Embed Size (px)

Citation preview

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved1

Professor Arun SharmaUniversity of Miami

Compliance as a Strategic Function

©Arun Sharma, All Rights Reserved2

Goals ‐ Background

Compliance leaders need expertise in three areas: – Compliance expertise which incorporates skills such as risk management, policy development, regulatory knowledge, investigation and monitoring/auditing.• Compliance leaders have strong competencies in this area.

– Leadership expertise with skills associated with leading and motivating compliance teams. • Compliance leaders are beginning to develop deep expertise in this area.

– Strategic expertise and skills required to give flight to the business and elevate the role of the compliance function within pharmaceutical firms. • Focus of the Session.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved3

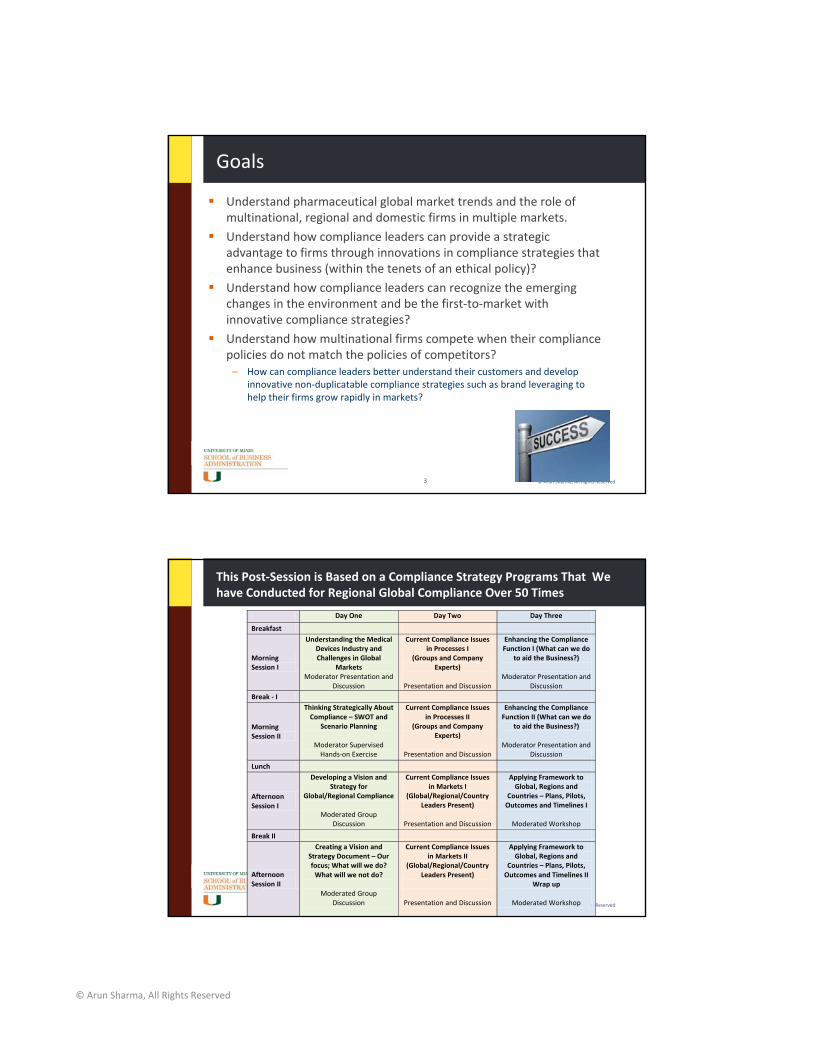

Goals

Understand pharmaceutical global market trends and the role of multinational, regional and domestic firms in multiple markets.

Understand how compliance leaders can provide a strategic advantage to firms through innovations in compliance strategies that enhance business (within the tenets of an ethical policy)?Understand how compliance leaders can recognize the emerging changes in the environment and be the first‐to‐market with innovative compliance strategies?

Understand how multinational firms compete when their compliancepolicies do not match the policies of competitors? – How can compliance leaders better understand their customers and develop

innovative non‐duplicatable compliance strategies such as brand leveraging to help their firms grow rapidly in markets?

©Arun Sharma, All Rights Reserved4

Day One Day Two Day Three

Breakfast

Morning Session I

Understanding the Medical Devices Industry and Challenges in Global

Markets Moderator Presentation and

Discussion

Current Compliance Issues in Processes I

(Groups and Company Experts)

Presentation and Discussion

Enhancing the Compliance Function I (What can we do

to aid the Business?)

Moderator Presentation and Discussion

Break ‐ I

Morning Session II

Thinking Strategically About Compliance – SWOT and

Scenario Planning

Moderator Supervised Hands‐on Exercise

Current Compliance Issues in Processes II

(Groups and Company Experts)

Presentation and Discussion

Enhancing the Compliance Function II (What can we do

to aid the Business?)

Moderator Presentation and Discussion

Lunch

Afternoon Session I

Developing a Vision and Strategy for

Global/Regional Compliance

Moderated Group Discussion

Current Compliance Issues in Markets I

(Global/Regional/Country Leaders Present)

Presentation and Discussion

Applying Framework to Global, Regions and

Countries – Plans, Pilots, Outcomes and Timelines I

Moderated Workshop

Break II

Afternoon Session II

Creating a Vision and Strategy Document – Our focus; What will we do? What will we not do?

Moderated Group

Discussion

Current Compliance Issues in Markets II

(Global/Regional/Country Leaders Present)

Presentation and Discussion

Applying Framework to Global, Regions and

Countries – Plans, Pilots, Outcomes and Timelines II

Wrap up

Moderated Workshop

This Post‐Session is Based on a Compliance Strategy Programs That We have Conducted for Regional Global Compliance Over 50 Times

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved5

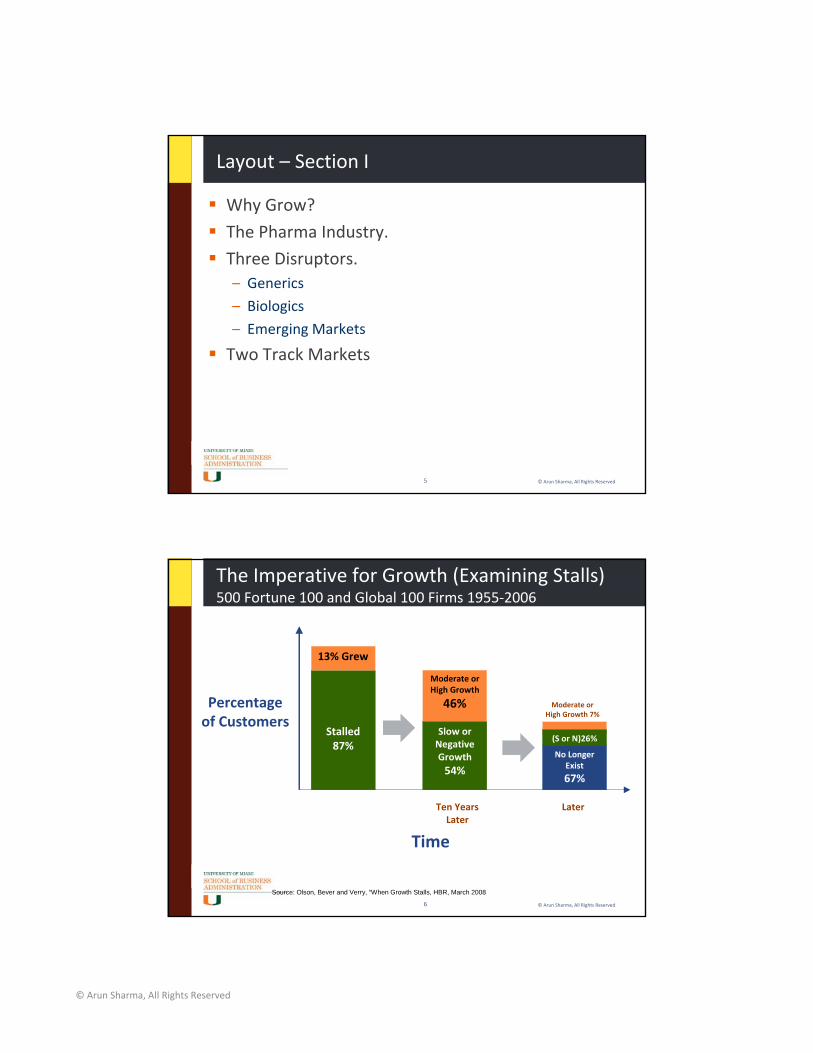

Layout – Section I

Why Grow?

The Pharma Industry.

Three Disruptors.– Generics

– Biologics

– Emerging Markets

Two Track Markets

©Arun Sharma, All Rights Reserved6

The Imperative for Growth (Examining Stalls)500 Fortune 100 and Global 100 Firms 1955‐2006

(S or N)26%

Percentage of Customers

Time

Moderate or High Growth

46%

Stalled87%

Later

Slow or Negative Growth 54%

13% Grew

No Longer Exist

67%

Moderate or High Growth 7%

Ten YearsLater

Source: Olson, Bever and Verry, “When Growth Stalls, HBR, March 2008

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved7

How do We Study Markets?

Understand Market Strategy Models.

What are the Fundamental Shifts in the Industry.– Change in Values.

Who are the Key Competitors?

Who are the Winners and Losers?

Is There is a Pending Crisis in the Industry?

What Are the Wild Cards?

Use Patterns to Predict Future.

©Arun Sharma, All Rights Reserved8

MARKET STRATEGY MODELS FOR THE PHARMACEUTICAL INDUSTRY

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved9

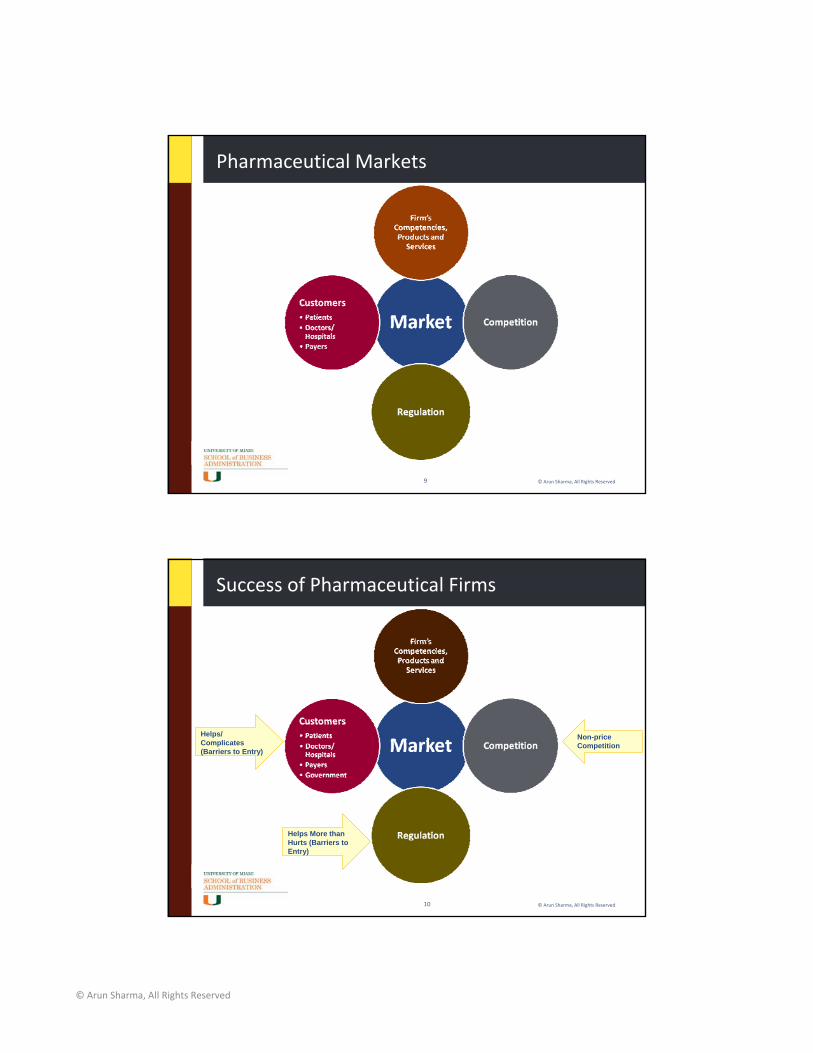

Pharmaceutical Markets

©Arun Sharma, All Rights Reserved10

Success of Pharmaceutical Firms

Helps More than Hurts (Barriers to Entry)

Helps/ Complicates (Barriers to Entry)

