Embed Size (px)

Citation preview

Capital Market

Assumptions Update Quarter 4, 2015

Prepared by the Asset and Risk Modelling Team

Distribution Technology

10 February 2016

Capital Market Assumptions Update, Q4 2015

ii

Contents 1 Introduction .................................................................................................................................... 1

2 Investment assumptions ................................................................................................................. 2

3 Assumption methodology ............................................................................................................... 3

3.1 Price inflation .......................................................................................................................... 3

3.2 Volatilities and correlations .................................................................................................... 3

3.3 Expected returns ..................................................................................................................... 3

4 Strategic asset allocation .............................................................................................................. 10

5 Efficient frontier ............................................................................................................................ 11

6 Risk profile boundaries ................................................................................................................. 12

Appendix A : Asset classes on risk / reward space ............................................................................... 13

Appendix B : Changes in assumptions per asset classes ....................................................................... 14

Appendix C : DT allocation - projections ............................................................................................... 16

Appendix D : Total expense ratio ......................................................................................................... 18

Capital Market Assumptions Update, Q4 2015

iii

Figures Figure 1: UK gilt yield curve .................................................................................................................... 4

Figure 2: UK index-linked gilt yield curve ................................................................................................ 5

Figure 3: Breakeven Inflation .................................................................................................................. 5

Figure 4: Investment grade credit spreads ............................................................................................. 6

Figure 5: Nominal sovereign yields ......................................................................................................... 6

Figure 6: Nominal yields .......................................................................................................................... 7

Figure 7: Efficient frontier ..................................................................................................................... 11

Figure 8: Asset class assumptions on the risk/reward space ................................................................ 13

Figure 9: Changes in asset class returns ............................................................................................... 14

Figure 10: Changes in asset class volatilities ......................................................................................... 15

Tables Table 1: Investment assumptions ........................................................................................................... 2

Table 2: UK gilt yields .............................................................................................................................. 4

Table 3: Index-linked gilt yields ............................................................................................................... 5

Table 4: Equity assumptions ................................................................................................................... 8

Table 5: Strategic asset allocations ....................................................................................................... 10

Table 6: Risk boundaries ....................................................................................................................... 12

Table 9: Total expense ratios ................................................................................................................ 18

Capital Market Assumptions Update, Q4 2015

1

1 Introduction

This report presents the quarterly review of the financial planning assumptions used within the

Distribution Technology (DT) Planning and Sales and Services Platform (“the Platform”). These

assumptions are used within the Platform to:

Build model portfolios;

Define the portfolio efficient frontier; and

Forecast portfolio outcomes

The review is based on index data analysed up to the end of December 2015 (Q4 2015) and

incorporates the views of major supranational entities where appropriate.

The assumptions and resulting asset allocations have been created with a view that they will be used

in a long term context. This means in the short term, pricing anomalies may exist that change the

relative attractiveness of an asset class.

DT provides this analysis on the understanding that investors will gain access to the outputs through

a regulated advice process. The decision regarding which asset class to include in an investor’s

portfolio as well as the amount to include should be made by advisers with the necessary Financial

Conduct Authority (FCA) permission to give advice on investments in consultation with their client.

DT accepts no liability in respect of any advice given to investors relating to investment strategies or

the purchase of specific products.

The following sections set out the methods that have been adopted and the data used in the analysis

to derive the assumptions.

Capital Market Assumptions Update, Q4 2015

2

2 Investment assumptions

Table 1 provides the real and nominal expected returns assumptions for this quarter as well as the

volatility assumptions.

Real expected

returns (% pa)

Nominal expected

returns (% pa) Volatility (% pa)

Cash -0.6% 1.9% 1.5%

UK corporate bonds 1.2% 3.7% 6.4%

UK index-linked gilts -0.7% 1.8% 7.6%

International bonds -0.7% 1.8% 8.2%

UK gilts -0.2% 2.3% 6.0%

Global high yield bonds 3.6% 6.1% 10.8%

UK equity 4.3% 6.8% 14.0%

Europe ex UK equity 4.5% 7.0% 19.1%

North American equity 4.1% 6.6% 15.2%

Japanese equity 2.8% 5.3% 16.2%

Asia Pacific ex Japan equity 5.6% 8.1% 18.6%

Emerging Market equity 6.5% 9.0% 21.2%

UK commercial property 2.2% 4.7% 10.7%

Commodities 3.4% 5.9% 20.4%

Absolute return 1.0% 3.5% 8.6%

Unclassified 2.0% 4.5% 7.2%

Table 1: Investment assumptions

Capital Market Assumptions Update, Q4 2015

3

3 Assumption methodology

3.1 Price inflation

We use the assumption of 2.5% for the expected rate of future price inflation. This is 0.5% above the

