Embed Size (px)

Citation preview

#12781315 v.1

Basics of Private Equity Regulations and Reporting – Tax Matters Presented at IIR’s 9th Annual Private Equity Tax & Compliance Practices 2010 By: Steven D. Bortnick

June 23, 2010 – Hyatt Harborside – Boston, MA

2

Part I – Current Withholding Regime

3

IRS Announcement

• Intention to audit all persons who make payments to non-U.S. persons that are subject to withholding tax

• First 5,000 letters mailed • IRS knows Funds make the payments

4

Withholding Risk

• Trust fund tax – responsible person personally liable

5

Acquisition

Parent Co. (U.S.)

Acq. Co.

$ equity

Bank $ 50x Target

merge

FC2

SH

cash

DE LP

$

Cayman LP

equity & debt 10x 2x

DE LLC

$

US1 FC1 US2

$ equity & debt

equity & debt

6

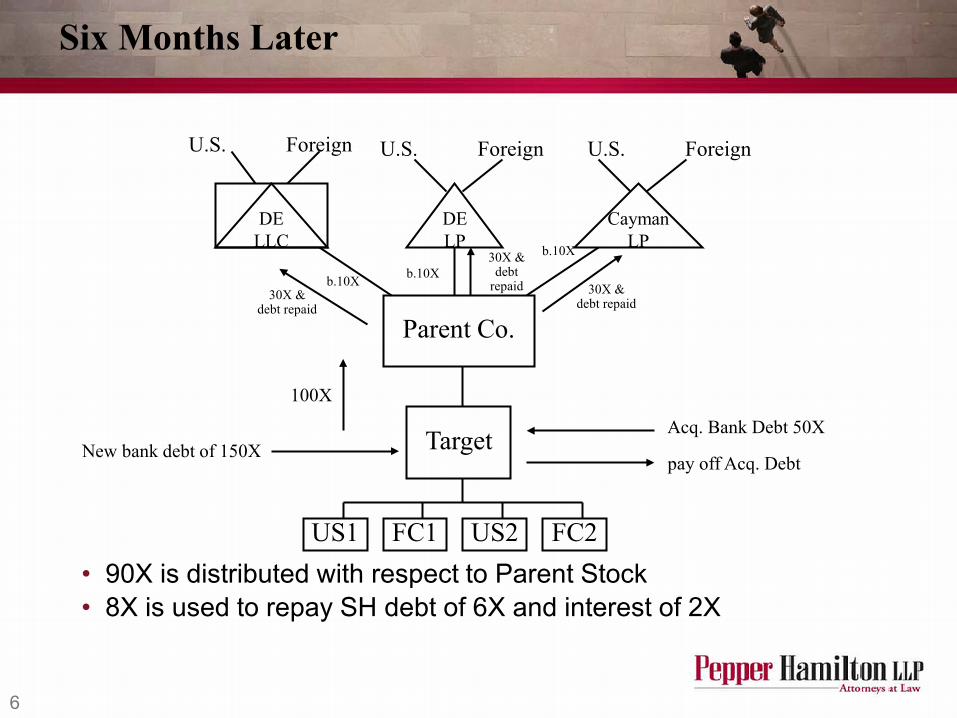

Six Months Later

• 90X is distributed with respect to Parent Stock • 8X is used to repay SH debt of 6X and interest of 2X

Parent Co.

Target

US1 FC1 US2 FC2

DE LP

Cayman LP

DE LLC

pay off Acq. Debt

Acq. Bank Debt 50X New bank debt of 150X

100X

30X & debt repaid

30X & debt repaid

b.10X b.10X 30X &

debt repaid

b.10X

Foreign U.S. Foreign U.S. Foreign U.S.

7

Issues

• Tax impact to investors • Withholding obligations of Parent Co. • Withholding obligations of Funds • Reporting obligations of Parent Co.

8

Classifying The Distribution - §316

• Taxable as a dividend to SH to the extent of current or accumulated earnings and profits

• Then a return of tax basis of SH • Then capital gain to SH

− Short term − Long term

9

E&P

• Accumulated e&p − Through close of prior year

• Current e&p − For the full taxable year – generally not based on when

distribution occurs • Consolidated e&p

− Distribution of 100X from Target to Parent never pulls pre-acquisition e&p from Target to Parent

− E&P post acquisition tiers up to Parent under consolidated tax return rules

10

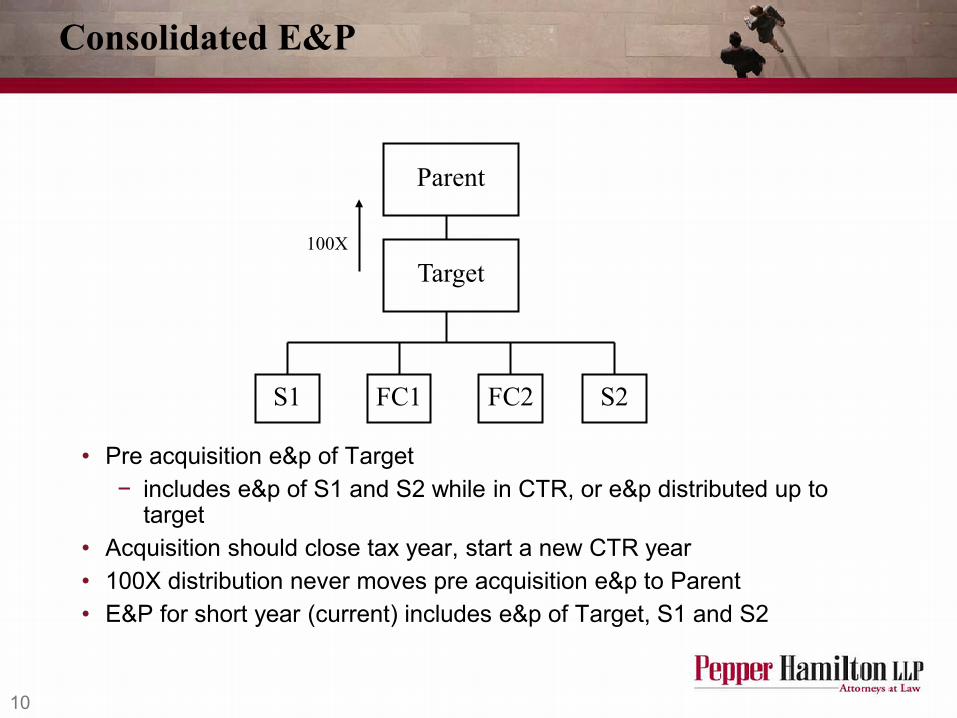

Consolidated E&P

• Pre acquisition e&p of Target − includes e&p of S1 and S2 while in CTR, or e&p distributed up to

target • Acquisition should close tax year, start a new CTR year • 100X distribution never moves pre acquisition e&p to Parent • E&P for short year (current) includes e&p of Target, S1 and S2

Parent

Target

S1 S2

100X

FC1 FC2

11

Current vs. Accumulated E&P

• Assume accumulated e&p is <100X> • Current year e&p, determined at the close of the tax

year, is 90X • Distribution of 100X is 90X dividend, 10X return of

basis/capital gain • “Nimble dividend rule” §1.316-1

12

Current vs. Accumulated E&P

• Assume accumulated e&p 100X • Current e&p <90X> • Distribution of 100X on June 30 −E&P available

100 - 45 (1/2 of current e&p) 55

− 55 of 100 is dividend • Rev. Rule 74-164

13

Current Year E&P Issues

• Cost of Acquisition − Deductible vs. non-deductible expenses of acquisition − Deductibility of refinancing costs − Deductibility of option exercise/cash out/restricted stock

grants

14

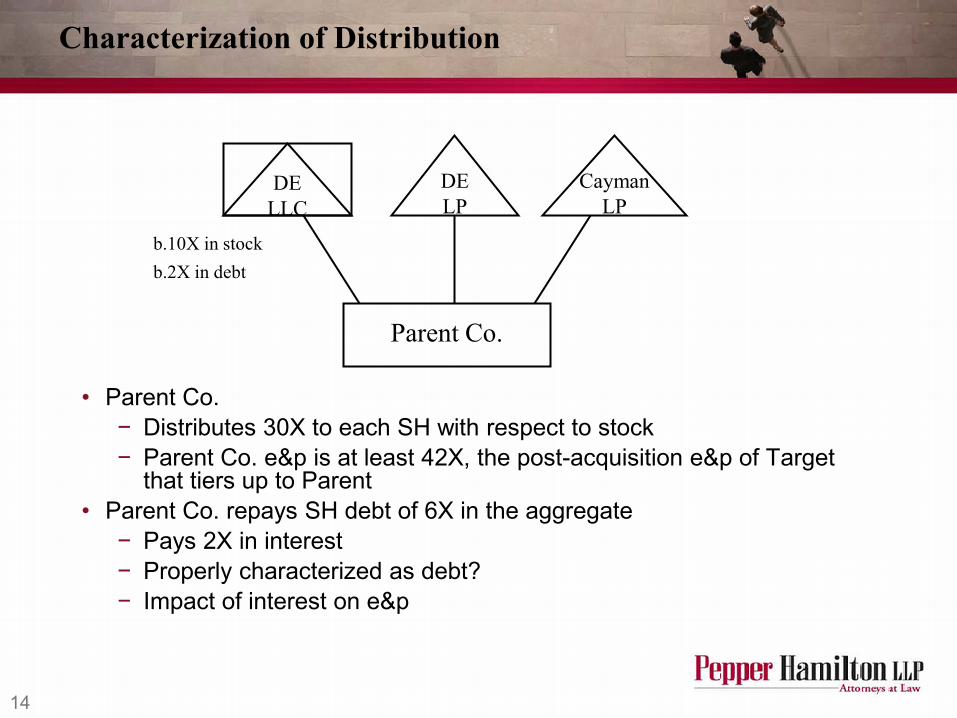

Characterization of Distribution

• Parent Co. − Distributes 30X to each SH with respect to stock − Parent Co. e&p is at least 42X, the post-acquisition e&p of Target

that tiers up to Parent • Parent Co. repays SH debt of 6X in the aggregate

− Pays 2X in interest − Properly characterized as debt? − Impact of interest on e&p

Parent Co.

