Embed Size (px)

Citation preview

Chapter 8

Net Present Value and

Other Investment Criteria

(Capital Budgeting)

The Capital Budgeting Issue

The Capital Budgeting Issue– One of the most important issues in Corporate

Finance• Launch a new project• Enter a new market

– Determines the nature of the firm’s operations and products for years to come

– Fixed asset investments are generally long-lived and not easily reversed once made

• Fixed assets define the business of the firm

Capital Budgeting

Techniques used to analyze potential business ventures to decide which are worth undertaking:

– *Net Present Value (NPV)• Preferred Approach

– *Internal Rate of Return (IRR)

– Payback Period

– Average Accounting Return (AAR)

– Profitability Index (PI)

Capital Budgeting

Good Capital Budgeting criterion must tell us two things

1. Is a particular project a good investment?

2. If we have more than one good project, but we can only take one of them, which one should we take?– We’ll see that: only the NPV criterion can

always provide the correct answer to both questions

Net Present Value (NPV)

Net Present ValueThe Basic Idea

The goal of the financial manager is to create value for the stockholders

Potential investments must be examined A widely used procedure for doing this is

the “Net Present Value” approach

Net Present ValueThe Basic Idea

We create value by identifying an investment worth more in the marketplace than it costs us to acquire

Capital Budgeting is about trying to determine whether a proposed investment or project will be worth more than it costs once it’s in place

Net Present ValueThe Basic Idea

The Net Present Value (NPV) – is the difference between an investment’s market value and its costs– A way of assessing the profitability of a proposed

investment– The preferred approach in principle and typically in

practice Given the goal of creating value for the

stockholders:– Capital budgeting is a search for investments with

positive net present values

Net Present ValueEstimating Net Present Value

Estimate the cost of the project or investment

Estimate the future cash flows– Discount those cash flows to estimate the

present value of the future cash flows

NPV = The Present Value of the Future Cash Flows less the initial cost of the project or investment.

Net Present ValueNet Present Value Rule

If NPV is positive:– Accept the project or investment– Increases the total value of the stock– The greater the NPV, the greater the increase in the value of the

stock If NPV is negative:

– Reject the project or investment– Decreases the total value of the stock

If NPV is zero:– Indifferent – between taking or not taking the project or

investment– Break-even proposition– Value is neither created nor destroyed

Net Present Value Example 8.1, Page 211

Suppose we are asked to decide whether or not a new consumer product should be launched.

Based on projected sales and costs, we expect that the cash flows over the five-year life of the project will be: $2,000 in the first two years, $4,000 in the nest two, and $5,000 in the last year.

It will cost about $10,000 to begin production. We use a 10% discount rate to evaluate new

products. What should we do here?

Net Present ValueExample 8.1, Page 211

hp 12C Keystrokes Inst Manual Pg 70, 71,& 72– Use Shift Keys: g – blue f – yellow

CHS g CF0 = -10,000 Cost to begin project g CFj = 2,000 1st Yr Cash Flow Amt g CFj = 2,000 2nd Yr Cash Flow Amt g CFj = 4,000 3rd Yr Cash Flow Amt g CFj = 4,000 4th Yr Cash Flow Amt g CFj = 5,000 5th Yr Cash Flow Amt i = 10% f NPV = 2,313

– Based on the NPV Rule: since NPV is positive, we should take on, or “Accept” the project.

– Note: When NPV is negative “Reject” the project.

