Embed Size (px)

Citation preview

Barclays Back-to-School Consumer Conference

Michael Polk

President and Chief Executive Officer

September 4, 2013

Forward-Looking Statement Statements in this presentation that are not historical in nature constitute forward-looking statements. These forward-looking statements relate to information or assumptions about the effects of sales, income/(loss), earnings per share, operating income, operating or gross margin improvements or declines, the European Transformation Plan, Project Renewal, capital and other expenditures, cash flow, dividends, restructuring and restructuring-related costs, costs and cost savings, inflation or deflation, particularly with respect to commodities such as oil and resin, debt ratings, and management's plans, projections and objectives for future operations and performance. These statements are accompanied by words such as "anticipate," "expect," "project," "will," "believe," "estimate" and similar expressions. Actual results could differ materially from those expressed or implied in the forward-looking statements. Important factors that could cause actual results to differ materially from those suggested by the forward-looking statements include, but are not limited to, our dependence on the strength of retail, commercial and industrial sectors of the economy in light of the continuation or escalation of the global economic slowdown or regional sovereign debt issues; currency fluctuations; competition with other manufacturers and distributors of consumer products; major retailers' strong bargaining power; changes in the prices of raw materials and sourced products and our ability to obtain raw materials and sourced products in a timely manner from suppliers; our ability to develop innovative new products and to develop, maintain and strengthen our end-user brands; our ability to expeditiously close facilities and move operations while managing foreign regulations and other impediments; our ability to implement successfully information technology solutions throughout our organization; our ability to improve productivity and streamline operations; changes to our credit ratings; significant increases in the funding obligations related to our pension plans due to declining asset values, declining interest rates or otherwise; the imposition of tax liabilities greater than our provisions for such matters; the risks inherent in our foreign operations and those factors listed in the company’s latest quarterly report on Form 10-Q and Exhibit 99.1 thereto filed with the Securities and Exchange Commission. Changes in such assumptions or factors could produce significantly different results. The information contained in this presentation is as of the date indicated. The company assumes no obligation to update any forward-looking statements contained in this presentation as a result of new information or future events or developments. This presentation contains non-GAAP financial measures within the meaning of Regulation G promulgated by the Securities and Exchange Commission. Included in this presentation is a reconciliation of these non-GAAP financial measures to the most directly comparable financial measures calculated in accordance with GAAP.

Nancy O’Donnell VP, Investor Relations (770) 418-7723 [email protected]

Alisha Dubique Sr. Manager, Investor Relations (770) 418-7706 [email protected]

INVESTOR RELATIONS CONTACTS:

3

$6B in sales with leading brands in five business segments

writing

tools

home solutions

commercial products

baby

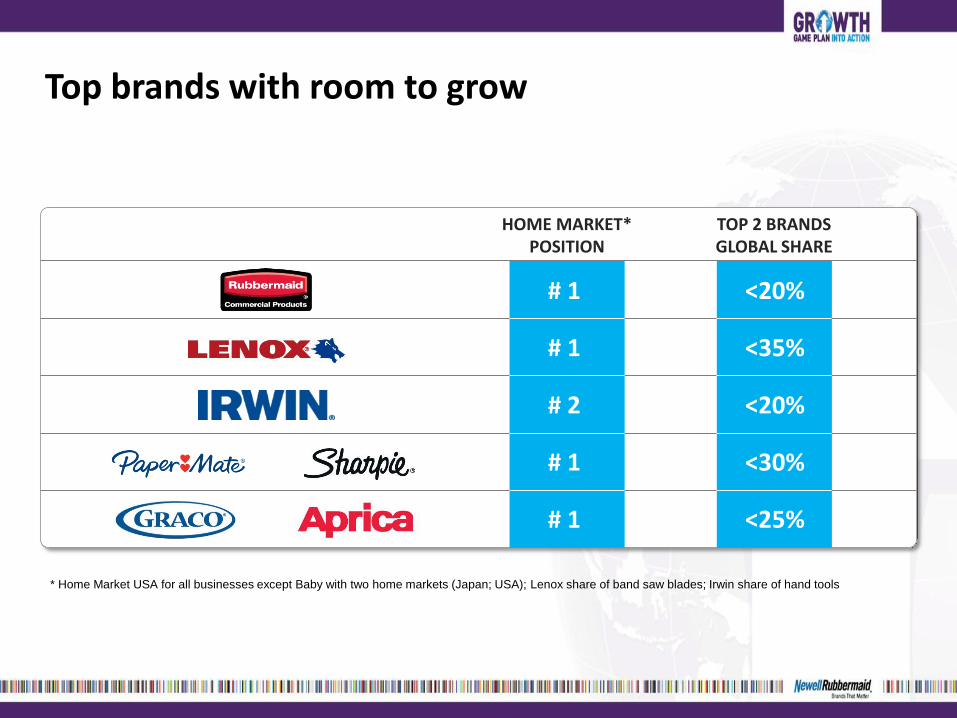

Top brands with room to grow

HOME MARKET* POSITION

TOP 2 BRANDS GLOBAL SHARE

# 1 <20%

# 1 <35%

# 2 <20%

# 1 <30%

# 1 <25%

* Home Market USA for all businesses except Baby with two home markets (Japan; USA); Lenox share of band saw blades; Irwin share of hand tools

