Embed Size (px)

Citation preview

Argon ST

Company Overview

March 2009

Slide 2

Safe Harbor Statement With the exception of historical information, the statements set forth in this presentation include forward-looking statements that involve risk and uncertainties. The company cautions that a number of important factors could cause actual results to differ materially from those forward-looking statements. These and other factors which could cause actual results to differ materially from those in the forward-looking statement are discussed in the company’s filings with the Securities and Exchange Commission, including its filings on forms S-4, 10-Q, and 10-K, including the most recent 10-Q dated February 6, 2009. The company also cautions that any guidance referred to herein is as of December 4, 2008 as re-affirmed February 5, 2009 and this presentation should not be regarded as an update.

Slide 3

Argon OverviewLeading developer of command, control, communicatio ns, computers,

combat systems, intelligence, surveillance, and rec onnaissance (C5ISR) systems

Corporate Headquarters Fairfax, VA

Ownership Public: NASDAQ (STST)

Founded 1997 Argon Engineering Assoc., Inc.

Fully Diluted Shares Approximately 22.0 million

Insider Ownership Approximately 40%

2008 Revenue $341 million

2009 Revenue Guidance $375 to $395 million

Key Programs SSEE, BLQ-10, SSTD, OT-TES,EP-3E/Guardrail modernization

Slide 4

Making Sense of it AllOur systems gather and deliver data, turn it into u seful and timely

intelligence, and allow the user to take decisive a ction

• We design, develop, and deploy – Sensors and countermeasures – Information operation and electronic attack systems

– Communication systems and networks

– Navigation systems– Geolocation systems

– Integrated net centric systems with the above capabilities

• These systems allow users to – Find, fix, track, target, engage, and assess the threat– Develop situational awareness and understanding

– Deliver the intelligence to make decisions

– Deny understanding of the environment to our enemies

Slide 5

Argon Value PropositionStrong technical achievements, employee skill sets, and customer

relationships create barrier to entry in our market

• Our engineers build complex ISR systems that requir e teams of engineers with high skill levels and clear ances– Demonstrated ability to deliver (more systems than competitors)– Low turnover of personnel

• The ISR market requires continuous refresh of syste ms as threat environments change and this market is growi ng in importance as a necessity in asymmetric warfare

• We have strong customer relationships and receive a significant amount of sole source business

• We continue to have growth opportunities with custo mers that have sustainable budgets and ability to pay

Slide 6

Argon Has Strong Investment CriteriaWe are a quality defense contractor in the C5ISR ma rket segment

with unique capability and demonstrated growth

• Argon’s objective is to be a national asset– We participate in programs of national importance– Our technical capabilities are recognized as world-class– We are a premier C5ISR company– Well positioned in SIGINT

• Significant backlog weighted toward desirable class ified work

• Strong opportunity pipeline in the ISR sector is st rong and growing

• Double digit top-line growth targets– Organic growth and disciplined acquisitions– Increased market share and growth of C5ISR market

– Proven and incented management team with significan t industry experience

Slide 7

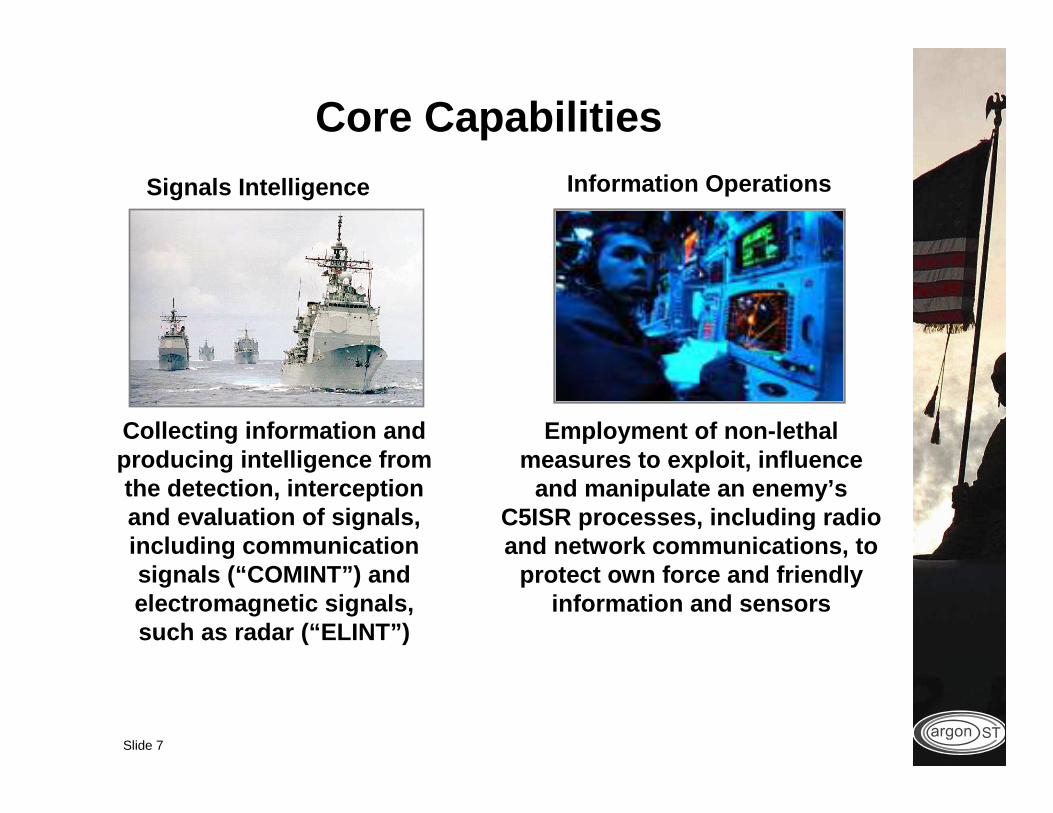

Core Capabilities

Collecting information and producing intelligence from the detection, interception and evaluation of signals, including communication signals (“COMINT”) and electromagnetic signals, such as radar (“ELINT”)

Signals Intelligence

Employment of non-lethal measures to exploit, influence

and manipulate an enemy’s C5ISR processes, including radio and network communications, to

protect own force and friendly information and sensors

Information Operations

Slide 8

Core Capabilities (cont.)

