Embed Size (px)

Citation preview

July 2015

Sponsored by:

BANK CAPITAL 2015 COMPLETING THE PUZZLE

000 Bank Capital 2015 Cover.indd 1 06/07/2015 08:58

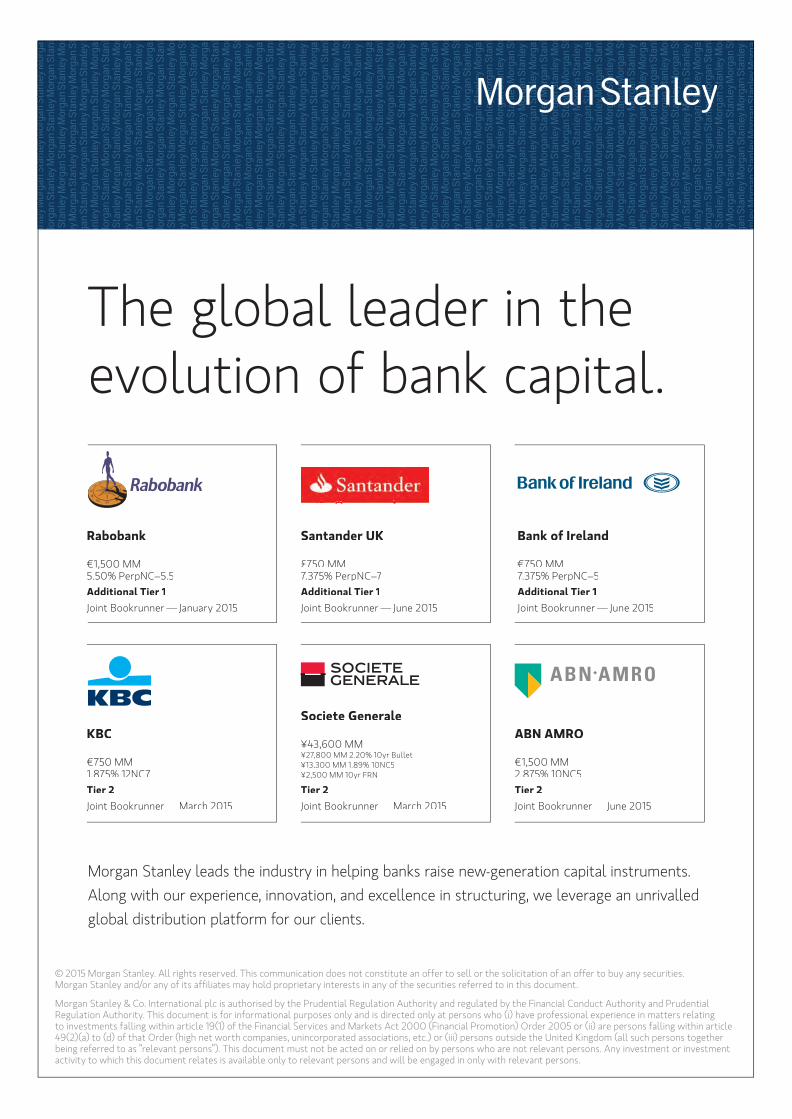

Global Perspective, Access and ExpertiseFor nearly 80 years, Morgan Stanley has mobilized capital to help governments, corporations, institutions and individuals achieve their financial goals. Our reputation and success are built on the innovative thinking and unique insight that have created new opportunities for investors around the world.

Through decades of dramatic change, our commitment to solving complex problems for clients has remained our priority, and is grounded in the first-class service and high standard of excellence that have always defined the firm.

Learn more at morganstanley.com.

© 2015 Morgan Stanley

Bank Capital | July 2015 | 1

BANK CAPITAL 2015

2 OVERVIEW Banks desperate to see the final act in post-crisis capital

4 THE REGULATORS The view from the top

6 TLAC / MREL A quantum, for solace: how much capital needs to be raised?

9 BANK CAPITAL ISSUERS’ ROUNDTABLE Seeking the best solution as regulators move the goalposts

19 PRIMARY MARKET UPDATE Banks await final orders with markets open for business

21 AT1 MAP European AT1 landscape: overview of structures

22 INSURANCE CAPITAL Insurers finally come face to face with Solvency II

24 BANK CAPITAL INVESTORS’ ROUNDTABLE Confronting shifting sands of bank capital risks

34 THE AT1 INVESTOR BASE A volatile asset class? Get real

36 AT1 SURVEY Polling the AT1 investor base

38 RATINGS Waiting for the captial raisings and recovery regimes to pay off

40 LIABILITY MANAGEMENT Sitting on their hands

Euromoney Institutional Investor PLC8 Bouverie Street, London, EC4Y 8AX, UKTel: +44 20 7779 8888 • Fax: +44 20 7779 7329 Email: [email protected] director, GlobalCapital group: John Orchard Managing editor: Toby FildesEditor: Ralph SinclairContributing editors: Nick Jacob, Philip MoorePEOPLE & MARKETSPeople and markets editor: Owen SandersonPUBLIC SECTOR and MTNs SSA editor: Tessa WilkieDeputy SSA editor and MTNs & CP editor: Craig McGlashanMTNs and CP reporter: Jonathan BreenFINANCIAL INSTITUTIONSFixed income editor: Graham BippartCovered bond editor: Bill ThornhillCovered bond reporter: Virginia FurnessFIG editor: Tom PorterSECURITIZATIONGlobal securitization editor: Will Caiger-SmithSecuritization reporter: Ryan BolgerSecuritization data analyst: Luka DimitrovCORPORATE FINANCINGCorporate finance editor: Jon HayCorporate bonds editor: Nathan CollinsLoans editor: Dan AldersonEquity senior reporter: Olivier HolmeyLeveraged loans reporter: Ross LancasterHigh yield bonds reporter: Victor JimenezSyndicated loans reporter: Elly WhittakerEMERGING MARKETSEmerging markets editor: Francesca YoungEmerging markets reporter: Steve GilmoreLatin America reporter: Oliver West

Head of product: Emmanuelle RathouisDesign and production manager: Gerald Hayes Deputy design and production manager: Emily FosterProduction: Andy BunyanNight editor: Julian MarshallCartoonist: Olly Copplestone • [email protected] & Project Manager: Sara Posnasky +44 20 7779 7301

AmericasUS Publisher - Capital Markets Group: James Barfield Tel: +1 212 224 3445Advertising and Sponsorship Associate Kevin Dougherty Tel: +1 212 224 3288Publisher: Oliver Hawkins +44 20 7779 7304Deputy publisher: Daniel Elton +44 20 7779 7305Associate publisher: Henry Krzymuski +44 20 7779 7303

Marketing Clare Cottrell +44 20 7827 6458Claudia Marquez Reyes +44 20 7827 6428Customer Services: +44 20 7779 8610

SubscriptionsEuropeJames Anderson +44 20 7779 8338 Katherine Clack +44 20 7779 8612Mark Goodes +44 20 7779 8605Philip Huntsman +44 20 7779 8036George Williams +44 20 7779 8274

Directors: PR Ensor (chairman), The Viscount Rothermere (joint president), Sir Patrick Sergeant (joint president), CHC Fordham (managing director), D Alfano, A Ballingal, JC Botts, DC Cohen, T Hillgarth, CR Jones, M Morgan, NF Osborn, J Wilkinson

Printed by MethodUK All rights reserved. No part of this publication may be reproduced without the prior consent of the publisher. While every care is taken in the preparation of this newspaper, no responsibility can be accepted for any errors, however caused.© Euromoney Institutional Investor PLC, 2015 ISSN 2055 2165

001 Contents Bank Cap.indd 1 06/07/2015 08:59

2 | July 2015 | Bank Capital

OVERVIEW OVERVIEW

THE BIGGEST CORPORATE collapses in the 21st century have tended to produce two things — regula-tion and movies. Enron spawned The Smartest Guys in the Room and the Sarbanes-Oxley Act. Lehman Broth-ers has been rather more prolific. So far it has provided source material for the Oscar-winning Inside Job, the Oscar-nominated Margin Call, and the not Oscar-nominated Too Big to Fail, which featured a very beardy performance from Paul Giamatti as former Federal Reserve chairman Ben Bernanke.

Its regulatory legacy, though, is still in the cutting room. Lehman’s demise can already be credited with Basel III, the USA’s Dodd-Frank Act and Europe’s CRD IV, and it will soon chalk up the next challenge for the world’s biggest banks — total loss-absorbing capacity, or TLAC.

When the Financial Stability Board in November unveiled its TLAC pro-posals, which require the global sys-temically important banks (G-SIBs) to hold bail-inable instruments equivalent to between 16% and 20% of their risk-weighted assets, it betrayed the ultimate goal of post-crisis banking regulation.

The FSB said the rules would address the “recapitalisation capac-ity” of banks. If Lehman proved any-thing, it was that if a bank was to fail on a Friday without cost to the tax-payer, it had to be raring to go as a via-ble institution by Monday.

“It is all about resolution now, not liquidation,” says Jackie Ineke, head of European financials credit research at Morgan Stanley in Zurich. “TLAC is now more important than capital to a great extent. In most cases as a bond-holder you will be resolved before liq-uidation is even thought about. That bank needs to be incredibly well capi-talised going into the next six months of its life post the resolution weekend.”

The FSB’s 16% lower level comes from the 8% minimum capital require-ment imposed by Basel III across core

equity, additional tier one and tier two, and then another 8% to replace that capital, which is assumed to have been completely wiped out in a resolution.

Banks are being forced to hold capi-tal for two adequately capitalised insti-tutions: the one they are now, and the reincarnation that will emerge should they run into trouble. Bail-ins not bail-outs. Resolution not liquidation. These are the placard slogans of contempo-rary banking regulation.

