Embed Size (px)

Citation preview

1ANALISIS TRIWULANAN: Perkembangan Moneter, Perbankan dan Sistem Pembayaran, Triwulan II - 2007

BULLETIN OF MONETARY ECONOMICS AND BANKING

Directorate of Economic Research and Monetary PolicyBank Indonesia

PatronPatronPatronPatronPatronBoard of Governor Bank Indonesia

Editorial BoardEditorial BoardEditorial BoardEditorial BoardEditorial BoardProf. Dr. Anwar Nasution

Prof. Dr. Miranda S. GoeltomProf. Dr. Insukindro

Prof. Dr. Iwan Jaya AzisProf. Iftekhar HasanDr. M. Syamsuddin

Dr. Perry WarjiyoDr. Halim Alamsyah

Dr. Iskandar SimorangkirDr. Solikin M. JuhroDr. Haris Munandar

Dr. Andi M. Alfian Parewangi

Editorial ChairmanEditorial ChairmanEditorial ChairmanEditorial ChairmanEditorial ChairmanDr. Perry Warjiyo

Dr. Iskandar Simorangkir

Executive DirectorExecutive DirectorExecutive DirectorExecutive DirectorExecutive DirectorDr. Andi M. Alfian Parewangi

SecretariatSecretariatSecretariatSecretariatSecretariatToto Zurianto, MBA

MS. Artiningsih, MBA

The Bulletin of Monetary Economics and Banking (BEMP) is a quarterly accreditedjournal published by Directorate of Economic Research and Monetary Policy-BankIndonesia. The views expressed in this publication are those of the author(s) anddo not necessarily reflect those of Bank Indonesia.

We invite academician and practitioners to write on this journal. Please submityour paper and send it via mail to: [email protected]. See the writing guideon the back of this book.

This journal is published quarterly; January √ April √ August √ October. The digitalversions including all back issues are available online; please visit our stable link:√http://www.bi.go.id/web/id/Publikasi/Jurnal+Ekonomi/. If you are interested to sub-scribe for printed version, please contact our distribution department: Publicationand Administration Section √ Directorate of Economy and Monetary Statistics,Bank Indonesia, Building Sjafruddin Prawiranegara, 2nd Floor - Jl. M. H. ThamrinNo.2 Central Jakarta, Indonesia, Ph. +62-21-3818202, Fax. +62-21-3802283,Email: [email protected].

BULLETIN OF MONETARY, ECONOMICSAND BANKING

Volume 14, Number 1, July 2011

QUARTERLY ANALYSIS: The Progress of Monetary, Banking and Payment System,

Quarter II - 2011

Author Team of Quarterly Report, Bank Indonesia

Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control

Policy

Trinil Arimurti, Budi Trisnanto

Sovereign Risk Analysis of Developing Countries: Findings From Credit Default Swap

Premium Behaviour

Moch. Doddy Ariefianto, Soenartomo Soepomo

Determinant of Bank Runs In Indonesia: Bad Luck or Fundamental ?

Iskandar Simorangkir

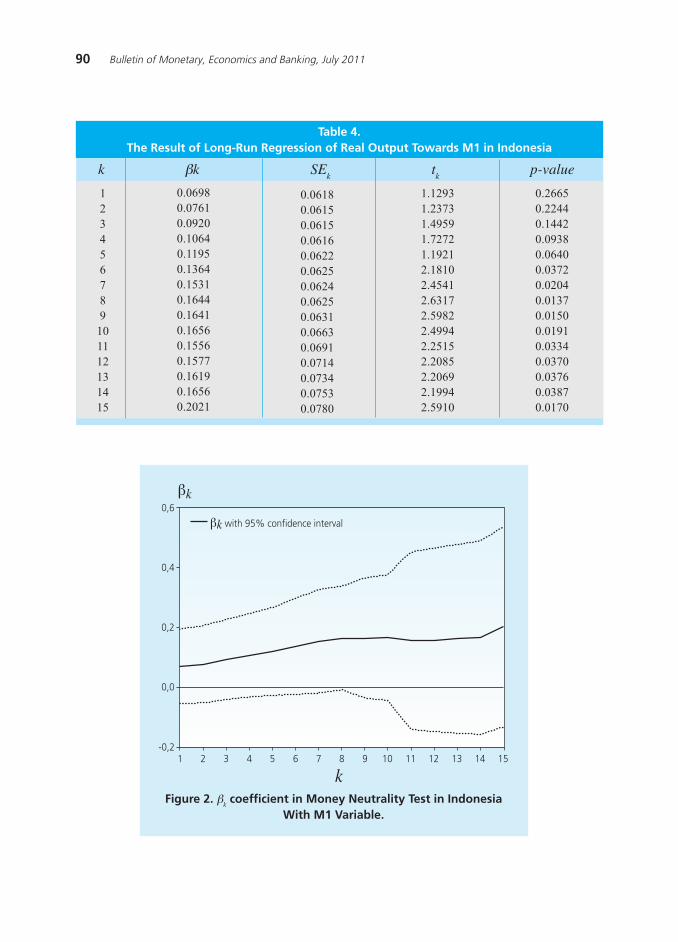

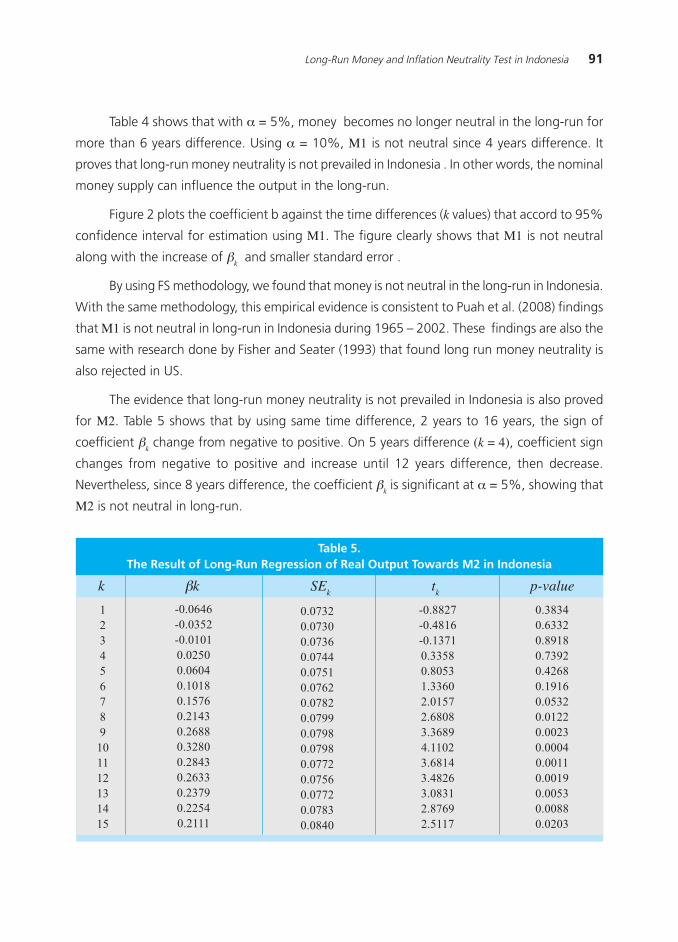

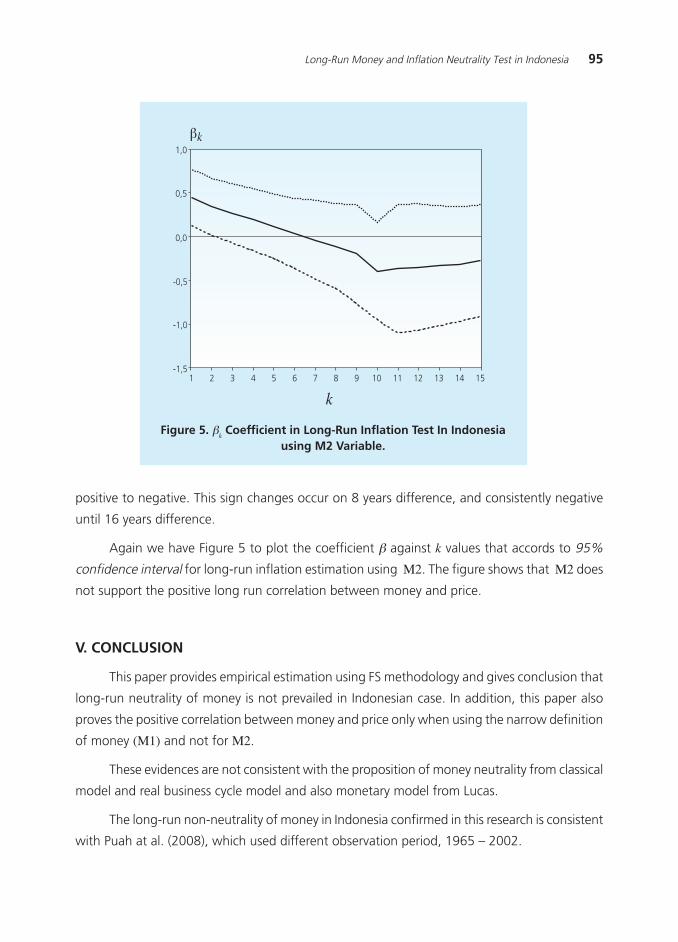

Long-Run Money and Inflation Neutrality Test inIndonesia

Arintoko

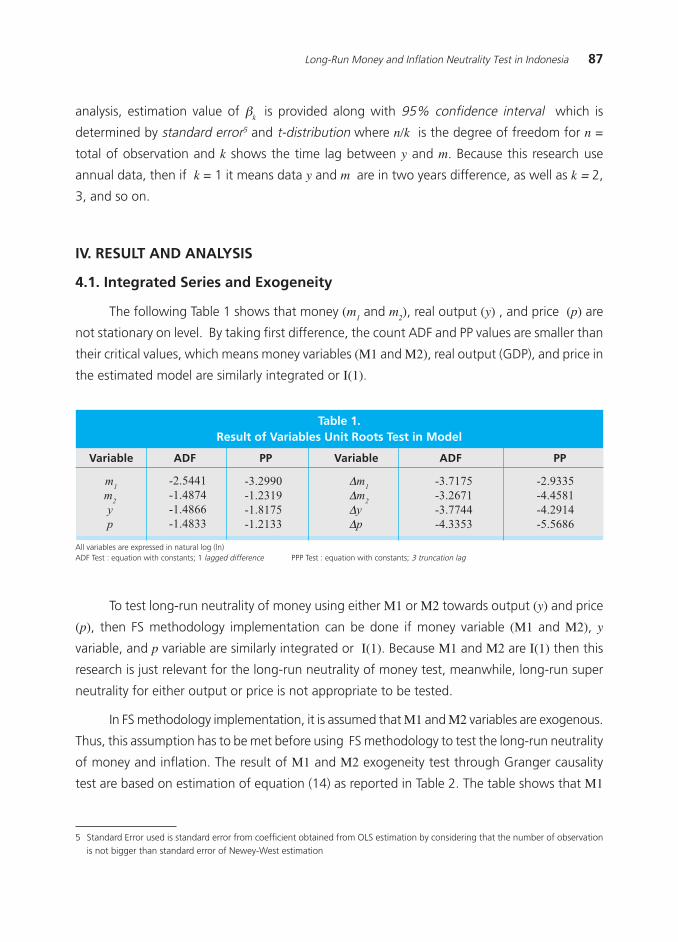

5

51

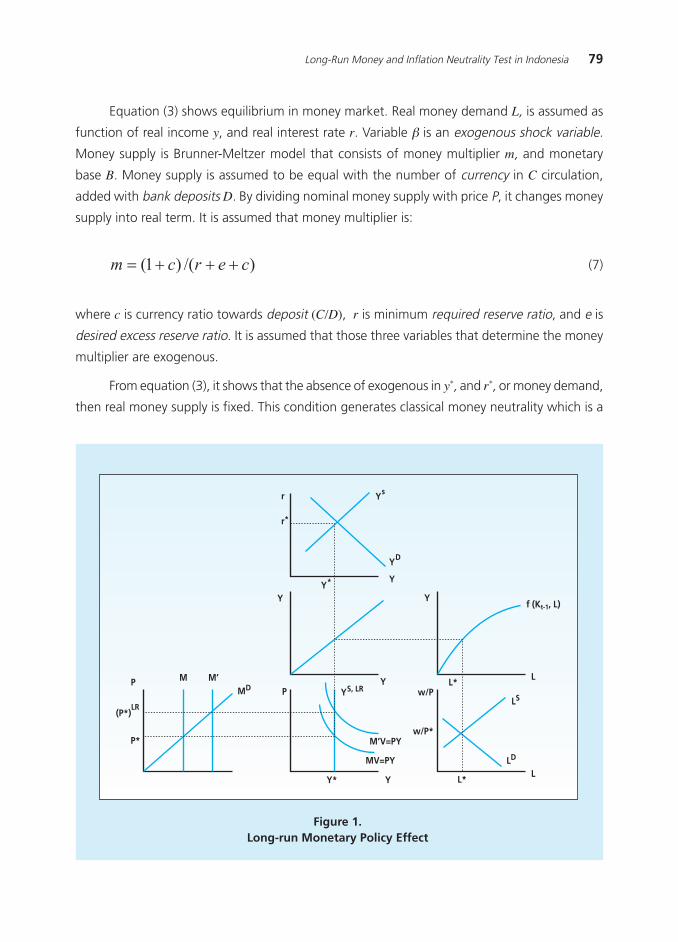

1

31

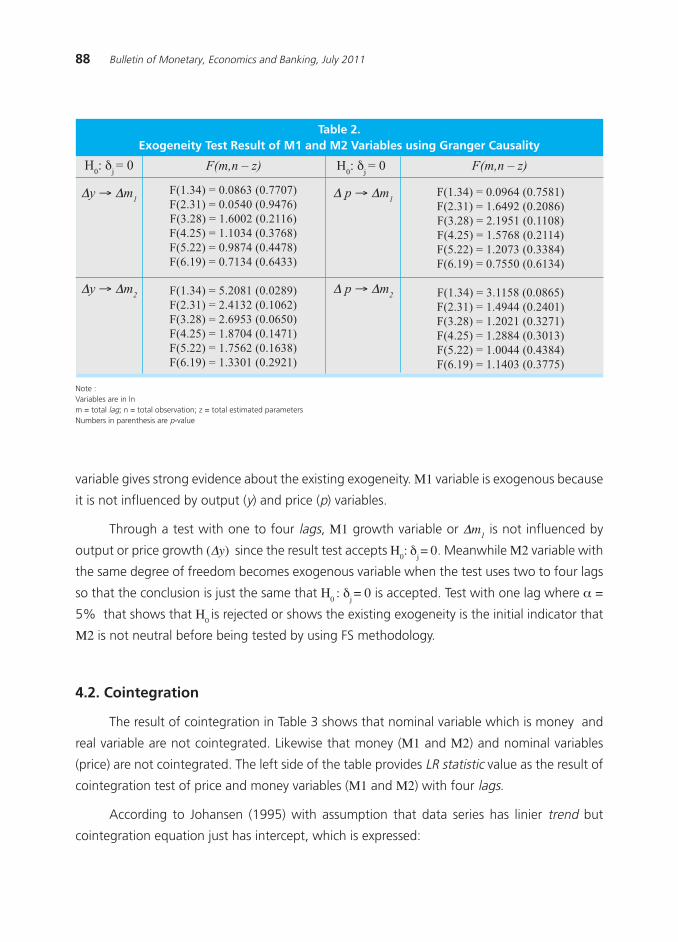

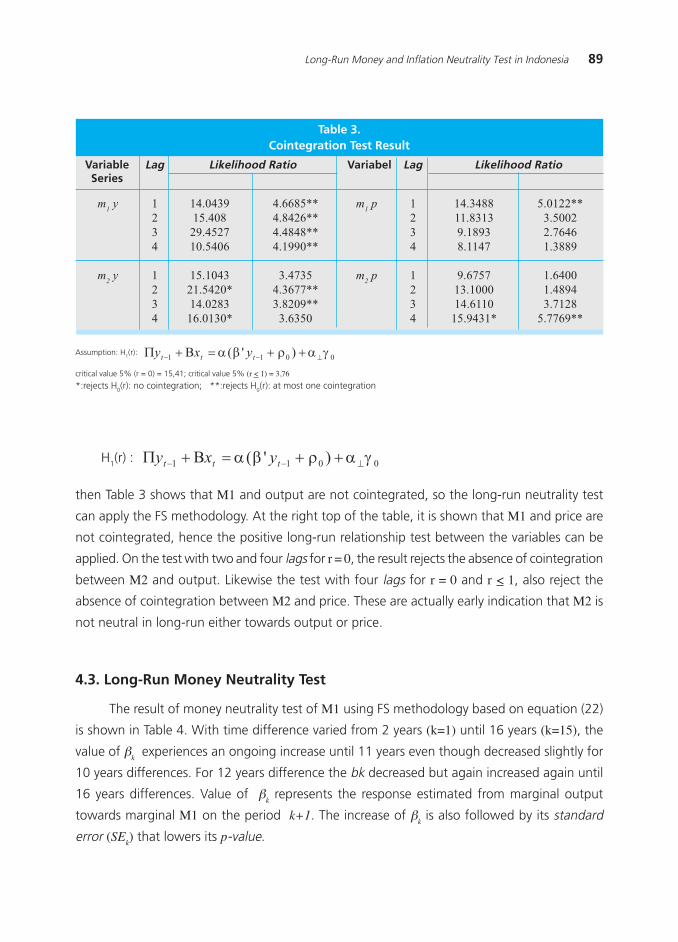

75

1QUARTERLY ANALYSIS: The Progress of Monetary, Banking and Payment System, Quarter II, 2011

