Embed Size (px)

Citation preview

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Euro Aviation ICT Forum Thursday 29 October, 2015

Divani Caravel Hotel, Athens

Jonathan Wober, Chief Financial Analyst

Aviation industry outlook

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

The leading independent supplier of global aviation knowledge

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

-10

-8

-6

-4

-2

0

2

4

6

8

10

19

47

19

50

19

53

19

56

19

59

19

62

19

65

19

68

19

71

19

74

19

77

19

80

19

83

19

86

19

89

19

92

19

95

19

98

20

01

20

04

20

07

20

10

20

13

-10

-8

-6

-4

-2

0

2

4

6

8

10

Operating margin Net Margin

Airline margins: cyclical and thin World airline operating and net margins (% of revenue) 1947 to 2014

Source: CAPA – Centre for Aviation, ICAO, A4A, IATA

1966

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

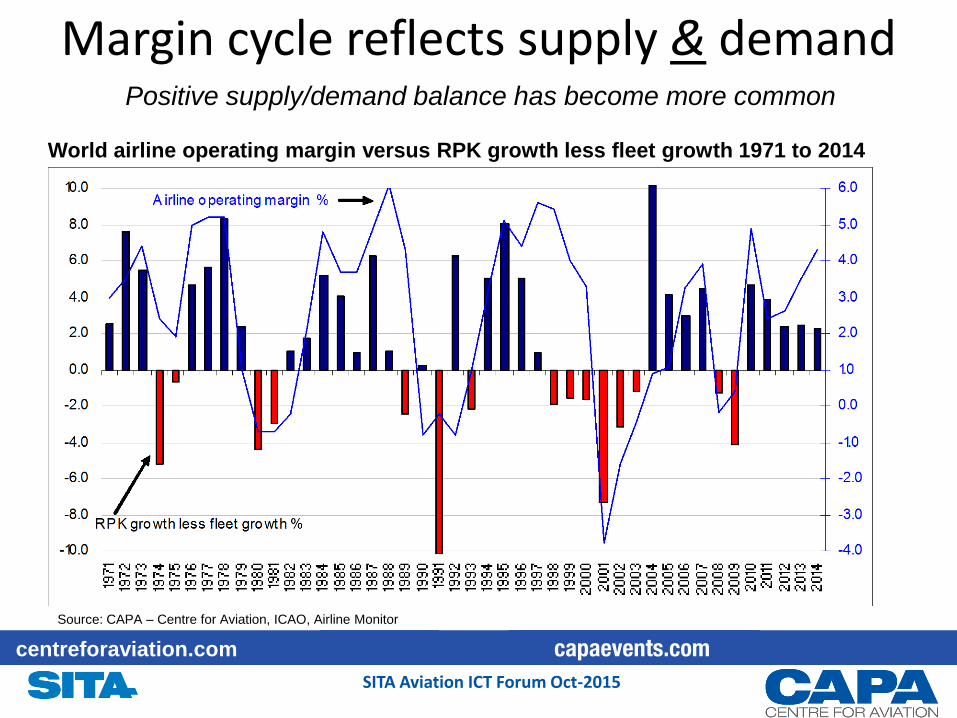

Margin cycle reflects supply & demand

World airline operating margin versus RPK growth less fleet growth 1971 to 2014

