Embed Size (px)

Citation preview

Submitted to Management Sciencemanuscript ()

Competing on Toxicity: The Impact of Supplier Pricesand Regulation on Manufacturers’ Substance

Replacement Strategies(Authors’ names blinded for peer review)

The recent proliferation of media reports on substances of concern has increased consumer fears, sparked scientific

debate, and highlighted the need for stronger chemical regulations. When a substance of concern is identified

(e.g., bisphenol-A (BPA) in reusable water bottles), it presents manufacturers with difficult decisions of whether

to proactively replace the substance in their products or to defer replacement and wait to see if regulation occurs.

In this paper, we examine how competition influences manufacturers’ decisions when a substance of concern is

identified within their products. We find that when manufacturers compete on toxicity, if they face a cost tradeoff

between the substance’s expected regulatory risk and the supplier price for the replacement substance, then a

high-end manufacturer can use his brand advantage to control the market. The competition between manufactur-

ers is highest when instead, the supplier charges an intermediate price for the replacement substance. To identify

ways to increase the number of manufacturers adopting a replacement, we examine whether manufacturers can

avoid competing and instead, share the cost to replace. Our results demonstrate that opportunities may exist

for manufacturers to collaborate to replace a substance, even when the shared cost to replace is greater than the

sum of their individual replacement costs.

Key words : Competition, collaboration, environmental regulations, substances of concern, game theory

1. Introduction

In recent years, the potentially-harmful chemicals contained in widely-used consumer products have

become regular topics in the mainstream media. For example, reports have been published on the poten-

tial hazards of triclosan in toothpastes (Kary 2014), bisphenol-A (BPA) in water bottles (Kuchment

2008), brominated flame retardants (BFRs) in electronics and furniture (Callahan and Roe 2012), and

phthalates in fashion goods (Pous 2012). While these substances of concern have generated consumer

fears and scientific debate, due to a lack of regulation (Fahmy 2010, Rizzuto 2013) they can still be

found in everyday consumer products. As a result, manufacturers face difficult tradeoffs when deciding

whether to replace these substances. On the one hand, replacing a substance can be very costly and it

may be unnecessary in an uncertain regulatory environment. On the other hand, due to competitive

requirements replacing a substance may be necessary and it may even present an opportunity for a

manufacturer to differentiate himself from competitors. In this study, we examine how competition

influences manufacturers’ strategic decisions when a substance of concern is identified within their

products. To identify ways to increase the number of manufacturers replacing a substance, we examine

whether manufacturers can avoid competing on toxicity and instead collaborate to replace a substance.

Our work is motivated by the efforts of market leaders in the reusable water bottle industry to replace

1

Authors’ names blinded for peer review2 Article submitted to Management Science; manuscript no. ()

bisphenol-A (BPA) from their products in 2007 – 2008 (Austen 2008, Bailin et al. 2008, Elias et al.

2013). At the time, the reusable water bottle industry was a growing market, comprised of two leading

companies, CamelBak and Nalgene. BPA, which was found in the polycarbonate plastic used to make

water bottles, was a growing substance of concern for consumers, retailers, and regulators (Kuchment

2008). Following early press coverage about the potential dangers of BPA in plastic baby bottles, envi-

ronmentally conscious customers in the reusable water bottle segment began to demand alternatives to

polycarbonate. Eastman Chemical, a supplier of copolyesters, had developed a replacement substance

called Tritan that was comparable in performance to polycarbonate plastics and did not contain BPA.

Taking into account the level of consumer sensitivity to BPA, the likelihood that the use of BPA would

be regulated, and the inherent competition to provide a BPA-free solution, CamelBak and Nalgene

had to decide whether to incur the cost to replace polycarbonate with BPA-free Tritan or to defer

replacement and wait to see if regulation would occur.

In this paper, we study a vertically differentiated market consisting of a high-end and a low-end

manufacturer selling a product that contains a substance of concern. Although the substance is not

regulated, there is a belief in the market that regulation may occur. A replacement substance is avail-

able from a supplier, but at a higher cost. The competing manufacturers must independently decide (1)

whether to proactively replace the substance or to defer replacement and wait to see if regulation hap-

pens and (2) what price to charge for their products. Many environmentalists believe that companies,

such as CamelBak and Nalgene, should never compete on toxicity. According to James Ewell, Sustain-

able Materials Director at GreenBlue, a nonprofit that focuses on making products more sustainable,

“we are trying to help companies understand that progress to solve this problem will not evolve as

rapidly if industry attempts to use toxicity as a means of differentiating their products,” (Ewell 2013).

We therefore examine ways for manufacturers to not compete on toxicity but instead work together

to replace a substance of concern. Our research adds to the growing operations management literature

that examines the negative impact competition can have on a firm’s environmental performance (e.g.,

Atasu et al. 2009, Majumder and Groenevelt 2001, Orsdemir et al. 2014, Toyasaki et al. 2010).

Our research goals are to (i) demonstrate how competition, consumer preferences, supplier prices,

and regulatory forces can facilitate or hinder manufacturers replacing a substance and (ii) identify

opportunities to increase the number of manufacturers replacing a substance of concern. Our results

show that when manufacturers compete on toxicity, if they face a cost tradeoff between the substance’s

expected regulatory risk and the supplier price for the replacement substance, then the high-end

manufacturer can use his brand advantage to control the market. For example, when the expected

regulatory risk and the supplier price are low, if the high-end manufacturer is willing to proactively

replace and sacrifice a potential cost benefit to deferring replacement, then he can charge a higher price

and capture more demand than the low-end manufacturer. The competition between the manufacturers

is highest when the supplier does not price the replacement substance in one of the extremes, but

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 3

instead charges an intermediate price. Under these conditions, a unique asymmetric equilibrium can

occur where the low-end manufacturer proactively replaces and is a niche-provider of a higher-priced

substance-free product, and the high-end manufacturer defers replacement and captures more demand

with a lower-priced product containing the substance of concern.

When the manufacturers can share the cost to replace, opportunities may exist for them to work

together to replace a substance of concern, even when the shared cost is greater than the sum of their

individual replacement costs. For example, if the low-end manufacturer’s strategy under competition

is to defer replacement and the high-end manufacturer’s strategy is to replace, then it may be advan-

tageous for the high-end manufacturer to incur a larger portion of the shared replacement cost to

help the low-end manufacturer to replace. This is even though when the manufacturers compete, the

high-end manufacturer already charges a higher price and captures more demand than the deferring

low-end manufacturer. Helping the low-end manufacturer enables the high-end manufacturer to better

use his brand advantage to further increase both his price and demand, resulting in higher profits.

2. Literature Review

The analytical modeling of firms’ environmental investment decisions is an emerging topic within the

environmental literature (e.g., Arora and Fosfuri 2003, Bagnoli and Watts 2003, Cortazar et al. 1998,

Kraft et al. 2013a,b, Raz et al. 2013, Yalabik and Fairchild 2011). A number of these papers examine

a competition-based setting. For example, Bagnoli and Watts (2003) study the effectiveness of firms’

investments in corporate social responsibility programs in attracting environmentally sensitive con-

sumers. Yalabik and Fairchild (2011) examine the impact that competition, consumer demands, and

regulation can have on firms’ carbon abatement decisions. With respect to substances of concern, Kraft

et al. (2013a) examine a firm’s development and implementation decisions to potentially replace a

substance in a multi-period setting. The authors show how market and regulatory forces can impact

a firm’s decisions. While the foundation for our model is also firms’ replacement decisions for a sub-

stance of concern, we model a much richer competition that includes a differentiated Bertrand price

competition based on consumer preferences. Incorporating these aspects allows us to (1) examine how

the consumer utility and the supplier price can drive manufacturers’ pricing and replacement decisions

when regulations are uncertain, (2) better define the resulting market structure with respect to price

and demand, and (3) identify when manufacturers can collaborate to replace a substance of concern.

In the last decade, there has been an emerging literature that applies analytical models to examine

the impact of regulation on firms’ environmental decisions (Krysiak 2008, Maxwell and Decker 2006,

Requate 2005, Tarui and Polasky 2005). In particular, a number of works have emerged within the

operations management literature (e.g., Ata et al. 2012, Atasu et al. 2009, Drake et al. 2012, Krass

et al. 2013, Kroes et al. 2012, Plambeck and Wang 2009). The focus of these works has been on

the use and structure of financial devices (e.g., taxes, rebates, and subsidies) to incentivize firms to

Authors’ names blinded for peer review4 Article submitted to Management Science; manuscript no. ()

improve their environmental performance. Our focus is not on the design of regulation but rather

on the impact regulatory uncertainty can have on manufacturers’ decisions. Note that there exists a

stream of environmental investment literature that examines regulatory uncertainty (e.g., Baker and

Shittu 2006, Farzin and Kort 2000, Hartl 1992, Isik 2004). However, these works typically either focus

solely on policy impacts or do not consider the problem aspects that we are interested in; e.g., none

of the papers listed model competition.

Firms collaborating to solve shared business problems has been well studied in a number of differ-

ent disciplines including research and development (e.g., Bhaskaran and Krishnan 2009, D’Aspremont

and Jacquemin 1988, Jap 2001, Kamien and Tauman 1984) and supply chain management (e.g., Bak-

shi and Kleindorder 2009, Corbett and DeCroix 2001, Jacobs and Subramanian 2011, Klassen 2000,

Kurtulus et al. 2012). Within corporate sustainability, firms working together to solve environmen-

tal issues is an emerging topic with the primary focus being on collaborations between supply chain

partners such as suppliers and manufacturers (e.g., Carter and Carter 1998, Geffen and Rothenberg

2000), manufacturers and retailers (e.g., Caro et al. 2013), or both (e.g., Vachon and Klassen 2008).

Despite this, Nidumolu et al. (2014) state that “when it comes to developing collaborative solutions

to systematic [environmental] problems, very little progress has been made,” even though there is a

“growing awareness of the critical need for improved collaboration” (pp. 77-78). Too often efforts have

failed due in large part to competitive self-interests and a lack of shared purpose between collabo-

rators. We contribute to this literature a model that examines how competition can influence firms’

substance replacement decisions and that investigates opportunities for horizontal competitors (rather

than supply chain partners) to collaborate and not compete on environmental issues.