The final act?The final TLAC rules are due to be presented at November’s G20 Lead-ers’ Summit in Turkey. The European Banking Authority will then unveil its own version, the minimum require-ment for own funds and eligible liabili-ties (MREL), by the end of the year, enabling national regulators to sit

down with every European bank and give them a final number for total capi-tal. This should be the final piece of the post-crisis capital puzzle for banks, which have had to raise eye-water-ing amounts already, largely via loss-absorbing instruments that didn’t exist only a few years ago.

“We now have a much better defini-tion of what the end state is going to be for bank capital,” says William Chalm-ers, global co-head of financial institu-tions group at Morgan Stanley.

“On the back of that, banks have been much more engaged with mov-ing towards their ultimate capital need,

beyond equity. We have also seen the remarkable development of a market for loss-absorbing instruments, par-ticularly AT1. Five years ago there were a lot of cynics as to whether the market for that product would ever really open up. Here we are now and people are making it one of the core pillars of their capital base.”

With the regulatory capital structure now all but settled and with the vast majority of institutions given a clean bill of health in the European Cen-tral Bank’s stress tests late last year, banks can start to look forward to a time when the capital ratios slide can assume a less prominent role in their investor presentations.

Concern for the collective creditwor-thiness of the European banking sector in the last few years has eased, helped by deleveraging and with another €85bn plus of AT1 and tier two issu-ance in 2014, according to Morgan Stanley figures.

It was not so long ago that investors drew much comfort from rapidly ris-ing capital buffers, pushing the com-mon equity tier one ratio to page one of many quarterly results presentations in 2011 and 2012, and setting Europe on a path to having nine institutions with a total capital ratio of 20% or more by the first quarter of this year (see chart on page 3).

“Banks that previously prided them-selves on premium capital levels are now accepting that they should ‘just’ be managed to regulatory expecta-tions,” says Chalmers. “They are now operating in line with others as banks are all being brought up to the same level.”

Banks are on schedule with the foundations. Now they have to worry about what the house is going to look like. “Among other things, banks are focused on getting back to being dividend paying stocks,” says Claus Skrumsager, co-head of global capital markets EMEA at Morgan Stanley.

“At some point investors will penal-

Banks have cleaned up and found an investor base for billions in new age loss-absorbing capital, but with regulators putting the finishing touches to the post-crisis framework, there is no shortage of challenges ahead, writes Tom Porter.

Banks desperate to see the final act in post-crisis capital

“Any impression of stability is perhaps a little illusory, and we

are still some time away from seeing

the full picture emerge. We have a

rock solid house built on shifting sands.”

William Chalmers, Morgan Stanley

002-3 Overview.indd 2 06/07/2015 09:00

Bank Capital | July 2015 | 3

OVERVIEW OVERVIEW

ise banks for holding too much capital. The question then is whether you use that capital to invest in more profit-able business or do you give it back to shareholders.

“That is why stock buybacks and dividends are still a regulation deter-mined activity right now. Regula-tors want to see further stability, big-ger cushions, business models fully entrenched and understood and then we will hopefully get back to normality on dividends.”

TLAC tormentThe era of fear and uncertainty may have passed. But the safety measures put in place by regulators have caused a tectonic shift in the mindset of lend-ers. With living wills, bail-in and now TLAC, they have to think first and fore-most about how to pay for their funer-al, rather than simply trying to make money while they are alive.

“As bank capital managers we always think in going concern terms,” says Erik Schotkamp, head of capital man-agement and long term funding at BBVA. “We don’t think about dying, we think about complying at the low-est cost and in the most transparent way we can to lower cost. But that is not necessarily consistent with the goal of thinking about your bank dying and having adequate capital to recapital-ise itself.”

One crucial question is whether bail-ins will be imposed on a multiple or single point of entry basis. This will have a material impact on internation-al banks like BBVA, which will all have to consider whether non-core busi-nesses will remain cost-effective from the capital standpoint.

Some argue this is the goal of regulators — to make the univer-sal bank model that became so loathed in the aftermath of the 2008 crisis too expen-sive for banks to oper-ate, and force lenders to be more region-ally or domestically focused.

It is also difficult to underestimate the impact TLAC is going to have on both bank capital issuance in the next few years and the creditor hierarchy

itself, particularly in Europe.Andrew Gracie, the man in charge of

resolution at the Bank of England, in a speech in December said that TLAC was intended to be “policy neutral for G-SIBs with or without holding com-panies”, as well as neutral in terms of bank structure or resolution strategy.

In practice, it is looking anything but. The US, Swiss and UK banks have a long established holdco-opco struc-ture, and some, such as Credit Suisse, have already ramped up issuance of TLAC eligible holdco senior.

But in continental Europe, where holdcos are expensive and legally chal-lenging to set up, TLAC has forced member states into unilateral action. Germany has drafted a law making all senior unsecured debt TLAC eligi-ble, leading investors to re-price Ger-man banks’ senior paper wider as they digest the new risk. Spain has taken a different approach, with legislation to give banks the option of issuing a new layer of ‘tier three’ capital, which would be labelled senior but contractually bail-inable.

For investors this takes bank capital even further away from the harmoni-sation they have been screaming for since the first AT1 trades were printed. With different solutions being applied across Europe, and with each coun-try having a national regulator whose interpretation of the resolution process could differ wildly to that of its neigh-bours, the time taken on each credit decision is only likely to rise further.

Parallel universeAnd there are some other pretty major plot twists for our protagonists still to negotiate. The Basel Committee on

Banking Supervision is scrutinising banks’ myriad methods for calculating risk-weighted assets and wants them standardised. Add in the fundamental review of the trading book, the leverage ratio and the persistent uncertainty surrounding banks’ Pillar 2 disclosures and it is clear capital requirements are still in their upward arc.

“The Basel risk weight consultation could prove very disruptive for banks’ capital planning,” says Alex Menounos, co-head of EMEA FIG DCM and head of EMEA debt syndicate at Morgan Stanley. “TLAC is currently viewed by many as the final missing link to defin-ing the capital structure, but a change in risk weight methodology could have a profound impact, in particular for banks with large mortgage and corpo-rate/SME portfolios.

“This is a significant potential head-wind for core equity as much as for the rest of the capital structure. In the near term, we may see some banks take a more conservative approach on CET1 by accumulating and building buffers to proactively manage any potential impact.”

In regulatory terms, this is another big year for bank capital. Early esti-mates suggested TLAC and MREL would mean another €500bn of loss-absorbing paper being printed.

Banks have a full range of proven instruments with which to get on with the job. But they are impatient to know what to use, and how much.

“The biggest win for the banks over the next 12 months would be a reali-sation on behalf of regulators that they have done enough and we are now approaching the endgame,” says Chalmers. “Right now, we are in a sort

of parallel universe where aspects of the post-crisis capital regime appear to be getting close to set-tlement, but there are still a number of mov-ing parts, for example risk weights.

“Any impression of stability right now is perhaps a little illu-sory, and we are still some time away from seeing the full picture emerge. We have a rock solid house built on shifting sands.” s

Source: Morgan Stanley

10.5 11.9

10.511.3

10.111.2

12.713.8

10.510.5

11.514.1

10.213.8

14.115.6

16.613.6

13.418.6

20.521.1

1.0 0.0 0.8 0.0 2.4 1.7 0.00.8

0.0 0.81.8

2.1

3.1

2.70.4

2.02.3

2.4 3.5

1.4

2.63.7

1.2 1.4 2.8 2.9 1.92.8 3.1

1.2

5.35.4

3.7

2.26.5

3.55.6

2.82.3

5.35.7

5.93.1

3.3

12.7 13.3 14.1 14.2 14.315.7 15.815.8

15.816.7 17

18.419.8 20 20.2

20.3 21.1 21.322.6

25.926.2

28.2

0

5

10

15

20

25

30 %

BNP

Santander

UniCre

d

CMZBK

SocGen

HSBC

BBVA DB

Erste

StanChart

RBS

Danske

CASA CS

ABN

Nordea

SEB

Rabobank

Lloyds

UBS

Swedbank SHB

CET1 Tier 1 Tier 2 CET1 FLT

Selected European banks’ capital ratios, targets and leverage ratios

002-3 Overview.indd 3 06/07/2015 09:00

4 | July 2015 | Bank Capital

THE REGULATORS

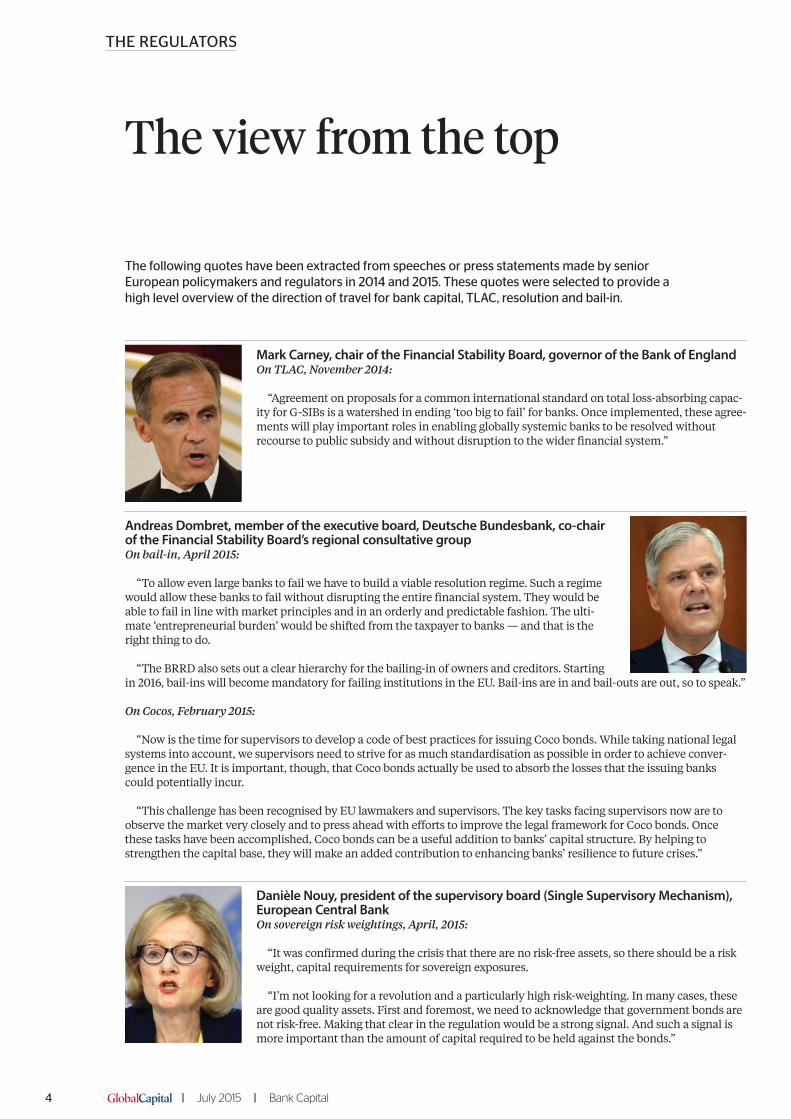

Mark Carney, chair of the Financial Stability Board, governor of the Bank of EnglandOn TLAC, November 2014:

