Embed Size (px)

Citation preview

1

JMUK Jayasinghe, 2009 | Confidential

“Applied Study on Local Finance for

Urban and Peri-Urban Producers” - Gampaha

Final Report Submitted to

Dr. Priyanie Amerasinghe

(Regional RUAF Coordinator)

By

J. M. Udith K. Jayasinghe, PhD

(Expert Consultant) Dept. of Agribusiness Management

Faculty of Agriculture & Plantation Management

Wayamba University of Sri Lanka Makandura, Gonawila (NWP)

2

JMUK Jayasinghe, 2009 | Confidential

EXECUTIVE SUMMARY

The aim of this study was to provide information, knowledge and clear

recommendations that will serve to broaden collective and individual financing opportunities for urban poor and peri-urban producers located in the RUAF partner city

of Gampaha. The specific objectives of it were: (1) identification and assessment of current practices of institutions and programs that finance urban agriculture; (2)

identification of the needs and demands for finance from urban poor engaged in urban agriculture, agro-processing or marketing; (3) proposal and recommendations to facilitate the access of small-scale urban producers to finance.

In order to achieve these objectives, a two-phased, but concurrently executed,

multidisciplinary structured survey based methodology was adopted, which included an extensive review of existing literature, identification and formulation of separate

sampling frameworks and the development of appropriate interview schedules, aiming at financial institutions (FIs) and urban agricultural producers (UAPs). The responses to each question included in the Interview Schedules for the FIs and UAPs were analyzed,

individually and collectively (i.e. cross comparisons / compare and contrast). In the process of selecting the most suitable financial intermediary, a “Step-wise Elimination

Procedure” was followed by considering the characters/features of the FIs, responsiveness

to the issues raised by the consultants with regard to their ability and willingness towards

financing UA and the requirements/demands from the UAPs.

We found that most of the existing FIs showed “positive attitude” and/or “sympathy”

towards the agricultural activities/communities, in general. Nevertheless, when it comes to the issue of access to their credit / loan / other financial support schemes, small-scale

agriculture does not take a prominent place. Similarly, the awareness of those FIs, in general, regarding urban agriculture was also limited. We have observed wide variation between the different types of financial institutions with regard their willing to participate

in financing UA (State Banks and Cooperatives more willing, while Private Institutions less willing to involve). When inquired from the FIs as to the reasons for not willing to

finance UA or agriculture in general, many common reasons emerged as being bottlenecks. High rates of default, together with the high risk involved in financing small

to medium-scale agricultural projects, was a recurring theme in the discussions. Another issue raised by some was that farmers „lack the motivation for repayment‟. The more eager and potential entities such as SANASA City Bank (SCB), People’s Bank (PB) and

Wayamba Development Bank (WDB) were willing to partner with an external body to

formulate and implement strategies and programs for financing UA. However, the

respondents raised issues such as the independence of the intermediaries and the administrative cost (i.e. evaluation, monitoring and repayment-collection) of such

programs.

Certain institutions such as SEEDS and CIC Agri Businesses (Urban Agricultural Division)

emerged as those that were able to provide other forms of services such as training and workshops on special topics of interest for the UAPs. We have noticed that the UAPs

have mainly utilized their “own funds and savings” for agricultural practices, with virtually none having accessed formal sources for this purpose. Further, informal sources

3

JMUK Jayasinghe, 2009 | Confidential

have been tapped by a few as well. The reasons for this vary among the respondents. A primary element being that, Formal FIs are “strict” and project an “unfriendly

environment” towards growers. Complains extend to the limit that they are unaware of any suitable financial product and/or its providers. Another interesting personal issue for

the UAPs was about their “dignity and self-respect” in relation to obtaining funds from these institutions; some of the growers raised this issue, indicating that they feel “uncomfortable” when accessing a FI such as a reputed public/private bank to obtain

loans for their agricultural activities. The responses from the UAPs, with regard to a „suitable‟ financial package for their venture, were symptomatic of the need for

flexibility, both in relation to obtaining financial support and paying it back.

The UAPs requested other forms of assistance from intermediaries such as training, both

technical and business related skills. Here the responses made feel that strong focus needs to be made, especially with regard to a proper extension / technical (agronomical / crop

management) support system. Furthermore, other forms of skill development were preferred (e.g. entrepreneurial, leadership, marketing). We would like to suggest both

public and private “Licensed Commercial Banks” (LCBs) and public “Licensed Specialized Banks” (LSBs) over the private LSBs, “Finance Companies” and “Other

Potential Institutions”, excluding the SEEDS. Out of the private LCBs, both Commercial

Bank (CB) and Sampath Bank (SB) have the potential to finance, but SB is leading. Out of

the public LCBs and LSBs, Bank of Ceylon (BoC), Peoples’ Bank (PB), Wayamba

Development Bank (WDB) and SANASA City Bank (SCB) are the potential institutions.

SCB is the institution with a relatively higher potential and ability. Currently, it is functioning according to a rigid framework of urban livelihood development and

possesses an inherent desire to deal with urban producers and agriculture in general and it is seeking a prospective client to collaborate. Further, the experience of dealing within

the Gampaha City, cordial relationships maintained with the farmer community and highly flexible nature of the institution, together with its apparent capabilities to develop

and implement novel financial packages / services for requested agricultural projects, makes it a suitable financial institution to consider. It also has other facilities such as field officers and profit sharing mechanisms.

The other potential entity is the PB, with the respective branch manager expressing a

very positive attitude towards urban agriculture and being experienced in dealing with financing rural agriculture in other provinces of Sri Lanka. It currently deals with the

small enterprises and lower income groups in the district. Further, being a state bank adds to its credibility. However, issues such as lot of paperwork and unclear specifications were apparent. Although, PB comes with financial stability, we have

observed a sort of “inflexibility”, i.e. it is difficult to tailor-make financial products without the consent from the higher authorities, which makes them unattractive to the

unique needs of UAPs. In light of the above empirical findings and revelations, we would like to name the following FIs to design and finance urban agricultural activities

in Gampaha, IN ORDER: SANASA City Bank Ltd. (SCB); People‟s Bank (PB), and Wayamba Development Bank (WDB).

4

JMUK Jayasinghe, 2009 | Confidential

Rationale of the Study The aim of this consultation is to provide information, knowledge and clear

recommendations that will serve to broaden collective and individual financing opportunities for urban poor and peri-urban producers located in the RUAF partner city of Gampaha.

Study Area

The study was carried out in the RUAF partner city of Gampaha (the capital of the Gampaha District in the Western Province of Sri Lanka). The Gampaha Municipal Council (GMC) consists of 33 Grama Niladhari (GN) divisions, which constitute the

geographical region of interest of this study.

Specific Objectives of the Study

Objective 1 – Identification and assessment of current practices of institutions and

programs that finance urban agriculture or other informal productive activities

(like micro-enterprise development) in the city and the existing opportunities, difficulties and bottlenecks for financing small-scale urban and peri-urban

agriculture they encounter.

Objective 2 – Identification of the needs and demands for finance from urban poor

engaged in urban agriculture, agro-processing or marketing.

Objective 3 – Proposal and recommendations to facilitate the access of small scale

urban producers to finance.

Methodology

Approaches Used to Achieve the Specific Objectives of the Study

As suggested in the preliminary work plan, which was approved by the Project

Coordinators of RUAF, a two-phased, but concurrently executed, multidisciplinary survey based methodology to complete the tasks specified below was adopted.

