Embed Size (px)

Citation preview

CHAPTER 4

Introduction to Macroeconomics

1

Slides prepared by Bruno Fullone, George Brown College

© 2010 McGraw-Hill Ryerson Limited

PART 2: GDP, GROWTH AND

FLUCTUATIONS

• Learning Objective 4.1: Why economists focus on GDP, unemployment, and inflation when assessing the health of an entire economy and what policy to pursue.

• Learning Objective 4.2 : That modern economic growth and sustained increases in living standards are historically recent phenomena

• Learning Objective 4.3 : That the promotion of modern economic growth requires savings and investment

• Learning Objective 4.4 : Why expectations, shocks, and sticky prices are responsible for short-run fluctuations in output and employment

2

In This Chapter You Will Learn:

In assessing the health and development of an economy, macroeconomists focus on:

• Real GDP

• Unemployment

• Inflation

3 LO4.1

4.1 Assessing the Health of the

Economy: Performance and Policy

• Real GDP measures the value of final goods and services produced within the borders of a given country during a given time period, typically a year.

• To calculate real GDP, nominal GDP must first be calculated

4 LO4.1

Real GDP

(real gross domestic product)

• The dollar value of all goods and services produced within the borders of a given country using the country’s current prices during the year the goods and services were produced.

5 LO4.1

Nominal GDP

• A failure of the economy to fully employ its labour force

• Occurs when a person cannot get a job despite being willing to work and actively seeking work

6 LO4.1

Unemployment

• An increase in the overall level of prices.

• Can cause decreases in standard of living

• surprise jump in inflation reduces the purchasing power of people’s savings

7 LO4.1

Inflation

• Can governments promote long-run economic growth?

• Can governments reduce the severity of recessions by smoothing out short-run fluctuations?

• Are certain government policy tools, more effective at mitigating short-run fluctuations than other government policy tools, e.g. monetary policy versus fiscal policy?

• Is there a trade-off between lower rates of unemployment and higher rates of inflation?

• Does government policy work best when it is announced in advance or when it is a surprise?

8 LO4.1

Macroeconomics models help

clarify government economic

policies

• Modern economic growth refers to an increase in output per person as compared with earlier times in which output (but not output per person) increased.

• The vast differences in living standards seen today between rich and poor countries are almost entirely the result of the fact that only some countries have experienced modern economic growth.

9 LO4.2

4.2 The Miracle of Modern

Economic Growth

Country GPD per capita, 2008 (U.S. dollars based on

purchasing power parity)

United States 46,859

Canada 39,183

United Kingdom 36,523

France 34,208

Japan 34,100

South Korea 27,647

Saudi Arabia 23,834

Russia 15,922

Mexico 14,560

China 5,963

India 2,762

North Korea 1,700

Tanzania 1,352

Burundi 389

Source: International Monetary Fund, www.imf.org, for all countries except North Korea, the data for which come from the

CIA World Factbook, www.cia.gov.

10 LO4.2

GDP per capita, selected countries Global Perspective 4.1

• To raise living standards over time an economy must devote at least some fraction of its current output to increasing future output

• Savings: The accumulation of funds that results when people in an economy spend (consume) less than their incomes during a given time period

• Savings fund Investment

11 LO4.3

4.3 Savings, Investment, and

Modern Economic Growth

• Investment refers to spending for the production and accumulation of capital and additions to inventories.

• Economists distinguish between financial investment and economic investment.

• Financial investment refers to the purchasing of financial assets (stocks, bonds, mutual funds) or real assets (houses, land, factories), or building such assets, in the expectation of financial gain.

• Economic investment refers to spending for the production and accumulation of capital and additions to inventories.

12 LO4.3

Investment

• Households are the principal source of savings, but businesses are the main economic investors

• These institutions collect the savings of households, rewarding savers with interest and dividends and sometimes capital gains (increases in asset values).

• The banks and other financial institutions then lend the funds to businesses, which invest in equipment, factories, and other capital goods

13 LO4.3

Banks and Other Financial

Institutions

• Expectations: The anticipations of consumers, firms, and others about future economic conditions.

• Expectations have a large effect on economic growth

• Expectations can become unmet due to shocks

14 LO4.4

4.4 Uncertainty, Expectations,

Shocks, and Short-Run

Fluctuations

• Shocks: Situations in which one thing is expected to occur but in reality something different occurs.

