Embed Size (px)

Citation preview

Please refer to page 14 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

CHINA

Inside

Market & Sector Performance

(HK stocks) 2

Market & Sector Performance

(China stocks) 3

Activity data watch 4

Policy outlook 5

Commodities space 6

Property market 7

Liquidity watch 8

Exchange rate 9

Industrial indicators 10

China in a snapshot 11

Macquarie China Macro Products 13

Data review and preview

Date Indicator Actual MacQ Cons. Prev. Review 27-Apr Industrial profits,

% yoy 11.1 -- -- 4.8

1-May NBS PMI 50.1 50.6 50.2 50.2 Preview 8-May Exports, %yoy -- -4.0 1.3 11.5 8-May Imports, %yoy -- -6.0 -4.0 -7.6 8-May Trade bal., US$

bn -- 36 36 30

Source: Bloomberg, Macquarie Research, May 2016

2 May 2016 Macquarie Capital Limited

Macro Monday Improved earnings outlook amid higher risk premium Investors cautious on macro uncertainties: Last week H-shares fell 2%

while A-shares dipped 0.7%. Market sentiment turned more cautious as

shown by lower daily turnover (Fig 6 & 12). Last week the oil price hit fresh

new highs for this year while the dollar fell to a 15-month low. But commodity

prices retreated in Shanghai as investors realized the prices had entered

“bubble” territory. Meanwhile, bond yields and credit spread continued to rise.

Earnings outlook has improved: While the financial sector saw worsened

earnings growth in 1Q16 due to the drag from brokers and insurance, the

earnings outlook for the rest of the market has improved notably. As the high-

frequency proxy for listcos, earnings growth for industrial companies (reported

by the NBS) jumped to 7.4% yoy in 1Q16 after six disappointing quarters with

little or negative growth. The main drivers behind the pick-up are the

rebounding property sector and the narrowed PPI deflation. Looking ahead,

we expect property investment to grow 7% this year (vs. 1% in 2015) and our

commodity team expects oil prices to rise above $50 in 2H16. If both are

correct, corporate earnings would see a large upswing this year despite lower

headline GDP growth (Thoughts on earnings cycle: A new start?).

…but with higher risk premium: Despite the improved earnings outlook, risk

premium has also edged up due to the recent turbulence in China’s bond

market. Currently, China’s bond market is under multiple headwinds including

neutralizing monetary policy, higher credit risks even from SOEs and rising

inflation expectation. In the past, the turmoil in the bond market could cause

stock prices to slump, such as in Aug 2011 and June 2013. Therefore,

investors now prefer to take a wait-and-see stance. Will another “credit

crunch” like June 2013 happen again? We think the chance is low, given all

the short-term liquidity tools developed by the PBoC since then. However,

credit spread was indeed ridiculously low earlier this year because of

abundant liquidity and poor risk pricing. As investors realize it, some short-

term pains are inevitable.

PMI weaker than expected but still upbeat: Yesterday, the NBS

manufacturing PMI came in at 50.1 (consensus: 50.3). That said, by looking

into details, we reckon that the recovery still continues. “Finished goods

inventory” dropped to 45.5, suggesting that demand remains strong and

potential restocking lies ahead. “New orders”, albeit moderating to 51.0 (last

month: 51.4), remains as the second highest since Oct 2014. Overall,

headline growth including industrial production and trade could turn lower in

April, mainly because the strong readings in March were boosted by base

effect. But growth momentum remained robust while the PPI deflation would

ease further (See April data preview: Fighting with deflation).

Two thematic reports on RMB and capital flows: At the beginning of this

year, China’s currency and capital outflows were the primary concerns

globally for investors. However, such concerns have eased a lot lately. These

are the first-order macro questions globally but are not well understood by the

street. For those interested in these topics, this Feb we published a thematic

report on the RMB (RMB: The inescapable dilemma). Last week, we

published another thematic study on China’s capital flows, Dissecting China’s

capital outflows in 2015, which aims to debunk the numerous myths on this

issue.

Macquarie Wealth Management Macro Monday

2 May 2016 2

Market & Sector Performance (HK stocks)

Fig 1 MSCI China sector performance: 1 week Fig 2 MSCI China sector performance: YTD

Source: DataStream, Macquarie Research, May 2016 Source: DataStream, Macquarie Research, May 2016

Fig 3 MSCI China fell 2.3% last week Fig 4 MSCI China valuation

Source: DataStream, Macquarie Research, May 2016 *Latest as of 29 April 2016. Source: DataStream, Macquarie Research, May 2016

Fig 5 A-H premium Index Fig 6 HK market daily turnover

Source: CEIC, Macquarie Research, May 2016 Source: Bloomberg, Macquarie Research, May 2016

-5.5

-5.5

-3.8

-3.5

-3.1

-2.5

-2.4

-2.3

-2.0

-1.9

-1.4

-1.0

-1.0

-0.6

-6 -5 -4 -3 -2 -1 0

Utilities

Diversified financial

Cons disc

Insurance

Industrials

Cons staple

Telecom

MSCI China

Healthcare

I.T.

Banks

Real estate

Materials

Energy

MSCI China: 1-week performance (%)

-19

-10

-10

-10

-10

-8

-8

-7

-5

-3

-1

2

9

15

-25 -15 -5 5 15

Insurance

Real estate

Cons disc

Utilities

Healthcare

Diversified financial

Banks

Industrials

MSCI China

Cons staple

I.T.

