Embed Size (px)

Citation preview

Builders' Association of India(All India Association of Engineering Construction Contractors & Builders)

Registered & Head Office:

G-1/G-20, Commerce Centre, J. DadajeeRoad, Tardeo, Mumbai - 400 034

Tel : (022) 23514134, 23514802, 23520507Fax : 022-23521328

Email : [email protected]

Delhi Office:

D1/203, Aashirwad ComplexGreen Park Main, New Delhi - 110 016

Tel : (011) 32573257Telefax: (011) 26568763

Email: [email protected]

75thAnnual Report and Accounts

2015-2016www.baionline.in

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20162

The Seventy fifth (75) Annual General Meeting of the Members of Builders' Association ofIndia, will be held on Saturday, 2nd July 2016 at 4.00 P.M. at Hotel Express Inn, Mumbai-Agra Road, Pathardi Phata, Nashik, to transact the following business :-

1. To confirm the Minutes of the Seventy fourth Annual General Meeting held on Saturday,12th September 2015 at 4.00 P.m. at the Lalit Plaza, Hotel The Lalit, Sahar Airport Road,Andheri (East), Mumbai - 4000 059 (Minutes have already been circulated to Membersand also printed in 'Indian Construction ' Journal, November 2015 issue - Page No.35).

2. To take note of the result of BAI Organisational Election for the year 2016-17 (Enclosed).

3. To take note of the result of BAI Trustees Election for the year 2016-19 (Enclosed).

4. To consider, and if thought fit, adopt the Annual Report of the Association for the yearending 31st March 2016.

5. To consider, and if thought fit, adopt the Audited Balance Sheet and Income & ExpenditureAccount of the Association for the year ending 31st March 2016.

6. To appoint Auditors to audit the accounts of the Association for the year 2016-17 and fixtheir remuneration.

7. To consider, any other item, with the permission of the chair.

C.G. DEOCHAKEHon. Gen. Secretary

Builders' Association of India

N O T I C E

Place : Mumbai

Dated: June 13, 2016

Note: (i) Queries on Accounts and Reports may kindly be communicated to BAI Headquarter on or before 28thJune 2016. Centres Chairmen are requested to kindly circulate this information amongst their members.Please note no floor queries on accounts will be entertained.

(ii) Please bring this copy of Annual Report.

Delhi Office: D1/203, Aashirwad Complex, Green Park Main, New Delhi 110 016 & 26568763 E-mail: [email protected]

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20163

BUILDERS' ASSOCIATION OF INDIAMANAGING COMMITTEE 2015-2016

PresidentMr. Lal Chand Sharma

Vice PresidentsMr. Anilbhai R. Zinzuwadia Mr. Ashok Agarwal Mr. G. C. Gupta Mr. V. M. Fazal Ali

Hon. Gen. Secretary Hon. Gen. TreasurerMr. Mahesh M. Mudda Mr. C. G. Deochake

Imm. Past PresidentMr. Sushanta Kumar Basu

TrusteesDr. D.C. Awasthi Shri D.L. Desai Shri J.R. Sethuramalingam Shri Jagdish Parekh

Shri P.K. Ramachandran Shri R. Ramaraj Shri S.K. Pradhan

State Chairmen / Co-ordinatorAndhra Pradesh Assam Bihar Chattisgarh

Shri Ch. Ramakotaiah Shri Kulesh Goswami Shri Manikant Shri N.R. PrasharDelhi Gujarat Jharkhand Karnataka

Shri Arun Sahai Shri Amit R. Patel Shri Chandrakant Raipat Shri A.R. Ravindra BhatKerala Madhya Pradesh Maharashtra Rajasthan

Shri R. Rajesh Shri Suresh Vaswani Shri Sunil Balkrishna Mundada Shri Ravi Kumar KheriaTamil Nadu Telangana Uttar Pradesh West Bengal

Shri N. Raghunathan Shri N. Nagesh Reddy Shri Sanjay Tyagi Shri S.K. Nag

MembersDr. Anand J. Gupta Dr. D. Thukkaram Dr. Dharmesh C. AwasthiDr. S.K. Manjarekar Shri A. Puhazhendi Shri Abhay GardeShri A.N. Balaji Shri Alex P. Cyriac Shri Ashok Kumar SharmaShri Avinash M. Patil Shri Baburao L. Shakkarwar Shri Basavaraj S. TotadShri Bhopinder R. Lal Shri C. Devarajan Shri Girish I. PatelShri G.M. Ravindra Shri Harshad N. Bhayani Shri H.N. Vijaya Raghava ReddyShri K. Padmanabhan Shri K. Subramani Shri K. VenkatesanShri K.J. George Shri K.S. Someshwar Reddy Shri L. MoorthyShri L. Venkatesan Shri M. Dhandavakrishnan Shri M.M. MohandasShri Mohan D. Bhate Shri Mu Mohanan Shri Mohanlal S. KatariaShri N. Raghunathan Shri Narendra Kumar Shri N. Sachitanand ReddyShri N.K. Gunasekaran Shri N.M. Patel Shri Naresh AgarwalShri Neelkanth S. Joshi Shri P. Subramani Shri P.P. JohnShri Prabir Kumar Mukherjee Shri Pradeep Kumar Jain Shri Pratap B. SalunkheShri R. Ethirajan Shri R. Sivakumar Shri R. SubburamanShri Ram M. Bhatia Shri Rajendra S. Athawale Shri Ravindra PradhanShri S. Ayyanathan Shri S.D. Kannan Shri S. GanapathyShri S.I. Chunkhare Shri Ved Khurana

Co-opted MembersShri Mukesh Verma Shri N. S. Muralidhara Dr. Tarro T. Manghnani Shri Vinod C. Gamdiwala

Special InviteesShri A. K. Srivastava Shri Agrawal Ashishkumar Subhash Shri Ahire Deepak DaulatraoShri Ashok Goyal Shri Bata G. Gopalakrishnan Shri Birendrasingh K. BhadoriaShri C. K. S. Panicker Shri C. Satish Kumar Shri Dhanwant Lal GuptaShri Dineshchandra R. Agrawal Shri D.P. Balaji Shri Harkant G. VachharajaniShri Jaideep P. Raje Shri K. Rajavel Shri K. Rama RaoShri K. Sudarshan Reddy Shri K.J. Saminath Shri K.K. PatelShri Kirtibhai Thakkar Shri Kunal Arvind Domadiya Shri Lal Chand RalhanShri Mafatbhai Patel Shri Mukesh V. Patel Shri N. Raja ReddyShri N.C. Sundaramurthy Shri N.M. Krishnamurthy Shri Navinbhai B. Vasoya PatelShri P. M. Harshe Shri R. Karna Boopathy Shri Rajendra M. UpadhyeShri Ramesh P. Marda Shri R. Saravanan Dr. S. KanagasundaramShri S. Prabhu Shri S. Shiva Prakash Shri Sanjay S. DesaleShri Shitalkumar Nawle Shri Shiv Kumar Kasana Shri Shrenik Manikant ShahShri Surinder Sharma Shri U.M. Gurushanthappa Shri Uday N. GokhaleShri V. Sivarajan Shri V. Venkatesan Shri V.S.K. Moorthy

Shri Vikram Kumar

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20164

President : Shri Avinash M. Patil[Nashik Centre]

Vice Presidents : 1. Shri Ravindra Pradhan 2. Shri R.N. Gupta [Jharkhand (Ranchi) Centre] [Delhi Centre]

3. Shri Mu. Moahan 4. Shri Rajiv B. Krishnani[Southern (Chennai) Centre] [Pune Centre]

Hon. Gen. Secretary : Shri C.G. Deochake

Hon. Gen. Treasurer : Shri Neerav Parmar

State Chairman (Andhra Pradesh) : Shri CH Ramakotaiah (Visakhapatnam Centre)

St. Co-ordinator (Assam) : Shri Kulesh Goswami (Guwahati Centre)

State Chairman (Chhattisgarh) : Shri Alok Shivhare (Durg-Bhilai Centre)

State Chairman (Gujarat) : Shri Nitin M. Shah (Baroda Centre)

State Chairman (Jharkhand) : Shri Devendra Tiwary (Jharkhand (Ranchi) Centre)

State Chairman (Karnataka) : Shri K.S.Someshwara Reddy (Karnataka (Bangalore Centre)

State Chairman (Kerala) : Shri John Paul K. (Kottayam Centre)

St. Co-ordinator (Madhya Pradesh) : Shri Suresh Vaswani (Bhopal Centre)

State Chairman (Maharashtra) : Shri Suresh B. Patil (Sangli Centre)

St. Co-ordinator (Rajasthan) : Shri Ravi Kumar Kheria (Rajasthan (Jaipur) Centre)

State Chairman (Tamil Nadu) : Shri M. Thirusangu (Tiruchirappalli Centre)

State Chairman (Telangana) : Shri B. Sugunakar Rao (Karimnagar Centre)

State Chairman (Uttar Pradesh) : Shri Sanjay Tyagi (Muzaffarnagar Centre)

St. Co-ordinator (West Bengal) : Shri Sudip Kumar Dutta (Eastern (Kolkata) Centre

Members of the Managing Committee representing Centres:

1. Shri Amar Bawa 2. Shri Ashok Agarwal

3. Shri Bhopinder Lal 4. Shri D. Kempanna

5. Shri G. Thilagar 6. Shri Harshad N. Bhayani

7. Shri Jaiprakash Bhatia 8. Shri Jawahar Mutha

9. Shri K. Annamalai 10. Shri K. Mathiyalagan

Ref.: 607/M/2015-16 dated March 30, 2016

TO:THE TRUSTEESTHE VICE-PRESIDENTSTHE STATE CHAIRMEN / CENTRE CHAIRMENTHE MANAGING COMMITTEE AND THE GENERAL COUNCIL MEMBERS

Dear Sirs,

The election process for 2016-17 of Builders' Association of India has been completed on 30th March 2016. Followingare the election results:

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20165

11. Shri L. Shantakumar 12. Shri M. Dhandavakrishnan

13. Shri Mahesh R. Mirani 14. Shri Mathew Alex Vellapally

15. Shri Mohan S. Kataria 16. Shri Mohinder Rijhwani

17. Shri Narendra P. Patel 18. Shri Naresh Kumar Agarwal

19. Shri Neelkanth S. Joshi 20. Shri P. Parameswaran

21. Shri Prabir Kumar Mukherjee 22. Shri Prince Joseph

23. Shri R. Ethirajan 24. Shri R. Krishnaswamy

25. Shri S. Prakash 26. Shri S. Ramaprabhu

27. Shri Sanjay Laxman Patil 28. Shri T.V. Chandrasekaran

Members of the Managing Committee representing Patron Members:

1. Dr. D. Thukkaram 2. Dr. Dharmesh C. Awasthi

3. Dr. Tarro T. Manghnani 4. Shri A. Chamaraja Reddy

5. Shri A. Puhazhendi 6. Shri Abhay M. Garde

7. Shri Baburao L. Shakkarwar 8. Shri Basavaraj S. Totad

9. Shri H.N. Vijaya Raghava Reddy 10. Shri Jagdish M. Parekh

11. Shri K. Ramanujam 12. Shri K. Subramani

13. Shri K.J. George 14. Shri L. Venkatesan

15. Shri M.G. Sundar 16. Shri Mohan D. Bhate

17. Shri N. Ramalingam 18. Shri Narendra Kumar

19. Shri O.K. Selvaraj 20. Shri P.P. John

21. Shri Pratap B. Salunkhe 22. Shri S. Ayyanathan

23. Shri S. Ganapathi 24. Shri Srinivasa Reddy

25. Shri Y. Ishwar Rao

Members of the Managing Committee representing Affiliated Associations:

1. Shri Atul Vijaykant Moog 2. Shri E. Manohar

3. Shri N. Velayutham 4. Shri R.R. Shridhar

The new office bearers will assume charge of their respective offices with effect from 1st April 2016 for a period of 1year as per the BAI Constitution.

Thanking you,

Yours faithfully,

RAJU JOHNRETURNING OFFICER

BAI ORGANISATIONAL ELECTIONS 2016-17

Copy to: 1. Shri V.M. Fazal Ali2. Shri J.R. Sethuramalingam Board of Scrutineers,3. Shri A.B. Chitale BAI Organisational Elections 2016-17}

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20166

Ref.: 608/M/2015-16 dated March 30, 2016

TO:THE TRUSTEESTHE VICE-PRESIDENTSTHE STATE CHAIRMEN / CENTRE CHAIRMENTHE MANAGING COMMITTEE AND THE GENERAL COUNCIL MEMBERS

Dear Sirs,

The election process for Trustees of Builders' Association of India for three year term i.e. 2016-2019 has been completedon 30th March 2016. Following are the election results: -

Trustee (East) : Shri Ashok K. Choudhary : (Jamshedpur Centre)

Trustee (North) : Shri Lal Chand Sharma : (Gautam Budh Nagar Centre)

Trustee (South) : 1. Shri M. Karthikeyan : (Southern (Chennai) Centre)

2. Shri N. Sachitanand Reddy : (Hyderabad Centre)

3. Shri R. Subburaman : (Madurai Centre)

Trustee (West) : 1. Shri D.L. Desai (Shankarbhai) : (Mumbai Centre)

2. Shri Vijay Jagannath Devi : (Satara Centre)

}

The new Trustees will assume charge with effect from 1st April 2016 for a period of 3 years as per the BAI Constitution.

Thanking you,

Yours faithfully,

RAJU JOHNRETURNING OFFICER

BAI TRUSTEES ELECTIONS 2016-19

Copy to: 1. Shri V.M. Fazal Ali2. Shri J.R. Sethuramalingam Board of Scrutineers,3. Shri A.B. Chitale BAI Organisational Elections 2016-17

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20167

Report of the President and Managing Committee ofBuilders' Association of India for the year 2015-16

Friends,

The President and the Managing Committee have greatpleasure in presenting the 75th Annual Report of theAssociation along with the Statement of Accounts and theAuditors' Report for the year 2015-16.

CONSTRUCTION INDUSTRY - OPPORTUNITIES

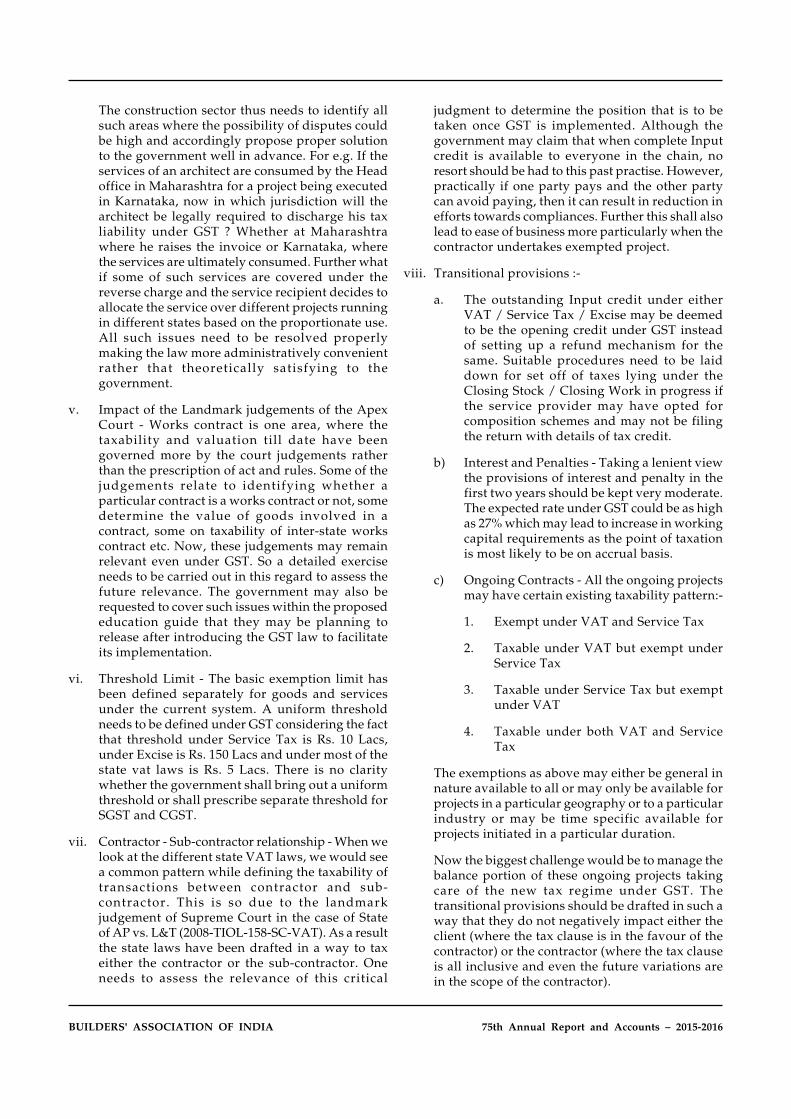

The construction is a high volume low profit business. Itcontributes about 8% to the gross domestic product (GDP).Its fixed capital investment in form of security deposit isless but working capital requirement is high. Apart fromits contribution to GDP, it is also one of the largestcontributors to employment of skilled and unskilledpeople outside of agriculture, employing a total of about41 million people.

The thrust on infrastructure development in the last fewyears has been a key driver for the construction industry,opening up opportunities for both the contracting industrythrough direct construction contracts as well as forancillary industries, including equipment and materialmarkets. In fact, nearly 60% of annual infrastructureinvestment covers construction sector.

Over the past three years i.e. 2012-2015, there has been asignificant slowdown in investment from 38% of GDP in2008-09 to 28% of G.D.P. in 2013-2014. This has impactedcapacity addition in various infrastructure sectors. Suchslowdown affected construction industry negatively. WithPublic - Private Partnership model (PPP) of infradevelopment Construction Industry graduated from cashand carry contracts to that of an entrepreneur in recentyears. Many infrastructure developers have successfullycompleted project in time. PPP in turn brought aboutgreater mechanisation and employment of skilledpersonnel for earlier completion of work.

Project are often awarded with only partial acquisition ofland, which can stalled project indefinitely if even 10-20%of the required land is not handed over to the developerin time. Furthermore, extensive environmental approvalsare required at the start of the project itself. Regulatoryauthorities at the central and the state levels lackcoordination, which leads to standoffs on criticalapprovals. This is compounded by other issues such ainadequate support in the shifting of utilities forconstruction.

Infrastructure sector requires long term investment atlower interest rate having a long gestation period. Inabsence of such finance infra players have to depend onBank finance which are for working capital and a shortterm duration and at higher interest rate. There is urgent

need for investment by Pension Fund & Insurance fundin infra sector.