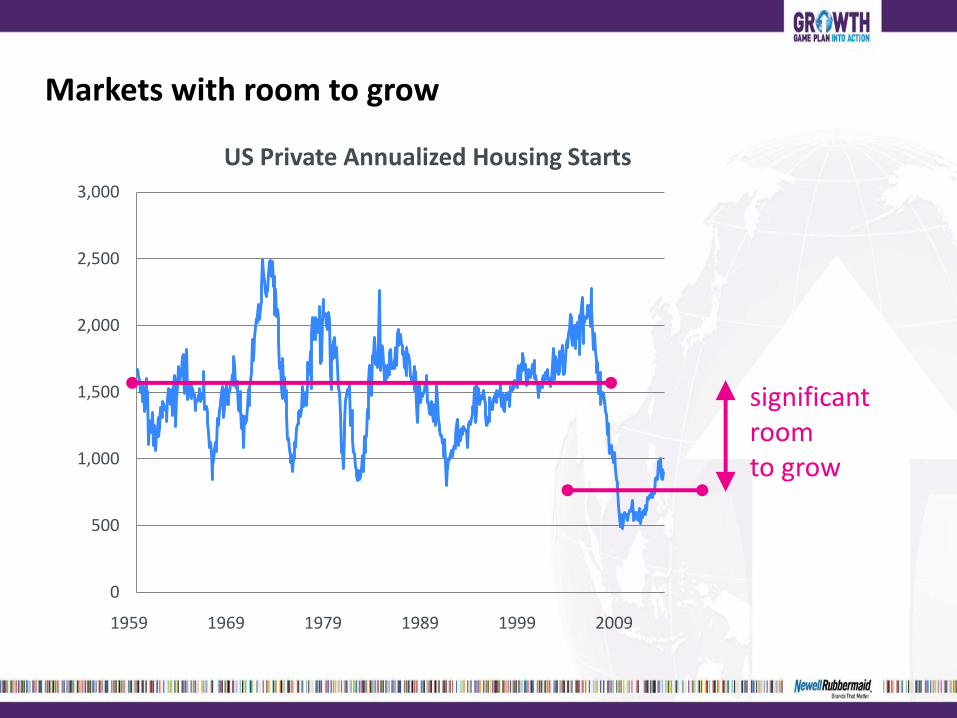

Markets with room to grow

0

500

1,000

1,500

2,000

2,500

3,000

1959 1969 1979 1989

US Private Annualized Housing Starts

1999 2009

significant room to grow

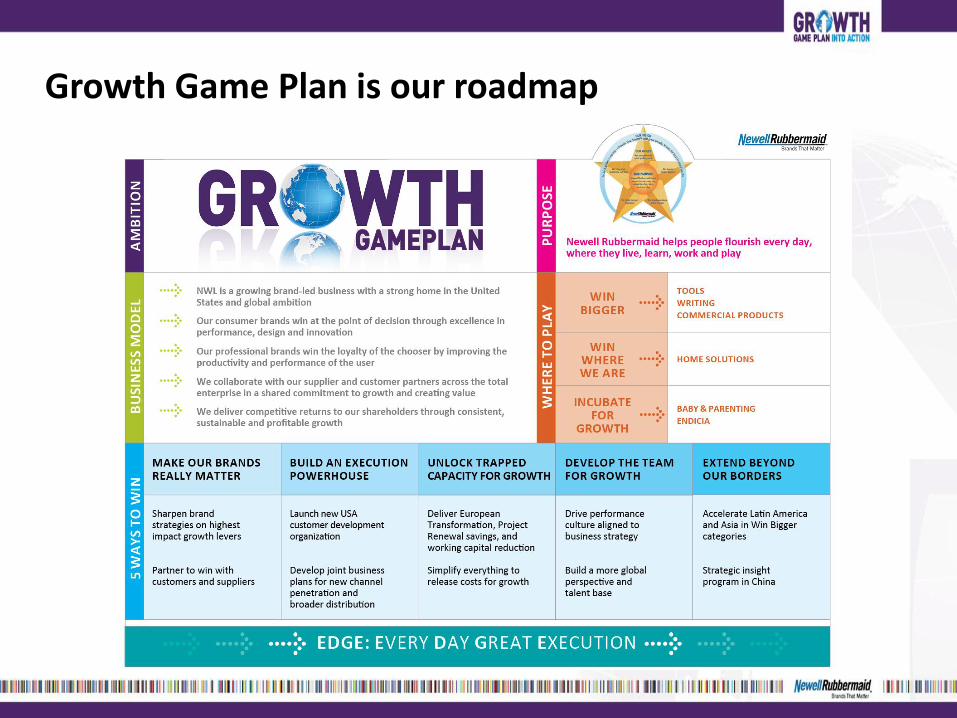

Growth Game Plan is our roadmap

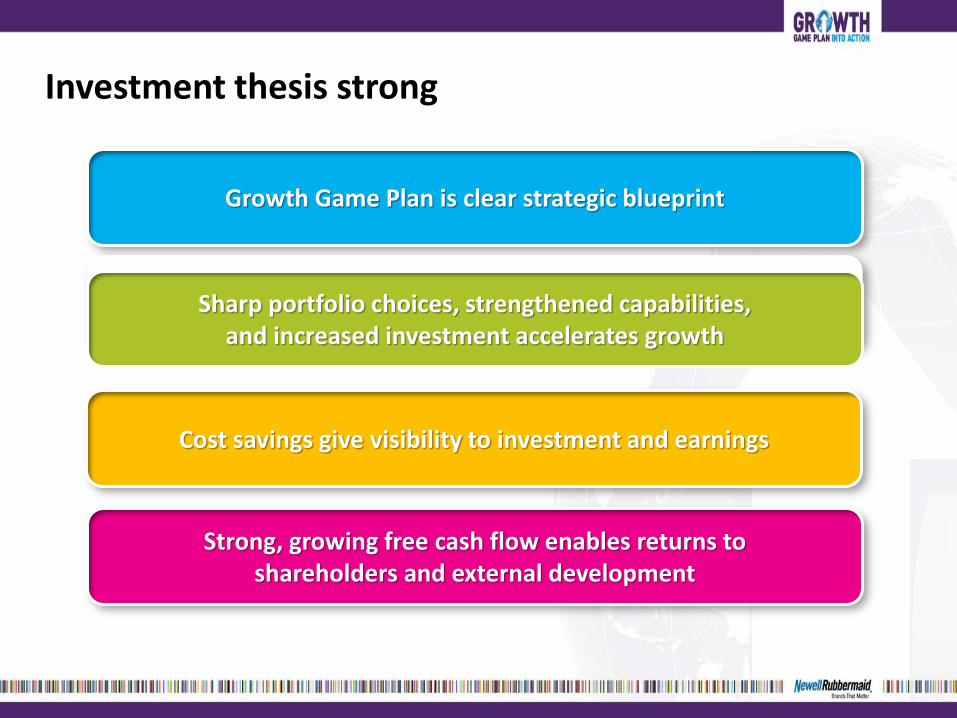

Growth Game Plan is clear strategic blueprint

Cost savings give visibility to investment and earnings

Sharp portfolio choices, strengthened capabilities, and increased investment accelerates growth

Strong, growing free cash flow enables returns to shareholders and external development

