Embed Size (px)

Citation preview

Journal of Accounting and Economics 17 (1994) 281-3b8. North-Holland

Debt-covenant violations and managers’ accounting responses

Amy Patricia Sweeney* Harvard University, Boston, MA 02163, USA

Received October 1992, final version received September 1993

This paper examines accounting changes, costs of default, and accounting-based covenants violated by 130 firms reporting violations in annual reports. I find that managers of firms approach- ing default respond with income-increasing accounting changes and that the default costs imposed by lenders and the accounting flexibility available to managers are important determinants of managers’ accounting responses. I also document that private lending agreements are the first violated, that net worth and working capital restrictions are the most frequently violated restric- tions, and that in 52 percent of the cases lenders require concessions from borrowers to resolve default.

Key words: Contracting; Accounting choice; Covenant violations

JEL classification: M40; G30

1. Introduction

Debt indenture provisions are hypothesized to be important determinants of managers’ accounting-policy choices. The extant empirical evidence is mixed.l Cross-sectional accounting-choice studies generally support the Debt Hypothe- sis: Ceteris paribus, the larger a*rm’s debt-equity ratio, the more likely thejrm’s

Correspondence to: Amy Patricia Sweeney, Graduate School of Business Administration, Harvard University, Boston, MA 02163, USA.

*I am grateful for the guidance and valuable comments of my dissertation committee: Andrew Christie, Clifford Smith, Jerry Zimmerman, and especially Ross Watts. I wish to thank Ray Ball (the editor), George Foster (the referee), Patricia Dechow, Krishna Palepu, Richard Sloan, and workshop participants at the Harvard Business School and the University of Michigan for valuable comments. I am grateful for financial support from the University of Rochester, the Arthur Andersen & Co. Foundation, and the Division of Research, Harvard Business School.

‘For a review of the literature see Holthausen and Leftwich (1983) Watts and Zimmerman (1986), or Christie (1990).

0165-4101/94/$07.00 0 1994---Elsevier Science B.V. All rights reserved

282 A. P. Sweeney, Debt-couenant violations and managers’ accounting responses

manager is to select income-increasing accounting procedures.’ However, recent time-series studies that examine managers’ accounting choices when firms are close to violating debt-covenant constraints present mixed results [see Healy and Palepu (1990), DeFond and Jiambalvo (1994), and DeAngelo, DeAngelo, and Skinner (1994)].

To provide a direct test of the proposition that managers change accounting procedures in response to tightening debt-covenant constraints, I examine the time series of managers’ accounting choices prior to firms violating accounting- based restrictions in debt agreements. I document whether managers change accounting procedures, which types of accounting procedures managers change, when managers make these changes, and to what extent these changes affect the restrictiveness of accounting-based covenants.

The results indicate that managers of firms approaching violations of ac- counting-based restrictions are more likely to make income-increasing dis- cretionary accounting changes and early adopt income-increasing mandatory accounting changes than control firms, matched on industry, size, and time period. Since the literature provides no theory of efficient accounting-policy choice in the absence of managerial manipulation, I rely upon this control group to provide a benchmark of efficient accounting-policy choice. The absence of an ideal control group (differing only with respect to closeness to covenants), leaves the results open to several interpretations.

One interpretation is that managers make accounting changes to offset increases in the tightness of accounting-based restrictions as their firms approach technical default.3 Another is that managers of default firms switch to the most efficient set of accounting choices for their financially distressed firms. While I cannot distinguish between these hypotheses because the latter hypothesis is not well-specified, I can test a more specific form of the efficiency- based hypothesis: the Cash-Management Hypothesis. Since the default firms experience a decline in operating cash flows prior to technical default (while the control firms do not), default managers have incentives to make cash- increasing changes. While the large majority of the accounting changes made by the default firms are cash-increasing, the default firms also make a signifi- cantly greater number of income-increasing, non-cash-increasing accounting changes than do the control firms. Further, cross-sectional analysis suggests that managers of default firms change accounting procedures in response to declines

21ncome-increasing accounting procedures refers to ‘accounting procedures that shift reported earnings from future periods to the current period’ [see Watts and Zimmerman (1986, p. 216)].

3Technical default is failure to comply with covenants in debt agreements, versus debt seroice default which is failure to make an interest or principal payment. Both types of default can be defined as events ofdefault which give lenders the right to take certain actions, such as calling the loan and seizing collateral.

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 283

in net worth rather than declines in operating cash flows. Thus, the cash-management hypothesis does not fully explain managers’ accounting

responses. Since my sample selection procedure requires firms to ex post violate

debt-covenant constraints, none of the firms examined in this study circumvents constraints and avoids violation completely. This selection bias may result in a sample of default firms that do not change accounting procedures because these firms required large earnings effects to delay technical default and/or these firms had few opportunities to increase income via accounting changes. Thus, the selection procedure biases against the null hypothesis that managers switch to income-increasing accounting procedures in years surrounding default.

In this paper, I extend the prior literature in several ways. First, I provide different and potentially more powerful tests of the covenant-based hypothesis by examining firms that violate minimum net worth and working capital covenants rather than dividend constraints [see Healy and Palepu (1990) and DeAngelo et al. (1994)] and by analyzing accounting changes rather than abnormal accruals [see DeFond and Jiambalvo (1994) and DeAngelo et al. (1994)]. This is the first study to document the changes in accounting methods managers make in response to debt-covenant violations. Second, I document whether accounting changes actually delay violation of accounting- based restrictions for one or more accounting periods. Finally, this paper provides evidence that managers’ accounting responses depend on whether default costs are imposed by creditors, whether managers have accounting flexibility, and whether significant tax costs are associated with the available accounting changes. In aggregate, this paper provides the most direct evidence to date in support of the covenant-based hypothesis that managers of firms approaching technical default respond with income-increasing accounting changes.

This study is organized as follows. Section 2 reviews relevant prior research and describes how the empirical tests conducted in this paper differ from other studies. Additional hypotheses are also developed in section 2. Section 3 de-

scribes the sample selection procedures for the default and control samples. A description of which accounting-based restrictions are most frequently viol- ated and a description of the default costs imposed on the violation firms is provided in section 4. In section 5, I document the voluntary and mandatory accounting changes managers make in the years surrounding technical default. Since all managers do not change accounting procedures in the years surround- ing technical default, section 5 explores whether managers’ accounting responses depend on the default costs imposed by creditors and the accounting flexibility available to managers. Using 22 cases, section 6 documents whether managers’ accounting changes actually delay technical default for one or more accounting periods. Section 7 concludes.

284 A.P. Sweeney, Debt-rovenant violations and managers’ accounting responses

2. Relation to prior research

A well-established hypothesis in the accounting literature is that managers change accounting policies to circumvent accounting-based restrictions found in debt agreements (i.e., the Covenant-Based Hypothesis). Early studies do not test the covenant-based hypothesis directly. Instead, early studies use firms’ debt-equity ratios as proxies for closeness to covenant constraints and test the debt hypothesis.4 Christie (1990) aggregates existing cross-sectional results and finds support for the debt hypothesis. Researchers interpret support for the debt hypothesis as evidence that managers change accounting policies to circumvent accounting-based restrictions found in debt agreements. However, firms exam- ined in existing cross-sectional studies are not necessarily close to their debt- covenant constraints at the point in time examined. Watts and Zimmerman (1990) question whether the documented association between leverage and accounting choice is misinterpreted by researchers as resulting from managerial opportunism, when in fact it results from the correlation between firms’ invest- ment opportunity set, financial policy, and their efficient set of accounting methods (i.e., the Efficiency-Based Hypothesis).5 Further, since it is costly for firms to switch back and forth between accounting procedures, firms’ current accounting policies depend on historical accounting policy choices and the time series of variables hypothesized to influence accounting policy [see Sweeney (1992)]. Thus, cross-sectional studies do not provide the most direct nor most powerful tests of the relation between accounting choice and debt contracts.

To provide more powerful tests, three recent studies examine the time series of managers’ accounting choices when firms are close to violating debt-covenant constraints6 Results from these time-series studies are mixed. Healy and Palepu (1990) document firms’ accounting and dividend responses to an increase in the

4Duke and Hunt (1990) and Press and Weintrop (1990) provide empirical evidence to support the validity of the debt-equity ratio as a proxy for the existence and closeness to debt-covenant constraints.

‘While Skinner (1993) finds that firms’ investment opportunities do affect the nature of their contracts, he also finds that the ‘traditional’ explanations for accounting choice are important after controlling for the effects of the investment opportunity set.

‘Several other papers examine the time series of managers’ accounting choices, but firms examined in these studies are not necessarily close to violating debt-covenant constraints. Schwartz (1982) examines the accounting changes made by firms that fail a financial liquidity screening. Schwartz concludes that managers make accounting changes to improve financial appearances and ‘influence the market’s perception of a firm’s staying power and creditworthiness’. Koch (1991) finds that firms with increased technical-default probabilities, as measured by Value Line’s financial strength ratings, are more likely than firms with low technical-default probabilities to make accounting changes that increase net income. Lilien, Mellman, and Pastena (1988) contrast over a ten-year period the patterns of accounting changes of successful and unsuccessful firms. Contrary to their expectations, they document that unsuccessful firms make more income-reducing ac- counting changes than successful firms.