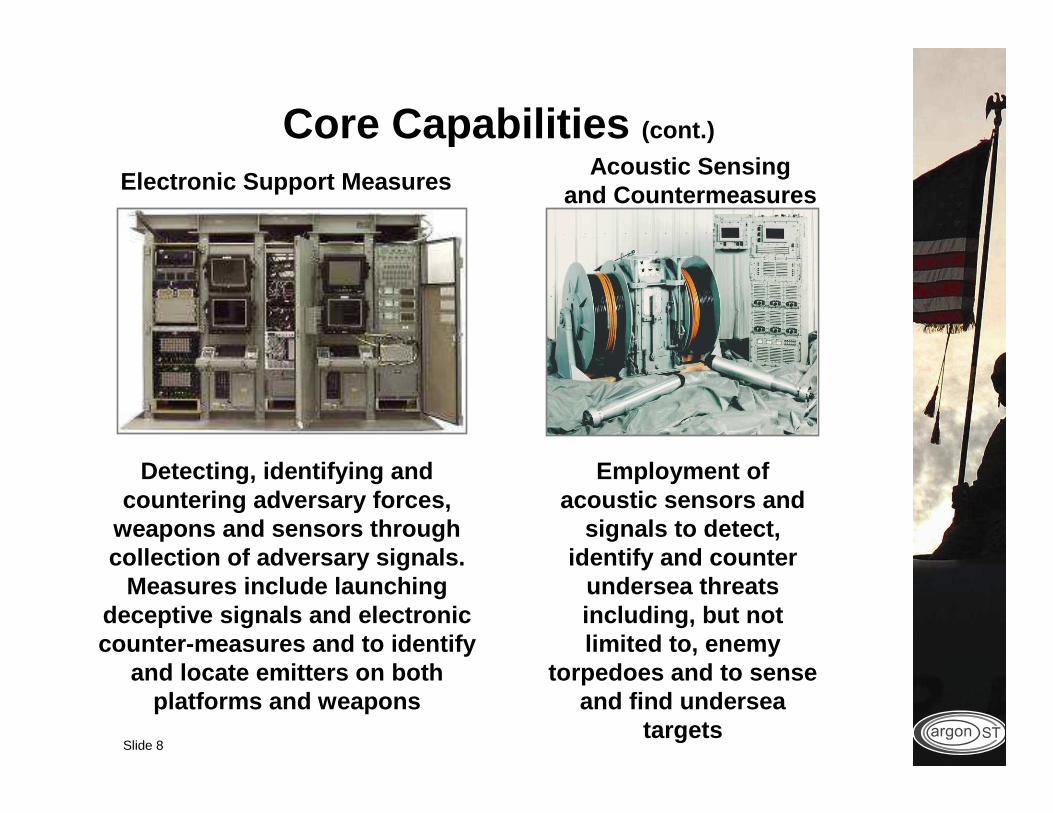

Employment of acoustic sensors and

signals to detect, identify and counter

undersea threats including, but not limited to, enemy

torpedoes and to sense and find undersea

targets

Acoustic Sensing and Countermeasures

Detecting, identifying and countering adversary forces,

weapons and sensors through collection of adversary signals.

Measures include launching deceptive signals and electronic counter-measures and to identify

and locate emitters on both platforms and weapons

Electronic Support Measures

Slide 9

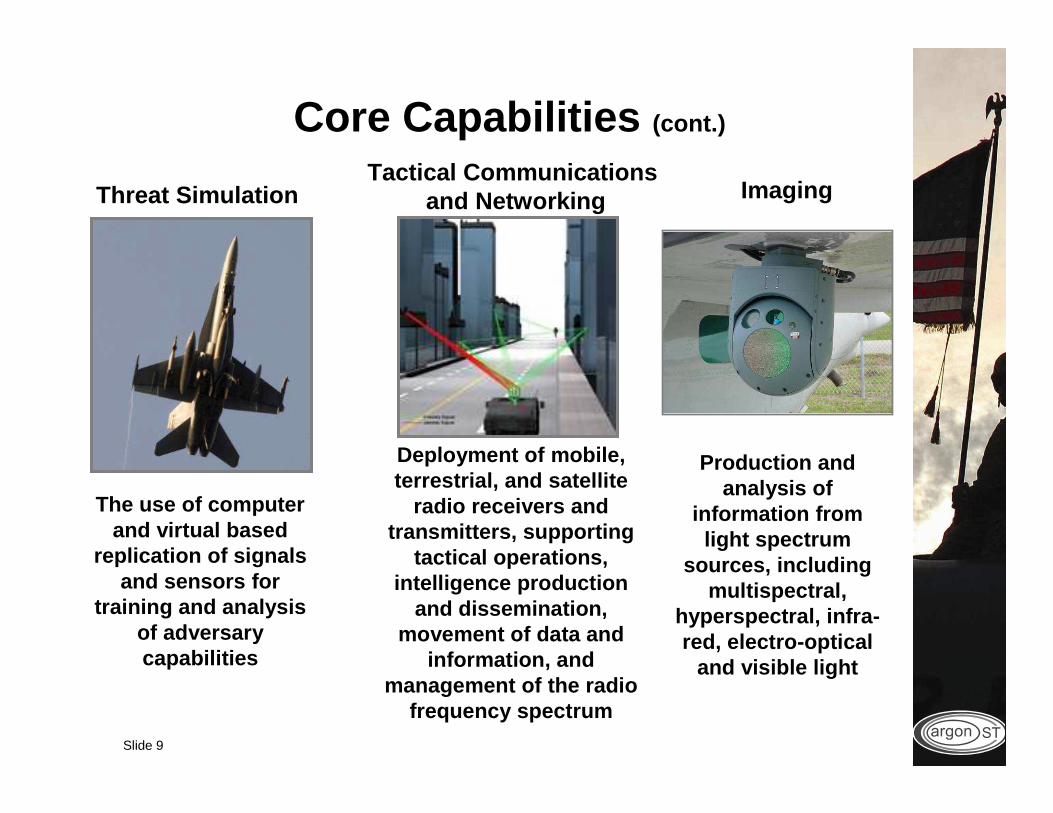

Core Capabilities (cont.)