DE LP

Cayman LP

DE LLC

b.10X in stock b.2X in debt

15

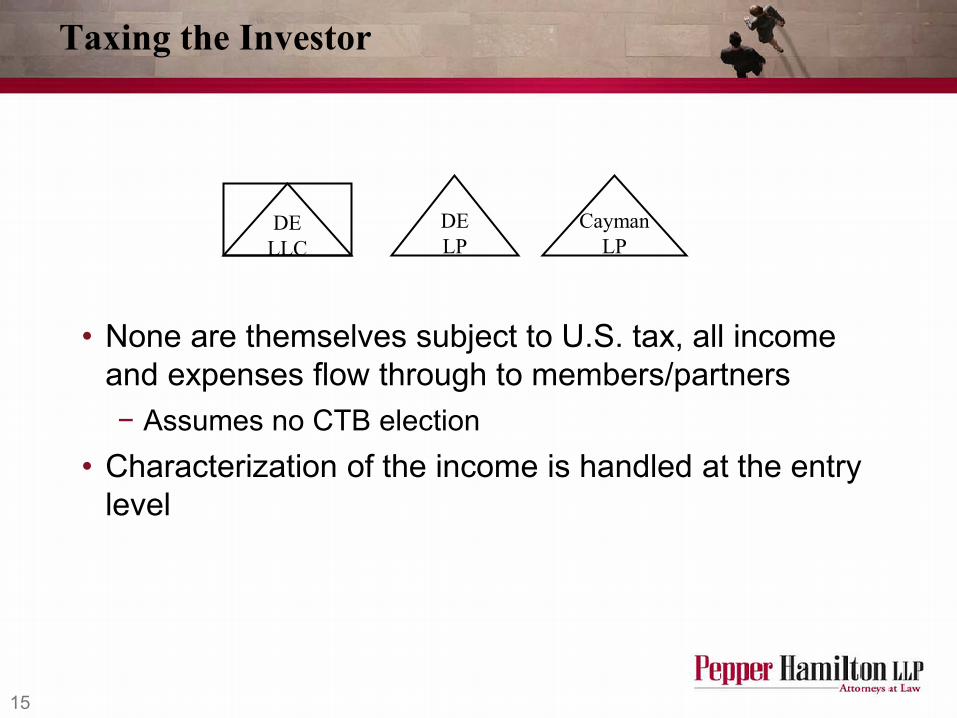

Taxing the Investor

• None are themselves subject to U.S. tax, all income and expenses flow through to members/partners − Assumes no CTB election

• Characterization of the income is handled at the entry level

DE LP

Cayman LP

DE LLC

16

Taxing The Investor

• U.S. individual − 15% on qualified dividend − No tax on return of basis − 35% maximum rate on short term capital gain, − 15% on long term capital gain − 35% maximum rate on interest

• U.S. corporate − 35% maximum rate or dividends (subject to dividend received

deduction) − No tax on return of basis − 35% maximum rate on capital gains − 35% maximum rate on interest

• U.S. tax exempts − So long as not debt funded, interest, dividend and capital

gains are not taxable

17

Taxing the Investor

• Non-U.S. persons − 30% tax on dividend

• Limited by e&p − No tax on return of basis − No tax on capital gains (unless FIRPTA) − Generally, 30% on interest, unless it is portfolio interest

18

Taxing the Investor

• Exceptions − Reduced rate of tax on dividends and interest under

applicable tax treaties − 80/20 companies

• More than 25% of gross income for prior three years from foreign sources – from active conduct of business outside U.S.

• Rarely, capital gains can be taxed to individual resident in U.S. for more than 183 days, or if the capital gains are connected to a U.S. business of investor

19

Collecting The Tax - Distribution

• All withholding agents are responsible for collecting the 30% tax from the payment and timely depositing it with IRS. §1.1441.1

• Withholding agent − Any person who has control over the funds − Parent, DE LLC, DE LP, Cayman LP are all withholding

agents

20

Parent Withholding

• If Parent receives a W-9 from DE LLC or DE LP, certifying that it is a U.S. person, Parent has no withholding obligation unless Parent knows the form to be untrue

• Cayman LP is a non-U.S. person − Unless Parent receives required information, there is

30% withholding on the dividend • Dividend is the distribution supported by e&p

− In our example, distribution of 30X, 14X is a dividend

21

Limiting The Tax

• Cayman LP timely provides Parent with W-81MY, on which it certifies that − it is a foreign person − it is not the beneficial owner of the income − it is a partnership

• Cayman LP also provides Parent with − fully executed W-9 from U.S. investor − fully executed W-8BEN from foreign investor who is beneficial

owner of the distribution • If foreign investor is also an intermediary; keep going up the chain

− Statement showing respective ownership interests of investors • Qualified Partnership status may minimize forms

22

Limiting The Tax

• If Parent timely receives the forms, and does not know they are incorrect: − The portion of the distribution allocable to U.S. investor

is not subject to 30% withholding tax − Portion attributable to the foreign investor is subject to

the 30% withholding tax unless it may claim the benefit of a tax treaty

• To claim treaty benefit − Form W-8BEN must have EIN or ITIN for foreign

investor, unless Parent is publicly traded − Form W-8BEN must claim the treaty benefit

23

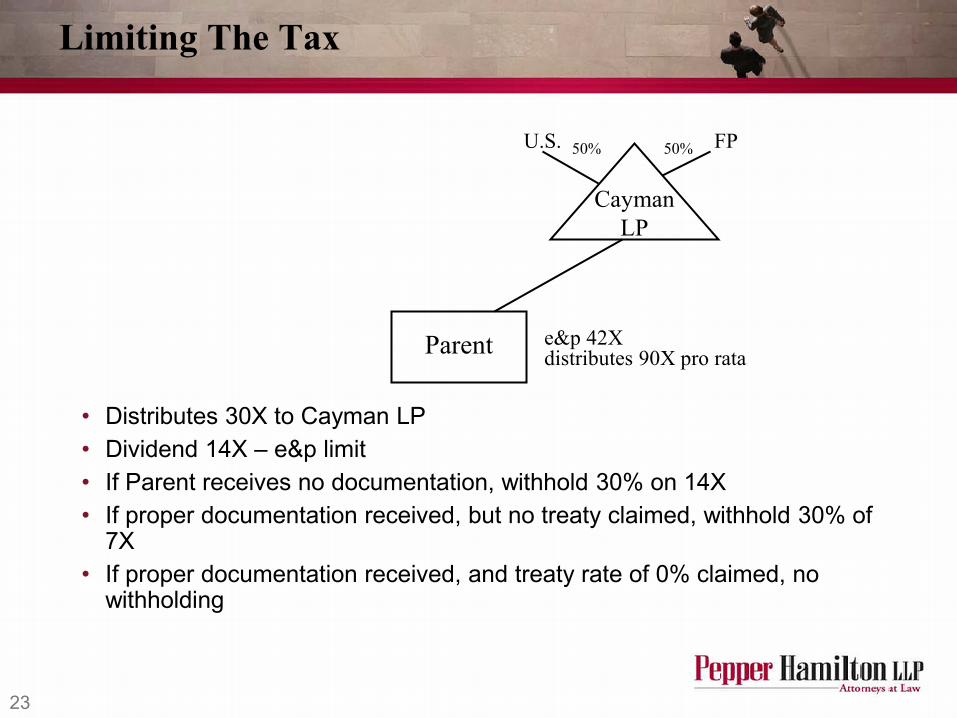

Limiting The Tax

• Distributes 30X to Cayman LP • Dividend 14X – e&p limit • If Parent receives no documentation, withhold 30% on 14X • If proper documentation received, but no treaty claimed, withhold 30% of

7X • If proper documentation received, and treaty rate of 0% claimed, no

withholding

Parent

Cayman LP

FP U.S.