QUARTERLY ANALYSIS:The Progress of Monetary, Banking and Payment System

Quarter II - 2011

Author Team of Quarterly Report, Bank Indonesia

The Board of Governors Meeting (Rapat Dewan Gubernur/RDG) of Bank Indonesia on 12

April 2011 has decided to maintain the BI rate by 6.75%. This decision does not change the

direction of Bank Indonesia»s monetary policy which tends to be strict in an effort to control the

inflationary pressures that are still high, amid the government efforts to reduce inflationary

pressure from volatile foods group. The Board of Governors considered that the strengthening

of the rupiah so far can reduce these inflationary pressures, particularly from the rising price of

international commodities (imported inflation). In addition, to minimize the negative impact of

short-term foreign capital flows on monetary stability and financial system, the Board of

Governors also has decided to replace the one-month holding period on SBI to six-month

holding period, which shall take effect on May 13, 2011. Looking ahead, Bank Indonesia assessed

that the possibility of the BI rate level adjustment is still open to dampen the incoming inflationary

pressures. Bank Indonesia believed that the implementation of monetary and macro-prudential

policy mix, supported also by the strengthened coordination of government policy, will be able

to maintain the macroeconomic stability and bring inflation to the target, which are 5% ± 1%

in 2011 and 4.5% ± 1% in 2012.

The Board of Governors considered that the global economic recovery in the future is

better as seen from the upward adjustment of global economic growth projections by various

international agencies. This improvement of global optimism will have an impact on world

trade volume which has now also increased. This will have positive influence on the demand

for export products to help encouraging domestic economic growth. However, the process of

global economic recovery is still faced with the uncertainties related to the risk of debt crisis

that hit several countries in Europe and the potential disruption of production after the

earthquake in Japan. In addition, the rising prices of oil and global food commodity are predicted

to continue which cause inflationary pressures in many developed countries and emerging

economies, including Indonesia.

2 Bulletin of Monetary, Economics and Banking, July 2011

On the domestic side, the Board of Governors observed that Indonesia»s economic growth

is forecasted to increase by 6.0 to 6.5% in 2011 and 6.1 to 6.6% in 2012. This economic

recovery is underpinned by a more balanced source of growth in line with the improving

investment performance and the export performance that remains solid. In the second quarter

of 2011, economic growth is forecasted to grow quite high at 6.4%. The role of investment to

increase the capacity of the economy, especially through FDI, is expected to rise in line with the

demand that remains strong, both from domestic and external, and also with the improvement

in sovereign credit rating. By sector, all sectors of the economy are predicted to grow high, with

the highest growth in the sector of transport & communication, trade, hotels & restaurants,

and construction.

The performance of Indonesia»s balance of payments recorded a surplus which is estimated

to be still high enough in 2011. This surplus is derived either from the current account or from

the capital and financial transactions. Export is forecasted to grow quite high. Capital inflows,

in the form of portfolio, are predicted to remain large, while the foreign direct investment (FDI)

is expected to increase. With such development until the end of March 2011, foreign reserves

stood at 105.7 billion U.S. dollars, equivalent to 6.3 months of imports and foreign debt

payments.

The strengthening trend in rupiah continued in March 2011. In addition to being in line

with the performance of BOP, which recorded a grand surplus and foreign investors» positive

perception toward the strength of Indonesia»s economic fundamentals, the strengthening of

rupiah is also a part of Bank Indonesia»s policy response to control inflationary pressures,

particularly from the rising prices of international commodity (imported inflation). Until the end

of March 2011 the rupiah was strengthened by 3.47% (ptp) to Rp8.708 per U.S. dollar. This

appreciation to Rupiah has not so far affected the competitiveness of Indonesia in terms of the

exchange rate, among others, reflected in the performance of Indonesia»s non-oil exports which

continue to show a relatively high improvement.

In regard to price, although the inflation has shown a declining trend, the risk of future

inflation pressures is expected to remain quite high. CPI inflation in March 2011 reached 6.65%

(yoy) or deflation of 0.32% (mtm) in line with inflation correction in alimentation products.

Although it is still relatively high, the inflationary pressure from the volatile foods group showed

a declining trend in line with the Government measures to strengthen the national food.

Meanwhile the moderate inflation of administered prices is associated with the minimum price

adjustment policies by the Government. However, the core inflation showed an increasing

trend, which was recorded at 4.45% (yoy) or 0.25% (mtm) in March 2011, as the propagated

impacts of the high prices of food and the rising inflation expectations. Looking ahead, the risk

3QUARTERLY ANALYSIS: The Progress of Monetary, Banking and Payment System, Quarter II, 2011

of inflationary pressures is expected to remain relatively high, influenced by the rising prices of

international commodity, the high domestic demand, and the high inflation expectations. Bank

Indonesia will continue to be alert to the risk of inflationary pressures and strengthen the

mixture of monetary and macro-prudential policy to control the inflation targets.

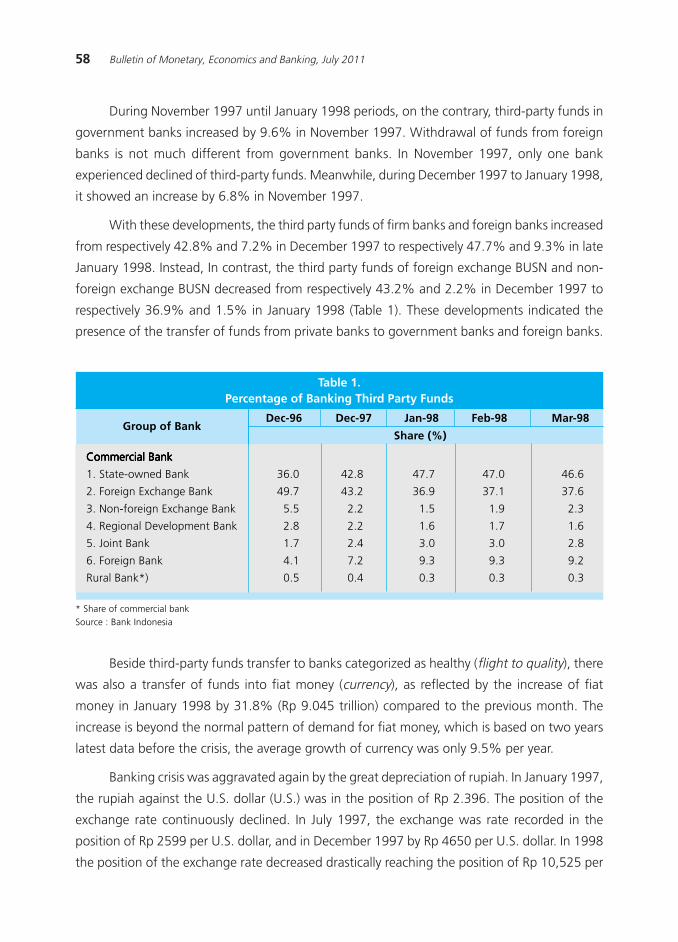

The stability of financial system is maintained along with the continuing improvement of

the intermediation function of banks and the banking liquidity which is in control. The banking

industry is under a stable condition characterized by the sustained capital and liquidity as

reflected in the high capital adequacy ratio (CAR) at the level of 18% and the ratio of

nonperforming loans (NPL) which is maintained fewer than 5% gross. The banking

intermediation is also getting better reflected in the rising credit growth, which in March 2011

reached 25.1% (yoy), supported by the growth in all types of loans including loans to Small

Medium Enterprises (SMEs).

4 Bulletin of Monetary, Economics and Banking, July 2011

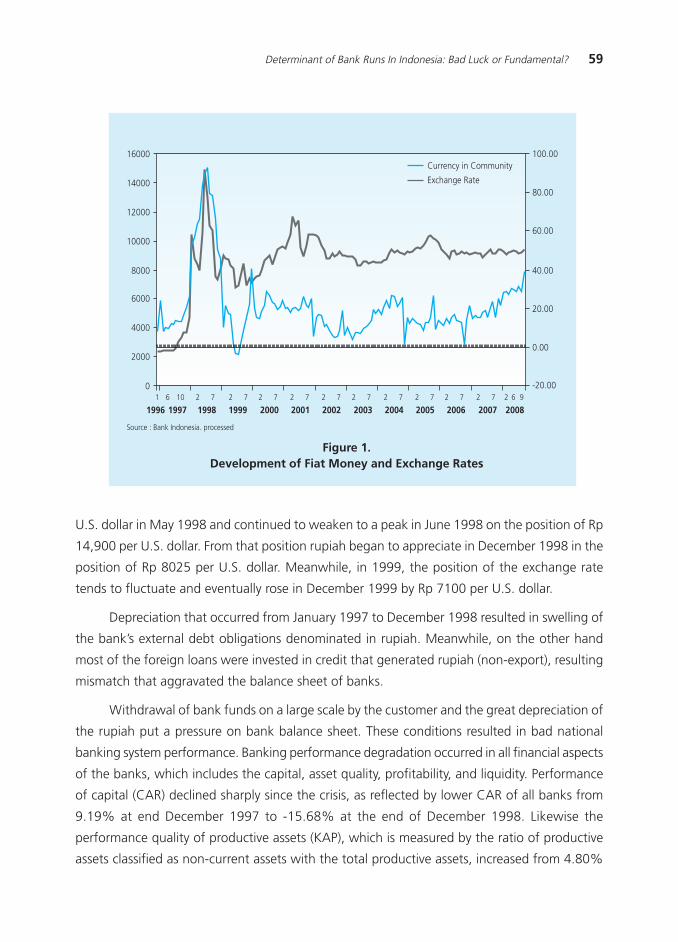

This page is intentionally left blank

5Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

PERSISTENCE OF INFLATION IN JAKARTA AND ITS IMPLICATIONON THE REGIONAL INFLATION CONTROL POLICY

Trinil Arimurti, Budi Trisnanto 1

The main objective of this study is to measure the persistence of inflation level in Jakarta. In addition,

this study intends to find out the source of inflation persistence and its implication to regional inflation

control. The analysis of the regional inflation behavior developed in this paper is explored to commodities

level. The empirical result indicates that the level of inflation persistence in Jakarta is relatively high,

stemmed from high level of inflation persistence for most of commodities that construct inflation. Using

the estimation results of the hybrid NKPC model, it shows that high inflation persistence in Jakarta mainly

caused by inflation expectation, which is a combination of forward and backward looking. In this regards,

it requires efforts gradually transform the behavior of inflation expectation to be more forward looking.

Keywords: inflation peristence, expectation, NKPC.

JEL Classification:E31, R10

1 The views on this paper are solely of the authhors and not necessaily reflect the views of Bank Indonesia. We thank to Yoni Depari,Sugiharso Safuan and researchers on Beureau of Economc Research and Beureau of Monetary Policy, DKM, Bank Indonesia;[email protected], [email protected].

Abstract

6 Bulletin of Monetary, Economics and Banking, July 2011

I. INTRODUCTION

According to the constitution No. 13, 1968 about Bank of Indonesia (Bank Indonesia)as

finally amended with law No. 4, 2003, the duty of Bank of Indonesia is to achieve and maintain

the stability of Rupiah value toward good and service or inflation stability.Therefore, the monetary

policy is directed to achieve and maintain the inflation in the low and stable rate. In this context,

the response of monetary policy is not only determined by the inflation rate that wants to be

achieved but is also determined by the inflation behavior itself. That will determine the amount

and timing of the response of monetary policy that needs to be applied in order to reach the

inflation desired. In the side of inflation rate that wants to be achieved, the monetary policy is

directed to achieve the inflation target which is stipulated decreasing gradually to the rate that

supports the perpetual economy growth. According to the law meant, the inflation target is

stipulated by the government after coordinating with Bank of Indonesia which is purposed to

increase the credibility of monetary policy. The assessment about the inflation behavior is related

to the inflation persistence or the speed of inflation rate back to its equilibrium rate following

the shock.

Some researchers have been conducted to see the inflation persistence in Indonesia. The

result of Yanuarty study (2007) and Alamsyah (2008), for example, is to conclude that the

degree of inflation persistence in Indonesia was generally high however tended to decrease in

the crisis aftermath period. While Harmanta (2009) stated that the backward lookinginflation

persistence in the era of ITF decreased, and for theforward lookingexperienced an increase.

Nevertheless, the study needs to be supported by the regional study, in term of looking more in

regional level. It is also motivated by the understanding that the national inflation is formed

from regional inflation. More specifically, the study of inflation persistence in region by considering

that each has inflation characteristic that implicates to the inflation controlling policy though

generally inflation pressure in region mostly related to the shock in supply

The implementation of Inflation Targeting Framework (ITF) in 2005 became the milestone

of the change of monetary policy frame done after the economic crisis in Indonesia. Principally

the monetary policy frame is in order to adopt the more credible policy frame that accomplish

to the use of interest rateas operational target and anticipative policy. ITF is hoped able to

change backward looking expectationthat becomes the source of the high inflation intact, to

becomeforward looking expectation. So that, it is hoped that ITF can push the decrease of

inflation persistence.

Next, the persistence inflation needs to be supported by analysis about the cause of

inflation persistence. As understood in CPI inflation component that its price is influenced by

7Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

government policy in the field of price and administered prices. The price in this commodity

tends to be flat and changes when there is a government policy. Besides that, there is component

that its price is influenced by supply shocksor is seasonally. For that, assessment is needed to

see the fundamental factors more detail. This is purposed so that the response of monetary

policy can be carried out more precise regarding monetary policy is for demand management.