Source: CAPA – Centre for Aviation, ICAO, Airline Monitor

Positive supply/demand balance has become more common

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

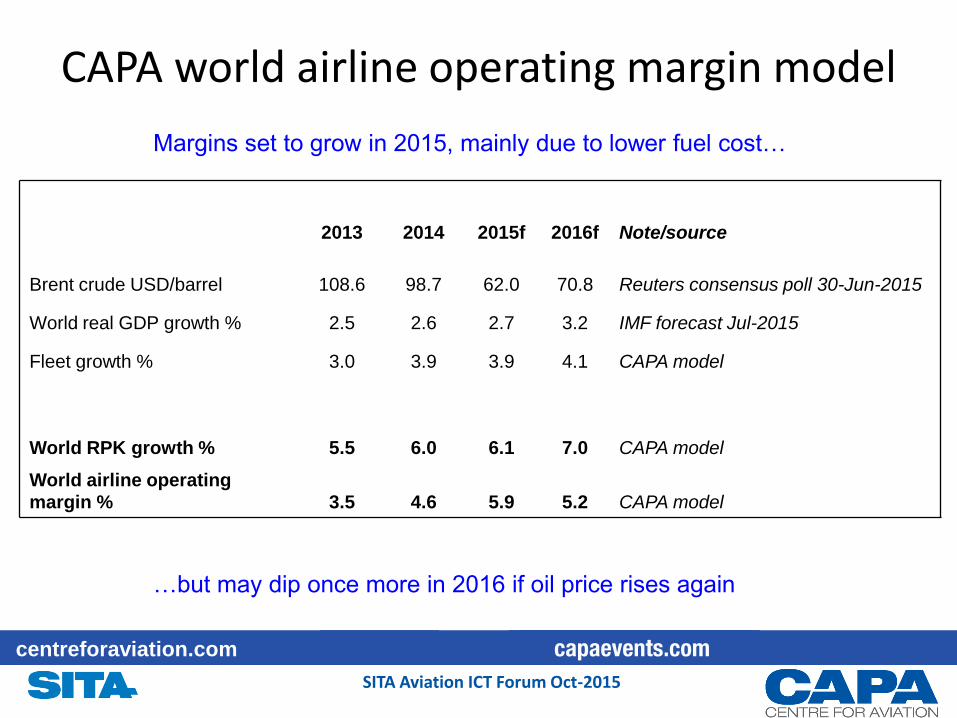

CAPA world airline operating margin model

2013 2014 2015f 2016f Note/source

Brent crude USD/barrel 108.6 98.7 62.0 70.8 Reuters consensus poll 30-Jun-2015

World real GDP growth % 2.5 2.6 2.7 3.2 IMF forecast Jul-2015

Fleet growth % 3.0 3.9 3.9 4.1 CAPA model

World RPK growth % 5.5 6.0 6.1 7.0 CAPA model

World airline operating

margin % 3.5 4.6 5.9 5.2 CAPA model

Margins set to grow in 2015, mainly due to lower fuel cost…

…but may dip once more in 2016 if oil price rises again

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

-6

-4

-2

0

2

4

6

8

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015e

2016e

High

Base case

Low

Geopoliticalcrisis/recession

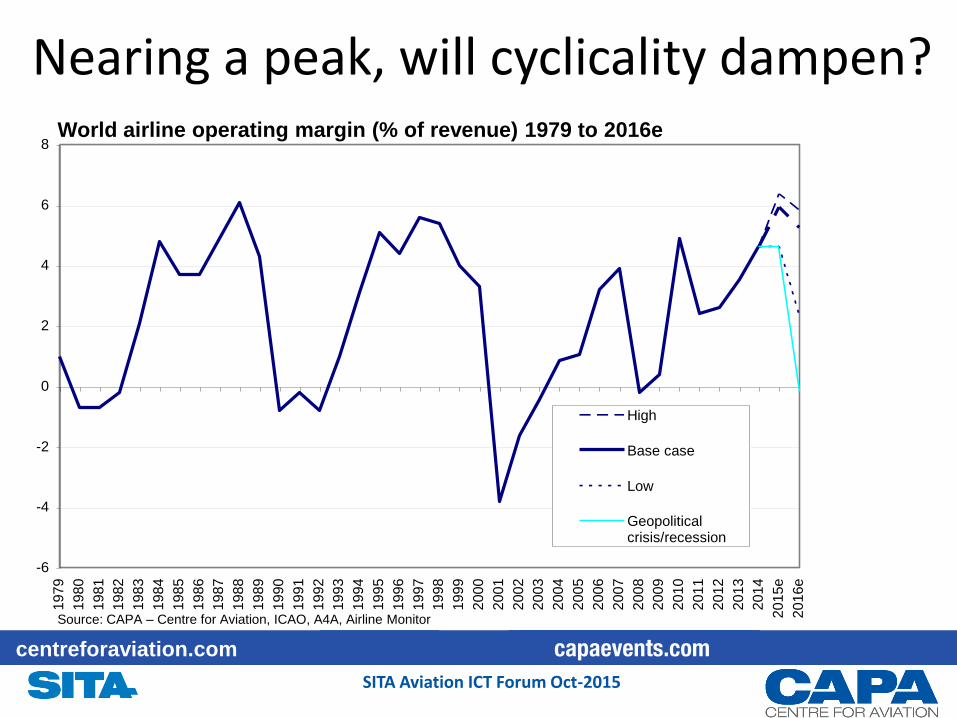

Nearing a peak, will cyclicality dampen? World airline operating margin (% of revenue) 1979 to 2016e

