Embed Size (px)

Citation preview

7/29/2019 ANZ Commodity Daily 764 250113.pdf

http://slidepdf.com/reader/full/anz-commodity-daily-764-250113pdf 1/5

ANZ RESEARCH

COMMODITY DAILY Contacts: Mark Pervan +613 9273 3716 | [email protected] Nick Trevethan +65 6681 6714 | [email protected]

Natalie Rampono +613 9273 3415 | [email protected]

MARKET HI GHLI GHTS COMMODI TY WRAP J anua r y 25 , 2013

• Oil p r i c es r ose on imp r ov ed g loba l manu fac tu r i ng da ta

• Gold fe l l on reduced sa fe-haven p lays

• Coppe r r ange - bound des p i te im p r ov ed f l as h P MI ’ s

• B u lk s up on pos i t i v e Ch ina P MI and s upp l y d i s r up t i ons

KEY THEMES

y Ov er n igh t themes – Commodities were mostly supported by

Chinese and US flash PMI’s. China’s flash HSBC manufacturing

PMI surprised on the upside yesterday at 51.9 (mkt: 51.7).

The preliminary reading for the output index rose to 52.2, a

22-month high. The ANZ inventory pulse measure remains

high signalling a positive outlook for future activity, although

some consolidation is likely in the near-term. The Markit US

PMI for January rose to 56, growing at the fastest pace in

nearly two years and is well above the 50 point level that

indicates sector expansion. Low US jobless claims also added

to the view the US economy remains on its recovery track.

The US Dow Jones Industrial average closed 0.3% higher andis just 0.5% below the record high reached in Q3 2007.

European stocks were up 0.5-1.0% on a strong preliminary

German PMI, with factories expanding at their strongest pace

in 12 months. Markets shrugged off France’s Flash PMI

reading, indicating an economy falling deeper into recession.

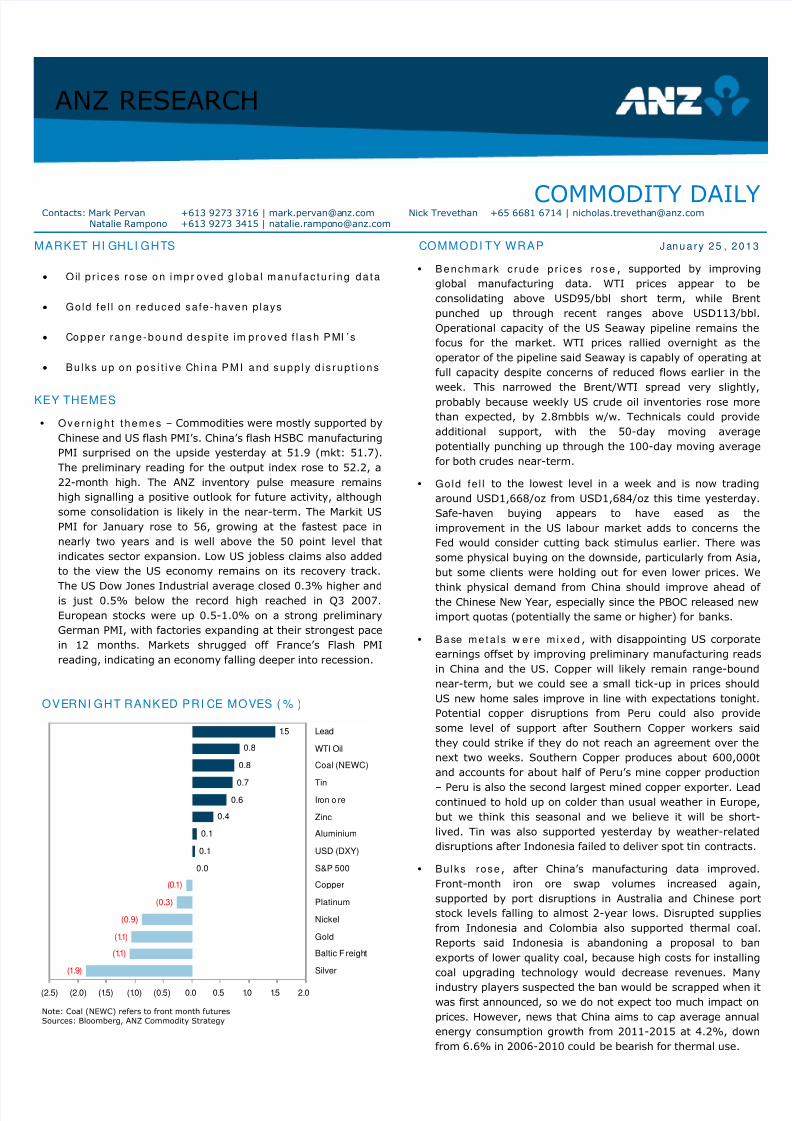

OVERNI GHT RANKED PRI CE MOVES ( % )