In other words, the response of monetary policy cannot be overdone if the source of inflation

pressure from the non √ fundamental factor.

The study of the phenomenon of the inflation persistence that becomes very important

to be done in order to support formulating effective monetary policy. This thing because

the affectivity of monetary policy can support the perpetual economy growthin order to

raise the society prosperity. The high inflation will give negative impact to the economy.

Purchasing powerof society will decrease and world business will be covered by the high of

uncertainty. The implication from the inflation persistence will also be felt in the level of

region so that it needs to be looked after by local government to be able actively act in

controlling inflation.

The study is finally needed to formulate the strategy of inflation control. The source of

inflation pressure makes the inflation persistence needs to be analyzed more edge so that

can be differentiate the fundamental form the temporary source of inflation pressure. The

monetary policy cannot be fully used to respond the inflation pressure from the side of

supply.Sectoral and regional policies are needed to decrease the inflation pressure from non-

fundamental factors. There are some studies of inflation persistence that has previously been

done in Indonesia that are more focused on the national scale or range. National inflation

constitutes theweighted averagefrom inflation in the region in Indonesia, therefore it needs

to study about the behavior of inflation in the region level,including to measure and search

for its cause, and also to know its implication toward the control of the region inflation with

the focus on Jakarta.

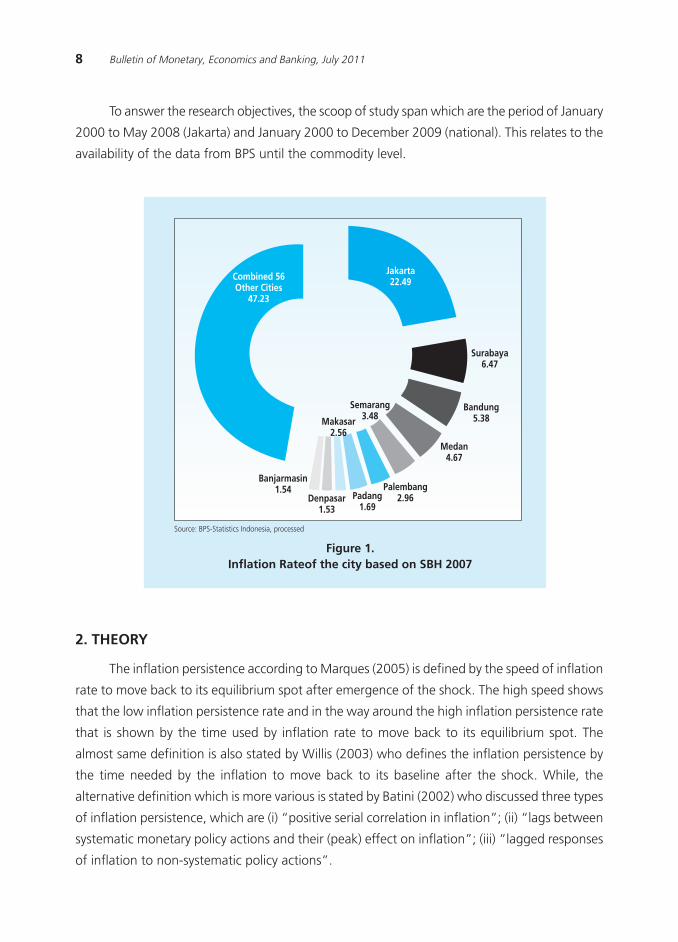

The choosing of Jakarta region is based on to its domination of national inflation rate

compared to the other regions in Indonesia. Despite there is the decreasing tendency,inflation

rate of Jakartacity is still the biggest among 66 cities that are measured by Living Cost Survey

(SBH). In 2007, it showed that the rateof Jakarta reached by 22.49% from national rate(Graphic

1), decreased from 27.66% based on SBH in 2002. The other reason is the movement of the

high volume of staple goods distribution in Jakarta.Next, the behavior of Jakarta inflation will

be compared with the national and 10 regions panel with the highest contribution of inflation

in Indonesia.

8 Bulletin of Monetary, Economics and Banking, July 2011

To answer the research objectives, the scoop of study span which are the period of January

2000 to May 2008 (Jakarta) and January 2000 to December 2009 (national). This relates to the

availability of the data from BPS until the commodity level.

Figure 1.Inflation Rateof the city based on SBH 2007

2. THEORY

The inflation persistence according to Marques (2005) is defined by the speed of inflation

rate to move back to its equilibrium spot after emergence of the shock. The high speed shows

that the low inflation persistence rate and in the way around the high inflation persistence rate

that is shown by the time used by inflation rate to move back to its equilibrium spot. The

almost same definition is also stated by Willis (2003) who defines the inflation persistence by

the time needed by the inflation to move back to its baseline after the shock. While, the

alternative definition which is more various is stated by Batini (2002) who discussed three types

of inflation persistence, which are (i) ≈positive serial correlation in inflation∆; (ii) ≈lags between

systematic monetary policy actions and their (peak) effect on inflation∆; (iii) ≈lagged responses

of inflation to non-systematic policy actions∆.

Combined 56Other Cities

47.23

Jakarta22.49

Surabaya6.47

Bandung5.38

Medan4.67

Semarang3.48

Palembang2.96

Makasar2.56

Denpasar1.53

Banjarmasin1.54

Padang1.69

Source: BPS-Statistics Indonesia, processed

9Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

The study about inflation persistence is important to increase the ability of inflation forecast,

retrieve the clarity of dynamic effect fromexogenous price shocks, gives information/direction

and fix the monetary policy, and in order to value whether the other monetary policy regime

will produce the different persistence, Stock (2004).

2.1 The Measurement of Inflation Persistence

In order to measure the inflation persistence rate, there are two approaches that can be

used,which are the univariate approach and multivariate model approach. The univariate

approach is only more stress to the time series data aspect,while the multivariate approach

also cover additional information such as real output and central bank interest rate (Dossche

and Everaert, 2005). From some studies that have been carried out, the univariate approach

by using autoregressive (AR) time series model constitutes the most common in empiric

research.

Some scalar measurement methods (univariate)that can be used to calculate the inflation

persistence such as (i) the sum of the autoregressive(AR) coefficients; (iii) the largest

autoregressive root; (iv) the half-life (Marques, 2005). With AR model, the inflation persistence

rate is measured from the range of its lag variable. Meanwhile LAR (the largestautoregressive

root) is generally explained by Levin and Piger (2004). In this method, inflation persistence is

acquired by finding the biggest square root, the equation of 1

0

KK K j

j

j

. While

thehalf-life method is adopted especially for evaluating deviation persistence frompurchasing

power parity equilibrium (Marques 2004). As described by Andrews and Chen (1994), the

half-life formula is T

n1 , where n is the amount of some inflations above 0.5 when the

big disturbance occurred as much as 1 unit and T is the amount of observation period.

Despite there are some concepts of different inflation persistence period measurement rate,

the estimation result acquired is not far different generally. (Clark, 2003).

The research focus in the inflation process enables the use of univariate model in this

paper. However, univariate model cannot be separated from some limitations; one of them is

that this model cannot identify the cause source of the observed persistenceof inflationso that

there is the probability of inflation process potential trigger to be ignored.

Marques (2004) stated that the AR model is a good inflation persistence measurer, and is

also directly related to the coefficient of mean reversion as the alternative of inflation persistence

rate measurement. The ARformula AR with order of p can be describedas follows:

10 Bulletin of Monetary, Economics and Banking, July 2011

From the result of the equation estimation, the inflation persistence rate is calculated by

adding AR coefficient, 1

K

j

j

.

The way to calculate the coefficient is the best persistence scalar measurement way

according to Andrews and Chen (1994). Inflation persistence is high if today inflation rate is

influenced by the value of its lag, so that the coefficient is close to 1. In this case, the inflation

can be said closed to the unit root process.

To retrieve the result of estimation, in every inflation series needs to be determined the

amount of proper lag variable dependent. In its determination, Akaike Information Criterion

(AIC) or Schwarz» Bayesian Information Criterion (SBIC) can be used.As stated by Levin and

Piger (2004), in measuring the persistence by using AR model, the equivalent equation as

follows needs also to be considered:

Where the dynamic parameter φj is a simple transformation from AR coefficient from the

equation (1) constitutes simple transformation from AR coefficient from equation (1).

Specifically, persistence concept is much related to the Impulse Response Function (IRF)

from the process of AR (ρ). Marques (2004) described the weakness and the strength of each

(1)

: Monthly inflation rateat the time of t

: The constant from the result of estimation process as control toward inflation Average

: The amount of AR Coefficient

: Random error term or residual from equation regression above

(2)

t

1

K

j

j

t

11Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

persistence measurement methods. The Cumulative Impulse Response Function (CIRF) concept

which is formulated as

1

1CIRF describes the monotonic correlation between CIRF and

the AR coefficient (ρ), so that the calculation is very dependent on the AR coefficient. The other

weakness of CIRF and ρ in measuring the inflation persistence is if there are 2 (two) of data

series, and both of the method cannot tell the different between the series that was highly

increased and then followed by the gradual decrease with the series that the increase was low

and then followed by the low high decrease in its IRF. Separated fromthe limitation that becomes

the weakness of univariate method, this scalar measurement methodmust be seen as the method

for estimating the inflation average speed to move back to its equilibrium after the emergence

of the shock.This scalar is considered more effective if the speed of inflation series convergence

is more uniformed.

Some critics toward the half-lifemethod in inflation persistence rate calculation have

been also explained in the previous research. If IRF is oscillating, this method will produce too

low inflation process persistence. Besides, if the inflation process is very persistent, the output

ofthe half-lifeis very high so it will be difficult to differentiate the change of persistence as the

time goes by. However this method is usually preferred because more understanding for its

measurement in time unit. Because of the limitation, some writers do thehalf-lifecalculation

directly from IRF. Meanwhile the critic towards thelargest autoregressive roothas ever been

stated by (2004). The persistence measurement by using this method is considered not good

since its function depends on the other root, not only from the biggest root. However the

advantage of this method is the easiness in calculating asymptotically valid confidence intervals

for its estimation result.

The calculation result of inflation persistence degree by using AR model estimated by

using OLS can be compared with the bootstrap estimation result. This is also useful to

anticipate of the probability of invalid measurement if the persistence degree closes to the

number of 1, so that the robustness check is important to be carried out. This procedure

has been used in some previous research, such as: O»Reilly and Whelan (2004) and Alamsyah

(2008).

In order to complete the observation toward inflation behavior change, rolling regression

method can be used to see whether the inflation process is changing as the time goes by, by

seeing the evolution from the AR coefficient. This method has been done also in some previous

research such as:Pivetta & Reis (2006), Debelle and Wilkinson (2002), O»Reilly and Whelan

(2004) and Alamsyah (2008). It is generally can be summarized that the estimation result of

12 Bulletin of Monetary, Economics and Banking, July 2011

inflation persistence degree by using the method showed the change of inflation process in

countries that became sample of object occurred. Nevertheless, this method has also the

weakness because not accurately showed the change of inflation persistence rate, so that the

factors influences such as monetary policy cannot be caught clearly.

In doing analysis toward inflation persistence degree, it is also need to be considered the

existence of structural breaks. Some literatures stated that the estimation of inflation persistence

rate will be exaggeratedif the existence of the inflation average value of structural break is not

calculated. Some techniques such as Andrew and Quandt test or Chow test can be carried out

to do the test toward the existence of structural break.

In order to measure of how long does the inflation take to absorb 50% of shockoccurred

before moving back to its average value, formula can be used (Gujarati, 2003) with simple

formula

1

h . Where h is the time needed by inflation to absorb the 50% of shock

occurred before moving back to its average value and ρ is the estimation result of inflation

persistence degree.

Some studies related to the inflation persistence have been done in Indonesia, such as by

Alamsyah (2008), Yanuarti (2007), Bank Indonesia inflation team (2006). Whole the research

were more stressed on the national inflation persistence and limited to general inflation

persistence and commodity group. Generally it is found that the inflation persistence degree in

Indonesia is relatively high in the observation period, though there is decreasing tendency in

the crisis aftermath period in 1997/1998. Nevertheless, there has not been a study about the

inflation persistence in regional level and covers until commodity level.

The study that has been done by Alamsyah (2008) is for seeing the inflation behavior

change in Indonesia at the time of before and after crisis, and also for seeing the cause sourceof

inflation persistence especially from the micro businessmen approached by using NKPC hybrid

model. By using univariate approach which is the sum of autoregressive coefficient (AR (1)) it is

found that the persistence degree in Indonesia is relatively high at the observation period of

1985-2007. Nevertheless, the persistence degree tends to be decreasing at the time of after

economic crisis.It is also founded that the inflation in Indonesia constitutes the combination of

backward and forward lookingbehavior. Therefore, the effort to stabilize the inflation

expectationto the target set by central bank, needs to control the inflation and increase the

monetary policy credibility in Indonesia.

Meanwhile, the study by Yanuarti (2007) was purposed to measure the inflation persistence

degree in Indonesia and also to research whether there is the change of inflation persistence

13Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

degree change in span of 1990-2006. By using gull sample, it is found that the inflation

persistence degree in Indonesia is very high; however tends to decrease at the time of after

crisis. Thesefindings are in line with Alamsyah findings (2008).

2.2 The Cause of Inflation Persistence

Inflation pressure source can be seen through the equation of New Keynesian Philips

Curve (NKPC), where the cause of inflation persistence can be seen by the inflation forward

looking) and (backward looking)behavior. This approach is the innovation of the inflation initial

model that describes the inflation dynamic as written in NKPC:

Next, according to Gali and Gertler (1999), beside forward looking oriented, inflation has

also backward lookingbehavior both of the behaviors described from the NKPC Hybrid model

that catch the inflation persistence characteristic.

The inflation structural equation that is usually called as New Keynesian Phillips Curvehybrid

consisted in this equation below (Angeloni et. al, 2004):

Where πt is inflation at the time of t; E

t (π

t +1) is the inflation expectation at the time of t+1

with informal condition at the time of t, µt is output gap and ξ

t is exogenous shock

substance.

By seeing the right side of the equation, it can be estimated that the four of inflation

sources : (i) extrinsic persistence that relates to the persistence of marginal cost or output gap.;

(ii) intrinsic persistence that relates to the inflation dependency toward the previous period

inflation (backward looking expectation); (iii) expectations-based persistence that relates to the

inflation expectation form that is based on to the forward looking; (iv) error term persistence

because of the inflation shock occurred.

1 tttt Ey

14 Bulletin of Monetary, Economics and Banking, July 2011

III. METHODOLOGY

3.1 Estimation Technique

Inflation persistence estimation is done by seeing univariate autoregressive (AR) time

series model process as Marques (2004) stated since the AR model is the measurer of good

inflation persistenceand also directly related to the mean reversion as alternative of inflation

persistence rate measurement. AR formula with the order p can be broken down as follows:

(3)

: Monthly inflation rate at the time of t

: The constant of estimation result, as control of average inflation

: The total of AR coefficient

: Random error term or residual from equation regression above

The inflation persistence rate is calculated by adding AR coefficient .

The inflation persistence can be said high if today inflation rate is very influenced by its lag

persistence, so that the coefficient is close to 1.in this case, inflation can be said close to

the unit root process.

