Embed Size (px)

Citation preview

CENTURY 21 ACCOUNTING © Thomson/South-Western

LESSON 8-3LESSON 8-3

Disposing of Plant Assets

CENTURY 21 ACCOUNTING © Thomson/South-Western

DISCARDING A PLANT ASSET WITH NO DISCARDING A PLANT ASSET WITH NO BOOK VALUEBOOK VALUE

Businesses usually dispose of plant assets in one of three ways: The plant asset is discarded because no useful life

remains The plant asset is sold because it is no longer needed

even though it might still be usable The plant asset is traded for another plant asset of the

same kind.

2

LESSON 8-3

page 235

CENTURY 21 ACCOUNTING © Thomson/South-Western

DISCARDING A PLANT ASSET WITH NO DISCARDING A PLANT ASSET WITH NO BOOK VALUEBOOK VALUE

If a plant asset has a salvage value of zero & its total accumulated depreciation is equal to the original cost value, the plant asset has no book value Some assets are assumed to have no salvage value

When a plant asset with no book value is discarded, a journal entry is recorded that removes the original cost of the plant asset & its related accumulated depreciation If the cost and accumulated depreciation are not removed from the

general ledger then the complany is overstating its aassets and the related depreciation.

3

LESSON 8-3

page 235

CENTURY 21 ACCOUNTING © Thomson/South-Western

4

LESSON 8-3

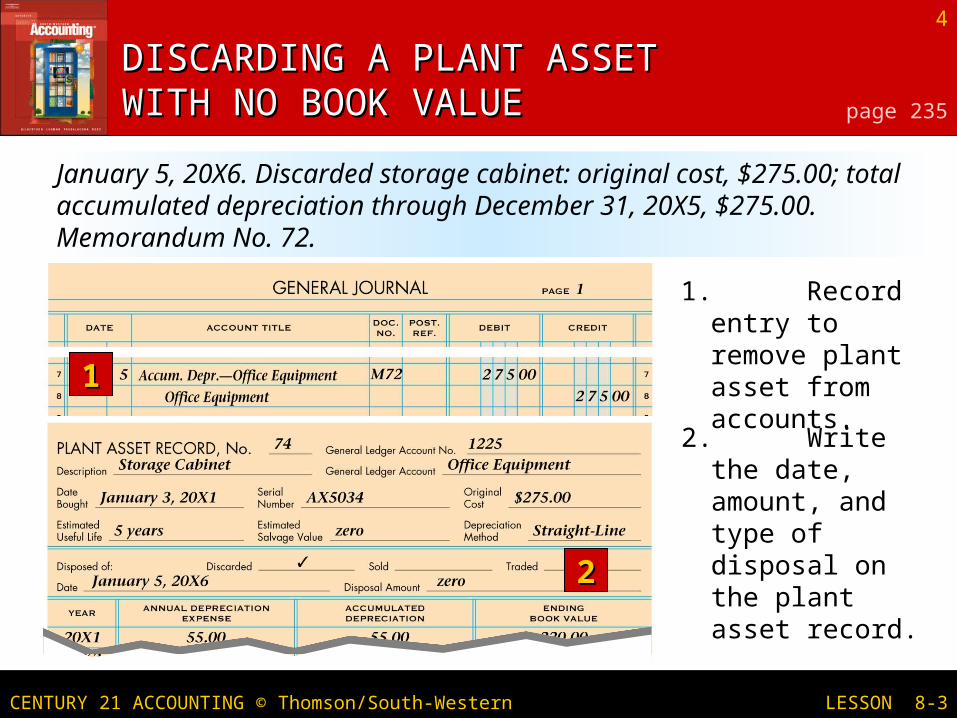

1. Record entry to remove plant asset from accounts.

2. Write the date, amount, and type of disposal on the plant asset record.

DISCARDING A PLANT ASSET DISCARDING A PLANT ASSET WITH NO BOOK VALUEWITH NO BOOK VALUE page 235

11

January 5, 20X6. Discarded storage cabinet: original cost, $275.00; total accumulated depreciation through December 31, 20X5, $275.00. Memorandum No. 72.