• Two types of shocks: demand shocks and supply shocks.

• Demand shocks: Sudden, unexpected changes in demand.

• Supply shocks: Sudden, unexpected changes in aggregate supply

• Economists believe that most short-run fluctuations are the result of demand shocks

15 LO4.4

Shocks

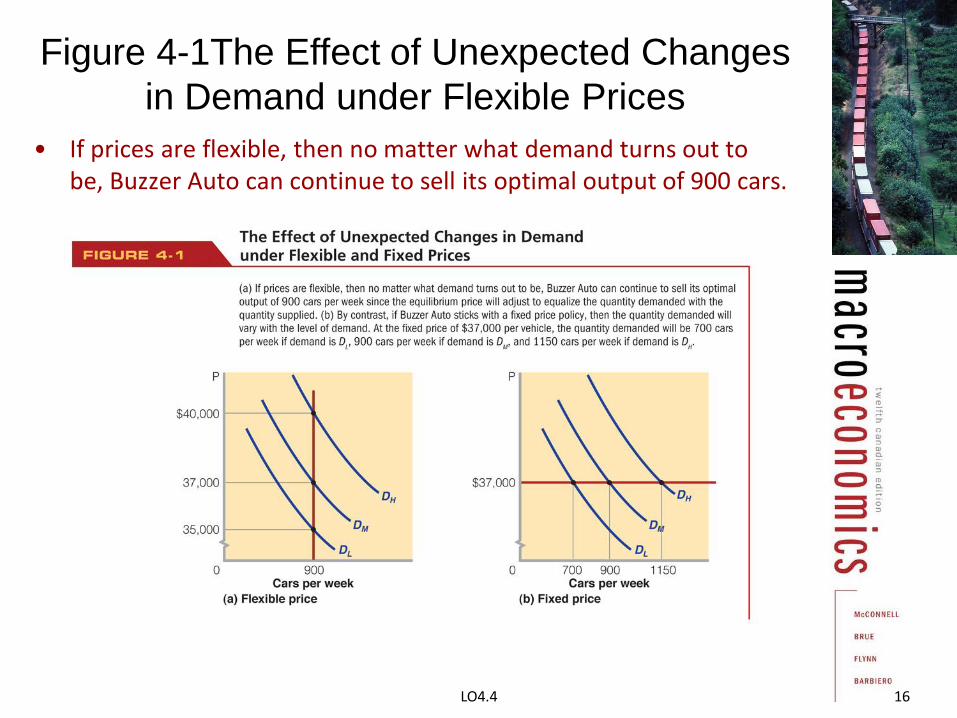

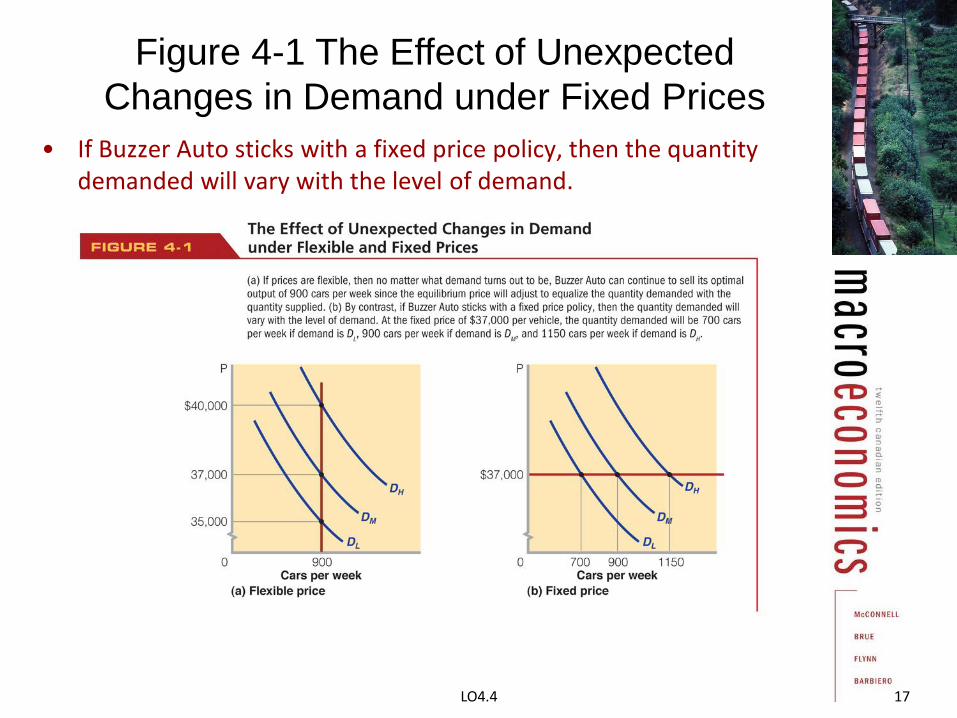

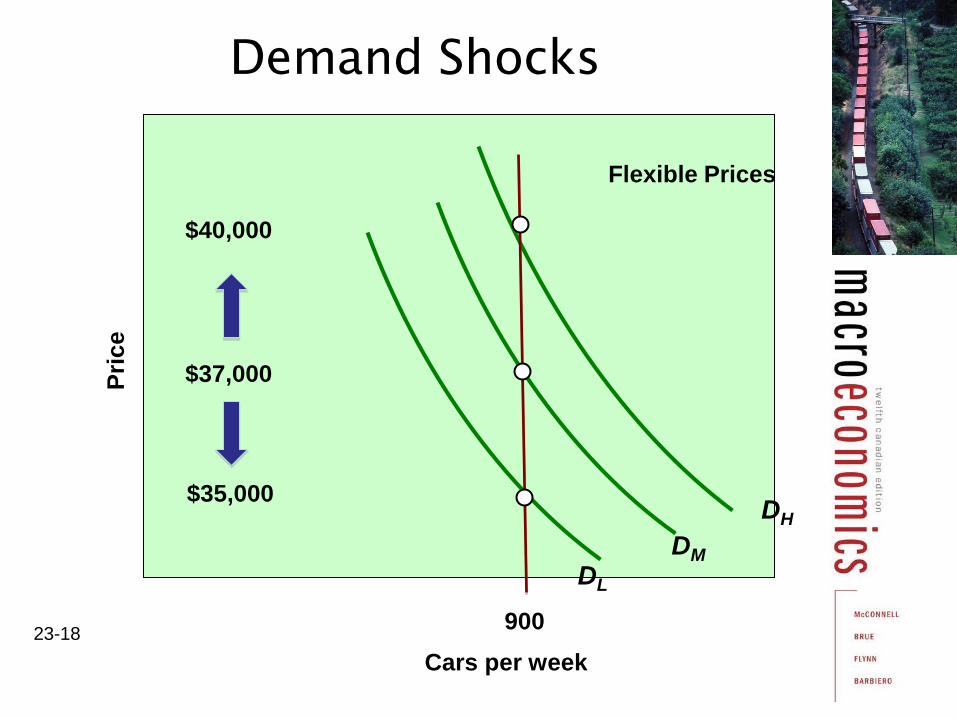

• If prices are flexible, then no matter what demand turns out to be, Buzzer Auto can continue to sell its optimal output of 900 cars.

