Embed Size (px)

Citation preview

1

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Deep Dive: THE CHANGING

RETAIL LANDSCAPE & THE EVOLVING

OPPORTUNITY FOR BETTER DEMAND

PLANNING

D E B O R A H W E I N S W I G

M a n a g i n g D i r e c t o r , F u n g G l o b a l R e t a i l & T e c h n o l o g y d e b o r a h w e i n s w i g @ f u n g 1 9 3 7 . c o m

U S : 6 4 6 . 8 3 9 . 7 0 1 7 H K : 8 5 2 . 6 1 1 9 . 1 7 7 9

C N : 8 6 . 1 8 6 . 1 4 2 0 . 3 0 1 6

1) Weseeanincreasingdisconnectbetweentheproliferationofmultiple distribution channels and some of the demand-planning models that were built around supplying goods tobrick-and-mortarstores.

2) Demandplanningaffectsinventoryplanning,whichfeedsintoaretailer’sreturnoncapital.Weexaminethefinancialdataofpubliclytradedretailersacrossdifferentproductverticals,andconclude that efficient demand planning is particularlyimportantfortheapparelandfootwearindustry.

3) We recommend that retailers adopt sophisticated demand-planning solutions to better align their inventory plans andpurchasingdecisionswiththeircustomers’demands.

4) In this report, we introduce the more prominent demand-planningsolutionsavailableonthemarket.Wealsohighlightsuccessful casesof apparel retailers that have leveraged thetechnologies of 7thonline – a provider of cross-channelmerchandise management solutions to the Apparel,Footwear, andAccessories (AFA) industry – in fulfilling theirdemand-planningstrategies.

2

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

3

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

TABLEOF CONTENTSEXECUTIVESUMMARY......................................................................................................................5

INTRODUCINGDEMANDPLANNING.................................................................................................6

OUREXPECTATIONSFORTHEEXTERNALCONSUMERRETAILENVIRONMENT...................................6

THECHALLENGESOFNEWCONSUMERNORMSTODEMANDPLANNING........................................10

OTHERKEYCHALLENGESINTHEAREAOFDEMANDPLANNING......................................................11

WHATTHECHANGESMEANFORDEMANDPLANNING...................................................................12

FINANCIALANALYSISOFINVENTORYTURNOVER...........................................................................15

COMMERCIALAPPLICATIONSOFDEMANDPLANNING...................................................................21

INTRODUCING7THONLINE.............................................................................................................21

APPENDIX.......................................................................................................................................24

4

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

5

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

EXECUTIVESUMMARYRetailersarefacedwithanincreasinglycomplexretailenvironment,drivenby strong demand for e-commerce, more sophisticated consumerpreferences, increasing channel complexity and intensifying competition.We see an increasing disconnect between the new norms of consumerretailandsomeofthesupply-chainanddemand-planningmodelsthatwerebuilt around supplying goods to brick-and-mortar stores. The challenge isexacerbated for retailers that have to match demand and supply acrossmultiple channels (owned stores,wholesale, online and franchised stores)andfashionretailers,whichtypicallyhaveshorterproductlifecycles.

Externalities are the primary reason why retailers that have to matchdemandandsupplyacrossdifferentchannelsaremoreexposedandinneedofbetterdemand-planningprocesses.Inadditiontothedirect-to-customerbusiness,theseretailerstypicallydependontheirwholesaleandfranchiseecustomersforconsistentandtrustworthydemandplans.

We recommend that retailers adopt sophisticated demand-planningsolutionstobetteraligntheirsupply-chainsoperationsandtheircustomers’needs. Sophisticated demand-planning solutions help integrate inventoryplans, demand forecasts and purchasing decisions to meet customers’demands. As demand-planning decisions need to be anchored on morescientific approaches, applications that integrate planning, buying,allocation and predictive analytics in real-time are seen as powerfulalternativestospreadsheets.

The transition tobetterdemand-planningsolutionswillenable retailers tocreate a single, firm-wide viewofdemandby consolidatingdemandplansacrosstheirowned-store,wholesaleande-commercechannels.Moreover,better demandplanningwill lead to an improvement in forecast accuracythat ismore responsive to demand signals in real-time. This is consistentwith a notable shift of retailers’ supply chains to demand-driven supplychains(DDSC),ratherthanmerelyreactivesystems.

Better demand planning enables retailers to provide wider productavailability and be responsive to customer needs in a cost-effective way.Studies indicate that retailerswithhigherdemand-planningmaturityhavedemonstratedbetteroperatingandfinancialresults,includinghighersales,lower operating expenses, lower inventory holdings and faster inventoryturnover.

Demand planning affects inventory planning, which feeds into a retailer’sthe return on capital. We examine the financial data of publicly tradedretailers across different product verticals and distribution models. Weconclude that efficient demand planning is particularly important for theapparelandfootwear(AFA)industry.

In the final section of the report, we introduce the most prominentdemand-planning solutions vendors. We also highlight successful casestudies in the apparel industry that have leveraged the technologies of7thonline–aproviderofcross-channelmerchandisemanagementsolutionsto the AFA industry – which helped these retailers fulfil their demand-planningstrategies.

Formulatinganefficientdemand-planningprocessisanimportantpartofmanagingaretailbusiness.

Betterdemandplanninghasprovenadvantagesinimprovingcustomerexperience,generatingcostsavingsandincreasingassetproductivity.

Commercialapplicationsofdemandplanningcanassistretailersinmatchingsupplyanddemandeffectivelytomeettheirperformancetargets.

6

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

INTRODUCINGDEMANDPLANNINGDemand planning refers to the business process of predicting futuredemand for products, and then aligning production and distributioncapabilitiesaccordingly.Theendresult is tocreateademandplanalignedwithfinancialgoalsandinventoryplans.Theprocessinvolvesthesharingoftimely data, accurate processing of this data and agreement from variousbusinessfunctionsonjointbusinessplansalongthesupplychain.

Sophisticateddemandplanningwouldhelpa supplychainachieve itsgoalofdelivering the rightproduct, at the right time,at the rightplaceandattherightprice.Acustomer-orienteddemand-planningprocesswillallowforample inventory levels to meet immediate demand, and future demandprojectionsdrivenoffpredictiveanalytics.

Source:Shutterstock

OUREXPECTATIONSFORTHEEXTERNALCONSUMERRETAILENVIRONMENTWeexpecttheevolvingnormsoftheconsumerretailenvironmenttodrivean increased urgency for better demand-planning solutions for retailers.Today’s retail landscape engenders greater complexities which theconventionaldemand-planningmodelscannolongeradequatelycopewith.Digitaldisruption(particularlyonthedemandside)hasgivenrisetochangesin the retail landscape, such as new competitors, more sophisticatedconsumersandnewdistributionchannelswhichretailersarepittedagainst.Themesweexploredinclude:1)theneedforretailerstoconstantlyevolve;2)growingalternativesforconsumersfromtheemergenceofonlineretailers;3) howdistribution is impacted from“on-shelf availability” to “ondemandavailability”;and4)howtheaddedcomplexityofsourcingfromandsellingtoemergingmarketsincreasesglobalization.

Theretaillandscapeisconstantlyevolving,ascustomers’needsincreasinglydefinehowcompaniesstructuretheirsupplychainsanddemandplanning.

