Embed Size (px)

Citation preview

January 7, 2015

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

All set to get growth bearings… NRB Bearings (NRB) is the leader in the needle roller bearings segment in India with ~70% market share. With customised offerings and a pure play on the mobility segment, NRB enjoys a sticky clientele across all leading OEMs coupled with a strong exports segment (forming ~23% of FY14 topline) that has grown at 25.7% CAGR in FY09-14. With automotive volumes showing early signs of recovery coupled with a strong launch pipeline and product refreshes ahead, we expect the consolidated topline and earnings to grow at 17.4% and 39.3% CAGR, respectively, in FY14-17E. We are initiating coverage on the stock with a BUY recommendation and an SoTP target price of | 165/share. Leader in needle bearing segment NRB is the leader in the needle bearing segment in India with ~70% market share. Needle roller bearings constituted ~55% of NRB’s topline in FY14. A needle roller bearing, as a customised product, requires NRB to work with OEMs from the conceptualisation stage. This enables it to build sticky clientele relationships with almost all major OEM players. Apart from needle bearings, cylindrical bearings are the other key product with needle and cylindrical bearings together forming ~68% of the topline. Early signs of auto revival + strong launch pipeline augur well for NRB For YTDFY15, auto volumes have recovered with 11.6% growth (mainly driven by two-wheeler segment growth, which was up 13.7% YoY). With the auto industry finally showing signs of a recovery after nearly two years of a demand slump coupled with a strong launch pipeline and product refreshes, we expect bearings demand from the OEM segment to pick up significantly. Therefore, net revenues from the OEM segment are expected to grow at 15% CAGR during FY14-17E to | 560 crore. De-risked geographical presence through strong exports… To expand its geographical footprints and foray into newer platforms, NRB has forayed into exports wherein it caters to global players such as Daimler, Renault, Volvo and Getrag. NRB’s exports, which grew at 25.7% CAGR over FY09-14, have also provided a natural hedge for its import of raw materials. Exports, which formed ~7.6% of the topline in FY10, now constitute ~23.3% of revenues in FY14. We expect NRB’s export revenues to grow at 23.3% CAGR in FY14-17E to | 260 crore in FY17E. Strong earnings growth to boost valuations… Given NRB’s leadership position in the needle roller bearings space with a pure play in the mobility segment recovery and strong consolidated earnings growth at 39.3% CAGR in FY14-17E, we initiate coverage on NRB with a BUY rating. We ascribe a multiple of 18x (at ~30% discount to SKF) on the FY17E earnings to arrive at a valuation of | 165/share.

Exhibit 1: Key financials (Consolidated) (| Crore) FY13 FY14 FY15E FY16E FY17ENet Sales 591.6 607.5 700.4 835.1 982.7 EBITDA 100.1 103.1 128.2 162.9 199.7 EBITDA Margin (%) 16.9 17.0 18.3 19.5 20.3 Interest 18.6 18.6 23.5 23.5 22.1 Depreciation 32.1 35.6 38.2 41.5 44.8 Net Profit 47.2 33.0 45.5 66.2 89.1 EPS (|) 4.9 3.4 4.7 6.8 9.2 RoCE (%) 14.4 12.6 15.2 19.0 22.5 RoE (%) 23.8 15.1 18.1 22.1 24.4

Source: Company, ICICIdirect.com Research

NRB Bearings (NRBBEA)| 132

Rating Matrix Rating : BuyTarget : | 165Target Period : 12-18 monthsPotential Upside : 25%

YoY growth (%)(Consolidated)

(YoY Growth) FY14 FY15E FY16E FY17ENet Sales 2.7 15.3 19.2 17.7 EBITDA 3.1 24.3 27.1 22.6 Net Profit (30.1) 37.8 45.6 34.7 EPS (30.1) 37.8 45.6 34.7

Current & target multiple (Consolidated)

(x) FY14 FY15E FY16E FY17EP/E 37.9 27.5 18.9 14.0 Target P/E 48.6 35.3 24.2 18.0 EV / EBITDA 15.1 12.1 9.4 7.7 P/BV 5.7 5.0 4.2 3.4 RoNW (%) 15.1 18.1 22.1 24.4 RoCE (%) 12.6 15.2 19.0 22.5

Stock Data Bloomberg/Reuters Code NRBBR IN / NRBB BOSensex 26,950 Average volumes 311,468 Market Cap (| crore) 1,280.3 52 week H/L 147 / 35Equity Capital (| crore) 19.4 Promoter's Stake (%) 58.9 FII Holding (%) 17.4 DII Holding (%) 10.7

Comparative return matrix (%)

Return % 1M 3M 6M 12MSKF India (3.3) 22.5 20.5 104.5 FAG Bearings (3.3) 17.6 34.5 122.1 NRB Bearings 3.4 2.8 42.4 207.2 Timken India 4.3 24.1 63.3 209.5

Price movement

020406080100120140160

Jan-

15

Sep-

14

Jun-

14

Mar

-14

Dec-

13

Sep-

13

Jun-

13

Mar

-13

Nov

-12

Aug

-12

May

-12

Feb-

12

4,000

5,500

7,000

8,500

10,000

Price (R.H.S) Nifty (L.H.S)

Research Analyst’s name

Chirag J Shah [email protected]

Bhupendra Tiwary [email protected]

Page 2ICICI Securities Ltd | Retail Equity Research

Company background NRB Bearings (NRB) is one of the leading bearing companies in India with ~7% market share (in terms of revenues). Incorporated in 1965, in collaboration with French needle bearing manufacturer Nadella SA (later acquired by Torrington and finally by Timken) and Sahney family, it is the first needle bearing manufacturing company in India. The current promoters i.e. the Sahney family bought out Timken’s 26% stake in 2005. NRB Bearings is a leader in needle roller bearing manufacturing in India with ~70% market share in needle roller bearings. Needle roller bearings comprise ~55% of the company’s topline. Needle bearings find application predominantly in the automotive space and have a focus on compact size applications. Hence, two-wheelers (2-W) form the major application for needle roller bearings. A needle roller bearing is a customised product. Hence, NRB works with OEMs from the conceptualisation stage to provide anti-friction solutions. This enables the company to build a sticky clientele relationship with major OEM players. Apart from needle roller bearings, NRB also categorises cylindrical bearings as its key product. Needle and cylindrical bearings form ~60-65% of NRB’s topline. NRB, whose domestic automotive segment forms ~62% of the topline, caters to almost all segment viz. two-wheelers (33% of revenues), CV (19% of revenues), PV (20% of revenues) and farm/off highway (forming 10% of revenues). Key clients include Hero MotoCorp, Bajaj Auto, HMSI and TVS Motors in the two-wheelers space and Tata Motors, Maruti Suzuki, Mahindra & Mahindra and Ashok Leyland in PV, CV space. Unlike its MNC counterparts, the company produces all its output indigenously given the integrated operation. NRB has manufacturing facilities at Jalna, Waluj, Hyderabad, Aurangabad, Thane, Pantnagar, Ranchi (SNL Bearing) and Thailand. The company also serves the after market business through its ~250 dealers and distributors.

Exhibit 2: NRB Bearings – Timeline of company’s milestone

First plant set up at Thane to produce needle roller

bearings

General bearing plant set up at Jalna to produce cylindrical, tapered, ball bearings and

spherical roller bearing

Incorporated as Needle Roller Bearing Company Ltd as Indo-

French JV with Nadella - France

New plant set up at Aurangabad, Maharashtra to meet growing

demand

NRB becomes publicly listed with listing on Bombay Stock

Exchange

Haridwar factory starts production catering to two wheeler OEM and replacement market

1965 1980

Name of the company changed to NRB Bearings Ltd. In 1991, Waluj Plant set up to

meet increasing demand

Sets up state-of the-art engineering & design centre at Thane plant; acquires SNL Bearings (formerly known

as Shreeram Needle Bearings

Establishes 100% subsidiary - 'NRB Bearings Thailand Ltd.' at Rayong

Thailand

2012

Industrial bearing undertaking demerged and listed as

separate company called NRB Industrial Bearings

20081966 1982 1990-91 1995 2000 2003

Source: Company, ICICIdirect.com Research

Shareholding pattern (Q2FY15)

Shareholder Holding (%)

Promoters 58.9

Institutional investors 28.1

General public 13.0

FII & DII holding trend (%)

19.0 19.0 19.017.4

1.2 1.2

4.8

10.7

0.0

5.0

10.0

15.0

20.0

Q3FY14 Q4FY14 Q1FY15 Q2FY15

(%)

FII DII

Page 3ICICI Securities Ltd | Retail Equity Research

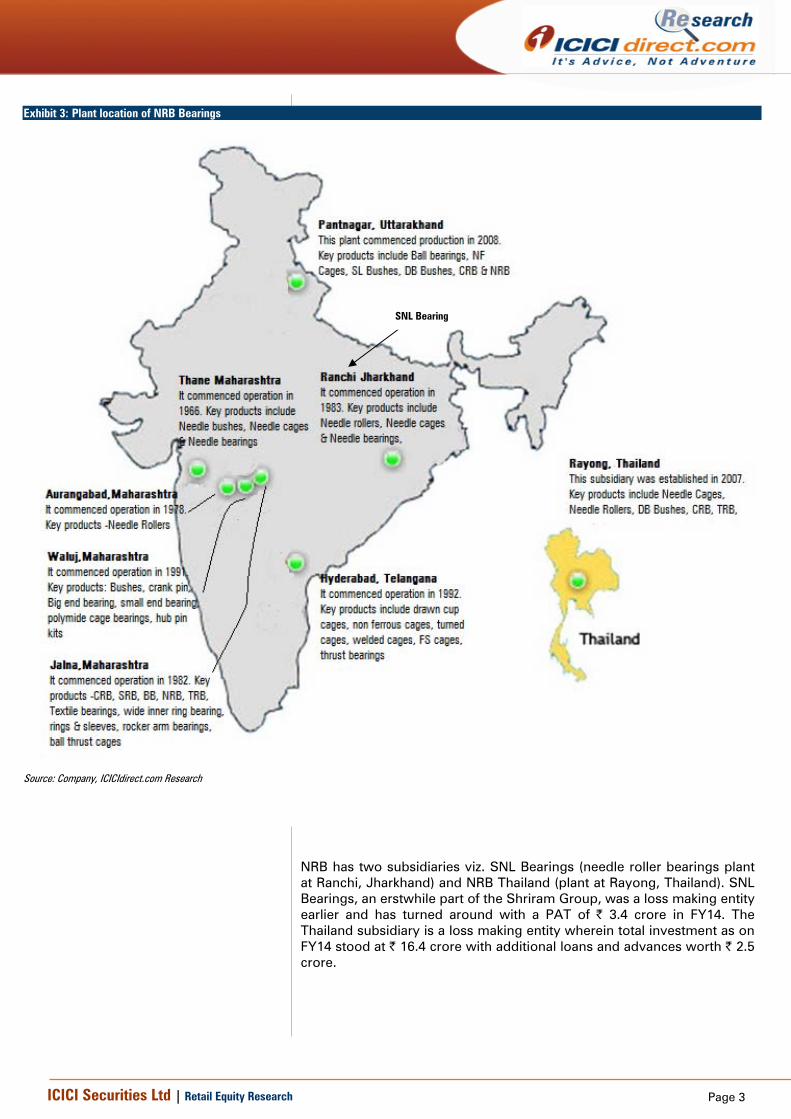

Exhibit 3: Plant location of NRB Bearings

Source: Company, ICICIdirect.com Research

NRB has two subsidiaries viz. SNL Bearings (needle roller bearings plant at Ranchi, Jharkhand) and NRB Thailand (plant at Rayong, Thailand). SNL Bearings, an erstwhile part of the Shriram Group, was a loss making entity earlier and has turned around with a PAT of | 3.4 crore in FY14. The Thailand subsidiary is a loss making entity wherein total investment as on FY14 stood at | 16.4 crore with additional loans and advances worth | 2.5 crore.

SNL Bearing

Page 4ICICI Securities Ltd | Retail Equity Research

Investment Rationale Leader in needle bearings segment

Needle bearings form ~5% of total bearings in India

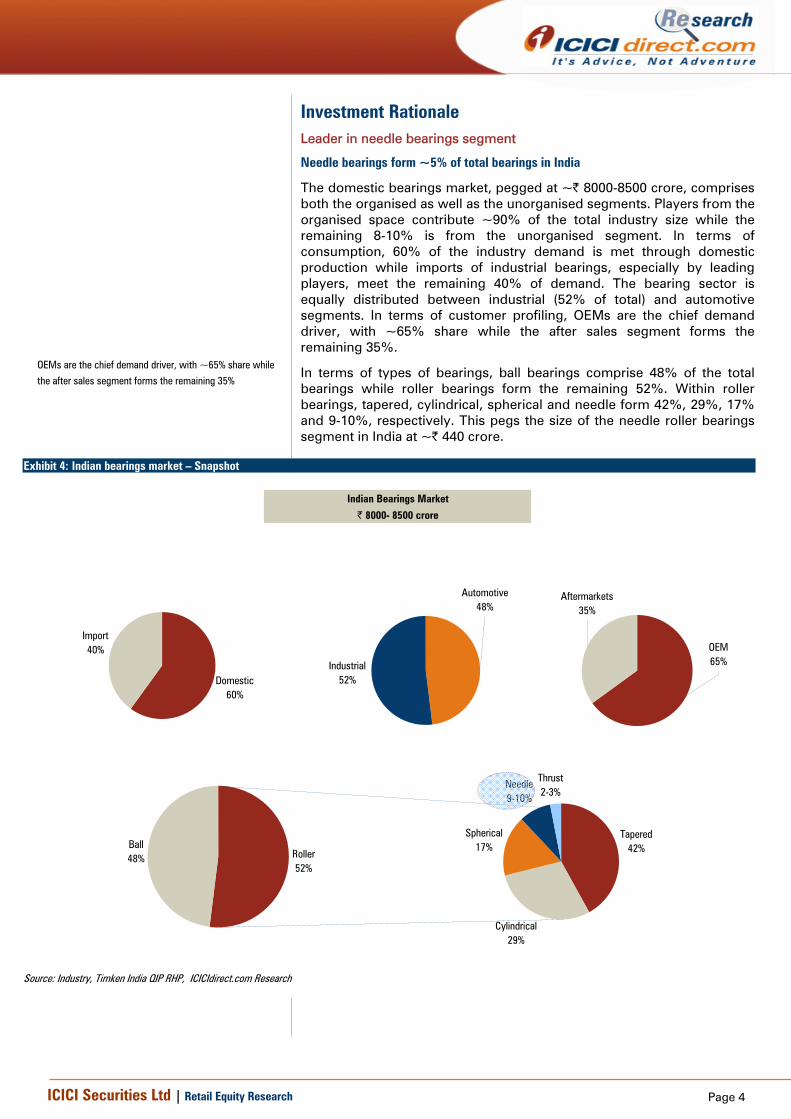

The domestic bearings market, pegged at ~| 8000-8500 crore, comprises both the organised as well as the unorganised segments. Players from the organised space contribute ~90% of the total industry size while the remaining 8-10% is from the unorganised segment. In terms of consumption, 60% of the industry demand is met through domestic production while imports of industrial bearings, especially by leading players, meet the remaining 40% of demand. The bearing sector is equally distributed between industrial (52% of total) and automotive segments. In terms of customer profiling, OEMs are the chief demand driver, with ~65% share while the after sales segment forms the remaining 35%.

