Embed Size (px)

Citation preview

ASSET ALLOCATION AND

THE EQUITY RISK PREMIUMCanada Pension Plan Seminar on

Demographic, Economic and Investment Perspectives for CanadaMay 2, 2003

Zainul Ali, Vice PresidentStrategic Research & Risk ManagementOMERS

2

Equity Risk Premium (ERP)• Definition:

• Expected (ex-ante) excess return on equity over a long-term fixed income investment

• Typically based on a risk less (e.g. Government of Canada) fixed income security

• Long term Government of Canada real return bond seems more appropriate in a pension plan context as it most closely matches the variability of the pension liability

3

Why is the ERP Important?• Huge implications for asset allocation strategy

• Helps plan sponsors to decide their strategic policy exposure to equity, debt and alternative investments

• For pension funds, the question is not so much what is therisk premium today, but what is the expected risk premium going forward?

• Historical evidence may not provide the best answer to the risk premium question

4

Meaning of Risk• Risk is not having enough money to pay the pension promise

• Risk in the traditional definition refers to volatility of prices and returns around some long term average – the classical CAPM model

• Problem with this is that we live in a world that is non-stationary, therefore, there is no fixed or learnable distribution of returns

• Stationarity assumes the past is a good proxy for the future and fails to capture the pattern of returns resulting from an investment regime change

5

Asset Allocation

… “but the long run is a misleading guide to current affairs. In the long run we are all dead”

“Economists set themselves too easy, too useless a task if in tempestuous seasons they can tell us that when the storm is long past, the ocean is flat again”

- John Maynard-Keynes

6

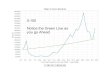

U.S. Equity Risk Premium(rolling 5-year avg.)

-15

-10

-5

0

5

10

15

20

25

1924

1926

1928

1930

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

%

US avg = 6.75%

DepressionWar

Peace Time & Reconstruction

OPEC/InflationForget the average. It's all about the regime!

Information Age. Fall of Communism. Capitalism expands.

Data Source: Canadian Institute of Actuaries & Russell/Mellon

7

Canadian Equity Risk Premium(rolling 5-year avg.)

-15

-10

-5

0

5

10

15

20

25

1924

1926

1928

1930

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

%

Cdn avg = 5.18%

Data Source: Canadian Institute of Actuaries & Russell/Mellon

8

Equity Risk PremiumCanada Vs. U.S. (rolling 5-year avg.)

-15

-10

-5

0

5

10

15

20

25

1924

1926

1928

1930

1932

1934

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

%

Cdn ERP Cdn avg. US ERP US avg

US avg =

Cdn avg = 5.18%

Correlation = 0.85

Secular bull market for bonds. Are we seeing the end of this?

Data Source: Canadian Institute of Actuaries & Russell/Mellon

9

Capital Market Expectations• Let’s see if we can build a return framework for equities,

bonds and the resulting ERP• To do this we must first build a scenario for the most

likely investment regime over the next 5 to 10 years• The issue is that when “boom” turns to “bust”, the

unpleasant memory can remain for a while with a generation of investors who endured the pain.

• Central to our analysis are the assumptions of lower investor expectations (coming off the excesses of the 90’s) and of modest economic growth for the next few years.

10

Changing Capital MarketsEconomic Environment Real ReturnsReal Returns

PeriodNumber of

YearsConsumer Price index

Real GDP per

EmployedReal Wage

Growth RRB* YieldsBoom 1924-28 5 (0.2) 3.7 1.1 3.2Depression 1929-32 4 (5.5) (4.6) 2.7 4.3Recovery 1933-38 6 0.8 3.2 1.5 3.3War 1939-45 7 2.6 7.2 1.9 2.5Reconstruction 1946-51 6 7.7 1.0 0.6 1.6High Growth 1952-56 5 0.5 6.3 4.4 1.9Stable Growth 1957-65 9 1.8 2.2 2.1 2.7Inflation Pressure 1966-74 9 5.4 2.8 2.6 3.9Stagflation 1975-82 8 9.4 0.1 0.6 4.6Tight Money 1983-91 9 4.3 0.4 0.1 4.7Fiscal Restraint 1992-99 8 1.5 1.5 0.2 4.3????????? 2000-2002 3 2.6 (0.2) (0.6) 3.5