As the first step, an “in-depth discussion” with the RUAF Regional Coordinator (online)

and Regional Coach – FStT Project – Gampaha (in-person) was carried out ON 23RD

July 2009 to have a broad understanding about the previous work carried out by the RUAF in this respect. Also, the “documents published previously” by the RUAF on this aspect were collected and reviewed comprehensively. During the discussion with the

RUAF Regional Coach on the current RUAF urban producer group, the consultants reviewed a number of issues in relation to UA within Gampaha. Primarily was the

revelation that although they had contacted around 300 growers or potential growers (from the 33 GN Divisions), many had declined to participate, either citing that they are

not interested in the FStT Project and/or satisfied with their current level/type of activities and only 93 urban producers were available for the project.

5

JMUK Jayasinghe, 2009 | Confidential

Objective 1 - Identification and assessment of current practices of institutions and programs that

finance urban agriculture

Approaches in Phase I:

A sampling framework (FIs) was developed that consisted of the

institutions/entities currently involved or those that have a potential to involve in financing urban agriculture (UA). The institutions covered, include: (1) Licensed

Commercial Banks (LCB); (2) Licensed Specialized Banks (LSB); (3) Co-

operatives; (4) Finance Companies, and (5) other Potential Institutions (Table 1).

Table 1 - List of Proposed Financial Institutions for Interviews:

1.0

Licensed

Commercial Bank

1.1 Public

1.1.1 Bank of Ceylon

1.1.2 Peoples Bank

1.1.3 National Development Bank

1.2 Private

1.2.1 Commercial Bank

1.2.2 Hatton National Bank

1.2.3 Nations Trust Bank

1.2.4 Pan Asia Bank

1.2.5 Sampath Bank

1.2.6 Seylan Bank

2.0

Licensed

Specialized Bank

2.1 Public

2.1.1 National Savings Bank

2.1.2 Wayamba Development Bank

2.2 Private

2.2.1 HDFC Bank

2.2.2 DFCC Bank

3.0

Co-operatives

3.1 District Cooperatives Rural Bank Union Ltd

3.2 SANASA City Bank Ltd

3.3 Gampaha Multi Purpose Cooperative Society Ltd

3.4 Henarathgoda SANASA Society Ltd

4.0

Finance Company

4.1 Citizens Development Business Finance Ltd

4.2 Senkadagala Finance Company Ltd

5.0

Other Potential

Institutions

5.1 CIC Agribusiness

5.2 Sarvodaya Economic Enterprise Development

Services (Guarantee) Ltd. (SEEDS)

6

JMUK Jayasinghe, 2009 | Confidential

Having obtained the contact details of each institution, a “telephone conversation” and/or a “short visit” (as required) was made with the senior

representative/s or responsible officer/s of these institutions to receive preliminary information with regard to their current practices on UA. Based on

the outcome of this preliminary contact, the institutions to be contacted were identified.

A Structured Interview Schedule was developed (See, ANNEX 1 -

“INTERVIEW SCHEDULE for FINANCIAL INSTITUTIONS”) based on

the Terms of Reference (ToR) and other recommended literature on UA financing and revised after consulting with the RUAF Regional Coordinator.

An in-depth interview was conducted with the officer/s responsible for financing

agricultural projects of the selected FI to gather information (See, ANNEX 2 -

“DATABASE - FINANCIAL INSTITUTIONS”)

Objective 2 - Identification of the needs and demands for finance from urban poor

engaged in urban agriculture, agro-processing or marketing.

Approaches in Phase II:

The Sampling Framework (UAPs) consists of small scale urban commercial producers in consultation with the RUAF Regional Coach for Gampaha, where

93 urban producers belong to 8 groups were of concern: (i) „Samagi‟; (ii) „Arunalu‟; (iii) „Pubudu‟; (iv) „Ekamuthu‟; (v) „Isuru‟; (vi) Siyane Shakthi‟; (vii)

„Dimuthu‟, and (viii) „Wasana‟ (See, ANNEX 3 - “DATABASE – URBAN

AGRICULTURAL PRODUCERS”) (Further to the discussion with the RUAF Regional Coach, the consultants resolved to work with only 93 farmers, since if the other

potential/current farmers were contacted, their responses would be biased in terms of emphasizing their nonparticipation and highlighting that they do not require financial or

any form of support).

A Structured Interview Schedule was developed (See, ANNEX 4 -

“INTERVIEW SCHEDULE for URBAN AGRICULTURAL

PRODUCERS”) based on the Terms of Reference (ToR) and other

recommended literature on UA financing and revised after consulting with the RUAF Regional Coordinator.

The leaders of the group and key member/s were informed of the study through the Regional Coach and asked to prepare for Group Interview Sessions, which

were carried out later with the aid of Interview Schedule.

7

JMUK Jayasinghe, 2009 | Confidential

Objective 3 - Proposal and recommendations to facilitate the access of small scale urban

producers to finance.

Approach:

The data collected through Phase 1 and 2 were coded using MS-Excel software (see,

ANNEX 2). The responses to each question included in the Interview Schedule were analyzed, individually and collectively (i.e. cross comparisons / compare and contrast)

to explore the behavior FIs. By giving reasons, the most appropriate FI was selected and several others were also selected as alternatives.

The Work Plan

ACTIVITY

Month 1 Month 2 Month 3

W1 W2

W3

W4

W5

W6

W7

W8

W9

W10

W11

W12

1. Discussion with RUAF Staff

2. SWF-1 = List of Financial Institutions SWF-2 = List of Producers

3. Preparation of Interview Schedule

4. Survey Plan

5. Data Collection & Coding

6. Data Analysis

7. Draft Report

8. Wrap up meetings with producers/institutions/RUAF

9. Final Report / Presentations

8

JMUK Jayasinghe, 2009 | Confidential

THE CURRENT PRACTICES OF THE LOCAL FINANCIAL

INSTITUTIONS AND RELATED OPPORTUNITIES, DIFFICULTIES

AND BOTTLENECKS FOR FINANCING SMALL SCALE URBAN

AND PERI-URBAN AGRICULTURE ENTERPRISES

OUTLINE

Twenty-two (22) institutions (Table 1) within the Gampaha Municipality Council (GMC) were sampled for this phase of the study, and they comprised both financial

institutions and others that are currently involved in supporting agriculture or those that have the potential to support in the near future.

The Central Bank of Sri Lanka (CBSL), categorizes financial institutions using a classification system (Refer for further details).This classification was adapted for this

purpose and the five main categories were considered.

CURRENT ROLE AS FINANCIAL INTERMEDIARY FOR AGRICULTURE As per the Structured Interview Schedule that was developed, the FIs were assessed in

terms of their perception, potential and constraints for involving in financing UA. Table 3 highlights the present status of the FIs in relation to their financing activities and

agriculture in general.

Table 3 – Current financing activities for agriculture:

Currently Financing

Agriculture?

Remarks

Bank of Ceylon

Yes

Peoples Bank

Yes Mainly for pineapple and other major commercial crops, as needed and after identifying the real need of the customers.