In terms of types of bearings, ball bearings comprise 48% of the total bearings while roller bearings form the remaining 52%. Within roller bearings, tapered, cylindrical, spherical and needle form 42%, 29%, 17% and 9-10%, respectively. This pegs the size of the needle roller bearings segment in India at ~| 440 crore.

Exhibit 4: Indian bearings market – Snapshot

Indian Bearings Market

| 8000- 8500 crore

Domestic60%

Import40%

Automotive48%

Industrial52%

Roller52%

Ball48%

Tapered42%

Cylindrical29%

Spherical17%

Needle9-10%

Thrust2-3%

OEM65%

Aftermarkets35%

Source: Industry, Timken India QIP RHP, ICICIdirect.com Research

OEMs are the chief demand driver, with ~65% share while

the after sales segment forms the remaining 35%

Page 5ICICI Securities Ltd | Retail Equity Research

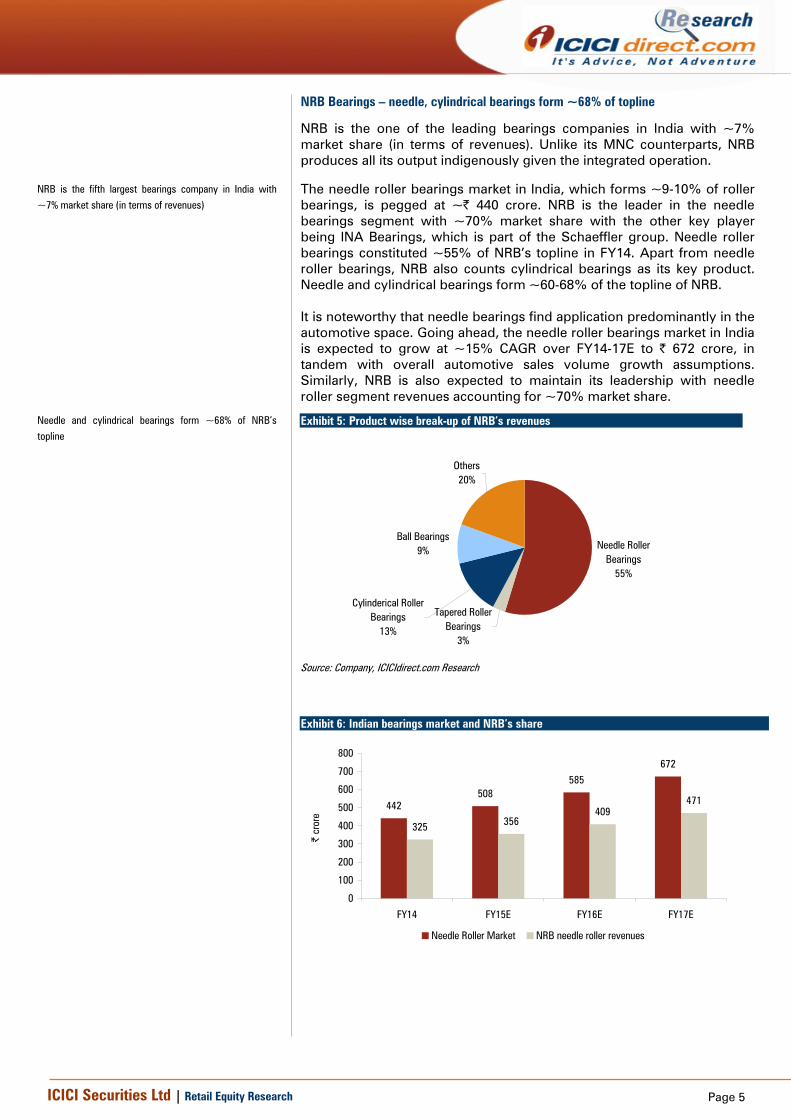

NRB Bearings – needle, cylindrical bearings form ~68% of topline

NRB is the one of the leading bearings companies in India with ~7% market share (in terms of revenues). Unlike its MNC counterparts, NRB produces all its output indigenously given the integrated operation.

The needle roller bearings market in India, which forms ~9-10% of roller bearings, is pegged at ~| 440 crore. NRB is the leader in the needle bearings segment with ~70% market share with the other key player being INA Bearings, which is part of the Schaeffler group. Needle roller bearings constituted ~55% of NRB’s topline in FY14. Apart from needle roller bearings, NRB also counts cylindrical bearings as its key product. Needle and cylindrical bearings form ~60-68% of the topline of NRB. It is noteworthy that needle bearings find application predominantly in the automotive space. Going ahead, the needle roller bearings market in India is expected to grow at ~15% CAGR over FY14-17E to | 672 crore, in tandem with overall automotive sales volume growth assumptions. Similarly, NRB is also expected to maintain its leadership with needle roller segment revenues accounting for ~70% market share.

Exhibit 6: Indian bearings market and NRB’s share

442508

585672

325 356409

471

0

100

200

300

400

500

600

700

800

FY14 FY15E FY16E FY17E

| cr

ore

Needle Roller Market NRB needle roller revenues

NRB is the fifth largest bearings company in India with

~7% market share (in terms of revenues)

Exhibit 5: Product wise break-up of NRB’s revenues

Needle Roller Bearings

55%

Tapered Roller Bearings

3%

Cylinderical Roller Bearings

13%

Ball Bearings9%

Others20%

Source: Company, ICICIdirect.com Research

Needle and cylindrical bearings form ~68% of NRB’s

topline

Page 6ICICI Securities Ltd | Retail Equity Research

Strong clientele base – Presence, diversification

Presence across major OEM players, new segments to open up opportunities

NRB is present across the auto OEM space through its exposure to the two-wheelers, four-wheelers, commercial vehicles (CV), passenger vehicles (PV) and off highway segments. With a proven track record over 49 years, it is a preferred supplier to leading domestic OEMs such as Hero MotoCorp, Bajaj Auto, Maruti Suzuki, Tata Motors, Ashok Leyland, etc. which is clearly depicted in the staggering 70% market share commanded by the company in the needle roller bearings space. A needle roller bearing is a customised product. Hence, the company works with OEMs from the conceptualisation stage to provide anti-friction solutions. This enables NRB to build a sticky clientele relationship with major OEM players.

Apart from the automotive segment, the company also enjoys a presence in the race boats segment wherein Ingersoll Rand is one of the key customers. Furthermore, NRB has also outlined growth opportunities in other mobility segments such as defence in the form of gun carriers, marine, Railways and MRTS wherein rising investment could open up avenues for bearings demands.

NRB, whose domestic automotive segment, forms ~62% of the topline, caters to almost all segment viz. two-wheelers (33% of revenues), CV (19% of revenues), PV (20% of revenues) and farm/off highway (forming 10% of revenues). Domestic automotive OEM revenues of NRB have grown at 14.3% CAGR during FY09-14 to | 368.6 crore.

Exhibit 7: Key customers of NRB Category Key customersTwo-wheeler OEMs Hero MotoCorp, HMSI, Bajaj Auto, TVS MotorPV Maruti Suzuki, Tata MotorsCV/Utility vehicle Mahindra & Mahindra, Ashok Leyland

Source: Company, ICICIdirect.com Research

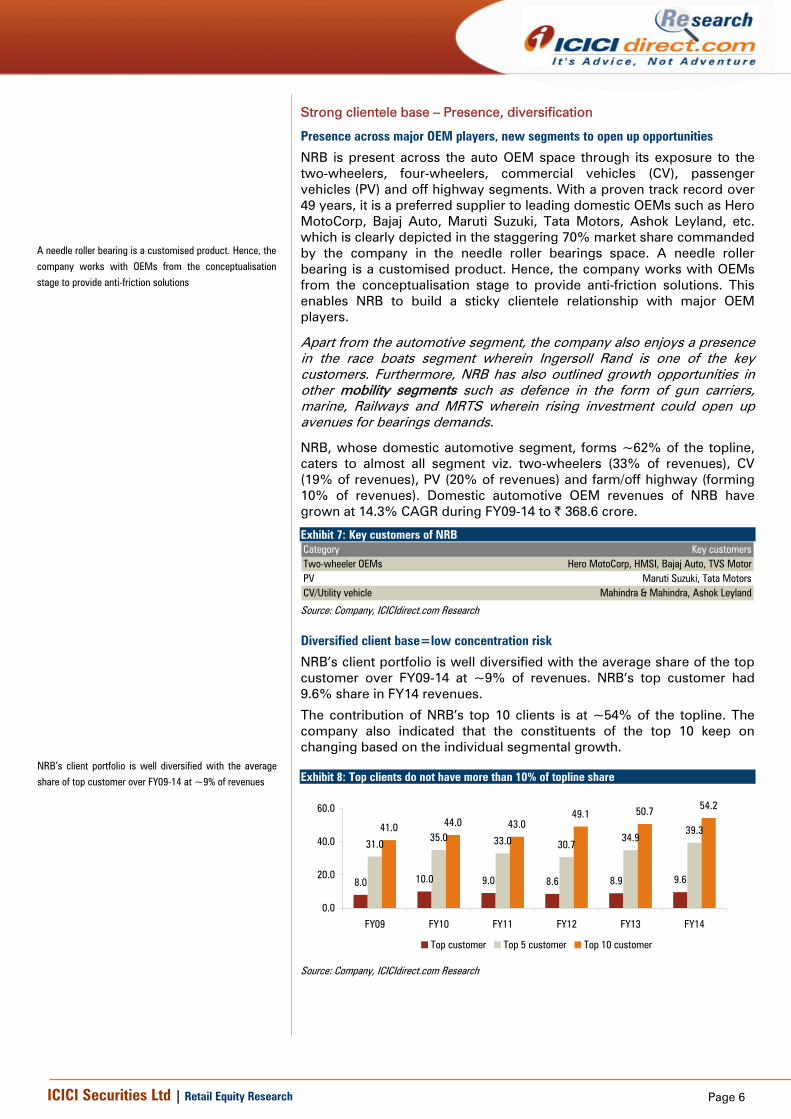

Diversified client base=low concentration risk

NRB’s client portfolio is well diversified with the average share of the top customer over FY09-14 at ~9% of revenues. NRB’s top customer had 9.6% share in FY14 revenues.

The contribution of NRB’s top 10 clients is at ~54% of the topline. The company also indicated that the constituents of the top 10 keep on changing based on the individual segmental growth.

Exhibit 8: Top clients do not have more than 10% of topline share

8.0 10.0 9.0 8.6 8.9 9.6

31.035.0 33.0 30.7

34.939.341.0 44.0 43.0

49.1 50.7 54.2

0.0

20.0

40.0

60.0

FY09 FY10 FY11 FY12 FY13 FY14

Top customer Top 5 customer Top 10 customer

Source: Company, ICICIdirect.com Research

A needle roller bearing is a customised product. Hence, the

company works with OEMs from the conceptualisation

stage to provide anti-friction solutions

NRB’s client portfolio is well diversified with the average

share of top customer over FY09-14 at ~9% of revenues

Page 7ICICI Securities Ltd | Retail Equity Research

Automotive segment recovery to boost demand…

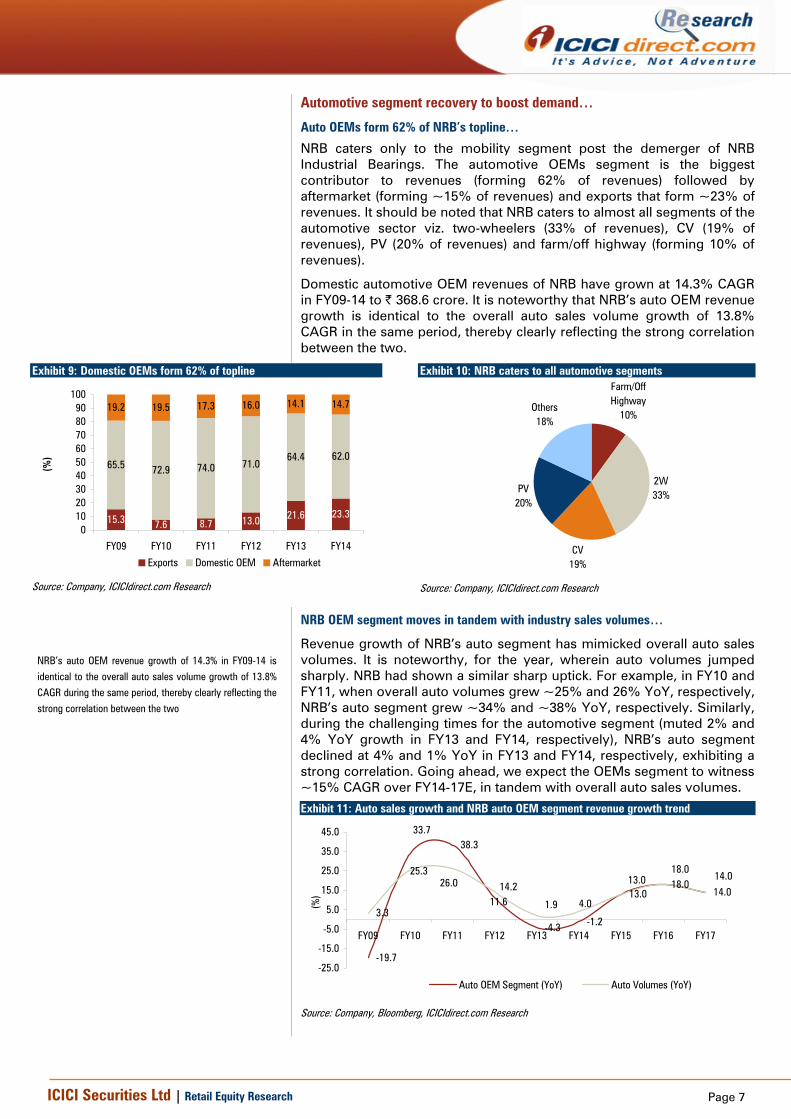

Auto OEMs form 62% of NRB’s topline…

NRB caters only to the mobility segment post the demerger of NRB Industrial Bearings. The automotive OEMs segment is the biggest contributor to revenues (forming 62% of revenues) followed by aftermarket (forming ~15% of revenues) and exports that form ~23% of revenues. It should be noted that NRB caters to almost all segments of the automotive sector viz. two-wheelers (33% of revenues), CV (19% of revenues), PV (20% of revenues) and farm/off highway (forming 10% of revenues).