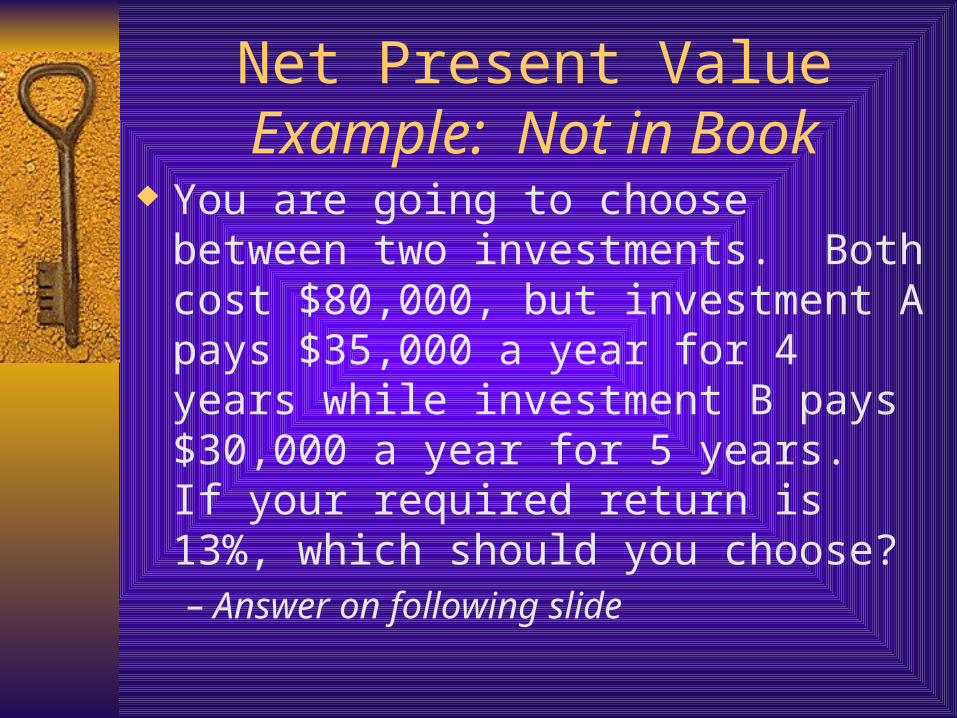

Net Present ValueExample: Not in Book

You are going to choose between two investments. Both cost $80,000, but investment A pays $35,000 a year for 4 years while investment B pays $30,000 a year for 5 years. If your required return is 13%, which should you choose?– Answer on following slide

Net Present ValueExample: Not in Book

Answer to previous slide:– NPV for Investment A = 24,106.50– NPV for Investment B = 25,516.94– Choose Investment B because it has a higher

NPV.

Net Present ValueExample: Problem 10.b. – Page 233

Darby & Davis, LLC, has identified the following two mutually exclusive projects. If the required return is 11 %, what is the NPV for each of these projects? Which project will you choose if you apply the NPV decision rule?Year Cash Flow (A) Cash Flow (B) 0 -17,000 -17,000 1 8,000 2,000 2 7,000 5,000 3 5,000 9,000 4 3,000 9,500NPV for Project (A) = $1,520.71NPV for Project (B) = $1,698.58Choose Project B it has the highest NPV

Internal Rate of Return(IRR)

The Internal Rate of Return

Internal Rate of Return (IRR) – is simply the discount rate that makes the NPV of an investment zero.– Put another way: It’s the rate of return at which the

discounted future cash flows = the initial cash outlay

– “Internal” rate – only depends on the cash flows of a particular investment, not on rates offered elsewhere

– Closely related to NPV

– The most important alternative to NPV

The Internal Rate of Return

IRR Rule: – Accept: if the IRR exceeds the “required rate of

return”

– Reject: if the IRR is below (less than) the “required rate of return”

– For Example: if your organization decides that it only wants to take on those projects with a return of 10% (10% is the required return), then you would:

• “Accept” all projects with an IRR greater than 10%

• “Reject” all projects with an IRR less than 10%.

The Internal Rate of Return Example 8.3, Page 220

hp 12C Keystrokes Inst Manual Pg 70, 71,& 72– Use Shift Keys: g – blue f – yellow

CHS g CF0 = -435.44 Up-Front Cost g CFj = 100 1st Yr Cash Flow g CFj = 200 2nd Yr Cash Flow g CFj = 300 3rd Yr Cash Flow f IRR = 15% Conclusion:

– Since IRR = 15% and the required rate of return is 18% – Reject: the IRR is below the “required rate of return”