e&p 42X distributes 90X pro rata

50% 50%

24

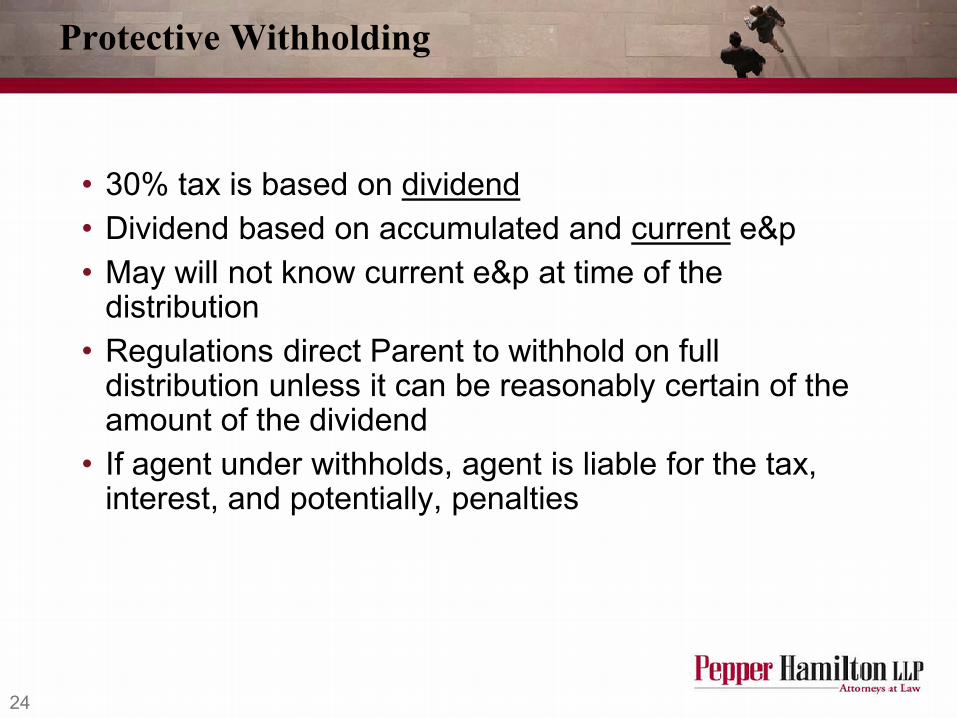

Protective Withholding

• 30% tax is based on dividend • Dividend based on accumulated and current e&p • May will not know current e&p at time of the

distribution • Regulations direct Parent to withhold on full

distribution unless it can be reasonably certain of the amount of the dividend

• If agent under withholds, agent is liable for the tax, interest, and potentially, penalties

25

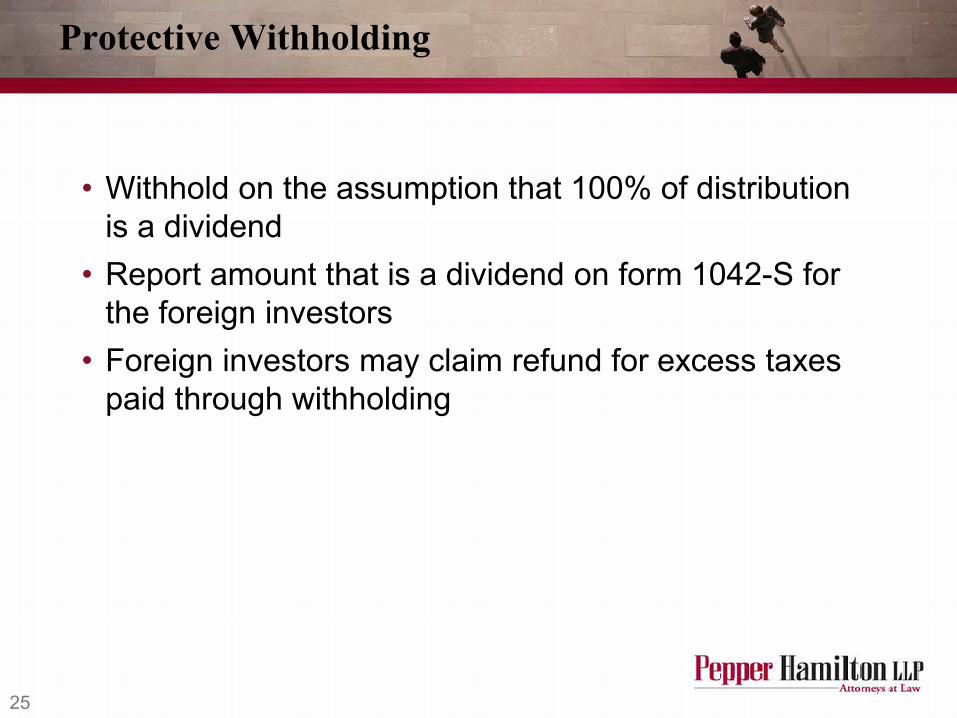

Protective Withholding

• Withhold on the assumption that 100% of distribution is a dividend

• Report amount that is a dividend on form 1042-S for the foreign investors

• Foreign investors may claim refund for excess taxes paid through withholding

26

Not So Protective Withholding

• Withhold based on reasonable expectation of e&p − Require Cayman LP on Foreign Investor to indemnify

Parent if not accurate and additional taxes are due − Value of indemnification?

27

Fund Withholding

• Delaware LP receives distribution free of withholding • Delaware LP must withhold on the portion of the

dividend that is allocable to foreign investor − Withholding occurs at earlier of date of distribution or

date on which form K-1 is to be distributed to partners − No ordering rule for distributions. Conservative view –

first distribution after receipt of dividend is subject to withholding

28

Fund Withholding

• Delaware LP may reasonably rely on statement from Parent as to portion of the distribution that is a dividend − If wrong, Delaware LP and Parent are liable for under

withheld taxes • Delaware LP may withhold on assumption that full

distribution is a dividend; LPs may then file for refunds

29

Fund Withholding

• Delaware LP withholds at 30% on payment to foreign investor unless Delaware LP − receives properly executed form W-8BEN claiming

treaty benefits to reduce tax rate or, − Receives W-8IMY, if foreign investor is not beneficial

owner, and supporting documents that may be relied upon to exempt (or reduce the rate of) the foreign investors from U.S. tax.

30

Fund Compliance

• Delaware LLC − From a withholding perspective, same issues as in

Delaware LP − Question is whether foreign investor may provide LLC

with W-8BEN on which the benefits of a tax treaty are claimed

• §894(c) concerns

31

Fund Compliance

• §1.894-1(d) − Foreign person may not claim treaty benefits unless the

income is derived by the person − Entity may claim benefits only if it is not fiscally

transparent under home county rules − Investor may “derive” the income if the entity is fiscally

transparent as to the investor − “Derived” means taxable when income is paid to the

entity

32

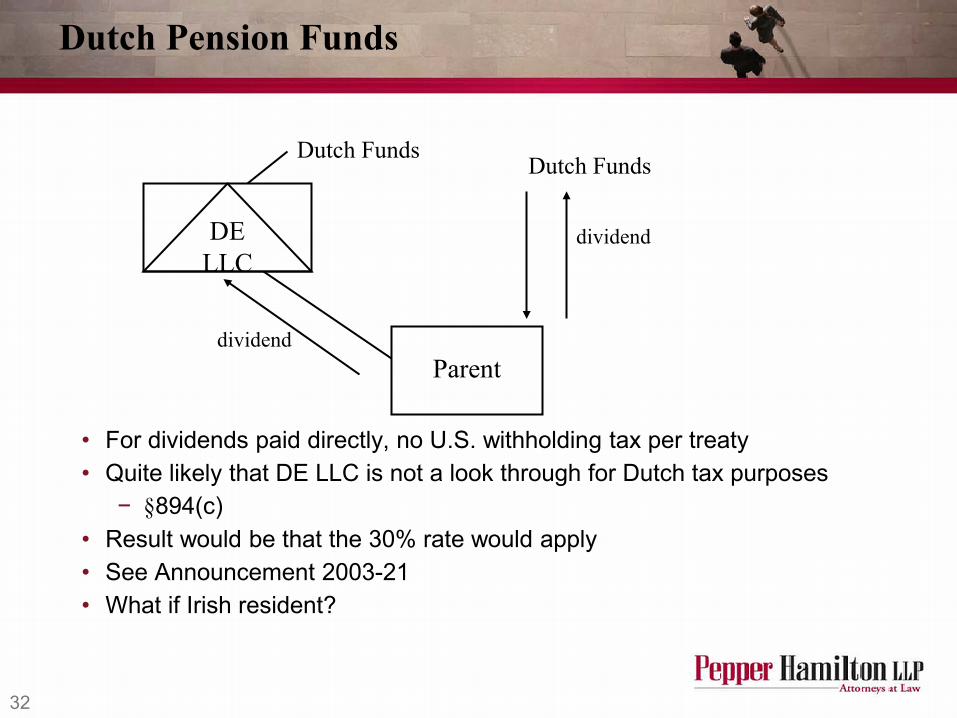

Dutch Pension Funds

• For dividends paid directly, no U.S. withholding tax per treaty • Quite likely that DE LLC is not a look through for Dutch tax purposes

− §894(c) • Result would be that the 30% rate would apply • See Announcement 2003-21 • What if Irish resident?