Domestic automotive OEM revenues of NRB have grown at 14.3% CAGR in FY09-14 to | 368.6 crore. It is noteworthy that NRB’s auto OEM revenue growth is identical to the overall auto sales volume growth of 13.8% CAGR in the same period, thereby clearly reflecting the strong correlation between the two.

Exhibit 9: Domestic OEMs form 62% of topline

15.3 7.6 8.7 13.0 21.6 23.3

65.5 72.9 74.0 71.064.4 62.0

19.2 19.5 17.3 16.0 14.1 14.7

0102030405060708090

100

FY09 FY10 FY11 FY12 FY13 FY14

(%)

Exports Domestic OEM Aftermarket

Source: Company, ICICIdirect.com Research

Exhibit 10: NRB caters to all automotive segments Farm/Off Highway

10%

2W33%

CV19%

PV20%

Others18%

Source: Company, ICICIdirect.com Research

NRB OEM segment moves in tandem with industry sales volumes…

Revenue growth of NRB’s auto segment has mimicked overall auto sales volumes. It is noteworthy, for the year, wherein auto volumes jumped sharply. NRB had shown a similar sharp uptick. For example, in FY10 and FY11, when overall auto volumes grew ~25% and 26% YoY, respectively, NRB’s auto segment grew ~34% and ~38% YoY, respectively. Similarly, during the challenging times for the automotive segment (muted 2% and 4% YoY growth in FY13 and FY14, respectively), NRB’s auto segment declined at 4% and 1% YoY in FY13 and FY14, respectively, exhibiting a strong correlation. Going ahead, we expect the OEMs segment to witness ~15% CAGR over FY14-17E, in tandem with overall auto sales volumes.

NRB’s auto OEM revenue growth of 14.3% in FY09-14 is

identical to the overall auto sales volume growth of 13.8%

CAGR during the same period, thereby clearly reflecting the

strong correlation between the two

Exhibit 11: Auto sales growth and NRB auto OEM segment revenue growth trend

-19.7

38.3

-4.3 -1.2

13.018.0

14.0

3.311.6

33.7

14.2

1.9 4.0

14.013.025.3

26.018.0

-25.0

-15.0

-5.0

5.0

15.0

25.0

35.0

45.0

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17

(%)

Auto OEM Segment (YoY) Auto Volumes (YoY)

Source: Company, Bloomberg, ICICIdirect.com Research

Page 8ICICI Securities Ltd | Retail Equity Research

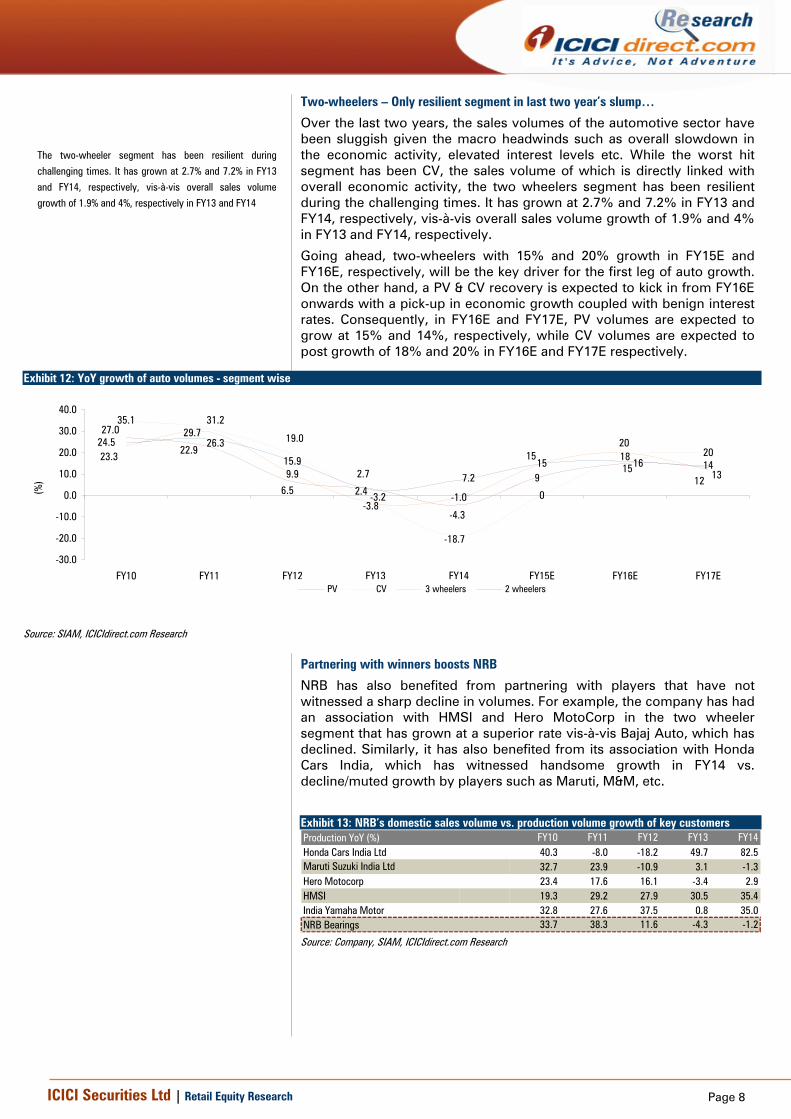

Two-wheelers – Only resilient segment in last two year’s slump…

Over the last two years, the sales volumes of the automotive sector have been sluggish given the macro headwinds such as overall slowdown in the economic activity, elevated interest levels etc. While the worst hit segment has been CV, the sales volume of which is directly linked with overall economic activity, the two wheelers segment has been resilient during the challenging times. It has grown at 2.7% and 7.2% in FY13 and FY14, respectively, vis-à-vis overall sales volume growth of 1.9% and 4% in FY13 and FY14, respectively.

Going ahead, two-wheelers with 15% and 20% growth in FY15E and FY16E, respectively, will be the key driver for the first leg of auto growth. On the other hand, a PV & CV recovery is expected to kick in from FY16E onwards with a pick-up in economic growth coupled with benign interest rates. Consequently, in FY16E and FY17E, PV volumes are expected to grow at 15% and 14%, respectively, while CV volumes are expected to post growth of 18% and 20% in FY16E and FY17E respectively.

Exhibit 12: YoY growth of auto volumes - segment wise

14

35.1

0

18 20

9.9

-1.0

1515.9

27.0

22.9

6.5

2.7

-4.3

915

31.2

19.0

-3.2

-18.7

23.3

29.7

-3.8

20

12

24.5 26.3

2.47.2

1516

13

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(%)

PV CV 3 wheelers 2 wheelers

Source: SIAM, ICICIdirect.com Research

Partnering with winners boosts NRB

NRB has also benefited from partnering with players that have not witnessed a sharp decline in volumes. For example, the company has had an association with HMSI and Hero MotoCorp in the two wheeler segment that has grown at a superior rate vis-à-vis Bajaj Auto, which has declined. Similarly, it has also benefited from its association with Honda Cars India, which has witnessed handsome growth in FY14 vs. decline/muted growth by players such as Maruti, M&M, etc.

Exhibit 13: NRB’s domestic sales volume vs. production volume growth of key customers Production YoY (%) FY10 FY11 FY12 FY13 FY14Honda Cars India Ltd 40.3 -8.0 -18.2 49.7 82.5Maruti Suzuki India Ltd 32.7 23.9 -10.9 3.1 -1.3Hero Motocorp 23.4 17.6 16.1 -3.4 2.9HMSI 19.3 29.2 27.9 30.5 35.4India Yamaha Motor 32.8 27.6 37.5 0.8 35.0NRB Bearings 33.7 38.3 11.6 -4.3 -1.2

Source: Company, SIAM, ICICIdirect.com Research

The two-wheeler segment has been resilient during

challenging times. It has grown at 2.7% and 7.2% in FY13

and FY14, respectively, vis-à-vis overall sales volume

growth of 1.9% and 4%, respectively in FY13 and FY14

Page 9ICICI Securities Ltd | Retail Equity Research

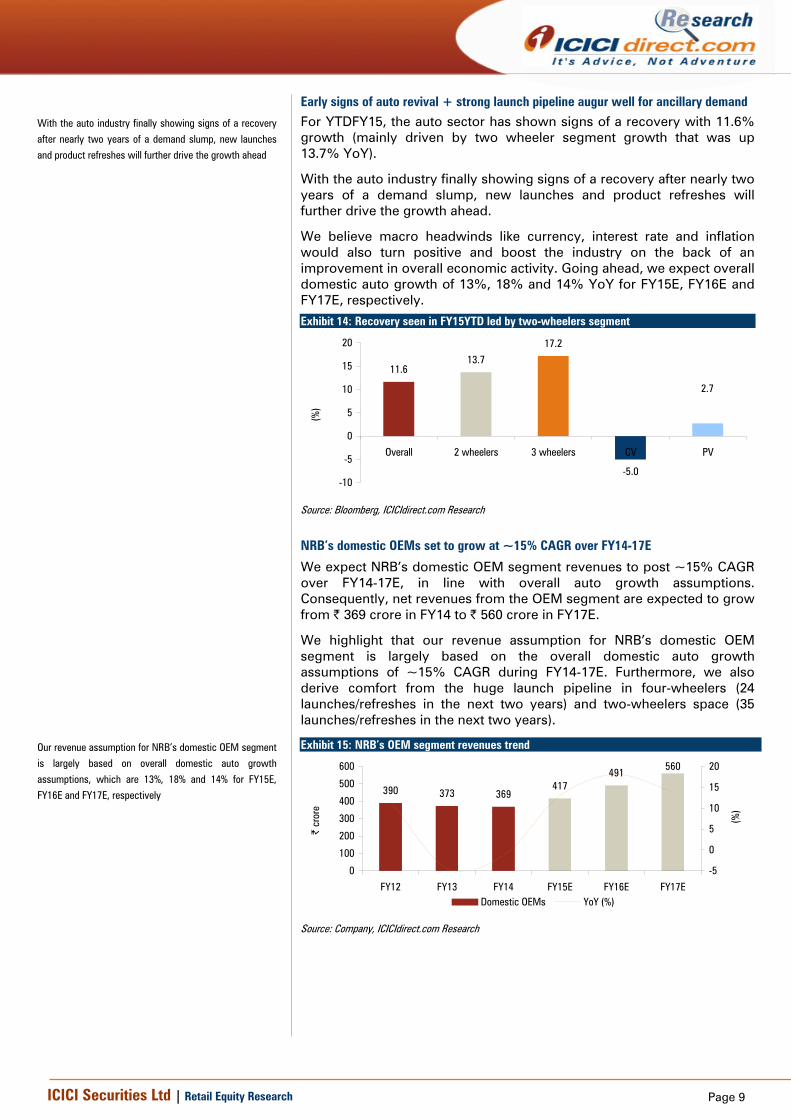

Early signs of auto revival + strong launch pipeline augur well for ancillary demand For YTDFY15, the auto sector has shown signs of a recovery with 11.6% growth (mainly driven by two wheeler segment growth that was up 13.7% YoY).

With the auto industry finally showing signs of a recovery after nearly two years of a demand slump, new launches and product refreshes will further drive the growth ahead.

We believe macro headwinds like currency, interest rate and inflation would also turn positive and boost the industry on the back of an improvement in overall economic activity. Going ahead, we expect overall domestic auto growth of 13%, 18% and 14% YoY for FY15E, FY16E and FY17E, respectively.

NRB’s domestic OEMs set to grow at ~15% CAGR over FY14-17E

We expect NRB’s domestic OEM segment revenues to post ~15% CAGR over FY14-17E, in line with overall auto growth assumptions. Consequently, net revenues from the OEM segment are expected to grow from | 369 crore in FY14 to | 560 crore in FY17E.

We highlight that our revenue assumption for NRB’s domestic OEM segment is largely based on the overall domestic auto growth assumptions of ~15% CAGR during FY14-17E. Furthermore, we also derive comfort from the huge launch pipeline in four-wheelers (24 launches/refreshes in the next two years) and two-wheelers space (35 launches/refreshes in the next two years).

