Embed Size (px)

Citation preview

Axon

Group

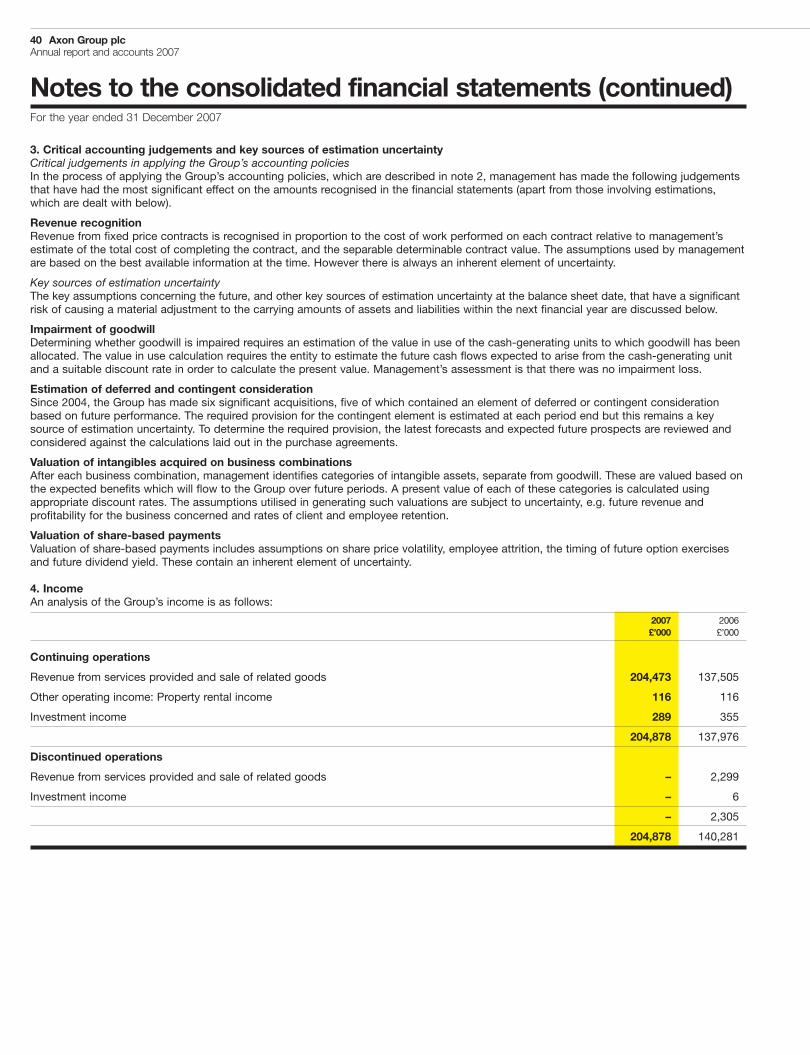

plcA

nnualreportandaccounts

2007

SAP-enabled Business TransformationAxon Group plcAnnual report and accounts 2007

www.axonglobal.com

12246 Axon R&A - cover:Layout 1 27/3/08 10:22 Page 1

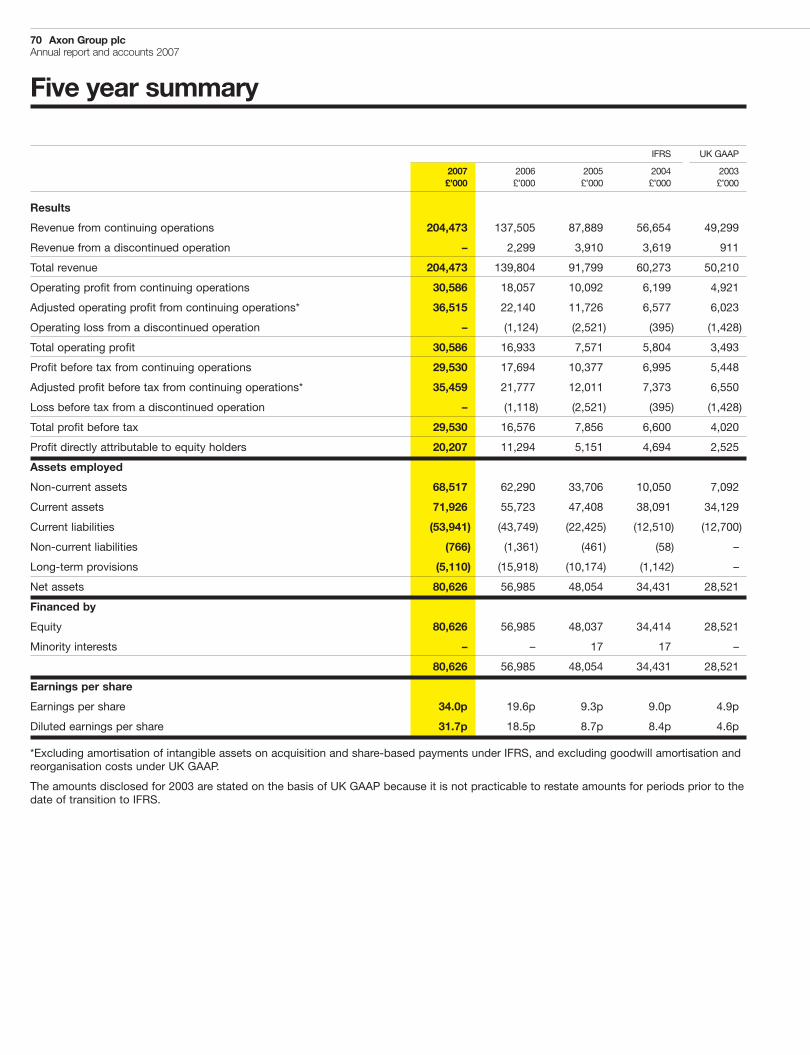

ifc Financial highlights01 Global reach10 Chairman’s statement11 Business review14 Financial review16 Board profiles18 Directors’ report21 Report on corporate governance24 Audit committee report25 Remuneration report30 Independent auditors’ report31 Consolidated income statement31 Consolidated statement of

recognised income and expense32 Consolidated balance sheet33 Company balance sheet34 Consolidated cash flow statement34 Company cash flow statement35 Notes to the consolidated

financial statements70 Five year summary71 Financial calendar 200872 Company information

and advisers

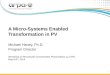

We have grown an average of 43%per annum since 2003.

+49%Revenue £m*

* From continuing operations

2003 49.3

2004 56.7

2005 87.9

2006 137.5

2007 204.5

+65%Adjusted operating profit £m**

**From continuing operations excluding amortisation of intangible assets on acquisition and share-based payments.

2003 6.0

2004 6.6

2005 11.7

2006 22.1

2007 36.5

+49%Adjusted diluted earningsper share pence per share**

**From continuing operations excluding amortisation of intangible assets on acquisition and share-based payments.

2003 8.2

2004 9.4

2005 14.0

2006 25.7

2007 38.4

+13%Dividend per 1p ordinary share 2003 2.5

2004 3.0

2005 3.5

2006 4.0

2007 4.5

The amounts disclosed for 2003 are stated on the basis of UK GAAP because it is not practicable to restate amounts for periods prior to the date of transition to IFRS.

01 Axon Group plcAnnual report and accounts 2007

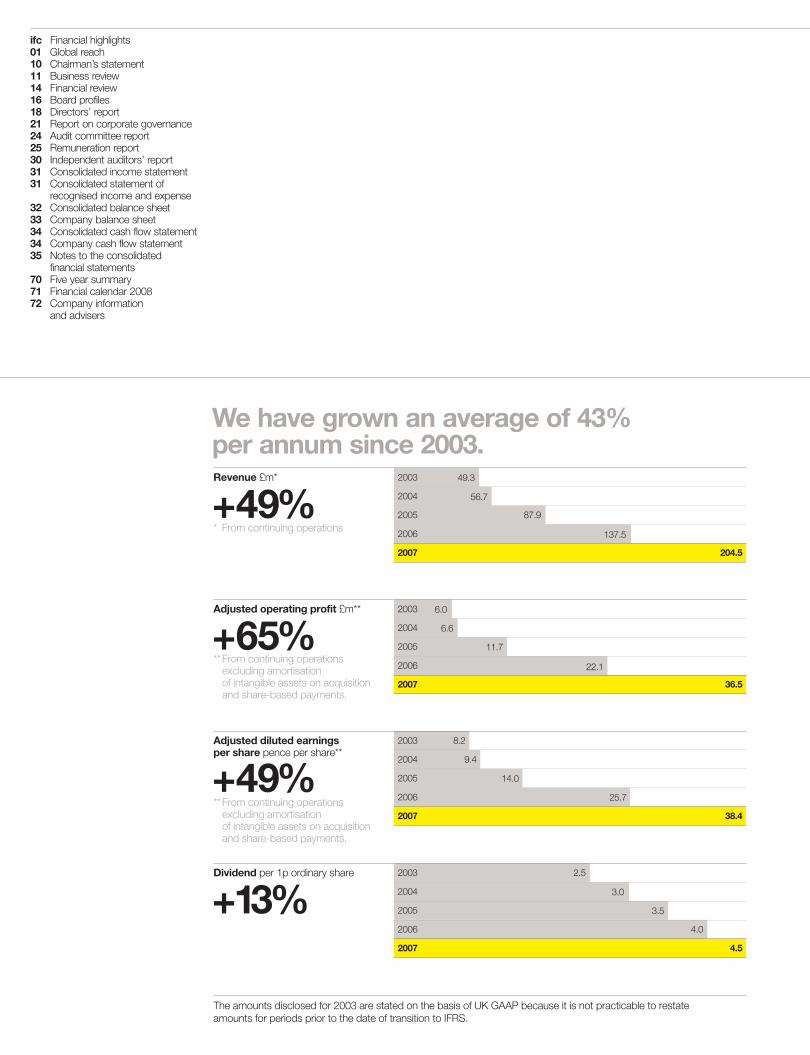

Axon is a Business Transformationconsultancy that designs, implements andsupports solutions to complex businessissues faced by large organisations thatuse SAP as their strategic platform.With a growing presence in the Americas,Asia, Europe and Australia we employ over1,650 people and deliver solutions in morethan 30 countries across the globe.

From small, highly targeted projects tothe transformation of entire organisations –we build strong relationships with a diversemix of clients around the world, acrossa broad range of sectors.

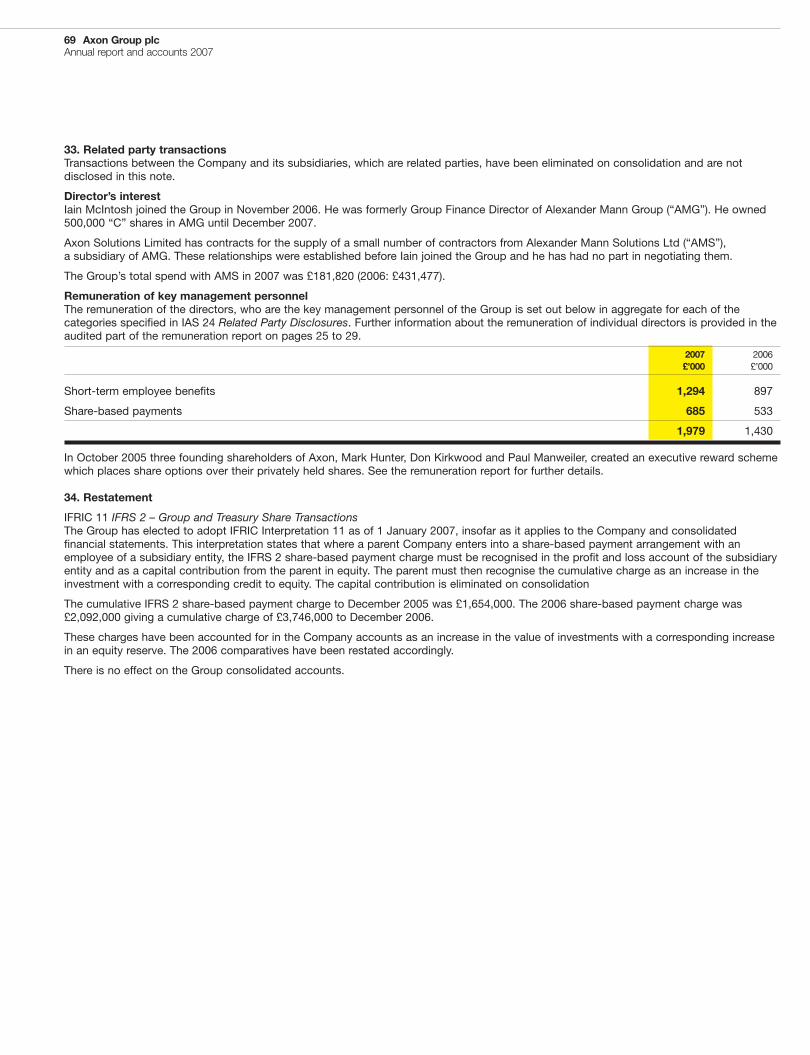

1. Chong Mei San(Lead FICO Consultant)The finance team ensured compliancewith Arch corporate accountingprinciples as well as satisfying localstatutory requirements. Axon providedviable solutions for localisationrequirements such as PRC GAAPvs US GAAP, Golden Tax Interfaceand Golden Audit.

2. Expanding Chinese OperationsArch Chemicals is constructinga new biocides plant in China to meeta strategic customer’s growing demandfor biocides used in the health andhygiene market.

02 Axon Group plcAnnual report and accounts 2007

1 2

03 Axon Group plcAnnual report and accounts 2007

3. Rapidly Growing Sales in ChinaSince 2003, Arch has been rapidlygrowing in China. Their product portfolioincludes health, hygiene and personalcare products, water products, woodcoatings and industrial biocides.

4. Tan Boon Hoi(Project Manager)Effective communication andcoordination were critical to the successof this project with resources workingacross multiple regions. Continualmonitoring and reporting of the projectstatus and deliverables contributedto the successful go-live of the project.

5. Ting Woo Lee(Lead Technical Consultant)Axon was responsible for the deliveryof reports, forms and interfacesin both Chinese and English. Whilstmanaged and delivered locally, thesewere developed in compliance withArch Chemicals’ global standards.

Arch ChemicalsArch Chemicals Inc, headquartered in Norwalk, USA, is a global biocidescompany with approximately $1.5 billion in annual sales. Since 2003,Arch Chemicals has strengthened its presence in China by establishingtrading and/or production facilities in Shanghai, Suzhou and Hong Kongto enhance its ability to provide superior products and technical supportservices in this fast-growing region.