Current programs include: "Krushi

Navodaya Loan Scheme" (KNLS), "Forward

Sales Contract" (FSC), "Athamaru Loan

Scheme" (ALS), "Micro Finance Loans"

(People's Fast)

National Development

Bank

Less for Agriculture Only for the large scale commercial agribusiness with complete project reports

9

JMUK Jayasinghe, 2009 | Confidential

Commercial

Bank

Less for Agriculture For commercial production of perennial crops such as cashew nut, coconut,

horticultural products, including pineapple

Hatton National Bank

Yes For high-scale commercial cultivations

Nations Trust Bank

Almost No Yes, if it is only very commercial

Pan Asia Bank

No

Sampath

Bank

Yes For the projects that are deemed feasible and come up with a sound project report

Seylan Bank

Yes However, at present provision of credit to

news members is very limited and for the small-scale agricultural projects it is very

unlikely

National

Savings Bank

Less for Agriculture Do not provide loans for agriculture as much emphasized on other financing

programs

Wayamba

Development Bank

Less for Agriculture Livestock - broilers; based on the project, time period is decided, discussion with

them, Field Officer - prepare a report after visiting - based on these loan is provided; "Bahuvarshika Naya Yojana Kramaya" -

pineapple (completed); "Kapruka

Sanwardhana Naya" - CDA - for

intercropping/ under cropping in coconut lands; No discrimination for agricultural

projects; "Krushi Navodaya"; "Pashu

Sampath Sanvardhanaya” - dairy cows

HDFC Bank No

DFCC Bank No

District

Cooperatives Rural Bank

Union Ltd

Yes For the members only; Paddy/ Floriculture/ Coconut under planting

(intercropping); any project that adds value for local production or generates

employment; "Wimana" loan scheme

SANASA City Bank Ltd

Yes For the members only; in many areas related to agricultural production and processing, including horticulture and

floriculture

10

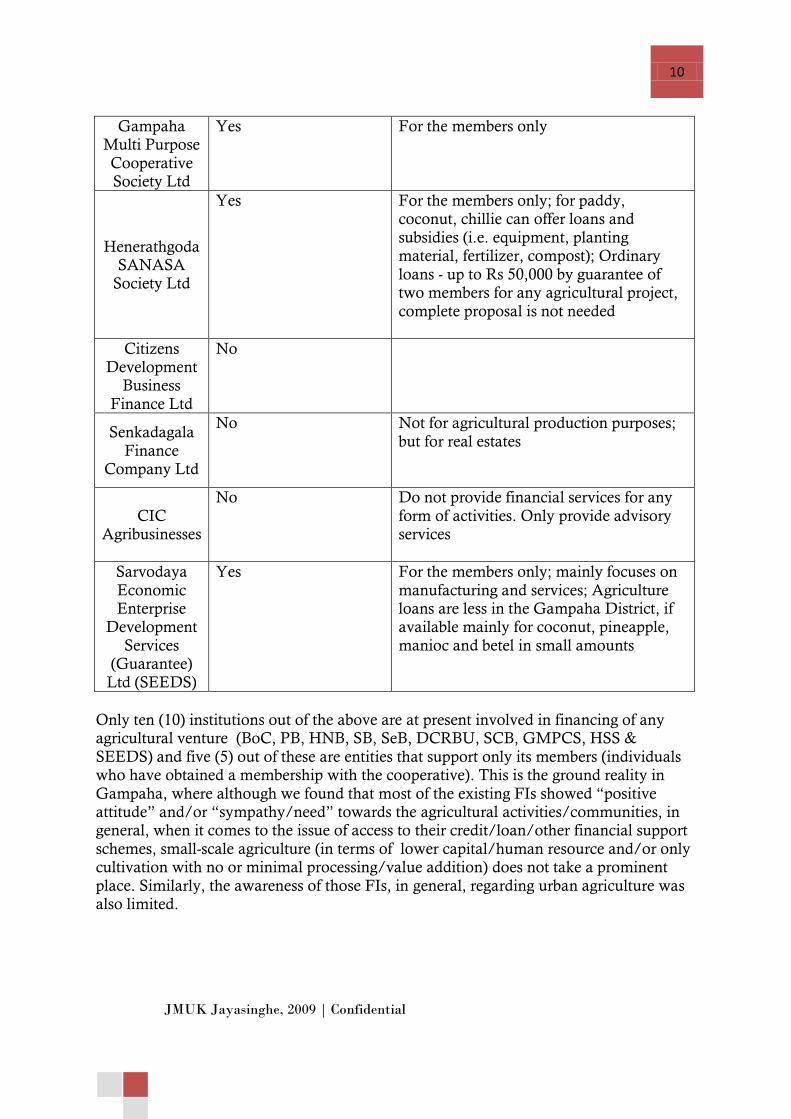

JMUK Jayasinghe, 2009 | Confidential

Gampaha Multi Purpose

Cooperative Society Ltd

Yes For the members only

Henerathgoda SANASA

Society Ltd

Yes For the members only; for paddy, coconut, chillie can offer loans and

subsidies (i.e. equipment, planting material, fertilizer, compost); Ordinary

loans - up to Rs 50,000 by guarantee of two members for any agricultural project,

complete proposal is not needed

Citizens Development

Business

Finance Ltd

No

Senkadagala

Finance Company Ltd

No Not for agricultural production purposes;

but for real estates

CIC Agribusinesses

No Do not provide financial services for any

form of activities. Only provide advisory services

Sarvodaya

Economic Enterprise

Development

Services (Guarantee)

Ltd (SEEDS)

Yes For the members only; mainly focuses on

manufacturing and services; Agriculture loans are less in the Gampaha District, if available mainly for coconut, pineapple,

manioc and betel in small amounts

Only ten (10) institutions out of the above are at present involved in financing of any agricultural venture (BoC, PB, HNB, SB, SeB, DCRBU, SCB, GMPCS, HSS &

SEEDS) and five (5) out of these are entities that support only its members (individuals who have obtained a membership with the cooperative). This is the ground reality in

Gampaha, where although we found that most of the existing FIs showed “positive attitude” and/or “sympathy/need” towards the agricultural activities/communities, in general, when it comes to the issue of access to their credit/loan/other financial support

schemes, small-scale agriculture (in terms of lower capital/human resource and/or only cultivation with no or minimal processing/value addition) does not take a prominent

place. Similarly, the awareness of those FIs, in general, regarding urban agriculture was also limited.

11

JMUK Jayasinghe, 2009 | Confidential

CAPABILITIES TO ACT AS A FINANCIAL INTERMEDIARY FOR URBAN

AGRICULTURE

Table 4 – Financing urban agriculture

Currently finance Urban

Agricultural practices in

Gampaha city?

How can you assist a program to

improve UA?

Bank of Ceylon

Yes Yes, We can accept any project / financial plan that is approved by the

higher authorities / parent decision making body; However, the bank can

only make recommendations to the governing body

Peoples Bank

Yes, animal husbandry and

commercial floriculture production

Yes, The bank would like to accept

any project / financial plan subjected to the approval by the higher authorities; Would like to come to an

agreement with any reliable institution / society after monitoring the project

sites for their feasibility; the bank is very flexible to provide funds for

agriculture, in principle, can even provide group loans under a well guided program

Commercial

Bank

Yes, but on case by case basis Yes, can assist urban agricultural projects, if the project proposal is acceptable to the bank; however, do

not target agricultural projects/farmers, in general, since

default is high - dedication is less - monitoring needed - high

administrative cost – requesters reluctance to offer collateral.