Exhibit 15: NRB’s OEM segment revenues trend

390 373 369417

491560

0

100

200

300

400

500

600

FY12 FY13 FY14 FY15E FY16E FY17E

| cr

ore

-5

0

5

10

15

20

(%)

Domestic OEMs YoY (%)

Source: Company, ICICIdirect.com Research

With the auto industry finally showing signs of a recovery

after nearly two years of a demand slump, new launches

and product refreshes will further drive the growth ahead

Exhibit 14: Recovery seen in FY15YTD led by two-wheelers segment

11.613.7

17.2

-5.0

2.7

-10

-5

0

5

10

15

20

Overall 2 wheelers 3 wheelers CV PV

(%)

Source: Bloomberg, ICICIdirect.com Research

Our revenue assumption for NRB’s domestic OEM segment

is largely based on overall domestic auto growth

assumptions, which are 13%, 18% and 14% for FY15E,

FY16E and FY17E, respectively

Page 10ICICI Securities Ltd | Retail Equity Research

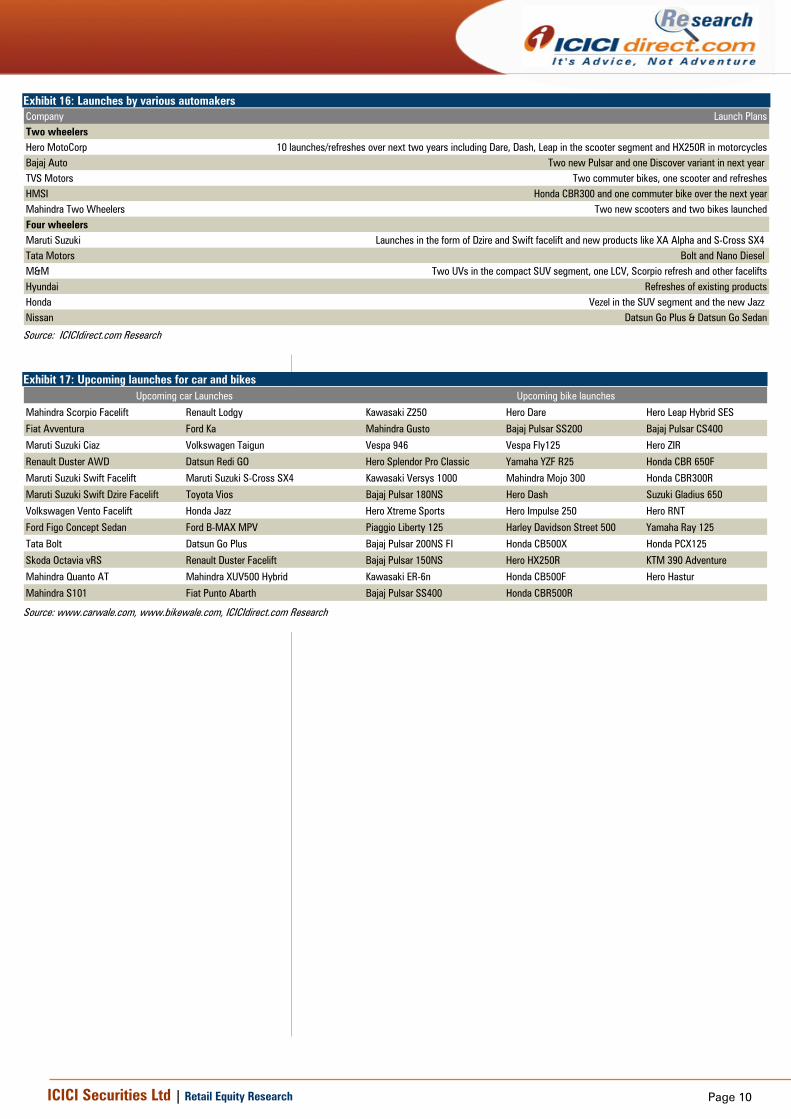

Exhibit 16: Launches by various automakers Company Launch PlansTwo wheelersHero MotoCorp 10 launches/refreshes over next two years including Dare, Dash, Leap in the scooter segment and HX250R in motorcyclesBajaj Auto Two new Pulsar and one Discover variant in next year TVS Motors Two commuter bikes, one scooter and refreshesHMSI Honda CBR300 and one commuter bike over the next yearMahindra Two Wheelers Two new scooters and two bikes launchedFour wheelersMaruti Suzuki Launches in the form of Dzire and Swift facelift and new products like XA Alpha and S-Cross SX4 Tata Motors Bolt and Nano Diesel M&M Two UVs in the compact SUV segment, one LCV, Scorpio refresh and other faceliftsHyundai Refreshes of existing productsHonda Vezel in the SUV segment and the new Jazz Nissan Datsun Go Plus & Datsun Go Sedan

Source: ICICIdirect.com Research

Exhibit 17: Upcoming launches for car and bikes

Mahindra Scorpio Facelift Renault Lodgy Kawasaki Z250 Hero Dare Hero Leap Hybrid SES

Fiat Avventura Ford Ka Mahindra Gusto Bajaj Pulsar SS200 Bajaj Pulsar CS400

Maruti Suzuki Ciaz Volkswagen Taigun Vespa 946 Vespa Fly125 Hero ZIR

Renault Duster AWD Datsun Redi GO Hero Splendor Pro Classic Yamaha YZF R25 Honda CBR 650F

Maruti Suzuki Swift Facelift Maruti Suzuki S-Cross SX4 Kawasaki Versys 1000 Mahindra Mojo 300 Honda CBR300R

Maruti Suzuki Swift Dzire Facelift Toyota Vios Bajaj Pulsar 180NS Hero Dash Suzuki Gladius 650

Volkswagen Vento Facelift Honda Jazz Hero Xtreme Sports Hero Impulse 250 Hero RNT

Ford Figo Concept Sedan Ford B-MAX MPV Piaggio Liberty 125 Harley Davidson Street 500 Yamaha Ray 125

Tata Bolt Datsun Go Plus Bajaj Pulsar 200NS FI Honda CB500X Honda PCX125

Skoda Octavia vRS Renault Duster Facelift Bajaj Pulsar 150NS Hero HX250R KTM 390 Adventure

Mahindra Quanto AT Mahindra XUV500 Hybrid Kawasaki ER-6n Honda CB500F Hero Hastur

Mahindra S101 Fiat Punto Abarth Bajaj Pulsar SS400 Honda CBR500R

Upcoming bike launchesUpcoming car Launches

Source: www.carwale.com, www.bikewale.com, ICICIdirect.com Research

Page 11ICICI Securities Ltd | Retail Equity Research

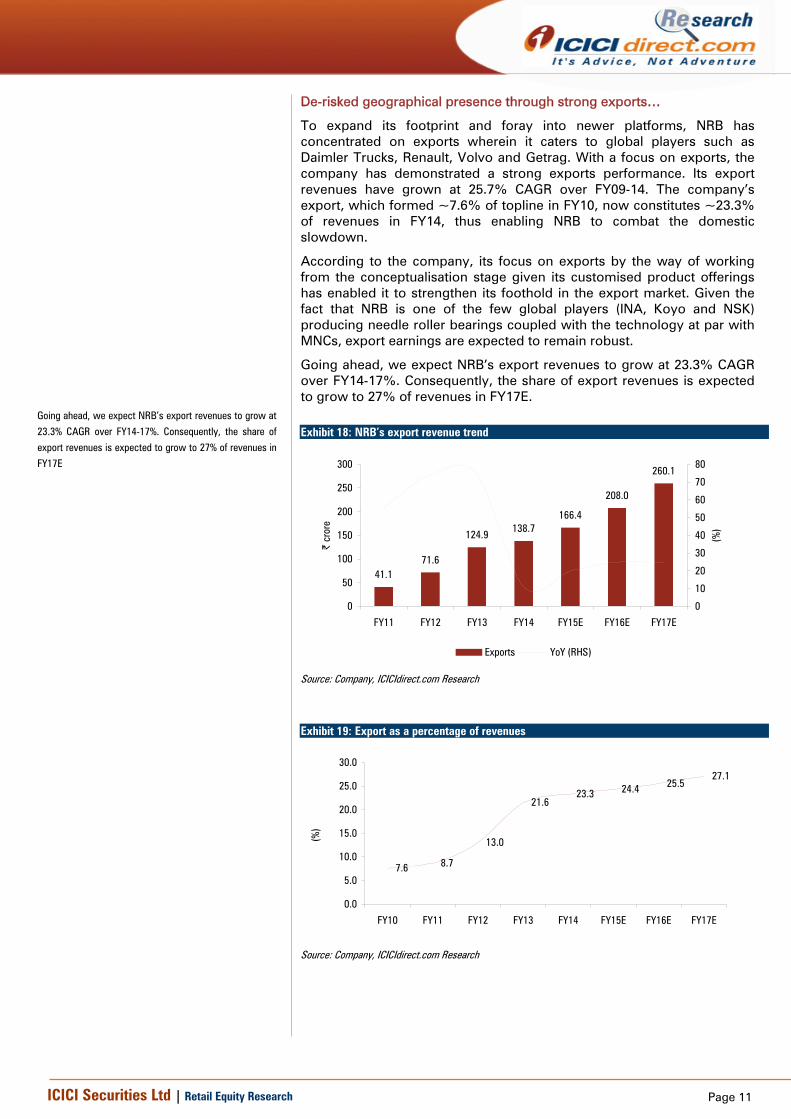

De-risked geographical presence through strong exports…

To expand its footprint and foray into newer platforms, NRB has concentrated on exports wherein it caters to global players such as Daimler Trucks, Renault, Volvo and Getrag. With a focus on exports, the company has demonstrated a strong exports performance. Its export revenues have grown at 25.7% CAGR over FY09-14. The company’s export, which formed ~7.6% of topline in FY10, now constitutes ~23.3% of revenues in FY14, thus enabling NRB to combat the domestic slowdown.

According to the company, its focus on exports by the way of working from the conceptualisation stage given its customised product offerings has enabled it to strengthen its foothold in the export market. Given the fact that NRB is one of the few global players (INA, Koyo and NSK) producing needle roller bearings coupled with the technology at par with MNCs, export earnings are expected to remain robust.

Going ahead, we expect NRB’s export revenues to grow at 23.3% CAGR over FY14-17%. Consequently, the share of export revenues is expected to grow to 27% of revenues in FY17E.

Exhibit 18: NRB’s export revenue trend

41.171.6

124.9 138.7166.4

208.0

260.1

0

50

100

150

200

250

300

FY11 FY12 FY13 FY14 FY15E FY16E FY17E

| cr

ore

0

10

20

30

40

50

60

70

80

(%)

Exports YoY (RHS)

Source: Company, ICICIdirect.com Research

Exhibit 19: Export as a percentage of revenues

7.6 8.7

13.0

21.623.3 24.4 25.5

27.1

0.0

5.0

10.0

15.0

20.0

25.0

30.0

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

(%)

Source: Company, ICICIdirect.com Research

Going ahead, we expect NRB’s export revenues to grow at

23.3% CAGR over FY14-17%. Consequently, the share of

export revenues is expected to grow to 27% of revenues in

FY17E

Page 12ICICI Securities Ltd | Retail Equity Research

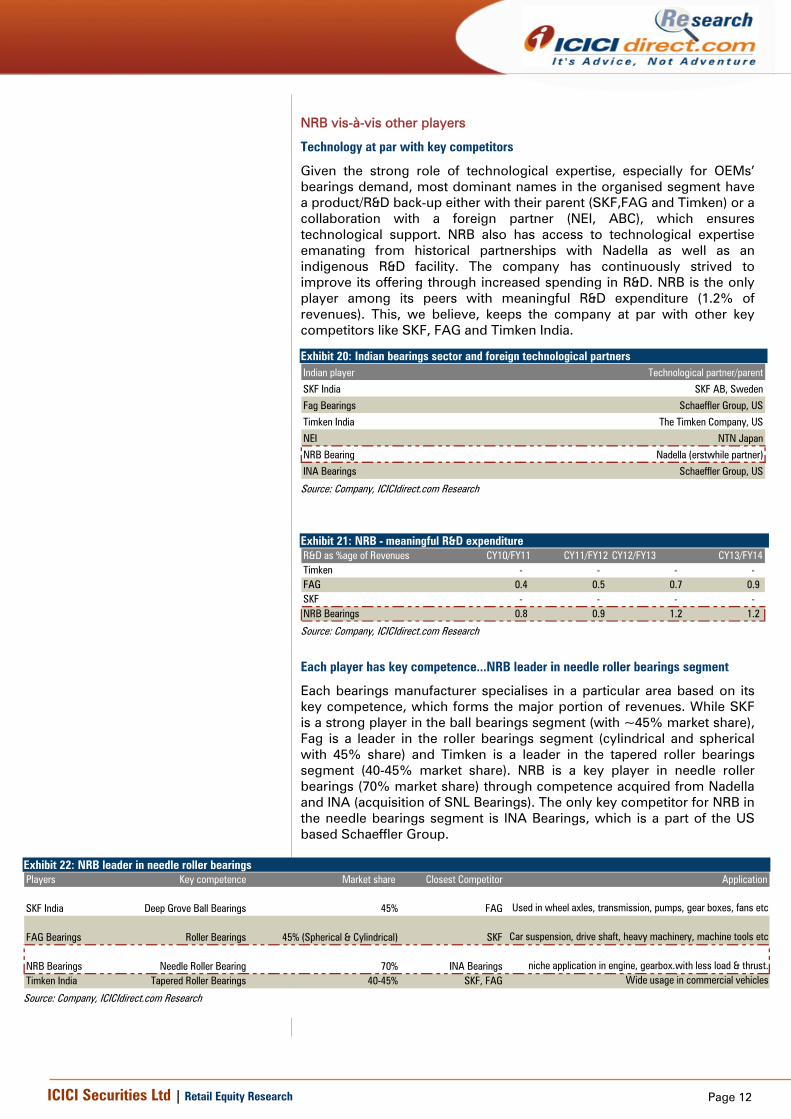

NRB vis-à-vis other players

Technology at par with key competitors

Given the strong role of technological expertise, especially for OEMs’ bearings demand, most dominant names in the organised segment have a product/R&D back-up either with their parent (SKF,FAG and Timken) or a collaboration with a foreign partner (NEI, ABC), which ensures technological support. NRB also has access to technological expertise emanating from historical partnerships with Nadella as well as an indigenous R&D facility. The company has continuously strived to improve its offering through increased spending in R&D. NRB is the only player among its peers with meaningful R&D expenditure (1.2% of revenues). This, we believe, keeps the company at par with other key competitors like SKF, FAG and Timken India.

Exhibit 20: Indian bearings sector and foreign technological partners Indian player Technological partner/parent

SKF India SKF AB, Sweden

Fag Bearings Schaeffler Group, US

Timken India The Timken Company, US

NEI NTN Japan

NRB Bearing Nadella (erstwhile partner)

INA Bearings Schaeffler Group, US

Source: Company, ICICIdirect.com Research

Exhibit 21: NRB - meaningful R&D expenditure R&D as %age of Revenues CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14Timken - - - - FAG 0.4 0.5 0.7 0.9 SKF - - - - NRB Bearings 0.8 0.9 1.2 1.2

Source: Company, ICICIdirect.com Research

Each player has key competence...NRB leader in needle roller bearings segment

Each bearings manufacturer specialises in a particular area based on its key competence, which forms the major portion of revenues. While SKF is a strong player in the ball bearings segment (with ~45% market share), Fag is a leader in the roller bearings segment (cylindrical and spherical with 45% share) and Timken is a leader in the tapered roller bearings segment (40-45% market share). NRB is a key player in needle roller bearings (70% market share) through competence acquired from Nadella and INA (acquisition of SNL Bearings). The only key competitor for NRB in the needle bearings segment is INA Bearings, which is a part of the US based Schaeffler Group.