Production and analysis of

information from light spectrum

sources, including multispectral,

hyperspectral, infra-red, electro-optical

and visible light

Imaging

The use of computer and virtual based

replication of signals and sensors for

training and analysis of adversary capabilities

Threat Simulation

Deployment of mobile, terrestrial, and satellite

radio receivers and transmitters, supporting

tactical operations, intelligence production

and dissemination, movement of data and

information, and management of the radio

frequency spectrum

Tactical Communications and Networking

Slide 10

Core Capabilities (cont.)

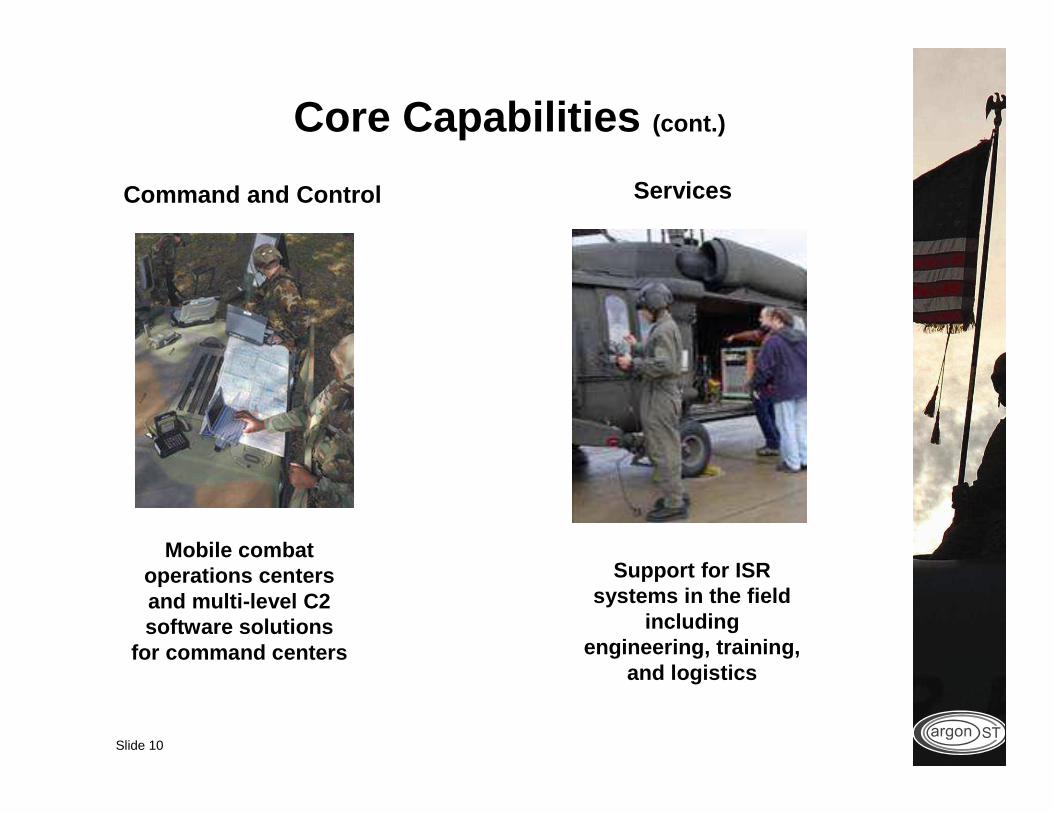

Support for ISR systems in the field

including engineering, training,

and logistics

Services

Mobile combat operations centers and multi-level C2 software solutions

for command centers

Command and Control

Slide 11

Maritime PlatformsU.S. Navy surface ships and submarines are our larg est set of

platforms using LIGHTHOUSE technology today

• Ships– Ships Signal Exploitation Equipment (SSEE)

• Increment E is under contract for 6th year of production• Increment F is starting testing leading to milestone C decision in

early FY10 to allow initial low rate production next year• International market is developing for SSEE systems

– Surface Ship Torpedo Defense (SSTD)• AN/SLQ-25C has passed testing• AN/SLQ-25 D is under development with completion planned this

year and is critical component to the Advanced Torpedo Torpedo Defense System

• International markets are likely to buy AN/SLQ-25C/D systems

– U.S. Coast Guard is now a customer for SSEE and var iant systems

– Target expansion onto shipboard infrastructure to i nclude networks, navigation, computing, displays, and inte lligence dissemination

Slide 12

Maritime Platforms (cont.)

U.S. Navy surface ships and submarines are our larg est set of platforms using LIGHTHOUSE technology today

• Submarines and UUVs• Communications and radar ESM systems for AN/BLQ-10• Special collection systems• Antenna, mast components and systems• Supplier to UK Trafalgar class submarines• Other international opportunities

• Torpedo seekers and electronics in development

• Argon has unique capability to supply these platforms

Slide 13

Airborne PlatformsThe airborne market is a growing market and include s manned and

unmanned platforms and our systems are well suited for current missions because of our advanced technology

• Current suppliers for EP-3E, Guardrail Modernizatio n, Rivet Joint, and others and we are well positioned for additional modernization if major new development programs slide to right

• Pursuing roles on EP-X, ACS, and others

• Production and delivery of aircraft electrical dist ribution, communication and control monitoring systems

• Multiple airborne reconnaissance quick reaction contracting efforts using combination of LIGHTHOUSE and beam forming that have large follow on potentia l

Slide 14

Land Based Systems

We are suppliers into fixed site and land mobile sy stems to gather and process intelligence

• Completion of significant milestones for first phas e of fixed site modernization program for a key U.S. intelligence community customer

• Awarded additional development work for the U.S. Army’s Enhanced Trackwolf transportable system

