Embed Size (px)

Citation preview

CVP Seminar

Heathrow Academy - 7th December 2016

WELCOME

Guy Hitchcock, Clean Vehicle Partnership

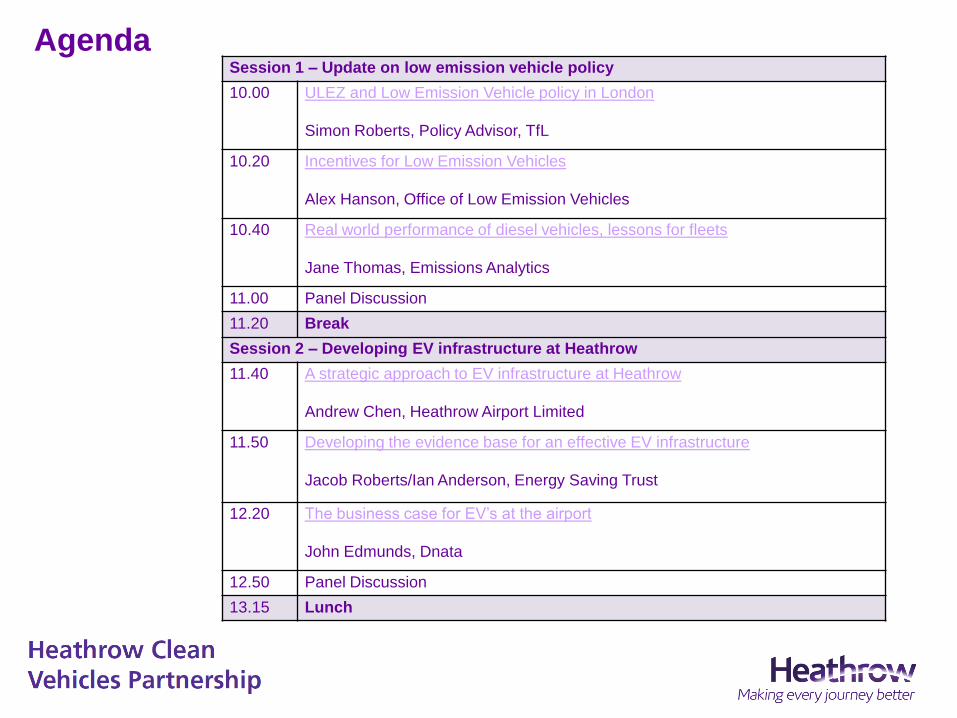

AgendaSession 1 – Update on low emission vehicle policy

10.00 ULEZ and Low Emission Vehicle policy in London

Simon Roberts, Policy Advisor, TfL

10.20 Incentives for Low Emission Vehicles

Alex Hanson, Office of Low Emission Vehicles

10.40 Real world performance of diesel vehicles, lessons for fleets

Jane Thomas, Emissions Analytics

11.00 Panel Discussion

11.20 Break

Session 2 – Developing EV infrastructure at Heathrow

11.40 A strategic approach to EV infrastructure at Heathrow

Andrew Chen, Heathrow Airport Limited

11.50 Developing the evidence base for an effective EV infrastructure

Jacob Roberts/Ian Anderson, Energy Saving Trust

12.20 The business case for EV’s at the airport

John Edmunds, Dnata

12.50 Panel Discussion

13.15 Lunch

ULEZ and Low

Emission Vehicle

policy in London

Contents

• Context

• Emission Surcharge (‘T-charge’)

• Emerging proposals for ULEZ

• Wider Electric Vehicle Policy

• Buses and Taxis

• Next Steps

2

Context

1952

Now

Impacts of air pollution

• Long term exposure estimated to

cause the equivalent of 9,400 deaths

in London per year and 29,000

nationally.

• The health impacts associated with

air pollution fall disproportionally on

our most vulnerable communities,

affecting the poorest and those from

minority ethnic groups more acutely.

6

NO2 Road Transport Problem

7

Aviation

8%

Mayor’s Clean Air Action Plan

1) Emission Surcharge (‘T-charge’) in

central London from 2017

2) Policy consultation

– ULEZ in Central London in 2019

instead of 2020

– Expanding the ULEZ Londonwide

for heavy vehicles only

– Expanding the ULEZ up to the

North and South Circular Roads for

all vehicles

3) Buses and Taxis

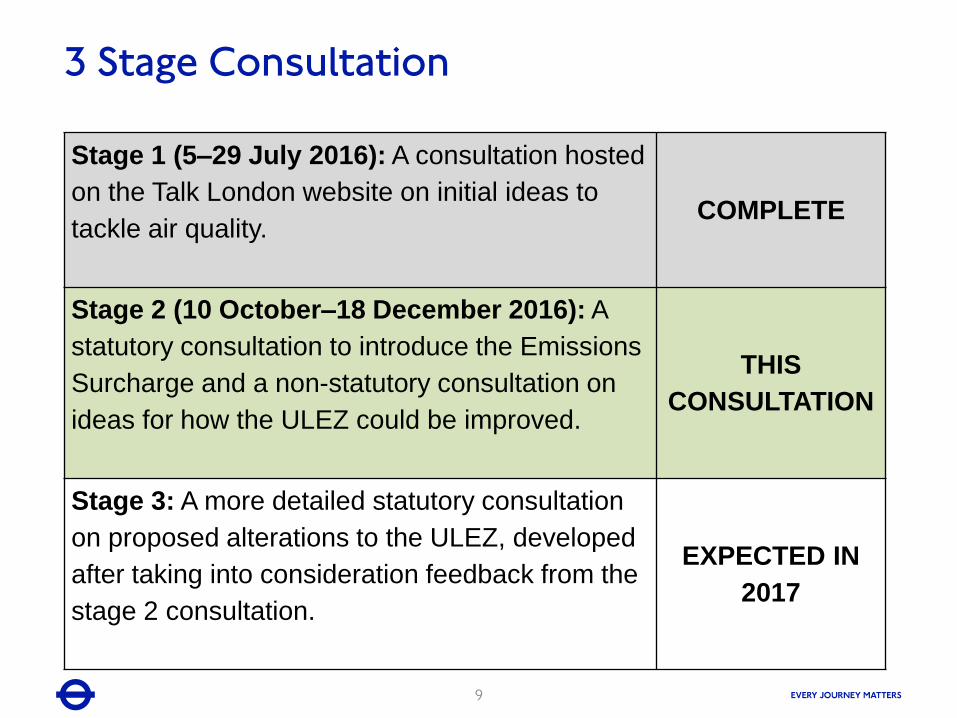

3 Stage Consultation

9

Stage 1 (5–29 July 2016): A consultation hosted

on the Talk London website on initial ideas to

tackle air quality.COMPLETE

Stage 2 (10 October–18 December 2016): A

statutory consultation to introduce the Emissions

Surcharge and a non-statutory consultation on

ideas for how the ULEZ could be improved.

THIS

CONSULTATION

Stage 3: A more detailed statutory consultation

on proposed alterations to the ULEZ, developed

after taking into consideration feedback from the

stage 2 consultation.

EXPECTED IN

2017

Emissions

Surcharge

What is the Emissions Surcharge ?