Non-price Competition

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved11

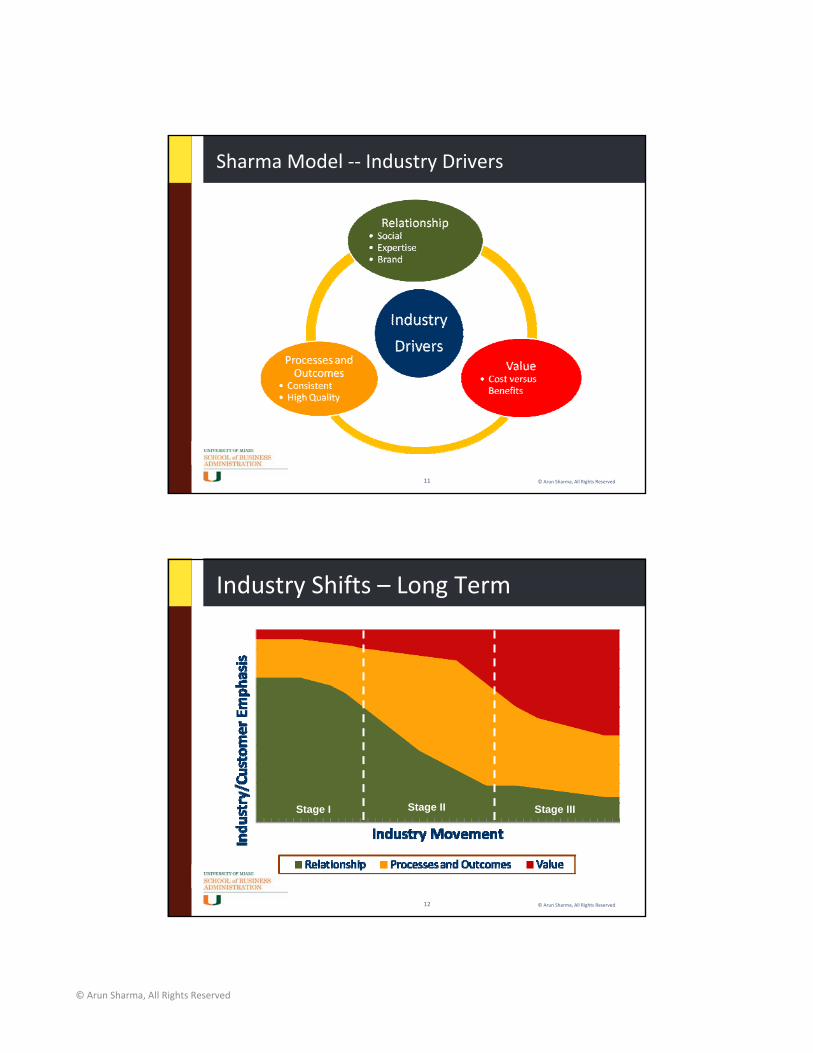

Sharma Model ‐‐ Industry Drivers

©Arun Sharma, All Rights Reserved12

Industry Shifts – Long Term

Stage IIIStage IIStage I

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved13

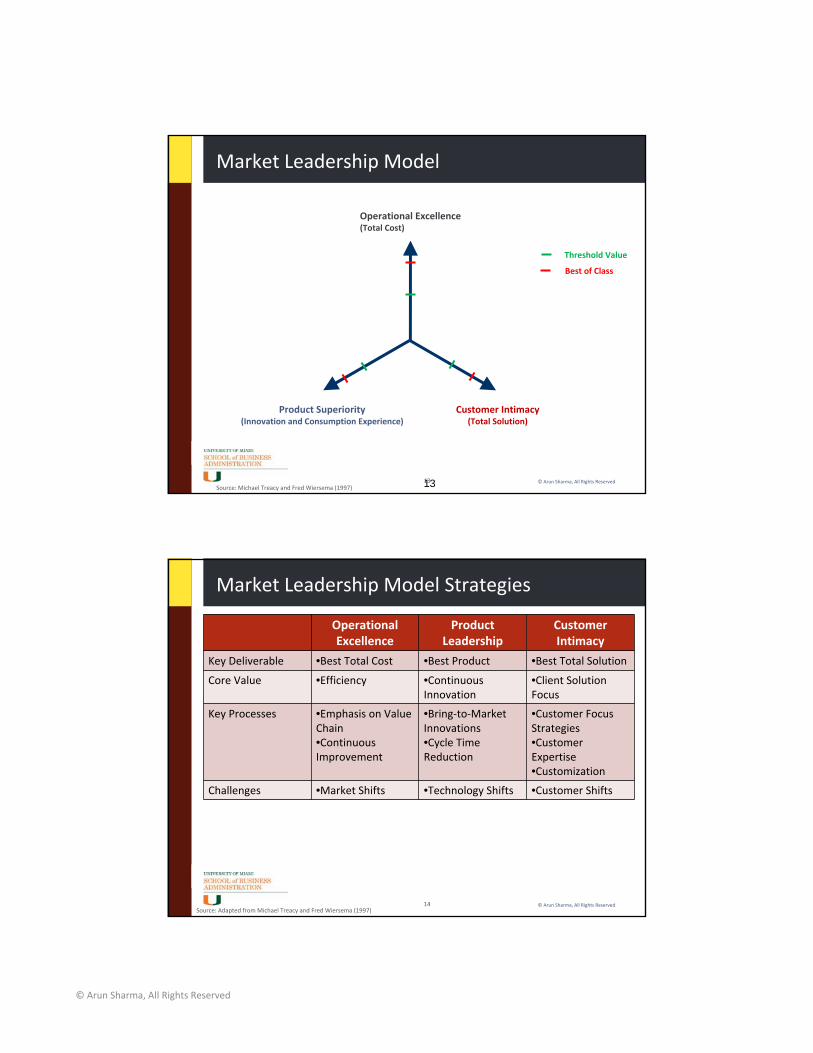

Market Leadership Model

13

Best of Class

Threshold Value

Customer Intimacy(Total Solution)

Operational Excellence(Total Cost)

Source: Michael Treacy and Fred Wiersema (1997)

Product Superiority(Innovation and Consumption Experience)

©Arun Sharma, All Rights Reserved14

Market Leadership Model Strategies

Operational Excellence

Product Leadership

Customer Intimacy

Key Deliverable •Best Total Cost •Best Product •Best Total SolutionCore Value •Efficiency •Continuous

Innovation•Client Solution Focus

Key Processes •Emphasis on Value Chain•Continuous Improvement

•Bring‐to‐Market Innovations•Cycle Time Reduction

•Customer Focus Strategies•Customer Expertise•Customization

Challenges •Market Shifts •Technology Shifts •Customer Shifts

Source: Adapted from Michael Treacy and Fred Wiersema (1997)

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved15

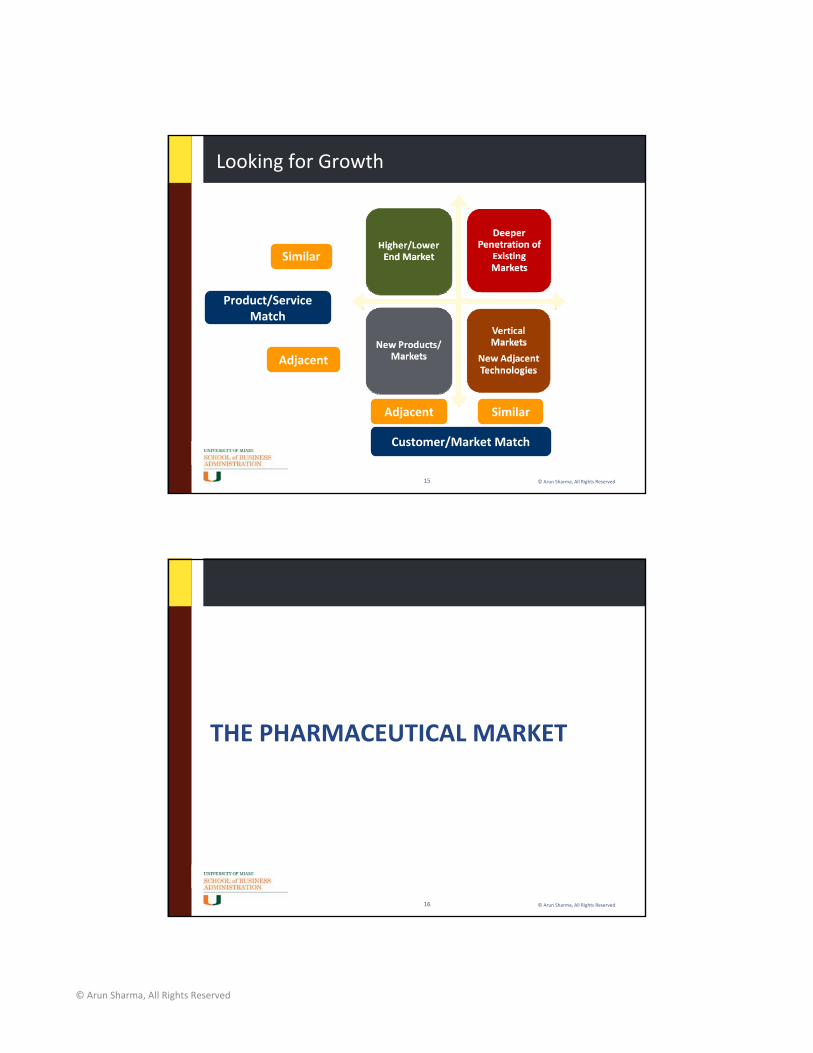

Looking for Growth

Customer/Market Match

Adjacent Similar

Product/Service Match

Adjacent

Similar

©Arun Sharma, All Rights Reserved16

THE PHARMACEUTICAL MARKET

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved17

Our Study of Industry and Trends

In 2013 more firms are missing their growth targets when compared to the last decade.

Concerns about the effectiveness of current market strategies have increased.

The Pharma business has nineteen Big Pharma firms and over 200 smaller firms.

– As long as reimbursements were high (gross margin for this industry was over 80%), there was little need for industry consolidation.

– The industry is under attack from the bottom (generic drugs) and the top (too many similar medicines).

– Emerging Market Firms are Growing.

©Arun Sharma, All Rights Reserved18

Industry Trends

2011 sales expected to be $900 Billion; 2015 ‐‐ $1 Trillion; 2020 ‐‐ $1.15 Trillion. – Slowest growth in 20 years.

– Emerging Markets will provide 75% of Growth in 2012‐2020.

Major Shifts in Developed Markets.– Reduction in Pricing in Developed Countries.

Generics have Grown in All markets.– Generics will be 85% of the Growth.

Innovation Cycle is Deeply Disrupted.– Some Developed Markets May Have negative Growth.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved19

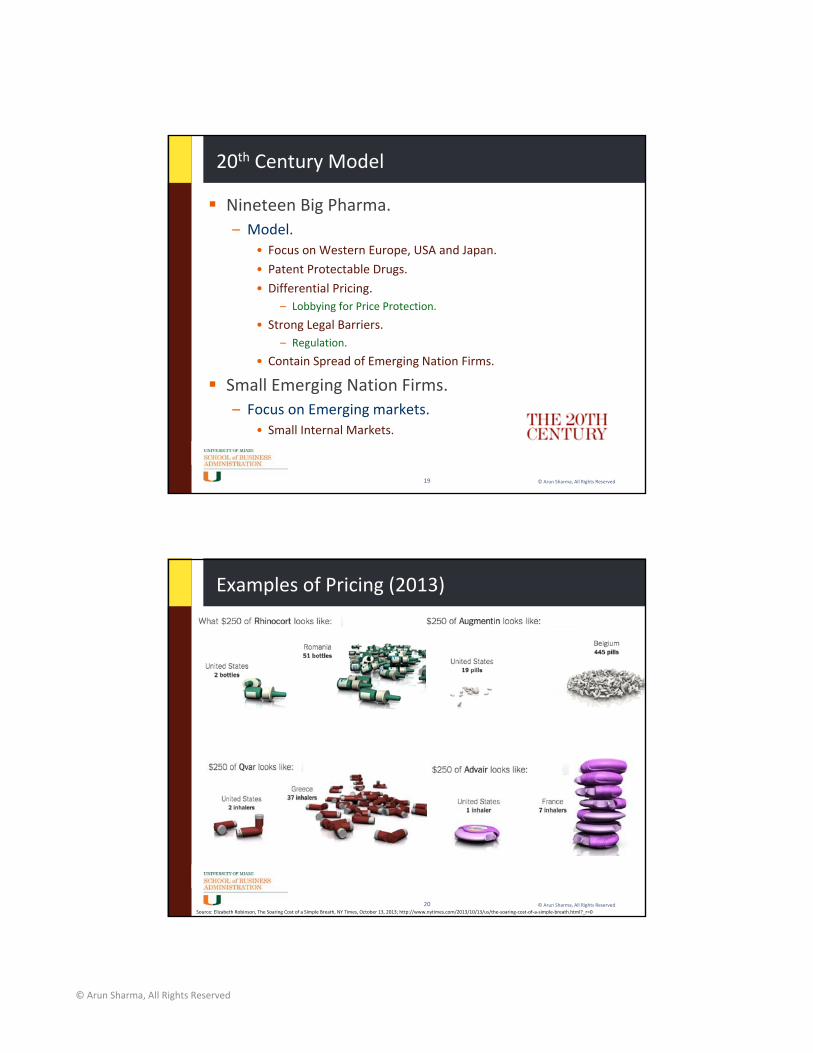

20th Century Model

Nineteen Big Pharma.– Model.

• Focus on Western Europe, USA and Japan.• Patent Protectable Drugs.

• Differential Pricing.– Lobbying for Price Protection.

• Strong Legal Barriers.– Regulation.

• Contain Spread of Emerging Nation Firms.

Small Emerging Nation Firms.– Focus on Emerging markets.

• Small Internal Markets.

©Arun Sharma, All Rights Reserved20

Examples of Pricing (2013)

Source: Elizabeth Robinson, The Soaring Cost of a Simple Breath, NY Times, October 13, 2013; http://www.nytimes.com/2013/10/13/us/the‐soaring‐cost‐of‐a‐simple‐breath.html?_r=0

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved21

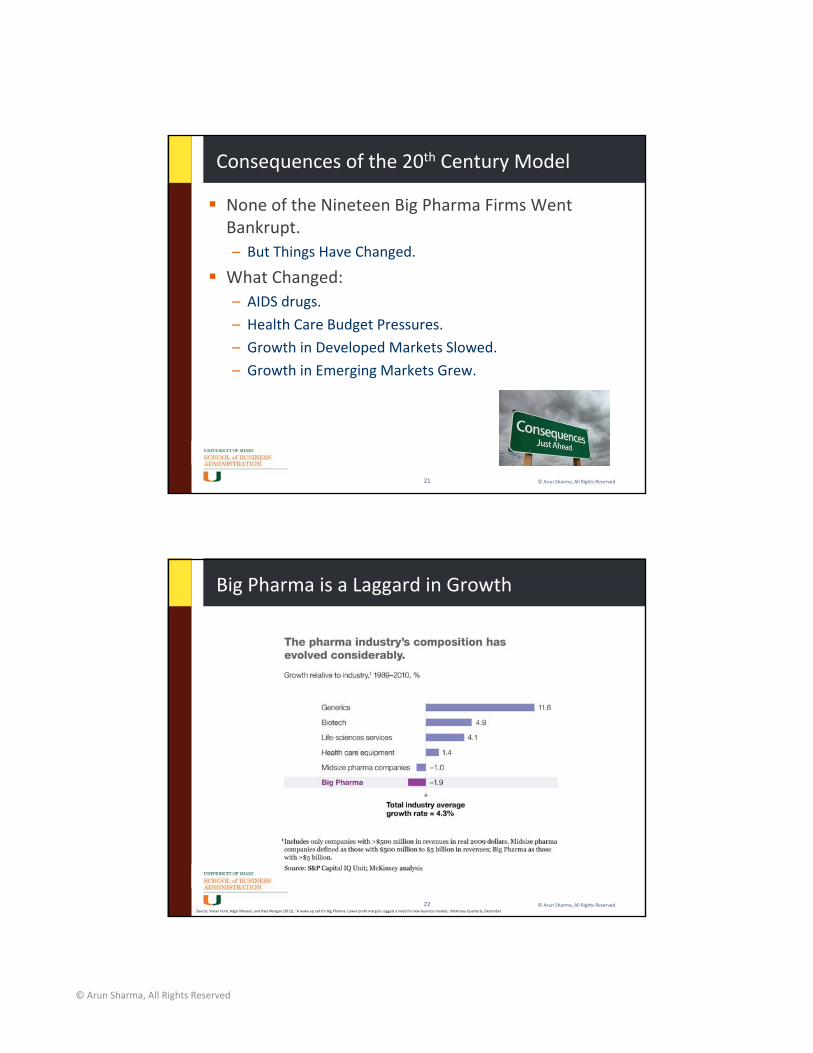

Consequences of the 20th Century Model

None of the Nineteen Big Pharma Firms Went Bankrupt.– But Things Have Changed.

What Changed:– AIDS drugs.

– Health Care Budget Pressures.

– Growth in Developed Markets Slowed.

– Growth in Emerging Markets Grew.

©Arun Sharma, All Rights Reserved22

Big Pharma is a Laggard in Growth

Source: Vivian Hunt, Nigel Manson, and Paul Morgan (2011), "A wake‐up call for Big Pharma: Lower profit margins suggest a need for new business models,: McKinsey Quarterly, December.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved23

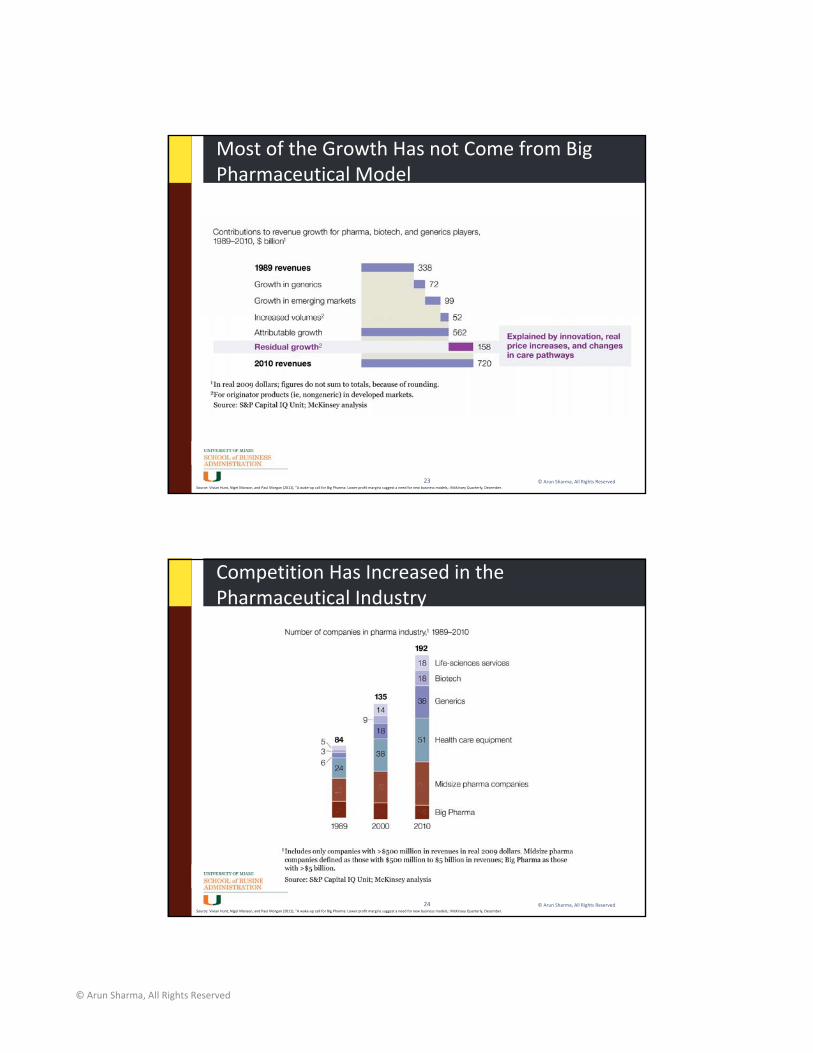

Most of the Growth Has not Come from Big Pharmaceutical Model

Source: Vivian Hunt, Nigel Manson, and Paul Morgan (2011), "A wake‐up call for Big Pharma: Lower profit margins suggest a need for new business models,: McKinsey Quarterly, December.