1924-74 51 2.2 3.0 2.1 2.91975-2002 28 4.8 0.6 0.2 4.4

1924-2002 79 3.1 2.1 1.4 3.5

* Real Return Bond(RRB) yields and returns simulated prior to 1992, using Mercer's Interest Rate Model** Canada 5-10 Year Bond returns prior to 1980

Best performing Canadian Asset ClassSource: Mercer’s

RRB*91-Day T-bills

SCM Universe Bond**

Canada Long Bonds

Canadian Equities

3.1 6.0 28.2(1.3) 10.6 (18.2)7.8 (0.6) 6.3 17.44.1 (2.0) 0.9 5.53.2 (6.7) (5.9) 8.20.5 1.2 1.6 1.8 14.91.1 1.8 2.2 1.2 6.82.3 0.3 0.0 (2.1) (2.2)3.8 2.2 (0.9) (1.6) 6.44.9 6.0 8.3 8.6 5.95.3 3.6 7.3 8.9 12.37.7 1.5 6.3 6.7 (8.7)

2.7 1.5 6.75.0 3.8 5.1 5.5 6.1

3.4 2.9 6.5

Returns

11

Economic Eras

1992-99: Fiscal RestraintIncreasing recognition and response to government deficit and debt issues facilitatesthe easing of monetary policy. Inflation falls to 1957-65 levels and reduced inflationexpectations spur spectacular bond and stock performance. The first signs of Declining real interest rates and recovering economic growth begin to appear.

1966-74: Inflation PressuresThe expanding economy is faced with increasing capital demands to expand social programsand provide schooling and jobs for the first wave of baby boomers reaching adulthood. TheUS finances expanding social programs, the Vietnam War, and the space program. Risinginflation pressures and rising real interest rates culminate with the oil crisis and the 1973-74bear market which reprices equities for a high real interest rate environment. Cash looksattractive on a risk adjusted basis compared to stocks and bonds.

1975-82: StagflationThe affects of the oil crisis lead to a period of persistent high inflation. Combined with higher realinterest rates, this ushers in a long period of sharply lower economic growth which we are still dealingwith today. Equities provide an effective hedge against inflation while bonds continue to depreciate ininflation adjusted terms.

1983-91: Tight Money

In an effort to reduce inflation pressures, the Bank of Canada maintains short term real interestrates at historically high levels. Falling inflation expectations boost bond returns as nominal interest rates begin a slow, choppy decline. But rising government deficits and debt keep realinterest rates on long bonds at historically high levels.

1957-65: Stable GrowthThe explosive growth of the early 1950’s subsides to an era of steady and comfortable economic growth,low inflation and low interest rates. Wage earners and shareholders both thrive under these idealconditions. Equity returns look extremely attractive compared to fixed income investments.

Source: Mercer’s

12

Setting AssumptionsHere’s our base case expectations for the next 10 years:

Inflation 3.0%

Real GDP Growth 3.0%

Real Interest Rates 3.5%

Upward pressures and moderate growth (BOC talking of a tighter bias,) should keep inflation at the upper end of the BOC range. Higher inflation, above 3%, means failure on the part of the Bank of Canada and this seems unlikely

13

Setting Assumptions cont.

• Real Economic growth is a function of:

- Productivity Growth - Labour Force Growth

14

Setting Assumptions cont.• Just under 2% real productivity growth in the past 40

years. Could be slightly higher going forward as investment spending picks up modestly after slowing from 1990’s levels. Corporate deleveraging seems to be coming to an end. (See chart)

• Labour expected to grow in line with population growth of approximately 1% per annum

• Over longer periods, moderate economic growth, and increased spending on technology should put upward pressure on the cost of capital causing real yields to increase.