Lack of adequate financing has also emerged as asignificant reason for delays in construction works. Thepast 24 months have been marked by an economicslowdown, and investors are becoming increasingly riskaverse. Consequently, equity players are shying awayfrom parking their funds in the infrastructure sector. Bankstoo have made lending norms more stringent and severalinfrastructure projects have been unable to achievefinancial closure within the prescribed timelines.

The government has set a massive investment target ofRs. 56 trillion in the infrastructure sector in the TwelfthFive Year Plan. For this to be realized during remainingyears of plan i.e. 2015-2017 period, it is imperative thatthe construction industry need to pick up pace and growat an annual average rate of 20%, which is unlikely to beachieved in the balance two years of plan period. This isnearly four times its current growth rate. New governmentneed to tackle this problem on war footing.

Sea Port Sector

Construction opportunities in the port sector mainly arisefrom the construction and reconstruction of berths, jettiesand terminals as well as in rail/road connectivity fromhighways to seaport. Total investment of Rs. 723 is billionenvisaged at major ports by the planning commission forthe Twelfth Plan period. Of the 264 projects planned atmajor ports during the Twelfth plan period, almost 25%of the projects relate to construction and reconstructionof berths and jetties, while rail/road connectivity projectsto seaport accounts for 21% of the total projects. On sevenmajor ports PP Projects worth Rs. 101.78 billion is readyfor bidding between 2015-2017 periods. Besides thisgovernment plans to develop new seaport at DurgarajPattanam in A.P. and at sagar is land in West Bengal atcost of Rs. 174 billion. All the above are besides seaportsbeing developed by State Government of GujaratMaharashtra, Karnataka, Tamil Nadu Orissa and AndhraPradesh on PPP basis.

Water supply & Sanitation

The pace of contract awards in the water and sanitationsector declined in the last two fiscal years. While contractsfor construction and related works for 15 projects worthRs. 121.02 billion were awarded in 2011-12, only eightprojects worth Rs. 24.91 billion were awarded in 2012-13.According to India Infrastructure Research, there are 44projects worth Rs. 305.60 billion would offer opportunityto construction Industry of these 28 projects areannounced, 11 have been awarded, remaining 5 are under

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20168

1. National Highway constitutes about 2% of total roadlength of about 484000 K.M. and stage highwayconstitute 3%, whereas remaining 95% constitutemajor district roads and rural roads. Indian roadscarry 85% of passenger traffic and 63% of freighttraffic. National Highway Authority was establishedto execute N.H.D.P. project of 5846 K.M. coveringPhase I connecting all four metros called GoldenQuadrilateral and 7142 K.M. Phase II called North-South and East-West corridors sometime in Year1999. Later on additional 37242 K.M. was addedunder Phase III to VIII, including 380 km. of SeaportConnectivity. As on 31st July 2015, GoldenQuadrilateral and 380 K.M. of Seaport Connectivityis completed. In respect of NS/EW Corridor 90% oflength is completed, whereas 279 K.M. length oftender remains to be awarded. Phases III and V is

National Highway Development Project

47% and 25% completed respectively. SinceGovernment was facing resource crunch to completeN.H.D.P project by 2007. In year 2006 MoRT & Hcame out with concept of Build Operate and Transfer(BOT) project under which Government was toacquire land required for Widening of Highways andGrant Environment clearances; whereasContractors/ Entrepreneurs were to invest it's ownfunds in construction of additional 2 lanes / 4 lanesto existing highway. In return these contractors weregranted toll collection rights for contracted numberof years along with maintenance of such road. Inrespect of those stretches of highways where therewas not sufficient traffic for BOT method,Government came with concept of "Annuity" underwhich contractor has to complete roads andGovernment would give annual payments for

planning.

Airport Sector

With respect to the pace of new project awards in theAirport sector, the progress has been slow. In the last twoyears (2011-12 and 2012-13), only two projects wereawarded. One was the Chandigarh (Mohali) InternationalAirport Modernisation Project Phase I, which wasawarded to Larsen & Toubro in August 2012; and the otherwas the Vadodara (Harni) Airport Integrated TerminalBuilding Project, which was awarded to B.L. Kashyap &Sons Limited in May 2011. Construction opportunities inthe airport sector are expected to increase in line with thegrowing demand for air transport. Massive projects havebeen lined up, ranging from large public-privatepartnership opportunities in greenfield airports todevelopment of cargo terminals. Besides, as stated earlier,the Airports Authority of India (AAI) has elaborate planswith respect to both air-side works at non-metro airports.On an average, about 66% of the total project cost of anairport pertains to construction. According to IndiaInfrastructure there are 74 airport projects worth Rs. 450billion that would offer significant construction

opportunities. Out of these 74 projects, 54 projects havebeen announced seven are stalled, five are planned, twoalready awarded and one is under bid. Most of thesefacilities are located in State of Maharashtra, Karnatakaand Kerala. To enable regional air connectivity, thedevelopment of low cost airports in Tier II and Tier IIIcities on priority basis is taken up. In long run 200 of suchno frill facilities will be developed. In the first phase 51such cities are under consideration. Each of these facilitieswill require investment of about Rs. 0.5 billion to Rs. 2.00billion depending upon requirement. These are in Stateof Andhra Pradesh, Jharkhand, Punjab, Bihar, UttarPradesh, Arunachal Pradesh, Madhya Pradesh, Orissa,Rajasthan.

Power Sector Opportunity

Time and cost overruns have become synonymous withproject execution in India. While some of the key risksimpeding construction activity appear to be externalfactors, they can be mitigates to a great extent throughthe timely identification of prerequisites. This isparticularly true of land acquisition and regulatoryapprovals.

Construction opportunity in the conventional power segment

Capacity (MW) Total project cost Construction component(Rs. billion) (Rs. billion)

Thermal* 21,940 1,028.00 411.20

Hydro 28,334 1,381.13 897.73-966.79

Nuclear** 42,700 4,270.00 854.00

*The Surguja power plant in Chhattisgarh has been excluded given the reports of the power Ministry shelving theproject

**Total project cost has been calculated by assuming the per unit cost at Rs.0.10 billion per MW

Source: India Infrastructure Research

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-20169

NHDP update (as of February 29, 2016) (km)

Phase Total length Total four/ Under Balance length Totalin km six-laned implementation for award in expenditure

completed in in km km in billionkm

GQ 5,846 5,846 NIL NIL 321.97

NSEW 7,142 6,427 458 257 652.70

III 11,809 6,825 3,227 1747 850.62

IV 13,203 2,054 4,654 6,495 103.40

V 6,500 2,339 781 3,380 306.80

VI 1,000 NIL 165 835 0.93

VII 700 22 19 659 10.44

Port connectivity 435 379 56 NIL -

Other NHs 1844 1,614 230 NIL NIL

Total 48,479 25,516 9,590 13,373 2246.86

GQ: Golden Quadrilateral; NSEW: North-South-East-West

Source: National Highways Authority Of India

contracted number of years. Third mode ofdevelopment was mix of BOT and Annuity. Givenbelow in Table 'A' comparative statement ofcompleted portion of various phases of N.H.D.P,

work in progress and balance length for whichtenders are yet to be invited. Another Table 'B' givesupdate on BOT, Annuity and Toll plus annuityprojects.

Table B

Status of BOT toll and BOT annuity projects ( as of February 29, 2016)

Format No. of projects Length (km) Cost (Rs. Billion )

Toll

Awarded 202 20017.39 1791.18

Completed 74 4887 -

Terminated 35 4447 -

Balance 10683 -

Annuity

Awarded 51 3,500.53 302.87

Completed 27 1,933.00 -

Terminated 3 155 -

Balance 1412 -

Toll + Annuity

Awarded 253 23517.92 2094.50

Completed 101 6820 -

Terminated 38 4602 -

Balance 12791 -

Source: National Highways Authority of India

2. Ministry's Proactive Steps

Ministry's focus is to save the lenders, so that thecapital does not fly away from the road sector. Effortis to bring the investor confidence back.

Since many developers could not pay premiumsN.H.A.I. allowed them to defer premium paymentsin respect of 11 developers covering 1000 K.M. oflength as per Table 'D' below:-

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201610

Table D

S.N Name of Developer Name of Project State Length in K.M.