11

• Same boundary and times as Congestion Charge

• £10 surcharge (on top of the Congestion Charge)

• Charge will apply to all eligible pre-Euro 4 vehicles

(broadly equivalent to vehicles from 2005 and older)

• 90% Residents discount will apply to the surcharge

• Same discounts and exemptions as Congestion

Charge, plus historic vehicles and showman’s vehicles

• 9+seater vehicles will be eligible for the charge

• Scheme will come in to force on 23 Oct 2017

• An online compliance checker will be available

Emissions surcharge

impacts

12

Vehicle type Affected vehicles per day

Cars 7,000

Vans 2,000

HGV 400

Non-TfL bus and coach 600Potential NOx emission reduction

in central London

Emerging

proposals for

ULEZ

The Ultra Low Emission Zone - As it stands

14

Euro 4 petrol (c.2006)

Euro 6 diesel (c.2015)

...or £12.50 a day

Euro VI (c.2014)

...or £100 a day

Exempt but

new licencing rules

Euro 3 (c.2007)

...or £12.50 a day

Additional hybrid or

electric standard

Starts Sept 202024/7

15

ULEZ

standards

• Petrol:

Euro 4

• Diesel:

Euro 6

• Motorcycle

and L-Cat:

Euro 3

Emerging proposals for ULEZ

Bringing ULEZ forward to 2019

16

17

Non-compliant levels (average day)

HGV Coach

2019 31% 49%

2020 24% 40%

2021 20% 29%

2022 16% 21%

2023 13% 13%

• Euro VI standard for heavy vehicles out to the

current Low Emission Zone (London-wide) boundary

• Estimated 30 per cent road transport NOx reduction

London wide ULEZ for heavy vehicles

ULEZ expansion up to N/S circular

for all vehicles

18

Central Up to N/S Circular

Area 21 sq. km 381 sq. km (18 times larger)

Population 136k 3.8m (28 times larger)

Vehicles ~150,000 ~660,000 (4.5 times as many)

Extending ULEZ up to N/S Circular

19

Petrol car Diesel car Van HGV Coach

2019 15% 57% 55% 29% 45%

2020 10% 37% 43% 19% 33%

2021 8% 32% 35% 15% 24%

2022 6% 27% 28% 12% 16%

2023 4% 22% 22% 9% 11%

Projected non-compliance with ULEZ standards

• Affects the same vehicles as central London ULEZ

• Could consider a lower charge

• Approximately 40 per cent reduction in road transport

NOx inside the zone

Expanding ULEZ – Key issues to resolve

20

• Boundary

• Date of

implementation

• Exemptions/discounts/

sunset period

• Charge level

Low Emission

Vehicle Policy

ULEV Delivery Plan• The Ultra Low Emission Vehicle Delivery Plan

(2015) sets out London’s specific challenges to

unlocking widespread ULEV uptake and 15 new

actions to overcome them.

• The actions are based upon three pillars needed

to support the conversion of diesel and petrol

vehicles to ULEVs. These are:

• Infrastructure: Confidence for drivers that they

can charge up or refuel when they need to

• Vehicles on the roads: Increasing visibility

including through our own fleets

• Marketing and incentives: Incentives and policy

mechanisms

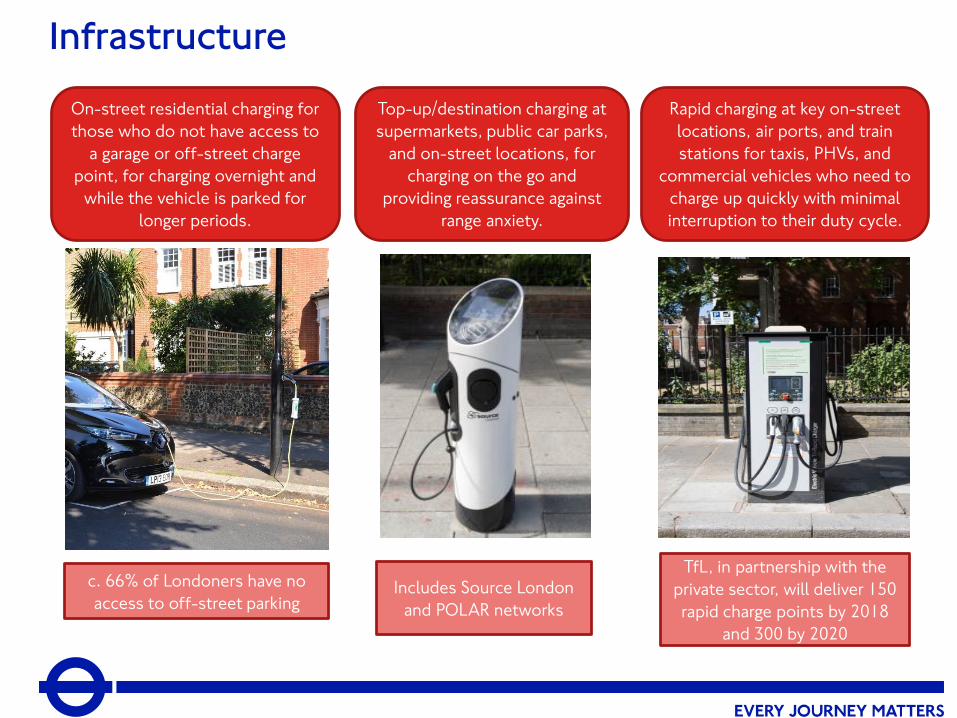

Infrastructure

On-street residential charging for

those who do not have access to

a garage or off-street charge

point, for charging overnight and

while the vehicle is parked for

longer periods.

Top-up/destination charging at

supermarkets, public car parks,

and on-street locations, for

charging on the go and

providing reassurance against

range anxiety.

Rapid charging at key on-street

locations, air ports, and train

stations for taxis, PHVs, and

commercial vehicles who need to

charge up quickly with minimal

interruption to their duty cycle.

c. 66% of Londoners have no

access to off-street parkingIncludes Source London

and POLAR networks

TfL, in partnership with the

private sector, will deliver 150

rapid charge points by 2018

and 300 by 2020

24

London has been awarded £13m from the government to

become a ‘Go Ultra Low’ City by 2020

~1,200 electric vehicle charge points to support residents

without off-street parking (approximately two thirds of

Londoners)

Charging infrastructure for car clubs to help industry

achieve target of 50 per cent of car club fleet to be ULEVs

by 2025

Helping deliver 300 rapid charge points by 2020 for

commercial fleets

Neighbourhoods of the Future - New local schemes

promote innovative charging infrastructure, policies and

initiatives to support the uptake of EVs across different

fleets.

• Industry led, with involvement from cities

across the UK (Manchester, Leeds and

Coventry)

• Economic benefits and health benefits

linked to improved air quality

• Helping fleets prepare for Ultra Low

Emission Zone (ULEZ)

• Already engaging with 700 organisations via

LoCITY

• LoCITY supports the roll-out of

infrastructure for alternatively fuelled

vehicles

LoCITY aims to increase the uptake and

availability of low emission commercial

vehicles as part of the Mayor’s Ultra Low

Emission Vehicle Delivery Plan

LoCITY Programme

LoCITY progress since launch Jan 2016

• Stakeholder engagement including annual

conference, interactive website and social

media

• Industry led working groups:

o vans under 3.5t

o construction and waste HGVs

o HGVs over 3.5t

o Policy, Planning, Procurement and Practice (4Ps)

• Research into:

o operator awareness and knowledge of ultra low emission

vehicles (ULEV)

o technical barriers preventing wider uptake of ULEVs

• Case study videos (electric van and process

evaluation)

• Refuelling and recharging infrastructure map

• Vehicle finder online tool

• Fleet Advice Programme (in progress)

Buses and

Taxis

Mayoral Announcements

• Introducing the ULEZ standards a year

early for double deck buses (2019)

• Single decker buses would meet

minimum Euro VI standard in 2019 and

be all electric or hydrogen in 2020

• Implementing up to 12 Low Emission

Bus Zones – tackling the worst

pollution hotspots by concentrating

cleaner buses on the dirtiest routes

• Only only procuring hybrid or zero emission double deck buses

from 2018

• Expanding the Euro V retrofit programme from 800 to over

4,000 buses and to 5,200 by 2021

• The Mayor wants to deliver the greenest taxi fleet in the world by:• Not licensing any more new diesel taxis and

only licensing new ‘zero emission capable’ taxis from 2018;

• Providing a £3,000 grant towards the first 9,000 ZEC taxis, in addition to the Government’s plug-in car grant;

• Delivering a rapid charging network from 2017;

• Introducing a scrappage scheme for the oldest taxis from 2017;

• Exploring options to convert to a cleaner fuel;

• Rewarding drivers who pioneer green technology, such as zero emission ranks.

29

Taxi Licensing

Private Hire Vehicles

30

• From 2018 all PHVs presented for licensing for the first time must meet either:

– Euro 6 (diesel/petrol) standards.

– At least Euro 4 (petrol-hybrids) emissions standards.

• From 2020:

– All newly manufactured PHVs (less than 18 months old) presented for licensing for the first time must be ZEC.

• From 2023:

– All PHVs presented for licensing for the first time must be ZEC.

Next Steps

Next steps

• Consultation closes on 18 December: tfl.gov.uk/airquality-

consultation or email [email protected].

• Mayoral decision on Emissions Surcharge expected in early

2017

• The Mayor will review the consultation results and decide

whether or not to proceed with further work to develop ULEZ

proposals

• Possible statutory consultation on specific proposals for ULEZ

in 2017

• TfL welcome the opportunity to meet stakeholders who wish

to have more in depth conversations.