© Arun Sharma, All Rights Reserved24

Competition Has Increased in the Pharmaceutical Industry

Source: Vivian Hunt, Nigel Manson, and Paul Morgan (2011), "A wake‐up call for Big Pharma: Lower profit margins suggest a need for new business models,: McKinsey Quarterly, December.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved25

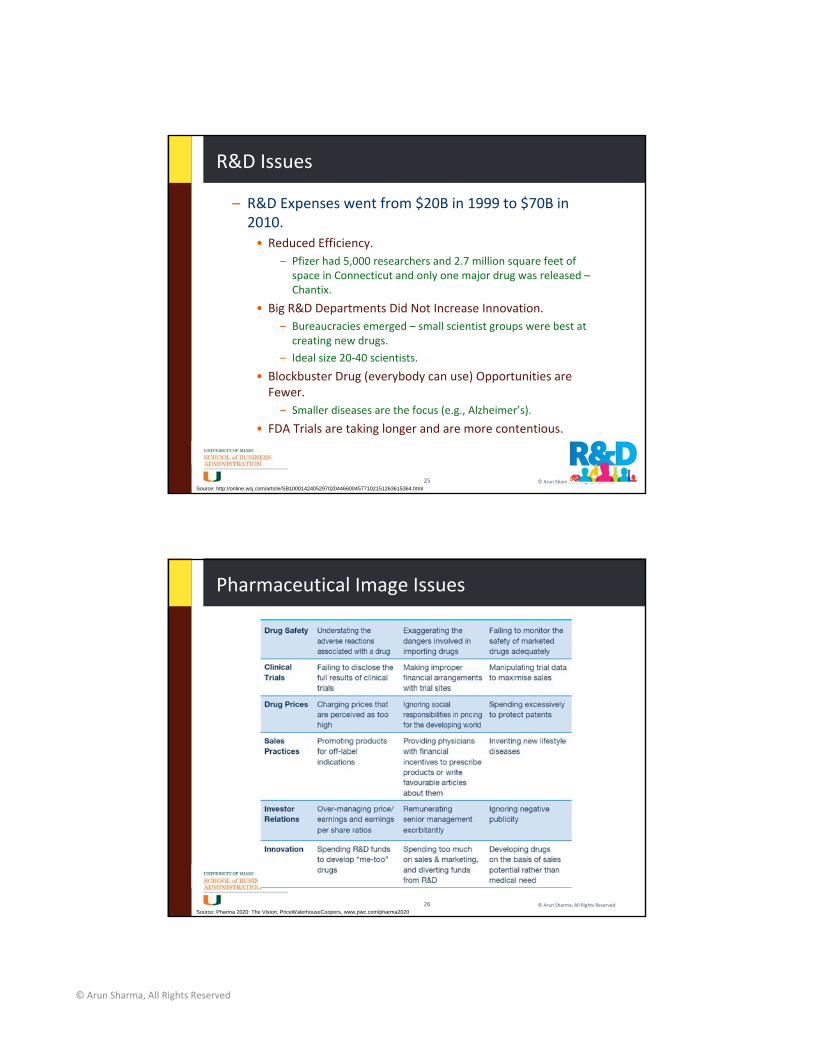

R&D Issues

– R&D Expenses went from $20B in 1999 to $70B in 2010.• Reduced Efficiency.

– Pfizer had 5,000 researchers and 2.7 million square feet of space in Connecticut and only one major drug was released –Chantix.

• Big R&D Departments Did Not Increase Innovation.– Bureaucracies emerged – small scientist groups were best at creating new drugs.

– Ideal size 20‐40 scientists.

• Blockbuster Drug (everybody can use) Opportunities are Fewer.– Smaller diseases are the focus (e.g., Alzheimer’s).

• FDA Trials are taking longer and are more contentious.

Source: http://online.wsj.com/article/SB10001424052970204466004577102151263615364.html

©Arun Sharma, All Rights Reserved26

Pharmaceutical Image Issues

Source: Pharma 2020: The Vision; PriceWaterhouseCoopers, www.pwc.com/pharma2020

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved27

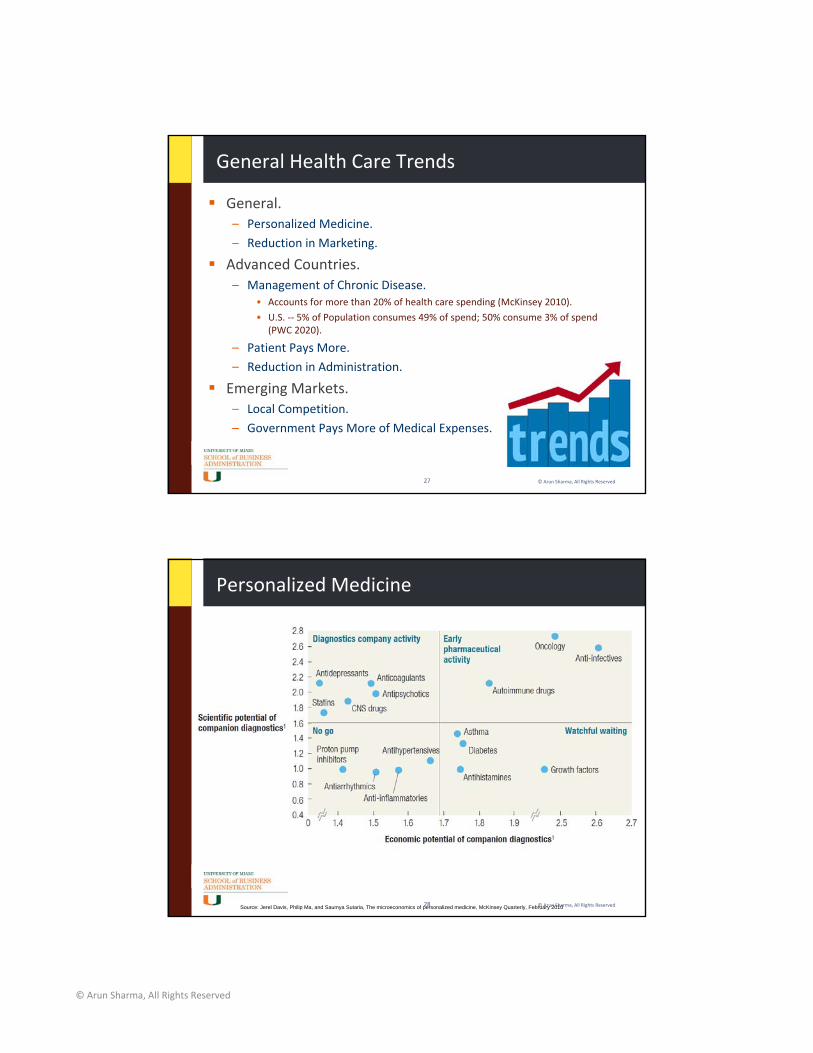

General Health Care Trends

General.– Personalized Medicine.

– Reduction in Marketing.

Advanced Countries.– Management of Chronic Disease.

• Accounts for more than 20% of health care spending (McKinsey 2010).

• U.S. ‐‐ 5% of Population consumes 49% of spend; 50% consume 3% of spend(PWC 2020).

– Patient Pays More.

– Reduction in Administration.

Emerging Markets.– Local Competition.

– Government Pays More of Medical Expenses.

©Arun Sharma, All Rights Reserved28

Personalized Medicine

Source: Jerel Davis, Philip Ma, and Saumya Sutaria, The microeconomics of personalized medicine, McKinsey Quarterly, February 2010

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved29

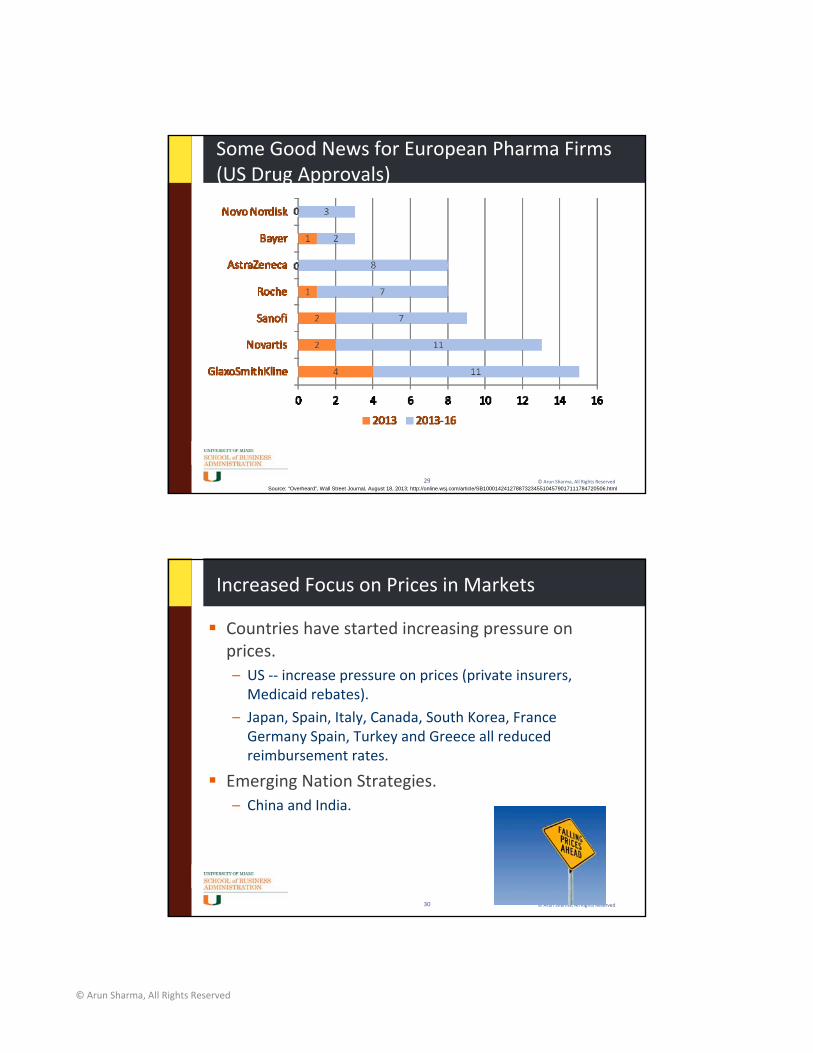

Some Good News for European Pharma Firms(US Drug Approvals)

Source: “Overheard”, Wall Street Journal, August 18, 2013; http://online.wsj.com/article/SB10001424127887323455104579017111784720506.html

©Arun Sharma, All Rights Reserved30

Increased Focus on Prices in Markets

Countries have started increasing pressure on prices.– US ‐‐ increase pressure on prices (private insurers, Medicaid rebates).

– Japan, Spain, Italy, Canada, South Korea, France Germany Spain, Turkey and Greece all reduced reimbursement rates.

Emerging Nation Strategies.– China and India.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved31

GENERICS

©Arun Sharma, All Rights Reserved32

Generic Market

Will Drive the Pharmaceutical Market.

Will Grow from $120 Billion in 2012 to $180 Billion in 2018.– 90% of the growth will come from Emerging Markets.

– From 37% of market share, developed countries will drop to 30% of world market share.