Parent

DE LLC

Dutch Funds

dividend

dividend

Dutch Funds

33

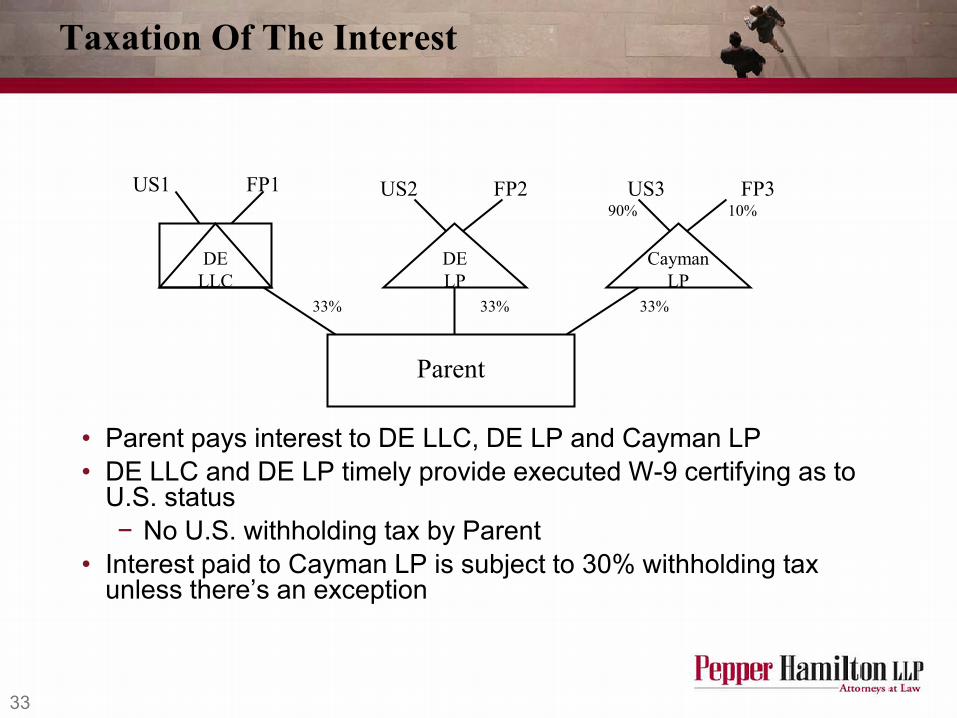

Taxation Of The Interest

• Parent pays interest to DE LLC, DE LP and Cayman LP • DE LLC and DE LP timely provide executed W-9 certifying as to

U.S. status − No U.S. withholding tax by Parent

• Interest paid to Cayman LP is subject to 30% withholding tax unless there’s an exception

Parent

DE LP

Cayman LP

DE LLC

FP3 US3 FP2 US2 FP1 US1

33% 33% 33%

90% 10%

34

Taxation Of The Interest

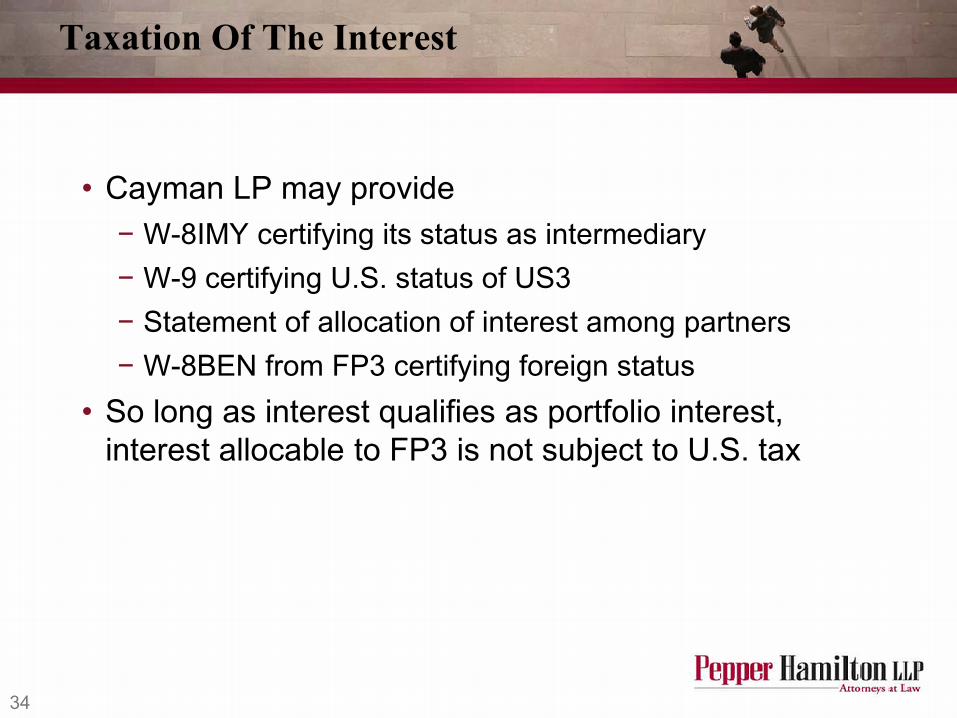

• Cayman LP may provide − W-8IMY certifying its status as intermediary − W-9 certifying U.S. status of US3 − Statement of allocation of interest among partners − W-8BEN from FP3 certifying foreign status

• So long as interest qualifies as portfolio interest, interest allocable to FP3 is not subject to U.S. tax

35

Portfolio Interest

• Debt in “registered form” − Bears bonds only if issued outside U.S. − Must know owners

• Amount of interest not “contingent” • Recipient must be foreign person • Recipient not a CFC • Recipient not a 10% owner of Parent equity

− 10% ownership is tested at partner, not partnership level. §1.871-14

− Cayman LP owns > 10%, but FP3 owns 10% of 33%, or 3.3%

36

Portfolio Interest

• Testing for 10% − Done at time withholding would have been required

• Distributed from fund • K-1 due date

− Practical application?

37

Reporting

• Portfolio Interest through LP and LLC • Reporting at Parent level • Reporting at Fund level • Audit risks

38

Part II - FATCA

39

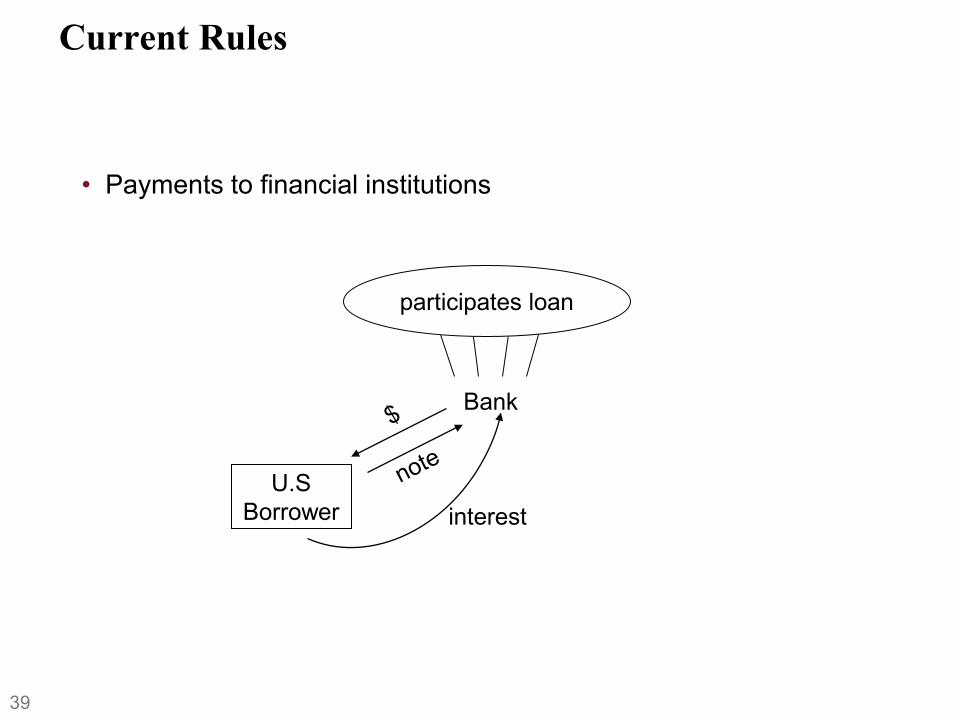

Current Rules

• Payments to financial institutions

Bank

U.S Borrower interest

participates loan

40

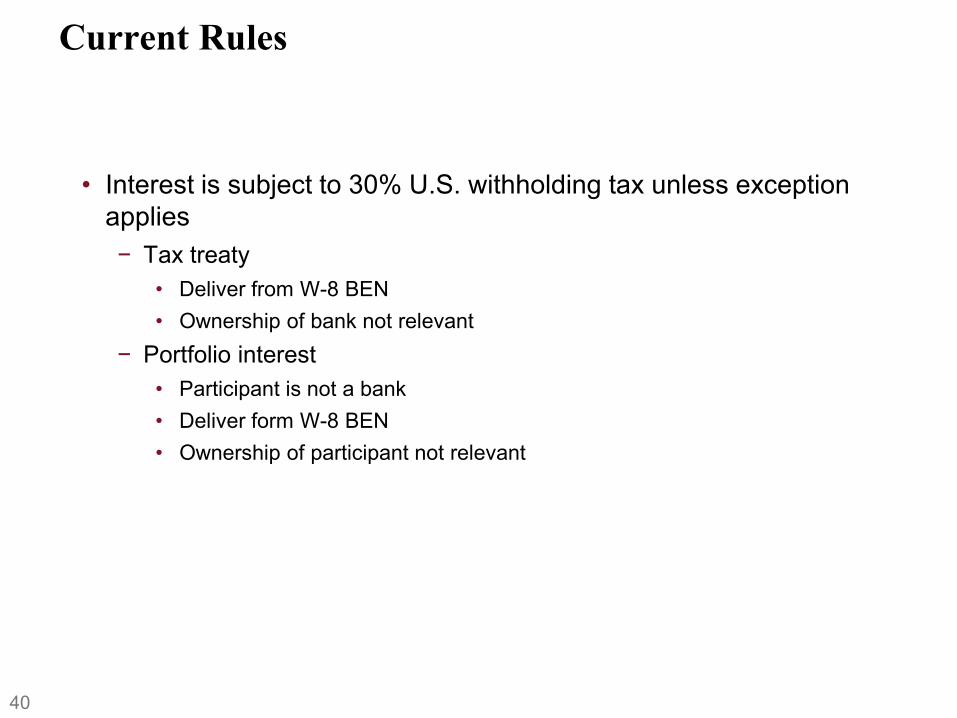

Current Rules

• Interest is subject to 30% U.S. withholding tax unless exception applies − Tax treaty