• Revision of Mayor’s Transport Strategy and London

Environment Strategy32

Alex Hanson, Consumer IncentivesHeathrow Fleets Conference December 2016

Incentives for ultra-low emission vehicles

Stretching Government goals and funding since 2011 …

R&D Incentives Energy Issues Comms Infrastructure Supply Chain

SPENDING REVIEW

NOVEMBER 2015

The government will spend more

than £600m between 2015-16 and

2020-21 to support uptake and

manufacturing of ultra-low emission

vehicles (ULEVs) …and keep the

UK on track for all new cars to be

effectively zero emission by 2040.

‘Our aim is for almost every car an

van to be a zero emission vehicle

by 2050 ... and we will invest

£500m over the next five years to

achieve it.’

MANIFESTO

MAY 2015

2

Joint ministers

3

Greg Clark - BEIS Chris Grayling- DfT

Nick Hurd - BEIS John Hayes - DfT

Zero emission vehicles? FOUR key UK policy drivers.

Inward Investment

Air Quality

Carbon

Energy Security

4

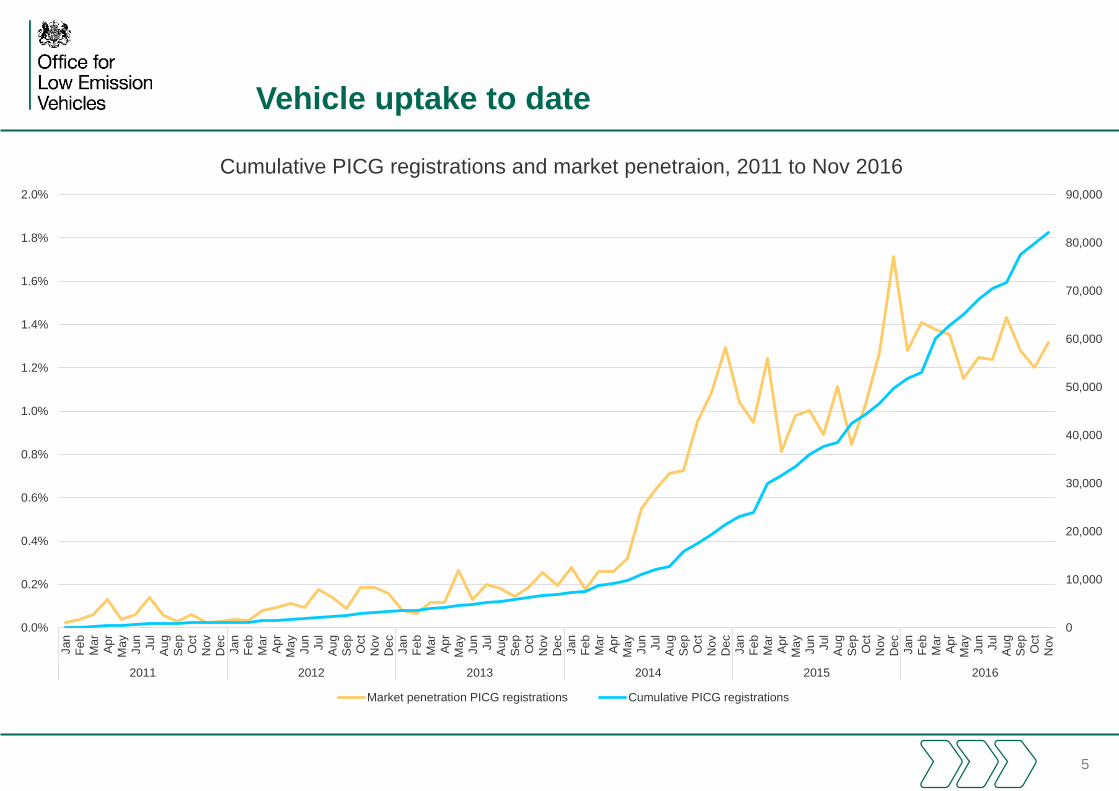

Vehicle uptake to date

5

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

rM

ay

Jun

Jul

Au

g

Se

p

Oct

Nov

2011 2012 2013 2014 2015 2016

Cumulative PICG registrations and market penetraion, 2011 to Nov 2016

Market penetration PICG registrations Cumulative PICG registrations

UK charging network

UK has largest rapid

network in Europe.

96% of motorway rest

areas have 1 – 6 rapids

Over 11,000 publicly

available chargepoints

3, 7 and 22kw

6 major network

operators, 3 UK SMEs

8 regional networks

60,000 residential

chargepoints installed

• Ensure drivers ‘never

more than 20 miles from

a chargepoint on the

strategic road network’

900 43/50kw

chargepoints

Most comprehensive policy programme in the world?

£10m Battery prize

£10m+ Hydrogen

£125m+ Research and development

£30m+ Chargepoint infrastructure

£40m Go Ultra Low Cities

£20m Taxis

£30m Buses

£20m+ Other vehicles

£400m+ Plug-in Car Grant

£15m Highways England chargepoints

£35m London

£2m+ Go Ultra Low comms campaign

+£290m Autumn Statement funding

8

OLEV incentive

schemes

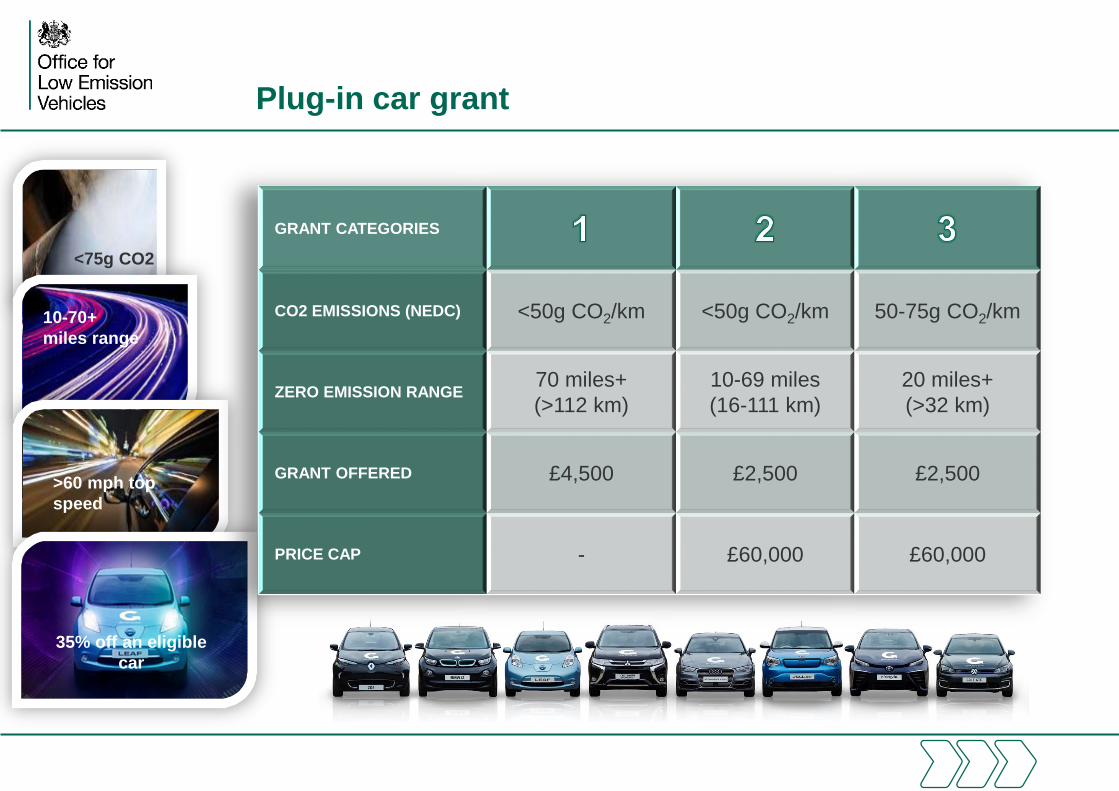

Plug-in car grant

12 D

ecem

ber

2016

12 D

ecem

ber

2016

<75g CO2

10-70+

miles range

>60 mph top

speed

35% off an eligible

car

GRANT CATEGORIES

CO2 EMISSIONS (NEDC) <50g CO2/km <50g CO2/km 50-75g CO2/km

ZERO EMISSION RANGE70 miles+

(>112 km)

