.2671 1.238 British Columbia -1.0869 1.445

R-Squared 0.1367 Standard error 27.6713

positively related to personnel costs and significantly negatively related to repairs and maintenance costs favouring monitoring theories of dividends. It also appears that when firms are more likely to use equity finance (high labour to capital ratio) they are also more likely to use internally generated funds.

III. CONCLUSIONS

These results support the notion that firms with high capital/labour ratios are more likely (and presumably find it cheaper and or easier) to acquire debt than are firms with low capital/labour ratios. While consistent with collateral-oriented theories, this finding does not impune the validity of tax-oriented theories but suggests that the net effect operates in the direction of collateral theories. In addition, monitoring effects dominate signalling effects in the dividend/retentions decision, though this

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

698 Gordon Anderson

does not imply that the latter are not present in the data. This evidence suggests significant relationships between technological factors and financial structure and has substantial implications for policy, since, given the current tax preference ac- corded debt and capital equipment, labour-intensive commercial activity appears doubly disadvantaged through employing less capital and having less access to tax-preferred financing instruments. Indeed modeling financial and real decisions independently appears to be a hazardous if not misleading exercise. This issue is worthy of further investigation in the context of a structural model that examines more explicitly links between the monitoring, signalling, collateral, and taxation effects on corporate financial structure and is critical for any cogent debate on corporate tax policy.

REFERENCES

Anderson, G.J. (1989) 'Is the cost of capital really independent of the level of investment and the financial structure of the firm?' Mimeo

Anderson, G.J. and R.W. Blundell (1982) 'Estimation and hypothesis testing in dynamic singular equation systems.' Econometrica 50, 1559-72

Auerbach, A.J. (1985) 'Taxes, firm financial policy and the cost of capital: an empirical analysis.' Journal of Public Economics 23, 27-58

Auerbach, A.J. and M.A. King (1983) 'Taxation, portfolio choice and debt-equity ratios: a general equilibrium model.' Quarterly Journal of Economics 97, 587-609

Berndt, E. and L.R. Christensen (1974) 'Testing for the existence of a consistent aggregate index of labour inputs.' American Economic Review 64, 391-403

Bhattacharya, S. (1979) 'Imperfect information, dividend policy and the "bird in the hand" fallacy.' Bell Journal of Economics 259-70

Boadway, R., N. Bruce, and J. Mintz (1984) 'Taxation, inflation, and the effective marginal tax rate on capital in Canada.' This JOURNAL 17, 62-79

Daly M., J. Jung, P. Mercier, and Thomas Schweitzer (1985) 'A comparison of effective marginal tax rates on income from capital in Canadian manufacturing.' Canadian Tax Journal 1155-92

Easterbrook, F. H. (1984) 'Two agency-cost explanations of dividends.' American Eco- nomic Review 74, 225-38

Engle, R.F., D.F. Hendry, and J.-F. Richard (1983) 'Exogeneity' Econometrica 51, 277- 304

Gordon, R.H., J.R. Hines, Jr., and L.H. Summers (1986) 'Notes on the tax treatment of firms.' Harvard Institute of Economic Research Discussion Paper No. 1239

King, M.A. (1974) 'Taxation and the cost of capital.' Review of Economic Studies 21-35 Lintner, J. (1956) 'Distribution of incomes of corporations among dividends, retained

earnings and taxes.' American Economic Review 46, 97-113 Maddala, G.S. (1983) Limited-Dependent and Qualitative Variables in Econometrics

(Cambridge: Cambridge University Press) Meyer, C. (1986) 'Corporation tax, finance and the cost of capital' Review of Economic

Studies 93-112 Modigliani, F. and M.H. Miller (1958) 'The cost of capital, corporation finance and the

theory of investment.' American Economic Review 48, 655-69 Nickell, S.J. (1978) The Investment Decisions of Firms (Cambridge: Cambridge University

Press) Rozeff, M.S. (1982) 'Growth, beta and agency costs as determinants of dividend payout

ratios.' Journal of Financial Research 5, 249-59

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions

Independence of technology 699

Scott, J.H. (1976) 'A theory of optimal capital structure.' Bell Journal of Economics 33-54

Smith, C. and J.B. Warner (1979) 'On financial contracting: an analysis of bond covenants.' Journal of Financial Economics 117-61

Summers L. (1986) 'Investment incentives and the discounting of depreciation al- lowances.' National Bureau of Economic Research Working Paper No. 1941

This content downloaded from 62.122.72.20 on Mon, 16 Jun 2014 21:54:18 PMAll use subject to JSTOR Terms and Conditions