• Deliver from W-8 BEN • Ownership of bank not relevant

− Portfolio interest • Participant is not a bank • Deliver form W-8 BEN • Ownership of participant not relevant

41

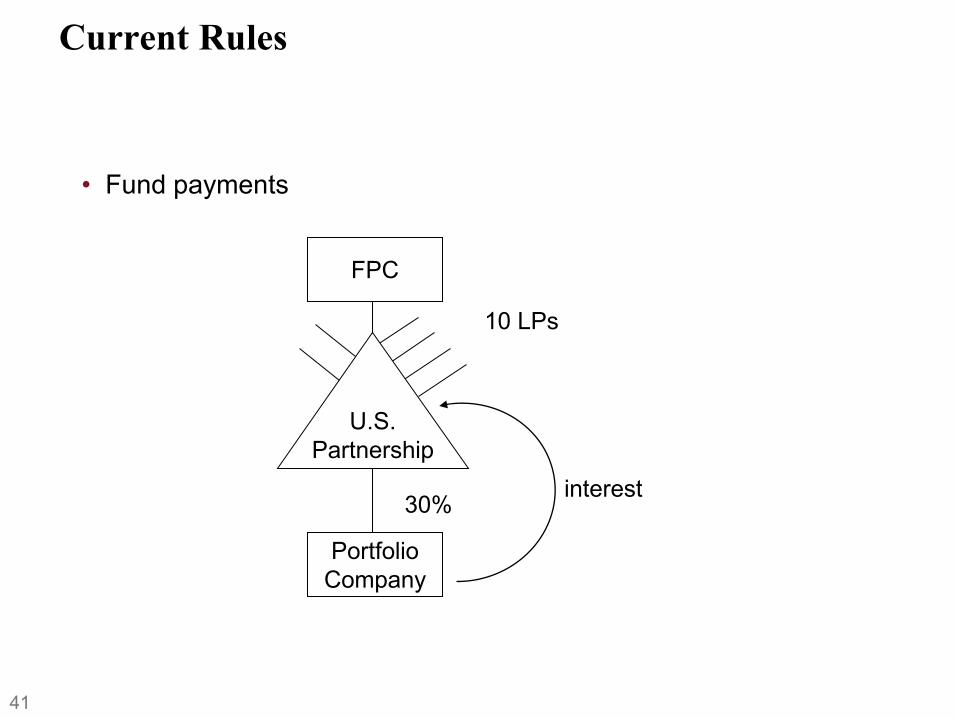

Current Rules

• Fund payments

10 LPs

interest 30%

FPC

Portfolio Company

U.S. Partnership

42

Current Rules

• U.S. partnership gave PC W-9, certifying U.S. person • U.S. partnership had W-8 BEN from FPC

− No withholding as portfolio interest − Ownership of FPC not relevant

43

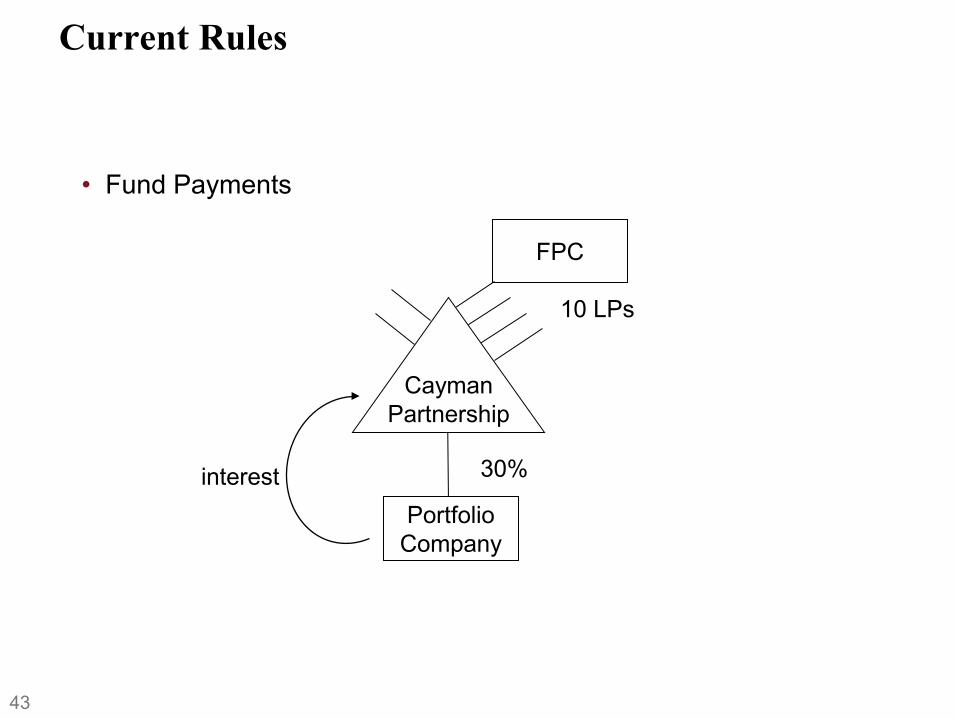

Current Rules

• Fund Payments

10 LPs

interest 30%

FPC

Portfolio Company

Cayman Partnership

44

Current Rules

• Cayman Partnership provides W-8 IMY and W-8 BEN from FPC (and other LPs) − No withholding as interest is all portfolio interest − Ownership of FPC not relevant

