Embed Size (px)

Citation preview

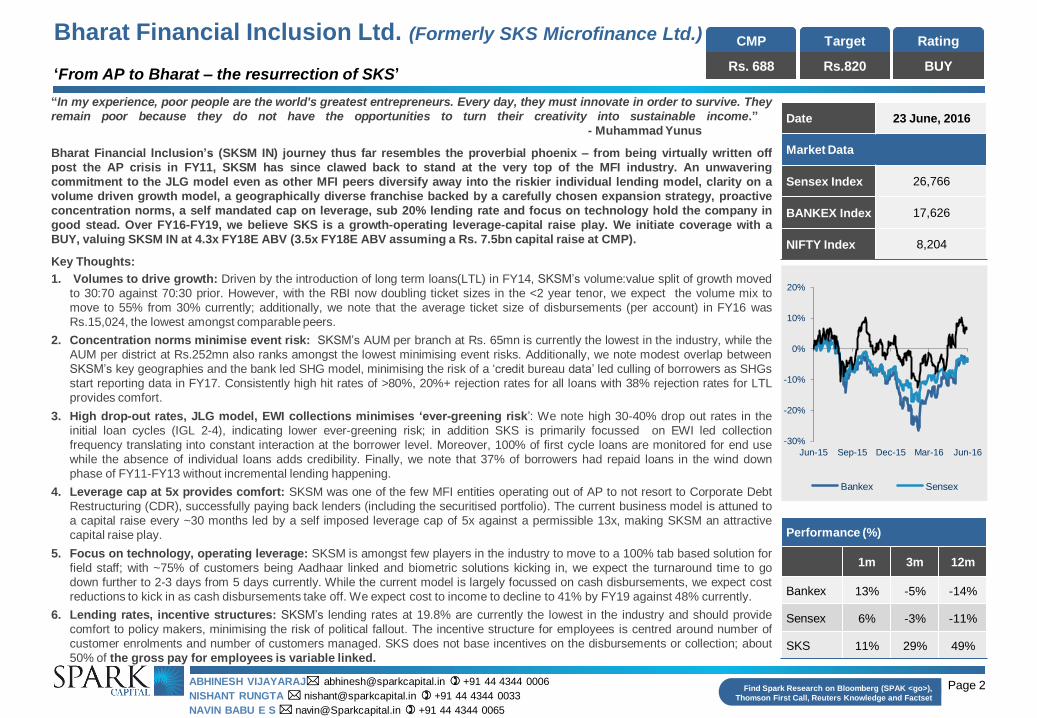

Bharat Financial Inclusion Limited

(Formerly SKS Microfinance Ltd.)

Initiating Coverage

June 2016

Page 2

Bharat Financial Inclusion Ltd. (Formerly SKS Microfinance Ltd.)

‘From AP to Bharat – the resurrection of SKS’

Find Spark Research on Bloomberg (SPAK <go>),

Thomson First Call, Reuters Knowledge and Factset

“In my experience, poor people are the world's greatest entrepreneurs. Every day, they must innovate in order to survive. They

remain poor because they do not have the opportunities to turn their creativity into sustainable income.”

- Muhammad Yunus

Bharat Financial Inclusion’s (SKSM IN) journey thus far resembles the proverbial phoenix – from being virtually written off

post the AP crisis in FY11, SKSM has since clawed back to stand at the very top of the MFI industry. An unwavering

commitment to the JLG model even as other MFI peers diversify away into the riskier individual lending model, clarity on a

volume driven growth model, a geographically diverse franchise backed by a carefully chosen expansion strategy, proactive

concentration norms, a self mandated cap on leverage, sub 20% lending rate and focus on technology hold the company in

good stead. Over FY16-FY19, we believe SKS is a growth-operating leverage-capital raise play. We initiate coverage with a

BUY, valuing SKSM IN at 4.3x FY18E ABV (3.5x FY18E ABV assuming a Rs. 7.5bn capital raise at CMP).

Key Thoughts:

1. Volumes to drive growth: Driven by the introduction of long term loans(LTL) in FY14, SKSM’s volume:value split of growth moved

to 30:70 against 70:30 prior. However, with the RBI now doubling ticket sizes in the <2 year tenor, we expect the volume mix to

move to 55% from 30% currently; additionally, we note that the average ticket size of disbursements (per account) in FY16 was

Rs.15,024, the lowest amongst comparable peers.

2. Concentration norms minimise event risk: SKSM’s AUM per branch at Rs. 65mn is currently the lowest in the industry, while the

AUM per district at Rs.252mn also ranks amongst the lowest minimising event risks. Additionally, we note modest overlap between

SKSM’s key geographies and the bank led SHG model, minimising the risk of a ‘credit bureau data’ led culling of borrowers as SHGs

start reporting data in FY17. Consistently high hit rates of >80%, 20%+ rejection rates for all loans with 38% rejection rates for LTL

provides comfort.

3. High drop-out rates, JLG model, EWI collections minimises ‘ever-greening risk’: We note high 30-40% drop out rates in the

initial loan cycles (IGL 2-4), indicating lower ever-greening risk; in addition SKS is primarily focussed on EWI led collection

frequency translating into constant interaction at the borrower level. Moreover, 100% of first cycle loans are monitored for end use

while the absence of individual loans adds credibility. Finally, we note that 37% of borrowers had repaid loans in the wind down

phase of FY11-FY13 without incremental lending happening.

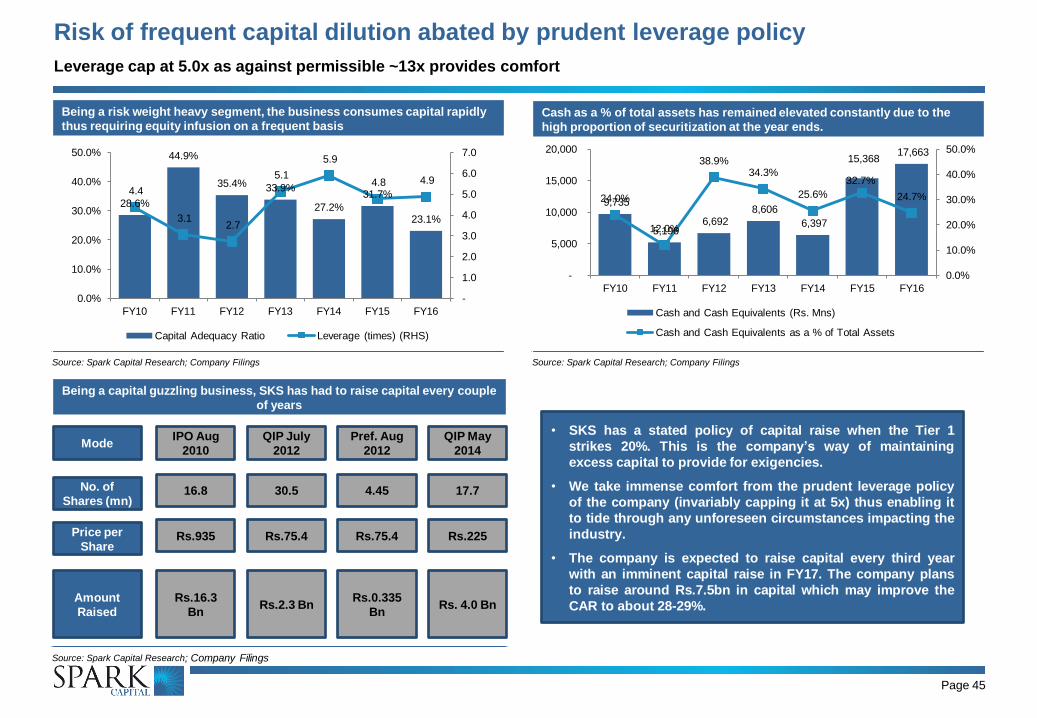

4. Leverage cap at 5x provides comfort: SKSM was one of the few MFI entities operating out of AP to not resort to Corporate Debt

Restructuring (CDR), successfully paying back lenders (including the securitised portfolio). The current business model is attuned to

a capital raise every ~30 months led by a self imposed leverage cap of 5x against a permissible 13x, making SKSM an attractive

capital raise play.

5. Focus on technology, operating leverage: SKSM is amongst few players in the industry to move to a 100% tab based solution for

field staff; with ~75% of customers being Aadhaar linked and biometric solutions kicking in, we expect the turnaround time to go

down further to 2-3 days from 5 days currently. While the current model is largely focussed on cash disbursements, we expect cost

reductions to kick in as cash disbursements take off. We expect cost to income to decline to 41% by FY19 against 48% currently.

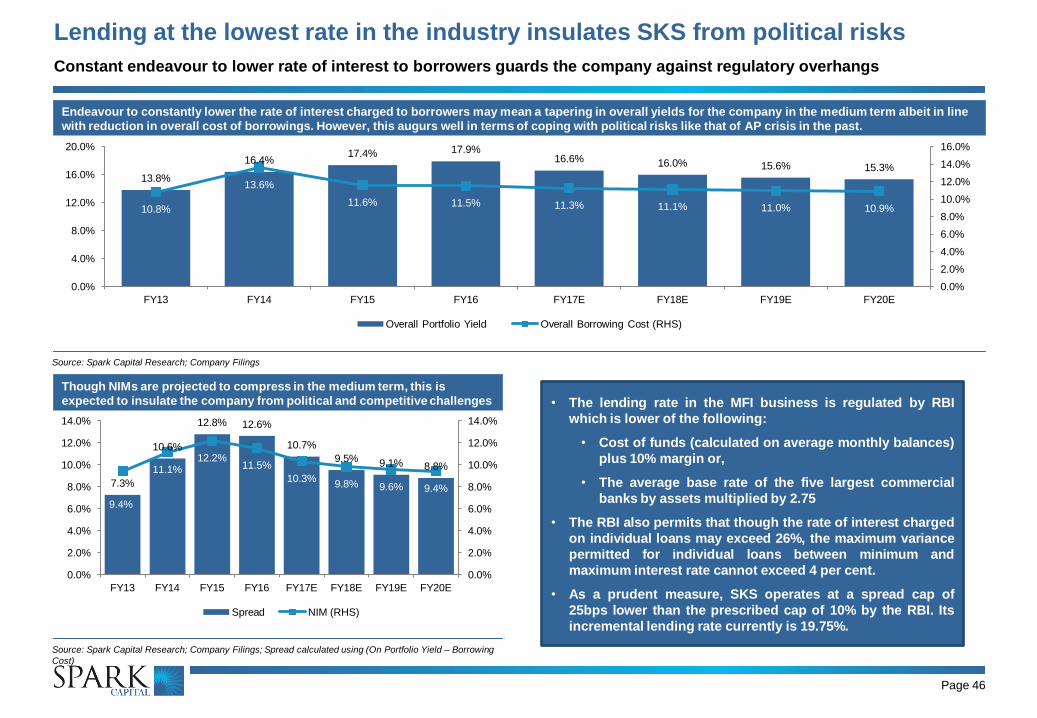

6. Lending rates, incentive structures: SKSM’s lending rates at 19.8% are currently the lowest in the industry and should provide

comfort to policy makers, minimising the risk of political fallout. The incentive structure for employees is centred around number of

customer enrolments and number of customers managed. SKS does not base incentives on the disbursements or collection; about

50% of the gross pay for employees is variable linked.

ABHINESH VIJAYARAJ [email protected] +91 44 4344 0006

NISHANT RUNGTA [email protected] +91 44 4344 0033

NAVIN BABU E S [email protected] +91 44 4344 0065

Performance (%)

1m 3m 12m

Bankex 13% -5% -14%

Sensex 6% -3% -11%

SKS 11% 29% 49%

Date 23 June, 2016

Market Data

Sensex Index 26,766

BANKEX Index 17,626

NIFTY Index 8,204

-30%

-20%

-10%

0%

10%

20%

Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Bankex Sensex

CMP

Rs. 688

Target

Rs.820

Rating

BUY

Page 3

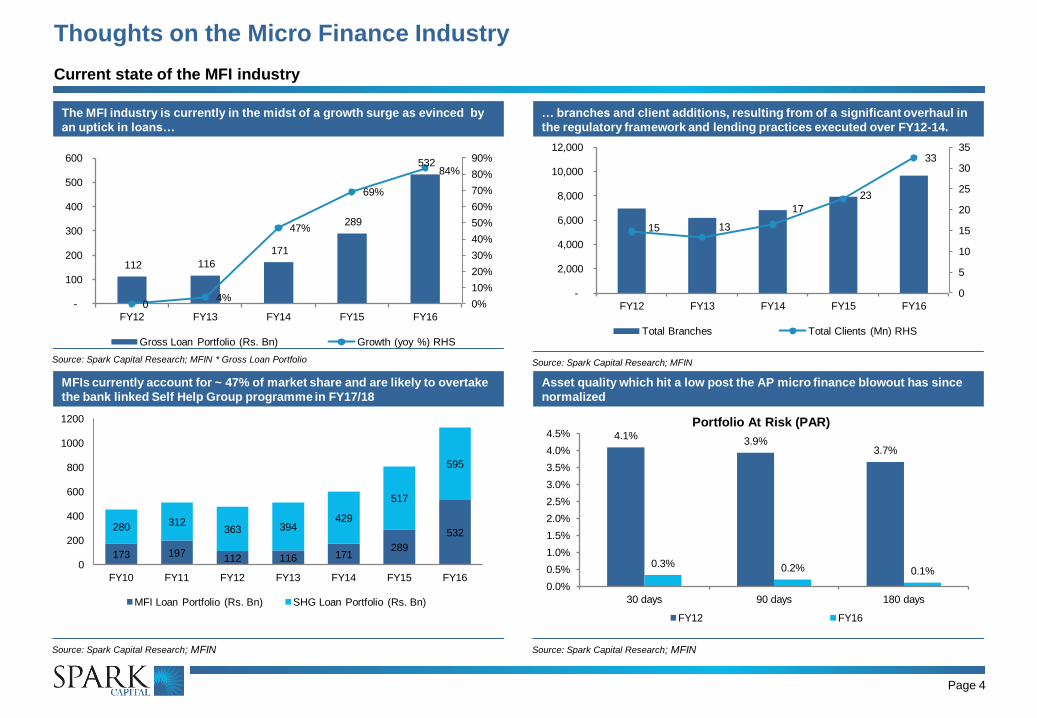

Industry Section

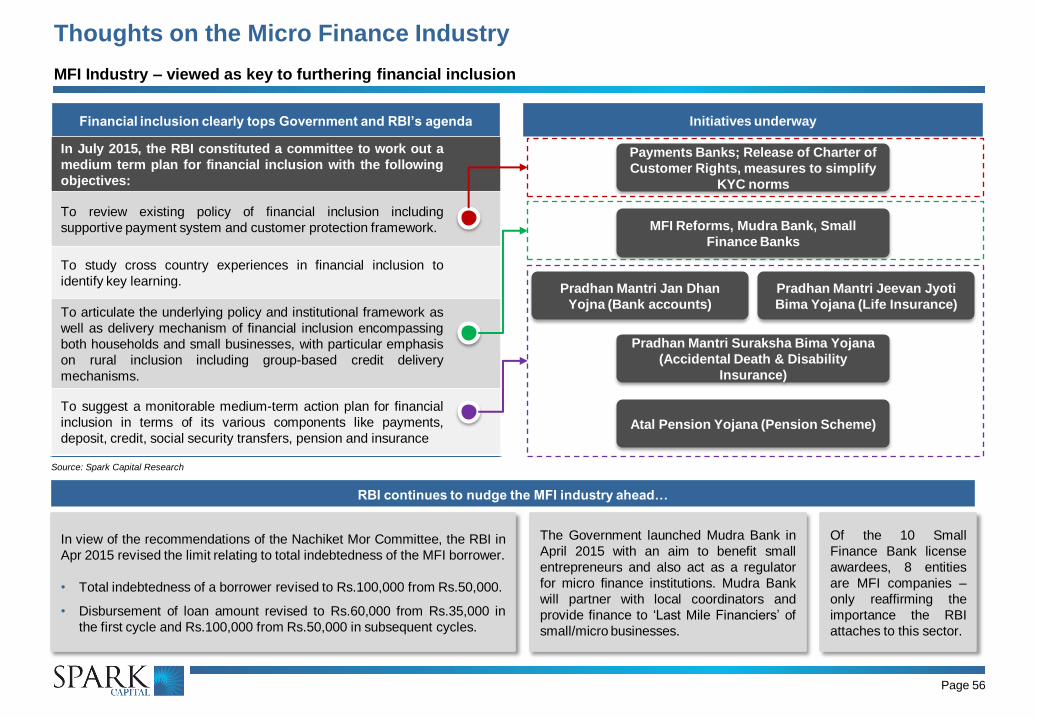

The MFI industry is currently in the midst of a growth surge as evinced by

an uptick in loans…

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

… branches and client additions, resulting from of a significant overhaul in

the regulatory framework and lending practices executed over FY12-14.

Source: Spark Capital Research; MFIN

Page 4

Asset quality which hit a low post the AP micro finance blowout has since

normalized

Source: Spark Capital Research; MFIN

MFIs currently account for ~ 47% of market share and are likely to overtake

the bank linked Self Help Group programme in FY17/18

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

Current state of the MFI industry

112 116

171

289

532

0 4%

47%

69%

84%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

100

200

300

400

500

600

FY12 FY13 FY14 FY15 FY16

Gross Loan Portfolio (Rs. Bn) Growth (yoy %) RHS

15 13

17

23

33

0

5

10

15

20

25

30

35

-

2,000

4,000

6,000

8,000

10,000

12,000

FY12 FY13 FY14 FY15 FY16

Total Branches Total Clients (Mn) RHS

4.1% 3.9%

3.7%

0.3% 0.2% 0.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

30 days 90 days 180 days

Portfolio At Risk (PAR)

FY12 FY16

173 197 112 116 171

289

532 280 312

363 394 429

517

595

0

200

400

600

800

1000

1200

FY10 FY11 FY12 FY13 FY14 FY15 FY16

MFI Loan Portfolio (Rs. Bn) SHG Loan Portfolio (Rs. Bn)

Page 5

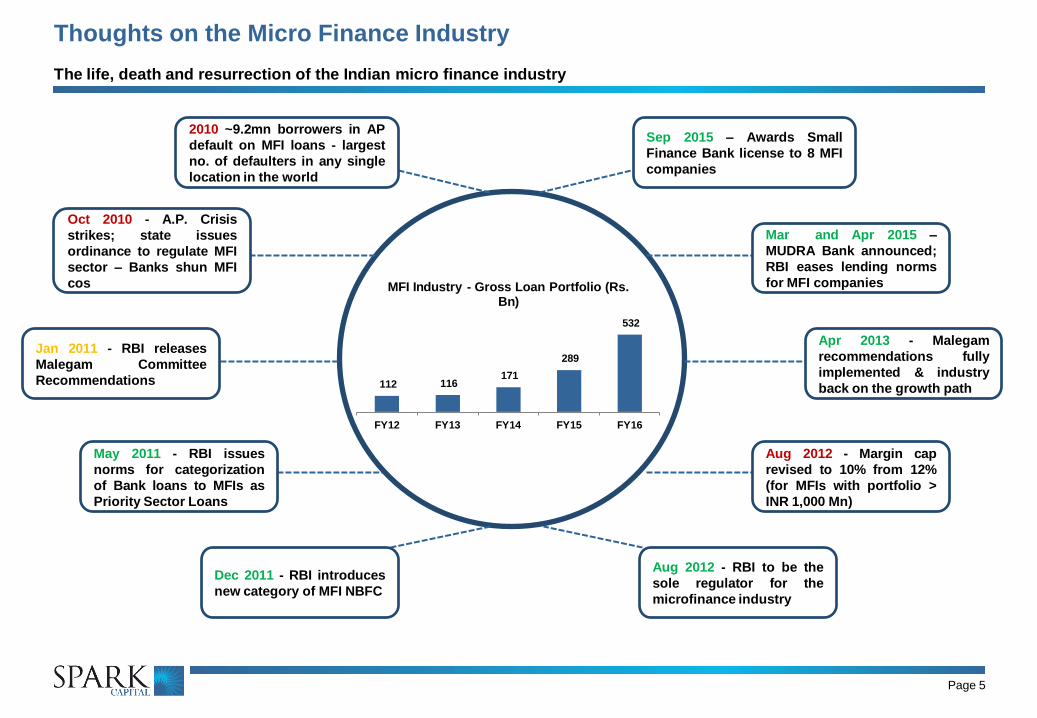

Thoughts on the Micro Finance Industry

The life, death and resurrection of the Indian micro finance industry

2010 ~9.2mn borrowers in AP

default on MFI loans - largest

no. of defaulters in any single

location in the world

Oct 2010 - A.P. Crisis

strikes; state issues

ordinance to regulate MFI

sector – Banks shun MFI

cos

Jan 2011 - RBI releases

Malegam Committee

Recommendations

May 2011 - RBI issues

norms for categorization

of Bank loans to MFIs as

Priority Sector Loans

Dec 2011 - RBI introduces

new category of MFI NBFC

Mar and Apr 2015 –

MUDRA Bank announced;