Axon China worked with Arch to roll the Chinese subsidiaries into Arch’sglobal SAP system. The subsidiaries are now using corporate businessprocesses, a common technology platform and global system governance.

4 5

3

04 Axon Group plcAnnual report and accounts 2007

1. Mahalakshmi Ravindran(Programme Manager)The Axon team included industryveterans who have spent their careersdriving operational improvement andregulatory compliance through the useof SAP technologies.

2. Texas Electricity MarketOnly 11 countries in the world usemore electricity than the State of Texas.TXU Energy has the largest numberof customers in Texas and has leadingaccess to one of the top competitiveelectric markets in the world.

3. Carsten Rueppel(Integration Manager)To ensure the benefits of a fullend-to-end business processes flow,the solution integrates to severaloutside systems including, to namea few, Interactive Voice Recognitionsoftware, the ERCOT market, onlineweb services, and documentmanagement and retrieval systems.

TXU EnergyTXU Energy, the largest retail electric provider in the State of Texas,provides electricity and related services to more than 2.1 million residentialand business customers in the most competitive electricity market in theUnited States. To remain the #1 choice for Texas consumers, TXU Energyoffers innovative products and solutions, allowing customers to chooseoptions that best meet their energy needs.

Axon is managing a major transformation of TXU Energy’s marketingand customer service operations by implementing SAP’s customerrelationship and billing solution. To complete the transformation the projectleverages comprehensive business intelligence, focused customeranalytics in CRM, intricate integration with ERCOT (the Texas independentgrid operator), flexible billing and pricing capabilities, convenientcustomer-facing web and telephony options, and efficiency-drivenimprovements to customer service operations.

21

3

05 Axon Group plcAnnual report and accounts 2007

4. Andre Vanhonschooten(Customer Services Lead)The solution provides a variety ofmethods for the customer to interactwith TXU Energy at their comfortand convenience. These methodsinclude 24/7 personal interactionwith customer service representatives,automated voice recognitionand easy-to-use web services.

5. Increasing CompetitionSince the market ‘opened’ in 2002,TXU Energy has experienced increasingcompetition. The company’s focushas been to improve its competitiveofferings while bringing innovativecomplementary products to market, suchas competitively priced service plans,innovative energy efficiency offerings,and renewable energy programmes.

5

4

06 Axon Group plcAnnual report and accounts 2007

1. A World LeaderNATS employs around 5,000 peoplein a wide range of roles. Air TrafficControllers and Air Traffic Assistantsmake up about half of the organisation,but a significant percentage of theworkforce is made up of engineers,scientists and research analysts.

2. Stuart Querns(Solution Architect)Axon and NATS developed a clear viewand understanding of the key businessrequirements and overall solution.The Axon team was able to offer a focalpoint for solution understanding,direction and challenge to support keycommunication and training, as wellas management of the project itself.

3. Three Phase ProgrammeNIBS2 was introduced in 3 phasesaligned with NATS’ business cycle.Phase 1 - Business planning on anactivity basis. Phase 2 - ActivityManagement, Employee, Managerand Contractor Self Service, RealEstate, Fixed Assets and BusinessWarehouse. Phase 3 - Integrated controlmaintenance of all NATS assets.

2 31

07 Axon Group plcAnnual report and accounts 2007

NATS

4. Dieter Bosch(Data Migration Lead)Data accuracy is fundamental to NATS.The successful planning and migrationof data to the new SAP system was asignificant project deliverable. Hundredsof thousands of records were testedand loaded, enabling benefits to bedriven from a solid base as the newprocesses were introduced.

5. Change Managementand CommunicationThe NIBS2 implementation wasunderpinned by a major changeand communication programme.Super-users were trained andhundreds of leaders were briefedon the system and asked to beambassadors for the changes withintheir business areas.

NATS provides air traffic control services at 15 of the UK's biggestairports, and "en-route" air traffic services for aircraft flying through UKairspace and the eastern North Atlantic. Last year NATS handled nearly2.5 million flights carrying more than 220 million passengers. NATS isleading the industry in terms of technological and business developmentand sells a range of product and consultancy services.

In 2007, NATS completed the introduction of its New Integrated BusinessSystem – NIBS2. The SAP-enabled business transformation programmehas providedNATSwith a single system tomanage its people, finance, assetsand activities. The programme has also introduced a significant numberof changes to NATS’ business processes. For example, integrated andcommon processes have now enabled staff to be deployed on value-addedactivities rather than transaction processing. Most importantly, NATSnow has better information available to them to make decisions on howto control the company more effectively.

The effective partnership between NATS and Axon was key to the successof the programme and helped NATS to win the 2007 SAP Quality Awardfor the best local implementation of a new SAP integrated business system.

5

4

08 Axon Group plcAnnual report and accounts 2007

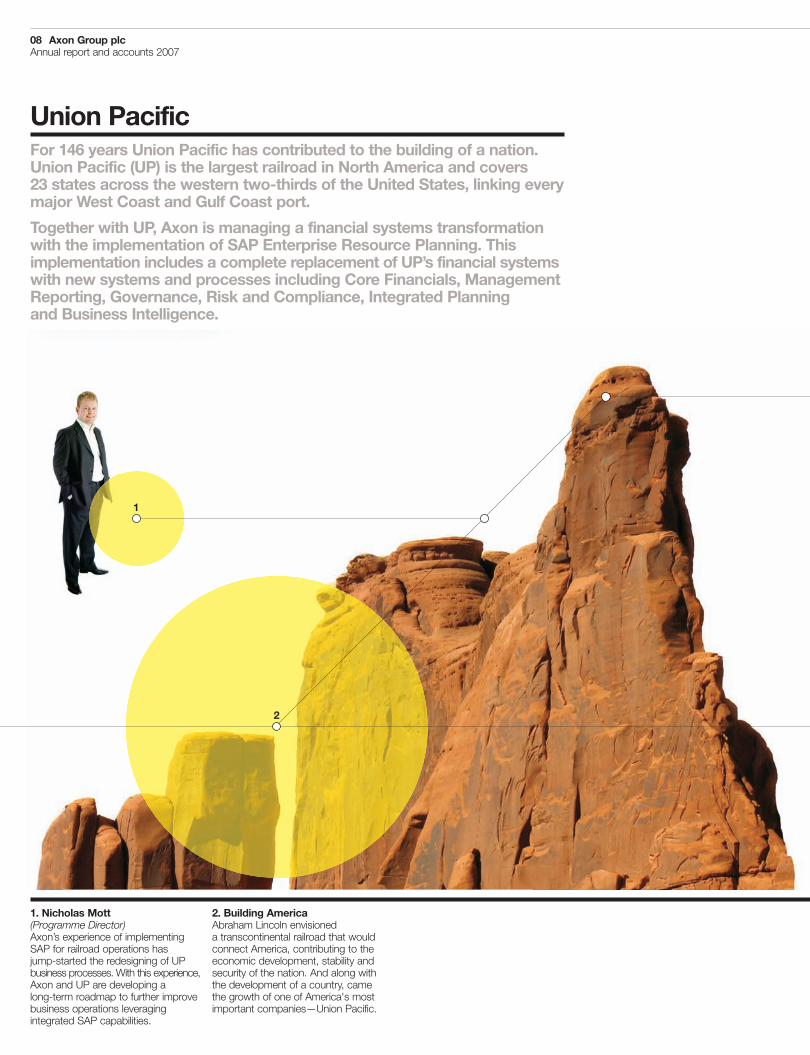

1. Nicholas Mott(Programme Director)Axon’s experience of implementingSAP for railroad operations hasjump-started the redesigning of UPbusiness processes. With this experience,Axon and UP are developing along-term roadmap to further improvebusiness operations leveragingintegrated SAP capabilities.

2. Building AmericaAbraham Lincoln envisioneda transcontinental railroad that wouldconnect America, contributing to theeconomic development, stability andsecurity of the nation. And along withthe development of a country, camethe growth of one of America's mostimportant companies—Union Pacific.

Union PacificFor 146 years Union Pacific has contributed to the building of a nation.Union Pacific (UP) is the largest railroad in North America and covers23 states across the western two-thirds of the United States, linking everymajor West Coast and Gulf Coast port.

Together with UP, Axon is managing a financial systems transformationwith the implementation of SAP Enterprise Resource Planning. Thisimplementation includes a complete replacement of UP’s financial systemswith new systems and processes including Core Financials, ManagementReporting, Governance, Risk and Compliance, Integrated Planningand Business Intelligence.

2

1

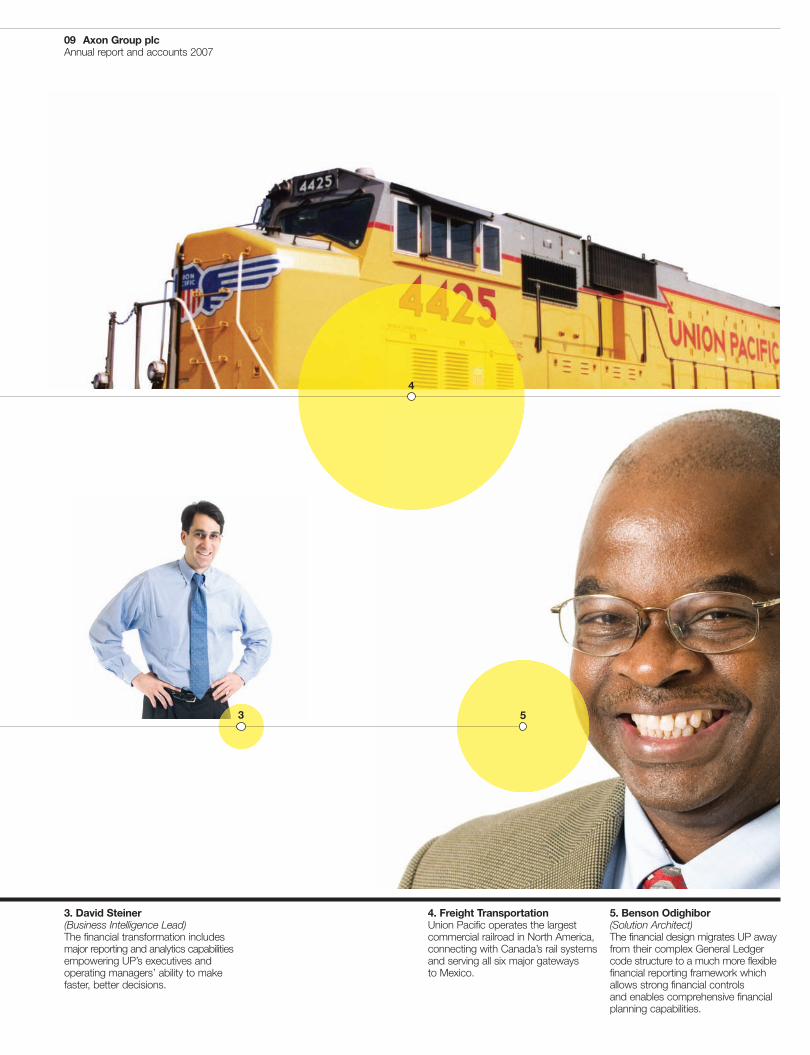

3. David Steiner(Business Intelligence Lead)The financial transformation includesmajor reporting and analytics capabilitiesempowering UP’s executives andoperating managers’ ability to makefaster, better decisions.

4. Freight TransportationUnion Pacific operates the largestcommercial railroad in North America,connecting with Canada’s rail systemsand serving all six major gatewaysto Mexico.

5. Benson Odighibor(Solution Architect)The financial design migrates UP awayfrom their complex General Ledgercode structure to a much more flexiblefinancial reporting framework whichallows strong financial controlsand enables comprehensive financialplanning capabilities.

09 Axon Group plcAnnual report and accounts 2007

53

4

09 Axon Group plcAnnual report and accounts 2007

10 Axon Group plcAnnual report and accounts 2007

I am very pleased to be writing my first Chairman’s reportat Axon. Since I joined the Board as a non-executive four yearsago I have seen the Group deliver on the strategy laid outin 2003 to become a global player in the delivery of BusinessTransformation services for large organisations that use SAPas their strategic platform.

Mark Hunter moved to Executive Chairman in March 2007and retired from the Board at the end of December. Mark foundedAxon in 1994 and as CEO grew it into a leading UK player inthe SAP services market. We all wish Mark the best for the futureand thank him for leaving Axon in such good shape.

Steve Cardell was appointed CEO in March 2007, having joinedAxon in 2001 and been COO since 2003. Steve has beenthe prime driver behind our expansion into business consultingand transformation services and in building our North Americanbusiness from scratch.

Steve has set out a revised vision for the Group to bethe world’s leading consulting firm for major organisationswho wish to transform themselves using SAP as theirtechnology platform.

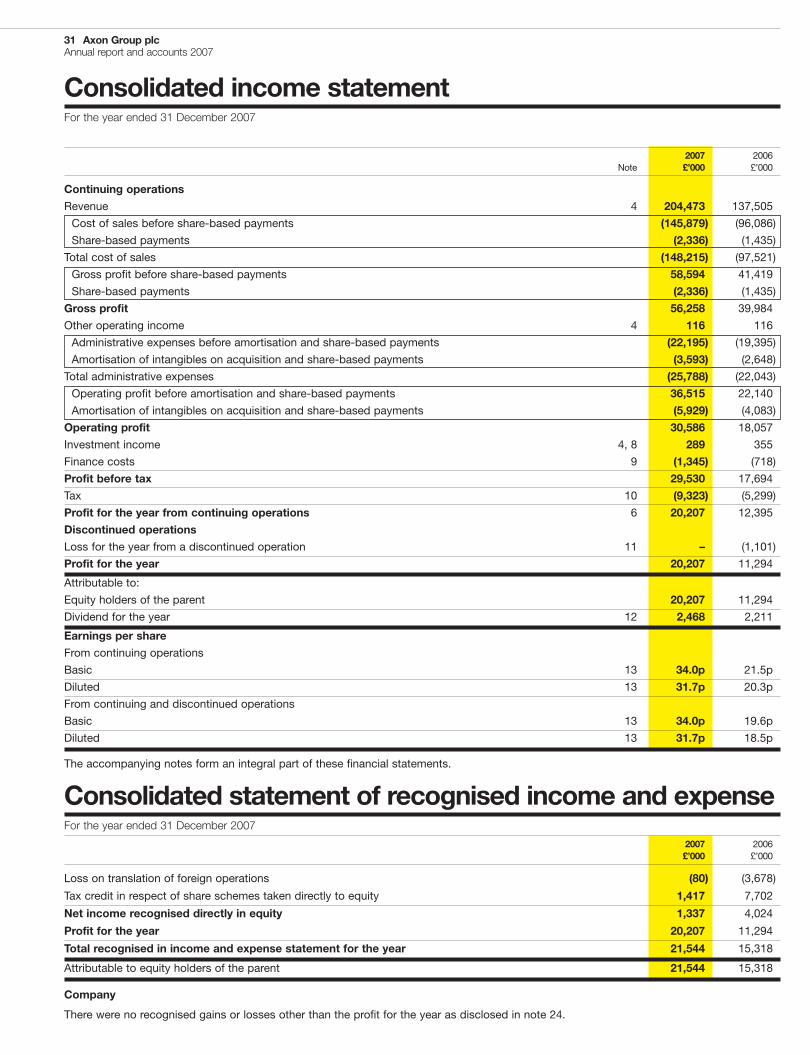

We grew Group revenues by 49% to £204.5m (2006: £137.5m)this year while also improving operating margins. Revenuesfrom our North American business more than doubled withorganic growth of 41%. North America represented 36%of total revenues in the year (2006: 23%). With less than 2%of the global SAP services market (source: Gartner), Axon’sopportunity for growth in the future remains considerable.