• Won subcontract role on large intelligence contract

• Targeting expansion of cyber security leveraging existing capabilities

Slide 15

Network SystemsEnabling fast, reliable delivery of information and intelligence to individual

terminals and ensuring interoperability across vast , dynamic networks

• Lead system integrator for the U.S. Army’s Operatio nal Test-Tactical Engagement System (OT-TES) communications upgrades

– Successful PEO demonstration in January 2009– Contract value recently raised– Selected as one of many on Simulation and Training Omnibus Contract

(STOC II) award

• Common Range Integrated Instrumentation System – Rap id Prototype Initiative (CRIIS-RPI) networked, time-sp ace-position reporting units have moved to production

• Successfully completed the Critical Design Review f or our low-earth orbit communications satellite payload develo pment, Orbcomm Generation 2, or OG2

• Additional expansion opportunities in Global Data S olutions and Thin-Client Solutions

Slide 16

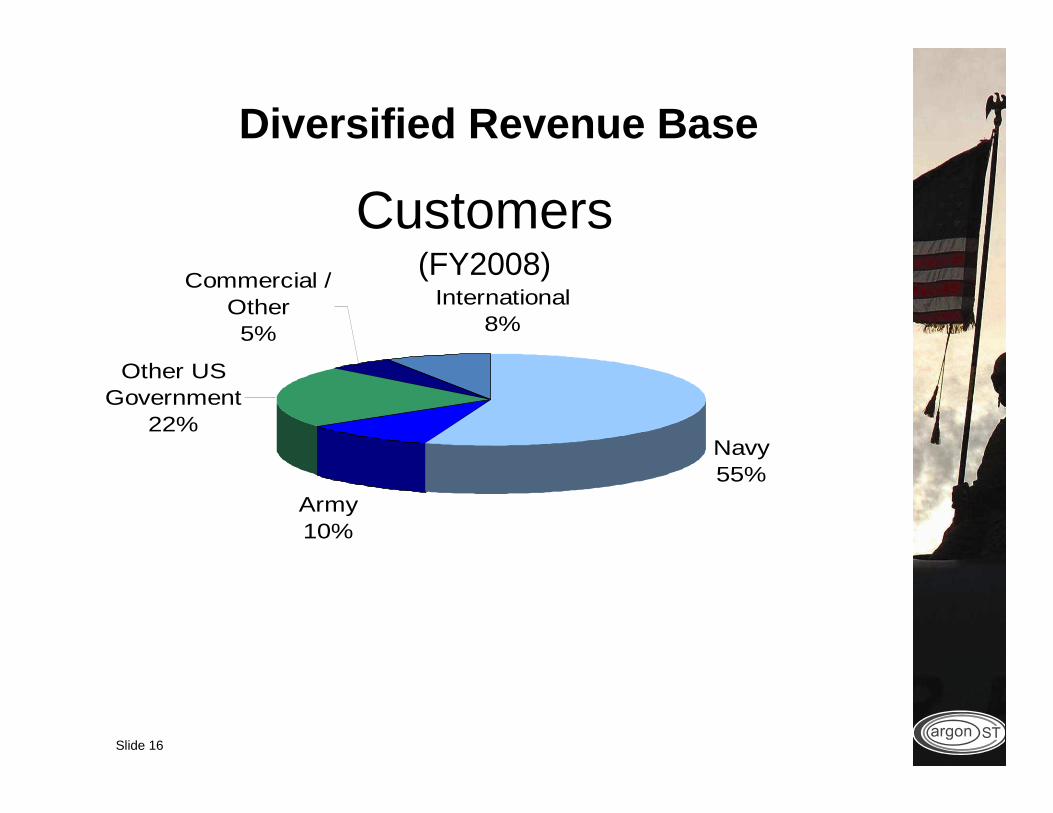

Navy55%

Army10%

Other US Government

22%

International8%

Commercial / Other5%

Diversified Revenue Base

Customers(FY2008)

Slide 17

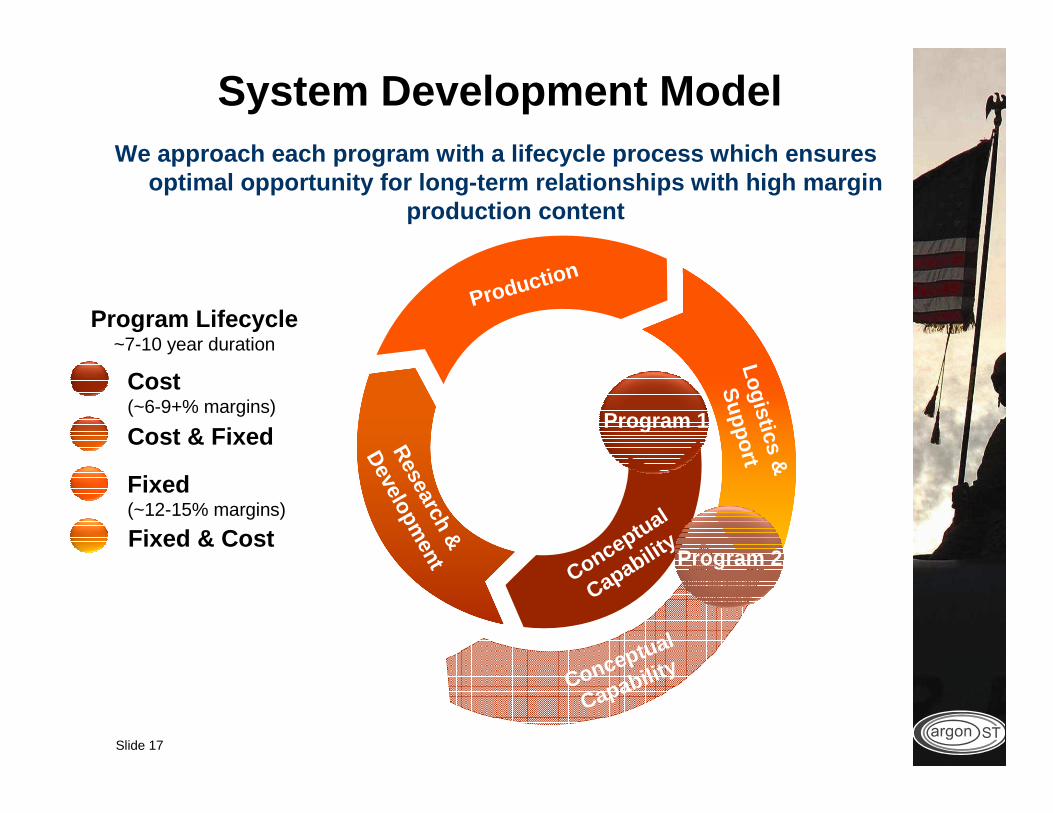

Cost(~6-9+% margins)