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 285

tightness of dividend constraints. They conclude that firms cut dividends but do not make accounting changes to circumvent the dividend restriction. DeAngelo, DeAngelo, and Skinner (1994) examine accounting choices of 76 NYSE firms with persistent losses and dividend reductions, about 40 percent of which are forced by binding dividend covenants. They find that managers’ accounting choices primarily reflect acknowledgment of their firms’ financial difficulties (via negative abnormal accruals and discretionary write-offs), rather than attempts to inflate reported income. DeFond and Jiambalvo (1994) examine the abnor- mal accruals of 94 firms that report covenant violations in annual reports. In contrast to DeAngelo et al., DeFond and Jiambalvo find that in the year prior to violation, abnormal accruals are positive and significant. In the year of viola- tion, DeFond and Jiambalvo find some evidence of positive abnormal accruals after controlling for management changes and auditor going-concern qualifica- tions.

In this paper, I provide different and potentially more powerful tests of the covenant-based hypothesis by analyzing accounting changes rather than abnor- mal accruals and by examining firms that violate minimum net worth and working capital covenants rather than dividend constraints. Interpretation of the abnormal accrual evidence is difficult for several reasons: (i) changes in accruals exhibit negative serial correlation [see Dechow (1993)]; (ii) changes in accruals are correlated with changes in the levels of firms’ economic activities [see Dechow, Sloan, and Sweeney (1993)]; and (iii) abnormal accrual measures misclassify the income effects of some accounting changes, such as LIFO liquidations. Thus, I analyze accounting changes rather than abnormal accruals. Healy and Palepu (1990) examine firms that are close to violating dividend constraints, a negative covenant. Negative covenants preclude or limit certain investment and financing activities unless certain accounting-based conditions are met [see Smith and Warner (1979) and Leftwich (1983)]. I examine firms that violate affirmative covenants, such as minimum net worth and working capital restrictions. Affirmative covenants require firms to maintain specified levels of accounting-based ratios, stocks, or flows. Empirically firms violate affirmative covenants; firms rarely violate negative covenants (see section 4). Violation of an affirmative covenant is an ‘event of default’ giving lenders the option to acceler- ate maturity of the debt [see Castle (1980)]. However, lenders do not have the right to call a loan simply because a negative covenant is binding. For an ‘event of default’ to occur in connection with a negative covenant managers must pay dividends or issue new debt when debt covenants restrict such actions. There- fore, as discussed by Healy and Palepu, violations of affirmative covenants are more likely than violations of negative covenants to trigger accounting re- sponses.

I also extend prior work by conditioning the expected accounting response on two assumptions underlying the covenant-based hypothesis: (i) that technical default is costly and (ii) that a manager has the accounting flexibility needed to

286 A.P. Sweeney, Debt-covenanl violations and managers’ accounling responses

respond to the ensuing default. In years prior to a reported violation, if technical default is going to occur under one accounting method, then the manager is expected to switch methods to avoid the violation. However, a manager is expected to switch methods only if income-increasing changes are available and only if the manager expects lenders to impose default costs. Thus, if the covenant-based hypothesis provides a valid interpretation of the basic results of this paper, then managers of firms having accounting Jiexibility and bearing default costs ought to be more likely to make income-increasing accounting changes in response to tightening debt-covenant constraints than managers offirms not having accounting Jlexibility and/or not bearing default costs.

I also hypothesize that managers change to income-increasing accounting procedures while in technical default. Often a firm remains in technical default for several years and frequently the costs of default are imposed only while the firm remains in default. For example, Omnimedical’s 1983 annual report indicates that ‘an amendment to the [violated] credit agreement provides for a l/2% increase in the interest rate for each quarter the company is not in compliance with the covenants of this agreement’. In another example, Nashua Corpora- tion’s 1983 restructuring agreement created a security interest in substantially all of the company’s assets for the benefit of lenders until either (i) Nashua prepays at least $18 million in borrowings from the proceeds of an offering of its capital stock or (ii) Nashua’s consolidated tangible net worth increases above the level at December 31, 1983 by at least $15 million of which at least $7.5 million must be attributable to net income for the period after December 31, 1983. Therefore, managers continue to have incentives to change accounting procedures while in default.7

3. Sample selection procedures

To provide a direct and powerful test of the relation between debt covenants and accounting choices, I identify points in time when firms violate accounting- based restrictions in their debt agreements and document the time series of managers’ accounting choices around these violations. In the extreme, since my sample selection criterion requires firms to violate debt-covenant constraints,

‘There are two reasons a manager would not exercise available accounting flexibility in years prior to default but would exercise that flexibility in post-default years. First, if the manager predicted no default costs, allowed the default to occur, but ex post creditors imposed default costs, then the manager would have incentives to change accounting procedures to resolve the default ex post, but not ex ante. Second, a manager would have incentive to change accounting procedures while in default, if the accounting flexibility available to the manager prior to default was insufficient to delay default, but the accounting flexibility available post-default was sufficient to resolve the default (either because the available accounting flexibility increased or because the firm’s perfor- mance improved such that the available flexibility became sufficient to resolve the default).

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 287

firms able to exercise their accounting flexibility to circumvent constraints and avoid violation are excluded. These excluded firms would provide the most powerful tests, but are difficult, if not impossible, to identify. Only firms that have exhausted their accounting flexibility are in the violation sample. This selection bias potentially results in a sample of default firms that do not change accounting procedures because the accounting flexibility available to managers was not enough to delay or prevent technical default.

Security and Exchange Commission (SEC) Regulation S-X, Rule 4-08, para- graph (c) requires disclosure of a covenant violation that ‘existed at the date of the most recent balance sheet being filed and which has not been subsequently cured’. If acceleration of the obligation has been waived, SEC regulation requires disclosure of the amount of the obligation and the period of the waiver. The Emerging Issues Task Force release 86-30 (1986) specifies that covenant violations must be disclosed in footnotes to firms’ annual reports if a ‘violation has occurred or would have occurred absent a loan modification’. Further, when a violation gives the creditor the right to call the debt, Financial Accounting Standard No. 78 (1983) requires that the debt be classified as a current liability unless a waiver covering more than one year has been granted. To justify the classification of the (violated) debt as long-term or to explain the reclassification of the debt as a current liability, firms must disclose information concerning covenant violations and the status of waivers for those violations. These dis- cussions are found either in Management’s Discussion and Analysis or in footnotes to firms’ annual financial statements.

An automated search of firms’ annual reports via the National Automated Accounting Research System (NAARS) resulted in 750 covenant violations by approximately 300 firms in the years 1977-1990.* To ensure that a firm is a first-time violator within the period 1980-1989, I exclude firms in violation during 1977-1979. To ensure uniformity across firms with respect to the relative importance of various accounting procedures, I include only firms in manufac- turing (i.e., SIC industries 20 through 39). The final sample of 130 firms consists of first-time violators within the period 1980-1989 that are on Compustat’s Expanded Annual Industrial or Annual Research Files.

Firms in the final sample are aligned in event time. The first year of violation is event year 0 in the time-series analysis of accounting choice. Each calendar year 1980 through 1989 is represented in the final sample of default years. However, more than 10 percent of the first-time violations occur in calendar years 1985 and 1989 (15.4 and 16.1 percent, respectively). Also, sample firms are

‘To identify covenant violations, I searched on the following keywords (and various combina- tions): ‘violation’, ‘default’, ‘covenant’, ‘noncompliance’, and ‘waiver’. This method of isolating a sample of default firms is also employed by Beneish and Press (1992, 1993), Chen and Wei (1993), and DeFond and Jiambalvo (1994). NAARS includes approximately 4,200 annual reports per year, suggesting that covenant violations occur in approximately 1.5 percent of the firm-years examined.

288 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

not evenly distributed across SIC industries 20 through 39. Although 17 differ- ent two-digit SIC industries are represented, SIC industries 35 and 36 have approximately 40 percent of the firms (17.7 and 22.0 percent, respectively). The industry and calendar-year clustering of the default sample mimics the cluster- ing of business failures in the 1980s as reported in Dun and Bradstreet Corpora- tion’s Business Failure Record.

A control sample is formed to account for industry-wide accounting policies. Firms in the same industry face similar contracting and financial reporting problems, and thus are expected to use similar accounting policies. Firms in the same industry also tend to change accounting procedures at the same time as a result of changing macro-economic effects and/or changes in the ex ante optimal set of accounting procedures (e.g., 1974 LIFO adoptions due to rising input prices and the steel industry depreciation switches in the 1960s). This suggests matching control firms to default firms by industry and time period. Firms are also matched on size because firms in the same three-digit SIC but of differing size are potentially in different industries and because earlier studies find a negative relation between a firm’s size and the likelihood that the firm employs income-increasing procedures [see Watts and Zimmerman (1986)]. Further, to ensure that the control firms represent surviving firms, and not firms that eventually file for bankruptcy, liquidate, or are taken over, all control firms are taken from Compustat’s Expanded Annual Industrial File and not Compus- tat’s Research File.’ Therefore, I compare default firms with all other firms on Compustat’s Industrial File in the same three-digit SIC industry and choose a control firm to minimize the absolute difference in total assets five years prior to the first year of default. The control firms’ accounting policies provide a benchmark for efficient accounting choice absent managerial manipulation.