Our European business has continued to prosper throughthe delivery of pan-European transformation programmesand our continued success in the Local Government sector.We have also seen encouraging early signs from our entryinto the Financial Services sector which opens up wider marketsin the medium-term even if the sector may face its owndifficulties in the short run.

The use of an offshore delivery model is integral to our proposition.We expanded our presence in Malaysia through the acquisitionof JSPC which has also given us a foothold in China.

Cash generation remained strong, with 128% of total operatingprofit of £30.6m (2006: £18.1m) being converted into operatingcash flow despite the high growth in revenues during the year.Net cash rose by £19.1m to £25.3m (2006: £6.2m netof £6m borrowing).

Adjusted operating profit* increased by 65% to £36.5m (2006:£22.1m) reflecting further leveraging of the indirect cost base.

Adjusted diluted earnings per share* are up 49% to 38.4p(2006: 25.7p), a very strong performance for our sector, anddiluted earnings per share are up 56% to 31.7p (2006: 20.3p).We continue to have a progressive dividend policy, and theBoard is recommending a final dividend of 2.5p per share,which combined with the interim dividend of 2.0p makes a totaldividend for the year of 4.5p (2006: 4.0p). The final dividendpayment will be made on 20 June 2008 to shareholders on theregister as at 23 May 2008.

All of Axon’s people around the world should be proud of theirperformance and I would like to thank them for their outstandingcontribution to the business.

There has been considerable uncertainty in the stockmarkets,with concern over potential regional and global recessions,which has had a very negative effect on technology sectorvaluations. However, based on SAP’s strong market positionand Axon’s scope to increase market share outside the UK,I look forward with confidence to further revenue growth in 2008.

Roy MerrittChairman4 March 2008

* Excluding amortisation of intangible assets on acquisition and share-based payments of £2.5mand £3.5m respectively (2006: £2.0m and £2.1m respectively) and related tax effect in relationto the adjusted profit after taxation as calculated in note 13.

In 2007, Axon sawstrong revenue growthacross each of itsoperating regions,delivered an increasein operating marginsand generatedstrong cash flows.

Chairman’s statement

11 Axon Group plcAnnual report and accounts 2007

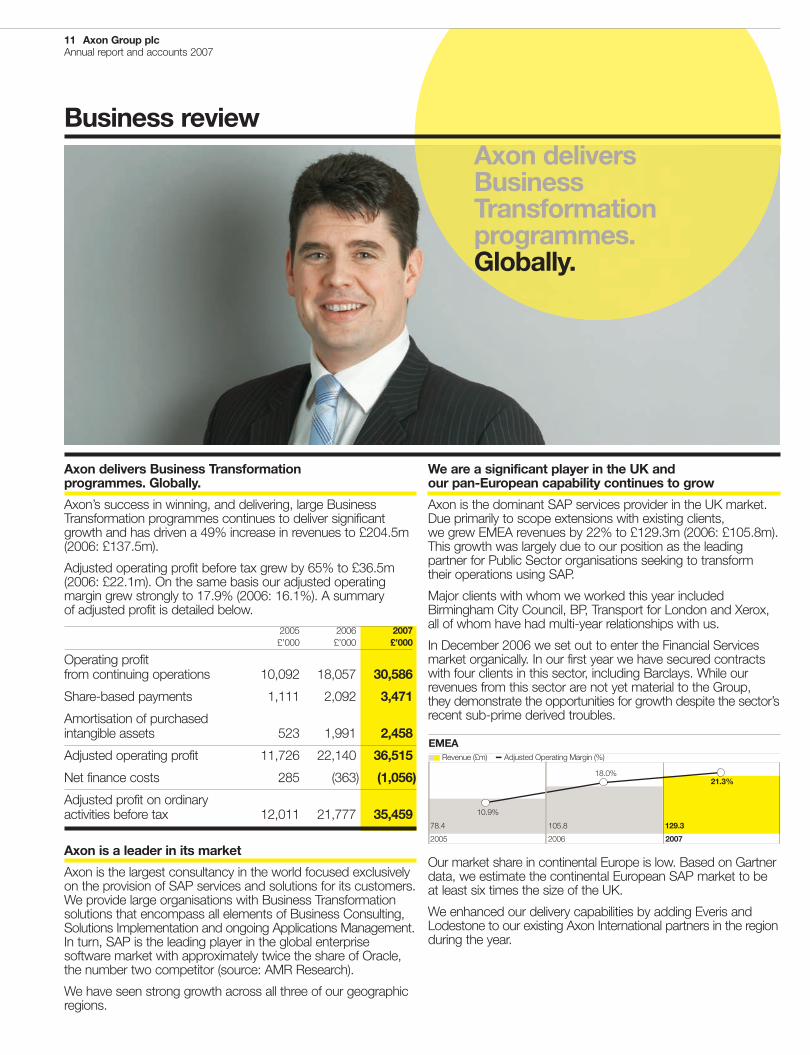

Axon delivers Business Transformationprogrammes. Globally.

Axon’s success in winning, and delivering, large BusinessTransformation programmes continues to deliver significantgrowth and has driven a 49% increase in revenues to £204.5m(2006: £137.5m).

Adjusted operating profit before tax grew by 65% to £36.5m(2006: £22.1m). On the same basis our adjusted operatingmargin grew strongly to 17.9% (2006: 16.1%). A summaryof adjusted profit is detailed below.

2005 2006 2007£’000 £’000 £’000

Operating profitfrom continuing operations 10,092 18,057 30,586

Share-based payments 1,111 2,092 3,471

Amortisation of purchasedintangible assets 523 1,991 2,458

Adjusted operating profit 11,726 22,140 36,515

Net finance costs 285 (363) (1,056)

Adjusted profit on ordinaryactivities before tax 12,011 21,777 35,459

Axon is a leader in its market

Axon is the largest consultancy in the world focused exclusivelyon the provision of SAP services and solutions for its customers.We provide large organisations with Business Transformationsolutions that encompass all elements of Business Consulting,Solutions Implementation and ongoing Applications Management.In turn, SAP is the leading player in the global enterprisesoftware market with approximately twice the share of Oracle,the number two competitor (source: AMR Research).

We have seen strong growth across all three of our geographicregions.

We are a significant player in the UK andour pan-European capability continues to grow

Axon is the dominant SAP services provider in the UK market.Due primarily to scope extensions with existing clients,we grew EMEA revenues by 22% to £129.3m (2006: £105.8m).This growth was largely due to our position as the leadingpartner for Public Sector organisations seeking to transformtheir operations using SAP.

Major clients with whom we worked this year includedBirmingham City Council, BP, Transport for London and Xerox,all of whom have had multi-year relationships with us.

In December 2006 we set out to enter the Financial Servicesmarket organically. In our first year we have secured contractswith four clients in this sector, including Barclays. While ourrevenues from this sector are not yet material to the Group,they demonstrate the opportunities for growth despite the sector’srecent sub-prime derived troubles.

Our market share in continental Europe is low. Based on Gartnerdata, we estimate the continental European SAP market to beat least six times the size of the UK.

We enhanced our delivery capabilities by adding Everis andLodestone to our existing Axon International partners in the regionduring the year.

Axon deliversBusinessTransformationprogrammes.Globally.

Business review

EMEA Adjusted Operating Margin (%)

10.9%

2005 2006 2007

78.4 105.8 129.3

18.0%21.3%

Revenue (£m)

12 Axon Group plcAnnual report and accounts 2007

Business review (continued)

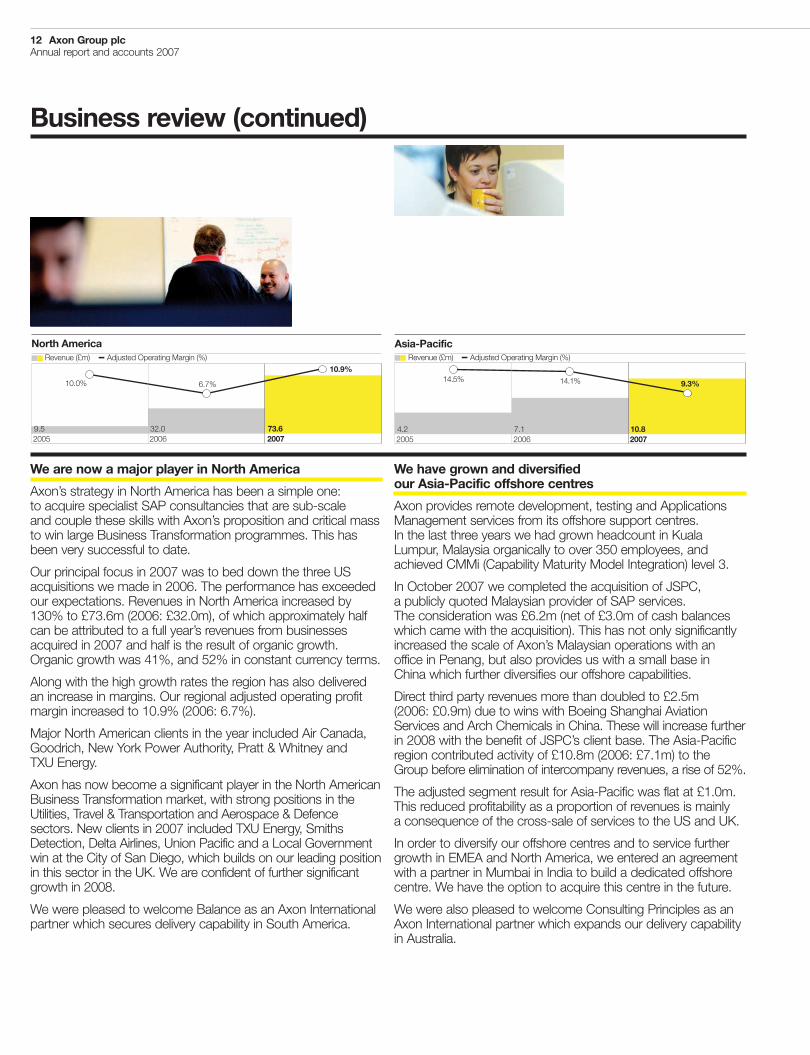

We are now a major player in North America

Axon’s strategy in North America has been a simple one:to acquire specialist SAP consultancies that are sub-scaleand couple these skills with Axon’s proposition and critical massto win large Business Transformation programmes. This hasbeen very successful to date.

Our principal focus in 2007 was to bed down the three USacquisitions we made in 2006. The performance has exceededour expectations. Revenues in North America increased by130% to £73.6m (2006: £32.0m), of which approximately halfcan be attributed to a full year’s revenues from businessesacquired in 2007 and half is the result of organic growth.Organic growth was 41%, and 52% in constant currency terms.

Along with the high growth rates the region has also deliveredan increase in margins. Our regional adjusted operating profitmargin increased to 10.9% (2006: 6.7%).

Major North American clients in the year included Air Canada,Goodrich, New York Power Authority, Pratt & Whitney andTXU Energy.

Axon has now become a significant player in the North AmericanBusiness Transformation market, with strong positions in theUtilities, Travel & Transportation and Aerospace & Defencesectors. New clients in 2007 included TXU Energy, SmithsDetection, Delta Airlines, Union Pacific and a Local Governmentwin at the City of San Diego, which builds on our leading positionin this sector in the UK. We are confident of further significantgrowth in 2008.

We were pleased to welcome Balance as an Axon Internationalpartner which secures delivery capability in South America.

We have grown and diversifiedour Asia-Pacific offshore centres

Axon provides remote development, testing and ApplicationsManagement services from its offshore support centres.In the last three years we had grown headcount in KualaLumpur, Malaysia organically to over 350 employees, andachieved CMMi (Capability Maturity Model Integration) level 3.

In October 2007 we completed the acquisition of JSPC,a publicly quoted Malaysian provider of SAP services.The consideration was £6.2m (net of £3.0m of cash balanceswhich came with the acquisition). This has not only significantlyincreased the scale of Axon’s Malaysian operations with anoffice in Penang, but also provides us with a small base inChina which further diversifies our offshore capabilities.

Direct third party revenues more than doubled to £2.5m(2006: £0.9m) due to wins with Boeing Shanghai AviationServices and Arch Chemicals in China. These will increase furtherin 2008 with the benefit of JSPC’s client base. The Asia-Pacificregion contributed activity of £10.8m (2006: £7.1m) to theGroup before elimination of intercompany revenues, a rise of 52%.

The adjusted segment result for Asia-Pacific was flat at £1.0m.This reduced profitability as a proportion of revenues is mainlya consequence of the cross-sale of services to the US and UK.

In order to diversify our offshore centres and to service furthergrowth in EMEA and North America, we entered an agreementwith a partner in Mumbai in India to build a dedicated offshorecentre. We have the option to acquire this centre in the future.

We were also pleased to welcome Consulting Principles as anAxon International partner which expands our delivery capabilityin Australia.

Adjusted Operating Margin (%)Revenue (£m)

A

North America

2005 2006 20079.5 32.0 73.6

10.0% 6.7%

10.9%

N

Asia-Pacific

2005 2006 20074.2 7.1 10.8

14.5% 14.1% 9.3%

Adjusted Operating Margin (%)Revenue (£m)

A

Business Consulting growth is drivenby Business Transformation programmes

Our Business Consulting division helps our clients to delivermore effective strategies by facilitating improvements in process,technology and people. It determines whether individual businessfunctions and systems meet the current objectives of the business;can change fast enough to meet the future needs of thebusiness; and are communicating adequately with each other.

Business Consulting revenues grew by 60% from £25.0min 2006 to £39.9m in 2007, which represents 19% of turnover(2006: 18%).