Source: Francisco Ballester, Sandoz

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved33

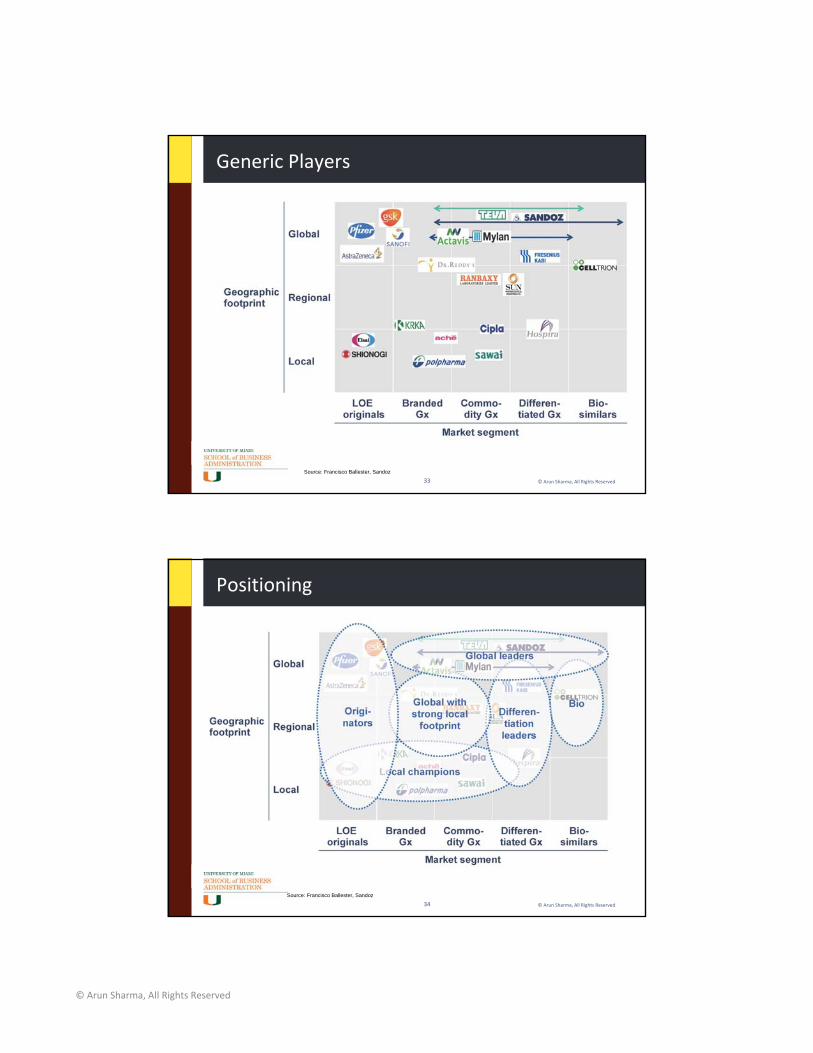

Generic Players

Source: Francisco Ballester, Sandoz

©Arun Sharma, All Rights Reserved34

Positioning

Source: Francisco Ballester, Sandoz

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved35

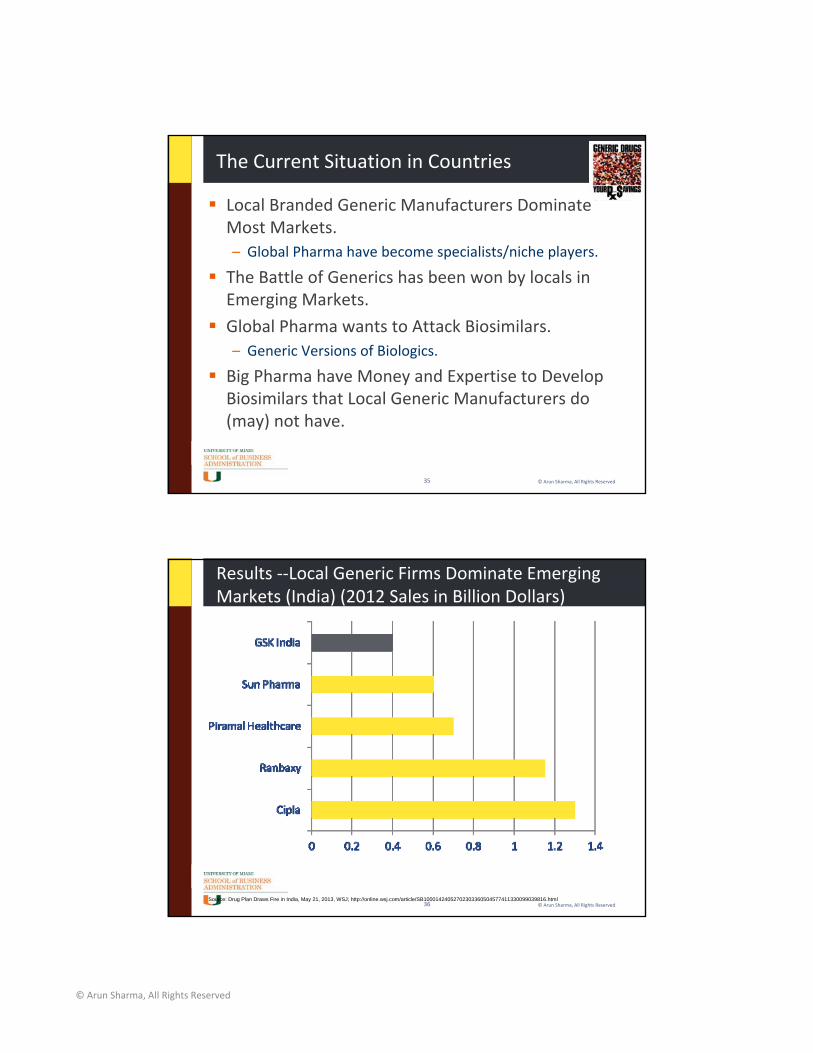

The Current Situation in Countries

Local Branded Generic Manufacturers Dominate Most Markets.– Global Pharma have become specialists/niche players.

The Battle of Generics has been won by locals in Emerging Markets.

Global Pharma wants to Attack Biosimilars.– Generic Versions of Biologics.

Big Pharma have Money and Expertise to Develop Biosimilars that Local Generic Manufacturers do (may) not have.

©Arun Sharma, All Rights Reserved36

Results ‐‐Local Generic Firms Dominate Emerging Markets (India) (2012 Sales in Billion Dollars)

Source: Drug Plan Draws Fire in India, May 21, 2013, WSJ; http://online.wsj.com/article/SB10001424052702303360504577411330099039816.html

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved37

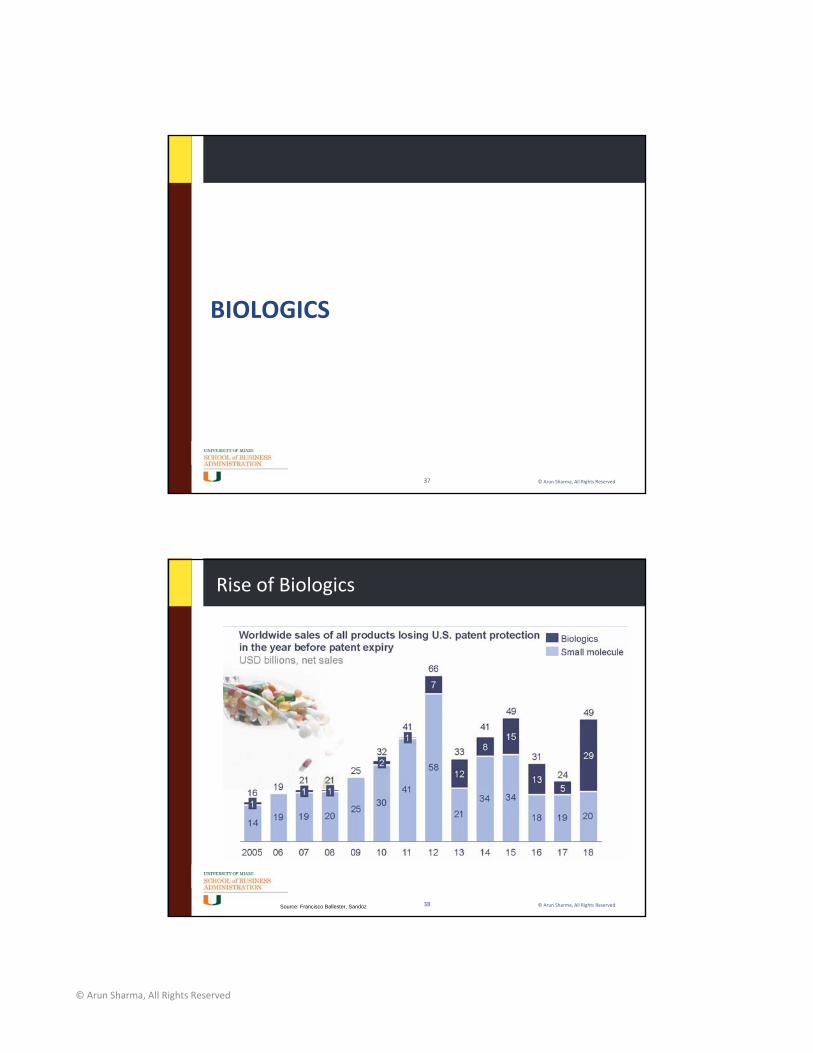

BIOLOGICS

©Arun Sharma, All Rights Reserved38

Rise of Biologics

Source: Francisco Ballester, Sandoz

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved39

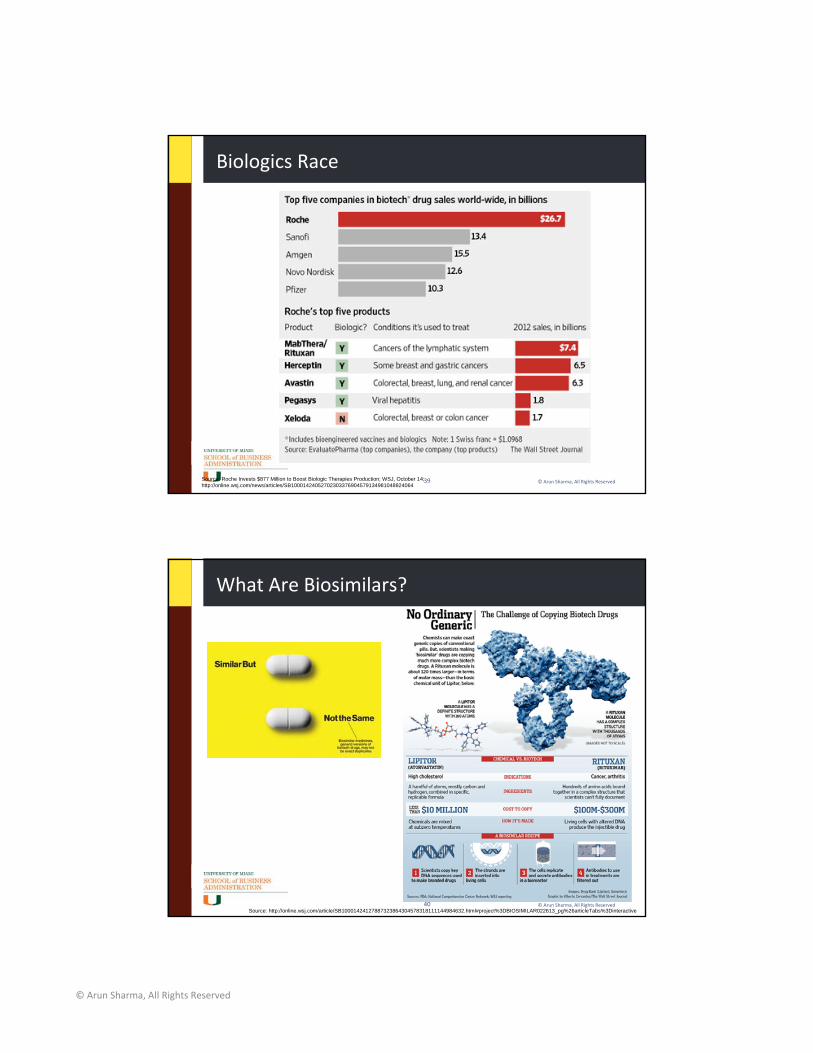

Biologics Race

Source: Roche Invests $877 Million to Boost Biologic Therapies Production; WSJ, October 14; http://online.wsj.com/news/articles/SB10001424052702303376904579134981048824064

©Arun Sharma, All Rights Reserved40

What Are Biosimilars?

Source: http://online.wsj.com/article/SB10001424127887323864304578318111144984632.html#project%3DBIOSIMILAR022613_pg%26articleTabs%3Dinteractive

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved41

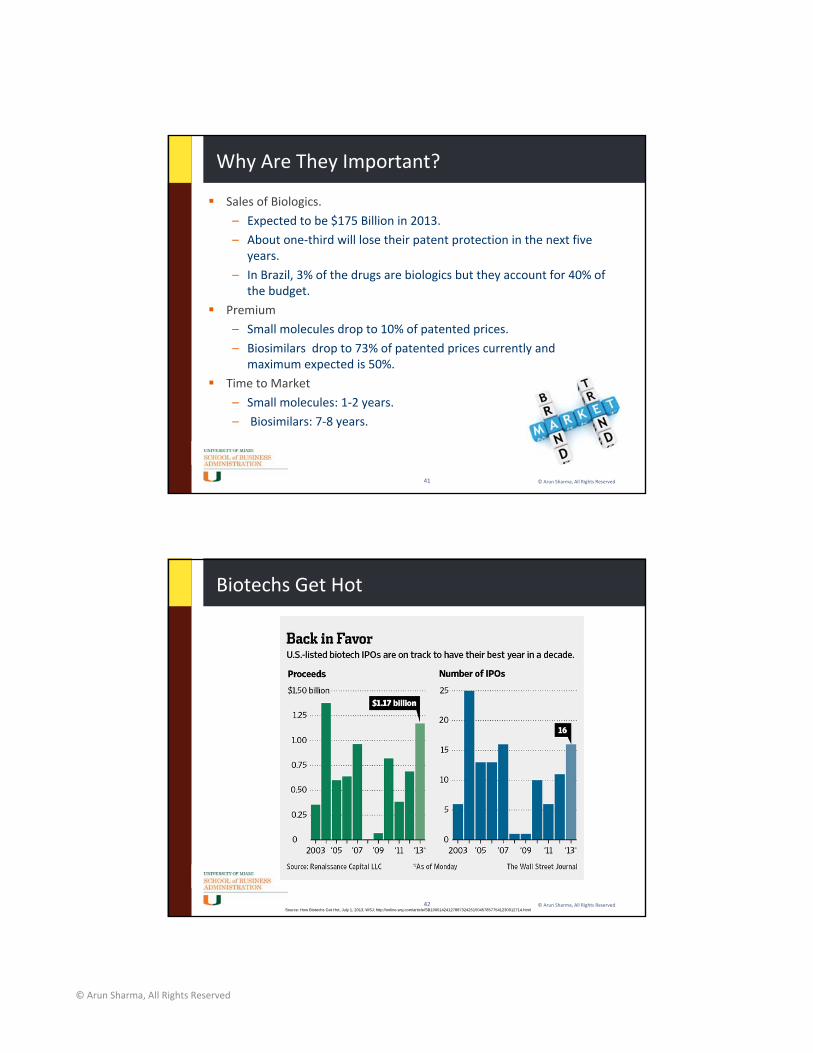

Why Are They Important?

Sales of Biologics.

– Expected to be $175 Billion in 2013.– About one‐third will lose their patent protection in the next five

years.

– In Brazil, 3% of the drugs are biologics but they account for 40% of the budget.

Premium– Small molecules drop to 10% of patented prices.

– Biosimilars drop to 73% of patented prices currently and maximum expected is 50%.

Time to Market

– Small molecules: 1‐2 years.– Biosimilars: 7‐8 years.

©Arun Sharma, All Rights Reserved42

Biotechs Get Hot

Source: How Biotechs Got Hot, July 1, 2013, WSJ; http://online.wsj.com/article/SB10001424127887324251504578577541230012714.html

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved43

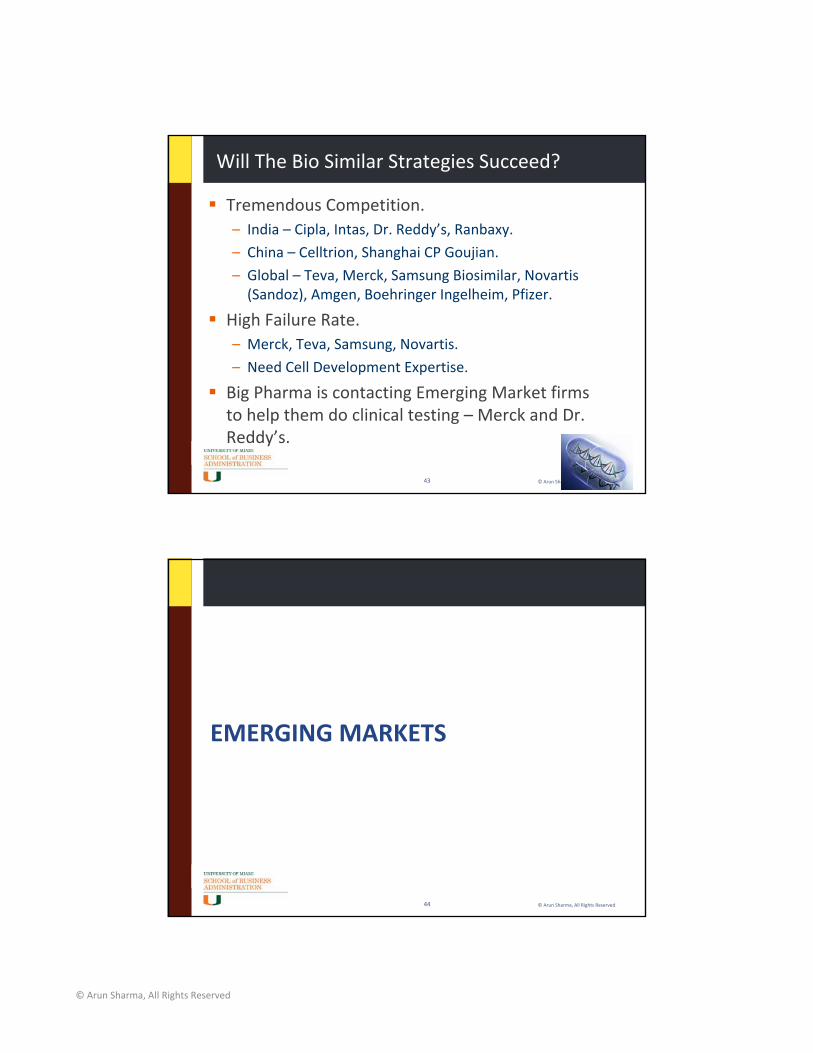

Will The Bio Similar Strategies Succeed?

