Embed Size (px)

Citation preview

Estd. 1941

BUILDERS ’ ASSOCIATION OF INDIA (All-India Association of Engineering Construction Contractors)

G-1/G-20, 7th Floor, Commerce Centre, J. Dadajee Road, Tardeo, Mumbai – 400034 Tel: (91-22) 23514134 , 23520507, 23514802 Fax: 23521328 ▲Grams BUILDASIND Web Site : www.baionline.in E-mail : [email protected] / [email protected]

Ref: 246/J/2009-10 dated July 20, 2009

MEMBERS OF THE MANAGING COMMITTEE OF BAI NOTICE

The Second Meeting of the Managing Committee of Builders’ Association of India for the year 2009-10 will be held on Saturday, the 8th August 2009 at 10.00 a.m. at Hotel Clarks Shiraz, Taj Road, Agra (Tel: 0562-2226128 - 32), to transact the following business:-

AGENDA 1. To confirm the Minutes of the last Managing Committee Meeting held on 2nd May 2009 at Chennai.

(Minutes already circulated).

2. To grant Leave of Absence.

3. Issues arising out of previous Meeting (Action taken Report enclosed).

4. To ratify decision of the Office Bearers of the Headquarter in postponing the BAI Trustees election for the term 2009-14. (Letter dated 18th June 2009, issued by Office Bearers enclosed).

5. To discuss constitutional amendment proposed by the Constitutional Amendment Committee. (Proposed Amendments enclosed).

6. To discuss and review the latest position of –

i. Abnormal increase in Cement Price vis-à-vis Competition Commission.

ii. Goods & Service Tax Act . (Write-up enclosed).

iii. Budget 2009 vis–a-vis Construction Industry. (Note enclosed).

7. To note letter dated 17th June 2009 received from Construction Industry Development Council (CIDC) on 2nd Vishwakarma Awards and decide BAI’s action plan. (Letter enclosed).

8. To consider applications received from Centres’ for holding “XXIV All India Builders’ Convention”.

9. To select theme for Builders’ Day 2009.

10. To take note of BAI’s ‘Study Tour to China’ in November 2009. (Details enclosed).

11. To take note of Centres which have submitted audited accounts for the year 2008-09. (Details enclosed).

12. To approve the draft annual report and audited annual accounts 2008-09 (Draft Annual Report and Audited Accounts enclosed).

13. To take note of reports from Chairmen of various functional Committees. (Reports received enclosed).

14. To take note of Membership position of each Centre as on 15th July 2009 and to admit New Members. (Statement enclosed).

15. To decide about date of the next Managing Committee and 68th Annual General Meeting.

16. Any other matter with the permission of the chair.

Members are requested to make it convenient to attend the meeting and also inform Headquarter about attending or not attending the meeting. Also please bring this copy of the agenda.

Thanking you,

Yours truly,

ANAND J. GUPTA

HON. GEN. SECRETARY BUILDERS ’ ASSOCIATION OF INDIA

Delhi Office: D1/203, Aashirwad Complex, Green Park Main, New Delhi 110 016 ✆ 26568763 E-mail: [email protected]

Estd. 1941

BUILDERS ’ ASSOCIATION OF INDIA (All-India Association of Engineering Construction Contractors)

G-1/G-20, 7th Floor, Commerce Centre, J. Dadajee Road, Tardeo, Mumbai – 400034 Tel: (91-22) 23514134 , 23520507, 23514802 Fax: 23521328 ▲Grams BUILDASIND Web Site : www.baionline.in E-mail : [email protected] / [email protected]

Ref: 247/J/2009-10 dated July 20, 2009

MEMBERS OF THE GENERAL COUNCIL OF BAI

NOTICE

The Second Meeting of the General Council of Builders’ Association of India for the year 2009-10 will be held on Saturday, the 8th August 2009 at 3.00 p.m. at Hotel Clarks Shiraz, Taj Road, Agra (Tel: 0562-2226128 - 32), to transact the following business:-

AGENDA

1. To confirm the Minutes of the last General Council Meeting held on 2nd May 2009 at Chennai (Minutes already circulated).

2. To grant Leave of Absence.

3. Issues arising out of previous meeting.

4. To ratify decision of the Office Bearers of the Headquarter in postponing the BAI Trustees election for the term 2009-14. (Letter dated 18th June 2009 issued by Office Bearers enclosed)

5. To discuss constitutional amendment proposed by the Constitutional Amendment Committee. (Proposed Amendment enclosed).

6. To take note of and approve/ratify decision taken by the Managing Committee at its meeting held on 8th August 2009 at Agra.

7. To take note of reports from State Chairmen. (Reports received enclosed).

8. To decide about date of next General Council Meeting and 68th Annual General Meeting.

9. Any other matter with the permission of the Chair.

Members are requested to make it convenient to attend the meeting and also inform Headquarter about attending or not attending the meeting. Also please bring this copy of the agenda.

Thanking you,

Yours truly,

ANAND J. GUPTA

HON. GEN. SECRETARY BUILDERS ’ ASSOCIATION OF INDIA

Delhi Office: D1/203, Aashirwad Complex, Green Park Main, New Delhi 110 016 ✆ 26568763 E-mail: [email protected]

B.A.I. Centres at : Agra, Agra Cant., Ahmedabad, Ahmednagar, Allahabad, Aligarh, Alleppey, Amravati, Aurangabad, Bangalore, Baghpat, Baramati, Bareily, Baroda, Belgaum, Bhandara, Bharuch, Bhopal, Butibori, Calicut, Chengleput, Chennai, Coimbatore, Delhi, Dhanbad, Dhule, Dindigul, Durgapur, Erode, Gautam Buddha Nagar, Ghaziabad, Goa, Greater Noida, Haldia, Hapur, Hyderabad, Ichalkaranji, Indore, Jabalpur, Jagdalpur, Jaipur, Jalgaon, Jamshedpur, Kannur, Kanpur, Kanyakumari, Karaikal, Karimnagar, Karur, Kochi, Kodaikanal, Kolkata, Kottayam, Kumbakonam, Latur, Loni, Lucknow, Madurai, Mangalore, Medak, Meerut, Meerut Cant., Modinagar, Moradabad, Moradabad Northern Railway, Mumbai, Musiri, Muzaffarnagar, Mysore, Nagpur, Nalgonda, Nanded, Nasik, Neyveli, Parbhani, Patna, Phaltan, Pondicherry, Pune, Pudukkottai, Raichur, Raipur, Ramnathpuram, Ranchi, Salem, Sangamner, Sangli, Satara, Shimoga, Sitapur, Solapur, Surat, Tezpur, Thanjavur, Theni, Thripunithura, Tiruchirapalli, Tirunelveli, Tirupur, Tiruvananthapuram, Tuticorin, Ulhasnagar, Vellore, Vijayawada, Visakhapatnam, Warangal.

Item No.3

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009

ACTION TAKEN REPORT ON THE MANAGING COMMITTEE MEETI NG HELD ON 2ND MAY 2009 AT CHENNAI

1. Item No.5

BAI Trustees Election for the term 2009-2014 Office Bearers of the Headquarter have issued letter No.153/J/2009-10 dated 18th June 2009 to the Returning Officer, BAI Organisational Election, directing him to with hold the Trustees election in view of the proposed constitutional amendment to be brought in during the Managing Committee Meeting at Agra on 8th August 2009. Accordingly, the Returning Officer had informed about this, to Managing Committee / General Council Members and Chairmen of all BAI Centres, vide Circular No.197/J/2009-10 dated 1st July 2009.

2. Item No.11

Co-option of Members on the Managing Committee for 2009-10 As authorised by the Managing Committee, the President co-opted the following Members on the Managing Committee : Shri P. Dinakar – Southern (Chennai) Centre Shri B. Baskar Rao – Southern (Chennai) Centre Shri Ram Avatar – Delhi Centre Shri C. Kumaravelu – Thiruchirapalli Centre Shri Taro T. Manghnani, Mumbai Centre [Representative from Trustee] Special Invitees to the Managing Committee for 2009-10

Shri P.K. Ramachandran – Kochi Shri M.M. Mohandas – Kochi Shri V.S.K. Moorthy - Kochi Shri H.G. Vachharajani – Ahmedabad Shri Vindobhai Gamdiwala C. Patel - Ahmedabad Shri Hanamant G. Kulkarni – Solapur Shri C.K. Raul – Mumbai Shri Mahesh Mirani – Pune Shri Raman Changede – Pune Shri R.B. Krishnani - Pune Shri Arun D. Bhandare – Ichalkaranji Shri Uday Gokhale – Ichalkaranji Shri Murali S. Nair – Jamshedpur Shri K. Chandrasekar – Coimbatore Shri A. Devarajan – Coimbatore Shri Joshy Joseph – Nashik Shri Rajeev Khattar – Agra Shri Basavaraj S. Totad – Bangalore Shri K. Manivannan - Dindigul Shri Kanaka Sebesan – Tiruchirappalli Shri N. Sivakumar – Tiruchirappalli Shri M. Sellapan – Tiruchirappalli Shri K. Seenichamy – Tiruchirappalli Shri R. Dhana Sekaran – Tiruchirappalli Shri S. Mohamed Hussian – Tiruchirappalli Shri A.K. Krishnan – Tiruchirappalli