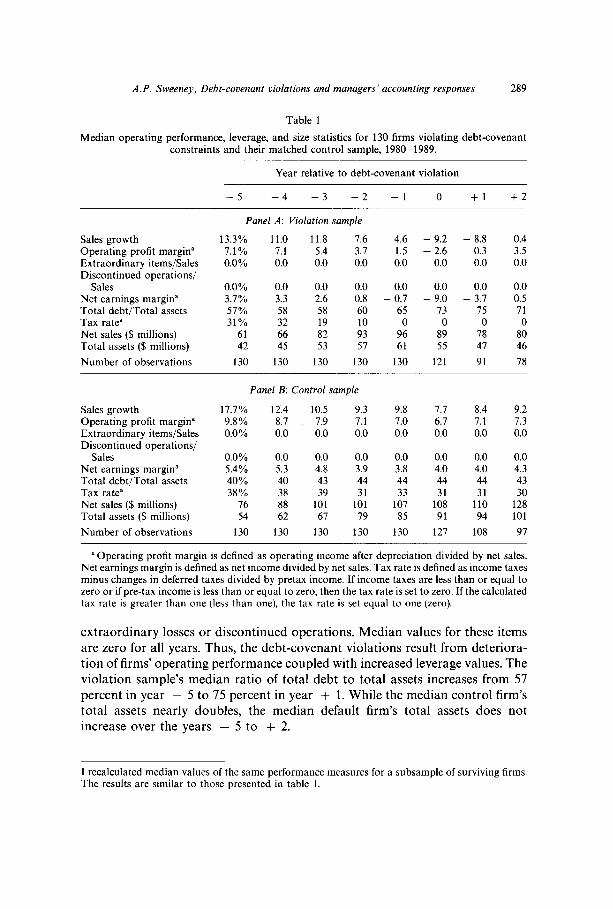

To help determine why firms violate accounting-based restrictions, I report median values of a number of measures of performance: sales growth, operating margins, extraordinary items to sales, discontinued operations to sales, and net earnings margins. Table 1 reports these measures of performance for event years -5 to +2 for the violation and control samples. The violation and control firms’ performance measures decline from years -5 to 0. Performance measures for the violation sample decline faster. The two groups’ performance measures diverge in year -1. While the control firms’ performance measures level off in years - 1 to +2, the violation sample continues to experience declining sales growth, operating profit margin, and net earnings margin through year + 1. lo The decline in net earnings margin is not driven by

‘Christie and Zimmerman (1991) provide evidence that managers of firms that are taken over act differently than managers of nonacquired firms with respect to accounting-policy choices.

“The number of observations is declining in table 1 due to missing Compustat data items. Thus, it is not clear whether the rebound in operating performance for the default sample results from actual improved firm performance in year + 2 or simply the disappearance of the least profitable firms.

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

Table 1

289

Median operating performance, leverage, and size statistics for 130 firms violating debt-covenant constraints and their matched control sample, 1980-1989.

Year relative to debt-covenant violation

-5 -4 -3 -2 -1

Sales growth Operating profit margin” Extraordinary items/Sales Discontinued operations/

Sales Net earnings margin” Total debt/Total assets Tax rate” Net sales (S millions) Total assets (S millions)

Number of observations

Panel A: Violation sample

13.3% 11.0 11.8 1.6 7.1% 7.1 5.4 3.1 0.0% 0.0 0.0 0.0

4.6 - 9.2 - 8.8 0.4 1.5 - 2.6 0.3 3.5 0.0 0.0 0.0 0.0

0.0% 0.0 0.0 0.0 0.0 0.0 0.0 0.0 3.7% 3.3 2.6 0.8 - 0.7 - 9.0 - 3.7 0.5 57% 58 58 60 65 73 15 71 31% 32 19 IO 0 0 0 0

61 66 82 93 96 89 78 80 42 45 53 57 61 55 47 46

130 130 130 130 130 121 91 78

7.7 6.7 0.0

Sales growth 17.7% 12.4 10.5 9.3 9.8 8.4 9.2 Operating profit margin” 9.8% 8.7 7.9 7.1 7.0 7.1 7.3 Extraordinary items/Sales 0.0% 0.0 0.0 0.0 0.0 0.0 0.0 Discontinued operations/

Sales 0.0% 0.0 0.0 0.0 0.0 0.0 0.0 Net earnings margin” 5.4% 5.3 4.8 3.9 3.8 4.0 4.3 Total debt/Total assets 40% 40 43 44 44 44 43 Tax ratea 38% 38 39 31 33 31 30 Net sales ($ millions) 76 88 101 101 107 110 128 Total assets ($ millions) 54 62 67 79 85 94 101

Number of observations 130 130 130 130 130 108 97

a Operating profit margin is defined as operating income after depreciation divided by net sales. Net earnings margin is defined as net income divided by net sales. Tax rate is defined as income taxes minus changes in deferred taxes divided by pretax income. If income taxes are less than or equal to zero or if pre-tax income is less than or equal to zero, then the tax rate is set to zero. If the calculated tax rate is greater than one (less than one), the tax rate is set equal to one (zero).

0.0 4.0 44 31

108 91

127

Panel B: Control sample

0 +1 +2

extraordinary losses or discontinued operations. Median values for these items are zero for all years. Thus, the debt-covenant violations result from deteriora- tion of firms’ operating performance coupled with increased leverage values. The violation sample’s median ratio of total debt to total assets increases from 57 percent in year - 5 to 75 percent in year + 1. While the median control firm’s total assets nearly doubles, the median default firm’s total assets does not increase over the years - 5 to + 2.

I recalculated median values of the same performance measures for a subsample of surviving firms. The results are similar to those presented in table 1.

290 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

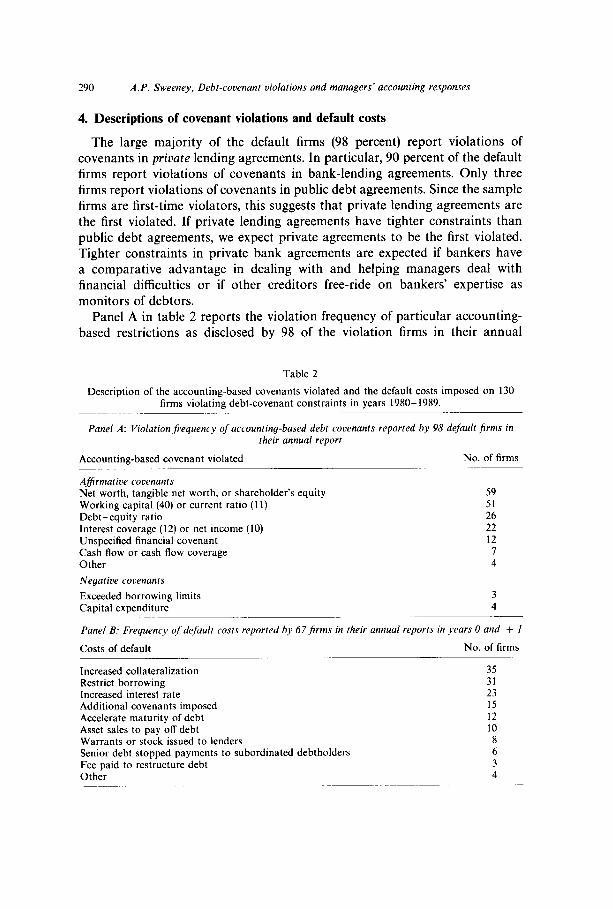

4. Descriptions of covenant violations and default costs

The large majority of the default firms (98 percent) report violations of covenants in prioate lending agreements. In particular, 90 percent of the default firms report violations of covenants in bank-lending agreements. Only three firms report violations of covenants in public debt agreements. Since the sample firms are first-time violators, this suggests that private lending agreements are the first violated. If private lending agreements have tighter constraints than public debt agreements, we expect private agreements to be the first violated. Tighter constraints in private bank agreements are expected if bankers have a comparative advantage in dealing with and helping managers deal with financial difficulties or if other creditors free-ride on bankers’ expertise as monitors of debtors.

Panel A in table 2 reports the violation frequency of particular accounting- based restrictions as disclosed by 98 of the violation firms in their annual

Description

Table 2

of the accounting-based covenants violated and the default costs imposed on 130 firms violating debt-covenant constraints in years 1980-1989.

Panel A: Violation frequency of accounting-based debt covenants reported by 98 default firms in their annual report

Accounting-based covenant violated

Ajirmative covenants Net worth, tangible net worth, or shareholder’s equity Working capital (40) or current ratio (I 1) Debt-equity ratio Interest coverage (12) or net income (10) Unspecified financial covenant Cash flow or cash flow coverage Other

Negative covenants

Exceeded borrowing limits Caoital exoenditure

No. of firms

59 51 26 22 12

I 4

3 4

Panel B: Frequency ~f‘d+dt costs reported by 67firms in their annual reports in years 0 and -I- I

Costs of default No. of firms

Increased collateralization 35 Restrict borrowing 31 Increased interest rate 23 Additional covenants imposed 15 Accelerate maturity of debt 12 Asset sales to pay off debt IO Warrants or stock issued to lenders 8 Senior debt stopped payments to subordinated debtholders 6 Fee paid to restructure debt 3 Other 4

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 291

reports. Since most firms report violations of more than one accounting-based covenant, the total number of accounting-based covenants reported as violated (188) exceeds the number of firms disclosing information on accounting-based covenants (98). These firms report 181 violations of affirmative covenants and only seven violations of negative covenants (four exceed capital expenditure limits and three exceed borrowing limits). Net worth and working capital restrictions are the affirmative covenants most often violated. Debt-equity ratios and income-based covenants are violated less frequently.

To document the costs of default for my sample of 130 firms, I use discussions found in the Management’s Discussion and Analysis and financial footnotes in event years 0 and + 1. Sixty-seven of the default firms disclosed in their annual reports that lenders required concessions to resolve the violations.’ ’ Panel B of table 2 documents the frequency of default costs. Since most firms report more than one type of default cost, the total number of default costs reported (147) exceeds the number of firms disclosing information on default costs (67). The most frequently reported costs of default include: increased collateralization, restriction on further borrowing, and increased interest rates.