(1.9)

(1.1)

(1.1)

(0.9)

(0.3)

(0.1)

0.0

0.1

0.1

0.4

0.60.7

0.8

0.8

1.5

(2.5) (2.0) (1.5) (1.0) (0.5) 0.0 0.5 1.0 1.5 2.0

Silver

Baltic F reight

Gold

Nickel

Platinum

Copper

S&P 500

USD (DXY)

Aluminium

Zinc

Iron o reTin

Coal (NEWC)

WTI Oil

Lead

Note: Coal (NEWC) refers to front month futures

Sources: Bloomberg, ANZ Commodity Strategy

y B enc hmar k c r ude p r i c es r os e , supported by improving

global manufacturing data. WTI prices appear to be

consolidating above USD95/bbl short term, while Brent

punched up through recent ranges above USD113/bbl.

Operational capacity of the US Seaway pipeline remains the

focus for the market. WTI prices rallied overnight as the

operator of the pipeline said Seaway is capably of operating at

full capacity despite concerns of reduced flows earlier in the

week. This narrowed the Brent/WTI spread very slightly,

probably because weekly US crude oil inventories rose more

than expected, by 2.8mbbls w/w. Technicals could provide

additional support, with the 50-day moving average

potentially punching up through the 100-day moving average

for both crudes near-term.

y Gold fe l l to the lowest level in a week and is now trading

around USD1,668/oz from USD1,684/oz this time yesterday.

Safe-haven buying appears to have eased as the

improvement in the US labour market adds to concerns the

Fed would consider cutting back stimulus earlier. There was

some physical buying on the downside, particularly from Asia,

but some clients were holding out for even lower prices. We

think physical demand from China should improve ahead of the Chinese New Year, especially since the PBOC released new

import quotas (potentially the same or higher) for banks.

y B ase me ta l s w e r e m ix ed , with disappointing US corporate

earnings offset by improving preliminary manufacturing reads

in China and the US. Copper will likely remain range-bound

near-term, but we could see a small tick-up in prices should

US new home sales improve in line with expectations tonight.

Potential copper disruptions from Peru could also provide

some level of support after Southern Copper workers said

they could strike if they do not reach an agreement over the

next two weeks. Southern Copper produces about 600,000t

and accounts for about half of Peru’s mine copper production

– Peru is also the second largest mined copper exporter. Leadcontinued to hold up on colder than usual weather in Europe,

but we think this seasonal and we believe it will be short-

lived. Tin was also supported yesterday by weather-related

disruptions after Indonesia failed to deliver spot tin contracts.

y Bulks rose, after China’s manufacturing data improved.

Front-month iron ore swap volumes increased again,

supported by port disruptions in Australia and Chinese port

stock levels falling to almost 2-year lows. Disrupted supplies

from Indonesia and Colombia also supported thermal coal.

Reports said Indonesia is abandoning a proposal to ban

exports of lower quality coal, because high costs for installing

coal upgrading technology would decrease revenues. Many

industry players suspected the ban would be scrapped when it

was first announced, so we do not expect too much impact on

prices. However, news that China aims to cap average annual

energy consumption growth from 2011-2015 at 4.2%, down

from 6.6% in 2006-2010 could be bearish for thermal use.

