Embed Size (px)

Citation preview

Section 20.1 ManagingPurchasing

Section 20.2 ManagingInventory

OBJECTIVES

Define purchasing Explore factors in purchasing management Learn about the process of purchasing

2Section 20.1: Managing Purchasing

Procurement is the act of purchasing. Vendors (suppliers) are businesses that sell

products or services to other businesses. In large companies, individuals who have

purchasing responsibilities are called buyers, or purchasing managers.

3Section 20.1: Managing Purchasing

Quality covers many aspects of a product or service. One tool for making decisions about quality is called

value analysis, which is a process for assessing the performance of a product or service relative to its cost.

Sales forecasting (demand forecasting) is predicting future sales based on past sales data (or other available information) and expected market conditions in the future.

4Section 20.1: Managing Purchasing

Sales and inventory data help purchasing managers schedule the best times to place reorders.

Sourcing is choosing appropriate vendors to supply desired goods or services.

Buyers planning to make a large or expensive purchase ask several vendors to provide a price quote. A quantity discount is a discount given to buyers for

purchasing a large quantity of a product or service from a vendor.

Volume buying means purchasing a large quantity from a vendor, typically to take advantage of a quantity discount.

A trade discount is a discount given to resellers who are in the same trade, industry, or distribution chain as a vendor.

Many vendors allow established business customers extra time to pay for purchases.

5Section 20.1: Managing Purchasing

Common types of purchasing paperwork are: Product Specification. This is a written, detailed

description of the characteristics. Purchase Order. This is a document issued by a buyer

to a vendor that lists the items to be purchased, their quantities and prices, and other relevant information, such as delivery or payment terms.

Invoice. An invoice (bill of sale) is a document issued by a vendor to a buyer on fulfillment of a purchase order.

Packing Slip. A packing slip is a list of all items in a shipment.

6Section 20.1: Managing Purchasing

OBJECTIVES

Learn why managing inventory is important Investigate ways to plan inventory levels and

investments Research methods for controlling inventory

levels

7Section 20.2: Managing Inventory

The quantity of merchandise is called the inventory level, and the monetary value of the merchandise is called the inventory value.

Inventory is a business asset. The goal of inventory management is not to have

too little or too much. A stock-out occurs when an item in inventory is completely

gone and can cause customers to go elsewhere to shop. Excess inventory ties up money that could be used for other

purposes. Obsolescence is the process of becoming obsolete, which

means no longer useful or desirable.

8Section 20.2: Managing Inventory

Start-up businesses do not have previous sales data on which to base inventory-level decisions. However, with proper planning, entrepreneurs can estimate how much inventory they should have for opening day.

An ongoing business uses many data sources for inventory-planning purposes. Inventory managers can use this data to predict how inventory levels are going to decrease over time and decide when to reorder merchandise

9Section 20.2: Managing Inventory

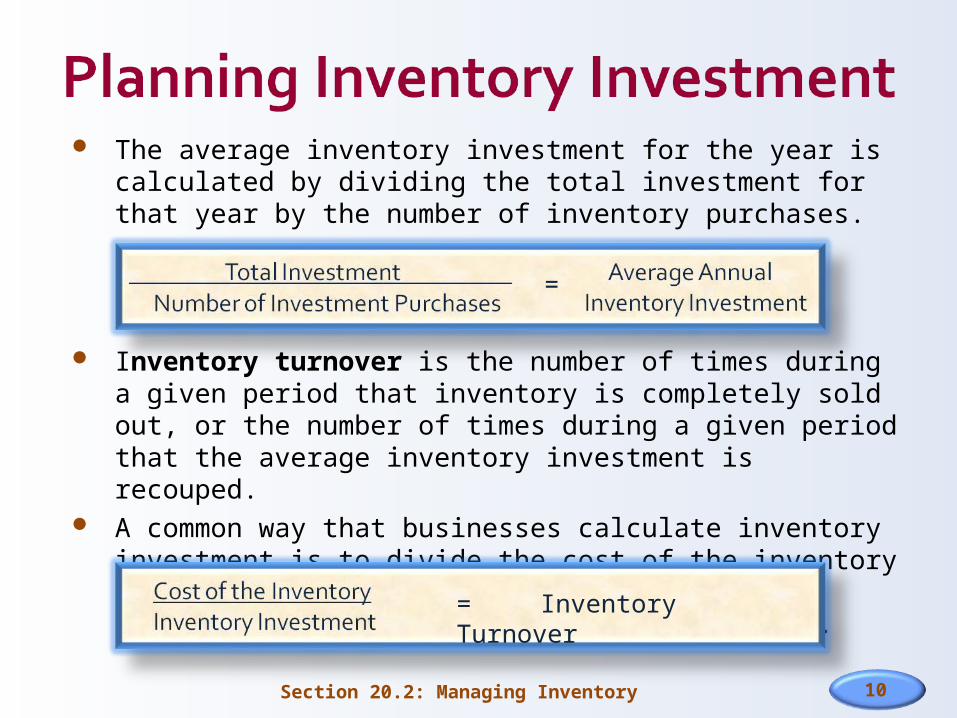

The average inventory investment for the year is calculated by dividing the total investment for that year by the number of inventory purchases.

Inventory turnover is the number of times during a given period that inventory is completely sold out, or the number of times during a given period that the average inventory investment is recouped.

A common way that businesses calculate inventory investment is to divide the cost of the inventory sold during a time period by the average inventory investment during that same period.

10Section 20.2: Managing Inventory

=

= Inventory Turnover

Inventory shrinkage is any loss of inventory that occurs between the time the inventory is purchased and the time it is sold or otherwise removed from the shelves.

An inventory system is a process for counting and tracking inventory so inventory value can be calculated. A visual inventory system is used by small businesses owners to

count inventory items physically. A perpetual inventory system tracks inventory on a continual

basis and calculates the inventory value, for accounting purposes, after each inflow or outflow occurs.

A periodic inventory system calculates inventory value for accounting purposes at periodic times when a physical inventory count is performed.

In a just-in-time (JIT) inventory system, the goal is to maintain just enough inventory to keep the business operating, with virtually no inventory kept in storage.

Some businesses use warehouses to store inventory, particularly if inventory levels are high.

11Section 20.2: Managing Inventory