10-69 miles

(16-111 km)

20 miles+

(>32 km)

GRANT OFFERED £4,500 £2,500 £2,500

PRICE CAP - £60,000 £60,000

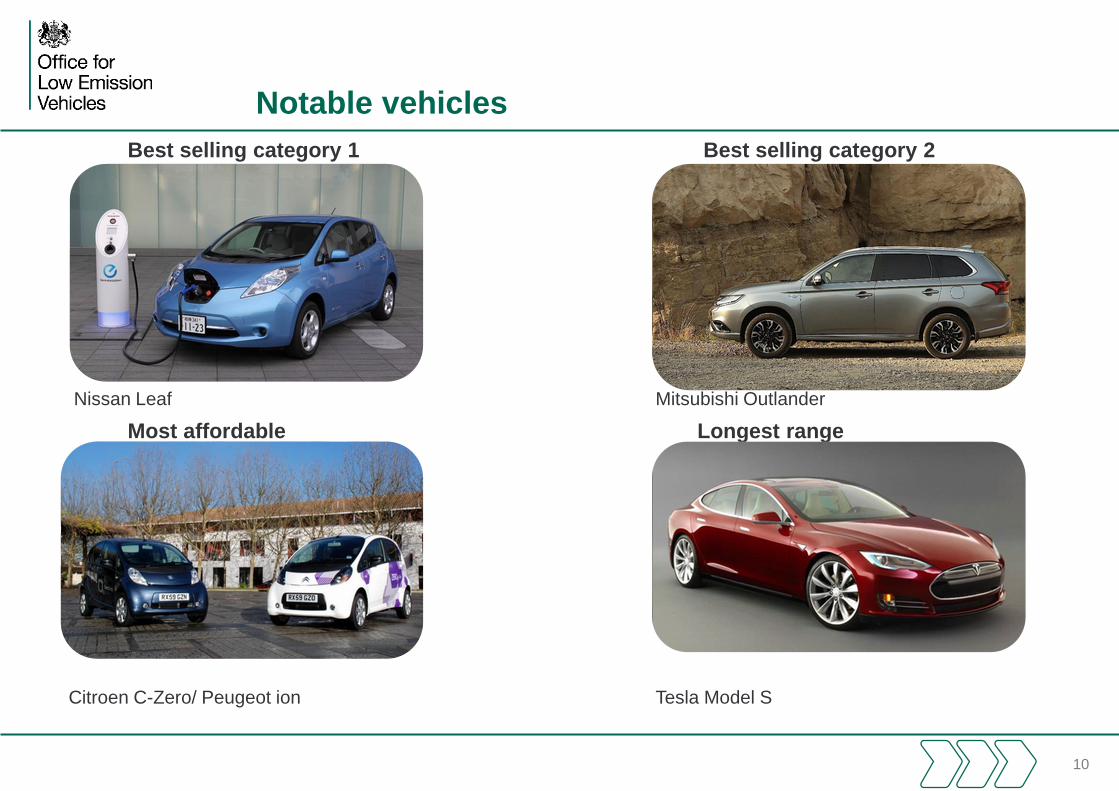

Notable vehicles

Best selling category 1 Best selling category 2

Nissan Leaf Mitsubishi Outlander

Most affordable Longest range

Citroen C-Zero/ Peugeot ion Tesla Model S

10

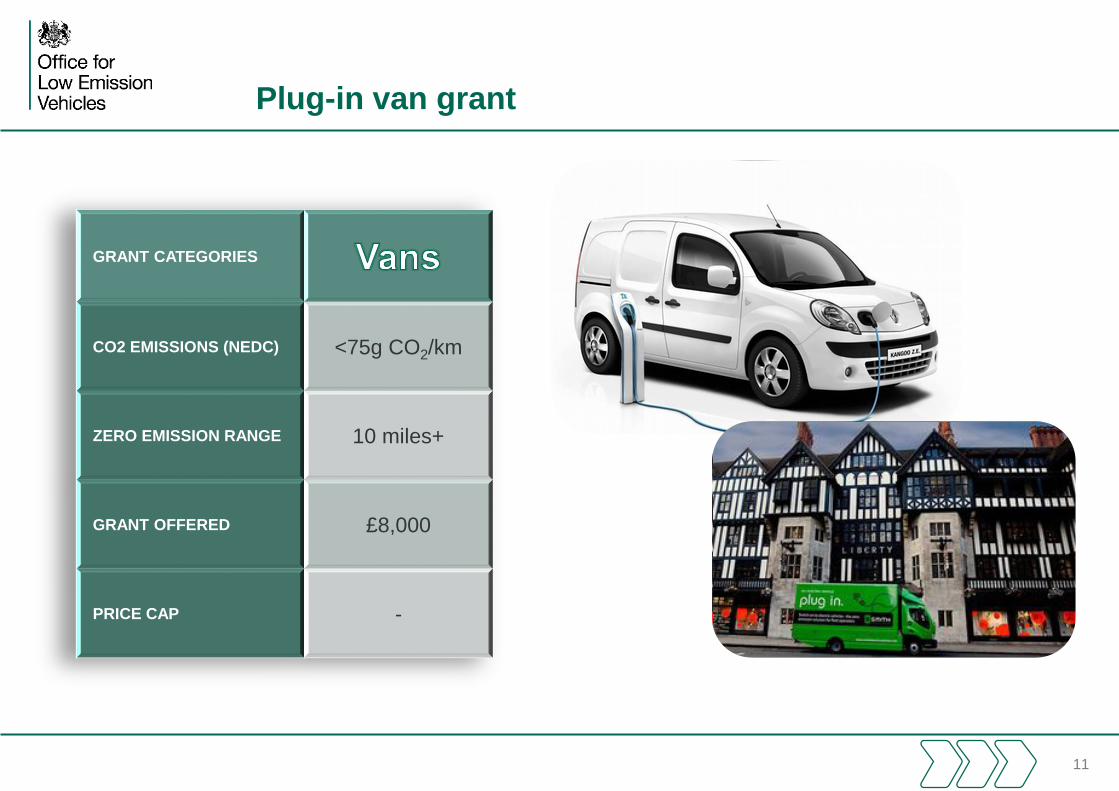

Plug-in van grant

11

GRANT CATEGORIES

CO2 EMISSIONS (NEDC) <75g CO2/km

ZERO EMISSION RANGE 10 miles+

GRANT OFFERED £8,000

PRICE CAP -

Plug-in motorcycle grant

12

GRANT CATEGORIES

CO2 EMISSIONS (NEDC) 0g CO2/km

ZERO EMISSION RANGE 30/50km

GRANT OFFERED £1,500

PRICE CAP -

Workplace charging

13

• Workplace charging

scheme

• 100% first year allowances

to companies investing in

charge points to end of

March 2019

Other infrastructure schemes

On street residential - £2.5m funding committed, details to be confirmed

Electric vehicle homecharge scheme - £500 per vehicle, up to charge points per household