RBI eases lending norms

for MFI companies

Apr 2013 - Malegam

recommendations fully

implemented & industry

back on the growth path

Aug 2012 - Margin cap

revised to 10% from 12%

(for MFIs with portfolio >

INR 1,000 Mn)

Aug 2012 - RBI to be the

sole regulator for the

microfinance industry

Sep 2015 – Awards Small

Finance Bank license to 8 MFI

companies

112 116 171

289

532

FY12 FY13 FY14 FY15 FY16

MFI Industry - Gross Loan Portfolio (Rs. Bn)

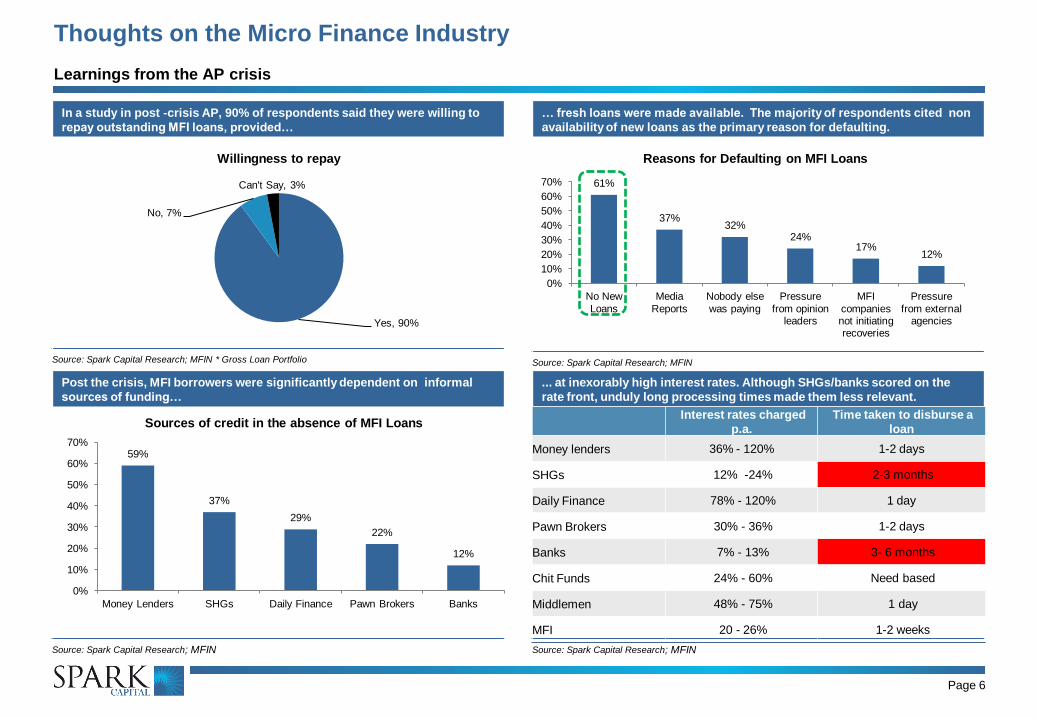

In a study in post -crisis AP, 90% of respondents said they were willing to

repay outstanding MFI loans, provided…

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

… fresh loans were made available. The majority of respondents cited non

availability of new loans as the primary reason for defaulting.

Source: Spark Capital Research; MFIN

Page 6

... at inexorably high interest rates. Although SHGs/banks scored on the

rate front, unduly long processing times made them less relevant.

Source: Spark Capital Research; MFIN

Post the crisis, MFI borrowers were significantly dependent on informal

sources of funding…

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

Learnings from the AP crisis

Yes, 90%

No, 7%

Can't Say, 3%

Willingness to repay

61%

37% 32%

24% 17%

12%

0%

10%

20%

30%

40%

50%

60%

70%

No New

Loans

Media

Reports

Nobody else

was paying

Pressure

from opinion leaders

MFI

companies not initiating recoveries

Pressure

from external agencies

Reasons for Defaulting on MFI Loans

59%

37%

29%

22%

12%

0%

10%

20%

30%

40%

50%

60%

70%

Money Lenders SHGs Daily Finance Pawn Brokers Banks

Sources of credit in the absence of MFI Loans

Interest rates charged

p.a.

Time taken to disburse a

loan

Money lenders 36% - 120% 1-2 days

SHGs 12% -24% 2-3 months

Daily Finance 78% - 120% 1 day

Pawn Brokers 30% - 36% 1-2 days

Banks 7% - 13% 3- 6 months

Chit Funds 24% - 60% Need based

Middlemen 48% - 75% 1 day

MFI 20 - 26% 1-2 weeks

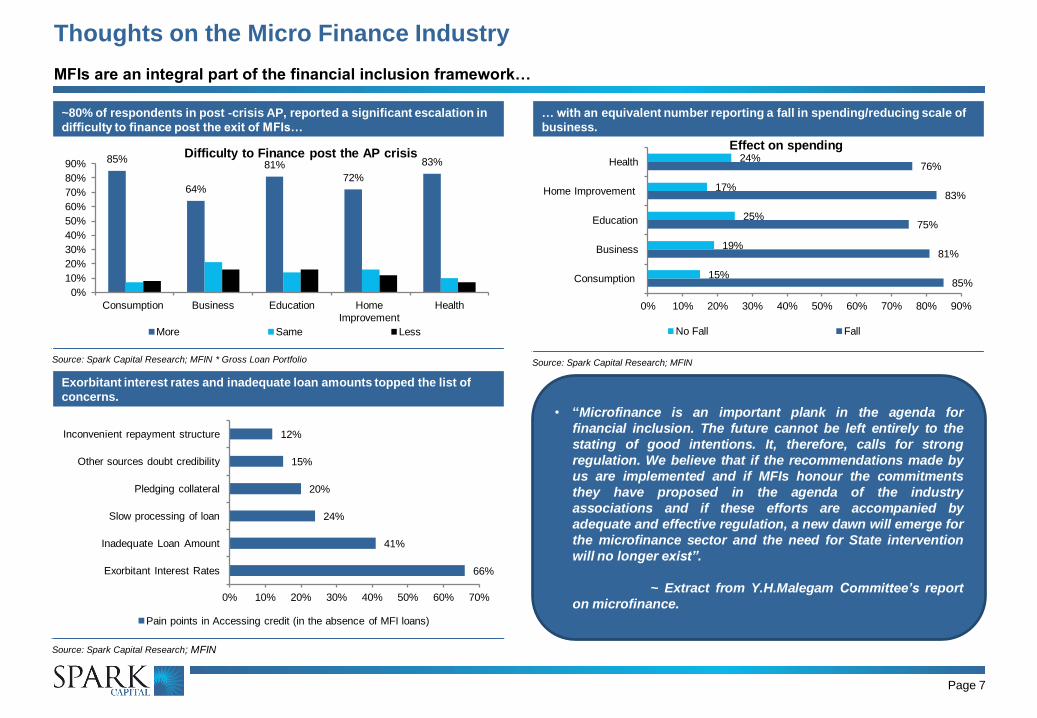

~80% of respondents in post -crisis AP, reported a significant escalation in

difficulty to finance post the exit of MFIs…

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

… with an equivalent number reporting a fall in spending/reducing scale of

business.

Source: Spark Capital Research; MFIN

Page 7

Exorbitant interest rates and inadequate loan amounts topped the list of

concerns.

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

MFIs are an integral part of the financial inclusion framework…

85%

64%

81%

72%

83%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Consumption Business Education Home

Improvement

Health

Difficulty to Finance post the AP crisis

More Same Less

66%

41%

24%

20%

15%

12%

0% 10% 20% 30% 40% 50% 60% 70%

Exorbitant Interest Rates

Inadequate Loan Amount

Slow processing of loan

Pledging collateral

Other sources doubt credibility

Inconvenient repayment structure

Pain points in Accessing credit (in the absence of MFI loans)

• “Microfinance is an important plank in the agenda for

financial inclusion. The future cannot be left entirely to the

stating of good intentions. It, therefore, calls for strong

regulation. We believe that if the recommendations made by

us are implemented and if MFIs honour the commitments

they have proposed in the agenda of the industry

associations and if these efforts are accompanied by

adequate and effective regulation, a new dawn will emerge for

the microfinance sector and the need for State intervention

will no longer exist”.

~ Extract from Y.H.Malegam Committee’s report

on microfinance.

85%

81%

75%

83%

76%

15%

19%

25%

17%

24%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Consumption

Business

Education

Home Improvement

Health

Effect on spending

No Fall Fall

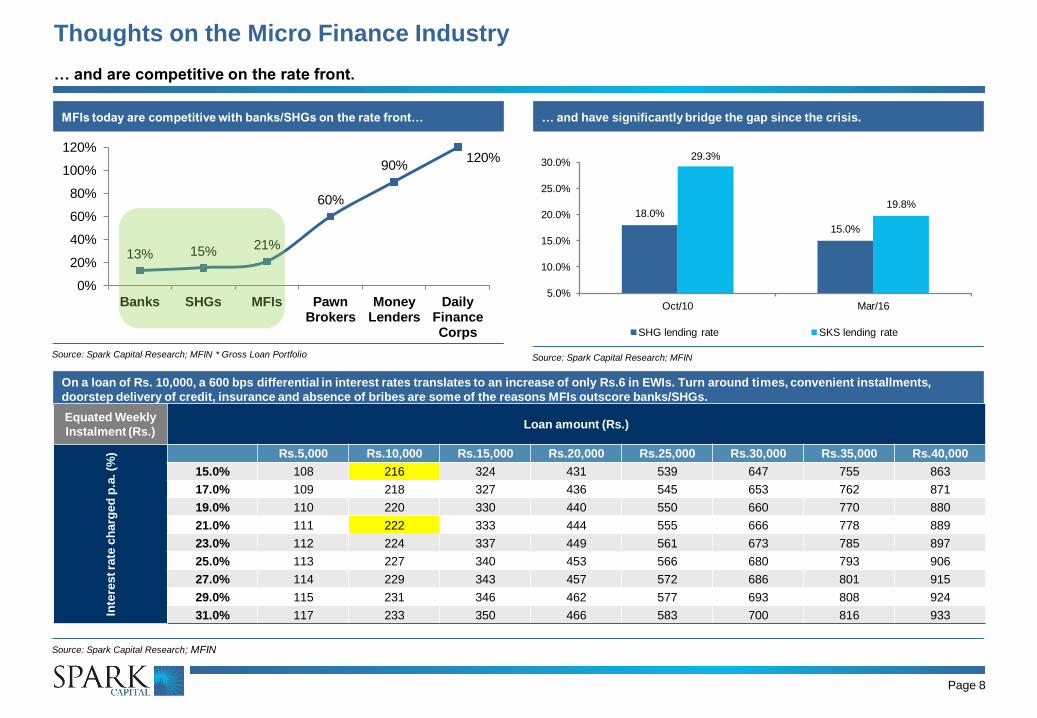

13% 15% 21%

60%

90% 120%

0%

20%

40%

60%

80%

100%

120%

Banks SHGs MFIs Pawn Brokers

Money Lenders

Daily Finance Corps

MFIs today are competitive with banks/SHGs on the rate front…

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

… and have significantly bridge the gap since the crisis.

Source: Spark Capital Research; MFIN

Page 8

On a loan of Rs. 10,000, a 600 bps differential in interest rates translates to an increase of only Rs.6 in EWIs. Turn around times, convenient installments,

doorstep delivery of credit, insurance and absence of bribes are some of the reasons MFIs outscore banks/SHGs.

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

… and are competitive on the rate front.

18.0%

15.0%

29.3%

19.8%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

Oct/10 Mar/16

SHG lending rate SKS lending rate

Equated Weekly

Instalment (Rs.) Loan amount (Rs.)

Inte

rest ra

te c

harg

ed

p.a

. (%

) Rs.5,000 Rs.10,000 Rs.15,000 Rs.20,000 Rs.25,000 Rs.30,000 Rs.35,000 Rs.40,000

15.0% 108 216 324 431 539 647 755 863

17.0% 109 218 327 436 545 653 762 871

19.0% 110 220 330 440 550 660 770 880

21.0% 111 222 333 444 555 666 778 889

23.0% 112 224 337 449 561 673 785 897

25.0% 113 227 340 453 566 680 793 906

27.0% 114 229 343 457 572 686 801 915

29.0% 115 231 346 462 577 693 808 924

31.0% 117 233 350 466 583 700 816 933

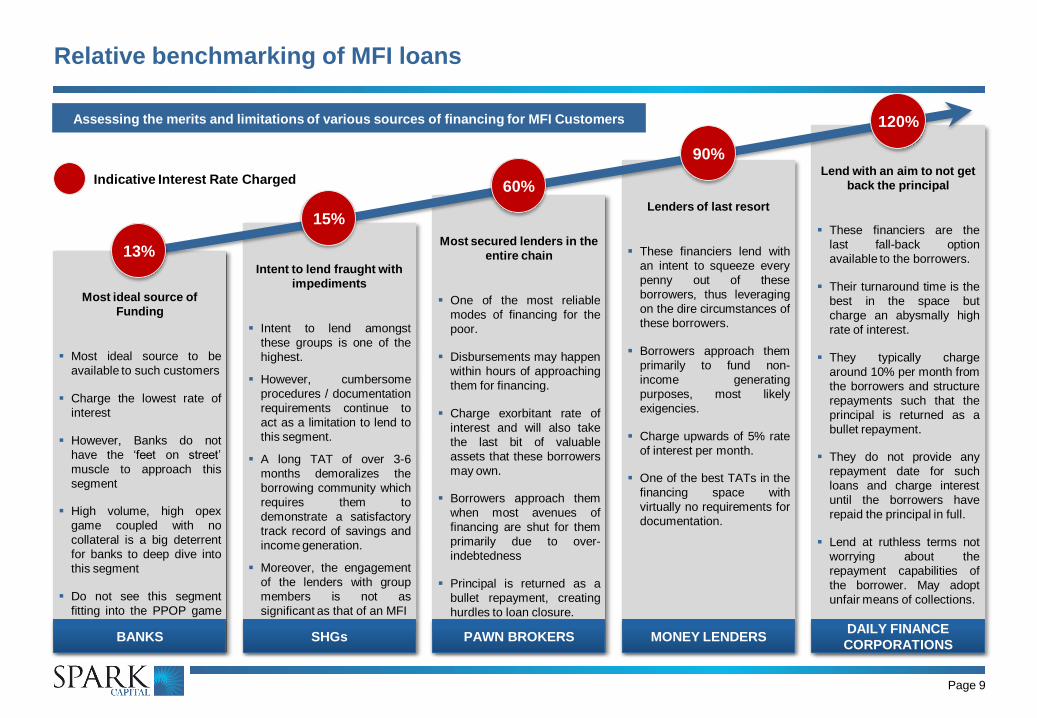

Most ideal source of

Funding

Most ideal source to be

available to such customers

Charge the lowest rate of

interest

However, Banks do not

have the ‘feet on street’

muscle to approach this

segment

High volume, high opex

game coupled with no

collateral is a big deterrent

for banks to deep dive into

this segment

Do not see this segment

fitting into the PPOP game

for banks

Intent to lend fraught with

impediments

Intent to lend amongst

these groups is one of the

highest.

However, cumbersome

procedures / documentation

requirements continue to

act as a limitation to lend to

this segment.

A long TAT of over 3-6

months demoralizes the

borrowing community which

requires them to

demonstrate a satisfactory

track record of savings and

income generation.

Moreover, the engagement

of the lenders with group

members is not as

significant as that of an MFI

Most secured lenders in the

entire chain

One of the most reliable

modes of financing for the

poor.

Disbursements may happen

within hours of approaching

them for financing.

Charge exorbitant rate of

interest and will also take

the last bit of valuable

assets that these borrowers

may own.

Borrowers approach them

when most avenues of

financing are shut for them

primarily due to over-

indebtedness

Principal is returned as a

bullet repayment, creating

hurdles to loan closure.

Lenders of last resort

These financiers lend with

an intent to squeeze every

penny out of these

borrowers, thus leveraging

on the dire circumstances of

these borrowers.

Borrowers approach them

primarily to fund non-

income generating

purposes, most likely

exigencies.

Charge upwards of 5% rate

of interest per month.

One of the best TATs in the

financing space with

virtually no requirements for

documentation.

Lend with an aim to not get

back the principal

These financiers are the

last fall-back option

available to the borrowers.

Their turnaround time is the

best in the space but

charge an abysmally high

rate of interest.

They typically charge

around 10% per month from

the borrowers and structure

repayments such that the

principal is returned as a

bullet repayment.

They do not provide any

repayment date for such

loans and charge interest

until the borrowers have

repaid the principal in full.

Lend at ruthless terms not

worrying about the

repayment capabilities of

the borrower. May adopt

unfair means of collections.

Relative benchmarking of MFI loans

Page 9

15%

60%

90%

120%

13%

BANKS SHGs PAWN BROKERS MONEY LENDERS DAILY FINANCE

CORPORATIONS

Indicative Interest Rate Charged

Assessing the merits and limitations of various sources of financing for MFI Customers

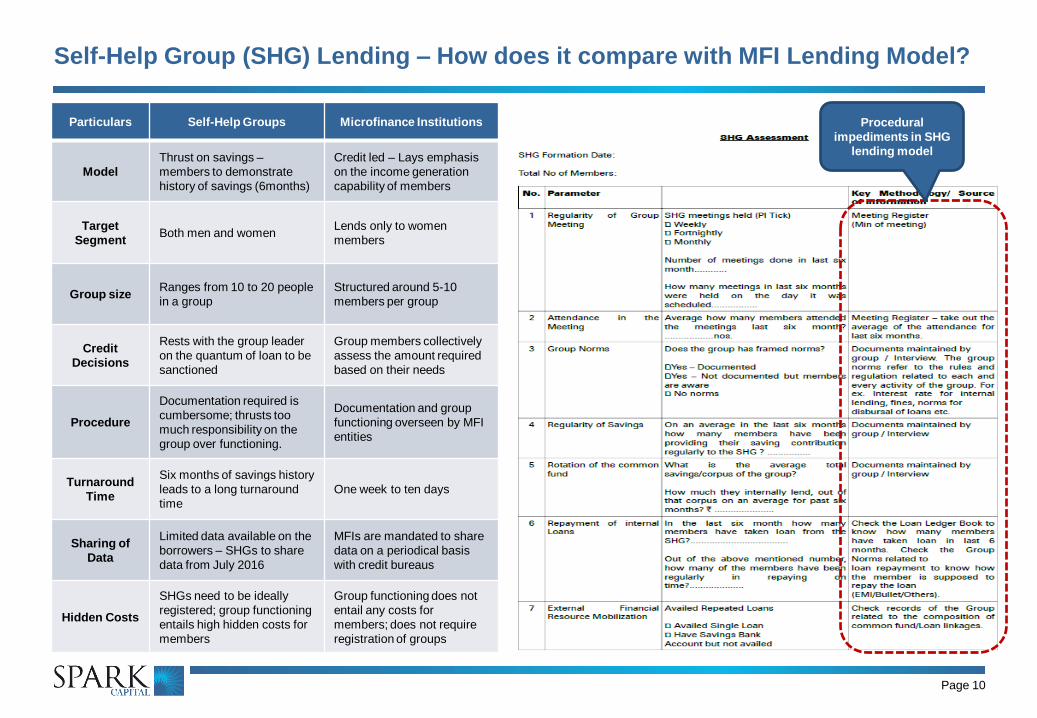

Self-Help Group (SHG) Lending – How does it compare with MFI Lending Model?

Page 10

Particulars Self-Help Groups Microfinance Institutions

Model

Thrust on savings –

members to demonstrate

history of savings (6months)

Credit led – Lays emphasis

on the income generation

capability of members

Target

Segment Both men and women

Lends only to women

members

Group size Ranges from 10 to 20 people

in a group

Structured around 5-10

members per group

Credit

Decisions

Rests with the group leader

on the quantum of loan to be

sanctioned

Group members collectively

assess the amount required

based on their needs

Procedure

Documentation required is

cumbersome; thrusts too

much responsibility on the

group over functioning.