“Agreement on proposals for a common international standard on total loss-absorbing capac-ity for G-SIBs is a watershed in ending ‘too big to fail’ for banks. Once implemented, these agree-ments will play important roles in enabling globally systemic banks to be resolved without recourse to public subsidy and without disruption to the wider financial system.”

Andreas Dombret, member of the executive board, Deutsche Bundesbank, co-chair of the Financial Stability Board’s regional consultative group On bail-in, April 2015:

“To allow even large banks to fail we have to build a viable resolution regime. Such a regime would allow these banks to fail without disrupting the entire financial system. They would be able to fail in line with market principles and in an orderly and predictable fashion. The ulti-mate ‘entrepreneurial burden’ would be shifted from the taxpayer to banks — and that is the right thing to do.

“The BRRD also sets out a clear hierarchy for the bailing-in of owners and creditors. Starting in 2016, bail-ins will become mandatory for failing institutions in the EU. Bail-ins are in and bail-outs are out, so to speak.”

On Cocos, February 2015:

“Now is the time for supervisors to develop a code of best practices for issuing Coco bonds. While taking national legal systems into account, we supervisors need to strive for as much standardisation as possible in order to achieve conver-gence in the EU. It is important, though, that Coco bonds actually be used to absorb the losses that the issuing banks could potentially incur.

“This challenge has been recognised by EU lawmakers and supervisors. The key tasks facing supervisors now are to observe the market very closely and to press ahead with efforts to improve the legal framework for Coco bonds. Once these tasks have been accomplished, Coco bonds can be a useful addition to banks’ capital structure. By helping to strengthen the capital base, they will make an added contribution to enhancing banks’ resilience to future crises.”

Danièle Nouy, president of the supervisory board (Single Supervisory Mechanism), European Central BankOn sovereign risk weightings, April, 2015:

“It was confirmed during the crisis that there are no risk-free assets, so there should be a risk weight, capital requirements for sovereign exposures.

“I’m not looking for a revolution and a particularly high risk-weighting. In many cases, these are good quality assets. First and foremost, we need to acknowledge that government bonds are not risk-free. Making that clear in the regulation would be a strong signal. And such a signal is more important than the amount of capital required to be held against the bonds.”

The following quotes have been extracted from speeches or press statements made by senior European policymakers and regulators in 2014 and 2015. These quotes were selected to provide a high level overview of the direction of travel for bank capital, TLAC, resolution and bail-in.

The view from the top

Bank Capital | July 2015 | 5

THE REGULATORS

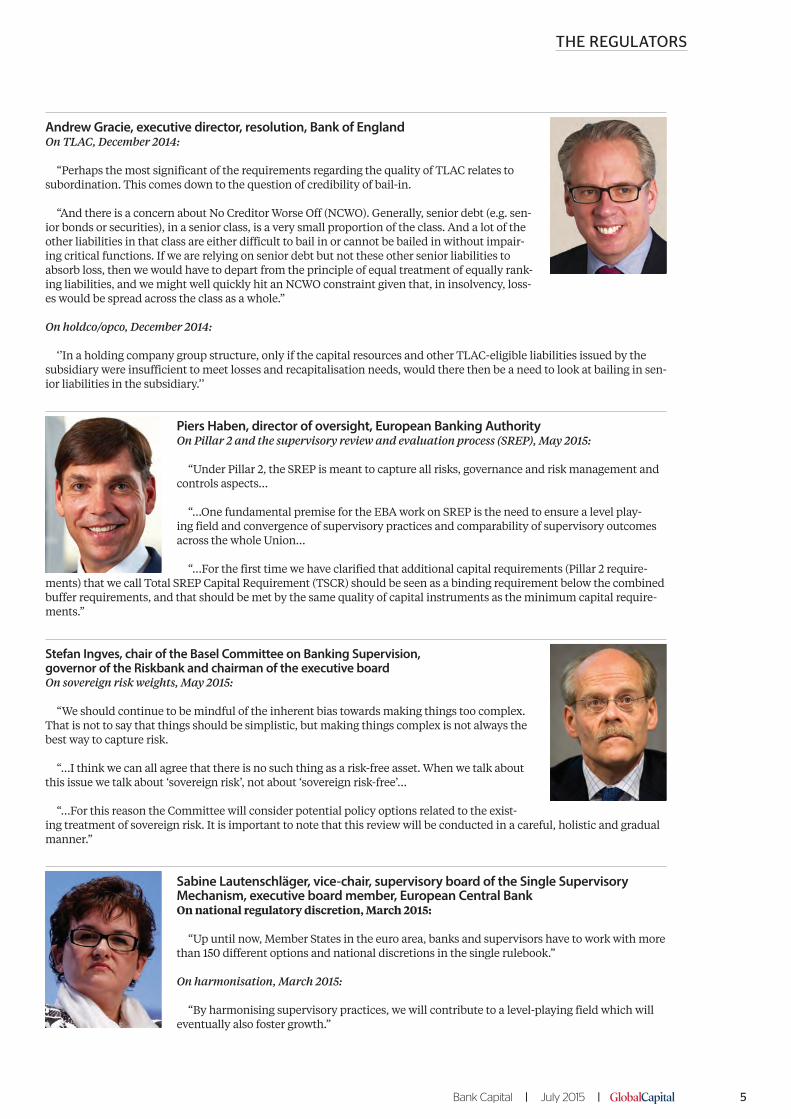

Andrew Gracie, executive director, resolution, Bank of EnglandOn TLAC, December 2014:

“Perhaps the most significant of the requirements regarding the quality of TLAC relates to subordination. This comes down to the question of credibility of bail-in.

“And there is a concern about No Creditor Worse Off (NCWO). Generally, senior debt (e.g. sen-ior bonds or securities), in a senior class, is a very small proportion of the class. And a lot of the other liabilities in that class are either difficult to bail in or cannot be bailed in without impair-ing critical functions. If we are relying on senior debt but not these other senior liabilities to absorb loss, then we would have to depart from the principle of equal treatment of equally rank-ing liabilities, and we might well quickly hit an NCWO constraint given that, in insolvency, loss-es would be spread across the class as a whole.”

On holdco/opco, December 2014:

‘’In a holding company group structure, only if the capital resources and other TLAC-eligible liabilities issued by the subsidiary were insufficient to meet losses and recapitalisation needs, would there then be a need to look at bailing in sen-ior liabilities in the subsidiary.’’

Piers Haben, director of oversight, European Banking AuthorityOn Pillar 2 and the supervisory review and evaluation process (SREP), May 2015:

“Under Pillar 2, the SREP is meant to capture all risks, governance and risk management and controls aspects…

“…One fundamental premise for the EBA work on SREP is the need to ensure a level play-ing field and convergence of supervisory practices and comparability of supervisory outcomes across the whole Union…

“…For the first time we have clarified that additional capital requirements (Pillar 2 require-ments) that we call Total SREP Capital Requirement (TSCR) should be seen as a binding requirement below the combined buffer requirements, and that should be met by the same quality of capital instruments as the minimum capital require-ments.”

Stefan Ingves, chair of the Basel Committee on Banking Supervision, governor of the Riskbank and chairman of the executive boardOn sovereign risk weights, May 2015:

“We should continue to be mindful of the inherent bias towards making things too complex. That is not to say that things should be simplistic, but making things complex is not always the best way to capture risk.

“…I think we can all agree that there is no such thing as a risk-free asset. When we talk about this issue we talk about ‘sovereign risk’, not about ‘sovereign risk-free’…

“…For this reason the Committee will consider potential policy options related to the exist-ing treatment of sovereign risk. It is important to note that this review will be conducted in a careful, holistic and gradual manner.”

Sabine Lautenschläger, vice-chair, supervisory board of the Single Supervisory Mechanism, executive board member, European Central BankOn national regulatory discretion, March 2015:

“Up until now, Member States in the euro area, banks and supervisors have to work with more than 150 different options and national discretions in the single rulebook.”

On harmonisation, March 2015:

“By harmonising supervisory practices, we will contribute to a level-playing field which will eventually also foster growth.”

