Embed Size (px)

Citation preview

Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved

1

Chapter 16Chapter 16Assessing Long-Term Debt, Equity, and Capital Structure

McGraw-Hill/Irwin Copyright © 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Introduction• Capital structure– Mix of debt and equity that finances firm’s

operations

• Funding decision factors– debt interest payments’ tax deductibility– risks posed by increased debt

16-2

Active vs. Passive Capital Structure Changes

Active management– Selling one type of capital to fund the retirement of

other kinds of capital

Passive management– Waiting for additional incoming capital– Adjust financing mix (debt or equity) over time

16-3

Active vs. Passive

Choice depends on three factors

– How quickly the firm is growing

– The flotation costs under the active management

approach

– The need for changes to the firm’s capital structure

16-4

Capital Structure Theory: The Effect of Financial Leverage

• Debt is referred to as “leverage”

• Debt magnifies potential risk and returns

16-5

Modigliani and Miller

The Modigliani and Miller (M&M) Theorem is a tool for examining the effects of various

variables on choice of optimal capitalstructure for firm.

16-6

Modigliani and Miller’s Perfect World

• No taxes

• No chance of bankruptcy

• Perfectly efficient markets

• Symmetric information sets for all participants

16-7

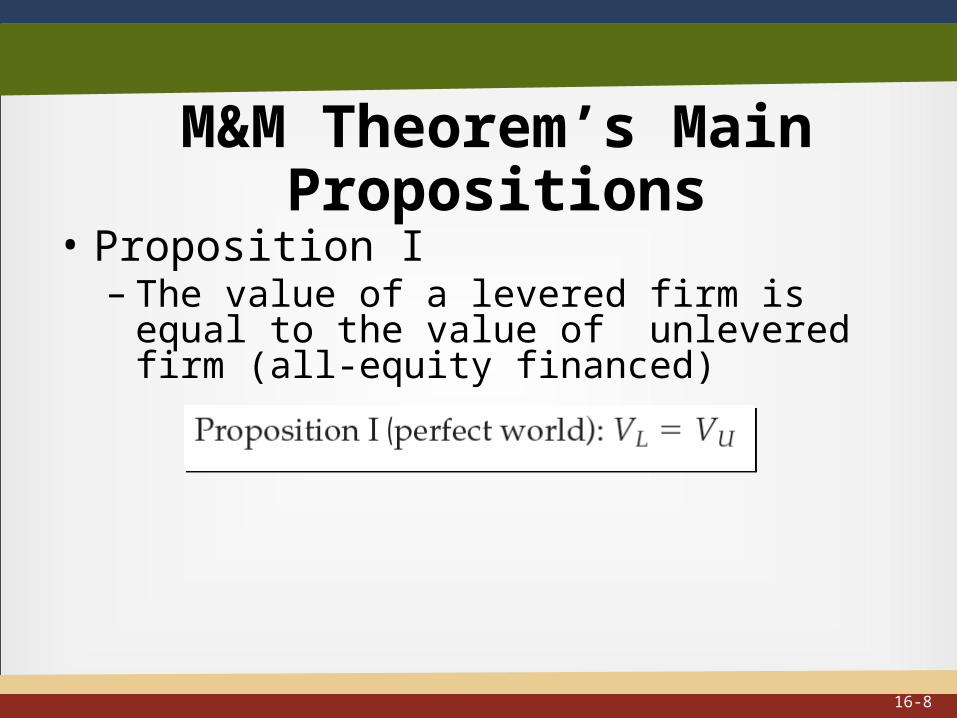

M&M Theorem’s Main Propositions

• Proposition I– The value of a levered firm is equal to the value of

unlevered firm (all-equity financed)