1 BSCPL Godhra-Gujarat-M.P. Border Gujarat 87

2 L G T Belar-Pali-Pindwara Rajasthan 244

3 L G T Samkhiali-Gandhidham Gujarat 56

4 Sadbhav Engineering Rohtak – Panipat Haryana 81

5 Sadbhav Engineering Hyderabad-Yadgiri A.P 36

6 IRB Infrastructure Ltd. Ahmedabad-Vadodara Gujarat 102

7 IRB Infrastructure Ltd. Tumkar-Chitradurga Karnataka 114

8 Gayatri-DLF J.V. Indore-Devas M. P 45

9 Reliance Infrastructure Hosur-Krishnagiri Karnataka 60

10 Essel Infra Project Ltd. Walajapet-Poonammalle T.N 93

11 Ashoka Buildcon Ltd. Belgaon-Dharwad Karnataka 82

Total 1000

The public-private partnership model, which has notreally lived up to expectation, has been changed.Government will fund 40% of project cost and balance60% to be funded by developer through equity and debt.The developer/concessioners will get biannual annuityover a period of concession (10 to 20 years). Thegovernment is offering 17 new projects covering 2,100 kmfrom 1st October 2015 in which the Government / NHAIis to take up to 40% of cost as Viability Gap Funding (VGF).The new model is mix of EPC and BOT models where theroad authority provides VGF, whereas the developers hasto chip in with the balance 60% and complete the project.In order to attract investments, N.H.A.I. did not receiveany response for Solan - Kaithalighat section in H.P.costing to Rs.522 crores on 1.11.2015. The government hasnow offered road developers the chance to choose theirown routes where they expect high volume traffic.Currently NHAI decides entire route before seeking bid.Under the new system it will only decide the two endpoints say Nagpur and Pune while letting any interestedprivate company to pick-up the route it deems mostprofitable in terms of toll earnings. This new system iscalled "Swiss challenge system", under which a privateoperator proposes a project and makes a bid, which thegovernment publicises while inviting third parties tomatch or exceed it. If a competitor betters the original bid,the first proposers get a chance to match it and begcontract. The original proposer has a right of first refusalmeaning thereby that a competitor can be awarded thecontract only if the first proposer refuses to match thesuperior bid. Industry experts say that under this system,private entity is required to make a lot of initial investmentover planning and evaluation, which he may not be ableto recover it he does not get contract.

Government on 15th May 2015 decided to allow BOT roaddevelopers to exit project completely two years afterconstruction is completed, so that equity is unlocked andcan be utilized in other projects. Prior to 2009, developers

could exit only after seven years. New policy decision ismade applicable to 80 such BOT projects. This wouldrelease Rs.45 billion equity. The Cabinet Committee onEconomic Affair on 26th August 2015 decided to extendfacility of existing project two years after construction evento projects completed prior to 2009. This is expected topave the way for more domestic fund and foreign fund tocome into this sector.

Ministry of Environment and Forest on 5th June 2014launched on-line clearance for infra projects, whereas on-line forest clearance was launched on 15th July 2014. Thisstep would help in speedy clearance with necessarytransparency and accountability in grant of regulatoryclearances. Government has permitted banks to raise longterm funds for lending to infra sectors. Reserve Bank ofIndia in pursuance thereof issued guidelines on 16th July2014 to commercial Banks to issue long term bonds withminimum period of maturity at seven years. The amountraised will be exempt from minimum regulatory pre-emption like Cash Reserve Ratio (CRR), StatutoryLiquidity Ratio (SLR) and priority sector lending.

Government is in the process of finalising the modalitiesfor completed highway project on EPC basis to be givenfor toll collection and maintenance for 20 year period. Thisbids would help government to raise funds for giving newcontracts. This would create a new business vertical forthose who are interested in operation and maintenance ofthe roach. Ministry of Road Transport G Highways hasfixed target of completing 8000 km at cost of Rs. 20000crores i.e. 22 km per day for 2015-2016.

Construction Opportunity in Monorail Project

The construction component in a monorail project alsostands at about 50% of the total project cost. Based on this,India Infrastructure Research has estimated a constructionopportunity of nearly Rs. 81.58 billion over the next twoto three years. Also, several projects are currently in the

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201611

planning and proposal stages and will be executed in thenext five to seven years, thus providing significantconstruction opportunity in the long run.

Construction Opportunity in Railways

In the railway sector, of the total project cost, 78% pertainsto construction works. Based on recent progress in eachof the pipeline projects, India Infrastructure ResearchApril 2015 issue list investment of Rs. 961.82 billion for 77projects covering 9400 km. of doubling, tripling and

quadrupling rail net work. In addition to theseopportunities, the ambitious high speed rail corridorsbetween Mumbai - Ahmedabad and Delhi - Varanasi -Patna also offer massive construction opportunities in thecoming years. Indian Railway in August 2014 came outwith a policy decision to allow 100% F.D.I. for executionof infrastructure projects in railway sector. Policy of rail-seaport connectivity having been finalised. For thispurpose Railway have formed a special purpose vehiclewith Seaport Authority called Rail Vikas Nigam Ltd. Ithas completed four projects as per Table A below:

Table A

Sr. Project Name Type of Work Distance Cost in Rs. StatusNo. in km billion

1. Panvel - Jawaharlal Neharu Doubling of Line 28.5 1.02 Completed and linesPort in Maharashtra are functional.

2. Mundra Port - Palanpur in To convert into 301.00 4.51 Completed and linesGujarat broad Gauge are functional.

3. Bharuch - Samni - Dahej To convert into 62.00 2.00 Completed and linesPort - Gujarat broad Gauge are functional.

4. Krishna Pattanam Port - Doubling of line 16.5 0.86 Completed.Venkatachalam with electrification

Total 408.00 8.39

In addition to above completed rail-seaport connectivity,Railways have given in principle approval to eight projects

in December 2014 entailing an investment of Rs. 52.87billion. Details are given in Table B below:

Sr. Name of Project State Length Cost in ModeNo. in k.m. Rs. Billion

1. Astarnga Port - Bhubaneswar - Orissa 75 13.10 Private Line ModeNew Line

2. Dighi Port - Indapur - Maharashtra 42 7.70 Joint Venture with RailNew Line Vikas Nigam Ltd.

3. Dighi - Jaigarh Port Maharashtra 35 7.71 Joint Venture with RailVikas Nigam Ltd.

4. Bhadrak - Dhamra Port - Orissa 64 7.60 Private Line ModeNew Line

5. Hazira Port - New Line Gujarat 47 7.34 Private Line

6. Gandhidham - Tuna Port - Gujarat 17 1.42 Private LineNew Line

7. Hamrapur - Kewas Port - Maharashtra 26 3.49 Joint Venture with RailNew Line Vikas Nigam Ltd.

8. Chhara Port - Kodinar - Gujarat 20 3.51 Private LineNew Line

Total 326 52.87

Table B

Dedicated western & Eastern Freight Rail CorridorCovering 3342 km envisages total investment of Rs. 80000crores out of which fourty% i.e. Rs. 32000 crores involvesconstruction out of 3342 km, tender for 1536 km is yet tobe awarded estimated to cost Rs. 16000 crores.

It can thus be seen that Indian Infra sector will generateconstruction opportunity of Rs. 20 trillion in next 3 yearsthat offer significant construction opportunity.Construction Industry now need to scale up it's capacitymodel for PPP projects.

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201612

HOUSING FOR ALL BY 2022 - REAL ESTATE - ANUPDATE

Report of the Technical group on Urban Housing shortage(2012-2017) and working group on Rural Housing (2012-2017) submitted the same in 2011 to their respectiveministries. Report estimated that almost a quarter ofIndian households lack adequate housing facility. Countryis on the verge of large scale urbanisation over the nextfew decades. As per 2011 census, country's population was121 crores and expected to reach 150 crores by 2050.

Present urbanisation rate of 28% in 2011 is to accelerate to52% by 2050. Urban population is expected to reach to 81crores by 2050 as per "KPMG India Analysis July 2014".Housing is a basic need for humans. Central Governmentacknowledges the importance of housing and aims toprovide housing to all it's citizen by 2022. In order to fulfillthis vision, 4.63 crores urban houses and 6.50 crores ruralhouses are required to be constructed by Government,private sector and on public private partnership. Detailsof statewise urban and rural housing requirement is givenin Table 'A' below:-

Table 'A'Details of Statewise Urban and Rural Housing Requirement

(Figures are in lakhs)

Sr. Name of State No. of Urban No. of Rural Total HousingNo. Housing Units Housing Units Units required

required in 2022 required in 2022 by 2022

1. Uttar Pradesh 54 146 200

2. Madhya Pradesh 22 51 74

3. Rajasthan 21 45 66

4. Delhi 30 3 33

5. Haryana 11 14 25

6. Punjab 10 13 23

Northern Region 148 272 421

7. Maharashtra 50 55 105

8. Gujarat 29 21 50

9. Goa 2 1 3

Western Region 81 77 158

10. A.P. including Telangana 37 40 77

11. Tamil Nadu 39 18 57

12. Karnataka 28 21 49

13. Kerala 27 9 36

Southern Region 131 88 219

14. Bihar 19 69 88

15. West Bengal 34 42 76

16. Orissa 9 26 35

17. Jharkhand 11 18 29

18. Chhattisgarh 8 14 22

Eastern Region 81 169 250

19. Hilly Region 22 44 65

All India 4.63 crores 6.50 crores 11.33 crores

20. Demand between 2014 and 2022 2.73 crores 2.70 crores 5.43 crores

21. Urban Housing shortage of E.W.S.in 2012 1.055 crores

22. Shortage of LIG in 2012 0.741 crores

23. Shortage of M.I.G. in 2012 0.082 crores

1.878 crores

24. Investment required upto 2022 1.80 Trillion Dollar 0.20 Trillion Dollar 2.00 Trillion Dollar

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201613

The total housing requirement of 11.33 crores by 2022includes housing shortage of 5.90 crores as on 2014. Thebreak-up of current housing shortage, requirement

between 2014 and 2022 is given in Table 'B' below :-

Sr. Particulars Urban Housing Rural Housing Total HousingNo. Units in crores Units in crores Units in crores

1. Shortage of Housing Units in 2014. 1.90 4.00 5.90

2. Demand between 2014 and 2022. 2.73 2.70 5.43

Total 4.63 6.70 11.33

As per K.P.M.G's estimates, development of such largequantity of houses may require investments of over USD2trillion i.e. Rs. 120 lakh crores (dollar at Rs. 60). This translatesto about USD250 to 260 billion annually i.e. Rs. 15 lakh croresto Rs. 15.60 lakh crores, more than double the annualinvestments witnessed in FY14. About 85 to 90% of the totalinvestments would be required for developing urbanhousing, where development costs are high due to factorssuch as land prices, construction cost, fees, and taxes. Withinurban housing, it is the affordable housing (houses for EWS/LIG households) which require attention on priority basis,as it alone would require about half of the total investmentsand 70% of urban housing needs envisaged. Theseinvestments need to be complemented with additionalinvestments of about USD1.5 trillion in urban infrastructureand commercial real estate. Thus, a total investment of overUSD3.5 trillion may be required for urban housing andsupporting infrastructure. Though, housing deficit is muchwider in rural areas compared to urban areas, it requiresonly a small portion of total investments envisaged till 2022,which can be meted out without much difficulty. In our view,the central government with participation from stategovernments, drafting a plan of delivering three crorehouses in rural areas with an investment of INR3.45 lakhcrore (USD58 billion) by 2022 is a good start.