Exhibit 22: NRB leader in needle roller bearings Players Key competence Market share Closest Competitor Application

SKF India Deep Grove Ball Bearings 45% FAG Used in wheel axles, transmission, pumps, gear boxes, fans etc

FAG Bearings Roller Bearings 45% (Spherical & Cylindrical) SKF Car suspension, drive shaft, heavy machinery, machine tools etc

NRB Bearings Needle Roller Bearing 70% INA Bearings niche application in engine, gearbox.with less load & thrust.Timken India Tapered Roller Bearings 40-45% SKF, FAG Wide usage in commercial vehicles

Source: Company, ICICIdirect.com Research

Page 13ICICI Securities Ltd | Retail Equity Research

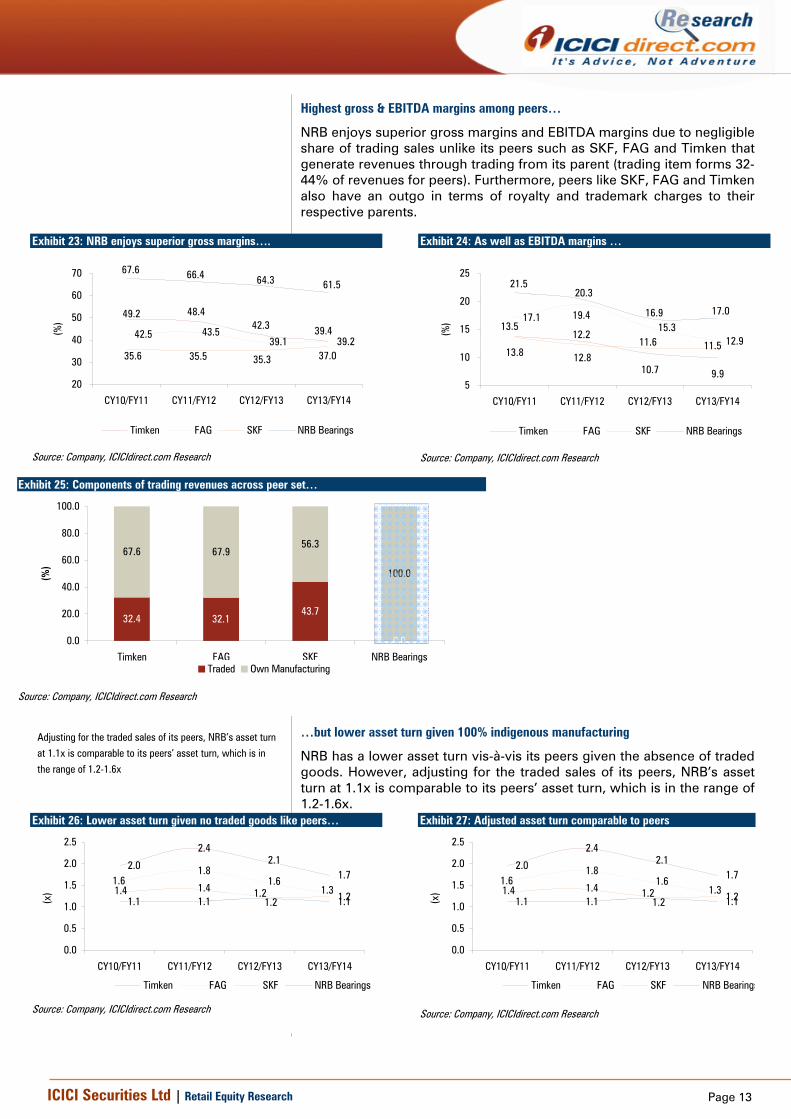

Highest gross & EBITDA margins among peers…

NRB enjoys superior gross margins and EBITDA margins due to negligible share of trading sales unlike its peers such as SKF, FAG and Timken that generate revenues through trading from its parent (trading item forms 32-44% of revenues for peers). Furthermore, peers like SKF, FAG and Timken also have an outgo in terms of royalty and trademark charges to their respective parents.

Exhibit 23: NRB enjoys superior gross margins….

42.5 43.539.1 39.2

39.442.348.449.2

35.6 35.5 35.3 37.0

61.564.366.467.6

20

30

40

50

60

70

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

(%)

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Exhibit 24: As well as EBITDA margins …

17.115.3

12.913.8 12.8

10.7 9.9

19.4

11.511.612.2

13.5

21.520.3

16.9 17.0

5

10

15

20

25

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

(%)

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Exhibit 25: Components of trading revenues across peer set…

32.4 32.143.7

0.0

67.6 67.956.3

100.0

0.0

20.0

40.0

60.0

80.0

100.0

Timken FAG SKF NRB Bearings

(%)

Traded Own Manufacturing

Source: Company, ICICIdirect.com Research

…but lower asset turn given 100% indigenous manufacturing

NRB has a lower asset turn vis-à-vis its peers given the absence of traded goods. However, adjusting for the traded sales of its peers, NRB’s asset turn at 1.1x is comparable to its peers’ asset turn, which is in the range of 1.2-1.6x.

Exhibit 26: Lower asset turn given no traded goods like peers…

2.0

2.42.1

1.71.81.6

1.21.1 1.1 1.11.3

1.6

1.21.41.4 1.2

0.0

0.5

1.0

1.5

2.0

2.5

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

(x)

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Exhibit 27: Adjusted asset turn comparable to peers

2.0

2.42.1

1.71.81.6

1.21.1 1.1 1.11.3

1.6

1.21.41.4 1.2

0.0

0.5

1.0

1.5

2.0

2.5

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

(x)

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Adjusting for the traded sales of its peers, NRB’s asset turn

at 1.1x is comparable to its peers’ asset turn, which is in

the range of 1.2-1.6x

Page 14ICICI Securities Ltd | Retail Equity Research

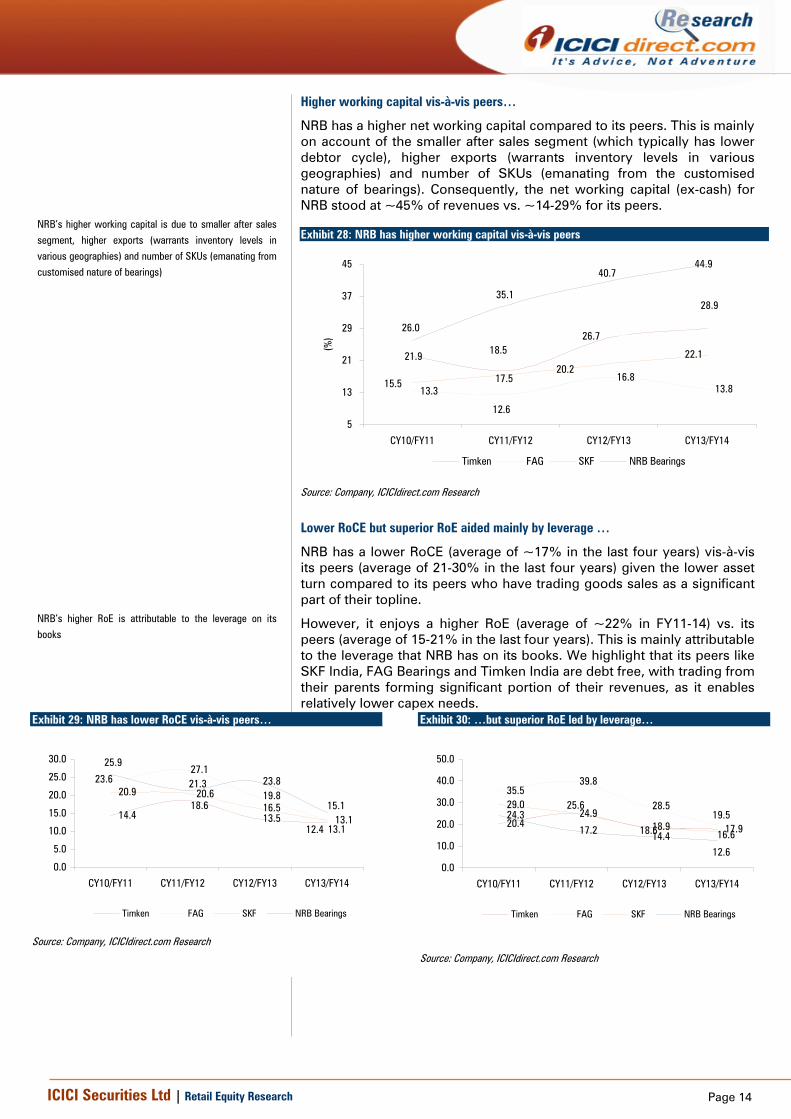

Higher working capital vis-à-vis peers…

NRB has a higher net working capital compared to its peers. This is mainly on account of the smaller after sales segment (which typically has lower debtor cycle), higher exports (warrants inventory levels in various geographies) and number of SKUs (emanating from the customised nature of bearings). Consequently, the net working capital (ex-cash) for NRB stood at ~45% of revenues vs. ~14-29% for its peers.

Exhibit 28: NRB has higher working capital vis-à-vis peers

13.316.8

13.8

28.9

26.718.521.9

12.6

15.5 17.520.2

22.1

44.940.7

35.1

26.0

5

13

21

29

37

45

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

(%)

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Lower RoCE but superior RoE aided mainly by leverage …

NRB has a lower RoCE (average of ~17% in the last four years) vis-à-vis its peers (average of 21-30% in the last four years) given the lower asset turn compared to its peers who have trading goods sales as a significant part of their topline.

However, it enjoys a higher RoE (average of ~22% in FY11-14) vs. its peers (average of 15-21% in the last four years). This is mainly attributable to the leverage that NRB has on its books. We highlight that its peers like SKF India, FAG Bearings and Timken India are debt free, with trading from their parents forming significant portion of their revenues, as it enables relatively lower capex needs.

Exhibit 29: NRB has lower RoCE vis-à-vis peers…

14.4 13.5

27.1

19.8

13.1

20.916.5

23.8

18.6

12.4

23.620.6

13.1

15.1

25.9

21.3

0.0

5.0

10.0

15.0

20.0

25.0

30.0

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

Exhibit 30: …but superior RoE led by leverage…

20.424.9

18.9 17.9

35.539.8

28.529.024.3

17.2 14.4

19.5

16.6

25.6

18.6

12.60.0

10.0

20.0

30.0

40.0

50.0

CY10/FY11 CY11/FY12 CY12/FY13 CY13/FY14

Timken FAG SKF NRB Bearings

Source: Company, ICICIdirect.com Research

NRB’s higher working capital is due to smaller after sales

segment, higher exports (warrants inventory levels in

various geographies) and number of SKUs (emanating from

customised nature of bearings)

NRB’s higher RoE is attributable to the leverage on its

books

Page 15ICICI Securities Ltd | Retail Equity Research

Subsidiaries form insignificant part…

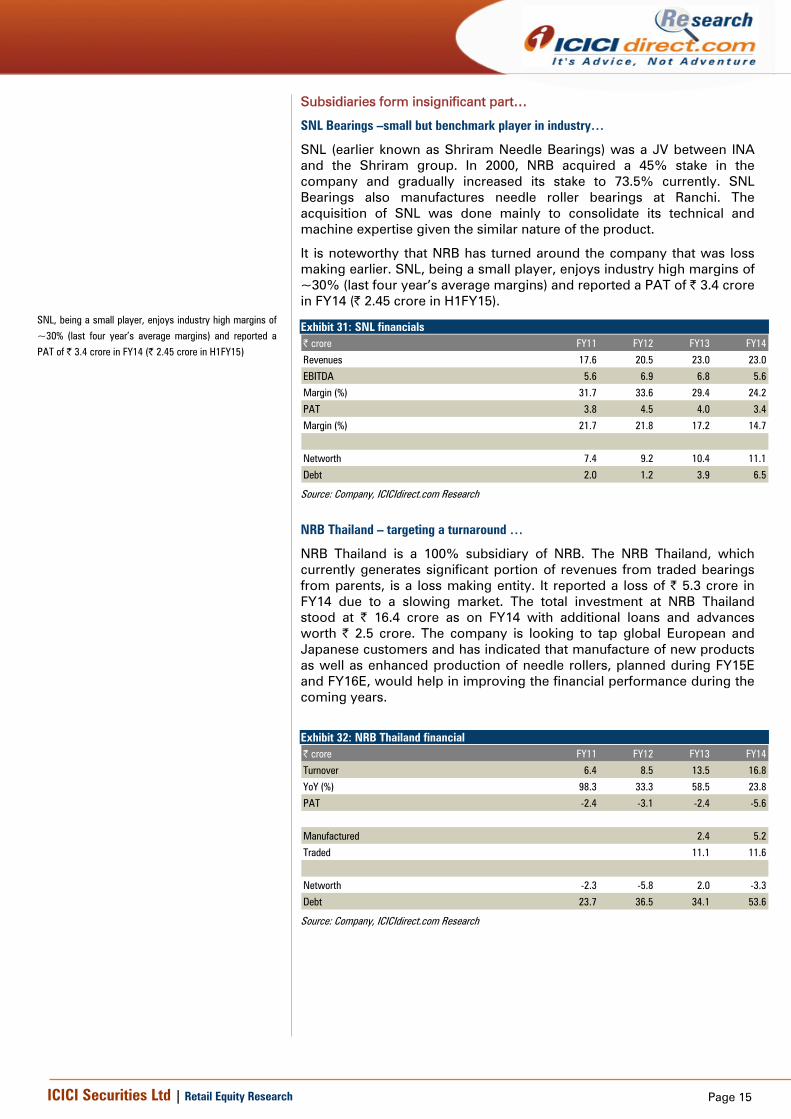

SNL Bearings –small but benchmark player in industry…

SNL (earlier known as Shriram Needle Bearings) was a JV between INA and the Shriram group. In 2000, NRB acquired a 45% stake in the company and gradually increased its stake to 73.5% currently. SNL Bearings also manufactures needle roller bearings at Ranchi. The acquisition of SNL was done mainly to consolidate its technical and machine expertise given the similar nature of the product.

It is noteworthy that NRB has turned around the company that was loss making earlier. SNL, being a small player, enjoys industry high margins of ~30% (last four year’s average margins) and reported a PAT of | 3.4 crore in FY14 (| 2.45 crore in H1FY15).

Exhibit 31: SNL financials | crore FY11 FY12 FY13 FY14

Revenues 17.6 20.5 23.0 23.0

EBITDA 5.6 6.9 6.8 5.6

Margin (%) 31.7 33.6 29.4 24.2

PAT 3.8 4.5 4.0 3.4

Margin (%) 21.7 21.8 17.2 14.7

Networth 7.4 9.2 10.4 11.1

Debt 2.0 1.2 3.9 6.5

Source: Company, ICICIdirect.com Research

NRB Thailand – targeting a turnaround …

NRB Thailand is a 100% subsidiary of NRB. The NRB Thailand, which currently generates significant portion of revenues from traded bearings from parents, is a loss making entity. It reported a loss of | 5.3 crore in FY14 due to a slowing market. The total investment at NRB Thailand stood at | 16.4 crore as on FY14 with additional loans and advances worth | 2.5 crore. The company is looking to tap global European and Japanese customers and has indicated that manufacture of new products as well as enhanced production of needle rollers, planned during FY15E and FY16E, would help in improving the financial performance during the coming years.