Technology adoption is one topic that has received considerable attention with regards to both firm

competition and firm collaboration. Technology adoption under competition is well-studied within

the economics literature (e.g., Fudenberg and Tirole 1985, Hannan and McDowell 1984, Hoppe 2000,

Jensen 1982, Katz and Shapiro 1986, Levin et al. 1987, Reinganum 1981) and an emerging topic within

the operations management literature (e.g., Gaimon 1989, Goyal and Netessine 2007, Huisman and

Kort 2004, Mamer and McCardle 1987, Wang and Seidmann 1995). Related to our paper, Wang and

Seidmann (1995) examine how the competition between suppliers affects their decision to adopt a

new technology (i.e., EDI). The authors find that a high adoption cost can lead to a partial adoption

equilibrium. We expand on this result in that we find a partial adoption equilibrium can occur when

a tradeoff exists between adoption cost and expected regulatory risk. Regarding the impact of market

size on technology adoption, Hannan and McDowell (1984) show that for the case of banks adopting

ATMs, firm size is positively correlated with adoption. Conversely, Levin et al. (1987) show that for the

case of grocers adopting optical scanners, firm size is negatively correlated with adoption. We show that

for the case of replacing a substance of concern, while a larger firm (i.e., higher demand firm) is more

likely to adopt a replacement than a smaller firm, he may also use his position to control the market

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 5

by not adopting. With regards to competitors collaborating to adopt a new technology, the literature

includes papers from both the economics literature (Clemson and Knez 1988, Teece 1992, and Axelrod

1997) and the strategy literature (e.g., Hagedoorn and Schakenraad 1994, Hamel 1991, Lado et al.

1997, Shan 1990). Concerning the impact of market size on technology adoption collaboration, Shan

(1990) examine cooperative relationships between high-technology firms jointly commercializing a new

technology. They find that competitive position impacts a firm’s propensity to cooperate, and hence,

larger firms are less likely to collaborate. Conversely, Hagedoorn and Schakenraad (1994) examine

the effect of technology alliances on firm performance. They show that larger firms are more likely to

partner. Both papers are empirical in nature. We develop an analytical model to show that when a large

firm’s competitive position is limited, collaboration and helping a smaller firm to adopt a replacement

substance can actually help a large firm to better use his brand advantage to improve his profits.

3. The Model

Next, we outline the model for the competition-only scenario analyzed in §4. In §5, we adapt the model

dynamics to the cost-sharing scenario.

We consider a vertically differentiated market consisting of two types of manufacturers, a high-

end (manufacturer 1) and a low-end (manufacturer 2). The two manufacturers are differentiated by

consumer preferences for their brands. Both manufacturers sell a product that contains a substance

of concern. Although the substance of concern is not regulated, there is a belief in the market that

regulation may occur. A supplier has developed a replacement substance that is available at a per unit

wholesale price of w. The manufacturers must first decide whether to proactively replace the substance

or to defer replacement and wait to see if regulation happens. The two manufacturers compete in a

dynamic game of perfect information (i.e., they make their replacement decisions sequentially) with

the high-end manufacturer (manufacture 1) moving first. Based on manufacturer 1’s position as the

high-end provider, it is in manufacturer 1’s best interest to closely monitor the potential risks of the

substance of concern and to act first to replace the substance (if necessary). In §6, we demonstrate

that our results do not change considerably when the low-end manufacturer can replace first.

Manufacturer i’s strategy, si (i = 1, 2), is either to proactively replace the substance (R) or to defer

replacement (D). If manufacturer i replaces the substance, then in addition to the cost per unit w, he

incurs a fixed replacement cost K that represents the cost to update his supply chain to manufacture

with the new substance. We assume that the manufacturers’ replacement costs are equal. This assump-

tion keeps the model tractable and is reasonable since manufacturers’ replacement costs can be either

increasing or decreasing in demand. For example, while a manufacturer with high demand may have a

larger and more costly supply chain, he may also have more resources available to him and more influ-

ence over his suppliers. In §7, we discuss how our results change when the manufacturers’ replacement

costs are asymmetric. Note that a manufacturer’s cost to remove a substance from his product can be

Authors’ names blinded for peer review6 Article submitted to Management Science; manuscript no. ()

substantial. For example, the Consumer Electronics Association estimates that the initial compliance

requirements for the European Union’s Restriction of Hazardous Substances (RoHS) directive, which

restricts the use of only six substances, cost the global electronics industry $32 billion (Carbone 2008).

If manufacturer i defers, then he risks a possible loss in demand and potential added costs if regula-

tion occurs. However, deferring is a viable option since not all substances of concern are proven to be

harmful; e.g., aspartame in diet soft drinks (see Brody 1983 and Halliday 2008).

Once the manufacturers make their replacement decisions, they then compete in a differentiated

Bertrand competition where each manufacturer simultaneously determines the price for his product.

Manufacturer i’s demand, Di (i = 1, 2), is based on consumers’ utility function for the product and

the replacement substance. Our modeling of consumer preferences follows Moorthy (1988) and prior

literature in sustainable operations (e.g., Atasu and Souza 2013, Atasu and Subramanian 2012). The

consumers are heterogenous, with a consumer valuation of θ for manufacturer 1’s product and δθ for

manufacturer 2’s product, with θ distributed uniformly over (the normalized support) [0,1] and 0<

δ < 1. The constant δ represents the consumer valuation discount factor of manufacturer 2’s product.

In addition to their utility for the product, consumers have a fixed utility v (δv) for the replacement

substance that is only realized if manufacturer 1 (manufacturer 2) replaces. To simplify our analysis, we

normalize our market size to 1. Given prices p1 and p2, and replacement strategy (s1, s2), a consumer’s

utility is U1(θ, v) = θ+ v1s1=R− p1 for manufacturer 1’s product, and U2(θ, v) = δθ+ δv1s2=R− p2 for

manufacturer 2’s product. We define 1si∈{1,2}=R as an indicator function such that a consumer incurs

utility v (δv) from the replacement substance only if manufacturer 1 (manufacturer 2) replaces. Based

on these functions, the market is divided into high-end consumers, represented by the set {θ|U1(θ, v)≥

0,U1(θ, v)≥ U2(θ, v)}; low-end consumers, represented by the set {θ|U2(θ, v)≥ 0,U2(θ, v)> U1(θ, v)};

and consumers who do not purchase the product, represented by the set {θ|U1(θ, v) < 0,U2(θ, v) <

0}. Due to the interdependency between consumers’ utility and the manufacturers’ demands, when

solving for the manufacturers’ optimal prices, we must incorporate additional constraints based on the

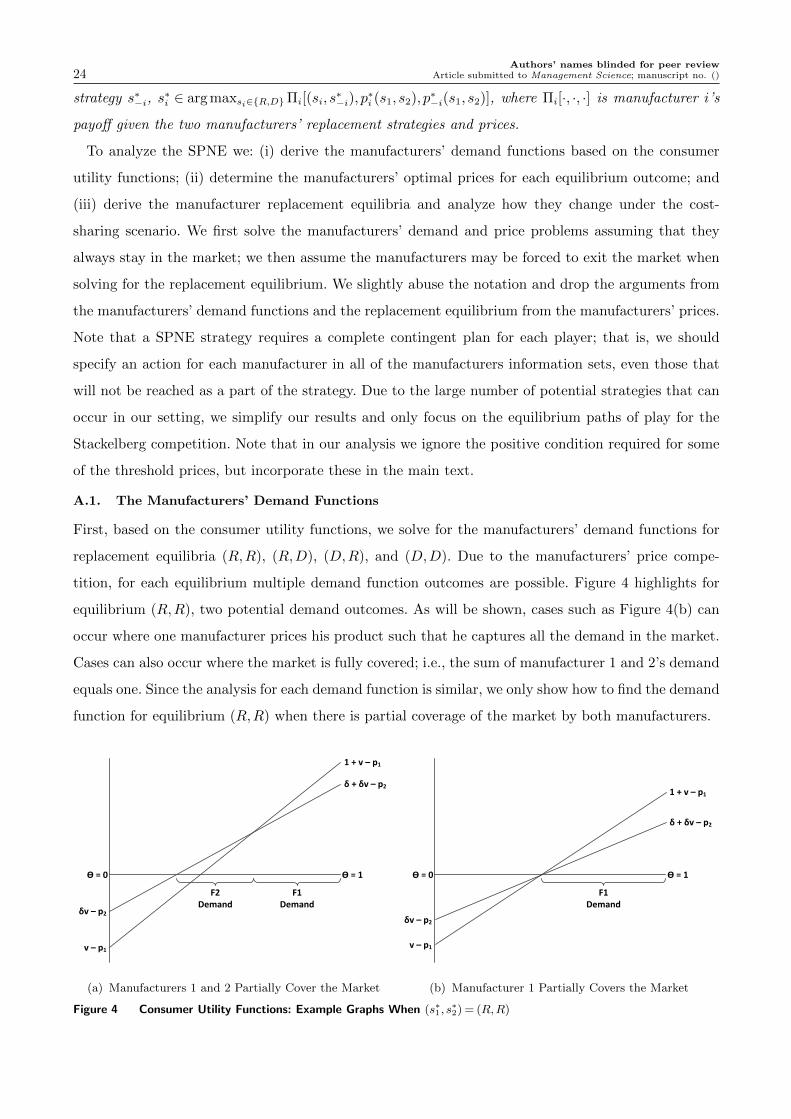

consumers’ preferences (see §A.1 for a visual representation of the manufacturers’ demand problem).

We discuss and solve for the manufacturers’ demand functions in §4.

After the manufacturers make their replacement and pricing decisions, regulation of the substance

is announced with probability q. If regulation occurs and manufacturer i has not replaced, then he is

forced to replace at a cost of αK with α > 0. Parameter α can represent either a time discount (i.e.,

α < 1) or a penalty (i.e., α ≥ 1) for delaying replacement. To capture the two drivers of regulatory

risk and to simplify our notation, we define the expected regulatory risk, r= αq, such that r takes into

account both the probability of regulation occurring and the subsequent cost the manufacturer incurs.

In order to study the range of potential scenarios a manufacturer may face, we consider cases when

there is a potential benefit to delaying replacement (i.e., r < 1 and thus, rK < K) and cases when

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 7

there is a potential risk in delaying replacement (i.e., r≥ 1 and thus, rK ≥K).1 Note that regulation

could also represent market requirements that force a manufacturer to replace. For example, many

large retailers such as Wal-Mart have banned the sale of products containing substances of concern

such as BPA and BFRs (Koch 2013, Mui 2008). To model the manufacturers’ decisions, we focus

on the demand period leading up to a potential regulation announcement, which is often very long.

For example, the length of time from the first popular press warning regarding BPA in baby bottles

until initial regulation in the U.S. was over a decade (Consumer Reports 1999, Layton 2009). Hence,

modeling the manufacturers’ decisions for only this demand period and not perpetuity is reasonable

since it captures the typical potential costs and profits a manufacturer incurs for the foreseeable future.

In summary, we present a comprehensive end-to-end model where firms’ investment decisions are

influenced by upstream supplier pricing, downstream consumer preferences, internal costs, and external

regulatory threats. The sequence of events is as follows: (i) The high-end manufacturer (manufacturer

1) decides whether to replace (R) the substance of concern or to defer replacement (D). (ii) The low-

end manufacturer (manufacturer 2) makes his replacement decision. (iii) Based on their replacement

decisions, the two manufacturers simultaneously compete in a differentiated Bertrand competition to

determine the prices for their products. (iv) Regulation occurs with probability q; if regulation occurs

and a manufacturer has not replaced the substance, then he is forced to replace. Table 1 summarizes

our notation. Our detailed theoretical analysis is given in Appendix A; results found in the appendix

are referenced A.x. To support our analysis, we conduct an extensive numerical study; the results are

referenced throughout the main text and the details of the analysis can be found in Appendix B.

