Embed Size (px)

Citation preview

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 1/45

Renewable Energy for Rural Economic Development Project

Evaluation of Capital Market Constraints toFinancing Renewable Power Projects in Sri Lanka

Final Report

Mangala Boyagoda

31 Frances Road

Wellawatte, Colombo 6, Sri LankaTel: 4517302; 0722 452452

E-mail: [email protected]

Colombo, 15th May 2007

Prepared for the DFCC Bank on behalf of the Ministry of Finance, Government of Sri

Lanka in terms of Contract dated 27th November 2006

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 2/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

1

Table of ContentsPage No

Executive Summary………………………………………………………………… 03

1.0

Introduction………………………………………………………………… 04

2.0 Objectives and Scope of Consultancy……………………………………. 06

3.0 Methodology……………………………………………………………….. 07

4.0 Data Sources ………………………………………………………………. 07

5.0 Limitations………………………………………………………………….. 07

6.0 The Renewable Power Sector and Projects……………………………… 08

6.1 Overview of the ESD and RERED Projects……………………… 086.2 Project performance in Facilitating Finance …………………… 106.3 Status of the Electricity Sector…………………………….……… 116.4 Funding Needs…………………………………………………….. 12

7.0 The Domestic Financial Sector……………………………………………… 137.1 The Banking System………………………………………………… 13

7.1.1 Evolution of the Banking Industry…..…………………… 137.1.2 Present Status ………………………………………………. 147.1.3 Constraints in Project Lending……………………………. 17

7.1.4

Viewpoint of PCIs …………….…………………………… 227.1.5 Absorptive Capacity of PCIs……………………………… 247.1.6 State Banks as PCIs…………………………………………. 25

7.2 Capital Markets………………………………………………………. 267.2.1 Evolution ……………………………………………………. 267.2.2 Present Status ……………………………………………….. 277.2.3 Constraints in Debt Markets………………………………... 30

8.0 Addressing Capital Market Constraints……………………………………. 32

9.0 The Proposed Renewable Energy Bond…………………………………… 339.1 Salient Features of RESB…………………………………………… 339.2 Observations on RESB……………………………………………… 34

10.0 Recommendations………………………………………………………….. 3510.1 Establishment of REDA……………………………………………. 35

10.1.1 Objectives……………………………………………………. 36

10.2 Alternate Issuance Process [1]……………………………………. 3610.2.1 The Participants……………………………………………. 3810.2.2 Advantages………………………………………………… 38

10.2.3 Role of SPV………………………………………………… 3910.2.4 Role of PCIs……………………………………………….. 39

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 3/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

2

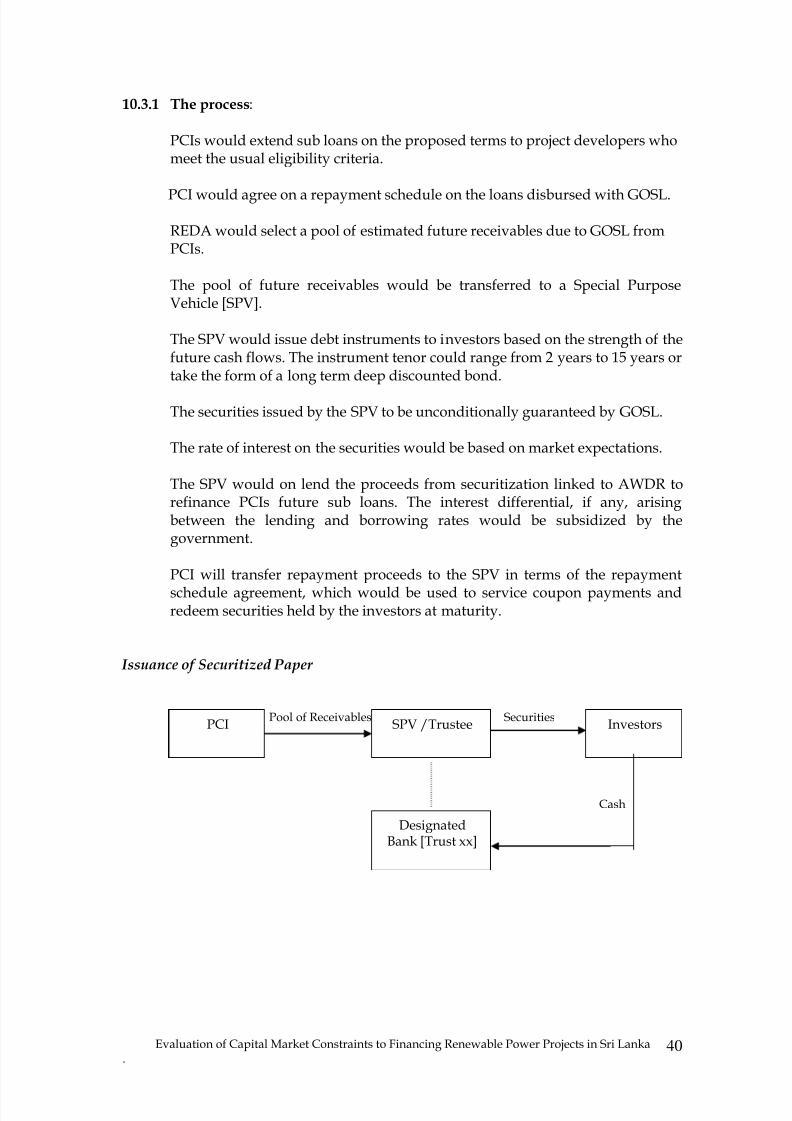

10.3 Alternate Issuance Process [2] …………………………………… 3910.3.1 The Process……………………………………………….. 4010.3.2 Advantages……………………………………………….. 41

10.4 Timing of the Bond Issue………………………………………… 41

10.5 Value Addition to Attract Investors……………………………. 4210.5.1 Eligibility for SRR Classification………………………… 4210.5.2 Eligibility for Liquid Assets………………………………… 42

10.6 Proposed Benchmark……………………………………………….. 42

10.7 Tax Exemptions……………………………………………………… 43

10.8 Support Required…………………………………………………. 4310.8.1 GOSL………………………………………………………. 4310.8.2 Central Bank………………………………………………. 43

10.9. Interim Support.………………………………………………….. 43

11.0 Annexures ……………………………………………………………….. Annexure 1.1 - Cash flows of On-grid Projects……………………… 44Annexure 1.2 - Cash flows of solar home projects………………….. 45

12.0 Acknowledgements……………………………………………………… 46

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 4/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

3

Executive Summary

The power sector in Sri Lanka has made notable progress over the past severaldecades, predominantly attributed to hydro electric power generation. In spite of thisfact, power sector strategies are yet to ensure that supply keep pace with the growing

demand. Among the several initiatives to foster energy efficiency and promoterenewable power development, is the World Bank initiative that ensured stablefunding to facilitate sector growth. The DFCC Bank, on behalf of the Government ofSri Lanka has now commissioned this study to identify medium term funding needs ofthe renewable power sector as well as the constraints to financing sector projects andto recommend appropriate financing mechanisms, to continue fostering the sector inthe absence of external support funds.

The salient issues that surfaced during the study include the several constraintsexperienced by the domestic banking sector that deter long term fixed interest rateproject lending; such constraints include the dearth of long term financial resources,

volatile financial market conditions, significant asset and liability mismatches, highintermediation costs and statutory impositions that affect the industry’s cost of funds.

The study also considered the viewpoint of selected Participating Credit Institutions,to ascertain both project related financing concerns and the possibility of extendingpower project funding out of own resources. In addition to the constraints common tothe banking industry set out above, these institutions operated within single borrowerand sector exposure limits that could restrict the development of the power sector.Recent measures to enhance minimum capital requirements of the banks wouldhowever serve to ease this pressure given that most participating credit institutionsbelong to the banking sector. The financial sector’s high cost of funds is also a

deterrent in suitably funding the renewable power sector. Primary attractions of theWorld Bank initiated credit schemes from the perspective of these instituitions, werethe low rate of interest and the ability to make use of the float of funds.

The answer to the dilemma is likely to manifest in several ways. Firstly, harnessingstrengthens of the state banks that have the greatest resources in the banking sector, inthe disbursement of any proposed credit line. Secondly, a dis-intermediation processthrough capital market instruments, although the capital market itself is not withoutits own limitations. The crowding out effect associated with the fact that thegovernment is the largest borrower in the debt market, the anomaly in the risk rewardstructure and the pricing of long term debt for example are factors that warrantattention if the renewable power sector is to be suitably positioned in the corporatedebt market. The proposal made by the Government of Sri Lanka to raise Rs 2,000million by way of a Renewable Energy Support Bond, by tapping the debt market is afurther viable option. The other alternative is to gain access to the capital market via aSpecial Purpose Vehicle fully backed by the government to mobilise long termfinancing assistance with private sector participation, through local capital markets.

Given the long term payback period of small scale power projects and the limitationsencountered by the banking industry and in equity markets, the proposed bondissuance, and the establishment of the Special Purpose Vehicle could be the idealfacilitator in accessing long term finance of a sustainable nature to help foster thepower industry.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 5/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

4

1.0 Introduction

Comprised of a total terrain of 65,610 square kilometers, Sri Lanka is home to a rapidlygrowing population that expanded from 16 million in 1990 to 19 million in 2005.Population density expressed in square meters, increased from 259 to 314 in that

period. Approximately 76% of the population lives in the rural areas where the mainoccupation is agriculture. In contrast, energy sector strategies have failed to keep pacewith the emergent population and increased industrialization, triggering a persistentcrisis in the sphere of electricity generation, transmission and distribution.