14

Tax

15

Vehicle excise duty

16

VED rates to March 2017 VED rates from 1 April 2017

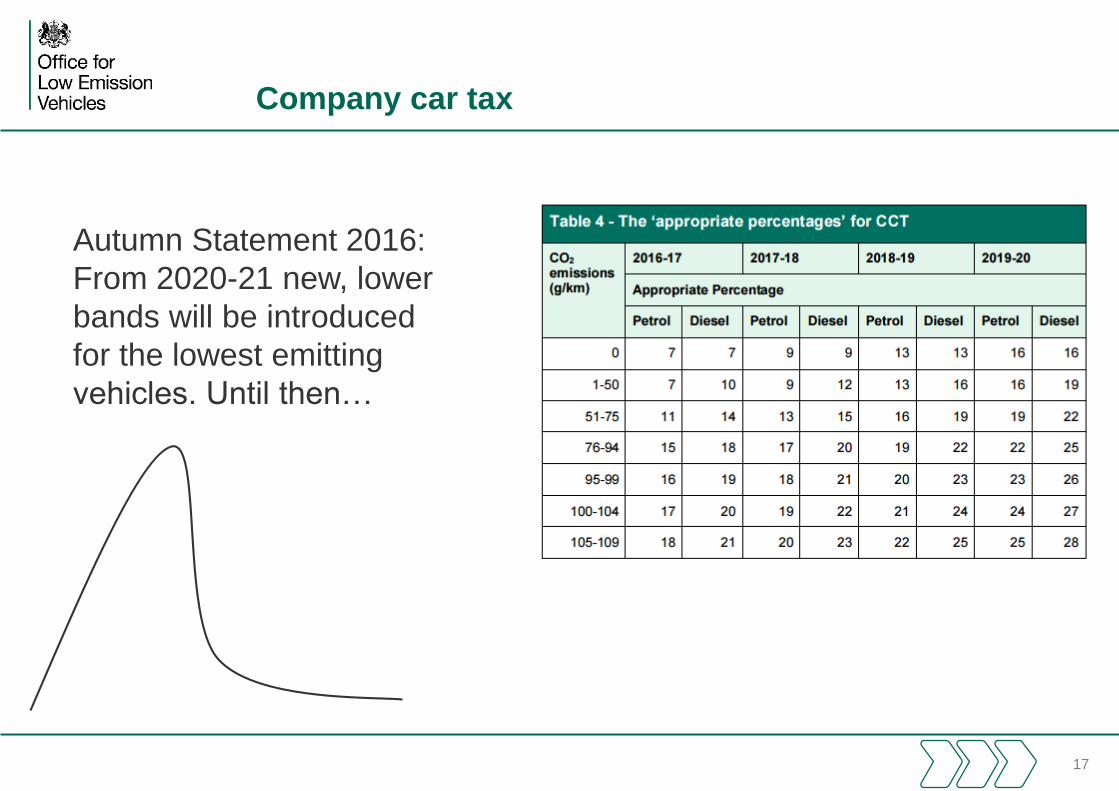

Company car tax

17

Autumn Statement 2016:

From 2020-21 new, lower

bands will be introduced

for the lowest emitting

vehicles. Until then…

Challenges: price and range …

OLEV also does…

19

Real-world performance of diesel vehiclesand lessons for fleets

Jane Thomas

7 December 2016

2

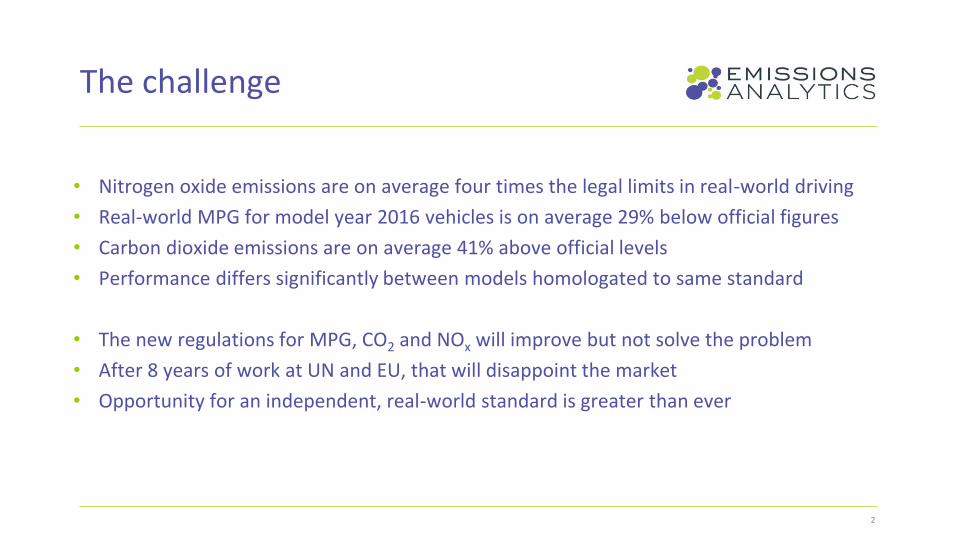

• Nitrogen oxide emissions are on average four times the legal limits in real-world driving

• Real-world MPG for model year 2016 vehicles is on average 29% below official figures

• Carbon dioxide emissions are on average 41% above official levels

• Performance differs significantly between models homologated to same standard

• The new regulations for MPG, CO2 and NOx will improve but not solve the problem

• After 8 years of work at UN and EU, that will disappoint the market

• Opportunity for an independent, real-world standard is greater than ever

The challenge

EMISSIONS ANALYTICS’ PROGRAMME

3

4

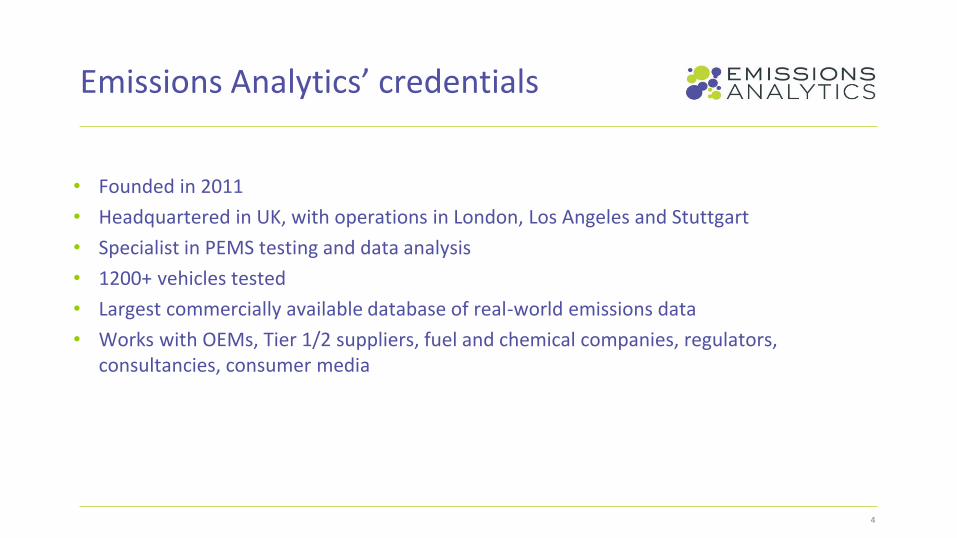

• Founded in 2011

• Headquartered in UK, with operations in London, Los Angeles and Stuttgart

• Specialist in PEMS testing and data analysis

• 1200+ vehicles tested

• Largest commercially available database of real-world emissions data

• Works with OEMs, Tier 1/2 suppliers, fuel and chemical companies, regulators, consultancies, consumer media

Emissions Analytics’ credentials

5

Equipment

• SEMTECH-DS and -LDV

• Portable Emissions Measurement System connects to tailpipe

• Captures emissions for CO2, CO, NO, NO2, total hydrocarbons

• At 1 Hertz

• Air temperature, pressure, humidity

• GPS for speed and altitude

• Engine data via CANBUS

• Fuel economy derived via carbon balance

• Weight addition 100kg

6

• Reproducibility must be weighed against authenticity

• Aim to drive same cycle identically each time

• Control what you can – driver, vehicle conditioning, driving style

• Careful QA of data

• Normalize out as much of remaining variability as possible

Approximate to laboratory

Use better economics of testing to test more cars

Trading slight deterioration in precision for greater sample size

Greater overall confidence

Emissions Analytics concept

7

VEHICLE PERFORMANCE TRENDS

8

9

• Rolling 12-month average of exceedance factor in blue

• Step-change technology launched Q2 to Q3 2014

• No further reduction in Conformity Factor since then

• Average CF dipped to 2.7 in 2014, but risen to 3.5 since then

NOx Conformity Factor

0.00

5.00

10.00

15.00

20.00

25.00

02/1

1/20

11

02/0

1/20

12

02/0

3/20

12

02/0

5/20

12

02/0

7/20

12

02/0

9/20

12

02/1

1/20

12

02/0

1/20

13

02/0

3/20

13

02/0

5/20

13

02/0

7/20

13

02/0

9/20

13

02/1

1/20

13

02/0

1/20

14

02/0

3/20

14

02/0

5/20

14

02/0

7/20

14

02/0

9/20

14

02/1

1/20

14

02/0

1/20

15

02/0

3/20

15

02/0

5/20

15

02/0

7/20

15

02/0

9/20

15

02/1

1/20

15

02/0

1/20

16

Co

nfo

rmit

y Fa

cto

r

Test date

Euro 5/6 NOx diesel Conformity Factor over time

EU REGULATORY CHANGES

10

11

Changes to EU regulations

• Type approval framework changes

• Initiated since dieselgate to tighten legal framework

• WLTC for fuel economy and CO2 regulation

• Multi-stage transition from NEDC

• Real Driving Emissions for NOx regulation, in four “packages”