4. The Manufacturers’ Competition Scenario

The manufacturers make two decisions: first, whether to proactively replace (R) the substance of

concern or to defer (D) replacement, and second, what prices to charge for their products. Following

the recursive nature of our solution method, we first discuss the manufacturers’ pricing decisions in

§4.1. Given the manufacturers’ prices, we then discuss the manufacturers’ replacement decisions in

§4.2. Our model allows us to capture the key drivers of the manufacturers’ decisions: supplier price w,

expected regulatory risk r, consumer utility for the replacement substance v, and consumer valuation

discount factor of manufacturer 2’s product δ. Note that δ represents a measure of market structure

and the heterogeneity between the manufacturers.

We define manufacturer i’s profit as:

πi(pi, p−i, (s1, s2)) =

(pi−w)Di(pi, p−i, (s1, s2))−K if si =R,

piDi(pi, p−i, (s1, s2))− rK if si =D.(1)

1 Due to delays in regulation (Grady 2010, Tavernise 2012), a manufacturer may be able to defer expensive investmentsand realize a time-discounted cost savings. Conversely, by not proactively replacing, a manufacturer may risk incurringadditional costs if regulation occurs and he is not prepared. As Mark Newton, Dell’s senior manager for environmentalsustainability, noted, “Being ahead of the curve on regulation indicates overall good management. Late adaptation hascost implications, for example the cost of making major changes in a very limited time frame” (ChemSec 2009).

Authors’ names blinded for peer review8 Article submitted to Management Science; manuscript no. ()

Table 1 Notation

Manufacturer Decision Variables

si Manufacturer i’s strategy; si∈{R (replace), D (defer replacement)}; s∗i is manufacturer i’s equilibrium strategy

pi Price charged by manufacturer i for his end product; pi > 0 and p∗i is the manufacturer’s optimal price forreplacement equilibrium (s1, s2)

Consumer Utility Parameters

θ Consumer valuation for the product; θ∼U [0,1]

v Additional consumer utility for the replacement substance; v ∈ (0,1)

δ Consumer valuation discount factor of manufacturer 2’s product; δ ∈ (0,1)

Replacement Cost and Regulation Parameters

w Supplier wholesale price for the replacement substance; w> 0

K Manufacturer cost to immediately replace the substance of concern

q Probability of regulation; q ∈ [0,1]

α Regulation penalty; α> 0

r Expected regulatory risk; r= αq

Notice that to simplify our analysis we assume that when a manufacturer defers replacement, his unit

cost is zero for the substance of concern. Assuming a unit cost of zero is a common assumption in

differentiated Bertrand models (Shy 1995, Singh and Vives 1984) and does not alter our insights. To

simplify the notation, we drop the arguments from the manufacturers’ demand functions and do not

denote the associated replacement equilibrium for prices pi and p−i.

To focus our analysis on competitive scenarios, we adopt the following assumptions:

Assumption 1. Let v <min{δ, v} where v= δ(2−δ)4−2δ−2δ2 .

Assumption 2. Let 0≤w<wmax where wmax = min{

max{δ(1+v)

2, v+2(1−δ)

2−δ

}, δv+ δ

2

}.

Assumptions 1 and 2 limit the number of cases where only either a symmetric equilibrium or one

in which only one manufacturer captures demand occur. For Assumption 1, a low value for δ would

suggest that the manufacturers may no longer be competitors. Thus, realistically δ will tend to be

closer to 1 than 0. Conversely, a consumer’s utility for a replacement substance will not likely outweigh

his utility for the product. Thus, v will tend to be closer to 0 than 1. For Assumption 2, if w≥wmax,

then the equilibrium is (D,D) or one in which only one manufacturer captures demand (see Appendix

A.3). Note that the terms comprising wmax are threshold supplier prices and defined in Theorem 1.

4.1. The Manufacturers’ Pricing Decisions

After the manufacturers make their replacement decisions, they compete in a differentiated Bertrand

competition to determine the prices of their products. Theorem 1 defines the manufacturers’ optimal

prices and demand functions for each replacement equilibrium, as a function of the supplier price w.

Theorem 1. The manufacturers’ optimal prices and demand functions for replacement equilibrium

(s∗1, s∗2) are:

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 9

(s∗1, s∗2) p∗i /D

∗i 0≤w<w1

s∗1 ,s∗2

w1s∗1 ,s

∗2≤w≤w2

s∗1 ,s∗2

w2s∗1 ,s

∗2<w<w3

s∗1 ,s∗2

w3s∗1 ,s

∗2≤w<wmax

(R,R)

p∗1, p∗2

(2+v)(1−δ)+3w

3, (1−δ)+(v+w)

2, δv 2(1−δ)(1+v)+3w

4−δ , δ(1−δ)(1+v)+w(2+δ)

4−δwδ,w

(1−v)(1−δ)+3w

3

D∗1,D∗2

2+v3, 1−v

3

(1−δ)+(v−w)

2(1−δ) , (1−δ)−(v−w)

2(1−δ)2(1+v)−w

4−δ , δ(1+v)−2wδ(4−δ)

δ(1+v)−wδ

,0

(R,D)p∗1, p

∗2 v,0 (1−δ)+(v+w)

2,0 2(1−δ)+v+2w

4−δ , δ[(1−δ)+w]−v(2−δ)4−δ w, (w− v)− (1− δ)

D∗1,D∗2 1,0 (1−δ)+(v−w)

2(1−δ) , (1−δ)−(v−w)

2(1−δ)2(1−δ)+v−w(2−δ)

(1−δ)(4−δ) , δ[(1−δ)+w]−v(2−δ)δ(1−δ)(4−δ) 0, (1+v)−w

δ

(D,R)p∗1, p

∗2 0, δv− (1− δ) 2(1−δ)+(w−δv)

3, (1−δ)+(2w+δv)

3

2(1−δ)+(w−δv)4−δ , δ(1−δ)+2w+δv(2−δ)

4−δw−δvδ,w

D∗1,D∗2 0,1 2(1−δ)+(w−δv)

3(1−δ) , (1−δ)−(w−δv)3(1−δ)

2(1−δ)+(w−δv)(1−δ)(4−δ) , (2−δ)(δv−w)+δ(1−δ)

δ(1−δ)(4−δ)δ(1+v)−w

δ,0

(D,D)p∗1, p

∗2

2(1−δ)4−δ , δ(1−δ)

4−δ

D∗1,D∗2

24−δ ,

14−δ

with

w1R,R = max

{0, v(1+2δ)−(1−δ)

3

}, w2

R,R = max{

0, 3δv−δ(1−δ)2+δ

}, and w3

R,R = δ(1+v)

2;

w1R,D = max{0, v− (1− δ)}, w2

R,D = max{

0, v(2−δ)−δ(1−δ)δ

}, and w3

R,D = v+2(1−δ)2−δ ;

w1D,R = max{0, δv− 2(1− δ)}, w2

D,R = max{

0, δv− 1−δ2

}, and w3

D,R = δv+ δ(1−δ)2−δ .

Note: For (s∗1, s∗2) = (R,R), the upper bound for the lower supplier price range is w≤w1

R,R, rather than w<w1R,R.

By Theorem 1, the manufacturers’ pricing decisions and demand functions are highly dependent upon

the supplier price w. For example, when (s∗1, s∗2) = (R,D) and the supplier price is low (i.e., 0≤ w <

w1R,D), the low unit cost for the replacement helps manufacturer 1 (high-end) capture all the demand in

the market by forcing manufacturer 2 (low-end) to price at his margin (i.e., p∗2 = 0). Conversely, when

the supplier price is high (i.e., w3R,D ≤w<wmax), the high unit cost forces the replacing manufacturer

1 to price at his margin (i.e., p∗1 =w), and then only manufacturer 2 captures demand since he can price

his product lower because it does not contain the expensive replacement substance. A similar result

occurs for equilibrium (D,R), but with manufacturer 2 (the replacing manufacturer) capturing all the

demand when w is low, and manufacturer 1 (the deferring manufacturer) capturing all the demand

when w is high. When the equilibrium is (R,R), although both manufacturers proactively replace, a

case can still occur in which only one manufacturer captures demand. This occurs when w is high and

manufacturer 1 can take advantage of his brand and the high price for both manufacturers products

to capture the only demand in the market.

Corollary 1 further illustrates Theorem 1 by demonstrating when the manufacturers partially or

fully satisfy the market demand.

Corollary 1. If (s∗1, s∗2) = (R,R), (R,D), or (D,R), then the manufacturers fully meet the market

demand if 0≤w≤w2s∗1,s∗2, and partially meet it otherwise. If (s∗1, s

∗2) = (D,D), then the manufacturers

always partially meet the market demand.

Authors’ names blinded for peer review10 Article submitted to Management Science; manuscript no. ()

For equilibria (R,R), (R,D), and (D,R), when the supplier price is low, the manufacturers fully

meet the market demand. When the supplier price is high, the price of the manufacturers’ products

increases and some consumers prefer not to purchase. Thus, the manufacturers only partially meet the

market demand. For equilibrium (D,D), the manufacturers always partially meet the market demand.

Next, we compare the manufacturers’ optimal prices and demand functions within each potential

replacement equilibrium.

Lemma 1. The manufacturers’ optimal prices and demand functions are such that

(a) If (s∗1, s∗2) = (R,R) or (D,D), then (i) p∗1 > p

∗2 and (ii) D∗1 >D

∗2,

(b) If (s∗1, s∗2) = (R,D), then (i) p∗1 > p

∗2 and (ii) D∗1 ≥D∗2 for 0≤w≤wR,D, D∗1 <D

∗2 otherwise,

(c) If (s∗1, s∗2) = (D,R), then

(i) p∗1 < p∗2 for 0≤w<w1

D,R, w1D,R ≤w≤w2

D,R if v1 < v, w2D,R <w<w

3D,R if v2 < v,

w3D,R ≤w<wmax if v3 < v; p∗1 ≥ p∗2 otherwise,

(ii) D∗1 ≤D∗2 for 0≤w≤wD,R, D∗1 >D∗2 otherwise,

with w2s∗1,s∗2<ws∗1,s∗2 <w

3s∗1,s∗2

and v3 < v2 < v1;

where wR,D = δ(1−δ)+2v

δ(3−δ) , wD,R = max{δv− δ(1−δ)

2,0}

, v1 = 1−δδ

, v2 = (1−δ)(5−2δ)2δ(4−δ) , and v3 = 1−δ

2δ.

Lemma 1 highlights the market structure for each potential replacement equilibrium. When the

equilibrium is symmetric (i.e., (s∗1, s∗2) = (R,R) or (D,D)), due to his brand advantage, manufacturer

1 is the market leader with both a higher priced product and higher demand. A similar result occurs

for equilibrium (R,D) when the supplier price w is low; i.e., 0 ≤ w ≤ wR,D. The low cost for the

replacement substance allows manufacturer 1 to charge a moderate price for his product containing

the replacement and thus, generate a higher demand than manufacturer 2. When w is high (i.e.,

wR,D < w < wmax), however, manufacturer 1 no longer captures more demand than manufacturer 2.