Investment thesis strong

We are making good progress

DELIVERY

consistently do what we say

STRATEGIC

shape the future

ACCELERATION

accelerate performance

2013

Core Sales +2-3% EPS* +3-6%

Core Sales +3-4% EPS* +5-8%

Core Sales >4% EPS* +6-9%

* Normalized EPS

2014 2012 2015 2016/17

Growth Game Plan sources of growth

45% 25% 30%

Enabled by reset of margin algorithm

operating income margin %

EMERGING

DEVELOPED

full portfolio, local needs and local price points

investment in sales and marketing

enabled by reducing high cost in developed world

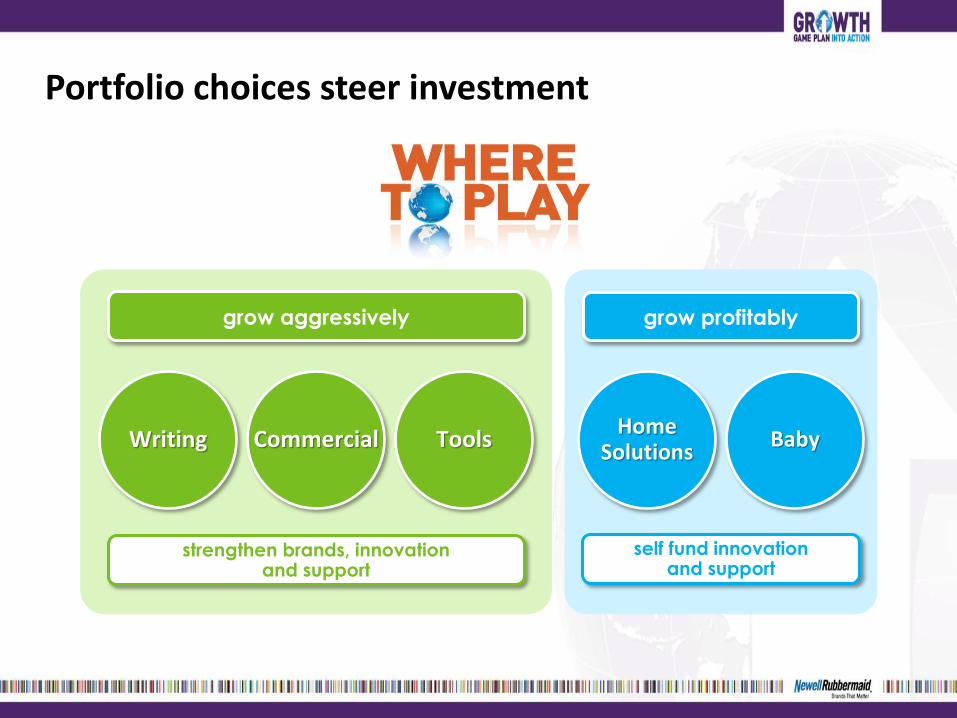

Portfolio choices steer investment

grow profitably

Tools Writing Commercial Home

Solutions Baby

grow aggressively

strengthen brands, innovation and support

self fund innovation and support

5 Ways to Win shape activities

make our brands

really matter

build an execution

powerhouse

unlock trapped

capacity for growth

develop the team for growth

extend beyond our

borders

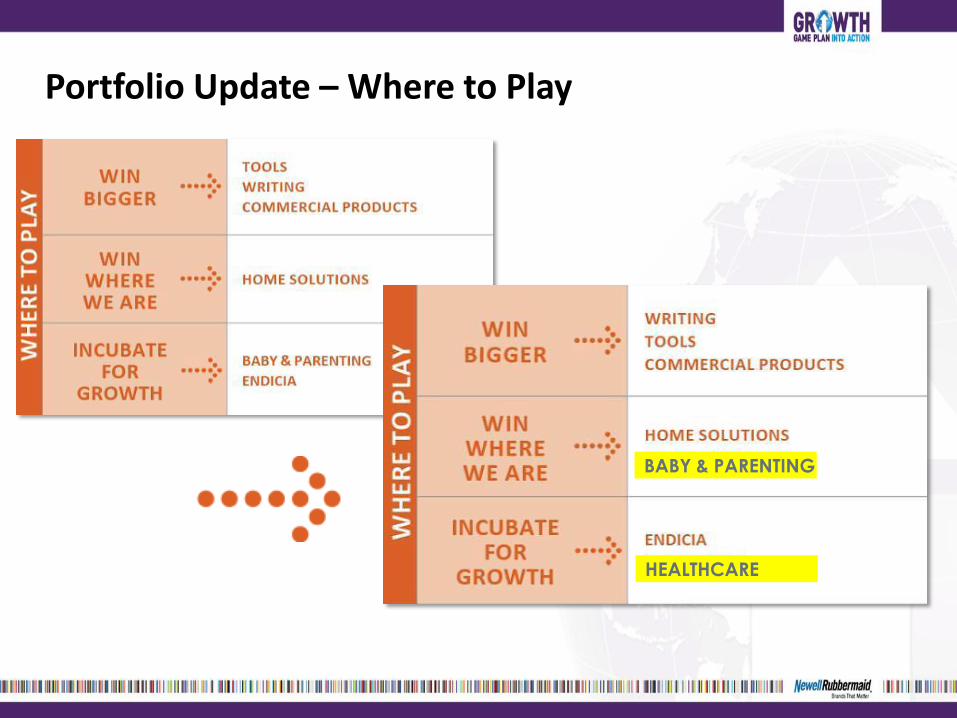

Portfolio Update – Where to Play

BABY & PARENTING

HEALTHCARE

2 Pillars supported by

3 Functions and

4 Winning Capabilities driving accelerated performance in