22

CENTURY 21 ACCOUNTING © Thomson/South-Western

5

LESSON 8-3

DISCARDING A PLANT ASSET WITH A DISCARDING A PLANT ASSET WITH A BOOK VALUEBOOK VALUE page 236

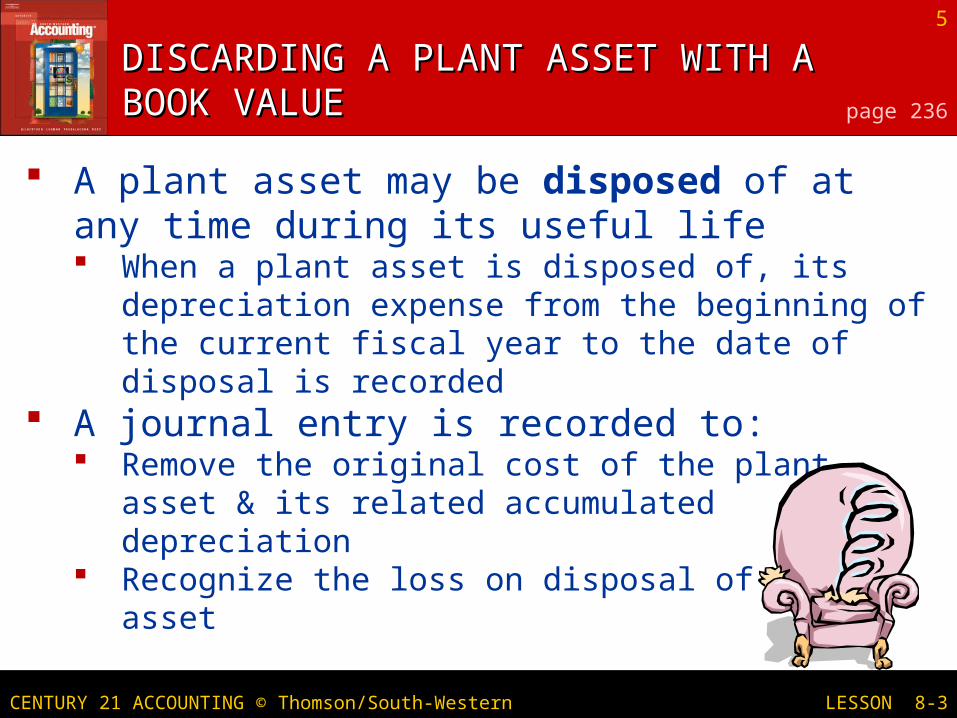

A plant asset may be disposed of at any time during its useful life When a plant asset is disposed of, its depreciation

expense from the beginning of the current fiscal year to the date of disposal is recorded

A journal entry is recorded to: Remove the original cost of the plant asset & its related