Any benefit manufacturer 1 may gain from proactively replacing is solely based on his ability to target

a smaller market that is willing to pay a higher price for a product containing the replacement. A

similar result occurs for equilibrium (D,R), but with the additional restriction that v must be sufficient

for p∗2 > p∗1 to hold. Given consumers’ lower preference for manufacturer 2’s product, there must be

some utility for the replacement substance for manufacturer 2 to be able to charge a higher price than

manufacturer 1. As we will show, understanding how the market structure changes with respect to w

for each potential equilibrium gives insight into the manufacturers’ replacement decisions and when

opportunities exist for the manufacturers to share costs.2

In §4.2 we characterize the manufacturer replacement equilibrium. To do so, we first order the

threshold supplier prices for the four potential equilibria. To delineate the manufacturers’ strategies,

we define the following parameters for a low and high supplier price.

2 Note that not all of the outcomes presented in §4.1 occur in equilibrium for the manufacturers’ replacement game. Forexample, as will be shown, equilibrium (D,R) in Lemma 1 does not occur for 0≤w≤w2

D,R or 0≤w≤wD,R.

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 11

Definition 1. Define wL =w2R,R ≡max

{0, 3δv−δ(1−δ)

2+δ

}and wH =w3

D,R ≡ δv+ δ(1−δ)2−δ .

Based on this, we define the replacement equilibrium for low, intermediate, and high supplier price

ranges by determining (1) manufacturer 2’s best response if s∗1 = R and if s∗1 = D; and then (2)

manufacturer 1’s best response. See Appendix A.3 for the complete analysis.

4.2. The Manufacturers’ Replacement Decisions

Next, we analyze the manufacturers’ replacement decisions. As part of our analysis, we highlight the

demand outcomes for each equilibrium. By §4.1 we know that cases can occur in which a manufacturer

does not capture demand. Since realistically a manufacturer would not be willing to proactively replace

a substance if he did not capture demand, we make the following assumption.

Assumption 3. A manufacturer is forced to exit the market if his best response payoff is less than

or equal to −K.

If Assumption 3 holds, then we replace the exiting manufacturer’s strategy with a dash in the

replacement equilibrium.3 Note that Assumption 3 does not mean that a manufacturer is forced to exit

the market if his payoff is negative or if he does not capture demand. We assume that a manufacturer

is willing to incur a negative payoff to proactively replace as long as he captures some demand and

maintains a presence in the market. In addition, if he defers replacement and r < 1, then he is willing

to stay in the market to see if regulation occurs, even if he does not capture demand.

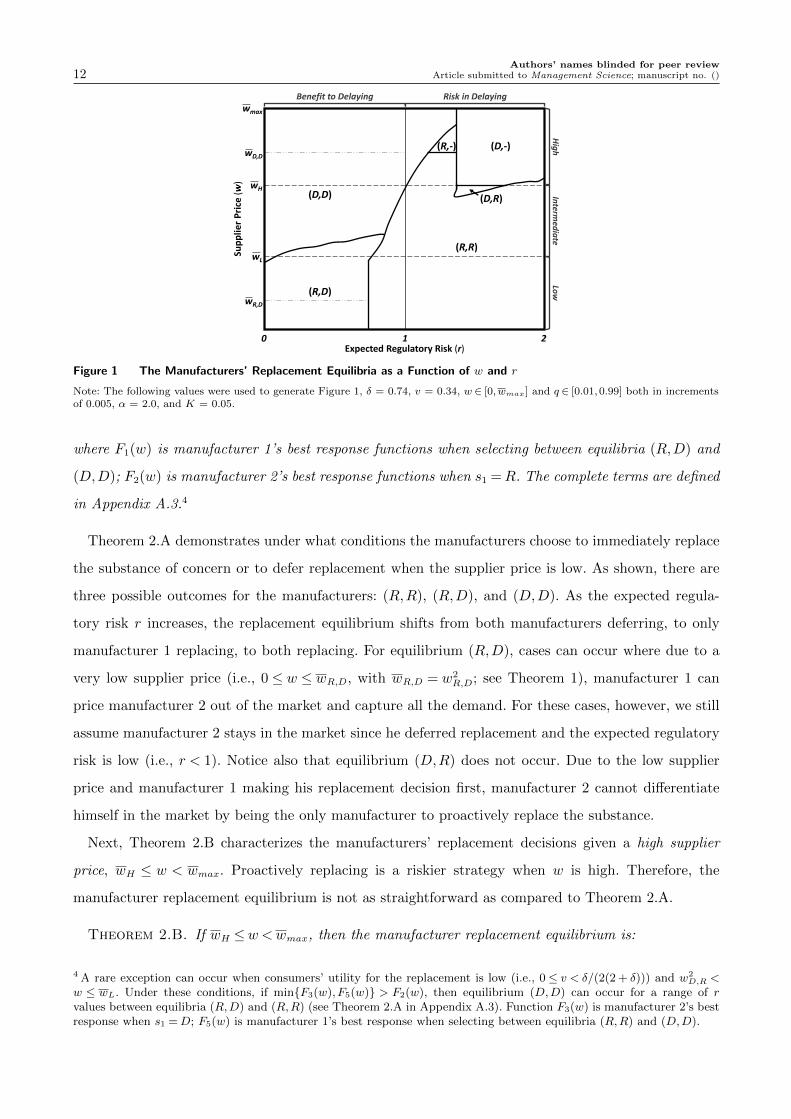

Figure 1 illustrates the manufacturers’ replacement strategies and is referenced throughout §4.2. We

define the equilibria with respect to two values: the supplier price w and the expected regulatory risk r.

This allows us to examine how a low (i.e., 0≤w≤wL), intermediate (i.e., wL <w<wH), or high (i.e.,

wH ≤w<wmax) supplier price impacts the manufacturers’ strategies when there is a potential benefit

(i.e., r < 1) or a potential risk (i.e., r≥ 1) in delaying replacement. We first discuss the manufacturers’

decisions when the supplier price is either low or high. We then discuss the more difficult to illustrate

case when the supplier price takes intermediate values.

Low and High Supplier Price: Due to the size of the manufacturer replacement equilibrium, we

divide our main result (Theorem 2) between the low and the high supplier price cases (see Appendix

A.3 for the complete theorem). Theorem 2.A characterizes the manufacturers’ replacement decisions

given a low supplier price, 0≤w≤wL.

Theorem 2.A. If 0≤w≤wL, then the manufacturer replacement equilibrium is:

(s∗1, s∗2) =

(D,D) if r < F1(w),

(R,D) if F1(w)≤ r < F2(w),

(R,R) if r≥ F2(w),

(2)

3 For these cases, we assume that the exiting manufacturer could re-enter the market. Thus, we do not solve for themonopoly prices and demands but instead continue to use the optimal prices and demand functions found in Theorem 1.

Authors’ names blinded for peer review12 Article submitted to Management Science; manuscript no. ()

Sup

plie

r P

rice

(w

)

(D,R)

Expected Regulatory Risk (r)

(R,R)

Benefit to Delaying Risk in Delaying

wH

wL

10 2

(R,-) (D,-)

(D,D)

(R,D)

wmax

Hig

hIn

termed

iate

Low

wD,D

wR,D

Figure 1 The Manufacturers’ Replacement Equilibria as a Function of w and r

Note: The following values were used to generate Figure 1, δ = 0.74, v = 0.34, w ∈ [0,wmax] and q ∈ [0.01,0.99] both in incrementsof 0.005, α = 2.0, and K = 0.05.

where F1(w) is manufacturer 1’s best response functions when selecting between equilibria (R,D) and

(D,D); F2(w) is manufacturer 2’s best response functions when s1 =R. The complete terms are defined

in Appendix A.3.4

Theorem 2.A demonstrates under what conditions the manufacturers choose to immediately replace

the substance of concern or to defer replacement when the supplier price is low. As shown, there are

three possible outcomes for the manufacturers: (R,R), (R,D), and (D,D). As the expected regula-

tory risk r increases, the replacement equilibrium shifts from both manufacturers deferring, to only

manufacturer 1 replacing, to both replacing. For equilibrium (R,D), cases can occur where due to a

very low supplier price (i.e., 0 ≤ w ≤ wR,D, with wR,D = w2R,D; see Theorem 1), manufacturer 1 can

price manufacturer 2 out of the market and capture all the demand. For these cases, however, we still

assume manufacturer 2 stays in the market since he deferred replacement and the expected regulatory

risk is low (i.e., r < 1). Notice also that equilibrium (D,R) does not occur. Due to the low supplier

price and manufacturer 1 making his replacement decision first, manufacturer 2 cannot differentiate

himself in the market by being the only manufacturer to proactively replace the substance.

Next, Theorem 2.B characterizes the manufacturers’ replacement decisions given a high supplier

price, wH ≤ w < wmax. Proactively replacing is a riskier strategy when w is high. Therefore, the

manufacturer replacement equilibrium is not as straightforward as compared to Theorem 2.A.

Theorem 2.B. If wH ≤w<wmax, then the manufacturer replacement equilibrium is:

4 A rare exception can occur when consumers’ utility for the replacement is low (i.e., 0≤ v < δ/(2(2 + δ))) and w2D,R <

w ≤ wL. Under these conditions, if min{F3(w), F5(w)} > F2(w), then equilibrium (D,D) can occur for a range of rvalues between equilibria (R,D) and (R,R) (see Theorem 2.A in Appendix A.3). Function F3(w) is manufacturer 2’s bestresponse when s1 =D; F5(w) is manufacturer 1’s best response when selecting between equilibria (R,R) and (D,D).

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 13

(1) If F2(w)≥ F3(w), then

(s∗1, s∗2) =

(D,D) if r < F3(w),

(D,−) if F3(w)≤ r < F4(w),

(R,R) or (R,−) if r≥ F4(w),

(3)

(2) If F2(w)<F3(w) and δ3+δ≤ v < v, then

(a) If F3(w)≤ F4(w), then

(s∗1, s∗2) =

(D,D) if r <max{F2(w),F5(w)},

(R,R) or (R,−) if max{F2(w),F5(w)} ≤ r < F3(w),

(D,−) if F3(w)≤ r < F4(w),

(R,R) or (R,−) if r≥ F4(w),

(4)

(b) If F3(w)>F4(w), then

(s∗1, s∗2) =

{(D,D) if r < F3(w),

(R,R) or (R,−) if r≥ F3(w),(5)

(3) If F2(w)<F3(w) and 0≤ v < δ3+δ

, then

(a) If F3(w)<F5(w), then Equation (3) holds,

(b) If F3(w)≥ F5(w), then Equation (4) holds,

where F2(w) and F3(w) are manufacturer 2’s best response functions when s1 =R and s1 =D; F4(w)

and F5(w) are manufacturer 1’s best response functions when selecting between equilibria (R,R)/(R,−)

and (D,−), and (R,R)/(R,−) and (D,D). The complete terms are defined in Appendix A.3.