Documentation and group

functioning overseen by MFI

entities

Turnaround

Time

Six months of savings history

leads to a long turnaround

time

One week to ten days

Sharing of

Data

Limited data available on the

borrowers – SHGs to share

data from July 2016

MFIs are mandated to share

data on a periodical basis

with credit bureaus

Hidden Costs

SHGs need to be ideally

registered; group functioning

entails high hidden costs for

members

Group functioning does not

entail any costs for

members; does not require

registration of groups

Procedural

impediments in SHG

lending model

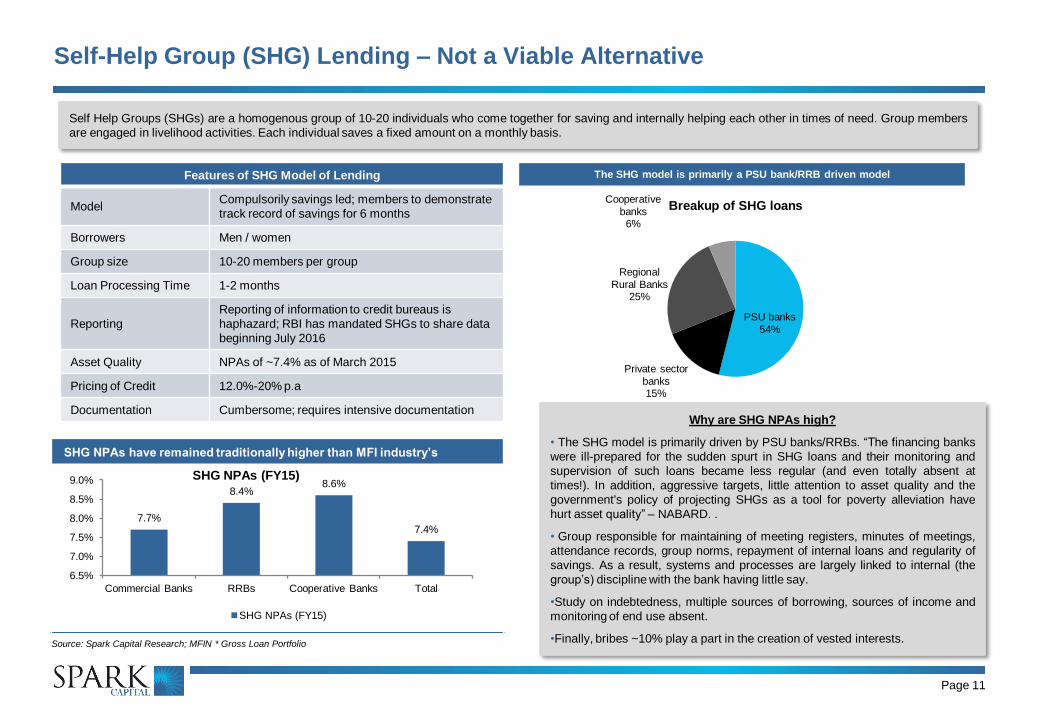

SHG NPAs have remained traditionally higher than MFI industry’s

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

Self-Help Group (SHG) Lending – Not a Viable Alternative

Page 11

Self Help Groups (SHGs) are a homogenous group of 10-20 individuals who come together for saving and internally helping each other in times of need. Group members

are engaged in livelihood activities. Each individual saves a fixed amount on a monthly basis.

Features of SHG Model of Lending

Model Compulsorily savings led; members to demonstrate

track record of savings for 6 months

Borrowers Men / women

Group size 10-20 members per group

Loan Processing Time 1-2 months

Reporting

Reporting of information to credit bureaus is

haphazard; RBI has mandated SHGs to share data

beginning July 2016

Asset Quality NPAs of ~7.4% as of March 2015

Pricing of Credit 12.0%-20% p.a

Documentation Cumbersome; requires intensive documentation

The SHG model is primarily a PSU bank/RRB driven model

Why are SHG NPAs high?

• The SHG model is primarily driven by PSU banks/RRBs. “The financing banks

were ill-prepared for the sudden spurt in SHG loans and their monitoring and

supervision of such loans became less regular (and even totally absent at

times!). In addition, aggressive targets, little attention to asset quality and the

government's policy of projecting SHGs as a tool for poverty alleviation have

hurt asset quality” – NABARD. .

• Group responsible for maintaining of meeting registers, minutes of meetings,

attendance records, group norms, repayment of internal loans and regularity of

savings. As a result, systems and processes are largely linked to internal (the

group’s) discipline with the bank having little say.

•Study on indebtedness, multiple sources of borrowing, sources of income and

monitoring of end use absent.

•Finally, bribes ~10% play a part in the creation of vested interests.

PSU banks

54%

Private sector

banks 15%

Regional

Rural Banks 25%

Cooperative

banks 6%

Breakup of SHG loans

7.7%

8.4% 8.6%

7.4%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

Commercial Banks RRBs Cooperative Banks Total

SHG NPAs (FY15)

SHG NPAs (FY15)

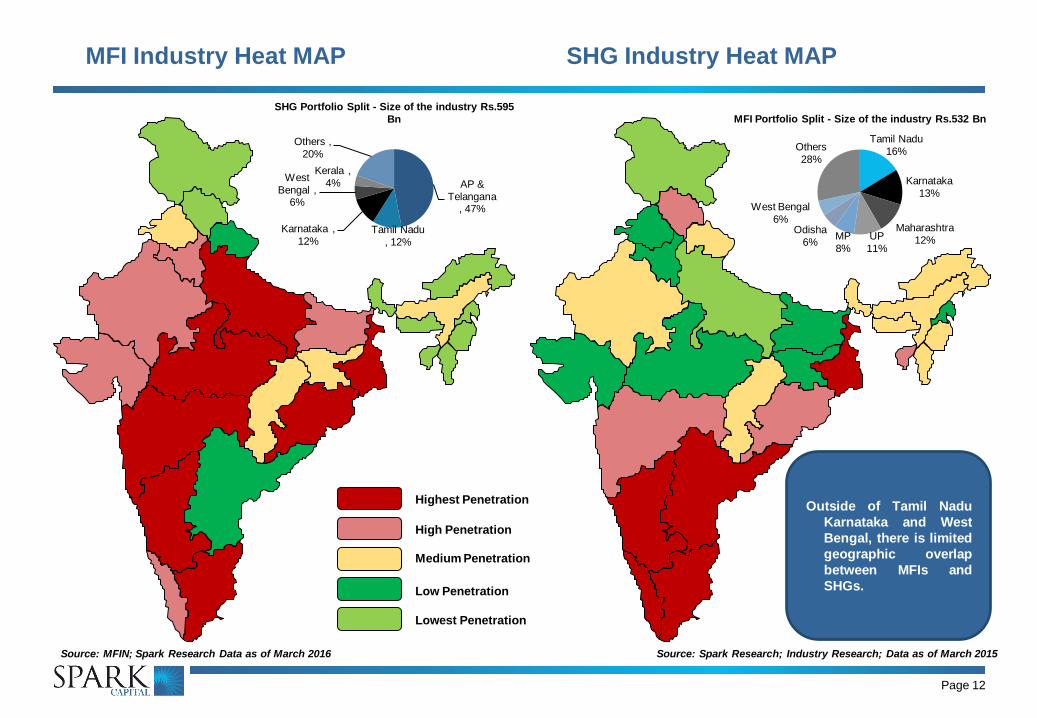

MFI Industry Heat MAP

Page 12

SHG Industry Heat MAP

Highest Penetration

High Penetration

Medium Penetration

Low Penetration

Lowest Penetration

Source: MFIN; Spark Research Data as of March 2016 Source: Spark Research; Industry Research; Data as of March 2015

AP &

Telangana , 47%

Tamil Nadu

, 12%

Karnataka ,

12%

West

Bengal , 6%

Kerala ,

4%

Others ,

20%

SHG Portfolio Split - Size of the industry Rs.595

Bn

Tamil Nadu

16%

Karnataka

13%

Maharashtra

12% UP

11%

MP

8%

Odisha

6%

West Bengal

6%

Others

28%

MFI Portfolio Split - Size of the industry Rs.532 Bn

Outside of Tamil Nadu

Karnataka and West

Bengal, there is limited

geographic overlap

between MFIs and

SHGs.

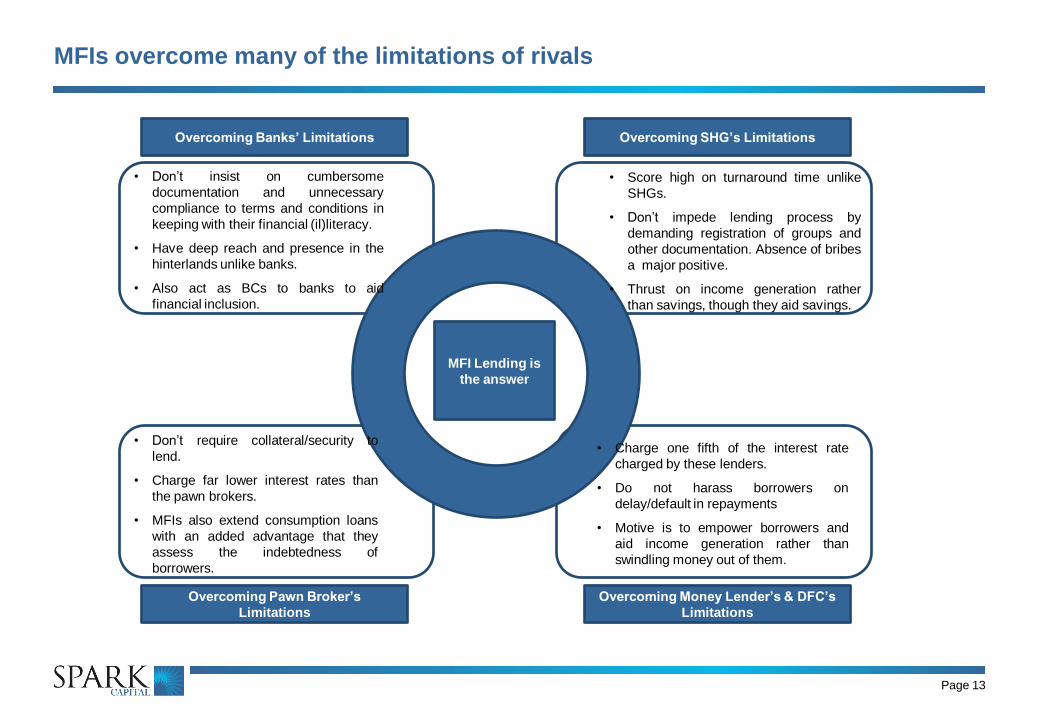

MFIs overcome many of the limitations of rivals

Page 13

Overcoming Banks’ Limitations

MFI Lending is

the answer

Overcoming SHG’s Limitations

Overcoming Pawn Broker’s

Limitations

Overcoming Money Lender’s & DFC’s

Limitations

• Don’t insist on cumbersome

documentation and unnecessary

compliance to terms and conditions in

keeping with their financial (il)literacy.

• Have deep reach and presence in the

hinterlands unlike banks.

• Also act as BCs to banks to aid

financial inclusion.

• Score high on turnaround time unlike

SHGs.

• Don’t impede lending process by

demanding registration of groups and

other documentation. Absence of bribes

a major positive.

• Thrust on income generation rather

than savings, though they aid savings.

• Don’t require collateral/security to

lend.

• Charge far lower interest rates than

the pawn brokers.

• MFIs also extend consumption loans

with an added advantage that they

assess the indebtedness of

borrowers.

• Charge one fifth of the interest rate

charged by these lenders.

• Do not harass borrowers on

delay/default in repayments

• Motive is to empower borrowers and

aid income generation rather than

swindling money out of them.

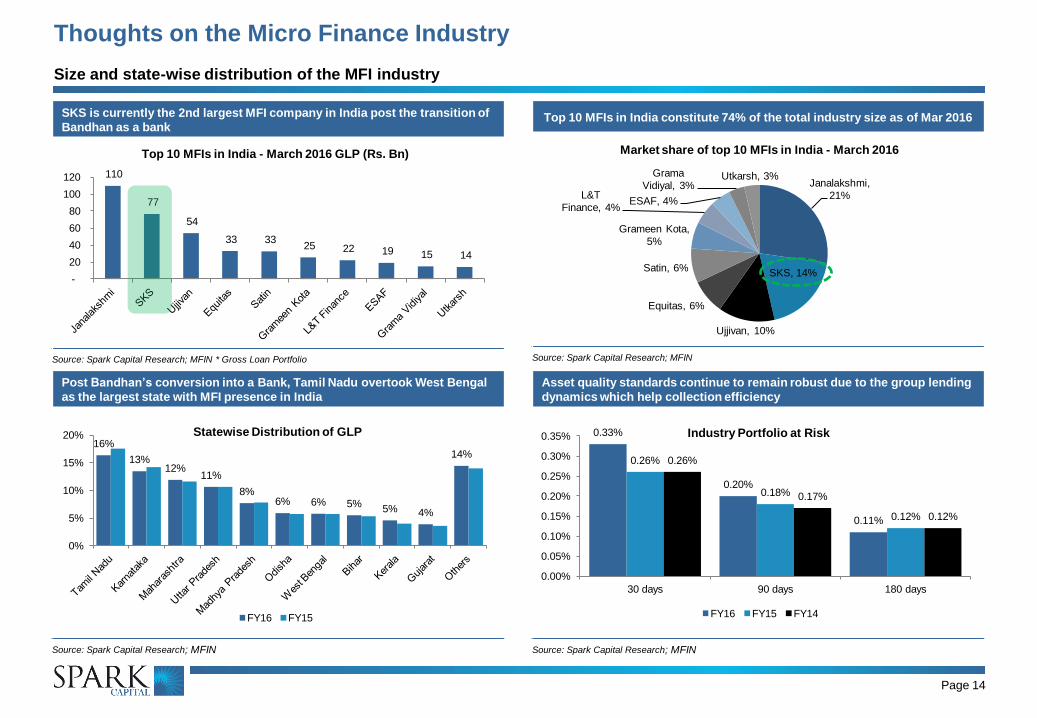

SKS is currently the 2nd largest MFI company in India post the transition of

Bandhan as a bank

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

Top 10 MFIs in India constitute 74% of the total industry size as of Mar 2016

Source: Spark Capital Research; MFIN

Janalakshmi,

21%

SKS, 14%

Ujjivan, 10%

Equitas, 6%

Satin, 6%

Grameen Kota,

5%

L&T

Finance, 4% ESAF, 4%

Grama

Vidiyal, 3% Utkarsh, 3%

Market share of top 10 MFIs in India - March 2016

110

77

54

33 33 25 22 19 15 14

-

20

40

60

80

100

120

Top 10 MFIs in India - March 2016 GLP (Rs. Bn)

Page 14

Asset quality standards continue to remain robust due to the group lending

dynamics which help collection efficiency

Source: Spark Capital Research; MFIN

Post Bandhan’s conversion into a Bank, Tamil Nadu overtook West Bengal

as the largest state with MFI presence in India

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

Size and state-wise distribution of the MFI industry

16%

13% 12%

11%

8% 6% 6% 5%

5% 4%

14%

0%

5%

10%

15%

20% Statewise Distribution of GLP

FY16 FY15

0.33%

0.20%

0.11%

0.26%

0.18%

0.12%

0.26%

0.17%

0.12%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

30 days 90 days 180 days

Industry Portfolio at Risk

FY16 FY15 FY14

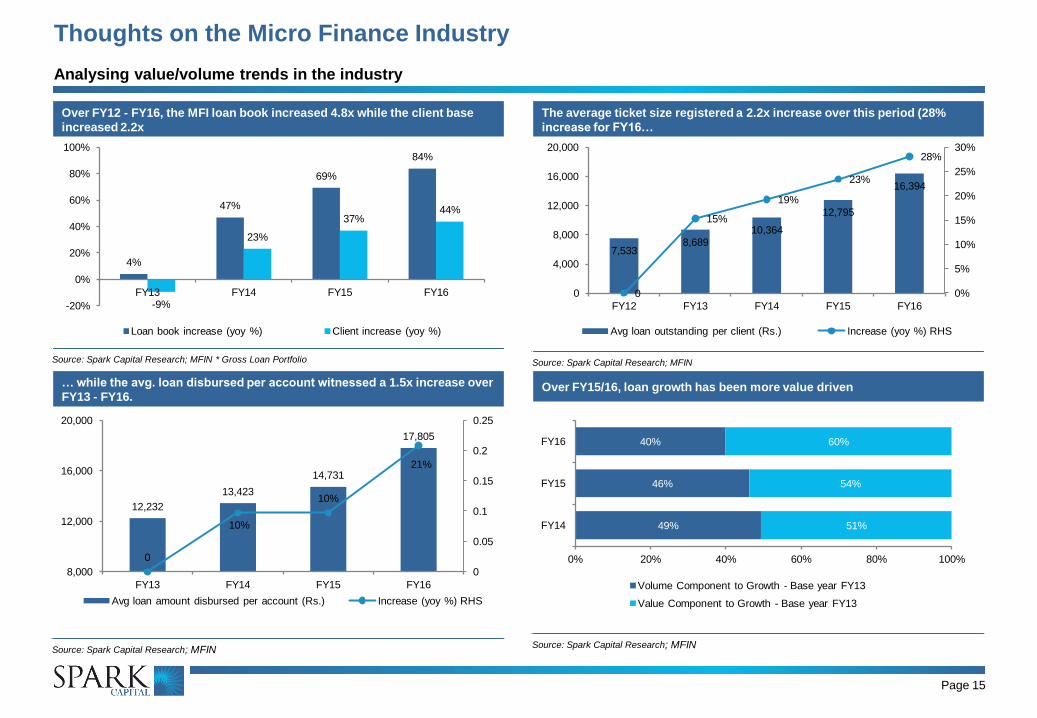

Over FY12 - FY16, the MFI loan book increased 4.8x while the client base

increased 2.2x

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

The average ticket size registered a 2.2x increase over this period (28%

increase for FY16…

Source: Spark Capital Research; MFIN

Page 15

Over FY15/16, loan growth has been more value driven

Source: Spark Capital Research; MFIN

… while the avg. loan disbursed per account witnessed a 1.5x increase over

FY13 - FY16.

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

Analysing value/volume trends in the industry

4%

47%

69%

84%

-9%

23%

37% 44%

-20%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16

Loan book increase (yoy %) Client increase (yoy %)

7,533 8,689

10,364

12,795

16,394

0

15%

19%

23%

28%

0%

5%

10%

15%

20%

25%

30%

0

4,000

8,000

12,000

16,000

20,000

FY12 FY13 FY14 FY15 FY16

Avg loan outstanding per client (Rs.) Increase (yoy %) RHS

49%

46%

40%

51%

54%

60%

0% 20% 40% 60% 80% 100%

FY14

FY15

FY16

Volume Component to Growth - Base year FY13

Value Component to Growth - Base year FY13

12,232

13,423

14,731

17,805

0

10%

10%

21%

0

0.05

0.1

0.15

0.2

0.25

8,000

12,000

16,000

20,000

FY13 FY14 FY15 FY16

Avg loan amount disbursed per account (Rs.) Increase (yoy %) RHS

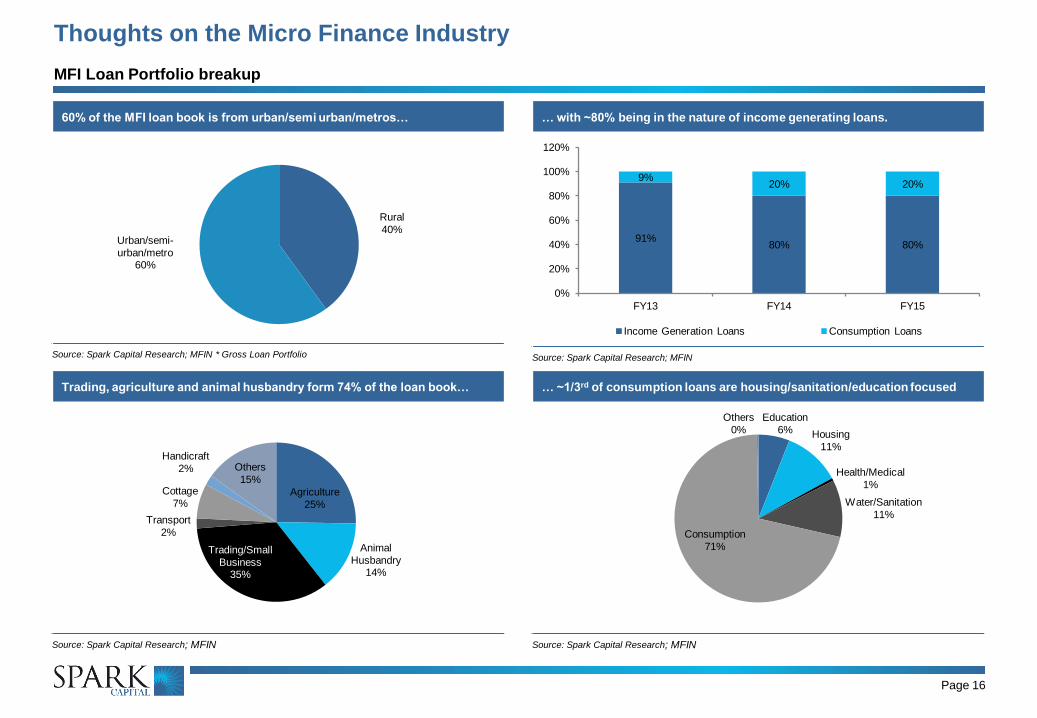

60% of the MFI loan book is from urban/semi urban/metros…

Source: Spark Capital Research; MFIN * Gross Loan Portfolio

… with ~80% being in the nature of income generating loans.

