Embed Size (px)

Citation preview

Fatou AssahSenior Financial Sector specialistSenior Financial Sector specialistThe World BankApril 2012

1

p

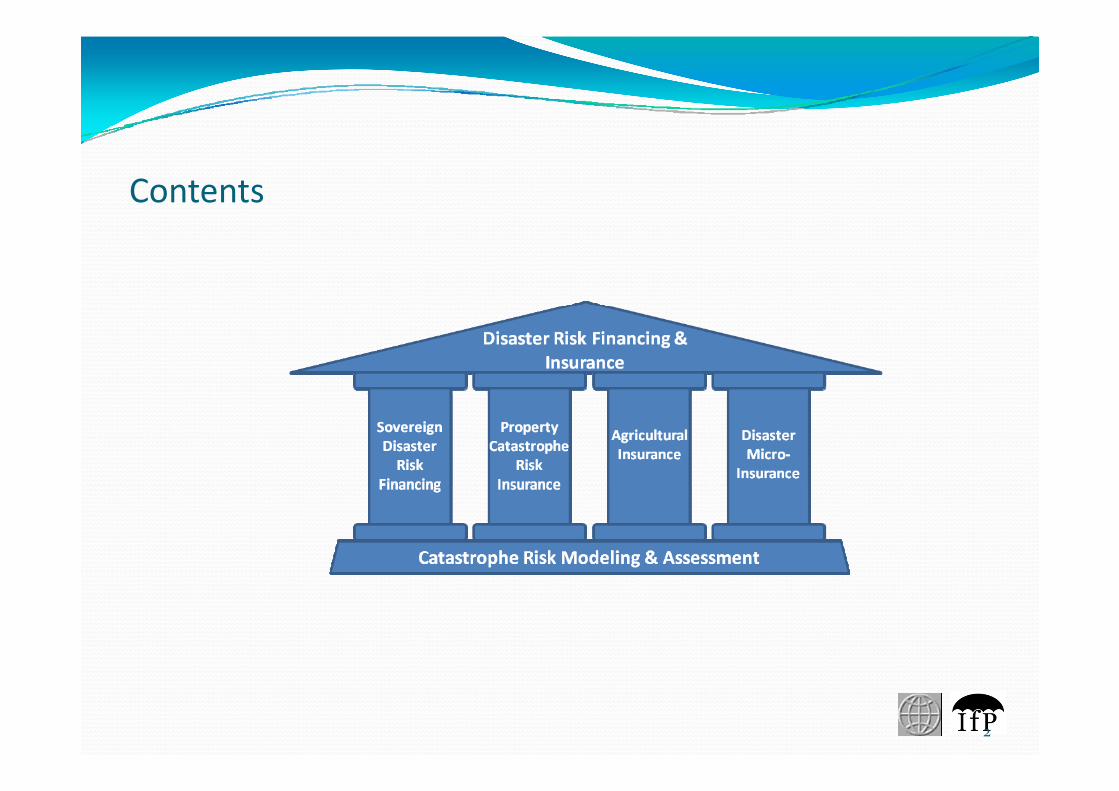

Contents

2

Disaster Risk Management FrameworkDisaster Risk Management Framework

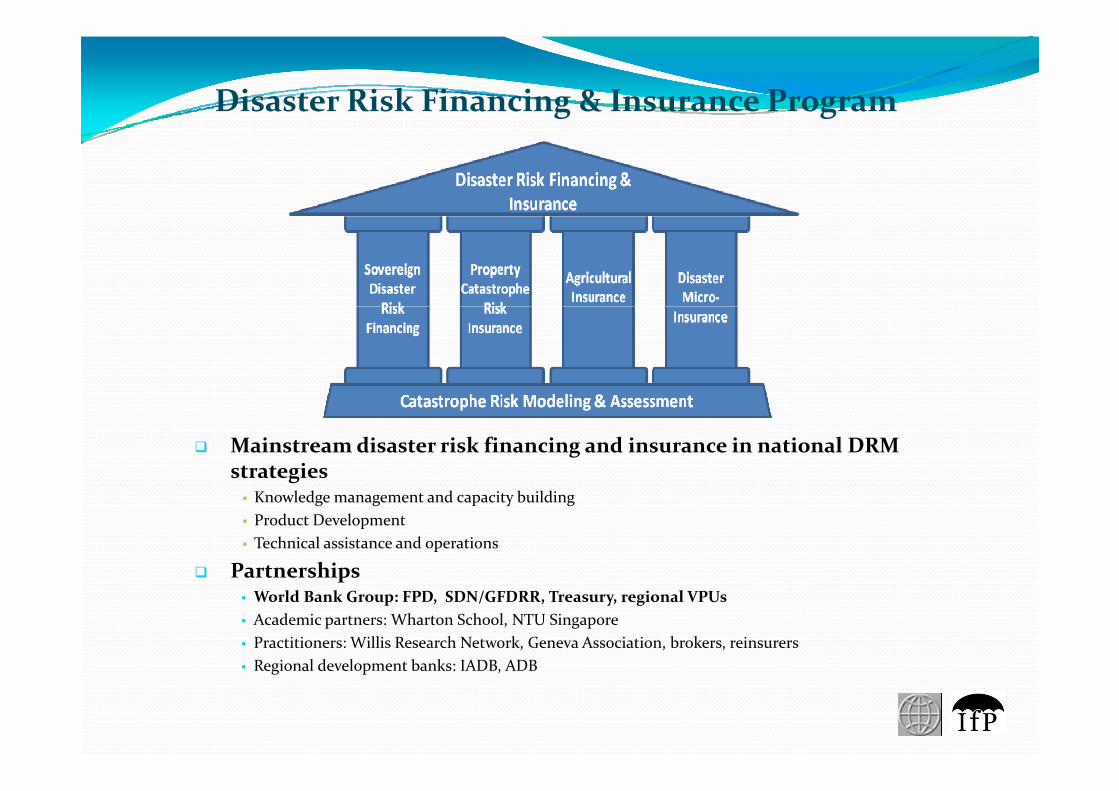

Disaster Risk Financing & Insurance Program

Mainstream disaster risk financing and insurance in national DRM strategies

Knowledge management and capacity buildingProduct DevelopmentTechnical assistance and operations

PartnershipsPartnershipsWorld Bank Group: FPD, SDN/GFDRR, Treasury, regional VPUsAcademic partners: Wharton School, NTU SingaporePractitioners: Willis Research Network, Geneva Association, brokers, reinsurersRegional development banks: IADB ADBRegional development banks: IADB, ADB

World Bank DRFI products and servicesCatastrophe

Bond(CAT Bond)

Insurance‐Linked

Securities

Recently launched a multi‐country, multi‐peril catastrophe bond platform to pool and transfer risks to the capital markets. Mexico has issued a USD 290 million bond to protect against earthquake and hurricane risk.

Major

Low

Risk Tran

Insurance against weather‐related losses, based on an index –Global Index Insurance Facility (GIIF)Weather

Insurance

Malawi Drought Hedgent pa

ct nsfer

CaribbeanCatastrophe

Risk InsuranceInsurance Parametric insurance against natural disasters

WBG Assisted 16 Caribbean Countries in

WBG provided Malawi its first‐ever weather risk management contract to protect against the risk of severe drought

Hedge

bility of E

ven

verity of I

mp

Re

Risk InsuranceFacility (CCRIF)

PoolsWBG Assisted 16 Caribbean Countries in establishing CCRIF against hurricanes and earthquakes