5 Operating Segments

1

Tools Writing Commercial Home

Solutions Baby

Finance / IT

Legal

HR

R&D Design

Customer

Development

Marketing Supply Chain

Development Delivery

We have reset the organization

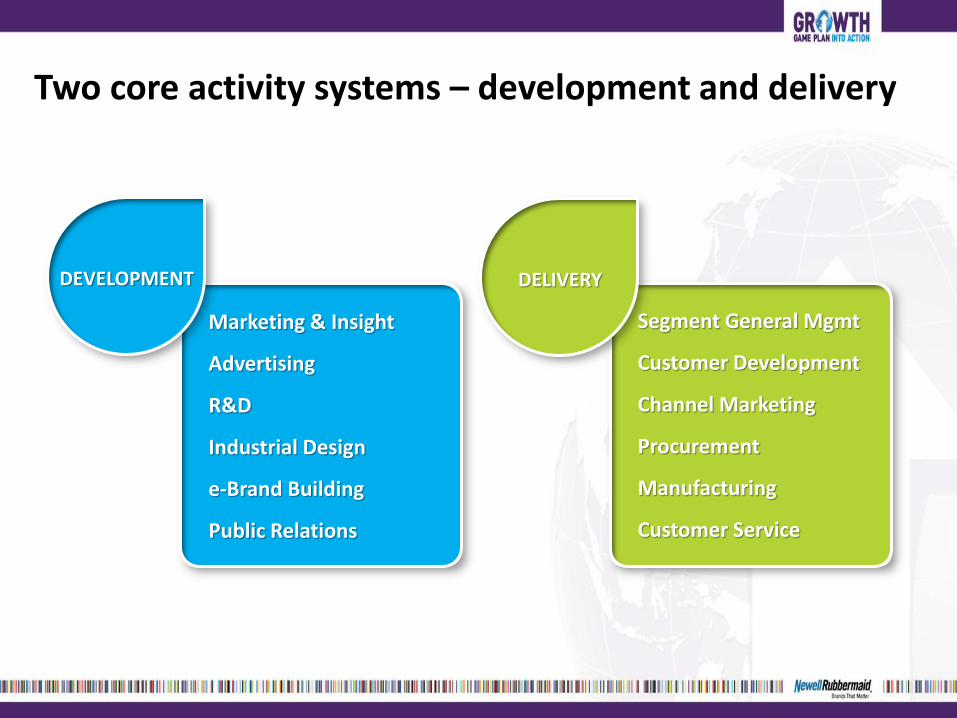

Two core activity systems – development and delivery

Marketing & Insight

Advertising

R&D

Industrial Design

e-Brand Building

Public Relations

Segment General Mgmt

Customer Development

Channel Marketing

Procurement

Manufacturing

Customer Service

DEVELOPMENT DELIVERY

Building four winning capabilities

grow profitably

Home Solutions

Baby

self fund innovation and support

Supply Chain

PLAN

SOURCE

MAKE

DELIVER

SERVE

Customer Development

Design

1000 ideas

Marketing & Insight

doubled insight invest

New InkJoy TV

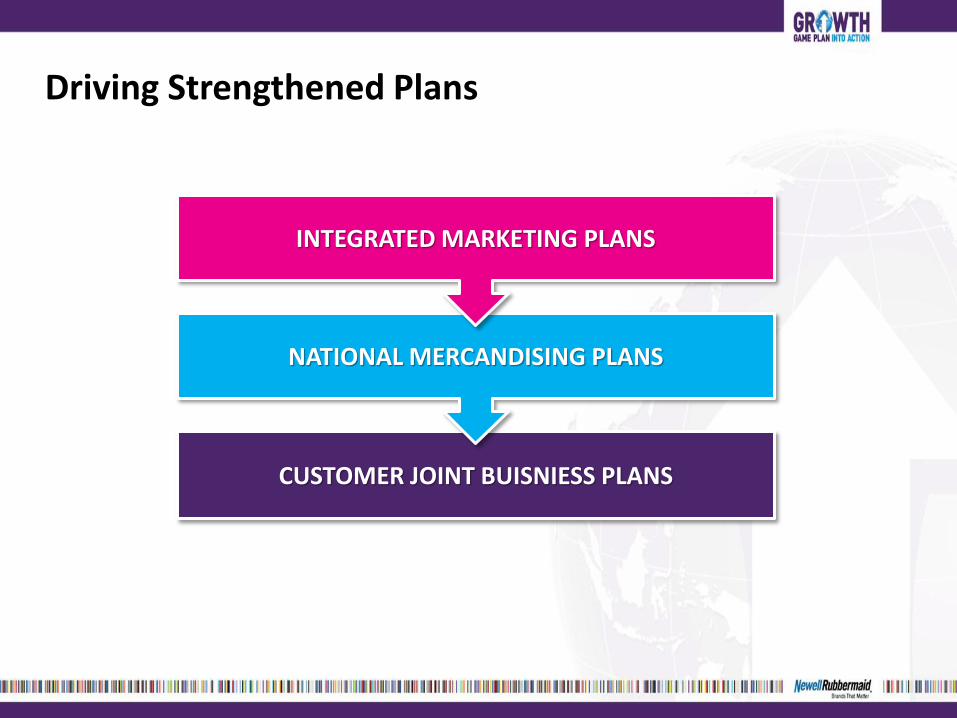

Driving Strengthened Plans

CUSTOMER JOINT BUISNIESS PLANS

NATIONAL MERCANDISING PLANS

INTEGRATED MARKETING PLANS

Big brand ideas on Tools

New advertising, big customer and tradesman activation

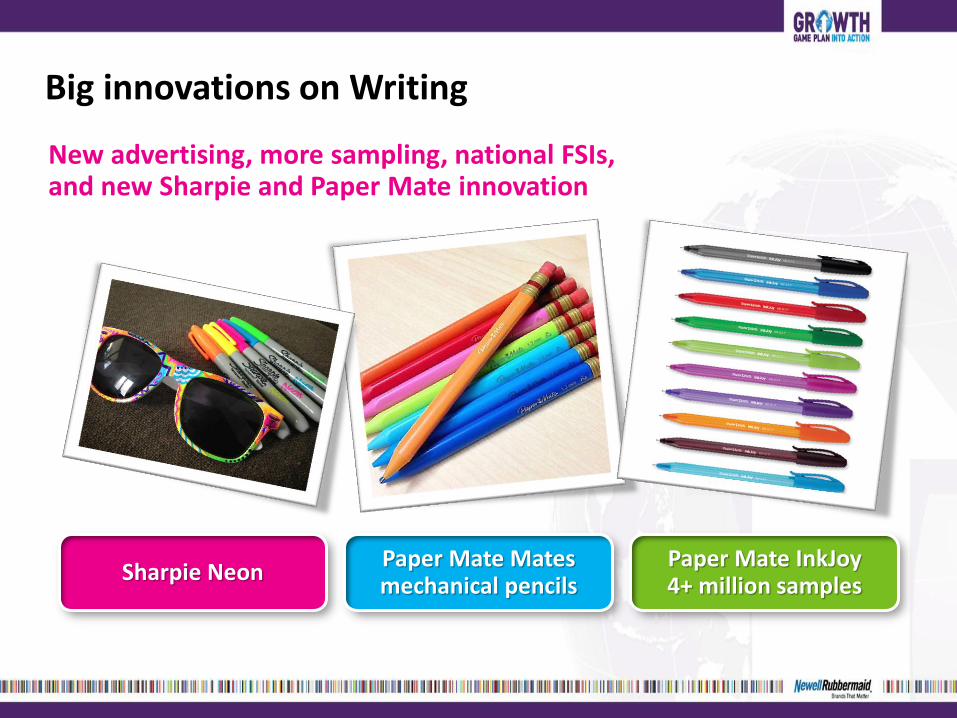

Big innovations on Writing

New advertising, more sampling, national FSIs, and new Sharpie and Paper Mate innovation