Cost & Fixed

Fixed(~12-15% margins)

Fixed & Cost

System Development ModelWe approach each program with a lifecycle process w hich ensures

optimal opportunity for long-term relationships wit h high margin production content

Logistics &

SupportR

esearch &

Developm

ent

Production

Conceptual

Capability

Conceptual

Capability

Program 1

Program 2

Program Lifecycle~7-10 year duration

Slide 18

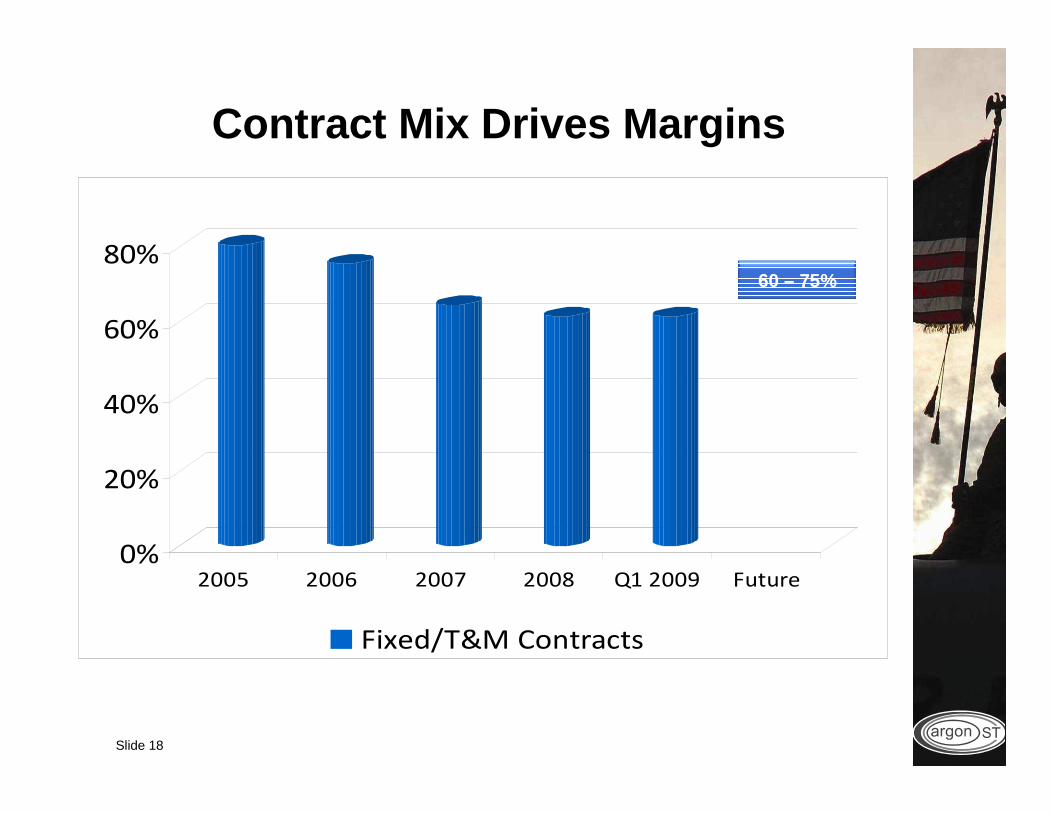

Contract Mix Drives Margins

0%

20%

40%

60%

80%

2005 2006 2007 2008 Q1 2009 Future

Fixed/T&M Contracts

60 – 75%

Slide 19

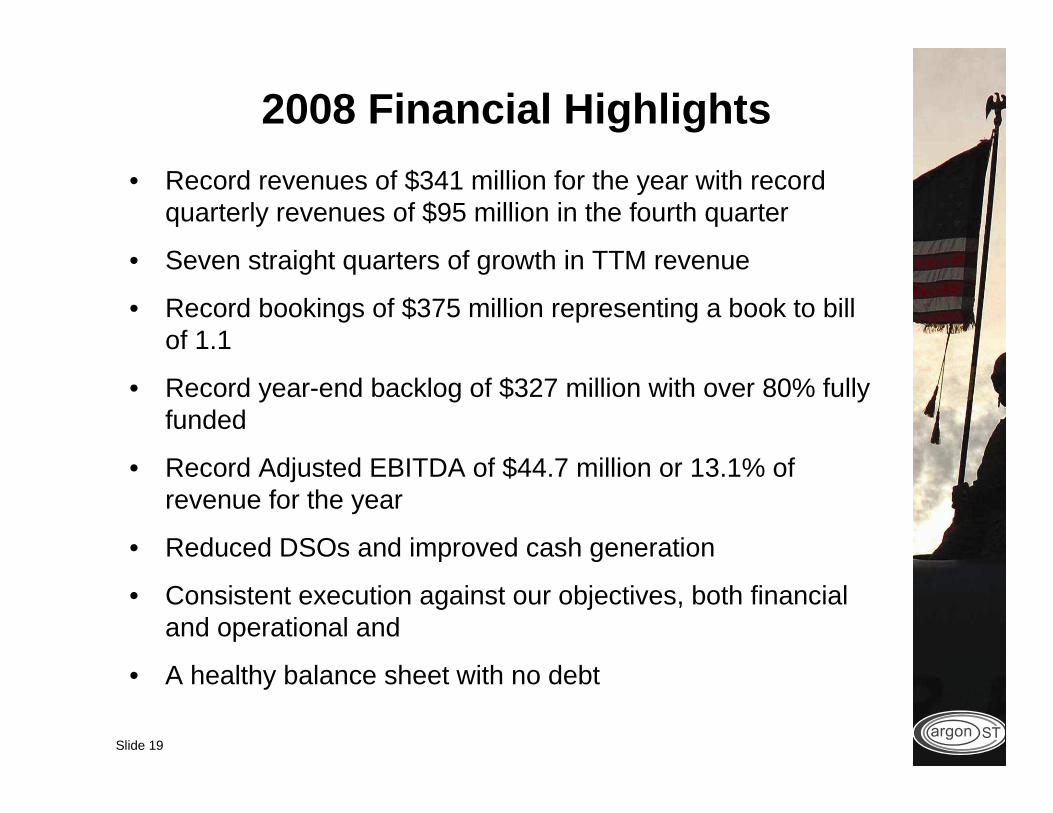

2008 Financial Highlights