Theorem 2.B demonstrates that when the supplier price is high, there are four possible replacement

equilibrium outcomes for the manufacturers: (R,R), (R,−), (D,−), and (D,D).5 Observe that equi-

libria in which the manufacturers offer differentiated products do not occur; i.e., (R,D) or (D,R).

When the supplier price is high, manufacturer 2 cannot capture demand by differentiating his prod-

uct. Instead, he must either follow manufacturer 1’s strategy (i.e., a symmetric equilibrium, (R,R)

or (D,D), occurs), or be forced to exit the market when the expected regulatory risk becomes too

costly. Note that for a fixed w, only either equilibrium (R,R) or equilibrium (R,−) can occur; both

cases cannot occur. Equilibrium (R,R) occurs when the supplier price is low (i.e., wH ≤w<w3R,R; see

Theorem 1) and equilibrium (R,−) occurs when the supplier price is high (i.e., w3R,R ≤w<wmax).

We divide the three cases in Theorem 2.B by two key measures: manufacturer 2’s best response

functions F2(w) and F3(w), and the consumers’ utility for the replacement substance v. Numerically,

we find that case (1) (i.e., F2(w) ≥ F3(w)) occurs when δ is high and the manufacturers are more

homogenous relative to cases (2) and (3) (i.e., F2(w)<F3(w)). For case (1), as the expected regulatory

5 If we were to assume that the manufacturers always stay in the market, then equilibria (R,−) and (D,−) would changeto equilibria (R,R) and (D,R), with manufacturer 1 capturing all the demand in both cases.

Authors’ names blinded for peer review14 Article submitted to Management Science; manuscript no. ()

risk r increases, the equilibrium shifts from (D,D) to (D,−) to either (R,R) if wH ≤ w < w3R,R or

(R,−) if w3R,R ≤ w < wmax (see Equation (3)). When the expected regulatory risk is low and the

supplier price is high, both manufacturers defer replacement. However, as the expected regulatory risk

increases, this along with manufacturer 1’s choice of price for his own product, can force manufacturer

2 to exit the market (i.e., equilibrium (D,−) or (R,−) occurs) as he cannot capture enough demand

by deferring replacement to offset his high expected regulatory cost (i.e., rK). Conversely, cases (2)

and (3) occur (i.e., F2(w)<F3(w)) when the manufacturers are more heterogenous, and therefore, the

consumers’ utility for the replacement v can have a greater influence on the manufacturers’ replacement

decisions. For example, a high consumer utility for the replacement v (i.e., δ3+δ≤ v < v), can simplify

the manufacturers’ decisions such that either a symmetric equilibrium occurs (i.e., (D,D) or (R,R)),

or if the supplier price is high enough, manufacturer 1 proactively replaces and forces manufacturer 2

out of the market (i.e., (R,−)); see Equation (5).

Lemma 2 highlights key insights into the occurrence of equilibria (R,R) and (R,D) when the supplier

price is low and equilibria (D,D), (D,−), and (R,−) when the supplier price is high.

Lemma 2. The manufacturer replacement equilibrium is such that:

(a) When the supplier price is low, 0≤w≤wL,

(i) If r≥ 1, then (s∗1, s∗2) = (R,R),

(ii) Only when r < 1, can (s∗1, s∗2) = (R,D) occur.

(b) When the supplier price is high, wH ≤w<wmax,

(i) If r < 1 and wD,D ≤w<wmax, then (s∗1, s∗2) = (D,D),

(ii) Only when r≥ 1, can (s∗1, s∗2) = (D,−) or (R,−) occur.

With wD,D = max{min{w3R,R,w

3R,D},wH}.

The manufacturers’ strategies are simplified when a cost tradeoff does not exist between the supplier

price and the expected regulatory risk. For example, if r≥ 1 and the supplier price is low 0≤w≤wL,

then as shown in the lower right region of Figure 1, the equilibrium is always (R,R). The expected

cost of regulation and the low unit cost for the replacement substance induce both manufacturers to

proactively replace. A similar result occurs when r < 1 and the supplier price is high wD,D ≤w<wmax(i.e., the upper left region in Figure 1), but with both manufacturers deferring to save costs.

The supplier price and the expected regulatory risk also define when an asymmetric equilibrium with

only manufacturer 1 proactively replacing occurs. When the supplier price is low, equilibrium (R,D)

can only occur when r < 1. This implies that manufacturer 1 can differentiate his product with the

replacement substance if he is willing to incur a cost to proactively replace; i.e., K > rK. The additional

cost, however, is worth manufacturer 1’s investment since by Lemma 1 he can charge a higher price

and generate more demand than manufacturer 2 when equilibrium (R,D) occurs in the low supplier

price range.6 Conversely, when the supplier price is high, equilibria (D,−) and (R,−) can only occur

6 Manufacturer 1’s demand is greater than manufacturer 2’s since wR,D >wL.

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 15

when r ≥ 1. Under these conditions, due to the high supplier price, manufacturer 2 cannot capture

demand by proactively replacing (i.e., s2 =R). However, due to the high expected regulatory risk and

manufacturer 1’s ability to use his brand advantage to force the low-end manufacturer to charge a

low price, deferring replacement (i.e., s2 =D) is an even less profitable strategy for manufacturer 1.

Therefore, manufacturer 2’s expected profit is −K and he is forced to exit the market.

Intermediate Supplier Price: The manufacturers’ most difficult replacement decisions occur when

the supplier offers an intermediate wholesale price; i.e., wL <w<wH . By not pricing the replacement

substance in one of the extremes (high or low), the supplier forces the manufacturers to evaluate

the difficult tradeoff between incurring additional costs to proactively replace versus possibly losing

demand and incurring regulatory costs if they defer replacement. First, we demonstrate that within

the intermediate supplier price range, all four potential replacement equilibrium can occur.

Lemma 3. If wL <w <wH , then the manufacturer replacement equilibrium can be (R,R), (R,−),

(R,D), (D,R), or (D,D). Equilibrium (R,−) only occurs when w3R,R ≤w<wH and δ

2−δ ≤ v < v.

Within this price range, both manufacturers almost always incur demand (by Lemma 3, equilibrium

(R,−) only occurs when both w and v are high). It is not possible to cleanly characterize the manufac-

turer replacement equilibrium for an intermediate supplier price due to the large number of conditions

required. Instead, we numerically examine the manufacturers’ most frequently occurring strategies as

r increases (for a fixed w). By Table 2, the two most frequently occurring cases are when either the

equilibrium shifts from (D,D) to (R,R) or from (D,D) to (R,D) to (R,R) as r increases.

Table 2 Intermediate Supplier Price: Manufacturers’ Replacement Decisions

Replacement equilibrium as r increases % of Median(for a fixed w) Cases w v δ(D,D) to (R,R) 51.5% 0.20 0.24 0.69(D,D) to (R,D) to (R,R) 27.8% 0.20 0.34 0.69(D,D) to (R,R) to (D,R) to (R,R) 11.0% 0.20 0.14 0.64(D,D) to (D,R) to (R,R) 5.3% 0.15 0.04 0.74(R,D) to (R,R) 2.8% 0.25 0.39 0.69

Note: A total of 28,140 scenarios were tested, resulting in 1,407 fixed w cases. The above strategies represent 98.4% of all casestested. Expected regulatory risk r values ranged from 0 to 2.

Unlike the low and the high supplier price cases, both equilibria (R,D) and (D,R) can occur when

the supplier charges an intermediate price. Consistent with our findings from the low supplier price

case, we numerically find that equilibrium (R,D) only occurs if r < 1 and that manufacturer 1 is able

to capture more demand with a higher priced product than manufacturer 2. Conversely, equilibrium

(D,R) only occurs if r≥ 1. As shown in Table 2, when consumers’ utility for the replacement is very

low (i.e., v = 0.14 or 0.04), manufacturer 1 can benefit by ignoring his brand advantage and ability

to replace first, and letting manufacturer 2 capture demand by being the only manufacturer in the

market with a product containing the replacement.7 Interestingly, for equilibrium (D,R), manufacturer

7 A low value for v also influences the size of this price range. The width of the intermediate price range is decreasing inv (Lemma A.2), thus the supplier’s choice of price is more likely to fall in the intermediate price range when v is low.

Authors’ names blinded for peer review16 Article submitted to Management Science; manuscript no. ()

2 often competes as a niche provider with a higher-priced substance-free product, while manufacturer

1 captures more demand with a lower-priced product.

To summarize §4, we illustrate three key insights. First, the manufacturers’ decisions are simplified

when the supplier charges a low (high) price and the expected regulatory risk is high (low). For this case,

a symmetric equilibrium occurs in which both manufacturers proactively replace (defer replacement).

Second, when there exists a cost trade-off between the expected regulatory risk and the supplier price,

the high-end manufacturer can control the market. For example, when the expected regulatory risk and

the supplier price are low, if the high-end manufacturer is willing to proactively replace and sacrifice

a potential cost benefit to deferring replacement (i.e., K > rK), then he can use his brand advantage

to charge a higher price and capture more demand than the low-end manufacturer. Conversely, when

both the supplier price and the expected regulatory risk are high, the high-end manufacturer can force

the low-end manufacturer to exit the market by limiting his ability to generate a high enough profit

to offset potential regulatory costs.8 Finally, the competition between the manufacturers is the highest

when the supplier offers an intermediate price for the replacement substance. In this price range,

typically both manufacturers capture some demand. In addition, equilibria in which the manufacturers

offer differentiated products can occur, with either the high-end (i.e., (R,D)) or the low-end (i.e.,

(D,R)) manufacturer proactively replacing.

Based on our understanding of the manufacturers’ replacement and pricing decisions under com-

petition, in §5 we examine whether opportunities exist for the manufacturers to avoid replacement

competition and instead, work together to replace the substance of concern.

5. The Manufacturers’ Cost-Sharing Scenario

Next, we examine opportunities for manufacturers to not compete on toxicity but instead, collaborate

to replace a substance of concern. In many industries, firms often share suppliers and have similar

components in their products. Within these industries, opportunities may exist for competitors to work

together and share the cost to implement a replacement substance. For example, leaders within the

jewelry industry collaborated to eliminate the use of cadmium after it was identified as a substance of

concern (Associated Press 2010). Within the furniture industry, manufacturers recently collaborated to

set industry-wide sustainability standards which included stringent self-regulation regarding chemicals

of concern (BIFMA 2014). Our goal is to identify ways to increase the number of manufacturers

replacing a substance of concern and thus, decrease the number of consumers exposed to the substance.

Nidumolu et al. (2014) characterize corporate environmental collaborations in two ways: (1) whether

the focus is either outcome or process based; and (2) whether the partnership is solely corporations

or includes additional stakeholders such as nonprofits and governments. Our approach is to model an

8 Due to the high-end manufacturer’s brand advantage and his ability to move first in the replacement game, outcomesin which only the low-end manufacturer captures demand do not occur for 0≤w<wmax (see Lemma A.1).