Sampath Bank

Yes - established a contract with farmers product to the

"Cargills" (financing guarantee from the Cargills)

Yes, the bank can consider any reputed financial plan to which the

approval of the higher authorities can be obtained given that the project /

plan is sustainable in the long run; The proposed "Cargills farmer

contract program" can be used as a sample / case for further discussion

12

JMUK Jayasinghe, 2009 | Confidential

Wayamba Development

Bank

It is not an issue whether the client is urban or rural.

However, there is no specific program aiming financing of

UA yet

Yes, a feasible credit facility can be arranged given that there should be a

third party to eliminate defaults and problems associated with payback;

The bank is willing to provide group loans for urban agriculturists,

however, the payback should be guaranteed; For a such scheme to be

considered, the approval of the higher authorities is required.

District

Cooperatives Rural Bank Union Ltd

Yes, the bank will finance

irrespective of client's

residency status

Yes, the cooperative bank can provide

financial services for small to medium

scale agriculture related activities; There is no plan to provide

infrastructure/goods (any forms of complementary services provision)

SANASA City Bank Ltd

Yes, the bank finance

irrespective of client's residency status

Yes, the City Bank likes to develop a

"Group Package" for agricultural entrepreneurs, where special attention may be given to the urban producers.

Those interested parties can get the group membership of such a program.

The bank is flexible and is willing to entertain new ideas of group savings

and loans. Third party ideas on such schemes are welcome.

Henerathgoda SANASA

Society Ltd

Yes, we do; however, not much

Yes, a low interest credit program for specific UA (New Program) can be

introduced if there is real need; there is a possibility of involving in a

"Revolving Fund" (for the group from Henerathgoda)

SEEDS

Currently not in Gampaha No, the SEEDS can not go beyond the

mandate of SSS to finance urban agriculture, where the theme is to uplift the living standards of

village/rural people.

The Private Licensed Commercial Banks such as Hatton National Bank and

Commercial Bank were found to be “least” in favor of providing credit scheme for small-scale urban agricultural projects. The reasons include that they do not want to extend

their portfolio into such enterprises as they are subjected to “inherent risks” associated

13

JMUK Jayasinghe, 2009 | Confidential

with agribusinesses (i.e. loss of market, crop failure). Further, these banks believed that this segment was incompatible with their existing customer base, and the small size of

the potential customer base for UA was not attractive from the banks‟ point of view. However, the manager of the Sampath Bank in Gampaha was an exception, where he is

interested in extending its financial portfolio towards these enterprises (highlighted the case of forming an agreement with „Cargills‟ – Sri Lanka‟s largest supermarket chain, in terms of outlets and retailing space).

Public institutions, both LCBs and Licensed Specialized Banks (LSBs) were more in

favor of UA-related financing opportunities. However here, rigid rules and regulations from the corporate national level frameworks (such as the need to get approval from the

parent decision-making body, limited independence of the relevant branch, excessive

paperwork, inflexibility with regard to forming new forms of financial products/services in addition to the existing packages, etc.) prohibitive towards providing finance for

agricultural activities.

However, the public LCBs such as Bank of Ceylon and People‟s Bank already provide a number of financial packages/services for small-scale agricultural and micro-

entrepreneurs at the moment, for example "Krushi Navodaya Loan Scheme" (KNLS),

"Forward Sales Contract" (FSC), "Athamaru Loan Scheme" (ALS) and "Micro Finance Loans"

(People's Fast). Although these schemes are wide open for the Urban Agricultural Producers (UAPs), there appears to a lot of paper work and unclear specifications. Although, these two banks come with financial stability, we have observed a sort of

“inflexibility”, i.e. it is difficult to tailor make financial products without the consent from the higher authorities, which makes them less approachable to the unique needs of

UAPs.

14

JMUK Jayasinghe, 2009 | Confidential

“KRUSHI NAVODAYA”

CREDIT PROGRAMME Implemented to empower small farmers by providing access to agricultural inputs at an affordable cost.

Loan amount: Up to Rs. 100,000 (Min. Rs. 10,000)

Eligibility: Export agricultural crops such as cinnamon, pepper, cardamom, etc., sugarcane, fruits, floriculture, cashew, livestock, fisheries, organic agriculture, agricultural inputs such as

seed and planting material and development of organic fertilizer, technology for value added agro based product, storage facilities, processing of fruit and food and rice flour milling; farmers, producers of minor export crops, chena cultivators, sugarcane growers, fruit growers, cashew planters, growers of floriculture, livestock farmers, fisherman, producers of organic agriculture, producers of seed, planting material and organic fertilizer, processing of fruit and food and rice flour millers.

Interest: 8% per annum to be charged from the borrower

Repayment: Up to 36 months or from the proceeds of the harvest in case of agricultural crops, whichever occurs early.

Security: Inters guarantee of two borrowers for loans up to Rs. 50,000; two guarantors

acceptable to the bank for loans above Rs. 50,000; assignment over insurance covering cultivation of crops, livestock, etc., wherever applicable.

15

JMUK Jayasinghe, 2009 | Confidential

MICRO FINANCE LOANS (PEOPLE’S FAST)

New People's Fast is a brand for Micro finance loan product. It provides financial assistance for: All business needs of micro, small and medium entrepreneurs, with relax collaterals, with speed loan disbursements.

Business Areas: To startup of enterprise / business; to improve existing enterprise / business; to expand your enterprise / business.

Sectors: Agriculture, Agro based industries, Industries, Self employment, Cottage industry, Trade, Services.

Eligibility criteria of this loan: Person with required skills; Engage in a profitable business (Agriculture, Animal husbandry, Industrial, cottage, Industry Trade, Service); Permanent resident of bank branch area.

Maximum Loan limit: Micro - Rs. 500,000; Small - Rs. 1,000,000; Medium - Rs. 5,000,000.

Interest rate: Negotiable

Non financial services for customers: People's Bank provides non financial services with identified service providers on Skill Development, Business Management, Business Planning, Entrepreneurship Development, Tax Planning etc.

16

JMUK Jayasinghe, 2009 | Confidential

SAMPATH BANK – CARGILLS CEYLON PARTNERSHIP Sampath Bank and Cargills (Ceylon) Plc sealed a Memorandum of Understanding (MoU) aimed at synergizing the competitive advantages of both corporates aimed at offering a variety of value added services to customers of both partners. Cargills has the largest chain of retail food outlets in the island with Cargills Food City rated the Most Valuable Retail Brand in Sri Lanka. The retail chain is geared with over 137 outlets spread across the island covering 19 districts. Cargills has developed a unique business model enabling the direct purchase of rice, vegetable and fruit from our local farming community located in Thambuththegama, Nuwaraeliya, Norochcholai, Hanguranketha, Dehiattakandiya, Bandarawela,

Gampaha/Divulapitiya and Neluwa. According to the company, in line with its ethos of fair trade Cargills currently partners over 7000 such farmers guaranteeing them a minimum price which is about 20% above the cost of production. As an initiative in these regard, it is now developing a mechanism for providing credit and other forms of financial instruments for farmers and farmer communities through partnering with Sampath Bank.

The Cooperatives contacted were, on the other hand, very positive and eager to provide finances to UA projects. They deal with on average, group savings for one-hundred (100)

to two-hundred (200) families, and have memberships of almost four-hundred (400) individuals. However, their services are limited to “members only” and often the lack of

transparent financial management/records together with the lack of other facilities such as limited human resource capabilities (few monitoring officers, service personnel, etc.)