45

Current Rules

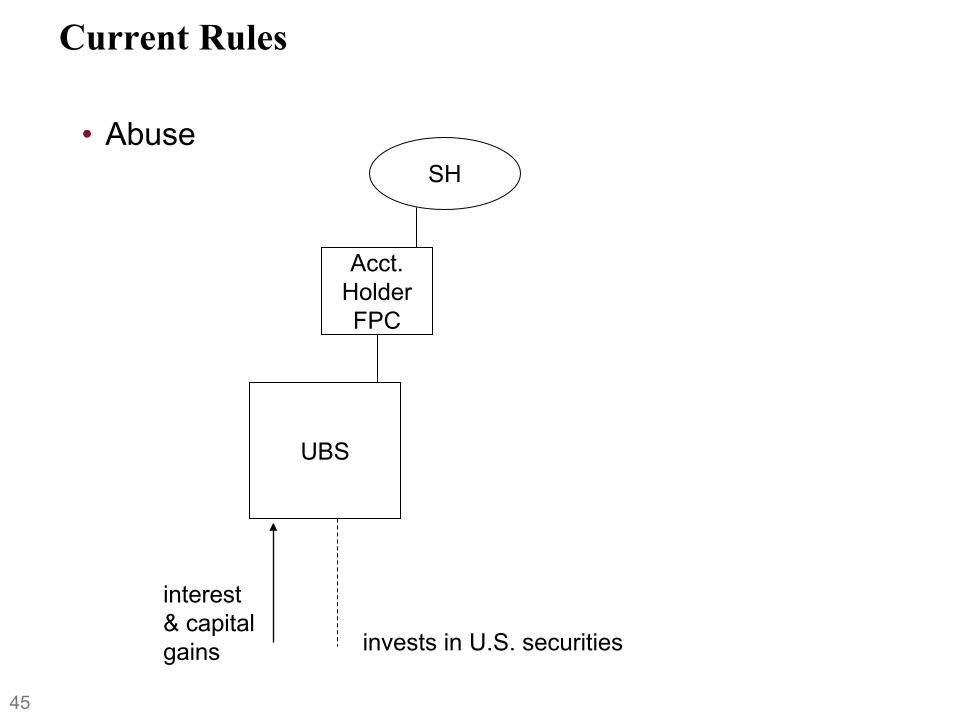

• Abuse

Acct. Holder FPC

SH

UBS

interest & capital gains invests in U.S. securities

46

Current Rules

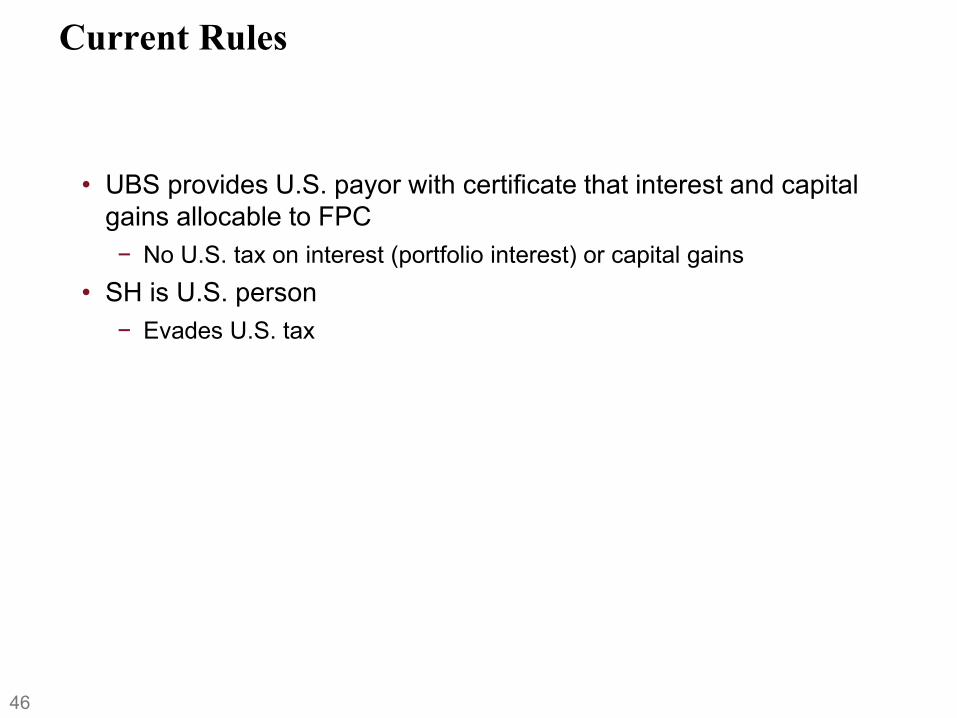

• UBS provides U.S. payor with certificate that interest and capital gains allocable to FPC − No U.S. tax on interest (portfolio interest) or capital gains

• SH is U.S. person − Evades U.S. tax

47

Current Rules

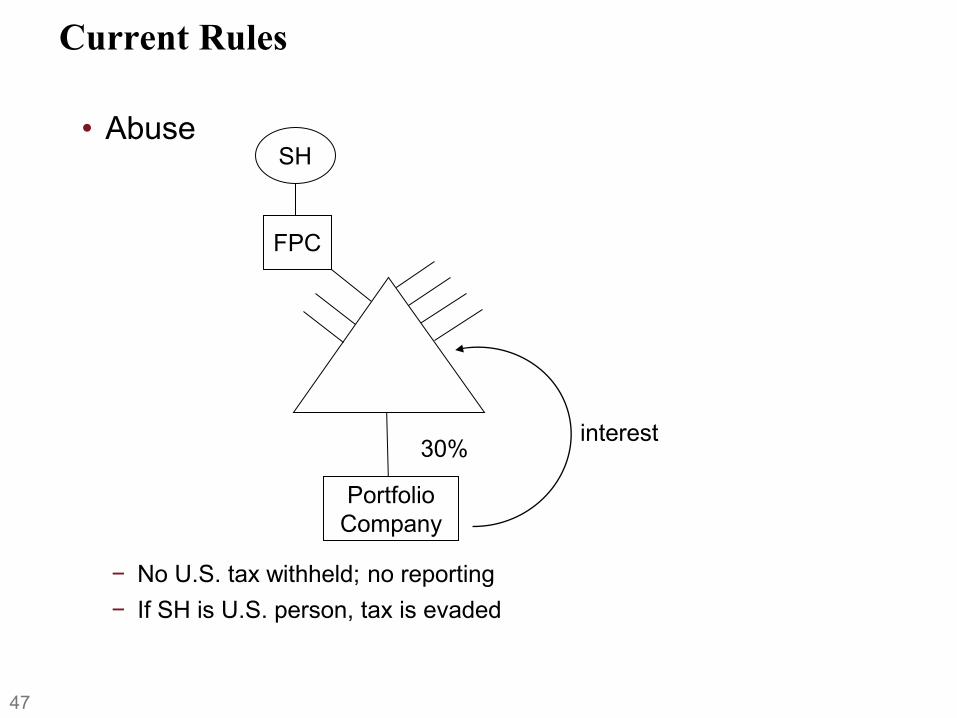

• Abuse

interest 30%

FPC

Portfolio Company

SH

− No U.S. tax withheld; no reporting − If SH is U.S. person, tax is evaded

48

FATCA(T)

• Imposes new reporting and withholding tax regime on payments of U.S. source “withholdable payments” to foreign entities

• The world is divided into − Foreign financial institutions (“FFI”) − Non financial foreign entities (“NFFE”)

• Effective date − Generally for payments made after 12/31/2012 − No FATCA withholding on “obligations” that are outstanding on or

before March 18, 2012

49

FATCA(T)

• New Regime − Payments of “withholdable payments” to foreign entities subject to

30% withholding tax unless recipient agrees to comply with new disclosure rules

• Withholdable payment − U.S. Source Interest (including portfolio interest), dividends, and

other fixed determinable annual or periodic income AND − Gross proceeds from the disposition of property (stocks or bonds)

that can produce U.S. source interest or dividends

50

Payments to FFI

• Withholdable payment subject to 30% withholding unless − FFI enters into agreement with IRS to disclose information about

certain U.S. account holders, including name, address, account balance, gross receipts, OR

− FFI agrees to be treated as a U.S. financial institution and treat each holder of a U.S. account that is a specified holder as a U.S. person, and thus being subject to 1099 reporting, etc. Eliminates need to report account balance

− Known as 1471(b) agreements

51

What is an FFI?

• Foreign bank, foreign custodian and foreign entities “primarily engaged in the business of investing, re-investing or trading in securities, partnership interests or commodities or any interest in such items − Includes foreign hedge funds, foreign private equity funds, − “Foreign Entity” means any entity that is not a U.S. person

• Place of organization key for corporations and partnerships

52

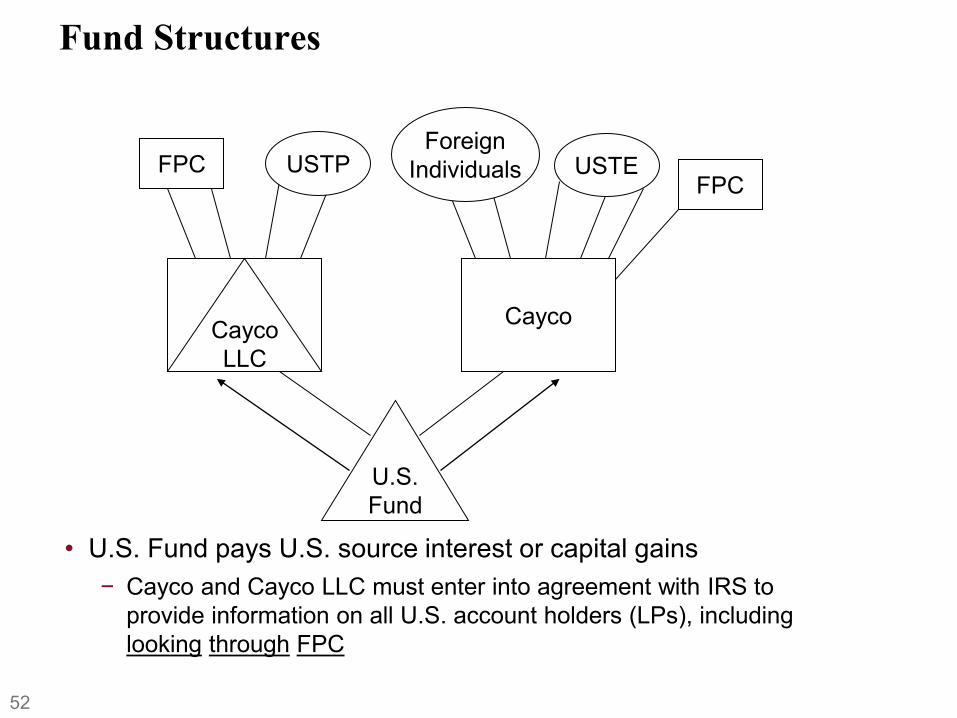

Fund Structures

• U.S. Fund pays U.S. source interest or capital gains − Cayco and Cayco LLC must enter into agreement with IRS to

provide information on all U.S. account holders (LPs), including looking through FPC