Sri Lanka’s energy sources consist primarily of biomass, hydro-electricity andpetroleum that contribute to 47%, 8% and 45% of total energy respectively. In thepower sector, the installed capacity for electricity generation from hydro, thermal andwind power presently stands at 2,407 MW, compared to 1,409 MW in 1999, which isnonetheless insufficient to meet the present demand from households as well ascommercial and industrial sectors. Less than 75% of households as yet have access to

electricity, while the demand for electrical power on the other hand is estimated to riseat an annual pace of 8% - 10%. Per capita consumption of electricity meanwhilereflected 348 kWh/ person in 2005.

A combination of factors has contributed to the emphasis in recent times forgenerating electricity through less conventional renewable sources. Electrification ofrural areas, for instance poses many challenges, foremost amongst which are the highcapital investment, operational costs and the difficulties associated with extendinggrid connected electricity lines to remote areas. In this context renewable sources ofenergy including solar power, small scale hydro power, wind power, biomass anddendro power, have emerged as an economical and sustainable alternative source to

promote medium term electricity generation to the rural populace, albeit in smallmeasure. In terms of the National Energy Policy and Strategies for Sri Lanka, whichwas introduced in 2006, as much as 80% of the total household electricity requirementis estimated to be generated through the extension of the national grid while off gridsources are being promoted to meet 10% of the requirement by the year 2015. Togetherwith economic benefits, renewable resources provide the advantage of achieving suchecological efficiencies as minimizing pollution and mitigating adverse climatic factorsthrough the provision of clean environment friendly energy.

The potential from renewable energy technologies in Sri Lanka have been estimated asset out in Figure 1.1

Figure 1.1

Energy Source Estimated Potential by year 2015

Solar Energy 11 MWWind Energy 50 MWMini Hydro Energy 300MW

Biomass Energy 90 MW

Source: DFCC Bank

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 6/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

5

In the light of the above facts, it is of the essence that Sri Lanka optimizes theconsiderable potential for energy generation from commercially viable off-gridrenewable sources so as to reduce dependence on imported petroleum and minimizethe resultant trade imbalances, in alleviating the prolonged energy problem.

The endeavour to implement renewable energy technologies have thus far beenfacilitated through dedicated credit support extended by external lending agencies.The World Bank and the Global Environment Facility [GEF] assisted Energy ServicesDelivery [ESD] Project introduced in 1997, at a time when more than half of thepopulation did not have access to electricity, provided an initial invaluable boost to thesector. Following the success of this project the Renewable Energy for Rural EconomicDevelopment [RERED] Project was launched in 2002 to provide electricity access torural households and small and medium enterprises through the deployment of off-grid renewable energy technologies as well as to promote private sector powergeneration from renewable energy sources. The credit support made available underboth projects played a pivotal role in nurturing the sector.

The challenges faced by Sri Lanka’s energy sector are evidenced in the composition ofthe total energy supply. The share of petroleum in the total energy supply hasexpanded significantly in recent times, from 32% in 1996 to almost 45% in 2005. Thetrend reflects the growing dependence on petroleum, in spite of power sector supportstrategies. It also highlights the difficulties presently encountered in power generationand the resultant slow growth of the sector.

In the quest to minimize petroleum dependence and accelerate the growth momentumof the sector it is indisputable that renewable energy technologies needs to be scaledup beyond the existing stage to one that facilitates the generation of greater

commercial capacity. For this to happen the sector needs continued and steadfastaccess to adequate funding at reasonable cost. Both the ESD Project and the REREDProject were concerned with addressing the issue of providing long term financingsupport for renewable energy investments. Such measures have served the purposeexcellently, with capacity installed often surpassing targets. However, given themagnitude of the task still ahead, the need to formulate a viable long term financingmechanism to augment electricity generation, transmission and distributionthroughout the country, remains a critical need.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 7/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

6

2.0 Objectives and Scope of Consultancy

The International Development Association [IDA], of the World Bank together withthe Global Environment Facility [GEF] has extended a line of credit and a grant fortechnical assistance respectively, to the Government of Sri Lanka [GOSL] to set up the

RERED project. The objectives of the RERED project include expanding commercialuse of energy generated from renewable sources and fostering rural economicdevelopment and thereby improve quality of rural life by providing access toelectricity. Under the project, the Ministry of Finance through a dedicated unit set upwithin the DFCC Bank has on lent proceeds of the credit line to eligible ParticipatingCredit Institutions [PCIs] by refinancing up to 80% of qualifying loans extended byPCIs to eligible sub borrowers.

With the RERED Project credit line now almost fully committed, the need to seekadditional sources of long term funds to foster the continued growth of the sector hasbeen identified. GOSL, with a view to addressing the issue, has requested the World

Bank for supplementary financing for the RERED Project through IDA credit in a sumof US$ 40 million. Meanwhile, DFCC Bank, on behalf of GOSL seeks to ascertainavenues to achieve the objective of raising long term financial resources on asustainable basis to facilitate sector growth, through domestic capital market sources.

The primary objective of the Consultancy assignment is to identify obstacles to raisinglong term debt capital within the domestic capital markets to finance renewable powerprojects. Supplementary objectives include evaluating options to facilitate mobilizinglong term capital, current exposure and absorptive capacity of present PCIs, assess theappetite of the two state banks in financing the sector and assess the sector growth andrelated funding requirements.

The scope of the present Consultancy is to, inter alia, review the development and thecurrent status of the domestic banking sector and capital markets, evaluateperformance of the ESD and RERED Projects as regards the provision of long termfinancing to the renewable energy sector, assess the medium term fundingrequirements of the sector and thereafter identify the constraints, risks and optionsassociated with long term financing of the renewable energy sector by means of boththe banking sector and capital market.

The final scope of the assignment is to comment on DFCC Bank’s alternate financingproposal and to recommend a suitable strategy for implementation of a viable longterm financing mechanism to sustain the growth of the renewable energy sector,particularly considering an absence of continued World Bank assistance.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 8/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

7

3.0 Methodology

The methodology adopted is primarily focused on the areas set out below.

3.1 An assessment of the two renewable energy projects implemented from

1997, in relation to its financing mechanism;

3.2 An assessment of the sector growth and funding needs based oninformation received;

3.3 The evolution of financial systems, both banking and capital markets,constraints and issues of the various members in the system includingthe Participating Credit Institutions and state banks;

3.4 Gap assessment between sector needs and financial system capabilities

3.5 Financing options to sustain sector growth

3.6 An assessment of the alternative proposal submitted by DFCC Bank

3.7 Recommendations

4.0 Data Sources

Information in this report has been compiled from publicly available documents; print

and electronic sources; in particular data published by the Central Bank of Sri Lanka,research material and other project data provided by the Administrative Unit of theDFCC Bank as well as from interviews with selected PCI and other relevantstakeholders.

5.0 Limitations

The contents of this report are subject to the following limitations;

5.1 The Consultant has in essence relied on the information supplied withregard to technical and specialized aspects of the ESD and REREDprojects and has not performed an independent review of these areas.

5.2 Information has been compiled from the most recent available data.

5.3 Statistics pertaining to few segments of the capital market is notreadily available from public sources and have not been captured in thereport.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 9/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

8

6.0 The Renewable Power Sector and Sector Projects

The renewable power sector captured in the study comprises primarily of small scalehydro, solar, wind and biomass sub-sectors. The two sector projects referredhereinafter are the ESD and RERED Projects.

6.1 Overview of the ESD and RERED Projects

The ESD and RERED projects, implemented with the assistance of the World Bank,facilitated the generation of both on-grid and off-grid renewable resource basedelectrification projects, as a means of addressing the severe constraints in power gridexpansion. Six Participating Credit Institutions [PCIs] namely DFCC Bank, NationalDevelopment Bank [NDB], Sampath Bank, Hatton National Bank [HNB], CommercialBank and Sarvodaya Economic Enterprises Development Services [SEEDS] wereappointed to assist in implementing the ESD project.

Following the successful implementation of the project, several other financialinstitutions, including commercial banks, leasing companies and micro financeinstitutions displayed a keen interest in participating in the implementation of thefollow-on RERED project. In addition to the 06 PCIs involved in the successful ESDproject 04 new PCIs were selected under the RERED project, namely Seylan Bank,Ceylinco Leasing Corporation, Lanka Orix Leasing Company and SanasaDevelopment Bank. More recently, Alliance Finance Co had been admitted as a PCI inthe program.

Proceeds of both credit lines were disbursed to PCIs at the Average Weighted DepositRate [AWDR]. PCIs assume the credit risk in extending sub loans to final borrowersoperating in different sub sectors and obtain refinance up to 80% of qualifying subloans. PCIs also have the flexibility of determining both tenor, subject to a maximumof 10 years, and the rate of interest to eligible sub-borrowers.

A total of US$ 30.1 million was committed to Sri Lanka under the ESD project, whileUS$ 83 million has been pledged in terms of the RERED project. The ESD projectfacilitated cumulative capacity installation of 350 kW by means of off-grid villagehydro schemes, whist an aggregate capacity of 31 MW was generated by way of mini

hydro schemes. Besides these, 20,953 solar home systems generating a capacity of984.6 kW were moreover installed under the project. A pilot wind farm supplying anannual capacity of 4.5 Gwh implemented under the ESD project, had furthermore beensuccessfully linked to the national grid.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 10/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

9

Figure 6.1

Projects implemented under ESD credit arrangements

0

10

20

30

40

MW

Target Installed

capacity

Mini hydro capacity

Source: Energy Sector Unit – World Bank

0

100

200

300

400

kw

Target Installed

Capacity

Village hydro schemes

Source: Energy Sector Unit

–World Bank Source: Energy Sector Unit

–World Bank

The on-going RERED project status data as at 30 th September 2006 reveal that thus faradditional capacities of 109 MW and 1 MW are being generated by way of gridconnected hydro and biomass schemes, while 927 kW and 35 kW are being installedthrough off grid community village hydro and biomass investments respectively.Moreover, non – PCIs have added 328 kW in hydro power through communityinvestments. A total of 73,604 solar systems have been installed as at the abovementioned date of review.