7/29/2019 ANZ Commodity Daily 764 250113.pdf

http://slidepdf.com/reader/full/anz-commodity-daily-764-250113pdf 2/5

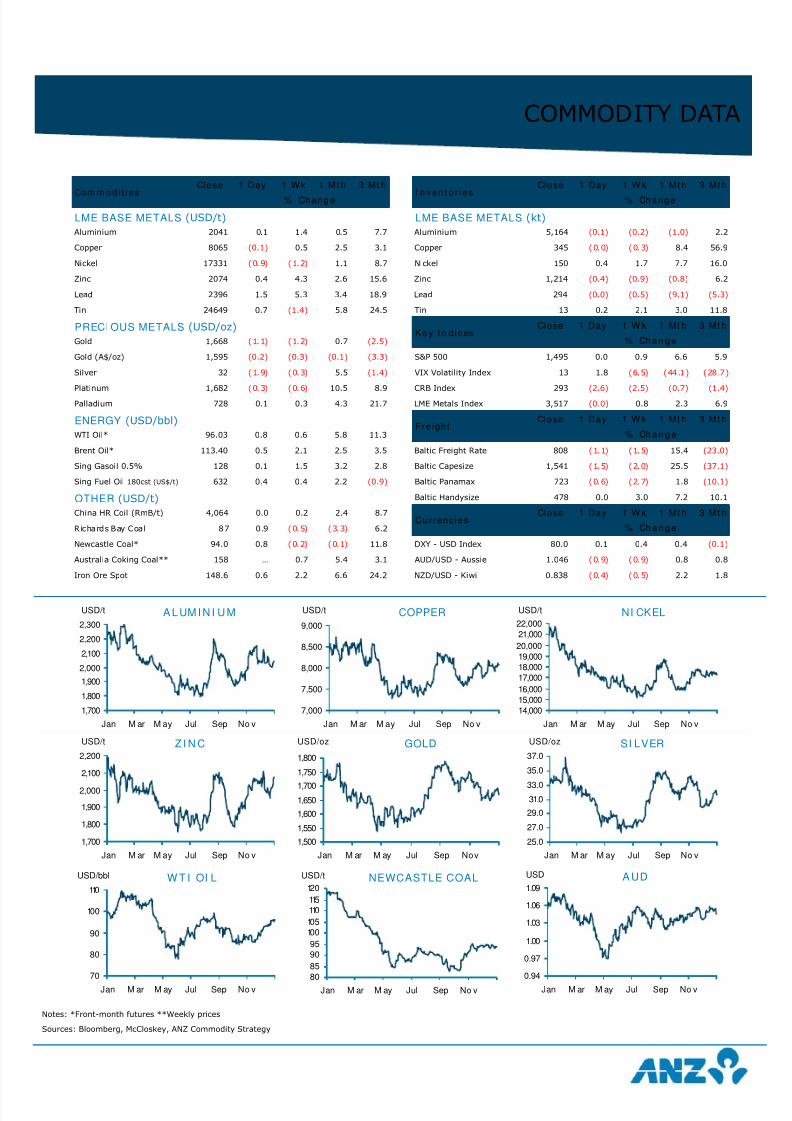

COMMODITY DATA

Close 1 Day 1 W k 1 Mt h 3 Mt h Close 1 Day 1 W k 1 Mt h 3 Mt h

LME BASE METALS (USD/t) LME BASE METALS (kt)

Aluminium 2041 0.1 1.4 0.5 7.7 Aluminium 5,164 (0.1) (0.2) (1.0) 2.2

Copper 8065 (0.1) 0.5 2.5 3.1 Copper 345 (0.0) (0.3) 8.4 56.9

Nickel 17331 (0.9) (1.2) 1.1 8.7 Nickel 150 0.4 1.7 7.7 16.0

Zinc 2074 0.4 4.3 2.6 15.6 Zinc 1,214 (0.4) (0.9) (0.8) 6.2

Lead 2396 1.5 5.3 3.4 18.9 Lead 294 (0.0) (0.5) (9.1) (5.3)

Tin 24649 0.7 (1.4) 5.8 24.5 Tin 13 0.2 2.1 3.0 11.8

PRECI OUS METALS (USD/oz) Close 1 Day 1 W k 1 Mt h 3 Mt h

Gold 1,668 (1.1) (1.2) 0.7 (2.5)

Gold (A$/oz) 1,595 (0.2) (0.3) (0.1) (3.3) S&P 500 1,495 0.0 0.9 6.6 5.9

Silver 32 (1.9) (0.3) 5.5 (1.4) VIX Volatility Index 13 1.8 (6.5) (44.1) (28.7)

Platinum 1,682 (0.3) (0.6) 10.5 8.9 CRB Index 293 (2.6) (2.5) (0.7) (1.4)

Palladium 728 0.1 0.3 4.3 21.7 LME Metals Index 3,517 (0.0) 0.8 2.3 6.9

ENERGY (USD/bbl) Close 1 Day 1 W k 1 Mt h 3 Mt h

WTI Oil* 96.03 0.8 0.6 5.8 11.3

Brent Oil* 113.40 0.5 2.1 2.5 3.5 Baltic Freight Rate 808 (1.1) (1.5) 15.4 (23.0)

Sing Gasoil 0.5% 128 0.1 1.5 3.2 2.8 Baltic Capesize 1,541 (1.5) (2.0) 25.5 (37.1)

Sing Fuel Oil 180cst (US$/t) 632 0.4 0.4 2.2 (0.9) Baltic Panamax 723 (0.6) (2.7) 1.8 (10.1)

OTHER (USD/t) Baltic Handysize 478 0.0 3.0 7.2 10.1

China HR Coil (RmB/t) 4,064 0.0 0.2 2.4 8.7 Close 1 Day 1 W k 1 Mt h 3 Mt h

Richards Bay Coal 87 0.9 (0.5) (3.3) 6.2

Newcastle Coal* 94.0 0.8 (0.2) (0.1) 11.8 DXY - USD Index 80.0 0.1 0.4 0.4 (0.1)

Australia Coking Coal** 158 … 0.7 5.4 3.1 AUD/USD - Aussie 1.046 (0.9) (0.9) 0.8 0.8