15

Financing Gap Trending in the right direction?

Financing Gap = capital spending – internal cash flow

16

Determining a Forward Looking ERP• Very difficult to calculate with any precision. Like trying to forecast

currencies

• High “model uncertainty”. One can only try to get a comfort level.

• No wonder this is such a contentious issue. Recent articles by leading academics come up with an expected ERP anywhere between –1% to 4.25%

• Beyond 5 to 10 years, one can only pretend to look at this (ERP and asset class returns) in a serious way. Career risk for CIO’s and committee members and pressure from stakeholders will dictate a shorter focus (with historical averages and educated guesses used for the longer term)

17

Canadian GDP vs. TSX Earnings GrowthCanadian GDP vs TSE Earnings Growth

(Annual % Change)

-60

-30

0

30

60

90

12/3

1/19

62

12/3

1/19

64

12/3

1/19

66

12/3

1/19

68

12/3

1/19

70

12/3

1/19

72

12/3

1/19

74

12/3

1/19

76

12/3

1/19

78

12/3

1/19

80

12/3

1/19

82

12/3

1/19

84

12/3

1/19

86

12/3

1/19

88

12/3

1/19

90

12/3

1/19

92

12/3

1/19

94

12/3

1/19

96

12/3

1/19

98

12/3

1/20

00

12/3

1/20

02

%

0

5

10

15

20

%

TSE Earnings Growth (lhs) Canadian GDP (rhs)

Avg GDP = 8.5%Avg Earnings = 8.9%

18

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

%

0

2

4

6

8

10

12

14

%

S&P Earnings Growth" US GDP (nominal)

Avg GDP = 7.5%Avg Earnings = 6.9%

U.S. GDP vs. S&P Earnings Growth(Annual % change)

19

Expected Real ReturnsEquities

ESR (t) = DY (t) + REG (t) + PE (t)

Expected real stock market returns

at time “t”

Starting dividend yield at time “t”

Real earnings growth starting

at time “t”

Valuation changestarting at time “t”

BONDSAn increase in expected inflation from 2% to 3% over 10 years causes the value of a real return bond (current 3% coupon) to drop from $100 to $91 with a resulting return of 5.4%

20

Expected Real Returns

• Net share repurchase (particularly the banks) and investors’ preference for more “up front” return should cause dividend yields to increase over time.

• Earnings cannot grow faster than the overall economy over any sustainable period of time. But the TSX is not representative of the Canadian economy and its earnings tend to grow somewhat faster.

• For valuation, a P/E contraction can be expected -consistent with past bubble investor behavior

21

TSX Dividend Yield(1956-2002)

2.0

0

1

2

3

4

5

6

7

Jan-

56Ja

n-57

Jan-

58Ja

n-59

Jan-

60Ja

n-61

Jan-

62Ja

n-63

Jan-

64Ja

n-65

Jan-

66Ja

n-67

Jan-

68Ja

n-69

Jan-

70Ja

n-71

Jan-

72Ja

n-73

Jan-

74Ja

n-75

Jan-

76Ja

n-77

Jan-

78Ja

n-79

Jan-

80Ja

n-81

Jan-

82Ja

n-83

Jan-

84Ja

n-85

Jan-

86Ja

n-87

Jan-

88Ja

n-89

Jan-

90Ja

n-91

Jan-

92Ja

n-93

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Per

cent

%

Average = 3.20

22

0102030405060708090

100

Dec-

56

Dec-

58

Dec-

60

Dec-

62

Dec-

64

Dec-

66

Dec-

68

Dec-

70

Dec-

72

Dec-

74

Dec-

76

Dec-

78

Dec-

80

Dec-

82

Dec-

84

Dec-

86

Dec-

88

Dec-

90

Dec-

92

Dec-

94

Dec-

96

Dec-

98

Dec-

00

Dec-

02

Avg. = 51.2%

TSX Pay-Out Ratio(4 year rolling average)