In 35 instances default firms granted lenders security interest in previously unpledged assets in consideration for waivers of or amendments to violated covenants. For example, in 1982 BTK Industries, Inc. obtained amendments to its revolving credit and term loan agreements to eliminate existing financial covenant violations. BTK’s 1982 annual report states: ‘In consideration for such amendments, the Company pledged additional collateral consisting of imported inventory, previously unpledged property, plant and equipment, common stock of its wholly-owned subsidiaries, and its primary registered trademark.’

In 31 cases lenders restricted further borrowings by default firms, and in 23 cases lenders increased interest rates. For example, in 1986 Hinderliter Indus- tries, Inc. violated most of the financial covenants in its line-of-credit agreement. The lender waived these covenant violations. In consideration for the waivers, the company agreed to reduce the maximum line of credit to $18 million (from $23 million) and to increase the interest rate on the line of credit to prime plus 3 percent (from prime plus 2 percent). The one percentage point increase in interest on the $15 million outstanding balance resulted in $150,000 increase in interest payments for Hinderliter in 1986. Hinderliter also agreed to pay a one- time restructuring fee of $112,000 to lenders for the waiver.

’ ‘Chen and Wei (1993) and Beneish and Press (1993) also use disclosures found in firms’ annual reports and IO-KS to document the costs of default. However, there is no assurance that the costs and consequences of default disclosed in firms’ annual reports and lo-KS are a complete and exhaustive list. These disclosed costs are, at best, a lower bound for the total costs imposed when firms default on debt-convenant restrictions. Further, there is potentially a selection bias as to which firms voluntarily disclose default costs in their annual reports.

292 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

Many of the costs of default documented in table 2 are not quantifiable. However, for the 23 firms that agreed to increase the interest rate on their defaulted debt, the incremental interest cost is quantifiable. The dollar values of the incremental interest cost range from $34,000 to $5,071,500. As a percentage of the total market value of common equity, the incremental interest costs range from 0.2 to 20 percent with the mean (median) equal to 3.2 (2.0) percent. Since most firms bore default costs in addition to these incremental interest costs, this is, at best, a lower bound on the magnitude of the costs of technical default.

5. Managers’ accounting responses

To provide a complete picture of managers’ accounting responses to ensuing defaults, I examine: several choices of accounting methods, voluntary ac- counting changes, changes in estimates, and the timing of adoption of manda- tory accounting changes. If managers already selected all available income- increasing accounting procedures in prior years, then they may have no further accounting flexibility available to avoid the ensuing technical default. Therefore, I first report accounting choices five years prior to the year of default. Second, I examine changes in accounting procedures in years - 5 to +2. I present cross-sectional tests that explore whether managers make these accounting changes in response to tightening debt-covenant constraints or declines in liquidity. I also examine whether managers’ accounting responses depend on whether lenders impose default costs and whether managers have accounting flexibility. Finally, to provide supporting evidence, I document whether the default firms early adopt income-increasing mandatory methods.

5.1. Accounting procedure choices jive years prior to default

For both the default sample and control sample, I collect data on inventory- valuation method, depreciation method, investment tax credit (ITC) treatment, and amortization period for prior period pension costs from annual reports and 10-Q. In year -5, 80 (71) percent of the default (control) firms employ straight-line depreciation, 75 (72) percent employ the FIFO inventory-valuation method, 32 (31) percent amortize prior pension service costs for more than 30 years, and 98 (97) percent employ the flow-through method for ITCs. Only the frequency of straight-line depreciation use differs significantly for the default and control firms in year -5. The default firms have little opportunity to increase reported earnings via changes in depreciation and ITC methods. However, 25 percent of the default firms use LIFO, and switching to FIFO can potentially increase reported earnings; and 68 percent of default firms could increase the period used to amortize prior pension service costs to the maximum permitted.

A.P. Sweeney, Debi-covenant violalions and managers’ accounting responses 293

5.2. Voluntary accounting changes

5.2.1. Changes in accounting procedures

In this section I compare the number and magnitude of the accounting changes made by the default and control samples in years - 5 to + 2. To identify years in which managers make accounting changes, I employ Compustat foot- notes. These footnotes indicate whether a firm’s financial statements reflect an accounting change(s), voluntary and/or mandatory.” For each firm-year identi- fied, I read the annual report and document the change(s) made and the reported effect of the change(s) on net income and/or retained earnings.

The identified voluntary accounting changes include: changes in pension accounting assumptions and/or cost method, LIFO adoptions or extensions, FIFO adoptions or extensions, depreciation method changes, changes in depre- ciable lives, changes in ITC treatment, and ‘Other’ types of accounting changes. I3 In addition to recording accounting changes, I also record the liquidation of LIFO inventories and the termination of pension plans as re- ported in the accounting-change years and event years -5 and 0.

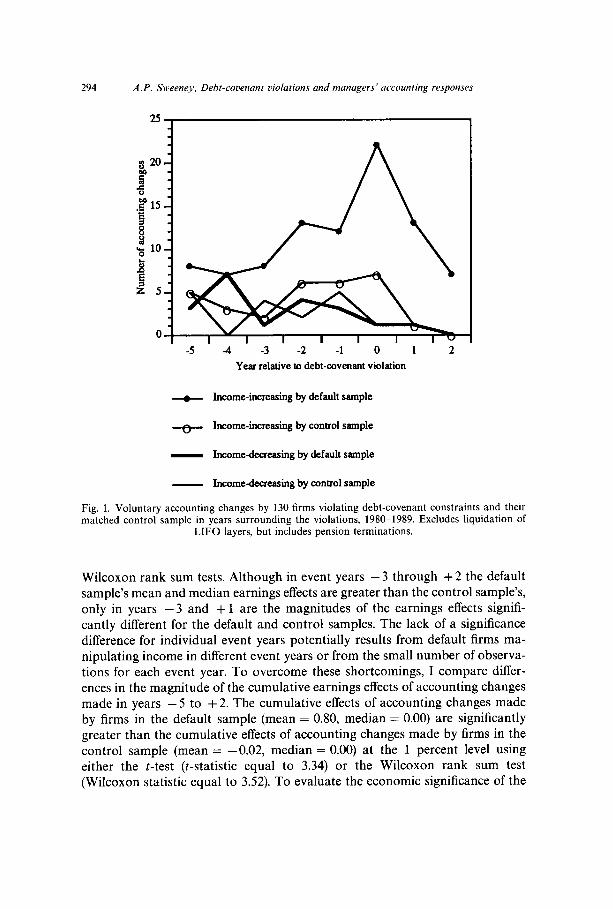

Fig. 1 shows the timing of voluntary accounting changes made by the default and control firms relative to the first year of default. The accounting changes are broken-out by income-increasing and income-decreasing, where an accounting change that is reported to increase (decrease) net earnings, retained earnings, or net sales, or to decrease (increase) expenses is classified as income-increasing (decreasing). The violation firms make a greater number of income-increasing changes in the default year than in surrounding years. The violation firms make two to three times as many income-increasing accounting changes as the control firms in event years -2 to + 2. In years 0, + 1, and +2 the proportion of violation firms making income-increasing changes is significantly greater than the proportion of control firms. These results support the covenant-based hypothesis. Further, these results are consistent with the hypothesis that man- agers change to income-increasing accounting procedures while in technical default.

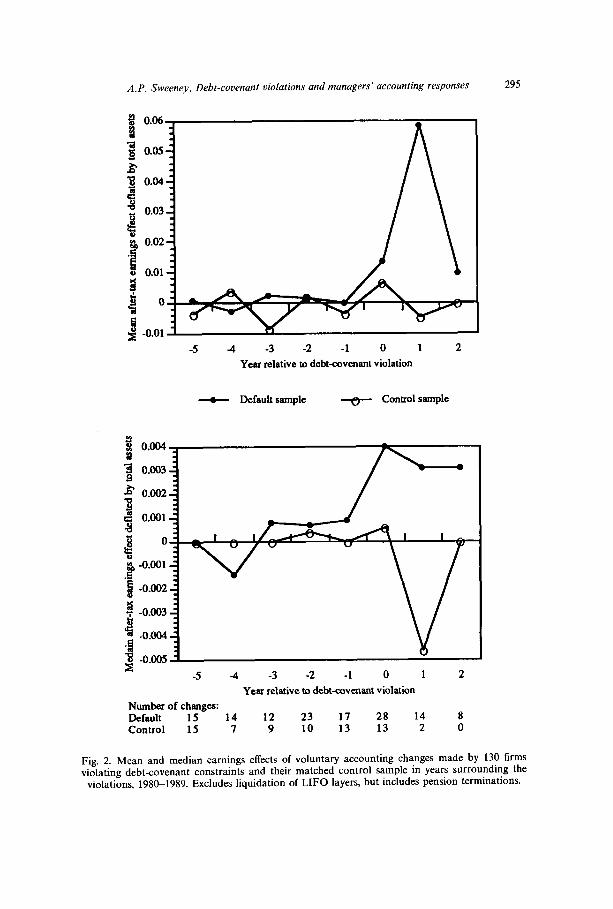

Fig. 2 reports by event year and sample the mean and median after-tax earnings effects resulting from voluntary accounting changes. The earnings effects are deflated by total assets in the year of the change. If no effect is reported, I set the earnings effect equal to zero.14 I calculate t-tests and

“In general, the Compustat footnotes accurately directed my search for accounting changes.