Tremendous Competition.– India – Cipla, Intas, Dr. Reddy’s, Ranbaxy.

– China – Celltrion, Shanghai CP Goujian.

– Global – Teva, Merck, Samsung Biosimilar, Novartis (Sandoz), Amgen, Boehringer Ingelheim, Pfizer.

High Failure Rate.– Merck, Teva, Samsung, Novartis.

– Need Cell Development Expertise.

Big Pharma is contacting Emerging Market firms to help them do clinical testing – Merck and Dr. Reddy’s.

©Arun Sharma, All Rights Reserved44

EMERGING MARKETS

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved45

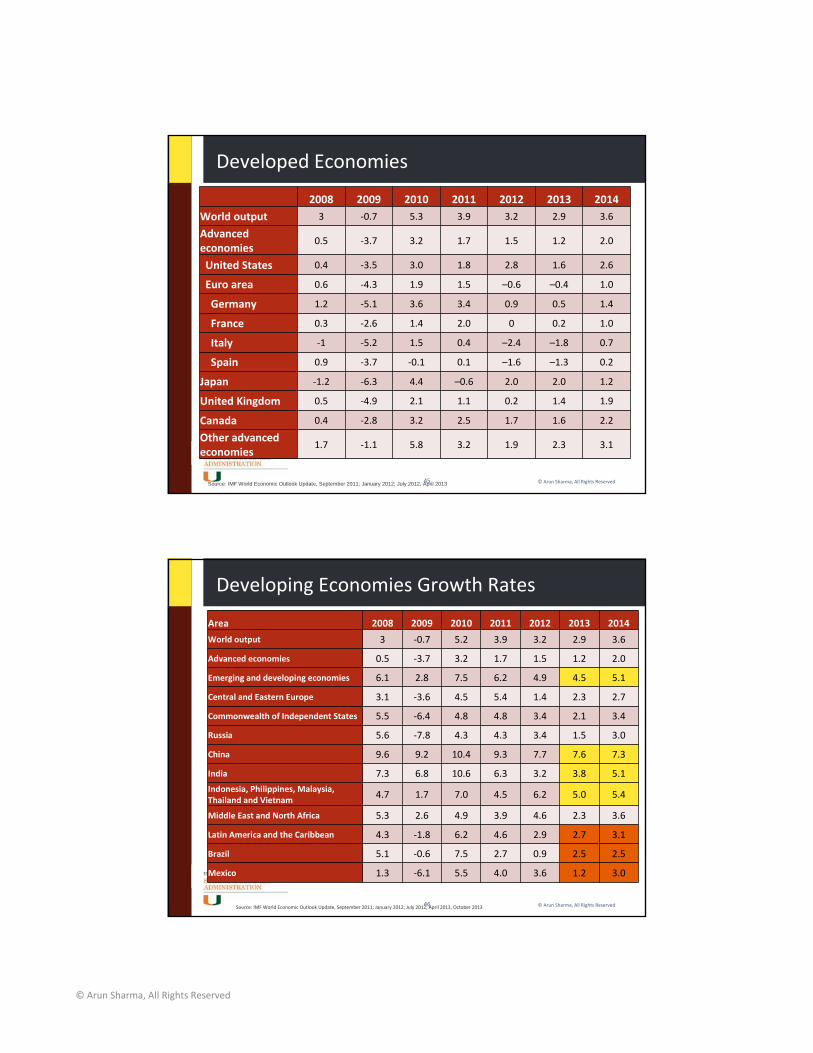

Developed Economies

2008 2009 2010 2011 2012 2013 2014World output 3 ‐0.7 5.3 3.9 3.2 2.9 3.6

Advanced economies

0.5 ‐3.7 3.2 1.7 1.5 1.2 2.0

United States 0.4 ‐3.5 3.0 1.8 2.8 1.6 2.6

Euro area 0.6 ‐4.3 1.9 1.5 –0.6 –0.4 1.0

Germany 1.2 ‐5.1 3.6 3.4 0.9 0.5 1.4

France 0.3 ‐2.6 1.4 2.0 0 0.2 1.0

Italy ‐1 ‐5.2 1.5 0.4 –2.4 –1.8 0.7

Spain 0.9 ‐3.7 ‐0.1 0.1 –1.6 –1.3 0.2

Japan ‐1.2 ‐6.3 4.4 –0.6 2.0 2.0 1.2

United Kingdom 0.5 ‐4.9 2.1 1.1 0.2 1.4 1.9

Canada 0.4 ‐2.8 3.2 2.5 1.7 1.6 2.2

Other advanced economies

1.7 ‐1.1 5.8 3.2 1.9 2.3 3.1

Source: IMF World Economic Outlook Update, September 2011; January 2012; July 2012, April 2013

©Arun Sharma, All Rights Reserved46

Developing Economies Growth Rates

Area 2008 2009 2010 2011 2012 2013 2014

World output 3 ‐0.7 5.2 3.9 3.2 2.9 3.6

Advanced economies 0.5 ‐3.7 3.2 1.7 1.5 1.2 2.0

Emerging and developing economies 6.1 2.8 7.5 6.2 4.9 4.5 5.1

Central and Eastern Europe 3.1 ‐3.6 4.5 5.4 1.4 2.3 2.7

Commonwealth of Independent States 5.5 ‐6.4 4.8 4.8 3.4 2.1 3.4

Russia 5.6 ‐7.8 4.3 4.3 3.4 1.5 3.0

China 9.6 9.2 10.4 9.3 7.7 7.6 7.3

India 7.3 6.8 10.6 6.3 3.2 3.8 5.1Indonesia, Philippines, Malaysia, Thailand and Vietnam 4.7 1.7 7.0 4.5 6.2 5.0 5.4

Middle East and North Africa 5.3 2.6 4.9 3.9 4.6 2.3 3.6

Latin America and the Caribbean 4.3 ‐1.8 6.2 4.6 2.9 2.7 3.1

Brazil 5.1 ‐0.6 7.5 2.7 0.9 2.5 2.5

Mexico 1.3 ‐6.1 5.5 4.0 3.6 1.2 3.0

Source: IMF World Economic Outlook Update, September 2011; January 2012; July 2012, April 2013, October 2013

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved47

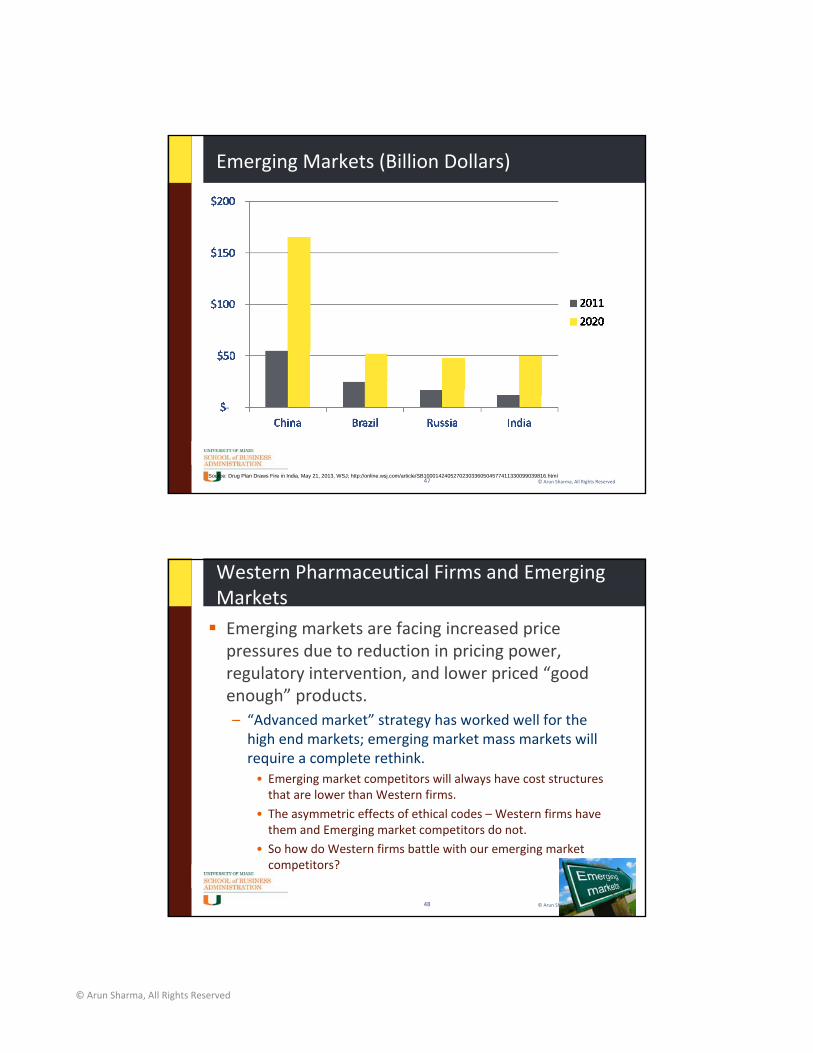

Emerging Markets (Billion Dollars)

Source: Drug Plan Draws Fire in India, May 21, 2013, WSJ; http://online.wsj.com/article/SB10001424052702303360504577411330099039816.html

©Arun Sharma, All Rights Reserved48

Western Pharmaceutical Firms and Emerging MarketsEmerging markets are facing increased price pressures due to reduction in pricing power, regulatory intervention, and lower priced “good enough” products. – “Advanced market” strategy has worked well for the high end markets; emerging market mass markets will require a complete rethink. • Emerging market competitors will always have cost structures that are lower than Western firms.

• The asymmetric effects of ethical codes – Western firms have them and Emerging market competitors do not.

• So how do Western firms battle with our emerging market competitors?

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved49

How Did Western Firms Compete in Emerging Markets?Followed Advanced Country Model.– Attempted to Enforce Patent Laws.

– Multinationals Buy Local Firms.• Sanofi‐Aventis buys Medley (Brazil).

– Pfizer buys 40% of Teuto (Brazil).

• Daiichi Sankyo buys Ranbaxy Labs (India).

• Abbott Buys Piramal in India.

– Multinationals Use Local Firms as R&D partners.• Lilly uses Jubiliant and Piramal (India) for faster R&D.

Problems of Growth – Market Mismatch.– Different markets ‐‐ different needs.

©Arun Sharma, All Rights Reserved50

China

China investigates baby formula firms for pricing violations in 2013.– Nestlé SA, Danone SA, Royal FrieslandCampina NV, Abbott Laboratories and Mead Johnson Nutrition.

– All firms under investigation reduce baby formula prices.

Other Industries– Pharma, Medical Devices, TVs, Automobiles.

Source: China Investigates Foreign Makers of Baby Formula, July 2, 2013, WSJ; http://online.wsj.com/article/SB10001424127887323297504578580920868011296.html; http://online.wsj.com/article/SB10001424127887323455104579012543957866998.html

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved51

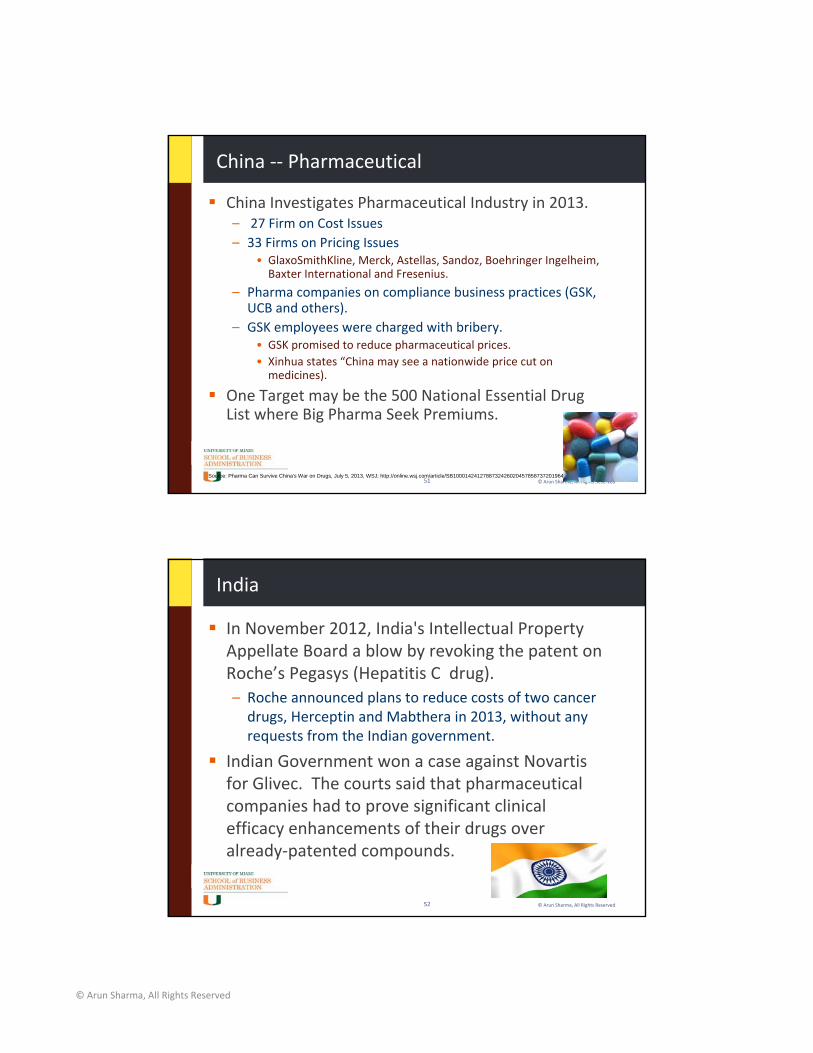

China ‐‐ Pharmaceutical

China Investigates Pharmaceutical Industry in 2013.– 27 Firm on Cost Issues– 33 Firms on Pricing Issues

• GlaxoSmithKline, Merck, Astellas, Sandoz, Boehringer Ingelheim, Baxter International and Fresenius.

– Pharma companies on compliance business practices (GSK, UCB and others).

– GSK employees were charged with bribery. • GSK promised to reduce pharmaceutical prices.• Xinhua states “China may see a nationwide price cut on medicines).

One Target may be the 500 National Essential Drug List where Big Pharma Seek Premiums.

Source: Pharma Can Survive China's War on Drugs, July 5, 2013, WSJ; http://online.wsj.com/article/SB10001424127887324260204578587372019648796.html

©Arun Sharma, All Rights Reserved52

India

In November 2012, India's Intellectual Property Appellate Board a blow by revoking the patent on Roche’s Pegasys (Hepatitis C drug).– Roche announced plans to reduce costs of two cancer drugs, Herceptin and Mabthera in 2013, without any requests from the Indian government.