Figure 6.2

Status of RERED Funds of US$ 75 mn

72%

17%

11%

Disbursed

Committed

Unutilized

Source: DFCC Bank

0

5,000

10,000

15,000

20,000

25,000

No

Target Installed

Nos

Solar home systems

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 11/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

10

The two renewable energy development projects have enabled the electrification ofalmost 100,000 rural households. The project initiatives have furthermore provided afirm foundation for entrepreneur and technical capabilities as well as financingcapabilities.

6.2 Project Performance in Facilitating Finance

Achievement of project disbursement targetsThe long term financing arrangements extended under both ESD and RERED creditprograms, has been identified as a key attribute that enabled PCIs to meet projectfunding targets. The credit facility provided the end user access to liquidity for bothcapital investment and working capital on affordable terms. While some projectdevelopers required long term financing to meet high infrastructure costs coupledwith relatively long term cash flow generation, other developers, such as solar systemdevelopers needed access to affordable finance. Some developers sought readily

accessible working capital. The financing structure of the two projects successfullyaddressed the needs of the various end users. The availability of long term financingto PCIs was a pre-requisite to match the long pay back periods, in particular of villageand mini hydro projects.

Payback period and financing costsThe ESD and RERED credit programs had been structured to effectively support thesector in terms of pay back as well as the rate of interest. Loans to sub borrowersincorporated maturity periods up to 10 years, while the rate of interest under REREDwas pegged to the least volatile and least costly benchmark in the country, the AWDR.

PCIs that receive refinance at AWDR extended sub loans at variable margins overAWDR, re-priced semi annually. The terms associated with grid connected mini hydroprojects were typically AWDR plus 4% to 5% for maturities of 6 to 8 years, while theterms for off-grid projects were AWDR plus 4% to 6% for similar maturities. Solarhome systems were however typically linked to AWDR plus a minimum margin of10% for maturities of 2 to 4 years, primarily due to high administrative costs involved.The long term nature of the repayment program together with the reasonable interestrate structure, matched the long term requirements of mini hydro developers. Thefloating rate benchmark, AWDR, being the least volatile moreover served to mitigatethe fluctuations in interest costs.

The suitability of the above financing schemes is reflected in the satisfactory collectionratios reported by PCIs that have been in excess of 95%. It is however pertinent to notethat some PCIs that extended sub loans for solar projects up to 5 year tenors hadexperienced difficulties in recoveries in the latter years. The delays in collection wereattributed to additional maintenance expenses incurred by the end user, such asreplacement of batteries used in solar home systems. Some PCIs thereafter disbursedsub loans to end users for periods of 3 to 4 years, which strategy had reportedlyresulted in a marked improvement in their collection ratios.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 12/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

11

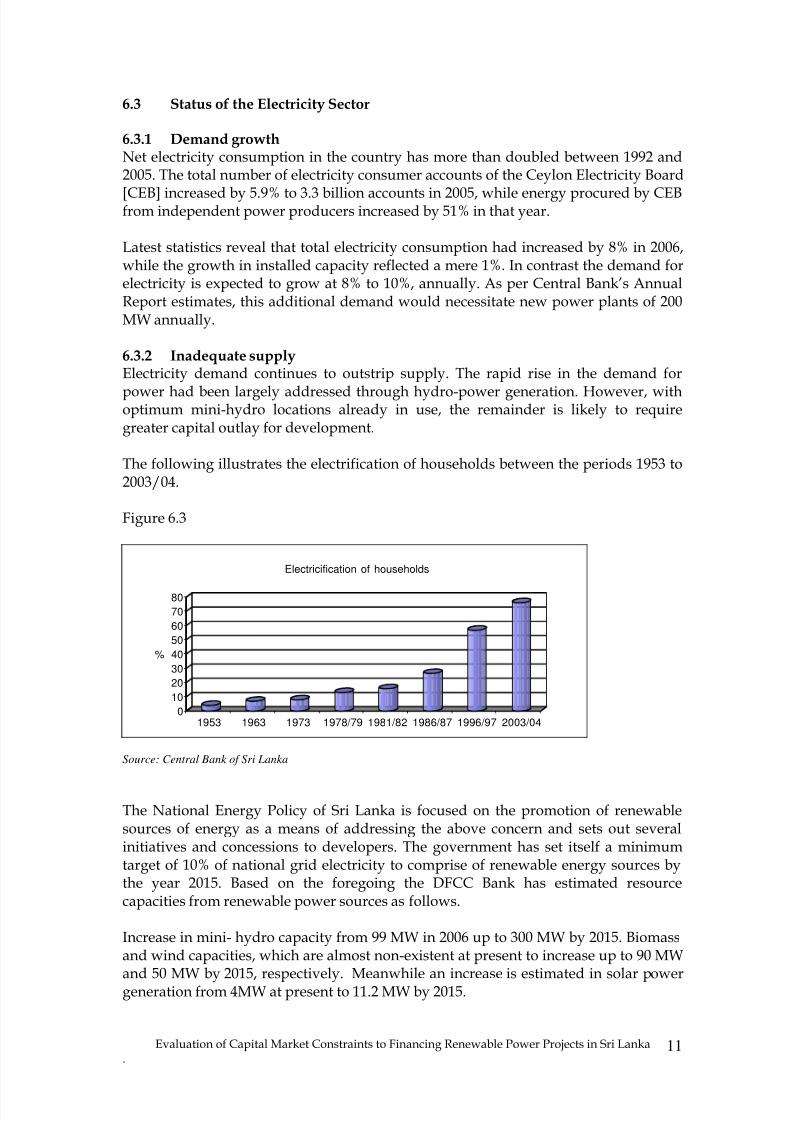

6.3 Status of the Electricity Sector

6.3.1 Demand growthNet electricity consumption in the country has more than doubled between 1992 and2005. The total number of electricity consumer accounts of the Ceylon Electricity Board

[CEB] increased by 5.9% to 3.3 billion accounts in 2005, while energy procured by CEBfrom independent power producers increased by 51% in that year.

Latest statistics reveal that total electricity consumption had increased by 8% in 2006,while the growth in installed capacity reflected a mere 1%. In contrast the demand forelectricity is expected to grow at 8% to 10%, annually. As per Central Bank’s AnnualReport estimates, this additional demand would necessitate new power plants of 200MW annually.

6.3.2 Inadequate supplyElectricity demand continues to outstrip supply. The rapid rise in the demand for

power had been largely addressed through hydro-power generation. However, withoptimum mini-hydro locations already in use, the remainder is likely to requiregreater capital outlay for development.

The following illustrates the electrification of households between the periods 1953 to2003/04.

Figure 6.3

0

10

20

30

40

50

60

70

80

%

1953 1963 1973 1978/79 1981/82 1986/87 1996/97 2003/04

Electricification of households

Source: Central Bank of Sri Lanka

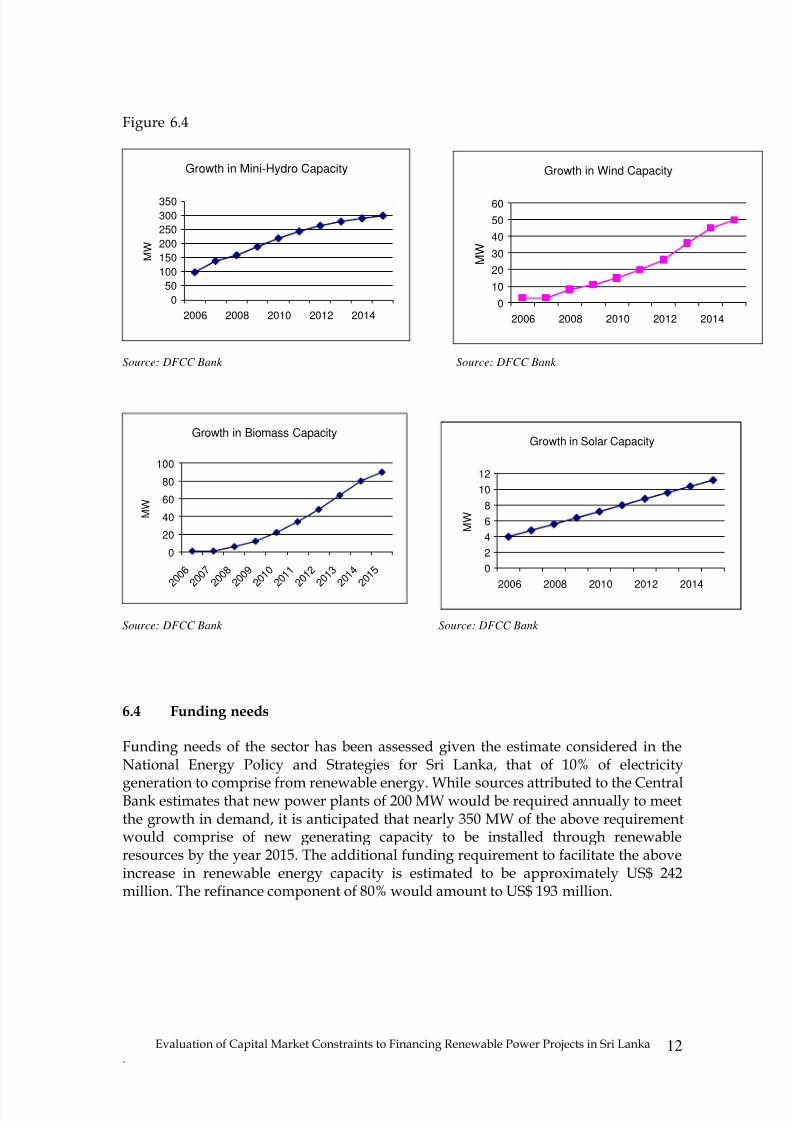

The National Energy Policy of Sri Lanka is focused on the promotion of renewablesources of energy as a means of addressing the above concern and sets out severalinitiatives and concessions to developers. The government has set itself a minimumtarget of 10% of national grid electricity to comprise of renewable energy sources bythe year 2015. Based on the foregoing the DFCC Bank has estimated resourcecapacities from renewable power sources as follows.