Shri M.V.G. Jawagar – Tiruchirappalli Shri M. Manimaran – Tiruchirappalli Shri R. Murugesan – Tiruchirappalli Shri K. Venkatesan – Vellore Shri M. Murugan – Tirunelveli Shri A. Lawrence Walter – Tirunelveli Shri M. Arulvel - Musiri Shri Mohamed Iqbal Qureshi – Ghaziabad Shri Rajiv Agarwal – Ghaziabad Shri R.S. Agarwal – Ranchi Shri R. Elangovan – Pondicherry Shri R. Sahadevan – Pondicherry Shri K.B. Sarvesvara Raja – Theni Shri A.M. Manickam – Neyveli Shri Y. Gabriel – Kanyakumari Shri T. Xavier Thomas - Kanyakumari Shri N. Karuppasamy – Tuticorin Shri T. Rajasekaran – Thanjavur Shri N.T. Balasundaram – Thanjavur Shri M. Sridhar - Kodaikanal Shri Jadhav Mahendra – Satara Shri S. Prakash – Mysore

3. Item No.12

Reconstitute and appoint Chairpersons & Co-Chairpersons of various functional Committees. 1. Shri Avinash M. Patil, Chairman, and Shri Anilbhai R. Zinzuwadia, Co-Chairman,

Banking & Finance Committee. 2. Shri M.V. Antony, Chairman, and Shri L. Moorthi, Co-Chairman, CIDC Standard

Contract Document Committee. 3. Shri B. Jayaram, Chairman, and Shri R. Murugan, Co-Chairman, Constitutional

Amendment Committee. 4. Shri K. Sriram, Chairman, and Shri G. Srinivasan, Co-Chairman, Corporate Affairs

Committee. 5. Shri Ved Khurana, Chairman, and Shri V.K. Rajendiran, Co-Chairman, CPWD Co-

ordination Committee. 6. Shri Raj Pal Arora, Chairman, and Shri R.R. Dhoot, Co-Chairman, Exhibitions &

Seminars Committee. 7. Shri A. Puhazhendi, Chairman, and Shri M.K. Sundaram, Co-Chairman, Grievances

Committee. 8. Shri K.P. Baney, Chairman, and Shri G. Ramamoorthi, Co-Chairman, Housing & Real

Estate Committee. 9. Prof. K.N. Vaid, Chairman, and Shri K.L. Mohan Rao, Co-Chairman, Human

Resources Development 10. Shri Cherian Varkey, Chairman, and Shri J.R. Sethuramalingm, Co-Chairman,

IFAWPCA Co-ordination Committee. 11. Shri D.L. Desai (Shankarbhai), Chairman, Indian Construction Bulletin Committee. 12. Shri C. Devarajan, Chairman, and Shri Kishore Viramgama, Co-Chairman,

Infrastructure Development Committee. 13. Shri Navin B. Vasoya Patel, Chairman, and Shri V.N. Varadarajan, Co-Chairman,

Irrigation Projects Committee. 14. Dr. Narendra D. Patel, Chairman, and Shri S.I. Chunkhare, Co-Chairman, ISO &

Environment Committee. 15. Shri Ram H. Daryani, Chairman, and Shri A.R. Jambekar, Co-Chairman, Law &

Arbitration Committee. 16. Shri K.K. Taparia, Chairman, and Shri Pradeep K. Chowdhury, Co-Chairman,

Mechanisation & Construction Committee.

17. Shri Lal Chand Sharma, Chairman, and Shri R. Prakash, Co-Chairman, Membership Development Committee.

18. Shri Prithpal Singh Anand, Chairman, and Shri D.K. Bhugra, Co-Chairman, Military Engineering Services Committee.

19. Shri U. Jayakodi, Chairman, and Shri S. Sankar, Co-Chairman, Project Export Promotion Council of India Co-ordination Committee.

20. Shri Naresh Grover, Chairman, and Shri CH Ramakotaiah, Co-Chairman, Provident Fund Committee.

21. Shri Narendra Kumar, Chairman, and Shri A.V.S. Mani, C0-Chairman, Public Relations Committee.

22. Shri Sushanta Kumar Basu, Chairman, and Shri Ravi Gupta, Co-Chairman, Railway Committee.

23. Dr. S. Vijaya Kumar, Chairman, and Shri M. Dhandavakrishnan, Co-Chairman, Research, Development & New Technology Committee.

24. Shri K. Viswanathan, Chairman, and Shri Mohanlal S. Katariya, Co-Chairman, Service Tax Committee.

25. Capt. A. Mohan, Chairman, and Shri Kaatoor Magalingam, C0-Chairman, Taxation Committee.

26. Shri D.C. Awasthi, Chairman, and Shri K. Appi Reddy, Co-Chairman, VAT Committee.

27. Dr. C.V. Ananthasayanam, Chairman, and Shri Ashok K. Choudhary, Co-Chairman, W.T.O. & ADB Committee.

4. Item No.16(ii)

Financial Assistance to Shri N.A. Samant As regards to the financial assistance to Shri N.A. Samant, an appeal was printed in ‘Indian Construction’ Bulletin, May 2009 issue, seeking members’ generous contribution, as Shri Samant was hospitalised.

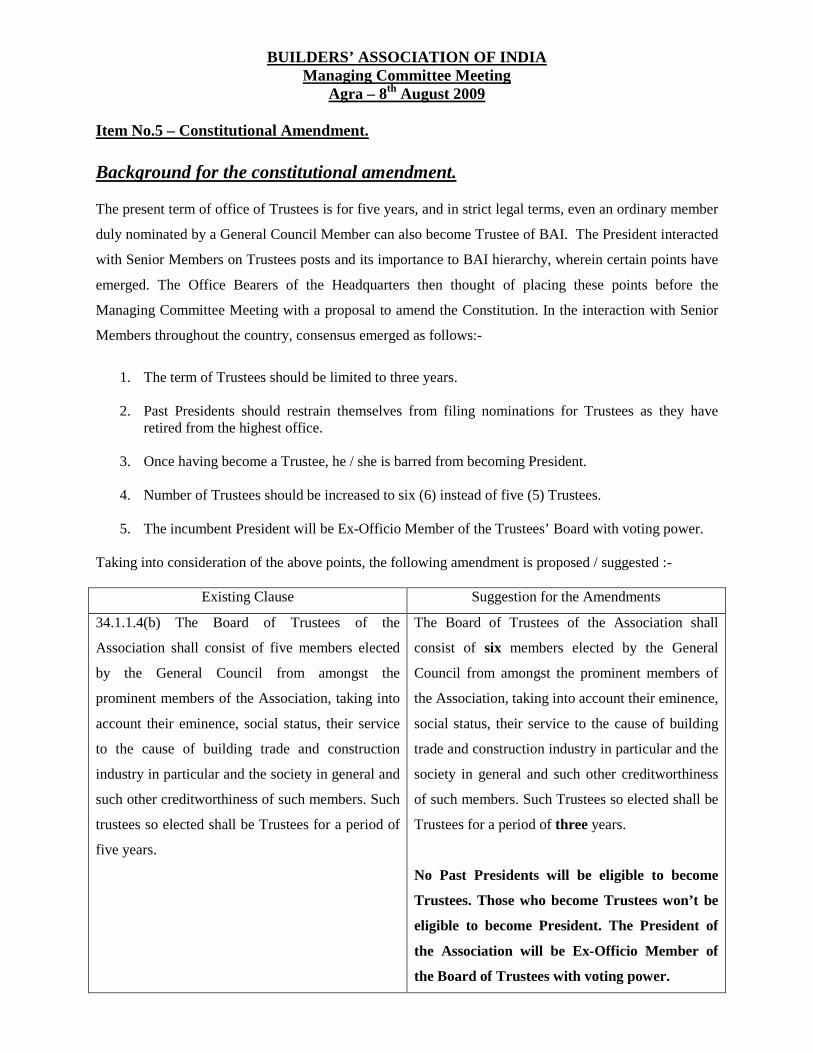

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009 Item No.5 – Constitutional Amendment. Background for the constitutional amendment. The present term of office of Trustees is for five years, and in strict legal terms, even an ordinary member

duly nominated by a General Council Member can also become Trustee of BAI. The President interacted

with Senior Members on Trustees posts and its importance to BAI hierarchy, wherein certain points have

emerged. The Office Bearers of the Headquarters then thought of placing these points before the

Managing Committee Meeting with a proposal to amend the Constitution. In the interaction with Senior

Members throughout the country, consensus emerged as follows:-

1. The term of Trustees should be limited to three years.

2. Past Presidents should restrain themselves from filing nominations for Trustees as they have

retired from the highest office.

3. Once having become a Trustee, he / she is barred from becoming President.

4. Number of Trustees should be increased to six (6) instead of five (5) Trustees.

5. The incumbent President will be Ex-Officio Member of the Trustees’ Board with voting power. Taking into consideration of the above points, the following amendment is proposed / suggested :-

Existing Clause Suggestion for the Amendments

34.1.1.4(b) The Board of Trustees of the

Association shall consist of five members elected

by the General Council from amongst the

prominent members of the Association, taking into

account their eminence, social status, their service

to the cause of building trade and construction

industry in particular and the society in general and

such other creditworthiness of such members. Such

trustees so elected shall be Trustees for a period of

five years.