Solutions Implementationhad a strong performance in 2007

We have a reputation for rapid, innovative implementationof complex business systems. Our Solutions Implementationteam works closely with the client at all levels defining anddelivering new business processes and systems, whilst ensuringthat the people within the organisation enthusiastically embracethe changes. Once the transition to a new platform has beenmade, we ensure that the new working environment is stableprior to focusing on the delivery of quantifiable business benefits.

As anticipated, Solutions Implementation performed stronglyin 2007 and revenues grew by 59% to £141.0m (2006: £88.7m)which represents 69% of turnover (2006: 65%).

We are rebuilding our ApplicationsManagement proposition

We provide ongoing support and evolution for our clientsthat have undergone a Business Transformation programme.Our focus is on niche, high value added applicationsmanagement. We run and support critical business applicationsfor our clients 24 hours per day, 7 days a week, 365 daysa year globally. This support ensures that the working practicesand software systems enable the business to respond to anyfurther internal or external imperatives.

Applications Management revenues decreased by 1%to £23.6m (2006: £23.8m), which represents 12% of turnover(2006: 17%), in part reflecting increased use of offshore resources.

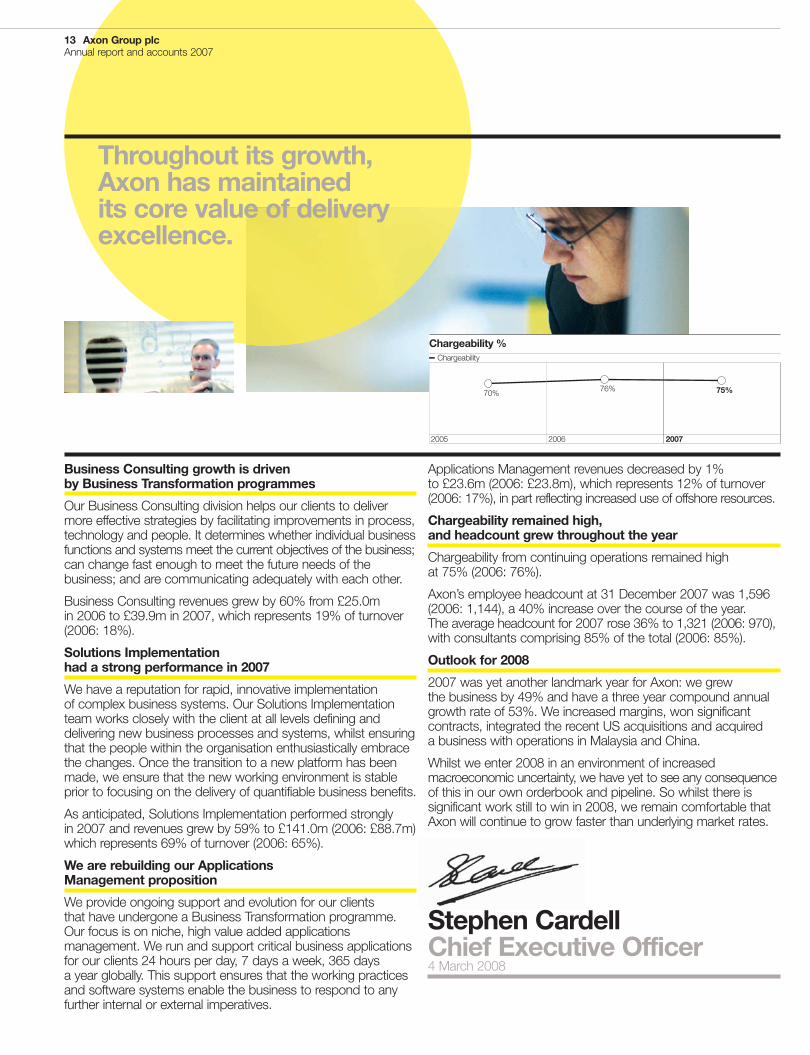

Chargeability remained high,and headcount grew throughout the year

Chargeability from continuing operations remained highat 75% (2006: 76%).

Axon’s employee headcount at 31 December 2007 was 1,596(2006: 1,144), a 40% increase over the course of the year.The average headcount for 2007 rose 36% to 1,321 (2006: 970),with consultants comprising 85% of the total (2006: 85%).

Outlook for 2008

2007 was yet another landmark year for Axon: we grewthe business by 49% and have a three year compound annualgrowth rate of 53%. We increased margins, won significantcontracts, integrated the recent US acquisitions and acquireda business with operations in Malaysia and China.

Whilst we enter 2008 in an environment of increasedmacroeconomic uncertainty, we have yet to see any consequenceof this in our own orderbook and pipeline. So whilst there issignificant work still to win in 2008, we remain comfortable thatAxon will continue to grow faster than underlying market rates.

Stephen CardellChief Executive Officer4 March 2008

Chargeability %

70%

2005 2006 2007

76% 75%

Chargeability

Throughout its growth,Axon has maintainedits core value of deliveryexcellence.

13 Axon Group plcAnnual report and accounts 2007

14 Axon Group plcAnnual report and accounts 2007

Top line growth across all regions

We had strong revenue growth of 49% across the Group withthird party revenues up 23% in EMEA, 132% in North Americaand 167% in Asia-Pacific.

All EMEA growth was organic and organic growth in NorthAmerica in constant currency terms was 52%.

Solid margin performance

Adjusted gross margins decreased from 30.1% (£41.4m)in 2006 to 28.7% (£58.6m). A higher proportion of totalrevenues came from North America which has lower marginsthan the UK. It is not anticipated that gross margins will increaseduring 2008. In the UK we expect margins to be lower thanrecent peaks which have benefited from very high levels ofchargeability and strong performance on fixed price projects.

Administration costs, excluding share-based paymentsand purchased intangible asset amortisation, showed anotherimprovement this year to 10.9% of revenue compared to 14.1%in 2006. This is a strong performance in light of increasesin the cost of recruitment and investment in back office teamsin Asia-Pacific and North America. We also put our moneywhere our mouth is and replaced our own disparate financesystems globally with SAP, which went live to plan in July 2007.

Adjusted operating profit in 2007 grew to £36.5m(2006: £22.1m), representing an adjusted operating marginof 17.9% (2006: 16.1%). Unadjusted operating profit grew69% to £30.6m (2006: £18.1m), equivalent to an operatingmargin of 15.0% (2006: 13.1%).

Good cash flow has again been usedto fund our geographic expansion

Although revenue grew by 49% in 2007, there was onlya 15% increase in trade debtors from £27.4m in 2006 to£31.4m in 2007. The business had another year of excellentperformance in terms of cash generation, with 128%of operating profit being converted into operating cash flow(2006: 133%) despite the high levels of growth. It is anticipatedthat this level of conversion of profits to cash will fall significantlyin 2008, reflecting the cash flow profiles of new project winsand that the year-on-year rate of improvement in working capitalmanagement cannot be sustained at recent levels.

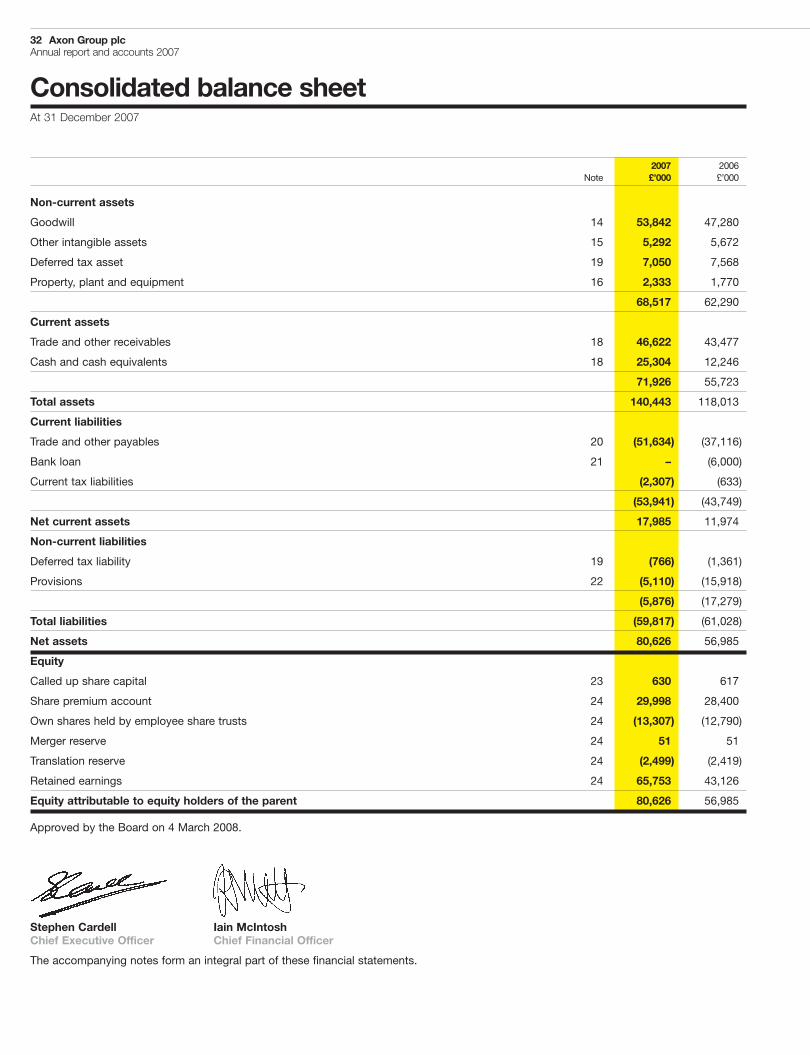

Net cash increased by £19.1m to £25.3m (2006: £6.2mnet of £6m borrowing), even after cash outflows of £11.7mfor the payment of dividends, the acquisition of JSPC andpayments with respect to earn-outs relating to earlier acquisitions.A significant portion of these balances are expected to beapplied in 2008 to payments of deferred consideration relatingto past acquisitions.

Net interest income before the cost of unwinding discountedprovisions for deferred consideration in 2007 reduced to £0.1mcompared to £0.3m in 2006, due to temporary recourse tobank funding during the year relating to acquisitions.

Topline growth acrossall regions translatedinto increased profitsand cash.

Financial review

15 Axon Group plcAnnual report and accounts 2007

We have continued to invest in infrastructureto support the business

Capital expenditure increased from £1.2m in 2006 to £3.3min 2007 and the majority of investments were on internal SAPsystems, computer equipment and office infrastructure.

Taxation

The tax charge for the year of £9.3m represents an effective taxrate of 32% on continuing operations (2006: 30%). The highercharge reflects increased US profitability.

Earnings per share grew

The adjusted profit after tax was £24.5m (2006: £15.7m)resulting in adjusted earnings per share of 41.2p (2006: 27.1p).Adjusted diluted earnings per share were 38.4p (2006: 25.7p),an increase of 49%. Profit after tax from continuing operationswas £20.2m (2006: £12.4m) resulting in earnings per shareof 34.0p (2006: 21.5p). Diluted earnings per share were 31.7p(2006: 20.3p), an increase of 56%.

Iain McIntoshChief Financial Officer4 March 2008

16 Axon Group plcAnnual report and accounts 2007

Board profiles

ExecutiveDirectors

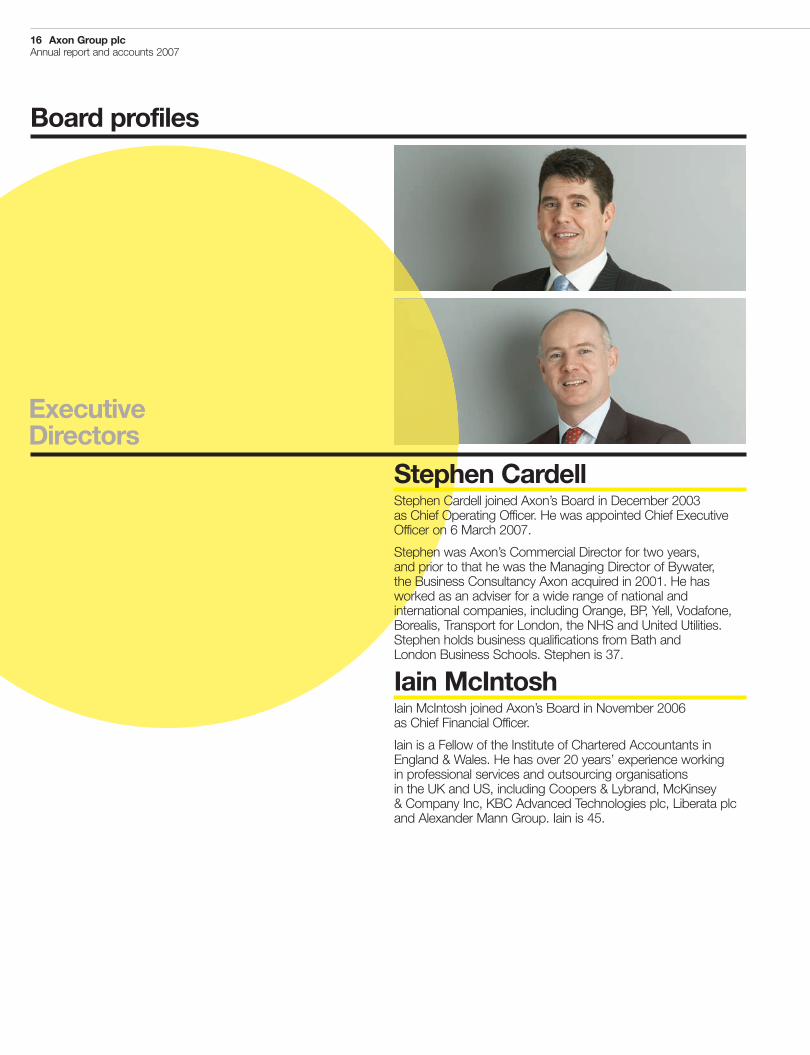

Stephen CardellStephen Cardell joined Axon’s Board in December 2003as Chief Operating Officer. He was appointed Chief ExecutiveOfficer on 6 March 2007.

Stephen was Axon’s Commercial Director for two years,and prior to that he was the Managing Director of Bywater,the Business Consultancy Axon acquired in 2001. He hasworked as an adviser for a wide range of national andinternational companies, including Orange, BP, Yell, Vodafone,Borealis, Transport for London, the NHS and United Utilities.Stephen holds business qualifications from Bath andLondon Business Schools. Stephen is 37.

Iain McIntoshIain McIntosh joined Axon’s Board in November 2006as Chief Financial Officer.