Telecom

Materials

Energy

MSCI China: YTD performance (%)

45

50

55

60

65

70

75

80

85

Feb-1

4

Mar-

14

Ap

r-1

4

May-1

4

Ju

n-1

4

Jul-1

4

Aug-1

4

Sep

-14

Oc

t-1

4

No

v-1

4

Dec-1

4

Jan-1

5

Feb

-15

Mar-

15

Ap

r-1

5

May-1

5

Jun-1

5

Ju

l-1

5

Aug-1

5

Sep-1

5

Oc

t-1

5

Nov-1

5

De

c-1

5

Jan-1

6

Feb-1

6

Mar-

16

Ap

r-1

6

MSCI China Index

22%

-34%39%

-25%

5

7

9

11

13

15

17

19

21

23

25

Ap

r-0

6

Ap

r-0

7

Ap

r-0

8

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

Ap

r-1

5

Ap

r-1

6

MSCI China 12m-forward PE

Avg. since 2004 = 11.4x

10.7x

+1 S.D. = 14.3x

-1 S.D. = 8.6x

85

95

105

115

125

135

145

155

165

175

Dec-0

8

Apr-

09

Au

g-0

9

Dec-0

9

Apr-

10

Au

g-1

0

Dec-1

0

Apr-

11

Au

g-1

1

Dec-1

1

Apr-

12

Au

g-1

2

Dec-1

2

Apr-

13

Au

g-1

3

Dec-1

3

Apr-

14

Au

g-1

4

Dec-1

4

Apr-

15

Au

g-1

5

Dec-1

5

Apr-

16

AH premium indexParity = 100

0

50

100

150

200

250

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oc

t-1

5

Ja

n-1

6

Ap

r-1

6

Weekly average daily turnover

HKD bn HKEx Main Board

70

Macquarie Wealth Management Macro Monday

2 May 2016 3

Market & Sector Performance (China stocks)

Fig 7 CSI300 sector performance: 1 week Fig 8 CSI300 sector performance: YTD

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 9 China stocks dipped 0.7% last week Fig 10 A-share valuation

Source: DataStream, Macquarie Research, May 2016

*Latest as of 29 April 2016. Source: DataStream, Macquarie Research, May 2016

Fig 11 CSI300 vs. ChiNext Fig 12 A-share daily turnover

Source: Bloomberg, Macquarie Research, May 2016 Source: Bloomberg, Macquarie Research, May 2016

-1.5

-1.1

-1.1

-0.6

-0.6

-0.6

0.1

0.3

0.4

0.8

2.1

-2 -1 0 1 2 3

Industrial

Material

Financial

Utilities

Telecom

CSI300

Cons Disc.

IT

Energy

Health Care

Cons Staples

CSI300 sectors: 1-week performance (%)

-30

-24

-21

-19

-18

-15

-15

-12

-11

-6

-6

-35 -25 -15 -5

Telecom

Industrial

Utilities

Cons Disc.

IT

CSI300

Health Care

Financial

Material

Energy

Cons Staples

CSI300 sectors: YTD performance (%)

1900

2300

2700

3100

3500

3900

4300

4700

5100

Feb

-14

Mar-

14

Ap

r-1

4

May

-14

Jun-1

4

Jul-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

Nov

-14

Dec-1

4

Jan-1

5

Feb

-15

Mar-

15

Ap

r-1

5

Ma

y-1

5

Jun-1

5

Jul-1

5

Au

g-1

5

Se

p-1

5

Oc

t-1

5

Nov

-15

Dec

-15

Jan-1

6

Feb

-16

Mar-

16

Ap

r-1

6

Shanghai Composite

70%

68%-43%

-27%

5

10

15

20

25

30

35

Apr-

06

Apr-

07

Apr-

08

Apr-

09

Apr-

10

Apr-

11

Apr-

12

Apr-

13

Apr-

14

Apr-

15

Apr-

16

Shanghai A-share 12m-forward PE

Avg. since 2004 = 14.2x

12.6x

+1 S.D. = 19.8x

-1 S.D. = 8.6x

85

135

185

235

285

Jan

-14

Feb-1

4M

ar-

14

Apr-

14

May-1

4

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Feb-1

5M

ar-

15

Apr-

15

May-1

5

Jun

-15

Jul-

15

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan

-16

Feb-1

6M

ar-

16

Apr-

16

CSI300 ChiNext

1 Jan 14 = 100 Stock market performance

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Ap

r-1

2

Ju

l-1

2

Oc

t-1

2

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oc

t-1

3

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oc

t-1

5

Ja

n-1

6

Ap

r-1

6

Weekly average daily turnover

RMB bn China stock market

Macquarie Wealth Management Macro Monday

2 May 2016 4

Activity data watch

Fig 13 NBS vs Caixin Manufacturing PMI Fig 14 Industrial growth rebounded in March

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 15 Coal usage weakened again going into April Fig 16 Trade growth rebounded in March

Note: The latest coal-consumption figure represents the month-to-date average daily coal consumption growth from a year ago.

