Embed Size (px)

Citation preview

Aligning Financial Capability Efforts to the Common Core Standards

October 14, 2014

Panelists:

Lisa S. KruegerAdjunct Professor, College of Business Administration

Rider University

Pat PageRhode Island Teacher of the Year

Rhode Island Department of Elementary and Secondary Education

Anne DeMallieMathematics Statewide Program Coordinator,

Massachusetts Department of Elementary and Secondary Education

Moderator:

Albert Barnor

Sr. Community Affairs Analyst, Boston Fed

www.bostonfed.org

Financial Literacy Education

& the Common Core

State Standards (CCSS)

in Mathematics

Boston Federal Reserve Bank

October 14, 2014

Lisa S. Krueger

Common Core State Standards

(CCSS)• Developed by the National Governors Association and the Council of

Chief State School Officers, NOT the federal government

• A set of rigorous academic standards in mathematics and English language arts/literacy (ELA) that outline learning goals for what a student should know and be able to do at the end of each grade.

• Voluntarily adopted by 45 states and the District of Columbia.

• The CCSS are a “Disruptive policy change” - an opportunity to spur innovation and increase willingness/need to expend resources in order to align with these standards.

• Implementation of the CCSS, including assessments (e.g., Smarter Balance and PARCC), instructional materials, professional development and information technology (IT) spending, is expected to cost as much as $15 billion dollars over the next 5 years.*

*Source: http://pioneerinstitute.org/download/national-cost-of-aligning-states-and-localities-to-the-common-core-standards/

Importance of Financial

LiteracyAmericans' ability to build a secure future for themselves

and their families requires the navigation of an

increasingly complex financial system. As we recover

from the worst economic crisis in generations, it is more

important than ever to be knowledgeable about the

consequences of our financial decisions. … We recommit

to improving financial literacy and ensuring all Americans

have access to trustworthy financial services and

products.

President Barack Obama Presidential Proclamation – National

Financial Literacy Month, March 31, 2011

Importance of Financial

LiteracyRecent economic challenges have highlighted the

importance of teaching our kids to understand personal

finance. The day-to-day relevance of economic concepts

and financial responsibility will only continue to increase

as the world is rapidly transformed by science and

technology. Providing students with the practical tools

they need to apply that knowledge will help them succeed

financially by creating businesses, driving innovation, and

achieving personal dreams. Working together, we can

infuse our classrooms with the necessary foundational

capabilities and make financial education a centerpiece of

our public and private agenda.

Richard D. Fairbank, Founder and CEO of Capital One.

Importance of Financial

LiteracyFinancial literacy is strongly correlated with use of

financial services, savings and retirement planning.

A compelling body of survey evidence from developed

countries shows that households with low levels of

financial literacy tend not to plan for retirement, borrow at

higher interest rates, acquire fewer assets and participate

less in the formal financial system relative to their more

financially-literate counterparts.

Source: World Bank, May 2009.

The State of

Economic/Financial Literacy

Education For the first time all 50 states

and DC include economics in the K-12 standards.

24 states require that a high school course in economics be offered.

22 states require that students take a course in economics.

62% of students on free & reduced lunch are taking an economics course (58% of students overall).

Source: Survey of the States, 2014, CEE.

The State of

Economic/Financial Literacy

Education• 43 states include personal

finance concepts in their standards.

• 35 states require that these standards are implemented.

• 19 states require that a high school course be offered.

• 17 states require that students take a course in personal finance in order to graduate.

• Only 6 states require testing of personal finance concepts.

Source: Survey of the States, 2014, CEE.

What is Financial Literacy?The OECD INFE (International Network on Financial Education) has defined financial literacy as follows:‘A combination of awareness, knowledge, skill, attitude and behaviour necessary to make sound financial decisions and ultimately achieve individual financial wellbeing.’

FLEC (The Financial Literacy Education Commission) of the US Treasury defines financial literacy as the ability to use knowledge and skills to manage financial resources effectively for a lifetime of financial well-being and defines financial education as the process by which people improve their understanding of financial products, services and concepts, so they are empowered to make informed choices, avoid pitfalls, know where to go for help and take other actions to improve their present and long-term financial well-being.

What is Financial Literacy?The good news is that there is general agreement on

what should be taught!