Iain is a Fellow of the Institute of Chartered Accountants inEngland & Wales. He has over 20 years’ experience workingin professional services and outsourcing organisationsin the UK and US, including Coopers & Lybrand, McKinsey& Company Inc, KBC Advanced Technologies plc, Liberata plcand Alexander Mann Group. Iain is 45.

17 Axon Group plcAnnual report and accounts 2007

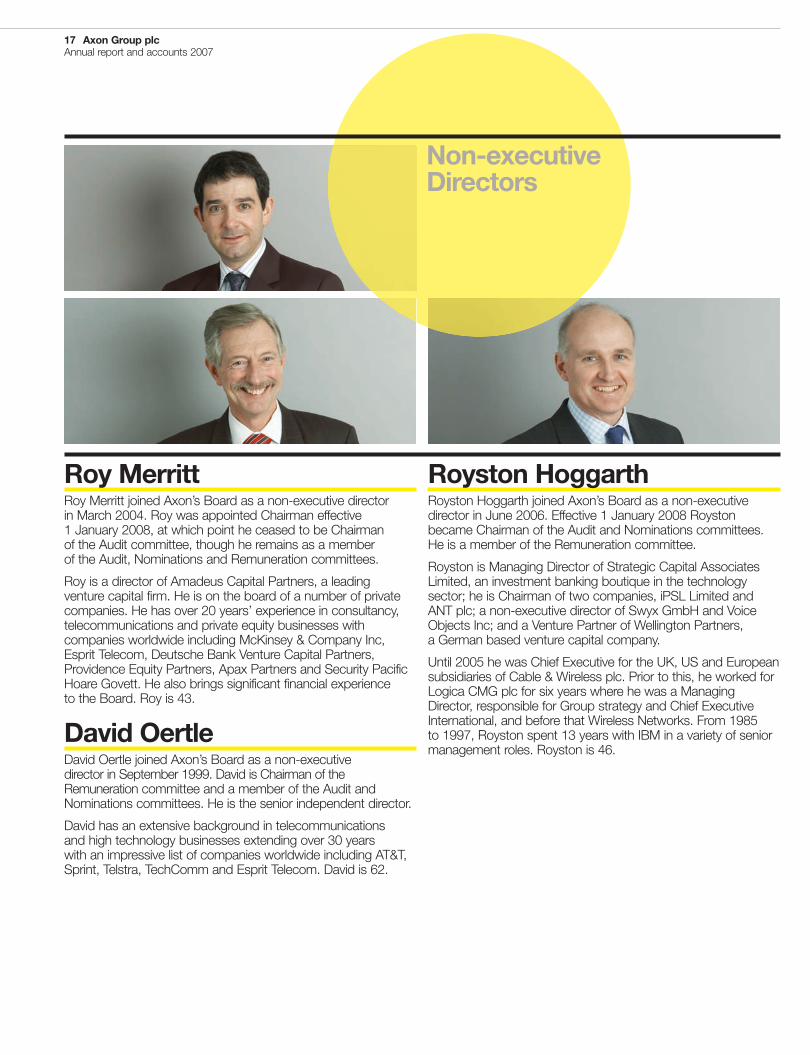

Roy MerrittRoy Merritt joined Axon’s Board as a non-executive directorin March 2004. Roy was appointed Chairman effective1 January 2008, at which point he ceased to be Chairmanof the Audit committee, though he remains as a memberof the Audit, Nominations and Remuneration committees.

Roy is a director of Amadeus Capital Partners, a leadingventure capital firm. He is on the board of a number of privatecompanies. He has over 20 years’ experience in consultancy,telecommunications and private equity businesses withcompanies worldwide including McKinsey & Company Inc,Esprit Telecom, Deutsche Bank Venture Capital Partners,Providence Equity Partners, Apax Partners and Security PacificHoare Govett. He also brings significant financial experienceto the Board. Roy is 43.

David OertleDavid Oertle joined Axon’s Board as a non-executivedirector in September 1999. David is Chairman of theRemuneration committee and a member of the Audit andNominations committees. He is the senior independent director.

David has an extensive background in telecommunicationsand high technology businesses extending over 30 yearswith an impressive list of companies worldwide including AT&T,Sprint, Telstra, TechComm and Esprit Telecom. David is 62.

Royston HoggarthRoyston Hoggarth joined Axon’s Board as a non-executivedirector in June 2006. Effective 1 January 2008 Roystonbecame Chairman of the Audit and Nominations committees.He is a member of the Remuneration committee.

Royston is Managing Director of Strategic Capital AssociatesLimited, an investment banking boutique in the technologysector; he is Chairman of two companies, iPSL Limited andANT plc; a non-executive director of Swyx GmbH and VoiceObjects Inc; and a Venture Partner of Wellington Partners,a German based venture capital company.

Until 2005 he was Chief Executive for the UK, US and Europeansubsidiaries of Cable & Wireless plc. Prior to this, he worked forLogica CMG plc for six years where he was a ManagingDirector, responsible for Group strategy and Chief ExecutiveInternational, and before that Wireless Networks. From 1985to 1997, Royston spent 13 years with IBM in a variety of seniormanagement roles. Royston is 46.

Non-executiveDirectors

18 Axon Group plcAnnual report and accounts 2007

Directors’ reportFor the year ended 31 December 2007

The directors present their annual report and the Group’s audited financial statements for the year ended 31 December 2007.

Revenue, results and dividend The financial results of the Group are shown in the income statement on page 31 and in the related notes.

Revenue from continuing operations was £204.5m (2006: £137.5m). Adjusted profit before taxation, excluding amortisation of intangibleassets on acquisition and share-based payments, from continuing operations was £35.5m (2006: £21.8m). Profit before taxation fromcontinuing operations was £29.5m (2006: £17.7m).

Profit for the year was £20.2m (2006: £11.3m). Diluted earnings per share was 31.7p (2006: 20.3p from continuing operations and 18.5p fromcontinuing and discontinued operations).

Net funds as at 31 December 2007 (being cash and cash equivalents, less borrowings) stood at £25.3m, compared to £6.2m as at31 December 2006.

The directors are recommending a final dividend of 2.5p per share, making 4.5p per share for the year (2006: 4.0p). If approved, thefinal dividend will be paid on 20 June 2008 to eligible shareholders on the Company’s Register of Members at the close of business on23 May 2008.

Principal activity and review of business The Group’s principal activity remains the provision of Business Transformation consultancyservices. The Group will continue to deepen its vertical industry penetration in the provision of these services in 2008. The operationaland financial activity of the Group is set out in more detail in the business and financial reviews on pages 11 to 15.

Branches In addition to other overseas subsidiaries, the Group operates a branch in Italy.

Board of directors and directors’ interests Details of the current directors who have served during the year are shown on pages 16 and17. Mark Hunter resigned from the Board effective 31 December 2007. In accordance with the Combined Code on Corporate Governance,which requires that all directors should be subject to re-election at intervals of no more than three years, David Oertle will be retiring andoffering himself for re-election at the forthcoming Annual General Meeting.

No director had any beneficial interest in the shares of any of the subsidiary undertakings of the Company at the balance sheet date.The beneficial interests of the directors in the shares of the Company are shown in the remuneration report on pages 25 to 29.

Interests in contracts No director had any material interest in any contract of significance to which the Company or any of its subsidiaryundertakings was a party during the financial year.

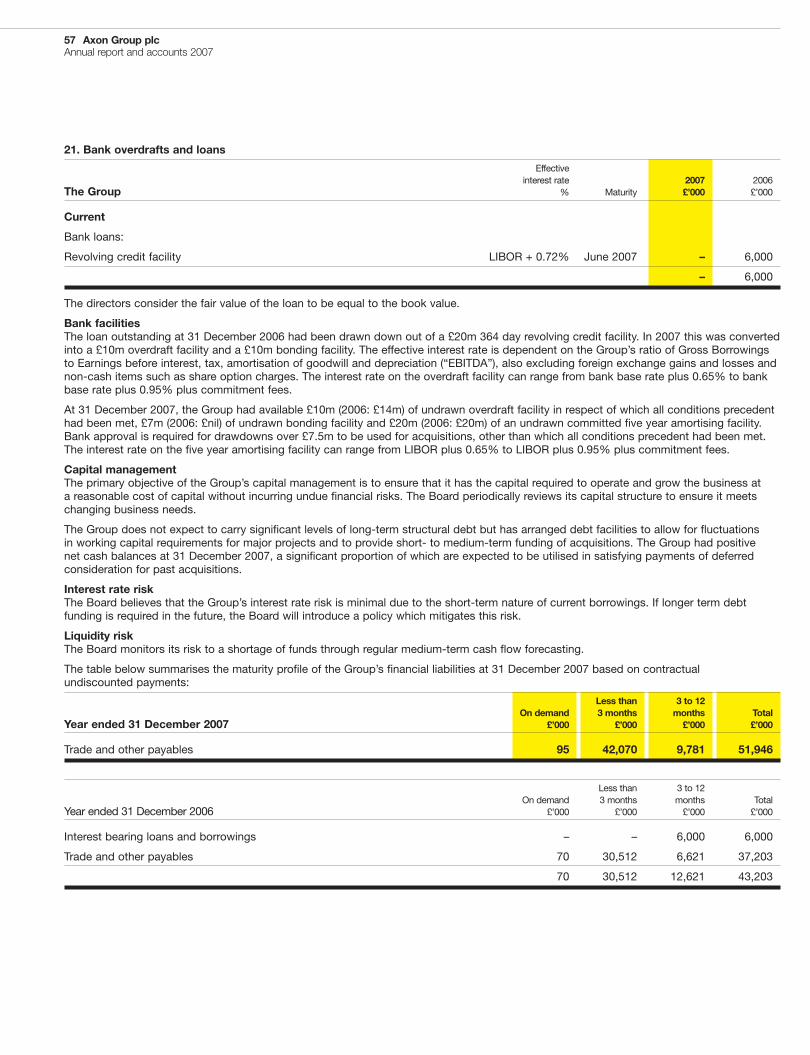

Financial risks The Board believes that the Group’s interest rate risk is minimal due to the short-term nature of current borrowings.If longer term debt funding is required in the future, the Board will introduce a policy which mitigates this risk.

The Group’s credit risk is primarily attributable to its trade receivables, as described in note 18.

Cash flow performance is monitored on an ongoing basis by the Board. Debt facilities have been established to fund future cash flowrequirements, as described in note 21.

For the most part, the Group’s exchange risk is naturally hedged with costs and revenues being incurred in the same currency. The mainexception to this is the provision of resources from Malaysia for clients in EMEA and North America, though Asia-Pacific intragroup revenuesrepresented less than 10% of Group revenues in the year.

Other risks and uncertainties Most of the Group’s revenues are undertaken under contracts which allow clients to terminate at shortnotice or allow clients to make rapid changes to the volume of work required. Loss of a major client at short notice could have a significantnegative impact on results.

Some contracts are undertaken under “fixed price” contracts whereby Axon is paid based on milestones related to the outputs delivered.In such cases there is a risk that more resources are required to achieve the milestones than was envisaged when the price was set.

In some cases clients require the provision of third party bonds to underwrite the Group’s contractual liabilities. Details of current bonds aredisclosed in note 27.

Short-term profitability is impacted significantly by the ability to secure sufficient work to ensure that consultants are highly chargeable andthat resource levels are managed to match demand.

Other important risks include not recruiting and retaining suitably skilled and experienced employees and incurring claims from clientsfor work for which they are not satisfied.

With Axon’s focus on SAP, a medium-term risk is that SAP fails to maintain a strong position in the market for software solutions for largecompanies.

Directors’ and officers’ liability insurance The Company maintains insurance cover for all directors and key personnel against liabilitieswhich may be incurred by them while carrying out their duties.

19 Axon Group plcAnnual report and accounts 2007

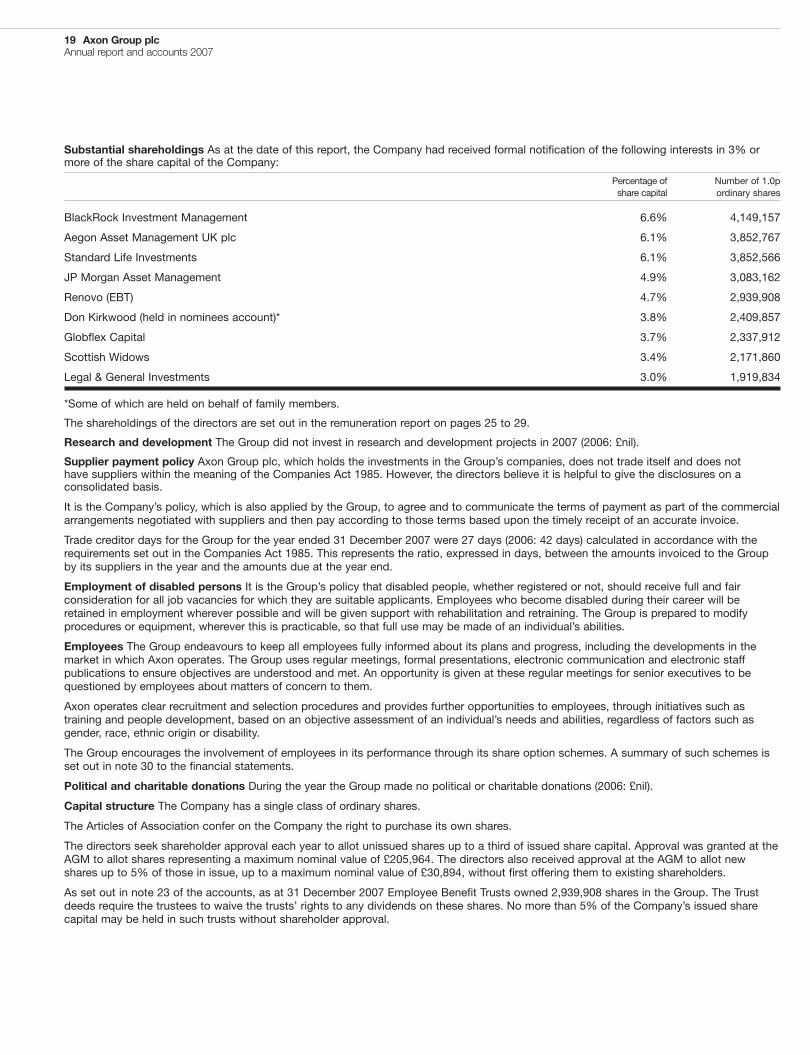

Substantial shareholdings As at the date of this report, the Company had received formal notification of the following interests in 3% ormore of the share capital of the Company:

Percentage of Number of 1.0pshare capital ordinary shares

BlackRock Investment Management 6.6% 4,149,157

Aegon Asset Management UK plc 6.1% 3,852,767

Standard Life Investments 6.1% 3,852,566

JP Morgan Asset Management 4.9% 3,083,162

Renovo (EBT) 4.7% 2,939,908

Don Kirkwood (held in nominees account)* 3.8% 2,409,857

Globflex Capital 3.7% 2,337,912

Scottish Widows 3.4% 2,171,860

Legal & General Investments 3.0% 1,919,834

*Some of which are held on behalf of family members.