Source: Wind, Macquarie Research, May 2016

Source: CEIC, Macquarie Research, May 2016

Fig 17 CPI and PPI inflation Fig 18 Vegetable prices fell further last week

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

47

48

49

50

51

52

53

54

Se

p-1

1

De

c-1

1

Mar-

12

Jun

-12

Se

p-1

2

Dec-1

2

Mar-

13

Jun

-13

Se

p-1

3

Dec-1

3

Ma

r-1

4

Ju

n-1

4

Se

p-1

4

Dec-1

4

Mar-

15

Jun

-15

Se

p-1

5

Dec-1

5

Mar-

16

NBS Caixin

Manufacturing PMI

8.8

9.29.0

6.9

8.07.7

7.2

7.9

6.86.8

5.65.9

6.1

6.8

6.06.1

5.75.6

6.25.9

5.45.4

6.8

0.0

0.2

0.4

0.6

0.8

1.0

1.2

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

Ma

y-1

4

Ju

l-1

4

Sep

-14

No

v-1

4

Ja

n-1

5

Ma

r-1

5

Ma

y-1

5

Ju

l-1

5

Sep

-15

No

v-1

5

Ja

n-1

6

Ma

r-1

6

Industrial production, yoy

Industrial production, qoq - RHS

% yoy % mom

-30

-20

-10

0

10

20

30

40

50

Ap

r-1

2

Jun-1

2

Aug

-12

Oc

t-1

2

Dec

-12

Feb

-13

Ap

r-1

3

Ju

n-1

3

Aug

-13

Oc

t-1

3

Dec-1

3

Feb

-14

Ap

r-1

4

Jun-1

4

Aug

-14

Oc

t-1

4

Dec-1

4

Feb

-15

Ap

r-1

5

Jun-1

5

Aug

-15

Oc

t-1

5

Dec-1

5

Feb

-16

Ap

r-1

6

Daily coal consumption at major IPPs

National power generation

% yoy

-25

-15

-5

5

15

25

35

-10

0

10

20

30

40

50

60

70

Mar-

11

Sep-1

1

Ma

r-1

2

Sep-1

2

Mar-

13

Sep-1

3

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Trade balance - LHS

Export - RHS

Import - RHS

US$ bn %, yoy

-8

-6

-4

-2

0

2

4

6

8

10

Se

p-0

2

Jun

-03

Mar-

04

Dec-0

4

Se

p-0

5

Jun

-06

Ma

r-0

7

Dec-0

7

Se

p-0

8

Jun

-09

Mar-

10

Dec-1

0

Se

p-1

1

Jun

-12

Mar-

13

Dec-1

3

Se

p-1

4

Jun

-15

Ma

r-1

6

CPI

PPI

% yoy

2.3%

-4.3%

80

90

100

110

120

130

140

150

160

10 Jan

10 Feb

20 Mar

20 Apr

20 May

20 Jun

20 Jul

20 Aug

20 Sep

20 Oct

20 Nov

20 Dec

20 Jan

20 Feb

20 Mar

30 Apr

Pork Vegetables

Jan 15 = 100

Macquarie Wealth Management Macro Monday

2 May 2016 5

Policy outlook

Fig 19 Monthly new RMB loans Fig 20 M2 grew 13.4% YoY in March

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 21 Fiscal spending remained strong in 1Q16 Fig 22 Fixed asset investment improved in March

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 23 Benchmark 1-year deposit and lending rates Fig 24 Reserve requirement ratio

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

2,510

727

1,370

0

500

1,000

1,500

2,000

2,500

3,000

Ja

n

Fe

b

Ma

r

Apr

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oct

No

v

De

c

2014 2015 2016

Rmb bnNew RMB loans

5

10

15

20

25

30

35

Mar-

07

Sep

-07

Mar-

08

Sep

-08

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

M2 growth%. yoy

13.4

-10

-5

0

5

10

15

20

25

30

35

40

Se

p-1

2

Dec

-12

Mar-

13

Jun-1

3

Se

p-1

3

Dec

-13

Mar-

14

Jun-1

4

Se

p-1

4

Dec

-14

Mar-

15

Jun-1

5

Se

p-1

5

Dec

-15

Mar-

16

Fiscal spending

% yoy

2013: 10.9%

20.3%

2014: 8.2%

2015: 13.2%

-5

0

5

10

15

20

25

30

Jan

-14

Mar-

14

Ma

y-1

4

Jul-14

Se

p-1

4

Nov-1

4

Jan

-15

Mar-

15

May

-15

Jul-

15

Se

p-1

5

Nov-1

5

Jan

-16

Mar-

16

Overall FAI Manufacturing

Infrastructure Real Estate

% yoy FAI

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Oc

t-1

0

Ap

r-1

1

Oc

t-1

1

Ap

r-1

2

Oc

t-1

2

Ap

r-1

3

Oc

t-1

3

Ap

r-1

4

Oc

t-1

4

Ap

r-1

5

Oc

t-1

5

Ap

r-1

6

1-year deposit rate 1-year lending rate

%

Nov 14

Feb 15

Jun 15

Oct 15

May 15

Aug 15

1.50

4.35

14

15

16

17

18

19

20

21

22

Oct-

10

Apr-

11

Oct-

11

Apr-

12

Oct-

12

Apr-

13

Oct-

13

Apr-

14

Oct-

14

Apr-

15

Oct-

15

Apr-

16

RRR

%

Feb 2015

Apr 2015

Oct 2015

Feb 2016

Sep 2015

16.5

Macquarie Wealth Management Macro Monday

2 May 2016 6

Commodities space

Fig 25 Iron ore prices flattened last week Fig 26 Steel prices eased 2.1% last week

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 27 Coal prices were flat last week Fig 28 Cement prices rose 0.4% last week

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 29 Copper prices softened 2.3% last week Fig 30 Brent crude oil prices jumped 7.1% last week

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

35

55

75

95

115

135

155

175

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

USD/ton Iron ore

66

1,600

2,100

2,600

3,100

3,600

4,100

4,600

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

RMB/ton Steel

3,075

300

350

400

450

500

550

600

650

700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014 2015 2016

RMB/ton Coal

384

285

305

325

345

365

385

405

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

RMB/ton Cement

297

4,200

4,700

5,200

5,700

6,200

6,700

7,200

7,700

8,200

8,700

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

USD/ton Copper

4,893

25

45

65

85

105

125

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

USD/barrel

48

Crude oil: Brent

Macquarie Wealth Management Macro Monday

2 May 2016 7

Property market

Fig 31 Home prices saw continued rise in March Fig 32 62 out of 70 cities saw home prices increase