For, estimation, the determination of the amount of dependent variable lagwhich is

according to theAkaike Information Criterion (AIC) and or Schwarz» Bayesian Information

Criterion (SBIC). In order to see the result of robustness obtained, and also bootstrap and

rolling regression procedure is conducted. Structural break test is carried out by applying the

technic such as Quandt (1960) and Chow test to do the test toward known and unknown

break to measure of how long does the inflation take to absorb 50% of shock that is occurred

before moving to its average value, the formula is:

In this paper, the cause of inflation persistence can be seen based on the inflation behavior

forward lookingand backward looking of the inflation behavior as follows:

t

1

K

j

j

t

15Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

Where πt is the inflation at the time of t; E

t (π

t +1) is an inflation expectation at the time of t+1

with information condition at the time of t, µt is the output gap and ξ

t is a exogenous shock

substance. The significant variable and has big coefficient is the variable that becomes the main

source of inflation pressure. Embarking from the analysis about the source of the inflation

pressure, and in order to see the inflation persistence source, more analysis is done.

In the analysis of the source of inflation persistence, the inflation is only focused on o the

5 commodities that has the highest of inflation persistence degree. The five commodities are

the most important commodities in controlling inflation. In order to analyze the source of

inflation persistence,anecdotal informationandanalysis are used and also the study that has

been done related to the commodities. The information collected such as about the market

structure and the commodity inflation characteristic.

3.2 Data

The data that will be used in this inflation persistence analysis are:

1. Monthly inflation (year-on-year), measured by using Consumer Price Index of the total of all

city in Indonesia (National inflation) and IHK of Jakarta city, also IHK 9 of other regions that

have the biggest rate toward national inflation. While the date used the year base 2002.

The IHK can be explained in detail in to 7 (seven) commodity groups : (i) Foodstuff, (ii) Food,

Baverages and Tobaccos, (iii) Estate, (iv) Clothes, (v) Health, (vi) Education, Recreation and

Sports, and (vii)Transportation and Communication.The sample span was started since January

2000 - May 2008 (December 2009 for national). The source of CPI data is retrieved from the

Statistic Center Bureau and International Financial Statistics (IFS).

2. The annual inflation target(source: Bank Indonesia)

The use of the year on year inflation data especially is because some reasons as stated by

Babecky (2008) as follows:

1. The use of month-to-month (m-t-m) inflation data or quarter-to-quarter (q-t-q) is very related

to the seasonal factor so that it is worried that it does not represent the real inflation

persistence

2. The both of inflation size m-t-m and q-t-q size are not monitored by certain economic

agent.

16 Bulletin of Monetary, Economics and Banking, July 2011

3. Central bank in determining the inflation target is more based on the annual inflation change

(y-o-y).

4. RESULT AND ANALYSIS

4.1 The development of Jakarta Inflation

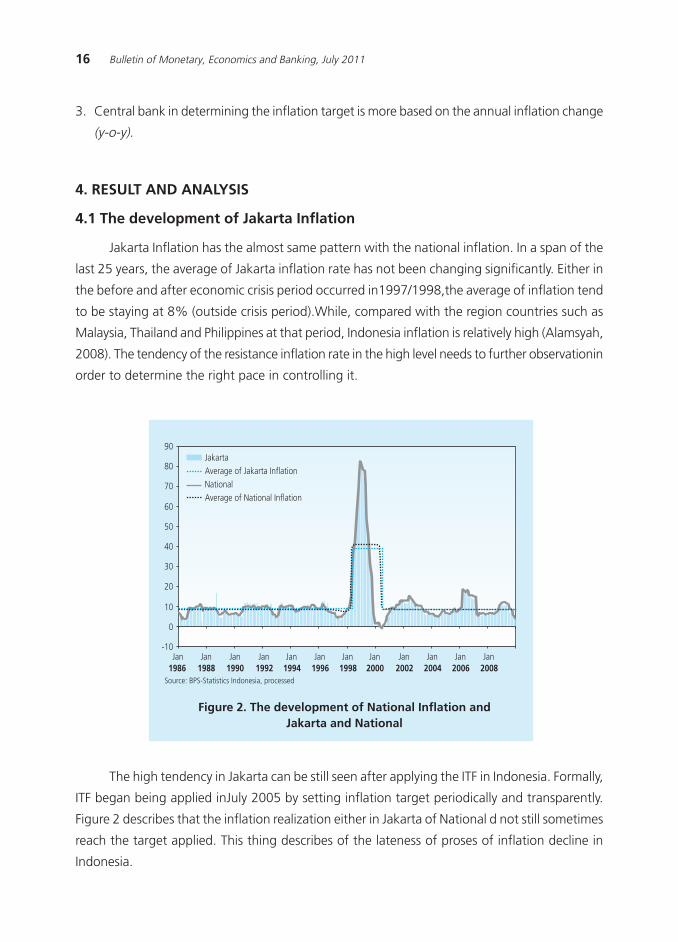

Jakarta Inflation has the almost same pattern with the national inflation. In a span of the

last 25 years, the average of Jakarta inflation rate has not been changing significantly. Either in

the before and after economic crisis period occurred in1997/1998,the average of inflation tend

to be staying at 8% (outside crisis period).While, compared with the region countries such as

Malaysia, Thailand and Philippines at that period, Indonesia inflation is relatively high (Alamsyah,

2008). The tendency of the resistance inflation rate in the high level needs to further observationin

order to determine the right pace in controlling it.

Figure 2. The development of National Inflation andJakarta and National

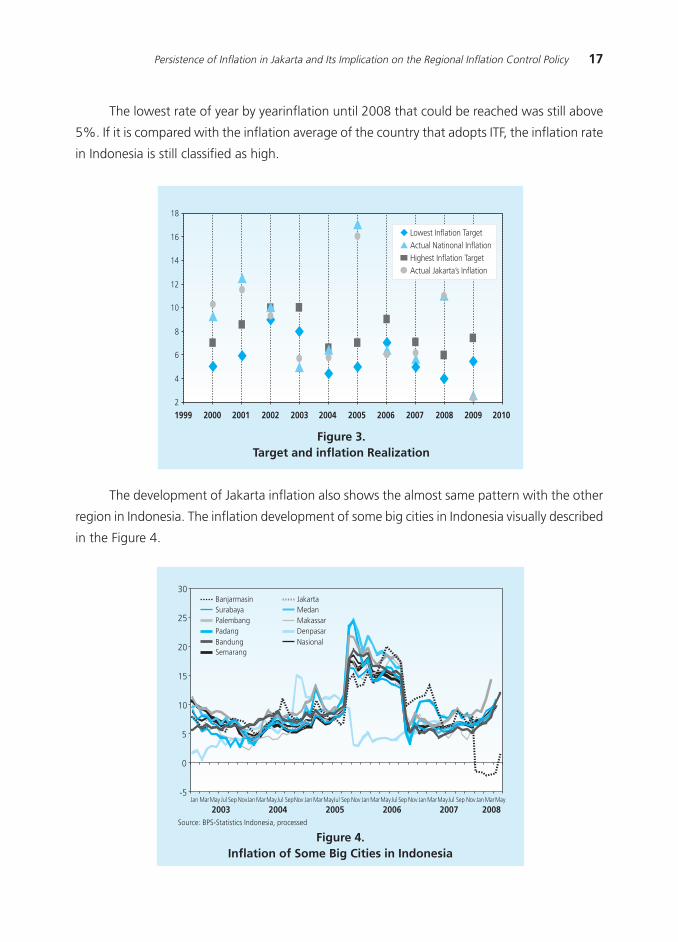

The high tendency in Jakarta can be still seen after applying the ITF in Indonesia. Formally,

ITF began being applied inJuly 2005 by setting inflation target periodically and transparently.

Figure 2 describes that the inflation realization either in Jakarta of National d not still sometimes

reach the target applied. This thing describes of the lateness of proses of inflation decline in

Indonesia.

-10

0

10

20

30

40

50

60

70

80

90Jakarta

NationalAverage of Jakarta Inflation

Average of National Inflation

Jan1986

Jan1988

Jan1990

Jan1992

Jan1994

Jan1996

Jan1998

Jan2000

Jan2002

Jan2004

Jan2006

Jan2008

Source: BPS-Statistics Indonesia, processed

17Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

The lowest rate of year by yearinflation until 2008 that could be reached was still above

5%. If it is compared with the inflation average of the country that adopts ITF, the inflation rate

in Indonesia is still classified as high.

Figure 3.Target and inflation Realization

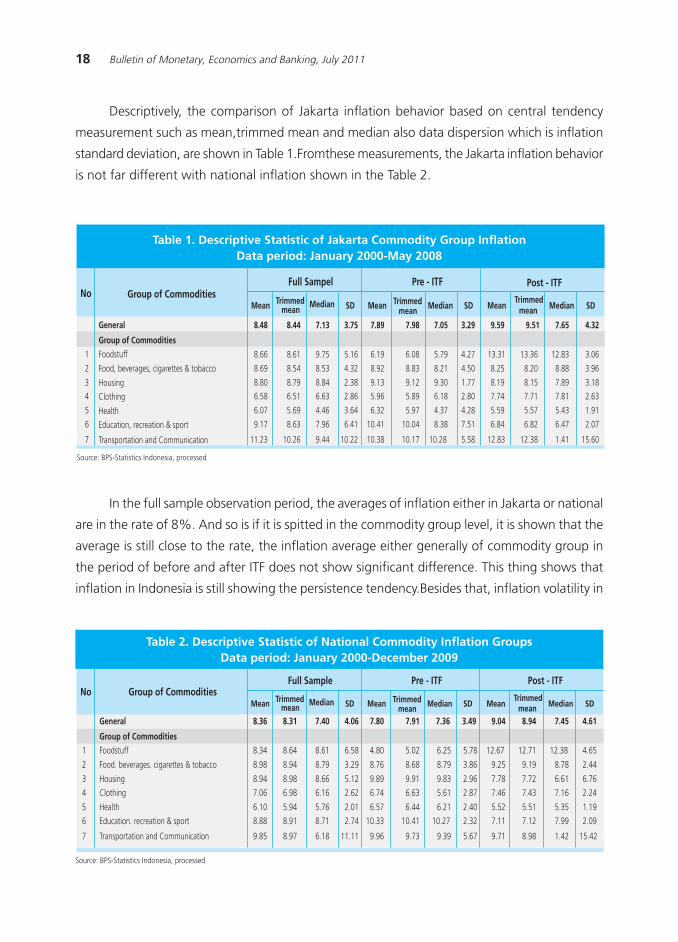

The development of Jakarta inflation also shows the almost same pattern with the other

region in Indonesia. The inflation development of some big cities in Indonesia visually described

in the Figure 4.

Figure 4.Inflation of Some Big Cities in Indonesia

-5

0

5

10

15

20

25

30BanjarmasinSurabayaPalembangPadangBandungSemarang

JakartaMedanMakassarDenpasarNasional

2003 2004 2005 2006 2007 2008Jan MarMay Jul Sep NovJan MarMayJul SepNov Jan MarMayJul Sep Nov Jan MarMayJul Sep Nov Jan MarMayJul Sep Nov Jan MarMay

Source: BPS-Statistics Indonesia, processed

18

16

14

12

10

8

6

4

2

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Lowest Inflation Target

Highest Inflation TargetActual Natinonal Inflation

Actual Jakarta»s Inflation

18 Bulletin of Monetary, Economics and Banking, July 2011

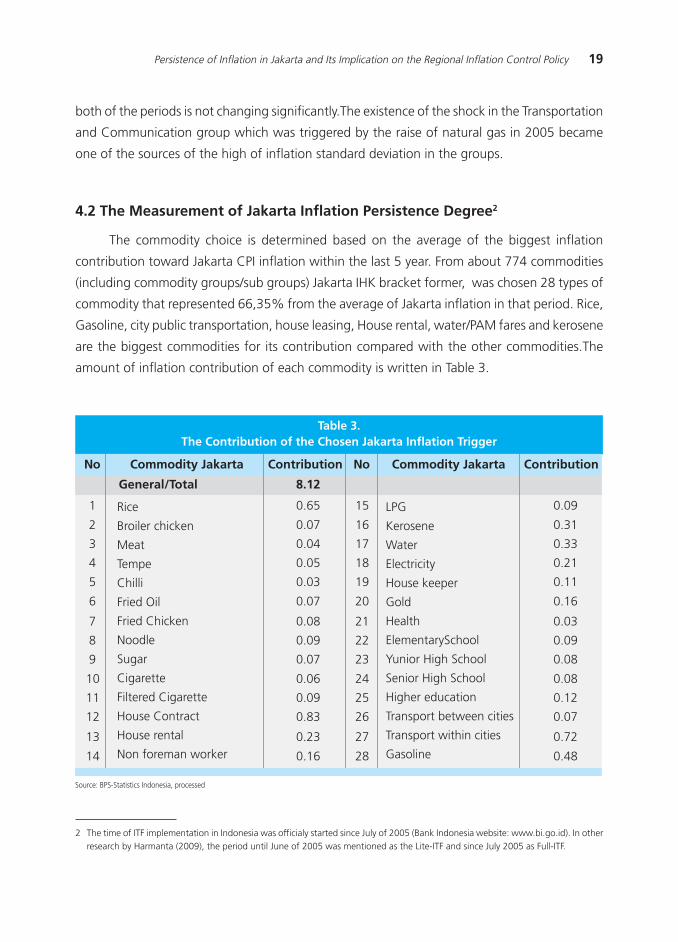

Descriptively, the comparison of Jakarta inflation behavior based on central tendency

measurement such as mean,trimmed mean and median also data dispersion which is inflation

standard deviation, are shown in Table 1.Fromthese measurements, the Jakarta inflation behavior

is not far different with national inflation shown in the Table 2.

In the full sample observation period, the averages of inflation either in Jakarta or national

are in the rate of 8%. And so is if it is spitted in the commodity group level, it is shown that the

average is still close to the rate, the inflation average either generally of commodity group in

the period of before and after ITF does not show significant difference. This thing shows that

inflation in Indonesia is still showing the persistence tendency.Besides that, inflation volatility in

Table 1. Descriptive Statistic of Jakarta Commodity Group InflationData period: January 2000-May 2008

Source: BPS-Statistics Indonesia, processed

Mean Trimmedmean

Median SD Mean Trimmedmean Median SD Mean

Trimmedmean Median SD

8.48 8.44 7.13 3.75 7.89 7.98 7.05 3.29 9.59 9.51 7.65 4.32

1 8.66 8.61 9.75 5.16 6.19 6.08 5.79 4.27 13.31 13.36 12.83 3.06

2 8.69 8.54 8.53 4.32 8.92 8.83 8.21 4.50 8.25 8.20 8.88 3.96

3 8.80 8.79 8.84 2.38 9.13 9.12 9.30 1.77 8.19 8.15 7.89 3.18

4 6.58 6.51 6.63 2.86 5.96 5.89 6.18 2.80 7.74 7.71 7.81 2.63

5 6.07 5.69 4.46 3.64 6.32 5.97 4.37 4.28 5.59 5.57 5.43 1.91

6 9.17 8.63 7.96 6.41 10.41 10.04 8.38 7.51 6.84 6.82 6.47 2.07

7 11.23 10.26 9.44 10.22 10.38 10.17 10.28 5.58 12.83 12.38 1.41 15.60

Pre - ITFNo

Full Sampel Post - ITFGroup of Commodities

General

Group of Commodities

Foodstuff

Food, beverages, cigarettes & tobacco

Housing

Clothing

Health

Education, recreation & sport

Transportation and Communication

Mean Trimmedmean

Median SD Mean Trimmedmean Median SD Mean

Trimmedmean Median SD

Pre - ITF Post - ITFNo Group of Commodities

Full Sample

General 8.36 8.31 7.40 4.06 7.80 7.91 7.36 3.49 9.04 8.94 7.45 4.61

Group of Commodities

1 Foodstuff 8.34 8.64 8.61 6.58 4.80 5.02 6.25 5.78 12.67 12.71 12.38 4.65

2 Food. beverages. cigarettes & tobacco 8.98 8.94 8.79 3.29 8.76 8.68 8.79 3.86 9.25 9.19 8.78 2.44

3 Housing 8.94 8.98 8.66 5.12 9.89 9.91 9.83 2.96 7.78 7.72 6.61 6.76

4 Clothing 7.06 6.98 6.16 2.62 6.74 6.63 5.61 2.87 7.46 7.43 7.16 2.24

5 Health 6.10 5.94 5.76 2.01 6.57 6.44 6.21 2.40 5.52 5.51 5.35 1.19

6 Education. recreation & sport 8.88 8.91 8.71 2.74 10.33 10.41 10.27 2.32 7.11 7.12 7.99 2.09

7 Transportation and Communication 9.85 8.97 6.18 11.11 9.96 9.73 9.39 5.67 9.71 8.98 1.42 15.42

Table 2. Descriptive Statistic of National Commodity Inflation GroupsData period: January 2000-December 2009

Source: BPS-Statistics Indonesia, processed

19Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

both of the periods is not changing significantly.The existence of the shock in the Transportation

and Communication group which was triggered by the raise of natural gas in 2005 became

one of the sources of the high of inflation standard deviation in the groups.