The shareholdings of the directors are set out in the remuneration report on pages 25 to 29.

Research and development The Group did not invest in research and development projects in 2007 (2006: £nil).

Supplier payment policy Axon Group plc, which holds the investments in the Group’s companies, does not trade itself and does nothave suppliers within the meaning of the Companies Act 1985. However, the directors believe it is helpful to give the disclosures on aconsolidated basis.

It is the Company’s policy, which is also applied by the Group, to agree and to communicate the terms of payment as part of the commercialarrangements negotiated with suppliers and then pay according to those terms based upon the timely receipt of an accurate invoice.

Trade creditor days for the Group for the year ended 31 December 2007 were 27 days (2006: 42 days) calculated in accordance with therequirements set out in the Companies Act 1985. This represents the ratio, expressed in days, between the amounts invoiced to the Groupby its suppliers in the year and the amounts due at the year end.

Employment of disabled persons It is the Group’s policy that disabled people, whether registered or not, should receive full and fairconsideration for all job vacancies for which they are suitable applicants. Employees who become disabled during their career will beretained in employment wherever possible and will be given support with rehabilitation and retraining. The Group is prepared to modifyprocedures or equipment, wherever this is practicable, so that full use may be made of an individual’s abilities.

Employees The Group endeavours to keep all employees fully informed about its plans and progress, including the developments in themarket in which Axon operates. The Group uses regular meetings, formal presentations, electronic communication and electronic staffpublications to ensure objectives are understood and met. An opportunity is given at these regular meetings for senior executives to bequestioned by employees about matters of concern to them.

Axon operates clear recruitment and selection procedures and provides further opportunities to employees, through initiatives such astraining and people development, based on an objective assessment of an individual’s needs and abilities, regardless of factors such asgender, race, ethnic origin or disability.

The Group encourages the involvement of employees in its performance through its share option schemes. A summary of such schemes isset out in note 30 to the financial statements.

Political and charitable donations During the year the Group made no political or charitable donations (2006: £nil).

Capital structure The Company has a single class of ordinary shares.

The Articles of Association confer on the Company the right to purchase its own shares.

The directors seek shareholder approval each year to allot unissued shares up to a third of issued share capital. Approval was granted at theAGM to allot shares representing a maximum nominal value of £205,964. The directors also received approval at the AGM to allot newshares up to 5% of those in issue, up to a maximum nominal value of £30,894, without first offering them to existing shareholders.

As set out in note 23 of the accounts, as at 31 December 2007 Employee Benefit Trusts owned 2,939,908 shares in the Group. The Trustdeeds require the trustees to waive the trusts’ rights to any dividends on these shares. No more than 5% of the Company’s issued sharecapital may be held in such trusts without shareholder approval.

20 Axon Group plcAnnual report and accounts 2007

Directors’ report (continued)

Change of control provisions Significant agreements which include change of control provisions that would come into effect in the eventof a takeover of Axon Group include contracts with BP, Birmingham City Council, Transport for London and TXU Energy. In these cases theclients have the right to terminate the contracts within defined periods from the date of notification ranging from 45 days to 12 months.The financial consequences of such termination would depend on the number of consultants working on any such contract at thepoint of termination and whether there were other clients to which they could be deployed at the end of any notice period.

Under provisions of the share purchase agreement relating to the acquisition of Zytalis Inc, earn-out payments are calculated based onthe financial performance of the business acquired. If a change of control occurs prior to 31 December 2009 which has a material adverseimpact on the business, then the earn-out payments will be deemed to be set at the earn-out caps. The maximum value of earn-outpayments that would be subject to these provisions is US $10.4m.

Directors’ responsibilities The directors are responsible for preparing the Annual Report and Group financial statements in accordance withapplicable United Kingdom law and those International Financial Reporting Standards (IFRSs) as adopted by the European Union.

The directors are required to prepare the financial statements for each financial year which present fairly the financial position of the Groupand the Company and the financial performance and cash flows of the Group and the Company for that period. In preparing those Groupfinancial statements the directors are required to:

• select suitable accounting policies in accordance with IAS 8: Accounting Policies and Changes in Accounting Estimates and Errors andthen apply them consistently;

• present information including accounting policies, in a manner that provides relevant, reliable, comparable and understandable information;

• provide additional disclosures when compliance with the specific requirements in IFRSs is insufficient to enable users to understand theimpact of particular transactions, other events and conditions on the Group’s financial position and financial performance; and

• state that the Group and Company has complied with IFRSs, subject to any material departure disclosed and explained in thefinancial statements.

The directors are responsible for keeping proper accounting records which disclose with reasonable accuracy at any time the financialposition of the Group and the Company and enable them to ensure that the Group and the Company financial statements comply withthe Companies Act 1985 and Article 4 of the IAS Regulation. They are also responsible for safeguarding the assets of the Group and theCompany and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Directors’ statement The directors confirm that the accounts on pages 31 to 69 show a true and fair view.

The directors who were members of the Board at the time of approving the directors’ report are listed on pages 16 and 17. Having madeenquiries of fellow directors and of the Company’s auditors, each of the directors confirms that:

• to the best of each of the directors’ knowledge and belief, there is no information relevant to the preparation of their report of which theCompany’s auditors are unaware; and

• each director has taken all the steps a director might reasonably be expected to have taken to be aware of the relevant audit informationand to establish that the Company’s auditors are aware of that information.

Annual General Meeting The 2008 Annual General Meeting of the Company is to be held on Friday, 25 April 2008. The business to beconsidered at the Meeting is set out in the accompanying Notice of Meeting and explanatory notes.

Auditors A resolution for the reappointment of Ernst & Young LLP will be proposed at the forthcoming Annual General Meeting.

By order of the Board

Stephen CardellChief Executive Officer

4 March 2008

21 Axon Group plcAnnual report and accounts 2007

Report on corporate governance

The Combined Code on Corporate Governance The Board fully acknowledges that it has overall responsibility for ensuring the effectivenessand regular review of the Group’s internal control systems, as detailed below. In accordance with the Listing Rules of the UK Listing Authority, thisstatement, together with the remuneration report, set out on pages 25 to 29, explains how Axon has applied The Principles of Good Governanceset out by the Financial Services Authority in Section 1 of The Combined Code on Corporate Governance July 2006 (the “Combined Code”) andreports on the Group’s compliance with the provisions contained in the Code of Best Practice throughout the period under review.

Compliance with the Combined Code The Board is committed to high standards of corporate governance. The Board has complied withthe provisions of the Combined Code throughout the accounting period and to the date of this report, with the following exceptions:

A.2.1 & A.2.2 Mark Hunter took on the role of Chairman and Chief Executive in May 2003. From 6 March 2007, these two roles wereseparated with Stephen Cardell appointed as CEO and Mark Hunter remaining as Executive Chairman. From 1 January 2008, Roy Merrittbecame non-executive Chairman and Mark Hunter left the Board so the Board should be fully compliant in this respect for 2008.

B.2.3 The non-executive directors were present at the meeting to approve the remuneration of the non-executives. The Board will seek toavoid this situation being repeated in future.

For 2008, under C.3.1 Roy Merritt ceased to be Chairman of the Audit committee when be became non-executive Chairman effective 1 January2008. Neither of the other two Audit committee members has recent and relevant financial experience. The Combined Code recommends that theChairman not be a member of the Audit committee. Given that Roy Merritt was an independent director when he joined the Board and that hehas recent relevant financial experience, the Board believes that he should remain an Audit committee member.

The Board of directors The Board of directors comprises a non-executive Chairman, a Chief Executive Officer, a Chief Financial Officer andtwo independent non-executive directors. The profiles of the current directors are set out on pages 16 and 17. The Articles allow there to benot more than eight and not less than two directors.

The non-executive directors contribute a wide range of skills and experience, forming a strong and independent element within the Board.The non-executive directors receive a fixed fee for services rendered, have served for less than nine years and have not been employees ofthe Group at any time. Their opinions carry significant weight in the decision making process, both operational and financial, and they arefree from any business or personal relationships that could interfere with their independent judgement. The non-executive directors ensurethat some meetings are set aside during the year without the executive directors present.

David Oertle is the nominated senior independent non-executive director to whom concerns may be conveyed.

The Board meets at regular intervals throughout the year (eight times in 2007 (2006: eight)) and has reserved for its consideration mattersincluding:

• the responsibility for the overall strategy of the Group;

• acquisitions and divestments;

• significant capital expenditure projects and any major financial proposals;

• assessment of exposure to key business risks;

• environmental issues;

• health and safety; and

• employee matters (including codes of conduct) and key senior appointments.

Appropriate detailed monthly information, both operational and financial, is provided to the Board in a timely manner to enable it todischarge its duties. The Board ensures that all directors receive appropriate training and induction, as required, and that they are ableto take independent professional advice in the furtherance of their duties.

The Board may appoint a director and revoke or terminate the appointment of a director as it thinks fit. Any director so appointed shalloffer himself for reappointment at the first AGM following appointment. All directors submit themselves for re-election at least once everythree years. The shareholders may also remove a director by ordinary resolution.

Financial reporting and KPIs Management reporting packs are prepared monthly both for each regional Board for EMEA, North Americaand Asia-Pacific as well as for the Group main Board. These include information on the historic, budgeted and forecast financialperformance of the business as well as operational data such as utilisation and chargeability.

A budget is agreed by the Board annually and performance against budget is reported monthly.

Management at regional, business unit, indirect department and project levels have on-line access to financial information for their area ofresponsibility derived from the Group’s global SAP systems.

Key performance indicators include revenue growth, gross margins, adjusted operating profit margins and chargeability of consultants.KPI data has been provided in the business and financial reviews.

Chargeability is calculated based on the percentage of time charged to client projects as a proportion of the total non-weekend daysavailable for a period. Adjusted operating profit excludes any costs related to share-based payments and amortisation of intangible assetscreated on acquisitions.

Report on corporate governance (continued)

22 Axon Group plcAnnual report and accounts 2007

Board committees The Company has formally established Audit, Remuneration and Nominations committees. The current membershipof the committees is shown on pages 16 and 17. The terms of reference for each of these committees are publicly available at the Group’sregistered office.

The Audit committee comprises the three non-executive directors and is chaired by Royston Hoggarth with effect from 1 January 2008.Prior to that date it was chaired by Roy Merritt. See the separate audit committee report on page 24 for further details.

The Remuneration committee is chaired by David Oertle and comprises the non-executive directors, including the non-executiveChairman, who was considered to be independent on appointment. The committee meets when necessary during the year to:

• review Remuneration policy and to determine the remuneration packages of the executive directors and key senior management; and

• approve proposals for the granting of share options to employees of the Group.

The minutes of the Remuneration committee are circulated to, and reviewed by, the Board. The remuneration report is set out onpages 25 to 29.

The Nominations committee is chaired by Royston Hoggarth and comprises the three non-executive directors. The committee meetswhen necessary during the year to formally review the performance of the Board as well as the balance of skills. A formal evaluation of theperformance of the Board was introduced in 2005 and is updated annually. The performance evaluation is an internal process where eachdirector completes a detailed questionnaire ranking performance. The process covers the effectiveness and constitution of each of thecommittees and the directors, the performance of the Chairman, the objectives, strategy, internal and external relationships, managementinformation and governance. The committee reviews actions from this review. Two new appointments to the Board have been made sinceits establishment.

Use of external recruitment consultants and advertising are considered on a case by case basis. In the case of the appointment of RoyMerritt as Chairman, no external search firm was involved. Roy was already well known to the Board through his role as Audit committeeChairman and non-executive director.

The Business Unit Board is chaired by the CEO, and comprises the CFO and four senior managers. The committee meets monthly toconsider financial performance, review of budgets and forecasts, capital expenditure proposals and any management issues. Significantmatters arising from such meetings are reported to the Board and senior managers are invited to present at Board meetings on financial andoperating performance, new initiatives, business and employee development and planning matters, as appropriate.

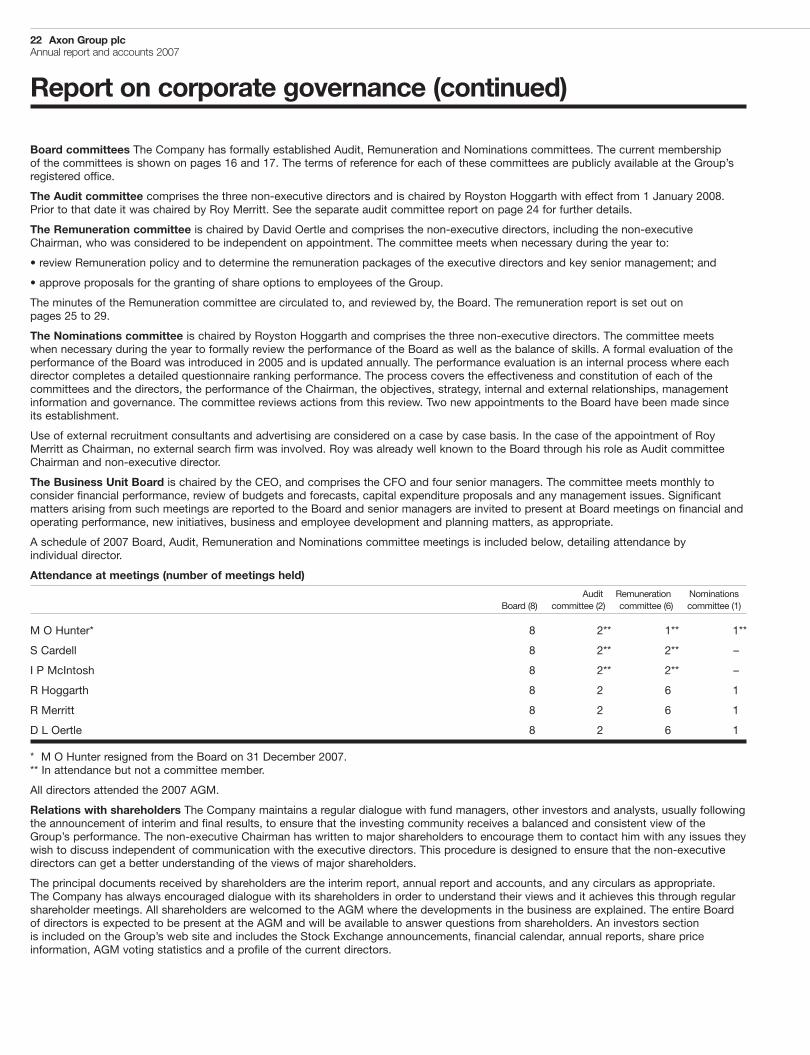

A schedule of 2007 Board, Audit, Remuneration and Nominations committee meetings is included below, detailing attendance byindividual director.