①Treasury Core Competencies

② JumpStart Coalition Standards

③CEE National Standards

④PISA Framework

⑤NEFE HSFPP

What is Financial Literacy?Treasury Core Competencies

Source: Federal Register / Vol. 75, No. 165 / Thursday, August 26, 2010 / Notices

What is Financial Literacy?Jumpstart Standards

What is Financial Literacy?CEE (Council for Economic Education)

National Standards for Financial Literacy

Earning Income

Buying Goods and Services

Using Credit

Saving

Financial Investing

Protecting and Insuring

What is Financial Literacy?PISA (Programme for International Student Assessment)

2012 Financial Literacy Framework

money and transactions

planning and managing finances

risk and reward

financial landscape

What is Financial Literacy?NEFE (National Endowment for Financial Education)

Source: www.HSFPP.org

What is Financial Literacy?

2007 2012 2014

www.moneyasyoulearn.org

Financial Literacy – Big Ideas

Financial Literacy – Big Ideas

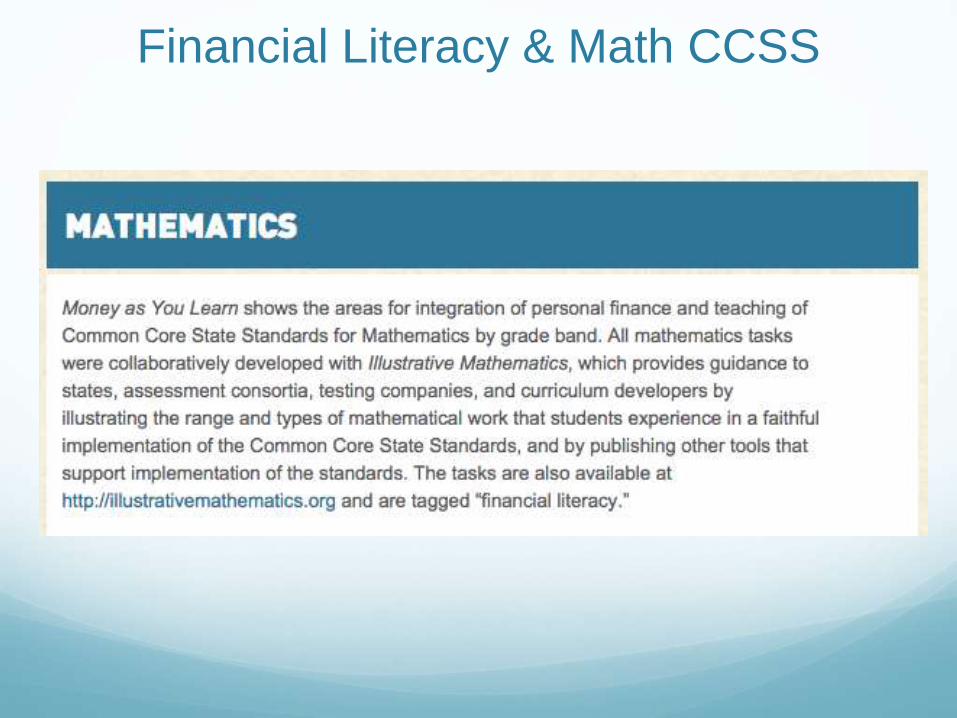

Financial Literacy & Math CCSSFinancial Literacy is an effective, rich and relevant context

to teach and assess the math common core.

Source:

http://www.moneyasyoulearn.org/ideas/

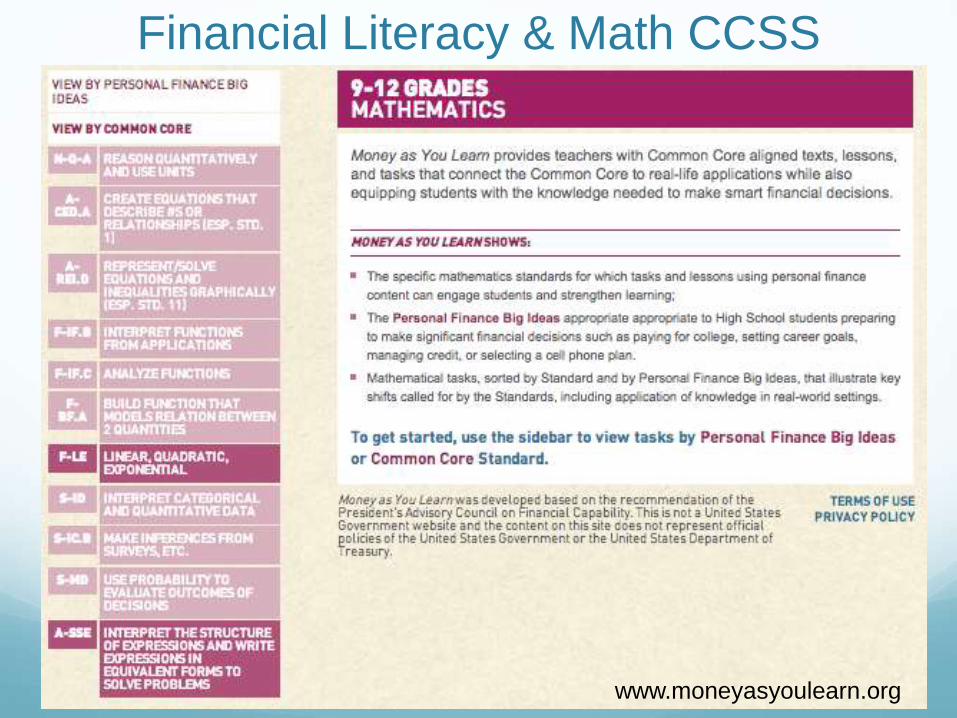

Financial Literacy & Math CCSS

Financial Literacy & Math CCSS

by Standard

www.moneyasyoulearn.org

Financial Literacy & Math CCSS

by Personal Finance Big Idea

www.moneyasyoulearn.org

Financial Literacy & Math CCSS

www.moneyasyoulearn.org

Financial Literacy & Math CCSS

www.moneyasyoulearn.org

Financial Literacy & Math CCSS

www.moneyasyoulearn.org

Financial Literacy & Math CCSS

www.moneyasyoulearn.org

Financial Literacy – Companion Site

www.moneyasyougrow.org

Financial Literacy Assessment

Role of assessment

Recall that only 6 states require testing of personal finance concepts, even though 43 states include personal finance concepts in their standards, 35 states require that these standards are implemented, 19 states require that a high school course be offered and 17 states require that students take a course in personal finance in order to graduate.

Florida is the first state to formally adopt a comprehensive set of financial literacy standards (CEE).

Financial Literacy AssessmentRole of assessment

Financial Literacy education will only work if districts and

schools are accountable.

Standardized assessments set clear expectations for

students and teachers and also for content developers.

Results can provide a baseline on which to measure

progress, can inform future instruction and curriculum

development, and can help target and tailor resources to

the most at risk and vulnerable students.

Do we need a comprehensive national assessment in

financial literacy?

R E S O U R C E S T O S U P P O R T

BUILDING FINANCIAL CAPABILITY IN TODAY’S YOUTH

Pat Page, MBA, MAT

Business and Computer Technology Educator

2014 RI Teacher of the Year

Board member, RI Jump$tart Coalition

Disclaimer: The professional perspective I present is my own. It may not reflect the policy or programmatic position of the East Greenwich Public Schools or the RI Department of Education and related entities.