Catastrophe Risk

Pro

bab

Sev

Risk etention

Catastrophe Risk Deferred

Drawdown Option(CAT DDO)

Contingent Loans

Provides immediate liquidity following a natural disaster, in the form of a contingent loan with associated risk framework reforms

MinorHigh

A few WB Disaster Risk Financing & Insurance Projects

Mongolia –Index‐based livestock

C ibbTurkey –E h k

Index‐based livestock insurance

Morocco –C i

ASEAN –Di Ri k Caribbean –

Regional insurance pool

Mexico –Catastrophe bond

Guatemala –

Earthquake insurance pool

Africa – India –A i lt l

Cat insurance law

Disaster Risk Financing & Insurance Review

GuatemalaContingent creditCost Rica–

Public Assets Cat Risk Transfer

Pan‐African drought risk pool

Malawi –Macro and micro

Agricultural insurance TA

Indonesia–National disaster risk financing strategy

Macro and micro schemes Pacific Islands –

Pacific Catastrophe Risk Assessment and Financing Initiativeg

Sovereign Disaster Risk

O i Fi i l t t i t i th

Sovereign Disaster Risk Financing

• Overview: Financial strategies to increase the financial response capacity of governments in th ft th f t l di t hil

Sovereign

the aftermath of natural disasters, while protecting their long‐term fiscal balances

• Primary beneficiaries: National & local Sovereign Disaster Risk

Financing

• Primary beneficiaries: National & local governments

• Product/Service lines:Financing • Product/Service lines:• Technical assistance (TA) in ex ante budget planning for natural disasters• Contingent financing (DPL with Cat DDO)• Sovereign catastrophe insurance pools (e.g., CCRIF)• Insurance‐linked securities (e.g., cat bonds, weather ( g , ,derivatives)