Source: CAPA – Centre for Aviation, ICAO, A4A, Airline Monitor

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

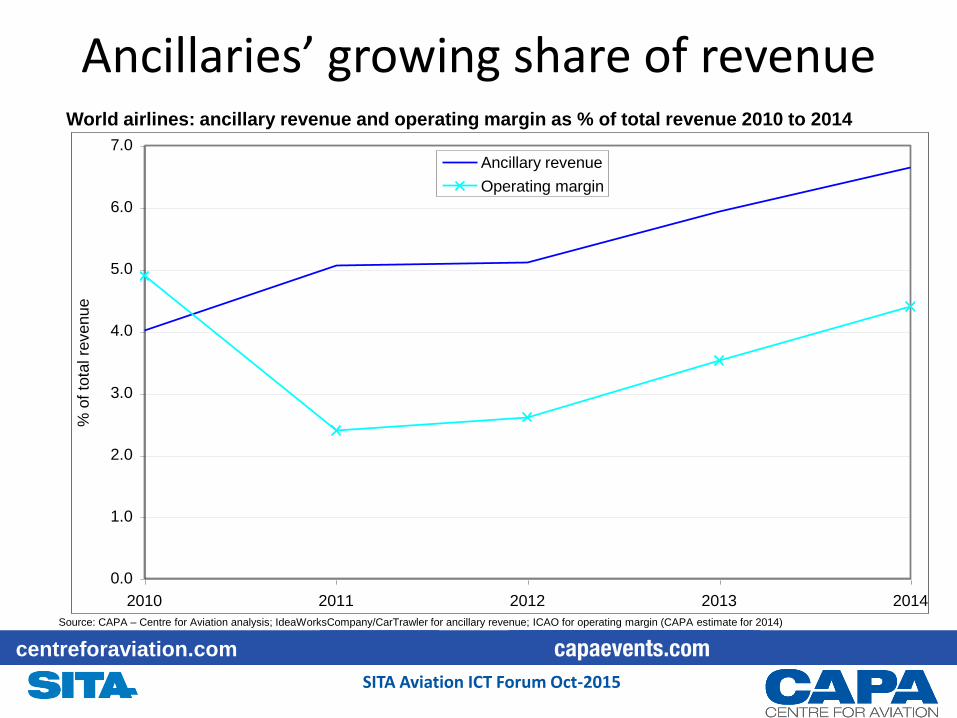

Ancillaries’ growing share of revenue World airlines: ancillary revenue and operating margin as % of total revenue 2010 to 2014

Source: CAPA – Centre for Aviation analysis; IdeaWorksCompany/CarTrawler for ancillary revenue; ICAO for operating margin (CAPA estimate for 2014)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2010 2011 2012 2013 2014

% o

f to

tal re

venue

Ancillary revenue

Operating margin

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Different ancillaries outside US vs in US, distorted by FFP mile sales

Baggage fees, 25%

Other a la carte

services, Onboard

retail, 15%

Travel retail, 5%

Sale of FFP miles,

55%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US major

Baggage fees, 20%

Other a la carte

services, 30%

Onboard retail,

20%

Travel retail, 20%

Sale of FFP miles,

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Outside US (non LCC)

Ancillary revenue components 2013 (% of ancillary revenue)