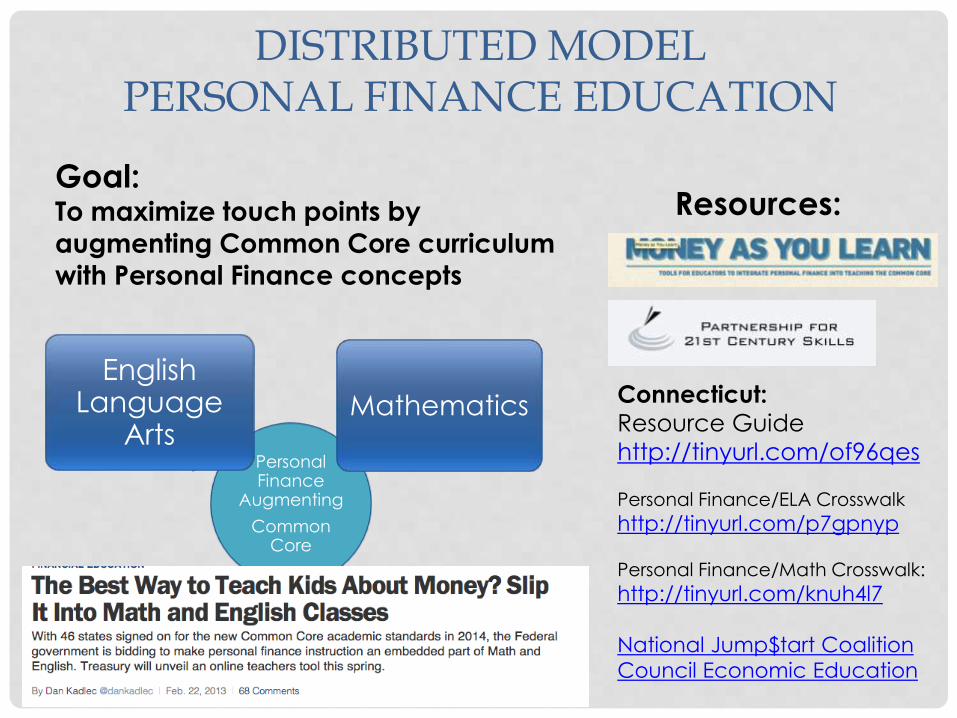

DISTRIBUTED MODEL PERSONAL FINANCE EDUCATION

Personal Finance

Augmenting

Common Core

English Language

ArtsMathematics

Goal: To maximize touch points by

augmenting Common Core curriculum

with Personal Finance concepts

Resources:

Connecticut:

Resource Guide

http://tinyurl.com/of96qes

Personal Finance/ELA Crosswalk

http://tinyurl.com/p7gpnyp

Personal Finance/Math Crosswalk:

http://tinyurl.com/knuh4l7

National Jump$tart Coalition

Council Economic Education

CONTEXTUAL MODEL PERSONAL FINANCE EDUCATION

Personal Finance

Supporting Common Core

Mathematics English Language Arts

Goal: To provide direct instruction

and relevant contextual application

within a Personal Finance Class in

support of CCSS.

Resources:

National Jump$tart Coalition

Council Economic Education

A MUST READ

Way-Holden

Study:

https://www.fdic.

gov/about/come

in/Mar3.pdf

An Organic and Integrated Approach to Building Financial Capability

POINTS TO PONDER…AND PAT’S PERSPECTIVE

Is the distinction between Financial Literacy versus Financial Capability more than semantics?

How do we address the teacher capability / confidence gap that has a direct correlation to student financial literacy and capability levels?

Should states consider a competency/credentialing model to identify teachers who are “qualified” and passionate about Personal Finance?

Financial Education inOur Schools

Financial Literacy Pilot Program

Anne DeMallieMathematics Statewide Program CoordinatorSTEM - Curriculum and Instruction