LACK OF WILLINGNESS TO PARTICIPATE IN FINANCING UA AND

FUTURE PROSPECTS When inquired from the institutions as to the reasons for not willing to finance UA or

agriculture in general, many came up with similar reasons. High rates of default, together with the high risk involved in crop failure were the commonest. Another issue

raised by some was that farmers lack the motivation/commitment for repayment. It has been observed in schemes that allow to payback after harvest, farmers spend their

income to purchase other items than repaying the loans first. An interesting revelation

was that if the FI was involved as an intermediary for a government project (i.e. if the IF was required to manage / distribute financial resources from the government/NGO)

farmers would feel that loans from governments‟/NGO‟s need not be paid back as they are “subsidies”. Certain FIs stressed the need for a third party to monitor, and it could be

a farmer organization and also group financial packages and not individuals. Although the number of institutions that have the potential and capabilities to play the

role of a financial intermediary is large, only a limited number were willing to offer finance and only a few of these were able to satisfy the requirements of a farmer

engaging in UA (flexibility, innovating new financial products, stability and competence,

17

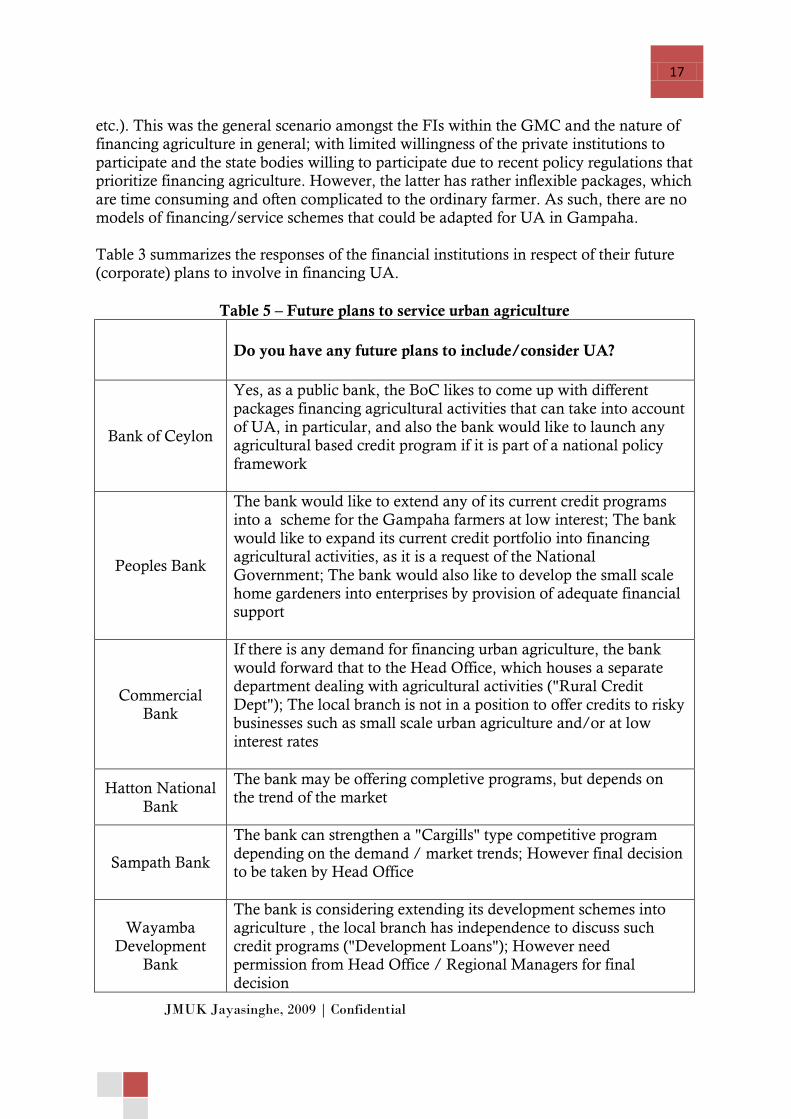

JMUK Jayasinghe, 2009 | Confidential

etc.). This was the general scenario amongst the FIs within the GMC and the nature of financing agriculture in general; with limited willingness of the private institutions to

participate and the state bodies willing to participate due to recent policy regulations that prioritize financing agriculture. However, the latter has rather inflexible packages, which

are time consuming and often complicated to the ordinary farmer. As such, there are no models of financing/service schemes that could be adapted for UA in Gampaha.

Table 3 summarizes the responses of the financial institutions in respect of their future (corporate) plans to involve in financing UA.

Table 5 – Future plans to service urban agriculture

Do you have any future plans to include/consider UA?

Bank of Ceylon

Yes, as a public bank, the BoC likes to come up with different

packages financing agricultural activities that can take into account of UA, in particular, and also the bank would like to launch any agricultural based credit program if it is part of a national policy

framework

Peoples Bank

The bank would like to extend any of its current credit programs into a scheme for the Gampaha farmers at low interest; The bank

would like to expand its current credit portfolio into financing agricultural activities, as it is a request of the National

Government; The bank would also like to develop the small scale home gardeners into enterprises by provision of adequate financial support

Commercial Bank

If there is any demand for financing urban agriculture, the bank

would forward that to the Head Office, which houses a separate department dealing with agricultural activities ("Rural Credit

Dept"); The local branch is not in a position to offer credits to risky businesses such as small scale urban agriculture and/or at low

interest rates

Hatton National

Bank

The bank may be offering completive programs, but depends on

the trend of the market

Sampath Bank

The bank can strengthen a "Cargills" type competitive program

depending on the demand / market trends; However final decision to be taken by Head Office

Wayamba

Development Bank

The bank is considering extending its development schemes into agriculture , the local branch has independence to discuss such

credit programs ("Development Loans"); However need permission from Head Office / Regional Managers for final

decision

18

JMUK Jayasinghe, 2009 | Confidential

District Cooperatives

Rural Bank Union Ltd

Under the 'Corporate Plan' of the cooperative, around 2.5 million rupees has been allocated for 100 loans (with good proposals), that

can be accessed by anybody who has land to be placed as security; "Wimana" loan scheme can be improved/diversified

SANASA City

Bank Ltd

Yes, the bank would like to contribute to urban people involved

with agriculture to become entrepreneurs. It likes to develop individual / group savings plans and loan schemes alone or with a

reputed institution which can share the ideas and legal framework of the bank.

Henerathgoda SANASA

Society Ltd

The bank plans to promote urban agricultural practices, home

gardening, etc. through the support of an agricultural instructor; The bank also plans to develop a loan scheme for the members

POTENTIAL ENTITIES FOR CONSIDERATION The more eager and potential entities (SANASA City Bank, People‟s Bank, and Wayamba Development Bank) were willing to partner with an external body to

formulate and implement strategies and programs for financing UA. However, the respondents raised issues such as the independence of the intermediaries and the

administrative cost (evaluation costs, monitoring costs, repayment-collection costs) of such programs that needs to be considered which many financial institutions did not like.

Table 4 indicates the views/opinions of the consultants about the institutions that showed potential and willingness to act as financial intermediaries for UA venture

within the GMC.