6 | July 2015 | Bank Capital

TLAC / MREL TLAC / MREL

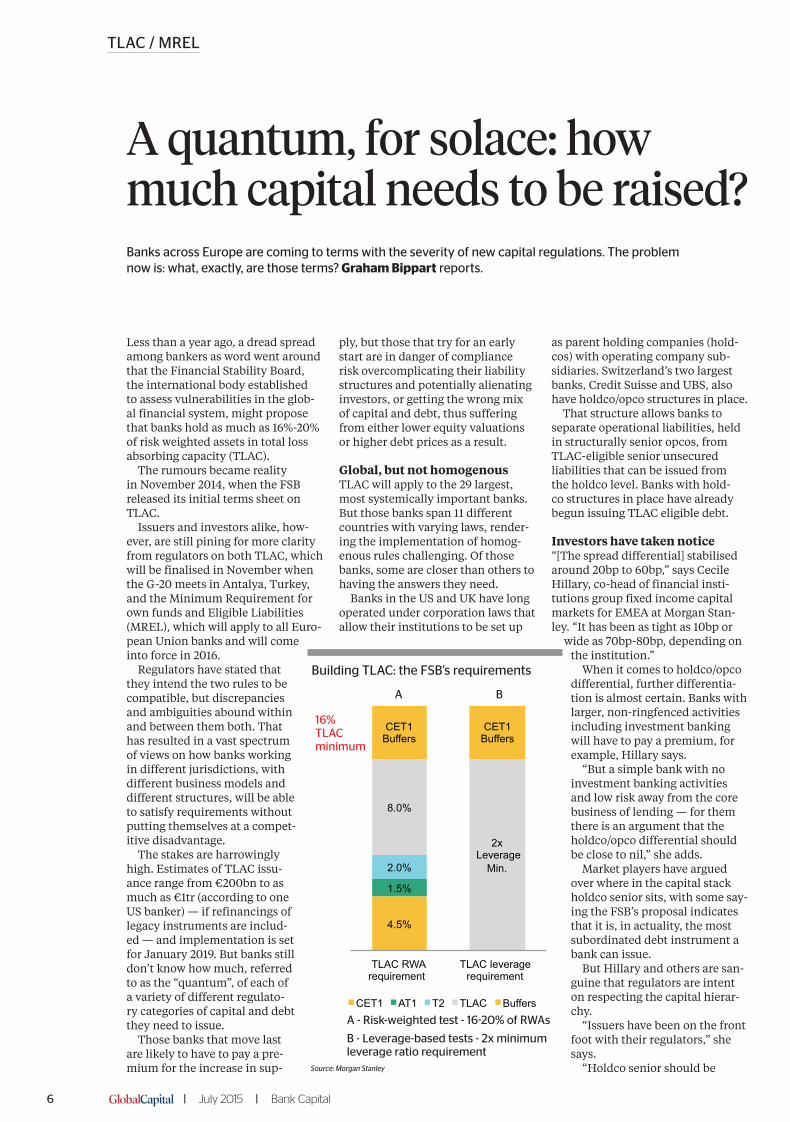

Less than a year ago, a dread spread among bankers as word went around that the Financial Stability Board, the international body established to assess vulnerabilities in the glob-al financial system, might propose that banks hold as much as 16%-20% of risk weighted assets in total loss absorbing capacity (TLAC).

The rumours became reality in November 2014, when the FSB released its initial terms sheet on TLAC.

Issuers and investors alike, how-ever, are still pining for more clarity from regulators on both TLAC, which will be finalised in November when the G-20 meets in Antalya, Turkey, and the Minimum Requirement for own funds and Eligible Liabilities (MREL), which will apply to all Euro-pean Union banks and will come into force in 2016.

Regulators have stated that they intend the two rules to be compatible, but discrepancies and ambiguities abound within and between them both. That has resulted in a vast spectrum of views on how banks working in different jurisdictions, with different business models and different structures, will be able to satisfy requirements without putting themselves at a compet-itive disadvantage.

The stakes are harrowingly high. Estimates of TLAC issu-ance range from €200bn to as much as €1tr (according to one US banker) — if refinancings of legacy instruments are includ-ed — and implementation is set for January 2019. But banks still don’t know how much, referred to as the “quantum”, of each of a variety of different regulato-ry categories of capital and debt they need to issue.

Those banks that move last are likely to have to pay a pre-mium for the increase in sup-

ply, but those that try for an early start are in danger of compliance risk overcomplicating their liability structures and potentially alienating investors, or getting the wrong mix of capital and debt, thus suffering from either lower equity valuations or higher debt prices as a result.

Global, but not homogenousTLAC will apply to the 29 largest, most systemically important banks. But those banks span 11 different countries with varying laws, render-ing the implementation of homog-enous rules challenging. Of those banks, some are closer than others to having the answers they need.

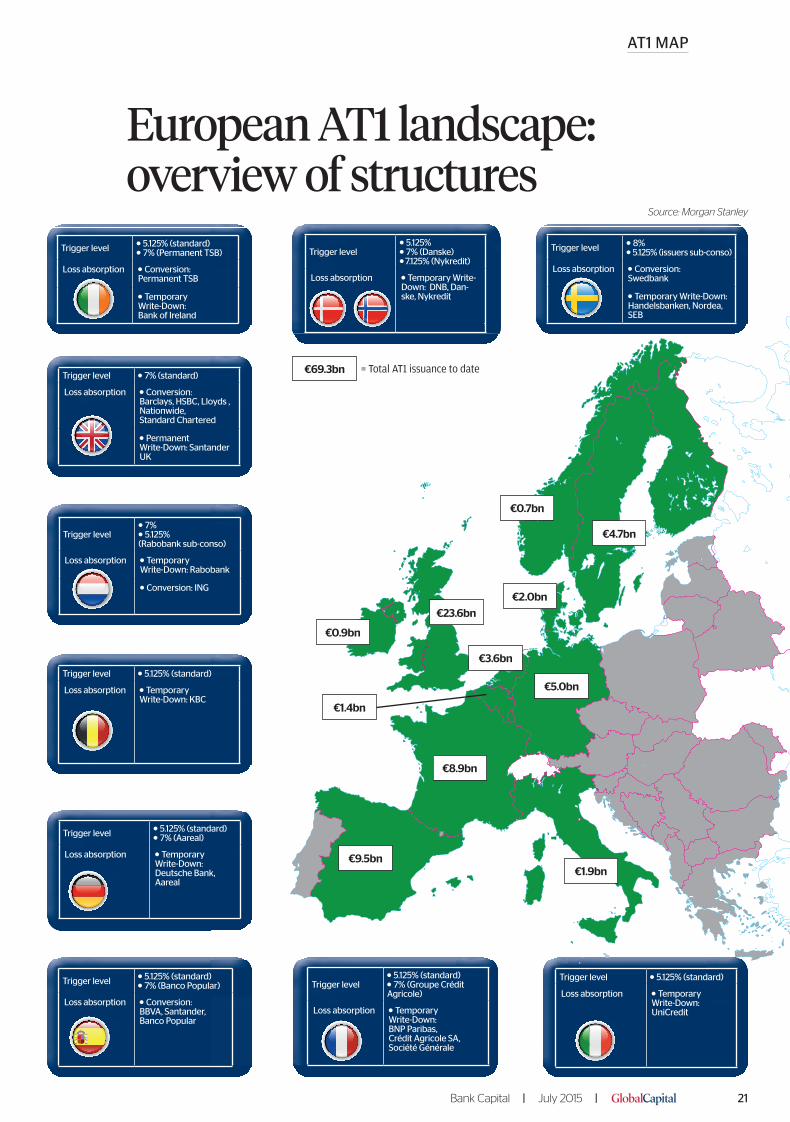

Banks in the US and UK have long operated under corporation laws that allow their institutions to be set up

as parent holding companies (hold-cos) with operating company sub-sidiaries. Switzerland’s two largest banks, Credit Suisse and UBS, also have holdco/opco structures in place.

That structure allows banks to separate operational liabilities, held in structurally senior opcos, from TLAC-eligible senior unsecured liabilities that can be issued from the holdco level. Banks with hold-co structures in place have already begun issuing TLAC eligible debt.

Investors have taken notice“[The spread differential] stabilised around 20bp to 60bp,” says Cecile Hillary, co-head of financial insti-tutions group fixed income capital markets for EMEA at Morgan Stan-ley. “It has been as tight as 10bp or

wide as 70bp-80bp, depending on the institution.”

When it comes to holdco/opco differential, further differentia-tion is almost certain. Banks with larger, non-ringfenced activities including investment banking will have to pay a premium, for example, Hillary says.

“But a simple bank with no investment banking activities and low risk away from the core business of lending — for them there is an argument that the holdco/opco differential should be close to nil,” she adds.

Market players have argued over where in the capital stack holdco senior sits, with some say-ing the FSB’s proposal indicates that it is, in actuality, the most subordinated debt instrument a bank can issue.

But Hillary and others are san-guine that regulators are intent on respecting the capital hierar-chy.

“Issuers have been on the front foot with their regulators,” she says.

“Holdco senior should be

Banks across Europe are coming to terms with the severity of new capital regulations. The problem now is: what, exactly, are those terms? Graham Bippart reports.

A quantum, for solace: how much capital needs to be raised?

4.5%

1.5%

2.0%

8.0%

2x Leverage

Min.

CET1 Buffers

CET1 Buffers

TLAC RWA requirement

TLAC leverage requirement

CET1 AT1 T2 TLAC Buffers

16%TLACminimum

A B

A - Risk-weighted test - 16-20% of RWAs

B - Leverage-based tests - 2x minimum leverage ratio requirement

Building TLAC: the FSB’s requirements

Source: Morgan Stanley

006-008 TLAC .indd 6 06/07/2015 09:02

Bank Capital | July 2015 | 7

TLAC / MREL TLAC / MREL

downstreamed as TLAC capacity. And capital instruments, whether at the holdco or opco level, would be bailed in before senior instruments.”

With that uncertainly seeming-ly behind them, banks with holdco structures — and investors in those banks — should be well positioned to meet TLAC requirements.

A ‘going concern’ for European banksBut banks on the continent have bemoaned TLAC’s “Anglo-Saxon” bias, illustrated in the exclusion of operational liabilities, like deriva-tives and corporate deposits, from bail-in eligibility.