4.2 The Measurement of Jakarta Inflation Persistence Degree2

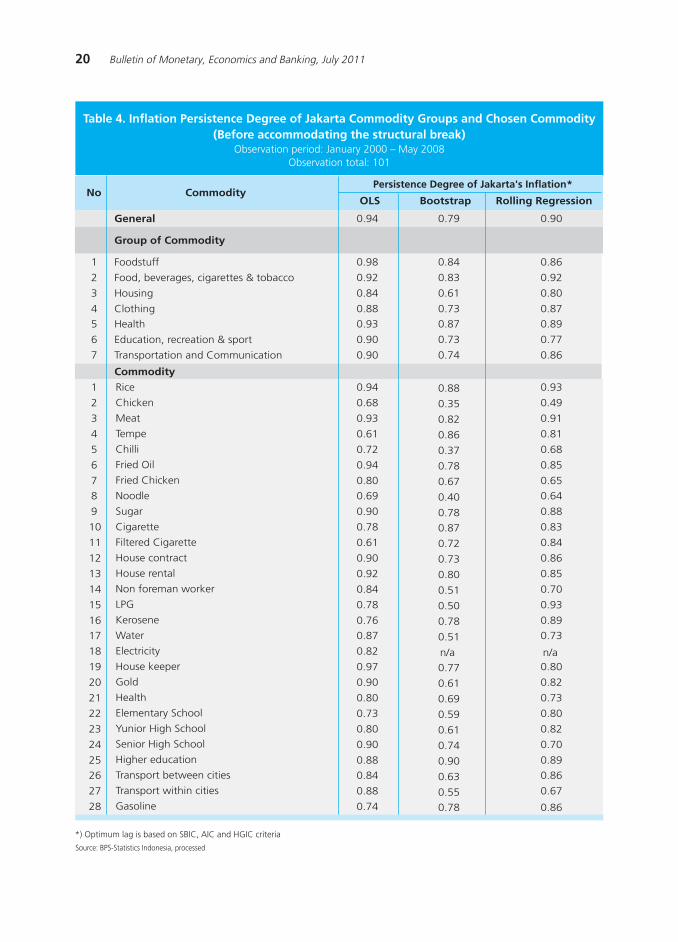

The commodity choice is determined based on the average of the biggest inflation

contribution toward Jakarta CPI inflation within the last 5 year. From about 774 commodities

(including commodity groups/sub groups) Jakarta IHK bracket former, was chosen 28 types of

commodity that represented 66,35% from the average of Jakarta inflation in that period. Rice,

Gasoline, city public transportation, house leasing, House rental, water/PAM fares and kerosene

are the biggest commodities for its contribution compared with the other commodities.The

amount of inflation contribution of each commodity is written in Table 3.

2 The time of ITF implementation in Indonesia was officialy started since July of 2005 (Bank Indonesia website: www.bi.go.id). In otherresearch by Harmanta (2009), the period until June of 2005 was mentioned as the Lite-ITF and since July 2005 as Full-ITF.

Table 3.The Contribution of the Chosen Jakarta Inflation Trigger

Source: BPS-Statistics Indonesia, processed

No Commodity Jakarta Contribution No

General/Total 8.12

1 0.65 15 0.09

2 0.07 16 0.31

3 0.04 17 0.33

4 0.05 18 0.21

5 0.03 19 0.11

6 0.07 20 0.16

7 0.08 21 0.03

8 0.09 22 0.09

9 0.07 23 0.08

10 0.06 24 0.08

11 0.09 25 0.12

12 0.83 26 0.07

13 0.23 27 0.72

14 0.16 28 0.48

Commodity Jakarta Contribution

Rice

Broiler chicken

Meat

Tempe

Chilli

Fried Oil

Fried Chicken

Noodle

Sugar

Cigarette

Filtered Cigarette

House Contract

House rental

Non foreman worker

LPG

Kerosene

Water

Electricity

House keeper

Gold

Health

ElementarySchool

Yunior High School

Senior High School

Higher education

Transport between cities

Transport within cities

Gasoline

20 Bulletin of Monetary, Economics and Banking, July 2011

Table 4. Inflation Persistence Degree of Jakarta Commodity Groups and Chosen Commodity(Before accommodating the structural break)

Observation period: January 2000 √ May 2008Observation total: 101

OLS Bootstrap Rolling Regression

General 0.94 0.79 0.90

Group of Commodity

1 Foodstuff 0.98 0.84 0.86

2 Food, beverages, cigarettes & tobacco 0.92 0.83 0.92

3 Housing 0.84 0.61 0.80

4 Clothing 0.88 0.73 0.87

5 Health 0.93 0.87 0.89

6 Education, recreation & sport 0.90 0.73 0.77

7 Transportation and Communication 0.90 0.74 0.86

Commodity

1 0.94 0.88 0.93

2 0.68 0.35 0.49

3 0.93 0.82 0.91

4 0.61 0.86 0.81

5 0.72 0.37 0.68

6 0.94 0.78 0.85

7 0.80 0.67 0.65

8 0.69 0.40 0.64

9 0.90 0.78 0.88

10 0.78 0.87 0.83

11 0.61 0.72 0.84

12 0.90 0.73 0.86

13 0.92 0.80 0.85

14 0.84 0.51 0.70

15 0.78 0.50 0.93

16 0.76 0.78 0.89

17 0.87 0.51 0.73

18 0.82 n/a n/a19 0.97 0.77 0.80

20 0.90 0.61 0.82

21 0.80 0.69 0.73

22 0.73 0.59 0.80

23 0.80 0.61 0.82

24 0.90 0.74 0.70

25 0.88 0.90 0.89

26 0.84 0.63 0.86

27 0.88 0.55 0.67

28 0.74 0.78 0.86

*) Optimum lag is based on SBIC, AIC and HGIC criteria

Persistence Degree of Jakarta's Inflation*No Commodity

Rice

Chicken

Meat

Tempe

Chilli

Fried Oil

Fried Chicken

Noodle

Sugar

Cigarette

Filtered Cigarette

House contract

House rental

Non foreman worker

LPG

Kerosene

Water

Electricity

House keeper

Gold

Health

Elementary School

Yunior High School

Senior High School

Higher education

Transport between cities

Transport within cities

Gasoline

Source: BPS-Statistics Indonesia, processed

21Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

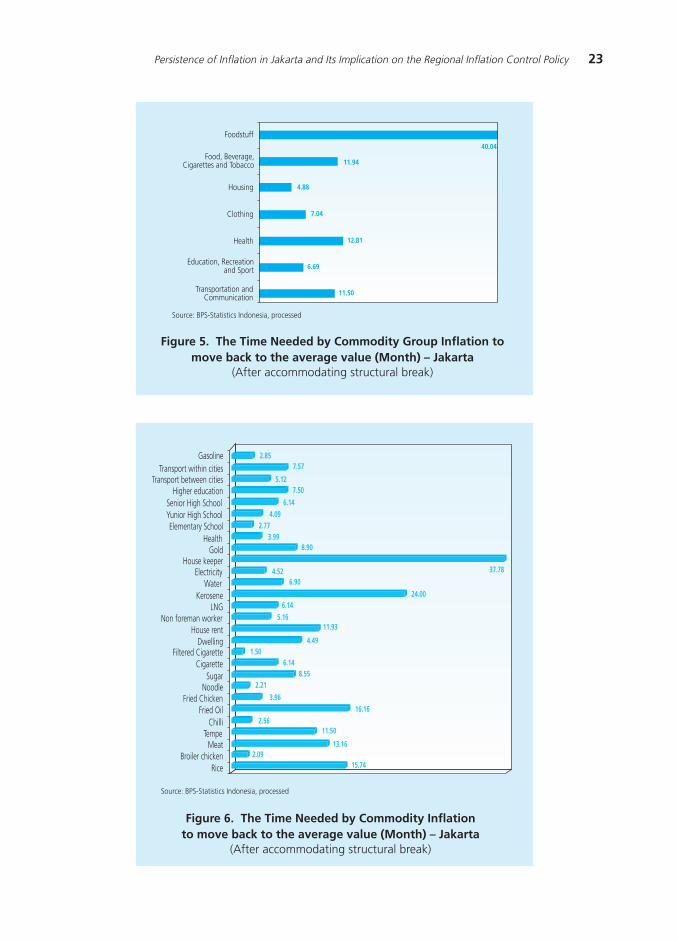

Beside the measurement of inflation persistence degree for major inflation contributor

commoditiesin Jakarta, we also conduct the measurement of CPI inflation persistence rate

based on to its disaggregation, which is broken into core inflation, volatile food inflation and

administered price inflation.

The estimation result of inflation persistence degree in Jakarta across commodity group

and commodityis provided in the Table 4. The inflation persistence degree is obtained by adding

the entire AR coefficient according to the inflation optimum lag of each commodity, or commodity

group. The determination of optimum lag is done by using the AIC/HQIC/SBIC criteria.The

Jakarta inflation persistence degree measurement by using 3 different techniques that shows

similar result, even though the OLS with rolling regression techniques shows closer estimation

result than the OLS with bootstrap.

By using the full sample, the result of Jakarta persistence degree estimation generally

shows that the Jakarta CPI inflation is still very persistent.This isin line with the national inflation

persistence in the same observation period which also showsthe high persistent degree3. From

7 commodity groups, almost all of them show the high inflation persistence degree. Only

housing/Estate group has lower inflation persistence rate than other group.

The estimation result also shows that the inflation persistence of Foodstuff, which is

greatly influenced by the supply and the distribution shock, is still high. While, the commodity

group with the biggest inflation persistence and consistent across the three approaches in the

Table 4 are processed processed food - drinks - cigarettes and tobacco, and Health group.

Across commodity level, Rice, Beef, Cooking Oil, Sugar, House contract and House rental are

commodities with the highest inflation persistence among others.

The high of the inflation persistence degree is probably related to the shock that

greatly influence the inflation in Indonesia. Therefore, it is necessary to conduct a test to

see whether there is structural breakin inflation data. Quandt-Andrews testis carried out

on inflation series to see whether there is structural breakalong observation period.Based

on the test, there is structural break in general inflation and in some commodities (House

group, education group, recreation & sport, and Transportation and Communication group)

and also commodity of (tempe, cigarette, cigarette filter, LPG/liquid gas, kerosene and

SLTA), see Table 5.

After adjusting for the structural break on Jakarta inflation data, the inflation persistence

degree shows a little different. Some commodities showa decrease of inflation persistence,

3 As shown in the result of national inflation persistence degree measurement which is provided in Table 4.

22 Bulletin of Monetary, Economics and Banking, July 2011

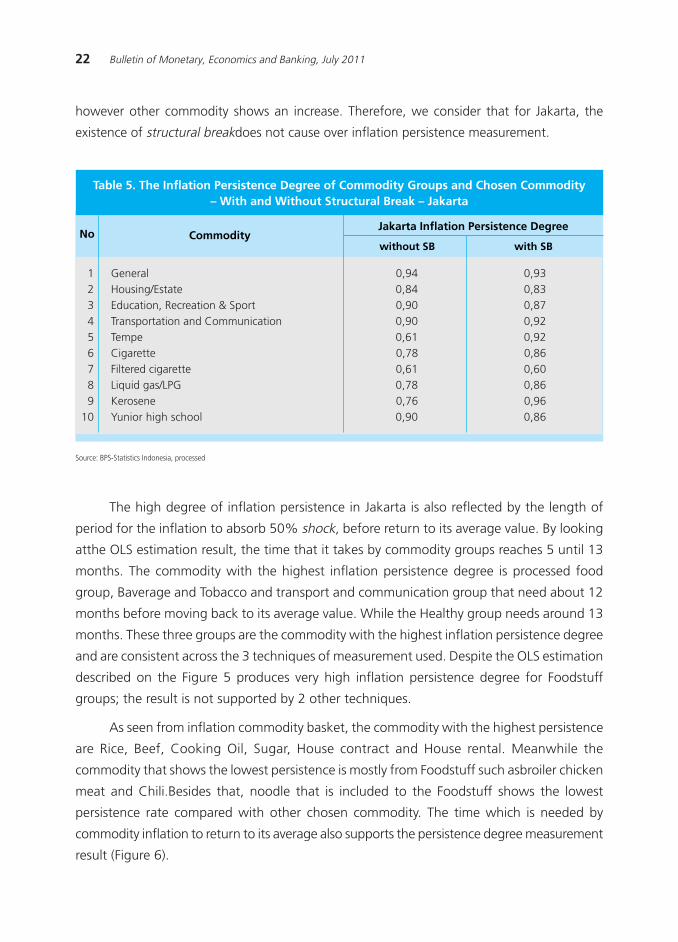

The high degree of inflation persistence in Jakarta is also reflected by the length of

period for the inflation to absorb 50% shock, before return to its average value. By looking

atthe OLS estimation result, the time that it takes by commodity groups reaches 5 until 13

months. The commodity with the highest inflation persistence degree is processed food

group, Baverage and Tobacco and transport and communication group that need about 12

months before moving back to its average value. While the Healthy group needs around 13

months. These three groups are the commodity with the highest inflation persistence degree

and are consistent across the 3 techniques of measurement used. Despite the OLS estimation

described on the Figure 5 produces very high inflation persistence degree for Foodstuff

groups; the result is not supported by 2 other techniques.

As seen from inflation commodity basket, the commodity with the highest persistence

are Rice, Beef, Cooking Oil, Sugar, House contract and House rental. Meanwhile the

commodity that shows the lowest persistence is mostly from Foodstuff such asbroiler chicken

meat and Chili.Besides that, noodle that is included to the Foodstuff shows the lowest

persistence rate compared with other chosen commodity. The time which is needed by

commodity inflation to return to its average also supports the persistence degree measurement

result (Figure 6).

