Embed Size (px)

Citation preview

54 Indian Gaming March 2006

The bingo industry currently faces some of its greatestchallenges and exhilarations. Attendance at bingo halls

around the country appears to be generally flat or contracting,but the breakpoints that will turn bingo onto a growth trackare becoming increasingly visible.

Bingo is considered to be a 'subset' of the gaming industryand probably represents about 6% of the gross annual wagerin America, or roughly $ billion a year in gross revenue (as com-pared to nearly $2 billion wagered on bingo in Canada). Yetbingo certainly earns the title of the most unique and complexgaming marketplace in the country, and one notoriously lack-ing in good metrics on any national scale.

Our industry has two main segments: tribal governmentbingo and bingo as charitable gaming. Both segments operatein relative isolation without the benefit of any 'national voice'speaking for bingo or raising the visibility and attraction of bingoto the general consumer. Both segments are fragmented froma regulatory perspective, and long outdated definitions of

bingo are slow to change. Tribal and charitable bingo revenues– and the direction of the industry at large – are both affectedby the same factors, including declining attendance, changingdemographics, rapid advances in technology and the need toimprove regulatory status.

These four factors are intimately linked. For example, atten-dance at bingo in general has been declining in nearly all measurable markets since the late 90s, but gradually, not pre-cipitously. Changing demographics is the main reason – olderplayers are moving on or succumbing to other forms of com-petition for their gaming and entertainment dollar, and we'renot creating new, younger players out of the baby-boomer pop-ulation fast enough to sustain or grow attendance levels. Buthang in there everyone, because there are solutions at hand.

One of the most important ingredients continues to be theintroduction of new technology to the industry, and this hasbeen made complicated by a very challenging regulatory situ-ation. In the charitable gaming world, there is no common setof rules governing bingo and each jurisdiction is basically ontheir own. The result is a mish-mash of bingo regulations thatvary widely from state to state and are often hard to rational-ize, especially when it comes to changes based on technology.Creating regulatory change in these jurisdictions can be a veryarduous task, and without a common voice, the charity groupsplaying bingo from state to state often have little chance of mak-ing coherent, positive changes happen.

In Indian Country, we all know the spectacular contro-versy that has been stirred up by advances in Class II (bingo)technology, which are most visible in Class II machine gaming but promise to affect all aspects of 'traditional' bingoas well. At this time, after an arduous year on behalf of theNIGC and a tribal government workgroup to put some senseto the situation, the question of “how is Class II gaming clarified?” is still being challenged. The federal DOJ is propos-ing to amend the Johnson Act to better define the differencebetween slot machines and what might constitute a facsimilethereof, in order to further separate Class II and Class III asthese categories are defined in the IGRA, while SenatorMcCain is proposing amendments to the IGRA itself. The hareof technology races on, but in the world of bingo, the tortoiseof regulation will always win the race, even if it means that muchneeded evolution in the bingo industry is put on hold.

Why is taking advantage of new technology so important tobingo? Because technology provides one of the most powerfulingredients to allow us to play bingo differently, to play more bingo,and to infuse new forms of color and excitement into the game.These attributes are essential to the cause of re-positioning bingoin a way that appeals to the next generations of players!

Bingo: Where is the Industry Heading?

BINGO

by Eric Casey

There is progress being made here and in other areas central to industry growth, but let's frame it first with a quicklook at the bingo market.

Tribal government bingo is a commercial enterprise andserves the economy of the nation as a for-profit business. Ofthe 224 Indian Nations operating gaming enterprises, mostinclude 'traditional' bingo played with paper and electronicbingo cards in their range of gaming and entertainment options.

In addition to 'traditional' bingo, numerous tribes offerClass II machine gaming. Even though these machines are slot-like in appearance, they operate on the same principles that gov-ern traditional bingo. How is 'traditional' bingo holding up inthe Indian gaming world, relative to the growth of Class IImachine and Class III gaming? There's really no way to tellon a country-wide level.

Because 'traditional' bingo and ClassII machine-based bingo revenues getlumped together into the reportingbucket for 'Class II' revenue, it's very difficult to separate the two and get a handle on how well 'traditional' bingo isdoing, a measurement that we could onlymake if the bingo room revenue and theClass II machine revenue were statedindividually.