The Board of Trustees of the Association shall

consist of six members elected by the General

Council from amongst the prominent members of

the Association, taking into account their eminence,

social status, their service to the cause of building

trade and construction industry in particular and the

society in general and such other creditworthiness

of such members. Such Trustees so elected shall be

Trustees for a period of three years.

No Past Presidents will be eligible to become

Trustees. Those who become Trustees won’t be

eligible to become President. The President of

the Association will be Ex-Officio Member of

the Board of Trustees with voting power.

BUILDERS’ ASSOCIATION OF INDIA

Managing Committee Meeting (Agra – 8th August 2009)

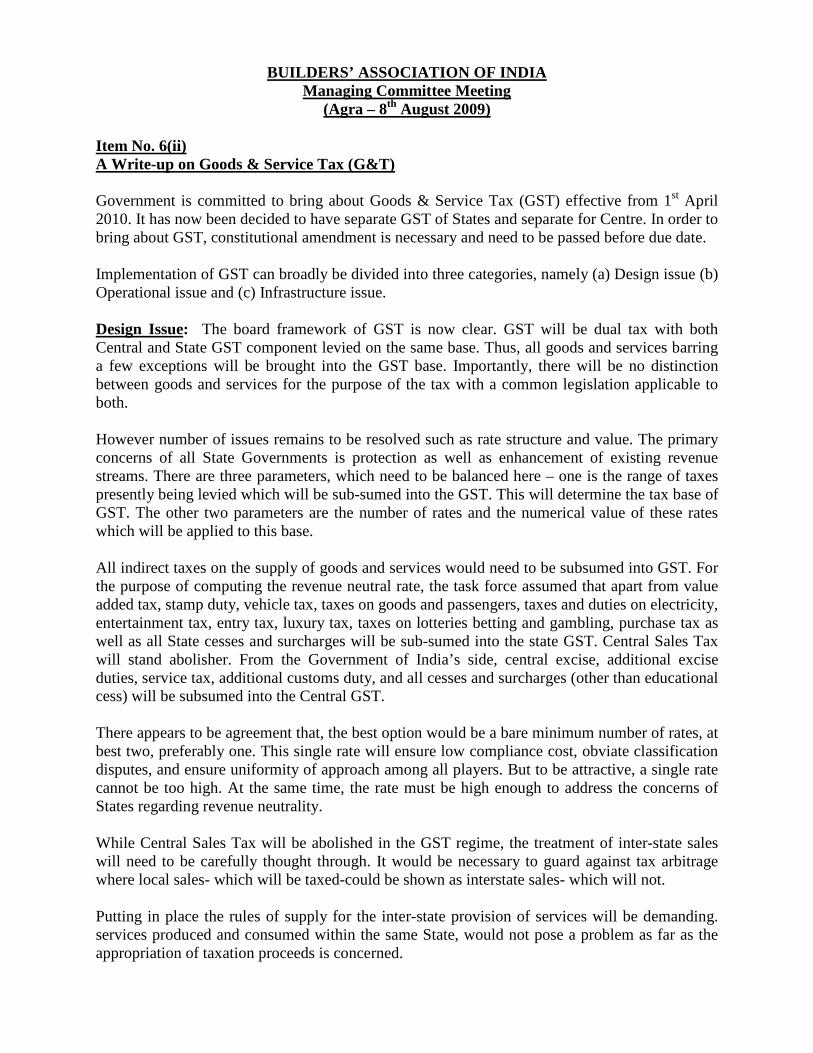

Item No. 6(ii) A Write-up on Goods & Service Tax (G&T) Government is committed to bring about Goods & Service Tax (GST) effective from 1st April 2010. It has now been decided to have separate GST of States and separate for Centre. In order to bring about GST, constitutional amendment is necessary and need to be passed before due date. Implementation of GST can broadly be divided into three categories, namely (a) Design issue (b) Operational issue and (c) Infrastructure issue. Design Issue: The board framework of GST is now clear. GST will be dual tax with both Central and State GST component levied on the same base. Thus, all goods and services barring a few exceptions will be brought into the GST base. Importantly, there will be no distinction between goods and services for the purpose of the tax with a common legislation applicable to both.

However number of issues remains to be resolved such as rate structure and value. The primary concerns of all State Governments is protection as well as enhancement of existing revenue streams. There are three parameters, which need to be balanced here – one is the range of taxes presently being levied which will be sub-sumed into the GST. This will determine the tax base of GST. The other two parameters are the number of rates and the numerical value of these rates which will be applied to this base.

All indirect taxes on the supply of goods and services would need to be subsumed into GST. For the purpose of computing the revenue neutral rate, the task force assumed that apart from value added tax, stamp duty, vehicle tax, taxes on goods and passengers, taxes and duties on electricity, entertainment tax, entry tax, luxury tax, taxes on lotteries betting and gambling, purchase tax as well as all State cesses and surcharges will be sub-sumed into the state GST. Central Sales Tax will stand abolisher. From the Government of India’s side, central excise, additional excise duties, service tax, additional customs duty, and all cesses and surcharges (other than educational cess) will be subsumed into the Central GST.

There appears to be agreement that, the best option would be a bare minimum number of rates, at best two, preferably one. This single rate will ensure low compliance cost, obviate classification disputes, and ensure uniformity of approach among all players. But to be attractive, a single rate cannot be too high. At the same time, the rate must be high enough to address the concerns of States regarding revenue neutrality.

While Central Sales Tax will be abolished in the GST regime, the treatment of inter-state sales will need to be carefully thought through. It would be necessary to guard against tax arbitrage where local sales- which will be taxed-could be shown as interstate sales- which will not.

Putting in place the rules of supply for the inter-state provision of services will be demanding. services produced and consumed within the same State, would not pose a problem as far as the appropriation of taxation proceeds is concerned.

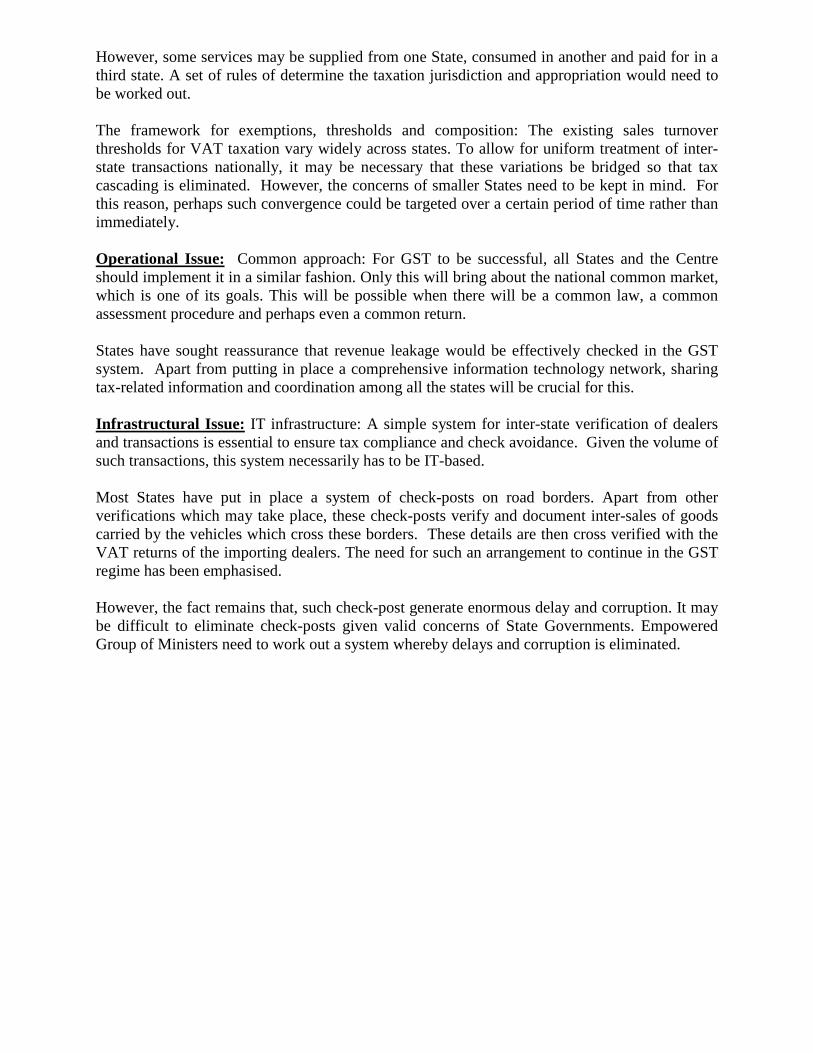

However, some services may be supplied from one State, consumed in another and paid for in a third state. A set of rules of determine the taxation jurisdiction and appropriation would need to be worked out.

The framework for exemptions, thresholds and composition: The existing sales turnover thresholds for VAT taxation vary widely across states. To allow for uniform treatment of inter-state transactions nationally, it may be necessary that these variations be bridged so that tax cascading is eliminated. However, the concerns of smaller States need to be kept in mind. For this reason, perhaps such convergence could be targeted over a certain period of time rather than immediately.