Exhibit 32: NRB Thailand financial | crore FY11 FY12 FY13 FY14

Turnover 3.2322 6.4 8.5 13.5 16.8

YoY (%) 98.3 33.3 58.5 23.8

PAT -2.4 -3.1 -2.4 -5.6

Manufactured 2.4 5.2

Traded 11.1 11.6

Networth -2.3 -5.8 2.0 -3.3

Debt 23.7 36.5 34.1 53.6

Source: Company, ICICIdirect.com Research

SNL, being a small player, enjoys industry high margins of

~30% (last four year’s average margins) and reported a

PAT of | 3.4 crore in FY14 (| 2.45 crore in H1FY15)

Page 16ICICI Securities Ltd | Retail Equity Research

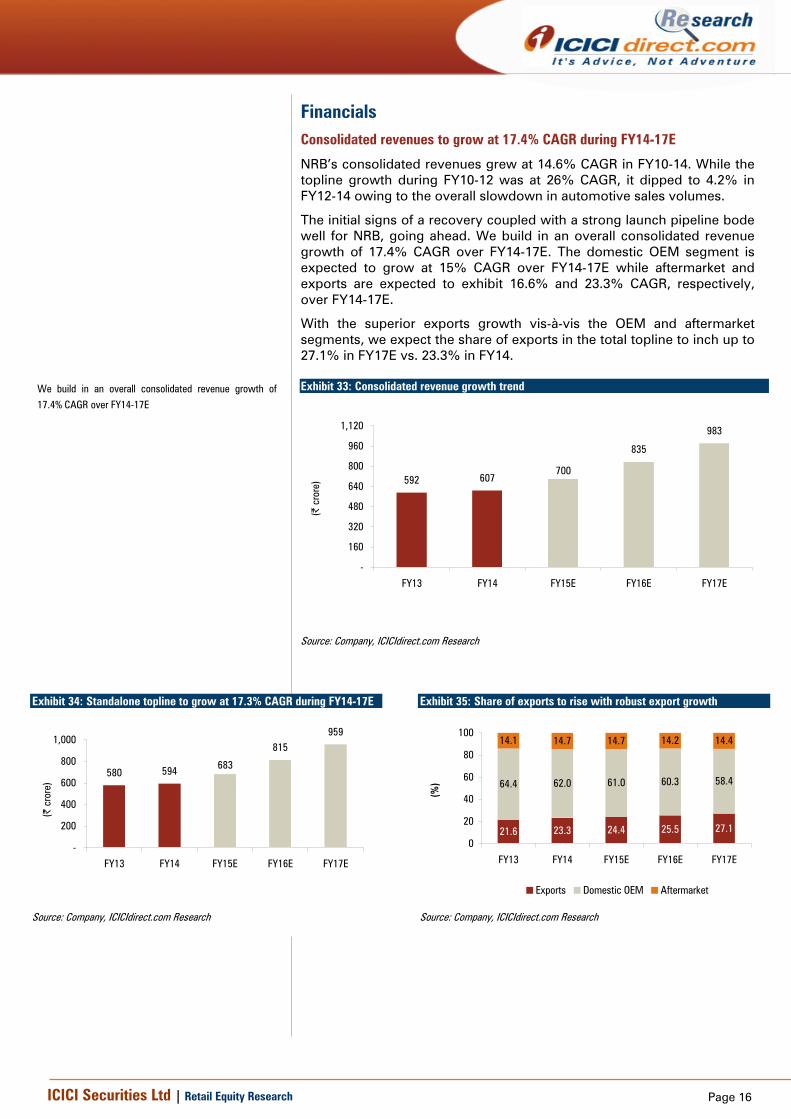

Financials Consolidated revenues to grow at 17.4% CAGR during FY14-17E

NRB’s consolidated revenues grew at 14.6% CAGR in FY10-14. While the topline growth during FY10-12 was at 26% CAGR, it dipped to 4.2% in FY12-14 owing to the overall slowdown in automotive sales volumes.

The initial signs of a recovery coupled with a strong launch pipeline bode well for NRB, going ahead. We build in an overall consolidated revenue growth of 17.4% CAGR over FY14-17E. The domestic OEM segment is expected to grow at 15% CAGR over FY14-17E while aftermarket and exports are expected to exhibit 16.6% and 23.3% CAGR, respectively, over FY14-17E.

With the superior exports growth vis-à-vis the OEM and aftermarket segments, we expect the share of exports in the total topline to inch up to 27.1% in FY17E vs. 23.3% in FY14.

Exhibit 33: Consolidated revenue growth trend

592 607

835

983

700

-

160

320

480

640

800

960

1,120

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Exhibit 34: Standalone topline to grow at 17.3% CAGR during FY14-17E

580 594

815959

683

-

200

400

600

800

1,000

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Exhibit 35: Share of exports to rise with robust export growth

21.6 23.3 24.4 25.5 27.1

64.4 62.0 61.0 60.3 58.4

14.1 14.7 14.7 14.2 14.4

0

20

40

60

80

100

FY13 FY14 FY15E FY16E FY17E

(%)

Exports Domestic OEM Aftermarket

Source: Company, ICICIdirect.com Research

We build in an overall consolidated revenue growth of

17.4% CAGR over FY14-17E

Page 17ICICI Securities Ltd | Retail Equity Research

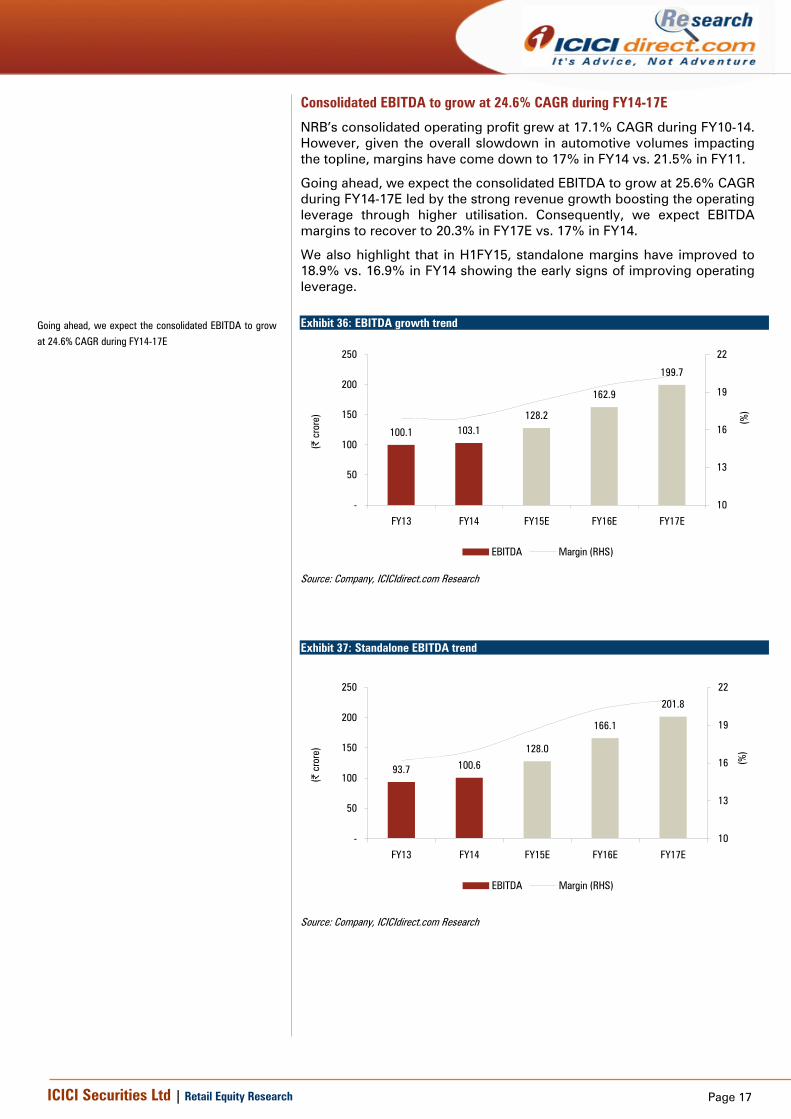

Consolidated EBITDA to grow at 24.6% CAGR during FY14-17E

NRB’s consolidated operating profit grew at 17.1% CAGR during FY10-14. However, given the overall slowdown in automotive volumes impacting the topline, margins have come down to 17% in FY14 vs. 21.5% in FY11.

Going ahead, we expect the consolidated EBITDA to grow at 25.6% CAGR during FY14-17E led by the strong revenue growth boosting the operating leverage through higher utilisation. Consequently, we expect EBITDA margins to recover to 20.3% in FY17E vs. 17% in FY14.

We also highlight that in H1FY15, standalone margins have improved to 18.9% vs. 16.9% in FY14 showing the early signs of improving operating leverage.

Exhibit 36: EBITDA growth trend

100.1 103.1128.2

162.9

199.7

-

50

100

150

200

250

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

10

13

16

19

22

(%)

EBITDA Margin (RHS)

Source: Company, ICICIdirect.com Research

Exhibit 37: Standalone EBITDA trend

93.7 100.6

128.0

166.1

201.8

-

50

100

150

200

250

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

10

13

16

19

22

(%)

EBITDA Margin (RHS)

Source: Company, ICICIdirect.com Research

Going ahead, we expect the consolidated EBITDA to grow

at 24.6% CAGR during FY14-17E

Page 18ICICI Securities Ltd | Retail Equity Research

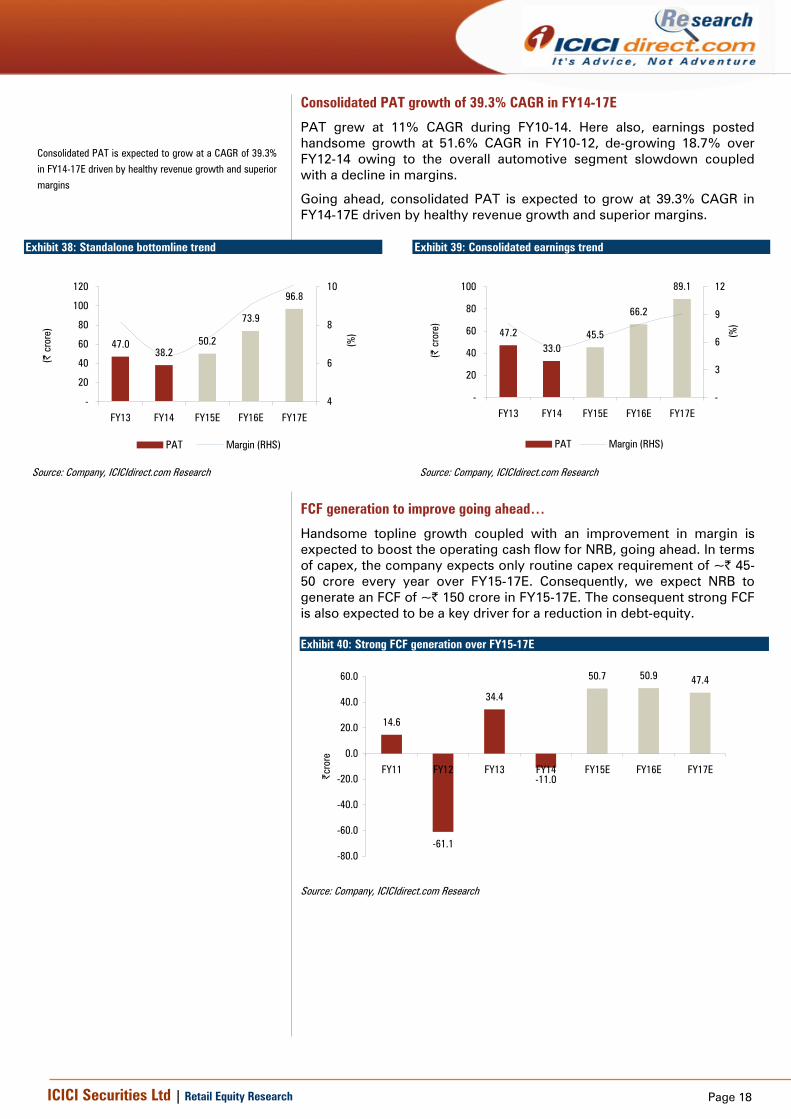

Consolidated PAT growth of 39.3% CAGR in FY14-17E

PAT grew at 11% CAGR during FY10-14. Here also, earnings posted handsome growth at 51.6% CAGR in FY10-12, de-growing 18.7% over FY12-14 owing to the overall automotive segment slowdown coupled with a decline in margins.

Going ahead, consolidated PAT is expected to grow at 39.3% CAGR in FY14-17E driven by healthy revenue growth and superior margins.