Bank of England’s inflation target of 2% for CPI inflation. The Bank’s measure excludes mortgages

and for our purposes we have decided that it would be prudent to allow an extra margin for retail

investors. The assumption is also consistent with the FCA’s intermediate inflation assumption set out

in COBS 13 Annex 21.

3.2 Volatilities and correlations

As in previous reviews, the correlations and volatilities have been derived from real monthly

historical index data denominated in Sterling.

The methodology for deriving volatility and correlation assumptions has been retained. The time

period used for assessing volatility is based on a 15 year rolling period for each representative index.

3.3 Expected returns

3.3.1 UK gilts

The estimate for the expected nominal return on conventional Gilts is derived from the yield to

maturity of the Barclays All Maturities Gilts Index. The nominal yield at 31 December 2015 has

increased by approximately 20 bps this quarter to 2.3% pa, resulting in an expected return of -0.2%

pa in real terms.

An All Maturity Index has been selected for the Gilts analysis because it best represents the

portfolios that are used within the Platform. It is also assumed that the duration of the portfolio is

held relatively constant through a managed fund environment and it is not held as an individual

security whose duration would decrease over time.

The table below sets out the nominal yields on Gilts for a range of maturities as at the review date.

1 The handbook can be located at http://fshandbook.info/FS/html/FCA/COBS/13/Annex2

Capital Market Assumptions Update, Q4 2015

4

Up to 5 years 5 - 10 years 10 - 15 years Over 15 years All stocks

Number 13 9 3 16 41

Nominal yield

(% pa) 1.0% 1.7% 2.2% 2.6% 2.3%

Table 2: UK gilt yields

Figure 1: UK gilt yield curve

Figure 1 above shows the change in the UK yield curve over the quarter. There has been a general

increase in yields across all terms during the quarter.

3.3.2 Index-linked gilts

Yields for Index-linked gilts (“ILGs”) are quoted based on inflation assumptions of 0% and 5%. Over

the quarter, yields have increased, particularly at the short end of the curve.

To arrive at the yield for 2.5% inflation, linear interpolation has been used. Based on this method,

the expected real return for this quarter is -0.7% pa, an increase of 10bps since last quarter.

The following table sets out the yields on ILGs for a range of maturities as at the review date.

Capital Market Assumptions Update, Q4 2015

5

Up to 5 years 5 to 15 years Over 15 years All stocks

Number 4 7 15 26

Yield on 0% inflation (%pa) -0.7% -0.6% -0.7% -0.7%

Yield on 5% inflation (%pa) -1.5% -0.7% -0.7% -0.7%

Interpolated yield on 2.5%

inflation (%pa) -1.1% -0.6% -0.7% -0.7%

Table 3: Index-linked gilt yields

Figure 2: UK index-linked gilt yield curve

There has been a general increase in real yields over the quarter across all terms.

Figure 3 below shows how Breakeven Inflation has changed over the quarter. There have been no

significant changes to inflation expectations over the quarter.

Figure 3: Breakeven Inflation

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y 12Y 15Y 20Y 25Y 30Y 40Y 50Y

-1.4

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

Nom

inal Y

ield

(%

)

Term (months)

UK Index-linked Curve (Q4 2015)

UK Index-linked Curve (Q3 2015)

5Y6Y7Y8Y9Y10Y 12Y 15Y 20Y 25Y 30Y 40Y 50Y

2

2.5

3

3.5

4

No

min

al Y

ield

Term

Interpolated Breakeven Inflation (Q4 2015)

Interpolated Breakeven Inflation (Q3 2015)

Capital Market Assumptions Update, Q4 2015

6

3.3.3 UK corporate bonds

There has been little change in corporate yields over the quarter; the small rise in gilt yields was

matched by an equivalent fall in credit spreads.