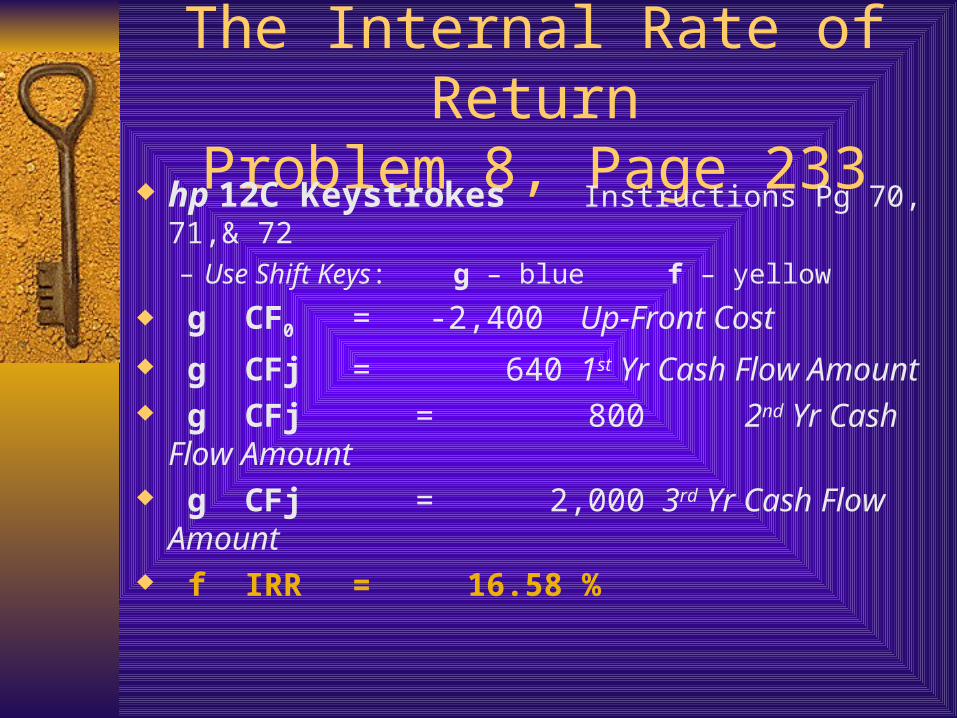

The Internal Rate of ReturnProblem 8, Page 233

hp 12C Keystrokes Instructions Pg 70, 71,& 72– Use Shift Keys: g – blue f – yellow

g CF0 = -2,400 Up-Front Cost

g CFj = 640 1st Yr Cash Flow Amount g CFj = 800 2nd Yr Cash Flow

Amount g CFj = 2,000 3rd Yr Cash Flow

Amount f IRR = 16.58 %

The Internal Rate of ReturnProblems with IRR

Non-conventional Cash Flows (Page 221):– Multiple Answers (rates of return) – the possibility that

more than one discount rate makes the NPV of an investment zero

– When cash flows aren’t conventional, strange things start to happen with IRR:

• Some computers/calculators just report the first IRR

• Others report the smallest IRR

– What is the return?....becomes difficult to answer

– Read Page 221 and 222

The Internal Rate of ReturnProblems with IRR

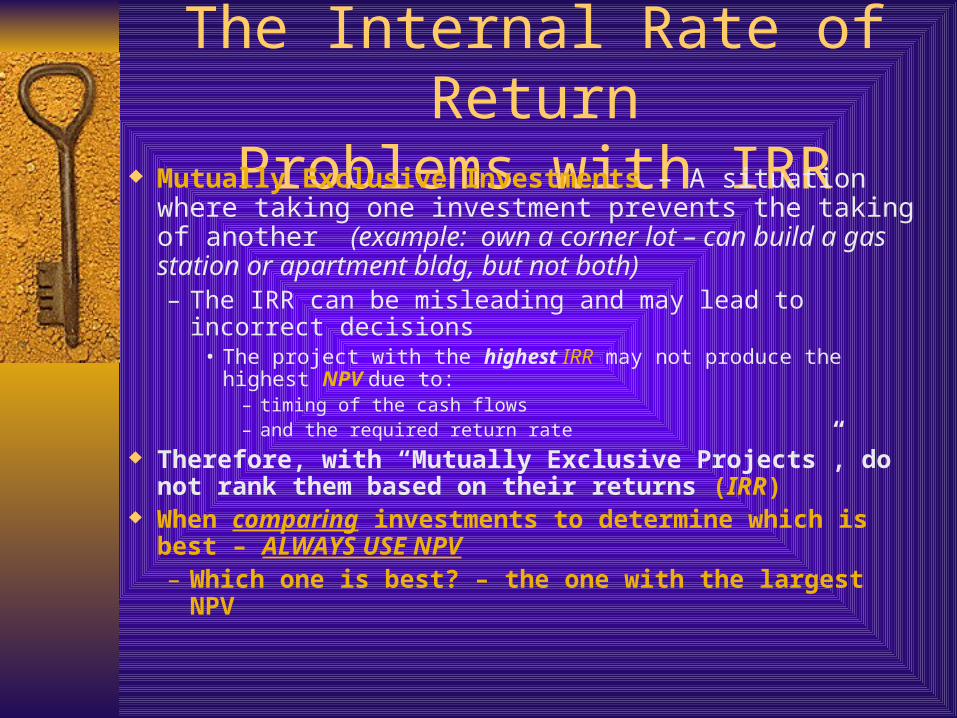

Mutually Exclusive Investments – A situation where taking one investment prevents the taking of another (example: own a corner lot – can build a gas station or apartment bldg, but not both)– The IRR can be misleading and may lead to incorrect decisions

• The project with the highest IRR may not produce the highest NPV due to:

– timing of the cash flows – and the required return rate

Therefore, with “Mutually Exclusive Projects”, do not rank them based on their returns (IRR)

When comparing investments to determine which is best – ALWAYS USE NPV– Which one is best? – the one with the largest NPV

The Internal Rate of ReturnRedeeming Qualities of IRR

IRR can be calculated w/o knowing the appropriate discount rate, NPV can’t.

Easy to understand and communicate.

The Payback Rule

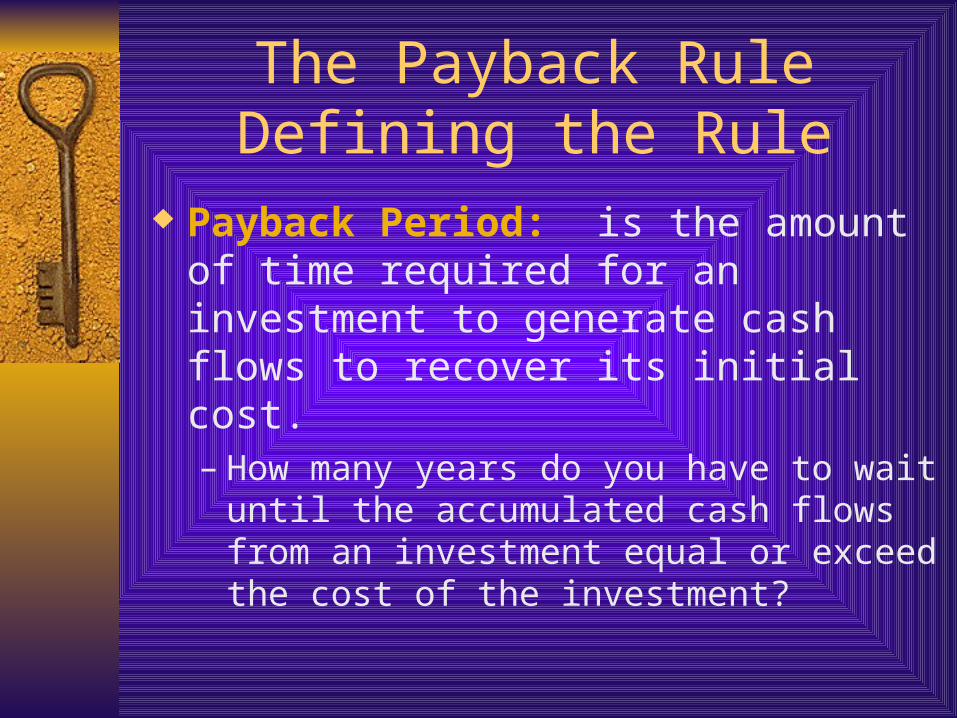

The Payback RuleDefining the Rule

Payback Period: is the amount of time required for an investment to generate cash flows to recover its initial cost.– How many years do you have to wait until the

accumulated cash flows from an investment equal or exceed the cost of the investment?