Most European banks are struc-tured as opcos, their senior unse-cured liabilities ranking pari passu with operational liabilities. And since the most recent TLAC proposal only recognises as eligible opco sen-ior equal to a maximum 2.5% of risk weighted assets (RWAs), the options for compliance look expensive.

“Effectively, we are being told to issue tier two, which is a massive cost,” said Waleed El-Amir, head of group strategic funding at UniCredit, at an industry conference in June. In its February reply to the FSB’s con-sultation on TLAC, the bank said that under the proposal, Europe-an banks would have to deleverage, form holdcos or issue “gone concern” subordinated debt like tier two, all of which would come with the risk of “seriously jeopardising [banks’] capacity to finance the economy” due to their expense. It would, ironi-cally, also force largely deposit fund-ed institutions such as Holland’s ING, to increase leverage.

Germany’s government became the first to try to tackle the prob-lem in March, when it introduced a bill to statutorily subordinate sen-ior unsecured debt from operational liabilities. That would allow German banks — of which Deutsche Bank is the only Global Systemically Impor-tant Bank (G-SIB) — to use existing senior unsecured debt to meet TLAC requirements.

It could also help resolution authorities to resolve smaller banks without falling foul of the EU bank recovery and resolution directive’s No Creditor Worse Off principle, which guarantees that, in a resolu-tion, no creditor would be worse off

than if the bank had been liqui-dated. Under the statute, senior unsecured holders could no long-er claim they are pari passu with secured creditors.

“There’s a lot of interest in Europe to have a clean statutory approach like the one we are likely to have in Germany,” says Khalid Krim, head of European capital solutions at Morgan Stanley.

France, Spain and Italy, which have similarly strict corporation laws making it near impossible for banks to set up holding companies, are likely to follow in Germany’s footsteps if the approach proves suc-cessful.

But European banks in other juris-dictions are likely to contractually subordinate senior debt to opera-tional liabilities in their deal docu-ments.

Which means that European inves-tors, already relatively bogged down by the differences in contract law between European jurisdictions, are going to have to navigate an increas-ingly complex landscape for bank investment.

“It’s very surprising that [Germa-ny] took the step to change the law themselves and come up with their own solution for TLAC. I don’t think that was particularly helpful in terms of harmonising things in the mar-ket,” says James MacDonald, senior portfolio manager at BlueBay Asset Management.

Too much to manage (TMTM)?The complexity can only get worse. Beyond the holdco/opco approach taken by US, UK and Swiss banks, the statutory approach being pur-sued by Germany and contractual bail-in, TLAC provides for what the market has termed “tier three” — subordinated debt that sits between tier two and senior unsecured, mak-ing it a less costly option than tier two.

Many European banks are looking into the possibility, says Krim. Dan-ske Bank was reported in December to be thinking about tier three issu-ance, for example. The problem for some European banks is that many existing tier twos include contractual clauses that restrict issuers from fur-ther subordinating them after issu-ance.

“We have spent a lot of time with

many banks in Europe, doing due diligence on the existing documen-tation they have and looking at what kind of changes they can make today when they issue tier two, so that those instruments don’t carry restrictions or limitations for too long,” says Krim.

Some banks have found that they have the flexibility to issue tier three, others have already begun to make changes to their EMTN programmes so that new tier two issuance would provide them with the flexibility to layer in less subordinated junior debt, Krim says.

“Legacy tier two is grandfathered at the moment, but it is losing its CRD IV credit year by year. So, towards the end of the implementa-tion period, some banks with out-standing legacy hybrid tier one and tier two debt will be looking at liabil-ity management exercises to make their TLAC capital structures more efficient.

“If you’re a bank that will be in the market offering tier two in 2016 and 2017, this is the thing to think about right now,” Krim says.

Acronymic Agony —and then there’s MRELNational authorities will be charged with defining the Pillar 2, or non-binding, loss absorbing capital requirements on a bank by bank basis, and though there is little clar-ity on what will be needed to comply with those idiosyncratic standards, the rule will come into force in 2016, though with a phase-in period last-ing until 2020.

MREL’s known terms differ from TLAC in some major respects.

TLAC requires eligible senior unsecured liabilities to be subor-dinated — contractually, statuto-rily or structurally — to be bail-ina-ble and only recognises senior up to

“Between now and November there

will be an incredible amount of jockeying,

lobbying and push-ing in order to try and get a solution

that works on a local basis”

Waleed El-Amir, UniCredit

006-008 TLAC .indd 7 06/07/2015 09:02

8 | July 2015 | Bank Capital

TLAC / MREL

2.5% of RWAs, while MREL puts no limit or stipulation on eligible sen-ior unsecured. TLAC requirements exclude common equity tier one buffers for the RWA measure, while MREL includes them, as well as Pil-lar 2. Both TLAC and MREL can be expressed as a percentage of RWAs or as a multiple of leverage, but G-SIBs and Domestic Systemically Important Banks must hold 8% of their total liabilities and own funds in order to access resolution funds.

And while TLAC requires bank lev-erage ratios to be two times the Basel III minimum of 3% plus additional buffers, MREL requires it to be two times the “relevant” leverage ratio set by national regulators.

All of this spells confusion for bankers and investors alike. And though TLAC was initially thought to be the most onerous of the two, even that remains unclear.

“I’m not sure the TLAC require-ment will be more binding,” says Robert Kendrick, bank credit analyst at Schroders. “You may end up with more MREL.”

When Andrew Gracie, executive director of resolution at the Bank of England, gave a speech on the FSB’s thinking behind TLAC and its rela-tionship to MREL in December of last year, he said: “Our view is that there is no question about their com-patibility.”

But market participants are less clear that that is the case. The good news, Krim says, is that the indus-try is expecting the final versions of both rules to converge in important ways.

“When we speak to FSB repre-sentatives in Europe or to the EBA and European regulators, there is a strong desire to see the two converge, so that what applies to G-SIBs would apply to other European banks,” Krim says.

“I do think there will be a conver-gence of the TLAC and MREL pro-posals,” he says. “The EBA and the FSB have been working together to ensure this happens.”

Krim says that a broadening of TLAC’s eligibility requirements for senior is likely, as well as perhaps an increase in the 2.5% cap, to be more in line with MREL. And MREL’s lev-erage ratio and RWA tests are like-ly to converge towards the current TLAC proposal.

“The leverage ratio requirement will stay, since it’s seen by regula-tors as an alternative proxy to the risk weight calculations,” Krim says. With concerns from regu-lators over the disparity of risk weight calculations across banks, the leverage ratio will remain a focus.

It should also be a focus for investors. With the European Cen-tral Bank taking over as single supervisor of the eurozone’s banks — with direct responsibility for the 120 most significant groups — there is an expectation that internal RWA calculations will become more har-monised. Until then, the leverage ratio is key.

“In the interim, it makes complete sense for investors to look into lever-age ratios, especially because, at the end of the day, if a bank is going into insolvency or into resolution, the RWA [measure] is going to be noth-ing,” says El-Amir. “It’s actually the underlying liability that is going to be bailed in. That’s actually the value the regulator’s going to look at.”

Issuers, though, will still have to deal with both RWA measures and leverage ratio requirements, both yet to be set in stone. “The first step is that the regulators define and design the requirements. The second step is that banks raise the indicated quan-tum,” Krim says.

A quantum, for solaceAnd here is where the real balancing act begins. With TLAC and MREL, the distinction between funding and capital has all but disappeared.

“It’s completely changing the way issuers are thinking about capital versus funding,” Hillary says.

For banks, the issue will be large-ly one of satisfying senior investors that they are sufficiently buffered against bail-in, while making sure equity investors aren’t shouldering excess cost.

Once there is clarity on the quan-tum in 2016 or 2017, Krim says, “mar-ket participants will look at whether there is a benefit, i.e.: are equity and debt investors giving the banks cred-it for filling the regulatory demands? Is a bank’s response to its total capi-tal strategy and its answer to MREL well received by the market? Or should it adjust how it’s doing it?”

Equity investors aren’t now giving

credit to banks with higher capital ratios than their peers, Krim says.

“At the moment, we need to see how equity investors, on the one side, and debt investors, on the other, are either giving brownie points or penalising banks for going one way or the other. It’s too early to tell what the right answer is, but we don’t yet see anything in credit spreads or share prices that is linked to these regulatory developments.”

That may be because there sim-ply isn’t enough detail, yet. Investors could begin making discrepancies across banks when they have an idea of how loss given defaults compare across different capital strategies, something the vast majority of banks are still working on.

“There’s massive uncertainty,” says UniCredit’s El-Amir.

“Between now and November, when the final term [TLAC] sheet is expected to come out, there will be an incredible amount of jockeying, lobbying and pushing in order to try and get a solution that works on a local basis” across different jurisdic-tions in Europe, he says.

For that reason, Hillary says there should be no reason for banks to rush to begin filling their — as yet unknown — requirements.

“There is no rush to fill TLAC capacity by any specific date other than the 2019 deadline,” Hillary says.

Indeed, front-running final regu-lations could prove costly, since the right mix of debt and capital is going to be crucial to efficiency.

“What’s important is for banks to communicate to their investors what their capital and TLAC targets are when the numbers are clearer,” she says.

Whatever the outcome of the final rules, one thing is already very clear. The job of the bank treasurer has never been so complex. s

“There is no rush to fill TLAC capacity

by any specific date other than the 2019

deadline”

Cecile Hillary, Morgan Stanley

006-008 TLAC .indd 8 06/07/2015 09:02

Bank Capital 9

Bank Capital Issuers’ Roundtable

: Where do we stand in terms of the regulatory landscape at the moment? With TLAC and MREL are we seeing the final pieces of the post-crisis capital structure, or does more need to be done to allow issuers to finalise their capital strategies?