accumulated depreciation Recognize the loss on disposal of the asset

CENTURY 21 ACCOUNTING © Thomson/South-Western

6

LESSON 8-3

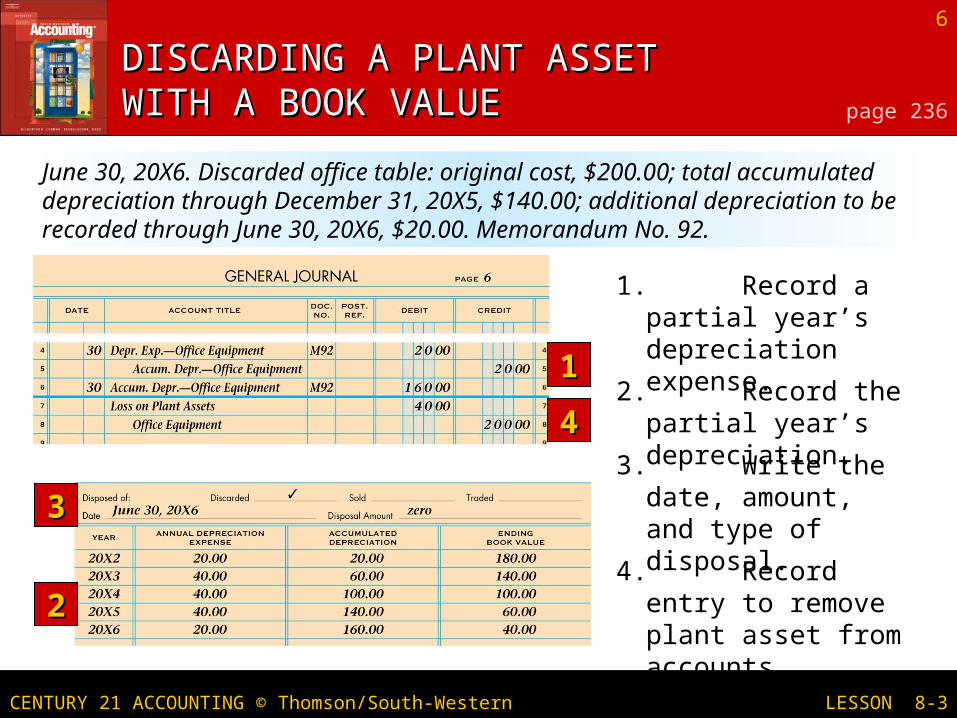

June 30, 20X6. Discarded office table: original cost, $200.00; total accumulated depreciation through December 31, 20X5, $140.00; additional depreciation to be recorded through June 30, 20X6, $20.00. Memorandum No. 92.

1. Record a partial year’s depreciation expense.

2. Record the partial year’s depreciation.

4. Record entry to remove plant asset from accounts.

3. Write the date, amount, and type of disposal.

DISCARDING A PLANT ASSET DISCARDING A PLANT ASSET WITH A BOOK VALUEWITH A BOOK VALUE page 236

11

44

33

22

CENTURY 21 ACCOUNTING © Thomson/South-Western

7

LESSON 8-3

SELLING A PLANT ASSETSELLING A PLANT ASSET page 237

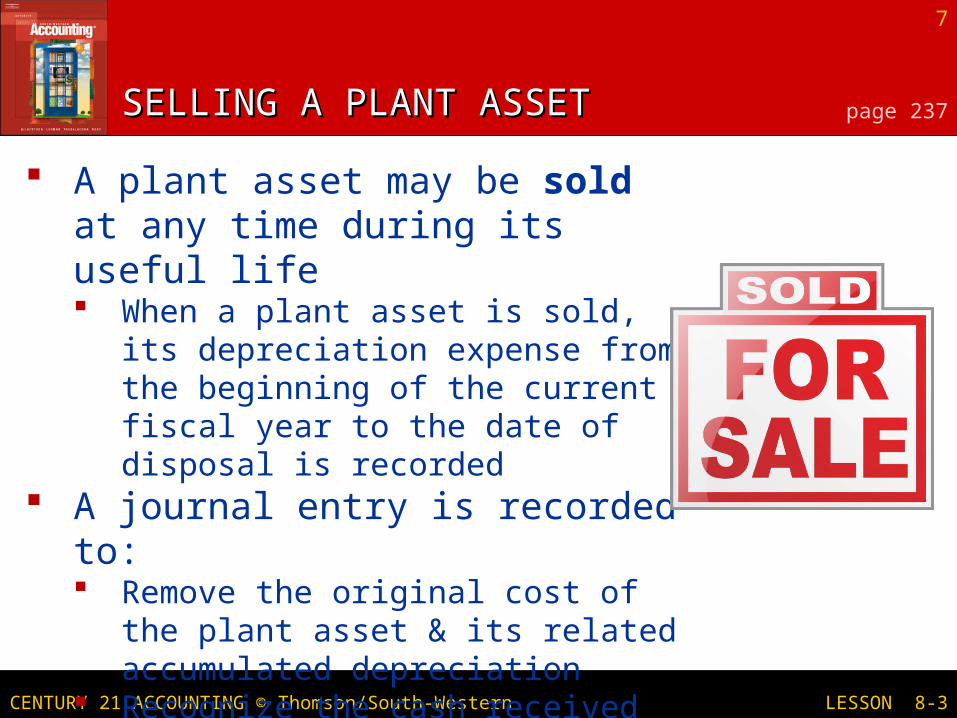

A plant asset may be sold at any time during its useful life When a plant asset is sold, its

depreciation expense from the beginning of the current fiscal year to the date of disposal is recorded