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 33 National property sales rebounded in 1Q16 Fig 34 Housing starts jumped in 1Q16

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

Fig 35 Top-city home sales remain strong in April Fig 36 Inventory-to-sales ratio eased in March

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

-15

-10

-5

0

5

10

15

20

Ma

r-1

2

Ju

n-1

2

Se

p-1

2

De

c-1

2

Ma

r-1

3

Ju

n-1

3

Sep

-13

De

c-1

3

Ma

r-1

4

Ju

n-1

4

Se

p-1

4

De

c-1

4

Ma

r-1

5

Ju

n-1

5

Sep

-15

De

c-1

5

Ma

r-1

6

yoy

mom annualized

% 70-city new home prices

0

10

20

30

40

50

60

70

Sep

-11

Nov-1

1

Jan-1

2

Mar-

12

May

-12

Ju

l-1

2

Sep

-12

Nov-1

2

Jan-1

3

Mar-

13

Ma

y-1

3

Jul-1

3

Sep

-13

Nov-1

3

Jan-1

4

Ma

r-14

May

-14

Jul-1

4

Sep

-14

Nov-1

4

Ja

n-1

5

Mar-

15

May

-15

Jul-1

5

Sep

-15

No

v-1

5

Jan-1

6

Mar-

16

Decline Flat IncreaseNo. of cities

-40

-20

0

20

40

60

80

100

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

Floor space sold

%, yoy

1Q04 - 2Q07: 37%

3Q07 - 4Q09: 20% 1Q10 - 2Q13:

9%

1Q16:33%

3Q13 - 1Q16: 6%

-30

-10

10

30

50

70

3Q

05

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

Housing starts

%, yoy

1Q04 - 2Q07: 14%

3Q07 - 2Q10: 23%

3Q10 - 4Q13: 11%

1Q16:19%

1Q14 - 1Q16: -9%

1000

2000

3000

4000

5000

6000

7000

8000

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2015 2016

thou sqm, 4wma Weekly housing transactions in 30 major cities

4

6

8

10

12

14

16

18

20

0

20

40

60

80

100

120

Jun-1

1

Sep

-11

Dec-1

1

Mar-

12

Jun-1

2

Sep

-12

Dec-1

2

Mar-

13

Ju

n-1

3

Sep

-13

Dec-1

3

Mar-

14

Jun-1

4

Sep

-14

Dec-1

4

Ma

r-15

Jun-1

5

Sep

-15

De

c-1

5

Mar-

16

Commodity housing inventory

Inventory-to-sales ratio (RHS)

sqm mn MonthsInventory in top 10 cities

Macquarie Wealth Management Macro Monday

2 May 2016 8

Liquidity watch

Fig 37 Strong liquidity supply Fig 38 Short-term interbank rates rose last week

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 39 Market interest rates Fig 40 Credit spread widened

Source: CEIC, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 41 Credit bond yields Fig 42 China vs US 10y Treasury yields

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

4.5

3.6

0.40.0

0.4 0.2 0.0

6.4

4.4

0.5

-0.9

1.2

0.30.8

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Total Loans Off-balance sheet

lending

FX purchase

Bond financing

Equity financing

Local govt debt

issuance

RMB, tn

Jan-Mar 2015 Jan-Mar 2016

Liquidity supply

1

3

5

7

9

11

Feb-0

7

Jul-

07

Dec

-07

May

-08

Oct-

08

Mar-

09

Au

g-0

9

Jan

-10

Jun

-10

Nov

-10

Apr-

11

Se

p-1

1

Feb-1

2

Jul-

12

Dec

-12

May

-13

Oct-

13

Mar-

14

Au

g-1

4

Jan

-15

Jun

-15

Nov

-15

Apr-

16

7-day repo rate 3m Shibor%

2.3

3.3

4.3

5.3

6.3

Ap

r-1

2

Jun

-12

Au

g-1

2

Oc

t-1

2

Dec

-12

Feb-1

3

Ap

r-1

3

Jun

-13

Au

g-1

3

Oc

t-1

3

Dec

-13

Feb-1

4

Ap

r-1

4

Jun

-14

Au

g-1

4

Oc

t-1

4

Dec

-14

Fe

b-1

5

Ap

r-1

5

Jun

-15

Au

g-1

5

Oc

t-1

5

Dec

-15

Feb-1

6

Ap

r-1

6

Expected annualized return of bank WMP: 3m

Annualized yield of Yu'E Bao

% pa

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Ap

r-1

1

Ju

l-1

1

Oc

t-1

1

Ja

n-1

2

Ap

r-1

2

Jul-1

2

Oc

t-1

2

Jan-1

3

Ap

r-1

3

Jul-1

3

Oc

t-1

3

Jan-1

4

Ap

r-1

4

Jul-1

4

Oc

t-1

4

Ja

n-1

5

Ap

r-1

5

Jul-1

5

Oc

t-1

5

Jan-1

6

Ap

r-1

6

Yield spread (RHS)

5y corporate bond (AA)