Increase in mini- hydro capacity from 99 MW in 2006 up to 300 MW by 2015. Biomassand wind capacities, which are almost non-existent at present to increase up to 90 MWand 50 MW by 2015, respectively. Meanwhile an increase is estimated in solar powergeneration from 4MW at present to 11.2 MW by 2015.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 13/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

12

Figure 6.4

Growth in Mini-Hydro Capacity

0

50

100

150

200

250

300

350

2006 2008 2010 2012 2014

M W

Source: DFCC Bank Source: DFCC Bank

Growth in Biomass Capacity

0

20

40

60

80

100

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

M W

Source: DFCC Bank Source: DFCC Bank

6.4 Funding needs

Funding needs of the sector has been assessed given the estimate considered in theNational Energy Policy and Strategies for Sri Lanka, that of 10% of electricity

generation to comprise from renewable energy. While sources attributed to the CentralBank estimates that new power plants of 200 MW would be required annually to meetthe growth in demand, it is anticipated that nearly 350 MW of the above requirementwould comprise of new generating capacity to be installed through renewableresources by the year 2015. The additional funding requirement to facilitate the aboveincrease in renewable energy capacity is estimated to be approximately US$ 242million. The refinance component of 80% would amount to US$ 193 million.

Growth in Solar Capacity

0

2

4

6

8

10

12

2006 2008 2010 2012 2014

M W

Growth in Wind Capacity

0

10

20

30

40

50

60

2006 2008 2010 2012 2014

M W

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 14/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

13

7.0 The Domestic Financial Sector

The ensuing discussion focuses on the financial systems and financing mechanismsrelative to funding the power sector. The domestic financial sector is comprised of thebanking system spearheaded by the Central Bank, financial institutions and capital

markets. The sector contributes almost 10% to the nation’s GDP. The analysis relates tothe development of the sector, the present status, market practices and impediments inmobilizing long term finance and makes special reference to the PCIs in the REREDproject and the two state owned banks.

7.1 The Banking System

7.1.1 Evolution

At the time the country gained independence in 1948, the banking industry was

dominated by 9 foreign banks that held over 60% of the banking sector assets. Two keypolicies changed the status quo of the industry. Firstly the nationalization of the Bankof Ceylon and the setting up of the state owned People’s Bank in 1961, whereupon thetwo banks then emerged to dominate the banking sector. The core objective of the statebanks at the time was to promote the rural economy, in particular providing finance tothe priority sectors of agriculture and industry. Secondly the economic reforms of 1977encouraged the presence of foreign banks once again in the country and paved theway for financial innovation in terms of products, services and technical capabilities.The entry of private commercial banks marked yet another milestone in banking. Thefirst private commercial bank, the Commercial Bank of Ceylon was incorporated in1969, followed by Hatton National Bank a year later.

The two development banks, DFCC Bank and the National Development Bank of SriLanka [NDB] were established in 1956 and 1999 as government owned developmentbanks to provide financial support for small and medium enterprises. The NationalSavings Bank was formed in 1972 to promote small scale savings. By 1998 there were26 commercial banks operating in the country comprising 18 foreign banks and 8 localbanks. The total assets of all financial institutions amounted to Rs 67,725 million in1980.

At present the domestic banking sector is comprised of 22 licensed commercial banks[11 domestic and 11 foreign banks], 14 licensed specialized banks, including 2development banks, 3 savings banks, 3 housing finance institutions and 6 regionaldevelopment banks. The total assets of financial institutions had expanded to Rs 3,144billion by 2005.

Changing focus: While the two Development Finance Institutions [DFIs] were established with theobjective of supporting long term capital formation in the country, with thesubsequent curtailment of the privilege of concessionary multilateral funding lines,one of these DFIs has now become a commercial bank, with a view to accessing public

deposits and short term lending rather than extending long-term project finance. It ispertinent to note that the development banking sector has moved towards a “universal

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 15/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

14

banking” concept rather than focus on the original objective of project lending. At thesame time commercial banks have set up “development banking units” to provideterm loans to projects in selected sectors.

The business scope of the banks have broadened to include consumer banking,

investment banking, fee based activities, venture capital, fund management, stockbroking and bank assurance products.

7.1.2 Present Status

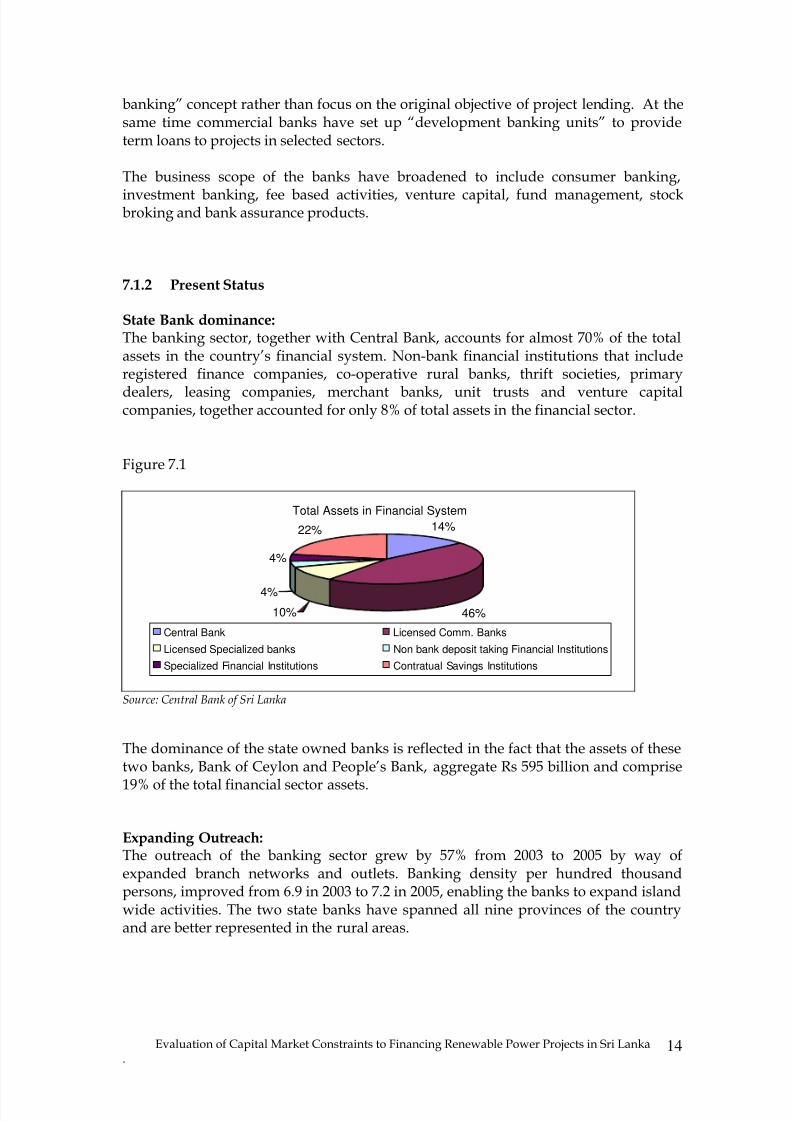

State Bank dominance:The banking sector, together with Central Bank, accounts for almost 70% of the totalassets in the country’s financial system. Non-bank financial institutions that includeregistered finance companies, co-operative rural banks, thrift societies, primary

dealers, leasing companies, merchant banks, unit trusts and venture capitalcompanies, together accounted for only 8% of total assets in the financial sector.

Figure 7.1

Total Assets in Financial System

14%

46%10%

4%

4%

22%

Central Bank Licensed Comm. Banks

Licensed Specialized banks Non bank deposit taking Financial Institutions

Specialized Financial Institutions Contratual Savings Institutions

Source: Central Bank of Sri Lanka

The dominance of the state owned banks is reflected in the fact that the assets of thesetwo banks, Bank of Ceylon and People’s Bank, aggregate Rs 595 billion and comprise

19% of the total financial sector assets.

Expanding Outreach:The outreach of the banking sector grew by 57% from 2003 to 2005 by way ofexpanded branch networks and outlets. Banking density per hundred thousandpersons, improved from 6.9 in 2003 to 7.2 in 2005, enabling the banks to expand islandwide activities. The two state banks have spanned all nine provinces of the countryand are better represented in the rural areas.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 16/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

15

Figure – 7.2

Bank Outreach

43%

2%14%

35%

6%Domestic Commercial Banks

Foreign Banks

Licensed Specialized Banks

State Banks

National Savings Bank

Source: Central Bank of Sri Lanka

Focus on short term lending:

The primary focus of the main banks remains on traditional banking services, namelydeposit mobilization, lending and investment activities. Overdrafts and trade financelending that are of short term nature aggregate Rs 161.2 billion and represent 13% ofthe total assets of Rs 1,242.2 billion of commercial banks. Loan advances of Rs 486.7billion of both short term and medium term maturities comprised 39% of total assets.Rs 436 billion relating to 27% of total assets are maintained in the form of liquid assets.The concentration towards short term lending is represented in the fact that 56% [Rs368 billion] of all advances of commercial banks [Rs 655 billion] are in the form of shortterm facilities, while medium and long term lending comprise 24% and 20% of totallending respectively. The major long term lending has been towards financing thehousing sector and represents 14% of all lending. The reasons for reluctance for long

term lending are discussed elsewhere in this report.

Figure 7.3

Maturity Profile of Commercial Banks Advances

56%24%

20%

Short term

Medium term

Long term

Source: Central Bank of Sri Lanka

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 17/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

16

Figure 7.4

Sector Composition of Lending

33%

5%4%

10%2%14%

17%

7%8% Trading

Financial

Agriculture

Industrial

Tourism

Housing

Consumption

Services

Others

Source: Central Bank of Sri Lanka

The following table illustrates the profile of long term assets with maturities greaterthan 5 years, relating to the major PCIs and the two state owned banks.