The nominal yield for UK Corporate Bonds this quarter is currently at 3.5%. We assume the same

default probability as previously, resulting in an expected return of 1.2% pa.

Figure 4: Investment grade credit spreads

3.3.4 International bonds

The broad market index that is used to represent International Bonds has a large exposure to high

quality sovereigns. This quarter, real yields for the index rose by approximately 15bps, which has

increased our expected real return assumption to -0.7% pa.

Figure 5: Nominal sovereign yields

0

200

400

600

800

1000

1200

Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 Jun 12 Dec 12 Jun 13 Dec 13 Jun 14 Dec 14 Jun 15 Dec 15

Cre

dit

Sp

rea

dd

s (

bp

s)

AAA Rated AA Rated A Rated BBB Rated High yield

0%

1%

2%

3%

4%

5%

Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 Jun 12 Dec 12 Jun 13 Dec 13 Jun 14 Dec 14 Jun 15 Dec 15

No

min

al Y

ield

UK Gilt All Maturities Germany All Maturities US Treasury All Maturities

Capital Market Assumptions Update, Q4 2015

7

3.3.5 Global high yield bonds

The nominal yield on the Barclays Capital Global High Yield Bond Index has increased by about 0.3%

this quarter to 8.2% pa. Therefore, taking into account the default risk, the assumption for Global

High Yield bonds is increased to 3.6% pa in real terms this quarter.

Figure 6: Nominal yields

0%

4%

8%

12%

Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 Jun 12 Dec 12 Jun 13 Dec 13 Jun 14 Dec 14 Jun 15 Dec 15

No

min

al Y

ield

Global High Yield Bonds UK Gilt All Maturities US Treasury All Maturities

Capital Market Assumptions Update, Q4 2015

8

3.3.6 Equities

The DT platform splits equities into geographical regions. The following indices are used to calculate

volatilities and correlations for equities:

MSCI UK Equity Total Return Index

MSCI Europe ex UK Equity Total Return Index

MSCI North American Equity Total Return Index

MSCI Japanese Equity Total Return Index

MSCI Asia Pacific ex Japan Equity Total Return Index

MSCI Emerging Market Equity Total Return Index

The methodology for generating expected returns incorporates the earnings yield via the payout

ratio, as well as taking into account the regional dividend yields, GDP and inflation forecasts. Our

research indicates that this method is more comprehensive as it captures any share buybacks over

time as well as the actual payment of dividends. We have used consensus data, sourced from

Bloomberg, for regional GDP and inflation forecasts. These consensus forecasts include contributions

from various Investment Banks, consultancies and other local agencies.

Table 4 gives the Q4 2015 real and nominal assumptions for all equity regions.

Equity regions Real expected returns (% pa) Nominal expected returns (% pa)

UK equity 4.3% 6.8%

Europe ex UK equity 4.5% 7.0%

North American equity 4.1% 6.6%

Japanese equity 2.8% 5.3%

Asia Pacific ex Japan equity 5.6% 8.1%

Emerging Market equity 6.5% 9.0%

Table 4: Equity assumptions

There have been reductions in expectations across all geographical regions, driven by both a

decrease in the dividend payout expectations and lower growth expectations. This has been more

pronounced in the more volatile equity regions, such as Asia Pacific ex Japan and emerging markets.

Capital Market Assumptions Update, Q4 2015

9

3.3.7 Cash

We have retained the methodology of using the yield on 5-15 years Index-Linked Gilts (at the 10 year

breakeven inflation point) for deriving the Cash assumption. This results in a real assumption

of -0.6% pa and a nominal assumption of 1.9% pa.

3.3.8 Property

For property the risk premium over Gilts has been maintained. Since there has been an increase in

yields for Gilts this quarter, the assumption for UK commercial property has similarly increased to

2.2% pa.

3.3.9 Commodities

The assumption for commodities is in line with the global growth forecast from IMF, as research

indicates that commodity prices are highly correlated with global growth. The IMF global growth

forecast has reduced its predictions for 2016, and hence the real assumption for commodities is

reduced to 3.4% pa.