7

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

1.Retailers–theNeedtoConstantlyEvolveWiththeemergenceofmulti-channelretailers,incumbentphysicalretailersneedtoconstantlyadapttostayrelevant.Thenewbreedofretailerstheyarepittedagainstisnimbleacrossmultiplechannels,isintroducingalargervarietyofmerchandiseandturningoverinventoryatafasterpaceandwithmoresophisticatedfulfilment.

Moreover, the broader retail landscape has become more complex –retailers are operating in an increasing number of locations, with morebusinessunits,moremanufacturingsourcesandshorterproductlifecycles,andaresellingtomoremarketsinwhichconsumershavediversetastes.

2.Consumers–GrowingAlternativeswiththeEmergenceofOnlineRetailersChanges in consumer demand are driving the need for better demandplanning.Consumersnowexpectgreater convenience, faster speed,morecustomizedordersandmorefrequentorderchanges.Retailersareobligedto offer more flexible return policies and more product choices to fast-changingconsumertastes,yetatthesametime,maintainaggressivepricingin order to stay relevant with the consumers they sell to. This allnecessitatesbetterdemandplanning.

Source:Shutterstock

In addition, retailers need to adapt tomore volatile and uncertain globalconsumer demand, which has become more pronounced following theglobalfinancialcrisis,andresultedinreduceddemandvisibilityforretailers.Globaluncertainties (sharpcurrency fluctuations, financialandcommoditymarket volatility, divergent monetary policies across leading economies)have hindered a recovery in consumer confidence and are beyond thecontrolofretailers.

Themulti-channelconsumer’sincreasingexpectationforspeedandconvenienceisdrivingtheneedforbetterdemandplanning.

Retailersfacegreatercompetition,morefrequentproductlaunchesandshorterproductlifecycles.

8

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

3.Distribution–from“On-ShelfAvailability”to“OnDemandAvailability”Constantly under pressure to deliver merchandise according to theircustomers’ choice of place and time, has led retailers to rethink demandplanning. Omni-channel and e-commerce have increased channelcomplexityandchallengedexistingfulfilmentmodels.

The blurring of channel boundaries has led to an increasing number ofpermutationsof fulfilmentoptionsexpectedbyconsumers,whichchangesorderpatternsandnecessitatesdemandplanning.Examplesinclude:

• Multi-channel/omni-channel retail changes consumer orderpatterns.Anexamplewouldbebuyingin-storeandexpectinghomedelivery or alternative site collection, then requesting free returnsacrossallchannels.

• Immediate fulfilment, such as same- or next-day delivery, isbecomingthestandard.

• Mobileshoppingisincreasinglybridgingthegapbetweenonlineandofflinecommerce.

• Returns policy/reverse logistics: Retailers need to plan for returnsand exchanges, which account for 30% of e-commerce purchases,comparedtojust8%forphysicalstores,accordingtoCBRE.DatafromMIT SloanManagement Review indicated that retailers spend $100billion (3.8% of their profits) per year restocking and repackagingreturns.

Figure1.Retailers’StoreClosings,2010-15

Source:Bloomberg/Companyreports/FungGlobalRetail&Technology

-70% -60% -50% -40% -30% -20% -10% 0%

SearsaerieChristopherandBanksAbercrombie&FitchPacificSunwearKmartRestorakonHardwareOfficeMax/OfficeDepotAéropostaleSaksFiohAvenueBebeStoresHollisterUSLands'EndStaplesBarnes&NobleNewYork&CompanyWilliams-SonomaJCPenneyDillard'sRiteAidCorpGap

Theincreaseindistributionchannelsandblurringoftheirboundarieshaveincreasedoperationalcomplexityandcausedretailerstorethinkdemandplanning

Retailershavebeenswitchingtodistributionchannelsfrombrick-and-mortarstores.

9

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

4. IncreasedGlobalization– theAddedComplexityof Sourcing fromandSellingtoEmergingMarketsOnthesupplyside,retailersareincreasinglysourcingfromawiderrangeofpartners in developing countries, in order to take advantage of the costdifferentialsintermsoflaborandtherawmaterialsofthevariouscountries.For example, as costs in China have increased, there has been a shift inretailers’sourcingneeds–insteadofsolelyrelyingonChina,theynowrelyonarangeoflower-costcountries.Thisincreasesthecomplexityofdemandplanning, as the other countries’ infrastructure may be less mature andmorepronetonegativeexternalities.

On the demand side, changes in global economics developments anddemographicshavegivenrisetotheemergenceofnewconsumermarkets.Retailers with better retail-planning capabilities are best positioned tocustomize their offering to satisfy local consumer demands and seize theopportunity.

Figure2.DriversthatLeadtoIncreasingComplexityAlongtheSupplyChain

Source:KPMG

ExistingDemand-PlanningProcessesareInadequateMany demand-planning processes and supply chains were built forsupplyinggoodstophysicalstores,i.e.brick-and-mortarstores,andarenowoutdated andno longer able tomeet thenewnormsof e-commerce andmulti-channel retail. Hence, it is critical for retailers to improve theirdemand-planningcapabilitiesinordertocopewiththeincreasingdemandsfromconsumers.

Astudyondemandplanningbasedonretailers’self-assessmentdatafoundthat some retailers’ demand planning lacks maturity and can beoverwhelmed by unforeseen demand fluctuations. Some retailers arerelativelynewtoestablishingmaturedemand-planningprocesses.

Emergingtrendsinproductdevelopment,distributionchannelsandcustomerpreferenceshaveledtoincreasingcomplexityalongthesupplychain

10

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

THECHALLENGESOFNEWCONSUMERNORMSTODEMANDPLANNINGRetailers often find it challenging to match supply and demand acrossmultiplecustomersandchannels.

ChallengesAmplifiedforRetailersthatSellAcrossDifferentChannelsThechallengefordemandplanningisexacerbatedforretailersthathavetomatch supply and demand across multiple channels (owned stores,wholesale, online and franchised stores). In addition to their direct-to-customer business, these retailers are exposed to the externalities ofdemand planning, as they typically depend on their wholesale andfranchiseecustomersforconsistentandtrustworthydemandplans.

Thebullwhipeffectreferstoincreasingswingsindemandordervariabilityinthesupplychain,whichareamplifiedasonemovesupthesupplychain.Anexamplewould be due to the variability inwholesale orders: a distributorlikelyreliesonexternalresellers’demandforecaststomaketheir inventoryforecasts.However,thisexposesadistributortoorderswingswhenresellerssupplyinferiororderforecasts.Overtime,somedistributorshaverespondedbyparingdownontheirproportionofrevenuefromwholesalechannels.

Nike:Nikelauncheditsdirect-to-customer(DTC)initiative,whichfocusesondirect selling to customers. The decline in wholesale channel sales is ageneral trend among apparel companies that are increasing their focusonthe higher-margin retail channel where they have an opportunity to buildtheirbrandrelationshipwithcustomersandcollectcustomerdata.

Under Armour: The revenue shareofUnderArmour’swholesale segmenthasdeclinedfrom73%oftotalsalesinFY2010to66%inthelastfiscalyear.

VFCorp:VFCorp.’swholesalerevenueasapercentageoftotalrevenuehasdeclinedfrom81%inFY2010to72%inthelastfiscalyear.

Figure3.ApparelRetailers–RevenuefromRetailvsWholesale,LatestFiscalYear

Source:CapitalIQ/FungGlobalRetail&Technology

Demandplanningasameansofcounteractingthebullwhipeffectwithbetterdemandforecasts.