13A list of the accounting changes categorized as ‘Other’ are available from the author upon request. This category includes: reclassification of assets, changes in method of revenue recognition, changes in method of expensing and capitalizing costs, changes in amortization period for prior period service costs, changes in allocation of overhead costs, changes in consolidation of subsidia- ries, and changes in fiscal year-end.

14The results presented in fig. 2 are qualitatively the same if either LIFO liquidations are included or if accounting changes with no reported earnings effect are dropped from the analysis. Deflating by either net sales or the market value of equity also leave the tenor of the results unchanged.

294 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

4 -3 -2 -1 0 1 2

Year relative to debt-covenant violation

Income-increasing by default sample

Income-increasing by control sample

Income-decreasing by &fault sample

Income-decreasing by control sample

Fig. 1. Voluntary accounting changes by 130 firms violating debt-covenant constraints and their matched control sample in years surrounding the violations, 1980-1989. Excludes liquidation of

LIFO layers, but includes pension terminations.

Wilcoxon rank sum tests. Although in event years - 3 through + 2 the default sample’s mean and median earnings effects are greater than the control sample’s, only in years -3 and + 1 are the magnitudes of the earnings effects signifi- cantly different for the default and control samples. The lack of a significance difference for individual event years potentially results from default firms ma- nipulating income in different event years or from the small number of observa- tions for each event year. To overcome these shortcomings, I compare differ- ences in the magnitude of the cumulative earnings effects of accounting changes made in years - 5 to + 2. The cumulative effects of accounting changes made by firms in the default sample (mean = 0.80, median = 0.00) are significantly greater than the cumulative effects of accounting changes made by firms in the control sample (mean = -0.02, median = 0.00) at the 1 percent level using either the r-test (t-statistic equal to 3.34) or the Wilcoxon rank sum test (Wilcoxon statistic equal to 3.52). To evaluate the economic significance of the

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 295

8 kl 0.06

II 0.05

: 0.04

z!

; 0.03

% 3 0.02

0

-0.01

-5 4 -3 -2 -1 0 1 2

Year relative to debt-covenant violation

+ Default sample -6_ Control sample

E -0.005

-5 4 -3 -2 -1 0 1 2

Year relative to debt-covenant violation

Number of changes: Default 15 14 12 23 17 28 8 Control 15 7 9 10 13 13 1; 0

Fig. 2. Mean and median earnings effects of voluntary accounting changes made by 130 firms violating debt-covenant constraints and their matched control sample in years surrounding the

violations, 1980-1989. Excludes liquidation of LIFO layers, but includes pension terminations.

Tab

le

3

Freq

uenc

y of

vol

unta

ry

acco

untin

g ch

ange

s by

ear

ning

s an

d ex

pect

ed

cash

-flo

w

effe

ct f

or

130

firm

s vi

olat

ing

debt

-cov

enan

t co

nstr

aint

s an

d th

eir

mat

ched

co

ntro

l sa

mpl

e in

ye

ars

- 5

to

+ 2,

rel

ativ

e to

th

e vi

olat

ion

year

s,

1980

-198

9.

Pens

ion

assu

mpt

ions

an

d/or

co

st

met

hod

Pens

ion

term

inat

ions

L

IFO

ad

opte

d or

ex

tend

ed

FIFO

ad

opte

d or

ex

tend

ed

Liq

uida

tion

of L

IFO

la

yers

D

epre

ciat

ion

met

hod

Dep

reci

able

liv

es

Inve

stm

ent

cred

its

Oth

er

38’

15’ 0 8’

65’ 5 3 1

20’

3 0 14 0 0 0 0 0 3

45d

17

18’

2 16

0

8d

0 69

d 38

9

4 4

2 1

1 35

’ 4

Tot

al

155’

20

10

20

20

5’

68

Perc

enta

ge

of t

otal

(X

) 16

10

5

10

59

Def

ault

sam

ple

Con

trol

sa

mpl

e

Inco

me-

In

com

e-

Not

In

dete

r-

Inco

me-

In

com

e-

Not

In

dete

r-

incr

easi

ng

decr

easi

ng

mat

eria

l m

inan

t T

otal

in

crea

sing

de

crea

sing

m

ater

ial

min

ant

Tot

al

Pan

el

A:

Ear

ning

s e&

Y

4 1 9 1 2 0 0 0 3

20

17

18

16

2 0 1 0 1 2 0 0 4 10 9

24 5 16 1

44 8 2 3 13

116

Non

incr

easi

ng

33”

3 In

crea

sing

12

2’

17

Pane

l B

: E

xpec

ted

cash

-jlo

w

effe

d

5 9

50’

10

4 6

5 25

5

11

155’

58

16

12

5

91

“An

acco

untin

g ch

ange

re

port

ed

to

incr

ease

(d

ecre

ase)

ne

t ea

rnin

gs,

reta

ined

ea

rnin

gs,

net

sale

s,

or

to

decr

ease

(i

ncre

ase)

ex

pens

es

is c

lass

ifie

d as

in

com

e-in

crea

sing

(d

ecre

asin

g).

“The

ac

coun

ting

chan

ges

cate

gori

zed

as ‘

Non

incr

easi

ng’

incl

ude:

FI

FO

adop

tions

or

ext

ensi

ons,

de

prec

iatio

n-re

late

d ch

ange

s,

chan

ges

in m

etho

ds

for

inve

stm

ent

tax

cred

its,

and

mos

t of

th

e ‘O

ther

’ ac

coun

ting

chan

ges.

T

he

acco

untin

g ch

ange

s ca

tego

rize

d as

‘I

ncre

asin

g’

incl

ude:

ch

ange

s in

pe

nsio

n as

sum

ptio

ns

and/

or

cost

m

etho

ds,

pens

ion

plan

te

rmin

atio

ns,

LIF

O

adop

tions

or

ex

tens

ions

, an

d L

IFO

liq

uida

tions

. ‘S

igni

fica

ntly

di

ffer

ent

from

th

e pr

opor

tion

for

the

cont

rol

sam

ple

at

the

1%

leve

l, us

ing

a tw

o-ta

iled

bino

mia

l te

st.

dSig

nifi

cant

ly

diff

eren

t fr

om

the

prop

ortio

n fo

r th

e co

ntro

l sa

mpl

e at

th

e 5%

le

vel,

usin

g a

two-

taile

d bi

nom

ial

test

.

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 291

accounting changes, section 6 documents whether for a subsample of 22 firms the earnings effects of accounting changes are sufficient to delay technical

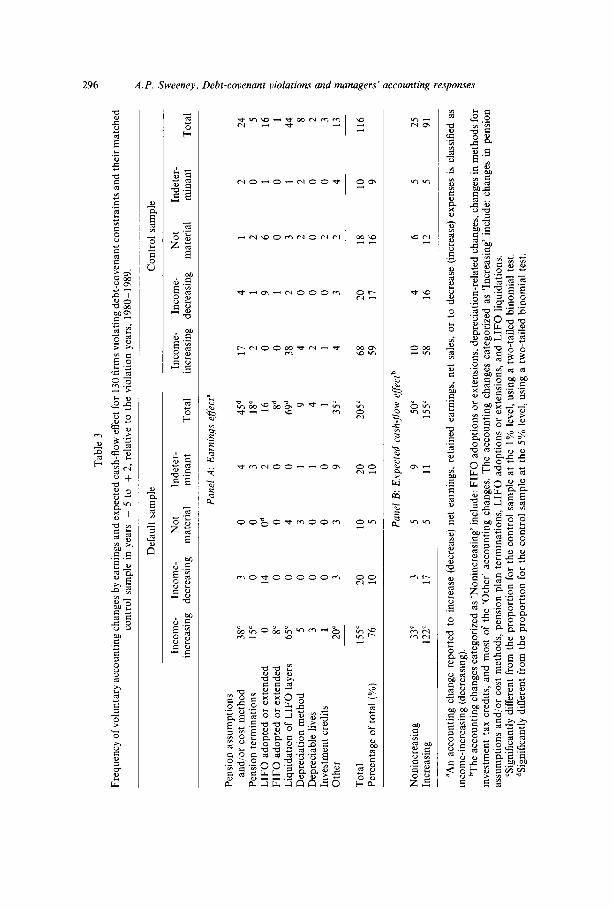

default for one or more accounting periods. As reported in the ‘total’ columns in table 3, the default firms made 205

voluntary accounting changes and 155 (76 percent) of these were income- increasing. Whereas, the control firms made 116 accounting changes and only 68 (59 percent) were income-increasing. The proportion of income-increasing changes made by the violation sample in years - 5 to + 2 differs significantly (at the 1 percent level) from the proportion made by the control sample. Table 3 also reports the frequency of particular accounting changes made by the violation and control firms. Since 80 percent of the default firms employed straight-line depreciation and 98 percent employed the flow-through method in year - 5, the default firms had little opportunity to increase reported earnings via changes in depreciation and ITC methods. Thus, the number of depreciation and ITC changes made by the default and control samples do not differ significantly over the sample period. The particular types of voluntary changes that differ significantly include: changes in pension assumptions and/or cost methods, pension terminations, FIFO adoptions or extensions, liquidations of LIFO inventories, and accounting changes categorized as ‘Other’.

In the absence of incentives to manipulate reported numbers because of closeness to debt-covenant constraints, managers of default firms have incen- tives to switch to the most efficient set of accounting policies for their financially distressed firms. For instance, the 69 LIFO liquidations by the default firms potentially reflect optimal decisions by managers to decrease inventory levels during periods of declining sales growth. The fact that the violation sample has a significantly greater number of LIFO inventory liquidations than the control sample is potentially explained by the fact that the default firms’ sales growth declines faster than that of the control firms (see table 1). Similarly, the 63 pension-related changes by the default firms potentially reflect optimal recon- tracting of pension benefits between financially distressed firms and their employees.