Gross wager reports from 2003 show$72.8 billion dollars in gross gamingrevenue in the U.S., of which $16.8 bil-lion was in Indian Country. One indus-try pollster states this as being comprisedof $14.8 billion dollars in Class III revenue, and $2 billion dollars in ClassII. No matter how accurate the figure is,with 'traditional' bingo revenue lumpedtogether with Class II machine revenue,we can't use the year-to-year ups or downs in these metrics tolook at the health of 'traditional' bingo halls in Indian Country. Every year, a few tribes will close bingo or scale itdown, usually to make room for more Class II or Class IIImachines and because they have limited gaming space avail-able to work with. On the other hand, each year some tribalgovernments show a renewed commitment to bingo, addingnew technology, improving bingo environments, and reinvig-orating bingo as an attractive profit center.

One point of very good news is that tribal governmentgaming revenue continues to grow in all forms, Class II andClass III. The NIGC reports that 2004's gross revenue figurehit a record $19.4 billion dollars. Taking place, according toNIGA numbers, in 28 states at 354 locations, this spectacularrevenue growth showcases the public support for and viabil-ity of tribal gaming. We may not know exactly how much ofthat $19.4 billion was generated in the 'traditional' bingorooms of Indian Country, but at least we bingo-people can allsmile knowing in our hearts that many loyal bingo customers

did in fact contribute mightily to other forms of gaming revenue in the casino.

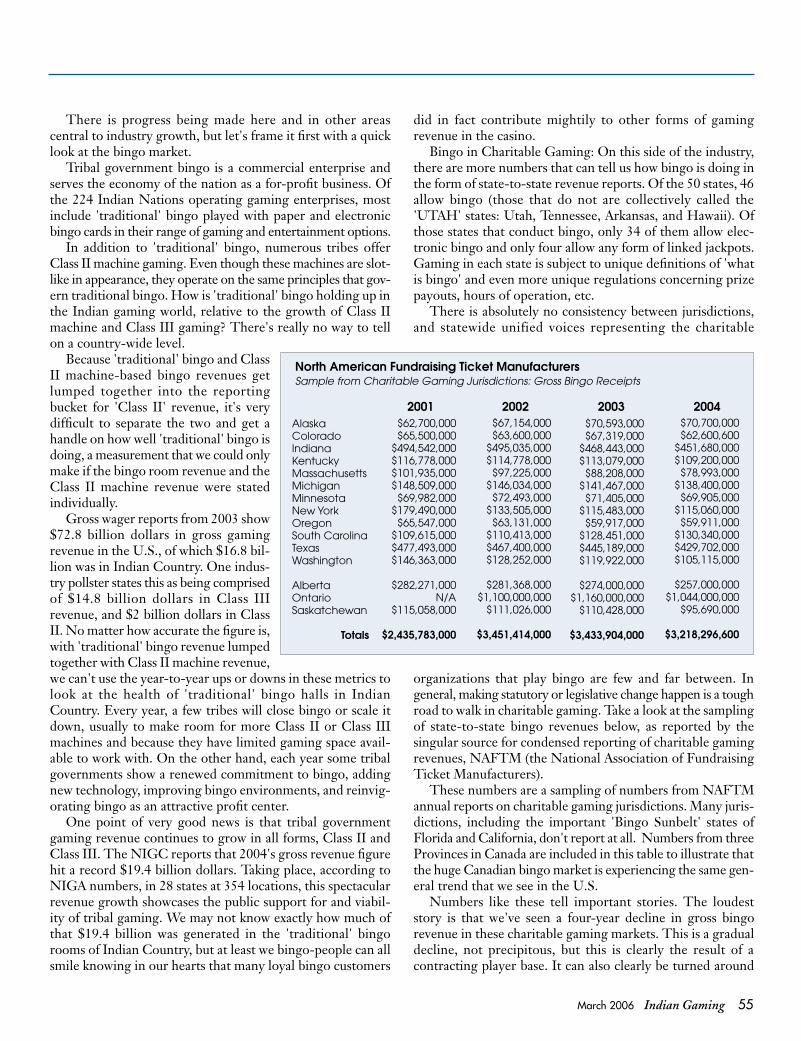

Bingo in Charitable Gaming: On this side of the industry,there are more numbers that can tell us how bingo is doing inthe form of state-to-state revenue reports. Of the 50 states, 46allow bingo (those that do not are collectively called the'UTAH' states: Utah, Tennessee, Arkansas, and Hawaii). Ofthose states that conduct bingo, only 34 of them allow elec-tronic bingo and only four allow any form of linked jackpots.Gaming in each state is subject to unique definitions of 'whatis bingo' and even more unique regulations concerning prizepayouts, hours of operation, etc.

There is absolutely no consistency between jurisdictions, and statewide unified voices representing the charitable

organizations that play bingo are few and far between. In general, making statutory or legislative change happen is a toughroad to walk in charitable gaming. Take a look at the samplingof state-to-state bingo revenues below, as reported by the singular source for condensed reporting of charitable gamingrevenues, NAFTM (the National Association of FundraisingTicket Manufacturers).