Source: Spark Capital Research; MFIN

Page 16

… ~1/3rd of consumption loans are housing/sanitation/education focused

Source: Spark Capital Research; MFIN

Trading, agriculture and animal husbandry form 74% of the loan book…

Source: Spark Capital Research; MFIN

Thoughts on the Micro Finance Industry

MFI Loan Portfolio breakup

Rural

40% Urban/semi-

urban/metro 60%

Agriculture

25%

Animal

Husbandry 14%

Trading/Small

Business 35%

Transport

2%

Cottage

7%

Handicraft

2% Others

15%

Education

6% Housing

11%

Health/Medical

1%

Water/Sanitation

11%

Consumption

71%

Others

0%

91% 80% 80%

9% 20% 20%

0%

20%

40%

60%

80%

100%

120%

FY13 FY14 FY15

Income Generation Loans Consumption Loans

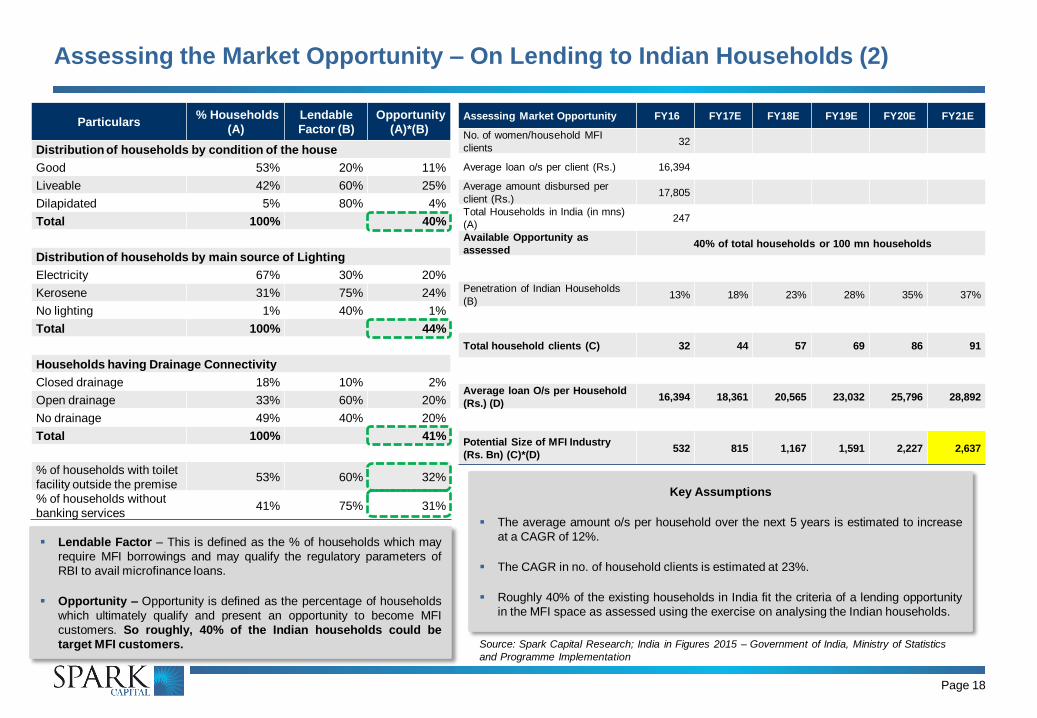

Assessing the Market Opportunity – On Lending to Indian Households (1)

Page 17

• To calculate the existing penetration of MFI

sector in the Indian households, it has been

assumed that there is only one MFI

borrower per household.

• With distribution of household income in

India being unduly skewed, it creates a huge

opportunity for the MFI players to tap into

the available opportunity.

• As the graph below indicates, the top

quintile of the households in India have 59%

of the total wealth (or household income).

• This creates a huge opportunity to cater to

the remaining 80% of the households in

India with various wealth related services.

States

No. Of

Households (in

mns)

Existing no. of

MFI clients (in

mns)

Existing

Penetration (on

households)

Avg. Household

Income (Rs. p.a)

Andaman & Nicobar Islands 0.1 - 0.0% 545,736

Andhra Pradesh 21.0 0.1 0.5% 449,023

Arunachal Pradesh 0.3 - 0.0% 456,177

Assam 6.4 0.5 8.4% 250,444

Bihar 18.9 1.9 10.2% 173,101

Chandigarh 0.2 - 0.0% 872,813

Chhattisgarh 5.6 0.6 10.4% 342,535

Dadra & Nagar Haveli 0.1 - 0.0% NA

Daman & Diu 0.1 - 0.0% NA

Delhi 3.3 0.6 16.6% 1,106,857

Goa 0.3 - 0.0% 1,291,608

Gujarat 12.2 1.2 10.1% 634,598

Haryana 4.7 0.5 10.4% 711,582

Himachal Pradesh 1.5 - 0.0% 572,394

Jammu & Kashmir 2.0 - 0.0% 316,186

Jharkhand 6.2 0.6 9.2% 263,193

Karnataka 13.2 3.8 29.0% 501,848

Kerala 7.7 1.2 15.8% 545,736

Lakshadweep 0.0 - 0.0% NA

Madhya Pradesh 15.0 2.8 18.7% 293,018

Maharashtra 23.8 3.7 15.6% 628,575

Manipur 0.5 - 0.0% 230,300

Meghalaya 0.5 - 0.0% 343,947

Mizoram 0.2 - 0.0% 451,508

Nagaland 0.4 - 0.0% 409,617

Orissa 9.7 2.1 22.1% 311,270

Pondicherry 0.3 0.1 40.5% 834,718

Punjab 5.4 0.6 10.4% 498,005

Rajasthan 12.6 0.8 6.0% 353,193

Sikkim 0.1 - 0.0% 1,007,015

Tamil Nadu 18.5 5.7 30.6% 623,901

Tripura 0.8 - 0.0% 369,839

Uttar Pradesh 32.9 3.1 9.5% 201,418

Uttrakhand 2.0 0.3 16.6% 584,430

West Bengal 20.1 2.2 10.9% 381,411

All India 246.7 32.4 13.2% 432,536

7% 7% 6% 6% 13% 10% 9% 8%

18% 14% 13% 10%

25% 21%

19% 17%

37% 48% 53% 59%

1993-94 2004-05 2009-10 2014-15E

Distribution of Household Income in India - Quintile Data - % of total income

Q1 (Bottom) Q2 Q3 Q4 Q5 (Top)

Source: Spark Capital Research; NCAER - CMCR

Assessing the Market Opportunity – On Lending to Indian Households (2)

Page 18

Particulars % Households

(A)

Lendable

Factor (B)

Opportunity

(A)*(B)

Distribution of households by condition of the house

Good 53% 20% 11%

Liveable 42% 60% 25%

Dilapidated 5% 80% 4%

Total 100% 40%

Distribution of households by main source of Lighting

Electricity 67% 30% 20%

Kerosene 31% 75% 24%

No lighting 1% 40% 1%

Total 100% 44%

Households having Drainage Connectivity

Closed drainage 18% 10% 2%

Open drainage 33% 60% 20%

No drainage 49% 40% 20%

Total 100% 41%

% of households with toilet

facility outside the premise 53% 60% 32%

% of households without

banking services 41% 75% 31%

Lendable Factor – This is defined as the % of households which may

require MFI borrowings and may qualify the regulatory parameters of

RBI to avail microfinance loans.

Opportunity – Opportunity is defined as the percentage of households

which ultimately qualify and present an opportunity to become MFI

customers. So roughly, 40% of the Indian households could be

target MFI customers.

Assessing Market Opportunity FY16 FY17E FY18E FY19E FY20E FY21E

No. of women/household MFI

clients 32

Average loan o/s per client (Rs.) 16,394

Average amount disbursed per

client (Rs.) 17,805

Total Households in India (in mns)

(A) 247

Available Opportunity as

assessed 40% of total households or 100 mn households

Penetration of Indian Households

(B) 13% 18% 23% 28% 35% 37%

Total household clients (C) 32 44 57 69 86 91

Average loan O/s per Household

(Rs.) (D) 16,394 18,361 20,565 23,032 25,796 28,892

Potential Size of MFI Industry

(Rs. Bn) (C)*(D) 532 815 1,167 1,591 2,227 2,637

Key Assumptions

The average amount o/s per household over the next 5 years is estimated to increase

at a CAGR of 12%.

The CAGR in no. of household clients is estimated at 23%.

Roughly 40% of the existing households in India fit the criteria of a lending opportunity

in the MFI space as assessed using the exercise on analysing the Indian households.

Source: Spark Capital Research; India in Figures 2015 – Government of India, Ministry of Statistics

and Programme Implementation

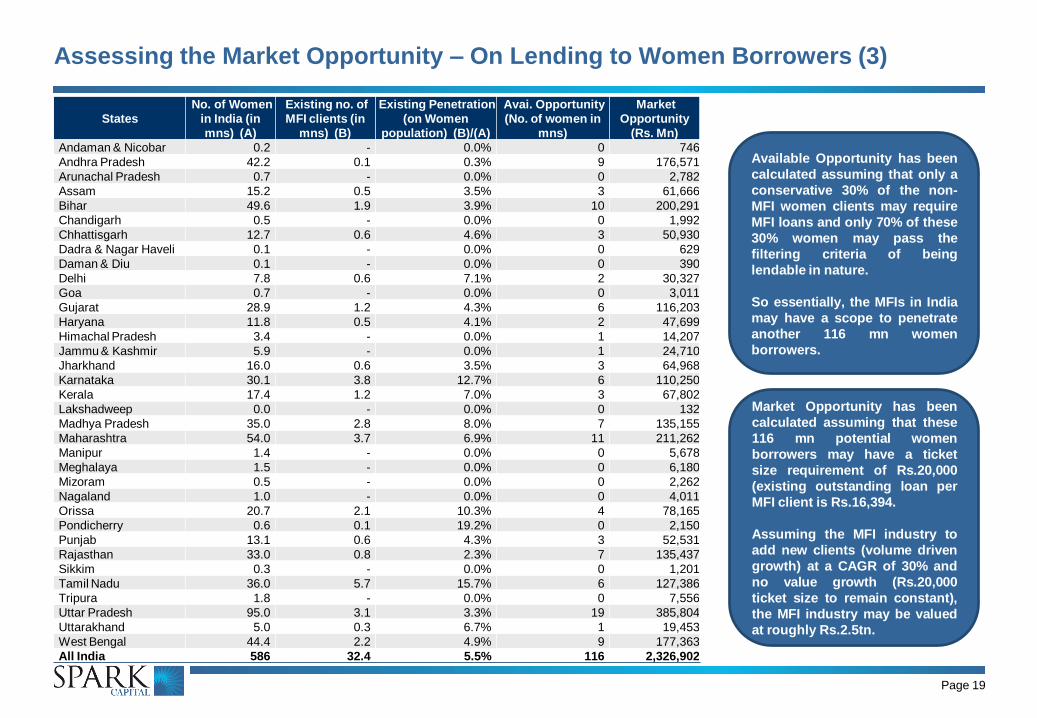

Assessing the Market Opportunity – On Lending to Women Borrowers (3)

Page 19

States

No. of Women

in India (in

mns) (A)

Existing no. of

MFI clients (in

mns) (B)

Existing Penetration

(on Women

population) (B)/(A)

Avai. Opportunity

(No. of women in

mns)

Market

Opportunity

(Rs. Mn)

Andaman & Nicobar 0.2 - 0.0% 0 746

Andhra Pradesh 42.2 0.1 0.3% 9 176,571

Arunachal Pradesh 0.7 - 0.0% 0 2,782

Assam 15.2 0.5 3.5% 3 61,666

Bihar 49.6 1.9 3.9% 10 200,291

Chandigarh 0.5 - 0.0% 0 1,992

Chhattisgarh 12.7 0.6 4.6% 3 50,930

Dadra & Nagar Haveli 0.1 - 0.0% 0 629

Daman & Diu 0.1 - 0.0% 0 390

Delhi 7.8 0.6 7.1% 2 30,327

Goa 0.7 - 0.0% 0 3,011

Gujarat 28.9 1.2 4.3% 6 116,203

Haryana 11.8 0.5 4.1% 2 47,699

Himachal Pradesh 3.4 - 0.0% 1 14,207

Jammu & Kashmir 5.9 - 0.0% 1 24,710

Jharkhand 16.0 0.6 3.5% 3 64,968

Karnataka 30.1 3.8 12.7% 6 110,250

Kerala 17.4 1.2 7.0% 3 67,802

Lakshadweep 0.0 - 0.0% 0 132

Madhya Pradesh 35.0 2.8 8.0% 7 135,155

Maharashtra 54.0 3.7 6.9% 11 211,262

Manipur 1.4 - 0.0% 0 5,678

Meghalaya 1.5 - 0.0% 0 6,180

Mizoram 0.5 - 0.0% 0 2,262

Nagaland 1.0 - 0.0% 0 4,011

Orissa 20.7 2.1 10.3% 4 78,165

Pondicherry 0.6 0.1 19.2% 0 2,150

Punjab 13.1 0.6 4.3% 3 52,531

Rajasthan 33.0 0.8 2.3% 7 135,437

Sikkim 0.3 - 0.0% 0 1,201

Tamil Nadu 36.0 5.7 15.7% 6 127,386

Tripura 1.8 - 0.0% 0 7,556

Uttar Pradesh 95.0 3.1 3.3% 19 385,804

Uttarakhand 5.0 0.3 6.7% 1 19,453

West Bengal 44.4 2.2 4.9% 9 177,363

All India 586 32.4 5.5% 116 2,326,902

Available Opportunity has been

calculated assuming that only a

conservative 30% of the non-

MFI women clients may require

MFI loans and only 70% of these

30% women may pass the

filtering criteria of being

lendable in nature.

So essentially, the MFIs in India

may have a scope to penetrate

another 116 mn women

borrowers.

Market Opportunity has been

calculated assuming that these

116 mn potential women

borrowers may have a ticket

size requirement of Rs.20,000

(existing outstanding loan per

MFI client is Rs.16,394.

Assuming the MFI industry to

add new clients (volume driven

growth) at a CAGR of 30% and

no value growth (Rs.20,000

ticket size to remain constant),

the MFI industry may be valued

at roughly Rs.2.5tn.

Page 20

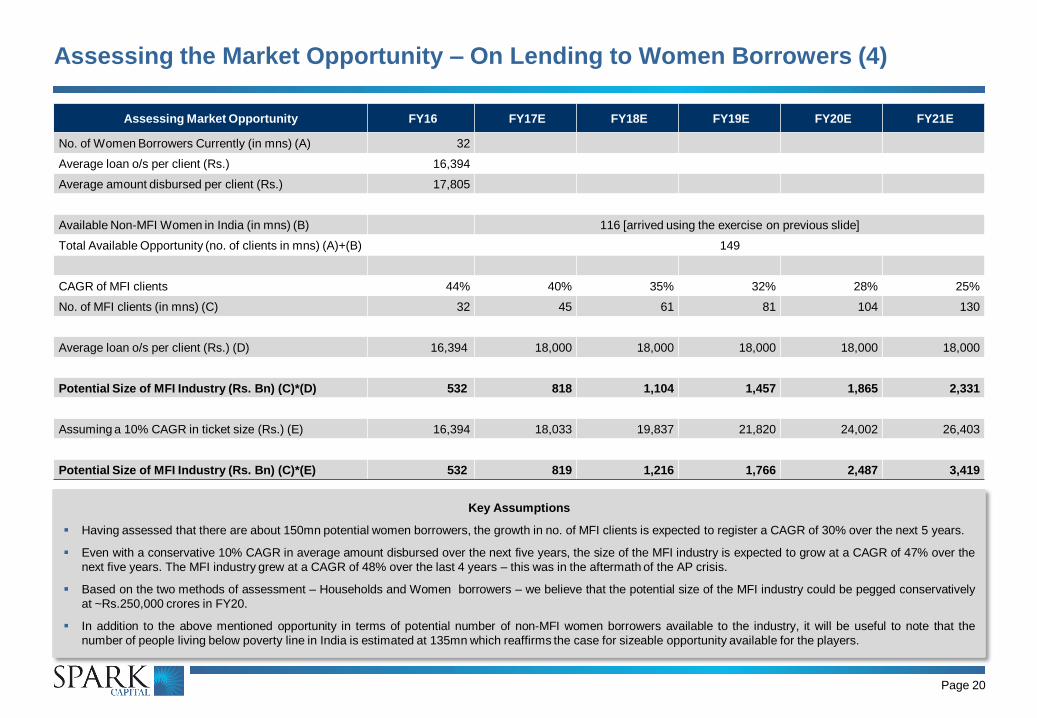

Assessing the Market Opportunity – On Lending to Women Borrowers (4)

Assessing Market Opportunity FY16 FY17E FY18E FY19E FY20E FY21E

No. of Women Borrowers Currently (in mns) (A) 32

Average loan o/s per client (Rs.) 16,394

Average amount disbursed per client (Rs.) 17,805

Available Non-MFI Women in India (in mns) (B) 116 [arrived using the exercise on previous slide]

Total Available Opportunity (no. of clients in mns) (A)+(B) 149

CAGR of MFI clients 44% 40% 35% 32% 28% 25%

No. of MFI clients (in mns) (C) 32 45 61 81 104 130

Average loan o/s per client (Rs.) (D) 16,394 18,000 18,000 18,000 18,000 18,000

Potential Size of MFI Industry (Rs. Bn) (C)*(D) 532 818 1,104 1,457 1,865 2,331

Assuming a 10% CAGR in ticket size (Rs.) (E) 16,394 18,033 19,837 21,820 24,002 26,403

Potential Size of MFI Industry (Rs. Bn) (C)*(E) 532 819 1,216 1,766 2,487 3,419

Key Assumptions

Having assessed that there are about 150mn potential women borrowers, the growth in no. of MFI clients is expected to register a CAGR of 30% over the next 5 years.

Even with a conservative 10% CAGR in average amount disbursed over the next five years, the size of the MFI industry is expected to grow at a CAGR of 47% over the

next five years. The MFI industry grew at a CAGR of 48% over the last 4 years – this was in the aftermath of the AP crisis.

Based on the two methods of assessment – Households and Women borrowers – we believe that the potential size of the MFI industry could be pegged conservatively

at ~Rs.250,000 crores in FY20.

In addition to the above mentioned opportunity in terms of potential number of non-MFI women borrowers available to the industry, it will be useful to note that the

number of people living below poverty line in India is estimated at 135mn which reaffirms the case for sizeable opportunity available for the players.