5y policy bank bond yield

% bp

1.8

2.8

3.8

4.8

5.8

6.8

7.8

Apr-

12

Jul-12

Oct-

12

Ja

n-1

3

Apr-

13

Jul-13

Oct-

13

Jan

-14

Apr-

14

Ju

l-14

Oct-

14

Jan

-15

Apr-

15

Jul-15

Oct-

15

Jan

-16

Apr-

16

1y AA corporate bond

1y LGFV bond

1y Railway bond

%

1.4

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

2.5

2.7

2.9

3.1

3.3

3.5

3.7

3.9

4.1

4.3

4.5

4.7

Oc

t/12

Dec

/12

Feb/1

3

Apr/

13

Jun/1

3

Aug/1

3

Oc

t/13

Dec

/13

Fe

b/1

4

Apr/

14

Jun/1

4

Aug/1

4

Oc

t/14

De

c/1

4

Feb/1

5

Apr/

15

Ju

n/1

5

Au

g/1

5

Oc

t/1

5

Dec

/15

Feb/1

6

Apr/

16

China 10y treasury yield

US 10y treasury yield (RHS)

% %

Macquarie Wealth Management Macro Monday

2 May 2016 9

Exchange rate

Fig 43 RMB weakened slightly last week Fig 44 CNY vs CNH

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 45 The dollar index Fig 46 CFETS RMB index

Source: Bloomberg, Macquarie Research, May 2016 *Staff estimate using the currency basket published by CFETS. Source: Wind, Macquarie Research, May 2016

Fig 47 Major currencies against USD Fig 48 FX reserves increased in March

Source: Bloomberg, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

5.95

6.05

6.15

6.25

6.35

6.45

6.55

6.65

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oc

t-1

4

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oc

t-1

5

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Fixing Spot

USD/CNY

6.49

6.59

6.0

6.1

6.2

6.3

6.4

6.5

6.6

6.7

De

c-1

3

Fe

b-1

4

Ap

r-1

4

Ju

n-1

4

Au

g-1

4

Oc

t-1

4

De

c-1

4

Fe

b-1

5

Ap

r-1

5

Ju

n-1

5

Au

g-1

5

Oc

t-1

5

De

c-1

5

Fe

b-1

6

Ap

r-1

6

Onshore CNY

Offshore CNH

USD/CNY

75

80

85

90

95

100

105

Ju

n-1

4

Ju

l-14

Au

g-1

4

Se

p-1

4

Oct-

14

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Apr-

15

Ma

y-1

5

Ju

n-1

5

Ju

l-15

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Apr-

16

DXY Index

93.1

88

90

92

94

96

98

100

102

104

106

Jun

-14

Jul-

14

Au

g-1

4

Se

p-1

4

Oct-

14

Nov-1

4

Dec-1

4

Jan

-15

Feb-1

5

Mar-

15

Apr-

15

May-1

5

Jun

-15

Jul-

15

Au

g-1

5

Se

p-1

5

Oct-

15

Nov-1

5

Dec-1

5

Jan

-16

Feb-1

6

Mar-

16

Apr-

16

CFETS RMB index*

Dec 14 = 100

97.3

70

75

80

85

90

95

100

105

Ju

l-1

4

Au

g-1

4

Se

p-1

4

Oc

t-1

4

No

v-1

4

De

c-1

4

Ja

n-1

5

Fe

b-1

5

Ma

r-1

5

Ap

r-1

5

Ma

y-1

5

Ju

n-1

5

Ju

l-1

5

Au

g-1

5

Se

p-1

5

Oc

t-1

5

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-1

6

Ap

r-1

6

RMB EURO JPY JPMorgan EM Currency index

1 Jul 2014 = 100 Currency value against USD

Appreciation

-71

18

-37

-17

-43

-94

-43

11

-87

-108 -99

-29

10

-120

-90

-60

-30

0

30

Ma

r-15

Ap

r-15

Ma

y-1

5

Ju

n-1

5

Ju

l-15

Au

g-1

5

Se

p-1

5

Oct-

15

No

v-1

5

De

c-1

5

Ja

n-1

6

Fe

b-1

6

Ma

r-16

Change in FX reserves

US$ bn

Macquarie Wealth Management Macro Monday

2 May 2016 10

Industrial indicators

Fig 49 Industrial earnings surged 11% in March Fig 50 Excavator sales rebounded in March

Source: CEIC, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 51 Railway freight fell 6% in March Fig 52 Container throughput rebounded 5.1% in March

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

Fig 53 Power consumption jumped 5.6% in March Fig 54 Auto sales grew 10% in March

Source: Wind, Macquarie Research, May 2016 Source: Wind, Macquarie Research, May 2016