With the current set of housing development policies in placeand assuming an annual growth in investments by aboutfive to six% in the housing sector (as witnessed since FY08),the required investments may fall short by about USD500

to 600 billion. This gap in funding would likely be restricteddue to several structural issues in the sector such as highgestation period of housing projects, limited and expensiveliquidity, spiralling land and construction cost, high fees andtaxes, unfavourable development norms, and affordabilityvis-à-vis housing prices for EWS/LIG households.

Mobilisation of such huge resources (funding, constructioncapacity, labour, technology, etc.) for mass scale affordablehousing development by the central and state governmentsmay be difficult, without participation from the privatesector. The private sector, which is often better in term ofmanaging construction risks and project delivery, shouldbe encouraged by central and state governments, byaddressing several structural issues

Since the beginning of the twenty first century, a slew ofregulatory reforms such as allowing foreign directinvestments, improving access to credit by households,providing tax incentives on housing loans, developingspecial economic zones and thrust on infrastructuredevelopment, coupled with high economic growth, havepropelled private sector participation in urban housingdevelopment. However, it has largely resulted in thedevelopment of Middle Income Group (MIG) and HighIncome Group (HIG) houses, leading to significant shortageof EWS/LIG or affordable houses. As per the report of theTechnical Group on Urban Housing Shortage, EWS/LIGhouses constitute more than 95% of the housing shortage in2012 as per detail given in Table 'C' below:

Table 'B'

Sr. Classification of Housing Units Number of Shortage inNo. Units in Million percentage term

1. Economically Weaker Section (EWS) 10.55 56.18

2. Low Income Group 7.41 39.44

3. Middle Income Group & above 0.82 4.38

Total 18.78 100.00

Table 'C'Urban Housing Shortage 2012

Source:- Report of the Technical Urban Group (TG-12) on Urban Housing Shortage 2012-2017. Ministry of Housing &Urban Poverty Alleviation September 2012.

Government has changed yearly income bend for E.W.S./LIG/MIG in July 2015, which is as per Table C-1 below :

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201614

Table C-1

Sr. Category of Housing Yearly income Bend Housing shortage as Revised yearlyNo. earlier in Rs. per Technical group income bend as on

on urban Housing 8.7.2015 in Rs.shortage 2012

1. EWS 60000 10.55 million Upto 3.00 lakh

2. LIG 60000 to 1.20 lakh 7.41 million Bet. 3.00 to 6 lakh

3. MIG Above 1.20 lakh 0.82 million Above 6 lakh

18.78 million

Despite such huge demand for all type of housing andmore particularly for EWS and LIG, development of urbanaffordable houses has been limited due to severalstructural issues making it unfeasible business propositionfor the private sector. Major structural issues restrictingprivate sector participation in urban affordable housingare depicted below:-

1) Real Estate is a low volume, high margin businessrequires very high long term capital requirement forpurchase of urban land at high price. Its workingcapital requirement is low. Any given project hasgestation period of 6/8 years. Most of real estateplayers are in unorganized sector. There are hardly50/60 listed companies on Mumbai Stock Exchange.

2) Town planners all these years prescribed horizontaldevelopment of cities with low or restrictive FSI/FAR in order to reduce migration into cities.Horizontal expansion of cities resulted in resourcestarved local urban bodies unable to provide civicinfrastructure in terms of roads, water mains,sewerage, and health/educational infrastructure.India's per capita urban infrastructure spending evenotherwise is about 17 dollar against requirement of100 dollars.

3) Currently 30/40 N.O.C. are required from variousdepartments / authorities / organisation whichtakes more than 18 months before approval ofbuilding plan. This delay add to the cost of projectby way of interest burden.

4) Migrant could not find flats at affordable price informal housing sector ultimately purchased ininformal housing sector. This resulted inproliferation of slums in all big towns. AffordableRental Housing should be encouraged.

5) Real estate being high capital intensity business withlong gestation period, has to depend on high interestrate, short term loans, either from Banks or fromprivate source in absence of institutions of such aspension funds, PF funds offering long terms loansat low interest rate. This add to overall project costbesides slowing down or delayed completion ofhousing projects.

6) Several indirect taxes such as VAT, stamp duty,service tax together add to about 35% of propertycost. Details of various taxes to be paid are as perTable 'D' below :-

Table 'D'

List of direct and indirect taxes imposed on real estate development.

Sr. No. Tax Percentage of property cost

1. Development agreement stamp duty 5

2. Stamp duty on purchase of property 5

3. Registration charges 1

4. Value added tax on purchase of construction material 1

5. Service tax to contractor on service component 2.6

6. VAT to contractor on goods component 4

7. Other levies such as service tax 2.6

8. Excise and custom duty 15

Total -35

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201615

Table 'E'

This analysis is based on a FAR/FSI of 1.5 times the land area. The actual requirement of land may decrease. If theunoccupied houses of about 94 lakh, as mentioned earlier, are occupied.

Urban housing land requirements

EWS LIG MIG HIG Total

Housing need Crore 1.7-1.9 1.3-1.5 0.8-1.0 0.4-0.5 4.4-4.8till 2022

Super-built Sq.ft 300 650 1,000 1,500up area

Land required Crore sq.ft 510-570 850-980 800-1,000 600-700 2,700-3,200

Land required Hectare 47,000- 78,000- 74,000- 55,000- 250,000-53,000 90,000 93,000 64,000 300,000

FAR/FSI# X 1.5 1.5 1.5 1.5

Land required Hectare 31,000- 52,000- 50,000- 37,000- 170,000-35,000 60,000 62,000 43,000 200,000

In view of revised income bend for EWS/LIG/MIG as stated in Table C-1, revised requirement of area / land is as perTable E-1 below:-

Table E-1Requirement of area under various categories

Sr. Category of Area for each Housing Total area Under new Total area requiredNo. Housing household as shortage requirement income bend as per new

per 2012 in million total housing definitionrequirement sq.mt. shortage in

million

1. EWS 30 sq.mt. 10.55 316.50 17.96 17.96x30=538.80million million sq.mt.

2. LIG 60 sq.mt. 7.41 444.60million

3. MIG

761.10

In view of above mentioned scenario, question that arisesis whether Real Estate and construction Industry is capableof delivering of about 70 lakh housing units every yearfrom 2015 to 2022, more so in the background of fact that

present deliverable capacity may be maximum upto 8/10lakh units yearly. Comparative statement of progressunder various Social Housing Scheme is as per Table Fbelow :

Table 'F'Comparative statement of progress under various social schemes

Sr. Name of scheme No. of housing Completed Under Shortfall inNo. to be constructed houses construction in number

as approved in number number

1. Rajiv Awas Yojna 120000 in 16 cities 1154 18281 100565

2. Affordable 20472 4528 2200 13744Housing

3. Jawaharlal Nehru 1440000 831000 36100 248000under RenewalMission

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201616

Real Estate (Regulation and Development) Bill, 2013- BAI submits its comments

BAI responded to the request of the 'Select Committee (Rajya Sabha) on Real Estate (Regulation and Development)Bill, 2013' of the Rajya Sabha Secretariat, Parliament of India, by sending its views and suggestions, which is printedbelow.

Subsequently, BAI was invited to interact with the 'Select Committee (Rajya Sabha) on Real Estate (Regulation andDevelopment) Bill, 2013', when the members of the Committee visited Mumbai on 30th June, 2015. BAI was representedby Mr. D. L. Desai (Shankarbhai), Trustee; Mr. Neerav Parmar, Chairman, BAI Mumbai Centre; Dr. Anand J. Gupta,Imm. Past Hon. Gen. Secretary and Mr. Raju John, Executive Secretary.

Though the task is stupendous, but can be achieved if notby 2022 but by 2030 subject to all the stake holders i.e.Government both Central, States and Local self, real estatedevelopers, professionals such as engineers, architects andconstruction contractors come together and initiatingfollowing steps to achieve result.

A) Town planning departments need to change conceptfrom low rise horizontal development of cities intohigh rise vertical development with higher densityi.e. high FAR/FSI. This would bring down cost ofproviding civic infrastructure, since urbanizationarea would be reduced.