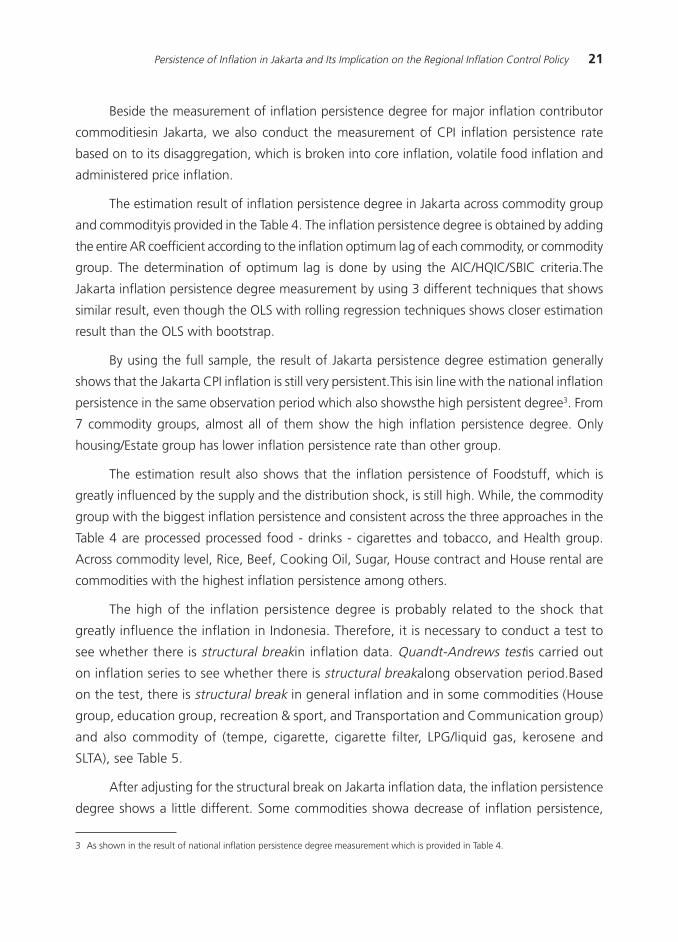

Table 5. The Inflation Persistence Degree of Commodity Groups and Chosen Commodity√ With and Without Structural Break √ Jakarta

NoJakarta Inflation Persistence Degree

1 General 0,94 0,932 Housing/Estate 0,84 0,833 Education, Recreation & Sport 0,90 0,874 Transportation and Communication 0,90 0,925 Tempe 0,61 0,926 Cigarette 0,78 0,867 Filtered cigarette 0,61 0,608 Liquid gas/LPG 0,78 0,869 Kerosene 0,76 0,96

10 Yunior high school 0,90 0,86

Commodity

Source: BPS-Statistics Indonesia, processed

without SB with SB

however other commodity shows an increase. Therefore, we consider that for Jakarta, the

existence of structural breakdoes not cause over inflation persistence measurement.

23Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

Figure 5. The Time Needed by Commodity Group Inflation tomove back to the average value (Month) √ Jakarta

(After accommodating structural break)

Figure 6. The Time Needed by Commodity Inflationto move back to the average value (Month) √ Jakarta

(After accommodating structural break)

11.94

40.04

4.88

7.04

12.81

6.69

11.50

Foodstuff

Food, Beverage,Cigarettes and Tobacco

Housing

Clothing

Health

Education, Recreationand Sport

Transportation andCommunication

Source: BPS-Statistics Indonesia, processed

2.857.57

5.127.50

6.144.09

2.773.99

8.90

4.526.90

6.145.16

11.93

4.491.50

6.148.55

2.21

3.96

2.56

2.0915.74

13.16

11.50

16.16

24.00

37.78

GasolineTransport within cities

Transport between citiesHigher education

Senior High SchoolYunior High SchoolElementary School

HealthGold

House keeperElectricity

WaterKerosene

LNGNon foreman worker

House rentDwelling

Filtered CigaretteCigarette

SugarNoodle

Fried ChickenFried Oil

ChilliTempe

MeatBroiler chicken

Rice

Source: BPS-Statistics Indonesia, processed

24 Bulletin of Monetary, Economics and Banking, July 2011

OLS Bootstrap Rolling Regression

Persistence Degree of Jakarta's Inflation*No Commodities

1 CPI Inflation 0.89 0.74 0.91

2 Core Inflation 0.88 0.69 0.89

3 Administered Prices Inflation 0.89 0.72 0.89

4 Volatile Food Inflation 0.92 0.81 0.86

*) Optimum lag is based on SBIC, AIC and HGIC criteria

As seen based on the disaggregation, Jakarta inflation is broken into core inflation,

administered price, and volatile food inflation. Table 6 writes the estimation result of Jakarta

inflation persistence degree by using 3 techniques; those are OLS, bootstrap and rolling

regression. The three inflations types are still very persistent in the observation period, as seen

from inflation persistence degree that is still high (0.88 - 0.92), so that in order to return to its

average will require between 7-12 months (Figure 7).

Figure 7.The time to move back to the average (month)

√ Jakarta Inflation

Table 6. Inflation Persistence Degree Based on Inflation Disaggregation √ JakartaMonthly inflation (y-o-y) in the period of Jan 2003 - Mar 2008

Source: BPS-Statistics Indonesia, processed

8.28

7.13

7.74

11.98

CPI Inflation

Core Inflation

Administered Prices Inflation

Volatile Food Inflation

Source: BPS-Statistics Indonesia, processed

25Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

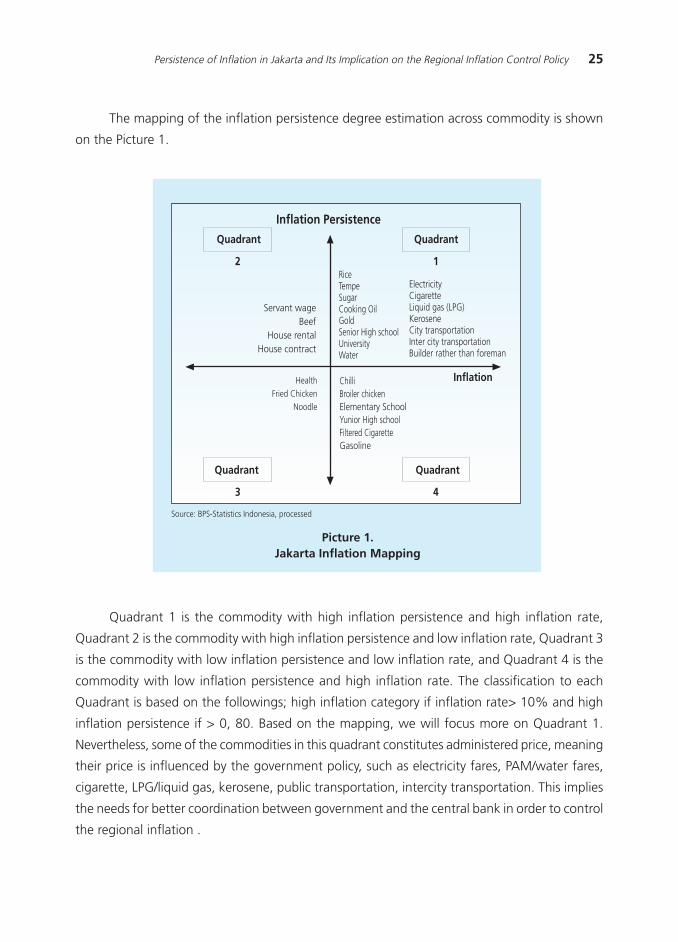

The mapping of the inflation persistence degree estimation across commodity is shown

on the Picture 1.

Picture 1.Jakarta Inflation Mapping

Quadrant 1 is the commodity with high inflation persistence and high inflation rate,

Quadrant 2 is the commodity with high inflation persistence and low inflation rate, Quadrant 3

is the commodity with low inflation persistence and low inflation rate, and Quadrant 4 is the

commodity with low inflation persistence and high inflation rate. The classification to each

Quadrant is based on the followings; high inflation category if inflation rate> 10% and high

inflation persistence if > 0, 80. Based on the mapping, we will focus more on Quadrant 1.

Nevertheless, some of the commodities in this quadrant constitutes administered price, meaning

their price is influenced by the government policy, such as electricity fares, PAM/water fares,

cigarette, LPG/liquid gas, kerosene, public transportation, intercity transportation. This implies

the needs for better coordination between government and the central bank in order to control

the regional inflation .

Quadrant

2

Inflation Persistence

Quadrant

1

Quadrant

3

Quadrant

4

Inflation

Servant wageBeef

House rentalHouse contract

HealthFried Chicken

Noodle

RiceTempeSugarCooking OilGoldSenior High schoolUniversityWater

ElectricityCigaretteLiquid gas (LPG)KeroseneCity transportationInter city transportationBuilder rather than foreman

ChilliBroiler chickenElementary SchoolYunior High schoolFiltered CigaretteGasoline

Source: BPS-Statistics Indonesia, processed

26 Bulletin of Monetary, Economics and Banking, July 2011

NKPC2SLS RegressionSample : 2000Q1 - 2009Q4Number of Observation : 37Dependent Variable : Inflation

Variable Independent Parameter Coeficient

L1.Inflation 0.46***(0.08)

F.Inflation 0.54***(0.08)

Outputgap 0.180.22

Constant 0.07(0.25)

R-squared 0.79

Instrument Variables : L2.Inflation Growth of Oil Prices

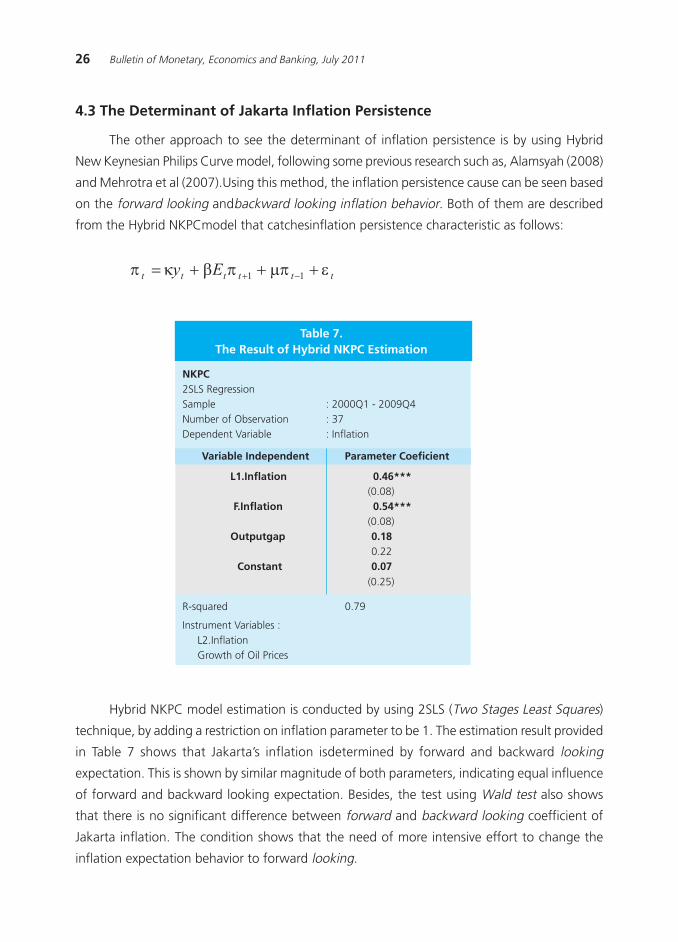

4.3 The Determinant of Jakarta Inflation Persistence

The other approach to see the determinant of inflation persistence is by using Hybrid

New Keynesian Philips Curve model, following some previous research such as, Alamsyah (2008)

and Mehrotra et al (2007).Using this method, the inflation persistence cause can be seen based

on the forward looking andbackward looking inflation behavior. Both of them are described

from the Hybrid NKPCmodel that catchesinflation persistence characteristic as follows:

Table 7.The Result of Hybrid NKPC Estimation

Hybrid NKPC model estimation is conducted by using 2SLS (Two Stages Least Squares)

technique, by adding a restriction on inflation parameter to be 1. The estimation result provided

in Table 7 shows that Jakarta»s inflation isdetermined by forward and backward looking

expectation. This is shown by similar magnitude of both parameters, indicating equal influence

of forward and backward looking expectation. Besides, the test using Wald test also shows

that there is no significant difference between forward and backward looking coefficient of

Jakarta inflation. The condition shows that the need of more intensive effort to change the

inflation expectation behavior to forward looking.

27Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

Meanwhile, output gap data is obtained by using HP filter technique. The estimation

showsthe output gap parameter is not significant to influence the inflation.In other word, the

output gap influence toward inflation has not been concluded yet.

The high inflation causes negative impact toward the economy. The high inflation will

give the uncertainty for economic agent in making decision beside influence the purchasing

power of society especially those with constant expectation. The economy management will

be more difficult if the inflation rate is persistent. By definition, the flow of inflation will take

more time before return to the its initial rate prior the shock. In addition, the inflation will also

require longer time to converge. These will amplify the effort needed to decrease the inflation

rate. Since Jakarta has the biggest weight in forming national inflation, then the high inflation

persistence in Jakarta implicates high effort to decrease national inflation.

Based on these assessment, the high inflation persistence degree in Jakarta is because of

the volatile food and administered price groups. This imply the need of stronger coordination

between the government and Bank Indonesia to control the inflation. While for the administered

price group is higly depends on the government effort to arrange the timing and the magnitude

of the price (and income) policy so that its impact toward inflation is minimum.

The high volatile food and administered price inflation will influence the influence

expectation, hence complicates the regional inflation control. Good coordination through the

existing coordination forums such as Bank Indonesia Governor council coordination meeting

with the government, inflation target stipulation forum, also forward looking inflation controlling

team, needs to be more optimized. Regarding to the Team for Monitoring and Controlling the

Regional Inflation / Tim Pemantauan dan Pengendalian Inflasi Daerah (TPID), its target to cover

all region in Indonesia (66 cities) needs to be monitored, considering its importance to reach

low and stable national inflation.

Beside that the TPID role can be optimized if it involve inter-regional coordination, especially

between the region with high economic linkage. In addition, TPID should realize its role to

provide information system (database) in monitoring the biggest inflation contributor commodity,

which is useful in determining price policy in regional level.

The effort to control inflation in region is subsequently can give positive impact toward

faster inflation convergence across region, hence the regional inflation can be easier to controlled.

The inflation control through monetary policy in national level, then is expected to be more

effective. The issue of convergence and coordination across region especially Jakarta and other

region should be interesting topic for next paper4.

4 Arimurti and Trisnanto, ≈Inter regional inflation convergence in Indonesia∆, forthcoming paper.

28 Bulletin of Monetary, Economics and Banking, July 2011

The inflation pressure sourced mainly from inflation expectation especially backward

looking one implies a more intensive dissemination of information and central bank policy to

direct the economic agent expectation to be forward looking, in order to achieve the low and

stable inflation. These attempts are also related to the credibility of policy maker that needs to

be strengthened and maintained.

5. SUMMARY

This research gives several important conclusions, first, the empirical test shows the CPI

inflation in Jakarta is persistent. Similar result is shown in a more disaggregated group, where

the administered price inflation, and volatile food inflation in Jakarta is classified to be very

persistent .Comodity groups with highest degree of persistence are Processed Foods, Beverages

and Tobaccos and Health. On commodity level, Rice, Beef, Cooking Oil, Sugar, and Dwelling.

In Jakarta, the comodity group mostly need 5-12 months to return to its average prior the

shock, while for the mostly commodity needs between 3-12 months. Second, in accordance

with the hybrid NKPC model result, it is found that the Jakarta»s inflation is a combination

between forward and backward looking behavior, This is in line with the result of national

inflation behavior (Alamsyah, 2008). Third, the cause of high inflation persistence degree in

Jakarta are because of the high of inflation persistence degree of volatile food and administered

price groups. This volatile food and administered price inflation affect the inflation expectation,

hence will complicate the inter regional inflation control.