-10

-5

0

5

10

15

20

25

30

35

Sep

-11

Dec

-11

Mar-

12

Jun-1

2

Sep

-12

Dec

-12

Mar-

13

Jun-1

3

Sep

-13

Dec

-13

Mar-

14

Jun-1

4

Sep

-14

Dec

-14

Mar-

15

Jun-1

5

Sep

-15

Dec

-15

Mar-

16

Industrial profits

%, yoy

11.1%

-50

-30

-10

10

30

50

70

90

110

130

150

Mar-

09

Sep-0

9

Ma

r-1

0

Sep-1

0

Mar-

11

Sep-1

1

Ma

r-1

2

Sep-1

2

Mar-

13

Sep-1

3

Mar-

14

Se

p-1

4

Mar-

15

Sep-1

5

Mar-

16

Excavator sales

% yoy

19%

-20

-15

-10

-5

0

5

10

15

20

25

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Ma

r-1

1

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Ma

r-1

6

Railway freight

% yoy

-6%

-20

-10

0

10

20

30

40

Mar-

09

Oc

t-0

9

May-1

0

Dec-1

0

Jul-1

1

Feb

-12

Sep

-12

Ap

r-1

3

Nov

-13

Jun-1

4

Jan-1

5

Aug

-15

Mar-

16

Container throughput

% yoy

5.1%

-10

-5

0

5

10

15

20

25

30

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Power consumption

% yoy

5.6%

-20

0

20

40

60

80

100

Mar-

09

Sep

-09

Mar-

10

Sep

-10

Mar-

11

Sep

-11

Mar-

12

Sep

-12

Mar-

13

Sep

-13

Mar-

14

Sep

-14

Mar-

15

Sep

-15

Mar-

16

Passenger vehicle sales

% yoy

10%

Macquarie Wealth Management Macro Monday

2 May 2016 11

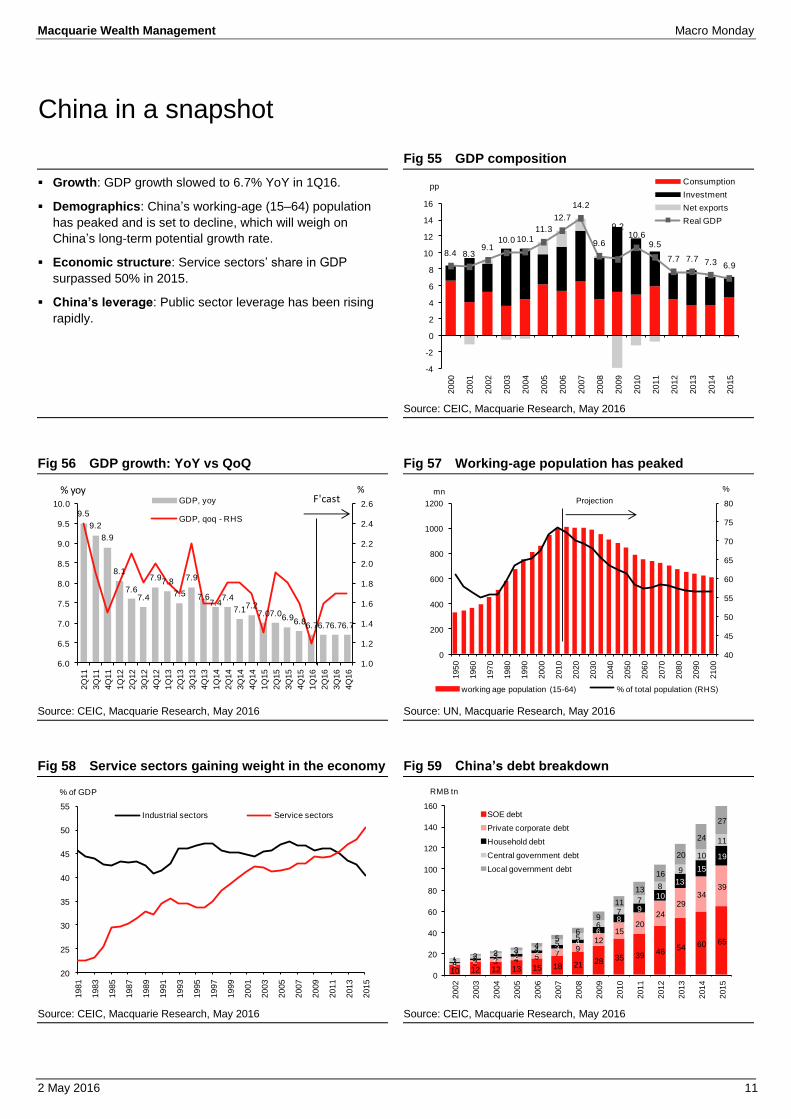

China in a snapshot

Fig 55 GDP composition

Growth: GDP growth slowed to 6.7% YoY in 1Q16.

Demographics: China’s working-age (15–64) population

has peaked and is set to decline, which will weigh on

China’s long-term potential growth rate.

Economic structure: Service sectors’ share in GDP

surpassed 50% in 2015.

China’s leverage: Public sector leverage has been rising

rapidly.

Source: CEIC, Macquarie Research, May 2016

Fig 56 GDP growth: YoY vs QoQ Fig 57 Working-age population has peaked

Source: CEIC, Macquarie Research, May 2016 Source: UN, Macquarie Research, May 2016

Fig 58 Service sectors gaining weight in the economy Fig 59 China’s debt breakdown

Source: CEIC, Macquarie Research, May 2016 Source: CEIC, Macquarie Research, May 2016

8.4 8.39.1

10.0 10.111.3

12.7

14.2

9.6

9.210.6

9.5

7.7 7.7 7.3 6.9

-4

-2

0

2

4

6

8

10

12

14

16

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Consumption

Investment

Net exports

Real GDP

pp

9.5

9.2

8.9

8.1

7.67.4

7.97.8

7.5

7.9

7.67.4

7.4

7.17.2

7.07.06.9

6.86.76.76.76.7

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2.6

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

10.0

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

3Q

12

4Q

12

1Q

13

2Q

13

3Q

13

4Q

13

1Q

14

2Q

14

3Q

14

4Q

14

1Q

15

2Q

15

3Q

15

4Q

15

1Q

16

2Q

16

3Q

16

4Q

16

GDP, yoy

GDP, qoq - RHS

% yoy %F'cast

40

45

50

55

60

65

70

75

80

0

200

400

600

800

1000

1200

1950

1960

1970

1980

1990

2000

2010

2020

2030

2040

2050

2060

2070

2080

2090

2100

working age population (15-64) % of total population (RHS)