Operational Issue: Common approach: For GST to be successful, all States and the Centre should implement it in a similar fashion. Only this will bring about the national common market, which is one of its goals. This will be possible when there will be a common law, a common assessment procedure and perhaps even a common return.

States have sought reassurance that revenue leakage would be effectively checked in the GST system. Apart from putting in place a comprehensive information technology network, sharing tax-related information and coordination among all the states will be crucial for this. Infrastructural Issue: IT infrastructure: A simple system for inter-state verification of dealers and transactions is essential to ensure tax compliance and check avoidance. Given the volume of such transactions, this system necessarily has to be IT-based.

Most States have put in place a system of check-posts on road borders. Apart from other verifications which may take place, these check-posts verify and document inter-sales of goods carried by the vehicles which cross these borders. These details are then cross verified with the VAT returns of the importing dealers. The need for such an arrangement to continue in the GST regime has been emphasised.

However, the fact remains that, such check-post generate enormous delay and corruption. It may be difficult to eliminate check-posts given valid concerns of State Governments. Empowered Group of Ministers need to work out a system whereby delays and corruption is eliminated.

BUILDERS’ ASSOCIATION OF INDIA

Managing Committee Meeting (Agra – 8th August 2009)

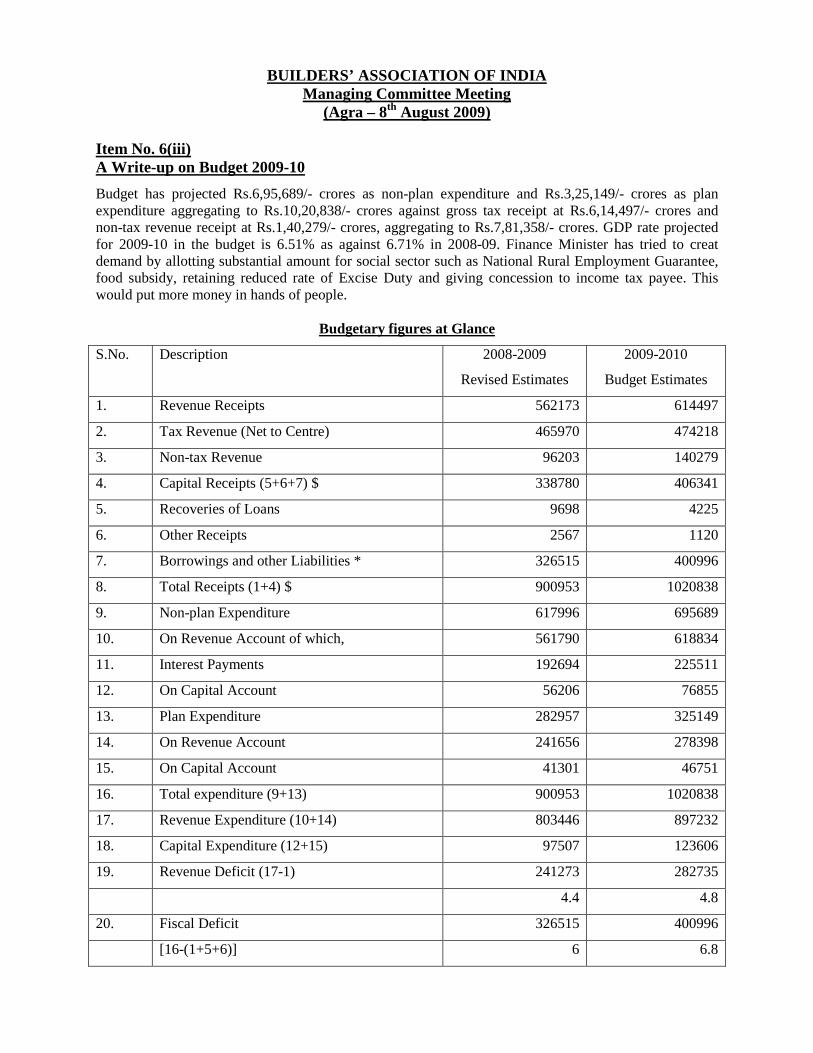

Item No. 6(iii) A Write-up on Budget 2009-10

Budget has projected Rs.6,95,689/- crores as non-plan expenditure and Rs.3,25,149/- crores as plan expenditure aggregating to Rs.10,20,838/- crores against gross tax receipt at Rs.6,14,497/- crores and non-tax revenue receipt at Rs.1,40,279/- crores, aggregating to Rs.7,81,358/- crores. GDP rate projected for 2009-10 in the budget is 6.51% as against 6.71% in 2008-09. Finance Minister has tried to creat demand by allotting substantial amount for social sector such as National Rural Employment Guarantee, food subsidy, retaining reduced rate of Excise Duty and giving concession to income tax payee. This would put more money in hands of people.

Budgetary figures at Glance

S.No. Description 2008-2009

Revised Estimates

2009-2010

Budget Estimates

1. Revenue Receipts 562173 614497

2. Tax Revenue (Net to Centre) 465970 474218

3. Non-tax Revenue 96203 140279

4. Capital Receipts (5+6+7) $ 338780 406341

5. Recoveries of Loans 9698 4225

6. Other Receipts 2567 1120

7. Borrowings and other Liabilities * 326515 400996

8. Total Receipts (1+4) $ 900953 1020838

9. Non-plan Expenditure 617996 695689

10. On Revenue Account of which, 561790 618834

11. Interest Payments 192694 225511

12. On Capital Account 56206 76855

13. Plan Expenditure 282957 325149

14. On Revenue Account 241656 278398

15. On Capital Account 41301 46751

16. Total expenditure (9+13) 900953 1020838

17. Revenue Expenditure (10+14) 803446 897232

18. Capital Expenditure (12+15) 97507 123606

19. Revenue Deficit (17-1) 241273 282735

4.4 4.8

20. Fiscal Deficit 326515 400996

[16-(1+5+6)] 6 6.8

In order to meet deficit, Government will borrow Rs.2,00,000/- crores from market and ask Reserve Bank of India to grant Rs.2,00,000/- crores i.e. Government will “monetise”. Disinvestment from Public Sector Undertakings targeted is Rs.1,210/- crores. Indirect Tax to fetch Rs.2,000/- crores. Central Goods and Service Tax (G&T) to be come operative from 1st April 2010. There is no consensus amongst States as regards rate of tax. State Goods & Service (SG&T) shall be separately operating in each State. Direct Tax Code draft suggesting structural changes in direct taxes will be released within 45 days for public debate. Government will finalise Direct Tax Code Bill taking into consideration suggestions received and place in the winter session of Parliament for sanction. Small and medium enterprises shall have option of declaring 8% profit on their turnover and pay Income Tax, if their turnover is less than Rs.40 lakh without complying with books of account. Tax can be paid by them at the time of filing return of income without paying advance tax. Commercial Banks funding to infrastructure companies is a long term commitment (10 to 15 years) whereas their funds (Fixed Deposits) are of short term tenure (1 to 5 years). This obviously runs the risk of mismatch in their books. Banks badly needed a specialised financing agency to take over such loans. Indian Infrastructure Finance Company Limited (IIFCL) will pick up such loans from Banks after 2 / 5 years. Such arrangement is known as “take out finance”. IIFCL is allowed to raise tax free bond of Rs.1 lakh crore to refinance 60% loans given by Commercial Banks to infrastructure developers. IIFCL accordingly may be able to finance projects to the tune of Rs.3 lakh crore in road sector, seaport projects being executed on PPP basis. In order to give momentum to rural housing, National Housing Bank will create Rs.2,000 crore funds to finance rural housing. Under Section 80IB(10) of Income Tax Act, income of real estate developers whose plans were approved before 31st March 2007, constructing flats of certain sizes were tax free. This was provided because real estate developers were taking investment risk. Contractors undertaking construction work is not entitled for such tax benefit. Accordingly, explanation to this section is introduced effective from 1st April 2001. Government is developing the blueprint for National Gas Grid. An amount of Rs.35,000 crores is projected to come from auction of 3G spectrum. Roads, Housing and Urban Development has received big budgetary support, thereby boosting prospect of construction sector. Highways Rs.20,450/- crores is provided for National Highways Development against Rs.17,550/- crores in

2008-2009. Rs. 8,578/- crores is provided from Central Road Fund. Rs. 1,988/- crores is provided as grants to State from Central Road Fund. Rs. 1,002/- crores is provided for Highway Maintenance from Central Road Fund. Rs.12,000/- crores for Pradhan Mantri Gram Sadak Yojna, which is 59% over 2008-09 provision. Rs.43,968/- crores

Housing

Rs. 8,800/- crores is provided under Indira Aawas Yojna, which is 63% higher than 2008-09 provision.

Rs. 3,973/- crores is provided under Rajiv Aawas Yojna and Slum free schemes. In addition, 1,00,000 dwelling units for paramilitary units to be constructed at different places. Urban Development Jawaharlal Nehru National Urban Renewal Mission (JNNURM) scheme originally applicable to 63 cities is now extended to Tier II and III cities. It has sanctioned 463 projects involving an amount of Rs.49,744/- crores compared to Rs.6,247/- crores provided in 2008-09. An extra amount of Rs.3,472/- crores is provided for Commonwealth Game. Rural Development An amount of Rs.9,203/- crores is provided for drinking water supply under Ministry of Rural Development. Service Tax

New Services included in the list of Taxable Services

The following new services are proposed to be included in the list of taxable services. These services would get covered under the list of taxable services from a date to be notified after the enactment of Finance (No. 2) Bill, 2009.