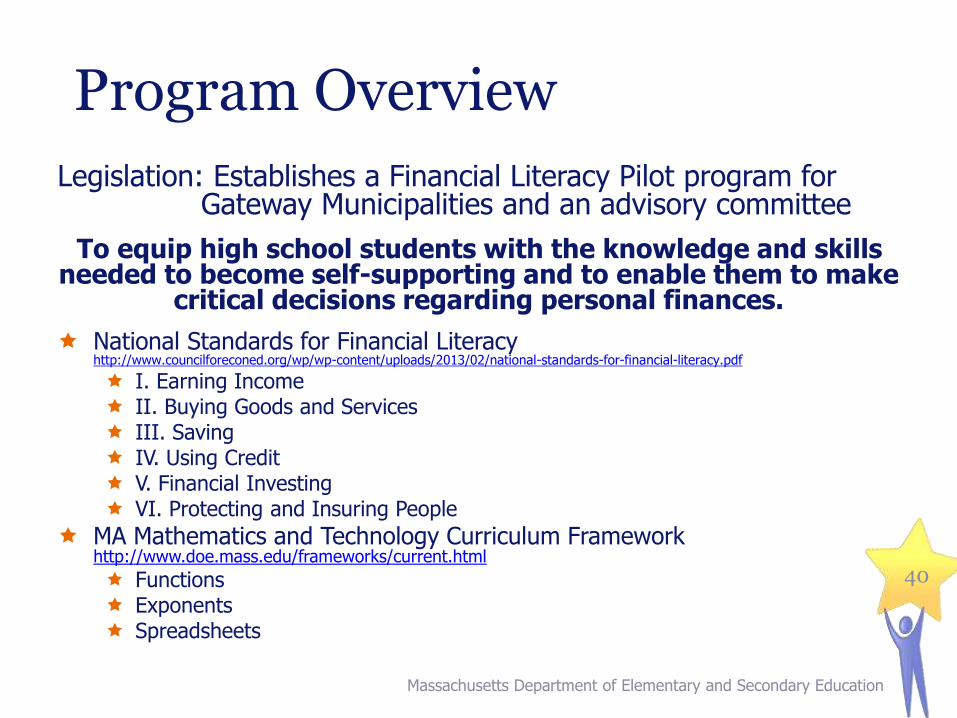

Program Overview

Legislation: Establishes a Financial Literacy Pilot program for Gateway Municipalities and an advisory committee

To equip high school students with the knowledge and skills needed to become self-supporting and to enable them to make

critical decisions regarding personal finances.

National Standards for Financial Literacyhttp://www.councilforeconed.org/wp/wp-content/uploads/2013/02/national-standards-for-financial-literacy.pdf

I. Earning Income II. Buying Goods and Services III. Saving IV. Using Credit V. Financial Investing VI. Protecting and Insuring People

MA Mathematics and Technology Curriculum Frameworkhttp://www.doe.mass.edu/frameworks/current.html

Functions Exponents Spreadsheets

Massachusetts Department of Elementary and Secondary Education

40

Timeline

Award – June 30, 2013 Planning Period

July 2013 - June 2014 1st Year of Implementation

July 2014 – June 2015 2nd Year of Implementation

July 2015 – June 2016* 3rd Year of Implementation

Massachusetts Department of Elementary and Secondary Education

41*Pending appropriation of funding

Grantees

Competitive grants awarded to 10 districts (11 high schools) partnered with banks, credit unions, community organizations, and/or higher education institute.

FY2014 Data

Massachusetts Department of Elementary and Secondary Education

42

Gateway Districts

High School(s)

Number of Teachers

Delivering Curriculum

Number of Students Engaged

Fall River BMC Durfee High School 30 560

Haverhill Haverhill, High School 3 570

Holyoke Dean Technical High School 3 74

Lowell Lowell High School 10 261

Lynn Lynn High School 5 608

Quincy North Quincy High School Quincy High School

34

7448

Revere Revere High School 10 92

Salem Salem High School 2 109

Springfield Putnam Vocational High School 4 546

Worcester Worcester Technical High School 7 50

District Strategy

All Students All Freshman Special Populations Community Outreach Stand alone course Add to Math courses Add to the multiple disciplines Add to Business Major (Voc) Add to Advisory Blocks Credit/Money Strong for Life Fair Family Financial Literacy Day 2014 National Economics Challenge

Massachusetts Department of Elementary and Secondary Education

43

Curriculum Resources

Academic Innovations

National Endowment for Financial Education (NEFE)

Junior Achievement

Valmo Village

Boston Federal Reserve Bank

Network for Teaching Entrepreneurship

National Financial Educators Council

Massachusetts Department of Elementary and Secondary Education

44

Evaluation

University of Massachusetts Donahue Institute (UMDI)

Student content knowledge?

Student behavioral changes?

Educator impact?

School/District impact?