mn %

Projection

20

25

30

35

40

45

50

55

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

Industrial sectors Service sectors

% of GDP

10 12 12 13 15 18 21 28 35 3946

54 60 65

2 2 3 4 5 79

1215

20

24

2934

39

1 2 2 2 23

4

6

8

9

10

13

15

19

2 3 3 34

55

6

7

7

8

9

10

11

1 2 2 34

56

9

11

13

16

20

24

27

0

20

40

60

80

100

120

140

160

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

SOE debt

Private corporate debt

Household debt

Central government debt

Local government debt

RMB tn

Macquarie Wealth Management Macro Monday

2 May 2016 12

Fig 60 China economic forecasts

Macquarie China Economic forecasts

Unit 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 2014 2015 2016 2017

Growth

GDP YoY, % 7.0 7.0 6.9 6.8 6.7 6.7 6.7 6.7 7.3 6.9 6.7 6.5

GDP QoQ,% 1.3 1.9 1.8 1.6 1.1 1.6 1.7 1.7 -- -- -- --

Inflation

CPI YoY, % 1.2 1.4 1.7 1.5 2.1 2.4 2.0 2.0 2.0 1.4 2.2 2.0

PPI YoY, % -4.6 -4.7 -5.7 -5.9 -4.8 -3.5 -3.0 -2.1 -1.9 -5.2 -3.5 -1.5

Activities

Industrial production YoY, % 6.4 6.3 5.9 5.9 5.9 -- -- -- 8.3 6.1 5.7 5.0

Retail sales YoY, % 10.5 10.2 10.7 11.1 10.3 -- -- -- 12.0 10.7 10.0 9.5

Fixed asset investment (ytd) YoY, % 13.5 10.4 8.7 9.3 10.7 -- -- -- 15.7 10.0 8.0 7.5

Manufacturing YoY, % 10.4 9.4 6.2 7.6 6.4 -- -- -- 13.5 8.1 6.0 6.0

Property YoY, % 9.0 3.9 0.8 -0.9 6.2 -- -- -- 11.1 2.5 4.0 4.0

Infrastructure YoY, % 22.8 17.6 16.6 15.6 19.2 -- -- -- 20.3 17.3 15.0 12.0

Trade

Exports YoY, % 4.6 -2.2 -5.9 -5.1 -9.3 -- -- -- 6.0 -2.6 1.0 3.2

Imports YoY, % -17.8 -13.6 -14.4 -11.9 -13.3 -- -- -- 0.7 -14.4 -2.0 2.1

Trade balance US$ bn 124 140 164 175 126 -- -- -- 380 602 650 690

Monetary

M2 (period-end) YoY, % 11.6 11.8 13.1 13.3 13.4 -- -- -- 12.2 13.3 13.0 12.0

New bank loans Rmb bn 3,670 2,880 3,340 1,820 4,607 -- -- -- 9,781 11,710 13,000 13,500

1-yr deposit rate (period-end) % 2.50 2.00 1.75 1.50 1.50 1.25 1.00 1.00 2.75 1.50 1.00 1.00

1-yr lending rate (period-end) % 5.35 4.85 4.60 4.35 4.35 4.10 3.85 3.85 5.60 4.35 3.85 3.85

RRR (period-end) % 19.5 18.5 18.0 17.5 17.0 16.5 16.0 15.5 20.0 17.5 15.5 13.0

Exchange rate (spot, period end) USDCNY

6.24 6.21 6.36 6.49 6.47 -- -- -- 6.20 6.49 6.60 6.50

Current account/Fiscal balance

Current account (as % of GDP) % -- -- -- -- -- -- -- -- 2.1 3.0 2.8 2.6

Fiscal balance (as % of GDP) % -- -- -- -- -- -- -- -- -2.1 -2.4 -3.0 -3.0

Note: Numbers in bold are forecast values.

Source: CEIC, Macquarie Research, May 2016

Macquarie Wealth Management Macro Monday

2 May 2016 13

Macquarie China Macro Products 1. Regular data comments:

Monthly data preview: April data preview: Fighting with deflation, 29 Apr 2016

IP/FAI/Property: 1Q16 data: A sweet spot for now, 15 Apr 2016

Money/Credit: Strong credit, weak exports, stable RMB, 16 Feb 2016

Trade data: Eight takeaways from Nov trade and FX reserve data, 8 Dec 2015

Inflation: August inflation: CPI inflation at 12-month high and PPI deflation at 71-month low, 10 Sep 2015

NBS PMI: What PMI data can and cannot tell us, 1 Sep 2015

2. Ad hoc comments:

Dissecting China’s capital outflows in 2015, 28 Apr 2016

Thoughts on earnings cycle: A new start?, 27 Apr 2016

Debt/equity swap: What can we learn from the past?, 8 Apr 2016

What are the channels of China’s capital outflows?, 24 Mar 2016

The implication of FOMC on RMB, 17 Mar 2016

An unexpected RRR cut for easing liquidity conditions and boosting growth, 29 Feb 2016

RMB: The inescapable dilemma, 5 Feb 2016

China in 2015: Huge divergence, 29 Jan 2016

What’s behind the sharp drop in FX reserves and the recent RMB depreciation? 7 Jan 2016

Update on capital flows: Huge outflows in 3Q15, but reversed in Oct, 19 Nov 2015

Takeaways from the 13th 5-year Plan, 4 Nov 2015

The PBoC cuts interest rate, RRR and liberalized deposit rate all at once, 23 Oct 2015

US marketing feedback: 9 Q&A on China, 8 Oct 2015

Myths and Realities: 7 Q&As on RMB, 11 Sep 2015

Aug FX reserves number indicates capital outflows are manageable, 7 Sep 2015

The PBoC cut interest rate and RRR for financial and economic stability, 25 Aug 2015