• #1 – establishing PEMS as a viable technology, preferred to random cycles

• #2 – regulated limits for NOx, and Conformity Factors – published

• #3 – cold start and PEMS-PN (particulate number) regulation – almost complete

• #4 – in-service surveillance – discussions to start late 2016/early 2017

• Monitoring phase currently underway – sharing data but not in force

12

Test cycles

New European Driving Cycle (NEDC)

World Light Duty Transient Cycle (WLTC)

Real Driving Emissions (RDE)

Emissions Analytics

Measurements MPG, CO2, CO, NOx MPG, CO2, CO, NOx NOx

MPG, CO2, CO, NOx, NO, NO2

Cycle Defined speed trace Defined speed traceUndefined with

aggregate and dynamic constraints

Defined route

Test location Laboratory Laboratory On road with PEMS On road with PEMS

Conduct By OEM By OEM By OEM Independent

Normalisation None NoneCO2 windows or power

binningBased on dynamic

characteristics

Average speed (mph) 21 29 Varies 28

Average acceleration (mph/s) 1.1 1.0 Varies 1.5

Average gradient (m/s) 0.0 0.0 Varies 0.8

13

Issues with Real Driving Emissions

• Conformity Factors

• 1.5 does not come fully into force until January 2021

• Initial 2.1 factor set to be achieved by all OEMs with just software changes

• No further reductions guaranteed

• Normalization tools

• Competitive tools: EMROAD and CLEAR, using different principles

• Transfer function: to increase number of valid points through modelled transformation

• PEMS-PN

• Unproven test equipment, industry push-back

• Structural

• Asymmetry of expertise between European Commission and OEMs

• Lack of appetite to create powerful, central EU regulator

14

• Conformity factor initially 2.1 – 168 mg/km

• Further increased by exclusions due to boundary conditions

• PEMS test-to-test variability of 30%, so OEMs will need to target ~129 mg/km to avoid getting caught by in-service surveillance

• 1 in 5 vehicles already meet this

Will Real Driving Emissions help?

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

14/09/2011 01/04/2012 18/10/2012 06/05/2013 22/11/2013 10/06/2014 27/12/2014 15/07/2015 31/01/2016

Con

form

ity

Fact

or

Test date

Euro 5 Euro 6

INDEPENDENT RATINGS FOR FLEETS

15

16

• Vehicle rating scheme based on their real-world NOx emissions, launched in April 2016

• Non-statutory complement to new Real Driving Emissions regulations

• But will also

• Discriminate between high and low emitters, rather than just pass/fail

• Be updated for each model year to keep up with new calibrations

• Ratings are published and into the public domain for free

• Manufacturers and consumer media can adopt as independent, voluntary standard

• Similar to New Car Assessment Programme (Euro NCAP, Global NCAP)

Robust, independent standard needed to measure and incentivize actions to bring about air quality improvements

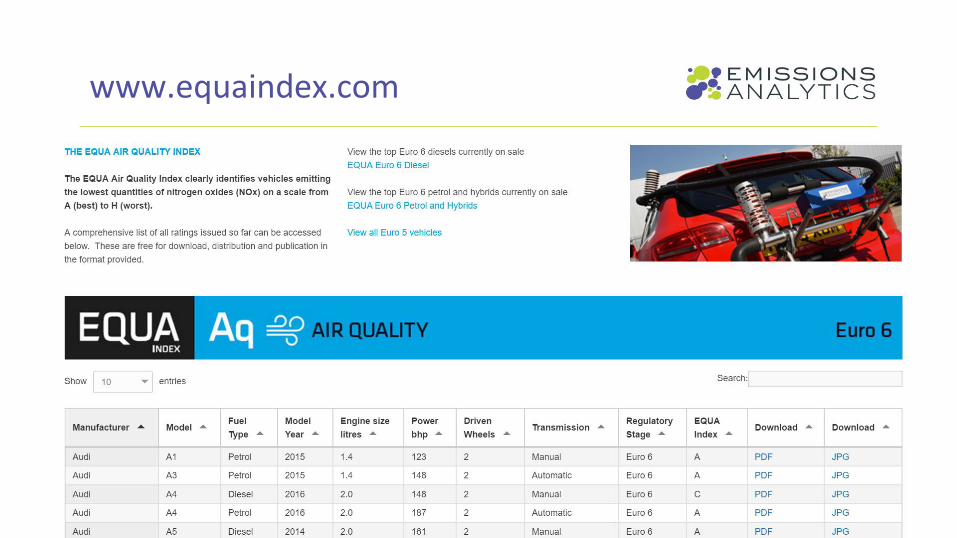

EQUA Air Quality Index

17

www.equaindex.com

18

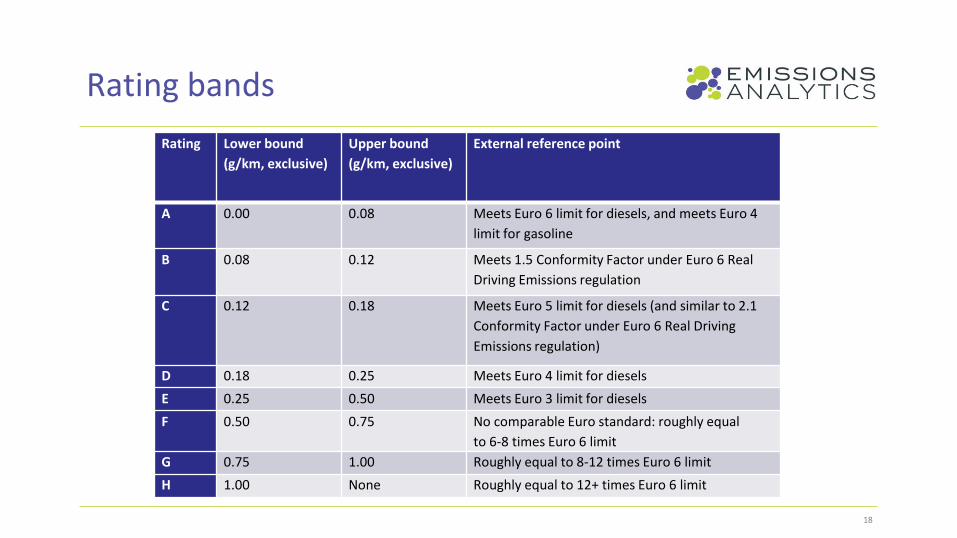

Rating bands

Rating Lower bound

(g/km, exclusive)

Upper bound

(g/km, exclusive)

External reference point

A 0.00 0.08 Meets Euro 6 limit for diesels, and meets Euro 4

limit for gasoline

B 0.08 0.12 Meets 1.5 Conformity Factor under Euro 6 Real

Driving Emissions regulation

C 0.12 0.18 Meets Euro 5 limit for diesels (and similar to 2.1

Conformity Factor under Euro 6 Real Driving

Emissions regulation)

D 0.18 0.25 Meets Euro 4 limit for diesels

E 0.25 0.50 Meets Euro 3 limit for diesels

F 0.50 0.75 No comparable Euro standard: roughly equal

to 6-8 times Euro 6 limit

G 0.75 1.00 Roughly equal to 8-12 times Euro 6 limit

H 1.00 None Roughly equal to 12+ times Euro 6 limit

19

Diesels with A ratings

20

www.equaindex.com

21

www.equaindex.com

22

www.equaindex.com

• MPG values for almost all vehicles on sale in last five years

• Over 66,000 model variants

• Around 5,000 test values

• Remainder extrapolated using new proprietary model of real-world MPG, based on technical characteristics of vehicles

Comprehensive alternative to official system

23

EQUA CO2

• “A1” to “H5”

• A to H for absolute emissions

• 1 to 5 for proximity to official –“honesty”

• 39% average CO2 excess – 189 g/km

• 16% higher emissions from petrol compared to diesel

• 1.5 litre engines better than most highly down-sized

• 2.0-3.0 litre engines most honest

IMPLICATIONS FOR FLEETS

24

25

EU fuel economy trends

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

2011 2012 2013 2014 2015

Fu

el

eco

no

my

(M

PG

)