http://www.doe.mass.edu/STEM/grants.html

Massachusetts Department of Elementary and Secondary Education

45

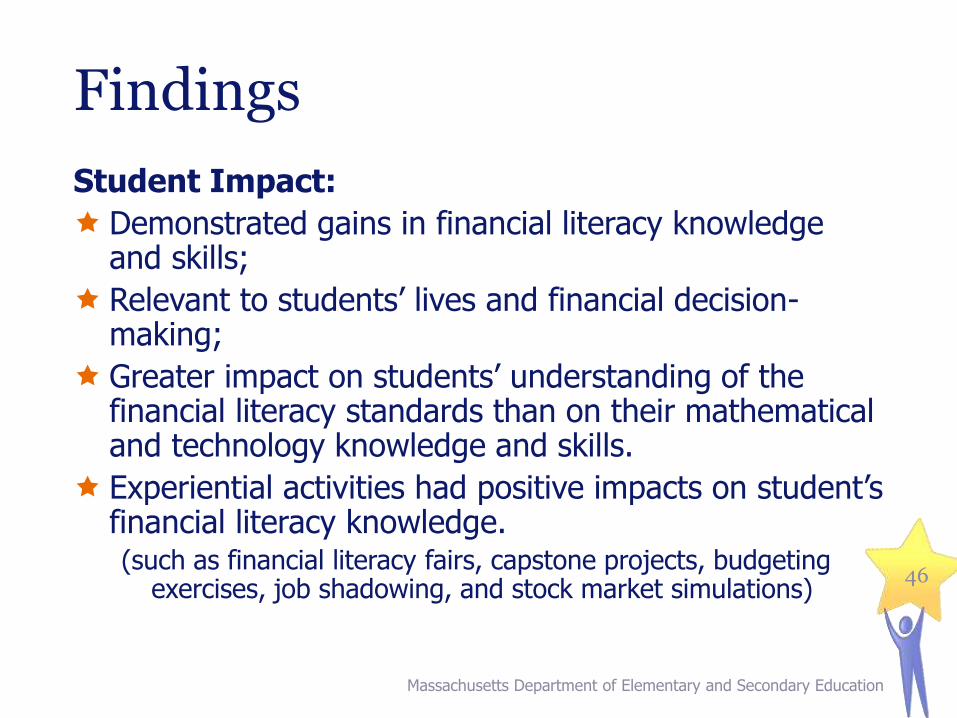

Findings

Massachusetts Department of Elementary and Secondary Education

46

Student Impact:

Demonstrated gains in financial literacy knowledge and skills;

Relevant to students’ lives and financial decision-making;

Greater impact on students’ understanding of the financial literacy standards than on their mathematical and technology knowledge and skills.

Experiential activities had positive impacts on student’s financial literacy knowledge. (such as financial literacy fairs, capstone projects, budgeting

exercises, job shadowing, and stock market simulations)

Findings

Massachusetts Department of Elementary and Secondary Education

47

Program Models

The sites created program models that contained a diversity of curricula and activities.

Sites commonly implemented their program through existing courses.

Several schools provided stand-alone events.

Several project leaders reported that experiential activities were the most effective way to engage students.

Findings

Massachusetts Department of Elementary and Secondary Education

48

Program Implementation

Factors that supported/facilitated the implementation: the establishment of courses dedicated to financial literacy,

the provision of collaboration and sharing opportunities,

the use of adaptable curriculum,

teacher and administrator enthusiasm, and

the use of technology.

Challenges commonly encountered included: finding curricula and approaches that engaged 9th and 10th

grade students,

the need for more financial literacy courses and interventions,

struggles to integrate new or unfamiliar content, and

software compatibility or other technology-related problems.

FY2015 Scale-up

Strategic considerations Students may be served best by exposure to financial literacy concepts

throughout the four years of high school. Financial literacy curriculum should be targeted to the interests and

capacities of different age groups. Increased family outreach may benefit student and family financial

decision-making.

Massachusetts Department of Elementary and Secondary Education

49

Gateway

Districts High School(s) FY14 FY15 FY16

Fall River BMC Durfee High School 560

Haverhill Haverhill, High School 570 610 675

Holyoke Dean Technical High School 74 175 225

Lowell Lowell High School 261 446 1080

Lynn Lynn High School 608 750 810

Quincy North Quincy High School

Quincy High School 122 137 137

Revere Revere High School 92 131 200

Salem Salem High School 109 130 250

Springfield Putnam Vocational High School 546 525 650

Worcester Worcester Technical High School 50 158 171

Next

Massachusetts Department of Elementary and Secondary Education

50

The FY14 Financial Literacy Pilot Program Legislative Report.

Year 2 of Implementation and evaluation is under way.

Our Goal:

To equip high school students with the knowledge and skills needed to become self-

supporting and to enable them to make critical decisions regarding personal finances.

Financial Education inOur Schools

Financial Literacy Pilot Program

Anne DeMallieMathematics Statewide Program CoordinatorSTEM - Curriculum and Instruction