Attendance at meetings (number of meetings held)

Audit Remuneration NominationsBoard (8) committee (2) committee (6) committee (1)

M O Hunter* 8 2** 1** 1**

S Cardell 8 2** 2** –

I P McIntosh 8 2** 2** –

R Hoggarth 8 2 6 1

R Merritt 8 2 6 1

D L Oertle 8 2 6 1

* M O Hunter resigned from the Board on 31 December 2007.** In attendance but not a committee member.

All directors attended the 2007 AGM.

Relations with shareholders The Company maintains a regular dialogue with fund managers, other investors and analysts, usually followingthe announcement of interim and final results, to ensure that the investing community receives a balanced and consistent view of theGroup’s performance. The non-executive Chairman has written to major shareholders to encourage them to contact him with any issues theywish to discuss independent of communication with the executive directors. This procedure is designed to ensure that the non-executivedirectors can get a better understanding of the views of major shareholders.

The principal documents received by shareholders are the interim report, annual report and accounts, and any circulars as appropriate.The Company has always encouraged dialogue with its shareholders in order to understand their views and it achieves this through regularshareholder meetings. All shareholders are welcomed to the AGM where the developments in the business are explained. The entire Boardof directors is expected to be present at the AGM and will be available to answer questions from shareholders. An investors sectionis included on the Group’s web site and includes the Stock Exchange announcements, financial calendar, annual reports, share priceinformation, AGM voting statistics and a profile of the current directors.

23 Axon Group plcAnnual report and accounts 2007

Going concern After making enquiries, the directors have formed a judgement, at the time of approving the financial statements, that thereis a reasonable expectation that the Group and Company have adequate resources to continue in operational existence for the foreseeablefuture. For this reason the directors continue to adopt the going concern basis in preparing the financial statements.

Environmental, Social and Governance (“ESG”) matters The Board recognises the obligations that the Group has towards those withwhom it has dealings, the environment and the responsibility for ethical conduct and that such factors are increasingly relevant to financialperformance in the longer term. The Board regularly reviews the significance of social, environmental and ethical matters to the business ofthe Group and the Company. Roy Merritt is the main Board member responsible for ESG issues. The Board does not consider there to bemajor risk issues facing the business from an ESG perspective in the short-term.

Social matters Axon is a socially responsible employer and various initiatives are in place to ensure that staff are treated fairly as they arecritical to its business success. The Group is also committed to protecting and enhancing the health and safety of its employees.

Communication is critical to employee relations and the Group uses quarterly staff forums and monthly electronic newsletters toensure all employees are fully informed about its plans and progress, including the developments in the market in which Axonoperates. Quarterly offsite meetings are held for senior management and directors to review strategy implementation and keybusiness opportunities. An electronic forum is also available to employees who wish to ask directors anonymous questions.

Annual performance reviews are conducted for employees and individual training and development needs are identified to ensure staffreceive supplementary training.

The Group encourages the involvement of employees in its performance through its share option schemes. A summary of such schemesis set out in note 30 to the financial statements.

During 2004 the Group introduced a flexible benefits scheme in the UK which allows eligible employees the ability to exercise choice overcertain elements of their reward package.

It is the Group’s policy that disabled people, whether registered or not, should receive full and fair consideration for all job vacancies forwhich they are suitable applicants. Employees who become disabled during their career will be retained in employment wherever possibleand will be given support with rehabilitation and retraining. The Group is prepared to modify procedures or equipment, wherever this ispracticable, so that full use may be made of an individual’s abilities.

Environmental matters Being primarily office based, and given the nature of our business, Axon does not have a material impact on theenvironment. However, the Group and its employees try to ensure that both services and products are procured in an environmentallyfriendly manner and that waste materials are disposed of appropriately, including recycling where economically possible. The Group hasexpanded the types of recycling that it undertakes to ensure that the amount of office waste is minimised.

The Group makes extensive use of electronic communications to reduce the amount of printing waste produced. This is supported bythe use of a centralised workflow and project management tool which both clients and employees have access to. Energy consumptionis also minimised with boilers and chillers switched off at times when staff are not in the building.

Where appropriate, electronic communication methods such as email, telephone and video conference facilities are used to avoidnon-essential travel.

The Group does not offer a company car scheme to employees and encourages its employees to travel to work using public transport.

ISO 14001 is the international standard for Environmental Management Systems. I am pleased to announce that the UK operationssuccessfully secured third party certification from SGS Group, the world’s leading inspection, verification, testing and certification company,of compliance with this standard in December 2007.

Ethical conduct The Board is committed to uphold ethical conduct throughout the Group and has in place a confidential whistle blowingpolicy to give the opportunity for any staff to report matters directly to Roy Merritt.

Health and safety Axon operates a formal Health and Safety policy, which is regularly monitored and reviewed by the Board. Under thepolicy significant incidents are reported without delay to the Board. No such incidents occurred in 2007.

Royston HoggarthChairman, Audit committee

4 March 2008

24 Axon Group plcAnnual report and accounts 2007

Audit committee reportFor the year ended 31 December 2007

The Audit committee comprises the two independent non-executive directors and the non-executive Chairman and is chaired by RoystonHoggarth. The executive directors may attend meetings of the committee by invitation and the committee meets with the external auditorswithout the executive directors or managers present. The Audit committee meets at least twice during the year and has formal agendaswhich cover all areas of responsibilities. Its terms of reference are:

• to monitor the effectiveness of the Group’s internal controls;

• to review the scope of the external audit; and

• to review the interim and annual financial statements, focusing particular attention on accounting policies and financial reportingcompliance.

It meets with the external auditors to review their plan for the audit, to discuss any matters arising from their audit visits and any reports thatthey may produce. In addition, the auditors have direct access to the committee should they need to raise any concerns. The committeealso reviews the level and type of services provided to the Group by the auditors, monitors their independence and objectivity as well as thescope and results of the audit. The Chairman of the Audit committee reports to the Board on the progress of the committee meetings andminutes are circulated to and reviewed by the Board.

The Audit committee receives reports twice a year from the external auditors on key matters which affect the interim and full year financialstatements. It reviews the process for monitoring the Group’s effectiveness of internal controls at least every six months. The Auditcommittee has again considered the need for a separate internal audit function and has decided that, due to the Company’s size, one isnot required at present, but will continue to review the requirement annually.

The Board regularly assesses the independence of its external auditors, Ernst & Young LLP, by reviewing the type of non-audit workundertaken. Having considered the services provided by its auditors, Ernst & Young LLP, the Board believe that they have maintainedan appropriate level of independence during 2007. The independence of Ernst & Young LLP will continue to be monitored regularly.

Internal control The Board is responsible for the effectiveness of the Group’s system of internal controls and has established a continuousprocess for identifying, evaluating and managing significant risks faced by the Group. Key business risks are reviewed monthly by theBoard, with formal reviews of the full internal control environment performed annually. Risks facing the Group can be categorised into fivecategories: business risks, operational risks, accounting and compliance risks, technology risks and risks associated with mergers andacquisitions. Where areas of improvement are brought to the committee’s attention, steps are taken to embed internal control and riskmanagement into the operations of the business. The Board regularly reviews the process, which has been in place throughout the year andup to the date of approval of this report, and which is in accordance with Internal Control: Guidance for Directors on the Combined Code,published in July 2006. Such systems of internal control are designed to manage rather than eliminate the risks of failure to meet businessobjectives, providing a reasonable but not an absolute assurance against material loss or misstatement.

Group objectives are captured in regular reviews of corporate strategy carried out by the executive directors with the involvement ofkey senior managers and reported to the Board. The reviews of corporate strategy form the basis for the establishment of the businessobjectives of the Group, which, in turn, are reflected fully in the business strategies, and financial objectives of the senior managers andtheir teams.

Key policies, processes and control procedures are communicated throughout the Group. Non-compliance is reviewed and any areas ofweakness identified are addressed and promptly reported to the Board. Continuing actions are taken throughout the year to embed riskmanagement and internal control into the day-to-day operations of the Group.

It is Axon’s policy continually to strengthen the effectiveness of the system of internal controls by recruiting, developing and managingemployees of the highest calibre and matching their skills to the appropriate disciplines. A Chief Financial Officer joined the Group andwas appointed to the Board in November 2006.

In relation to potential acquisitions, external advisers, together with senior management within the Group, are appointed under clearlydefined scopes to carry out commercial, financial and legal due diligence. The Board is kept fully up to date with any issues arising duringsuch due diligence.

Royston HoggarthChairman, Audit committee

4 March 2008

25 Axon Group plcAnnual report and accounts 2007

Remuneration reportFor the year ended 31 December 2007

Unaudited information This report has been prepared in accordance with the Directors’ Remuneration Report Regulations 2002. The reportalso meets the relevant requirements of the Listing Rules of the Financial Services Authority and describes how the Board has applied thePrinciples of Good Governance relating to directors’ remuneration. As required by the Regulations, a resolution to approve the report will beproposed at the Annual General Meeting of the Company to which the financial statements will be presented.

Remuneration committee’s objectives The terms of reference of the Remuneration committee are:

• to agree a set of policies within which each executive director’s and senior manager’s remuneration package is agreed; and

• to assist the Board in wider aspects of remuneration policy, such as the granting of share-based incentives.

The Remuneration committee is also responsible for setting the Company Chairman’s pay and conditions (with the Chairman absent fromsuch discussions).

Remuneration policy From the establishment of Axon, the Group’s policy has been to attract, retain and motivate the best people for eacharea of the business and to align their objectives to Group performance in order to deliver and grow value to shareholders.

The Remuneration committee objectively compares the remuneration packages of an executive with that of a similar executive in the sameindustry sector and to those in other appropriate companies based on size, complexity of industry and geographical mix. Historically, theRemuneration committee has not commissioned reports specific to Axon from independent consultants but has instead reviewedindependent market research including trends in competitors and other appropriate companies’ remuneration policies. However, since theyear end, the Remuneration committee has appointed New Bridge Street Consultants LLP to advise on the remuneration policy and toundertake a review and report to the Committee on senior executive remuneration during 2008, with particular reference to the structure offuture equity incentives. The Group will engage with major shareholders and the principal shareholder representative bodies as appropriate.No executive director plays a part in the discussion of his or her own remuneration.

In setting remuneration packages for executive directors, the Remuneration committee considers how these compare with remuneration foremployees more generally. There are no pension arrangements or equity schemes in place that are designed only for executive directors.

The Remuneration committee has discretion to consider corporate performance on environmental, social and governance (“ESG”) issueswhen setting the remuneration of executive directors. The committee does not believe that ESG risks are inadvertently raised by theincentive structures currently in place.

Executive directors The Remuneration packages of executives will continue to comprise an annual base salary, cash bonus andparticipation in long-term incentive schemes. No other annual employment-related benefits are provided since the Remuneration committeebelieves that the emphasis should be on reward for Company performance. Overall performance targets relating to the cash bonus planand to the executive share option schemes are, in the opinion of the Remuneration committee, challenging. Bonuses based on Groupperformance targets form a substantial proportion (up to 60%) of total remuneration calculated on overall performance targets. The rewardsearned by the executive directors in 2007 have reflected the results of the Group.

Base salary The base salary of executive directors will be determined by the Remuneration committee at the start of each year havingregard to personal and Group performance, competitive market practice and pay levels more broadly within the Group.

Historically, Mark Hunter and Stephen Cardell have received significantly lower base salaries than similar executives in comparablecompanies. After a review of comparable companies in December 2007, the committee has decided the remuneration of the Chief ExecutiveOfficer should move towards mid-market levels.

For 2008, base salaries for Stephen Cardell and Iain McIntosh were increased to £350,000 and £195,000 respectively. The Remunerationcommittee believes these salary levels are now in line with survey data for larger UK FTSE Small Cap companies allowing for the absence ofbenefits and pension provision within these executives’ packages.

The Company reimburses the amount by which Stephen Cardell is impacted by incremental US taxes payable on his remuneration over andabove those payable in the UK.

Cash bonus The Remuneration committee sets the objectives that must be met if a cash bonus is to be paid. Cash bonuses for executivedirectors are based entirely on the financial performance of the Group and the Remuneration committee agrees a cap. For 2008 the caps areset up to a maximum of 100% and 80% of base salary for the Chief Executive Officer and Chief Financial Officer respectively, which theRemuneration committee believes to be in line with comparable sized UK listed companies.

The financial performance measure for executive directors in 2007 was year-on-year growth in revenue and adjusted profit before tax(“PBT”). These measures have been chosen as the best measures of short-term operational financial performance. Maximum bonuses arepayable in respect of 2007 as significant year-on-year revenue and adjusted PBT growth in excess of targets was achieved. Revenue andadjusted PBT growth year-on-year have been selected by the Remuneration committee as the appropriate performance measures for 2008for executive directors. The Group does not publish a profit forecast for 2008 and bonus targets cannot be disclosed prior to 31 December2008 due to commercial sensitivity. Consistent with previous financial years, the Remuneration committee has set significant year-on-yeargrowth targets which will have to be achieved for cash bonuses to be payable. Any bonuses paid by the Group are non-pensionable.