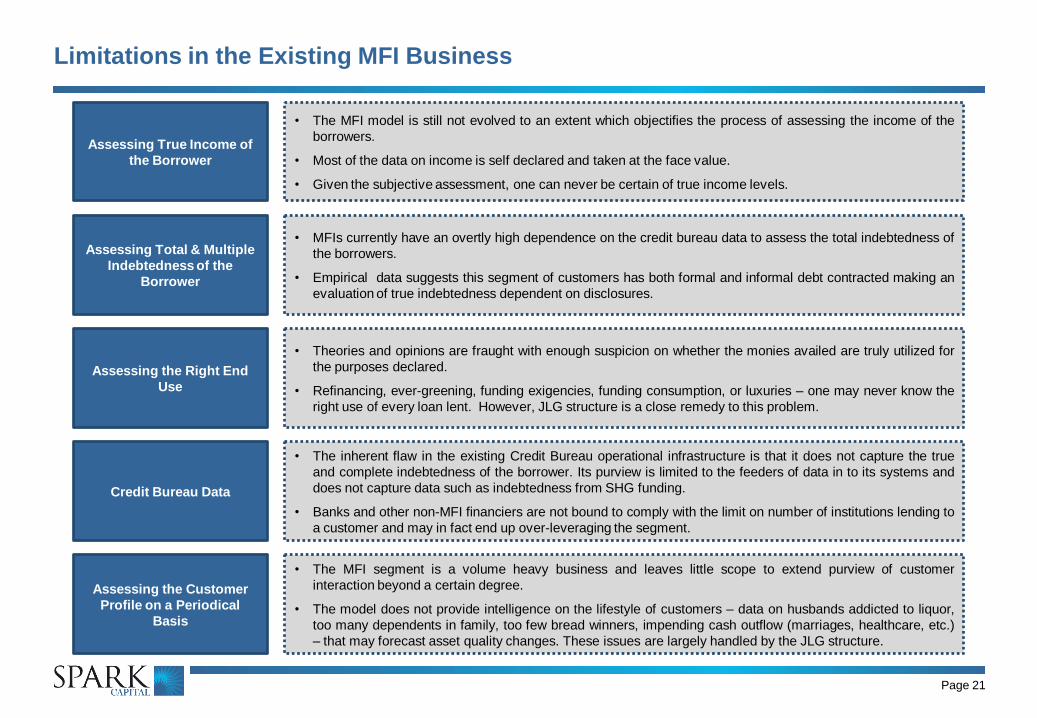

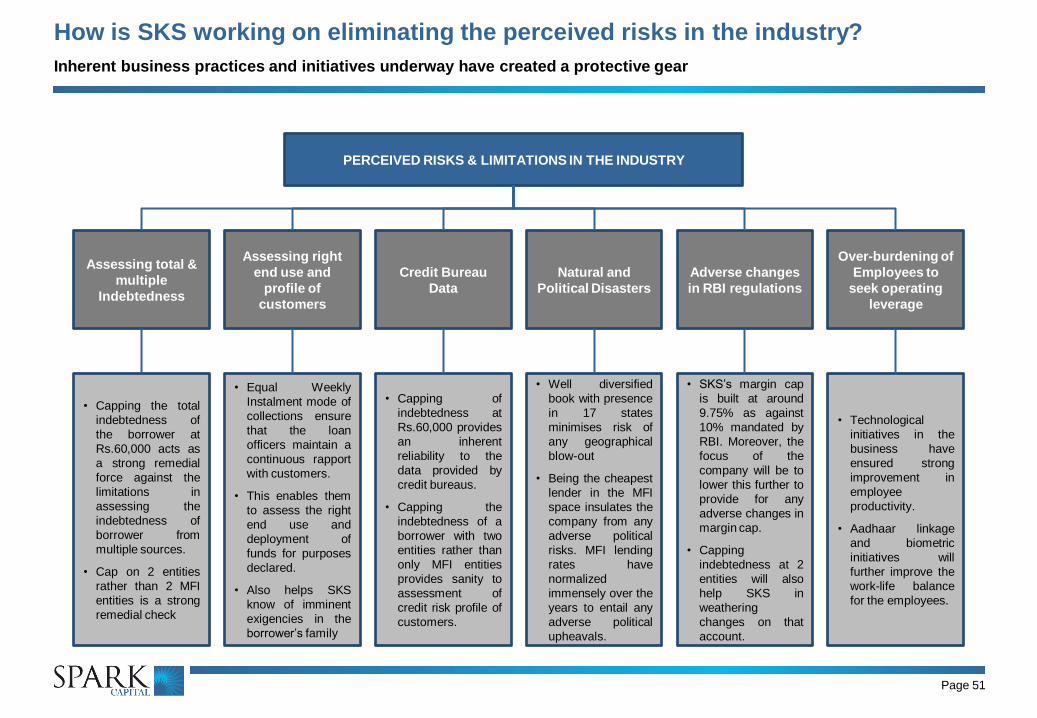

Limitations in the Existing MFI Business

Page 21

Assessing True Income of

the Borrower

Assessing Total & Multiple

Indebtedness of the

Borrower

Assessing the Right End

Use

Credit Bureau Data

• The MFI model is still not evolved to an extent which objectifies the process of assessing the income of the

borrowers.

• Most of the data on income is self declared and taken at the face value.

• Given the subjective assessment, one can never be certain of true income levels.

• MFIs currently have an overtly high dependence on the credit bureau data to assess the total indebtedness of

the borrowers.

• Empirical data suggests this segment of customers has both formal and informal debt contracted making an

evaluation of true indebtedness dependent on disclosures.

• Theories and opinions are fraught with enough suspicion on whether the monies availed are truly utilized for

the purposes declared.

• Refinancing, ever-greening, funding exigencies, funding consumption, or luxuries – one may never know the

right use of every loan lent. However, JLG structure is a close remedy to this problem.

• The inherent flaw in the existing Credit Bureau operational infrastructure is that it does not capture the true

and complete indebtedness of the borrower. Its purview is limited to the feeders of data in to its systems and

does not capture data such as indebtedness from SHG funding.

• Banks and other non-MFI financiers are not bound to comply with the limit on number of institutions lending to

a customer and may in fact end up over-leveraging the segment.

Assessing the Customer

Profile on a Periodical

Basis

• The MFI segment is a volume heavy business and leaves little scope to extend purview of customer

interaction beyond a certain degree.

• The model does not provide intelligence on the lifestyle of customers – data on husbands addicted to liquor,

too many dependents in family, too few bread winners, impending cash outflow (marriages, healthcare, etc.)

– that may forecast asset quality changes. These issues are largely handled by the JLG structure.

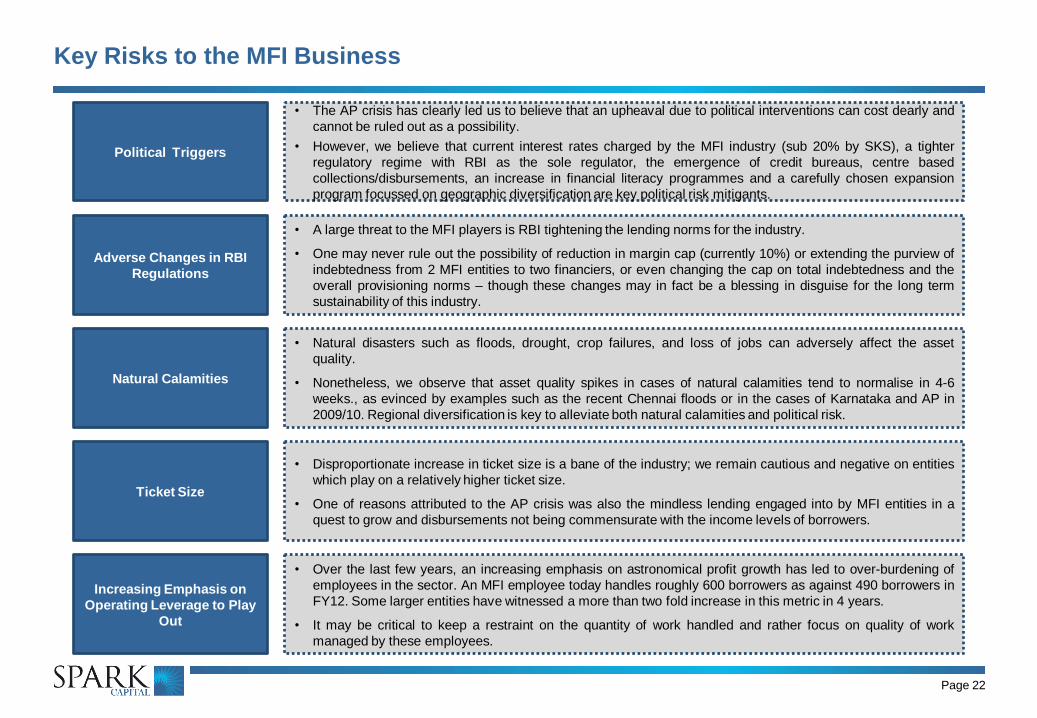

Key Risks to the MFI Business

Page 22

Political Triggers

Adverse Changes in RBI

Regulations

Natural Calamities

Ticket Size

• The AP crisis has clearly led us to believe that an upheaval due to political interventions can cost dearly and

cannot be ruled out as a possibility.

• However, we believe that current interest rates charged by the MFI industry (sub 20% by SKS), a tighter

regulatory regime with RBI as the sole regulator, the emergence of credit bureaus, centre based

collections/disbursements, an increase in financial literacy programmes and a carefully chosen expansion

program focussed on geographic diversification are key political risk mitigants.

• A large threat to the MFI players is RBI tightening the lending norms for the industry.

• One may never rule out the possibility of reduction in margin cap (currently 10%) or extending the purview of

indebtedness from 2 MFI entities to two financiers, or even changing the cap on total indebtedness and the

overall provisioning norms – though these changes may in fact be a blessing in disguise for the long term

sustainability of this industry.

• Natural disasters such as floods, drought, crop failures, and loss of jobs can adversely affect the asset

quality.

• Nonetheless, we observe that asset quality spikes in cases of natural calamities tend to normalise in 4-6

weeks., as evinced by examples such as the recent Chennai floods or in the cases of Karnataka and AP in

2009/10. Regional diversification is key to alleviate both natural calamities and political risk.

• Disproportionate increase in ticket size is a bane of the industry; we remain cautious and negative on entities

which play on a relatively higher ticket size.

• One of reasons attributed to the AP crisis was also the mindless lending engaged into by MFI entities in a

quest to grow and disbursements not being commensurate with the income levels of borrowers.

Increasing Emphasis on

Operating Leverage to Play

Out

• Over the last few years, an increasing emphasis on astronomical profit growth has led to over-burdening of

employees in the sector. An MFI employee today handles roughly 600 borrowers as against 490 borrowers in

FY12. Some larger entities have witnessed a more than two fold increase in this metric in 4 years.

• It may be critical to keep a restraint on the quantity of work handled and rather focus on quality of work

managed by these employees.

Page 23

Company Section

Page 24

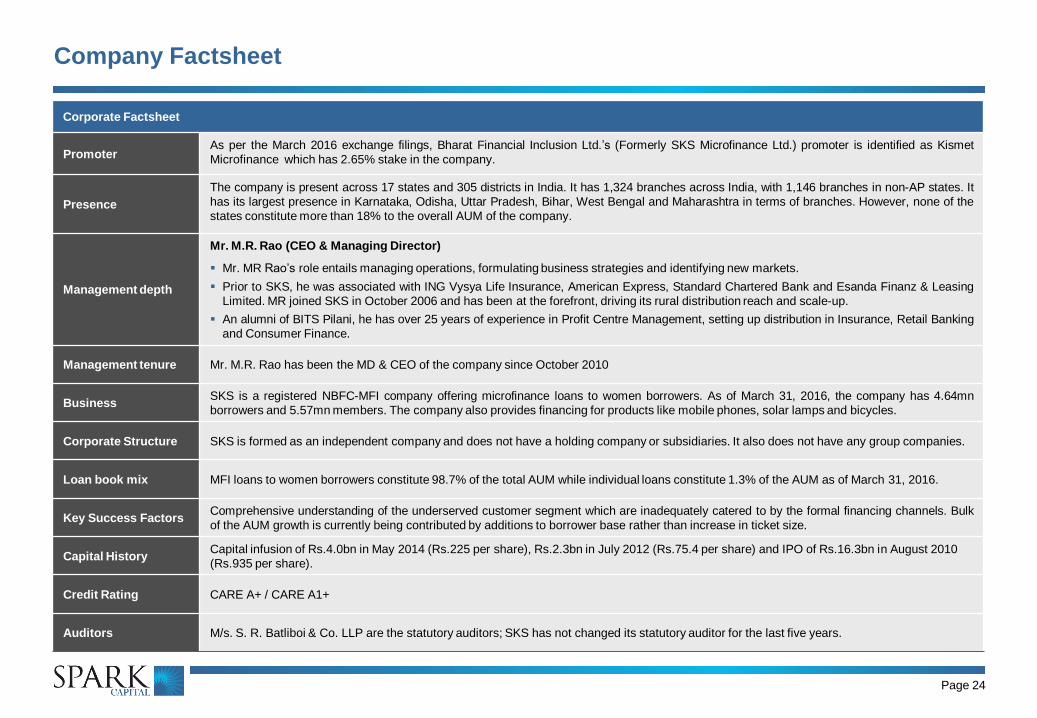

Corporate Factsheet

Promoter As per the March 2016 exchange filings, Bharat Financial Inclusion Ltd.’s (Formerly SKS Microfinance Ltd.) promoter is identified as Kismet

Microfinance which has 2.65% stake in the company.

Presence

The company is present across 17 states and 305 districts in India. It has 1,324 branches across India, with 1,146 branches in non-AP states. It

has its largest presence in Karnataka, Odisha, Uttar Pradesh, Bihar, West Bengal and Maharashtra in terms of branches. However, none of the

states constitute more than 18% to the overall AUM of the company.

Management depth

Mr. M.R. Rao (CEO & Managing Director)

Mr. MR Rao’s role entails managing operations, formulating business strategies and identifying new markets.

Prior to SKS, he was associated with ING Vysya Life Insurance, American Express, Standard Chartered Bank and Esanda Finanz & Leasing

Limited. MR joined SKS in October 2006 and has been at the forefront, driving its rural distribution reach and scale-up.

An alumni of BITS Pilani, he has over 25 years of experience in Profit Centre Management, setting up distribution in Insurance, Retail Banking

and Consumer Finance.

Management tenure Mr. M.R. Rao has been the MD & CEO of the company since October 2010

Business SKS is a registered NBFC-MFI company offering microfinance loans to women borrowers. As of March 31, 2016, the company has 4.64mn

borrowers and 5.57mn members. The company also provides financing for products like mobile phones, solar lamps and bicycles.

Corporate Structure SKS is formed as an independent company and does not have a holding company or subsidiaries. It also does not have any group companies.

Loan book mix MFI loans to women borrowers constitute 98.7% of the total AUM while individual loans constitute 1.3% of the AUM as of March 31, 2016.

Key Success Factors Comprehensive understanding of the underserved customer segment which are inadequately catered to by the formal financing channels. Bulk

of the AUM growth is currently being contributed by additions to borrower base rather than increase in ticket size.

Capital History Capital infusion of Rs.4.0bn in May 2014 (Rs.225 per share), Rs.2.3bn in July 2012 (Rs.75.4 per share) and IPO of Rs.16.3bn in August 2010

(Rs.935 per share).

Credit Rating CARE A+ / CARE A1+

Auditors M/s. S. R. Batliboi & Co. LLP are the statutory auditors; SKS has not changed its statutory auditor for the last five years.

Company Factsheet

Page 25

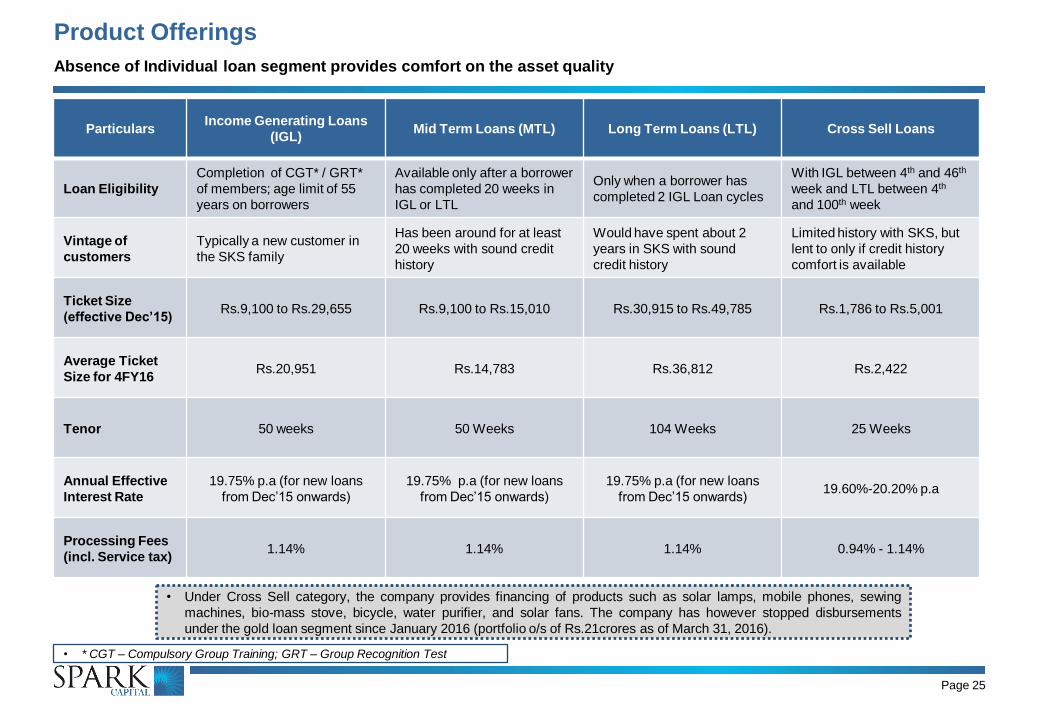

Product Offerings

Absence of Individual loan segment provides comfort on the asset quality

Particulars Income Generating Loans

(IGL) Mid Term Loans (MTL) Long Term Loans (LTL) Cross Sell Loans

Loan Eligibility

Completion of CGT* / GRT*

of members; age limit of 55

years on borrowers

Available only after a borrower

has completed 20 weeks in

IGL or LTL

Only when a borrower has

completed 2 IGL Loan cycles

With IGL between 4th and 46th

week and LTL between 4th

and 100th week

Vintage of

customers

Typically a new customer in

the SKS family

Has been around for at least

20 weeks with sound credit

history

Would have spent about 2

years in SKS with sound

credit history

Limited history with SKS, but

lent to only if credit history

comfort is available

Ticket Size

(effective Dec’15) Rs.9,100 to Rs.29,655 Rs.9,100 to Rs.15,010 Rs.30,915 to Rs.49,785 Rs.1,786 to Rs.5,001

Average Ticket

Size for 4FY16 Rs.20,951 Rs.14,783 Rs.36,812 Rs.2,422

Tenor 50 weeks 50 Weeks 104 Weeks 25 Weeks

Annual Effective

Interest Rate

19.75% p.a (for new loans

from Dec’15 onwards)

19.75% p.a (for new loans

from Dec’15 onwards)

19.75% p.a (for new loans

from Dec’15 onwards) 19.60%-20.20% p.a

Processing Fees

(incl. Service tax) 1.14% 1.14% 1.14% 0.94% - 1.14%

• Under Cross Sell category, the company provides financing of products such as solar lamps, mobile phones, sewing

machines, bio-mass stove, bicycle, water purifier, and solar fans. The company has however stopped disbursements

under the gold loan segment since January 2016 (portfolio o/s of Rs.21crores as of March 31, 2016).