Retailersfaceadditionalchallenges,astheyneedtomatchsupplyanddemandacrossmultiplesaleschannels.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Prada

PVH

Burberry

Tod's

SalvatoreFerragamo

HugoBoss

Esprit

RalphLauren

Sketchers

G-IIIApparel

StevenMadden

Retail% Wholesale%

11

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Other retailers have increased the amount of excessive inventory as abufferagainstsharpfluctuationsindemand.

Itwouldbenefit retailers to control thebullwhipeffect and improve theirsupply-chain performance by coordinating information and demandplanning.

Figure4.Impacts&TopRecommendationsforDemandPlanningforRetailersthatSellinDifferentChannels

Impacts TopRecommendations

Lowdemand-planningmaturityhampersretaildemand-planningteams'abilitytohandoffaccurateforecaststosupply-planningteams

• AdministerGartner’sretaildemand-planningmaturityself-assessmenttoidentifycurrentmaturitylevelandestablishnear-termpriorities

• Identifytechnologyanddatarequirementsneededtoestablishedforecast-accuracymeasurements

Inconsistentdemand-planningprocessesandoutputsacrosskeycustomersrestrictretailers'abilitytocreateasinglefirm-wideviewofdemand

• Measureaccuracyofcustomerforecastsasinputintodemandconsolidationactivity,andmakesupplydecisionsaccordingly

• Tomanagesituationsoflimitedsupply,createscarcityofsupplyrulesandguidelines

Creatingaconsolidateddemandplanforretailer-ownedstoreandwholesalechannelsischallengingforverticallyintegratedretailers

• Capturedemandstreamsfromallchannelsintoasingleconsolidatedviewofdemand

• Addthecapabilitytoviewsupplyanddemandinbothunitsanddollarstoimprovebusinesstrade-offdecisions

Source:Gartner

OTHERKEYCHALLENGESINTHEAREAOFDEMANDPLANNINGWe have identified other major challenges that retailers face in demandplanning,whichinclude:

• Insufficientinternalcollaborationleadingtodisaggregateddemandforecast outputs: There may be a lack of communication andcoordination among departments. This results in siloed demandplanningacrossowned-stores,wholesaleande-commercechannelsratherthanafirm-wideforecastfordemand.

• Poordata integrity:Thelackofanintegrateddemand-planningtoolorprocesswill lead to inconsistentdemand forecasts.Forexample,someretailersmaystillberelyingonspreadsheetsforforecasting.

• Lack of robust forecast assumptions and methodology: Irregularsalespromotionsandmarketingactivities that impact sales, butdonot havehistorical patterns,maybe left out of a demand-planningmodelthatreliesonhistoricalpatterns.

• Lackofstandardizationwithresellers:Theresellersandfranchiseesthat retailers sell to may lack the technology standardization andformalsalesandoperationsplanning(S&OP)processes.

• Difficultyingettingtimelycustomerdemanddata.

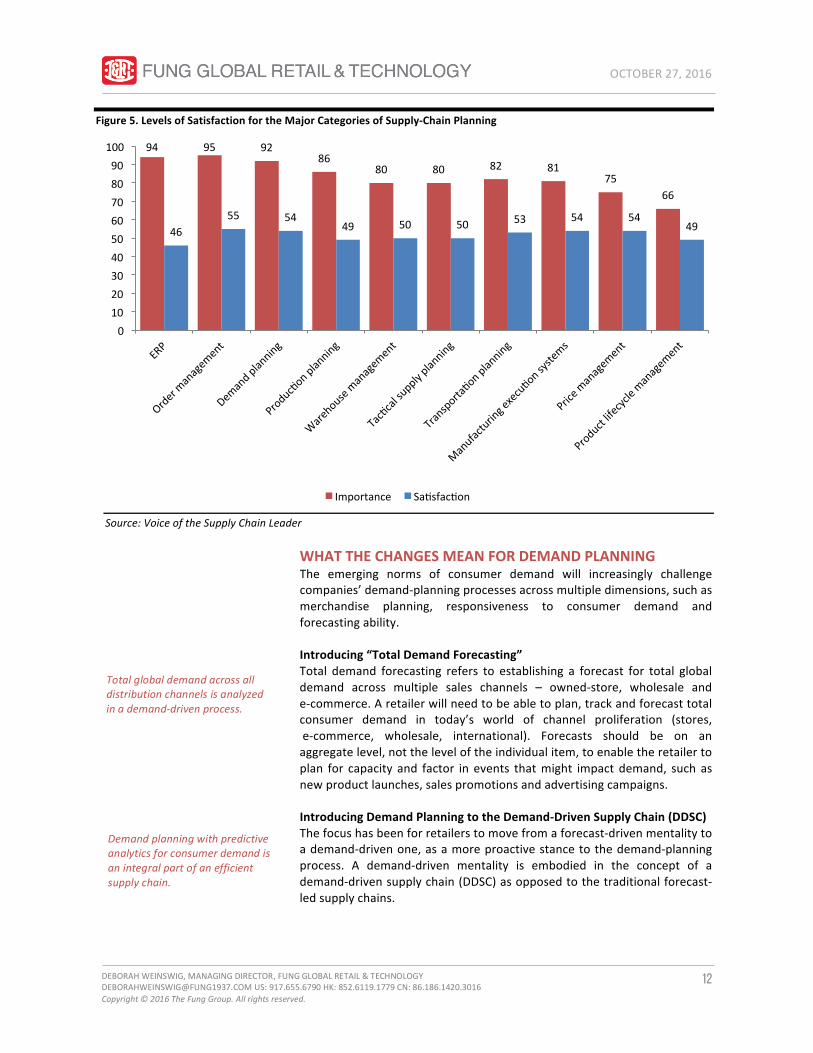

Demandplanninghasthelargestgapbetweensatisfactionandperformance.

12

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Figure5.LevelsofSatisfactionfortheMajorCategoriesofSupply-ChainPlanning

Source:VoiceoftheSupplyChainLeader

WHATTHECHANGESMEANFORDEMANDPLANNINGThe emerging norms of consumer demand will increasingly challengecompanies’demand-planningprocessesacrossmultipledimensions,suchasmerchandise planning, responsiveness to consumer demand andforecastingability.

Introducing“TotalDemandForecasting”Total demand forecasting refers to establishing a forecast for total globaldemand across multiple sales channels – owned-store, wholesale ande-commerce.Aretailerwillneedtobeabletoplan,trackandforecasttotalconsumer demand in today’s world of channel proliferation (stores,e-commerce, wholesale, international). Forecasts should be on anaggregatelevel,nottheleveloftheindividualitem,toenabletheretailertoplan for capacity and factor in events thatmight impact demand, such asnewproductlaunches,salespromotionsandadvertisingcampaigns.

IntroducingDemandPlanningtotheDemand-DrivenSupplyChain(DDSC)Thefocushasbeenforretailerstomovefromaforecast-drivenmentalitytoademand-drivenone,asamoreproactivestancetothedemand-planningprocess. A demand-driven mentality is embodied in the concept of ademand-drivensupplychain(DDSC)asopposedtothetraditionalforecast-ledsupplychains.

Totalglobaldemandacrossalldistributionchannelsisanalyzedinademand-drivenprocess.

Demandplanningwithpredictiveanalyticsforconsumerdemandisanintegralpartofanefficientsupplychain.

94 95 9286

80 80 82 8175

66

4655 54

49 50 50 53 54 5449

0102030405060708090100

Importance Saksfackon

13

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

TheKeyBenefitsofDemandPlanningThe aim of demand planning is to ensure that a retailer can achieve thehighest level of customer satisfaction through on-time deliveries withminimuminventoryandcosts.