Iron Ore Spot 148.6 0.6 2.2 6.6 24.2 NZD/USD - Kiwi 0.838 (0.4) (0.5) 2.2 1.8

% Ch a n g eCurrenc ies

% Ch a n g eK ey In d i ces

% Ch a n g eFre ight

Com m od i t ies I n ven t o r ies% Chang e % Change

80

85

90

95

100

105

110

115

120

Jan M ar M ay Jul Sep No v

NEWCASTLE COALUSD/t

1,500

1,550

1,600

1,650

1,700

1,750

1,800

Jan M ar M ay Jul Sep Nov

GOLDUSD/oz

70

80

90

100

110

Jan M ar M ay Jul Sep No v

W T I OI LUSD/bbl

0.94

0.97

1.00

1.03

1.06

1.09

Jan M ar M ay Jul Sep No v

A UDUSD

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

Jan M ar M ay Jul Sep No v

NI CKELUSD/t

7,000

7,500

8,000

8,500

9,000

Jan M ar M ay Jul Sep No v

COPPERUSD/t

1,700

1,800

1,900

2,000

2,100

2,200

2,300

Jan M ar M ay Jul Sep No v

A L UM I N I U MUSD/t

1,700

1,800

1,900

2,000

2,100

2,200

Jan M ar M ay Jul Sep No v

Z I N CUSD/t

25.0

27.0

29.0

31.033.0

35.0

37.0

Jan M ar M ay Jul Sep No v

SI LVERUSD/oz

Notes: *Front-month futures **Weekly prices

Sources: Bloomberg, McCloskey, ANZ Commodity Strategy

7/29/2019 ANZ Commodity Daily 764 250113.pdf

http://slidepdf.com/reader/full/anz-commodity-daily-764-250113pdf 3/5

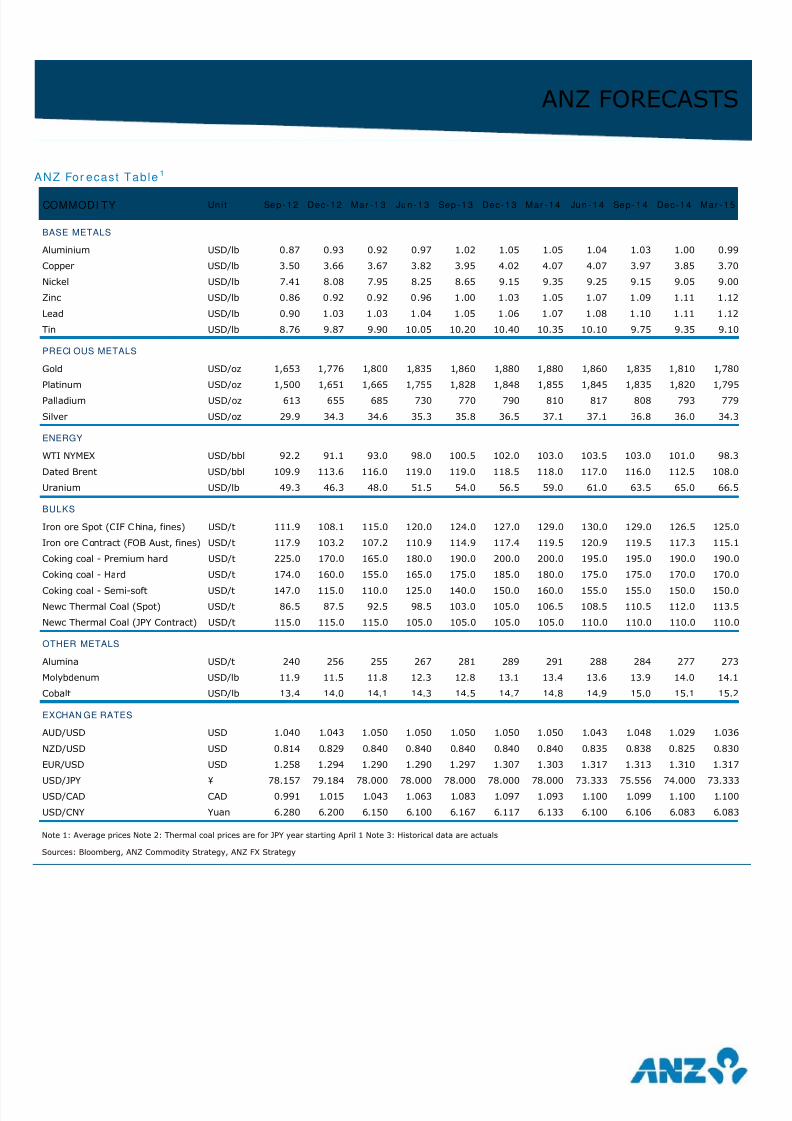

ANZ FORECASTS

ANZ For ecast Table 1

COMMODI TY Un i t Sep -1 2 Dec- 12 Mar - 1 3 Jun - 13 Sep -1 3 Dec-1 3 Mar - 14 Jun -1 4 Sep - 14 Dec- 14 Mar - 15