Figure 7.5

Interest Earning Assets Total AssetsMaturity

more than 5yearsRs mn

Total

Rs mn

% Maturitymore than 5

yearsRs mn

Total

Rs mn

%

DFCC Bank 2,800 41,145 6.8% 9,500 50,039 18.9%NDB Bank 1,836 34,676 5.3% 5,251 50,955 10.3%HNB 16,408 143,464 11.4% 22,205 166,012 13.4%Comm. Bank 9,481 160,018 5.9% 14,857 180,077 8.3%Seylan Bank 10,823 96,903 11.2% 14,688 113,608 12.9%Sampath Bank 4,170 72,348 5.8% 6,544 84,811 7.7%Bank of Ceylon 23,867 281,362 8.5% 29,106 319,504 9.1%People’s Bank 20,724 258,672 8.0% 24,383 275,262 8.9%Source: Annual Reports 2005 and 2005/06

Note: People’s Bank data is prior to deduction of provisions

Deposit base key funding source:The primary source of funding of the commercial banks is the deposit base of Rs 945.5billion that account for 76% of total assets of Rs 1242.2 billion. LCBs mobilized agreater proportion of resources in 2005 through rupee deposits, 63% and foreigncurrency deposits, 22%.

The Average Weighted Deposit Rate [AWDR] associated with borrowings declinedfrom 12.9% in 1990 to 7.6% in 2006. Interest rates on savings deposits, including long

term minor savings, ranged from 3% to 10.25% in 2005 while the average interest rate

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 18/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

17

was approximately 5%. The interest rates on 2 year fixed deposits ranged from 8.5% to11.5% p.a.

The greater proportion of the country’s deposit base, 41% is captive to the state ownedbanks.

Figure 7.6

Distribution of Deposit Base

41%

19%

33%

1% 4% 2%

State Banks

NSB

Commercial Banks

Other LSB

Finance Companies

Others

Source: Central Bank and Annual Reports 2005

7.1.3 Constraints in Project Lending

Lack of long term deposit base:The deposit base of commercial banks is primarily comprised of short term maturitiesof up to one year. The savings base of Rs 511 billion account for almost half of the totaldeposits in the system which is used as the core for medium term lending. The liabilitystructure of the banking sector is thus a barrier to support long term lending. In theabsence of dedicated long term credit lines the banking sector is consequentlyreluctant to finance such long term projects as infrastructure, housing and otherdevelopment activities essential for economic growth.

Figure 7.7

Composition of Interest Bearing Deposits

17%

24%

7%9%

24%

19% Savings - State Banks

Savings - Commercial Banks

Savings - Others

FDs - State Banks

FDs - Commercial Banks

FDs - Others

Source: Central Bank of Sri Lanka

Figure 7.7 illustrates that almost 50% of the total deposit base comprises of savings

deposits which are less than one year. More than 80% of total fixed deposits alsomature in less than one year.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 19/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

18

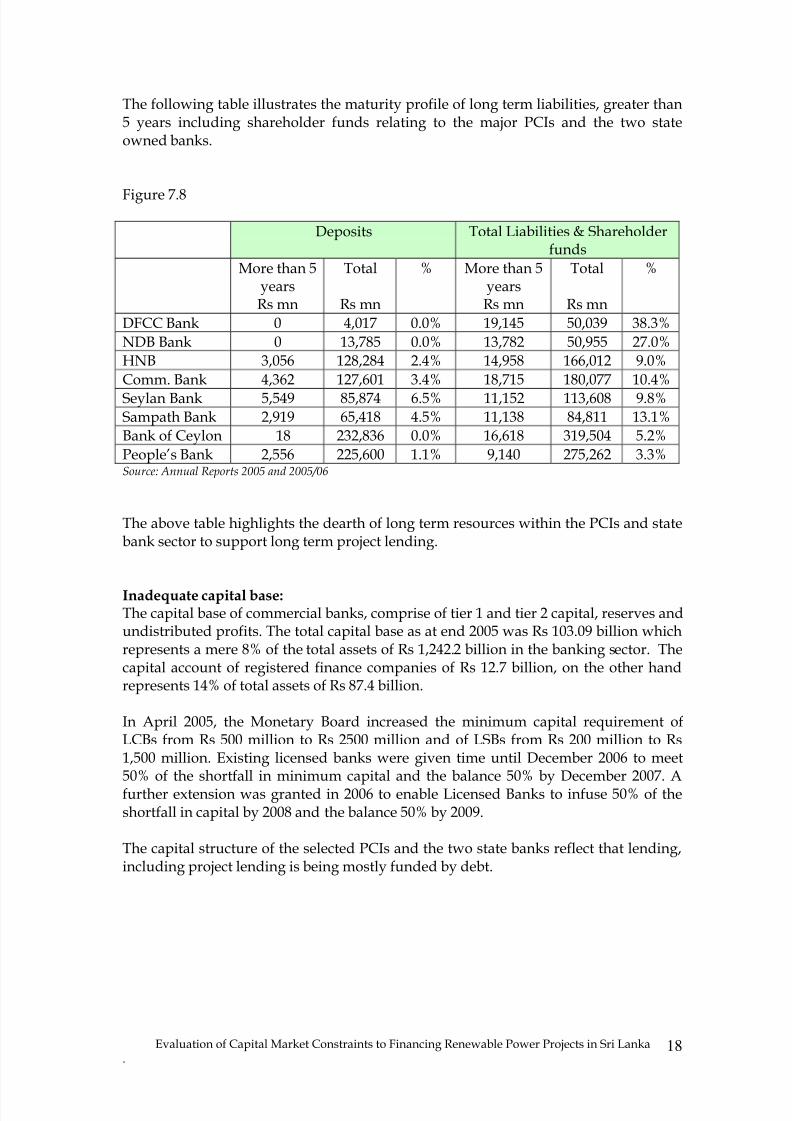

The following table illustrates the maturity profile of long term liabilities, greater than5 years including shareholder funds relating to the major PCIs and the two stateowned banks.

Figure 7.8

Deposits Total Liabilities & Shareholderfunds

More than 5yearsRs mn

Total

Rs mn

% More than 5yearsRs mn

Total

Rs mn

%

DFCC Bank 0 4,017 0.0% 19,145 50,039 38.3%NDB Bank 0 13,785 0.0% 13,782 50,955 27.0%HNB 3,056 128,284 2.4% 14,958 166,012 9.0%Comm. Bank 4,362 127,601 3.4% 18,715 180,077 10.4%

Seylan Bank 5,549 85,874 6.5% 11,152 113,608 9.8%Sampath Bank 2,919 65,418 4.5% 11,138 84,811 13.1%Bank of Ceylon 18 232,836 0.0% 16,618 319,504 5.2%People’s Bank 2,556 225,600 1.1% 9,140 275,262 3.3%Source: Annual Reports 2005 and 2005/06

The above table highlights the dearth of long term resources within the PCIs and statebank sector to support long term project lending.

Inadequate capital base:The capital base of commercial banks, comprise of tier 1 and tier 2 capital, reserves andundistributed profits. The total capital base as at end 2005 was Rs 103.09 billion whichrepresents a mere 8% of the total assets of Rs 1,242.2 billion in the banking sector. Thecapital account of registered finance companies of Rs 12.7 billion, on the other handrepresents 14% of total assets of Rs 87.4 billion.

In April 2005, the Monetary Board increased the minimum capital requirement ofLCBs from Rs 500 million to Rs 2500 million and of LSBs from Rs 200 million to Rs1,500 million. Existing licensed banks were given time until December 2006 to meet50% of the shortfall in minimum capital and the balance 50% by December 2007. Afurther extension was granted in 2006 to enable Licensed Banks to infuse 50% of theshortfall in capital by 2008 and the balance 50% by 2009.

The capital structure of the selected PCIs and the two state banks reflect that lending,including project lending is being mostly funded by debt.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 20/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

19

Figure 7.9

Shareholders FundsRs mn

Total AssetsRs mn

%

DFCC Bank 11,516 50,039 23.0%

NDB Bank 7,840 50,955 15.3%HNB 11,239 166,012 6.8%Comm. Bank 15,768 180,077 8.8%Seylan Bank 4,626 113,608 4.1%Sampath Bank 5,632 84,811 6.6%Bank of Ceylon 16,182 319,504 5.1%People’s Bank 4,181 275,262 1.5%Source: Annual Reports 2005 and 2005/06

Mismatch in assets and liabilities:

Asset and liability mismatches of a significant nature are inherent within most bankingand non-banking financial institutions. Figure 7.5 and figure 7.8 depict the mismatchthat exists in the longer term tenor maturities. The study revealed that most long termlending had been backed by short term borrowings that expose the PCIs to liquidityrisks. The risk is managed by retaining a higher interest spread that adversely affectslong term lending rates. Interest rate risk however is mitigated through floating ratelending. Fixed rate lending that is essential for small scale power projects is rare.

Pricing benchmarked to floating rates:Project and term lending is mostly pegged to a floating rate benchmark, with a smaller

fraction of lending extended on fixed rates. Banks have moreover begun to deviatefrom pegging the lending rate to Treasury Bills [TB} and instead adopt the AverageWeighted Prime Lending Rate [AWPLR] as the benchmark lending rate, in the absenceof an active inter-bank market. A risk premium ranging from 0.5% to 4% is usuallyincorporated in the pricing. The benchmark rate is re-priced periodically, mostlyquarterly.

Project and term fixed lending rates presently range from 13.5% to 17% p.a. TheAWPLR on the other hand declined from 18.5% in 1990 to 15.4% in 2006. The averageweighted lending rate applicable on the entire loan portfolio of commercial banksstood at 15.4% by end 2005.

The primary impact on small scale power project proponents arising from the above isas follows.