The key business benefits that can be derived from demand planningsolutionsare:

• Accurateinventorylevelsforecastsacrossallchannelsandregions.

• Increasedefficienciesandstreamlineprocesses.

• Improvedcustomersatisfaction.

• Ability to respond to extreme seasonality and volumes, optimizedinventorypositions.

• Seamlessintegrationacrossmultiplechannels.

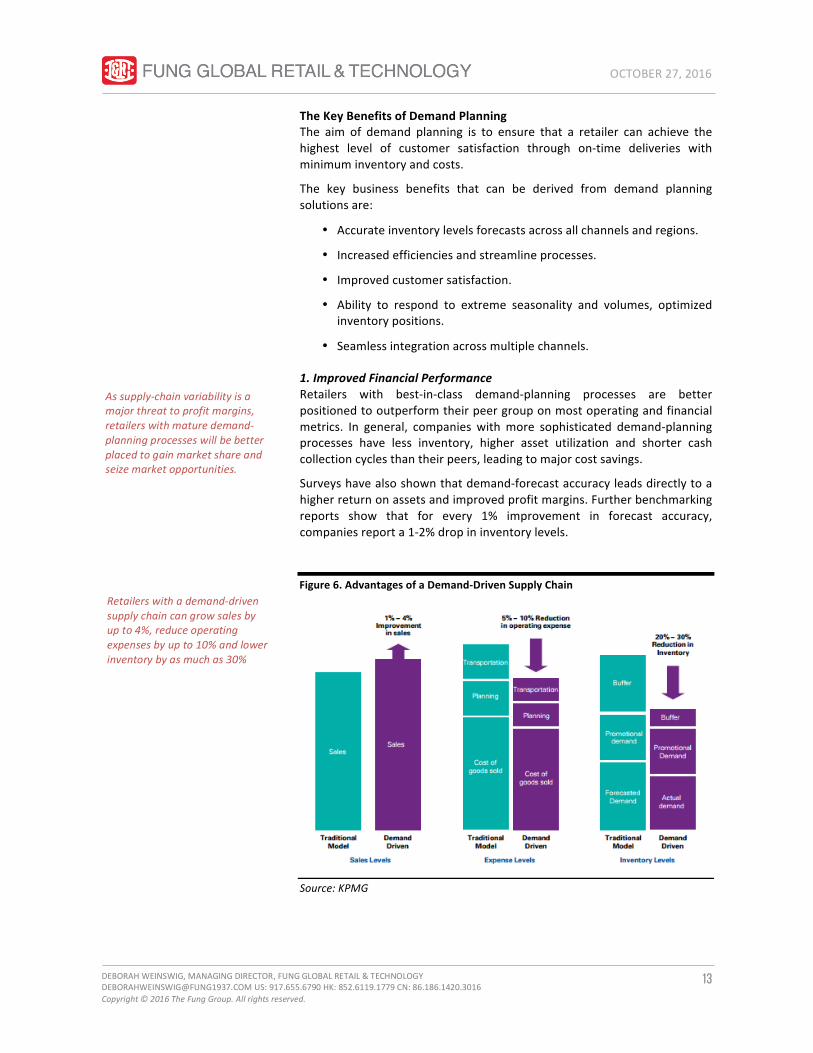

1.ImprovedFinancialPerformanceRetailers with best-in-class demand-planning processes are betterpositionedtooutperformtheirpeergrouponmostoperatingandfinancialmetrics. In general, companies withmore sophisticated demand-planningprocesses have less inventory, higher asset utilization and shorter cashcollectioncyclesthantheirpeers,leadingtomajorcostsavings.

Surveyshavealsoshownthatdemand-forecastaccuracyleadsdirectlytoahigherreturnonassetsandimprovedprofitmargins.Furtherbenchmarkingreports show that for every 1% improvement in forecast accuracy,companiesreporta1-2%dropininventorylevels.

Figure6.AdvantagesofaDemand-DrivenSupplyChain

Source:KPMG

Assupply-chainvariabilityisamajorthreattoprofitmargins,retailerswithmaturedemand-planningprocesseswillbebetterplacedtogainmarketshareandseizemarketopportunities.

Retailerswithademand-drivensupplychaincangrowsalesbyupto4%,reduceoperatingexpensesbyupto10%andlowerinventorybyasmuchas30%

14

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

IntroducingInventoryTurnoverandWhyItMattersforRetailersThe inventoryturnoverratiomeasureshowefficientlyacompanymanagesinventory,andtherateatwhichinventoryissoldoveraspecificperiod.Theinventory turnover ratio and profit margins are the primary drivers thatdirectlyimpactreturnoncapital(ROC),whichmeasureshowwellacompanyuses itscapital togeneratereturns. Ingeneral,ahigher inventory turnoverratio is preferred, as it indicates that a retailer is efficient in turning itsinventorytosales.

Advantagesofhighinventoryturnoverforaretailer:

• Betterfinancingterms:Higherinventoryturnoverallowsaretailertorely on its suppliers’ capital to finance its inventory rather than itsown capital. When inventory is turned over more rapidly, moreinventories are financed through payment terms provided bysuppliersratherthanaretailer’sworkingcapital.

• Lowerriskofobsolescence:Ahigherinventoryturnoverservesasamoat for retailers’ profit margins. Should a retailer’s rate ofinventory turnover dip, there is the risk of the inventory turningobsolete, or the risk of having to liquidate inventory at suboptimalprices.

• Higher operating leverage: Higher inventory turns means thatoperatingcostscanbespreadacrossalargerrevenuebase.Retailerswillbeabletochargelowerpricesrelativetotheirpeers,whichsetsoff a virtuous cycle of lowerprices attracting customers to shop attheirstores.

More sophisticated demand-planning solutions seek to address theunderlyingreasonsthatcouldleadtoalowinventoryturnoverratio,whichincludearetailer:

• Makinginefficientinventorypurchasingdecisions.

• Keeping toomuch inventoryonhand.Retailers thathaveexcessiveinventory on handmay need to sell off their obsolete inventory atheavilydiscountedprices,whichdepressesprofitmargins.

Demandplanningaffectsinventoryturnover,whichultimatelyinfluencesaretailer’sreturnoncapital