Transport of Goods through Rail: Presently, transportation of goods in containers by rail, by other than Government railways is taxable under section 65(105)(zzzp) since 2006. It is now proposed to impose service tax on goods transported by railways including Government railways, whether in containers or otherwise. Suitable abatement and exemption to specified goods would be provided through issuance of notification at the appropriate time.

Transport of Coastal Goods; and Goods transported through Inland water:

Coastal goods (as defined under the Customs Act) and transport of goods through National Waterways, and inland waters are proposed to be brought under tax net. Suitable abatement and exemption to specified goods would be provided through issuance of notification at the appropriate time.

Legal Consultancy Service: As in the case of management consultancy or engineering consultancy service, any consultancy, advice or technical assistance provided in any discipline of law is proposed to be subjected to service tax. However, the tax would be limited to services provided by a business entity to another business entity. It has been defined that a business entity includes firms, associates, enterprises, companies etc. but does not include an individual. Thus, services provided by an individual advocate either to an individual or even to a business entity would be outside the scope of the taxable service. Similarly, the services provided by a corporate legal firm to an individual would also be outside the purview of taxable service. Any service of appearance before any court of law or any statutory authority would also be kept outside this levy.

Amendments in Rules (pertaining to service taxpayers):

Changes in the Works Contract (Composition Scheme for Payment of Service Tax) Rules, 2007: These rules provide a simplified procedure for working out the tax liability by the service providers providing works contract service. Instead of working out the service element from the value of works contract and paying service tax at full rate (i.e. 10%) the service provider is allowed to pay 4% on the ‘gross amount charged’ for the works contract. The reason for prescribing the lower rate under the scheme is that the service provider need not bifurcate the gross value of works contract. It was expected that the gross value should be shown to include the total value of materials as well as services used in providing the taxable services.

However, it has been reported that in certain cases, the taxpayers are not including the full value of the goods required for execution of works contract for working out service tax liability under the Composition Scheme by either excluding the value of goods received free of cost from their client or splitting the contract into a sale contract (for a portion of goods required to execute the works contract) and works contract (for only a portion of the total value of goods and the labor charges), thus reducing the value of works contract for the purposes of calculating service tax. In order to plug this loophole, the Explanation appearing in sub-rule (3) is being amended to provide that the composition scheme would be available only to such works contracts where the gross value of works contract includes the value of all goods used in or in relation to the execution of works contract whether received free of cost or for consideration under any other contract. This condition would not apply to those works contracts, where either the execution of works contract has already started or any payment (whether in part or in full) has been made on or before the date of the amendment, i.e. 07.07.2009, from which the said amendment becomes effective (refer notification No.23/2009-ST dated 07.07.2009). Amendments made in CENVAT Credit Rules (pertaining to service tax). Rule 3(5B) of the CENVAT Credit Rules provide that, if value of any input or capital goods on which CENVAT credit has been taken, is written off fully or where provision to write off has been made in the books of account before being put to use, the ‘manufacturer’ shall pay an amount equivalent to the CENVAT credit taken on such item. Similar provision is presently not prescribed in case of taxable service provider. The said sub-rule is being amended to bring taxable service provider within the ambit of the said restriction. This provision would come into force immediately (Refer notification No.16/2009-CE (NT), dated 07.07.2009).

Rule 6(3) provides an option for a provider of taxable as well as exempt services, using common inputs or input services, but opting not to maintain separate accounts to pay an amount of 8 per cent of the value of exempted service. This provision was made when the rate of tax on taxable services was 12 per cent. Since the service tax rate has been reduced to 10 per cent, the said amount payable on the exempted services is being reduced from 8 per cent to 6 per cent of the value of exempted service. This provision would come into force immediately (Refer notification No16/2009-CE (NT), dated 07.07.2009).

For changes made in the Taxation of Services (Provided from Outside India and Received in India) Rules, 2006, please see para 7.1

Except this, there is no change in applicable service tax rates. Excise Duty (a) No change in excise duty on steel, cement and other construction materials.

(b) Excise Duty was not applicable to site pre-cast members such as beam, column, slab, but due to withdrawal of such exemption in 2006, the same was applicable. It is now propose to restore full exemption including pre-fabricated concrete slabs or blocks, when used for further construction at site.

Commodity Transaction Tax (CTT) is abolished. Minimum alternative tax increased from presently applicable 10% to 15%. Fringe Benefit Tax applicable to employer is abolished instead liability is shifted to employees. Direct Tax

There is no change in Income Tax on registered firms and individuals. Personal Income Tax exemption limit hiked by Rs.10,000/-. No surcharge of 10% on Personal Income Tax.

BUILDERS’ ASSOCIATION OF INDIA

Managing Committee Meeting Agra – 8th August 2009

Item No.13

Report from VAT Committee As the VAT Committee was constituted by our President on 11th May, 2009, there was no report from this Committee during GC/MC meeting, held at Chennai on 2nd May, 2009. Major developments during the last quarter are, therefore, being enumerated as below:- 1. In the State of Uttar Pradesh, BAI succeeded in getting major relief to all contractors by way of order dated 31-3-2009 from Allahabad High Court in writ petition no. 1575/2007 ( Builders Association of India Vs State of U.P.) wherein operating paragraph of impugned order reads thus:- “In the result, writ petition is allowed. The circular dated 4-6-2007 by Commissioner, Trade Tax is hereby quashed. The orders passed by assessing authority demanding State Development Tax are hereby set aside. There shall be no order as to cost.” With this order, the liability of State Development Tax @ 1% of turn-over on contractors from 1-5-2005 to 31-12-2007 became nil and considering average annual turnover of Rs. 10,000 crores approx. in U.P., the contractors fraternity in U.P. were relieved of liability of almost Rs. 270 crores. This favorable order was result of regular and aggressive follow-up of VAT Committee with Advocates and Parawai at High Court at Allahabad. 2. Second positive and fructifying action was filing of writ petition no. 643/2008 in march, 2008 (Builders Association of India Vs State of U.P. and others) in High Court of Judicature at Allahabad vide which BAI challenged notification dated 4th March, 2008 from Principal Secretary, Tax & Registration, directing all contractees to deduct 4% Tax at source from the running bills of contractors. Hon’ble High Court questioned the Government on validity of this notification; wherein there is no provision of inter state purchase in the Act itself. U.P. Government was obliged to amend the said Act, 2008 by inserting sub-section 14 in section 34 vide notification dated 28-2-2009 by way of UP VAT (Amendment) Act, 2009 (UP Act. No. 11 of 2009) wherein inserted sub-section 14 in section 34 reads thus:- “in section 34 of the principal Act, after sub-section (13) the following sub-section shall be inserted, namely:- (14) No deduction under this section shall be made on the turnover of sale where such sale takes place – (i) in the course of inter state sale or commerce; or (ii) outside the state; or

(iii) in the course of export out of, or import into, the territory of India” This amendment reduced liability of tax on inters state purchase, thereby reducing the tax liability. Thus writ petition filed by BAI in High Court in March, 2009 resulted in amendment of U P VAT Act, 2008 in about a year’s time.

3. Third achievement has been that of announcement of Compounding Scheme under U P VAT Act, 2009 by U P Government as on 7th June, 2009 merely after one year and five months from date of implementation of VAT i.e. 1-1-2008. The main features of VAT scheme are:-

a. Scheme is effective from 1-1-2008 and has three options:-

(i) Compounding @ 2% of turn-over and 2% to be deducted at source from running bills and one can purchase material worth 5% of contract value from outside the state.

(ii) Compounding @ 6% of turn-over and 6% to be deducted at source from running bills for those who can bring material to be used in the works contract from outside the state with no limit.

(iii) Regular assessment under the Act under the provisions of sub-section 14 of section 34 of the Act.

b. Contractor assessee, once opted for a particular compounding scheme, can neither

withdraw from the scheme nor switch over from one scheme to another. Option of composition is one time.

c. There is provision of refund of commercial tax, if the amount of TDS during a financial

year is more than 2% of turn-over in the said year.

d. If both main contractor and sub-contractor are registered and have opted same scheme, the amount of works turn-over and TDS can be adjusted in the returns of main contractor.

e. Main and Sub-contractors, opting for the scheme, cannot avail benefit of Input Tax

Credit.

It is worth mentioning that BAI could have got a better deal from U P Government as we started with proposal of 1% compounding scheme for purchases within state, but this percentage did not get favour of the Government as under old scheme of U P Trade Tax Act, the Government took the plea that when this percentage was increased from 1% to 2% in February, 2005, there is nothing on record to prove that BAI raised any objection whether oral or in writing. Government took this as consent of BAI and clarified that Government will not like to reduce it from 2% to 1%. We wish express our gratitude to Shri Lal Chand Sharma, Imm. Past Vice President (North); Shri R K Jain VP (North); Shri Mahesh Mangarani, State Chairman; Shri Charanjit Singh of Lucknow; Shri D L Desai (Shankerbhai); all Centers Chairmen and especially all members of U P Centre Kanpur for their continued support and encouragement.