Source: CAPA – Centre for Aviation using data from IdeaWorksCompany/CarTrawler

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

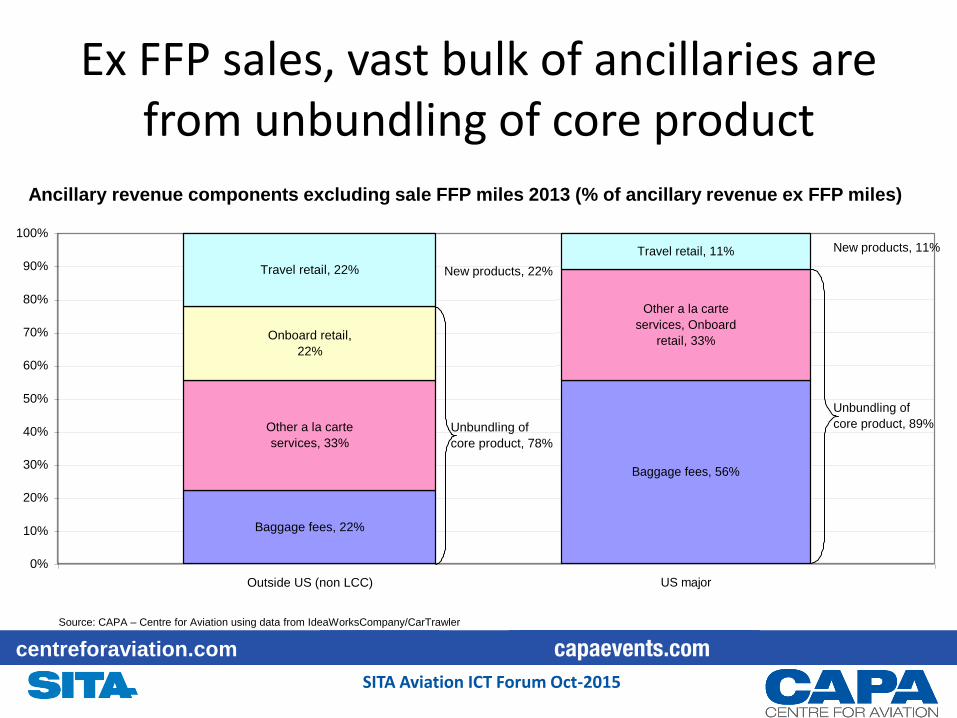

Ex FFP sales, vast bulk of ancillaries are from unbundling of core product

Baggage fees, 56%

Other a la carte

services, Onboard

retail, 33%

Travel retail, 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US major

Unbundling of

core product, 89%

New products, 11%

Ancillary revenue components excluding sale FFP miles 2013 (% of ancillary revenue ex FFP miles)

Source: CAPA – Centre for Aviation using data from IdeaWorksCompany/CarTrawler

Baggage fees, 22%

Other a la carte

services, 33%

Onboard retail,

22%

Travel retail, 22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Outside US (non LCC)

Unbundling of

core product, 78%

New products, 22%

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Cash flow is exceeding capital investment currently

* Estimated on-balance sheet capex as % of EBITDA.

Source: CAPA – Centre for Aviation, Airline Monitor, IATA

World airline capital expenditure as a percentage of operating cash flow 1979 to 2016E*

0%

50%

100%

150%

200%

250%

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015e

2016e

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Uses for surplus cash?

Debt repayment

Shareholder returns: dividends, buybacks

But

Consolidation: mergers and acquisitions?

– Impeded by ownership & control restrictions

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

-6

-4

-2

0

2

4

6

8

10

12

2007 2008 2009 2010 2011 2012 2013 2014 2015f

N America Europe Asia Pacific Global Middle East Lat Am Africa

N America

Global

Asia PAcific

EuropeL America

Mid East

Africa

N America airline margin leads, Europe lags

Source: CAPA – Centre for Aviation, IATA

Airline EBIT margin (%) by region 2007 to 2015f

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Europe margins under-perform post recession

Source: CAPA – Centre for Aviation, IATA

Airline average EBIT margin (%) by region 2010 to 2015f

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

N America Asia Pacific Global Lat Am Middle East Europe Africa

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

0 200 400 600 800 1000 1200 1400

Market concentration (HHI based on share of seats)