15

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

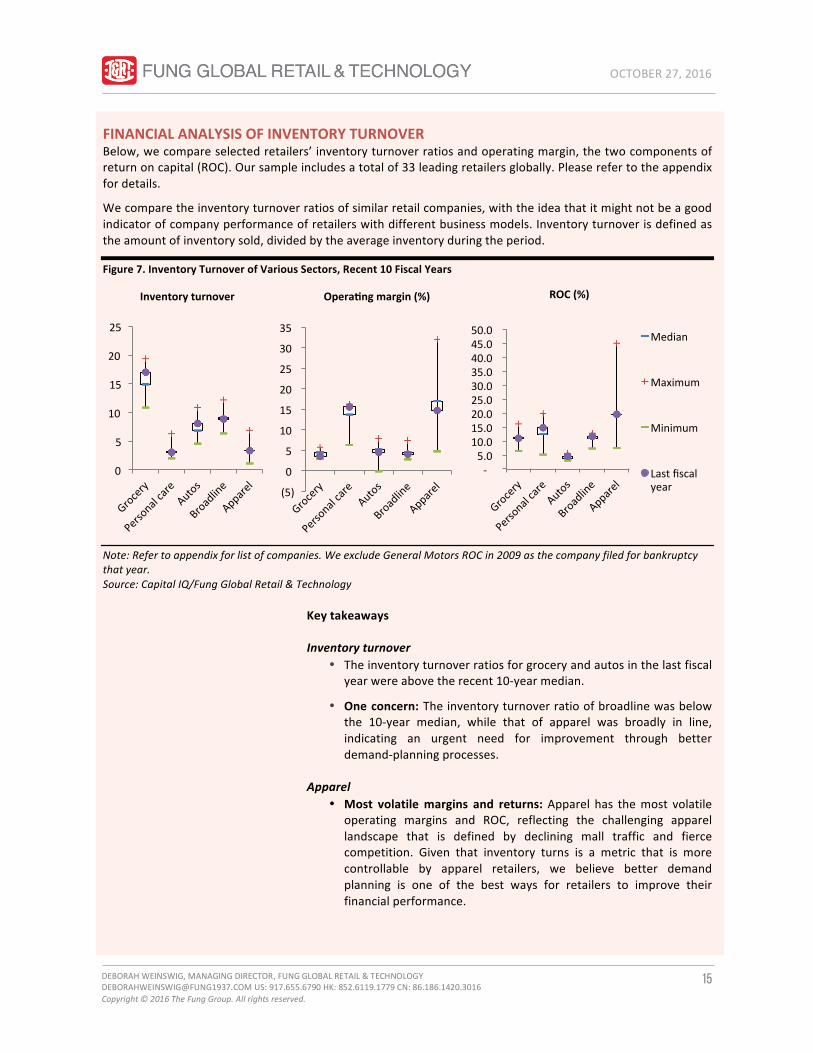

FINANCIALANALYSISOFINVENTORYTURNOVERBelow,wecompareselectedretailers’inventoryturnoverratiosandoperatingmargin,thetwocomponentsofreturnoncapital(ROC).Oursampleincludesatotalof33leadingretailersglobally.Pleaserefertotheappendixfordetails.

Wecomparetheinventoryturnoverratiosofsimilarretailcompanies,withtheideathatitmightnotbeagoodindicatorofcompanyperformanceofretailerswithdifferentbusinessmodels.Inventoryturnoverisdefinedastheamountofinventorysold,dividedbytheaverageinventoryduringtheperiod.

Figure7.InventoryTurnoverofVariousSectors,Recent10FiscalYears

Note:Refertoappendixforlistofcompanies.WeexcludeGeneralMotorsROCin2009asthecompanyfiledforbankruptcythatyear.Source:CapitalIQ/FungGlobalRetail&Technology

Keytakeaways

Inventoryturnover• Theinventoryturnoverratiosforgroceryandautosinthelastfiscal

yearwereabovetherecent10-yearmedian.

• Oneconcern:Theinventoryturnoverratioofbroadlinewasbelowthe 10-year median, while that of apparel was broadly in line,indicating an urgent need for improvement through betterdemand-planningprocesses.

Apparel• Most volatilemargins and returns: Apparel has themost volatile

operating margins and ROC, reflecting the challenging apparellandscape that is defined by declining mall traffic and fiercecompetition. Given that inventory turns is a metric that is morecontrollable by apparel retailers, we believe better demandplanning is one of the best ways for retailers to improve theirfinancialperformance.

0

5

10

15

20

25

Inventoryturnover

(5)

0

5

10

15

20

25

30

35

Operagngmargin(%)

-5.010.015.020.025.030.035.040.045.050.0

ROC(%)

Median

Maximum

Minimum

Lastfiscalyear

16

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Figure8.InventoryTurnoverofSub-categoriesoftheAFAIndustryRetail,Recent10FiscalYears

Source:CapitalIQ/FungGlobalRetail&Technology

Apparel–MeasuringthePerformanceofSubcategories• The relatively wide range between the historical maximum

and minimum inventory turnover ratio imply that there ismuch room for improvement through better demandplanning.

• The inventory turnover ratios of fast-fashion and generalapparelinthemostrecentfiscalyeararebelowthehistorical10-yearmedian.

Figure9.InventoryTurnoverandMarginsofSub-categoriesoftheAFAIndustryRetail,Recent10FiscalYears

Source:CapitalIQ/FungGlobalRetail&Technology

ConclusionsRetailers with the highest inventory turnover include grocery and fastfashion, industries defined by relatively higher volumes. High inventoryturnover in low-margin industries is necessary to offset lower per-unitprofitswithhigherunitsalesvolumeandremaincash-flowpositive.

0

2

4

6

8

Fastfashion

Luxury Generalapparel

Inventoryturnover

0

5

10

15

20

25

30

35

Fastfashion

Luxury Generalapparel

Operagngmargin(%)

0

10

20

30

40

50

Fastfashion

Luxury Generalapparel

ROC(%)

Median

Maximum

Minimum

Lastfiscalyearmedian

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

- 1.0 2.0 3.0 4.0 5.0 6.0

Ope

ragn

gmargin(%

)

Inventoryturns(x)

Fastfashion Luxury Apparel-General

Fastfashion2016

Luxury2016Apparel-General

2016

Ahighinventoryturnoverratioisakeyadvantageinretail,allthingsequal.

Sophisticateddemand-planningsolutionswillleadtomoreefficientinventorymanagementandhigherreturns.

17

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

2.TheImpactofDistributingonDifferentChannelsWe also examine the impact of shifting distribution models to demandplanning needs. The three ongoing trends that have been impacting thedistributionmodelandprofitabilityofbrandsandretailersare:

• Theincreasingprominenceofe-commerce.

• Thescalingbackofretailersfromwholesaledistribution.

• Theomni-channelstrategiesofretailers.

BrandsLeaningTowardsOmni-ChannelandDTCStrategiesSome apparel retailers such asNike, VF Corp andG-III ApparelGroup arescalingbacktheirwholesaleoperationsandfocusingmoreonDTC(directtocustomer) channels, resulting in increasing DTC contribution to the salesmix. For other brands, such as Sketchers and Burberry, theirmost recentfinancialresultswerenegativelyimpactedbywholesaledistribution.