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 17

outcome-based model with a simplified cost-sharing scenario, where the partnership is between manu-

facturers 1 and 2 (see Appendix A.4 for the detailed analysis). To analyze this setting, we define KC as

the total shared cost for both manufacturers to replace the substance of concern, with manufacturer 1

paying tKC , manufacturer 2 paying (1− t)KC , and t∈ [0,1]. We do not restrict KC to be less than or

greater than the sum of the manufacturers’ individual replacement costs 2K. We modify the sequence

of events from Section 3 as follows: before competing to replace the substance (with manufacturer 1

acting first), the manufacturers can choose not to compete and instead, share the cost to replace. We

assume that the manufacturers share the cost to replace if a negotiated value of t∈ [0,1] can be found

such that both manufacturers have higher profits under cost sharing than under competition. To deter-

mine t, we apply a Nash bargaining solution to model the negotiation of costs, with the manufacturers’

status-quo points being their profits if they were to compete. Modeling cooperative settings through

the use of bargaining solutions is a common practice within the operations literature (e.g., Bakshi and

Kleindorder 2009, Nagarajan and Sosic 2008, Plambeck and Taylor 2005).

If the manufacturers share the cost to replace, then they both replace with manufacturer 1’s profit

equal to π1(p1, p2) = (p1 −w)D1(p1, p2)− tKC and manufacturer 2’s profit equal to π2(p2, p1) = (p2 −

w)D2(p2, p1)− (1− t)KC . Although the manufacturers work together to replace the substance, they

still compete on price with the resulting optimal prices and demand functions equal to those from the

price competition for equilibrium (R,R) (see Theorem 1). If an agreed upon value of t∈ [0,1] cannot be

negotiated, then the manufacturers compete to replace the substance. Our model setup supports Lado

et al. (1997) and Nidumolu et al. (2014), who emphasize that the most successful collaborative models

combine competitive and cooperative aspects to achieve superior performance.

We first define for each possible manufacturer replacement equilibrium under competition, the condi-

tions under which both manufacturers prefer to share the cost to replace. Recall that πi(p∗1, p∗2, (s

∗1, s∗2))

is manufacturer i’s profit under competition equilibrium (s∗1, s∗2).

Theorem 3. The manufacturers share the cost to replace

(a) If (s∗1, s∗2) = (R,R) or (R,−), and KC ≤ 2K,

(b) If (s∗1, s∗2) = (R,D), (D,R), (D,−), or (D,D), and 1 − G2(w)−π2(p∗2,p

∗1,(s∗1,s∗2))

KC≤ t∗s∗1,s∗2

≤G1(w)−π1(p∗1,p

∗2,(s∗1,s∗2))

KC,

and compete otherwise;

where Gi(w) = (p∗i −w)Di(p∗i , p∗−i) is manufacturer i’s margin times demand under cost sharing and

t∗s∗1,s∗2= max

[0,min

[1, 1

2+

[G1(w)−G2(w)]−[π1(p∗1,p∗2,(s∗1,s∗2))−π2(p

∗2,p∗1,(s∗1,s∗2))]

2KC

]]is the Nash bargaining solution

for replacement equilibrium (s∗1, s∗2).

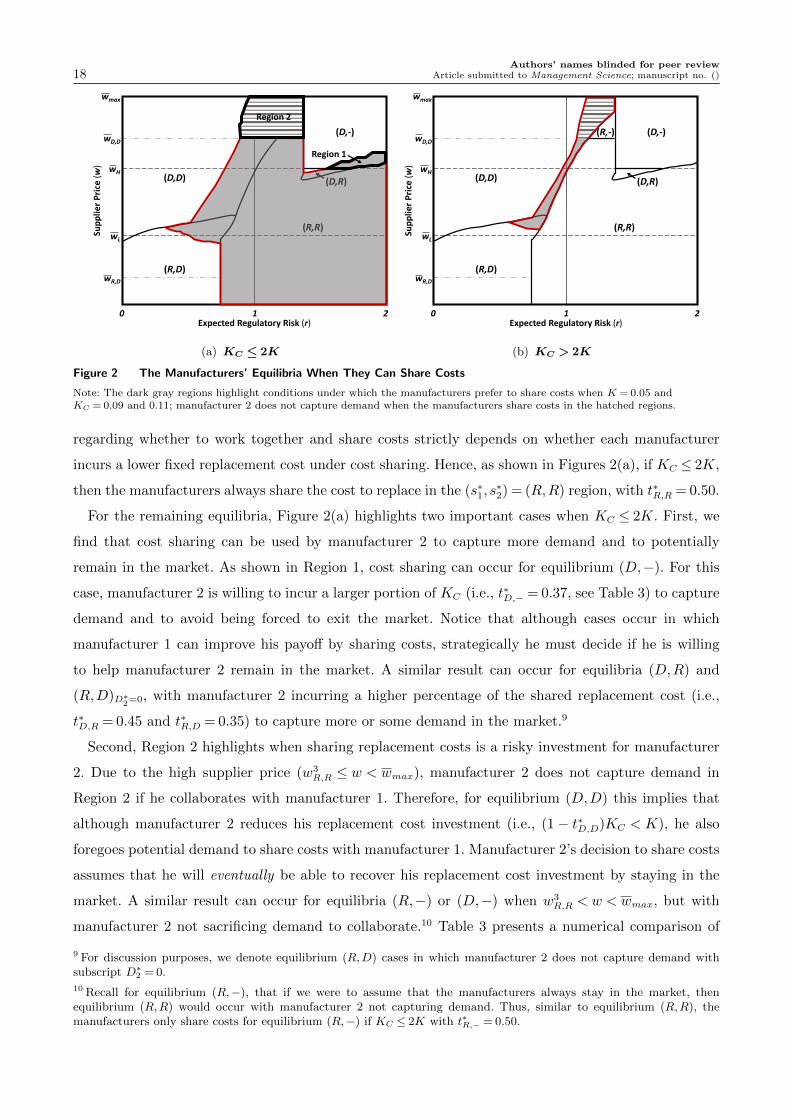

Based on the values from Figure 1, Figure 2 illustrates Theorem 3 for two cases: KC ≤ 2K (Figure

2(a)) and KC > 2K (Figure 2(b)). The dark gray regions highlight the cases when the manufacturers

prefer to share costs rather than compete. By Theorem 3a, if the manufacturers’ replacement equi-

librium under competition is for both of them to proactively replace (i.e., (R,R)), then their decision

Authors’ names blinded for peer review18 Article submitted to Management Science; manuscript no. ()

Sup

plie

r P

rice

(w

)

Expected Regulatory Risk (r)10 2

wH

wL

wmax

wD,D

(D,R)

(R,R)

(R,-) (D,-)

(D,D)

(R,D)wR,D

Region 2

Region 1

(a) KC ≤ 2K

Sup

plie

r P

rice

(w

)

Expected Regulatory Risk (r)10 2

wH

wL

wmax

wD,D

(D,R)

(R,R)

(R,-) (D,-)

(D,D)

(R,D)wR,D

(b) KC > 2K

Figure 2 The Manufacturers’ Equilibria When They Can Share Costs

Note: The dark gray regions highlight conditions under which the manufacturers prefer to share costs when K = 0.05 andKC = 0.09 and 0.11; manufacturer 2 does not capture demand when the manufacturers share costs in the hatched regions.

regarding whether to work together and share costs strictly depends on whether each manufacturer

incurs a lower fixed replacement cost under cost sharing. Hence, as shown in Figures 2(a), if KC ≤ 2K,

then the manufacturers always share the cost to replace in the (s∗1, s∗2) = (R,R) region, with t∗R,R = 0.50.

For the remaining equilibria, Figure 2(a) highlights two important cases when KC ≤ 2K. First, we

find that cost sharing can be used by manufacturer 2 to capture more demand and to potentially

remain in the market. As shown in Region 1, cost sharing can occur for equilibrium (D,−). For this

case, manufacturer 2 is willing to incur a larger portion of KC (i.e., t∗D,− = 0.37, see Table 3) to capture

demand and to avoid being forced to exit the market. Notice that although cases occur in which

manufacturer 1 can improve his payoff by sharing costs, strategically he must decide if he is willing

to help manufacturer 2 remain in the market. A similar result can occur for equilibria (D,R) and

(R,D)D∗2=0, with manufacturer 2 incurring a higher percentage of the shared replacement cost (i.e.,

t∗D,R = 0.45 and t∗R,D = 0.35) to capture more or some demand in the market.9

Second, Region 2 highlights when sharing replacement costs is a risky investment for manufacturer

2. Due to the high supplier price (w3R,R ≤ w < wmax), manufacturer 2 does not capture demand in

Region 2 if he collaborates with manufacturer 1. Therefore, for equilibrium (D,D) this implies that

although manufacturer 2 reduces his replacement cost investment (i.e., (1− t∗D,D)KC < K), he also

foregoes potential demand to share costs with manufacturer 1. Manufacturer 2’s decision to share costs

assumes that he will eventually be able to recover his replacement cost investment by staying in the

market. A similar result can occur for equilibria (R,−) or (D,−) when w3R,R < w < wmax, but with

manufacturer 2 not sacrificing demand to collaborate.10 Table 3 presents a numerical comparison of

9 For discussion purposes, we denote equilibrium (R,D) cases in which manufacturer 2 does not capture demand withsubscript D∗2 = 0.

10 Recall for equilibrium (R,−), that if we were to assume that the manufacturers always stay in the market, thenequilibrium (R,R) would occur with manufacturer 2 not capturing demand. Thus, similar to equilibrium (R,R), themanufacturers only share costs for equilibrium (R,−) if KC ≤ 2K with t∗R,− = 0.50.

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 19

under what conditions the manufacturers prefer to compete versus share costs when KC ≤ 2K.