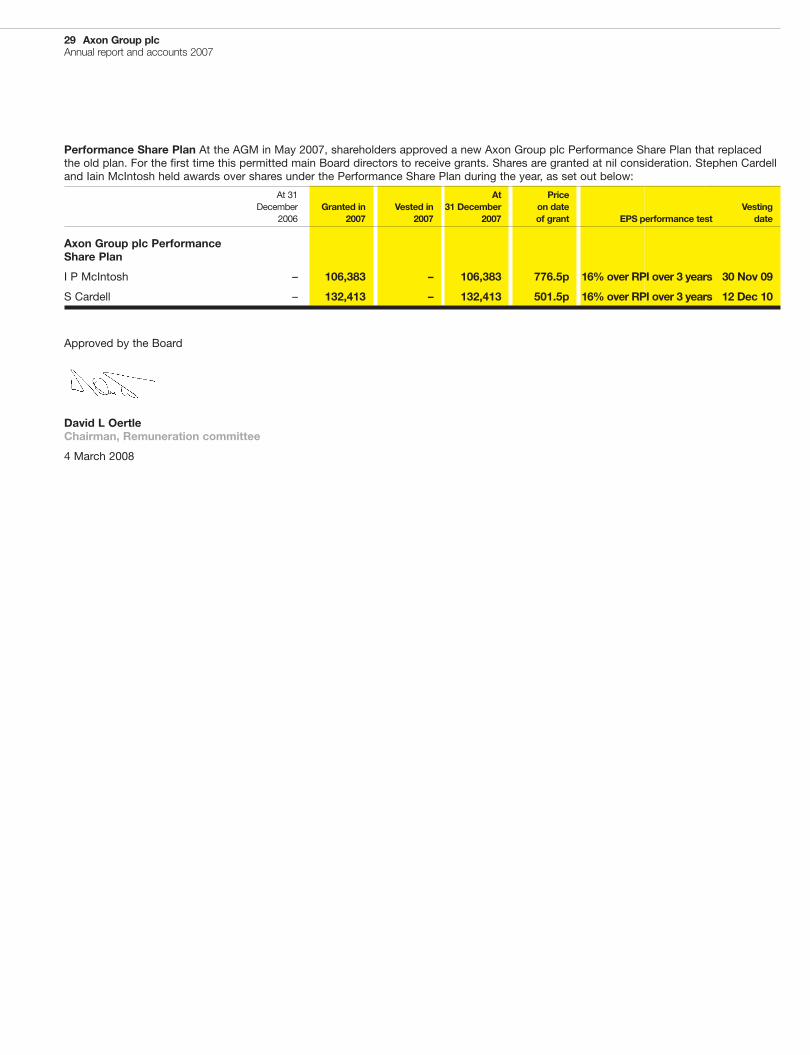

Long-term incentives The Company operates the Axon Group plc Performance Share Plan as the principal long-term incentivearrangement for executive directors, under which conditional awards are granted.

Awards granted in 2007 will vest subject to the achievement of real growth in earnings per share of 16% over a three year performanceperiod. There is no provision for retesting of this performance condition. At the time of award, the Remuneration committee believed that thetarget was sufficiently challenging in the prevailing market conditions and when compared to other companies in the Company’s sector andthat a single target was appropriate to encourage executives to exceed this level of performance.

Remuneration report (continued)

26 Axon Group plcAnnual report and accounts 2007

The operation of the Performance Share Plan will be reviewed by the Committee during the year with the assistance of its independentadvisers.

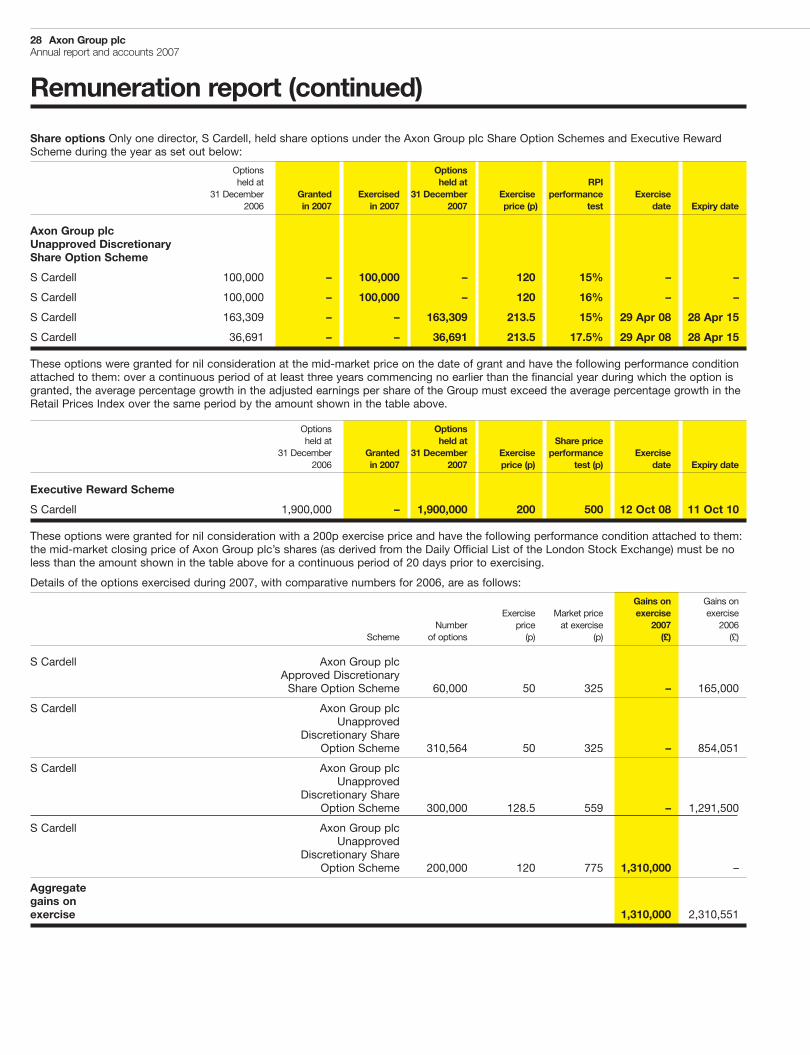

The details of the directors’ holdings are listed on pages 28 and 29 of this report. Full details of the other long-term incentive schemesoperated by the Company (in a number of which executive directors have participated in past years), including the performance conditions,are set out in note 30 to the financial statements

Pensions The Group does not contribute to any pension schemes on behalf of executive directors except for payments to the UK GroupPersonal Pension Plan made under a defined contribution salary sacrifice scheme whereby employees may elect to forgo part of their basicpay in return for pension payments made by the Group. This provides for the employee to receive the benefit of any reduction to theCompany’s National Insurance liability as a result of electing to make a pension payment. Iain McIntosh was a member of the plan in 2006and 2007 on the same basis as that available to other UK employees.

External directorships The Remuneration committee has discretion to approve whether an executive director may accept externalappointments. Stephen Cardell holds one non-executive directorship, for which he receives no remuneration, which was approved by theRemuneration committee on 23 February 2005. No other executive director currently holds any non-executive directorships.

Chairman and non-executive directors The Board determines the remuneration of non-executive directors. Their remuneration is notpensionable and they are not eligible for performance-related remuneration by way of a cash bonus or participation in any share optionscheme. Remuneration for the non-executive directors excluding the Chairman has been set at £35,000 effective 1 January 2008, with anadditional £5,000 for acting as Chairman of either the Audit or Remuneration committees. These fee levels have been set to reflect the timecommitment and responsibility of each role and are considered to be in line with levels at comparable UK listed companies.

Reflecting his appointment as non-executive Chairman from 1 January 2008, Roy Merritt’s remuneration was increased to £75,000 per annumby the Remuneration committee.

Service contracts Set out below are details of the contractual arrangements in respect of current directors of the Company:

CompensationDate of contract Notice period payable*

S Cardell 6 March 2007 12 Months Nil

D L Oertle 28 April 2000 3 Months Nil

R Merritt 1 January 2008 3 Months Nil

R Hoggarth 3 June 2006 3 Months Nil

I P McIntosh 6 November 2007 12 Months Nil

*There are no specific provisions in any of the service contracts for compensation to be paid in the event of early termination.

Directors’ contracts do not contain specific end dates, but are subject to the notice periods set out above. Contracts are available forinspection at the Group’s registered office.

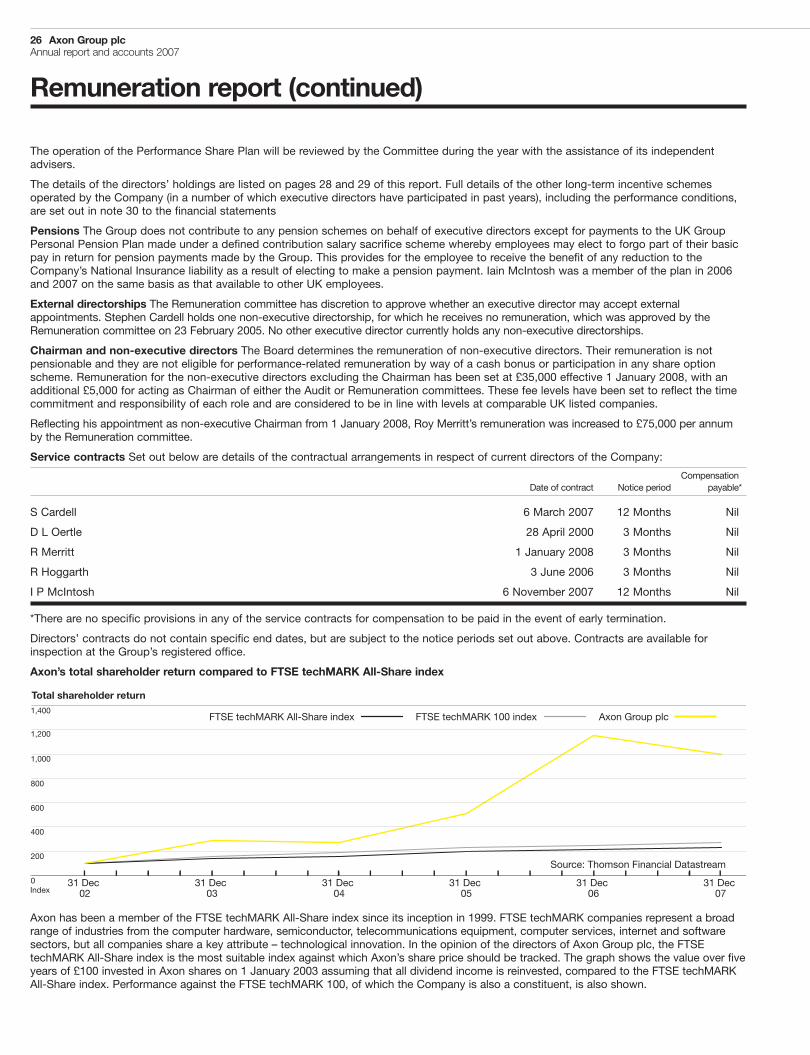

Axon’s total shareholder return compared to FTSE techMARK All-Share index

Axon has been a member of the FTSE techMARK All-Share index since its inception in 1999. FTSE techMARK companies represent a broadrange of industries from the computer hardware, semiconductor, telecommunications equipment, computer services, internet and softwaresectors, but all companies share a key attribute – technological innovation. In the opinion of the directors of Axon Group plc, the FTSEtechMARK All-Share index is the most suitable index against which Axon’s share price should be tracked. The graph shows the value over fiveyears of £100 invested in Axon shares on 1 January 2003 assuming that all dividend income is reinvested, compared to the FTSE techMARKAll-Share index. Performance against the FTSE techMARK 100, of which the Company is also a constituent, is also shown.

1,400

1,200

1,000

800

600

400

200

0

Total shareholder return

31 Dec02

31 Dec03

31 Dec04

31 Dec05

31 Dec 07

31 Dec 06

FTSE techMARK 100 indexFTSE techMARK All-Share index Axon Group plc

Source: Thomson Financial Datastream

Index

27 Axon Group plcAnnual report and accounts 2007

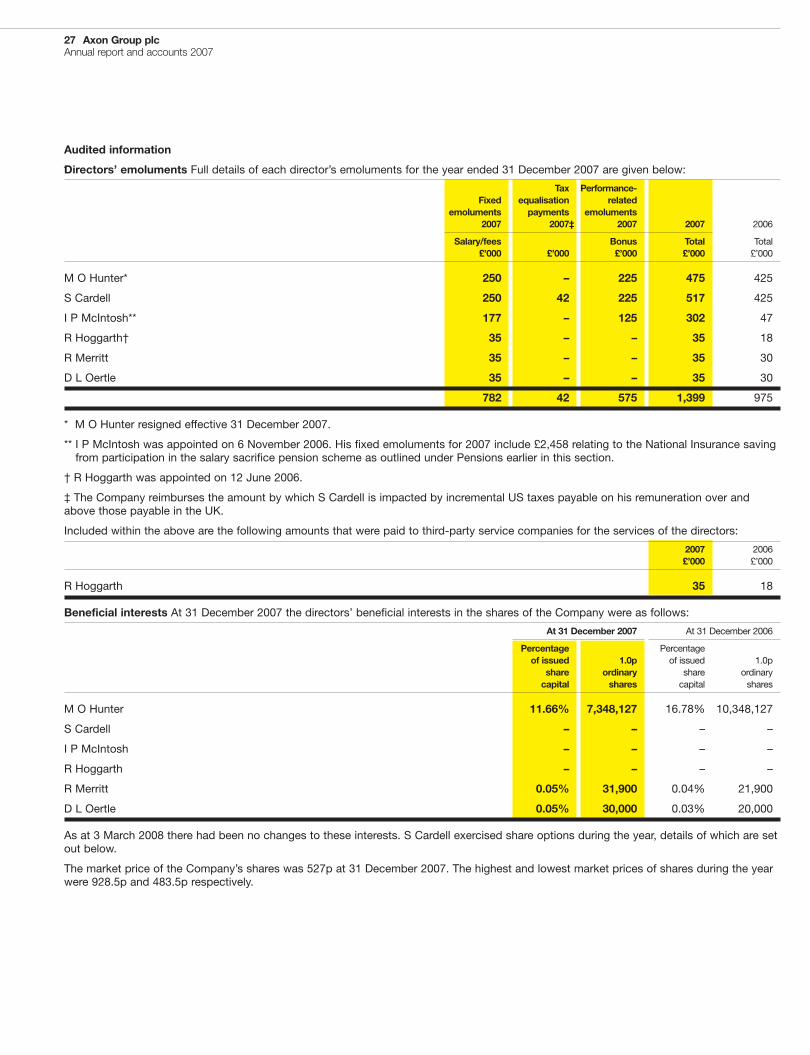

Audited information

Directors’ emoluments Full details of each director’s emoluments for the year ended 31 December 2007 are given below:ˆ

Tax Performance-Fixed equalisation related

emoluments payments emoluments2007 2007‡ 2007 2007 2006

Salary/fees Bonus Total Total£’000 £’000 £’000 £’000 £’000

M O Hunter* 250 – 225 475 425

S Cardell 250 42 225 517 425

I P McIntosh** 177 – 125 302 47

R Hoggarth† 35 – – 35 18

R Merritt 35 – – 35 30

D L Oertle 35 – – 35 30

782 42 575 1,399 975

* M O Hunter resigned effective 31 December 2007.

** I P McIntosh was appointed on 6 November 2006. His fixed emoluments for 2007 include £2,458 relating to the National Insurance savingfrom participation in the salary sacrifice pension scheme as outlined under Pensions earlier in this section.

† R Hoggarth was appointed on 12 June 2006.