B) The present building approval plans byMunicipalities is not only time consuming butcumbersome. Real estate developers have to obtainminimum 30 N.O.C's from different department /Organisation, resulting in cost escalation. Many ofN.O.C's are irrelevant and are duplication. It issuggested that a single window clearance systemconnecting regulatory authorities at Central, Stateand Urban Local Body level, supported by atechnology plat form would help reducecomplexities and delay.

C) There is dire need to reduce indirect taxesaggregating to 35% as shown in Table 'D' by allauthorities to incentivise affordable housingdevelopment to improve housing affordability.

D) The Land Acquisition Rehabilitation & ResettlementAct 2013, is expected to have a majot impact on largescale township and affordable housing projects.Needless to state that few provision of LARR Act2013 are deleted or be suitably amended to achievehousing target.

E) Ministry of Skill Development & Entrepreneurshipsrealesed a report in April 2015 stating therein thatbuilding construction and real estate sectoremployed 45.40 million people in 2013 which isexpected to reach to 76.60 million by 2022. Most ofconstruction workers are not skilled. It is thereforenecessary for Construction Skill DevelopmentCouncil of India (CSDCI) to undertake onsite training

of construction workers. State governments shouldrealese 20% of building & other ConstructionWorkers Welfare Cess collected at rate of 1% onconstruction contract amounting to Rs. 13000 croresas on March 2015. This would enhance productivityof worker and saving in wastage of constructionmaterial.

F) Present cast-in-situ construction system need to bechanged to errection of readymade various buildingcomponent such as beam, column, slabsmanufactured in factory. It is necessary tostandardise design parameters. Alternatively mainconstruction contractors need to promote specialisedfoundation, superstructure and finishing contractorsfor timely and faster completion project.

G) Increased environment concern has reducedavailability of natural sand and coarse aggregate,delaying housing projects. Ministry of Housing ofstates and centre jointly with trade bodies such asBAI, CREDAI, CFI, NHBF fund research on use ofalternative such as construction waste, flyash, slagfrom steel plant in place and steal of natural sand.

H) Housing Regulatory Authorities to be formed in eachstate to regulate real estate sector and bring abouttransparency. There has to be "carpet area" norm/standards for building approval plan by Urban LocalBodies, sale on carpet area basis by real estatedevelopers to avoid possible litigation on chargedarea for flat. It should also be made mandatory forregistration and grading of real estate developers forprofessionalisation of real estate business.

I) Provident Fund corpus & Insurance Funds beinvested in housing projects either throughinstrumentality of REITS or other specially createdbonds by RBI. This will provide long term fundingrequirement to housing sector at lower interest ratethan that of Banks. Housing Finance Companies needto increase home loan tenure from 20 years to 30years, so as to reduce equated monthly installments.(EMI) to be paid by flat purchasers. Necessary taxincentives to be given to all the schemes.

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201617

Builders' Association of India (BAI) is an apex all Indiabody of Engineering Construction Contractors andBuilders, founded in 1941, has more than 15,000 businessentities as members through its 152 plus Centres (Branches)throughout the country. The fundamental aim of theAssociation is to bring about all round improvements inthe construction and development sector, while strivingtowards resolution of operational as well as policy levelproblems faced by the construction industry. This involvesmaking efforts to obtain from policy makers andauthorities, the level of attention that the constructionindustry deserves in view of its tremendous contributionand importance to the economy.

BAI believes itself, as one of the chief vehicles of deliveringthe national objective of housing for all by 2022. In orderto fulfill objective, construction of 50-60 million urban unitsper year is required. This could be achieved withinvolvement of real estate developers. Given the highincome and employment multiplier of housing, real estatedevelopment needs to be actively promoted. Housingdevelopment also reduces income inequalities. For all thesereasons, real estat development needs a supporting policyenvironment. Our view on RERA set out below emanatefrom this sense of responsibility.

The precise objective for RERA needs to be well thoughtout. Regulation for the sake of regulation would only addone more layer of approvals, increase transaction cost, andmake housing even more expensive for the ultimateconsumer. As it is, real estate is regulated by a multiplicityof laws. Consumer rights are adequately safeguardedthrough the Consumer Protection Act, 1986. The Bill isweak on the issues to be addressed an lumps all projectstogether.

The Bill proposes to cover "Commercial/industrial andother related projects", alongwith Residential projects.Commercial sector and other related segments haveresources and expertise to evaluate and conduct requireddue diligences and are safeguarded by the provision invarious other laws. Hence, if there be an issue that requiresregulation, it may at best relate only to the residentialprojects and not commercial or industrial projects.Accordingly, the Bill should focus on the Residentialprojects and leave all other projects out of its coverage.

The Bill proposes to cover all 'existing projects', where thecompletion certificate has not been received. It is not clear,how the projects which are already on-going can be covered

retroactively. This, if covered would invariably lead todelay due to registration and other requirements, costoverrun, and addition such delay would cost flatpurchasers extra money by way of interest on loans fromhousing finance companies / Banks. It may also raise anissue in respect of flat sold prior to RERA Act coveredunder relevant State Acts, such as Maharashtra OwnershipFlat Act. Further, the requirement to bring projects whichare ongoing within the coverage of the Bill is also arbitrary.Thirdly, including the existing as well as underdevelopment projects within The Bill would create a hugebacklog. Hence, it is only the "Green Field" projects (i.e.projects launched and registered after notification of theRER&D Act), that may be appropriately covered underthe proposed Bill.

Under the provision of the Bill, registration is online anddeemed in 15 days but the regulator will subsequentlyALLOT a user log in ID until then the sales cannot be made.We are concerned, as to how would deemed registrationin 15 days help if developers still have to wait for the login ID. On the other hand, the regulator will subsequentlyscrutinize all documents and can cancel registration if hethinks they are not in order. The question which arises isthat if there is deemed registration, how subsequentscrutiny can may be effected only if there is a subsequentinfraction or misdemeanor.

According to Section 7(a), the Real Estate RegulatoryAuthority may revoke the registration upon being satisfiedthat the promoter has made willful default in doinganything required of him by or under the Act or the rulesand regulations made thereunder. However, willful defaultis not defined in the Act. This implies possibility ofcompletely arbitrary principles in determining what thewillful default is. Hence, it is requested first of all that whatconstituted willful default may need to be clearly defined.Secondly, for the process of revocation to be equitable, itshould be made clear that the process of revocation wouldfollow the principal of natural justice and provide for thepromoter being given adequate opportunity of beingheard. Revocation of registration cannot and should notbe arbitrary.

Section 5 in its current form restricts the validity ofregistration to be conterminous with the likely period oftime within which the completion of the project isenvisaged by the promoter under provision of 4(2)(i)(c). itdoes not take into account other stakeholders like the plansanctioning authority, 'competent authority' or functional

Ref: 144/J/2015-16 dated June 16, 2015

The Joint Director (Com III)Rajya Sabha Secretariat,Room No. 212A, Parliament House Annexe,New Delhi 110001

Respected Sir,

Sub: BAI's Suggestion on the Real Estate (Regulation and Development) Bill, 2013

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201618

Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitation and Resettlement (SecondAmendment) Bill, 2015

- BAI submits its comments

BAI responded to the request of the 'Joint Committee on the Right to Fair Compensation and Transparency in Land Acquisition,Rehabilitation and Resettlement (Second Amendment) Bill, 2015' of the Lok Sabha Secretariat, Parliament of India, by sendingits views and suggestions, which is printed below.

Ref: 143/J/2015-16 dated June 10, 2015To,

The Joint Secretary (RS),Lok Sabha Secretariat,Room No.328, 3rd Floor,Parliament House Annexe,New Delhi 110001

Sub: Suggestions in respect of "Right to Fair Compensation and Transparency in Land Acquisition, Rehabilitationand Resettlement (Second Amendment Bill, 2015).

Respected Sir,

Builders' Association of India (BAI) is an apex all Indiabody of Engineering Construction Contractors andBuilders, founded in 1941, has more than 15,000 businessentities as members through its 152 plus Centres (Branches)throughout the country. The fundamental aim of theAssociation is to bring about all round improvements inthe construction and development sector, while strivingtowards resolution of operational as well as policy levelproblems faced by the construction industry. This involvesmaking efforts to obtain from policy makers and

authorities, the level of attention that the constructionindustry deserves in view of its tremendous contributionand importance to the economy.

BAI welcomes the Land Acquisition, Resettlement andRehabilitation Act 2013 and relevant Amendment to thoseprovisions in Amendment Bill 2015. It is a step in the rightdirection. However after going through the same, thefollowing are the suggestions from BAI to be added to theBill for better implementation and use of the act in theinterest of development.

agencies or financial agencies who are not answerable tothe Regulatory Authority which results in the delays onthe project. At many places, plan sanctioning authoritiesgrants phasewise commencement certificate, as such, itneed to be covered. On the other hand, the 'promoter' ismade solely responsible and liable to be penalized fordelays and non-compliance. Hence, it is necessary to bringall entities associated with grant of approval for the projectssuch as Urban Local Bodies into the ambit of RERA, andin particular Section 5 to enable the Real Estate RegulatoryAuthority to issue appropriate direction to them for thesake of timely completion of projects. The grant ofoccupancy certificate/completion certificate/plinthcertificate should be provided for on a time bound andautomatic basis. Further, it should be explicitly providedthat the project promoters are not liable for delays onaccount of want of approvals from statutory authorities.