Ave

EB

IT m

arg

in 2

01

0-2

01

5f

Europe

Asia Pacific

N America

Lat America

Middle East

Africa

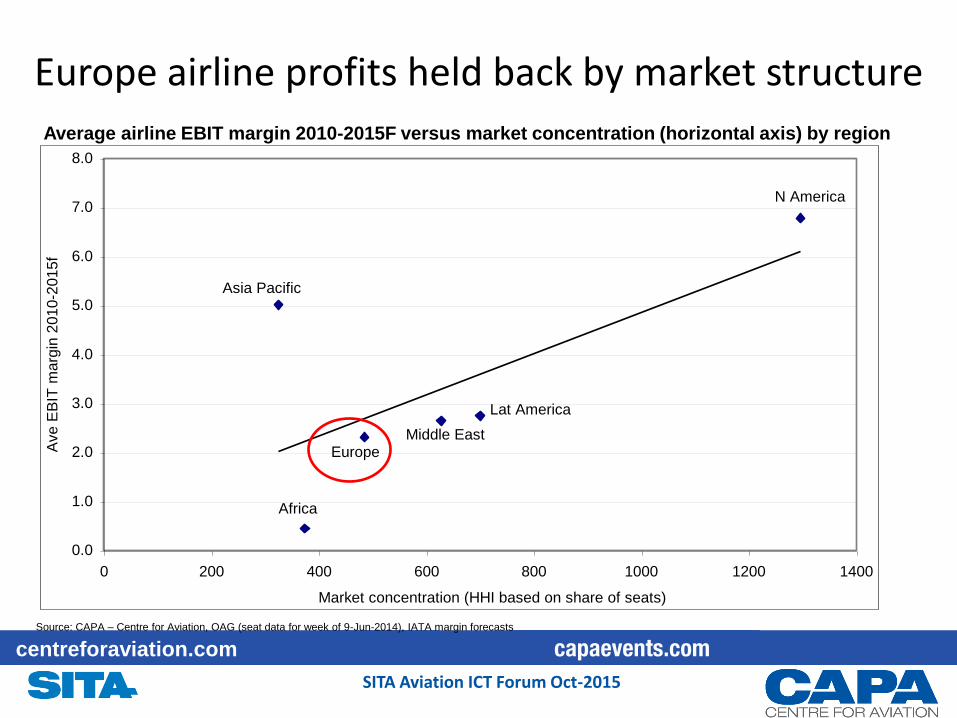

Europe airline profits held back by market structure

Source: CAPA – Centre for Aviation, OAG (seat data for week of 9-Jun-2014), IATA margin forecasts

Average airline EBIT margin 2010-2015F versus market concentration (horizontal axis) by region