BASE METALS

Aluminium USD/lb 0.87 0.93 0.92 0.97 1.02 1.05 1.05 1.04 1.03 1.00 0.99

Copper USD/lb 3.50 3.66 3.67 3.82 3.95 4.02 4.07 4.07 3.97 3.85 3.70

Nickel USD/lb 7.41 8.08 7.95 8.25 8.65 9.15 9.35 9.25 9.15 9.05 9.00

Zinc USD/lb 0.86 0.92 0.92 0.96 1.00 1.03 1.05 1.07 1.09 1.11 1.12

Lead USD/lb 0.90 1.03 1.03 1.04 1.05 1.06 1.07 1.08 1.10 1.11 1.12

Tin USD/lb 8.76 9.87 9.90 10.05 10.20 10.40 10.35 10.10 9.75 9.35 9.10

PRECI OUS METALS

Gold USD/oz 1,653 1,776 1,800 1,835 1,860 1,880 1,880 1,860 1,835 1,810 1,780

Platinum USD/oz 1,500 1,651 1,665 1,755 1,828 1,848 1,855 1,845 1,835 1,820 1,795

Palladium USD/oz 613 655 685 730 770 790 810 817 808 793 779

Silver USD/oz 29.9 34.3 34.6 35.3 35.8 36.5 37.1 37.1 36.8 36.0 34.3

ENERGY

WTI NYMEX USD/bbl 92.2 91.1 93.0 98.0 100.5 102.0 103.0 103.5 103.0 101.0 98.3

Dated Brent USD/bbl 109.9 113.6 116.0 119.0 119.0 118.5 118.0 117.0 116.0 112.5 108.0

Uranium USD/lb 49.3 46.3 48.0 51.5 54.0 56.5 59.0 61.0 63.5 65.0 66.5

BULKS

Iron ore Spot (CIF China, fines) USD/t 111.9 108.1 115.0 120.0 124.0 127.0 129.0 130.0 129.0 126.5 125.0

Iron ore Contract (FOB Aust, fines) USD/t 117.9 103.2 107.2 110.9 114.9 117.4 119.5 120.9 119.5 117.3 115.1

Coking coal - Premium hard USD/t 225.0 170.0 165.0 180.0 190.0 200.0 200.0 195.0 195.0 190.0 190.0

Coking coal - Hard USD/t 174.0 160.0 155.0 165.0 175.0 185.0 180.0 175.0 175.0 170.0 170.0

Coking coal - Semi-soft USD/t 147.0 115.0 110.0 125.0 140.0 150.0 160.0 155.0 155.0 150.0 150.0

Newc Thermal Coal (Spot) USD/t 86.5 87.5 92.5 98.5 103.0 105.0 106.5 108.5 110.5 112.0 113.5

Newc Thermal Coal (JPY Contract) USD/t 115.0 115.0 115.0 105.0 105.0 105.0 105.0 110.0 110.0 110.0 110.0

OTHER METALS

Alumina USD/t 240 256 255 267 281 289 291 288 284 277 273

Molybdenum USD/lb 11.9 11.5 11.8 12.3 12.8 13.1 13.4 13.6 13.9 14.0 14.1

Cobalt USD/lb 13.4 14.0 14.1 14.3 14.5 14.7 14.8 14.9 15.0 15.1 15.2

EXCHAN GE RATES

AUD/USD USD 1.040 1.043 1.050 1.050 1.050 1.050 1.050 1.043 1.048 1.029 1.036

NZD/USD USD 0.814 0.829 0.840 0.840 0.840 0.840 0.840 0.835 0.838 0.825 0.830

EUR/USD USD 1.258 1.294 1.290 1.290 1.297 1.307 1.303 1.317 1.313 1.310 1.317

USD/JPY ¥ 78.157 79.184 78.000 78.000 78.000 78.000 78.000 73.333 75.556 74.000 73.333

USD/CAD CAD 0.991 1.015 1.043 1.063 1.083 1.097 1.093 1.100 1.099 1.100 1.100

USD/CNY Yuan 6.280 6.200 6.150 6.100 6.167 6.117 6.133 6.100 6.106 6.083 6.083

Note 1: Average prices Note 2: Thermal coal prices are for JPY year starting April 1 Note 3: Historical data are actuals

Sources: Bloomberg, ANZ Commodity Strategy, ANZ FX Strategy

7/29/2019 ANZ Commodity Daily 764 250113.pdf

http://slidepdf.com/reader/full/anz-commodity-daily-764-250113pdf 4/5

I MPORTANT NOTI CE The distribution of this document or streaming of this video broadcast (as applicable, “publication”) may berestricted by law in certain jurisdictions. Persons who receive this publication must inform themselves about and observe all relevantrestrictions.