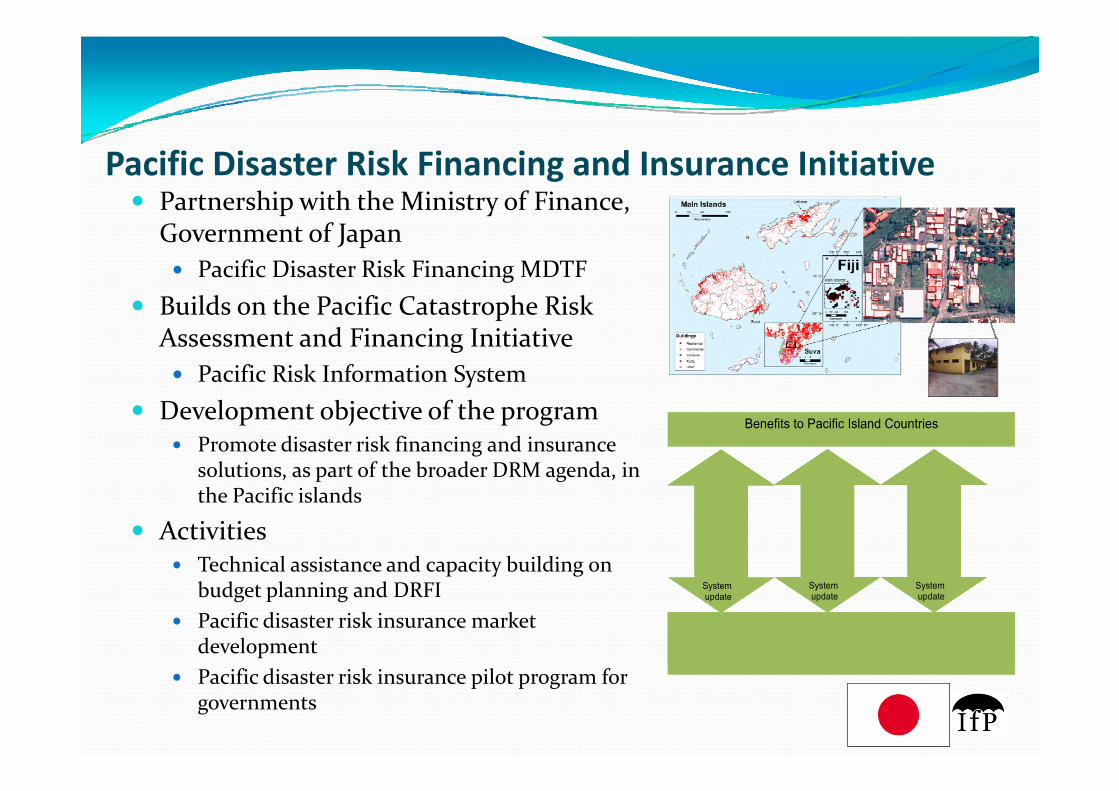

Pacific Disaster Risk Financing and Insurance InitiativePartnership with the Ministry of Finance, p yGovernment of Japan

Pacific Disaster Risk Financing MDTFBuilds on the Pacific Catastrophe Risk Builds on the Pacific Catastrophe Risk Assessment and Financing Initiative

Pacific Risk Information SystemDevelopment objective of the program

Promote disaster risk financing and insurance solutions, as part of the broader DRM agenda, in the Pacific islands

ActivitiesTechnical assistance and capacity building on p y gbudget planning and DRFIPacific disaster risk insurance market developmentPacific disaster risk insurance pilot program for governments