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

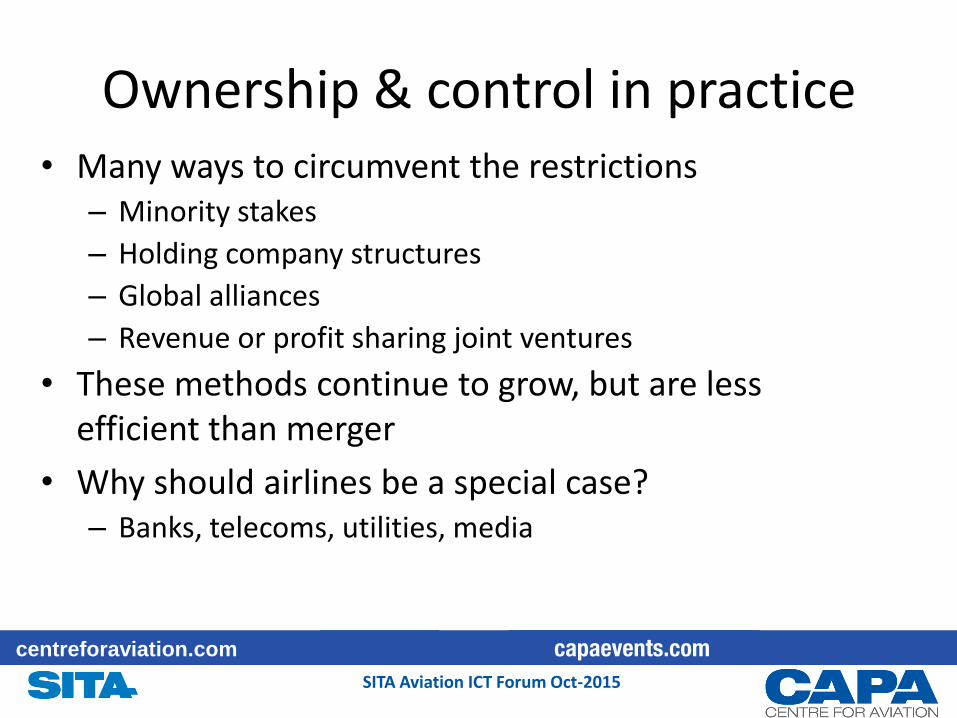

Ownership & control in practice • Many ways to circumvent the restrictions

– Minority stakes

– Holding company structures

– Global alliances

– Revenue or profit sharing joint ventures

• These methods continue to grow, but are less efficient than merger

• Why should airlines be a special case? – Banks, telecoms, utilities, media

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

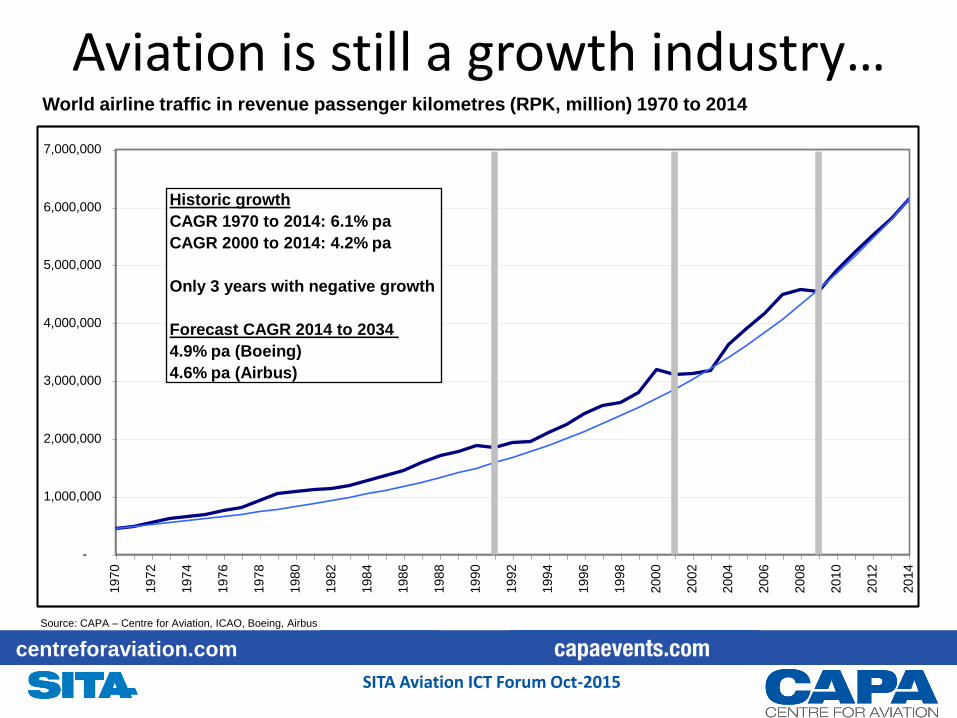

Aviation is still a growth industry…

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Historic growth

CAGR 1970 to 2014: 6.1% pa

CAGR 2000 to 2014: 4.2% pa

Only 3 years with negative growth

Forecast CAGR 2014 to 2034

4.9% pa (Boeing)

4.6% pa (Airbus)

Source: CAPA – Centre for Aviation, ICAO, Boeing, Airbus

World airline traffic in revenue passenger kilometres (RPK, million) 1970 to 2014

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

…but Europe will grow less rapidly Forecast CAGR in Europe revenue passenger kilometres (RPK, million) 2014 to 2034