Khalid Krim, Morgan Stanley: If I look at where we are now in June 2015 we’re still waiting for some clarity on the regulatory side coming from the European Banking Authority on the minimum requirement eligible liabilities (MREL), and from the Financial Stability Board on total loss-absorbing capacity (TLAC). When we talk to banks and investors around Europe there is a high level of understanding of the direction of travel, though we’re missing some key details and clarification.

But clearly we have issuers now working on their total capital strategy. They are able to plan an issue, be it tier one or tier two capital, in the market and start to communicate to the investor community how the

resolution regime will work in their country, and how they think going forward they should be perceived as a bank.

2015 will be a year where we will continue to see banks implementing the CRD IV capital plan in tier one and tier two, and where we see more work being done to get familiar with the requests and expectations from the new supervisor, the ECB acting as Single Supervisory Mechanism (SSM).

The final pieces and the final judgment need to come by year-end but I think we’ve made significant progress.

: Erik, Rogier, could you give us an issuer’s view? With things as they are at the moment, how easy is it for you to get on with implementing a total capital strategy?

Rogier Everwijn, Rabobank: Rabobank has already been active in implementing the total capital strategy

Participants in the roundtable were:Leopold Bian, bank analyst, BlackRock

Rogier Everwijn, head of capital and secured products, Rabobank

Scott Forrest, head of capital strategy, Royal Bank of Scotland

Khalid Krim, head of capital solutions, EMEA, Morgan Stanley

Matthieu Loriferne, senior vice president of credit research, Pimco Europe

Alex Menounos, head of EMEA syndicate and co-head of EMEA FIG DCM, Morgan Stanley

Vishal Savadia, director, head of capital issuance and struc-turing, Lloyds Banking Group

Erik Schotkamp, head of capital management and long term funding, BBVA

Tom Porter, moderator, GlobalCapital

Issuers seek best solution as regulators move the goalposts

European banks have rolled up their sleeves and got on with the job of issuing loss-absorbing instruments to meet the new capital demands of Basel III, with another €80bn of capital printed across additional tier one (AT1) and tier two in 2014. AT1 accounted for 48% of capital volume in 2014 as banks made strides towards filling their 1.5% of risk weighted assets bucket. Still more banks have made debuts in the AT1 market in 2015 and many early issuers are expected to return to take advantage of cheaper pricing later this year.

Just as the post-crisis capital framework was settling down, the Financial Stability Board unveiled proposals to require banks to hold a new quantum of loss-absorbing debt equivalent to between 16% and 20% of RWAs. For issuers, the rules have been changed in the middle of the game. European jurisdictions have already revealed divergent plans to help their banks comply, and until the rules are finalised in November, issuers remain in the dark as to what they will have to issue by 2019.

Issuers and investors gathered at Morgan Stanley’s offices in London in June 2015 to discuss how to navigate the much altered route to capital compliance.

009-018 Issuers Roundtable.indd 9 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

10 Bank Capital

since 2012 in preparing for the Bank Recovery and Resolution Directive (BRRD) when the crisis management directive was proposed — especially for the bail-in tool, because for us this was the most threatening part of the whole resolution package.

We started readying ourselves for operating at a total capital ratio of 20% initially, and our goal was to have that by year-end 2016. Since we were already above 21% by year end 2014 and with the TLAC proposals we have revised our target for year-end 2016 to mid-20s%. We will wait for the TLAC results to come out by the end of this year and then we can reset our target again for 2019, the introduction date for TLAC.

Erik Schotkamp, BBVA: If you think just about products like additional tier one, back in 2011 I remember sitting in this same sort of format with people from the EBA and banks were not believing this could fly.

That has now become a standardised product with a standardised term sheet. That took us four years. If I think about TLAC — and that for me is the next thing for us in terms of how we’re going to be managing this — that will take a lot of technical standards, a lot more than a CRD IV-compliant product because you need to talk about co-operation, implementation of BRRD laws in countries outside of the G20, convergence of regulatory standards; this is going to take a long time.

It’s a big thing for investors, talking to them, not knowing necessarily where they are or where they’re going to be or how they need to think about pricing and how this is all going to work.

I sense that Pillar 1, the base set core capital, tier two, AT1, most people know what they look like. There’s uncertainty on risk-weighted asset density, in the south of Europe we’re worried about Deferred Tax Assets and in the north of Europe we are worried about their mortgages in terms of risk-weighted assets.

But for me the really big thing going forward is how is TLAC going to turn out and what will I have to plan for. You can talk about material volumes but it’s how you have to fulfil it and what sort of regulatory co-ordination you need, which lacks a lot of clarity.

: What are investors’ main uncertainties around this new regulation, and have banks been responding in the right way?

Matthieu Loriferne, Pimco: We have more certainty at the bottom of the capital structure, be it common equity tier one (CET1) requirements or the various buffers. Everything is not clear but, as Khalid says, we have better visibility today.

If you move up the capital structure actually this is where the ambiguity lies and in particular regarding TLAC.

For us it’s more difficult to understand, not necessarily the target but how the banks are going to fulfil those requirements; what instruments they’re going to issue. Most important in our view is what would be the rights of bondholders and how are they going to be treated. Pimco fully understands the risks associated with investing in the new resolution environment, including that of being bailed in at the senior part of the capital structure. Understanding and recognising when those losses will happen and how the bondholders will be treated is what is most important to investors.

Leopold Bian, BlackRock: I agree that certainty

definitely has been a factor here at the bottom of the capital structure. You’ve seen that in the issuance of AT1 compared to tier two this year. There’s a big difference. Issuers aren’t going to rush out to print tier two until they have more clarity.

One thing I would add that still gives me a little bit of uncertainty is the SSM. I want to understand a little bit better how the whole SREP review process works and the interaction between the SSM and issuers.

From my perspective it feels that there’s not much that the SSM wants banks to disclose. Obviously you have some disclosure in a few countries but that’s something that still remains a lot in the dark. This is something I want more clarity on, on top obviously of TLAC and MREL, which depending on the issuer one should be more important than the other, but in any case it seems that we’ll get more clarity on this by year end.

Krim, Morgan Stanley: The SSM is trying to analyse and make sure that if there’s any Pillar 2 disclosure given to the market and to the investor community by banks, it is something which is methodology analysed. In the UK we had some disclosures and I’m sure Scott or Vish can comment on that in the context of the UK, their approach to Pillar 2a and Pillar 2b. In Europe we are behind and I think we still need to see what comes out in terms of a harmonised framework before any disclosure is made.

It’s only a couple of months that the SSM has been in place. Often when we speak to issuers they tell us they need to get to know the supervisor and understand the requirements. It’s a new supervisor so I think it will take a bit of time before we have this piece of information and clarity into the market.

: Scott, Vish, can you add anything on the Pillar 2a requirements in the UK?

Scott Forrest, Royal Bank of Scotland: Fundamentally from an issuer’s perspective if you are tasked with raising capital, raising secured funding or unsecured funding in the debt capital markets then you want to ensure that the dialogue you’re providing your investor base is the right type of information.

In that context the Pillar 2a disclosures are a welcome advance in the UK. From a bank’s perspective what you don’t want to be is an outlier. You want to ensure that in terms of disclosure you’re there as part of a pack. Otherwise from a markets perspective there can be some idiosyncrasies which will start to creep in.

Khalid Krim MORGAN STANLEY

009-018 Issuers Roundtable.indd 10 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

Bank Capital 11

So as long as the disclosure’s done on a consistent, methodical basis, then it’s a fundamentally good thing, and one that we’re supportive of.

Vishal Savadia, Lloyds: I completely agree. Transparency is increasingly important for all issuers, particularly as we engage in our investor dialogue. Whilst the UK has been a front mover in terms of framework for Pillar 2 and disclosure provided by banks, what is clearly visible is that there continues to be significant differences in the framework between jurisdictions, either coming through SREP or some of the Pillar 2 requirements in other parts of Europe.

Those differences are becoming more apparent, which unfortunately again moves us away from the objective of trying to harmonise the regulatory framework which was, if we think back, one of the goals of Basel III. Its early form was a degree of harmonisation from which we seem to be moving away.

But at the same time where banks do have the ability to be transparent and provide that additional investor disclosure, that should be regarded as a positive step.

: Is this one of the things that investors are really pushing you for at the moment?

Savadia, Lloyds: It’s more that, as Mathieu pointed out, conceptually we know where we are and where we’re going in terms of the regulatory capital framework, we know the components of the capital stack and the regulatory objectives to migrate towards a TLAC/MREL framework. We all know the direction of travel, however calibration of the final framework is obviously the very important next step.

Additionally, how the regulatory framework will be applied is key. We have to remember, the purpose of items like TLAC/MREL is to try to improve the ability to stabilise a bank facing a severe stress over a weekend. This raises important questions, such as what is the subordination hierarchy, how might the different liability classes be treated in a stress scenario. It is items like this that we are getting more visibility of through regulatory dialogue but not necessarily through actual framework as yet. This is increasingly important and something the disclosure investors are requesting.

Alex Menounos, Morgan Stanley: Not so long ago we held a similar roundtable where we debated whether Additional Tier 1 would even work for some real money investors and what the capacity for such an instrument would be. Yes, we still face several headwinds with respect to the regulatory framework, the timelines and with respect to calibration, but fundamentally we know that we have the tools available to build the capital structure.

It is comforting to be in a position where we’ve seen a significant amount of the capital required already issued. Most jurisdictions have seen supply, and while some banks have yet to issue, they should take comfort in the fact that the market is there for them. I think it is important to acknowledge how far we’ve come.

Bail-in, MREL, TLAC are all big themes. I am not convinced there will be a harmonised solution across Europe. What we may eventually see is a mix of strategies, with some jurisdictions lobbying hard for a ‘German proposal’ approach, while others adopting a holdco senior or even a ‘Tier 3’ approach. We may even see different approaches within the same jurisdiction, as

some may favour issuing more own funds to fill TLAC requirements, while others explore potential efficiencies in creating a new bail-inable asset class.