• Record revenues of $341 million for the year with record quarterly revenues of $95 million in the fourth quarter

• Seven straight quarters of growth in TTM revenue

• Record bookings of $375 million representing a book to bill of 1.1

• Record year-end backlog of $327 million with over 80% fully funded

• Record Adjusted EBITDA of $44.7 million or 13.1% of revenue for the year

• Reduced DSOs and improved cash generation

• Consistent execution against our objectives, both financial and operational and

• A healthy balance sheet with no debt

Slide 20

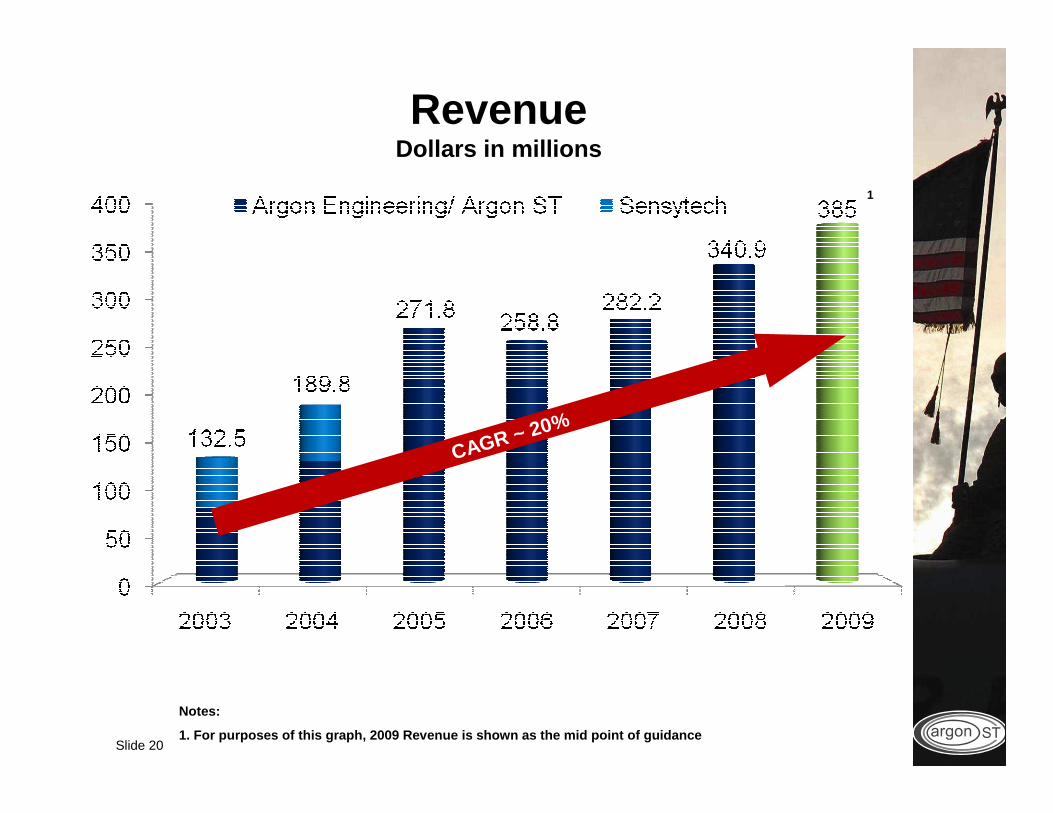

RevenueDollars in millions

1

Notes:

1. For purposes of this graph, 2009 Revenue is shown as the mid point of guidance

CAGR ~ 20%

Slide 21

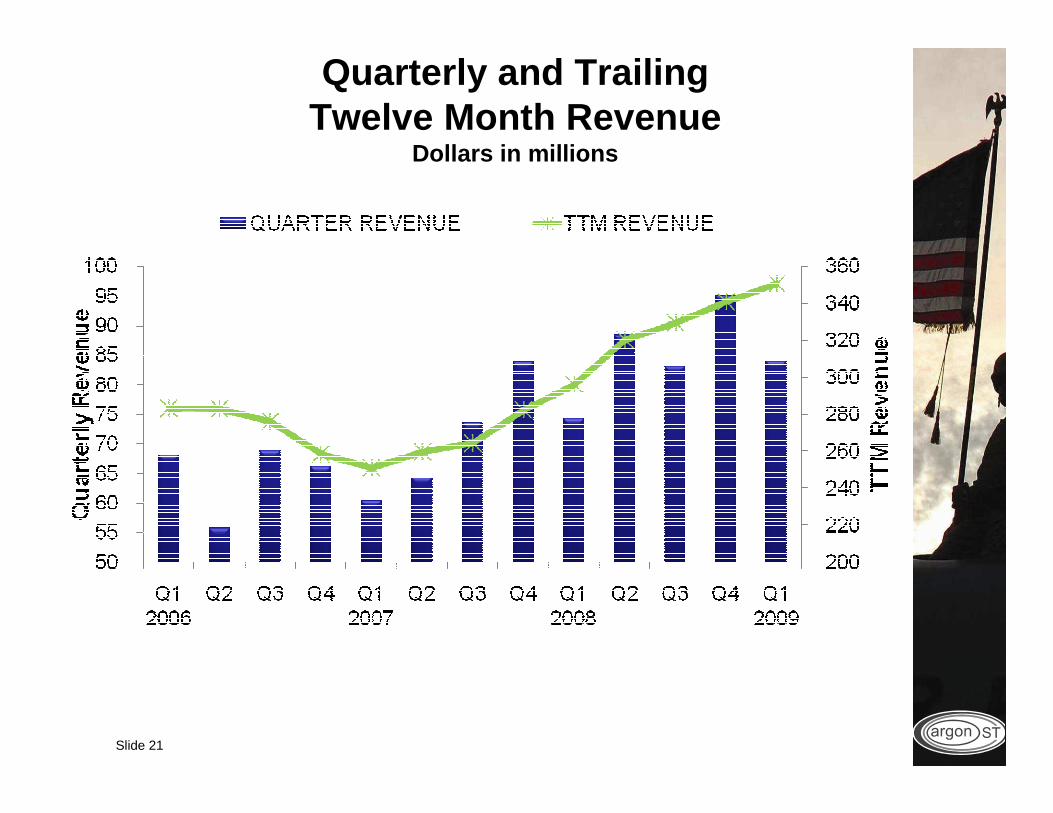

Quarterly and Trailing Twelve Month Revenue

Dollars in millions

Slide 22

Strategies For Sustainable Revenue Growth

• Technology-based new product introductions

• Expand market footprint with existing customers

• New capabilities to attract new customers

• Investments in international markets

• Technology transfer across business segments

• Supply chain and operations excellence

• Strategic acquisitions to enhance the existing portfolio

Slide 23

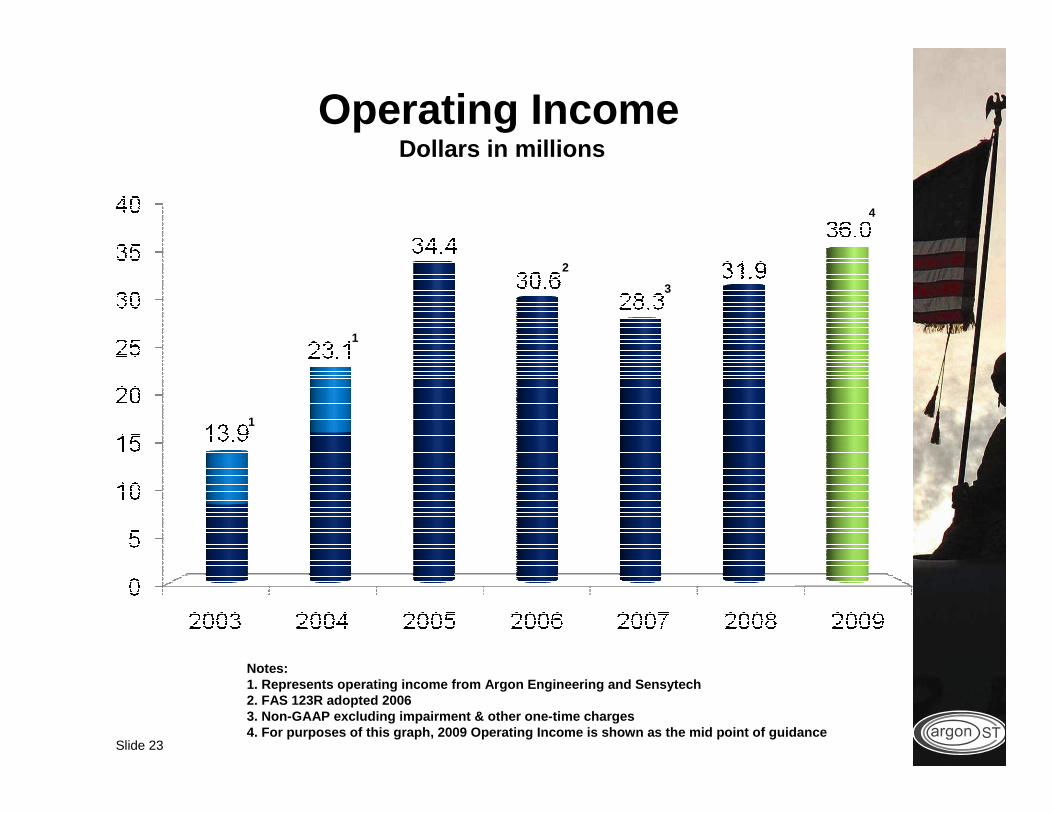

Operating IncomeDollars in millions

4

1

Notes:1. Represents operating income from Argon Engineeri ng and Sensytech2. FAS 123R adopted 20063. Non-GAAP excluding impairment & other one-time c harges4. For purposes of this graph, 2009 Operating Incom e is shown as the mid point of guidance