16 LO4.4

Figure 4-1The Effect of Unexpected Changes

in Demand under Flexible Prices

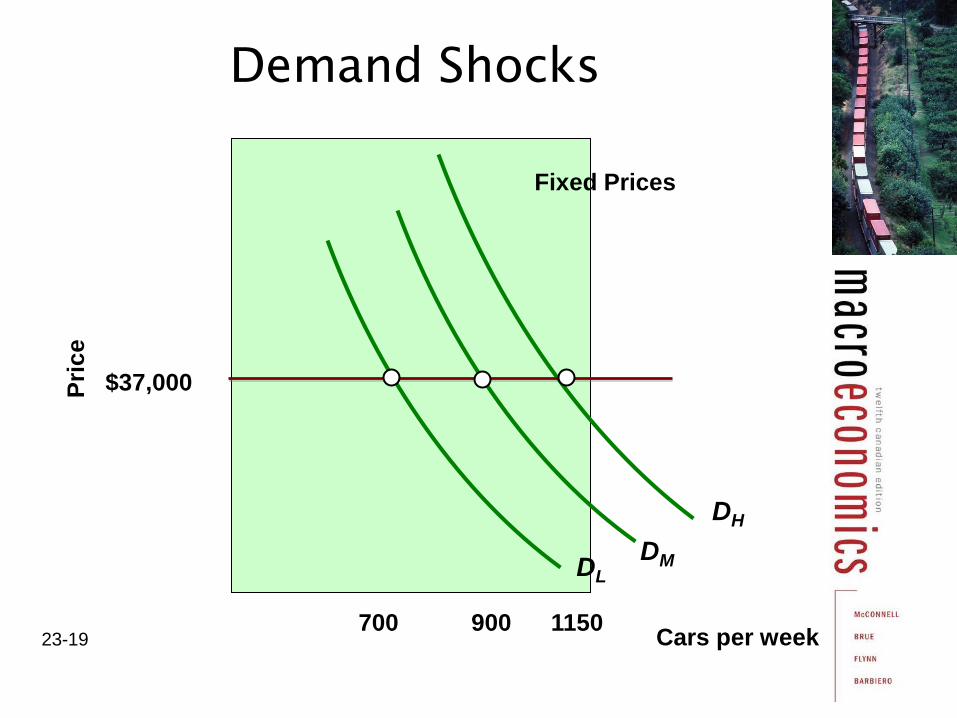

• If Buzzer Auto sticks with a fixed price policy, then the quantity demanded will vary with the level of demand.

17 LO4.4

Figure 4-1 The Effect of Unexpected

Changes in Demand under Fixed Prices

23-18

Demand Shocks

Cars per week

Pri

ce

DM

DL

DH

900

$40,000

$37,000

$35,000

Flexible Prices

23-19

Demand Shocks

Cars per week

DM DL

DH

700 900 1150

$37,000

Fixed Prices

Pri

ce

• If the prices of goods and services could always adjust quickly to unexpected changes in demand, then the economy could always produce at its optimal capacity since prices would adjust to ensure that the quantity demanded of each good and service would always equal the quantity supplied.

20 LO4.4

Demand Shocks and Flexible Prices

• In reality, many prices in the economy are inflexible and do not change rapidly when demand changes unexpectedly.

• Manufacturing firms typically attempt to deal with unexpected changes in demand by maintaining an inventory

• Inventory : Goods that have been produced but remain unsold.

• If demand falls for many goods and services across the entire economy for an extended period of time, then many firms will find inventories piling up and will be forced to cut production resulting in recession, with GDP falling and unemployment rising.

• If, however, demand is unexpectedly high for a prolonged period of time, the economy will boom and unemployment will fall.

21 LO4.4

Demand Shocks and Inflexible Prices

• Inflexible prices (sticky prices): Product prices that remain in place (at least for a while) even though supply or demand has changed.

• Flexible prices: Product prices that react within seconds to changes in supply and demand.

22 LO4.4

How Sticky are Prices?

Item Months Coin-operated laundry machines 46.4 Newspapers 29.9 Haircuts 25.5 Taxi fares 19.7 Veterinary services 14.9 Magazines 11.2 Computer software 5.5 Beer 4.3 Microwave ovens 3.0 Milk 2.4 Electricity 1.8 Airline tickets 1.0 Gasoline 0.6

Source: Mark Bils and Peter J. Klenow, “Some Evidence on the Importance of Sticky Prices,” Journal of Political Economy, October 2004, pp. 947–85.

23 LO4.4

Table 4-1 Average Number of Months between Price

Changes for Selected Goods and Services

• Companies selling final goods and services know that consumers prefer stable, predictable prices that do not fluctuate rapidly with changes in demand.

• In certain situations a firm may be afraid that cutting its price may be counterproductive because its rivals might simply match the price cut—a situation often referred to as a price war.

24 LO4.4

What Causes Sticky Prices?

• Price stickiness moderates over time.

• If unexpected changes in demand begin to look permanent, many firms will allow their prices to change so that price changes (in addition to quantity changes) can help to equalize quantities supplied with quantities demanded.

• Prices go from stuck in the extreme short run to fully flexible in the long run.

25 LO4.4

Categorizing Macroeconomic Models

Using Price Stickiness

The Last Word: Inventory

Management and Recessions

• Computerized inventory tracking

• Unexpected changes in demand easier to observe

• Firms make better output and employment decisions

• Less severe business cycles

• Only one mild recessions since adoption -Possible explanation

LO4.4 26

4.1 Assessing the Health of the Economy: Performance and Policy

4.2 The Miracle of Modern Economic Growth and its Components

4.3 Savings, Investment, and Modern Economic Growth

4.4 Uncertainty, Expectations, Shocks, and Short-Run Fluctuations

27 LO4.1

Chapter 4 Summary