1. The base rate in computing the AWPLR is the TB. The AWPLR is severalpercentages higher than the TB, presently 2.5% over 3 month TB which resultsin higher cost of financing.

2. Periodic re-pricing results in greater exposure to interest rate fluctuations fromthe borrower’s perspective.

Financing renewable power projects in the above context from a proponentperspective becomes s a costly and risky affair.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 21/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

20

Debt financing is costlyThe recent successful offer made by a leading PCI, Commercial Bank, for the issue ofunsecured, subordinated debentures redeemable in 5 to 10 years and carrying fixedand floating rates of interest exemplifies the banking sector cost of funds. The issueentailed the following terms as depicted in Figure 7.10.

Figure 7.10Type of Interest Rate of Interest Tenor

Fixed Interest Rate 14%p.a. payable annually 10 yearsFixed Interest Rate 13.75% p.a. payable annually 7 yearsFixed Interest Rate 13.5% p.a. payable annually 5 yearsFloating Interest Rate 1 year gross Treasury Bill rate +1% p.a.

payable annually10 years

Floating Interest Rate 1 year gross Treasury Bill rate +1% p.a.payable annually

7 years

Floating Interest Rate 1 year gross Treasury Bill rate +1% p.a.

payable annually

5 years

The cost of debt finance in the present context is extremely high and has a directimpact on lending activities.

High reserve requirement:The Statutory Reserve Requirement [SRR] placed on the domestic banking sector isidentified as one of the highest in the region. The obligatory need to maintain a highreserve requirement of 10% of deposits in non-interest bearing cash reserves togetherwith a mandatory 20% in liquid assets increases the cost of long term borrowingespecially due to the upward yield curve. This necessitates a higher interest spread,thus inflating the pricing that affect prospective rural grid and off-grid developers.

High Bank Intermediation Cost:The intermediation cost of LCBs is still the highest in the region. The interest spreadretained by regional banks is below 3% compared to Sri Lanka’s 4.2% in 2004.Although LCB’s AWDR declined by 6.7% from 12.9% in 1990 to 6.2% in 2005, theAWPLR declined only by 6.3% during the period, from 18.5% in 1990 to 12.2 % in 2005.The high intermediation cost has been brought about consequent to assets and liabilitymismatches, high reserve requirement, extent of non-performing advances, the lack ofeffective risk management frameworks, high dependence on fund based activities andoperational inefficiencies. This further impedes the bank ability to provide low pricedlong term funds to the renewable power sector.

Figure 7.11

Commercial Banks Interest Spread

0

5

10

15

20

1990 2001 2002 2003 2004 2005 2006

%AWPLR

AWDR

Source: Central Bank of Sri Lanka

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 22/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

21

Sector exposure limitations of the banks:The twin exposure limits of the banks could restrict lending to a given borrower orindustry sector. The Central Bank prescribed Single Borrower Limit [SBL] thatpresently stand at 30% of capital could limit lending to power project developers.

The sector exposure limit maintained as a measure of prudence on the other handwould restrict advances to any given sector.

Measures taken by Central Bank to augment the capital base of the banks byincreasing the minimum capital requirement as stated in Section 7.1.3 page 18, mayserve to ease the present limitation. In spite of this fact, state banks may continue tohave an edge over other commercial banks in terms of exposure limits. It is alsopertinent to note that the SBL could be broadened in the event banks engaged insyndicated lending to approved prioritized sectors.

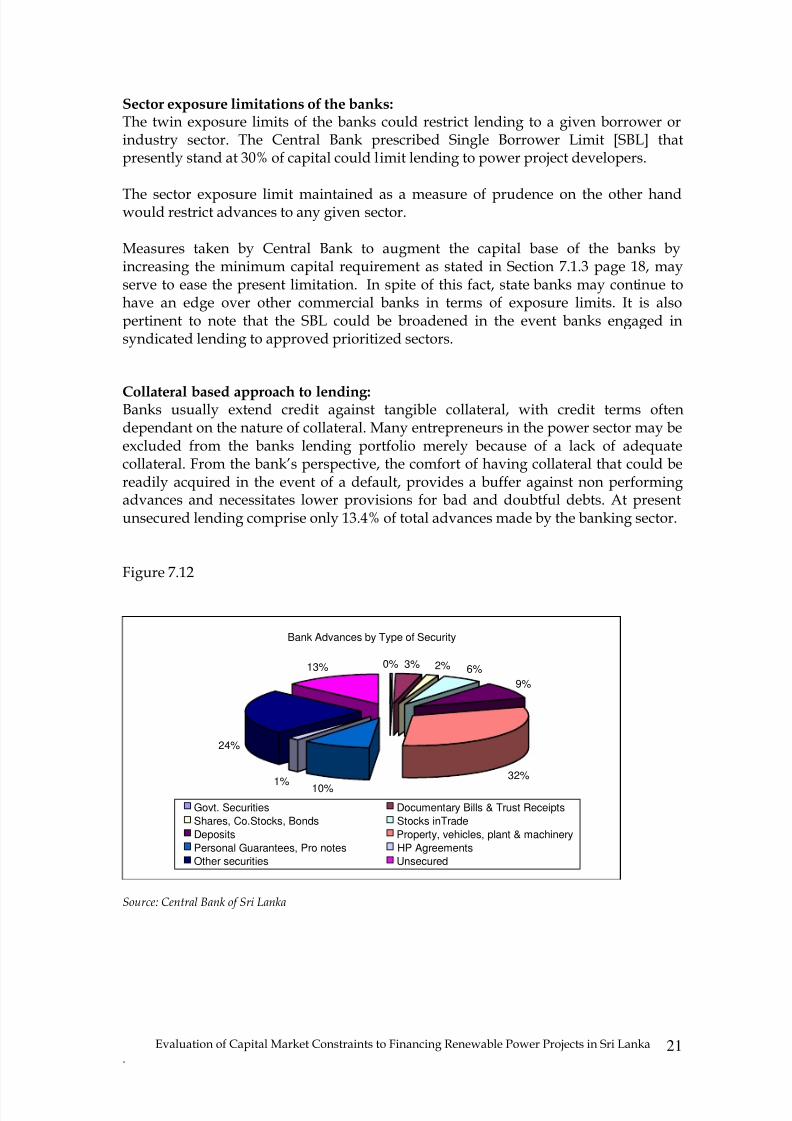

Collateral based approach to lending:Banks usually extend credit against tangible collateral, with credit terms oftendependant on the nature of collateral. Many entrepreneurs in the power sector may beexcluded from the banks lending portfolio merely because of a lack of adequatecollateral. From the bank’s perspective, the comfort of having collateral that could bereadily acquired in the event of a default, provides a buffer against non performingadvances and necessitates lower provisions for bad and doubtful debts. At presentunsecured lending comprise only 13.4% of total advances made by the banking sector.

Figure 7.12

Bank Advances by Type of Security

0% 3% 2%

9%

32%

10%1%

24%

13% 6%

Govt. Securities Documentary Bills & Trust Receipts

Shares, Co.Stocks, Bonds Stocks inTrade

Deposits Property, vehicles, plant & machinery

Personal Guarantees, Pro notes HP AgreementsOther securities Unsecured

Source: Central Bank of Sri Lanka

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 23/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

22

7.1.4 Viewpoint of PCIs

The Consultant conducted interviews with selected PCIs and other stakeholders inorder to make an objective assessment of their commitment to promote renewableenergy projects as well as to ascertain specific concerns in funding the sector. The

following salient observations reflect the broad consensus among the stakeholders.

1. Project lending under both ESD and RERED schemes to promote ruralelectrification had been mostly committed for mini hydro projects. Two PCIshad however focused on financing solar home systems. 70%of disbursementsunder the ESD project were for mini hydro projects, followed by solar projectsthat received 28% of the funds. Meanwhile 67% of the RERED credit line hadbeen deployed to fund mini hydro projects and 32% for solar projects.

2. Most PCIs had engaged in a syndication process to synergize technical skillsand minimize risk exposure. Technical expertise was available in house with

some PCIs, while some others had obtained outside assistance.

3. The average loan tenor ranged from 6 to 8 years, besides a grace period of 1 to2 years. The rate of interest on an average amounted to AWPLR + 5% for minihydro projects, while solar projects received lending at a flat rate ranging from10%p.a. to 12%p.a.

4. One PCI reported exposure to this sector of 5% of their total asset book whilesome PCIs are considering the imposition of a sector exposure limit.

5. The lack of power generation at optimal capacity was a concern reported by

PCIs. Power generated reflected only 35% to 40% of expected capacity, thereasons for which are presently being investigated.

6. Since most of the optimum sites for mini-hydro projects are already in use, thecost of developing less favourable sites could be considerably higher resultingin the escalation of project cost estimates.

7. A time lag of 2 to 3 years is reported in the legal process relating to theacquisition of land, while project cost estimates could escalate in the interim.

8. The possibility of a revision in the Power Purchase Agreement for mini hydro

projects with the Ceylon Electricity Board [CEB] and concerns of introducing atiered structure in the tariff setting for grid connected projects. PCIs alsoexpressed concern on the likelihood of the requirement of a guarantee fromthe PCI to CEB. The CEB has meanwhile indicated the possibility oftransferring grid connection costs to developers, in view of the high costincurred in absorbing power from remotely located projects into the grid. Anagreement has not been reached in this regard, as yet.

9. Lack of proper planning on the part of the CEB in supplying electricity accessto under privileged areas. The possibility of connection to the national grid hasat times prompted borrowers to defer solar system implementation plans. Thisis primarily due to end user preference to obtain grid connectivity rather thana solar powered energy option.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 24/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

23

10. Recovery issues were experienced in some instances. One PCI that focused onsolar home systems had disbursed almost 60% of that portfolio to the Northand East provinces, the recovery of which is doubtful under presentconditions. Some PCIs had incurred losses associated with the tsunami. Whilethe overall recovery rate is very satisfactory, approximately 95%, such

incidences have prompted PCIs to consider requesting equity contributions upto 40% for future lending.