Model Year of vehicle tested

Diesel - EQUA Mpg Diesel - official Petrol - EQUA Mpg Petrol - official

• Real-world average diesel MPG declining since 2012

• Official MPG kept rising until 2014, but even that now declining

• Gasoline still showing gently improving trend

• No mix correction

26

EU fuel economy gap

• Diesel gap sharply increasing

• Weaker trend for gasoline

• (Low sample size in 2011)

-32.0

-30.0

-28.0

-26.0

-24.0

-22.0

-20.0

2011 2012 2013 2014 2015 2016

EQU

A M

pg

vari

ance

to

off

icia

l MP

G

Model Year of vehicle tested

Diesel Petrol

27

Perils of downsizing

-45.0

-40.0

-35.0

-30.0

-25.0

-20.0

-15.0

-10.0

-5.0

0.0

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

EQ

UA

Mp

g v

ari

an

ce t

o o

ffic

ial M

PG

Engine size class (litres)

Diesel Petrol

• The smaller the engine, the bigger the gap between real-world and official MPG

• Sub-1.5 litre gasoline engines have particularly large deficits

• NEDC rewards downsizing, but 1.5-2.0 litre optimal for mixed driving in reality

28

Opportunities

• Provide EQUA Index data on fleet websites and in documentation to enable consumers to make better informed decisions

• Construct vehicle lists in knowledge of real-world emissions

• Better match consumers to their usage, and increase satisfaction

• Incorporate EQUA Mpg into total cost of ownership models

• Corporate Social Responsibility reporting

29

Issues?

• WLTC will be the real-world solution for MPG and CO2 – it won’t

• Manufacturers won’t like it – they are using EQUA already

• Is PEMS valid for measuring MPG – PSA are doing it

• Will it confuse consumers? It is the solution to the confusing transition from NEDC to WLTC

• Hiding behind official figures has been proven to be dangerous – NEDC

Opportunity in a consistent, independent, real-world performance currency

A Strategic Approach

to EV Infrastructure at

Heathrow Clean Vehicles Partnership

7 Dec 2016

Andrew Chen- Emissions Strategy Manager,

Heathrow

Heathrow first published an Air Quality Strategy & Action Plan in 2000

and in 2014 published an additional target to reduce ground-based

NOx emissions through Responsible Heathrow

LEVEL 1 LEVEL 2 LEVEL 3 LEVEL 4 LEVEL 5

AVOIDING RISKBEING SEEN

TO BE GOOD

‘DOING’

SUSTAINABILITY

LIVING

SUSTAINABILITY

LEADING

SUSTAINABILITY

Avoid Risk

PR for Reputation

Take Action

Integrate into Core Business

Leverage Value Through Business ModelsA

CT

IVIT

Y

From Responsible Heathrow

to Level 5 leadership

Sustainability Strategy

We will deliver, partner and advocate

to fulfil our vision. By working with

others we can create a better, fairer

future.

It’s our long term vision to create

a place where people are proud

to live, work, travel and progress.

Aircraft activity

1) Reduce emissions from aircraft at the gate

2) Phase out oldest and dirtiest aircraft

3) Improve taxiing efficiency

Airport traffic

4) Provide more and better EV charging points

5) Incentivise low-emission vehicles

6) Work with partners to set up emission zones and

standards

Vehicles airside

7) Reduce emissions from our own fleet

8) Pool vehicles to reduce numbers and emissions

9) Lead the move to electric vehicles airside

Energy

10) Modernise our heating supply

In 2015 we also published a “Blueprint for reducing

emissions” to set out a clear narrative and commit to ten

tangible actions to reduce emissions by the end of 2015

In 2016 we published our second “Blueprint

for reducing emissions” with ten tangible

actions to reduce emissions in 2016

Aircraft activity• Bring in the newest and cleanest aircraft

• Continue to drive down emissions from aircraft at the gate

• Improve taxiing efficiency

Airport traffic • Charge forward with electric cars and buses

• Heathrow Cycles

• Drive sustainable freight operations

Airside vehicles• Plug in more electric airside vehicles

• Provide a pool of low emission vehicles

• Efficient driver training and education

Vehicle emissions

programmeHeathrow is committed to improving local air quality by working collaboratively with the airport community

to reduce emissions. By increasing vehicle efficiency, reducing vehicle journeys and improving charging

infrastructure; The Vehicle Emissions Programme will work with all stakeholders to support Heathrow’s

commitment to reduce ground-based NOx emissions.

Vehicles Leadership Group (VLG)Role: Provide leadership, steer, challenge and decisions to ensure alignment between strategy, programme outputs and operations

whilst meeting the emissions target

WS1: HAL, Supplier & 3rd party (Airside) Fleet Efficiency

Vehicles Working Group (VWG)Role: Share work stream plans, progress, risks & issues to ensure