These LIFO-related and pension-related changes not only increase reported earnings, but also decrease cash outflows. The decline in default firms’ liquidity

positions in years - 5 to 0 (see table 1) potentially motivates managers to make the LIFO-related and pension-related changes. Panel B of table 3 reports accounting changes categorized by their expected cash-flow effects. The ‘Nonin- creasing’ category includes FIFO adoptions or extensions, depreciation-related changes, changes in methods for investment tax credits, and most of the ‘Other’ accounting changes. The ‘Increasing’ category includes changes in pension assumptions and/or cost methods, pension plan terminations, LIFO adoptions or extensions, and LIFO liquidations.’ 5 The violation firms make a significantly

15Although LIFO liquidations do not necessarily increase cash-flows, 1 classify them as cash- ‘increasing’ because most of the default firms’ marginal tax rate are zero in the years surrounding

298 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

greater number of cash-increasing and non-cash-increasing accounting changes than the control firms. The greater frequency of income-increasing, non-cash- increasing accounting changes made by the violation sample is consistent with the hypothesis that managers of violation firms make some of the accounting changes to lower the probability of technical violation. The greater frequency of income-increasing, cash-increasing accounting changes made by the violation sample is consistent with two hypotheses: (i) managers of violation firms make some of the accounting changes to lower the probability of technical violation, and (ii) managers of violation firms make some of the accounting changes to offset declines in liquidity.

5.2.2. Cross-sectional analysis of voluntary accounting changes

To help distinguish between these alternative hypotheses, I examine the relation between the magnitude of the earnings effects resulting from accounting changes and increases in the tightness of debt-covenant constraints and declines in liquidity. If managers change accounting procedures because of a tightening debt-covenant constraint and/or a decline in liquidity, then the magnitude of the earnings effects resulting from the accounting change ought to be directly related to the magnitude of the change in the tightness of debt-covenant constraint and/or the decline in liquidity. To investigate the marginal effects of these two motives on managers’ accounting decisions, I estimate the following regression:

Eficti, = a0 + al Djdofmu,, + a,ANet Worthjt

+ adDjaefaplt * ANet Worthj,)

+ 4Dcashflow * ALhuidityjJ

+ adDjd.fault * Dcasmow * ALiquidWjJ + ejt,

where Effectjt is the magnitude of the earnings effect resulting from an ac- counting change by firm j in year t. Each accounting change made by firm j is treated as a separate observation. The regression is estimated using data in the year of the accounting change. Intercept and slope dummies are employed to determine whether managers of default and control firms respond differently to

covenant violations (see table 1). Thus, the cash savings via reductions in production and inventory carrying costs are likely to outweigh the tax costs of LIFO liquidations. Reclassifying LIFO liquidations (and LIFO adoptions) as ‘nonincreasing’ does not change the tenor of the results. For a detailed discussion of the expected cash-flow effects see Sweeney (1992).

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 299

tightening debt-covenant constraints and/or declines in firms’ liquidity posi-

tions. Djdefault is equal to one for firms in the default sample and zero for the control firms.

Since the majority of the default firms violate net worth covenants (see table 2) the change in net worth normalized by total assets (ANet Worth,) proxies for increases in the tightness of a firm’s debt-covenant constraints. The greater the decline in net worth, the greater the earnings effects resulting from income- increasing accounting changes necessary to offset the increased tightness of debt-covenant constraints. However, a decline in net worth also signifies a decline in firm performance. Thus, a negative relation between EfSectjt and ANet Worth,, is consistent with managers changing to income-increasing ac- counting procedures to ‘loosen’ tightening debt-covenant constraints and/or to offset poor firm performance.

Managers’ incentives to offset poor performance arise from either earnings- based compensation contracts [see Healy (1985)] or from benefits associated with reporting smoothly increasing earnings per share [see Barth, Elliott, and Finn (1993)]. These incentives entice managers to make income-increasing

changes only when earnings per share are positive. When earnings per share are negative, managers have incentives to take an ‘earnings bath’. The default sample’s median earnings is negative in years - 1 to + 1 (see table 1). Thus, in years - 1 to + 1 managers’ incentives to make income-increasing accounting changes must arise from tightening debt-covenant constraints and fear of losing their jobs. Gilson (1989) documents that when firms are either in default, bankruptcy, or restructuring debt to avoid bankruptcy, 52 percent of the firms experience a senior management change. Gilson adds that this is greater than twice the frequency of turnover in firms with similar operating performance that are not in default, bankruptcy, or restructuring debt to avoid bankruptcy. Thus, default increases the probability of managers losing their jobs.

The change in operating cash flows normalized by total assets (ALiqGdityjJ is employed as a proxy for the change in a firm’s liquidity position.“j The greater the decline in operating cash flows, the greater the earnings effects resulting from cash-increasing accounting changes necessary to offset the decline in liquidity. Thus, a negative relation between Efictjt and ALiquidityj, is expected. Since a relation between Efictjt and ALiquidityj, is only expected if the accounting change has a cash-flow effect, ALipidityjt, is multiplied by a dummy variable, D cashflow. D cashflow equals one if the accounting-change observation is expected to

r60perating cash flows are defined as net income plus depreciation plus deferred tax minus changes in inventory balance minus changes in accounts receivable plus changes in accounts payable minus the effect of the accounting changes. Changes in working capital and changes in operating cash flows are likely to be highly correlated. Therefore, I do not use changes in working capital as a proxy for increases in the tightness of firms’ debt-covenant constraints even though working capital covenants are violated frequently (see table 2).

300 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

have a positive cash-flow effect (i.e., pension-related and LIFO-related changes) and zero otherwise.

The results are presented in table 4. While the control firms do not, the default firms do make income-increasing accounting changes over the time period examined (i.e., a0 is insignificantly different from zero at conventional levels; a0 + al is significantly positive at the 1 percent level). However, after controlling for the marginal effects of changes in net worth and operating cash flows, the mean earnings effect resulting from individual accounting changes made by the

Table 4

Tests of the relation between the magnitude of earnings effects resulting from accounting changes and increases in the tightness of debt-covenant constraints after controlling for changes in firms’ liquidity circumstances. Sample of accounting changes made by 130 firms violating debt-covenant constraints and 130 matched control firms, 1980- 1989. If a firm reports no effect of the accounting

change, then the effect is set to zero.a

Effectj, = aa + ai Djacr.“lr + a2 ANet Worth,, + a3(Dldcfaun * ANet Worth,,)

+ a4 (D,,,,,,,,*ALiquidityjt) + a5(Dja.r.,lx * Dcashuow * ALiquidityjt) + ejt

Estimated coefficients

(t-statistics)

Tests of null hypothesis: ai+ai+,=O

(F-value) [p-value]

a, Intercept

a2 ANet Worth,,

a3 (Djdefault * ANet WorthjJ

a4 (DCas~f~ow * ALiquidity,,)

a5 (D+r.ua * DEas~f~orv * ALiquidityj,)

Adjusted RZ N F-test [p-value] White’s test [p-value]

0.003 (0.70)

0.005 a, a, + = 0.008 (1.01) (6.22) [O.Ol]

- 0.036 ( - 0.51)

- 0.007 a2 + a3 = 0.043 - ( - 0.10) (9.20) [O.OO]

0.015 (0.3 1)

- 0.004 04 + as = 0.011 ( - 0.08) (0.68) [0.41]

3.51 219

2.59 [0.03] 7.49 CO.761

‘Effectj, is the change in net income resulting from the accounting change as a percentage of firm j’s total assets. DJdefaul, is a dummy variable equal to one if firm j is from the default sample and zero if firm j is from the control sample. ANet Worth,, is the change in firm j’s net worth from year t - 1 to year t adjusted for the effect of the accounting change normalized by firm j’s total assets. Dcashflow is dummy variable equal to one if the accounting-change observation is expected to have a positive cash flow effect, and zero otherwise (i.e., DEarhflow is set to one if the accounting change is either a pension-related change or a LIFO liquidation). Aliquidityj, is the change in firm j’s operating cash flow from year t - 1 to year t adjusted for the effect of the accounting changes in year t (normalized by firm j’s total assets).

A.P. Sweeney, Debt-covenanr violarions and managers’ accounting responses 301

default firms is not significantly greater than the mean earnings effect resulting from individual accounting changes made by the control firms (i.e., a, is not significantly different from zero at conventional levels). While managers of default firms respond to changes in net worth, managers of the control firms do not (i.e., a2 + a3 is significantly negative, a2 is not significantly different from zero at conventional levels). However, the default firms do not respond in a significantly different fashion to changes in net worth than the control firms (i.e., a3 is not significantly different from zero at conventional levels). The results presented in table 4 also fail to support the hypotheses that managers of the default and control firms respond to changes in operating cash flows (i.e., a4 and a4 + a5 are insignificantly different from zero at conventional levels).

In summary, the results presented in table 4 fail to provide conclusive evidence that managers of default firms make income-increasing accounting changes to offset tightening debt-covenant constraints. Although their firms are closer to violating net worth covenants, managers of default firms do not respond more to declines in net worth than do managers of control firms. In addition, table 4 provides no evidence to support the proposition that the difference in number and magnitude of income-increasing changes made by the default and control samples is explained by differences in their cash-flow circumstances. However for the specification of eq. (1) to provide a powerful test of the relation between managers’ accounting decisions and tightening con- straints, managers must respond contemporaneously to changes in the tightness of debt-covenants and liquidity constraints. If managers anticipate changes in firm circumstances or if managers respond in a lagged fashion to changes in firm circumstances, then this specification lacks power. Given that it is costly to change accounting procedures, it is unlikely that managers respond in a completely contemporaneous fashion to changes in firm circumstances [see Sweeney (1992)].