Source:Shutterstock

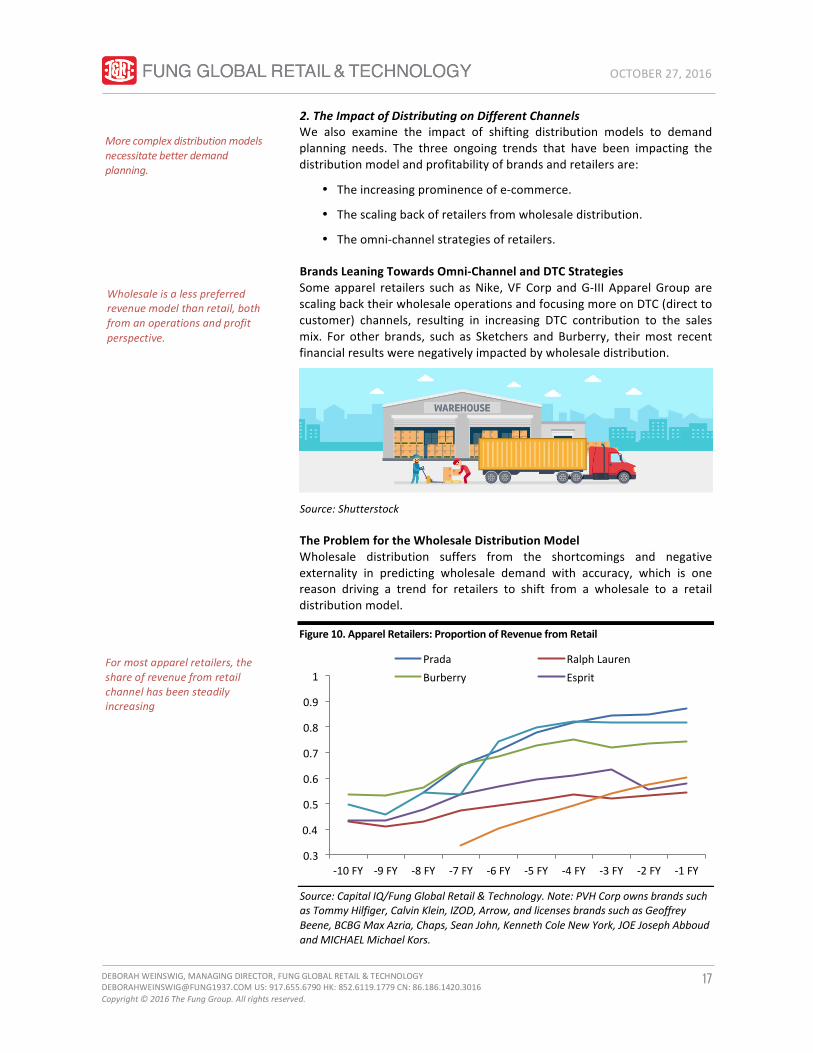

TheProblemfortheWholesaleDistributionModelWholesale distribution suffers from the shortcomings and negativeexternality in predicting wholesale demand with accuracy, which is onereason driving a trend for retailers to shift from a wholesale to a retaildistributionmodel.

Figure10.ApparelRetailers:ProportionofRevenuefromRetail

Source:CapitalIQ/FungGlobalRetail&Technology.Note:PVHCorpownsbrandssuchasTommyHilfiger,CalvinKlein,IZOD,Arrow,andlicensesbrandssuchasGeoffreyBeene,BCBGMaxAzria,Chaps,SeanJohn,KennethColeNewYork,JOEJosephAbboudandMICHAELMichaelKors.

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-10FY -9FY -8FY -7FY -6FY -5FY -4FY -3FY -2FY -1FY

Prada RalphLaurenBurberry Esprit

Morecomplexdistributionmodelsnecessitatebetterdemandplanning.

Wholesaleisalesspreferredrevenuemodelthanretail,bothfromanoperationsandprofitperspective.

Formostapparelretailers,theshareofrevenuefromretailchannelhasbeensteadilyincreasing

18

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

For example, resellers who buy from these brands may have lesssophisticated demand-planning systems that cause them to place ordersbased on inaccurate demand forecasts. These resellers may cancel andreturnordersorsellproductsatheavilydiscountedprices.SellingatalowerASPwouldleadtolowerprofitability.

Generally, DTC revenue earns higher margins for apparel companiescomparedtosalesthroughthewholesalechannel.However,webelievethewholesalerevenuemodelisheretostay.

3.DemandPlanningProcessesareIncreasinglyEmbeddedintoanOrganizationalCultureDemand planning plays a critical role in helping retailers achieve theirgrowth objectives, as it is an integrated business-planning process thatdrivesdecisionmakingattheenterpriselevel.

Source:Shutterstock

Demand planning should capture the total global demand across all saleschannels, which serves as a foundation for stakeholders of a company toplan ahead. The data is available for, and can be used to support, otherfunctionalareasinmakingoperationalandmanagerialdecisions.

Betterdemand-planningsolutionsleadtomoreconsistentdemandforecasts,whichenableretailerstocreateasingle,firm-wideviewofdemand.

Asdemandplanning iscloselytiedwithoverallprofitabilityandthehealthofaretailer,belowaresomenotabletrendsinthearea:

• Increasingfrequencyofsalesandoperationsplanning:Historically,demand and capacity planning was done in monthly cycles.Nowadays,many companies have sped up their planning cycles toweekly,orasoftenasdailyforfast-movingcategories.

• Demand planning established as a best practice: The breadth ofdemand planning can be broadened to cover Integrated BusinessPlanning(IBP),whichallowsstakeholderstobeinvolvedinbalancingsupplyanddemandinawaythatmaximizesprofits.

Theevolvingroleofdemandplanningwithinanorganizationfromreactivetoproactive.

19

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

• Companies can integrate the valueof their products intodemandplanning: Instead of merely reacting to market changes,organizations can proactively shape their demand. For example, aretailercandecidetoshiftdemandtohigher-marginproducts.

TechnologicalDevelopmentsinDemandPlanningSolutionsThe demand-planning process has evolved over time to incorporatemoreintegratedprocessesandbettercaptureanenterpriseviewofdemand.

For example, mature demand-planning solutions make use of predictiveanalyticstoestablishaccuratedemandforecaststhatcanbereadilyappliedtototalconsumerdemandforecasting.

Figure11.TechnologicalDevelopmentinDemandPlanningProcesses

Source:FungGlobalRetail&Technology

Below are some benefits and unique functions of proprietary demand-planningsolutions:

• Provideenterprise levelvisibility intodemandacrossalldistributionchannelsandregions.

• Offeraclearmethodologyandimplementationstrategytooptimizeplanningandforecasting.

• Demonstratetheexactrelationshipbetweenproductandprofits.

ManualPlanning

BasicHomegrownSystems

Commericalapplicakons• Sooware• Consulkng

Demandplanninghasevolvedfrombeingdoneonspreadsheetstocommercialapplicationstotailortomorecomplexneeds

20

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Figure12.TechnologicalDevelopmentsintheDemand-PlanningProcesses

StagesofDemandPlanning Characteristics

1 Manualplanningsolutions • Definition:Referstorelyingonmanualmethodstomanageinventoryandplanning,for example, entering the products and quantities that have been delivered intospreadsheets.Suitableforsmallbusinessesthatcarryalimitedamountofinventoryorthatturnsoverinventoryslowly.

• Advantage:Savemoneyonsoftware,bettercontrolwithoutrelianceoncomputer.

• Disadvantage:Labor-intensive,pronetohumanerror.

2 Basichomegrownsystems • Definition:Referstoaretailmanagementsystembuiltbyin-housetalent.

• Advantage:Betterfit.

• Disadvantage:Therisksandexpenseeventuallybecomeoverwhelming,asahome-grownsystemlagsbehindthecompany’sgrowth.

3A Commercialapplications-demand-planningsoftware

• Definition:Referstoacomputer-basedsystemforretailsalesanalysisanddemandplanning.

3B Commercialapplications–demand-planningconsulting

• Definition: Refers to consulting services including demand planning and retailanalytics.-e.g.:Fashionretailersdeploymoderndemand-planningtechniquestoshortenleadtime,adoptefficientinventorypolicyandenhanceproductquality.

Source:FungGlobalRetail&Technology

EvolutionandFutureStateofDemandPlanningWe highlight other technologies that can facilitate or potentially disruptdemandplanninginthefollowingtable.