Cayco Cayco LLC

U.S. Fund

FPC FPC USTE

Foreign Individuals USTP

53

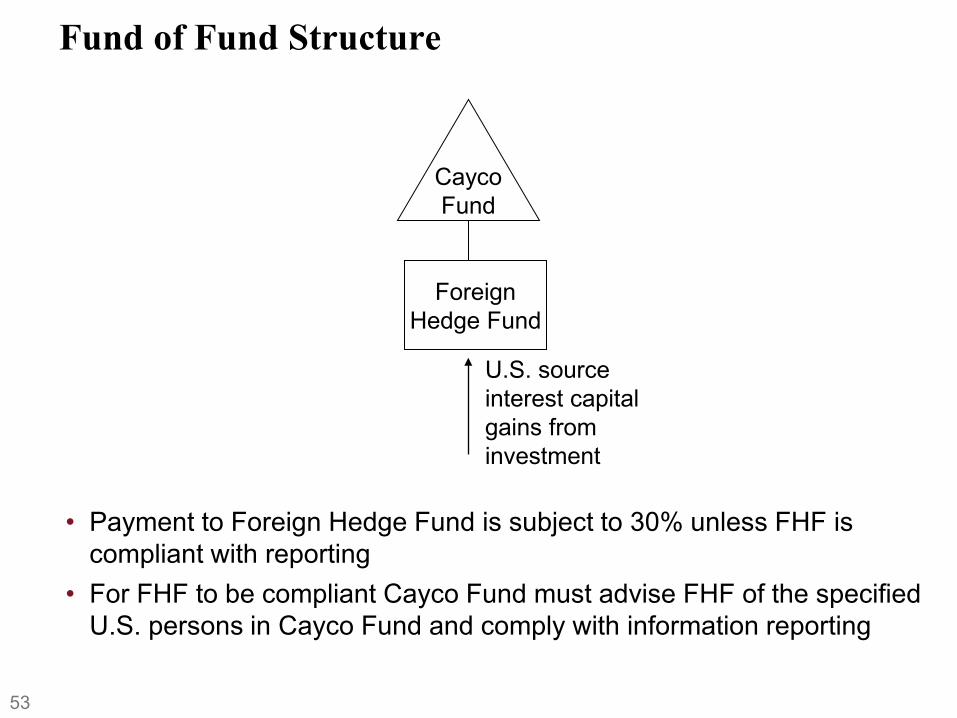

Fund of Fund Structure

• Payment to Foreign Hedge Fund is subject to 30% unless FHF is compliant with reporting

• For FHF to be compliant Cayco Fund must advise FHF of the specified U.S. persons in Cayco Fund and comply with information reporting

Cayco Fund

Foreign Hedge Fund

U.S. source interest capital gains from investment

54

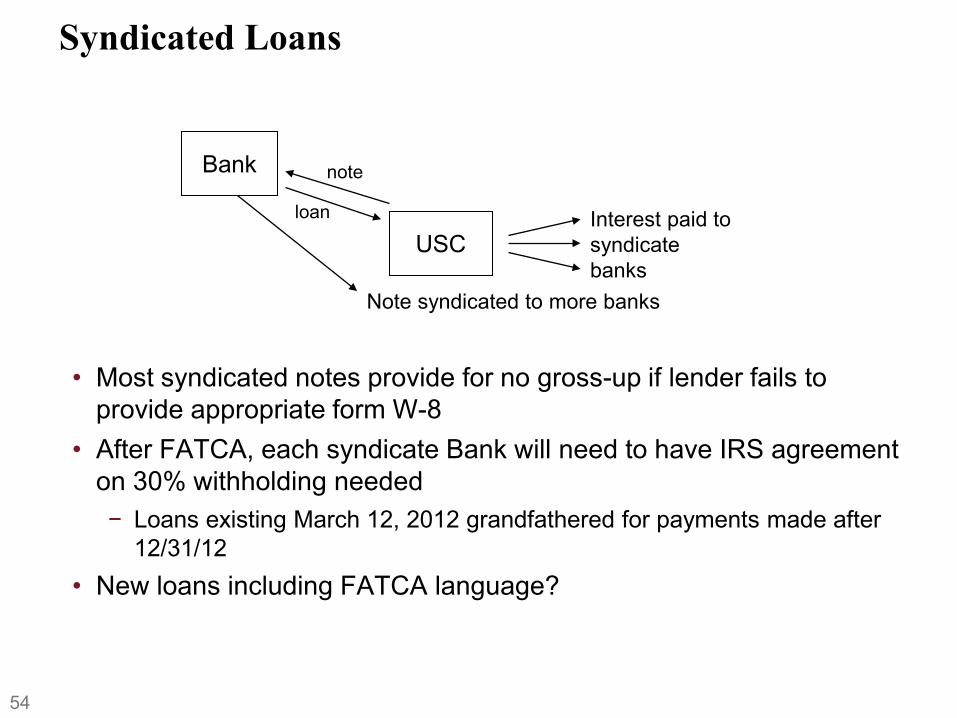

Syndicated Loans

• Most syndicated notes provide for no gross-up if lender fails to provide appropriate form W-8

• After FATCA, each syndicate Bank will need to have IRS agreement on 30% withholding needed − Loans existing March 12, 2012 grandfathered for payments made after

12/31/12 • New loans including FATCA language?

Bank

USC

note

loan

Note syndicated to more banks

Interest paid to syndicate banks

55

FATCA and Treaties

• The §1471 withholding is independent of treaties • If the 30% is withheld, FFI can claim refund based on treaty, but no

interest will be paid with respect to the refund • To claim refund, must prove FFI is not U.S. owned foreign entity

56

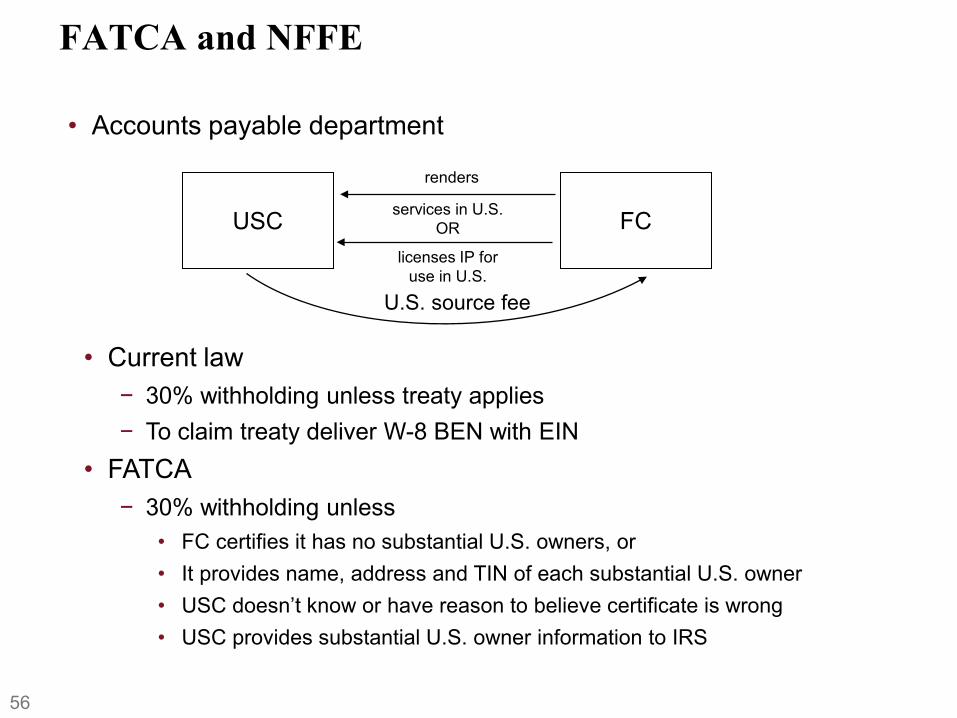

FATCA and NFFE

• Accounts payable department

• Current law − 30% withholding unless treaty applies − To claim treaty deliver W-8 BEN with EIN

• FATCA − 30% withholding unless

• FC certifies it has no substantial U.S. owners, or • It provides name, address and TIN of each substantial U.S. owner • USC doesn’t know or have reason to believe certificate is wrong • USC provides substantial U.S. owner information to IRS

USC FC

renders

services in U.S. OR

licenses IP for use in U.S.

U.S. source fee

57

Part III – Reporting Uncertain Tax Positions

58

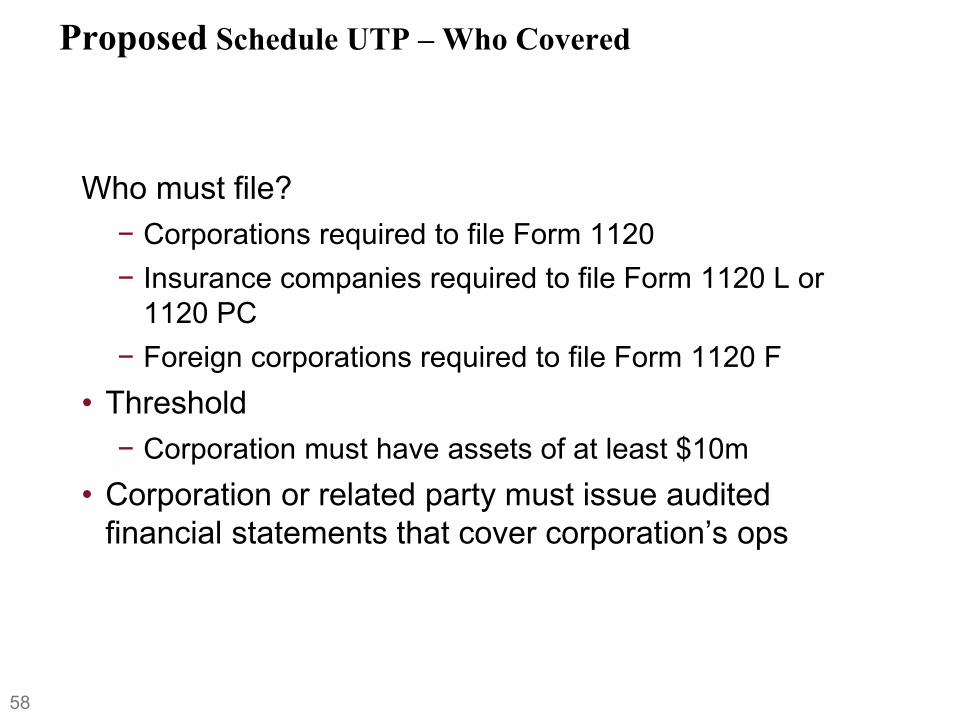

Proposed Schedule UTP – Who Covered

Who must file? − Corporations required to file Form 1120 − Insurance companies required to file Form 1120 L or