16-8

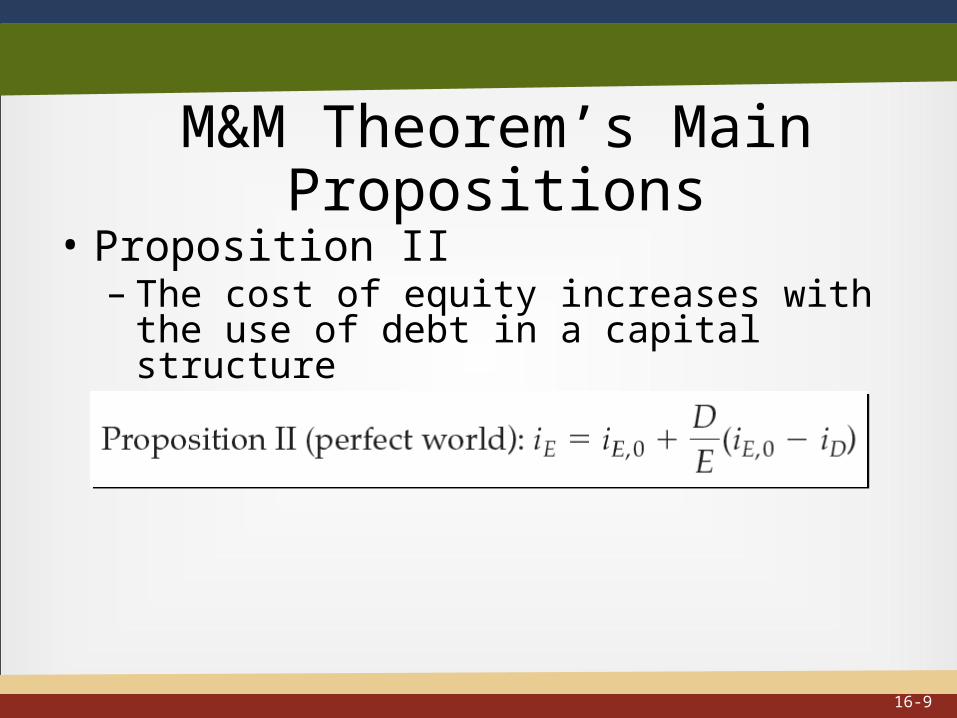

M&M Theorem’s Main Propositions

• Proposition II– The cost of equity increases with the use of debt

in a capital structure

16-9

Effect of Leverage on Cost of Equity

• Cost of Equity increases as debt increases

• Weighted Average Cost of Capital (WACC) does not change

16-10

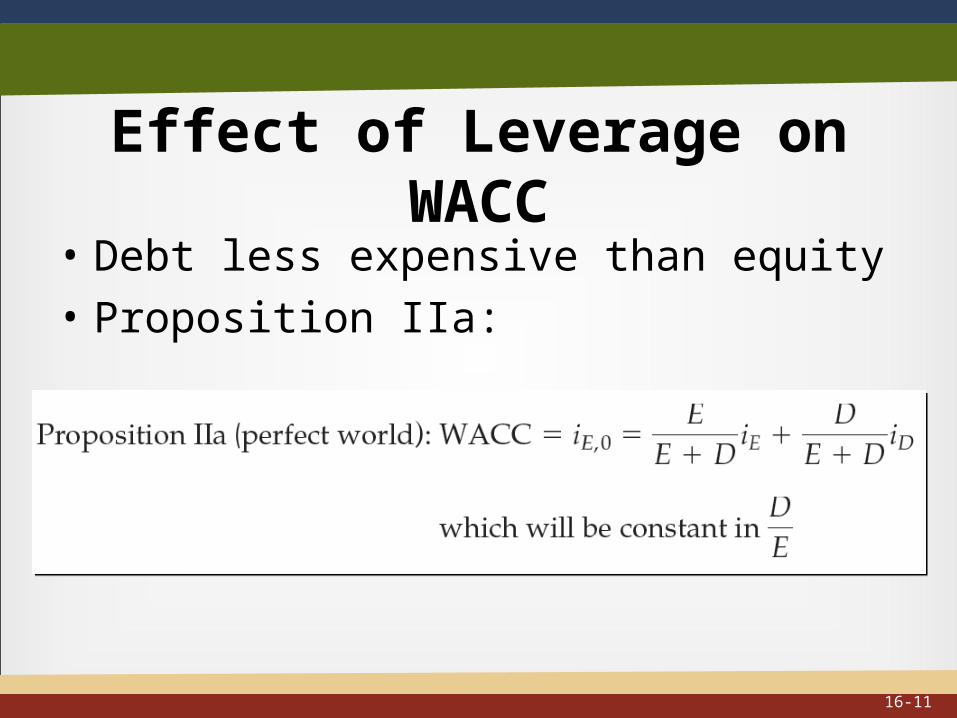

Effect of Leverage on WACC• Debt less expensive than equity• Proposition IIa:

16-11

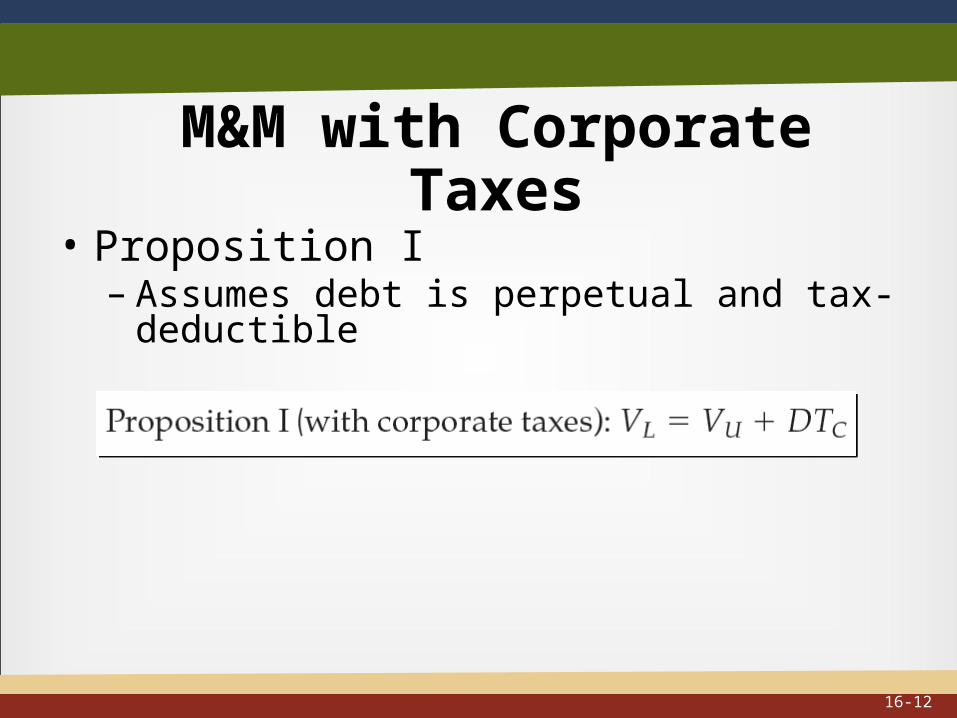

M&M with Corporate Taxes• Proposition I– Assumes debt is perpetual and tax-deductible