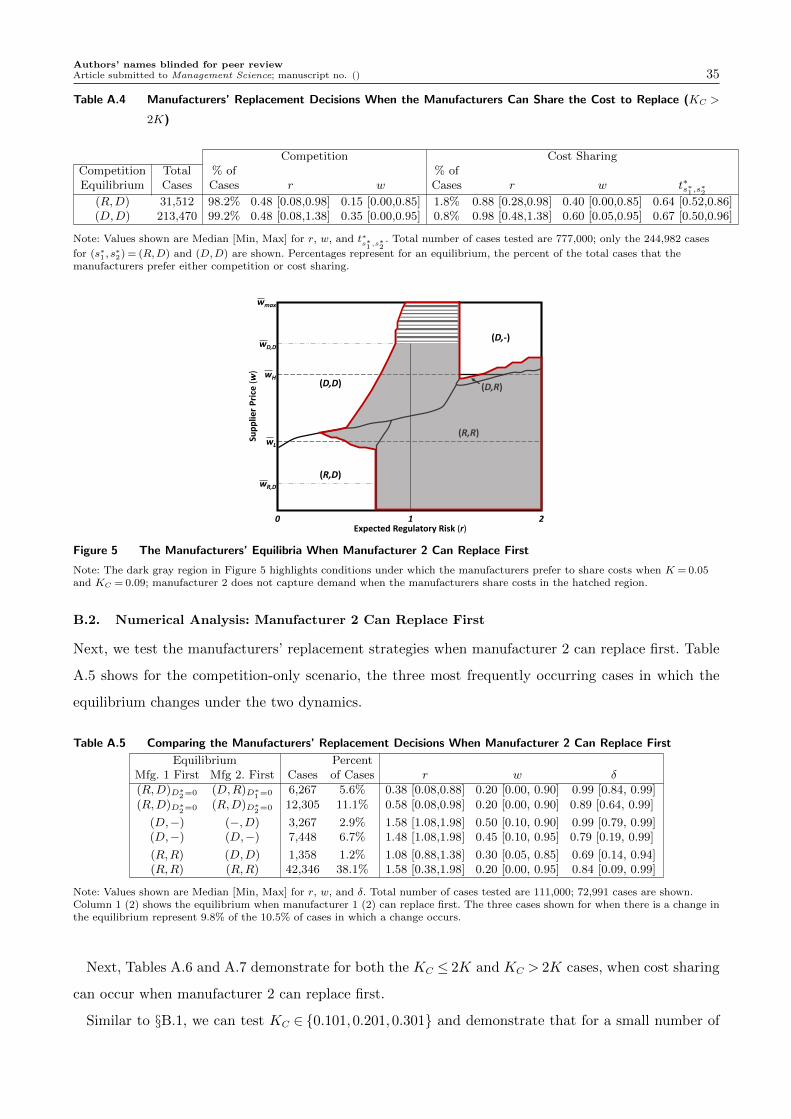

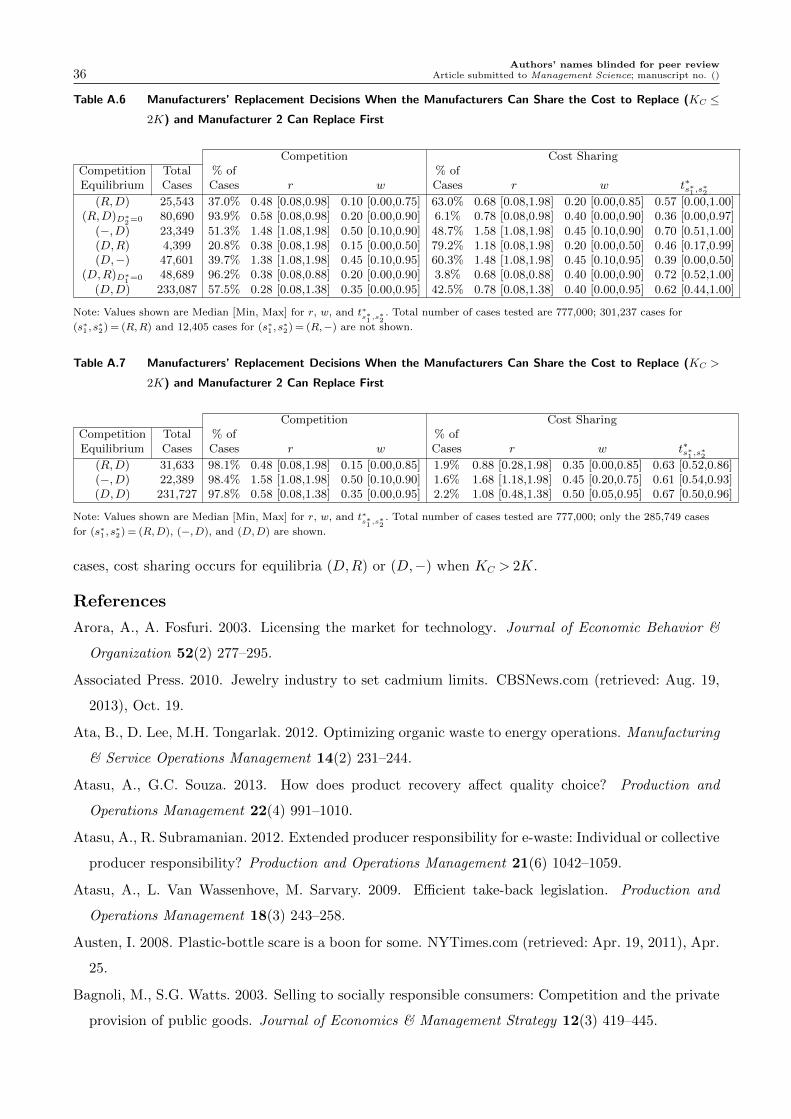

Table 3 Manufacturers’ Replacement Decisions When the Manufacturers Can Share the Cost to Replace (KC < 2K)

Competition Cost SharingCompetition Total % of % ofEquilibrium Cases Cases r w Cases r w t∗s∗1 ,s∗2

(R,D) 25,412 37.2% 0.48 [0.08,0.98] 0.10 [0.00,0.75] 62.8% 0.68 [0.08,0.98] 0.20 [0.00,0.85] 0.57 [0.00,1.00](R,D)D∗

2=0 130,412 95.4% 0.48 [0.08,0.98] 0.20 [0.00,0.90] 4.6% 0.78 [0.08,0.98] 0.40 [0.00,0.90] 0.35 [0.00,0.97]

(D,R) 3,360 8.3% 1.38 [1.08,1.88] 0.20 [0.10,0.40] 91.7% 1.28 [1.08,1.98] 0.20 [0.05,0.40] 0.45 [0.17,0.50](D,−) 71,087 47.7% 1.38 [1.08,1.98] 0.45 [0.10,0.95] 52.3% 1.48 [1.08,1.98] 0.45 [0.05,0.95] 0.37 [0.00,0.50](D,D) 222,910 59.9% 0.28 [0.08,1.38] 0.35 [0.00,0.95] 40.1% 0.78 [0.08,1.38] 0.40 [0.00,0.95] 0.61 [0.44,1.00]

Note: Values shown are Median [Min, Max] for r, w, and t∗s∗1 ,s∗2

. Total number of cases tested are 777,000; 307,978 cases for

equilibrium (R,R) and 15,841 cases for equilibrium (R,−) are not shown. Percentages represent for an equilibrium, the percent ofthe total cases that the manufacturers prefer either competition or cost sharing.

Due to coordination costs, the manufacturers’ shared replacement cost to eliminate the use of a

substance of concern may be greater than the sum of their individual costs. Although the manufacturers

increasingly prefer to compete (Figure 2(b)) whenKC > 2K, they may still share costs if the equilibrium

under competition is (R,D) or (D,D).

Lemma 4. If wL < w < wmax and the manufacturer replacement equilibrium under competition is

(R,D) or (D,D), then the manufacturers may prefer to share the cost to replace when KC > 2K.

When KC > 2K, cost sharing may still occur for equilibria (R,D) or (D,D) when the supplier price

is not low. For equilibrium (R,D), when the manufacturers compete, manufacturer 1 has a higher price

and a higher demand than manufacturer 2. However, by sharing costs and helping manufacturer 2 to

replace, manufacturer 1 can actually increase both his price and his demand.11 As shown in Figure

2(b), cost sharing occurs for equilibrium (R,D) when there is less benefit to deferring replacement for

manufacturer 2 (i.e., r is close to 1) and the supplier price w is high. The high w prevents manufacturer

1 from significantly using his brand advantage over manufacturer 2 to control the pricing of and

demand for the manufacturers’ products. Conversely, the r value suggests that manufacturer 2 does

not benefit much from deferring replacement. Thus, an opportunity exists for manufacturer 1 to incur

a larger portion of KC (i.e., t∗R,D = 0.64; see Table A.4 in Appendix B.1) to ensure both manufacturers

proactively replace and as a result, to better utilize his brand advantage to differentiate his product.

For equilibrium (D,D), notice in Figure 2(b) that the manufacturers share costs when the supplier

price is high but the expected regulatory risk is not sufficient to induce both manufacturers to replace.

For these cases, if manufacturer 1 is willing to incur a larger portion of the shared replacement cost to

offset manufacturer 2’s costs (i.e., t∗D,D = 0.67; see Table A.4), then both manufacturers can increase

their profits by collaborating to implement the replacement substance. Note that our findings for

11 Analytically this result can be seen by comparing manufacturer 1’s margin and demand for equilibrium (R,R) whenwL <w<w

3R,R, with his margin and demand for (R,D) when w1

R,D ≤w≤w2R,D in Theorem 1.

Authors’ names blinded for peer review20 Article submitted to Management Science; manuscript no. ()

equilibria (R,D) and (D,D) are not restricted to KC being only slightly greater than 2K. Examples

exist for both equilibria in which cost sharing occurs when KC is 25 - 50% greater than 2K.

There are a growing number of opportunities for manufacturers to work together to replace sub-

stances of concern. New regulatory initiatives, such as TSCA (Toxic Substances Control Act) reform

in the United States (Rizzuto 2013) and California’s new Safer Consumer Products Regulation (Lee

2013), as well as NGO substance of concern lists such as The SIN “Substitute It Now!” List (The SIN

List 2014) guarantee that the pressure on manufacturers to make difficult decisions regarding the use

of substances of concern in their products will continue to increase in the coming years. For example,

consumer advocacy groups have recently called for the removal of triclosan and phthalates from health

and beauty products (Coolidge 2013, Kary 2014, Koch 2013). Our results in §5 suggest that opportu-

nities exist for manufacturers to collaborate to eliminate the use of a substance of concern. In some

cases the opportunities are intuitive (e.g., a shared cost savings) but in other cases they are not (e.g.,

working together when the shared cost is greater than the sum of the manufacturers’ individual costs).

The key insight, however, is that competing on toxicity does not always make sense for manufacturers

and that collaborating to replace a substance of concern can be a viable option from both an economic

and an environmental perspective.