11. Financing of renewable power projects would be costlier, due to depreciationof the rupee on the one hand and increasing cost of raw material such as solarcells, in the international market, on the other hand.

12. A lack of enthusiasm was witnessed in assisting wind power projects whichremain in an experimental stage, as well as biomass projects due to possibleconstraints in raw material supply.

13. While PCIs remain committed to promoting the sector, doubts were expressedin deploying their own financial resources to fund renewable power projects,in the absence of RERED type assistance due to the inherent high asset liabilitymismatches that could be compounded by engaging in long term fixed ratelending. Given PCIs cost profiles any lending out of own resources would bepegged to the AWPLR plus a probable margin of 5%. This would expose theproducer to a severe interest rate risk.

Figure 7.13

AWPLR

0

5

10

15

20

1990 2001 2002 2003 2004 2005 2006

%

Source: Central Bank of Sri Lanka

The study further revealed that PCIs who receive long term refinancing benefit fromthe positive cash flows associated with the overall project repayment structure. PCIsreceive refinance repayable in 20 semi annual installments from the date of firstdisbursement after a grace period of 5 years. Borrowers on average receive 6 to 8 yearfunding excluding a grace period of 1 to 2 years. The agreement with PCIs stipulatesthat the interim cash surplus should either be made available for financing sectorprojects or repaid to the government after 6 months. However, such interim surplusfunds are often re-lent to regular customers on market terms and not necessarily to the

same sector. It was observed that a primary attraction of the credit scheme has beenPCIs ability to take advantage of the interim float.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 25/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

24

7.1.5 Absorptive Capacity of PCIs

Discussions with present PCIs revealed that they remain committed to promoting therenewable energy sector. The collection performance in respect of sub loans extendedunder the scheme has been very satisfactory, reportedly over 95%. Two thirds of sub

loans extended under the ESD project has already been repaid to PCIs by subborrowers. Thus PCIs present exposure is mainly in relation to disbursementspertaining to the RERED credit line. As discussed in Section 7.1.4, one PCIs exposureto the sector is presently 5% of the total assets, while some PCIs are at presentconsidering placing limits for financing the sector.

In spite of the above, PCIs display a willingness to continue their role in promoting thesector. Their capacity for future projects would be essentially dependant on the meritsof individual power projects, specifying a possible enhancement in promoter’s equityinvestment and their internal lending criteria.

Possibility also exists to broaden the range of PCIs, as witnessed in the inclusion of anew PCI, Alliance Finance Company in 2007 and by implementing measures asdiscussed in Section 7.16 below which would facilitate greater penetration, especiallyin the rural areas.

Based on available data it is estimated that PCI would have the capacity to absorb thefollowing.

Rs bn

2008 - 2.452009 - 3.052010 - 3.452011 - 3.352012 - 3.402013 - 3.232014 - 3.032015 - 2.19

Refinance up to 80% of the above would be available for PCIs.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 26/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

25

7.1.6 State Banks as PCIs

The two state owned banks have considerable capacity to engage in RERED type

project lending, given that they possess the greatest resources in the local financialsystem.

1. The total asset base as well as the deposit base of the two banks are significant;almost double that of other banks and financial institutions.

2. The sector exposure and single borrower exposure limits of the state banks arecomparatively higher than their peers.

3. Both banks possess a comparatively higher number of branch locations as well

as a wider spread branch network spanning both urban and rural provinces.The two banks together account for 35% of all bank branches in the island.

4. Both banks are considerably experienced in small scale project lending.

The reasons stated above spotlight the state banks as an attractive vehicle to speedilyreach the rural populace and could be considered as potential PCIs in thedisbursement of any future credit line for renewable sector projects.

Both banks however lack the technical expertise in dealing with specialized projects of

this nature. Hiring outside talent is one option that could address this problem.Entering into a syndication process with more experienced PCIs is another alternativeavailable to the state banks.

However, given limitations associated with the eligibility criteria for PCIs, Bank ofCeylon could be initially evaluated for admittance as a PCI for the program. The Bankis rated AA (lka) by Fitch Ratings Lanka Limited, with recent results reflectingstrengthened fundamentals.

On the strength of a major re-structuring drive, People’s Bank too, has displayed amarked improvement in performance, in terms of profitability, growth in deposits,

growth in capital funds, and by achieving a significant reduction in non-performingadvances. With consistent profit growth over the past 6 years and improved financialratios, People’s Bank presently displays the potential to sufficiently recover andqualify as a prospective PCI at a subsequent stage.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 27/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

26

7.2 Capital Markets

Besides the banking sector, local capital markets have evolved to some extent to

facilitate the formation of capital investments.

7.2.1 Evolution

Sri Lanka’s capital market consists of the equities and debt markets. The debt marketcomprises government securities and listed and unlisted corporate debt markets.While the equity and government securities markets have evolved to some extent, thecorporate debt market is yet in an emergent state in comparison to such regionalplayers as India, Korea, Malaysia and Japan.

At the time of gaining independence Sri Lanka’s capital markets were relativelyunderdeveloped, with a limited number of market participants and few financialinstruments. Money market activities primarily consisted of trading in bills ofexchange. Treasury bills [TBills] were introduced in 1950s and were of moderatevalues. The TBill yield at the beginning of 1960 was 2% p.a. compared to a Bank rate of3%. Trading in TBills in the secondary market commenced in 1981, while repurchaseand reverse repurchase windows were introduced in the mid nineties with theobjective of developing a secondary market for government securities.

Until 1997 the government made use of two instruments, TBills and Rupee Loans, toraise funds; the latter represented the administrative borrowings of the government

out of captive sources. The introduction of a Treasury bonds [TBonds] market forgovernment securities in 1997 however permitted market forces to determine theyield. The TBond market initially for maturities of 2 to 3 years has since matured tosome extent to accommodate the issue of a 20 year bond. Meanwhile the AccreditedPrimary Dealer system was also replaced with a System of Primary Dealers in the midnineties.

A short term corporate securities market emerged with the introduction of commercialpaper [CP] in 1993. The outstanding value of CPs in the late nineties wasapproximately Rs 2,000 to Rs 3,000 million and incorporated yields of 4% to 6% overTB yields compared to present rates of 2% to 4% over net TB yields. Listed corporate

bonds [debentures] reflected Rs 151 million in 1997 and stands at Rs 11.9 billion in2005. A unit trust industry meanwhile emerged in 1991. The industry of 6 unit trustsoperating in 1997 had mobilized Rs 2,700 million from 25,000 unit holders. Theindustry remains passive comprising 5 unit trusts that had mobilized Rs 5.4 billionfrom 23,500 unit holders by 2005.

The Colombo Stock Exchange [CSE] was meanwhile set up in 1984 and reflectedmarginal trades. The fully automated Central Depository System for share transactionsand the Securities and Exchange Commission {SEC} were established 7 years later.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 28/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

27

7.2.2 Present Status

Robust equity market but few listings:As at end 2005, there were just 239 entities listed on the Colombo Stock Exchange[CSE] with a market capitalization of Rs 584 billion. This reflects 21% of the national

GDP. The value of shares traded in 2005 was Rs 114.5 billion, compared to 13.9 billionin 2001. The key index the ASPI appreciated from 621 to 1,922 between the years 2001to 2005. The share price index relating to the power and energy sector however reflectsonly 125 as at 2005 [base 1985 – 100].

Figure 7.14

Growth of Share Market

0

20000

40000

60000

80000100000

120000

140000

1990 2001 2002 2003 2004 2005

R s m n

0

500

1000

1500

2000

2500

Value ofShares traded

ASPI [1985 -100]

Source: Central Bank of Sri Lanka

Government securities dominate debt market:Sri Lanka has an active government securities market consisting of Treasury Bills,Treasury Bonds, Development Bonds, loans and more recently, Index Linked Bonds.Bills and Bonds are traded in the secondary market. Treasury Bills [TB] outstanding asat end 2005 amounted to Rs 234 billion while the rates on 364 days TBs fluctuated from13.74% in 2001 to 10.37% in 2005. Of the total domestic debt of Rs 1,265 billionoutstanding as at end 2005, Rs 234 billion [19%] represented TBs, while Rs 751 billion[59%] and Rs 140 billion [11%] represented Treasury Bonds and Rupee Loansrespectively.

Figure 7.15

Composition of Government DomesticDebt

19%

59%

11%

11%

Treasury Bills Treasury Bonds

Rupee Loans Others

Source: Central Bank of Sri Lanka Source: Central Bank of Sri Lanka

Ownership of Government Domestic Debt

24%

13%

34%

21%

8%

Banking Sector Savings Institutions

Provident & Pension Funds Private Sector

Others

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 29/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

28

Ownership of Treasury Bills

33%

17%31%

8%11%

Banks Savings

Private Sector Insurance & Finance Cos

Others

Source: Central Bank of Sri Lanka Source: Central Bank of Sri Lanka

The above graphs illustrate the paradigm shift in the ownership of TBills, from banks

and Central Bank towards the private sector. Rupee Loans are held by institutionssuch as the Employees’ Provident Fund [EPF] which is managed by the Central Bank,the Employees’ Trust Fund [ETF] and insurance companies.

Transactions in TBills in secondary market increased from Rs 390 billion in 2004 to Rs443 billion in 2005 due to attractive yields. Moreover, the yields associated withgovernment securities are net of the withholding tax element of 10% presentlyimposed on interest income, resulting in a higher gross yield to the investor.

Under developed listed corporate debt market:

The total market capitalization of listed corporate debt of Rs. 11,914 million as atDecember 2005 is considerably insignificant when compared to the Rs. 584 billion ofequity listed on the CSE.