Resultant of BAI vigorous, positive and constructive activities, Commercial Tax Department for the first time started sending invitations to BAI for discussions and deliberations on Tax matters pertaining to construction industry. It is established in U P Government that BAI is true spokes-organization of construction fraternity. Such meeting took place on 29th May, 2009 in the meeting Hall of Commercial Tax Department at Lucknow. Meeting was presided by Shri Anil Sant, commissioner, Commercial Tax and attended by 10 senior officers of the department and almost 25 leading BAI members from all over U P, including Corporate Sector. Meeting was a success.

4. VAT Committee Chairman visited Hyderabad thrice during the last six months and met Shri G. Lakhmi Prasad, Additional Commissioner (Law) and Shri Asutosh Misra, Principal Secretary, Tax & Revenues, Government of Andhra Pradesh to resolve burning issues, faced by contractors in A.P. Shri S. N. Reddy had developed excellent rapport with the Commercial Tax department and Government and succeeded in formation of committee in later half of 2008 and Shri G Lakshmi Prasad is Convener of Committee. Chairman, VAT Committee was accompanied by either of functionaries viz Shri S N Reddy, State Chairman, Shri Sudarshan Reddy, Shri V Sudhaker and Shri Udhay Bhasker, both Members of said committee. Shri Lakshmi Prasad informed us on 2nd July, 2009 that comprehensive proposal covering all issues is ready and is being circulated within department for getting feedback and appraisal from the officers of the department. Thereafter, the proposal will be forwarded to Principal Secretary, Tax & Revenue, who in turn will forward to Cabinet with his recommendations. This proposal was delayed due to elections and pre-occupation of Chief Minister, who is Minister-in-charge for this department. This proposal is likely to be cleared by state assembly during its session, commencing 26th July, 2009. 5. It have been learnt that Empowerment Committee of State Finance Ministers is seriously discussing and deliberating introduction GSA (Goods and Services Act) in the Parliament in near future and is planning to introduce this ACT with effect from 1st April, 2010 if passed by Parliament and assented by President of India. VAT Committee is in regular contact and dialogue with two officers, both of rank of Addl. Commissioner (Legal) from U.P. and A.P. as these two officers are actively involved in evolving GSA draft. This committee will come out with its report on GSA shortly.

D. C. Awasthi Chairman, VAT Committee

K. Appi Reddy Co-Chairman, VAT Committee

BUILDERS’ ASSOCIATION OF INDIA

Managing Committee Meeting Agra – 8th August 2009

Item No.13

Report from Shri K. Viswanathan, Chairman, Service Tax Committee

We are giving below the following Service Tax report for inclusion in the Agenda for the Agra Managing Committee & General Council Meeting. 1. No downward change in Composition rate proportionate to reduction in Service tax rate from 12% to 10%. 2. Amendments in Works Contract (Composition Scheme for payment of Service Tax). The Gross value of works contract includes the value of all goods used in or in relation to the execution of works contract whether received free of cost or for consideration under any other contract. The Government has sought to levy this tax on a prospective and not on retrospective basis and will not apply to those works contract where either the execution of works contract has already started or any payment (whether in part or full) has been made on or before the date of amendment i.e. 7.7.2009. 3. CENTRAL EXCISE - CHAPTER 68 Goods manufactured at the site of construction for use in construction work at such site have been fully exempted. (Notification No.15/2009 of Central Excise) I request you to take up the above for discussion in the Managing Committee / General Council Meeting to be held at Agra on 8th August 2009. K.VISWANATHAN Chairman, Service Tax Committee

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009

Item No.13

Report of Shri K.L. Mohan Rao, Co-Chairperson, Human Resource Development Committee

Development Human Capital in India A report by NCCET

The stress on the investment on the development of human capital in the union budget is a pointer that the need of more& more finishing school is there. The potential India, in the field of Human Capital has to be expanded in every field of Construction. While lot of stress is being is given on that, job guarantee in the rural side has given rise to shortage of manpower. The man power which otherwise used to migrate to city in search of livelihood, which went back to their home town on a short break this time is refusing to return to work as they have been offered lot of intensive & assurances under the Rojgar Yojana. This has been experienced by leading construction companies in India. Now the companies are on the lookout for the man power available locally. While doing so they are also trying their hand on the availability of trained and certified workforce. This only a tip of Iceberg, in the months to come there will be more and more shortage of man power in construction. The infrastructure getting a major boost in the budget as a result of the global meltdown, prompting the Government of India in giving an indirect stimulus to the economy by investing extensively in the Infrastructure project. The need of the hour will be to train the manpower in the alternate specialised fields like Marine Engineering, Gas Pipe lying, Heavy fabrications etc. apart from the regular mason, bar bender, scaffolding carpenter, plumber, tile layer which are already in short supply. Karnataka Effort Here training has been taken up in a massive scale. The government has been conducting job fare in all districts every alternate month. This has resulted in the motivation as well as the awareness of different avenues available to the unemployed youths. In a very humble way Koushalya Shaale, has been tying up with all available sources and agencies willing to take part in the manpower development. Tie-ups with the Engineering Colleges This has got a very positive response from most of the engineering colleges from the rural side. It is a total WIN –WIN situation for all in the region. The youths of the area will be getting exposed to the civil Engineering fields , at the same time efforts are being made to get them employed in Govt. projects with the agencies working there. The local youths who are trained in the area specific requirement of the Infrastructure projects in that districts. Though positive response is there, the results will come only after the two months training is completed. A group of youths have been identified by a leading company from Koushalya Shaale to be further trained and absorbed in their project works after 15 to 20 days of training. A very small start but

a very significant achievement. Now the Koushalya Shaale has invited the industry to take part in training in area specific trade which will get tailor-made for them after the trainees have undergone 60 hrs of training in Civil site safety and 60 hrs of personality development, working in groups and leader development programme. Response is there though slow. We anticipate heavy response after the first success story reaches the industry. Tie- up with BAI Belgaum An agreement has been reached between the BAI, a leading engineering institution, Nirmiti Kendra and Koushalya Shaale on 2nd July 2009. Koushalya Shaale with the help of the Govt. sponsored programme has identified and received application for training in different field like mason carpenters , ITI fitters , mechanics electrical wiremen etc these candidates will be trained in Belgaum as per the requirement of the BAI members to be absorbed in their projects. The training will be carried out for 300 hrs, where they will also be subjected in training of manufacturing of Fly Ash Bricks for the consumption of the BAI members. Thus we are also addressing the green issue. We intend to start training by 20th 0f July 2009. Tie up with Industry. We are in continuous negotiation with The International Plumbing Association, INSDAG, Construction equipment companies to associate with them in the field of training. Certification of the existing Labour Force under Modular Employable Skill Certification:

Construction industry is an unorganised sector. NCCET has taken action and has been partially successful.

In most of the developed and developing countries, any worker who works in industry must possess a certificates issued by the appropriate authority. Without valid certificates, it is not possible to work in any industry. Construction workers in Middle East could be cited as a best example to it.

In our country no industry is insisting on an individual's certificate at the time of recruitment. Anybody can work in any industry without proper training and skill certification.

Government of India has emerged with a massive program, called MES (Modular Employable Skill). It is being organized in two ways as follows.

1. Training the construction workers by competent authority. 2. Testing and certification of the trained workers.

Government in this initiative for the first time evokes industries to involve an agenda to train their work force for their suitable requirement, besides asking prominent industrial bodies to assume responsibility for testing and certification of the workers.

Implementation

Expectation is that any worker in a construction industry must possess the skill certificate issued by the competent authority. It could be mandatory for the industry to appoint only certified workers to serve at the construction sites. Many projects funded by World Bank and

IDBI operate under a contract class, insisting that the company involved in construction should in principle have a minimum of 40 percent certified work force.

Before enforcing the law, Government came forward to assess the skilled workers who are already working in construction industry and certify them. It has identified some of the organizations who are working for the welfare of the construction industry, in the assessment process.

Construction Industry Development Council (CIDC) is a part of the Planning Commission for the betterment of construction industry. It is one of the organisations assigned with the task of assessing capability of the construction workers.

South India is the jurisdiction where CIDC - MES Assessment Cell functions. After the assessment process, this cell facilitates the workers with an all powerful NCVT certificate. Its team of experts will visit various construction sites at the time convenient to the contractors to assess construction workers, without wasting their time and money. The said team would conduct a simple test to determine skill levels at the site itself (In MES Module).

As many as 3100 certification has been done for the existing experienced construction workers, in companies like Ahaluwalia Construction, JMC Projects, GINA Engineering etc, by our Senior Member Mr. Murlidhar under the Banner of Construction Industry Development Council - Directorate General of Employment & Training, Ministry of Labour & Employment, Government of India. Under the state Government banner Koushalya Shaale trained & Certified 936 members construction field, and Certified in Spoken English, Basic Computer & Tally – 374 for the children of construction workers. Total - 1310 members. K.L. MOHAN RAO Co-Chairperson, Human Resource Development committee Builders Association of India

BUILDERS’ ASSOCIATION OF INDIA

Managing Committee Meeting Agra – 8th August 2009

Item No.13

Report of Shri K.K. Taparia, Chairman, Mechanisation of Construction Committee

Phase 1 (June 2009- September 2009)

• Formation of Expert Research Body in consultation with BAI either INHOUSE or to be given to a Professional Research Agency for Primary Research

• Research on Ground Realties on Indian Mechanization scenario to understand scope for Improvement

o Degree of Mechanization sector wise, development wise, Investment wise etc. into

� Real Estate � Infrastructure � Industrial � Commercial etc.

o Indian Demand/Supply Scenario to understand many parameters like Psychology, Investments, urgency etc.

o Technology Knowledge , Availability & Affordability o Government Role o Understanding Trend in growth of Mechanization o Work done in past and planning by institutions etc.