A journal entry is recorded to: Remove the original cost of the plant

asset & its related accumulated depreciation

Recognize the cash received Recognize the gain or loss on disposal

of the asset

CENTURY 21 ACCOUNTING © Thomson/South-Western

8

LESSON 8-3

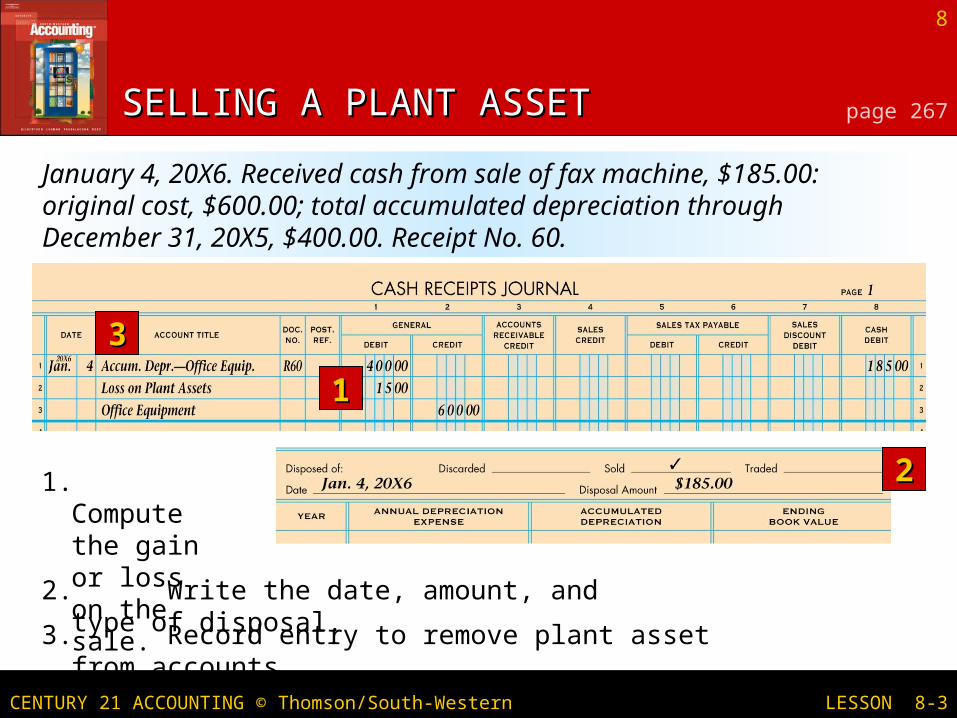

3. Record entry to remove plant asset from accounts.

1. Compute the gain or loss on the sale.

2. Write the date, amount, and type of disposal.

SELLING A PLANT ASSETSELLING A PLANT ASSET page 267

11

22

33

January 4, 20X6. Received cash from sale of fax machine, $185.00: original cost, $600.00; total accumulated depreciation through December 31, 20X5, $400.00. Receipt No. 60.

CENTURY 21 ACCOUNTING © Thomson/South-Western

9

LESSON 8-3

TRADING A PLANT ASSETTRADING A PLANT ASSET page 238

Sometimes a business will need to upgrade or buy a new asset Instead of selling or disposing of the