Sharpie Neon Paper Mate Mates mechanical pencils

Paper Mate InkJoy 4+ million samples

Big innovations on Baby

Sustained innovation wins in Japan and USA

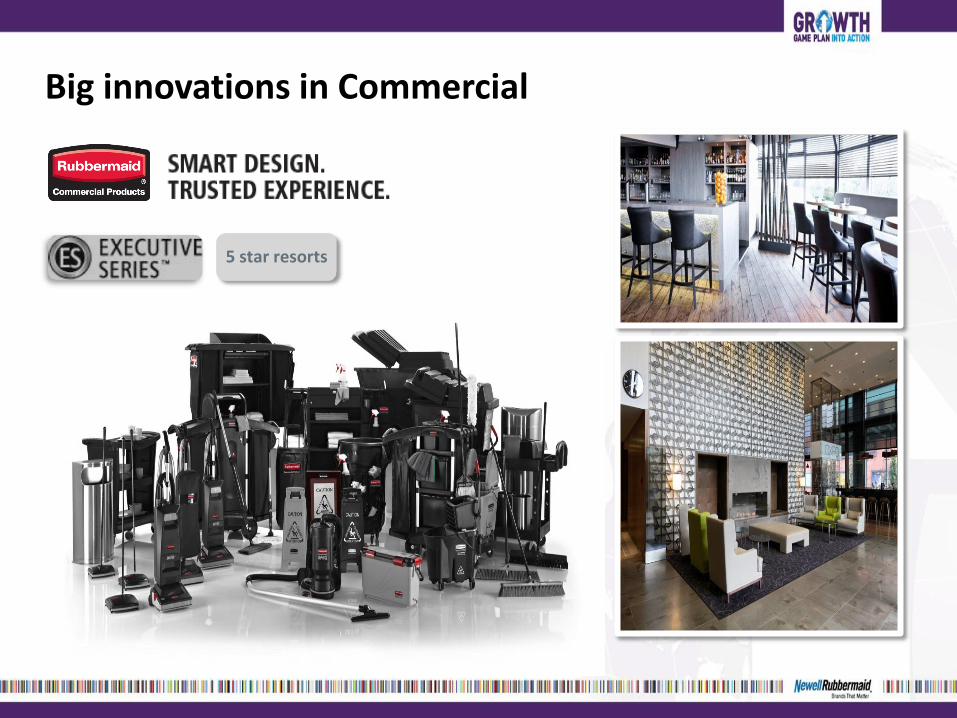

Big innovations in Commercial

5 star resorts

New Platforms on Tools

New Markets

expanding IRWIN in Brazil

10 categories, more than 500 SKUs

with top 100 customers

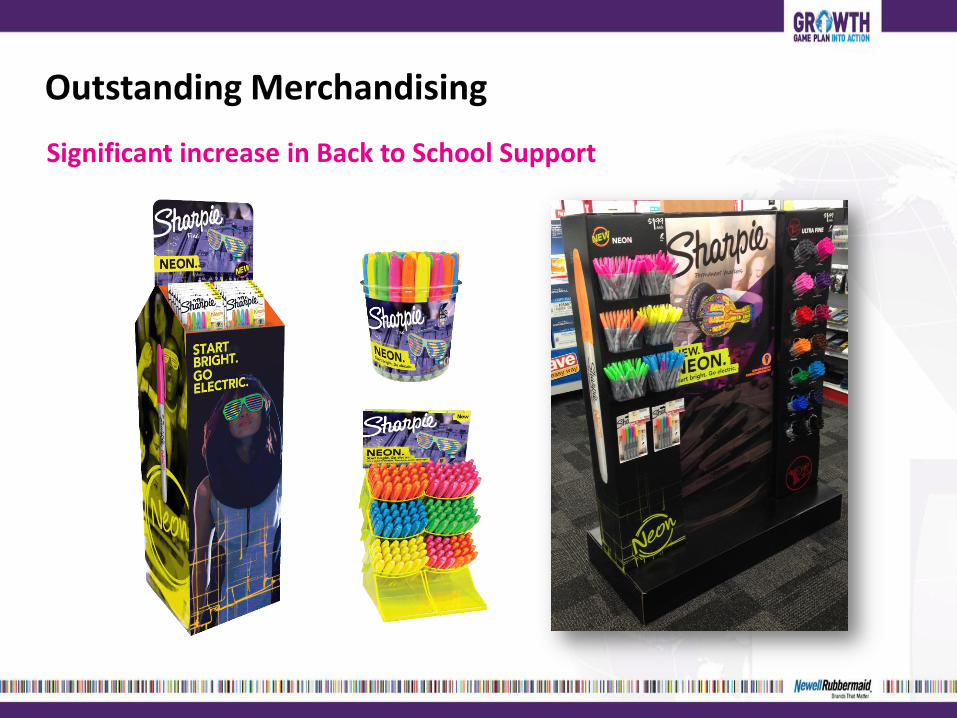

Outstanding Merchandising

Significant increase in Back to School Support

Outstanding Merchandising

Significant increase in Back to School Support

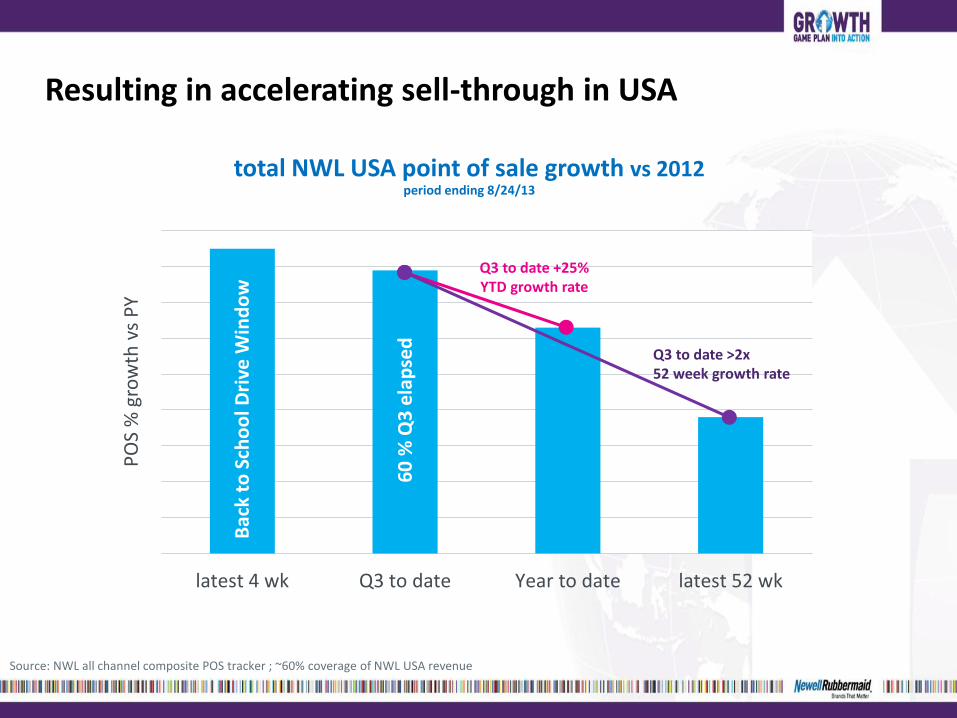

Resulting in accelerating sell-through in USA

latest 4 wk Q3 to date Year to date latest 52 wk

Source: NWL all channel composite POS tracker ; ~60% coverage of NWL USA revenue

PO

S %

gro

wth

vs

PY

Bac

k to

Sch

oo

l Dri

ve W

ind

ow

60

% Q

3 e

lap

sed

Q3 to date +25% YTD growth rate

Q3 to date >2x 52 week growth rate

total NWL USA point of sale growth vs 2012 period ending 8/24/13

And strong momentum across Latin America

Nearly 30% higher core growth rate in 2013

Enabled by savings: visibility to investment (and earnings)