3. Thematic Research

China 2016 Outlook, 14 Dec 2015

(Annual outlook for 2016)

China Liquidity Series (II) - Why China needs to cut RRR 20 times in the next five years?, 16 Mar 2015

(A primer on China’s monetary policy transition)

China Liquidity Series (I) - A guide to RMB and the PBoC, 17 Jul 2014

(A primer on how to understand RMB, liquidity and monetary policy in China)

A U-shaped recovery: Outlook for the remainder of this year, 7 Aug 2015

(Taking stock of economic development in 1H15 and update macro outlook for 2H15)

Mini-cycle, China style: Lessons from the near past, 28 May 2014

(A study on the stop-go mini-cycle, the most important macro pattern in China and a major market mover)

Understanding “stimulus,” 16 Apr 2014

(An early attempt in quantifying mini-stimulus measures)

4. Macro Monday

Property and commodities outperform stocks and bonds, 25 Apr 2016

The consensus for 2016 GDP set to be revised up, 18 Apr 2016

Debating debt/equity swap, 11 Apr 2016

A macro sweet spot, 4 Apr 2016

Macquarie Wealth Management Macro Monday

2 May 2016 14

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperform – return >3% in excess of benchmark return Neutral – return within 3% of benchmark return Underperform – return >3% below benchmark return Benchmark return is determined by long term nominal GDP growth plus 12 month forward market dividend yield

Macquarie – Asia/Europe Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie – South Africa Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie - Canada

Outperform – return >5% in excess of benchmark return Neutral – return within 5% of benchmark return Underperform – return >5% below benchmark return

Macquarie - USA Outperform (Buy) – return >5% in excess of Russell 3000 index return Neutral (Hold) – return within 5% of Russell 3000 index return Underperform (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated from the volatility of historical price movements. Very high–highest risk – Stock should be

expected to move up or down 60–100% in a year – investors should be aware this stock is highly speculative. High – stock should be expected to move up or down at least 40–60% in a year – investors should be aware this stock could be speculative. Medium – stock should be expected to move up or down at least 30–40% in a year. Low–medium – stock should be expected to move up or down at least 25–30% in a year. Low – stock should be expected to move up or down at least 15–25% in a year. * Applicable to Asia/Australian/NZ/Canada stocks only

Recommendations – 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions – For quarter ending 31 March 2016

AU/NZ Asia RSA USA CA EUR Outperform 50.34% 59.09% 46.67% 44.76% 60.66% 46.12% (for global coverage by Macquarie, 3.72% of stocks followed are investment banking clients)

Neutral 34.14% 25.66% 32.00% 49.90% 30.33% 35.10% (for global coverage by Macquarie, 4.79% of stocks followed are investment banking clients)

Underperform 15.52% 15.26% 21.33% 5.33% 9.02% 18.78% (for global coverage by Macquarie, 2.31% of stocks followed are investment banking clients)

Company-specific disclosures: Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures.

Analyst certification: We hereby certify that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. The Analysts responsible for preparing this report receive compensation from Macquarie that is based upon various factors including Macquarie Group Limited (MGL) total revenues, a portion of which are generated by Macquarie Group’s Investment Banking activities. General disclosure: This research has been issued by Macquarie Securities (Australia) Limited ABN 58 002 832 126, AFSL 238947, a Participant of the ASX and Chi-X Australia Pty Limited. This research is distributed in Australia by Macquarie Wealth Management, a division of Macquarie Equities Limited ABN 41 002 574 923 AFSL 237504 ("MEL"), a Participant of the ASX, and in New Zealand by Macquarie Equities New Zealand Limited (“MENZ”) an NZX Firm. Macquarie Private Wealth’s services in New Zealand are provided by MENZ. Macquarie Bank Limited (ABN 46 008 583 542, AFSL No. 237502) (“MBL”) is a company incorporated in Australia and authorised under the Banking Act 1959 (Australia) to conduct banking business in Australia. None of MBL, MGL or MENZ is registered as a bank in New Zealand by the Reserve Bank of New Zealand under the Reserve Bank of New Zealand Act 1989. Apart from Macquarie Bank Limited ABN 46 008 583 542 (MBL), any MGL subsidiary noted in this research, , is not an authorised deposit-taking institution for the purposes of the Banking Act 1959 (Australia) and that subsidiary’s obligations do not represent deposits or other liabilities of MBL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of that subsidiary, unless noted otherwise. This research contains general advice and does not take account of your objectives, financial situation or needs. Before acting on this general advice, you should consider the appropriateness of the advice having regard to your situation. We recommend you obtain financial, legal and taxation advice before making any financial investment decision. This research has been prepared for the use of the clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient, you must not use or disclose this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. This research is based on information obtained from sources believed to be reliable, but the Macquarie Group does not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. The Macquarie Group accepts no liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. The Macquarie Group produces a variety of research products, recommendations contained in one type of research product may differ from recommendations contained in other types of research. The Macquarie Group has established and implemented a conflicts policy at group level, which may be revised and updated from time to time, pursuant to regulatory requirements; which sets out how we must seek to identify and manage all material conflicts of interest. The Macquarie Group, its officers and employees may have conflicting roles in the financial products referred to in this research and, as such, may effect transactions which are not consistent with the recommendations (if any) in this research. The Macquarie Group may receive fees, brokerage or commissions for acting in those capacities and the reader should assume that this is the case. The Macquarie Group‘s employees or officers may provide oral or written opinions to its clients which are contrary to the opinions expressed in this research. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures © Macquarie Group