Embed Size (px)

DESCRIPTION

This paper is mine.

Citation preview

Chapter 5Legal Liability

Key objectives:

1. Appreciate the litigious environment in which CPAs operate. 2. Understand the difference between business failure, audit failure and audit risk. 4. Describe accountant's liability to clients and related defenses. 5. Describe accountant's liability to third parties under common law and related defenses. 6. Describe accountant's civil liability under federal securities laws and related defenses.

1. Current Legal Environment

The legal environment is one of the most important issues facing the profession today. Several years ago, KPMG agreed to a $456 million fine from the federal government. Several Big 5 firms paid large settlements in the 1990s to the federal government in connection with the audits of savings and loans. Andersen effectively ceased operations in 2002 due to a Justice Department suit against the firm. Laventhol and Horwath (at the time the 7th largest firm) entered bankruptcy in 1990, partially due to legal liability concerns. The firms report that they spend over 10% of practice revenues on insurance and related defense costs. Many smaller CPA firms have stopped providing audit services, and firms have become much more selective about their clients.

What are some fairly recent changes in the area of legal liability? (Discussion)

33

1. Proportionate versus joint and several liability. Proportionate liability applies to securities litigation as a result of the Private Securities Litigation Reform Act of 1995.

2. Operation of practice as limited liability corporations (LLC) and limited liability partnerships (LLP) - this is currently allowed in most states, and most of the Big 4 operate as LLPs.

2. Business Failure, Audit Failure and Audit Risk - One reason that CPAs face so much litigation is the inability of financial statement users to distinguish among these terms.

A. Business Failure - Defining business failure is more complicated than it seems. It encompasses bankruptcy, liquidation, default, or merely poor performance. Many suits are brought merely because of a decline in the company's stock price. Many business failures result in litigation, often involving the CPA. Recall from Ch. 3 the auditor's responsibility for reporting on going concern.

B. Audit Failure - The issuance of an incorrect audit opinion due to a failure to comply with Generally Accepted Auditing Standards. Note that the auditor may issue an incorrect opinion when GAAS has been followed due to audit risk.

C. Audit Risk - Risk that the auditor issues an unqualified opinion when the financial statements are materially misstated. A small degree of audit risk is present on all engagements because of the use of sampling and the difficulty in detecting certain types of errors. (Discussed in greater detail in Chapter 9.)

34

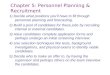

(not to scale)

Representation of Business Failures, Audit Failures and Audit Risk

(box represents population of clients)

The diagram above may help illustrate the concept. The box represents all companies. In a given year: A fairly large percentage (say 5%) of companies may fail. A much smaller percentage (say 1%) of companies will receive

incorrect audit opinions due to audit risk. A much smaller percentage of companies (say 1/10%) will receive

incorrect opinions due to audit failure.

Auditors should have to defend themselves when the circles intersect. That is, when an incorrect audit opinion has been issued and a loss has occurred. Unfortunately, the profession often has to defend itself in business failures that do not involve an incorrect audit opinion. This is important because a large part of the cost of the liability crisis is the cost of defending against litigation.

This should not be read as a wholesale defense of the profession. Real and perceived audit failures continue to occur, and the problems that preceded the passage of SOX were not solely confined to Andersen.

What factors may have resulted in increased (decreased) audit failures in recent years? (Discussion)

Business Failures

Audit Risk

Audit Failure

35

3. Sources of Legal Liability - There are four main sources of legal liability:

Client - common law Third parties - common law Federal securities acts Criminal liability

We will focus primarily on third party liability under common law and the federal securities acts. These are the major areas of litigation for CPA firms.

4. Responsibilities to Third Parties under Common Law - see below for required degree of negligence to be held liable:

Ordinary negligence

Primary beneficiaries (known third party) under Ultramares Doctrine

Foreseen Users (most jurisdictions)

Gross negligence Other third parties

A. Ultramares Doctrine - This landmark 1931 case established that ordinary negligence is insufficient to establish liability to third parties that lack privity, unless they are a primary beneficiary that the auditor was informed about prior to the audit (known third party).

Note that under Ultramares the auditor can still be held liable to other third parties for gross negligence.

B. Foreseen users – Case law has expanded the ability of third parties to recover for ordinary negligence. Most states allow recovery for ordinary negligence by foreseen users that are part of a reasonably limited and identifiable group of users.

C. Foreseeable Users - A few states follow a broader rule and allow recovery by users the auditor should have reasonably foreseen as likely financial statement users.

36

5. Responsibility to Third Parties - Securities Acts

A. 1933 Securities Act - Applies to registrations and prospectuses for newly issued securities.

User must only prove that the financial statements contained a material misrepresentation or omission.