• * CGT – Compulsory Group Training; GRT – Group Recognition Test

Page 26

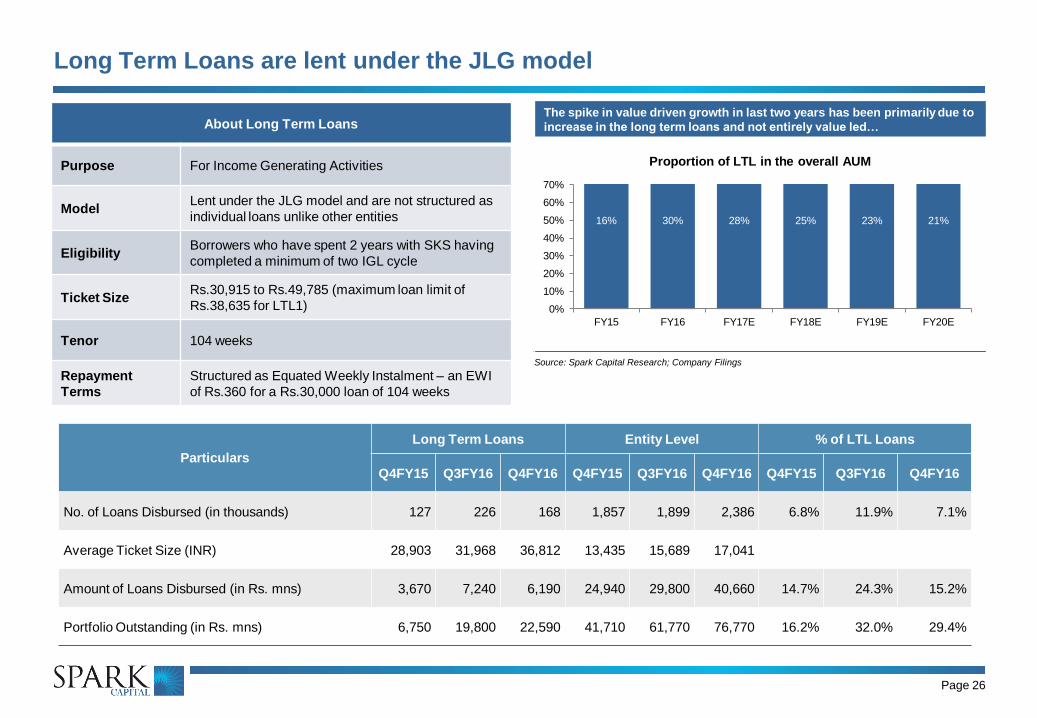

Long Term Loans are lent under the JLG model

About Long Term Loans

Purpose For Income Generating Activities

Model Lent under the JLG model and are not structured as

individual loans unlike other entities

Eligibility Borrowers who have spent 2 years with SKS having

completed a minimum of two IGL cycle

Ticket Size Rs.30,915 to Rs.49,785 (maximum loan limit of

Rs.38,635 for LTL1)

Tenor 104 weeks

Repayment

Terms

Structured as Equated Weekly Instalment – an EWI

of Rs.360 for a Rs.30,000 loan of 104 weeks

Particulars

Long Term Loans Entity Level % of LTL Loans

Q4FY15 Q3FY16 Q4FY16 Q4FY15 Q3FY16 Q4FY16 Q4FY15 Q3FY16 Q4FY16

No. of Loans Disbursed (in thousands) 127 226 168 1,857 1,899 2,386 6.8% 11.9% 7.1%

Average Ticket Size (INR) 28,903 31,968 36,812 13,435 15,689 17,041

Amount of Loans Disbursed (in Rs. mns) 3,670 7,240 6,190 24,940 29,800 40,660 14.7% 24.3% 15.2%

Portfolio Outstanding (in Rs. mns) 6,750 19,800 22,590 41,710 61,770 76,770 16.2% 32.0% 29.4%

The spike in value driven growth in last two years has been primarily due to

increase in the long term loans and not entirely value led…

Source: Spark Capital Research; Company Filings

16% 30% 28% 25% 23% 21%

0%

10%

20%

30%

40%

50%

60%

70%

FY15 FY16 FY17E FY18E FY19E FY20E

Proportion of LTL in the overall AUM

Page 27

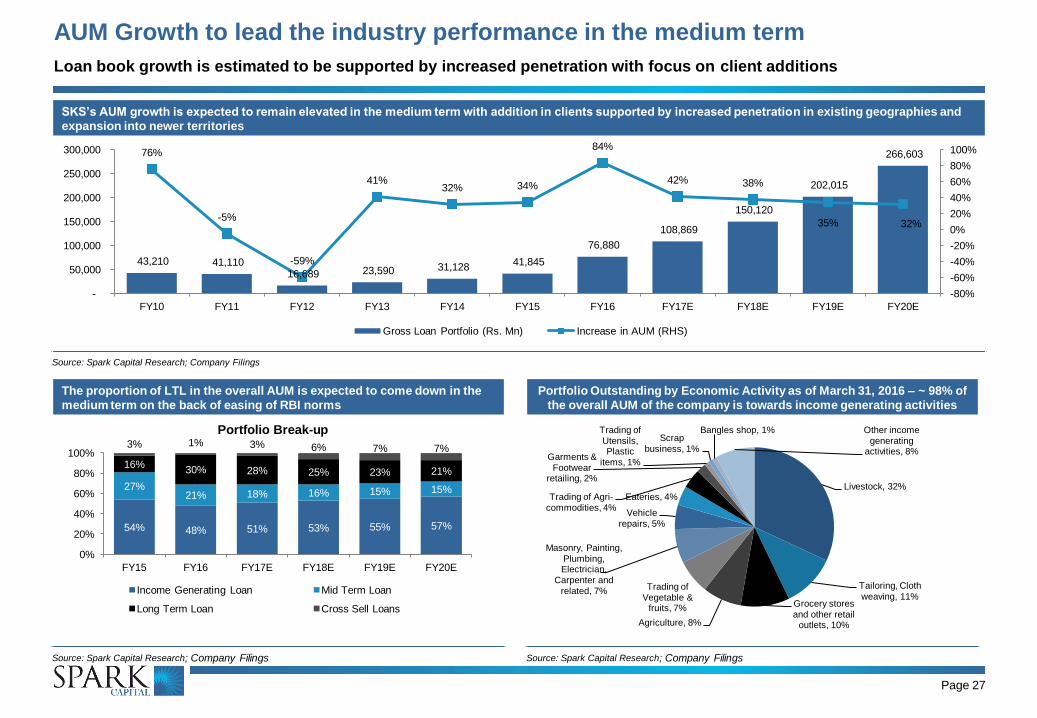

AUM Growth to lead the industry performance in the medium term

The proportion of LTL in the overall AUM is expected to come down in the

medium term on the back of easing of RBI norms

Source: Spark Capital Research; Company Filings

SKS’s AUM growth is expected to remain elevated in the medium term with addition in clients supported by increased penetration in existing geographies and

expansion into newer territories

Source: Spark Capital Research; Company Filings

43,210 41,110 16,689 23,590 31,128

41,845

76,880

108,869

150,120

202,015

266,603 76%

-5%

-59%

41% 32% 34%

84%

42% 38%

35% 32%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

-

50,000

100,000

150,000

200,000

250,000

300,000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

Gross Loan Portfolio (Rs. Mn) Increase in AUM (RHS)

54% 48% 51% 53% 55% 57%

27% 21% 18% 16% 15% 15%

16% 30% 28% 25% 23% 21%

3% 1% 3% 6% 7% 7%

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17E FY18E FY19E FY20E

Portfolio Break-up

Income Generating Loan Mid Term Loan

Long Term Loan Cross Sell Loans

Portfolio Outstanding by Economic Activity as of March 31, 2016 – ~ 98% of

the overall AUM of the company is towards income generating activities

Source: Spark Capital Research; Company Filings

Livestock, 32%

Tailoring, Cloth weaving, 11%

Grocery stores and other retail

outlets, 10% Agriculture, 8%

Trading of Vegetable &

fruits, 7%

Masonry, Painting, Plumbing, Electrician,

Carpenter and

related, 7%

Vehicle repairs, 5%

Eateries, 4% Trading of Agri-commodities, 4%

Garments &

Footwear retailing, 2%

Trading of Utensils, Plastic

items, 1%

Scrap

business, 1%

Bangles shop, 1% Other income generating

activities, 8%

Loan book growth is estimated to be supported by increased penetration with focus on client additions

…as evident from the split of volume-value-impact of LTL in the last 3 years

Source: Spark Capital Research; Company Filings; *Due to introduction of Long Term Loans

Page 28

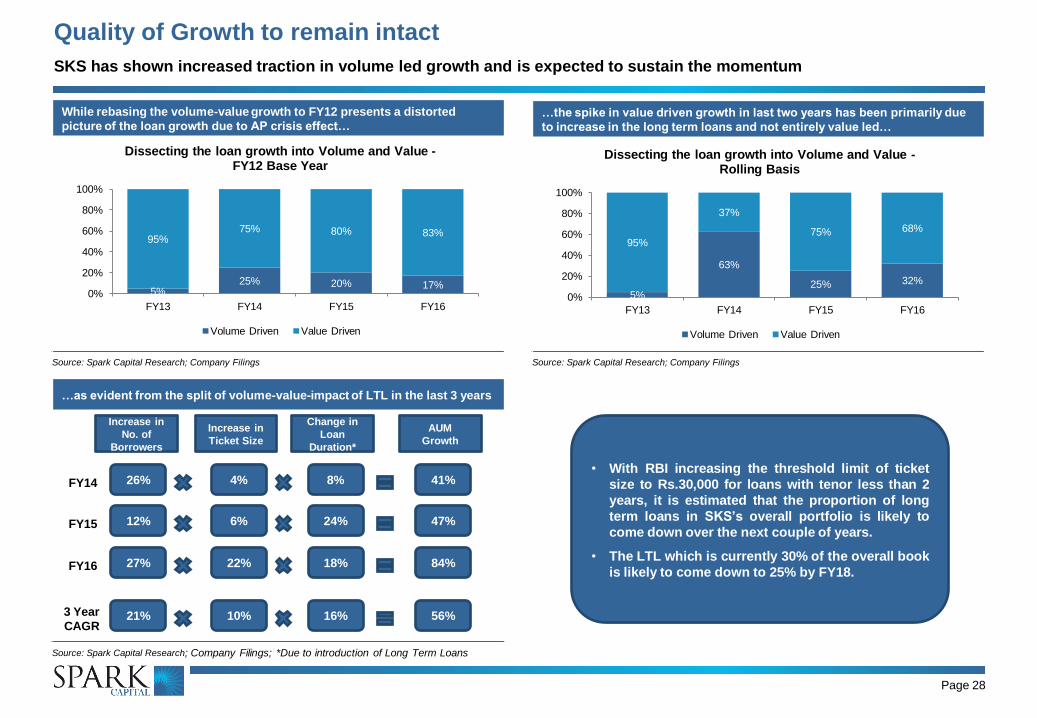

Quality of Growth to remain intact

SKS has shown increased traction in volume led growth and is expected to sustain the momentum

…the spike in value driven growth in last two years has been primarily due

to increase in the long term loans and not entirely value led…

Source: Spark Capital Research; Company Filings

While rebasing the volume-value growth to FY12 presents a distorted

picture of the loan growth due to AP crisis effect…

Source: Spark Capital Research; Company Filings

5% 25% 20% 17%

95% 75% 80% 83%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16

Dissecting the loan growth into Volume and Value - FY12 Base Year

Volume Driven Value Driven

5%

63%

25% 32%

95%

37%

75% 68%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16

Dissecting the loan growth into Volume and Value - Rolling Basis

Volume Driven Value Driven

• With RBI increasing the threshold limit of ticket

size to Rs.30,000 for loans with tenor less than 2

years, it is estimated that the proportion of long

term loans in SKS’s overall portfolio is likely to

come down over the next couple of years.

• The LTL which is currently 30% of the overall book

is likely to come down to 25% by FY18.

Increase in

No. of

Borrowers

Increase in

Ticket Size

Change in

Loan

Duration*

AUM

Growth

FY14

FY15

FY16

26% 4% 8% 41%

12% 6% 24% 47%

27% 22% 18% 84%

3 Year

CAGR 21% 10% 16% 56%

Page 29

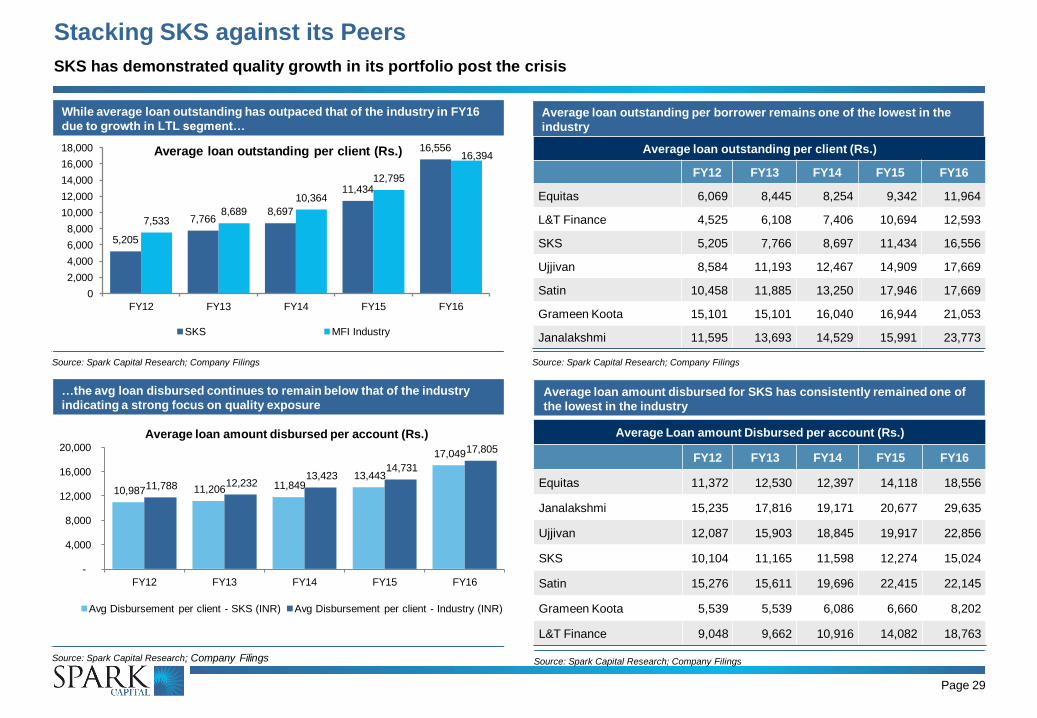

Stacking SKS against its Peers

SKS has demonstrated quality growth in its portfolio post the crisis

Average loan outstanding per borrower remains one of the lowest in the

industry

Source: Spark Capital Research; Company Filings

…the avg loan disbursed continues to remain below that of the industry

indicating a strong focus on quality exposure

Source: Spark Capital Research; Company Filings

While average loan outstanding has outpaced that of the industry in FY16

due to growth in LTL segment…

Source: Spark Capital Research; Company Filings

5,205

7,766 8,697

11,434

16,556

7,533 8,689

10,364

12,795

16,394

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

FY12 FY13 FY14 FY15 FY16

Average loan outstanding per client (Rs.)

SKS MFI Industry

Average loan outstanding per client (Rs.)

FY12 FY13 FY14 FY15 FY16

Equitas 6,069 8,445 8,254 9,342 11,964

L&T Finance 4,525 6,108 7,406 10,694 12,593

SKS 5,205 7,766 8,697 11,434 16,556

Ujjivan 8,584 11,193 12,467 14,909 17,669

Satin 10,458 11,885 13,250 17,946 17,669

Grameen Koota 15,101 15,101 16,040 16,944 21,053

Janalakshmi 11,595 13,693 14,529 15,991 23,773

Average loan amount disbursed for SKS has consistently remained one of

the lowest in the industry

Source: Spark Capital Research; Company Filings

Average Loan amount Disbursed per account (Rs.)

FY12 FY13 FY14 FY15 FY16

Equitas 11,372 12,530 12,397 14,118 18,556

Janalakshmi 15,235 17,816 19,171 20,677 29,635

Ujjivan 12,087 15,903 18,845 19,917 22,856

SKS 10,104 11,165 11,598 12,274 15,024

Satin 15,276 15,611 19,696 22,415 22,145

Grameen Koota 5,539 5,539 6,086 6,660 8,202

L&T Finance 9,048 9,662 10,916 14,082 18,763

10,987 11,206 11,849 13,443

17,049

11,788 12,232 13,423

14,731

17,805

-

4,000

8,000

12,000

16,000

20,000

FY12 FY13 FY14 FY15 FY16

Average loan amount disbursed per account (Rs.)

Avg Disbursement per client - SKS (INR) Avg Disbursement per client - Industry (INR)

Page 30

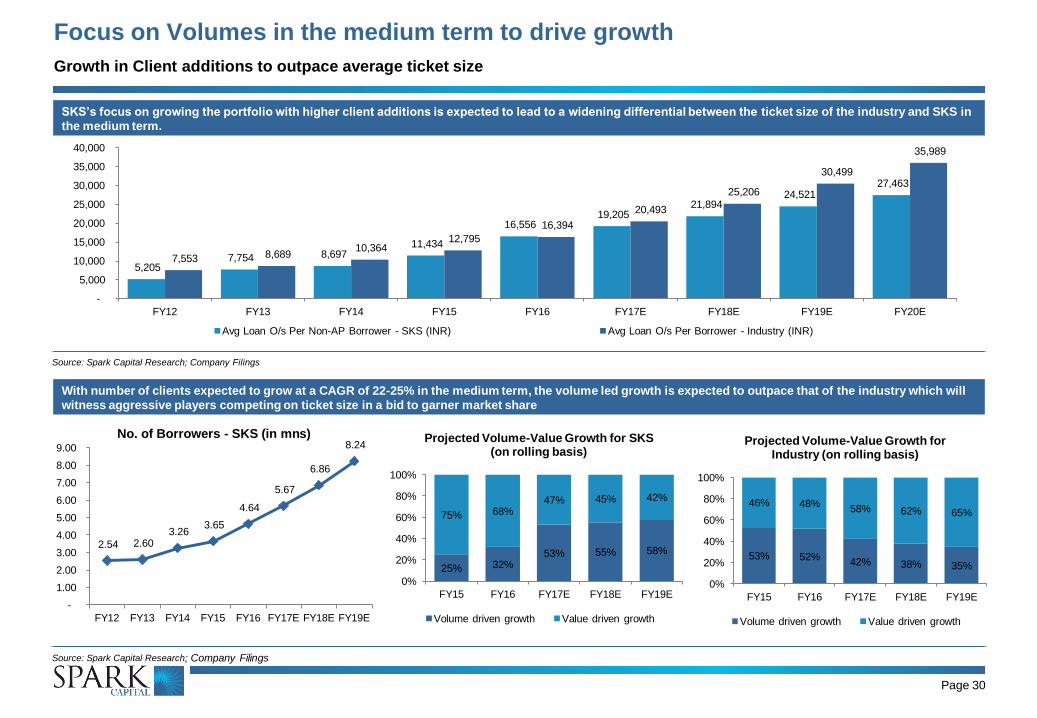

Focus on Volumes in the medium term to drive growth

Growth in Client additions to outpace average ticket size

With number of clients expected to grow at a CAGR of 22-25% in the medium term, the volume led growth is expected to outpace that of the industry which will

witness aggressive players competing on ticket size in a bid to garner market share

Source: Spark Capital Research; Company Filings

SKS’s focus on growing the portfolio with higher client additions is expected to lead to a widening differential between the ticket size of the industry and SKS in

the medium term.

Source: Spark Capital Research; Company Filings

5,205 7,754 8,697

11,434

16,556 19,205

21,894 24,521

27,463

7,553 8,689 10,364

12,795

16,394

20,493

25,206

30,499

35,989

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

Avg Loan O/s Per Non-AP Borrower - SKS (INR) Avg Loan O/s Per Borrower - Industry (INR)

2.54 2.60 3.26

3.65

4.64

5.67

6.86

8.24

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

No. of Borrowers - SKS (in mns)

25% 32% 53% 55% 58%

75% 68% 47% 45% 42%

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17E FY18E FY19E

Projected Volume-Value Growth for SKS (on rolling basis)

Volume driven growth Value driven growth

53% 52% 42% 38% 35%

46% 48% 58% 62% 65%

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17E FY18E FY19E

Projected Volume-Value Growth for Industry (on rolling basis)

Volume driven growth Value driven growth

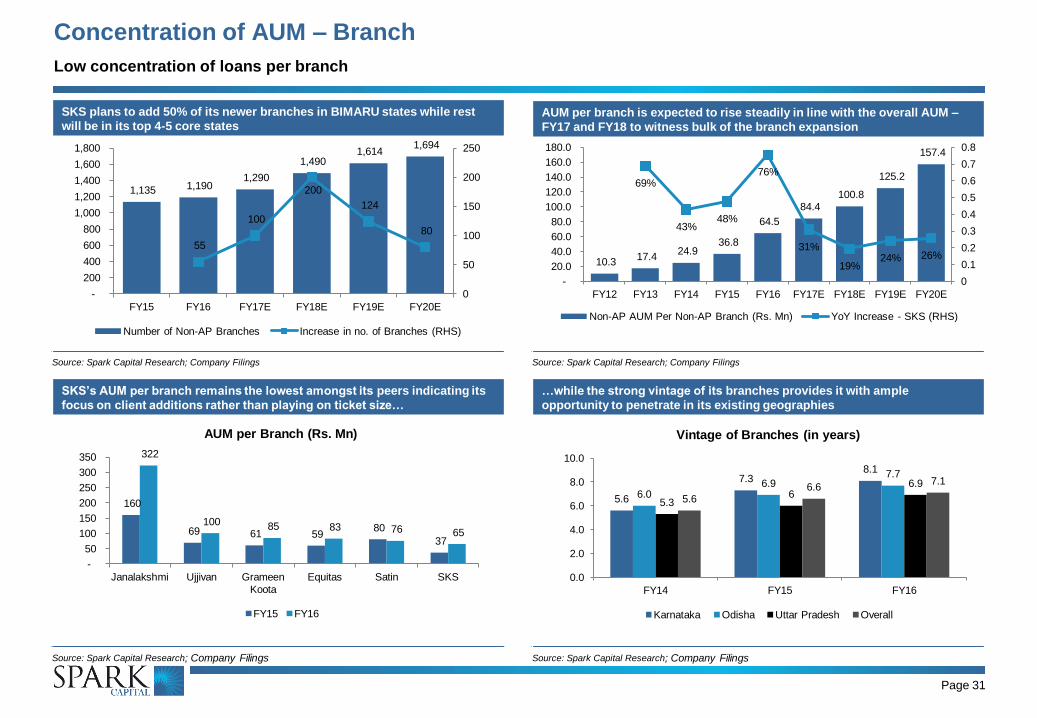

Page 31

Concentration of AUM – Branch

Low concentration of loans per branch

AUM per branch is expected to rise steadily in line with the overall AUM –

FY17 and FY18 to witness bulk of the branch expansion

Source: Spark Capital Research; Company Filings

…while the strong vintage of its branches provides it with ample

opportunity to penetrate in its existing geographies

Source: Spark Capital Research; Company Filings

SKS’s AUM per branch remains the lowest amongst its peers indicating its

focus on client additions rather than playing on ticket size…

Source: Spark Capital Research; Company Filings

SKS plans to add 50% of its newer branches in BIMARU states while rest

will be in its top 4-5 core states

Source: Spark Capital Research; Company Filings

1,135 1,190 1,290

1,490 1,614

1,694

55

100

200

124

80

0

50

100

150

200

250

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

FY15 FY16 FY17E FY18E FY19E FY20E

Number of Non-AP Branches Increase in no. of Branches (RHS)