23

TSE Trailing P/E Ratio

0

5

10

15

20

25

30

35

40

Jan-

56

Jan-

58

Jan-

60

Jan-

62

Jan-

64

Jan-

66

Jan-

68

Jan-

70

Jan-

72

Jan-

74

Jan-

76

Jan-

78

Jan-

80

Jan-

82

Jan-

84

Jan-

86

Jan-

88

Jan-

90

Jan-

92

Jan-

94

Jan-

96

Jan-

98

Jan-

00

Jan-

02

Avg. = 17.5

Beginning of:1960s = 20.1x1970s = 16.31980s = 8.71990s = 12.32000s = 33.2

p/e = 20.6 as of Feb'03

TSX Trailing P/E Ratio

24

S&P 500 Trailing P/E Ratio Vs. Inflation

-1

4

9

14

19

24

29

34

39

44

Jan-

54Ja

n-55

Jan-

56Ja

n-57

Jan-

58Ja

n-59

Jan-

60Ja

n-61

Jan-

62Ja

n-63

Jan-

64Ja

n-65

Jan-

66Ja

n-67

Jan-

68Ja

n-69

Jan-

70Ja

n-71

Jan-

72Ja

n-73

Jan-

74Ja

n-75

Jan-

76Ja

n-77

Jan-

78Ja

n-79

Jan-

80Ja

n-81

Jan-

82Ja

n-83

Jan-

84Ja

n-85

Jan-

86Ja

n-87

Jan-

88Ja

n-89

Jan-

90Ja

n-91

Jan-

92Ja

n-93

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-99

Jan-

00Ja

n-01

Jan-

02Ja

n-03

Perc

ent %

P/E Ratio CPI

Beginning of:1960s = 18.8x1970s = 16.71980s = 7.91990s = 13.42000s = 33.6 Prosperous (Feeling Good)

regime. Compare to now.

Stock Market still expensive!

29.6x

P/E decline from 30x to 25x = -1.8%/yr

over 10 years!

Avg = 17.1

25

Lower Expectations?• Trailing P/E at the end of February 2003 was 25.9 X.

The previous five decades started out with P/E’s of:

1960 20.1 X1970 16.3 X1980 8.7 X1990 12.3 X2000 33.2 X

P = P/E • E

Assuming E remains constant a drop in P/E from 20.6 to just 18 will result in stocks declining slightly more than 1.0% per year for the next 10 years in Canada. Worse outlook for the S&P 500

26

Estimated ERPDividend yield (+ net share repurchase) 2.50%Real Earnings Growth 3.25%P/E Change (1.0%)Real Stock Return 4.75%Inflation 3.0%Nominal Stock Return 7.75%Less Real Return Bond Nominal Return 5.40%Expected ERP 2.35% *

* Less than half the Canadian long term average

Different Approach, Same Answer?Expected Equilibrium P/E 18.0 XEarnings Yield (inverse of P/E) 5.5%Normalized Payout Ratio 50%Dividend Yield 2.75%

+ Expected real earnings growth 3.25%- P/E Contraction (1.0%)- Expected real equity return 5.0%- RRB Real Return 2.4%

Expected ERP 2.6%

28

TIPS vs. S&P 500CORR 0.88R2 0.78

Inflation Indexed Bond Yields can rise 100 bps over 5 years with a 7% rise in the S&P (850-1200)

29

Three Post War Investment Regimes

Regimes

4.1%- 1.8%8.0%ERP

7.8%- 2.2%0.3Bond Index(Real Return)

11.9%- 4.0%8.3%S&P 500 Index(Real Return)

1982-19991967-19811949-1966

Source: SED

30

Three Post War Investment Regimes• The point is capital market returns can change dramatically

and last for a long time from one regime to another

• Investor optimism of the ’80’s and ’90’s is behind us. Diminished expectations are shaping the mindset of investors early in the new century

• Question is how long will this last? And would investors bail out of riskier equities for bonds if there is no commensurate reward?