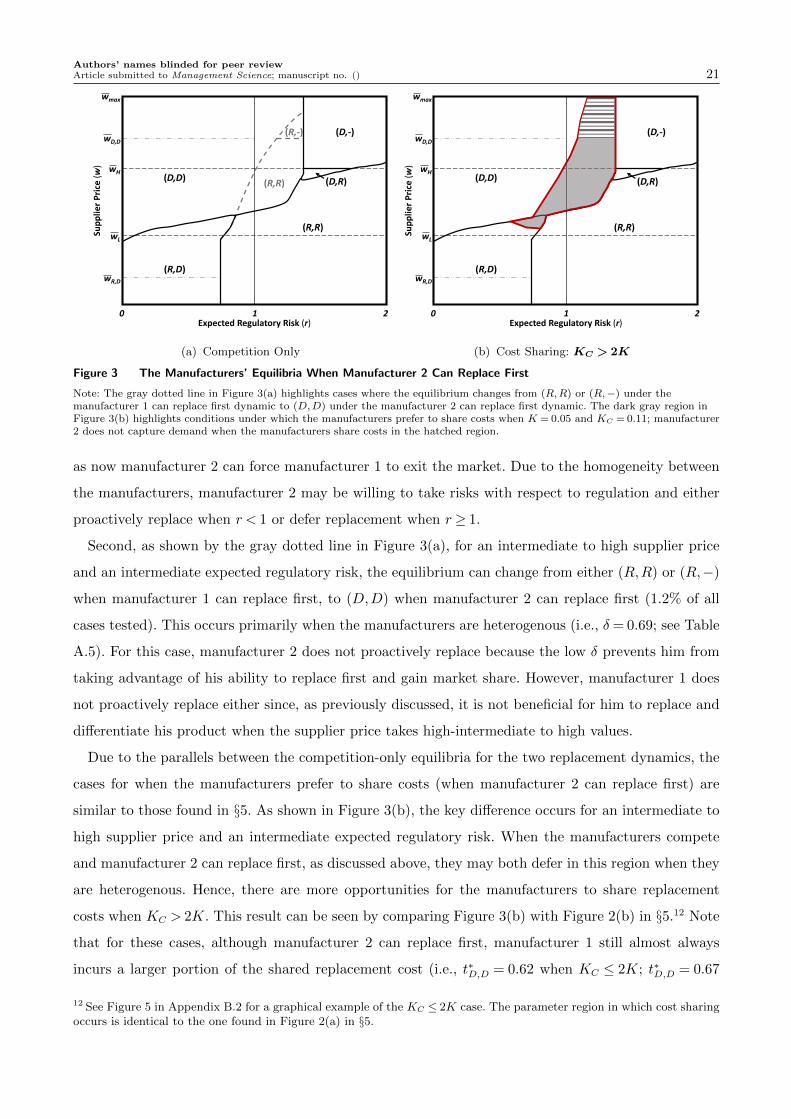

6. Extension: Manufacturer 2 Can Replace Before Manufacturer 1

In §4 and §5, the high-end manufacturer (manufacture 1) moves first in our replacement game. In

this section, we examine how the manufacturers’ strategies change when we alter the replacement

dynamic and allow the low-end manufacturer (manufacturer 2) to move first. To gain market share,

a low-end manufacturer may be willing to take risks that a brand leader would not. To model this

scenario we reverse steps 1 and 2 in the sequence of events in §3 such that now manufacturer 2 makes

his replacement decision before manufacturer 1. Our results show how the insights discussed in §4 and

§5 are robust and do not highly depend upon which manufacturer can replace first.

For the competition-only scenario, we do not find a significant difference between the manufactur-

ers’ replacement strategies under the two dynamics. Numerically, in only 10.5% of the 111,000 cases

tested did the replacement equilibrium change when manufacturer 2 can replace first. Table A.5 in

Appendix B.2 lists the most frequently occurring cases and for comparison, the conditions under which

the equilibria do not change. There are two primary cases for when a change occurs. First, when

the manufacturers are homogenous (i.e., δ = 0.99) and a cost tradeoff exists between the substance’s

expected regulatory risk and the supplier price, then a difference in equilibrium can occur as manu-

facturer 2 leverages his ability to replace first to capture all the demand in the market. For example,

when r and w are low, the equilibrium can change from (R,D)D∗2=0 when manufacturer 1 can replace

first, to (D,R)D∗1=0 when manufacturer 2 can replace first (5.6% of all cases tested). Similarly, when

r and w are both high, the equilibrium can change from (D,−) to (−,D) (2.9% of all cases tested)

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 21

Sup

plie

r P

rice

(w

)

Expected Regulatory Risk (r)10 2

wH

wL

wmax

wD,D

(R,R) (D,R)

(R,R)

(R,-) (D,-)

(D,D)

(R,D)wR,D

(a) Competition Only

Sup

plie

r P

rice

(w

)

Expected Regulatory Risk (r)10 2

wH

wL

wmax

wD,D

(D,R)

(R,R)

(D,-)

(D,D)

(R,D)wR,D

(b) Cost Sharing: KC > 2K

Figure 3 The Manufacturers’ Equilibria When Manufacturer 2 Can Replace First

Note: The gray dotted line in Figure 3(a) highlights cases where the equilibrium changes from (R,R) or (R,−) under themanufacturer 1 can replace first dynamic to (D,D) under the manufacturer 2 can replace first dynamic. The dark gray region inFigure 3(b) highlights conditions under which the manufacturers prefer to share costs when K = 0.05 and KC = 0.11; manufacturer2 does not capture demand when the manufacturers share costs in the hatched region.

as now manufacturer 2 can force manufacturer 1 to exit the market. Due to the homogeneity between

the manufacturers, manufacturer 2 may be willing to take risks with respect to regulation and either

proactively replace when r < 1 or defer replacement when r≥ 1.

Second, as shown by the gray dotted line in Figure 3(a), for an intermediate to high supplier price

and an intermediate expected regulatory risk, the equilibrium can change from either (R,R) or (R,−)

when manufacturer 1 can replace first, to (D,D) when manufacturer 2 can replace first (1.2% of all

cases tested). This occurs primarily when the manufacturers are heterogenous (i.e., δ= 0.69; see Table

A.5). For this case, manufacturer 2 does not proactively replace because the low δ prevents him from

taking advantage of his ability to replace first and gain market share. However, manufacturer 1 does

not proactively replace either since, as previously discussed, it is not beneficial for him to replace and

differentiate his product when the supplier price takes high-intermediate to high values.

Due to the parallels between the competition-only equilibria for the two replacement dynamics, the

cases for when the manufacturers prefer to share costs (when manufacturer 2 can replace first) are

similar to those found in §5. As shown in Figure 3(b), the key difference occurs for an intermediate to

high supplier price and an intermediate expected regulatory risk. When the manufacturers compete

and manufacturer 2 can replace first, as discussed above, they may both defer in this region when they

are heterogenous. Hence, there are more opportunities for the manufacturers to share replacement

costs when KC > 2K. This result can be seen by comparing Figure 3(b) with Figure 2(b) in §5.12 Note

that for these cases, although manufacturer 2 can replace first, manufacturer 1 still almost always

incurs a larger portion of the shared replacement cost (i.e., t∗D,D = 0.62 when KC ≤ 2K; t∗D,D = 0.67

12 See Figure 5 in Appendix B.2 for a graphical example of the KC ≤ 2K case. The parameter region in which cost sharingoccurs is identical to the one found in Figure 2(a) in §5.

Authors’ names blinded for peer review22 Article submitted to Management Science; manuscript no. ()

when KC > 2K). The brand difference between the two manufacturers plays a larger role than the

replacement dynamic in determining the manufacturer that incurs the larger portion of the shared

cost. See Tables A.6 and A.7 in Appendix B.2 for the complete numerical analysis.

7. Managerial Insights and Conclusion

In this paper, we examine how competition influences manufacturers’ strategic decisions when a sub-

stance of concern is identified within their products. To identify ways to increase the number of

manufacturers adopting a replacement, we examine whether manufacturers can avoid competing and

instead, share the cost to replace the substance. We study a vertically differentiated market consisting

of a high-end and a low-end manufacturer selling a product that contains a substance of concern. A

replacement substance is available, but at a higher cost. The manufacturers must decide (1) whether

to proactively replace or to defer replacement and wait to see if regulation occurs and (2) what price to

charge for their products. Our work is motivated by the reusable water bottle industry’s struggles to

replace BPA from their products and by environmentalists’ calls for firms to not compete on toxicity

but instead to collaborate to replace substances of concern. Our results provide insights for manu-

facturers decisions regarding substances of concern, and can act as a starting point for suppliers and

regulators interested in influencing the adoption of safer products by industries.

We find that when manufacturers compete on toxicity, if they do not face a cost tradeoff between

the expected regulatory risk and the supplier price for the replacement substance, then their decisions

are simplified and a symmetric equilibrium occurs in which they either both replace or both defer

replacement. If instead, they face a cost tradeoff, then the high-end manufacturer can use his brand

advantage to control the market. For example, when the expected regulatory risk and the supplier price

are low, if the high-end manufacturer is willing to proactively replace and sacrifice a potential cost

benefit to deferring replacement, then he can charge a higher price and capture more demand than the

low-end manufacturer. Conversely, when the expected regulatory risk and the supplier price are high,

the high-end manufacturer can force the low-end manufacturer to exit the market. The competition

between the manufacturers is highest when the supplier does not price the replacement in one of the

extremes but instead offers an intermediate price. Under these conditions, both manufacturers almost

always capture demand and asymmetric equilibria can occur where either the high-end or the low-end

manufacturer proactively replaces. In addition, a unique equilibrium can occur when consumers’ utility

for the replacement substance is low. Under these conditions, the low-end manufacturer proactively

replaces and is a niche-provider of a higher-priced, substance-free product, while the high-end manufac-

turer ignores his brand advantage and defers replacement to capture more demand with a lower-priced

product containing the substance of concern.

Our results also suggest that competing on toxicity does not always make sense for manufacturers

and that collaborating to replace a substance of concern can be a viable option from both an economic

Authors’ names blinded for peer reviewArticle submitted to Management Science; manuscript no. () 23

and an environmental perspective. When the shared cost to replace a substance is less than manufac-

turers’ individual replacement costs, the low-end manufacturer can use cost sharing to overcome his

brand disadvantage and capture more demand in the market. In addition, opportunities may exist for

manufacturers to collaborate to replace a substance, even when the shared cost to replace is greater than

the sum of the manufacturers’ individual replacement costs. For example, if the manufacturers’ strate-

gies are to differentiate their products with the high-end manufacturer proactively replacing, then the

high-end manufacturer can actually benefit from incurring a large portion of the shared replacement

cost to help the low-end manufacturer replace. This is even though under competition, the high-end

manufacturer can already charge a higher price and capture more demand than the low-end manufac-

turer. Helping the low-end manufacturer to replace, enables the high-end manufacturer to better use

his brand advantage to further increase both his price and his demand, resulting in higher profits.

We develop a stylized model to study the replacement of a substance of concern. In our analysis

we assume that the manufacturers’ replacement costs are symmetric. Numerically, we examine how

our insights change when the replacement costs are asymmetric, with manufacturer 2’s cost being

either less than or greater than manufacturer 1’s cost.13 To test this scenario, we set manufacturer

1’s cost K1 = K and manufacturer 2’s cost K2 = δK or 0.5K when his cost is lower; K2 = K/δ or

2K when his cost is higher. For the competition-only scenario, we do not find a significant difference

when we compare the manufacturers’ replacement strategies for symmetric and asymmetric costs. For

all four K2 costs, the replacement equilibrium changed in less than 5.0% of the 111,000 cases tested.

For the cost sharing scenario, we examine if the manufacturers share costs when KC ≤K1 +K2 and

KC > K1 +K2. Proportionally, cost sharing occurs for a similar percentage of cases as those found

in Tables 3 and A.4. The few differences occur when the asymmetric costs make it difficult to find a

mutually profitable division of KC , and thus, less cost sharing occurs. For example, for equilibrium