asset they may trade it in to obtain the new asset at a lower payout of cash

A journal entry is recorded to: Remove the original cost of the plant

asset & its related accumulated depreciation

Recognize the cash paid Records the new plant asset at its

original cost

CENTURY 21 ACCOUNTING © Thomson/South-Western

10

LESSON 8-3

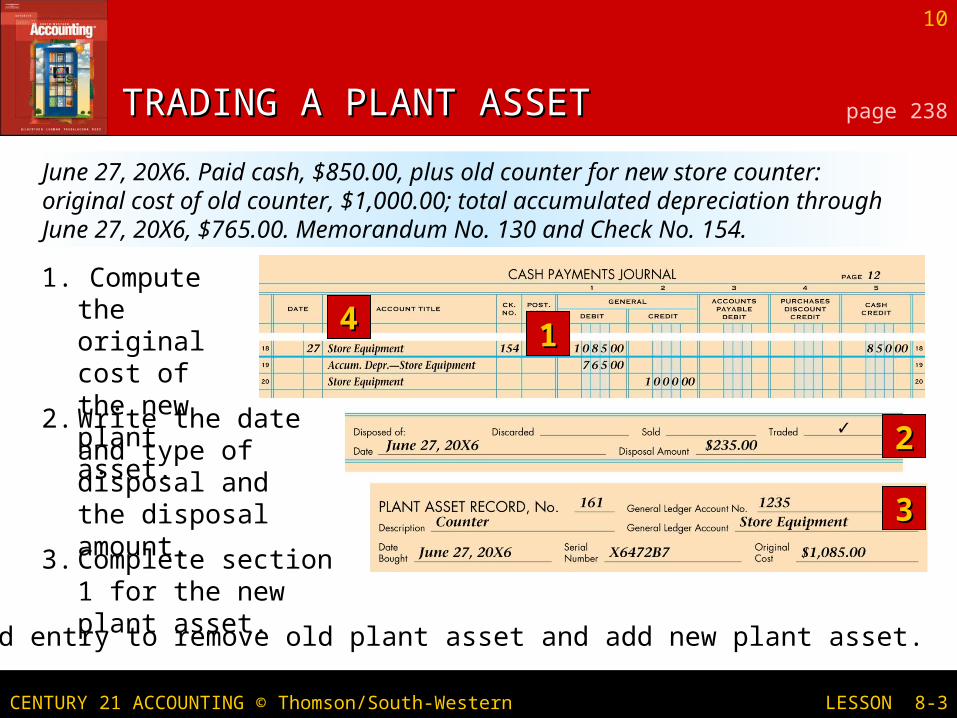

1. Compute the original cost of the new plant asset.

TRADING A PLANT ASSETTRADING A PLANT ASSET page 238

1144

June 27, 20X6. Paid cash, $850.00, plus old counter for new store counter: original cost of old counter, $1,000.00; total accumulated depreciation through June 27, 20X6, $765.00. Memorandum No. 130 and Check No. 154.

4. Record entry to remove old plant asset and add new plant asset.

2. Write the date and type of disposal and the disposal amount.

22

33

3. Complete section 1 for the new plant asset.

CENTURY 21 ACCOUNTING © Thomson/South-Western

11

LESSON 8-3

SELLING LAND & BUILDINGSSELLING LAND & BUILDINGS page 239

Land is considered a permanent plant asset Its useful life is not estimated Annual depreciation is not recorded for