1120 PC − Foreign corporations required to file Form 1120 F

• Threshold − Corporation must have assets of at least $10m

• Corporation or related party must issue audited financial statements that cover corporation’s ops

59

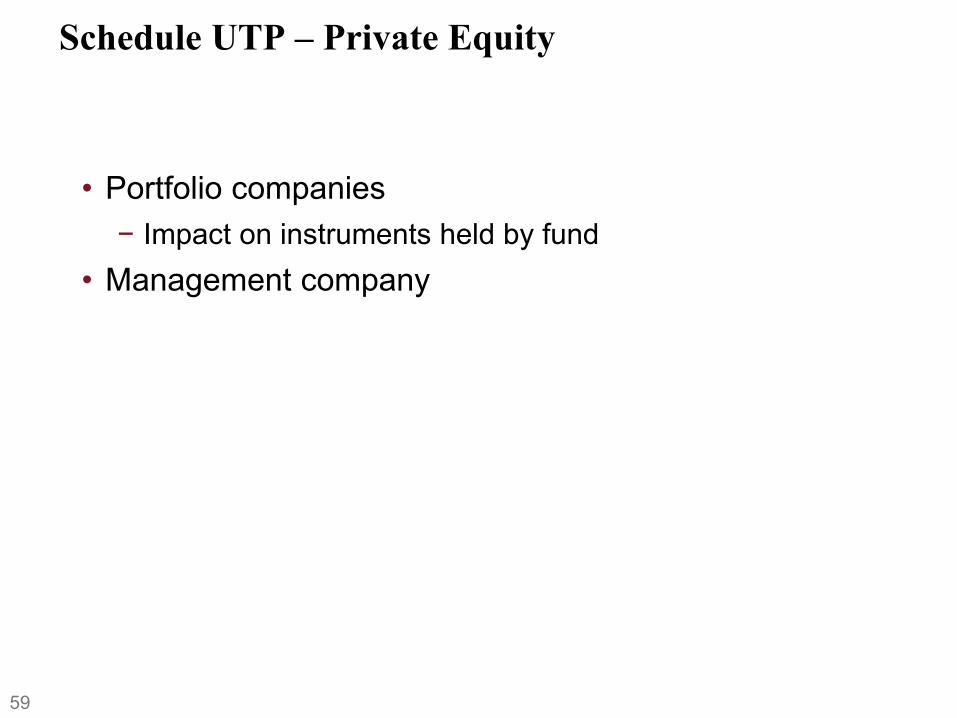

Schedule UTP – Private Equity

• Portfolio companies − Impact on instruments held by fund

• Management company

60

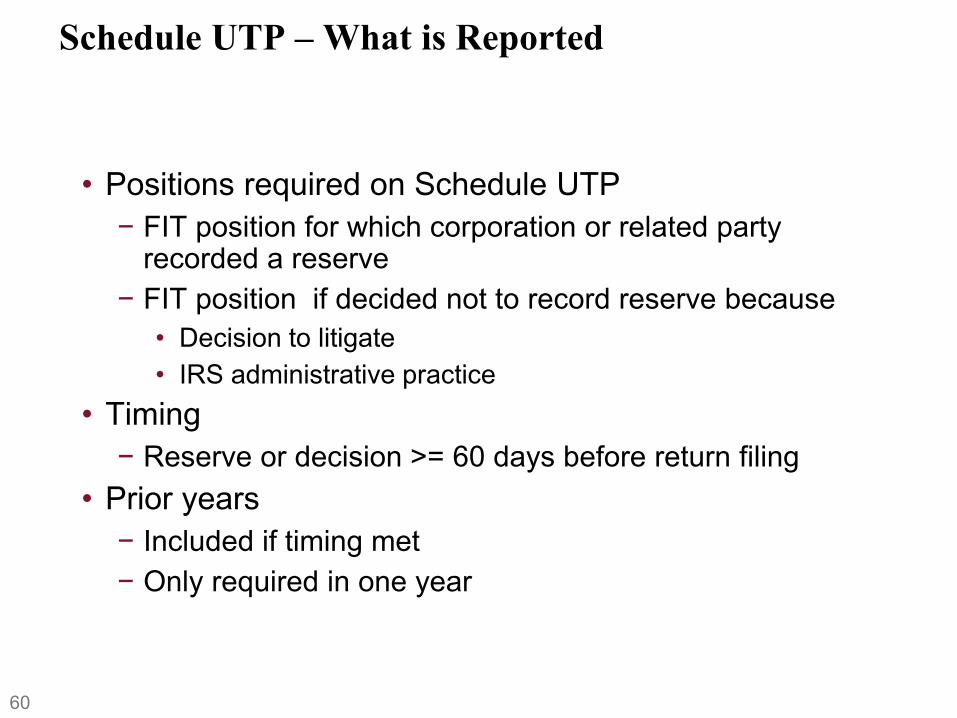

Schedule UTP – What is Reported

• Positions required on Schedule UTP − FIT position for which corporation or related party

recorded a reserve − FIT position if decided not to record reserve because

• Decision to litigate • IRS administrative practice

• Timing − Reserve or decision >= 60 days before return filing

• Prior years − Included if timing met − Only required in one year

61

Schedule UTP – Info on Schedule

• Primary Code section involved • Whether permanent or temporary • TIN of pass through entity • Maximum tax adjustment • Concise description of UTP

62

Part IV - FBAR

63

FBAR Filing Requirement

• Form TD F 90-22.1 • Due June 30 • Must be received by June 30 (no timely mailing rule

as with most IRS forms)

64

US Persons

• US Citizen • US Resident • Domestic entity

− Includes US LLC that elected to be a DRE • Exclusion for foreign person in and doing business in

the US

65

FBAR Reportable Accounts

• Bank • Securities brokerage • Commodities future or option and other financial

accounts in foreign country • CDs • Checking accounts • Mutual funds or similar pooled funds that issues

shares available to the general public with regular asset valuations and regular redemption periods

• NOT hedge, venture or private equity funds (though being considered)

66

Financial Interest in Foreign Account

• Owner of record or legal title even if not beneficial owner

• Beneficial owner • In a financial account of corporation if own (directly or

indirectly) > 50% voting power in corp. • In a financial account of partnership if own (directly or

indirectly) > 50% of capital or profits of partnership • In a financial account of another entity if own > 50%

voting power, total value of equity, assets or interests in profits

67

Deemed Financial Interest

• Trust settlor if deemed to be owner • Beneficial interest in > 50% of the assets of trust or

receives > 50% of the current income of trust

68

Signature Authority

• Officers or employees that have signature or other authority over a foreign financial account may be required to file FBAR

• Exception for certain persons with no financial interest in account

• Extension of deadline to June 30, 2011 if no financial interests

69

BERWYN 400 Berwyn Park 899 Cassatt Road

Berwyn, PA 19312-1183 610.640.7800

FAX 610.640.7835

BOSTON 15th Floor, Oliver Street Tower

125 High Street Boston, MA 02110-2736

617.204.5100 FAX 617.204.5150

DETROIT Suite 3600

100 Renaissance Center Detroit, MI 48243-1157

313.259.7110 FAX 313.259.7926

HARRISBURG Suite 200

100 Market Street P.O. Box 1181

Harrisburg, PA 17108-1181 717.255.1155

FAX 717.238.0575

NEW YORK The New York Times Building

37th Floor, 620 Eighth Ave New York, NY 10018-1405

212.808.2700 FAX 212.286.9806

ORANGE COUNTY Suite 1200

4 Park Plaza Irvine, CA 92614-5955

949.567.3500 FAX 949.863.0151

PHILADELPHIA 3000 Two Logan Square

Eighteenth and Arch Streets Philadelphia, PA 19103-2799

215.981.4000 FAX 215.981.4750

PITTSBURGH 50th Floor

500 Grant Street Pittsburgh, PA 15219-2502

412.454.5000 FAX 412.281.0717

PRINCETON Suite 400

301 Carnegie Center Princeton, NJ 08543-5276

609.452.0808 FAX 609.452.1147

WASHINGTON Hamilton Square

600 Fourteenth Street, N.W. Washington, DC 20005-2004

202.220.1200 FAX 202.220.1665

WILMINGTON Hercules Plaza, Suite 5100

1313 Market Street P.O. Box 1709

Wilmington, DE 19899-1709 302.777.6500

FAX 302.421.8390

www.pepperlaw.com

Our Locations

70

Steven D. Bortnick

• Partner in Tax Practice Group of Pepper Hamilton LLP • Resident in the Princeton and New York offices • Focuses practice on domestic and international tax and private

equity matters • Handles broad range of cross-disciplinary transactions

including asset, stock, cross-border and domestic acquisitions, tax-free spinoffs, recapitalizations and reorganizations

• Experienced in structuring of domestic and international private equity transactions from tax and venture capital operating company standpoints

• Worked with pooled investment vehicles • Counsels corporate entities on tax issues • Advises U.S. citizens and corporations in overseas investment • Involved in formation of private equity and hedge funds

609.951.4117 212.808.2715 [email protected]