10.3 17.4

24.9 36.8

64.5

84.4 100.8

125.2

157.4

69%

43% 48%

76%

31%

19% 24% 26%

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

Non-AP AUM Per Non-AP Branch (Rs. Mn) YoY Increase - SKS (RHS)

5.6

7.3 8.1

6.0 6.9

7.7

5.3 6

6.9

5.6 6.6

7.1

0.0

2.0

4.0

6.0

8.0

10.0

FY14 FY15 FY16

Vintage of Branches (in years)

Karnataka Odisha Uttar Pradesh Overall

160

69 61 59 80

37

322

100 85 83 76 65

-

50

100

150

200

250

300

350

Janalakshmi Ujjivan Grameen

Koota

Equitas Satin SKS

AUM per Branch (Rs. Mn)

FY15 FY16

Page 32

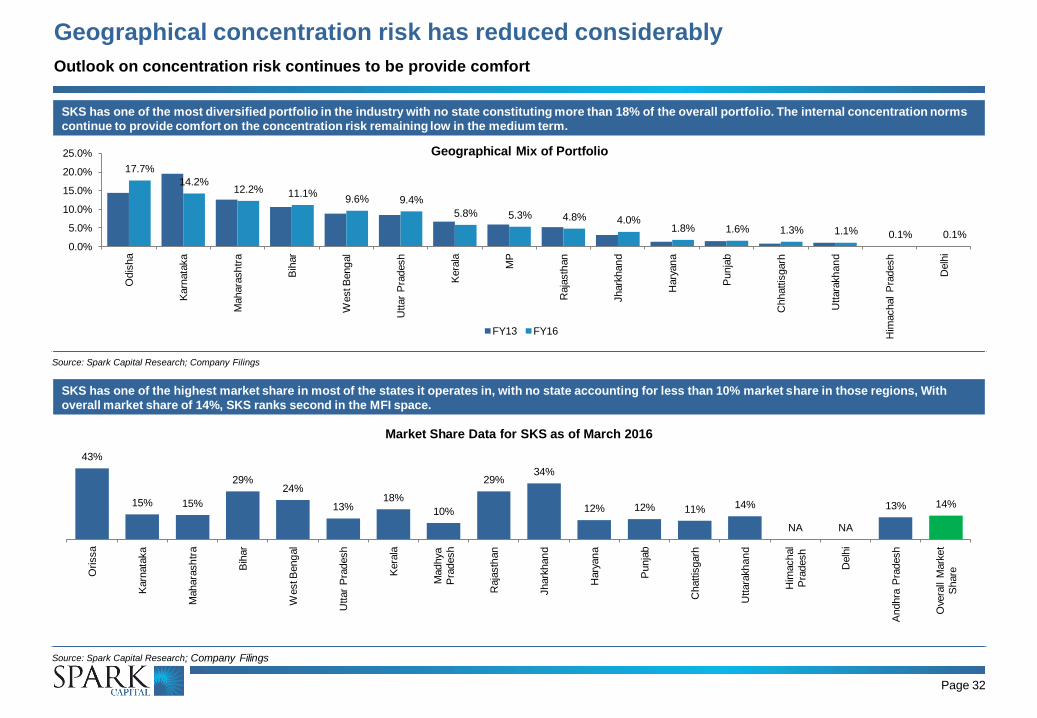

Geographical concentration risk has reduced considerably

Outlook on concentration risk continues to be provide comfort

SKS has one of the highest market share in most of the states it operates in, with no state accounting for less than 10% market share in those regions, With

overall market share of 14%, SKS ranks second in the MFI space.

Source: Spark Capital Research; Company Filings

SKS has one of the most diversified portfolio in the industry with no state constituting more than 18% of the overall portfolio. The internal concentration norms

continue to provide comfort on the concentration risk remaining low in the medium term.

Source: Spark Capital Research; Company Filings

17.7%

14.2% 12.2% 11.1%

9.6% 9.4%

5.8% 5.3% 4.8% 4.0% 1.8% 1.6% 1.3% 1.1% 0.1% 0.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Odis

ha

Karn

ata

ka

Mahara

sh

tra

Bih

ar

West B

eng

al

Uttar

Pra

desh

Kera

la

MP

Raja

sth

an

Jhark

han

d

Hary

an

a

Punja

b

Chhattis

garh

Uttara

kh

an

d

Him

achal

Pra

desh

Delh

i

Geographical Mix of Portfolio

FY13 FY16

43%

15% 15%

29% 24%

13% 18%

10%

29% 34%

12% 12% 11% 14%

NA NA

13% 14%

Orissa

Karn

ata

ka

Mahara

sh

tra

Bih

ar

West B

eng

al

Uttar

Pra

desh

Kera

la

Madhya

Pra

desh

Raja

sth

an

Jhark

han

d

Hary

an

a

Punja

b

Chattis

garh

Uttara

kh

an

d

Him

achal

Pra

desh

Delh

i

Andhra

Pra

desh

Ove

rall

Mark

et

Share

Market Share Data for SKS as of March 2016

Page 33

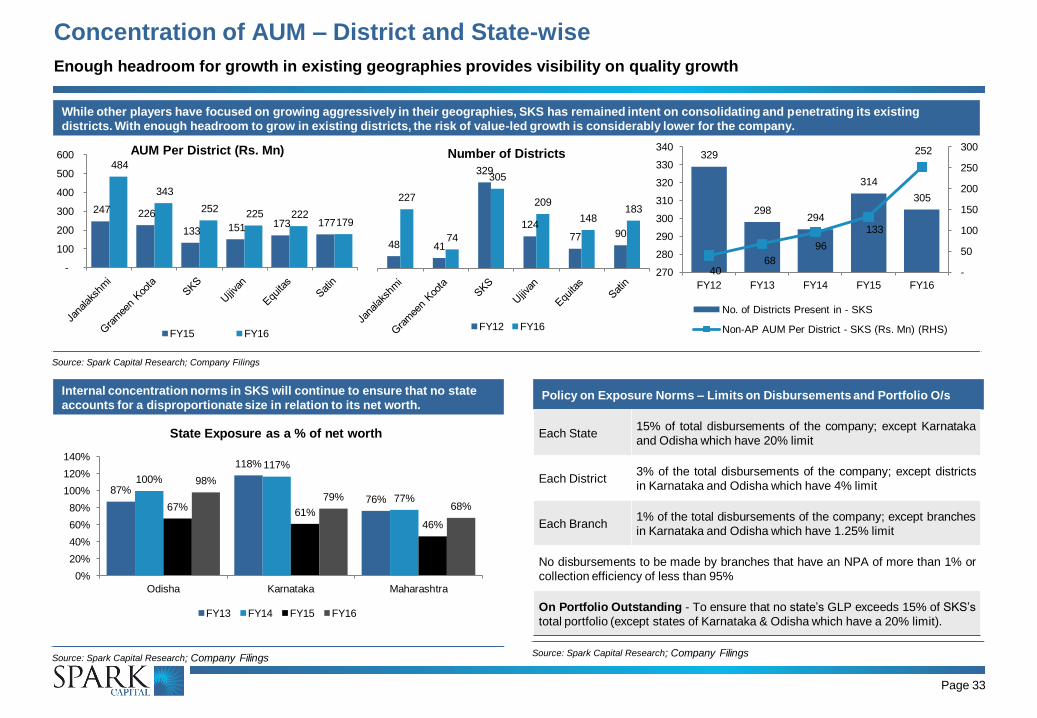

Concentration of AUM – District and State-wise

Enough headroom for growth in existing geographies provides visibility on quality growth

Policy on Exposure Norms – Limits on Disbursements and Portfolio O/s

Source: Spark Capital Research; Company Filings

Internal concentration norms in SKS will continue to ensure that no state

accounts for a disproportionate size in relation to its net worth.

Source: Spark Capital Research; Company Filings

While other players have focused on growing aggressively in their geographies, SKS has remained intent on consolidating and penetrating its existing

districts. With enough headroom to grow in existing districts, the risk of value-led growth is considerably lower for the company.

Source: Spark Capital Research; Company Filings

87%

118%

76%

100%

117%

77% 67%

61% 46%

98%

79% 68%

0%

20%

40%

60%

80%

100%

120%

140%

Odisha Karnataka Maharashtra

State Exposure as a % of net worth

FY13 FY14 FY15 FY16

Each State 15% of total disbursements of the company; except Karnataka

and Odisha which have 20% limit

Each District 3% of the total disbursements of the company; except districts

in Karnataka and Odisha which have 4% limit

Each Branch 1% of the total disbursements of the company; except branches

in Karnataka and Odisha which have 1.25% limit

No disbursements to be made by branches that have an NPA of more than 1% or

collection efficiency of less than 95%

On Portfolio Outstanding - To ensure that no state’s GLP exceeds 15% of SKS’s

total portfolio (except states of Karnataka & Odisha which have a 20% limit).

247 226

133 151 173 177

484

343

252 225 222

179

-

100

200

300

400

500

600 AUM Per District (Rs. Mn)

FY15 FY16

48 41

329

124

77 90

227

74

305

209

148 183

Number of Districts

FY12 FY16

329

298 294

314

305

40 68

96

133

252

-

50

100

150

200

250

300

270

280

290

300

310

320

330

340

FY12 FY13 FY14 FY15 FY16

No. of Districts Present in - SKS

Non-AP AUM Per District - SKS (Rs. Mn) (RHS)

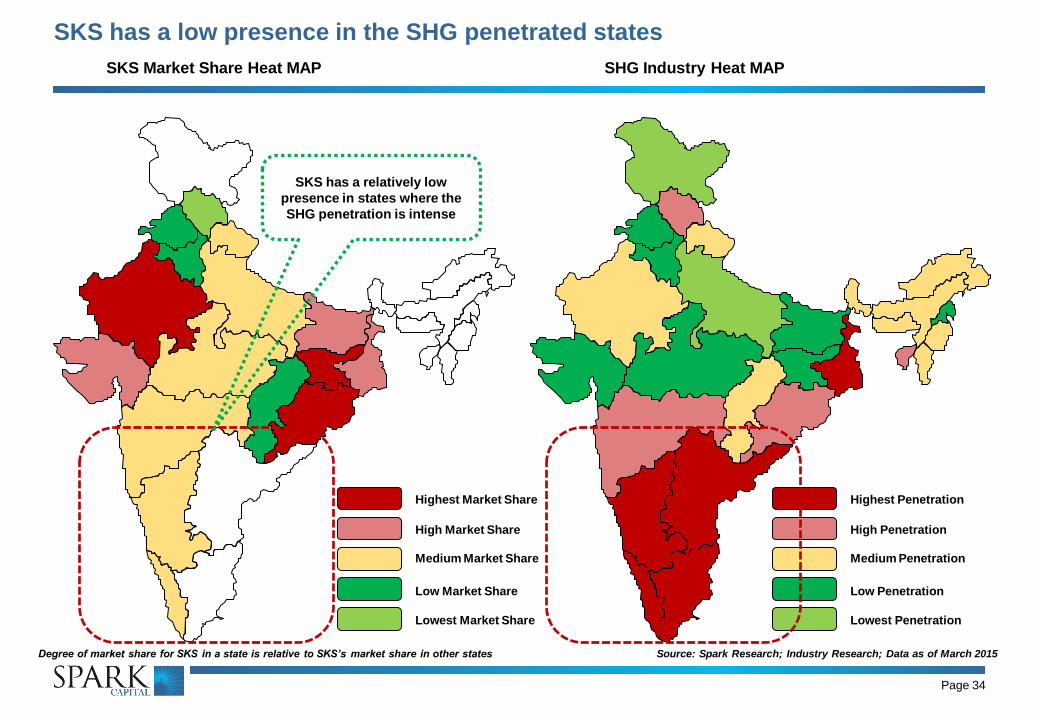

SKS Market Share Heat MAP

Page 34

SHG Industry Heat MAP

Highest Market Share

High Market Share

Medium Market Share

Low Market Share

Lowest Market Share

Highest Penetration

High Penetration

Medium Penetration

Low Penetration

Lowest Penetration

Degree of market share for SKS in a state is relative to SKS’s market share in other states Source: Spark Research; Industry Research; Data as of March 2015

SKS has a relatively low

presence in states where the

SHG penetration is intense

SKS has a low presence in the SHG penetrated states

Page 35

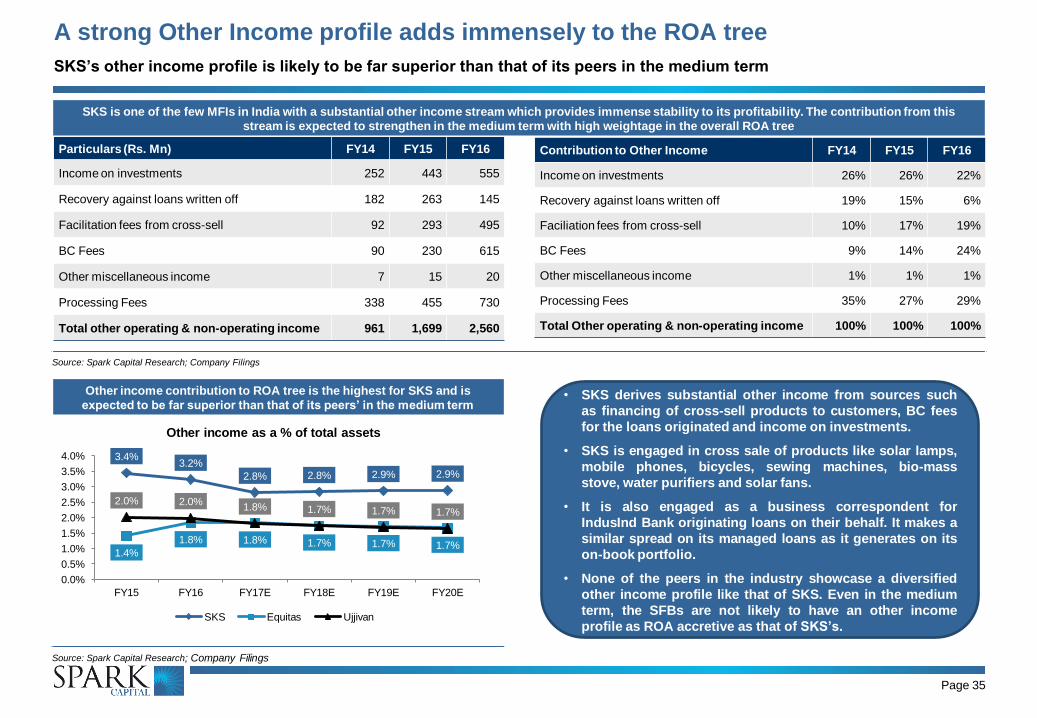

A strong Other Income profile adds immensely to the ROA tree

SKS’s other income profile is likely to be far superior than that of its peers in the medium term

Other income contribution to ROA tree is the highest for SKS and is

expected to be far superior than that of its peers’ in the medium term

Source: Spark Capital Research; Company Filings

SKS is one of the few MFIs in India with a substantial other income stream which provides immense stability to its profitability. The contribution from this

stream is expected to strengthen in the medium term with high weightage in the overall ROA tree

Source: Spark Capital Research; Company Filings

Particulars (Rs. Mn) FY14 FY15 FY16

Income on investments 252 443 555

Recovery against loans written off 182 263 145

Facilitation fees from cross-sell 92 293 495

BC Fees 90 230 615

Other miscellaneous income 7 15 20

Processing Fees 338 455 730

Total other operating & non-operating income 961 1,699 2,560

Contribution to Other Income FY14 FY15 FY16

Income on investments 26% 26% 22%

Recovery against loans written off 19% 15% 6%

Faciliation fees from cross-sell 10% 17% 19%

BC Fees 9% 14% 24%

Other miscellaneous income 1% 1% 1%

Processing Fees 35% 27% 29%

Total Other operating & non-operating income 100% 100% 100%

3.4% 3.2%

2.8% 2.8% 2.9% 2.9%

1.4%

1.8% 1.8% 1.7% 1.7% 1.7%

2.0% 2.0% 1.8% 1.7% 1.7% 1.7%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

FY15 FY16 FY17E FY18E FY19E FY20E

Other income as a % of total assets

SKS Equitas Ujjivan

• SKS derives substantial other income from sources such

as financing of cross-sell products to customers, BC fees

for the loans originated and income on investments.

• SKS is engaged in cross sale of products like solar lamps,

mobile phones, bicycles, sewing machines, bio-mass

stove, water purifiers and solar fans.

• It is also engaged as a business correspondent for

IndusInd Bank originating loans on their behalf. It makes a

similar spread on its managed loans as it generates on its

on-book portfolio.

• None of the peers in the industry showcase a diversified

other income profile like that of SKS. Even in the medium

term, the SFBs are not likely to have an other income

profile as ROA accretive as that of SKS’s.

Mobile Phones and Solar Lamps are the highest selling products under its cross-sell umbrella. They also contribute the most to the profitability of the segment.

Source: Spark Capital Research; Company Filings

Page 36

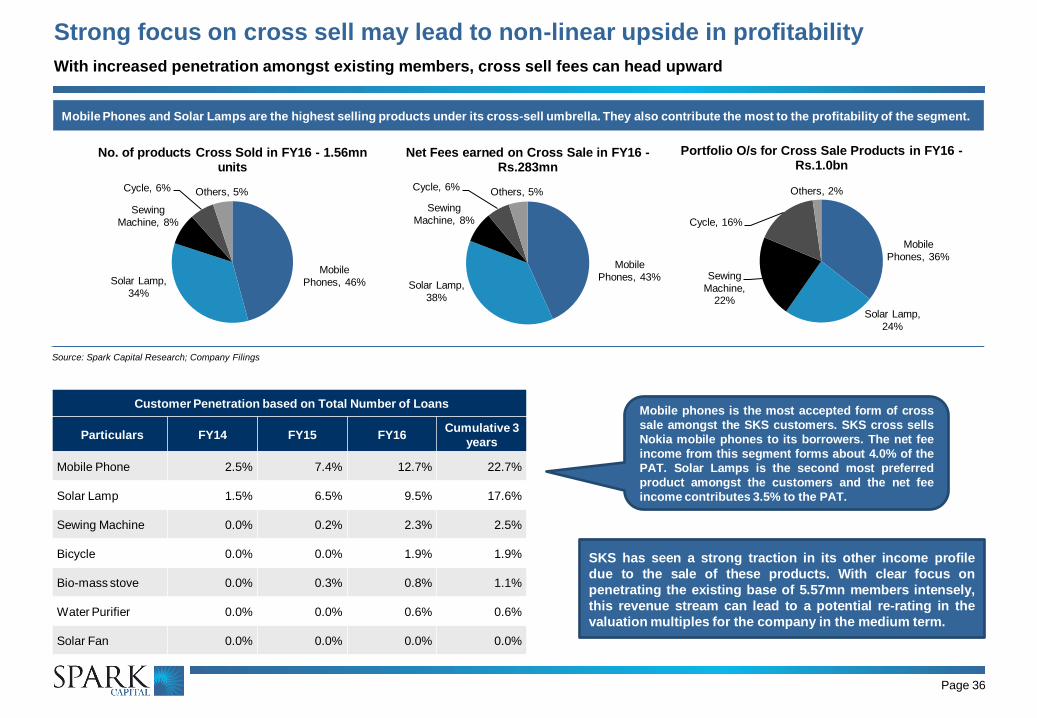

Strong focus on cross sell may lead to non-linear upside in profitability

With increased penetration amongst existing members, cross sell fees can head upward

Mobile

Phones, 46% Solar Lamp,

34%

Sewing

Machine, 8%

Cycle, 6% Others, 5%

No. of products Cross Sold in FY16 - 1.56mn units

Mobile

Phones, 43% Solar Lamp,

38%

Sewing

Machine, 8%

Cycle, 6% Others, 5%

Net Fees earned on Cross Sale in FY16 - Rs.283mn

Mobile

Phones, 36%

Solar Lamp,

24%

Sewing

Machine, 22%

Cycle, 16%

Others, 2%

Portfolio O/s for Cross Sale Products in FY16 - Rs.1.0bn

Customer Penetration based on Total Number of Loans

Particulars FY14 FY15 FY16 Cumulative 3

years

Mobile Phone 2.5% 7.4% 12.7% 22.7%

Solar Lamp 1.5% 6.5% 9.5% 17.6%

Sewing Machine 0.0% 0.2% 2.3% 2.5%

Bicycle 0.0% 0.0% 1.9% 1.9%

Bio-mass stove 0.0% 0.3% 0.8% 1.1%

Water Purifier 0.0% 0.0% 0.6% 0.6%

Solar Fan 0.0% 0.0% 0.0% 0.0%

Mobile phones is the most accepted form of cross

sale amongst the SKS customers. SKS cross sells

Nokia mobile phones to its borrowers. The net fee

income from this segment forms about 4.0% of the

PAT. Solar Lamps is the second most preferred

product amongst the customers and the net fee

income contributes 3.5% to the PAT.