Indian Government won a case against Novartis for Glivec. The courts said that pharmaceutical companies had to prove significant clinical efficacy enhancements of their drugs over already‐patented compounds.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved53

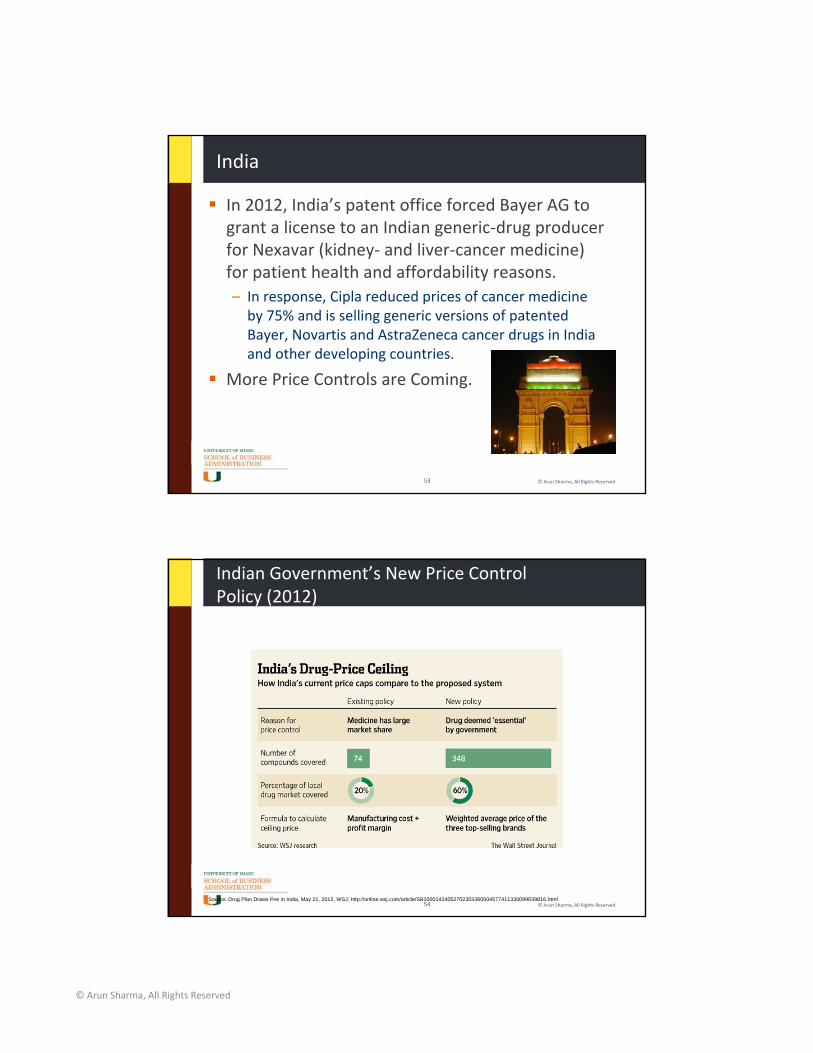

India

In 2012, India’s patent office forced Bayer AG to grant a license to an Indian generic‐drug producer for Nexavar (kidney‐ and liver‐cancer medicine) for patient health and affordability reasons. – In response, Cipla reduced prices of cancer medicine by 75% and is selling generic versions of patented Bayer, Novartis and AstraZeneca cancer drugs in India and other developing countries.

More Price Controls are Coming.

©Arun Sharma, All Rights Reserved54

Indian Government’s New Price Control Policy (2012)

Source: Drug Plan Draws Fire in India, May 21, 2012, WSJ; http://online.wsj.com/article/SB10001424052702303360504577411330099039816.html

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved55

Implication from China and India

Traditionally, firms would withdraw drugs from the emerging market when faced with regulatory price pressures. The actions of firms suggest that emerging markets are too large to ignore and firms are willing to reduce prices dramatically.

Local firms are willing to create generic versions of pharmaceuticals.

Other large emerging nations would want to follow the same policy. If China and India succeed, will other emerging nations follow?

©Arun Sharma, All Rights Reserved56

Industry Trends Latin America

Highest Growth Countries (worldwide):– Venezuela, Argentina, China, Ukraine, Vietnam, India and Brazil.• 2015 Size – China #3; Brazil #6; India #8; Mexico # 14; Venezuela #15 in the World.

Latin American Market Estimate for 2012– $70 Billion; Brazil is 40% of the Market; Mexico 20%.

Affluent and Aging Population.

Growth in Government and Private Insurance.– Pharmaceutical Coverage is Low in Latin America.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved57

Industry Trends Latin America

High Price Sensitivity– But also Brand and Relationship Sensitive.

Competition– Local Firms Will Dominate (2,000 firms in LAC).

• Government Relationships, Provider Relationships, Distribution Channel Relationships, Low Prices– Big Pharma Will Need Partners (Government, Local Firms).

– Value Focus will be needed.

– Innovation Will Not be a Differentiator.

– Need to Reduce Costs

– Enhance Brand and Relationships. LatinAmerica

©Arun Sharma, All Rights Reserved58

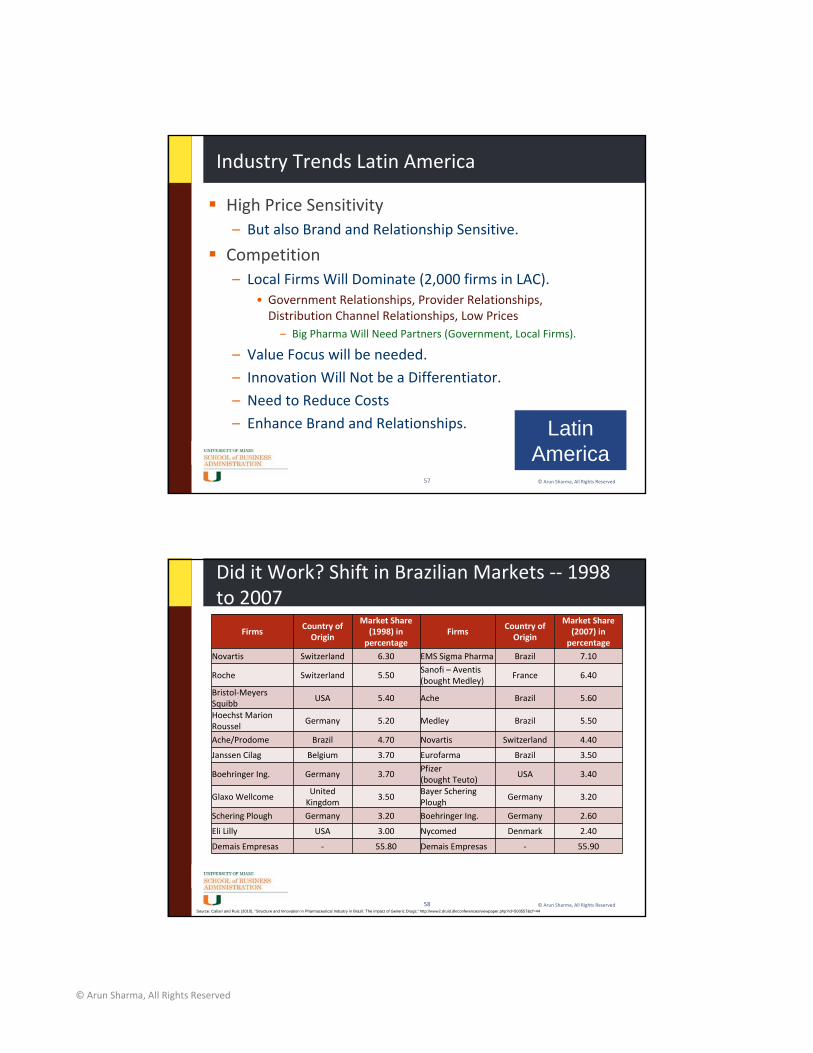

Did it Work? Shift in Brazilian Markets ‐‐ 1998 to 2007

FirmsCountry of Origin

Market Share (1998) in percentage

FirmsCountry of Origin

Market Share (2007) in percentage

Novartis Switzerland 6.30 EMS Sigma Pharma Brazil 7.10

Roche Switzerland 5.50Sanofi – Aventis (bought Medley)

France 6.40

Bristol‐Meyers Squibb

USA 5.40 Ache Brazil 5.60

Hoechst Marion Roussel

Germany 5.20 Medley Brazil 5.50

Ache/Prodome Brazil 4.70 Novartis Switzerland 4.40

Janssen Cilag Belgium 3.70 Eurofarma Brazil 3.50

Boehringer Ing. Germany 3.70Pfizer(bought Teuto)

USA 3.40

Glaxo WellcomeUnited Kingdom

3.50Bayer Schering Plough

Germany 3.20

Schering Plough Germany 3.20 Boehringer Ing. Germany 2.60

Eli Lilly USA 3.00 Nycomed Denmark 2.40

Demais Empresas ‐ 55.80 Demais Empresas ‐ 55.90

Source: Caliari and Ruiz (2010), “Structure and Innovation in Pharmaceutical Industry in Brazil: The impact of Generic Drugs;” http://www2.druid.dk/conferences/viewpaper.php?id=500557&cf=44

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved59

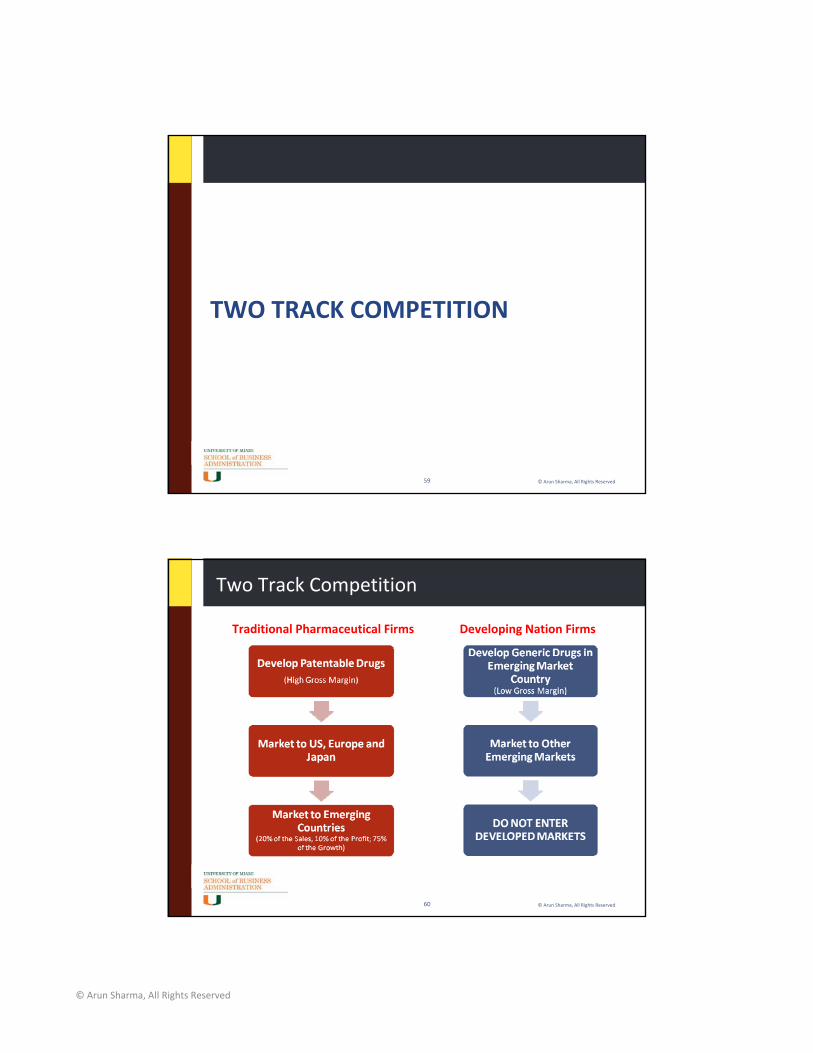

TWO TRACK COMPETITION

©Arun Sharma, All Rights Reserved60

Two Track Competition

Developing Nation FirmsTraditional Pharmaceutical Firms

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved61

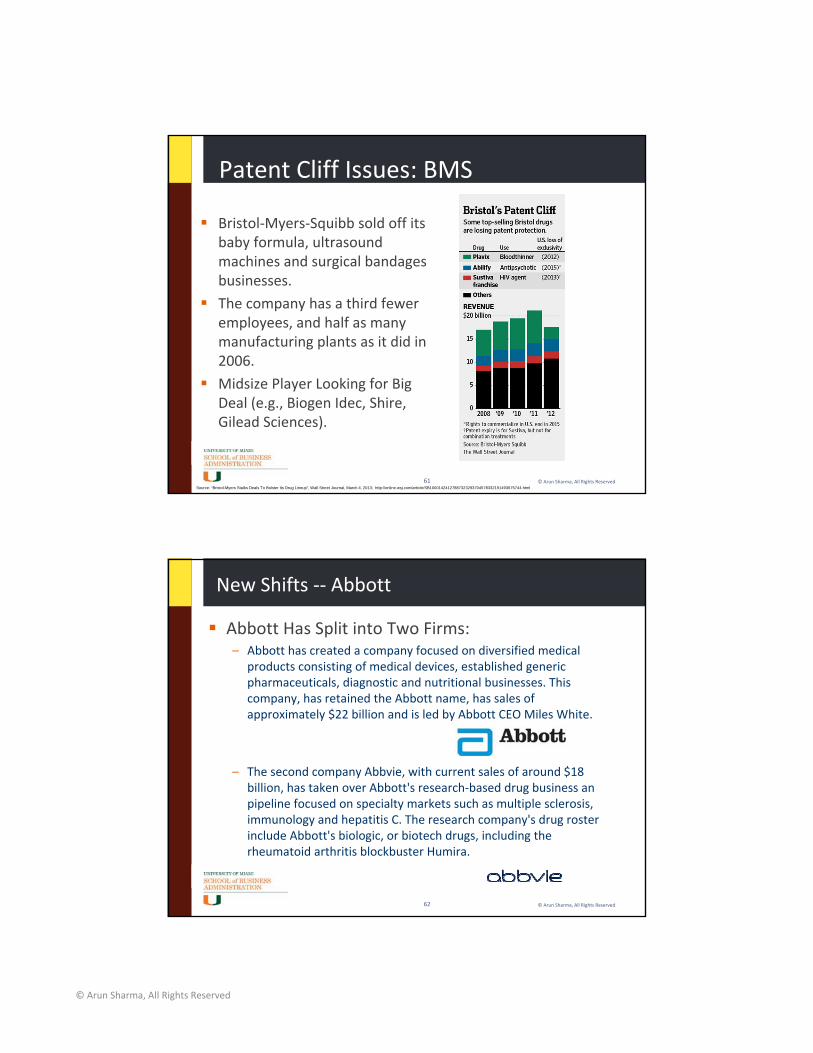

Patent Cliff Issues: BMS

Bristol‐Myers‐Squibb sold off its baby formula, ultrasound machines and surgical bandages businesses.

The company has a third fewer employees, and half as many manufacturing plants as it did in 2006.

Midsize Player Looking for Big Deal (e.g., Biogen Idec, Shire, Gilead Sciences).

Source: “Bristol-Myers Stalks Deals To Bolster Its Drug Lineup”, Wall Street Journal, March 4, 2013; http://online.wsj.com/article/SB10001424127887323293704578332191493675744.html

©Arun Sharma, All Rights Reserved62

New Shifts ‐‐ Abbott

Abbott Has Split into Two Firms:– Abbott has created a company focused on diversified medical

products consisting of medical devices, established generic pharmaceuticals, diagnostic and nutritional businesses. This company, has retained the Abbott name, has sales of approximately $22 billion and is led by Abbott CEO Miles White.

– The second company Abbvie, with current sales of around $18 billion, has taken over Abbott's research‐based drug business an pipeline focused on specialty markets such as multiple sclerosis, immunology and hepatitis C. The research company's drug roster include Abbott's biologic, or biotech drugs, including the rheumatoid arthritis blockbuster Humira.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved63

SCENARIO PLANNING FOR PHARMACEUTICAL MARKET

©Arun Sharma, All Rights Reserved64

Scenario Planning

What are the 3‐4 Most Probable Business Scenarios in our Markets?