it The book value of land is always its

original cost Usually land is sold at the same time the

buildings on it are sold A separate plant record is maintained

for the land & the building

CENTURY 21 ACCOUNTING © Thomson/South-Western

12

LESSON 8-3

SELLING LAND & BUILDINGSSELLING LAND & BUILDINGS page 239

A journal entry is recorded to: Remove the original cost of the land &

building & the building’s related accumulated depreciation

Recognizes the cash received Records the gain on disposal of the

plant assets

CENTURY 21 ACCOUNTING © Thomson/South-Western

13

LESSON 8-3

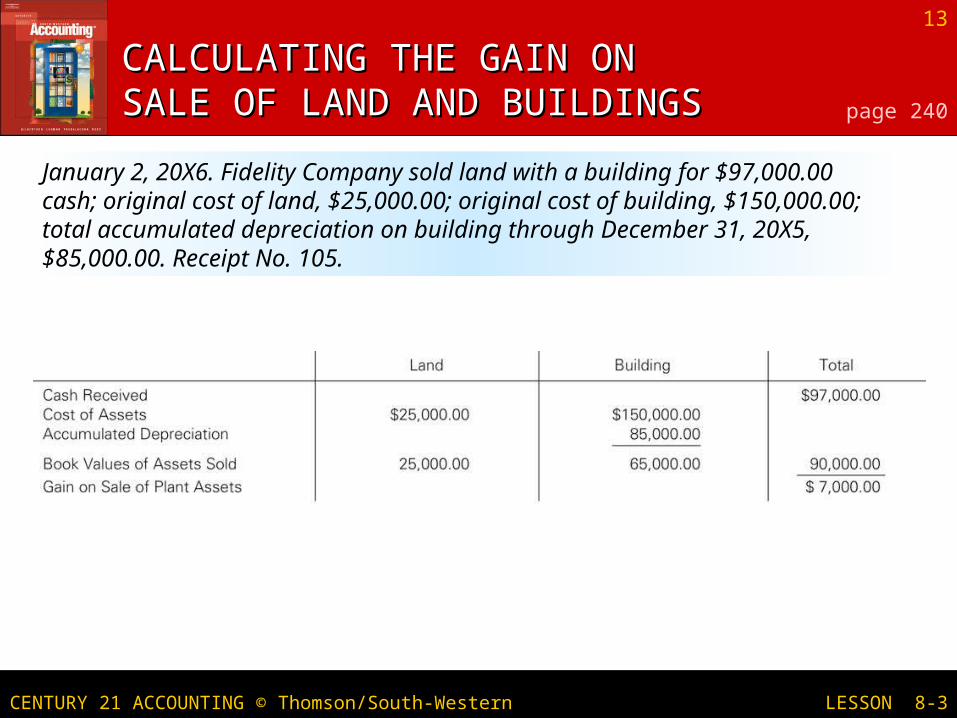

CALCULATING THE GAIN ON CALCULATING THE GAIN ON SALE OF LAND AND BUILDINGSSALE OF LAND AND BUILDINGS page 240

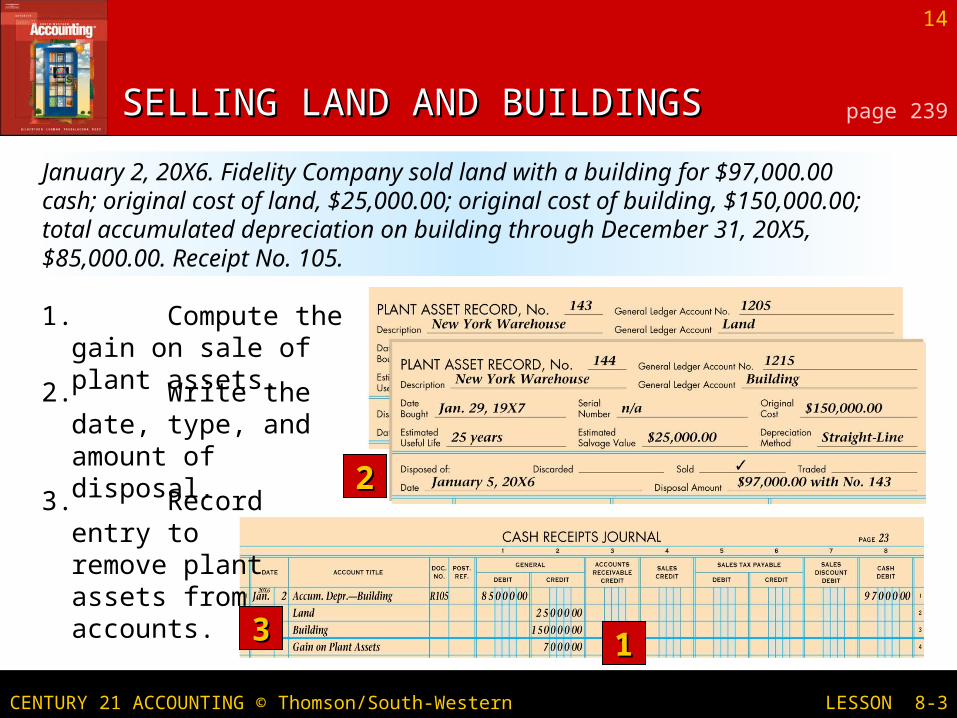

January 2, 20X6. Fidelity Company sold land with a building for $97,000.00 cash; original cost of land, $25,000.00; original cost of building, $150,000.00; total accumulated depreciation on building through December 31, 20X5, $85,000.00. Receipt No. 105.

CENTURY 21 ACCOUNTING © Thomson/South-Western

14

LESSON 8-3

3. Record entry to remove plant assets from accounts.

1. Compute the gain on sale of plant assets.

2. Write the date, type, and amount of disposal.

SELLING LAND AND BUILDINGSSELLING LAND AND BUILDINGS page 239

1133

January 2, 20X6. Fidelity Company sold land with a building for $97,000.00 cash; original cost of land, $25,000.00; original cost of building, $150,000.00; total accumulated depreciation on building through December 31, 20X5, $85,000.00. Receipt No. 105.

22