EMEA Transformation

Best Cost Back Office

Best Cost Finance

New Organization Model

Global Supply Chain

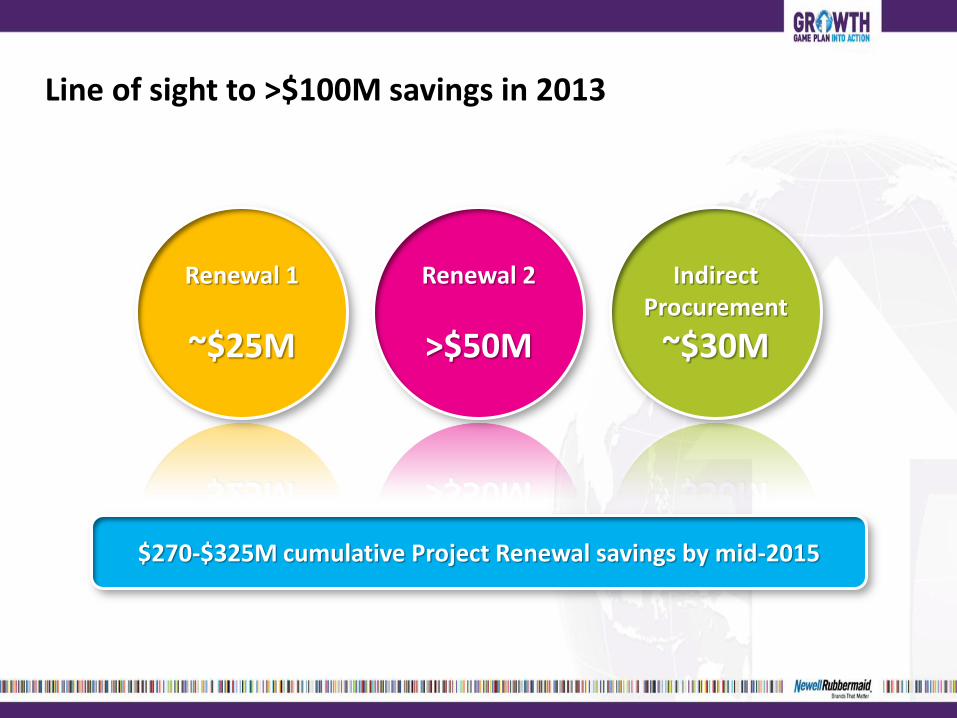

Line of sight to >$100M savings in 2013

Renewal 1

~$25M

Renewal 2

>$50M

Indirect Procurement

~$30M

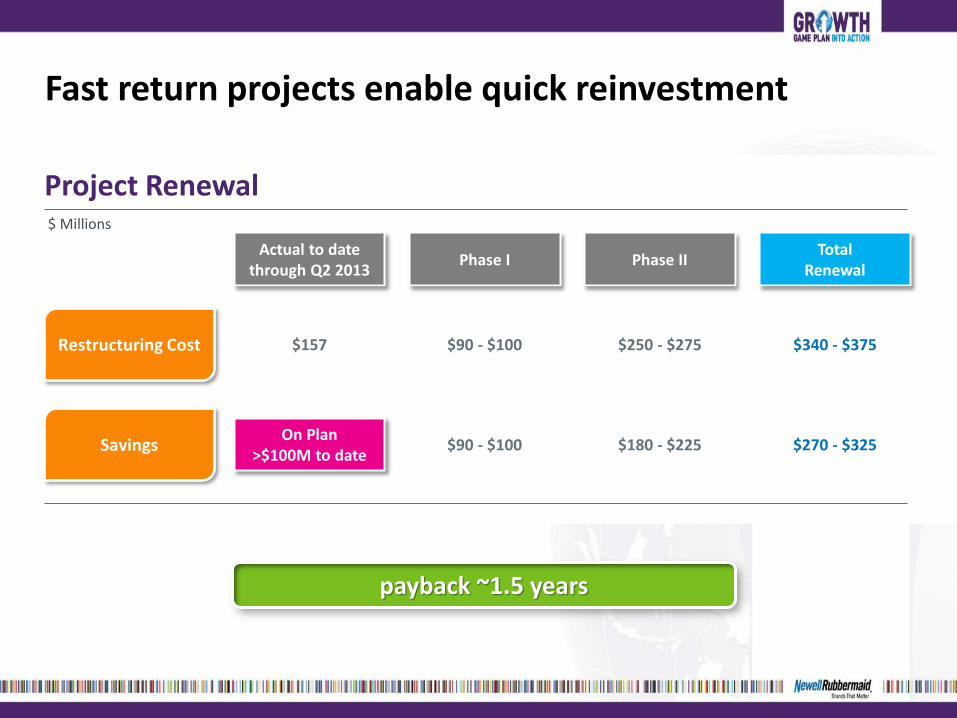

$270-$325M cumulative Project Renewal savings by mid-2015

Fast return projects enable quick reinvestment

Restructuring Cost

Savings

Actual to date through Q2 2013

$157 $90 - $100

On Plan >$100M to date

$90 - $100

$ Millions

Phase I

Project Renewal

$250 - $275

$180 - $225

Phase II

$340 - $375

$270 - $325

payback ~1.5 years

Total Renewal