Source: CAPA – Centre for Aviation, Boeing, Airbus

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

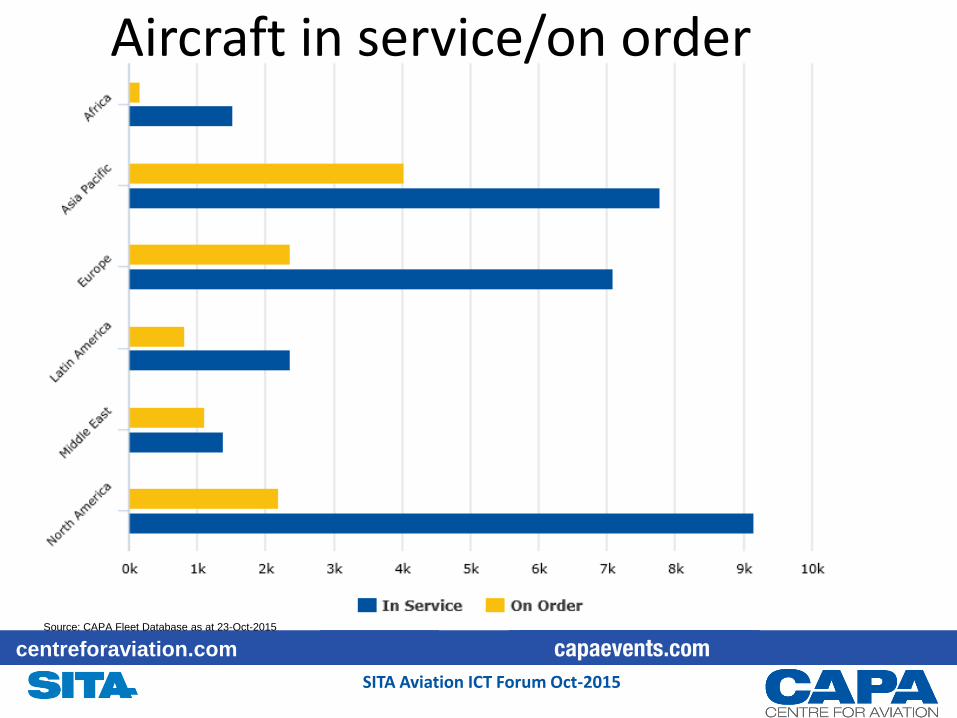

Aircraft in service/on order

Source: CAPA Fleet Database as at 23-Oct-2015

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

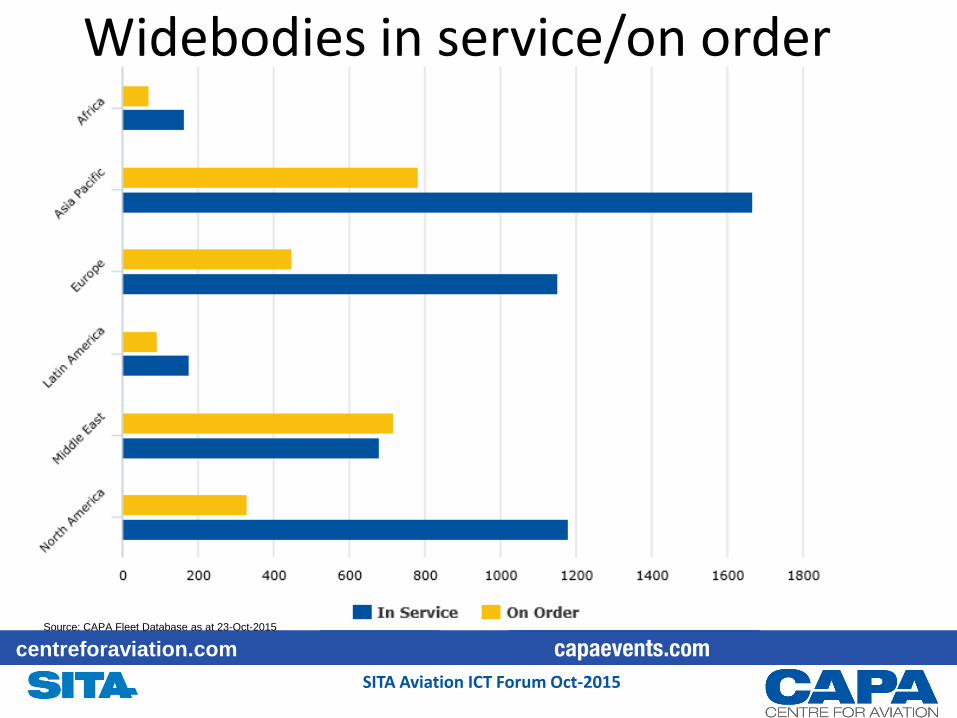

Widebodies in service/on order

Source: CAPA Fleet Database as at 23-Oct-2015

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

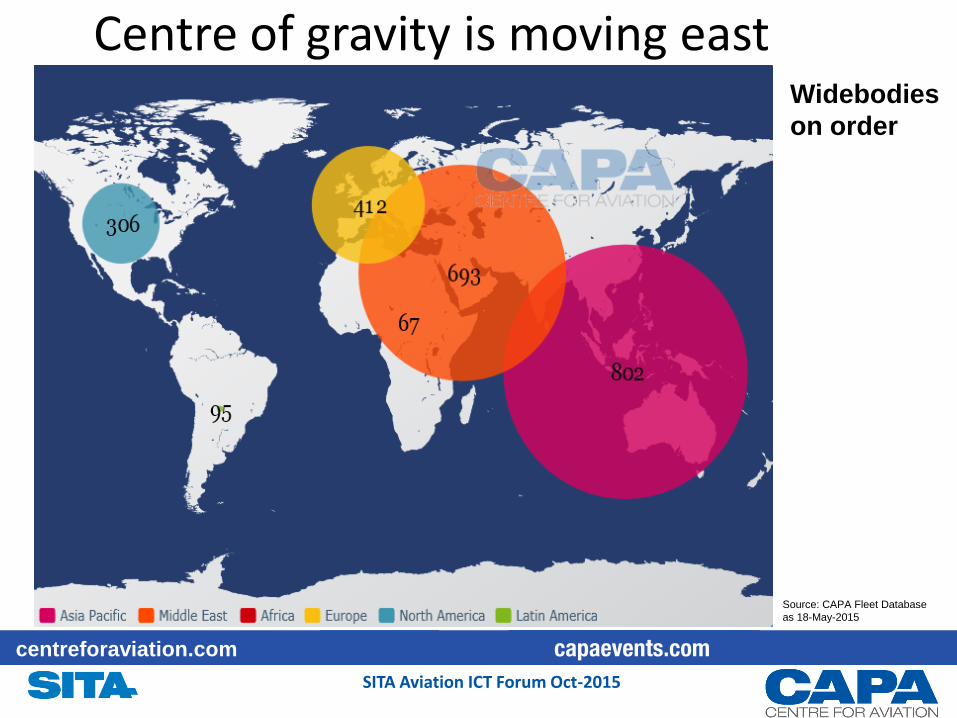

Centre of gravity is moving east

Source: CAPA Fleet Database

as 18-May-2015

Widebodies

on order

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Summary • Airline profits still cyclical

– Cost and capacity discipline may reduce cyclicality

• Ancillary revenue is growing – Will see more new revenue generation

• Europe’s airline profits held back by fragmentation – Ownership & control restrictions will reduce, slowly

– Partnerships and alliances will continue to grow

• Aviation is still a growth industry – Europe’s growth will be slower

– Europe will have to solve problems of infrastructure & taxes

• Centre of gravity is moving eastwards

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Summary • Airline profits still cyclical

– Cost and capacity discipline may reduce cyclicality

• Ancillary revenue is growing – Will see more new revenue generation

• Europe’s airline profits held back by fragmentation – Ownership & control restrictions will reduce, slowly

– Partnerships and alliances will continue to grow

• Aviation is still a growth industry – Europe’s growth will be slower

– Europe will have to solve problems of infrastructure & taxes

• Centre of gravity is moving eastwards