5.2.3. Default costs and accounting flexibility

Only 53 of the 130 default firms make accounting changes in the years examined. I hypothesize that managers’ accounting responses depend on whether default costs are imposed by creditors and whether managers have accounting flexibility available. To test this hypothesis, I compare the ac- counting responses of default firms having accounting flexibility and bearing default costs to the accounting responses of default firms not having accounting flexibility and/or not bearing default costs.” The mean cumulative earnings

“A firm is categorized as bearing default costs if the firm reports costs of default in its annual report in year 0 or + 1. A firm is categorized as having accounting flexibility conditional on whether the firm is a taxpayer. If the firm is not a taxpayer in years - 1 to + 1, then the firm is considered to have accounting flexibility if the firm employs at least one income-decreasing accounting procedure in year -2 (i.e., LIFO, accelerated depreciation or the deferral method for

302 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

effect of all accounting changes made in years - 1 to + 1 by the 54 firms bearing default costs and having accounting flexibility is 1.95 percent of total assets, while the mean cumulative effect for the 76 firms not bearing default costs and/or not having accounting flexibility is only 0.36 percent of total assets. The difference in means is statistically significant at the 2 percent level using a two- tailed test (t-statistic equal to 2.42). I also calculate a chi-square statistic to tests for the independence of a firm’s accounting response (changing to income- increasing procedures) and whether or not the firm has accounting flexibility and bears default costs. The chi-square test rejects the null of independence at the 5 percent level. These results support the hypothesis that managers ofJirms having accounting jlexibility and bearing default costs are more likely to make income-increasing accounting changes in response to tightening debt-covenant constraints than managers of firms not having accounting jlexibility and/or not bearing default costs.

5.3. Mandatory accounting changes

Mandatory accounting changes are also examined since managers have discretion over the timing of their adoption. The mandatory changes recorded include: SFAS 13 (capitalization of leases), SFAS 34 (interest capitalization), SFAS 43 (compensated absences), SFAS 52 (foreign currency translation), SFAS 86 (development costs of computer software), SFAS 87 and 88 (pension ac- counting), and SFAS 96 (income taxes). There are no significant differences between the proportion of default and control firms adopting particular manda- tory methods in the sample years. The default sample adopts 108 mandatory accounting methods in years - 5 to + 2; and the control sample adopts 100. For both samples (approximately) 50 percent of the adopted methods are income- increasing. The similarity in the particular mandatory methods adopted by the default and control firms is not surprising since the samples are matched by industry and time period.

To provide supporting evidence that managers of default firms change their accounting decisions in response to ensuing technical defaults, I document whether managers of default firms accelerate (delay) the adoption of mandatory accounting changes that increase (decrease) income. I classify each mandatory change by its income effect and by the timing of its adoption. A mandatory method adopted prior to the effective da-f the Statement of Financial Accounting Standards (SFAS) is considered an early adoption. I construct 2 x 2

IT&) or if the firm has a pension plan. If the firm is a taxpayer in any year - 1 to + 1, then the firm is considered to have accounting flexibility if the firm employs at least one non-tax-increasing, income-decreasing accounting procedure in year - 2 (i.e., accelerated depreciation or the deferral method for ITCs) or if the firm has a pension plan.

A.P. Sweeney, Debt-covenant violations and managers’ accounting responses 303

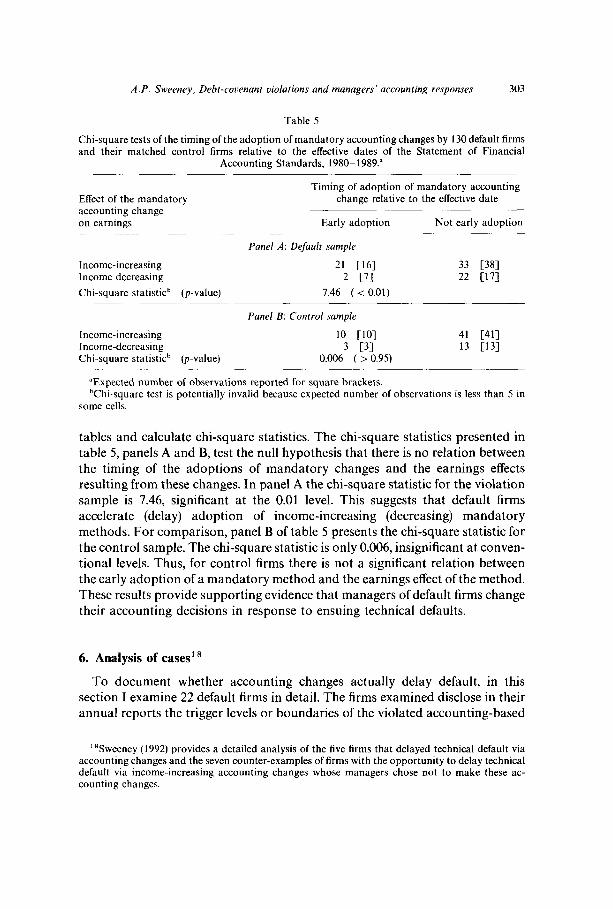

Table 5

Chi-square tests of the timing of the adoption of mandatory accounting changes by 130 default firms and their matched control firms relative to the effective dates of the Statement of Financial

Accounting Standards, 1980- 1989.”

Effect of the mandatory accounting change on earnings

Income-increasing Income decreasing

Chi-square statisticb (p-value)

Timing of adoption of mandatory accounting change relative to the effective date

Early adoption Not early adoption

Panel A: De&t& sample

21 1161 33 [38]

2 c71 22 [17]

7.46 ( < 0.01)

Panel B: Control sample

Income-increasing 10 [lo] 41 [41] Income-decreasing 3 c31 13 [I33 Chi-square statisti? (p-value) 0.006 ( > 0.95)

“Expected number of observations reported for square brackets. %hi-square test is potentially invalid because expected number of observations is less than 5 in

some cells.

tables and calculate chi-square statistics. The chi-square statistics presented in table 5, panels A and B, test the null hypothesis that there is no relation between the timing of the adoptions of mandatory changes and the earnings effects resulting from these changes. In panel A the chi-square statistic for the violation sample is 7.46, significant at the 0.01 level. This suggests that default firms accelerate (delay) adoption of income-increasing (decreasing) mandatory methods. For comparison, panel B of table 5 presents the chi-square statistic for the control sample. The chi-square statistic is only 0.006, insignificant at conven- tional levels. Thus, for control firms there is not a significant relation between the early adoption of a mandatory method and the earnings effect of the method. These results provide supporting evidence that managers of default firms change their accounting decisions in response to ensuing technical defaults.

6. Analysis of cases’ ’

To document whether accounting changes actually delay default, in this section I examine 22 default firms in detail. The firms examined disclose in their annual reports the trigger levels or boundaries of the violated accounting-based

“Sweeney (1992) provides a detailed analysis of the five firms that delayed technical default via accounting changes and the seven counter-examples of firms with the opportunity to delay technical default via income-increasing accounting changes whose managers chose not to make these ac- counting changes.

304 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

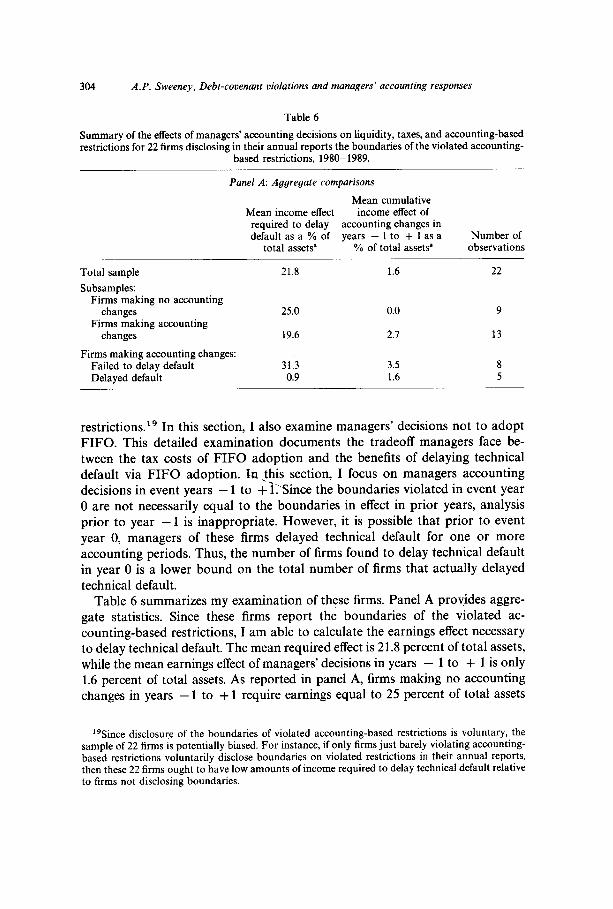

Table 6

Summary of the effects of managers’ accounting decisions on liquidity, taxes, and accounting-based restrictions for 22 firms disclosing in their annual reports the boundaries of the violated accounting-

based restrictions, 1980-1989.