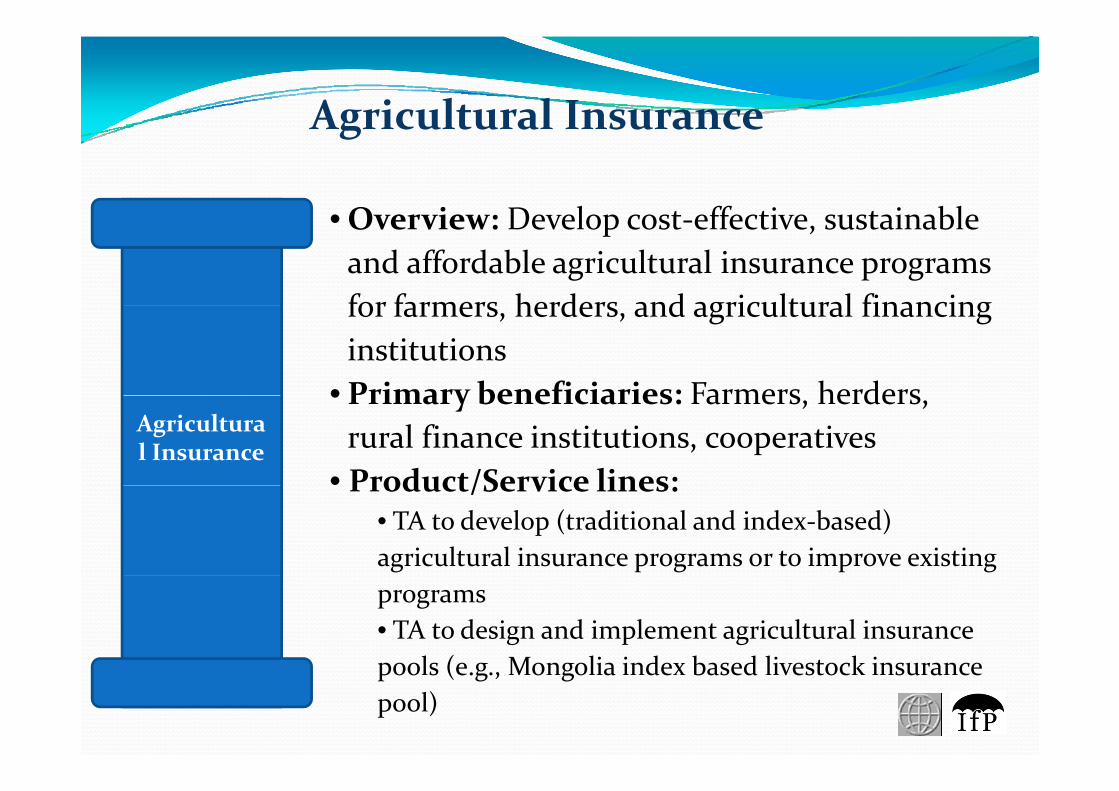

Agricultural Insurance

• Overview: Develop cost effective sustainable

Agricultural Insurance

• Overview: Develop cost‐effective, sustainable and affordable agricultural insurance programs for farmers herders and agricultural financing for farmers, herders, and agricultural financing institutions

• Primary beneficiaries: Farmers herders Agricultural Insurance

• Primary beneficiaries: Farmers, herders, rural finance institutions, cooperatives

• Product/Service lines:Product/Service lines:• TA to develop (traditional and index‐based) agricultural insurance programs or to improve existing programs• TA to design and implement agricultural insurance pools (e g Mongolia index based livestock insurance pools (e.g., Mongolia index based livestock insurance pool)

d ’ l l l h ( )India’s National Agricultural Insurance Scheme (NAIS)World Bank assistance in modification of the NAIS – the largest crop insurance scheme in g p

the worldThe National Agricultural Insurance Scheme has been in place since 1999 and uses an area yield‐based index approachThe Government requested assistance from the World Bank in strengthening the scheme to reduce delays in claims payments and to reduce delays in claims payments and to increase take‐upIn 2010 the government approved a plan to move to a modified NAIS scheme on a pilot ove to a od ed S sc e e o a p otbasis, reflecting many of the recommendations from the World Bank’s technical assistanceOne key modification is the introduction of a weather index insurance product to complement the area yield‐based coverUse of mobile phone technology to improve data quality and expedite data transfer of crop data quality and expedite data transfer of crop cutting experiments (CCEs) [2011 WB Innovation Award]