Burden of proof is on the auditor to demonstrate due diligence in the conduct of the audit.

B. 1934 Securities Act - Applies to existing publicly-traded companies.

Most suits are brought under rule 10b-5, the antifraud provisions of the Act.

In Hochfelder v. Ernst & Ernst (1976), court ruled knowledge and intent to deceive (scienter) are necessary to find the auditor liable. However, this standard has been weakened over time.

In some cases, courts have ruled gross negligence or recklessness constitutes constructive fraud and is equivalent to scienter.

Multiple Choice 5-17 (a)

Major, Major and Sharpe audit MacLain Industries. Subsequent to the offering, misstatements were revealed, and Major was sued by shareholders. Major will avoid liability if:

1. The misstatements were caused by MacLain.2. It can be shown than at least some of the shareholders did not

read the financial statements.3. It can prove due diligence in the audit.4. MacLain expressly assumed any liability in connection with

the offering.

Multiple Choice 5-17 (c)

Donald & Co. audited the financial statements of Markum securities. The audit was improper in several respects, and the shareholders have sued under rule 10b-5 of the 1934 Act. Which is likely to be Donald's best defense?

1. Section 10b does not apply to them. 2. They did not intentionally certify false financial statements. 3. They were not in privity of contract with the creditors. 4. The engagement letter disclaimed liability.

6. Summary of Liability to Third Parties

37

Liability RegimeReliance Degree of Negligence

Common Law:Primary beneficiary and foreseen usersOther third parties

RequiredOrdinary negligence

Gross negligence

1933 Securities Act - new securities

Not Required No requirement. Material misrepresentation or omission required

1934 Securities Act - public companies

Required "Scienter" - knowledge or intent to deceive (1)

(1) Auditor is also likely to be held liable for gross negligence.

7. Auditor Defenses

In most third party suits under common law, the auditor will first argue lack of privity. The main auditor defense in most suits is that of nonnegligent performance. Of course, auditors still face the inability of courts and jurors to understand GAAS and distinguish audit failure from audit risk.

Summary of Auditor Defenses

Defenses Against Client SuitsDefenses Against Third Parties and Under 1934 Securities Act1

Lack of duty to perform service Lack of duty to perform service

Nonnegligent performance (audit in accordance with audit standards)

Nonnegligent performance (audit in accordance with audit standards)1

Contributory negligence

Absence of causal connection (no reliance on F/S)

Absence of causal connection (no reliance on F/S)

(1) Due diligence defense (nonnegligent performance) is also available under 1933 Securities Act.

Homework Problems5-20 5-23

Sample Multiple Choice (text)5-16 (b), (c) 5-17 (a), (b), (c)

38

Problem 5-20

a. Nonnegligent performance (compliance with GAAS) and contributory negligence.

The fraud is a reasonably complex one, and would be difficult to uncover, unless the inventories were all counted on the same day as suggested by the auditor. The president contributed to the inability to find the fraud by failing to follow the auditor's suggestion regarding the observing of inventories. Note that inventories normally are counted on one day to prevent this sort of activity.

b. Lack of privity and nonnegligent performance (see above). The lack of privity defense is not likely to be successful since this was a known third party.

c. The auditor is likely to be able to successfully defend herself against the client suit due to the contributory negligence. The company is responsible for its internal control structure, and the president's statement that it was impractical to count inventory on one day places considerable burden on the company.

The auditor will also likely be successful defending against the third party by demonstrating due care in the performance of the audit.

d. The results would not be different if brought under SEC Act of 1934. If the suit were brought under Rule 10b-5, it is highly unlikely the plaintiff could demonstrate intent to deceive.

Problem 5-23

a. Hanover will likely not be found liable to the purchasers of the common stock if the suit is brought under Rule 10b-5 of the Securities Exchange Act of 1934 because there was no knowledge or intent to deceive by the auditor. However, if the purchasers are original purchasers and are able to bring suit under the Securities Act of 1933, the plaintiffs will likely succeed because they must only prove the existence of a material error or omission.

b. Hanover was aware that the financial statements were to be used to obtain financing from First National Bank. Hanover is likely to be held responsible for negligence to the bank as a known third party that relied on the financial statements.

c. The plaintiffs might state a common law action for negligence. However, they will most likely not prevail due to the privity requirement. There was no contractual relationship between the defrauded parties and the CPA firm. Although the exact status of the privity rule is unclear, it is doubtful that the simple negligence in this case would extend Hanover's liability to the trade creditors who transacted business with Barton Corp. However, the facts of the case as presented in court would determine this.