This findings has several policy implications; first,the needsto intensify the dissemination

of information and policy in order to direct inflation expectation to be more on forward looking.

Second, the need to optimizethe coordination between the government and the Central Bank

through the existing coordination forums such as Bank Indonesia governor council coordination

meeting with government, inflation target stipulation forum, and also inflation controlling

team.

29Persistence of Inflation in Jakarta and Its Implication on the Regional Inflation Control Policy

REFERENCES

Alamsyah, H. (2008). Inflation Persistance and Its Impact Towards Choice and Respond of

Monetary Policy in Indonesia

Angeloni, I., Aucremanne, L., Ehrmann, M., Gali, J., Levin, A., & Smets, F. (2004). Inflation

Persistence in the Euro Area : Preliminary Summary of Findings.

Babecky, J., CorRicelly, F., & Horvath, R. (2008, June). Assessing Inflation Peristence: Micro

Evidence on an Inflation Targeting Economy. CERGE-EI .

Batini, N. (2002, December). Euro Area Inflation Persistence. European Central Bank Working

Paper Series .

Debelle, G., & Wilkinson, J. (2002). Inflation Targeting and the Inflation Process: Some Lessons

from an Open Economy. Research Bank of Australia - Research Discussion Paper 2002-01 .

Dossche, M., & Everaert, G. (2005, June). Measuring Inflation Persistence: A Structural Time

Series Approach. National Bank of Belgium Working Paper .

Federal Reserve Bank of San Fransisco. (2006, October 13). Inflation Persistence in an Era of

Well-Anchored Inflation Expectations. FRBSF Economic Letter .

Harmanta. (2009). Monetary Policy Credibilityand its impact towardsInflation Persistence and

Disinflation Strategy in Indonesia: with Dynamic Stochastic General Equilibrium (DSGE) Model.

Jakarta: Faculty of Business and Economics,Post Graduate Program ofEconomic Science,

University of Indonesia.

Levin, A. T., & Piger, J. M. (2004, April). Is Inflation Persistence Intrinsic in Industrial Economies?

European Central Bank Working Paper Series .

Marques, C. R. (2005). Inflation Peristence: Facts or Artefacts? Economic Bulletin .

Marques, C. R. (2004, June). Inflation Persistence: Facts or Artefacts? European Central Bank

Working Paper Series .

O»Reilly, G., & Whelan, K. (2004, April). Has Euro-Area Inflation Persistence Change Over Time?

European Central Bank Working Paper Series .

Pivetta, F., & Reis, R. (2006). The Persistence of Inflation in the United States. Journal of Economic

Dynamics and Control , April.

Stock, J. H. (2004, December). Inflation Persistence in the Euro Area: Evidence from Aggregate

and Sectoral Data.

30 Bulletin of Monetary, Economics and Banking, July 2011

Tim Inflasi. (2007). Core Inflation Persistence. Strategic Issue. Governor Council Meeting

Materials, 4 January. Jakarta: Bank Indonesia.

Willis, J. L. (2003). Implications of Structural Changes in the U.S. Economy for Pricing Behavior

and Inflation Dynamics. Federal Reserve Bank of Kansas City Economic Review .

Yanuarti, T. (2007). Has Inflation Persistence in Indonesia Changed?

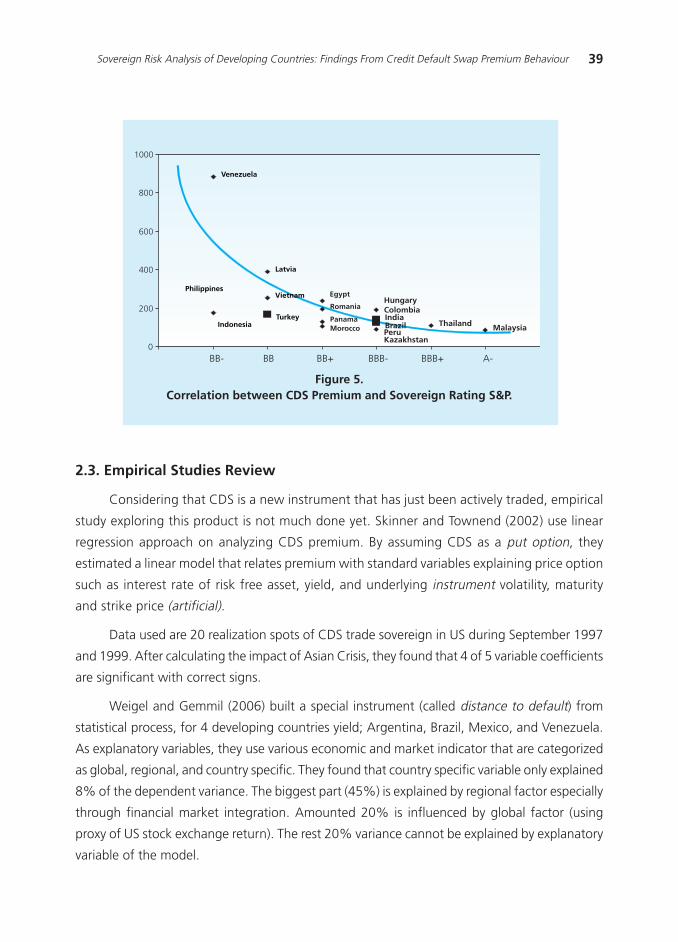

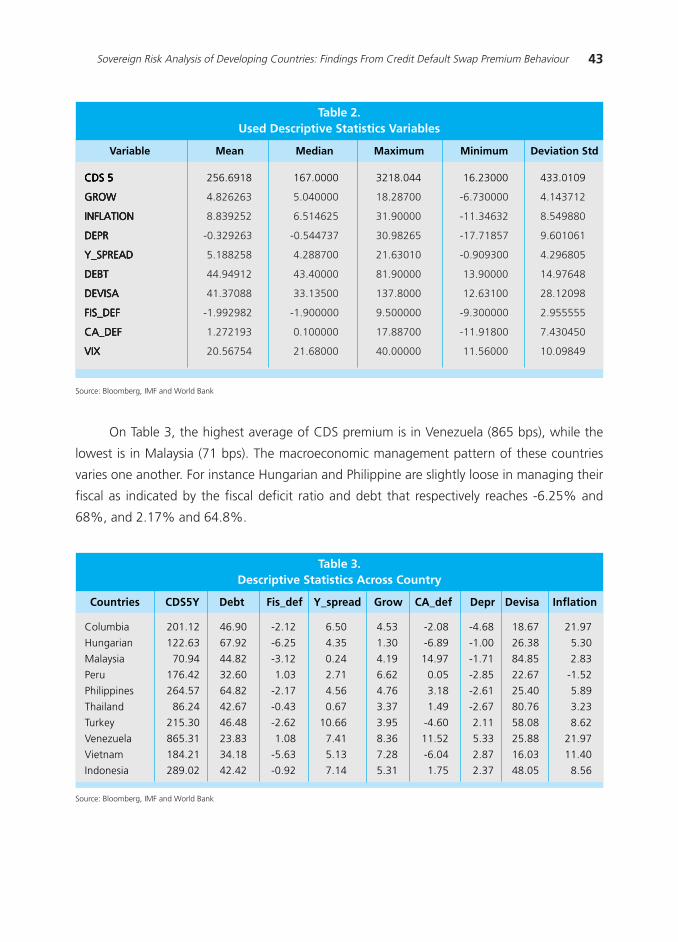

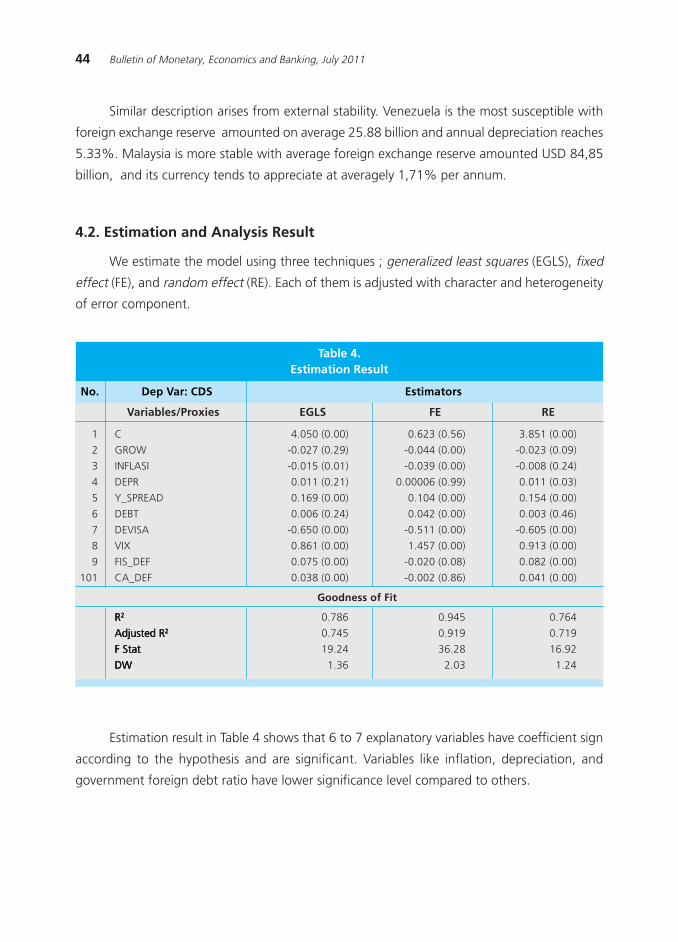

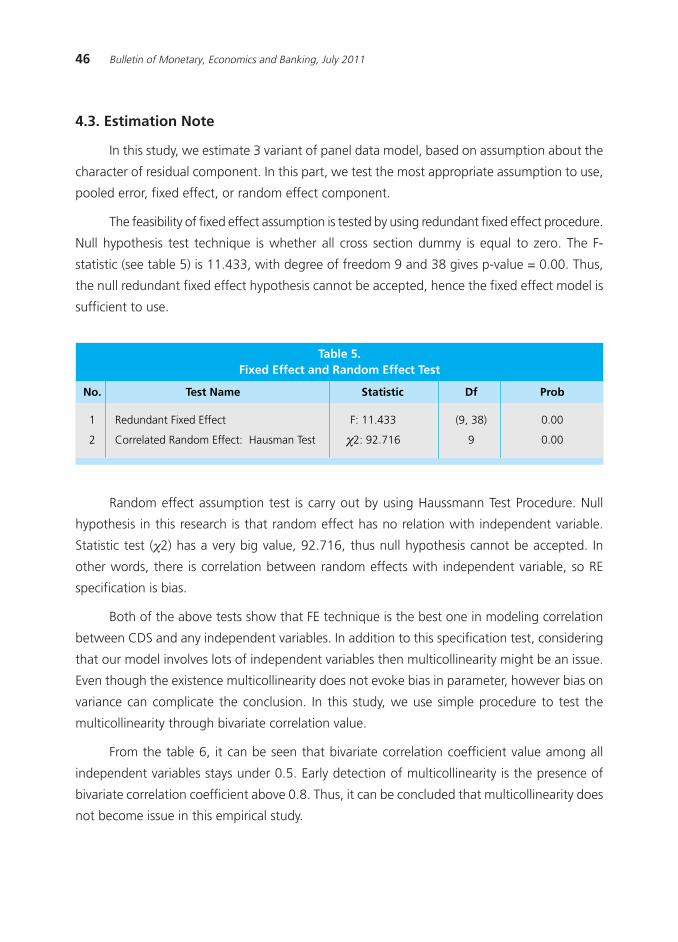

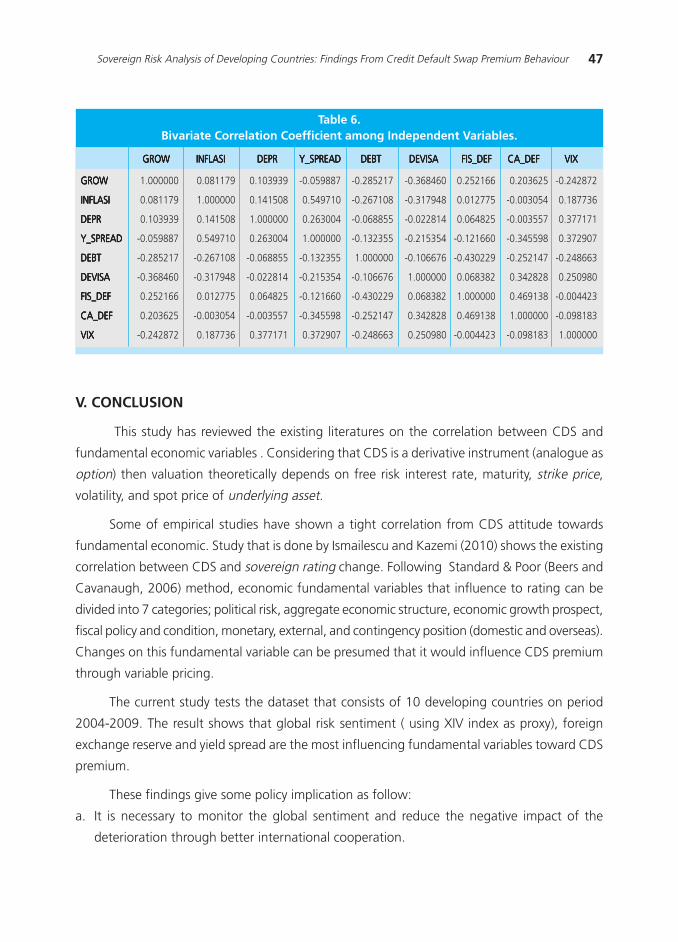

31Sovereign Risk Analysis of Developing Countries: Findings From Credit Default Swap Premium Behaviour

SOVEREIGN RISK ANALYSIS OF DEVELOPING COUNTRIES:FINDINGS FROM CREDIT DEFAULT SWAP PREMIUM BEHAVIOUR

Moch. Doddy Ariefianto dan Soenartomo Soepomo 1

This study conducts econometric analysis CDS Premium relations towards variables usually used

as a sovereign rating explanatory. Estimation with data panel econometric found that global risk appetite

is the most important influencing variable followed by foreign exchange reserve and yield spread. This

item is consistent with the existing empiric literature and shows a high correlation between developing

countries economy and world economic cycle.

JEL Classification : F34, F32, G13, G15, C23

Keywords::::: Sovereign Risk, Credit Default Swap, Panel Data

1 The authors are lecturer in Economic and Business Faculty, University of Ma Chung, Malang; [email protected] [email protected] .

Abstract

32 Bulletin of Monetary, Economics and Banking, July 2011

I. INTRODUCTION

Foreign debt has already become important source of fund in developing countries. This

external financing is needed in order to fill the saving-investment gap that is usually negative.

Foreign debt can be in any forms such as government debt, government bond, corporate

bond, bilateral-multilateral loan, etc.

The price of the loan depends on the scheme, economic condition (fiscal and monetary),

and reputation. In some decades recently, there is a kind of institution trend that does

specialization in debt valuation. This institution, which is always called as rating agency institution,

measures the ability of certain entity, quantitatively and qualitatively, to pay (credit risk) and

give this entity a ranking. Special for sovereign entity, the rating has been established since

1975 by Standard and Poor»s (Beers and Cavanaugh, 2006).