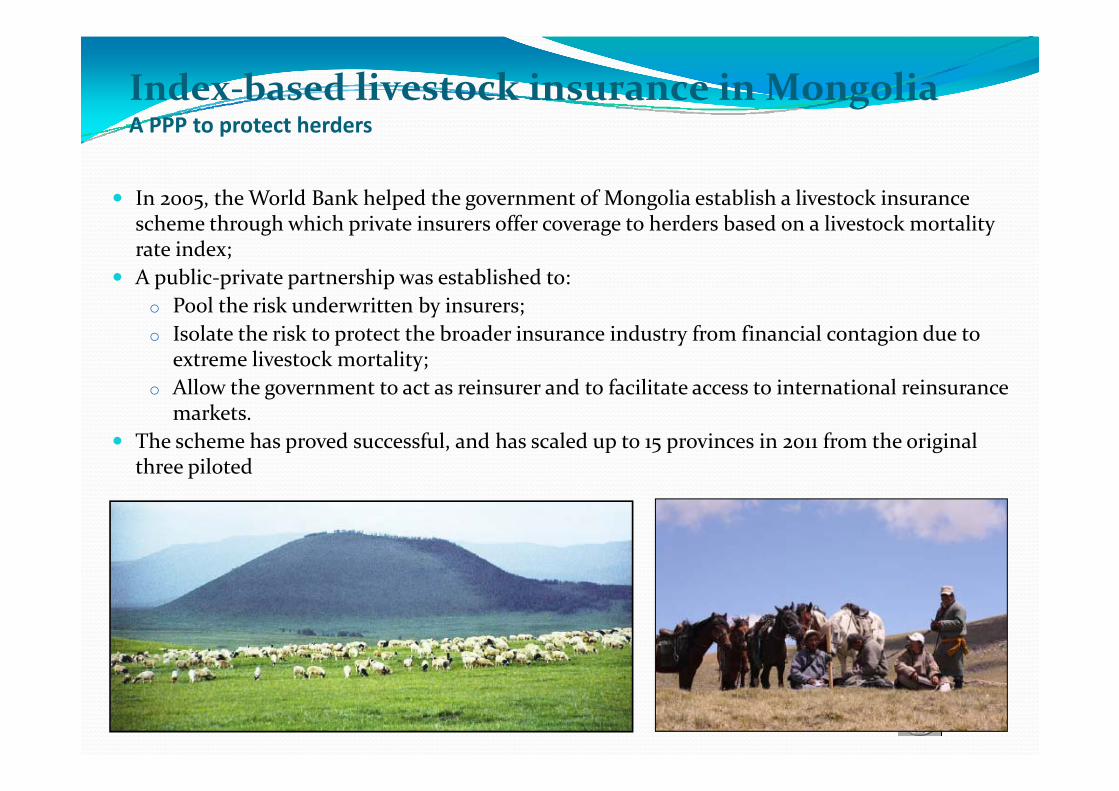

Index‐based livestock insurance in MongoliaA PPP to protect herdersA PPP to protect herders

In 2005, the World Bank helped the government of Mongolia establish a livestock insurance h h h hi h i i ff h d b d li k li scheme through which private insurers offer coverage to herders based on a livestock mortality

rate index;A public‐private partnership was established to:

o Pool the risk underwritten by insurers;o Pool the risk underwritten by insurers;o Isolate the risk to protect the broader insurance industry from financial contagion due to

extreme livestock mortality;o Allow the government to act as reinsurer and to facilitate access to international reinsurance g

markets.The scheme has proved successful, and has scaled up to 15 provinces in 2011 from the original three piloted

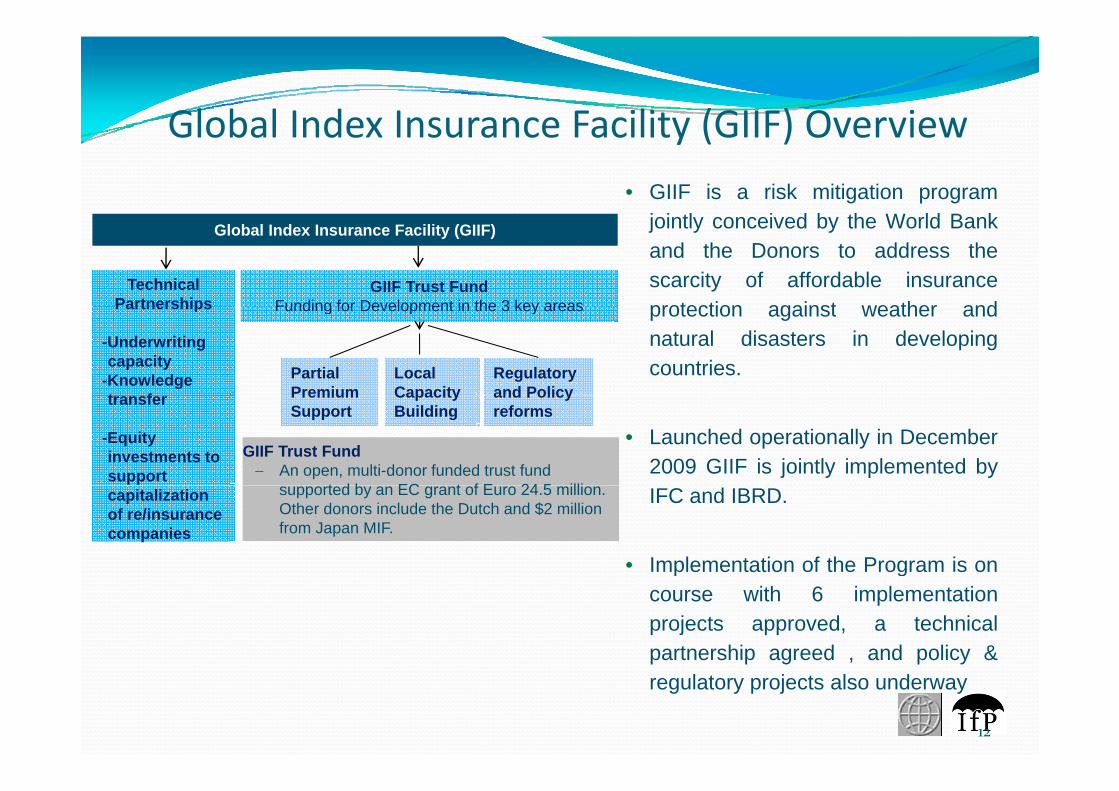

Global Index Insurance Facility (GIIF) OverviewGlobal Index Insurance Facility (GIIF) Overview • GIIF is a risk mitigation program

j i tl i d b th W ld B k

GIIF Trust FundFunding for Development in the 3 key areas

Global Index Insurance Facility (GIIF)