Exhibit 38: Standalone bottomline trend

47.038.2

50.2

73.9

96.8

-

20

40

60

80

100

120

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

4

6

8

10

(%)

PAT Margin (RHS)

Source: Company, ICICIdirect.com Research

Exhibit 39: Consolidated earnings trend

47.233.0

45.5

66.2

89.1

-

20

40

60

80

100

FY13 FY14 FY15E FY16E FY17E

(| c

rore

)

-

3

6

9

12

(%)

PAT Margin (RHS)

Source: Company, ICICIdirect.com Research

FCF generation to improve going ahead…

Handsome topline growth coupled with an improvement in margin is expected to boost the operating cash flow for NRB, going ahead. In terms of capex, the company expects only routine capex requirement of ~| 45-50 crore every year over FY15-17E. Consequently, we expect NRB to generate an FCF of ~| 150 crore in FY15-17E. The consequent strong FCF is also expected to be a key driver for a reduction in debt-equity. Exhibit 40: Strong FCF generation over FY15-17E

14.6

-61.1

34.4

-11.0

50.7 50.9 47.4

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

FY11 FY12 FY13 FY14 FY15E FY16E FY17E|cro

re

Source: Company, ICICIdirect.com Research

Consolidated PAT is expected to grow at a CAGR of 39.3%

in FY14-17E driven by healthy revenue growth and superior

margins

Page 19ICICI Securities Ltd | Retail Equity Research

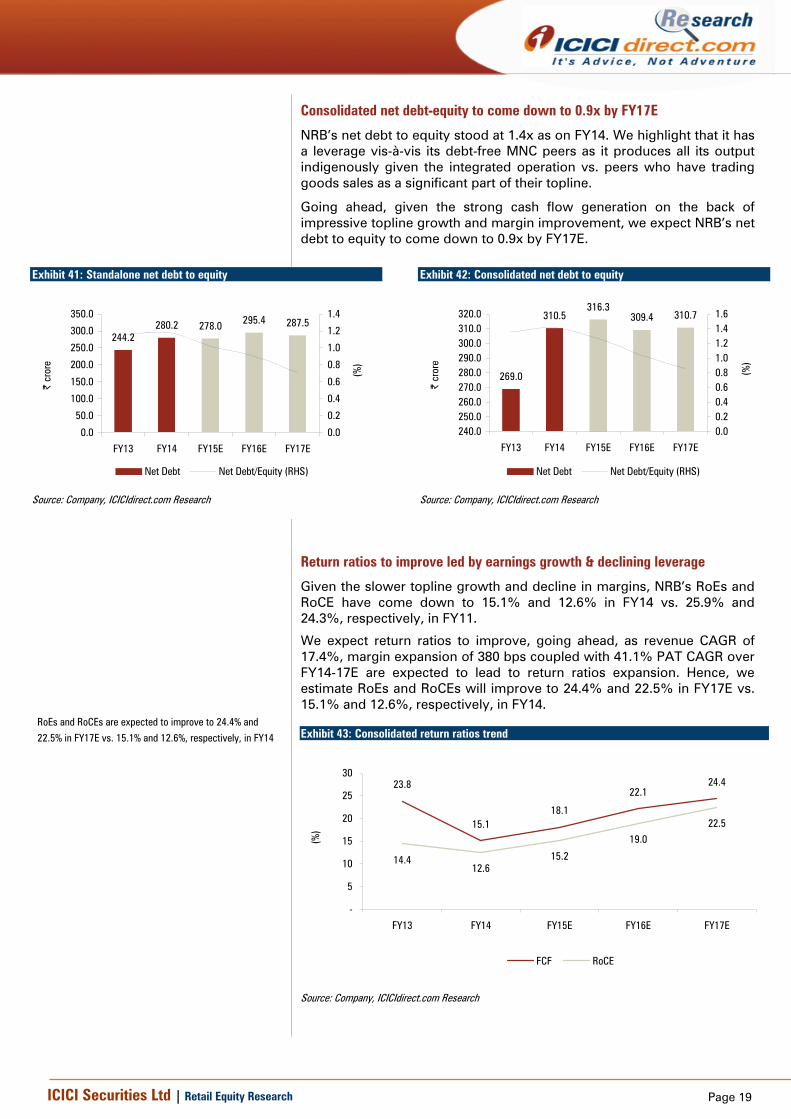

Consolidated net debt-equity to come down to 0.9x by FY17E

NRB’s net debt to equity stood at 1.4x as on FY14. We highlight that it has a leverage vis-à-vis its debt-free MNC peers as it produces all its output indigenously given the integrated operation vs. peers who have trading goods sales as a significant part of their topline.

Going ahead, given the strong cash flow generation on the back of impressive topline growth and margin improvement, we expect NRB’s net debt to equity to come down to 0.9x by FY17E.

Exhibit 41: Standalone net debt to equity

244.2280.2 278.0 295.4 287.5

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

FY13 FY14 FY15E FY16E FY17E

| cr

ore

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

(%)

Net Debt Net Debt/Equity (RHS)

Source: Company, ICICIdirect.com Research

Exhibit 42: Consolidated net debt to equity

269.0

310.5316.3

309.4 310.7

240.0250.0260.0270.0280.0290.0300.0310.0320.0

FY13 FY14 FY15E FY16E FY17E|

cror

e0.00.20.40.60.81.01.21.41.6

(%)

Net Debt Net Debt/Equity (RHS)

Source: Company, ICICIdirect.com Research

Return ratios to improve led by earnings growth & declining leverage

Given the slower topline growth and decline in margins, NRB’s RoEs and RoCE have come down to 15.1% and 12.6% in FY14 vs. 25.9% and 24.3%, respectively, in FY11.

We expect return ratios to improve, going ahead, as revenue CAGR of 17.4%, margin expansion of 380 bps coupled with 41.1% PAT CAGR over FY14-17E are expected to lead to return ratios expansion. Hence, we estimate RoEs and RoCEs will improve to 24.4% and 22.5% in FY17E vs. 15.1% and 12.6%, respectively, in FY14.

Exhibit 43: Consolidated return ratios trend

23.8

15.118.1

22.124.4

14.412.6

15.2

19.022.5

-

5

10

15

20

25

30

FY13 FY14 FY15E FY16E FY17E

(%)

FCF RoCE

Source: Company, ICICIdirect.com Research

RoEs and RoCEs are expected to improve to 24.4% and

22.5% in FY17E vs. 15.1% and 12.6%, respectively, in FY14

Page 20ICICI Securities Ltd | Retail Equity Research

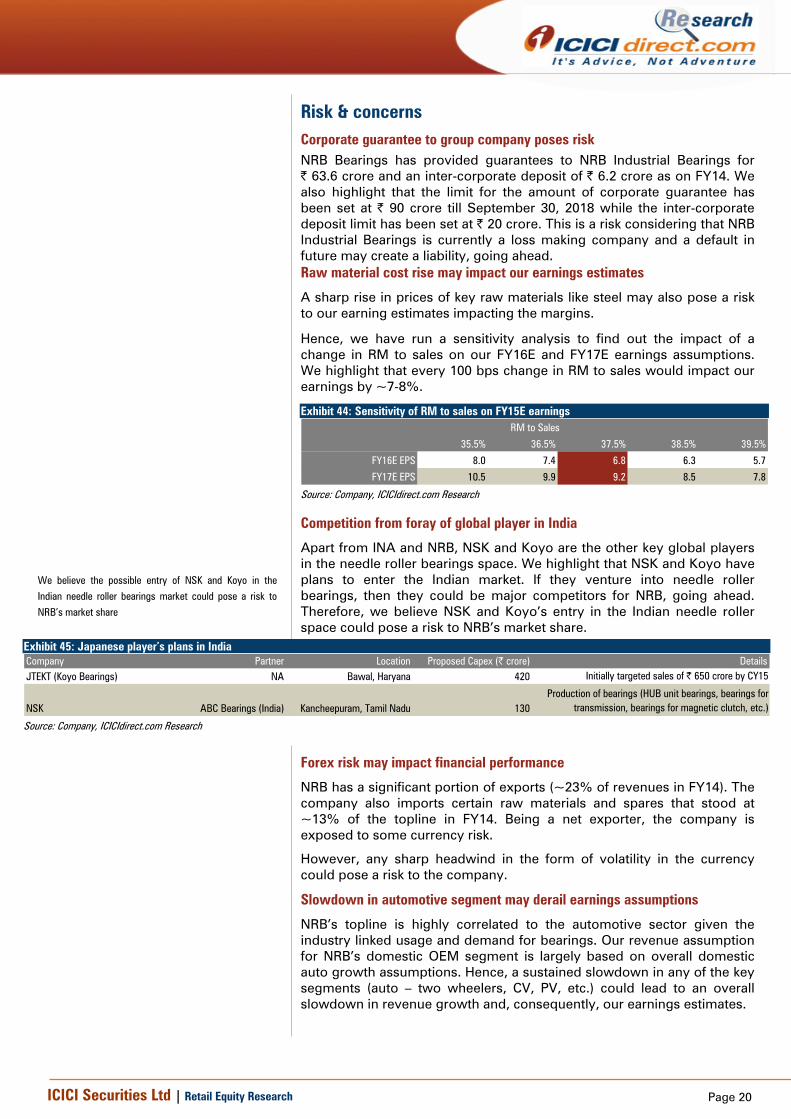

Risk & concerns Corporate guarantee to group company poses risk NRB Bearings has provided guarantees to NRB Industrial Bearings for | 63.6 crore and an inter-corporate deposit of | 6.2 crore as on FY14. We also highlight that the limit for the amount of corporate guarantee has been set at | 90 crore till September 30, 2018 while the inter-corporate deposit limit has been set at | 20 crore. This is a risk considering that NRB Industrial Bearings is currently a loss making company and a default in future may create a liability, going ahead. Raw material cost rise may impact our earnings estimates

A sharp rise in prices of key raw materials like steel may also pose a risk to our earning estimates impacting the margins.

Hence, we have run a sensitivity analysis to find out the impact of a change in RM to sales on our FY16E and FY17E earnings assumptions. We highlight that every 100 bps change in RM to sales would impact our earnings by ~7-8%.

Exhibit 44: Sensitivity of RM to sales on FY15E earnings

35.5% 36.5% 37.5% 38.5% 39.5%

FY16E EPS 8.0 7.4 6.8 6.3 5.7

FY17E EPS 10.5 9.9 9.2 8.5 7.8

RM to Sales

Source: Company, ICICIdirect.com Research

Competition from foray of global player in India

Apart from INA and NRB, NSK and Koyo are the other key global players in the needle roller bearings space. We highlight that NSK and Koyo have plans to enter the Indian market. If they venture into needle roller bearings, then they could be major competitors for NRB, going ahead. Therefore, we believe NSK and Koyo’s entry in the Indian needle roller space could pose a risk to NRB’s market share.

Exhibit 45: Japanese player’s plans in India Company Partner Location Proposed Capex (| crore) DetailsJTEKT (Koyo Bearings) NA Bawal, Haryana 420 Initially targeted sales of | 650 crore by CY15

NSK ABC Bearings (India) Kancheepuram, Tamil Nadu 130Production of bearings (HUB unit bearings, bearings for

transmission, bearings for magnetic clutch, etc.)

Source: Company, ICICIdirect.com Research

Forex risk may impact financial performance

NRB has a significant portion of exports (~23% of revenues in FY14). The company also imports certain raw materials and spares that stood at ~13% of the topline in FY14. Being a net exporter, the company is exposed to some currency risk.

However, any sharp headwind in the form of volatility in the currency could pose a risk to the company.

Slowdown in automotive segment may derail earnings assumptions

NRB’s topline is highly correlated to the automotive sector given the industry linked usage and demand for bearings. Our revenue assumption for NRB’s domestic OEM segment is largely based on overall domestic auto growth assumptions. Hence, a sustained slowdown in any of the key segments (auto – two wheelers, CV, PV, etc.) could lead to an overall slowdown in revenue growth and, consequently, our earnings estimates.

We believe the possible entry of NSK and Koyo in the

Indian needle roller bearings market could pose a risk to

NRB’s market share

Page 21ICICI Securities Ltd | Retail Equity Research

Valuation NRB has been a key player in the domestic bearings industry considering its leadership position in needle roller bearings. Being an automotive centric supplier with customised product offerings, the company also enjoys a sticky client relationship like its MNC peers such as SKF, FAG & Timken and has a presence across all leading OEM players in India.

NRB has consistently demonstrated a handsome financial performance with revenues and earnings CAGR of 15.6% and 65.9%, respectively, in FY09-14. Going ahead, with the overall improvement in the economy and other macro factors such as easing of inflation and lowering of interest rates, automotive volumes are expected to bounce back. NRB, being an important player in the automotive bearings space with a leadership position in needle roller bearings, is expected to be a key beneficiary. We also expect NRB’s export revenues to grow at 23.3% CAGR in FY14-17E as the company continues to expand its footprint in newer geographies.

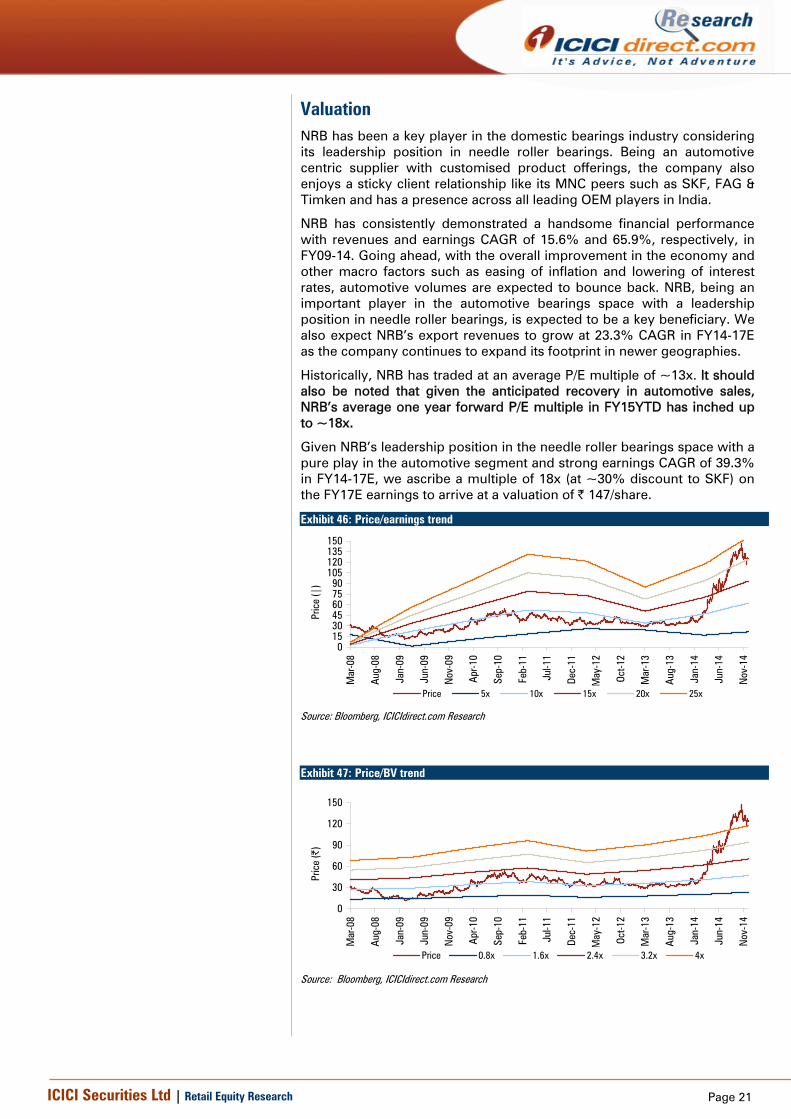

Historically, NRB has traded at an average P/E multiple of ~13x. It should also be noted that given the anticipated recovery in automotive sales, NRB’s average one year forward P/E multiple in FY15YTD has inched up to ~18x.

Given NRB’s leadership position in the needle roller bearings space with a pure play in the automotive segment and strong earnings CAGR of 39.3% in FY14-17E, we ascribe a multiple of 18x (at ~30% discount to SKF) on the FY17E earnings to arrive at a valuation of | 147/share.