: What are some of the other headwinds? TLAC is the most pressing issue but what’s next on the agenda, risk weights?

Menounos, Morgan Stanley: The Basel consultation on risk weights in my mind could be the next big topic.

Everwijn, Rabobank: I agree with you on the Basel IV proposals. At one end you had the improved quantity and quality of capital Basel III proposals, followed by BRRD basically avoiding taxpayers bailing out banks followed by TLAC — recapitalisation should be done by the buffers a bank is holding themselves resulting in elevated capital ratios. And that’s all fine if you have time to build up your ratios, a phasing in would be welcomed.

But if at the same time you are confronted with the asset side of the balance sheet, with risk weights pushed further north by basically compressing your total capital ratios, it makes managing capital ratios life really difficult.

Loriferne, Pimco: Before we move into Basel IV and risk weights there is another very important topic to discuss. It would be good to harmonise the definition of the CET1 ratio which still varies across different European jurisdictions. That is one of the key agenda items of Danièle Nouy, who chairs the SSM. She is currently working on harmonising and removing some of the national discretions. To me as an investor it’s a concern that at this stage of the regulatory agenda, the CET1 ratio from one bank might differ materially from another one despite being regulated by the same entity so before we get into the risk weight discussion, which obviously will take an enormous amount of time, it would be good to remove some of the biggest differences stemming from national discretions across Europe.

Bian, BlackRock: I totally agree with Alex that a lot has been done and if you compare, for example, what has been done in the banking space to the insurance space on the regulatory front, banks are way ahead. In the insurance space, Solvency II comes next year, and insurance companies are still submitting internal models for approval and they don’t know if they’re going to get approved or not. The

Rogier Everwijn RABOBANK

009-018 Issuers Roundtable.indd 11 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

12 Bank Capital

implementation of Basel III and CRD IV seems very smooth compared to that.

Obviously there are a lot of moving parts in the regulatory landscape, but let me touch upon the point of RWAs. It’s absolutely fair to worry about it from an issuer perspective but investors should worry about it too. It’s crazy to think that AT1 securities for example have MDA or loss triggers that are reliant on a ratio whose denominator is going to change.

It’s very hard to look at Pillar 3 disclosures and see which banks are better prepared or which banks will suffer more from the RWA reviews that are being conducted. You can have an idea but you don’t know the quantum and that can be a very meaningful factor when thinking about what capital ratios will be in a year or two years’ time.

Forrest, RBS: But I think the other element from the UK context is ICB and how that will interplay with other regulations. You’re going to look at two separate entities, one of which would be ringfenced and one of which would be non-ringfenced as well. So all of these things coming together all at the same time do present a number of challenges in terms of how you’re going to solve for your capital position, and how you’re going to solve for your TLAC position, when there’re still a number of unknown variables in the equation.

Savadia, Lloyds: Before we get to the proposed changes in risk weightings, we’ve yet to see harmonisation of leverage requirements across Europe. The UK has again been a front mover in terms of setting leverage requirements but we’ve yet to see the consultation at the European level. Before we switch focus to the risk weight consultation, which remains very much a work in progress, it is important to get further clarity on items which we’ve been discussing for quite some time.

Krim, Morgan Stanley: We’re all waiting for harmonisation but the starting point is that we have a set of rules that are discussed internationally at FSB and Basel level. When it comes to implementation it can’t be one size fits all. When you look at the TLAC rules and you try and implement them in continental Europe I think it’s very different to trying to do that in the US, the UK or Switzerland. I think what issuers and investors are facing is a diversity in legal regimes across jurisdictions that aren’t enabling us to implement these rules in the same way.

I agree with Mathieu on that point, let’s at least harmonise CET1 before we move on to Basel IV and everything else. What is key is to make sure that we have banks that are adequately capitalised and better supervised. It’s easy to say but in practice that’s been happening in the last couple of years.

In terms of loss-absorbing capacity it’s not only the quantum, the race to the top as we call it, with people going to 20% plus on total capital. In my view, it’s more about how transparent you are in terms of your resolvability and how easy it is for investors to understand their position in the waterfall. When investors provide equity, tier one, tier two, senior debt to a banking group, where do you sit in that scenario?

Ultimately I could see a situation where a bank that is more transparent in terms of resolution planning, even if they have less capital than another bank in terms of quantum, may get better credit from the market, just because they will be perceived as being clearer

and transparency and disclosure should and will be rewarded in my view.

Schotkamp, BBVA: This is about transparency and the needs that investors have. I go back to the experience of the AT1s. You worry about disclosure on Pillar 2, you worry about RWA bases, lots of variables but on top of that what are you going to get is the maximum distributable amounts, and my coupon, where do I sit?

That dynamic has taken time for the investor base to get hold of and to model. The devil in TLAC is it is non-hierarchical, it doesn’t sit on top, it comes in between, before combined buffer requirements, and therefore it affects payments on the whole of the capital stack and non-compliance may even provoke core capital shortages.

As an investor, the amount of information you’re going to need on where that capital sits, how much each unit complies, what it can destroy, the variables you’re looking at in terms of disclosure and understanding are mind-boggling, I can tell you. We’re a multiple point of entry strategy firm, we’re trying to do the numbers and these things are exponentially more difficult to explain.

Given the importance of TLAC compliance you will have to start disclosing your maturity profile and your buffers. I don’t want to dramatise it but we have talked to competitors and they say for them it has strategic consequences. It will stop them doing certain businesses in certain countries because the whole thing becomes so enormously complex.

Maybe after all that’s the goal of politicians, maybe this is the squeeze the industry’s been subject to and it is about pushing people away from the business models that were built between the late 1990s and 2007.

Does it now make sense to be number five in a market 10,000 miles away from here with a regulator that doesn’t want to hear about TLAC and thinks we’re all nuts because there was no crisis?

It seems to be getting more complex rather than simpler. What happens to an overseas franchise in a resolution situation? Are we going to recapitalise it, are we going to let it drop? Can we defend that in Frankfurt or does the host regulator want to have a say?

Savadia, Lloyds: You’re absolutely right. What TLAC or MREL rules require banks to do is further explain their business strategy. Banks which should benefit are those which have a clear business model, with a low risk, less volatile and less complex group structure. Operating in fewer jurisdictions also helps as there are fewer areas

Erik Schotkamp BBVA

009-018 Issuers Roundtable.indd 12 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

Bank Capital 13

that may attract additional capital and so on.That is where the focus should be. It is not only the

size of the capital stack and is institution X running higher capital levels than institution Y. More important in my mind, is getting comfortable with the level of loss-absorbing capital in institution X’s structure given its target operating model.

: As issuers, are you confident that you know what your respective regulators would do in a resolution situation, do you have a good enough idea of the process?

Everwijn, Rabobank: These are current discussions and to your point, Erik, they don’t care about the complexity of an organisation. They want you to make it as clean as possible in order to be able to resolve that company in a weekend; close on Friday and re-open on Monday. That is their ultimate goal and if the organisation starts to get too complicated they want you to make it easier.

Krim, Morgan Stanley: I agree with that, I think we need to keep it simple. Coming back to what Erik was saying, you referred to the time when ‘the bank is dying’. No one wants to plan their own funeral, but if you organise them it’s easier for people to manage them and reduce some of the pain associated to this process.

In our dialogue with regulators, we are seeing supervisors that are moving from the supervision side to the resolution side which is a good thing. They admit that they may not know all the banks but what they need to make it work is a manual to make sure that if there is a fire in the building if and when they come in, they know how to handle it, how to limit the impact on the building itself but also the buildings around it.

The TLAC term sheet you could say was simple, but I think the concepts and the implications of it are complex to implement so we will need a clear resolution strategy to complement and support the requirement for higher loss absorbing capacity.

Forrest, RBS: In terms of resolvability it’s not necessarily one model that will fit all banks. For those institutions viewed as being systemically important then yes, the recovery over the weekend and being able to come in and create a fresh start on Monday morning is there. But there will be some institutions that have less systemic importance and you could foresee circumstances where the regulator wouldn’t be so concerned, and in fact would just let them go over the weekend.

: Is it this kind of uncertainty that is causing fluctuations in holdco-opco differentials, for example?

Forrest, RBS: The holdco-opco differential really came into focus earlier this year, though for some issuers it had always been there. We took the decision to issue from holdco and for those earlier issuances there was discussion but it just depends ultimately on the dynamic of the market at the particular point in time whether there is a differential there or not.

You’ve seen a huge amount of volatility over the last few weeks so the differential between opco and holdco has bounced around significantly. It’s an investor’s prerogative to value any credit in whichever way they deem suitable.

That’s reflective of the position we are in whereby

we’re striving for harmonisation, and it’s been said a few times already, we’re falling short of that. We’ve got a number of differing models, there’s ultimately confusion there in the market and where you have that you’ll have volatility.

Savadia, Lloyds: Arguably the rating agencies are also a factor here. Inconsistency in recent frameworks hasn’t helped the market fully triangulate just where that holdco premium should be. To me it importantly comes back down to the view of the business and group structure.

: What would you like to see from ratings agencies? We don’t have one here but let’s assume that at least one of them will read it.

Savadia, Lloyds: They released their initial methodologies and then paused to let the regulation develop, which I think was positive. However, from the perspective of the UK you would like to see a degree of consistency in the application of ratings for similar ranking liabilities. For example, holdco loss-absorbing debt versus loss-absorbing debt from an institution without a holdco in place. It seems that capital issuance out of the operating company currently benefits from a ratings standpoint versus similar holdco liabilities despite them both being loss-absorbing instruments.

Such inconsistencies create uncertainty for the market and the investor community.