1. COUNTRY/ REGION SPECI FI C I NFORMATI ON:AUSTRALI A . This publication is distributed in Australia by Australia and New Zealand Banking Group Limited (ABN 11 005 357 522)(“ANZ”). ANZ holds an Australian Financial Services licence no. 234527. A copy of ANZ's Financial Services Guide is available athttp://www.anz.com/documents/AU/aboutANZ/FinancialServicesGuide.pdf and is available upon request from your ANZ point of contact. If

trading strategies or recommendations are included in this publication, they are solely for the information of ‘wholesale clients’ (as definedin section 761G of the Corporations Act 2001 Cth). Persons who receive this publication must inform themselves about and observe all

relevant restrictions.

BRAZI L. This publication is distributed in Brazil by ANZ only for the information of the Central Bank of Brazil. No securities are being

offered or sold in Brazil under this publication, and no securities have been and will not be registered with the Securities Commission -CVM.

BRUNEI. JAPAN. KUWAI T. MALAYSI A. SWI TZERLAND. TAI PEI . This publication is distributed in each of Brunei, Japan, Kuwait,Malaysia, Switzerland and Taipei by ANZ on a cross-border basis.

EUROPEAN ECONOMI C AREA ( “ EEA” ) : UNI TED KI NGDOM. ANZ is authorised and regulated in the United Kingdom by the FinancialServices Authority (“FSA”). This publication is distributed in the United Kingdom by ANZ solely for the information of persons who would

come within the FSA definition of “eligible counterparty” or “professional client”. It is not intended for and must not be distributed to anyperson who would come within the FSA definition of “retail client”. Nothing here excludes or restricts any duty or liability to a customer

which ANZ may have under the UK Financial Services and Markets Act 2000 or under the regulatory system as defined in the Rules of theFSA. GERMANY. This publication is distributed in Germany by the Frankfurt Branch of ANZ solely for the information of its clients. OTHER

EEA COUNTRI ES. This publication is distributed in the EEA by ANZ Bank (Europe) Limited (“ANZBEL”) which is authorised and regulatedby the FSA in the United Kingdom, to persons who would come within the FSA definition of “eligible counterparty” or “professional client” in other countries in the EEA. This publication is distributed in those countries solely for the information of such persons upon theirrequest. It is not intended for, and must not be distributed to, any person in those countries who would come within the FSA definition of

“retail client”.

FIJI . For Fiji regulatory purposes, this publication and any views and recommendations are not to be deemed as investment advice. Fiji

investors must seek licensed professional advice should they wish to make any investment in relation to this publication.

HONG KONG. This publication is distributed in Hong Kong by the Hong Kong branch of ANZ, which is registered by the Hong KongSecurities and Futures Commission to conduct Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on

corporate finance) regulated activities. The contents of this publication have not been reviewed by any regulatory authority in Hong Kong.If in doubt about the contents of this publication, you should obtain independent professional advice.

I N D I A. This publication is distributed in India by ANZ on a cross-border basis. If this publication is received in India, only you (thespecified recipient) may print it provided that before doing so, you specify on it your name and place of printing. Further copying or

duplication of this publication is strictly prohibited.

NEW ZEALAND. This publication is intended to be of a general nature, does not take into account your financial situation or goals, and isnot a personalised adviser service under the Financial Advisers Act 2008.

OMAN . This publication has been prepared by ANZ. ANZ neither has a registered business presence nor a representative office in Omanand does not undertake banking business or provide financial services in Oman. Consequently ANZ is not regulated by either the CentralBank of Oman or Oman’s Capital Market Authority. The information contained in this publication is for discussion purposes only and neither

constitutes an offer of securities in Oman as contemplated by the Commercial Companies Law of Oman (Royal Decree 4/74) or the CapitalMarket Law of Oman (Royal Decree 80/98), nor does it constitute an offer to sell, or the solicitation of any offer to buy non-Omanisecurities in Oman as contemplated by Article 139 of the Executive Regulations to the Capital Market Law (issued vide CMA Decision1/2009). ANZ does not solicit business in Oman and the only circumstances in which ANZ sends information or material describingfinancial products or financial services to recipients in Oman, is where such information or material has been requested from ANZ and by

receiving this publication, the person or entity to whom it has been dispatched by ANZ understands, acknowledges and agrees that thispublication has not been approved by the CBO, the CMA or any other regulatory body or authority in Oman. ANZ does not market, offer,sell or distribute any financial or investment products or services in Oman and no subscription to any securities, products or financialservices may or will be consummated within Oman. Nothing contained in this publication is intended to constitute Omani investment, legal,

tax, accounting or other professional advice.