Table 6 – Features of potential financial institutions

Future Prospects for

Financing UA Current Practices Drawbacks

Bank of Ceylon

The BoC has potential

to develop and implement a financial

support program for

urban agricultural

producers given that such a program should be in line with its

current programs at the national level. Being a

national institution, it has been subjected to

the rules and regulations imposed by

the government, and as

“Agricultural

Farming – NRCS (New

Comprehensive

Rural Credit

Scheme)” – [Interest 8%; max = 500,000 (pre) to

5 million (post); repayment = 240

days; Agro Identity Card]

"Krushi Navodaya

Loan Scheme"

(KNLS) – [Interest

Inflexibility, lack of independence/initiative

to develop novel packages

19

JMUK Jayasinghe, 2009 | Confidential

result, there exists a less flexibility in terms of

administering a financial program by

the relevant branch. It is somewhat difficult to

develop a program that only caters to a

particular group of people such as those chillie cultivators in

Gampaha, because if there is any program

available, it may be a common program with

rigid requirements.

*%; 10,000 to 100,000;

repayment = 36 months / after

harvest]

Peoples Bank

The PB has potential and strong willingness to involve with

financing urban agricultural activities

within Gampaha. Like in all public financial

institutions, PB will also have to be compliance with the requirements

of the central governing body. Although PB can

be considered a financial institution

with strong financial stability and integrity and willing to support

agriculture in Sri Lanka, the local branch

at Gampaha is not in position to made own

decisions in this respect (i.e. lack of flexibility). The PB can only

provide financial support, mainly in

terms of credit, but could not go beyond

provision of other requirements for

Current programs

include: "Krushi Navodaya Loan

Scheme" (KNLS), "Forward Sales Contract" (FSC),

"Athamaru Loan Scheme" (ALS),

"Micro Finance Loans" (People's

Fast)

Inflexibility, cannot provide other facilities/requirements,

inability to develop innovative financial

packages without national-level

authorization

20

JMUK Jayasinghe, 2009 | Confidential

farmers, for example training, legal advice

etc.

Sampath Bank

Sampath Bank has a potential to finance UA,

given its present involvement with

"Cargills". However, our opinion is that it would like to provide

such loans on individual basis rather

than on groups/ clusters given the past

experiences related to pay back and defaults in agricultural loans. The

bank is culturally sensible and has a true

desire to invest in national development.

However is less flexible and able to provide only a limited financial

support.

"Cargills farmer

contract program"

Limited financial

support, lack of experience in dealing with group loans for

UA ventures

Wayamba

Development Bank

The WDB has willingness to involve in

a financial support program for urban

agricultural producers; however it is necessary for involvement of

higher authorities for

any extensive program.

There exists less flexibility in terms of

administering a financial program by the relevant branch,

although independent and experienced, there

is an issue with capabilities and

resources to develop

"Bahuvarshika Naya

Yojana Kramaya" –

(pineapple); "Kapruka

Sanwardhana Naya"

– (with the

Coconut

Development Authority -

intercropping/ under cropping in

coconut lands); "Krushi Navodaya";

"Pashu Sampath

Sanvardhanaya

(dairy cows)

Inflexibility, lack other resources (e.g. sufficient field officers,

etc) to implement program, limited

capability to develop novel services

21

JMUK Jayasinghe, 2009 | Confidential

and implement a successful scheme.

SANASA

City Bank Ltd

The SCB has a relatively higher

potential and ability; currently involved in

urban livelihood development, and has the inherent desire to

deal with urban producers and

agriculture in general and is already seeking a

prospective client to partner with. Further, the experience of

dealing within the Gampaha City, cordial

relationships with the farmer community and

highly flexible nature of the institution, together with its apparent

capabilities to develop and implement novel

financial packages / services for requested

agricultural projects, makes it a suitable financial institution to

consider. It also has

No standard packages, design customized

programs for entrepreneur‟s

requirements, interest rate and

repayment time can be decided jointly

Need to obtain membership

22

JMUK Jayasinghe, 2009 | Confidential

other facilities such as field officers and profit

sharing mechanisms.

COMPLEMENTARY SERVICES PROVISION It is generally accepted that support for UA needs to be an integrated approach where

financial services are complemented with training, marketing support, etc. In this light, this study also focused on identifying institutions that could provide these

complementary support services. They were assessed from both ends of whether they can provide minimal support services in addition to financing (e.g. availability of a

conference hall) to the fully fledged training providing institutions. Table 7 summarizes

the responses from the prospective entities.

Table 7 – Institutions that can provide complementary services

What other services will you able to provide for UAPs?

Wayamba Development

Bank

The bank has affiliations with external organizations/institutions that

are able to provide training programs, the good customers/clients of the bank can be directed / sent for these sessions/events

District Cooperatives

Rural Bank Union Ltd

Marketing support can be provided; The cooperative can undertake proposal evaluation for its members

SANASA City Bank Ltd

The City Bank can provide its 'Conference Hall' and other amenities which can be used to provide training sessions/seminars/workshops

for the urban producers; Furthermore other facilities such as annual bonding sessions, out door trips and recreational activities can be

organized / provided at subsidized rates for members

Henerathgoda SANASA

Society Ltd

The cooperative is able to provide subsidies for equipments, training, legal advice (during regular monthly meetings)

CIC Agri Businesses

CIC AB provides advisory/extension services for UAPs through

workshops, seminars, leaflets, internet, etc. Special workshops/training sessions are also conducted covering topics such as "Managing Limited Resources", "Cultivation Practices", etc. The

company is also able to tailor make advisory/extension programs; It is free of charge for producers who purchase inputs from the company;

For other special requests, charges apply: for e.g. 1 day program - Rs 2000 per head (without meals) - between 40 and 50 participants. Other

supportive divisions of CIC AB such as 'Agri Advisory Service' and 'Agri Education Tours' are also involved

23

JMUK Jayasinghe, 2009 | Confidential

SEEDS

Sarvodaya consists of three sections: SEEDS, MTI & REDS; MTI - provide training; REDS - market identifying, supporting (e.g.

Anthurium cultivation), even non-members can be trained and supported; Need to coordinate with the Enterprise Development

Office for this purpose

Here again we find that not many institutions have the capability to satisfy the training

needs of the urban producer. SEEDS and CIC Agri Businesses (Urban Agricultural Division) emerged as those that were able to provide other forms of services such as

training and workshops on special topics of interest for the UAPs. CIC AB has the greater capability out of the two for satisfying the training needs of the UAPs. However,

the drawback lies in that for specially designed workshops, they charge a payment.

Otherwise, for producers who are purchasing inputs from them they provide free advisory services.

At present CIC AB is involved in supporting home-gardening practices in urban areas

(such as Colombo) and also has the support of the corporate agribusiness firm and other extremely active divisions. SEEDS, on the other hand, are a not-for-profit, NGO whose theme is of rural upliftment. It also brings years of experience in working with rural

micro enterprise development and training of agricultural entrepreneurs. Both these institutions are willing to work with a coordinating body or association for the providing

services for the training needs of its growers.

A summary of key bottlenecks for financing UA is given in Table 8.