3.3.10 Absolute return

We retain the same risk premium over gilts of 1.2% pa, resulting in a real return assumption of

1.0% pa.

3.3.11 Unclassified

The unclassified asset class is based on an equally weighted combination of UK Gilts and UK Equity

and forms a medium level of risk. We also assume that this asset class is uncorrelated to all other

asset types. This quarter the assumption for this asset class is 2.0% pa in real terms.

Capital Market Assumptions Update, Q4 2015

10

4 Strategic asset allocation

The assumptions in this update note are used in two distinct ways; for constructing an efficient frontier from which investors can select an asset allocation

that suits their risk appetite and to forecast the distribution of investment outcomes for a given asset allocation strategy.

Table 5 shows the current strategic asset allocations which were implemented in October 2015 for each risk profile (“RP”). No changes are proposed to

asset allocations this quarter.

Risk profile Cash

UK

Corporate

Bonds

UK Index

Linked

Bonds

Inter-

national

Bonds UK Gilts

Global

High Yield

Bonds UK Equity

Europe Ex

UK Equity

North

American

Equity

Japanese

Equity

Asia Pacific

ex Japan

Equity

Emerging

Market

Equity

UK

Property Commodities

Absolute

Return

1 100% - - - - - - - - - - - - - -

2 41% 13% 5% 6% 13% 5% 12% - - - - - 5% - -

3 10% 23% 7% 7% 16% 5% 15% - 9% - - - 8% - -

4 5% 27% 5% - 8% 6% 22% 5% 9% 5% - - 8% - -

5 - 24% - - 5% 6% 28% 5% 14% 5% 6% - 7% - -

6 - 19% - - - 5% 31% 5% 9% 5% 10% 11% 5% - -

7 - 5% - - - 5% 35% 5% 7% 5% 16% 17% 5% - -

8 - - - - - 5% 23% 5% 5% 5% 22% 30% 5% - -

9 - - - - - - 16% 5% 5% 5% 26% 43% - - -

10 - - - - - - 5% - 5% - 27% 63% -

Table 5: Strategic asset allocations

Capital Market Assumptions Update, Q4 2015

5 Efficient frontier

The current asset allocations are plotted on the risk-reward space using the Q4 2015 assumptions as

seen in Figure 7. We also show how these allocations were positioned using the previous

assumptions, as at 30 September 2015.

Figure 7: Efficient frontier

RP 1 RP 2 RP 3 RP 4 RP 5 RP 6 RP 7 RP 8 RP 9 RP 10

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0.00% 2.10% 4.20% 6.30% 8.40% 10.50% 12.60% 14.70% 16.80% 18.90% 21.00%

Exp

ect

ed

re

turn

(%

pa)

Volatility (%pa)