• Possibly, but over the long term, stocks (because of their inherent risks) will command a premium over bonds. Otherwise, capitalism will suffer

31

Asset and Liability Behavior• Given the debate and controversy surrounding the “correct ERP”,

how should plan sponsors assess the impact of a high/low ERP?

• Theory suggests that a lower ERP will shift the efficient frontier downwards i.e. lower return for the same risk in a mean varianceworld

• Some fiduciaries may decide to reduce their equity exposure in favour of bonds. Not so fast!

32

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

Base (ERP:1.75) Deflation (ERP -6.25) Stagflation (ERP3.50)

Stagnation (ERP 0.0) Current Expectation(ERP 2.25)

Fund

ed R

atio

0.94*

0.80*

0.98*1.05*1.02*

You would think that with an Equity Risk Premium of 3.5% your Funded Ratio should be relatively safe looking forward!

It’s more about outcomes (on funded status) than absolute ERP’s

Typical Public Sector Pension PlanFunded Ratio – (Year 10)

* Mean

33

Asset and Liability Behavior• Examine the possible outcomes on the plan’s funded ratio for a

base case and various stress testing scenarios

• A low ERP does not necessarily mean a bad thing. Look at the base case scenario with an ERP of 1.75%. More that half of the outcomes have a funded ratio above 102%, probably because both stocks and bonds have high absolute returns

• Compare this to an ERP of 3.5% in stagflation. All of the outcomes are below 1%

34

Asset and Liability Behavior• A useful guide for fiduciaries is to place more emphasis on the

lower part of the distribution of outcomes that arise from a high/low premium, i.e. pay attention to the “tails” of the distribution. Penalize those outcomes that do not meet your initial risk/return objectives

• Pay attention also to the year to year change in the funded status. May be o.k. to live with an undesirable outcome for one year. Question is how long can you or your plan members (political pressure) put up with long periods of under-funding

• As a fiduciary, understanding both the economic/investment regime confronting you for the next several years and the assumptions underlying the various scenarios is key

35

Is There A Recovery Policy?110

105

100

90

80

FundedRatio

Time Horizon

How deep a decrease can the Board withstand , and how quickly do they want to recover?

36

Looking Down the Road• For CPP and many public sector pension plans, returns from

traditional assets in the current investment regime may not be sufficient to meet the required pension promise (regardless of the absolute value of the ERP)

• Need to consider other types of investments. Think of prospective returns as a multiple of the required pension return over the next 5-10 years

* expected multiple of required return

37

Looking Down the Road• Assuming a nominal equities return of 7.5%, the following inputs

may be used (as examples) for the efficient frontier asset mix decision:

Stocks 0.9 X - 1.0 X *Bonds 0.5 X - 0.7 XReal Estate 1.0 X - 1.2 XPrivate Equity 1.0 X - 2.0 XInfrastructure 1.1 X – 1.5 XAbsolute Return Strategies 1.0 X – 1.2X

* expected multiple of required return

38

Summary• These are difficult times for plan sponsors. Risk seem inordinately

high – economic and geopolitical

• The equity risk premium is an important issue. Going forward, it may well be below historical averages. As fiduciaries, you should understand the consequences and the impact on the plan’s funded status

• A lower ERP does not mean stocks are all bad, only that the outcome may not be as favourable as anticipated

• More important, understanding both the current investment regime and the assumptions underlying the asset allocation process is crucial. Too often, this is blindly delegated to the actuary/consultant who smoothes things out with naïve assumptions over very long periods of time, thereby missing shorter term financial shocks and contribution volatility.