Table 8 – Key bottlenecks for financing UA

Key Bottlenecks Examples of FIs that exhibited this

bottleneck

Unaware of UA / Limited awareness of

UA

Most of the Licensed Commercial Banks

(Private), Licensed Specialized Banks (Private) and Finance Companies

Perception of financing agriculture, especially small-scale production as “risky”

Most of the Licensed Commercial Banks (Private)

Concerned about farmer behavior in

relation to repayment

Peoples Bank, Wayamba Development

Bank, Commercial Bank

Perceive that UA segment is small and unprofitable and/or does not match with

current strategic objectives

Commercial Bank, Nations Trust Bank

Lack of a potential entity to partner with / collaborate

SANASA City Bank Ltd, Wayamba Development Bank, Henerathgoda

SANASA Society Ltd

24

JMUK Jayasinghe, 2009 | Confidential

Standard financial products / inflexible nature of the FI / rigid rules and

regulations

Bank of Ceylon, Peoples Bank, Wayamba Development Bank

Targeting only large-scale commercial enterprises / mainly those that are

involved in the processing sector (“value addition & marketing”)

Commercial Bank, Hatton National Bank, Nations Trust Bank

Provision limited to geographic /

socioeconomic boundaries

Almost all Cooperatives, SEEDS

Concerns about independence and administrative costs

SANASA City Bank, Sampath Bank, Wayamba Development Bank, Peoples

Bank, Commercial Bank

Current economic recession / financial crisis coupled with the crashing of some reputed financial institutions recently in the

local context, creating a „cautious‟ / „risk averse‟ attitude

Most of the Licensed Commercial Banks (Private), Licensed Specialized Banks (Private) and Finance Companies

25

JMUK Jayasinghe, 2009 | Confidential

DEMAND FOR FINANCE FROM THE URBAN AGRICULTURAL

PRODUCERS (UAP) AND THEIR SPECIFIC CONDITIONS

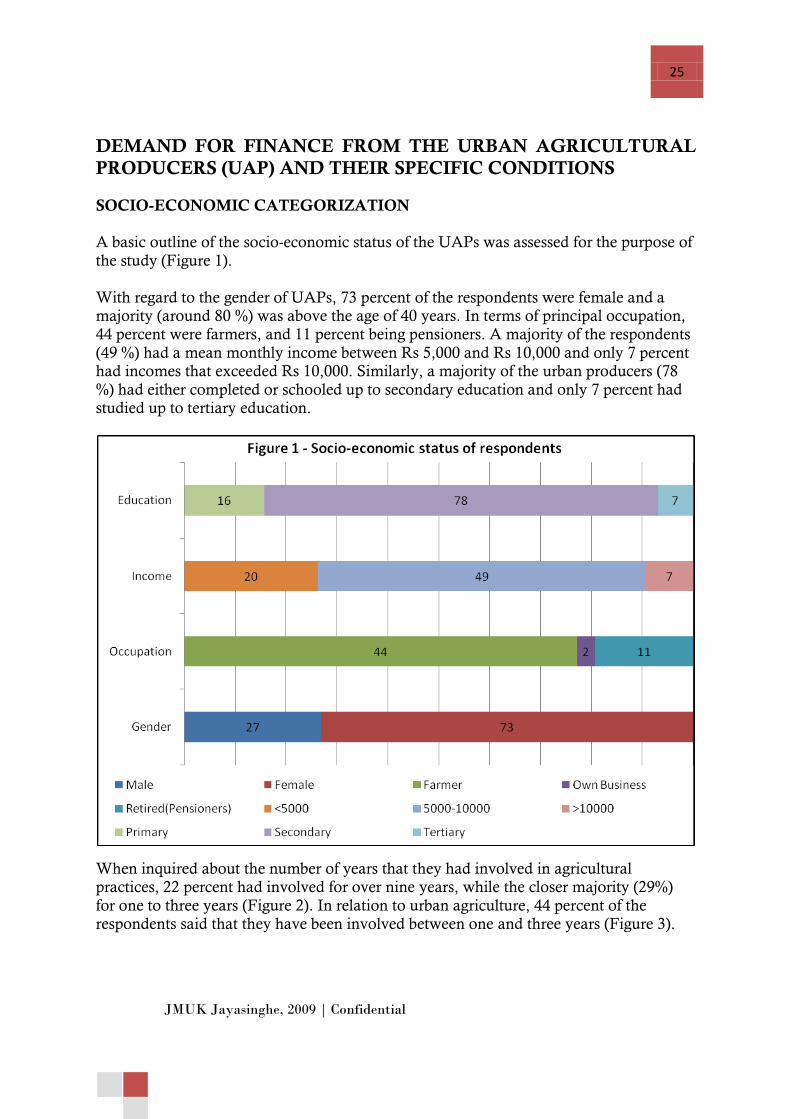

SOCIO-ECONOMIC CATEGORIZATION A basic outline of the socio-economic status of the UAPs was assessed for the purpose of

the study (Figure 1).

With regard to the gender of UAPs, 73 percent of the respondents were female and a majority (around 80 %) was above the age of 40 years. In terms of principal occupation,

44 percent were farmers, and 11 percent being pensioners. A majority of the respondents

(49 %) had a mean monthly income between Rs 5,000 and Rs 10,000 and only 7 percent had incomes that exceeded Rs 10,000. Similarly, a majority of the urban producers (78

%) had either completed or schooled up to secondary education and only 7 percent had studied up to tertiary education.

When inquired about the number of years that they had involved in agricultural practices, 22 percent had involved for over nine years, while the closer majority (29%)

for one to three years (Figure 2). In relation to urban agriculture, 44 percent of the respondents said that they have been involved between one and three years (Figure 3).

26

JMUK Jayasinghe, 2009 | Confidential

27

JMUK Jayasinghe, 2009 | Confidential

FINANCING MEANS, METHODS AND PERCEPTION The UAPs have mainly utilized their “own funds and savings” (72%) for agricultural

practices, with virtually none having accessed formal sources for this purpose (Figure 4). Informal sources have been tapped by nearly one fourth (28%) as well. Many farmers

have utilized their own incomes (from pensions, savings, profit from cultivation of other crops, etc.) for financing their UA venture.

The reasons for this vary among the respondents, from being „private reasons‟ for not obtaining funds (33%) to „strict requirements‟ for obtaining credits/loans (11%). However, several common constructs emerged that reflected their perception. A primary

element being that, formal FIs are “strict” and project an “unfriendly environment” towards growers (18%). Complains extend to the limit that they are unaware of any

suitable financial product and/or its providers (14%). Another interesting personal issue for the UAPs was about their “dignity and self-respect” in relation to obtaining funds

from FIs; some of the growers raised this issue, indicating that they feel uncomfortable

when accessing a FI such as a reputed public/private bank to obtain loans for their agricultural activities (21%) (Figure 5).

28

JMUK Jayasinghe, 2009 | Confidential

When inquired deeply for reasons for these issues, a common response was that they do

not have a “good relationship” with the FIs and that the FIs tend to overpower them. A good majority indicated that they were unable to understand the existing financial

packages/services offered by institutions, especially because they have no prior experience of utilizing them fully. When asked “what was their opinion about financial institutions in terms of their past experiences” (Figure 6), 18 percent of the respondents

indicated that they were subjected to risks and about 10 percent reported that they faced numerous challenges when accessing the FIs, including higher interest rates, coupled

with unclear specifications and conditions, together with the fact that many existing packages were not in line/ not in sync with their cultivation practices.

FINANCIAL REQUIREMENTS The responses from the UAPs, with regard to a „suitable‟ financial package for their venture, were symptomatic of the need for flexibility (55%), both in relation to obtaining

financial support and paying it back. Lower interest rates (67%); ability to pay back after harvest (48%), and recognition of farmer group/cluster members‟ mutual guarantees

(33%) were mentioned, amongst the others, as their key requirements. There was no

29

JMUK Jayasinghe, 2009 | Confidential

particularly preferred form of financial support; credit/loan schemes were accepted, nevertheless, there were certain preferences for subsidy schemes and grants (Figure 7).