PEOPLE’S REPUBLI C OF CHI NA . If and when the material accompanying this publication does not only relate to the products and/orservices of Australia and New Zealand Bank (China) Company Limited (“ANZ China”), it is noted that: This publication is distributed byANZ or an affiliate. No action has been taken by ANZ or any affiliate which would permit a public offering of any products or services of such an entity or distribution or re-distribution of this publication in the People’s Republic of China (“PRC”). Accordingly, the products andservices of such entities are not being offered or sold within the PRC by means of this publication or any other method. This publication

may not be distributed, re-distributed or published in the PRC, except under circumstances that will result in compliance with anyapplicable laws and regulations. If and when the material accompanying this publication relates to the products and/or services of ANZChina only, it is noted that: This publication is distributed by ANZ China in the Mainland of the PRC.

QATAR. This publication has not been, and will not be: lodged or registered with, or reviewed or approved by, the Qatar Central Bank("QCB"), the Qatar Financial Centre ("QFC") Authority, QFC Regulatory Authority or any other authority in the State of Qatar ("Qatar"); orauthorised or licensed for distribution in Qatar, and the information contained in this publication does not, and is not intended to,constitute a public offer or other invitation in respect of securities in Qatar or the QFC. The financial products or services described in thispublication have not been, and will not be: registered with the QCB, QFC Authority, QFC Regulatory Authority or any other governmentalauthority in Qatar; or authorised or licensed for offering, marketing, issue or sale, directly or indirectly, in Qatar.

Accordingly, the financial products or services described in this publication are not being, and will not be, offered, issued or sold in Qatar,

and this publication is not being, and will not be, distributed in Qatar. The offering, marketing, issue and sale of the financial products or

services described in this publication and distribution of this publication is being made in, and is subject to the laws, regulations and rulesof, jurisdictions outside of Qatar and the QFC. Recipients of this publication must abide by this restriction and not distribute this publication

in breach of this restriction. This publication is being sent/issued to a limited number of institutional and/or sophisticated investors (i) upontheir request and confirmation that they understand the statements above; and (ii) on the condition that it will not be provided to any

person other than the original recipient, and is not for general circulation and may not be reproduced or used for any other purpose.

7/29/2019 ANZ Commodity Daily 764 250113.pdf

http://slidepdf.com/reader/full/anz-commodity-daily-764-250113pdf 5/5

SI NGAPORE. This publication is distributed in Singapore by the Singapore branch of ANZ solely for the information of “accredited

investors”, “expert investors” or (as the case may be) “institutional investors” (each term as defined in the Securities and Futures Act Cap.289 of Singapore). ANZ is licensed in Singapore under the Banking Act Cap. 19 of Singapore and is exempted from holding a financial

adviser’s licence under Section 23(1)(a) of the Financial Advisers Act Cap. 100 of Singapore. In respect of any matters arising from, or inconnection with the distribution of this publication in Singapore, contact your ANZ point of contact. UNI TED ARAB EMI RATES. This publication is distributed in the United Arab Emirates (“UAE”) or the Dubai International Financial Centre(as applicable) by ANZ. This publication: does not, and is not intended to constitute an offer of securities anywhere in the UAE; does not

constitute, and is not intended to constitute the carrying on or engagement in banking, financial and/or investment consultation businessin the UAE under the rules and regulations made by the Central Bank of the United Arab Emirates, the Emirates Securities andCommodities Authority or the United Arab Emirates Ministry of Economy; does not, and is not intended to constitute an offer of securitieswithin the meaning of the Dubai International Financial Centre Markets Law No. 12 of 2004; and, does not constitute, and is not intendedto constitute, a financial promotion, as defined under the Dubai International Financial Centre Regulatory Law No. 1 of 200. ANZ DIFC

Branch is regulated by the Dubai Financial Services Authority (“DFSA”). The financial products or services described in this publication areonly available to persons who qualify as “Professional Clients” or “Market Counterparty” in accordance with the provisions of the DFSArules. In addition, ANZ has a representative office (“ANZ Representative Office”) in Abu Dhabi regulated by the Central Bank of the UnitedArab Emirates. ANZ Representative Office is not permitted by the Central Bank of the United Arab Emirates to provide any bankingservices to clients in the UAE. UNI TED STATES. If and when this publication is received by any person in the United States or a "U.S. person" (as defined in Regulation

S under the US Securities Act of 1933, as amended) (“US Person”) or any person acting for the account or benefit of a US Person, it isnoted that ANZ Securities, Inc. (“ANZ S”) is a member of FINRA (www.finra.org) and registered with the SEC. ANZ S’s address is 277 Park