Bian, BlackRock: I agree with that last point. The rating agencies’ approach with regard to ratings between holding companies’ senior debt and operating companies’ senior debt in frameworks where potentially you have law with explicit subordination in insolvency; that’s a bit weird. Maybe rating agencies have been used to rating non-financials, where you have structural subordination from holding companies and things like that, but obviously big banks won’t go into insolvency so the process is a little bit different.

I very much agree with what they’re trying to do, which is build a framework around probability of default and loss given default, I give you that, but they still have to adjust the methodology for that.

I’m interested in seeing things like the double leverage that the holding company carries, so I can assess what the actual subordination is even if I’m a senior investor in a holding company but everything is being downstreamed in equity. This matters. Again

Vishal Savadia LLOYDS

009-018 Issuers Roundtable.indd 13 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

14 Bank Capital

it goes into the probability of default versus loss-given default type of framework. Disclosure around that would be very welcome to help us solve this puzzle.

Krim, Morgan Stanley: So let’s assume that there was some downstreaming one-for-one, would you then look at holdco and opco debt as being the same risk?

Bian, BlackRock: Comparing opco debt from Germany, for example, if the draft law is passed and senior debt is explicitly subordinated to TLAC excluded liabilities, I think it’s fair enough to make this comparison. Obviously with legacy opco debt in the UK you’re talking about a different thing. But I guess explicit bail-inable senior debt in continental Europe versus holding company senior debt in UK is a fair comparison, absolutely, if the double leverage is not there.

Loriferne, Pimco: One of the reasons why there is this inconsistency and also why there is this relatively large spread between opco and holdco, especially in the UK, could be the confusion between the US and UK resolution regimes: the US framework has been well understood and well communicated for a few years now. TLAC came in late last year, and UK banks have only recently started to issue more from the holding companies in order to comply with the new requirements.

We need to understand that at least in Europe and the UK in particular the holdco cannot be forced to recap the opco beyond its original investment and it’s totally different than what we have in the US with the source of strength doctrine. So maybe it has made it harder to understand why in the UK the opco would be the first to take on the losses before passing on to the holding company depending on the level of losses incurred.

This is why the disclosure on how internal TLAC is being downstreamed from the holding company down to the opco is of paramount importance to us, in order have a good understanding of how losses will be spread across various parts of the capital structure.

: Germany and Spain have taken different routes to avoid this problem altogether. What do we think of Germany’s rather elegant solution of counting all senior debt towards TLAC?

Schotkamp, BBVA: The solution may be elegant, but the way it’s been done is not. Germany has a certain philosophy that allows them to take the approach they have taken. Can we think about a German solution being applied to Europe? If it is we think — and this is more the Spanish view — it needs to go through the revision of the BRRD and be done at a European level so the unilateral nature that Germany has chosen is curious.

BBVA and others have been able to survive from a liquidity point of view by having access to markets and not having to dig too deep into the usage of collateral. The statutory approach moves a financing instrument that’s been very useful at very important times into the capital stack. If this is what we want then that’s good, but make no mistake, your capital requirements will move you earlier on into a liquidity problem. Everybody at this table knows that banks die from liquidity problems and not from capital problems, and this is where the capital regulation overshoot is really worrisome.

Spain has defined an instrument that we could use

as a bank — it’s an option, we don’t have to — to create an extra stack of capital to potentially protect the usability of another instrument. I like that option.

Forrest, RBS: Erik has hit the nail on the head. For me with the German model, yes, you can see that as a solution. Taking a piece of legislation and saying, ‘this is going to have retrospective effect’, is a game-changer. If it’s something which has got a forward-looking basis — we’ve all sat round the table and talked about changes in terms of issuance of AT1, TLAC, etc — then it gives you time to plan for that.

As an investor, if you are holding a piece of paper which is senior today but then when a law passes it’s no longer senior, it is forming part of the capital structure, that is an instrument which prices at a different level and the ramifications of that are pretty significant.

Everwijn, Rabobank: I agree. It is the availability of senior unsecured funding you want to secure. That leads to the discussion we’re having with the rating agencies. First of all what’s the probability of default and secondly what is the loss-given default or failure? Our view is that we should have a buffer high enough to make sure that the probability of default is virtually zero and therefore immunise the operational liabilities you have outstanding.

If then for whatever reason the company makes losses greater than the capital you have on the balance sheet then you should use all the senior debt and all that is ranking pari passu with operational liabilities. Why differentiate? You sold an instrument that was senior in ranking to all the other instruments and you simply can’t change the rules during game.

Menounos, Morgan Stanley: I would like to explore the other side of the argument for a moment. Not all jurisdictions are represented in this discussion and not all regions are similar with respect to estimated gap to TLAC. There is an instinctive attractiveness in the ability to flick a switch and create a layer of bail-in capital from existing securities. After all, the adjustment phase, as well as the end point, could be pretty expensive if you consider the creation of a new class of securities that is structurally subordinated to outstanding securities.

Even if we end up with a structurally subordinated senior debt, my view is that there would still be a negotiation between issuers and investors around the right amount of capital, and this would depend on the bank, the business model and the jurisdiction. I fully agree that banks don’t ultimately fail because of capital holes, but it is the capital hole that leads to a run on

Scott Forrest ROYAL BANK OF SCOTLAND

009-018 Issuers Roundtable.indd 14 06/07/2015 09:04

Bank Capital Issuers’ Roundtable

Bank Capital 15

liquidity that ultimately brings a bank down.So we may get a combination of approaches, which is

unfortunately not going to help harmonisation and may eventually drive bigger differentials across Europe.

Krim, Morgan Stanley: We want to be able to say that whatever regime you use or route you choose, statutory or contractual or structural, it’s equal. On statutory harmonisation we need to give comfort to investors and issuers that going statutory works. Germany is going its own way but I think we need to see if there is a statutory solution in Europe, and explain how it works. We also need to think about the probability of default element. Will we really have a senior bail-in for any bank? It’s a tool that is nice to have and the fall-back solution. People are, however, focused on this bail-in tool and it is seen as being the only one that will be used by resolution authorities. There’s recovery planning, there are other resolution tools, and I don’t think any resolution authority would say my best option is to go for a senior bail-in. They want to have it because it’s the way to avoid a bailout but there will be other ways to resolve banks. Bail-in is new and triggers interest and focus but we should see it as a remote scenario.

Everwijn, Rabobank: I disagree with you there because we have sold certain paper to certain investors on the basis that it was senior unsecured. That is an agreement that we have made, even if the risk is limited. It’s the trust in the system. You can’t change the rules. If you don’t want to build up your capital ratios then there are alternatives, you have to create new instruments that can fill the gap, like the Spanish proposal. Then you have new issuance that is fulfilling that requirement if you want to optimise the cost of capital, but don’t try to touch senior unsecured.

Krim, Morgan Stanley: That’s what I’m saying, my point is bail-in of senior unsecured, even if it’s theoretically something that you can touch from a statutory standpoint, shouldn’t be the base case, it shouldn’t be what resolution authorities, issuers or even investors think would be the base case scenario in a resolution scenario.

Menounos, Morgan Stanley: But isn’t that the compromise then, in that harmonisation will have only been achieved on paper and in effect, banks may adopt different strategies?

Forrest, RBS: Another thing from an investor’s perspective. As a bank working on capital you’ve got a close, continuous and evolving relationship with the regulator. They’ve got much more visibility in terms of banks’ business requirements, capital requirements, business needs, stresses and strains as the business is run.

So in terms of the very end point, it’s bail-in and I totally agree with you, that’s the very end point there but there are a number of actions and levers that would come into effect before you even got to that end situation.

Bian, BlackRock: I think it adds a lot of cyclicality in business models. It’s great if you have a one weekend crisis and everything is very resolvable, but if you don’t get market access for a year or more, banks will have no other solution than shrinking the business. By shrinking the business it just adds to cyclicality. It could become a

self-fulfilling spiral if they breach buffers and there’s a lot of uncertainty and more money’s being withdrawn from the banks and banks have to shrink even more aggressively.

It’s fair to try to find a fine balance between what is your capital stack and what is your bail-in stack, but you also have to think about the unintended consequences from the actions you’re taking, or the risk that you’re overdoing in terms of regulation.

Schotkamp, BBVA: It is changing the rules of the game and I am hearing the same from other investors as well. It seems to be a concern for people. But I don’t see anything in the media, I hear no groups of investors saying what are we doing here? It seems all to be fine.

We do have the tier three in Spain and I kind of like it because thinking on a forward-looking basis, being conservative, management says ‘what is the cheapest option?’ How much did Deutsche Bank’s senior widen after the German law was announced? 10bps. Well, we’re going to go statutory because that’s cheap.

Markets in a way are telling us, ‘guys, go for statutory bail-in of senior unsecured because the spread pick-up or the spread widening you will see once that gets done is manageable’. This gets to the point, this is not going concern capital, this is if you’re dying you need to have something and that’s costly: an insurance policy for your funeral. We need to do this as cheaply as possible because that’s optimisation from a financial management point of view.

Loriferne, Pimco: Investors need to continue to be very selective. In our bond funds, we have broad guidelines in order to avoid being trapped in one particular tier in the capital structure in one particular country.

It’s important to understand that unexpected rule changes are very risky for everybody involved. If I look at the spreads of senior debt in Germany it’s widening much more than just 10bp, as the recent regulatory changes start to sink into investors’ minds. The senior spread has more than doubled for one bank in particular. So it clearly has direct implications in terms of cost of funding and it’s in the issuers’ hands to decide whether or not they want to reprice the entire senior stack of their capital structure.

We all understand senior is at risk. What matters is how those losses are passed on to the senior bondholders and this is where the No Creditor Worse Off is important. If you do change the law and make senior structurally subordinated then it begs the question, how will senior be treated, is senior becoming

Leopold Bian BLACKROCK

009-018 Issuers Roundtable.indd 15 06/07/2015 09:04