These numbers are a sampling of numbers from NAFTMannual reports on charitable gaming jurisdictions. Many juris-dictions, including the important 'Bingo Sunbelt' states ofFlorida and California, don't report at all. Numbers from threeProvinces in Canada are included in this table to illustrate thatthe huge Canadian bingo market is experiencing the same gen-eral trend that we see in the U.S.

Numbers like these tell important stories. The loudeststory is that we've seen a four-year decline in gross bingo revenue in these charitable gaming markets. This is a gradualdecline, not precipitous, but this is clearly the result of a contracting player base. It can also clearly be turned around

March 2006 Indian Gaming 55

AlaskaColoradoIndianaKentuckyMassachusettsMichiganMinnesotaNew YorkOregonSouth CarolinaTexasWashington

AlbertaOntarioSaskatchewan

Totals

$62,700,000$65,500,000

$494,542,000$116,778,000$101,935,000$148,509,000$69,982,000

$179,490,000$65,547,000

$109,615,000$477,493,000$146,363,000

$282,271,000N/A

$115,058,000

$2,435,783,000

$67,154,000$63,600,000

$495,035,000$114,778,000$97,225,000

$146,034,000$72,493,000

$133,505,000$63,131,000

$110,413,000$467,400,000$128,252,000

$281,368,000$1,100,000,000

$111,026,000

$3,451,414,000

$70,593,000$67,319,000

$468,443,000$113,079,000$88,208,000

$141,467,000$71,405,000

$115,483,000$59,917,000

$128,451,000$445,189,000$119,922,000

$274,000,000$1,160,000,000

$110,428,000

$3,433,904,000

$70,700,000$62,600,600

$451,680,000$109,200,000$78,993,000

$138,400,000$69,905,000

$115,060,000$59,911,000

$130,340,000$429,702,000$105,115,000

$257,000,000$1,044,000,000

$95,690,000

$3,218,296,600

North American Fundraising Ticket ManufacturersSample from Charitable Gaming Jurisdictions: Gross Bingo Receipts

2001 2002 2003 2004

56 Indian Gaming March 2006

BINGO

by making bingo attractive to new players. Another story worth noting is that electronic bingo has been

in place in many of these jurisdictions for quite some time, andhas absolutely -even dramatically- improved the average perplayer spend at bingo. One question then, is what would thesegross revenue numbers look like if electronic bingo had NOTbeen deployed in these states? Thanks to electronics, we're get-ting more bingo-spend out of fewer players, and there are many,many managers of the tribal bingo halls in Indian Country thatecho this statement.

The challenge is common to all: how do we attract andcreate new bingo players? A major industry focus over thelast 10 years has been on the integration of new bingo tech-nology, both at the bingo hall level and the regulatory level.This process will remain ongoing, because there's still along way to go, especially with regulators, and because tech-nology itself will continually evolve to deliver new toolsinto our marketplace.

What has become clearly apparent is that electronic bingo,by itself is only one part of the solution. Learning from thebooming, commercial, for-profit bingo markets in Europeand Latin America, a huge lesson coming from our industry'sglobalization of ideas is that the atmosphere of the facilities,the types of bingo being played, and the amenities beingoffered to the customers are each every bit as important toattracting and pleasing new bingo players.

Experiments in Canada that incorporate new facility designaesthetics, quality food and beverage offerings, and a variety oftraditional and hi-tech electronic gaming are starting to bearresults. In some locations, we even see the inclusion of mini-casinoand sports book environments conjoining the bingo hall – morereasons for customers to come to and stay on the property.

In the U.S., this 'holistic' approach to bingo reinvention willbe slow in coming in the charitable gaming markets. But all ofthe design principles driving the 'new bingo' are available to thebingo halls of Indian Country, not to mention whatever final def-initions of 'Class II' bingo emerge from the regulatory cauldron.

The bingo industry in the U.S. is playing for a big prize: abigger and broader than ever bingo demographic. It's becom-ing clearer and clearer what we need to do to win. How, as anindustry, we get it done is being written door-to-door by intre-pid bingo managers, hall operators, manufacturers, pro-activecharitable organizations, and tribal governments that are push-ing bingo forward into the future. It's an industry effort andthere's big success up ahead when we turn the corner into thenext generations of bingo players. ¨

Eric Casey is Director of Sales and Strategic Planning withPlanet Bingo. Casey has 15 years experience in the bingoindustry, working with all segments of the marketplace. Hecan be reached by calling (760) 773-0197 or [email protected]