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved65

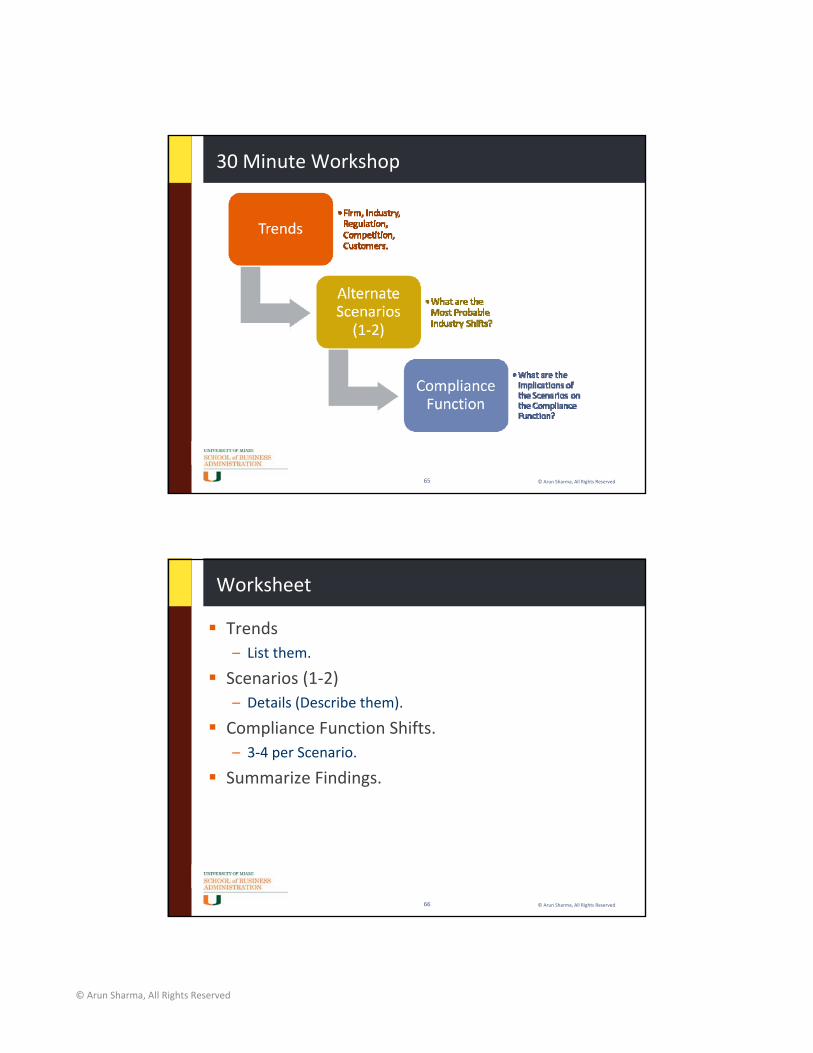

30 Minute Workshop

©Arun Sharma, All Rights Reserved66

Worksheet

Trends– List them.

Scenarios (1‐2)– Details (Describe them).

Compliance Function Shifts.– 3‐4 per Scenario.

Summarize Findings.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved67

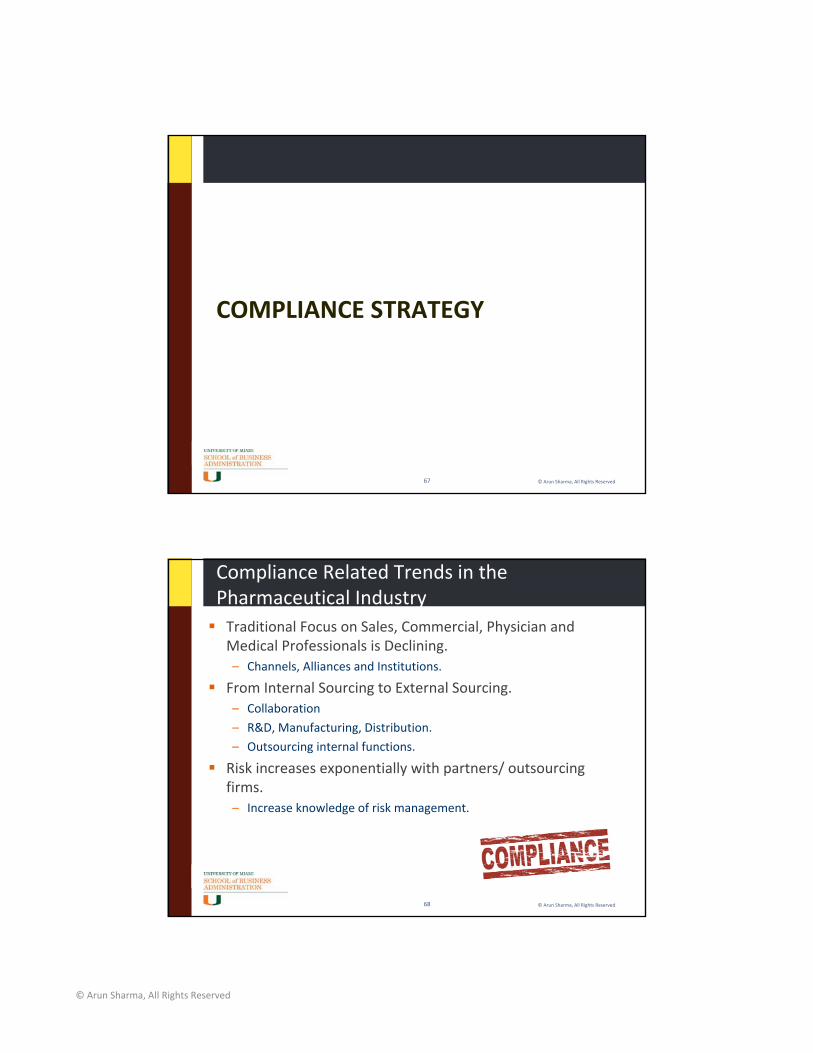

COMPLIANCE STRATEGY

©Arun Sharma, All Rights Reserved68

Compliance Related Trends in the Pharmaceutical IndustryTraditional Focus on Sales, Commercial, Physician and Medical Professionals is Declining.– Channels, Alliances and Institutions.

From Internal Sourcing to External Sourcing.– Collaboration

– R&D, Manufacturing, Distribution.– Outsourcing internal functions.

Risk increases exponentially with partners/ outsourcing firms.– Increase knowledge of risk management.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved69

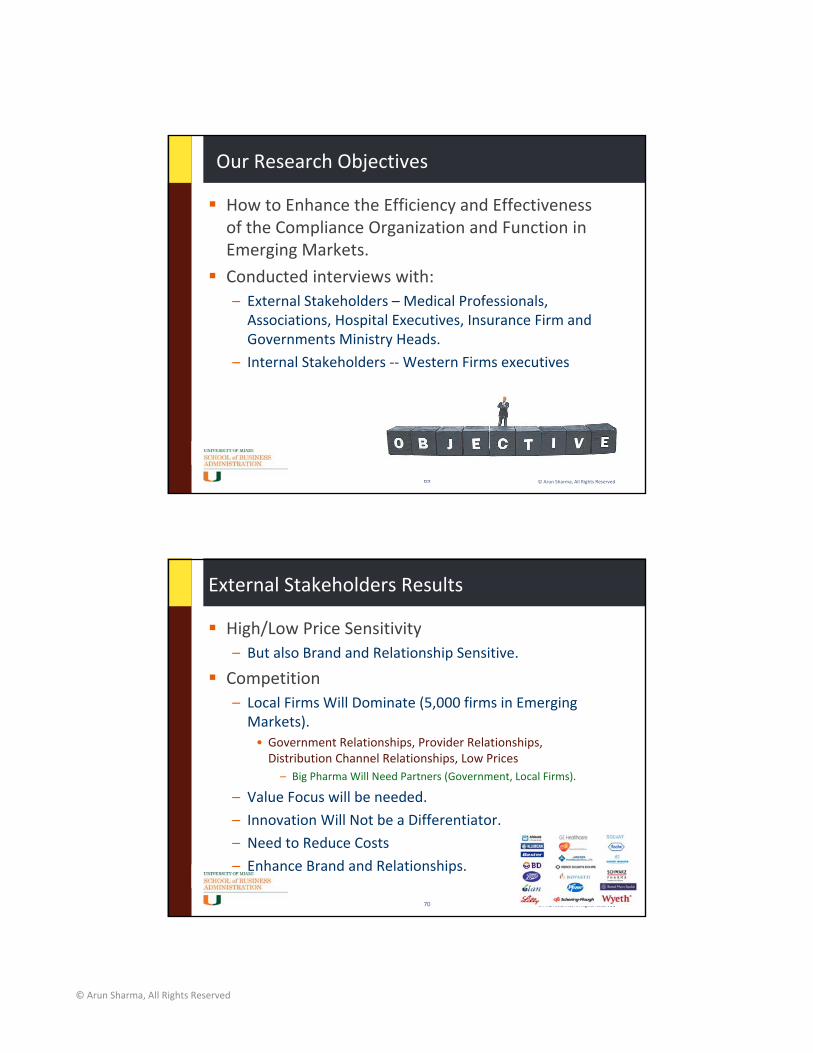

Our Research Objectives

How to Enhance the Efficiency and Effectiveness of the Compliance Organization and Function in Emerging Markets.

Conducted interviews with:– External Stakeholders – Medical Professionals, Associations, Hospital Executives, Insurance Firm and Governments Ministry Heads.

– Internal Stakeholders ‐‐Western Firms executives

©Arun Sharma, All Rights Reserved70

External Stakeholders Results

High/Low Price Sensitivity– But also Brand and Relationship Sensitive.

Competition– Local Firms Will Dominate (5,000 firms in Emerging Markets).• Government Relationships, Provider Relationships, Distribution Channel Relationships, Low Prices– Big Pharma Will Need Partners (Government, Local Firms).

– Value Focus will be needed.

– Innovation Will Not be a Differentiator.

– Need to Reduce Costs

– Enhance Brand and Relationships.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved71

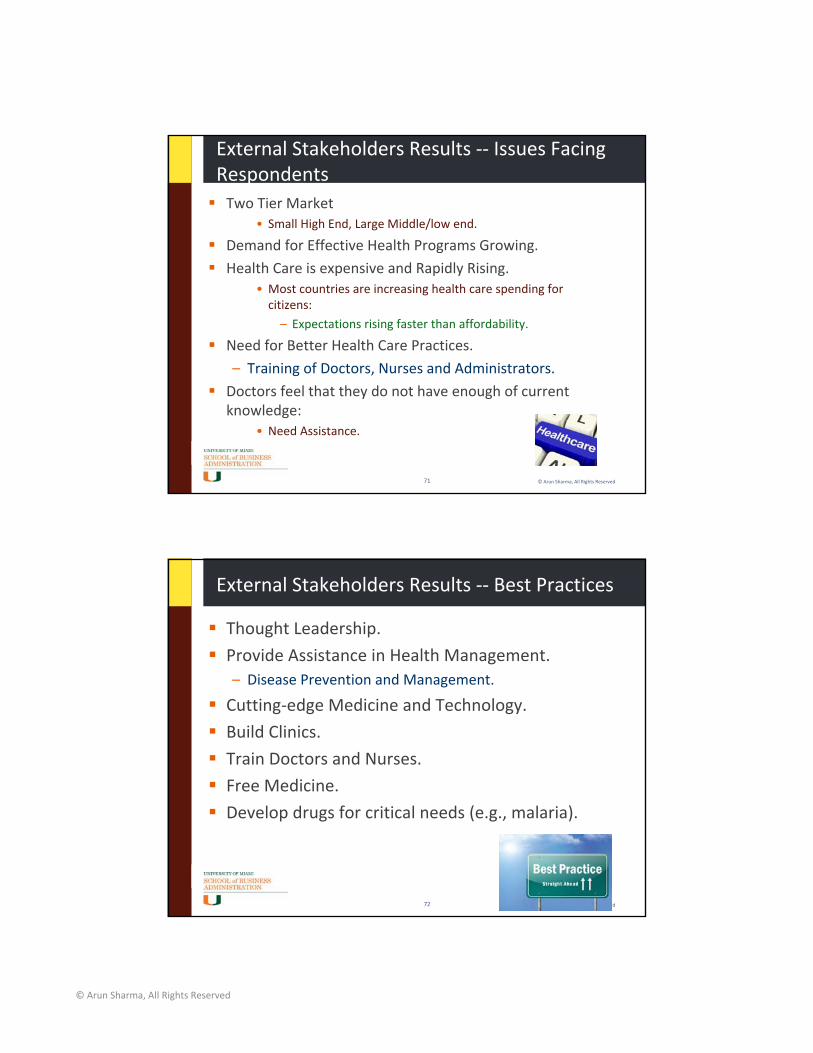

External Stakeholders Results ‐‐ Issues Facing RespondentsTwo Tier Market

• Small High End, Large Middle/low end.

Demand for Effective Health Programs Growing.

Health Care is expensive and Rapidly Rising.• Most countries are increasing health care spending for citizens:

– Expectations rising faster than affordability.

Need for Better Health Care Practices.

– Training of Doctors, Nurses and Administrators.

Doctors feel that they do not have enough of current knowledge:

• Need Assistance.

©Arun Sharma, All Rights Reserved72

External Stakeholders Results ‐‐ Best Practices

Thought Leadership.

Provide Assistance in Health Management.– Disease Prevention and Management.

Cutting‐edge Medicine and Technology.

Build Clinics.

Train Doctors and Nurses.

Free Medicine.

Develop drugs for critical needs (e.g., malaria).

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved73

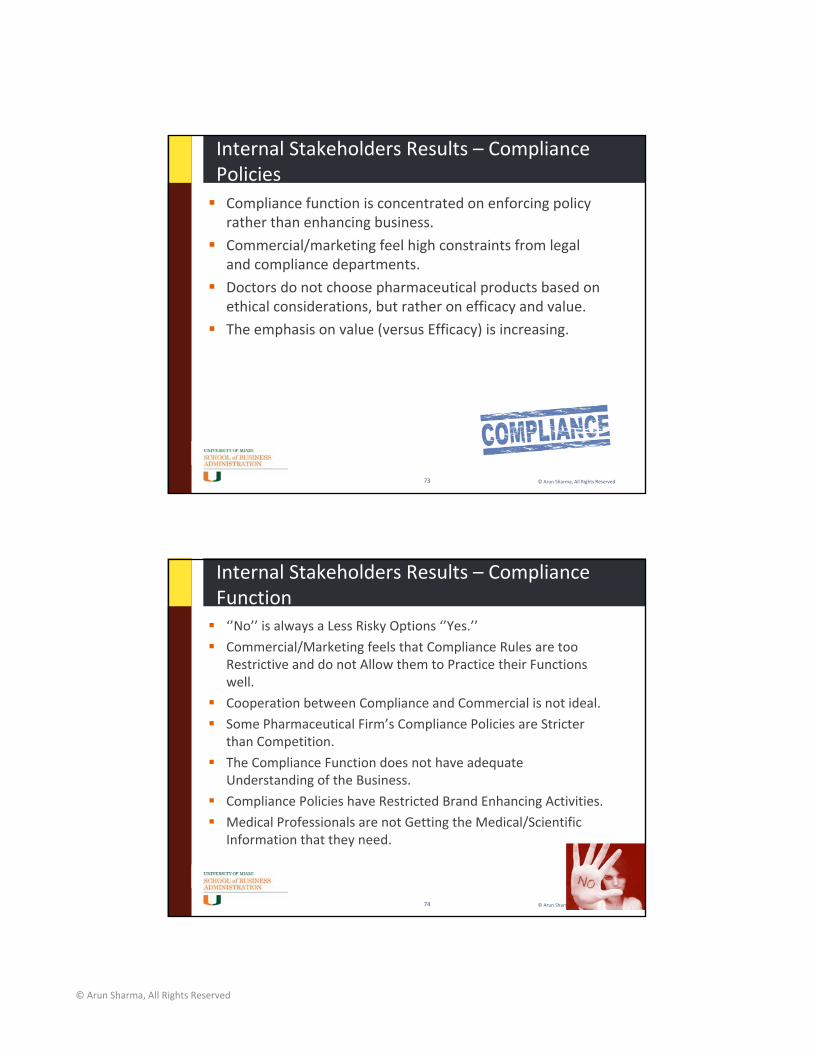

Internal Stakeholders Results – Compliance PoliciesCompliance function is concentrated on enforcing policy rather than enhancing business.

Commercial/marketing feel high constraints from legal and compliance departments.