Figure13.DisruptiveTechnologyRelatedtoDemandPlanning

Technology Benefits

Predictiveanalytics • Reduceforecastingerrors

• Betterpredictionsforproductandpartsdemand

• Reduceoverallresourcesneededforinventorymanagement

Automation • Easiertotrackpurchasing

• Areductionindemandofhumaninputandoutput

Sensorsandautomaticidentification

• The adoption of RFID systems makes inventory management easier and moreaccurate,improvingdemandplanning

Wearablesandmobiletechnologies

• Mobileandtabletdevicessuchassmartwatchescouldhelpsitemanagersobservereal-timeperformanceofinventorylevelsanddeliveries

• Supportsupply-chainmanagementfunctions

21

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Technology Benefits

Cloudcomputingandbigdata • Greaterinventoryaccuracyandminimizecostbybetteroptimizingoperations

3Dprinting • Facilitateson-demandproductionandcanreduceinventoryholdings

Machinelearning • Providesmorerelevantdata• Optimizingproductionworkflowsandinventory

Source:FungGlobalRetail&Technology

COMMERCIALAPPLICATIONSOFDEMANDPLANNINGCommercial applications that provide tools and advice for retailers fordemandplanningincludethefollowing(Refertotheappendixfordetailsonthedemand-planningsolutionsforselectedpeergroups.).

• 7thonline

• F.CurtisBarry&Company

• Oracle

• JDA

• SAPRetail

• FirstInsight

INTRODUCING7THONLINE7thonline is a company that provides cross-channel, global demandplanning solutions for the Apparel, Footwear, and Accessories (AFA)industry. 7thonline offers cloud-based solutions that are specificallydesigned for the AFA industry covering all channels, including wholesale,retail and ecommerce. The company provides a basis for planning globaldemand,ratherthanbeinglimitedbyaretail-heavyworldview.

DistinguishingFeaturesof7thonline• Provides both retail-/store-based and wholesale-/account-based

assortmentplanning.

• Provides corporate-level demand-planning services for corporateteams to see total demand, followed by planning, forecasting andtracking.

• PossessesAFA industry-specificknowledge,specialized forshort-lifecycleandfast-turnovergoods.

• Advanced cloud-based technologies such as AFA industry-specificandproprietaryalgorithms.

The key capabilities of 7thonline span planning, demand forecasting andinventoryoptimizingforomni-channelbrands,including:

• Providesa comprehensiveassortmentand sizeoptimization servicethat adopts its technologies, such as proprietary optimizationalgorithms.

22

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

• Provides customers with real-time inventory information with itscloud-basedtechnologies.

• Provides consulting services, as well as ensures efficientimplementationwithquickoutcomes.

• Provides comprehensive services covering planning, demandforecastingandinventoryoptimizationforomni-channelbrands.

How7thonlineWorks7thonline has built out tools to support these types of complexmultichannel brands. These brands can use 7thonline to perform bothretail-/store-based planning and wholesale-/account-based assortmentplanning.

• 7thonlinegetstoknowclients’needsaccordingtotheirselectionofplanningplans.

• Forbettermerchandiseandassortmentplanningservices,7thonlineanalyzes the clients’ performance or indicators, and provides anoptimizedplanforclients.

• Detailssuchasinventoryandsalesinformationwillbeupdatedinthesystemwithaccuracyandspeed.

• 7thonlineenablesclientstoforecastandmakereports.

According to users, the benefits of 7thonline include improved sales,profitabilityandmoreefficientworkingcapitalmanagement.Forexample,the overall results for a direct-to-consumer suite saw up to 30% lowermarkdowns,a5-10%increaseinfull-pricesell-through,a1-3%reductioninlost sales,1-3 timesgreater inventory turnsandup toa30% reduction inadministrativeexpenditures,accordingtothecompany’sofficialsite.

23

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Figure14.7thonline–SelectedCaseStudies

Patagonia JimmyJazz BrooksBrothers

EffectivePlanning

• Planningbasedoncategory,classandseasonalattributes.

• Useglobaldemandplanningtodrivesupplychain/resourceefficiency.

• Buyersdonotneedtoloadinformationfromthedatabasetoexcelspreadsheets.

• Thedivision’smonthlybudgetmeetingswereshortenedfromtwodaystoone.

• Thesystemupdatesdaily,sothecompanyisenabledtoseeatanytimewhat’sonorderforeverymonth.

• Cloud-basedsolutionensuresquickspeedtomarket.

• Thevisibilityoftotaldemand,totalresults,totalinventorypositionsinatimelymannerandacrosstheentireorganization.

DemandForecasting

• Analyzecurrenttrendsonaweeklybasis.

• Comparecurrentdatawiththatfromabouttwoyearsprevious.

• Greataccuracyinfuturebusinessforecasts.

• Thesystemforecastsintothefuturewhethertherewillbeasmallorabiggainandhowmuchofarisk.

• Bemoreproactiveaboutanalyzingdataandstayaheadoffast-changingtrends.

• Totaldemand,totalresults,totalinventorypositionsarevisible.

• Thetimelyvisibilityofdemandsacrosstheentireorganizationhelpsforecastdemandmoreaccurately.

InventoryOptimization

• Inventoryplanningatthestyle,colorandsizelevel

• Inventorylevelsreduction• Salesandsell-throughrates

increase

• Modernizeandstreamlineinventoryprocess

Source:Companydata

24

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

APPENDIX Figure15.CompanyComparison

7thonline Oracle JDA

Targetbusinesssize/scalability

Tier-1,fast-growingMedium Medium Notindicatedoncompanywebsite

Solutionofferings

DTC(retail&ecommerce) Enterpriseplanning Manufacturing&DistributionSolutions

Merchandiseplanning&execution

Supply-chainmanagement Omni-ChannelRetailSolutions

Wholesalemerchandiseplanning&execution

Data,humanresources,financialmanagement

PricingandRevenueManagementforService-BasedIndustries

Characteristics Demand-driven,withtotalenterpriseviewofdemand

Utilizesbigdata Experienceinwideindustries

Specializedforshort-lifecycle,fast-turngoods

Providespackagedsolutionsforgrowingcompanies

ComplementedbythinktankJDALabswithregardstosupply-chaininnovations

Industry-specific,proprietaryalgorithms

Industryfocus Apparel,footwear,accessories 24includingretail,wholesaledistribution,healthcare,chemicals

About20includingFashion,Restaurants&FoodServiceandConsumerElectronics

Yearfounded 1999 1989 1985

Offices US,MainlandChina India,Netherlands,Russia,Greece,US,France,Chile,DubaiIreland,SouthKorea,Germany,China,Singapore,Japan,UK,Canada

Mexico,India,Poland

Source:Companydata/FungGlobalRetail&Technology

Figure16.CompanyComparison

F.CurtisBarry&Company SAPRetail FirstInsight

Targetbusinesssize/scalability

Notindicatedoncompanywebsite

Small,medium Notindicatedoncompanywebsite

Solutionofferings Businessprocessassessment&improvement

Merchandisingoptimization,includingprice,promotion,andmarkdown

Guidanceforproductdesign,buying,assortmentplanning,pricing

Systemsselection&implementation

StoreoperationsincludingaportfolioofPOSsolutions

Forward-lookingviewofcustomerdemandandmerchandiseprofitability

Third-partyfulfillmentevaluating&callcenter

Supplychain Inventoryinvestmentrecommendations

25

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

F.CurtisBarry&Company SAPRetail FirstInsight

Characteristics Multi-channelindustryknowledgecoveringbusiness,operationsandsystems

SAPHANA,in-memorycomputingplatformthatacceleratesbusinessprocessesandsimplifiesITenvironment

InsightSuite,theworld’sonlyforward-lookingpredictiveanalyticplatform,enablespredictionwithnosaleshistory

Multi-channelbusinessproducts

Quickreactionwithinclients’timelineandbudget

Constantcommunicationandsuccessfulimplementationswithvendors

Industryfocus Apparel,Luxury,Healthcare,PetSupplies,Electronics

25includingretail,wholesaledistribution,banking,healthcare,hightech

Luxury,consumerproducts

Yearfounded 1984 1996 2007

Offices US US,Europe,MiddleEast&Africa,AsiaPacific

US

Source:Companydata/FungGlobalRetail&Technology

Figure17.SampleofRetailCompanies

Subsector Company MarketCap(US$mn) Companydescription

Apparel–FastFashion

IndustriadeDisenoTextilSA

112,386 IndustriadeDiseñoTextil,S.A.,afashionretailerthatdistributesclothing,footwear,accessoriesandhouseholdtextileproductsthroughvariousstoreformatsinEurope,theAmericas,Asiaandinternationally.