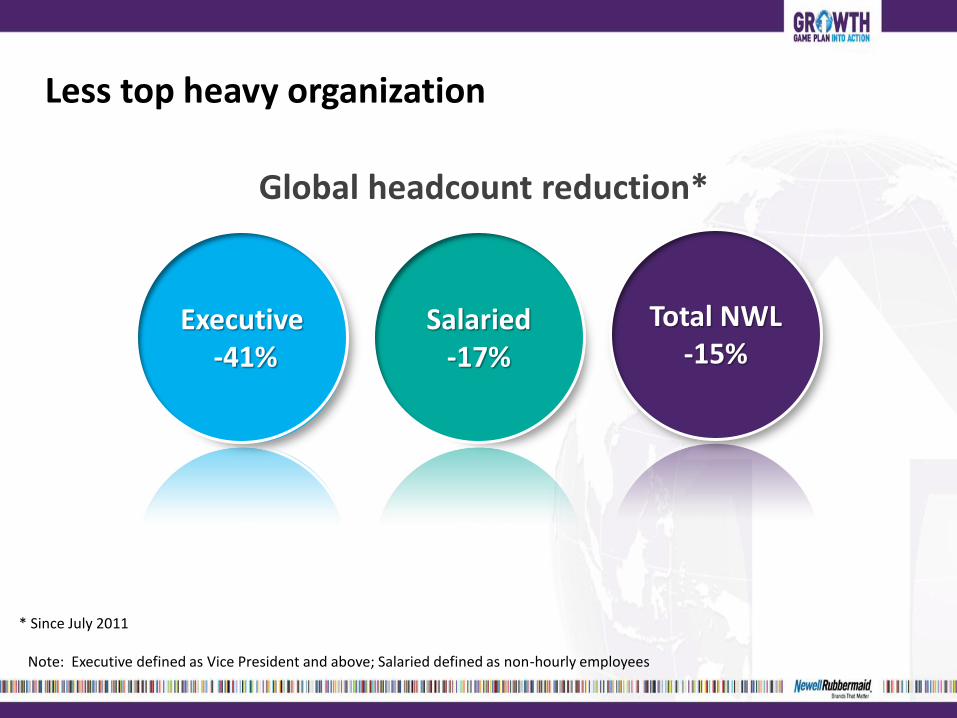

Less top heavy organization

Global headcount reduction*

Executive -41%

Salaried -17%

Total NWL -15%

* Since July 2011

Note: Executive defined as Vice President and above; Salaried defined as non-hourly employees

Good progress, with more to come

+2.5% core sales growth

+10.4% normalized EPS growth

+40 bps normalized operating margin

+65.3% increase in dividends paid

Q2 YTD 2013 results

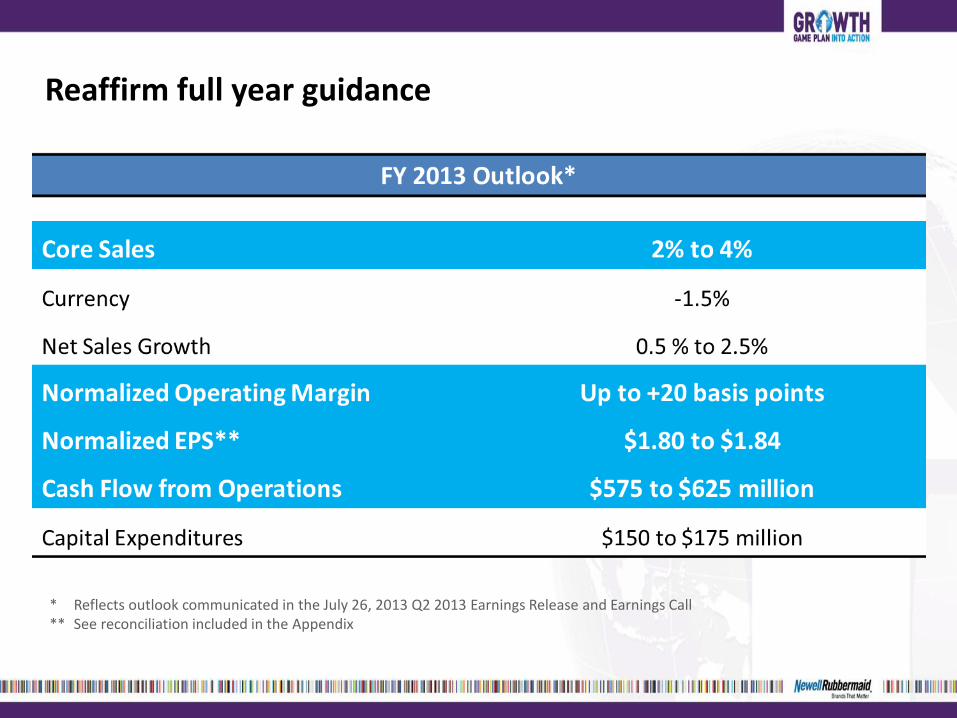

Reaffirm full year guidance

* Reflects outlook communicated in the July 26, 2013 Q2 2013 Earnings Release and Earnings Call ** See reconciliation included in the Appendix