Avenue, 31st Floor, New York, NY 10172, USA (Tel: +1 212 801 9160 Fax: +1 212 801 9163). Except where this is a FX relatedpublication, this publication is distributed in the United States by ANZ S (a wholly owned subsidiary of ANZ), which accepts responsibilityfor its content. Information on any securities referred to in this publication may be obtained from ANZ S upon request. Any US Person

receiving this publication and wishing to effect transactions in any securities referred to in this publication must contact ANZ S, not itsaffiliates. Where this is an FX related publication, it is distributed in the United States by ANZ's New York Branch, which is also located at277 Park Avenue, 31st Floor, New York, NY 10172, USA (Tel: +1 212 801 9160 Fax: +1 212 801 9163). ANZ S is authorised as a broker-dealer only for US Persons who are institutions, not for US Persons who are individuals. If you have registered to use this website or haveotherwise received this publication and are a US Person who is an individual: to avoid loss, you should cease to use this website byunsubscribing or should notify the sender and you should not act on the contents of this publication in any way.

2. DI SCLAI MERExcept if otherwise specified above, this publication is issued and distributed in your country/region by ANZ, on the basis that it is only forthe information of the specified recipient or permitted user of the relevant website (collectively, “recipient”). This publication may not be

reproduced, distributed or published by any recipient for any purpose. It is general information and has been prepared without taking intoaccount the objectives, financial situation or needs of any person. Nothing in this publication is intended to be an offer to sell, or a

solicitation of an offer to buy, any product, instrument or investment, to effect any transaction or to conclude any legal act of any kind. If,despite the foregoing, any services or products referred to in this publication are deemed to be offered in the jurisdiction in which this

publication is received or accessed, no such service or product is intended for nor available to persons resident in that jurisdiction if itwould be contradictory to local law or regulation. Such local laws, regulations and other limitations always apply with non-exclusive

jurisdiction of local courts. Before making an investment decision, recipients should seek independent financial, legal, tax and otherrelevant advice having regard to their particular circumstances.

The views and recommendations expressed in this publication are the author’s. They are based on information known by the author and onsources which the author believes to be reliable, but may involve material elements of subjective judgement and analysis. Unlessspecifically stated otherwise: they are current on the date of this publication and are subject to change without notice; and, all price

information is indicative only. Any of the views and recommendations which comprise estimates, forecasts or other projections, are subjectto significant uncertainties and contingencies that cannot reasonably be anticipated. On this basis, such views and recommendations maynot always be achieved or prove to be correct. Indications of past performance in this publication will not necessarily be repeated in thefuture. No representation is being made that any investment will or is likely to achieve profits or losses similar to those achieved in thepast, or that significant losses will be avoided. Additionally, this publication may contain ‘forward looking statements’. Actual events or

results or actual performance may differ materially from those reflected or contemplated in such forward looking statements. Allinvestments entail a risk and may result in both profits and losses. Foreign currency rates of exchange may adversely affect the value,price or income of any products or services described in this publication. The products and services described in this publication are notsuitable for all investors, and transacting in these products or services may be considered risky. ANZ and its related bodies corporate andaffiliates, and the officers, employees, contractors and agents of each of them (including the author) (“Affiliates”), do not make anyrepresentation as to the accuracy, completeness or currency of the views or recommendations expressed in this publication. Neither ANZ

nor its Affiliates accept any responsibility to inform you of any matter that subsequently comes to their notice, which may affect theaccuracy, completeness or currency of the information in this publication.Except as required by law, and only to the extent so required: neither ANZ nor its Affiliates warrant or guarantee the performance of anyof the products or services described in this publication or any return on any associated investment; and, ANZ and its Affiliates expressly

disclaim any responsibility and shall not be liable for any loss, damage, claim, liability, proceedings, cost or expense (“Liability”) arisingdirectly or indirectly and whether in tort (including negligence), contract, equity or otherwise out of or in connection with this publication.If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to besecure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. ANZ andits Affiliates do not accept any Liability as a result of electronic transmission of this publication.ANZ and its Affiliates may have an interest in the products and services described in this publication as follows:• They may receive fees from customers for dealing in the products or services described in this publication, and their staff and

introducers of business may share in such fees or receive a bonus that may be influenced by total sales.• They or their customers may have or have had interests or long or short positions in the products or services described in thispublication, and may at any time make purchases and/or sales in them as principal or agent.• They may act or have acted as market-maker in products described in this publication.

ANZ and its Affiliates may rely on information barriers and other arrangements to control the flow of information contained in one or morebusiness areas within ANZ or within its Affiliates into other business areas of ANZ or of its Affiliates.Please contact your ANZ point of contact with any questions about this publication including for further information on the abovedisclosures of interest.