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Summary • Airline profits still cyclical

– Cost and capacity discipline may reduce cyclicality

• Ancillary revenue is growing – Will see more new revenue generation

• Europe’s airline profits held back by fragmentation – Ownership & control restrictions will reduce, slowly

– Partnerships and alliances will continue to grow

• Aviation is still a growth industry – Europe’s growth will be slower

– Europe will have to solve problems of infrastructure & taxes

• Centre of gravity is moving eastwards

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Summary • Airline profits still cyclical

– Cost and capacity discipline may reduce cyclicality

• Ancillary revenue is growing – Will see more new revenue generation

• Europe’s airline profits held back by fragmentation – Ownership & control restrictions will reduce, slowly

– Partnerships and alliances will continue to grow

• Aviation is still a growth industry – Europe’s growth will be slower

– Europe will have to solve problems of infrastructure & taxes

• Centre of gravity is moving eastwards

SITA Aviation ICT Forum Oct-2015

centreforaviation.com

Summary • Airline profits still cyclical

– Cost and capacity discipline may reduce cyclicality

• Ancillary revenue is growing – Will see more new revenue generation

• Europe’s airline profits held back by fragmentation – Ownership & control restrictions will reduce, slowly

– Partnerships and alliances will continue to grow

• Aviation is still a growth industry – Europe’s growth will be slower

– Europe will have to solve problems of infrastructure & taxes

• Centre of gravity is moving eastwards