Technical Partnerships

jointly conceived by the World Bankand the Donors to address thescarcity of affordable insuranceprotection against weather andFunding for Development in the 3 key areas

Regulatory and Policy

Local Capacity

Partnerships

-Underwriting capacity

-Knowledge t f

Partial Premium

protection against weather andnatural disasters in developingcountries.

and Policy reforms

GIIF Trust Fund− An open, multi-donor funded trust fund

t d b EC t f E 24 5 illi

Capacity Building

transfer

-Equity investments to support

Premium Support

• Launched operationally in December2009 GIIF is jointly implemented by

supported by an EC grant of Euro 24.5 million. Other donors include the Dutch and $2 million from Japan MIF.

capitalization of re/insurance companies

IFC and IBRD.

• Implementation of the Program is onp gcourse with 6 implementationprojects approved, a technicalpartnership agreed , and policy &

12

regulatory projects also underway

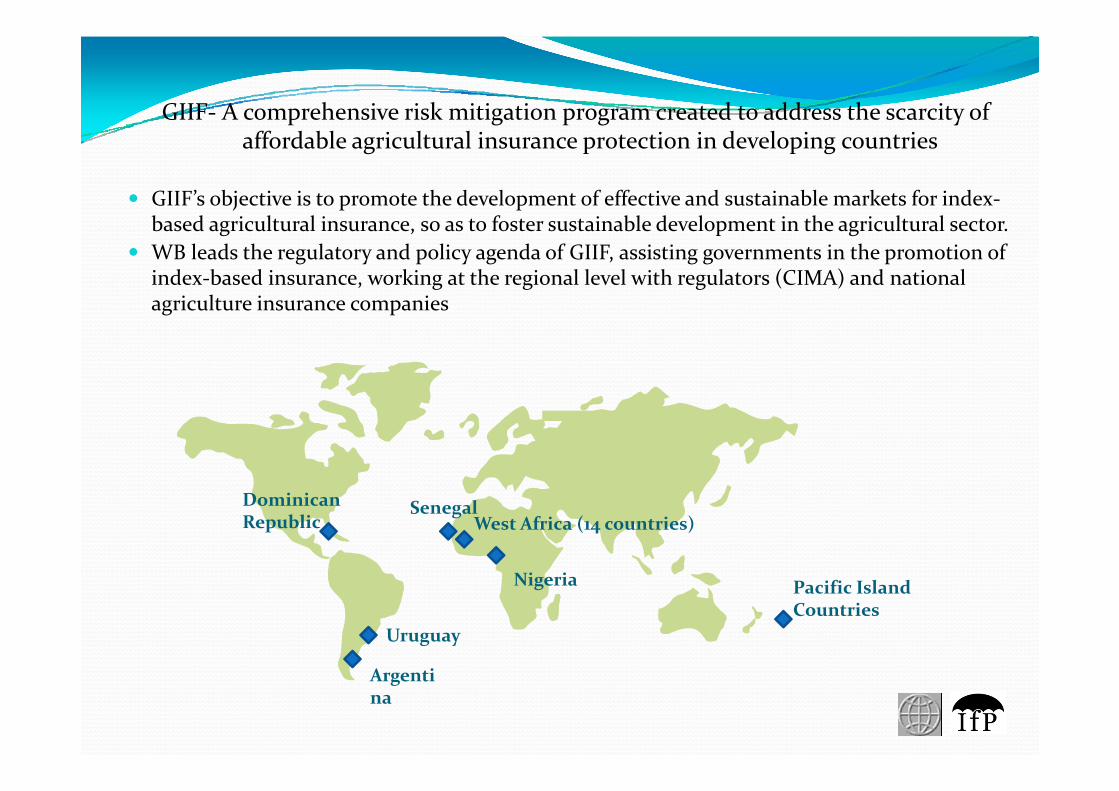

GIIF‐ A comprehensive risk mitigation program created to address the scarcity of affordable agricultural insurance protection in developing countries

GIIF’s objective is to promote the development of effective and sustainable markets for index‐b d l l f bl d l h l lbased agricultural insurance, so as to foster sustainable development in the agricultural sector.WB leads the regulatory and policy agenda of GIIF, assisting governments in the promotion of index‐based insurance, working at the regional level with regulators (CIMA) and national agriculture insurance companiesagriculture insurance companies

Ni i

West Africa (14 countries)SenegalDominican

Republic

Pacific Island Countries

Nigeria

Uruguay

Argentina

Snapshot of sub‐project results in ACP1. The Syngenta Foundation for Sustainable Agriculture and UAP Insurance in Kenya:

• 21,000 farmers insured, through a successfully partnership between the project,Agriculture input shops and an MFI The project has successfully deployed anAgriculture input shops and an MFI. The project has successfully deployed aninnovative mobile platform, for product distribution and administration.