Previous assumptions Revised assumptions

Capital Market Assumptions Update, Q4 2015

12

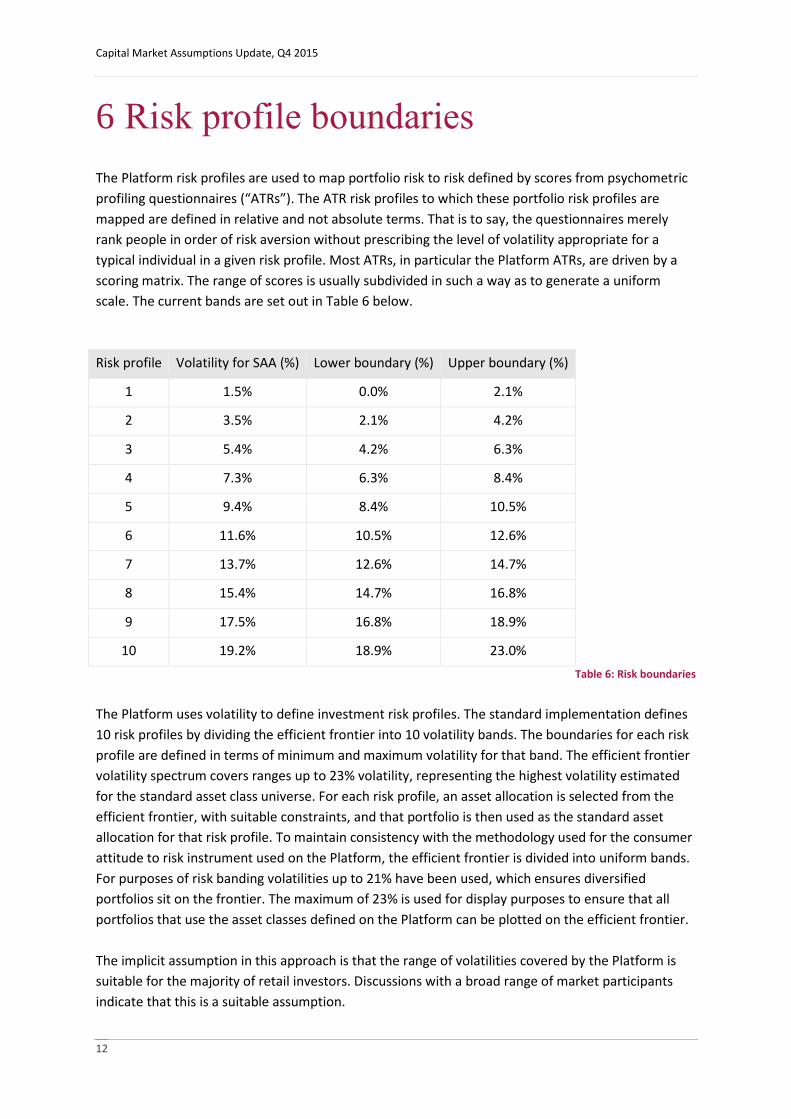

6 Risk profile boundaries

The Platform risk profiles are used to map portfolio risk to risk defined by scores from psychometric

profiling questionnaires (“ATRs”). The ATR risk profiles to which these portfolio risk profiles are

mapped are defined in relative and not absolute terms. That is to say, the questionnaires merely

rank people in order of risk aversion without prescribing the level of volatility appropriate for a

typical individual in a given risk profile. Most ATRs, in particular the Platform ATRs, are driven by a

scoring matrix. The range of scores is usually subdivided in such a way as to generate a uniform

scale. The current bands are set out in Table 6 below.

Risk profile Volatility for SAA (%) Lower boundary (%) Upper boundary (%)

1 1.5% 0.0% 2.1%

2 3.5% 2.1% 4.2%

3 5.4% 4.2% 6.3%

4 7.3% 6.3% 8.4%

5 9.4% 8.4% 10.5%

6 11.6% 10.5% 12.6%

7 13.7% 12.6% 14.7%

8 15.4% 14.7% 16.8%

9 17.5% 16.8% 18.9%

10 19.2% 18.9% 23.0%

Table 6: Risk boundaries

The Platform uses volatility to define investment risk profiles. The standard implementation defines

10 risk profiles by dividing the efficient frontier into 10 volatility bands. The boundaries for each risk

profile are defined in terms of minimum and maximum volatility for that band. The efficient frontier

volatility spectrum covers ranges up to 23% volatility, representing the highest volatility estimated

for the standard asset class universe. For each risk profile, an asset allocation is selected from the

efficient frontier, with suitable constraints, and that portfolio is then used as the standard asset

allocation for that risk profile. To maintain consistency with the methodology used for the consumer

attitude to risk instrument used on the Platform, the efficient frontier is divided into uniform bands.

For purposes of risk banding volatilities up to 21% have been used, which ensures diversified

portfolios sit on the frontier. The maximum of 23% is used for display purposes to ensure that all

portfolios that use the asset classes defined on the Platform can be plotted on the efficient frontier.

The implicit assumption in this approach is that the range of volatilities covered by the Platform is

suitable for the majority of retail investors. Discussions with a broad range of market participants

indicate that this is a suitable assumption.

Capital Market Assumptions Update, Q4 2015

Appendix A: Asset classes on risk / reward space

Figure 8 shows each asset class return on the risk / reward chart.