H&MHennes&MauritzAB

48,131 H&MHennes&MauritzAB(publ)providesclothes,shoes,bags,jewelry,make-upproducts,underwearandaccessoriesforwomen,men,teenagersandchildren.

FastRetailingCo.Ltd. 35,625 FastRetailingCo.,Ltd.,throughitssubsidiaries,operatesasanapparelretailerinJapanandinternationally.

NextPlc 8,377 NEXTplcengagesintheretailofclothing,footwear,accessoriesandhomeproductsformen,womenandchildrenintheUK,therestofEurope,theMiddleEast,Asiaandinternationally.

Apparel–Luxury

LVMHMoëtHennessyLouisVuittonS.E.

91,421 LVMHMoëtHennessyLouisVuittonS.E.operatesasaluxury-productscompanyworldwide.

HermèsInternationalSociétéencommanditeparactions

41,665 HermèsInternationalsociétéencommanditeparactions,togetherwithitssubsidiaries,engagesintheproductionandretailandwholesaledistributionofgoodsworldwide.

26

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Subsector Company MarketCap(US$mn) Companydescription

ChristianDiorSE 33,742 ChristianDiorSE,throughitssubsidiaries,engagesintheproduction,distributionandretailoffashionandleathergoods,winesandspirits,perfumesandcosmetics,footwearandaccessories,andwatchesandjewelry.

Coach,Inc. 9,965 Coach,Inc.providesluxuryaccessoriesandlifestylebrands.

MichaelKorsHoldingsLimited

8,272 MichaelKorsHoldingsLimitedengagesinthedesign,marketing,distributionandretailingofbrandedwomen’sapparelandaccessories,andmen’sapparel.

Apparel&Sportswear

NIKE,Inc. 86,219 NIKE,Inc.,togetherwithitssubsidiaries,designs,develops,marketsandsellsathleticfootwear,apparel,equipmentandaccessoriesworldwide.

AdidasAG 34,130 AdidasAG,togetherwithitssubsidiaries,designs,develops,producesandmarketsathleticandsportslifestyleproductsworldwide.

TheGap,Inc. 10,524 TheGap,Inc.operatesasanapparelretailcompanyworldwide.

FootLocker,Inc. 9,052 FootLocker,Inc.operatesasanathleticshoesandapparelretailer.

Abercrombie&FitchCo. 1,066 Abercrombie&FitchCo.,throughitssubsidiaries,operatesasaspecialtyretailerofcasualapparel.

Source:CapitalIQ/FungGlobalRetail&Technology

Figure18.SampleofRetailCompanies

Subsector Company MarketCap(US$mn) CompanyDescription

Grocery

TheKrogerCo. 29,043 TheKrogerCo.,togetherwithitssubsidiaries,operatesasaretailerintheUS.

KoninklijkeAholdDelhaize 28,771 KoninklijkeAholdDelhaizeN.V.operatesfoodretailstoresintheUS,EuropeandSouthEastAsia.

WoolworthsLimited 24,649 WoolworthsLimitedengagesinretailoperations.

TescoPLC 20,873 TescoPLC,togetherwithitssubsidiaries,operatesasagroceryretailer.

WholeFoodsMarket,Inc. 8,952 WholeFoodsMarket,Inc.operatesnaturalandorganicfoodssupermarkets.

Beauty&PersonalCare

UnileverPLC 120,770 UnileverN.V.operatesinthefast-movingconsumergoodsmarketworldwide.

27

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

Subsector Company MarketCap(US$mn) CompanyDescription

L'OrealSA 101,671 L’OréalS.A.,throughitssubsidiaries,manufacturesandsellscosmeticproductsforwomenandmenworldwide.

TheEstéeLauderCompaniesInc.

31,687 TheEstéeLauderCompaniesInc.manufacturesandmarketsskincare,makeup,fragranceandhaircareproductsworldwide.

AmorepacificCorp. 20,804 AMOREPACIFICCorporationengagesinmanufacturing,marketingandtradingofcosmetics,personalcaregoods,foodandotherrelatedproducts.

ShiseidoCompany,Limited 10,312 ShiseidoCompany,Limitedproducesandsellscosmetics,cosmeticsaccessoriesandtoiletriesinJapanandinternationally.

Autos

ToyotaMotorCorporation 169,597 ToyotaMotorCorporationdesigns,manufactures,assemblesandsellspassengervehicles,minivansandcommercialvehicles,andrelatedpartsandaccessories.

VolkswagenAG 70,562 VolkswagenAktiengesellschaft,togetherwithitssubsidiaries,manufacturesandsellsautomobilesprimarilyinEurope,NorthAmerica,SouthAmericaandAsiaPacific.

BayerischeMotorenWerkeAktiengesellschaft

55,627 BayerischeMotorenWerkeAktiengesellschaft,togetherwithitssubsidiaries,develops,manufacturesandsellscarsandmotorcycles,sparepartsandaccessoriesworldwide.

HondaMotorCo.,Ltd. 53,724 HondaMotorCo.,Ltd.develops,manufacturesanddistributesmotorcycles,automobiles,powerproductsandotherproductsworldwide.

GeneralMotorsCompany 49,513 GeneralMotorsCompanydesigns,buildsandsellscars,crossovers,trucksandautomobilepartsworldwide.

Broadline

Wal-MartStoresInc. 211,393 Wal-MartStores,Inc.operatesretailstoresinvariousformatsworldwide.

CostcoWholesaleCorporation

65,119 CostcoWholesaleCorporation,togetherwithitssubsidiaries,operatesmembershipwarehouses.

TargetCorp. 39,223 TargetCorporationoperatesasageneralmerchandiseretailer.

CarrefourSA 19,689 CarrefourSAoperatesasamulti-local,multi-format,multi-channelretailerprimarilyinFrance,restofEurope,LatinAmericaandAsia.

Source:CapitalIQ/FungGlobalRetail&Technology

28

OCTOBER27,2016

DEBORAHWEINSWIG,MANAGINGDIRECTOR,FUNGGLOBALRETAIL&[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2016TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFungGlobalRetail&TechnologyNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comEsmePauAnalystIvyHuangResearchAssistantHONGKONG:8thFloor,LiFungTower888CheungShaWanRoad,KowloonHongKongTel:85223004406LONDON:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomTel:44(0)2076168988NEWYORK:1359Broadway,9thFloorNewYork,NY10018Tel:6468397017

FungGlobalRetailTech.com