Doctors do not choose pharmaceutical products based on ethical considerations, but rather on efficacy and value.

The emphasis on value (versus Efficacy) is increasing.

©Arun Sharma, All Rights Reserved74

Internal Stakeholders Results – Compliance Function‘’No’’ is always a Less Risky Options ‘’Yes.’’

Commercial/Marketing feels that Compliance Rules are too Restrictive and do not Allow them to Practice their Functions well.

Cooperation between Compliance and Commercial is not ideal.

Some Pharmaceutical Firm’s Compliance Policies are Stricter than Competition.

The Compliance Function does not have adequate Understanding of the Business.

Compliance Policies have Restricted Brand Enhancing Activities.

Medical Professionals are not Getting the Medical/Scientific Information that they need.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved75

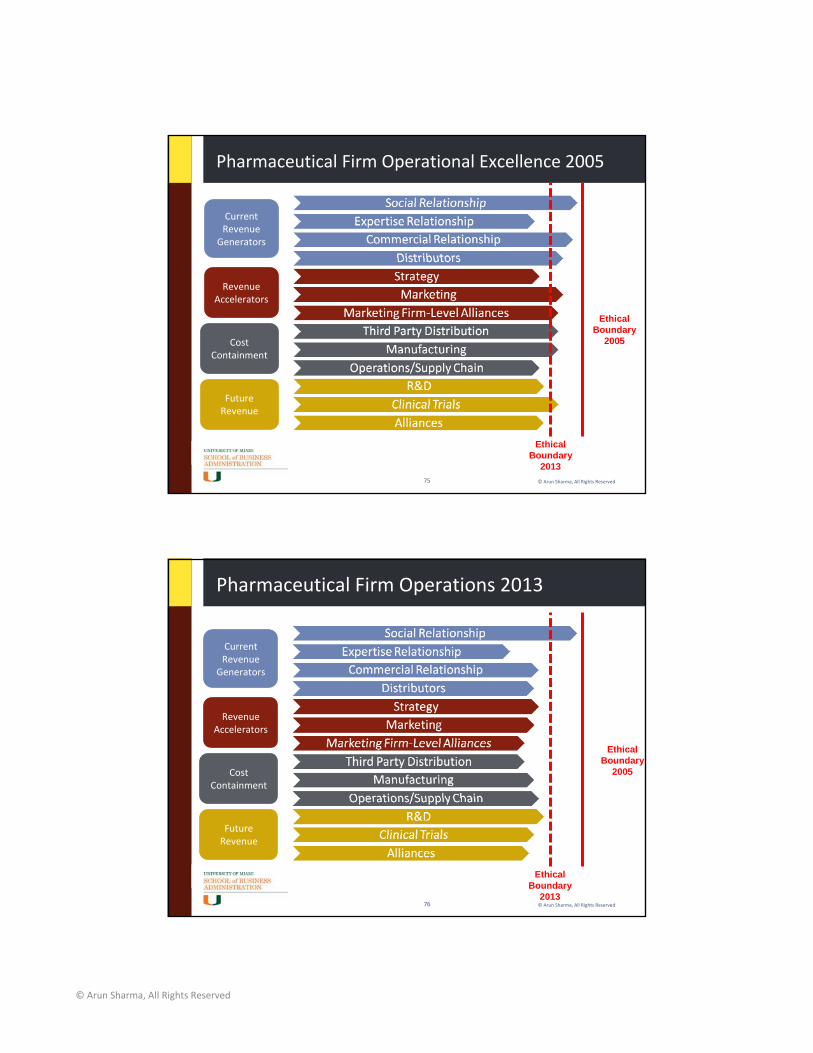

Pharmaceutical Firm Operational Excellence 2005

Future Revenue

Current Revenue

Generators

Revenue Accelerators

Cost Containment

Ethical Boundary

2005

Ethical Boundary

2013

©Arun Sharma, All Rights Reserved76

Pharmaceutical Firm Operations 2013

Future Revenue

Current Revenue

Generators

Revenue Accelerators

Cost Containment

Ethical Boundary

2005

Ethical Boundary

2013

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved77

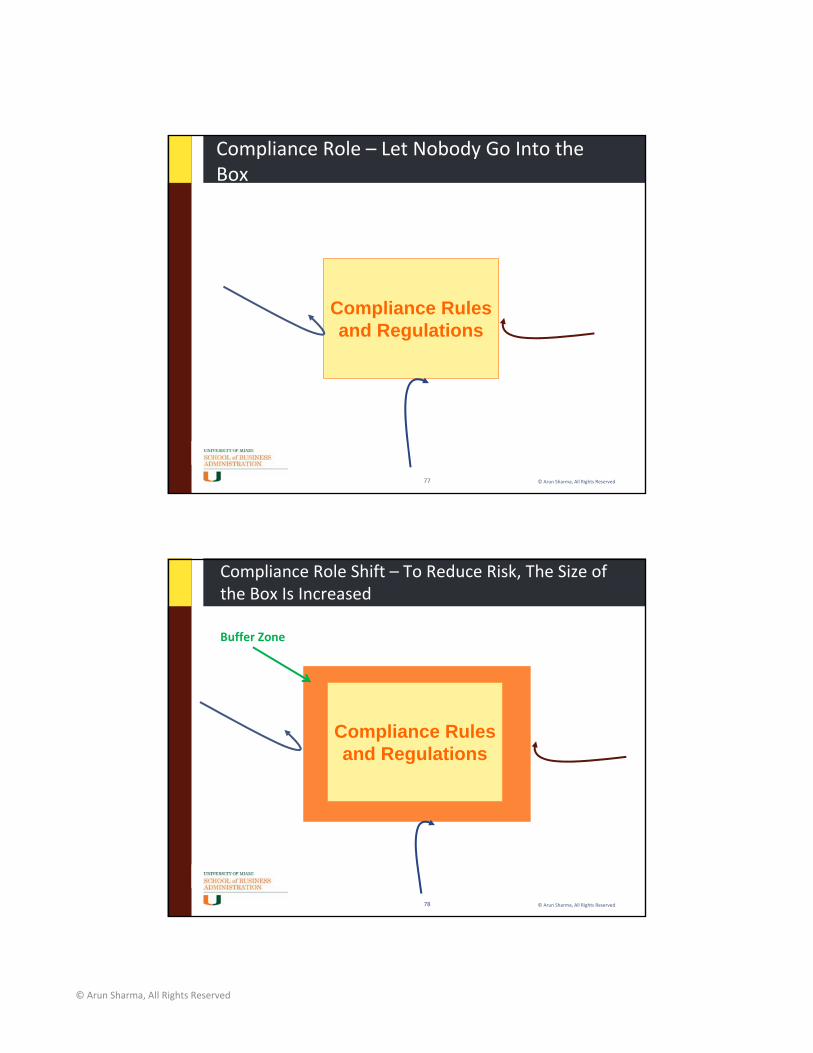

Compliance Role – Let Nobody Go Into the Box

Compliance Rules and Regulations

©Arun Sharma, All Rights Reserved78

Compliance Role Shift – To Reduce Risk, The Size of the Box Is Increased

Compliance Rules and Regulations

Buffer Zone

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved79

Compliance Function Issues

Control Function.– Strategic?

– Involved in Market Strategy Planning?

Understanding of Business?

Programmed to Say NO.

What Happens to Functions that are Control Functions and not Strategic?– They Get Outsourced.

• IRB, IT, Banking Risk Management, HR.

©Arun Sharma, All Rights Reserved80

Emerging Compliance Issues – Moving Toward Compliance 2.0Different Compliance Requirements for Different Firms– Advanced Country Firms and Emerging Country Firms.

Multichannel Partners.

Direct to Patient by Firm and Distribution.

Patient Level Compliance.– Adherence, Promotion, Prevention.

Digital Compliance.

Standardized Compliance Programs– Rise of Third Party Compliance Certifiers.

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved81

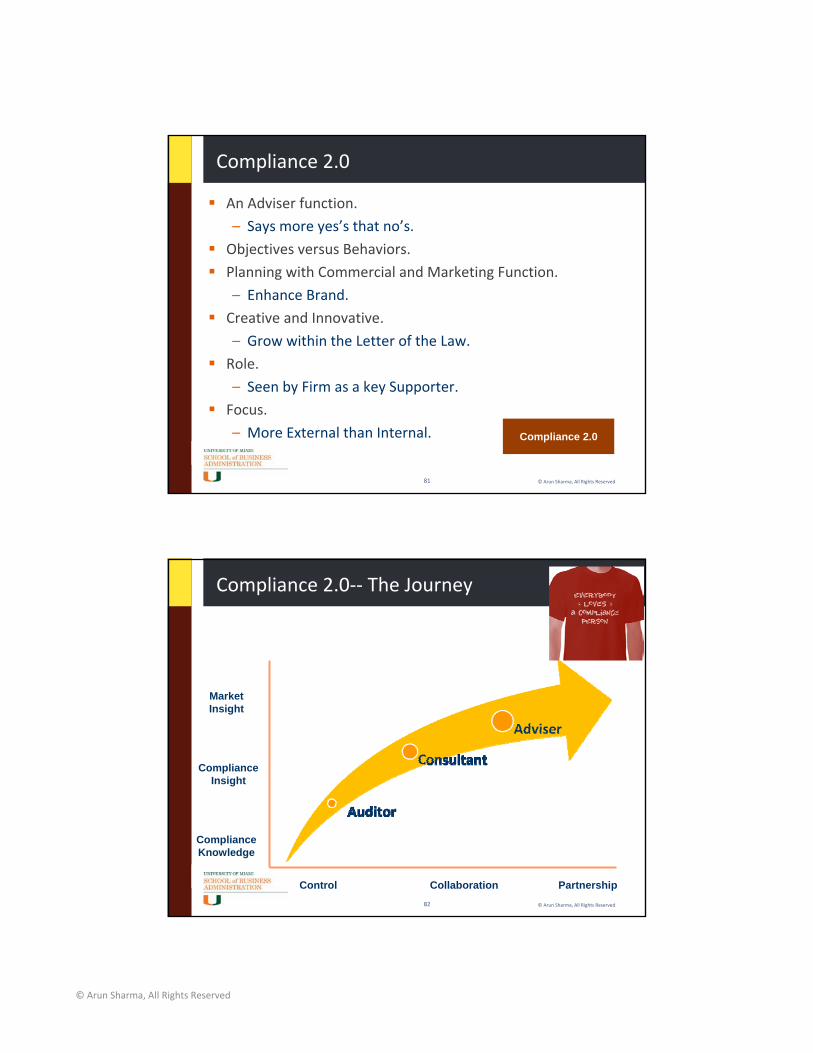

Compliance 2.0

An Adviser function.

– Says more yes’s that no’s.

Objectives versus Behaviors.

Planning with Commercial and Marketing Function.

– Enhance Brand.

Creative and Innovative.

– Grow within the Letter of the Law.

Role.

– Seen by Firm as a key Supporter.

Focus.

– More External than Internal. Compliance 2.0

©Arun Sharma, All Rights Reserved82

Compliance 2.0‐‐ The Journey

PartnershipCollaboration

Compliance Insight

Control

Market Insight

Compliance Knowledge

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved83

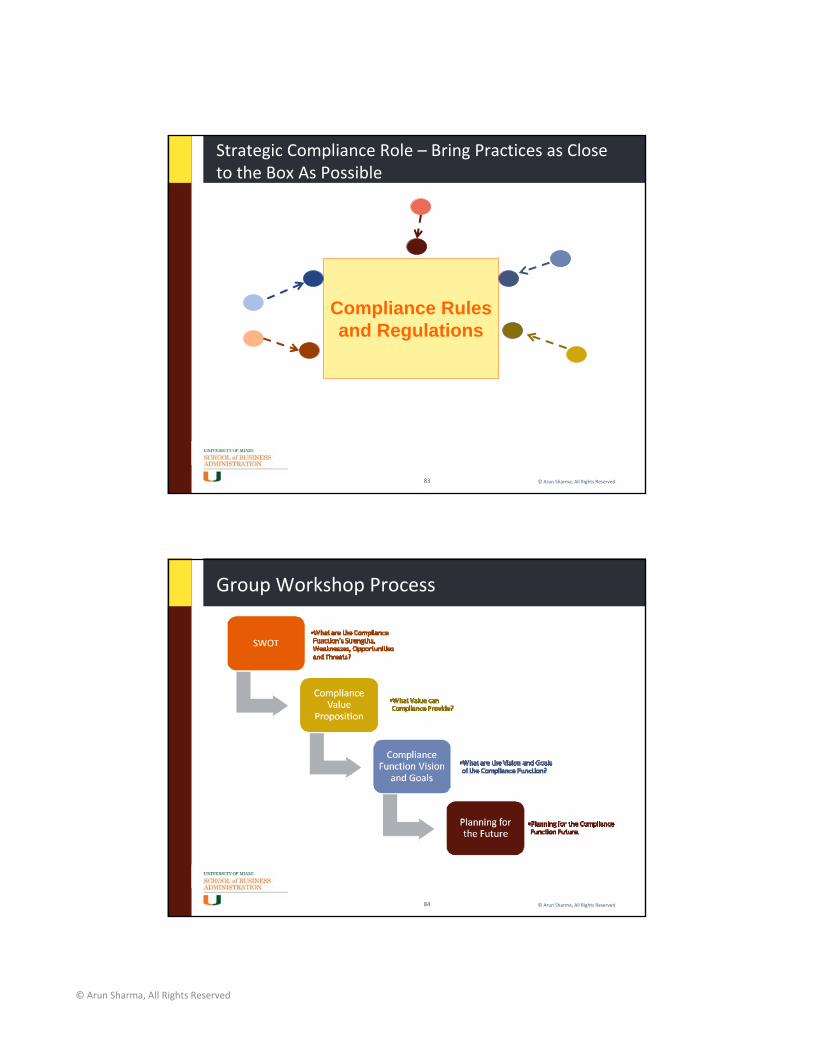

Strategic Compliance Role – Bring Practices as Close to the Box As Possible

Compliance Rules and Regulations

©Arun Sharma, All Rights Reserved84

Group Workshop Process

© Arun Sharma, All Rights Reserved

©Arun Sharma, All Rights Reserved85

Summary

Fundamental Shifts in Markets– Branded versus Generic

– Advanced Markets versus Developing Markets

– Best versus “good enough.”

Compliance Needs to be More Strategic.

©Arun Sharma, All Rights Reserved86

Arun Sharma

Dr. Arun Sharma is Executive Director of the JAE Leadership Institute and Professor in the Marketing Department at the School of Business Administration, University of Miami. Arun has extensive knowledge of firms through his experience in consulting, and conducting seminars. He is a well known expert in Global Market Trends, Leadership Strategies, Sustainable Competitive Strategies, and Market Strategy and his expertise is in designing and implementing corporate strategies. He has consulted and conducted seminars for companies such as Accenture, Agilent Technologies, Ambrosetti, American Express, AT&T, Bell South, Citrix, Ericcson, Exxon, Goodyear, HP, IBM, Lucent, Macy’s, MasterCard, Motorola, Siemens, Sprint, Telecom Italia, Telecom Italia Mobil, Visa International, Wal‐Mart and Western Union. He has extensive expertise in business and consumer markets, technology, financial, telecommunication, healthcare, consumer goods and consulting industries.

He has previously taught at the University of Illinois at Urbana‐Champaign where he received his Ph.D. in marketing in 1988. Arun also has an MBA and a Bachelor of Engineering degree in Metallurgy. Prior to joining the academic world, he worked for three years in a high‐technology firm where he handled product management and sales management responsibilities.

Arun has published extensively (over 80 refereed articles) and is on the review board of major journals and has received many excellence in research and excellence in teaching awards from the School of Business Administration at the University of Miami. He can be contacted at 305.284.1770, Fax: 305.667.2557 and email: [email protected].