2. The International Livestock Research Institute in Kenya:2 600 t t h b i d 20 000 li t k it i d i t d ht i• 2,600 contracts have been issued, 20,000 livestock units insured against drought innorthern Kenya.

3. MicroEnsure in Rwanda:• 935 farmers insured during the pilot season, 88 MFI and banking personnel trained on

index insurance in Rwanda.

4. PlaNet Guarantee – 7 countries in Francophone West Africa:4. PlaNet Guarantee 7 countries in Francophone West Africa:• 3 product pilots launched across 2 countries, regional index insurance hub for West

Africa established in Dakar, 679 farmers insured under the initial pilots.

5 Guy Carpenter in Mozambique:5. Guy Carpenter in Mozambique:• Data collection finalized, product modeling underway, workshop and product launch

planning for 2012 has commenced.

14

• In October 2011, the ILRI Livestock Insurance program, to which GIIF is Insurance program, to which GIIF is providing premium support, made its first indemnity payments to drought afflicted livestock herders in N h KNorthern Kenya

• The project has insured 2,600 households and 20,000 livestock head to dateead to date

• The payouts hugely improve awareness and trust in the product

15

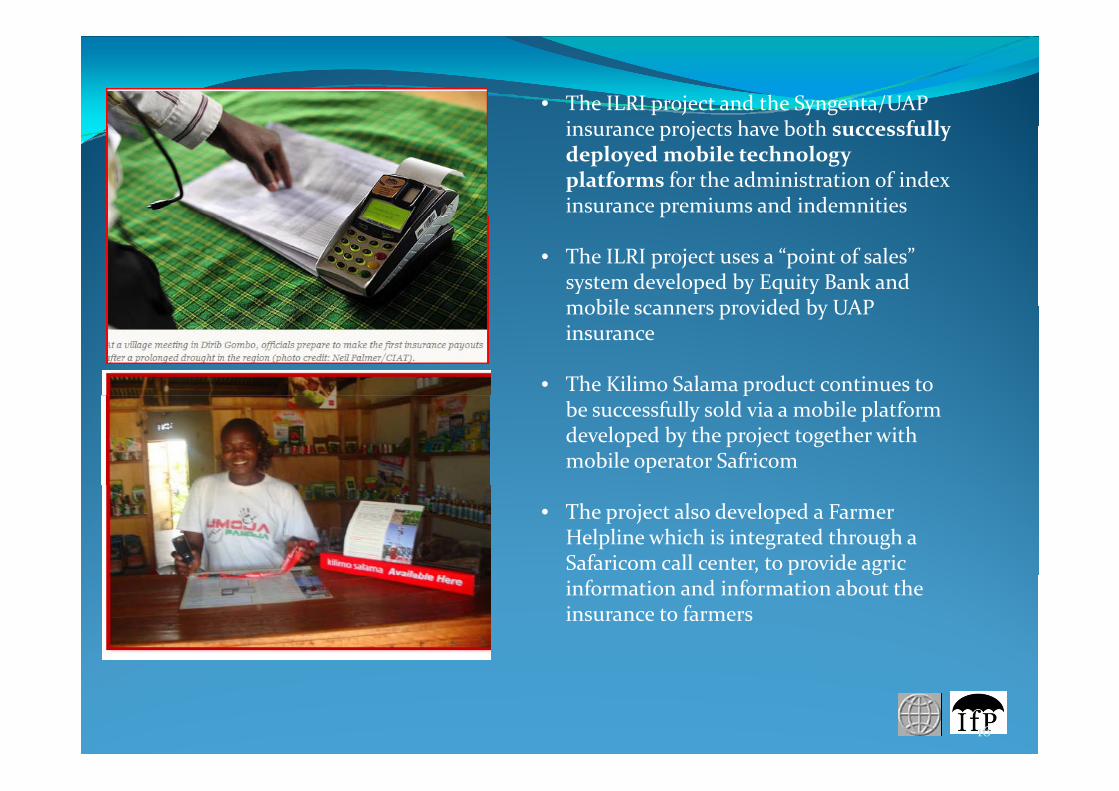

• The ILRI project and the Syngenta/UAP insurance projects have both successfullyinsurance projects have both successfullydeployed mobile technology platforms for the administration of index insurance premiums and indemnities p