SKS has seen a strong traction in its other income profile

due to the sale of these products. With clear focus on

penetrating the existing base of 5.57mn members intensely,

this revenue stream can lead to a potential re-rating in the

valuation multiples for the company in the medium term.

Page 37

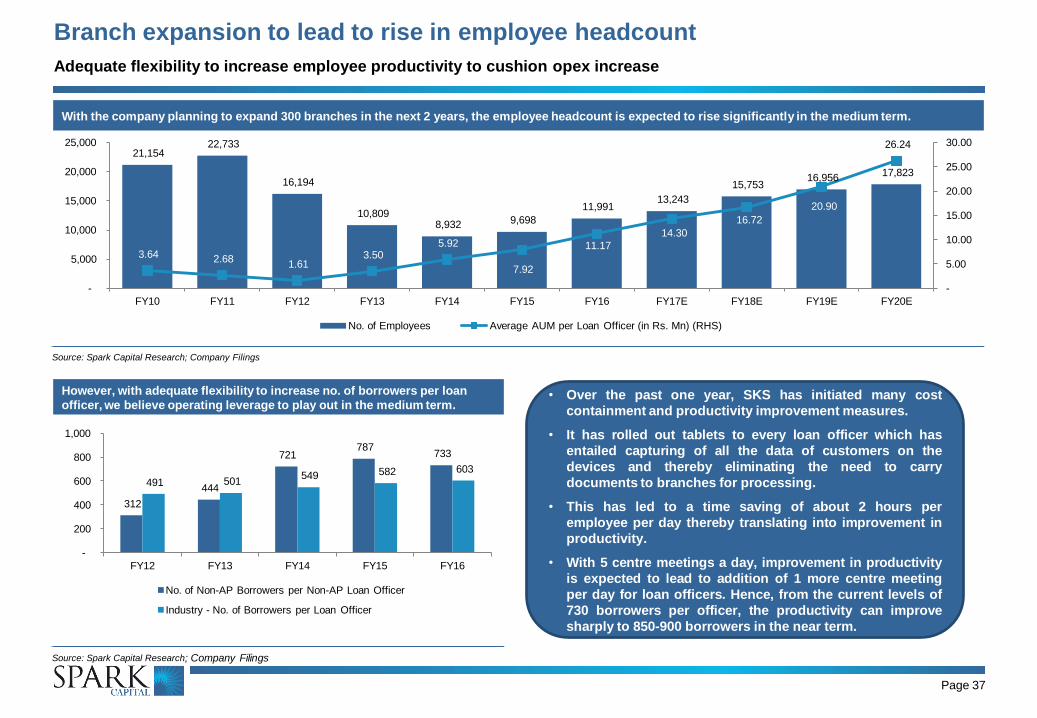

Branch expansion to lead to rise in employee headcount

Adequate flexibility to increase employee productivity to cushion opex increase

However, with adequate flexibility to increase no. of borrowers per loan

officer, we believe operating leverage to play out in the medium term.

Source: Spark Capital Research; Company Filings

With the company planning to expand 300 branches in the next 2 years, the employee headcount is expected to rise significantly in the medium term.

Source: Spark Capital Research; Company Filings

21,154 22,733

16,194

10,809 8,932 9,698

11,991 13,243

15,753 16,956

17,823

3.64 2.68 1.61

3.50 5.92

7.92

11.17

14.30

16.72

20.90

26.24

-

5.00

10.00

15.00

20.00

25.00

30.00

-

5,000

10,000

15,000

20,000

25,000

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

No. of Employees Average AUM per Loan Officer (in Rs. Mn) (RHS)

312

444

721 787

733

491 501 549 582 603

-

200

400

600

800

1,000

FY12 FY13 FY14 FY15 FY16

No. of Non-AP Borrowers per Non-AP Loan Officer

Industry - No. of Borrowers per Loan Officer

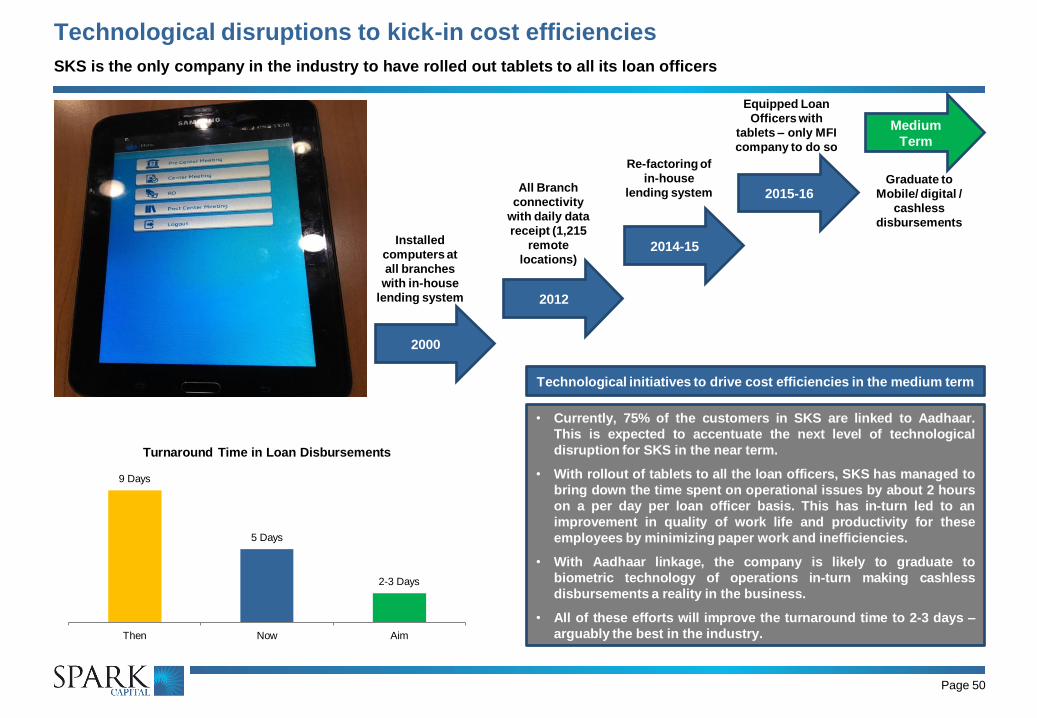

• Over the past one year, SKS has initiated many cost

containment and productivity improvement measures.

• It has rolled out tablets to every loan officer which has

entailed capturing of all the data of customers on the

devices and thereby eliminating the need to carry

documents to branches for processing.

• This has led to a time saving of about 2 hours per

employee per day thereby translating into improvement in

productivity.

• With 5 centre meetings a day, improvement in productivity

is expected to lead to addition of 1 more centre meeting

per day for loan officers. Hence, from the current levels of

730 borrowers per officer, the productivity can improve

sharply to 850-900 borrowers in the near term.

Page 38

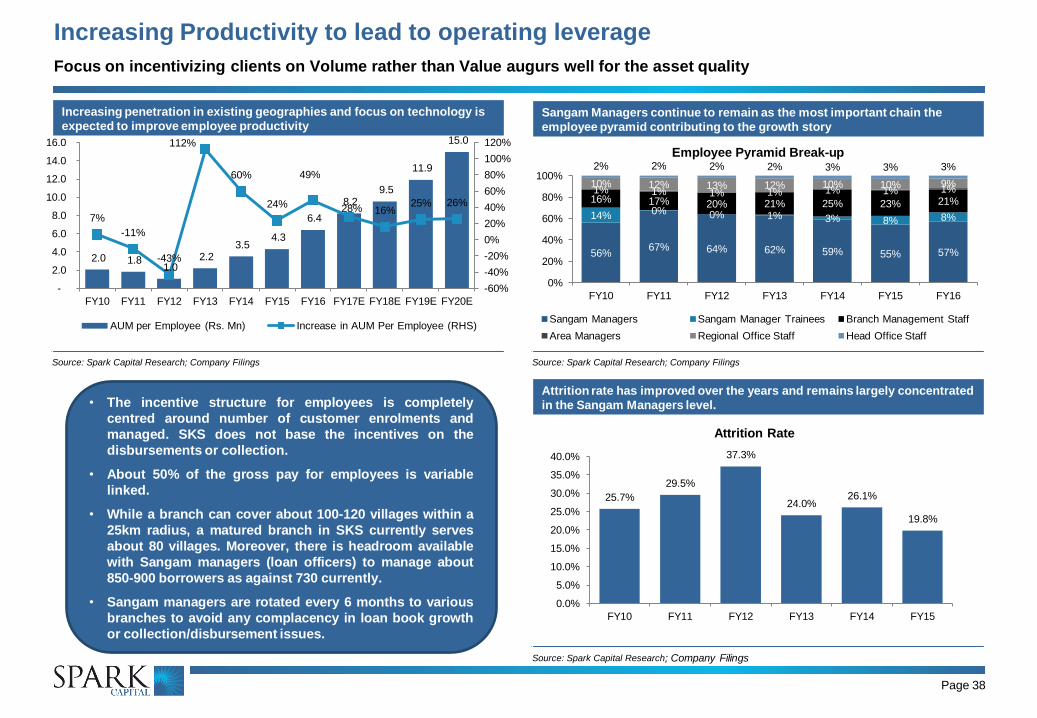

Increasing Productivity to lead to operating leverage

Focus on incentivizing clients on Volume rather than Value augurs well for the asset quality

Sangam Managers continue to remain as the most important chain the

employee pyramid contributing to the growth story

Source: Spark Capital Research; Company Filings

Attrition rate has improved over the years and remains largely concentrated

in the Sangam Managers level.

Source: Spark Capital Research; Company Filings

Increasing penetration in existing geographies and focus on technology is

expected to improve employee productivity

Source: Spark Capital Research; Company Filings

2.0 1.8 1.0

2.2 3.5

4.3

6.4

8.2 9.5

11.9

15.0

7%

-11%

-43%

112%

60%

24%

49%

28% 16% 25% 26%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E FY20E

AUM per Employee (Rs. Mn) Increase in AUM Per Employee (RHS)

56% 67% 64% 62% 59% 55% 57%

14% 0% 0% 1% 3% 8% 8%

16% 17% 20% 21% 25% 23% 21% 1% 1% 1% 1% 1% 1% 1% 10% 12% 13% 12% 10% 10% 9%

2% 2% 2% 2% 3% 3% 3%

0%

20%

40%

60%

80%

100%

FY10 FY11 FY12 FY13 FY14 FY15 FY16

Employee Pyramid Break-up

Sangam Managers Sangam Manager Trainees Branch Management Staff

Area Managers Regional Office Staff Head Office Staff

25.7%

29.5%

37.3%

24.0% 26.1%

19.8%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

FY10 FY11 FY12 FY13 FY14 FY15

Attrition Rate

• The incentive structure for employees is completely

centred around number of customer enrolments and

managed. SKS does not base the incentives on the

disbursements or collection.

• About 50% of the gross pay for employees is variable

linked.

• While a branch can cover about 100-120 villages within a

25km radius, a matured branch in SKS currently serves

about 80 villages. Moreover, there is headroom available

with Sangam managers (loan officers) to manage about

850-900 borrowers as against 730 currently.

• Sangam managers are rotated every 6 months to various

branches to avoid any complacency in loan book growth

or collection/disbursement issues.

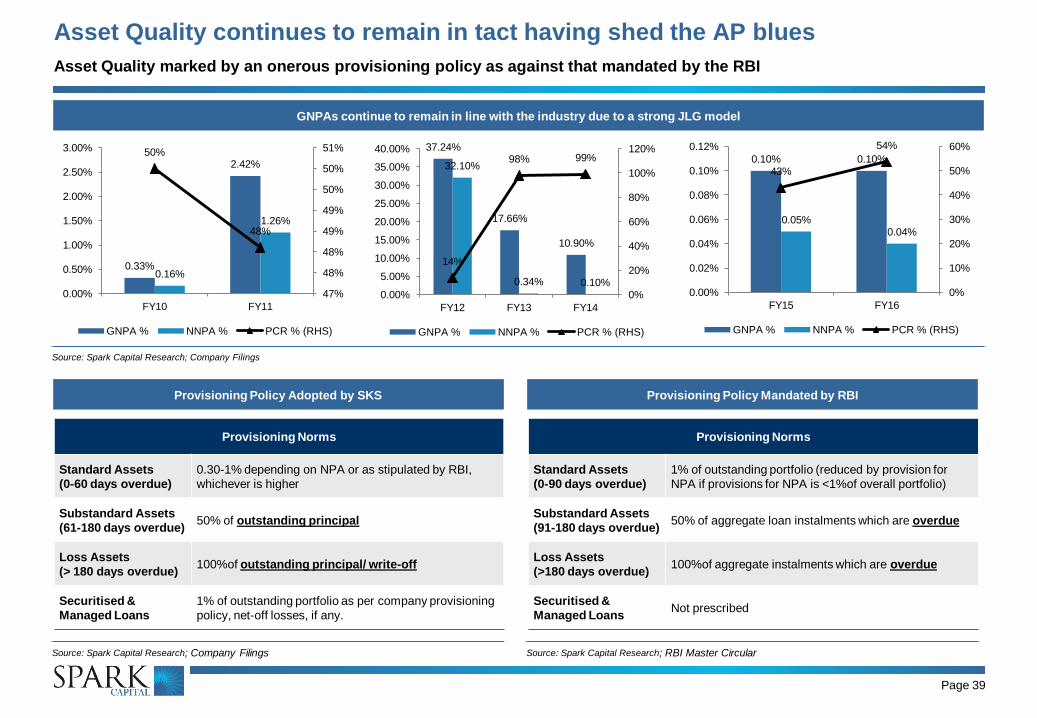

Page 39

Asset Quality continues to remain in tact having shed the AP blues

Asset Quality marked by an onerous provisioning policy as against that mandated by the RBI

GNPAs continue to remain in line with the industry due to a strong JLG model

Source: Spark Capital Research; Company Filings

0.33%

2.42%

0.16%

1.26%

50%

48%

47%

48%

48%

49%

49%

50%

50%

51%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

FY10 FY11

GNPA % NNPA % PCR % (RHS)

37.24%

17.66%

10.90%

32.10%

0.34% 0.10%

14%

98% 99%

0%

20%

40%

60%

80%

100%

120%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

FY12 FY13 FY14

GNPA % NNPA % PCR % (RHS)

0.10% 0.10%

0.05% 0.04%

43%

54%

0%

10%

20%

30%

40%

50%

60%

0.00%

0.02%

0.04%

0.06%

0.08%

0.10%

0.12%

FY15 FY16

GNPA % NNPA % PCR % (RHS)

Provisioning Policy Mandated by RBI

Source: Spark Capital Research; RBI Master Circular

Provisioning Norms

Standard Assets

(0-90 days overdue)

1% of outstanding portfolio (reduced by provision for

NPA if provisions for NPA is <1%of overall portfolio)

Substandard Assets

(91-180 days overdue) 50% of aggregate loan instalments which are overdue

Loss Assets

(>180 days overdue) 100%of aggregate instalments which are overdue

Securitised &

Managed Loans Not prescribed

Provisioning Policy Adopted by SKS

Source: Spark Capital Research; Company Filings

Provisioning Norms

Standard Assets

(0-60 days overdue)

0.30-1% depending on NPA or as stipulated by RBI,

whichever is higher

Substandard Assets

(61-180 days overdue) 50% of outstanding principal

Loss Assets

(> 180 days overdue) 100%of outstanding principal/ write-off

Securitised &

Managed Loans

1% of outstanding portfolio as per company provisioning

policy, net-off losses, if any.

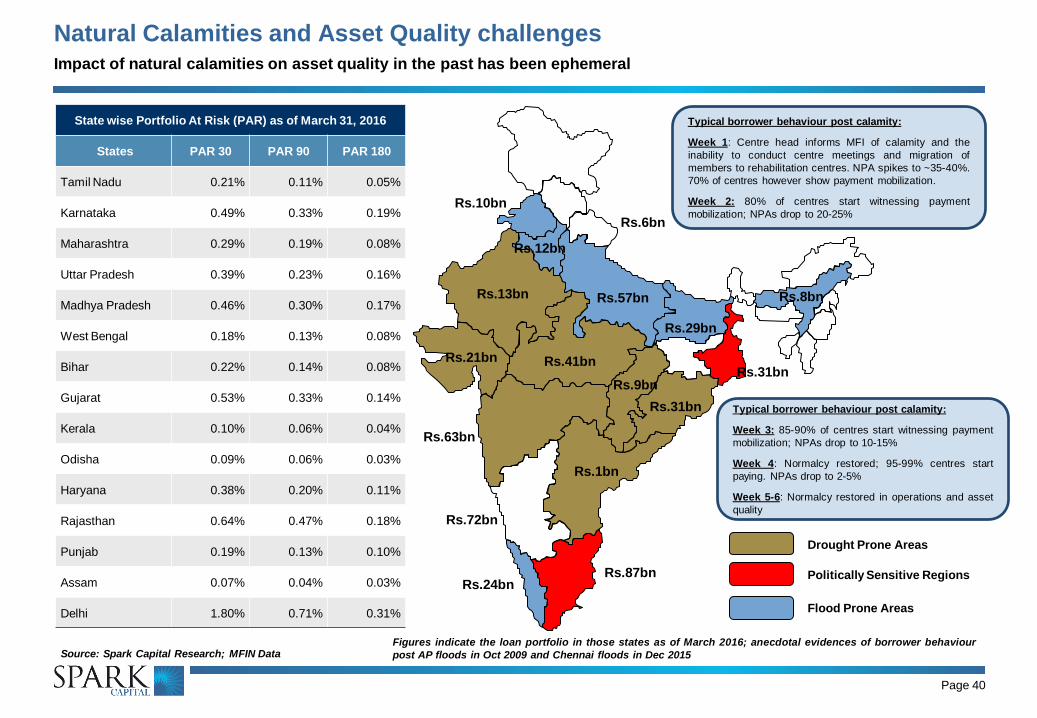

Natural Calamities and Asset Quality challenges

Page 40

Drought Prone Areas

Politically Sensitive Regions

Figures indicate the loan portfolio in those states as of March 2016; anecdotal evidences of borrower behaviour

post AP floods in Oct 2009 and Chennai floods in Dec 2015

Rs.87bn

Rs.72bn

Rs.63bn

Rs.57bn

Rs.41bn

Rs.31bn

Rs.31bn

Rs.29bn

Rs.24bn

Rs.21bn

Rs.13bn

Rs.10bn

Rs.12bn

Rs.9bn

Rs.8bn

Rs.6bn

Rs.1bn

Flood Prone Areas

Typical borrower behaviour post calamity:

Week 1: Centre head informs MFI of calamity and the

inability to conduct centre meetings and migration of

members to rehabilitation centres. NPA spikes to ~35-40%.

70% of centres however show payment mobilization.

Week 2: 80% of centres start witnessing payment

mobilization; NPAs drop to 20-25%

Source: Spark Capital Research; MFIN Data

State wise Portfolio At Risk (PAR) as of March 31, 2016

States PAR 30 PAR 90 PAR 180

Tamil Nadu 0.21% 0.11% 0.05%

Karnataka 0.49% 0.33% 0.19%

Maharashtra 0.29% 0.19% 0.08%

Uttar Pradesh 0.39% 0.23% 0.16%

Madhya Pradesh 0.46% 0.30% 0.17%

West Bengal 0.18% 0.13% 0.08%

Bihar 0.22% 0.14% 0.08%

Gujarat 0.53% 0.33% 0.14%

Kerala 0.10% 0.06% 0.04%

Odisha 0.09% 0.06% 0.03%

Haryana 0.38% 0.20% 0.11%

Rajasthan 0.64% 0.47% 0.18%

Punjab 0.19% 0.13% 0.10%

Assam 0.07% 0.04% 0.03%

Delhi 1.80% 0.71% 0.31%

Typical borrower behaviour post calamity:

Week 3: 85-90% of centres start witnessing payment

mobilization; NPAs drop to 10-15%

Week 4: Normalcy restored; 95-99% centres start

paying. NPAs drop to 2-5%

Week 5-6: Normalcy restored in operations and asset

quality

Impact of natural calamities on asset quality in the past has been ephemeral

Page 41

History of strong repayments even in crisis adds credibility to asset quality