When asked to specify in what areas/forms they needed financial assistance, the

following (essential) inputs emerged: equipments (53%), fertilizer (46%) and pesticides (11%). The respondents especially highlighted their need for a support scheme in

obtaining/purchasing fertilizer (e.g. Muriate of Potash).

The stability of the FI was also considered important. Furthermore, they mentioned the recent crash of FIs in a local context (e.g., Ceylinco/Golden Key Scandal, “Sakvithi” Scam

etc.) and preferred to deal with a reputable bank than other entities.

SPECIAL CONSIDERATIONS

The UAPs requested other forms of assistance from intermediaries such as training (both technical and business related skills), which was requested by 64 percent of the UAPs,

Legal Advice (24%) and Marketing Support (29%). Here the responses made feel that strong focus needs to be made, especially with regard to a proper extension/technical

(agronomical/crop management) support system (Figure 8).

30

JMUK Jayasinghe, 2009 | Confidential

Furthermore, other forms of skill development namely, business management skills, leadership development, marketing orientation improvement, were preferred. Support

for marketing activities was a recurring point in the sessions and a considerable number of respondents were aware of the importance of agri-food marketing for the success of

their UA enterprises. In addition to this, certain structural recommendations were made. Some of these were

common collective suggestions, such as: need for proper communication mechanism with the institutions/entities they obtain support/assistance from and the FI to be an

agricultural community-level involved entity. Others were from minor groups and certain individuals, such as: involvement with a state bank, regulation that only officials

of the UA enterprise should deal with the bank and provision of allowances (travel, telephone, etc.) to the officials. Existing literature on financing UA indicates the need for community participation the importance of the role of both FIs and UAPs in

funds/resource management. In this regard respondents were asked to state their views on a few broad ranges of topics/issues, such as level of autonomy for FIs, level of

government control/supervision, whether they had any opinions on the primary source of resources, and the distribution of resources among UAPs, etc. Around 33 percent

were in favor of an independent financial intermediary. With respect to government supervision, majority preferred involvement at District level (16%) and then at

Municipality level (12%). With regard to the issue of the role of UAPs in the management of funds/resources, opinions varied. It was observed that certain

individuals demanding complete control, whilst the majority preferring responsible

involvement in any funds/resource management system.

31

JMUK Jayasinghe, 2009 | Confidential

PROPOSALS AND RECOMMENDATIONS TO CREATE A MORE

ENABLING/FACILITATING FINANCING ENVIRONMENT FOR

SMALL-SCALE URBAN PRODUCERS

Based on the analysis of information obtained through structured interviews

supported by the interview schedule, the following recommendations can be made:

“LCBs (both public and private)”, “LSBs (public)” and “Cooperatives” are

preferred, in general, over the “LSBs (private)”, “Finance companies” and “other Potential institutions” (excluding, SEEDS).

Out of the LCBs (private), both Commercial Bank (CB) and Sampath Bank (SB)

have the potential to finance UA activities in Gampaha, but Sampath Bank is leading.

Out of the LCBs (public) and LSBs (public), Bank of Ceylon (BoC), Peoples’ Bank

(PB), Wayamba Development Bank (WDB) and SANASA City Bank (SCB) are the

potential institutions.

LCBs (public) and LSBs (public) can be recommended over LCBs (private), or

in other words: BoC, PB, WDB and SCB is better than CB and SB.

Out of the three public banks listed above, i.e. BoC, PB and WDB, all three are

in good standing to finance UA, however, in my opinion, the PB and WDB are

more suitable as they displayed their willingness and to explore new ways. Both banks were willing to persuade their top management to come up with a suitable

program for farmers, there by engaging in innovative ways of banking. The BoC

came across as being a little bureaucratic and the respective branch is less willing to deal in this regard as it needs the approval from the head office in Colombo

The most potential public bank is the PB. The manager of this bank had

expressed a very positive attitude towards in UA in general and being experienced in dealing with financing rural agriculture in other provinces of Sri Lanka. It

currently deals with the small enterprises or lower income groups in the district. In comparison to the PB, the WDB lacks related staff and lesser capacity to be

involves in financing activities.

Out of the Cooperatives, all except “Gampaha Multi Purpose Cooperative Society” (GMPCS), which was facing an internal crisis at the time of this study,

were willing to and had the capacity to finance UA programs.

SCB, Henarathgoda SANASA Society (HSS) and District Cooperatives Rural Bank Union Ltd. (DCRBU) were willing to finance UA programs, but the first

two institutions were more “eager” to participate by designing an appropriate

financial package by them. The HSS deals with a huge customer base; facilities

32

JMUK Jayasinghe, 2009 | Confidential

are limited for those within a specific region within the Gampaha City; lack of field officers and “nontransparent” financial resources (no clear accounting

details and lack of reliable financial controls, with financial management decisions being completely under the preview of a small number of individuals)

make it an unlikely candidate over and above the SCB. DCRBU has not shown any reason to select over the SCB, based on my observations.

I have observed that the SCB as an institution with the highest potential and

ability. Currently, it is functioning according to a rigid framework of urban livelihood development, has the inherent desire to deal with urban producers and agriculture in general, and is already seeking prospective clients to collaborate.

Further, the experience of dealing within the Gampaha City, cordial relationships with the farmer community and highly flexible nature of the institution, together

with its apparent capabilities to develop and implement novel financial packages/services for requested agricultural projects, makes it a suitable financial

institution to consider. In comparison to other FIs, and amongst the Cooperatives in particular, it also has other facilities such as field officers and profit sharing

mechanisms

“SEEDS” is also willing to participate in designing a package, but it is constrained by its current policy framework, as approval for such a project

requires the change of its Strategic Action Plan, which, I believe, at this moment, would not be compatible with the principles/plans of the RUAF.

Finally, by considering all above, I would like to name the following FIs

to design and finance urban agricultural activities in Gampaha, IN

ORDER:

1. SANASA City Bank Ltd.

2. People’s Bank

3. Wayamba Development Bank

33

JMUK Jayasinghe, 2009 | Confidential

LIMITATIONS OF THE STUDY AND PROBLEMS ENCOUNTERED Some of the key problems that the consultant faced in carrying out this study are pointed

below:

Non-participation of certain financial and other potential institutions for the study

citing various reasons such as lack of interest in agricultural/urban agricultural projects and there is “no incentive” for participation.

Discussions were limited to 15-20 minutes, on an average, for the most cases

especially with LCBs and LSBs as they were “so busy” with their regular

customers. Because of this, it was not possible to dwell deeply on descriptive

shallow issues and cover wider areas, both conceptually and physically.

It was difficult to obtain facts to prove certain claims as many things were

“confidential” and cannot be released to outsiders.

The scope and focus was limited to the facts explored in the ToR and the

Structured Interview Schedule developed in turn.

Given the exploratory nature of the study, there could be issues that could create problems / errors in the final analysis and recommendations of the consultants;

most of the output obtained is qualitative information, and interpretation of such findings is typically based on the judgment of the consultant: thus the conclusions may be biased at times.

Lobbying among some banks was evident, as revealed from the responses given by the institutions. Some may have been discouraged in the process.

Given the recent financial turmoil in the local context, the response of institutions

as well as, to a limited extent, the producers could be cautious and more risk averse than earlier / usual.