It is also feared that including "Tenants", within the ambitof the Bill, would drift the focus away from the core of theBill to streamline and cover the "Developer-Buyers"relationships. "Tenants" enter into a property only afterthe Developer has acquired the "Occupancy Certificate' andthen the "Apartment" is handed over the "Buyer". Byinvolving "Tenants", who are temporary occupants on rent(for a limited time period), the Bill's "Developer-Buyer"

mandate would get diluted. Flat buyer when gives his flaton rental, then motive is to earn "profit". Bill can not includesuch transaction in the bill. Hence, it is urged that the Billrestricts its scope only to "Developer-Buyer" and anyactivity beyond the handover of the real estate project tothe 'Buyer' should stay outside the ambit of the bill.

Some of these suggestions are further elaborated in theattachment and some technical aspect are also commentedupon.

It is requested that the above suggestions may please begiven serious consideration for bringing the bill inalignment with its objectives as well as the goal of housingfor all by 2022.

Best Regards

Yours sincerely,

LAL CHAND SHARMAPRESIDENT

BUILDERS' ASSOCIATION OF INDIA

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201619

i) The timeframe of successful implementation of theprovisions of the land acquisition act has been thebiggest challenge in the implementation of anydevelopment endeavour of the government or anyprivate party. There are several cases for delays inland acquisition and payments of compensation tothe affected parties (for example the land acquisitionby MIDC in Raigad district of Maharashtra has beengoing for almost 10 years and the same is stillnowhere near completion). Although the act specifiestimeline, the adherence of the provisions of the actwithin the timelines mentioned is of utmostimportance to benefit all affected and interestedparties. Hence a stronger framework forimplementation , accountability of the implementingagency(state or central government) , timelycompletion of all the stages to be completed , financialpreparation for the compensation to be paid to theaffected parties are areas of utmost importance.

ii) The Land Acquisition, rehabilitation and resettlementact should be made applicable for project underprivate bodies as well. Due to political reasons thegovernment has refrained from using the act forprivate players. Over the last one year, the newGovernment of India has launched programs likedevelopment of 100 smart cities, severalinfrastructure works, etc. For the success of theseschemes by the government, involvement of theprivate sector is imperative.

The Government in the past has successfully createdcities like Navi Mumbai by land acquisition throughCIDCO and subsequently auction of the land toprivate players for development. It is impossible forthe government to achieve the desired rate ofdevelopment without the involvement of the privatesector. The revenue generated through these can beuse for the development of the village, towns, andcities. This lacuna in the act is to be rectified and theact should be applicable for large scale projectsinvolving acquisition of land for the private sector aswell.

Also there are several areas of the countries whereinfrastructure development schemes of thegovernment have still not reached mainly becausethe government is not able to raise funds throughthe use of BOT schemes and other forms of fundingschemes for the development of infrastructureschemes. The land acquisition act can be used for thedevelopment of such areas by allowing use of landalong the infrastructure lines for private use andauction instead of only relying on BOT schemes forthe development of infrastructure in these areas.

iii) As per the provision of this act if private companypurchased land equal or more than such limits inrural or urban areas as may be prescribed byappropriate government through private

negotiations with the owner of land than he shall fallwithin the purview of this act. The BAI takes strongobjections on this compulsory inclusion of a privatenegotiation within the purview of this act and thesame should be excluded or the applicability shouldbe at the discretion of the private party if they requireany government intervention for the acquisitionprocess. Only if government intervention is asked foronly then the provisions of this act should be followedby the private company.

iv) Although the section 30(2) of the act defines thecompensation for land owners in the first schedule,the promise made by the government of four timecompensation in rural areas and two timescompensation in urban areas needs to be more clearlyspelled out without any ambiguity on the same.

v) There have been several instances in the past wherehuge chunks of land have been converted to 'NoDevelopment Zone', 'Eco Sensitive Zone', ' GreenZone' , ' Lands affected due to construction of Dams'etc due to change in zoning by the government. Thishas locked all the present and future potentialdevelopment of such plots with no future to thelandowners/affected parties on such lands. Suchform of acquisition by the government in the form ofchange in zoning should be included under the actand adequate compensation to the farmer/landowner/affected party should be paid.

vi) There are several instances when the acquisitionpolicies of the state government are not adequatelycompensating the affected parties. For example as perthe current policy in cities of Maharashtra in the eventof acquisition by government for lands falling underreservations or road widening, the affected party isgranted TDR instead of monetary compensation inlieu of surrendering of land. However, in this casethe TDR granted does not take into account, the valueof land from which TDR is generated. The value ofthe TDR granted should be commensurate to themarket price of the land being acquired from the landowner and accordingly adequate TDR should beissued to compensate the affected party from whomthe acquisition is done.

Therefore kindly take the abovementionedsuggestion into consideration. I therefore request youto kindly grant me opportunity of being heard beforethe committee.

Thanking you,Yours sincerely,

LAL CHAND SHARMAPRESIDENT

BUILDERS' ASSOCIATION OF INDIA

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201620

Goods & Service Tax

An Interactive Session on 'Goods & Service Tax' (GST) wasorganizes by Builders' Association of India (BAI) onThursday, 1st October 2015 at MC Ghia Hall of IndianTextile Accessories & Machinery Manufacturers'Association, Mumbai.

The main speakers were : Mr. Rajkamal Shah, HonoraryService Tax Consultant, BAI; Mr. P. Purushotham,Honorary Tax Consultant, BAI and Mr. Sandesh Mundra.Co-Chairman, Goods & Service Tax Committee, BAI.

Apart from all senior functionaries of BAI from acrossIndia, Taxation managers of corporate constructioncompanies and major construction companies wereinvited to the interactive session.

Mr. Neerav Parmar, Chairman, BAI Mumbai Centrewelcomed the gathering and was also the moderator forthe interactive session.

Mr. P. Purushottam spoke on, Constitution Bill - Outcome;Bearing on Construction Industry and RecommendaryIssues - GST Regime, vis-à-vis Apex Coujrt / SupremeCourt Decisions.

Mr. Rajkamal Shah spoke on, Transition Issues - AConcern; ITC/Cenvat Credit - Under GST and Accounts& Documents - Highlights.

Mr. Sandesh Mundra spoke on, Review of negative list /Mega exemption; Probable GST Rate - A hint and TaxableEvent - Concern or Useful.

It being an interactive session, the talks by the speakerswere interspersed with queries, suggestions, clarifications,etc. by the gathering.

Mr. D. L. Desai (Shankarbhai), Trustee, BAI gave theconcluding remarks.

Mr. C. G. Deochake, Hon. Gen. Treasurer, BAI; Mr. SunilMundada, State Chairman, BAI Maharashtra and Mr. K.Viswanathan, Taxation Committee Chairman, BAI alsograced the dais during the interactive session. Theorganising of the interactive session was co-ordinated byMr. Raju John, Executive Secretary, BAI.

Based on the outcome of the discussions in the interactivesession, points were finalized for drafting a representationto be made to the Union Finance Ministry by BAI. We aregiving below the said points.

GST Model in India and Precaution Points for theConstruction Sector.

The Goods and Services Tax (GST) is a value added tax(VAT) on the supply of goods or services. It is levied andcollected on value addition at each stage on such suppliesbased on input tax credit method for both intra state aswell as inter-state purchases.

When we say "Supply" we are moving from the age old

tradition of taxing the events of manufacturing or sale orof rendition of service. Hence this is the most paradigmshift in the taxing event which may tax even the freesupplies and branch transfers, something which theconstruction community is not at all used to.

The initial aspiration of the government was to have asingle GST which would have been the most simplifiedform of indirect taxation. However, the government overthe years of efforts and negotiation with States had tocontend itself with a dual GST model to bring all thestakeholders on a common platform. However despite thedilutions in the initial model, the government and itsofficials continue to emphatically focus on following tobe achieved in this new taxation system:-

A) Clarity and Simplicity in definitions

B) Certainty in Assessment

C) Ease of doing business

Lets now look at some of the major features of the biggesttax reform not only at our country level, but possibly atthe global level also looking to India's democratic andfederal structure and the efforts already spent on the task:--

1. DUAL GOODS AND SERVICE TAX - GST in Indiaas per the current constitutional draft shall have twocomponents: one levied by the Centre (hereinafterreferred to as Central GST), and the other levied bythe States (hereinafter referred to as State GST). Thusone CGST Law would be passed by the centre andone SGST Law would be passed by each of the statesbased on a model SGST Law recommended by thecentre. Besides the tax charged on interstate supplyshall be a combination of SGST and CGST and shallbe known as IGST (Integrated Goods and ServiceTax) which shall continue to be administered moreor less in a manner similar to CST.

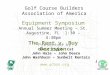

2. REVENUE NEUTRAL RATES - Centre has set up adetailed machinery to work out the revenue neutralrates which would ensure that there is no loss ofrevenue to centre or state, post implementation ofGST in India. The expected Revenue neutral ratesmay possibly be in the range of 18-27%. Besides thereare also talks that these rates may be different forgoods and different for services. In addition to GST,the 1% additional tax also now looks a certainty,hopefully only for the first two years, leviable onthe supply of goods from one state to another. Thisadditional revenue shall be kept by the state of origin.Now from a construction sector's perspective onemay have apprehensions, that the tax outgo shallincrease significantly. However lets look at a typicalbuilding construction project and see the currentimpact of the multiple taxes on the project :-

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201621

Existing Taxes under a BuildingContract

Particulars Amt in Rs. Excise VAT Service Tax Total Tax Tax in Rs

Cement 15 12% 15% 27.00% 4.05

Steel 25 12% 5% 17.00% 4.25

Other Materials 15 12% 10% 22.00% 3.3

Sand / Aggregate 10 0% 5% 5.00% 0.5

Labour 20 14% 14.00% 2.8

Admin & o/h 3 14% 14.00% 0.42

Depreciation 2 15% 14% 29.00% 0.58

Profit 10 14% 14.00% 1.4

Composition VAT 2% 2

Total 100 19.4

Note - The above figures are based on a typical building construction project assuming the total project value to be Rs. 100.However the actual proportion may vary.