16-12

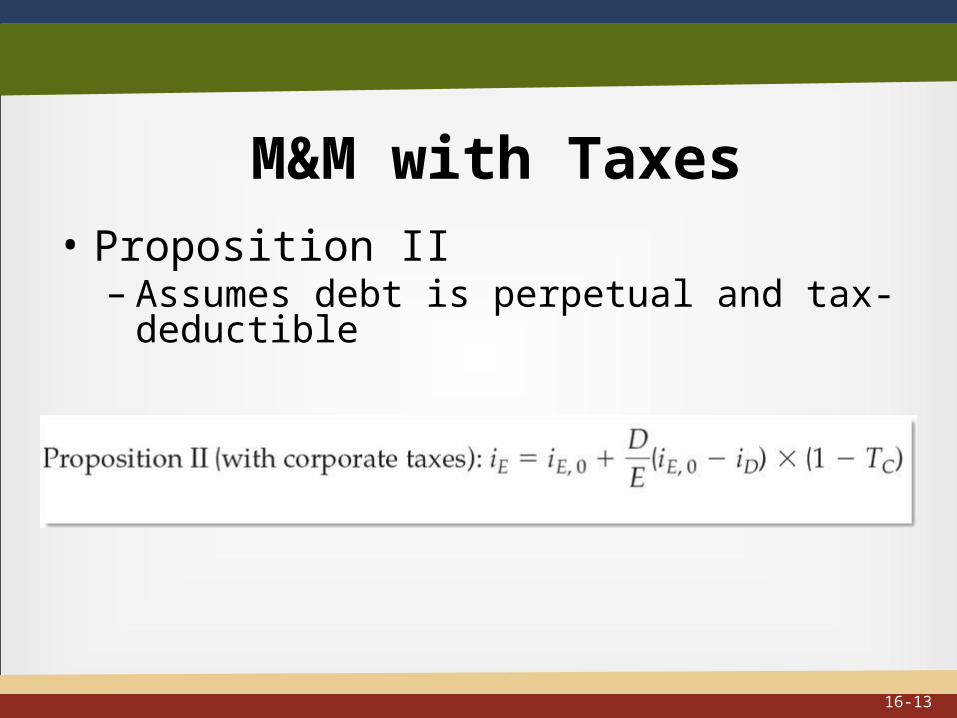

M&M with Taxes• Proposition II– Assumes debt is perpetual and tax-deductible

16-13

Choice to Re-leverage• Increased debt increases

– Cash flows to equity holders

– Volatility of cash flows to equity

16-14

Break-Even EBIT• Solving for EPS creates investor indifference

between capital structures– Express EPS as function of EBIT for each capital

structure– Set them equal to each other– Solve for the break-even EBIT

16-15

M&M with Corporate Taxes and Bankruptcy

• Assumes firm may go bankrupt

– Bondholders bear some of firm risk

– Bondholders demand higher compensation in return for risk

16-16

Types of Bankruptcies in the U.S.• Chapter 7– Business liquidation– Immediate cessation of business operations

• Chapter 7 Claimant payout order• Secured lenders (including bondholders)• Lawyers • Employees• Government• Unsecured debt holders• Equity holders

16-17

Types of Bankruptcies in the U.S.

• Chapter 11

– Firm remains in operation

– May reorganize under court supervision

– Creditors register with the bankruptcy court

– Firm may emerge from bankruptcy

16-18

Costs of Financial Distress• Loss of consumer and supplier confidence • May face tighter credit and higher rates• Declining partnership opportunities with other

firms• Potential loss of best employees

16-19

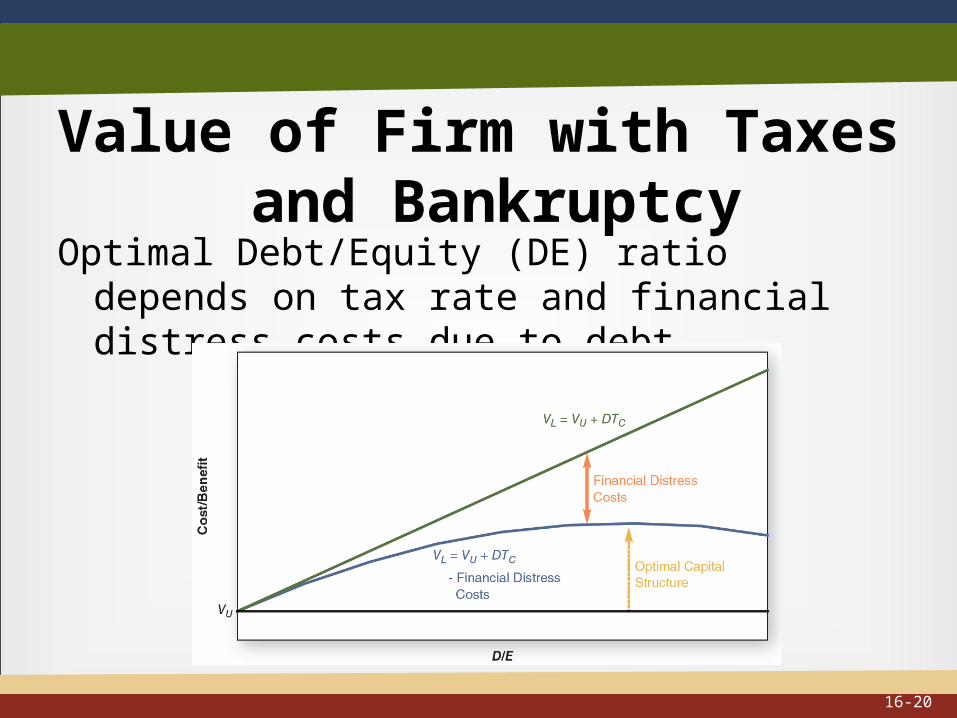

Value of Firm with Taxes and Bankruptcy

Optimal Debt/Equity (DE) ratio depends on tax rate and financial distress costs due to debt

16-20

Capital Structure Theory vs. Reality

• Factors affecting capital structures– Firms with high taxes should use more debt– Firms with stable, predictable income streams can

use more debt

16-21

Observed Capital Structures

• Economic sectors with lowest D/E ratios tend to have low or variable income streams

• Economic sectors with highest D/E ratios tend to have high, stable income streams

16-22