1

2

3

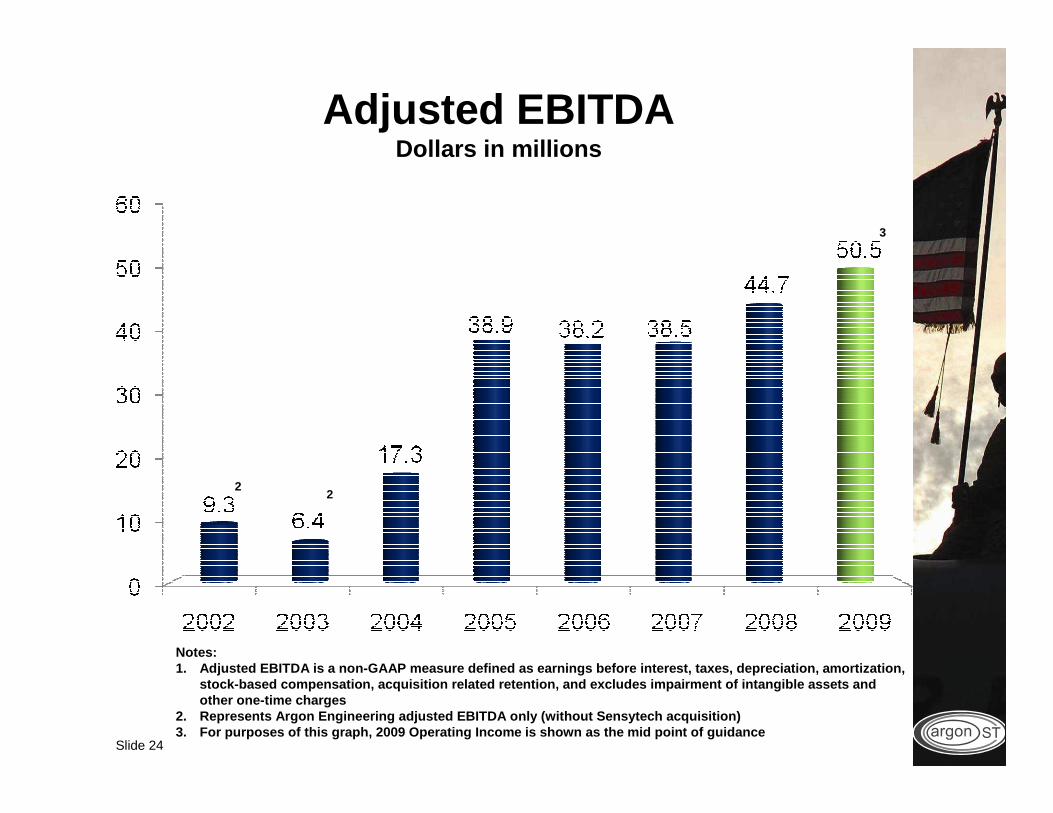

Slide 24

Adjusted EBITDADollars in millions

2

3

Notes:1. Adjusted EBITDA is a non-GAAP measure defined as earnings before interest, taxes, depreciation, amor tization,

stock-based compensation, acquisition related reten tion, and excludes impairment of intangible assets and other one-time charges

2. Represents Argon Engineering adjusted EBITDA only (without Sensytech acquisition)3. For purposes of this graph, 2009 Operating Income is shown as the mid point of guidance

2

Slide 25

Earnings Per Share (Diluted)Dollars

Notes:

1. Represents earnings from Argon Engineering and S ensytech

2. FAS 123R adopted 2006

3. Non-GAAP excluding impairment & other one-time c harges

1

1

23

Slide 26

Backlog Provides Visibility for Future Growth

Dollars in millions

Slide 27

Strong and Stable Balance Sheet

$ 329.6$ 340.3TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY

274.8292.4Equity

4.8 4.0Other liabilities

0.60.1Other current

12.74.4Deferred revenue

$ 36.7 $ 39.4Accounts payable and accrued expenses

LIABILITIES AND STOCKHOLDERS' EQUITY

$ 329.6$ 340.3TOTAL ASSETS

8.7 4.9Intangibles & Other assets

170.2 173.9Goodwill

22.827.6Property, equipment and software, net

9.3 13.6 Other current

95.6104.9Accounts receivable

$ 23.0$ 15.4Cash and cash equivalents

30 Sep 200730 Sep 2008

ASSETS

Slide 28

Q1 FY2009 Results (in $ millions except EPS)

30 Dec 07 28 Dec 08 Y/Y

• Contract revenue $ 74.3 $ 84.0 13.1%

• Income from ops $ 6.8 $ 7.6 12.5%

• Net Income $ 4.3 $ 5.2 21.2%

• Diluted shares 22.3 22.0

• EPS (Diluted) $ .19 $ .24 22.6%

Slide 29

2008 Operational Highlights

• Achieved key results that will facilitate future gr owth opportunities : – Completed the design and development on SSEE Inc F

– Achieved breakthroughs in system performance for airborne platforms by combining LIGHTHOUSE technology with special airborne processing

– Successfully tested the new AN/SLQ-25C configuration of surface ship torpedo defense system and received certification for production

– Demonstrated Common Range Integrated Instrumentation System – Rapid Prototype Initiative radios and started low rate initial production

– Successful prototype testing of Operational Test – Tactical Engagement System

• Expanded our customer base– Coast Guard, intelligence agencies, satellite communication payloads

– More relationships with large primes

• Improved efficiency– Production emphasis on Six Sigma processes

– Reduced operating costs

Slide 30

2009 Business Focus

• Maintain and expand our role with the Navy– Expand into platform computing, navigation, collection processing, and intelligence

dissemination

– Expand our role in torpedo seekers, countermeasures, and UUV sensors

• Grow airborne reconnaissance– Expand position on current system upgrades to meet urgent requirements

– Capture new roles on planned competitions such as EP-X and ACS

• Accelerate growth with the intelligence agencies

• Achieve growth in communications and networks– OT-TES, CRIIS – RPI, CRIIS, and test range targets

– Gateways, satellite communications, telematics

– Navigation systems

• Expand ground sensor role in the U.S. market

• Continue to evaluate strategic acquisitions to comp lement our technology and/or to achieve new customer relations hips

Slide 31

2009 Business Focus (cont.)

• Predicting the future has always been difficult, th is is especially true in the current environment

– Dramatic dislocations in the financial community– Very large federal deficit

– New Executive Branch with a large and ambitious domestic agenda

• Our positives for 2009– Solid backlog

– A base of momentum programs

– Excellent customer relationships– State-of-the-art technology

– A quality staff to provide development, production and support of our systems

• We continue to see important work in our pipeline a nd are cautiously optimistic that we will continue the gro wth we achieved in 2008 through 2009 and beyond

Slide 32

FY 2009 Outlook & Guidance

• For the fiscal year ending September 30, 2009:

– Revenue is anticipated to be in the range of $375 to $395 million

– Operating income is anticipated to be in the range of $34 to $38 million

– Adjusted EBITDA is anticipated to be in the range of $48 to $53 million