Thus based on above, its clear, that even today atypical construction project ends up bearing indirecttaxes to the tune of 20%. Based on the type of theproject and availability of typical exemptions the%shall vary from 15 - 25%.

3. DESTINATION BASED TAXATION - The mostcritical change which GST shall bring in our taxationsystem is that it shall shift the tax collection rightfrom the state of origin to the state of destination.That is if the goods move from Gujarat to Orissa, itsthe state of Orissa which shall have the right to collecttax on such transaction. The concept, which is pickedup from the prevalent global practise has somegenuine reasons, key being:-

a. Promoting economic efficiency - Since its thejurisdiction of consumption, which woulddefine the rates of taxation, the source ofprocurement and the tax rates prevailing atsuch source location would stop playing anyrole when it comes to identifying the most costeffective vendor. Hence the buyer wouldalways choose the most economically efficientvendor subject of course to the considerationsof logistics.

b. Equitable distribution of revenue - Globally ithas been felt that the a destination basedrevenue model leads to a more equitabledistribution of tax revenue amongst all the taxjurisdictions. This would reduce the currentdisparities and would lead to a uniforminfrastructural development across all thestates of the country. The idea is to empowerthe backward states with more tax revenues.This shall lead to an overall development andgrowth of the country and in turn highercollections to all states in the long run.

4. CENVAT CHAIN - Unlike the current scenariowhich leads to cascading of taxes, under GST,complete cross credit of taxes would be available.That is credit of CGST would be available againstCGST liability, credit of SGST would be availableagainst the SGST liability, credit of both CGST andSGST would be available against IGST liability andvice versa. The only hitch in the chain would be non-availment of credit of the 1% additional tax paid onthe inter-state supply of goods which shall distortthe prices to some extent.

5. REGISTRATION - All suppliers already registeredeither under VAT, Excise and Service Tax may notbe required to register again, except to the extent ofsubmission of any additional information which maybe required to be given to justify a uniforminformation database. There shall continue to beseparate PAN based registration for CGST as wellseparately for each state SGST.

6. IMPORTS AND EXPORTS - Going by the theory ofa destination based consumption, we can safely saythat the exports shall be Zero rated and imports shallbe treated at par with the inter-state transactions withIGST leviable on them. Imports shall also besubjected to Basic Customs Duty which is proposedto be continued even under the GST regime.

7. ADMINISTRATION OF GST - As per therecommendations of the Task force report on GST,the Central Board of Excise and Customs (CBEC)shall be responsible for implementation of CGST andstate tax administrations will be separatelyresponsible for implementation for SGST. Thedifferent assessing authorities may again create someproblems as one may accept a valuation and anotherauthority may reject the same value. Hence it is bettersuited to have just one assessing authority.

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201622

8. GOODS AND SERVICE TAX COUNCIL - As perthe Constitution Amendment Bill, 2014 ('Bill'), therewill be a Goods and Service Tax Council which shallmake recommendations to the Union and the Statesabout the basic structure of the law and the futuremodifications. The Bill provides that theadministration of GST would be the responsibilityof the GST Council which would then become the

Steps needed for GST Implementation Time (in Months)

• Both the houses of the Parliament pass the bill independently with 2/3rd majority 1

• 50% of the states ratify in their assemblies + Receipt of Presidential Assent 4

• Formation of GST Council 1

• Model GST law should come out for public suggestion at both central and state level 3

• Elaborate Discussion on the Negative List 1

• Central GST Law is passed by the centre + Presidential Assent 1

• State GST Law is passed by the states (after battling with Municipalities and Local Bodies)+ Governor's Assent 3

• Educating the end users 3

• GSTN - IT Network is established 1

• New Registration numbers are allotted 1

Minimum Time 19

Now let's look at certain issues which may be criticalfrom a construction sector's perspective when it comesto implementation of GST in India :-

i. Proposed Negative List / Exemptions under GST(under both SGST and CGST) - Under the currentregime the negative list / exemptions of goods andservices have been separately defined for Excise,Service Tax and VAT. Ideally for the ease ofbusiness, there should be a single andcomprehensive negative/exemption list for allforms of GST i.e. CGST, SGST and IGST. It can bevery well seen that the government has over aperiod of last 3-4 years constantly made a seriouseffort to tone down the exemptions. The intentionis to continue the exemptions only for the activitiesinvolving immense public interest. Hence theconstruction sector should give a properrepresentation to the government identifyingprojects critical to country's development andwhere development is taking place solely on thebasis of public interest. Government may be biasedtowards exempting those projects where thegovernment itself is directly / indirectlyreimbursing the tax component making it a taxneutral transaction for them.

ii. Negative List for Input Credit - A problem whichthe construction sector faced in the current scenariois that it has found itself in the exclusions list forthe purpose of availment of Input Credit by therecipient of the construction services both underVAT and Service Tax. If such a provision is

continued, then it may go against the basic themebehind GST i.e. removal of cascading impact oftaxes. Besides the building is a very critical elementwithout which it may not be possible to producegoods or render services.

iii. Treatment of works contracts - Looking to currentdraft of the constitutional amendment bill, whichhas retained the Article 366 (29A) (article whichpermitted states to levy sales tax on works contracton deeming basis) when it should have been eitherremoved or amended with a clear sunset clause.The retention of this article has added to thegrowing confusion about the taxability of worksContracts under the proposed GST regime whichpromises to treat both goods and services at par.The moot question now is whether the constructionactivity shall be treated as Goods or services or anyseparate criteria shall be set for composite contractsto levy GST on them. Globally the trend seems tobe to treat the construction activity as a serviceirrespective of the element of material which getsincorporated in works contract.

iv. Identifying the Destination - One of the mostinteresting and complex rules which will beintroduced under GST are the place of supply rules.These rules determine the place of consumptionof goods and services which will determine thejurisdiction having the sovereign right to collectthe revenue. Thus there is every possibility that twojurisdictions claim their area to be the place ofconsumption in order to maximise their revenues.

apex indirect tax policy making body of the country.This GST Council would be formed by the Centraland State level ministers in charge of the financeportfolio.Now, although I am not the finance minister, butstill I made an attempt to draw some practical timelines with which the government could implementthe GST in a satisfactory manner :-

BUILDERS' ASSOCIATION OF INDIA 75th Annual Report and Accounts – 2015-201623

The construction sector thus needs to identify allsuch areas where the possibility of disputes couldbe high and accordingly propose proper solutionto the government well in advance. For e.g. If theservices of an architect are consumed by the Headoffice in Maharashtra for a project being executedin Karnataka, now in which jurisdiction will thearchitect be legally required to discharge his taxliability under GST ? Whether at Maharashtrawhere he raises the invoice or Karnataka, wherethe services are ultimately consumed. Further whatif some of such services are covered under thereverse charge and the service recipient decides toallocate the service over different projects runningin different states based on the proportionate use.All such issues need to be resolved properlymaking the law more administratively convenientrather that theoretically satisfying to thegovernment.

v. Impact of the Landmark judgements of the ApexCourt - Works contract is one area, where thetaxability and valuation till date have beengoverned more by the court judgements ratherthan the prescription of act and rules. Some of thejudgements relate to identifying whether aparticular contract is a works contract or not, somedetermine the value of goods involved in acontract, some on taxability of inter-state workscontract etc. Now, these judgements may remainrelevant even under GST. So a detailed exerciseneeds to be carried out in this regard to assess thefuture relevance. The government may also berequested to cover such issues within the proposededucation guide that they may be planning torelease after introducing the GST law to facilitateits implementation.

vi. Threshold Limit - The basic exemption limit hasbeen defined separately for goods and servicesunder the current system. A uniform thresholdneeds to be defined under GST considering the factthat threshold under Service Tax is Rs. 10 Lacs,under Excise is Rs. 150 Lacs and under most of thestate vat laws is Rs. 5 Lacs. There is no claritywhether the government shall bring out a uniformthreshold or shall prescribe separate threshold forSGST and CGST.

vii. Contractor - Sub-contractor relationship - When welook at the different state VAT laws, we would seea common pattern while defining the taxability oftransactions between contractor and sub-contractor. This is so due to the landmarkjudgement of Supreme Court in the case of Stateof AP vs. L&T (2008-TIOL-158-SC-VAT). As a resultthe state laws have been drafted in a way to taxeither the contractor or the sub-contractor. Oneneeds to assess the relevance of this critical

judgment to determine the position that is to betaken once GST is implemented. Although thegovernment may claim that when complete Inputcredit is available to everyone in the chain, noresort should be had to this past practise. However,practically if one party pays and the other partycan avoid paying, then it can result in reduction inefforts towards compliances. Further this shall alsolead to ease of business more particularly when thecontractor undertakes exempted project.

viii. Transitional provisions :-