• The ILRI project uses a “point of sales” system developed by Equity Bank and mobile scanners provided by UAP mobile scanners provided by UAP insurance

• The Kilimo Salama product continues to pbe successfully sold via a mobile platform developed by the project together with mobile operator Safricom

• The project also developed a Farmer Helpline which is integrated through a Safaricom call center, to provide agric information and information about the insurance to farmers

16

Lessons learnt on first generation weather indexLessons learnt on first generation weather index insurance (Malawi, Mongolia, China) (1)Weather index insurance for small farmers in developing countries is still Weather index insurance for small farmers in developing countries is still new:

Initial results of pilots have been mixed (often low voluntary demand/up‐take)Sustainability and scalability are not yet proven.

Weather index insurance is not a panacea:Can only enhance existing agricultural supply chains and businesses not create Can only enhance existing agricultural supply chains and businesses, not create themIt can help support expansion in rural finance and agricultureI h d i h d i h h i i i i i i i It must go hand in hand with other investments in extension services, irrigation, strengthening of input and output markets, other financial services and products etc.

No one size fits all agricultural insurance products:No one‐size‐fits‐all agricultural insurance products:There is not only one suitable crop insurance product for all situationsIndemnity‐based or index‐based products must be fitted to local circumstancesy pWeather index insurance is one risk transfer product to be considered according to the crop type, key peril exposure, data availability, farmer size, delivery channels, loss adjustment needs.

Lessons learnt on first generation weather indexLessons learnt on first generation weather index insurance (2)Sustainability and scalability will not be achieved unless operational hurdles Sustainability and scalability will not be achieved unless operational hurdles can be overcome:

Robust product delivery channels to farmers, linkages to finance or supply chain with additional farmer products and services (“Bundling”)p ( g )Local ownership through capacity building and technology transfer for all actorsStrong local partners and incentives

Just as important for scalability (if not more) than technical hurdles:Just as important for scalability (if not more) than technical hurdles:Investment in data and weather infrastructureInvestment in training and capacity building for farmers and insurance companiesSynthesizing best practices for contract design, insurance and reinsuranceFavourable regulatory framework

Meso and macro‐level applications of WII merit greater attention:Meso and macro level applications of WII merit greater attention:Meso‐level coverage as a means of enhancing famers access to rural finance (through banks and input suppliers/pre‐financiers)Macro‐level coverage for governments as a means of food security, and ex‐ante Macro level coverage for governments as a means of food security, and ex ante weather‐induced disaster risk financing.

GIIF‐Early Lessons in Implementation y pKey factors for developing index insurance

Challenges in moving forward with index insurance

1. Sufficient quality and quantity of historical weather data and adequate infrastructure

1. Availability and quality of weather data and weather measuring infrastructure

2. Technical capacity of local institutions tod l i d i d t

2. Adequate capacity building for local institutions to develop the needed technical skills to analyze risks and

develop index insurance products3. Ability to raise awareness amongst

beneficiaries (e.g. farmers, rural households, etc.)

develop, price and distribute appropriate and affordable insurance products

3. Awareness raising and training for b fi i i ll d t

households, etc.)4. Distribution channels to reach beneficiaries

in a cost efficient manner5. Cost of insurance and the ability and beneficiaries as well as product

marketing campaigns4. Best if insurance is offered as part of

wider package of financial services

5 Cost o su a ce a d t e ab ty a dwillingness to pay for insurance premiums

6. Climate change and uncertainty about weather events

wider package of financial services5. Enabling legal and regulatory

environment for index insurance products

19

products

Disaster Microinsurance Disaster Microinsurance

• Overview: Facilitate access to disaster insurance products to protect the livelihood of h l d d

Disaster

the poor against natural disasters and promote DRR in conjunction with social programsP i b fi i i L i Disaster

Micro‐insurance

• Primary beneficiaries: Low‐income populationsP d t/S i li• Product/Service lines:

• TA to develop disaster insurance products and programs appropriate for low‐income populationsprograms appropriate for low income populations

Property Catastrophe Risk

• Overview: Develop competitive and sustainable

p y pInsurance

• Overview: Develop competitive and sustainable catastrophe insurance markets and increase property catastrophe insurance penetration

Property

• Primary beneficiaries: Households, small‐ and medium‐enterprises; national governments

Property Catastroph

e Risk Insurance

• Product/Service lines:• TA to promote property catastrophe insurance of public dwellingspublic dwellings• TA to promote property catastrophe insurance of private dwellings• TA to establish national (regional) insurance or reinsurance pools to facilitate development of domestic (regional) propert catastrophe insurance domestic (regional) property catastrophe insurance markets

THANK YOU

22