Figure 8: Asset class assumptions on the risk/reward space

Cash

UK Corporate Bonds

UK Index-Linked Gilts

International Bonds

UK Gilts

UK Equity

Europe ex UK Equity

North American Equity

Japanese Equity

AsiaPac ex Japan Equity

Emerging Market Equity

UK Commercial Property

Commodities

Absolute return

Global High Yield Bonds

Unclassified

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

0.0% 2.1% 4.2% 6.3% 8.4% 10.5% 12.6% 14.7% 16.8% 18.9% 21.0% 23.1%

Exp

ecte

d r

eal re

turn

%p

a

Volatility %pa

Capital Market Assumptions Update, Q4 2015

14

Appendix B: Changes in assumptions per asset classes

Figure 9 shows the expected real returns over the last four quarters for all asset classes. Figure 10 shows the change in volatility expectations.

Figure 9: Changes in asset class returns

CashUK Corporate

BondsUK Index-

Linked GiltsInternational

BondsUK Gilts

Global HighYield Bonds

UK EquityEurope ex UK

Equity

NorthAmerican

Equity

JapaneseEquity

AsiaPac exJapan Equity

EmergingMarket Equity

UKCommercial

PropertyCommodities

AbsoluteReturn

Unclassified

Q1 2015 -1.0% 0.5% -0.9% -1.1% -0.5% 2.4% 4.4% 4.0% 4.1% 2.7% 5.4% 6.2% 1.9% 3.8% 0.7% 2.0%

Q2 2015 -0.8% 1.1% -0.9% -0.8% -0.1% 2.5% 4.3% 4.3% 4.0% 2.9% 5.6% 6.3% 2.3% 3.8% 1.1% 2.1%

Q3 2015 -0.8% 1.2% -0.8% -0.9% -0.4% 3.4% 4.4% 4.6% 4.3% 3.0% 5.9% 6.7% 2.0% 3.5% 0.8% 2.0%

Q4 2015 -0.6% 1.2% -0.7% -0.7% -0.2% 3.6% 4.3% 4.5% 4.1% 2.8% 5.6% 6.5% 2.2% 3.4% 1.0% 2.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Exp

ecte

d R

etu

rns

Capital Market Assumptions Update, Q4 2015

Figure 10: Changes in asset class volatilities

CashUK Corporate

BondsUK Index-

Linked GiltsInternational

BondsUK Gilts

Global HighYield Bonds

UK EquityEurope ex UK

Equity

NorthAmerican

Equity

JapaneseEquity

AsiaPac exJapan Equity

EmergingMarket Equity

UKCommercial

PropertyCommodities

AbsoluteReturn

Unclassified

Q1 2015 1.5% 6.3% 7.5% 8.3% 5.9% 10.8% 13.8% 19.0% 15.5% 16.8% 18.6% 21.4% 11.5% 21.3% 8.7% 7.1%

Q2 2015 1.5% 6.4% 7.5% 8.3% 6.0% 10.9% 13.9% 19.0% 15.5% 16.8% 18.5% 21.4% 12.3% 20.9% 8.8% 7.1%

Q3 2015 1.5% 6.4% 7.6% 8.3% 6.0% 10.8% 14.0% 19.0% 15.3% 16.4% 18.6% 21.3% 11.9% 20.9% 8.7% 7.2%

Q4 2015 1.5% 6.4% 7.6% 8.2% 6.0% 10.8% 14.0% 19.1% 15.2% 16.2% 18.6% 21.2% 10.7% 20.4% 8.6% 7.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Vo

lati

lity

16

Appendix C: DT allocation -

projections

The following tables show the potential losses and gains which have been calculated for each risk

profile, based on an initial investment of £10,000. We have applied the effect of the Total Expense

Ratios as set out in Appendix F. For each risk level we show a range of percentile outcomes, based

on the 5th, 50th and 95th percentiles2.

2 Percentiles are used to give a measure of confidence for a particular outcome. So for a 95

th percentile

outcome, we would expect actual returns to remain below this with 95% confidence.