Exhibit 46: Price/earnings trend

0153045607590

105120135150

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-1

0

Sep-

10

Feb-

11

Jul-1

1

Dec-

11

May

-12

Oct-1

2

Mar

-13

Aug-

13

Jan-

14

Jun-

14

Nov

-14

Pric

e (|

)

Price 5x 10x 15x 20x 25x

Source: Bloomberg, ICICIdirect.com Research

Exhibit 47: Price/BV trend

0

30

60

90

120

150

Mar

-08

Aug-

08

Jan-

09

Jun-

09

Nov

-09

Apr-1

0

Sep-

10

Feb-

11

Jul-1

1

Dec-

11

May

-12

Oct-1

2

Mar

-13

Aug-

13

Jan-

14

Jun-

14

Nov

-14

Pric

e (|

)

Price 0.8x 1.6x 2.4x 3.2x 4x

Source: Bloomberg, ICICIdirect.com Research

Page 22ICICI Securities Ltd | Retail Equity Research

Exhibit 48: I-direct estimate vs. consensus | crore Consensus I-Direct Deviation over consensus (%)

Revenues

FY15E 712.7 700.4 -1.7

FY16E 851.2 835.1 -1.9

FY17E 990.2 982.7 -0.8

EBITDA

FY15E 134.5 128.2 -4.7

FY16E 164.7 162.9 -1.1

FY17E 194.4 199.7 2.7

PAT

FY15E 57.5 45.5 -20.9

FY16E 76.0 66.2 -12.9

FY17E 96.8 89.1 -7.9

Source: Bloomberg. ICICIdirect.com Research

Peer matrix

We highlight that with an expected recovery in economic growth, the overall bearings pack multiples have got re-rated over the last six months. Given the lower base and expected earnings growth over the next two or three years, the premium multiples seem justified.

We also highlight that given the leverage on the books coupled with the leadership position of its peers, NRB is trading at a discount to leading MNC players such as SKF India and FAG Bearings.

Exhibit 49: Peer matrix

M Cap

(| Cr) CY14E CY15E CY16E CY14E CY15E CY16E CY14E CY15E CY16E CY14E CY15E CY16E CY14E CY15E CY16E

SKF India 7050 42.4 50.0 60.3 32.4 27.5 22.8 21.2 17.7 14.3 15.9 16.7 17.6 18.9 20.2 21.7

FAG Bearings 5783 98.6 127.1 143.3 35.3 27.4 24.3 22.4 18.3 14.0 15.6 17.3 18.4 14.9 17.5 18.4

NRB Bearings 1280 4.7 6.8 9.2 27.5 18.9 14.0 14.8 11.6 9.5 18.1 22.1 24.4 15.2 19.0 22.5

RoE (%) RoCE (%)

Company

EPS (|) P/E (x) EV/EBITDA (x)

Source: Company, Bloomberg, ICICIdirect.com Research *The estimates for NRB Bearings is for FY15E, FY16E and FY17E respectively

Page 23ICICI Securities Ltd | Retail Equity Research

Sensitivity analysis

We highlight that revenue growth explanation remains the major driver of valuations. Every 200 bps change in our base revenue growth will have a ~3% impact on our target price assumptions, maintaining the same multiples.

Exhibit 50: Sensitivity of revenue growth to our target price

165 15.2% 17.2% 19.2% 21.2% 23.2%

13.7% 149 153 157 161 165

15.7% 153 157 161 165 169

17.7% 157 161 165 170 174

19.7% 161 165 170 174 178

21.7% 165 170 174 178 182 F

Y17

topl

ine

grow

th

FY16 topline growth

Source: Company, ICICdirect.com Research

Every 100 bps change in margins from our base assumptions would have a 7% impact on our target price assumptions.

Exhibit 51: Sensitivity of margins to our target price

18.3% 19.3% 20.3% 21.3% 22.3%

Target Price 141 153 165 178 190

FY17E Margins

Source: Company, ICICIdirect.com Research

Page 24ICICI Securities Ltd | Retail Equity Research

Tables and ratios (Consolidated)

Exhibit 52: Profit & loss account (| Crore) FY13 FY14 FY15E FY16E FY17ETotal Operating Income 591.6 607.5 700.4 835.1 982.7 Other Income 8.9 2.9 3.4 3.8 4.1 Total Revenue 600.5 610.3 703.8 838.9 986.9

Cost of materials consumed 227.6 228.0 262.9 313.5 368.9 Purchase of stock-in-trade 0.4 - - - - Change in inventories (16.4) 5.9 6.8 8.1 9.6 Employee Expenses 102.0 101.0 116.1 133.5 154.9 Other Expenses 177.9 169.4 186.3 217.1 249.6 Total Operating Expenditure 491.6 504.3 572.2 672.3 783.0

EBITDA 100.1 103.1 128.2 162.9 199.7 Interest 18.6 18.6 23.5 23.5 22.1 PBDT 90.3 87.4 108.1 143.1 181.7 Depreciation 32.1 35.6 38.2 41.5 44.8 PBT 58.2 51.8 69.9 101.6 136.9 Total Tax 10.2 18.1 23.4 34.0 45.9 PAT before MI 48.0 33.7 46.5 67.6 91.1 Minority Interest 0.9 0.7 1.0 1.4 2.0 PAT 47.2 33.0 45.5 66.2 89.1

EPS 4.9 3.4 4.7 6.8 9.2

Source: Company’s Annual Report, ICICIdirect.com Research

Exhibit 53: Balance sheet (| Crore) FY13 FY14 FY15E FY16E FY17EEquity Capital 19.4 19.4 19.4 19.4 19.4 Reserve and Surplus 178.6 199.7 231.6 279.8 346.4 Total Shareholders funds 197.9 219.0 251.0 299.2 365.8

Minority Interest 1.7 2.4 3.4 4.8 6.8

Total Debt 272.3 316.2 336.2 336.2 316.2

Deferred Tax Liability 10.2 12.3 12.3 12.3 12.3 Total Liabilities 482.1 550.0 603.0 652.6 701.2 Gross Block 496.1 543.0 583.0 633.0 683.0 Acc: Depreciation 277.9 310.2 348.4 389.9 434.6 Net Block 218.1 232.8 234.6 243.1 248.3 Capital WIP 19.3 38.3 38.3 38.3 38.3 Total Fixed Assets 237.5 271.1 272.9 281.5 286.7 Goodwill on Consolidation 0.5 0.5 0.5 0.5 0.5

Investments 0.1 0.1 0.1 0.1 0.1

Inventory 147.5 145.0 163.1 183.0 215.4 Debtors 151.5 184.2 189.1 208.8 245.7 Loans and Advances 57.0 70.3 81.1 96.7 113.8 Other Current Assets 0.0 0.0 0.0 0.0 0.0 Cash 3.3 5.8 39.4 48.8 31.6 Total Current Assets 359.3 405.3 472.7 537.3 606.4 Current Liabilities 90.1 106.1 122.4 145.9 171.7 Provisions 25.1 20.8 20.8 20.8 20.8 Net Current Assets 244.1 278.4 329.5 370.6 413.9

Total Assets 482.1 550.0 603.0 652.6 701.2

Source: Company’s Annual Report, ICICIdirect.com Research

Page 25ICICI Securities Ltd | Retail Equity Research

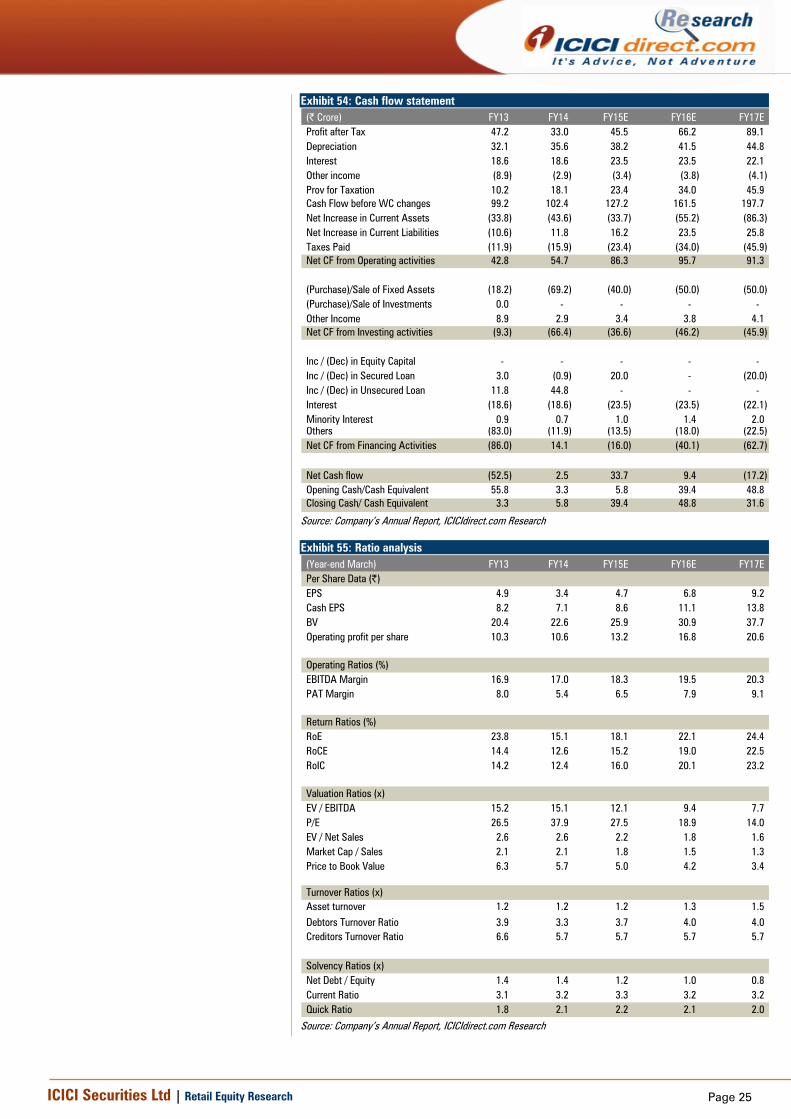

Exhibit 54: Cash flow statement (| Crore) FY13 FY14 FY15E FY16E FY17EProfit after Tax 47.2 33.0 45.5 66.2 89.1 Depreciation 32.1 35.6 38.2 41.5 44.8 Interest 18.6 18.6 23.5 23.5 22.1 Other income (8.9) (2.9) (3.4) (3.8) (4.1) Prov for Taxation 10.2 18.1 23.4 34.0 45.9 Cash Flow before WC changes 99.2 102.4 127.2 161.5 197.7 Net Increase in Current Assets (33.8) (43.6) (33.7) (55.2) (86.3) Net Increase in Current Liabilities (10.6) 11.8 16.2 23.5 25.8 Taxes Paid (11.9) (15.9) (23.4) (34.0) (45.9) Net CF from Operating activities 42.8 54.7 86.3 95.7 91.3

(Purchase)/Sale of Fixed Assets (18.2) (69.2) (40.0) (50.0) (50.0) (Purchase)/Sale of Investments 0.0 - - - - Other Income 8.9 2.9 3.4 3.8 4.1 Net CF from Investing activities (9.3) (66.4) (36.6) (46.2) (45.9)

Inc / (Dec) in Equity Capital - - - - - Inc / (Dec) in Secured Loan 3.0 (0.9) 20.0 - (20.0) Inc / (Dec) in Unsecured Loan 11.8 44.8 - - - Interest (18.6) (18.6) (23.5) (23.5) (22.1) Minority Interest 0.9 0.7 1.0 1.4 2.0 Others (83.0) (11.9) (13.5) (18.0) (22.5) Net CF from Financing Activities (86.0) 14.1 (16.0) (40.1) (62.7)

Net Cash flow (52.5) 2.5 33.7 9.4 (17.2) Opening Cash/Cash Equivalent 55.8 3.3 5.8 39.4 48.8 Closing Cash/ Cash Equivalent 3.3 5.8 39.4 48.8 31.6

Source: Company’s Annual Report, ICICIdirect.com Research

Exhibit 55: Ratio analysis (Year-end March) FY13 FY14 FY15E FY16E FY17EPer Share Data (|)EPS 4.9 3.4 4.7 6.8 9.2 Cash EPS 8.2 7.1 8.6 11.1 13.8 BV 20.4 22.6 25.9 30.9 37.7 Operating profit per share 10.3 10.6 13.2 16.8 20.6

Operating Ratios (%)EBITDA Margin 16.9 17.0 18.3 19.5 20.3 PAT Margin 8.0 5.4 6.5 7.9 9.1

Return Ratios (%)RoE 23.8 15.1 18.1 22.1 24.4 RoCE 14.4 12.6 15.2 19.0 22.5 RoIC 14.2 12.4 16.0 20.1 23.2

Valuation Ratios (x)EV / EBITDA 15.2 15.1 12.1 9.4 7.7 P/E 26.5 37.9 27.5 18.9 14.0 EV / Net Sales 2.6 2.6 2.2 1.8 1.6 Market Cap / Sales 2.1 2.1 1.8 1.5 1.3 Price to Book Value 6.3 5.7 5.0 4.2 3.4

- - - - Turnover Ratios (x)Asset turnover 1.2 1.2 1.2 1.3 1.5 Debtors Turnover Ratio 3.9 3.3 3.7 4.0 4.0 Creditors Turnover Ratio 6.6 5.7 5.7 5.7 5.7

Solvency Ratios (x)Net Debt / Equity 1.4 1.4 1.2 1.0 0.8 Current Ratio 3.1 3.2 3.3 3.2 3.2 Quick Ratio 1.8 2.1 2.2 2.1 2.0

Source: Company’s Annual Report, ICICIdirect.com Research

Page 26ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts' valuation for a stock. Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction; Buy: >10%/15% for large caps/midcaps, respectively; Hold: Up to +/-10%; Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk, ICICI Securities Limited, 1st Floor, Akruti Trade Centre, Road No. 7, MIDC, Andheri (East) Mumbai – 400 093

Page 27ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Chirag Shah PGDBM; Bhupendra Tiwary MBA (FINANCE), Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures: ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which are available on www.icicibank.com. ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current. Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this company, or in certain other circumstances. This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months. ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction. ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned in the report in the past twelve months. ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any material conflict of interest at the time of publication of this report. It is confirmed that Chirag Shah PGDBM; Bhupendra Tiwary MBA (FINANCE), Research Analysts of this report have not received any compensation from the companies mentioned in the report in the preceding twelve months. Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ICICI Securities or its subsidiaries collectively or Research Analysts do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month preceding the publication of the research report. Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. It is confirmed Chirag Shah PGDBM; Bhupendra Tiwary MBA (FINANCE), Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report. ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report. We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

![Reliance Capital Limited - ICICI Directcontent.icicidirect.com/Mailimages/IM_MLD_B275.pdf · email: mohan.vellore@relianceada.com] information memorandum of private placement for](https://img.pdfslide.net/doc/110x75/5eaa30f8b27ced36813c42d2/reliance-capital-limited-icici-email-mohanvellorerelianceadacom-information.jpg)