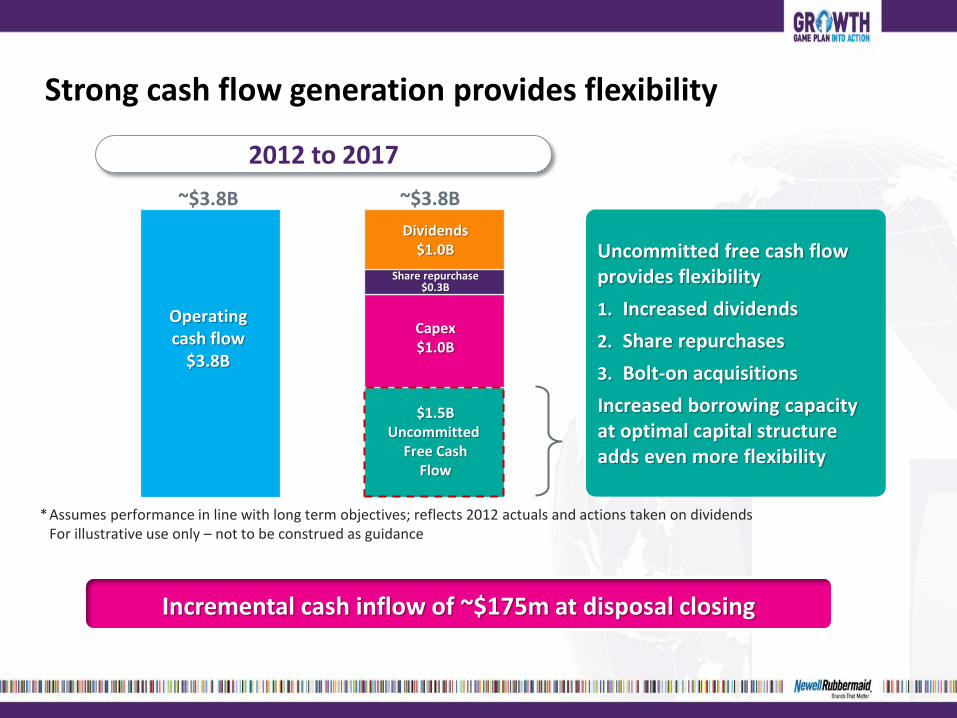

Strong cash flow generation provides flexibility

Operating cash flow

$3.5B

~$1.5 billion in uncommitted free cash flow over next 5 years provides flexibility for:

• Accelerated structural cost reductions

• Increased dividends

• Share repurchase

• Bolt-on acquisitions

Capex $1.0B

Dividends $1.0B

~$3.8B ~$3.8B

Share repurchase $0.3B

$1.5B Uncommitted

Free Cash Flow

Operating cash flow

$3.8B

* Assumes performance in line with long term objectives; reflects 2012 actuals and actions taken on dividends For illustrative use only – not to be construed as guidance

2012 to 2017

Uncommitted free cash flow provides flexibility

1. Increased dividends

2. Share repurchases

3. Bolt-on acquisitions

Increased borrowing capacity at optimal capital structure adds even more flexibility

Incremental cash inflow of ~$175m at disposal closing

Our confidence grows stronger everyday

Clear strategy

Strong, seasoned leadership team

Major increase in funds for investment or earnings

Disciplined, strategic approach to resource allocation

Organization with great capacity to change

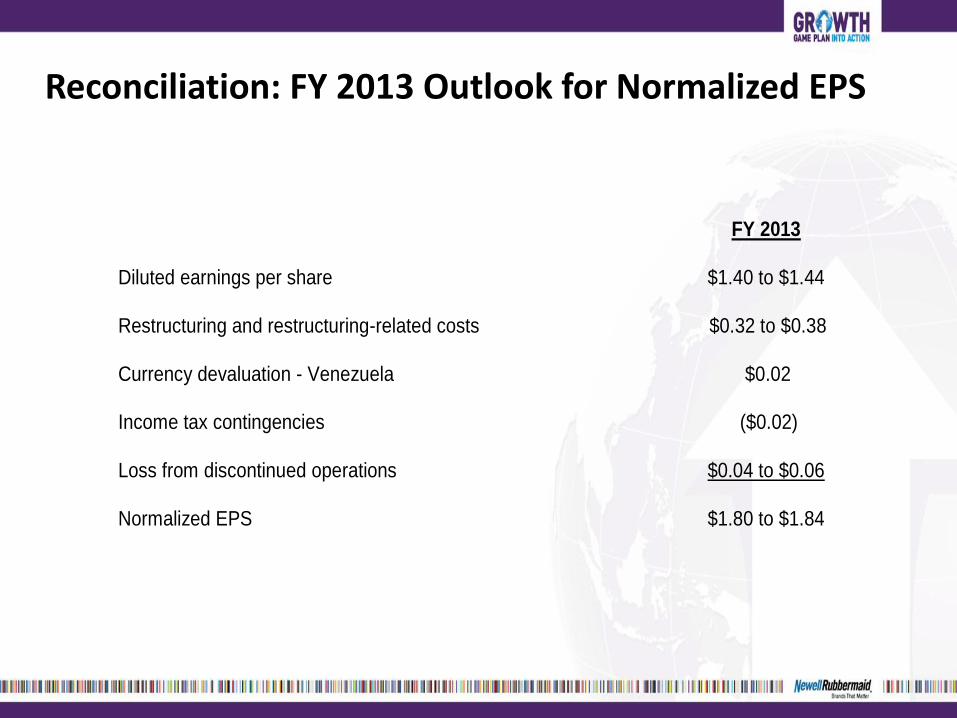

Reconciliation: FY 2013 Outlook for Normalized EPS

FY 2013 Diluted earnings per share $1.40 to $1.44

Restructuring and restructuring-related costs Currency devaluation - Venezuela Income tax contingencies Loss from discontinued operations

$0.32 to $0.38 $0.02 ($0.02)

$0.04 to $0.06

Normalized EPS $1.80 to $1.84