• Report preparation on Understanding penetration of Mechanization in Developed Nations in their Growth Stage in Past to understand their strategies

� Government Role of respective nations � Private Institutional Roles � Financial Institutional Role � Real Estate & Infrastructure Demand � Technology Investments � Economic Phase

• GDP • Capital Formation

• Need • Government Policies

• Demand & supply • Productivity of Execution • Degree of Mechanization

• Consolidated Report Generation by Using Primary and Secondary Research Reports on Indian Ground Reality, Comparison to Understand economic phases and Gap Analysis with developed nation.

• A state level Report to be prepared for Understanding scope and Required Efforts ETC.

• A STATE LEVEL Execution Team to be formed in Consultation with State Level Chairman’s.

• Analysis of above reports in preparing a plan for improving Degree of Mechanization • National objectives and Regional objectives will be decided by the Mechanization

Committee after studying the report.

Phase 2 (October 2009 – December 2009)

• Penetration of seriousness through awareness of this Report to all the concerned government departments

• Penetration of seriousness through awareness of this Report to all the concerned Government Institutions, Private Institutions, financial institutions, Government Councils, training institutes etc.

• A central committee will coordinate & control all India campaign.

• A campaign committee to be formed on all the BAI centers for penetration TO THE TARGET GROUPS.

• An expert committee for Planning & execution of awareness through campaigns, Seminars, quizzes, presentations, round table discussion through participation of all levels target audience, influencers, general public etc.

• A special focus campaign is to be designed for Future Engineers and managers specially civil and mechanical engineering students.

• Efforts to be taken to create Mechanization committee in Engineering and management institutions.

• Specific marketing communications to be prepared as mailers and to be sent on regular basis to target audiences and influencers.

• Awareness Campaign/branding/positioning/Marketing may be given to a professional agency.

Phase 3 (January 2010 – May 2010)

• In this phase a Strict Monitoring, training if required, Guiding, Supporting & controlling by central committee on Pan India Level.

• A THRUST TO BE CREATED ON ALL LEVELS TO IMPLIMENT THE Necessary SUGGESTIONS OF REPORT IN IMPROVING DEGREE OF MECHNISATION.

K.K. TAPARIA Chairman, Mechanisation of Construction Committee

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009

Item No.13

Report of Shri Anilbhai Zinzuwadia, Co-Chairperson, Banking & Finance Committee

I am thankful to the President for appointing me as the Co-Chairperson of Banking & Finance Committee for 2009-10. The Committee has taken up the issues concerning to the contractors on the finance and made various representations requesting the Finance Ministry to consider establishing a Construction Bank, as exists in China, which deals with all construction funding i.e. loans at low interest, security for abroad projects, bill discounting for work done, bank guarantees at small margins, term loans for new machineries, training school at all regions, so that we meet shortage of skilled workers, operators, project managers, etc. The Committee requested the Finance Ministry to consider to establish National Infrastructure Bank, as exists in USA for funding exclusively for infrastructure projects. The Committee requested the Hon’ble Finance Minister, Governor of Reserve Bank of India and Indian Banks’ Association, to sympathetically consider the following issues:- (a) Reduction in interest rate on finances issued to construction companies. (b) Reduction in Bank Guarantee Margin and interest rate. (c) Provision for funding for purchasing heavy construction equipments. (d) Reduction in Bills Discounting Facilities in all Nationalised Banks.

ANILBHAI ZINZUWADIA Co-Chairperson, Banking & Finance Committee

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009

Item No.13

Report of Shri Navin B. Vasoya Patel, Chairman, Irrigation Projects Committee Thank you for appointing me as the Chairman of Irrigation Projects Committee of BAI. Initially, I have started getting problems from the contractors working for Irrigation Projects in the State of Gujarat. Project of Restoration and Strengthening the existing Earthen Embankment on the banks of River Tapi, near Surat City of Gujarat, constructed in 10 packages by various contractors. The most of the package works are completed by the contractors within a year and a half and the project work is at the completion stage. For all those contractors for their common problems, I have represented to the Secretary, Water Resources Department of Government of Gujarat, for the problems like wrongfully deducting the testing charges @ 1% of the estimated cost, as there is no provision of deducting such charges in the agreement. Wringfully deduction of payment for the item of providing and laying geo-fabric with a lap of 0.50 m. even though it is stipulated in the specification, the department is not paying for the lap length. This is also brought to the notice of the Government for making stipulated payment as per the agreement like price variation in approved extended time limit. The Secretary, Water Resources Department, had given the assurances to resolve these problems and arranging a meeting with concerned officers and affected contractors in my presence. There is also a very big project Sujalam Sufalam Yojana of about Rs.4,500 crores executed and completed by various contractors. A part of this project is construction of 360 Km long Canal 2ith 12.0 m bed width and various structures on the Canal from Kadana Dam on River Mahi to the scarcity area of North Gujarat. The contractors are facing numerous problems like time limit extension, approval of excess / extra items, price variation, etc. I have represented along with affected contractors to the concerned Chief Engineer, and Additional Secretary for individual and common problems of contractors. Government is considering fulfilling the same. Thus, I have started to represent the contractors of the Irrigation Projects on behalf of Builders’ Association of India, initially from Gujarat State. As I am going abroad for a month, I will not be able to attend the MC / GC Meeting at Agra. After returning from abroad in due course, I will expand the activity of BAI with the help of all the Members of Managing Committee, State Chairmen, and Centres’ Chairmen. NAVIN B. VASOYA PATEL Chairman, Irrigation Projects Committee Builders’ Association of India

BUILDERS’ ASSOCIATION OF INDIA Managing Committee Meeting

Agra – 8th August 2009

Item No.13

REPORT FROM SHRI RAM H. DARYANI, CHAIRMAN, LAW & AR BITRATION COMMITTEE IN CONNECTION WITH FILING A PIL IN THE SUPREME COUR T OF INDIA

In last 10-12 years of practice in the field of arbitration I have come to conclusion that the process of arbitration has failed miserably. It cannot be denied that the intentions of the law makers were honourable. They intended that arbitration should take load off the shoulders of judiciary. But due to several reasons the result has been totally reverse. The load on the judiciary has increased many folds. If this is analyzed in the right spirit it will be seen that there are two factors which have produced results contrary to the expectations. These factors are:

1. The arbitrators are not independent and impartial. 2. The awards of the arbitrators are invariably challenged as a matter of ritual.

The arbitrators are not independent and impartial. Government of India is the largest purchaser in India. Therefore Government of India is the largest litigant in India. The purchases are done through tenders floated by various government organizations. In the tender documents invariably in the arbitration clause only departmental officers are appointed as arbitrators. By any stretch of imagination these serving departmental officers can never be impartial and independent. During process of many arbitration meetings I have categorically asked the arbitrators off the record about their impartiality. They all have agreed that they cannot be impartial as they are serving officers. Under the circumstances having arbitrators who are not impartial is against the spirit of arbitration in particular and justice in general. Therefore I believe that BAI should fight tooth and nail to remove such one sided clauses from the contract agreements; which contractors have to accept as they have to remain in business. BAI has been trying since last 30 years or so, to get the “Standard Contract Documents” approved. But every time some politician comes and gives assurances and the matter is put on the back burner. I personally believe that government will not relinquish power so easily. The only possible chance is to bring a pressure from the Apex Court of India. Thinking on these lines I believe that filing a PIL is the only way out. I have done some research on the subject and also consulted some eminent lawyers. A view has emerged that winning a PIL is a fairly good possibility. The PIL can be argued on 3 basic points.

a) The arbitration clauses of Railway, CPWD and MES are against the spirit of the Arbitration Act. As per Section 11 (8). The relevant section is reproduced below:

(8) The chief Justice or the person or institution designated by him in appointing an arbitrator, shall have due regard to – (a) any qualifications required of arbitrator by the agreement of the parties; and (b) other considerations are likely to secure the appointment of an independent and impartial arbitrator.

b) One of the cardinal principles of natural justice is: 'Nemo debet esse judex in propria causa' (No man shall be a judge in his own cause). The deciding authority must be impartial and without bias.

c) Article 14 of Constitution of India is reproduced below:

14. Equality before law.—The State shall not deny to any person equality before the law or the equal protect ion of the laws within the territory of India. Railway, CPWD and MES are instrumentality of Government of India. Therefore providing departmental officers as arbitrators is being impartial citizens of India. It may please be noted that Article 14 is one of the ‘Fundamental Rights’ as guaranteed by the Constitution of India. Therefore this PIL can be referred to the Constitution Bench. Under the circumstances I am of the opinion that BAI, being the only All India organisation looking after welfare of the contractors, must go for this PIL. The awards of the arbitrators are invariably challenged as a matter of ritual. Another point which is responsible for failure of Arbitration process is the ritualistic approach of the departments to defend the case till the last available resource; that is Supreme Court of India. It does not matter whether the appeal has any substance or not. This matter is further aggravated by the attitude of the judiciary. During one seminar, the senior legal luminary, Shri. Fali Nariman opined “The mentality of the judges has to change as they consider the award of arbitrator as a signed piece of paper”. In fact, the process of challenging the award is very difficult, if one goes by the word of law. But changing the mentality of the judges is beyond any law. Therefore only the time will bring the change. But one thing I must say. The change has started coming. Till now Article 14 was no where seen in Court judgments. I have seen Article 14 being invoked in at least two judgments. One is Stav Infrastructure v. Union of India by Patna High Court. Another is Pawanhans Helicopters v. Associate Engineering by Supreme Court of India. For the time being, I propose that, BAI should move a PIL on the above subject matter. I am not aware what has been done in the past by the Committee of “Law & Arbitration”. I had requested the Secretariat to provide the record. Till date it is not provided. In case there some on going projects, I will surely carry them forward. RAM H. DARYANI CHAIRMAN, LAW & ARBITRATION COMMITTEE

BUILDERS’ ASSOCIATION OF INDIA

General Council Meeting Agra – 8th August 2009

Item No.7

Report of Shri Pratap B. Salunkhe State Chairman, Maharashtra

It is my pleasure to submit State Chairman report to you. With commitment and conviction to add value to BAI, I and all Maharashtra State Centers are putting sincere efforts. Herewith I am putting brief activities since last Managing Committee / General Council Meeting. Senior Members Meeting :

After attending last Managing Committee/General Council Meeting on 2nd May 2009, I had decided to focus on certain issues on priority basis like increasing membership strength, opening of new centers, taxes etc. So to decide a line of action, a Senior Members Meeting is called on 11th May 2009 at Mumbai. The meeting was quite successful. Senior members had taken responsibility to strengthen small Centers. Maharashtra State Level Meeting :

A State Level Meeting is organised on 13th June 2009 at Ichalkaranji Centre. Our respected President, Shri A.K. Yussouf, along with Vice President, Shri Ram M. Bhatia; Hon Gen Secretary, Shri Anand J. Gupta; Past President, Shri P.R. Mundle; Past State Chairman, Maharashtra, Shri Mohan Kataria; and Imm. Past State Chairman, Maharashtra, Shri Avinash M. Patil and other dignitaries addressed the meeting. Issues like VAT, Service Tax, DSR, were discussed. More than 110 members from all over Maharashtra attended the meeting. Installation of State Chairman, Maharashtra:

Installation as State Chairman is done in presence of Hon’ble Minister of Rural Development & Tourism, Maharashtra, Shri Vijaysinh Mohite Patil; Hon’ble Ex Minister of Textile, Maharashtra, Shri Prakashrao Aawade; Hon’ble MLA Shri Rajeev Awale; Hon’ble MLA Shri Sanjay Patil. All of them assured to solve problems of builders and contractors. President Shri A.K. Yussouf; Vice President Shri Ram M. Bhatia along with office bearers were present and addressed in the installation. Nearly 1000 citizens, BAI members, contractors were present for the installation function. President Visit :

From 13th June to 17th June 2009, was very special for us. Myself and President Shri A.K. Yussouf arranged visits to BAI Centers spread over Maharashtra. In this visit, 12 Centers are covered. Each visited Centre has shown keen interest and members had actively contributed. During the visit, I and President addressed the need to add more members and motivated them to do activities like seminars, workshops etc. It is result of this visit that many of Centers aggressively adding new members to their tally. Ichalkaranji Centre has added 17 new Patron Members and more and more Centers are doing well in the concern. I am expressing my sincere thanks for giving me this opportunity to share. Yours truly, PRATAP B. SALUNKHE State Chairman, Maharashtra Builders Association of India

ATTENDANCE SHEET FORMING PART OF ANNUAL REPORT FOR THE YEAR 2008-2009 ATTENDANCE (OUT OF FOUR MEETINGS )

Name Attendance Name Attendance S.P. Goel, President 4 Shri Praphulla Kumar 2 Shri N. Narendra Kumar, Vice President 4 Shri L.D. Kotwani 0 Shri Lal Chand Sharma, Vice President 4 Shri Bhagwan J. Deokar 4 Shri A. Puhazhendi, Vice President 4 Shri Potekar Manoj Laxmanrao 2 Shri Jawahar Mutha, Vice President 4 Shri Mohan D. Bhate 3 Shri Anand J. Gupta, Hon. Gen. Secretary 4 Shri N.M. Patel 4 Shri C.G. Deochake, Hon. Gen. Treasurer 4 Shri Mohan S. Kataria 3 Shri K.J. George 1 State Chairman Shri D.L. Desai (Shankarbhai) 3 Shri S. Narasimha Reddy (Andhra Pradesh) 3 Shri S.I. Chunkhare 3 Shri Rajkumar Agarwal (Madhya Pradesh) 0 Shri Ram M. Bhatia 1 Shri Arun Sahai (Delhi) 0 Shri T.T. Manghnani (Rep. Trustees) 4 Shri Uttam Chand Jain (Chattisgarh) 0 Shri Tarak R. Mamalatdarna (Gujrat) 2 Members co-opted to Managing Committee Shri Navin Modi (Jharkhand) 0 Shri K. Basavaraja Gowda 3 Shri K. Subramani (Karnataka) 4 Dr. D. Thukkaram 2 Shri M.M. Mohandas (Kerala) 3 Shri G. Vasudevan 0 Shri Avinash M. Patil (Maharashtra) 3 Shri Narayan H. Bhatia 1 Shri V.N. Varadharajan (Tamil Nadu) 4 Shri Ravindra Tyagi (Uttar Pradesh) 0 Special Invitees to the Managing Committee Shri Pradip Kumar Mukherjee (West Bengal) 2 Shri A. Ramasamy 1 Shri B. Chandra Mohanan 2 Members of the Managing Committee Shri B. Karthikeyan 0 Shri B. Jayaraman 1 Shri C.K. Raul 0 Shri G. Ramamoorthy 4 Shri C.K.S. Panicker 3 Shri A.V. Ramasamy 2 Shri C.T. Narayanan 3 Shri P. Dinakar 3 Shri D.K. Bhugra 1 Shri R.K. jain 2 Shri G. Udayakumar 1 Shri Anilbhai R. Zinzuwadia 3 Shri Joshy Joseph 2 Shri Jagdish Parekh 1 Shri K. Mathiyalagan 1 Shri R.R. Dhoot 2 Shri K. Seenichamy 1 Shri L. Moorthi 4 Shri M. Sellapan 1 Shri Narendra D. Patel 1 Shri M.R. Ravi 1 Shri J.R. Sethuramalingam 3 Shri Murali S. Nair 1 Shri V.S.K. Moorthy 3 Shri Muruganandam 0 Shri B.R. Ravichandran 4 Shri N. Sukumar 3 Shri M. Dhandavakrishnan 3 Shri Neeraj Tyagi 0 Shri Nalin Vinayak 0 Shri R. Kumaraswamy 0 Shri Prithipal Singh Anand 1 Shri Rishi Raj 0 Shri Harshad Bhayani 2 Shri S. Prakash 1 Shri K. Sriram 4 Shri Sachin Chandra 2 Shri Madan M. Jagota 1 Shri Shivkumar Bhalla 1 Shri S. Prabhu 2 Shri Uday Gokhale 0 Dr. C.V. Ananthasayanam 2 Shri V. Sudhakar 0 Shri M.V. Antony 3 Shri Y.S. Rama Raju 1 Shri Pratap Salunkhe 1 Shri M.S. Nandakumar 2 Chairpersons of Committees Shri D. Kempanna 2 Shri Lal Chand Ralhan 3 Shri Jaiprakash Bhatia 0 Shri R. Murugan 2 Shri V.M. Fazal Ali 3 Shri K.P. Baney 3 Shri Iqbal Waheed 0 Dr. Kirty Dave 0 Prof. K.N. Vaid 0 Patron Members Category Shri B. Seenaiah 0 Shri S.K. Pradhan 1 Shri Mahesh Mudda 0 Shri Ashok Chaudhary 1 Shri Cherian Varkey 3 Shri Y.N. Singh 0 Shri Sanjiv Shah 2 Shri Prabir Kumar Mukherjee 1 Shri P.R. Mundle 3 Shri K. Ramanujam 0 Shri R.N. Raju 0 Shri Varkey John 0 Shri Raj Pal Arora 3 Shri Dhanwant Lal Gupta 1 Shri N. Sriram 3 Shri N.C. Sundramurthy 2 Capt. Mohan 2 Shri Varghese Kannampally 2 Shri D.C. Awasthi 4 Shri H.N. Vijaya Raghava Reddy 2 Shri Basavaraja S. Totad 2 Representing Affiliated Associations Shri P. Jayapal 4 Shri Senthil Kumar 0 Shri Mathew Alex Vellappally 1 Shri Vinodbhai Gamdiwala C. Patel 3 Shri URC Devarajan 0

Discrepancy, if any, may kindly be informed to the Head Quarter Secretariat on or before 20thAugust 2009.