Risk profile 1

Value after 1 year 5 years 10 years 20 years

5th percentile £9,600 £8,900 £8,300 £7,200

50th percentile £9,900 £9,500 £8,900 £8,000

95th percentile £10,100 £10,000 £9,700 £8,900

Risk profile 2

Value after 1 year 5 years 10 years 20 years

5th percentile £9,400 £8,700 £8,100 £7,300

50th percentile £10,000 £9,800 £9,700 £9,400

95th percentile £10,500 £11,200 £11,600 £12,100

Risk profile 3

Value after 1 year 5 years 10 years 20 years

5th percentile £9,200 £8,300 £7,700 £7,000

50th percentile £10,000 £10,100 £10,200 £10,400

95th percentile £10,900 £12,300 £13,400 £15,400

Risk profile 4

Value after 1 year 5 years 10 years 20 years

5th percentile £9,000 £8,000 £7,400 £6,900

50th percentile £10,100 £10,400 £10,800 £11,600

95th percentile £11,300 £13,500 £15,700 £19,700

Risk profile 5

Value after 1 year 5 years 10 years 20 years

5th percentile £8,700 £7,600 £7,000 £6,500

50th percentile £10,100 £10,600 £11,300 £12,800

95th percentile £11,800 £14,900 £18,200 £25,000

Risk profile 6

Value after 1 year 5 years 10 years 20 years

5th percentile £8,500 £7,200 £6,600 £6,100

50th percentile £10,200 £10,800 £11,800 £13,900

95th percentile £12,200 £16,300 £21,000 £31,400

Risk profile 7

Value after 1 year 5 years 10 years 20 years

5th percentile £8,200 £6,800 £6,200 £5,700

50th percentile £10,200 £11,000 £12,100 £14,700

95th percentile £12,600 £17,800 £23,900 £38,400

Risk profile 8

Value after 1 year 5 years 10 years 20 years

5th percentile £8,000 £6,500 £5,800 £5,300

50th percentile £10,200 £11,100 £12,400 £15,400

95th percentile £13,000 £19,100 £26,500 £45,200

Risk profile 9

Value after 1 year 5 years 10 years 20 years

5th percentile £7,800 £6,100 £5,300 £4,700

50th percentile £10,200 £11,200 £12,600 £15,800

95th percentile £13,400 £20,500 £29,600 £52,900

Risk profile 10

Value after 1 year 5 years 10 years 20 years

5th percentile £7,600 £5,800 £5,000 £4,400

50th percentile £10,300 £11,300 £12,800 £16,500

95th percentile £13,800 £21,900 £32,700 £61,700

18

Appendix D: Total expense ratio

The table below shows the Total Expense Ratios (“TER”) used in the production environment.

Asset classes Total Expense Ratio (%)

Cash 0.5%

UK Corporate Bonds 1.1%

UK Index Linked Gilts 0.5%

International Bonds 1.3%

UK Gilts 0.6%

Global High Yield Bonds 1.0%

UK Equity 1.6%

Europe ex UK Equity 1.7%

North American Equity 1.6%

Japanese Equity 1.7%

Asia Pacific ex Japan Equity 1.7%

Emerging Market Equity 1.8%

UK Commercial Property 1.6%

Commodities 1.6%

Absolute return 1.2%

Table 7: Total expense ratios

Basis of Preparation and Use

You should not rely on this information in making an investment decision and it does not constitute a recommendation or advice in the

selection of a specific investment or class of investments.

The information does not indicate a promise, forecast or illustration of future volatility or returns. The outputs represent a range of

possible indications of volatility and returns for various collections of asset classes. Distribution Technology Limited (“DT”) is not liable for

the data in respect of direct or consequential loss attaching to the use of or reliance upon this information.

DT does not warrant or claim that the information in this document or any associated form is compliant with obligations governing the

provision of advice or the promotion of products as defined by the Financial Services Act.

Copyright

© Distribution Technology Ltd 2015 onwards. All rights reserved.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or any means, electronic or

mechanical, including photocopying and recording for any purpose other than the purchaser’s personal use without the prior written

permission of DT.

Source of information

Bank of England, Barclays Capital Inc., Bloomberg LLC, Heriot Watt University Gilt database, International Monetary Fund (IMF),

Investment Property Databank, Markit iBoxx and Office of National Statistics

Trademarks

DT may have patents or pending patent applications, trademarks, copyrights or other intellectual property rights covering subject matter

in this document. The furnishing of this document does not give you any license to these patents, trademarks, copyrights or other

intellectual property rights except as expressly provided in any written license agreement from DT.

All other companies and product names are trademarks or registered trademarks of their respective holders.

www.distribution-technology.com