The Payback RuleDefining the Rule

Payback Rule: an investment is acceptable if its calculated payback period is less than some pre-specified number of years.– Accept: if the payback period is less than or

equal to the specified number of years– Reject: if the payback period is greater than

the specified number of years Example 8.2, Page 213:

– Calculating Payback

The Payback RuleAnalyzing the Rule

Severe shortcomings as compared to NPV– No discounting: the time value of money is ignored

• Projects may be accepted that are worth less than they cost

– Considers no risk differences • Calculated the same way for both very risky and very safe

projects

– Problems with determining the exact cut-off period

– Cash flows after the payback period are ignored• Bias toward short term investments

• Profitable long term investments may be rejected

The Payback RuleRedeeming Qualities of the Rule Useful for relatively minor decisions In general: an investment that pays back

rapidly and has benefits extending beyond the cutoff period probably has a positive NPV

The Payback RuleSummary of the Rule

A kind of “break-even” measure– In an accounting sense

– Not an economic sense• because time value is ignored

It determines how long it takes to recover the initial investment, not the impact an investment will have on the value of the stock

Due to its simplicity, it’s a useful simple rule of thumb - as a screen for dealing with many minor investment decisions

Average Accounting Return

The Average Accounting Return Average Accounting Return (AAR): An

investment’s average net income divided by its average book value:

Average net incomeAverage book value

AAR Rule: – Accept the project if its average accounting return

exceeds a target average account return– Reject: Otherwise

Example in book: Page 216 and 217– Excel Spreadsheet

The Average Accounting Return The AAR Rule has many problems:

– AAR is not a true rate of return. It ignores time value.• It’s a ratio of two accounting numbers and not comparable to

returns offered in the financial markets.

• Based on accounting net income and book values, instead of cash flows and market values

– Doesn’t indicate the effect on share price from taking the investment

– However, it is easy to calculate and needed info is usually available

The Profitability Index

The Profitability Index Profitability Index (PI) – Present Value of an investment’s

future cash flows divided by its initial cost. Also called the Benefit-Cost RatioPI = PV / Initial Cost

If a project costs $200 and the present value of its future cash flows is $220:PI = PV / Initial CostPI = 220 / 200 = 1.10– For every dollar invested $.10 in NPV results– PI measures the value created per dollar invested

• Often proposed as a measure of performance for government or other not-for-profit investments

• When capital is scarce, it may make sense to allocate it to those projects with the highest PIs

The Profitability Index PI > 1 for projects with a positive NPV PI < 1 for projects with a negative NPV

– Remember: Positive NPV means that the PV of the future cash flows is greater than the initial investment

PI may lead to incorrect decisions when considering mutually exclusive projects– The PI Index cannot be used to rank mutually exclusive

projects Always go with the project with the highest

NPV!

The Practice ofCapital Budgeting

While NPV is considered superior, its calculation involves only “estimated” future cash flows. – The result can be very “soft”.

• For this reason firms typically use multiple criteria for evaluating a proposal

Chapter 8Suggested Homework

Know Chapter theories, concepts and definitions

Suggested NPV Homework problems:– Problem 8.1 – Page 229– Problems 6, 9, and 10.b. – Page 233– Problem 16.b & c – Page 235– Problem 19.b & c and 22.b & c – Page 236– Problem 23.b and c – Page 237

Chapter 8Suggested Homework

Suggested IRR Homework problems:– Problem 5 - Page 232-3

– Problem 8, 10a - Page 233

– Problem 16a - Page 235

– Problem 23a - Page 236-7

– Problem 25a - Page 237

Chapter 8Suggested Homework

Suggested Payback Rule Homework problems:– Problems 1 - Page 232

Suggested Average Accounting Return Homework problems:– Problem 4, Page 232

Suggested Profitability Index Homework:– Problem 13, Page 234