Credit risk measurement is not actually new. A credit risk model in default probability

form has been formulated by Altman with his famous Z-statistics in 1968. The development

of credit risk modeling is already advanced including its sophisticated statistic technique and

calibration of variables used. Cantor (2004) gave a review about the credit risk modeling.

The sovereign risk is important and attracting a huge attention of investors. Unlike

private credit risk, investor cannot seize the collateral or government income when event

default occurs. That is why the credit valuation for government loans becomes more

important.

As credit corporate risk, sovereign risk can also be influenced by domestic and

international condition (Beers and Cavanaugh, 2006), including economic or political condition.

Fiscal pressure, for instance, caused by large outstanding debt and government deficit, can

force the government to delay the installment and interest payment as well as the regime

transformation caused by political turbulence. The ruling government today can reject the

debt from previous government.

Interaction pattern of modern economic nowadays has a very high interrelation one

another. Practically, there are no countries that can isolate their economy from external shock.

Subprime mortgage crisis in the US in 2007 and the world economic contraction during

2008-2009 are the real evidences in terms of high interrelation among countries. Thus, a

country can experience an economic crisis as the impact of external turbulence, and make

the existing government to restructure their loan payment.

Further innovation in credit risk management in the early 21st century is the emergence

of Credit Default Swap (CDS). This derivative instrument has a function like bond insurance.

33Sovereign Risk Analysis of Developing Countries: Findings From Credit Default Swap Premium Behaviour

CDS holder (called as protection buyer) can exchange his bond with the sum of nominal face

value, to CDS seller (protection seller) in the case of default (Taylor, 2007). To get this protection,

CDS buyer must pay a certain premium (stated in percentage of debt).

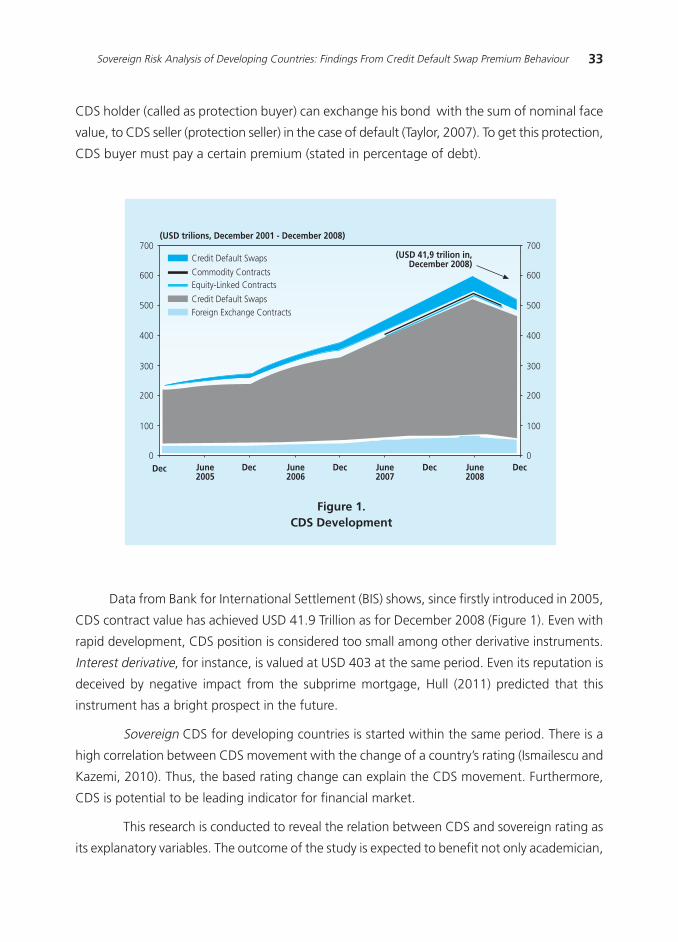

Figure 1.CDS Development

Data from Bank for International Settlement (BIS) shows, since firstly introduced in 2005,

CDS contract value has achieved USD 41.9 Trillion as for December 2008 (Figure 1). Even with

rapid development, CDS position is considered too small among other derivative instruments.

Interest derivative, for instance, is valued at USD 403 at the same period. Even its reputation is

deceived by negative impact from the subprime mortgage, Hull (2011) predicted that this

instrument has a bright prospect in the future.

Sovereign CDS for developing countries is started within the same period. There is a

high correlation between CDS movement with the change of a country»s rating (Ismailescu and

Kazemi, 2010). Thus, the based rating change can explain the CDS movement. Furthermore,

CDS is potential to be leading indicator for financial market.

This research is conducted to reveal the relation between CDS and sovereign rating as

its explanatory variables. The outcome of the study is expected to benefit not only academician,

700

600

500

400

300

200

100

0Dec June

2005Dec June

2006Dec June

2007Dec June

2008Dec

(USD trilions, December 2001 - December 2008)

(USD 41,9 trilion in,December 2008)

Credit Default Swaps

Commodity ContractsEquity-Linked Contracts

Credit Default SwapsForeign Exchange Contracts

700

600

500

400

300

200

100

0

34 Bulletin of Monetary, Economics and Banking, July 2011

(1)

but also for policy maker.This paper consists of five sections. Next section presents the theory

and empirical literature about CDS. The third section explains the methodology of research

including our empirical scheme. The forth section discusses result and analysis, while conclusion

and policy implication will close the presentation.

II. THEORY

2.1. CDS Valuation Overview

Duffie (1999) suggested to considering CDS as swap default able floating rate notes

towards default free floating rate note. As a swap, the owner of CDS has a right to exchange

his default-able instruments with the cash flow from default free instrument that belongs to

swap seller. This swap is triggered when the credit event occur. The credit event can be in any

forms such as outright default from underlying securities issuer, restructuring, rescheduling, or

even just the postponement of interest/installment payment (Hull, 2011).

Skinner and Townend (2002), in the other hand, used a put option approach in valuing

CDS. As a put option, CDS buyer has a right to sell securities that belong to him at par value

when credit event occurred. Furthermore, they also explained that CDS premium meet the put

and call parity:

Where X is noticed as strike price from the option (par value), B is noticed as a security that

contain credit risk, p is CDS premium, D is coupon value, and r is interest rate of risk free

portfolio. They showed that this inequality will be fulfilled, so that the CDS premium is analogue

to the premium of an option.

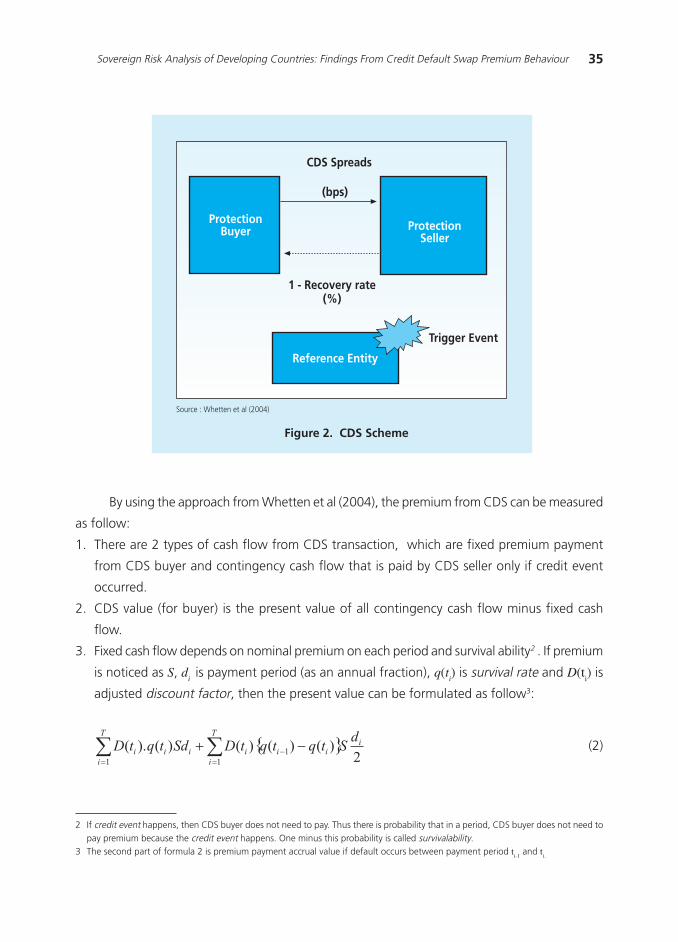

Whetten et al (2004), on the other hand, use the insurance approach. A CDS buyer gets

insurance upon the minimum underlying securities price. If the event credit occurred, then CDS

buyer can exchange his securities with cash at par value. In another scheme, CDS buyer can sell

securities himself and CDS seller would compensate its deviation to the par value. In other

words, CDS seller just pays (1-a), where a is security market value after credit event occur

(recovery rate), see Figure 2.

35Sovereign Risk Analysis of Developing Countries: Findings From Credit Default Swap Premium Behaviour

Figure 2. CDS Scheme

By using the approach from Whetten et al (2004), the premium from CDS can be measured

as follow:

1. There are 2 types of cash flow from CDS transaction, which are fixed premium payment

from CDS buyer and contingency cash flow that is paid by CDS seller only if credit event

occurred.

2. CDS value (for buyer) is the present value of all contingency cash flow minus fixed cash

flow.

3. Fixed cash flow depends on nominal premium on each period and survival ability2 . If premium

is noticed as S, di is payment period (as an annual fraction), q(t

i) is survival rate and D(t

i) is

adjusted discount factor, then the present value can be formulated as follow3:

CDS Spreads

(bps)

ProtectionBuyer Protection

Seller

1 - Recovery rate(%)

Reference Entity

Trigger Event

Source : Whetten et al (2004)

2 If credit event happens, then CDS buyer does not need to pay. Thus there is probability that in a period, CDS buyer does not need topay premium because the credit event happens. One minus this probability is called survivalability.

3 The second part of formula 2 is premium payment accrual value if default occurs between payment period ti-1

and ti.

(2)

36 Bulletin of Monetary, Economics and Banking, July 2011

4 Most of material in this part are summarized from Beers and Cavanaugh (2006)

4. Whereas the number of contingency cash flow can be calculated as a difference of recovery

rate (R) from the par value, or

(3)

5. In equilibrium condition, premium value will equalize the fixed and contingency cash flow

payment, or explicitly stated:

(4)

6. With a little math, we can obtain the CDS premium valuation as follow:

(5)

2.2. Sovereign Rating Approach Towards CDS Premium4

Sovereign rating is credit risk evaluation for government entity, and not specifically for

certain issuer. The rating reflects credit risk evaluation for all entities in a country. The other

credit risk entity would always be smaller or equal with sovereign rating. Thus, the sovereign

rating becomes very important since the domestic credit price will be affected if the sovereign

rating degrades.

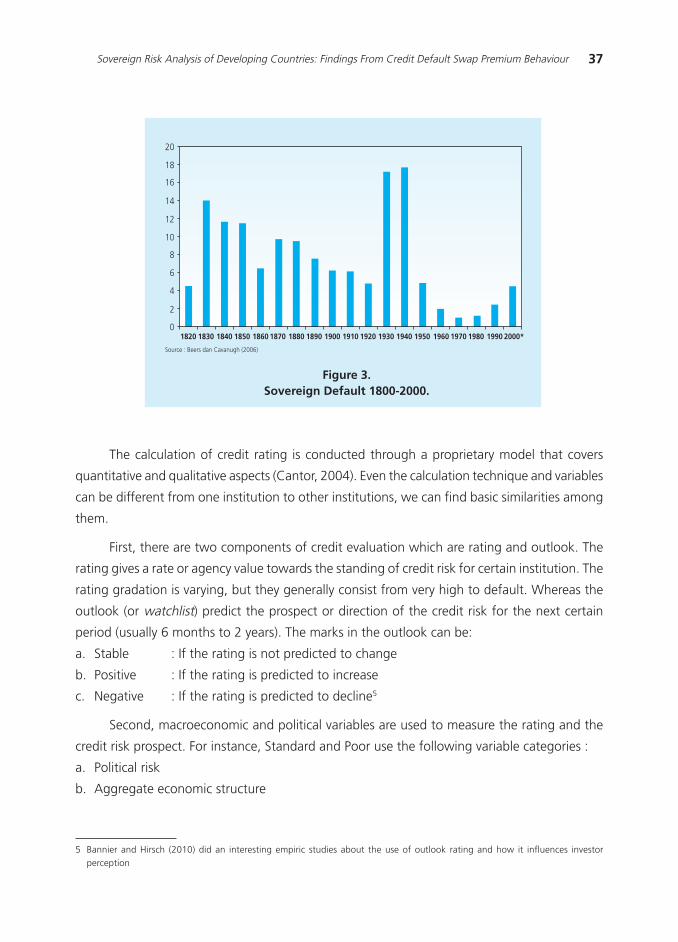

Sovereign default occurrence declined during 1970-1980s but it increased even still below

the average in 1900-1950s (see Figure 3). The decline was because the traditional factors that

worsen the fiscal condition (such as the wars, revolution, and the policy that are not prudent)

had decreased drastically . In modern era, the weakness of debt management, the low economic

productivity, and the contingent liabilities (from the collapse of banking system) are the main

reason of sovereign default.

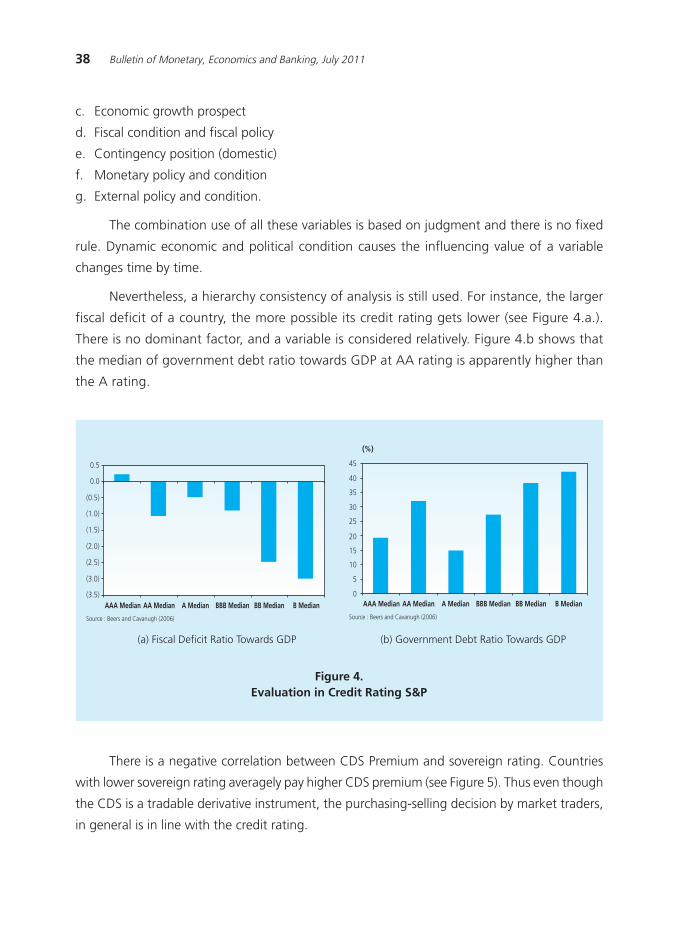

37Sovereign Risk Analysis of Developing Countries: Findings From Credit Default Swap Premium Behaviour

The calculation of credit rating is conducted through a proprietary model that covers

quantitative and qualitative aspects (Cantor, 2004). Even the calculation technique and variables

can be different from one institution to other institutions, we can find basic similarities among

them.

First, there are two components of credit evaluation which are rating and outlook. The

rating gives a rate or agency value towards the standing of credit risk for certain institution. The