collaboration, coordinated delivery and management of dependencies

WS2: Surface Access Fleet

Efficiency

WS4: Strategy and Engagement

WS3: Vehicle Charging

Infrastructure

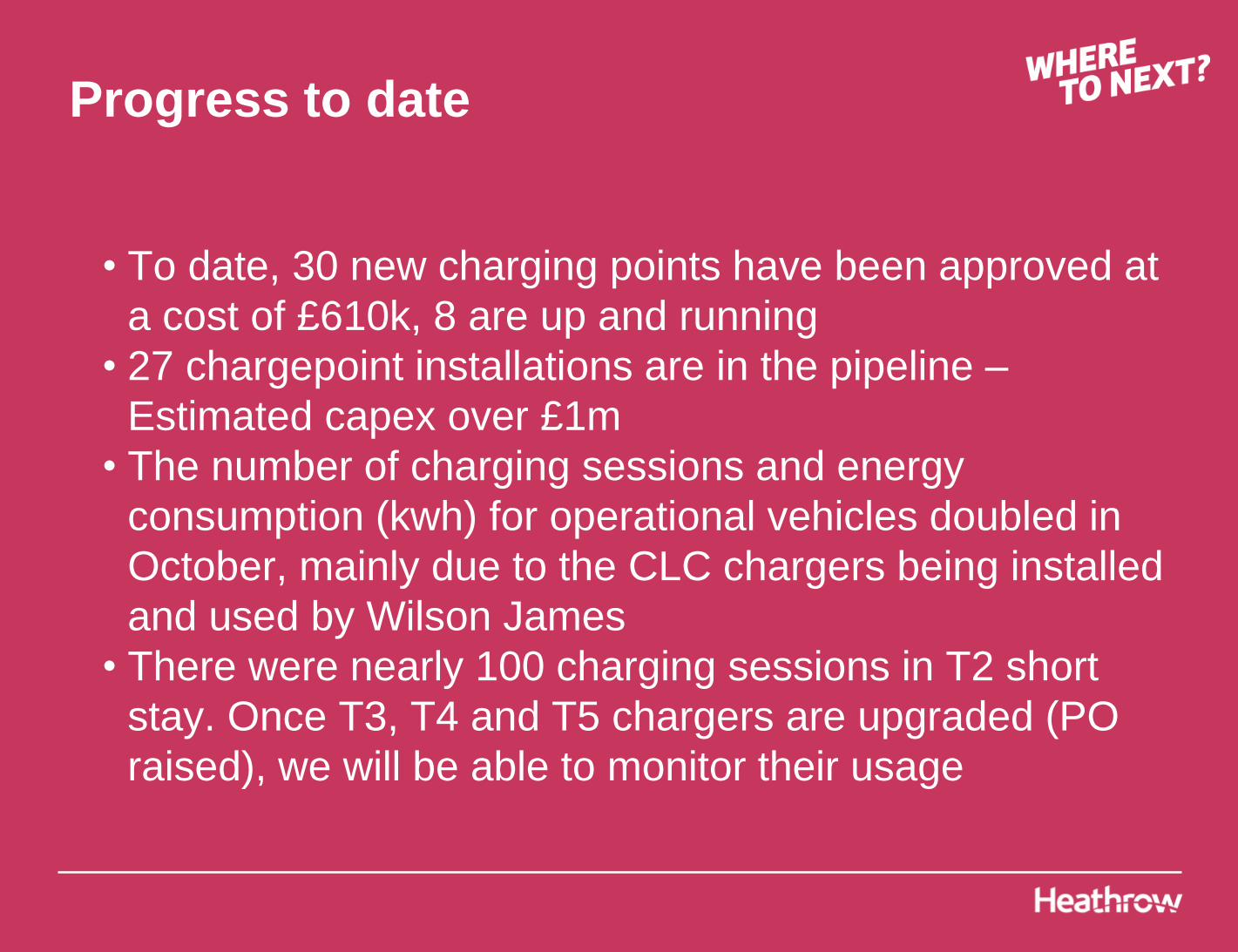

Progress to date

• To date, 30 new charging points have been approved at

a cost of £610k, 8 are up and running

• 27 chargepoint installations are in the pipeline –

Estimated capex over £1m

• The number of charging sessions and energy

consumption (kwh) for operational vehicles doubled in

October, mainly due to the CLC chargers being installed

and used by Wilson James

• There were nearly 100 charging sessions in T2 short

stay. Once T3, T4 and T5 chargers are upgraded (PO

raised), we will be able to monitor their usage

Electric Vehicle Infrastructure at Heathrow Airport

Evidencing Demand

Heathrow Airport CVP Seminar

7th December 2016

Jacob Roberts, Technical Project Manager

Ian Featherstone, Fleet Knowledge Manager

Intro to Energy Saving Trust’s Transport Team

The Energy Saving Trust

Set up to support

Government

Independent and impartial

Long history supporting

organisations

Not for profit

Wide range of EV work

(OLEV, DfT, TfL, Commercial)

Unique expertise in EV

infrastructure mapping

Saving energy and reducing

emissions at our core

Wide network of partners

Experts from across industry

and public sector

Background

The Challenge: Air Quality

Poor air quality is thought to cause 9,500 premature

mortalities in London every year

The Ultra-Low Emission Zone (ULEZ) is central to Transport

for London’s plans to decrease NOx concentrations in

Greater London – especially in Central London

Outside of Central London,

Heathrow Airport is the most

visible area of poor air quality

Ultra-Low Emission Vehicles (ULEVs)

ULEVs emit no tailpipe emissions and therefore do not

contribute to local air pollution

This makes ULEVs a significant part of how we can improve

urban air quality

They do not necessarily need to be electric or plug-in hybrid

vehicles, but these are the most readily available at present

Electric Vehicles at Heathrow Airport

17.6% of air pollution at Heathrow Airport is caused by

ground vehicles, airside and landside

Increasing the amount of ULEVs at Heathrow is central to

how HAL plan to improve air quality

To make plug-in vehicles feasible… you need somewhere to

plug them in!

Evidencing Demand for Charging Infrastructure

Our Project

Heathrow have commissioned EST to produce a report to

answer some key questions.

How many electric vehicles could realistically operate at Heathrow?

Where, how much and what type of charging infrastructure would be

required to meet demand?

What will the air quality benefits of the electric vehicle adoption be?

What can Heathrow do to encourage electric vehicle use, besides provide

infrastructure?

How many vehicles?

Some vehicles operating airside at Heathrow Airport already

have a suitable electric alternative

These vehicles are cars, small vans and MPVs

How many vehicles?

As the electric vehicle market develops, electric alternatives

to many other vehicles types will become available

Large electric vans are beginning to come onto the market

and will likely be widely available in 3-5 years

Manufacturers are currently developing and trialling electric

HGVs

How many vehicles?

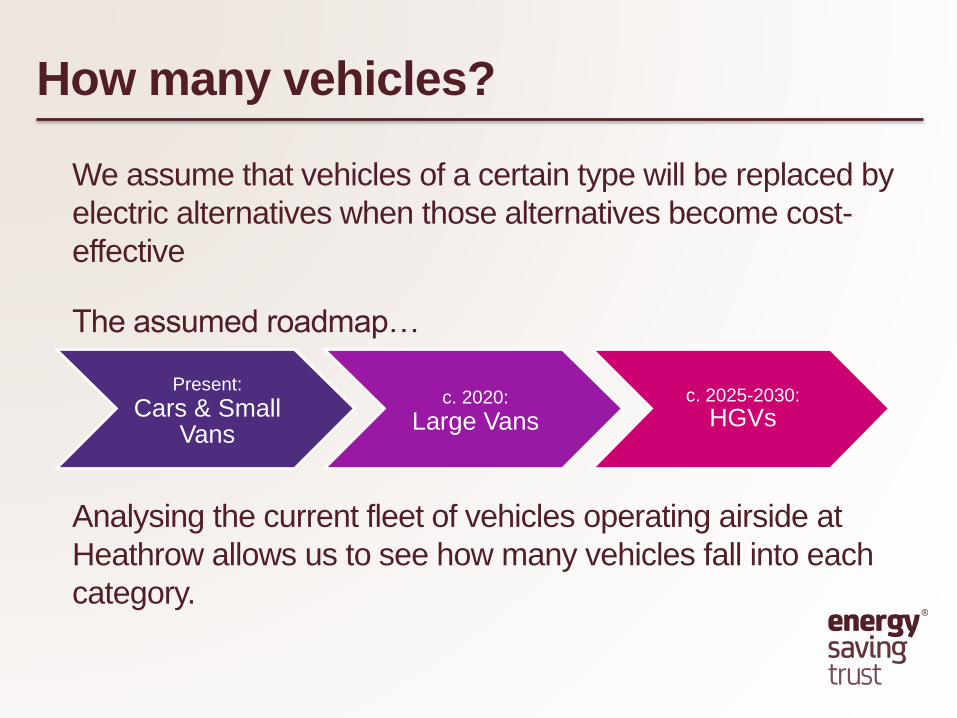

We assume that vehicles of a certain type will be replaced by

electric alternatives when those alternatives become cost-

effective

The assumed roadmap…

Analysing the current fleet of vehicles operating airside at

Heathrow allows us to see how many vehicles fall into each

category.

Present:

Cars & Small Vans

c. 2020:

Large Vansc. 2025-2030:

HGVs

Charging infrastructure?

Through telematics data, we determine three key factors

required to recommend location, type and quantity of electric

vehicle charging points

Combining this with what we know about the existing

vehicles, we can calculate how much electricity will be

required and how quickly > the chargepoint type

Typical daily mileage

Where vehicles stop

How long they stop for

For example…

Take a Ford Fiesta…

If this vehicle were electric, we at least know where the

chargepoint needs to go

45 miles per

day

Stops at the

canteen for an

hour at lunch

time

For example…

Take a suitable electric alternative…

You know where the vehicle stops, how long it stops for and

how much electricity needs to be delivered in that time

45 miles per

day

Stops at the

canteen for an

hour at lunch

time

Roughly

0.3kWh per

mile

How many chargepoints?

Using telematics to understand how many vehicles are

stopped at that location at the same time allows you to infer

how many chargepoints will be required.

The process of analysing the vehicles stopping at a location

and determining the number of vehicles stopped at the same

time is repeated across all locations where vehicles

commonly stop.

Summary

Summary: What evidence is needed?

Vehicle registration

number

Make Model

Telematics

Daily mileage

Where the

vehicle stops

How long the vehicle stops

for

Thank you for listening

Any questions?

Ian FeatherstoneFleet Knowledge Manager

T: 020 7227 0312

M: 07769 742930

Jacob RobertsTechnical Project Manager

T: 020 7654 2613

M: 07447 947353

ELECTRIC VEHICLES

John Edmunds

Business manager

Quick word from the sponsor

Introduction

• Dnata’s interest in EV

• Cost potential savings

• What have we used and why

• The road a head

Dnata’s interest in EV

• Government commitment – global warming

• CVP working group – (this forum)

• Other Airport/handler Experience

• Airport authority

• Reduction in emissions

• Potential savings - benefits

Costs - Benefits

• Purchase EV More expensive than our normal purchase

EV more expensive to lease

• MaintenanceNo oils, filters etc

3 x cheaper to run electric car

No issues with diesel particulate filters or catalysts

Fewer running parts

Support at dealerships needs to be better

Cost - Benefits

• Fuel• EV far cheaper to run particularly in an airport environment

• 6th of the cost

• Infrastructure is better but still needs improvement

What we have used -

The Road a head

• Chicken or the egg – or in this case charger or the EV

• Charging areasPier 7 Chargers – Electric lifter

Freemantle/HAL – Pier 6 Project

HAL EV Charging Project

Questions