Total sample

Subsamnles:

Panel A: Aggregate comparisons

Mean cumulative Mean income effect income effect of

required to delay accounting changes in default as a % of years - 1 to + 1 as a

total assetsa % of total assets’

21.8 1.6

Number of observations

22

Firms making no accounting changes

Firms making accounting changes

25.0 0.0 9

19.6 2.1 13

Firms making accounting changes: Failed to delay default 31.3 3.5 8 Delayed default 0.9 1.6 5

restrictions.” In this section, I also examine managers’ decisions not to adopt FIFO. This detailed examination documents the tradeoff managers face be- tween the tax costs of FIFO adoption and the benefits of delaying technical default via FIFO adoption. Inthis section, I focus on managers accounting decisions in event years - 1 to + 11 Since the boundaries violated in event year 0 are not necessarily equal to the boundaries in effect in prior years, analysis prior to year - 1 is inappropriate. However, it is possible that prior to event year 0, managers of these firms delayed technical default for one or more accounting periods. Thus, the number of firms found to delay technical default in year 0 is a lower bound on the total number of firms that actually delayed technical default.

Table 6 summarizes my examination of these firms. Panel A provides aggre- gate statistics. Since these firms report the boundaries of the violated ac- counting-based restrictions, I am able to calculate the earnings effect necessary to delay technical default. The mean required effect is 21.8 percent of total assets, while the mean earnings effect of managers’ decisions in years - 1 to + 1 is only 1.6 percent of total assets. As reported in panel A, firms making no accounting changes in years - 1 to + 1 require earnings equal to 25 percent of total assets

“Since disclosure of the boundaries of violated accounting-based restrictions is voluntary, the sample of 22 firms is potentially biased. For instance, if only firms just barely violating accounting- based restrictions voluntarily disclose boundaries on violated restrictions in their annual reports, then these 22 firms ought to have low amounts of income required to delay technical default relative to firms not disclosing boundaries.

Tab

le 6

(co

ntin

ued)

Pan

el B

: In

divi

dual

com

pani

es

Com

pany

na

me

Inco

me

effe

ct

requ

ired

to

de

lay

defa

ult

as a

% o

f to

tal

asse

tsa

Inco

me

effe

ct

of a

ccou

ntin

g ch

ange

s in

ye

ars

- 1

to

+ 1

as

a %

of

tota

l as

set?

Eff

ect

of c

hang

es

Cas

h D

elay

ed

flow

T

axes

de

faul

t

Acm

e U

nite

d C

orp

App

lied

Dev

ices

A

rt’s

Way

Man

uf

BM

C I

ndus

trie

s B

arbe

r-G

reen

e C

o C

olum

bia

Gen

eral

C

omdi

al

Cor

p C

usto

med

ix

Cor

p E

lect

roni

c M

issi

les

Face

t E

nter

pris

es

Fost

er

(L.B

.) C

o H

arni

schf

eger

IR

T C

arp

Met

ropo

litan

M

or-F

lo

Indu

stri

es

Rob

erts

on

(H.H

.)

Surv

ival

Tec

hnol

ogie

s T

exfi

Ind

ustr

ies

Tob

in P

acki

ng

Co

Uni

vers

al

Secu

rity

W

ean

Inc

Wur

ltech

In

dust

ries

0.2

55.0

1.

1 53

.0

47.0

4.

9

::;

4.7

L 3.0

7.

0 9.

0 10

0.0

36.6

1.

0 0.

8 3.

0 42

.0

77.0

15

.0

1.5

11.2

0.3

4.0

Non

e 3.

0 14

.0

- 0.

2 1.

6 N

one

Non

e 1.

5 0.

0 1.

0 0.

0 1.

0 2.

1 1.

3 N

one

3.3

0.0

Non

e 2.

5 N

one

Non

e N

one

N/A

N

one

20

Non

e N

one

N/A

N

/A

20

Non

e t0

N

one

20

Non

e

$1

Non

e N

one

N/A

N

one

N/A

Non

e 1Q

FI

FO

20

No

FIFO

N

/A

No

LIF

O

Non

e N

o FI

FO

Non

e N

o FI

FO

Non

e N

o L

IFO

N

one

1-2Q

FI

FO

N/A

N

o FI

FO

N/A

N

o FI

FO

20

No

FIFO

N

one

No

LIF

O

20

No

LIF

O

Non

e N

o FI

FO

Non

e N

o L

IFO

N

one

24

LIF

O

Non

e lQ

, 1F

Y

FIFO

N

/A

No

FIFO

N

one

No

FIFO

N

one

No

FIFO

N

/A

No

FIFO

N

one

1Q

FIFO

N

/A

No

FIFO

b

Acc

ount

ing

choi

ces

in e

vent

yea

r 0

post

acc

ount

ing

chan

ges

Inve

ntor

y D

epre

ciat

ion

ITC

s

Stra

ight

-lin

e $

Stra

ight

-lin

e Fl

ow-t

hrou

gh

a

Stra

ight

-lin

e Fl

ow-t

hrou

gh

:

Stra

ight

-lin

e Fl

ow-t

hrou

gh

2 z St

raig

ht-l

ine

Flow

-thr

ough

A

ccel

erat

ed

8.

Stra

ight

-lin

e Fl

ow-t

hrou

gh

fz

Stra

ight

-lin

e Fl

ow-t

hrou

gh

%

Stra

ight

-lin

e Fl

ow-t

hrou

gh

9 St

raig

ht-l

ine

Flow

-thr

ough

St

raig

ht-l

ine

Flow

-thr

ough

A

ccel

erat

ed

Flow

-thr

ough

;

Stra

ight

-lin

e %

St

raig

ht-l

ine

2

Stra

ight

-lin

e a ::

Stra

ight

-lin

e Fl

ow-t

hrou

gh

P B

oth

Flow

-thr

ough

h

Stra

ight

-lin

e Fl

ow-t

hrou

gh

g St

raig

ht-l

ine

Stra

ight

-lin

e Fl

ow-t

hrou

gh

5 Fl

ow-t

hrou

gh

‘“,

Stra

ight

-lin

e 2

Stra

ight

-lin

e Fl

ow-t

hrou

gh

@

“The

inc

ome

effe

ct r

equi

red

to d

elay

def

ault

is t

he

incr

emen

t to

rep

orte

d in

com

e re

quir

ed

to b

oost

in

com

e an

d/or

re

tain

ed

earn

ings

be

yond

th

e ac

coun

ting-

base

d re

stri

ctio

n vi

olat

ed i

n ev

ent

year

0. T

he c

umul

ativ

e in

com

e ef

fect

of

acco

untin

g ch

ange

s in

yea

rs

- 1

to

+ 1

is th

e su

m o

f th

e ea

rnin

gs

effe

cts

resu

lting

fr

om a

ll ac

coun

ting

chan

ges

mad

e in

eve

nt y

ears

-

1 th

roug

h +

1.

Tot

al a

sset

s ar

e m

easu

red

in t

he y

ear

of t

he v

iola

tion.

z

306 A.P. Sweeney, Debt-covenant violations and managers’ accounting responses

to delay technical default, whereas firms making accounting changes require 19.6 percent and firms that delay technical default require only 0.9 percent. This evidence suggests that only firms with small required earnings effects actually delay technical default for one or more quarters via accounting changes.

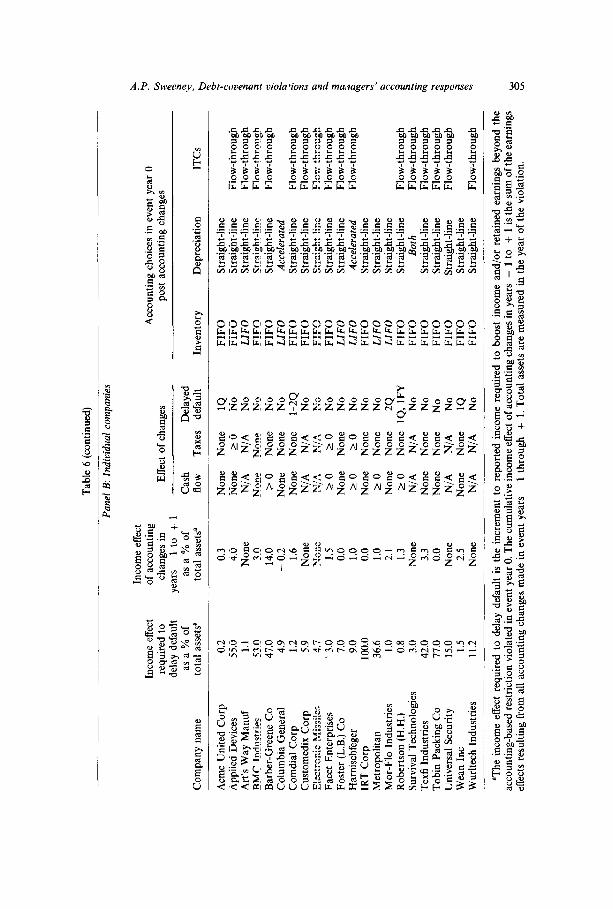

Panel B of table 6 provides details on individual companies. Twelve of the 22 firms make income-increasing accounting changes in event years - 1 to + 1. Only one firm makes income-decreasing changes in event years - 1 to + 1. The results show that five firms delay technical default for one or more quarters. Cash flows potentially increase because of accounting changes for five firms (not the same five that delayed technical default), and for three firms managers’ decisions potentially decreased cash flows (via increased taxes). Managers’ decisions have no significant effect on cash flows or the timing of the technical defaults for the remaining six firms that make accounting changes in event years -1 to +l.