Figure 7.16

Type of Entity No of

Issuers

No of

Listings

Market Capitalisation

SL Rs. Million

Listed commercial banks 4 19 9,655

Listed non-bank finance institutions 3 13 249

Listed corporate entities 2 6 607

Unlisted commercial banks 0 0 0

Unlisted non-bank finance institution 1 2 250

Unlisted corporate entities 2 6 1,153

Total 12 46 11,914

Source: Colombo Stock Exchange

A total of 12 entities, comprising primarily of commercial banks and listed non-bankfinance institutions, had been responsible for the issue of the above mentioned listedcorporate debt. Such debt has been primarily in the form of debentures and has

incorporated varying maturity tenors at the time of issue, comprising both fixed

Ownership of Treasury Bonds

7%14%

27%

46%

6%

Banks Savings Private Sector EPF Others

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 30/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

29

coupon interest issuances and floating coupon interest issuances. Most corporatedebentures were issued for 5-year tenors that indicate the nature of investor appetite.The following table depicts the infrequent nature of secondary market trading in listedcorporate debt.

Figure 7.17

Listed

Corporate Debt

Equity

Value traded (SL Rs. million) 199 59,052

Volume traded (million) 2 2,752

Trades (No.) 1,362 645,083

Source: Colombo Stock Exchange

Informal unlisted corporate debt market:Market instruments include commercial paper [CP], debentures and medium termpromissory notes. Statistics pertaining to unlisted corporate debt is not readilyavailable, other than CPs and debentures issued with the assistance of the bankingsector. A total of Rs 2.8 billion in bank backed CP was outstanding as at 2005consisting mainly of less than 3 month tenor maturities. CPs to the tune of Rs 10.9billion at an interest rate range of 8.9% to 14.25% had been issued in 2005 comparedwith Rs 14.5 billion issued in 2004 at interest rates ranging from 7.75% to 14%.

Pricing of unlisted debt is linked to the yield on government securities.

An emerging asset backed securities market:At present an Asset Backed Securities [ABS] market has emerged with issuerscomprising mainly of leasing companies, engaging in the private placement ofissuances. Investors in ABS are mainly banks, institutional investors and high net-worth individuals. The role of the Trustee in the ABS market is presently centered ontwo custodians. The SEC has at present initiated the enactment of a Securitisation Actto facilitate the development of this market. While statistics pertaining to the ABSmarket outstanding were not readily available at this juncture, market sourcesestimates the figure to be Rs 15 billion. Pricing of ABS is also linked to governmentsecurities.

The power and energy sector has not engaged in securitization.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 31/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

30

7.2.3 Constraints in the Debt Market

The scope of the study has excluded the option of equity financing as a viable meansof financing power projects, at this juncture. This is due to the many hindrances inlisting power project entities, such as the modest size of the company and the lack of a

proven financial track record. As such the study henceforth focuses on the debtmarket for financing sector projects.

Anomaly in the risk reward structure:Listed debt is generally priced in relation to the yield on gilt-edged instruments. Therisk premium attached may vary from 1% to 3% thus increasing the pricing of listeddebt. Interest on fixed rate debt issues range between 14% and 17% depending on theinvestor risk appetite. A fundamental issue that arises is that the yield to an investor ingilt-edged instruments is considerably higher than that offered by the banking sector,which is the AWDR. This affects the cost of accessing the capital market. This is

illustrated in the following table.

Figure 7.18

Fiscal policy direction:A greater part of the composition of government debt is domestic debt that consists56% of total government debt. The fiscal policy of tapping the domestic debt market asa means of funding the high government budget deficit restricts capital market

activities. Considering that the government is the largest borrower in the capitalmarket, this leads to a crowding out effect with the corporate sector competing forlimited funds.

Monetary policy:Sustaining a consistent interest rate policy is often challenged by the constant pressureon inflation and exchange rates. The lack of a clear direction in interest rates hamperscapital market activities, especially the pricing of debt. A case in point is the recentwithdrawal of the reverse repurchase window that had earlier been introduced with aview to stabilizing the short term money market. The withdrawal has resulted inuncertainty among the market participants.

0%

5%

10%

15%

20%

25%

Jan-

00

Jul-

00

Jan-

01

Jul-

01

Jan-

02

Jul-

02

Jan-

03

Jul-

03

Jan-

04

Jul-

04

Jan-

05

Jul-

05

Jan-

06

Jul-

06

AWDR 3M T Bill Prime Lending Rate

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 32/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

31

Lack of instruments:The lack of diversity in capital market instruments as well as limited investmentopportunities has also restricted primary and secondary capital market activities.Investors could be reluctant to participate in capital market activities due to the lack ofan exit mechanism and prefer adopting a buy and hold strategy.

Absence of a credible long-term yield curveAt present an active secondary market yield curve for government securities has notbeen observed beyond 3 years. Hence, the establishment of a credible long-term yieldcurve is difficult. In the absence of such a realistic long-term benchmark yield curvethe pricing of long term debt for power projects becomes a challenge.

Captive sources:

Large provident funds and pension funds such as the EPF and ETF are primarilycaptive to the government. Although the funds’ portfolio sizes are significant, theirparticipation in capital markets is inadequate.

Lack of awareness and reachMost savers and investors lack the knowledge and opportunity to derive benefits fromcapital market investments. Even though savers receive a negative return on banksaving programs, savings still remains the most popular vehicle for investmentprimarily due to the lack of knowledge and the lack of reach. This demonstrates thatdespite the shift witnessed in the ownership of government securities, savings still

comprise the major part of banks’ funding base. Meanwhile, primary dealers who areexpected to broad base investment in government securities are mainly confined toColombo.

The issues stated above are some of the constraints that PCIs and other financiers ofrenewable power projects would encounter when looking to finance long termactivities via the debt market.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 33/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

32

8.0 Addressing Capital Market Constraints

The report thus far focused on a discussion of the macro economic environment withspecific relevance to the corporate debt market and provided an overview of the

domestic debt market. It also focused on factors that currently inhibit the developmentof Sri Lanka’s corporate securities market.

The salient issues that constantly surface during the course of the study include thelack of breadth, the lack of depth, the lack of investment knowledge, the lack of marketknowledge, the risk-reward anomaly, the absence of an active secondary market andthe absence of a credible long-term yield curve.

To achieve the objective of developing the listed corporate debt market in Sri Lanka,the issues discussed in the report warrant immediate attention. Some of the keymeasures include fiscal discipline, pension reforms and the rectification of the risk

reward anomaly, creation of retail market awareness with regard to corporate debt,the design and implementation of a comprehensive training program to cover allstakeholders and the design and implementation of a strategy to revive the unit trustindustry.

Whilst the scope of this study does not entail recommending strategy to deal withcapital market constraints, the fore-going paragraphs would provide a general insightinto possible remedies to alleviate market impediments, given the consideration ofdepending on capital markets to mobilize funds for future needs of the renewableenergy sector.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 34/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

33

9.0 The Proposed Renewable Energy Support Bond

As a means of sustaining the growth of both on-grid and off-grid renewable resourcebased power projects in the context of the imminent completion of RERED, the

government has requested the World Bank to consider a supplementary financingpackage of US$ 40 million and is at present evaluating the possibility of issuing a Rs2,000 million Renewable Energy Support Bond [RESB].

Electricity is a priority sector that has thus far been subsidized by the government andbacked by donor support. The government has not only extended concessionaryfinance to the sector, but has also assumed the credit risk of PCIs as well as theexchange risk associated with foreign financial assistance for the purpose ofdeveloping the sector.

Financing of long term projects through the local debt market would only happen at a

price, given the fairly under developed state of the market. Thus the success of smallscale power projects would be dependant on the financial support that is madeavailable. The proposed RESB has taken into account this need for a further financialsubsidy for the sector.

9.1 Salient features of the RESB proposal:

1. The issuer would be the Treasury.2. The bond would be of long tenor, 10 to 15 years and would incorporate a

variable coupon linked to TBill, TBond, AWDR or AWPLR together with apremium thereon.

3. In the alternative, the bond may also be issued at a discount to face value,based on market expectations.

4. The bond may be offered on a tender as for TBills, as a debt listed on theColombo Stock Exchange or take the form of a private placement.

5. The proceeds from the bond issuance would be made available for partialrefinance of project loans extended by PCIs. The rate of interest considered forrefinance to PCIs is the AWDR.

6. PCIs would obtain refinance directly from CBSL and service obligations toCBSL on due dates.

7. CBSL would create a sinking fund from the debt service payments from PCIs tosettle coupon payments and to redeem the bond at maturity.

8. The fund would be invested by CBSL in an interest earning instrument until itsliquidation. The interest would be credited to the fund.

9. Any shortfall arising between the liquidated sinking fund and the redemptiondues, would be funded for instance through a Treasury subsidy.

8/6/2019 Dfccfinalr Report 1 1

http://slidepdf.com/reader/full/dfccfinalr-report-1-1 35/45

Evaluation of Capital Market Constraints to Financing Renewable Power Projects in Sri Lanka .

34

9.2 Observations on the proposed RESB:

1. The RESB structure would provide a sound platform for financing the powersector in the medium term and has been structured to meet most expectations

of all participants.

2. The RESB should ideally be structured so as to attract the larger investor basecomprising commercial banks, insurances companies, provident funds andhigh net worth individuals.

3. From an investor’ perspective a higher premium may be demanded in respectof a deep discounted bond, in the absence of a credible long term yield curveand the lack of periodic cash flows over the term of the investment. Hence thebond should ideally be issued as an interest bearing bond with fixed ratecoupons or floating rate coupons.

4. CBSL’s resource capacity and expertise to manage an active sinking fund needsto be ascertained, on the premise that active fund management does not form apart of CBSL’s core objectives.

5. While the RESB would provide a conduit to financing the sector, it could alsobe used as an ideal mechanism to mitigating some of the constraintsencountered by the banking system in mobilizing funds from the domesticcapital market. This aspect of the issue would be discussed in the ensuing

recommendations.

6. There is a need to establish an agency that would undertake on a dedicatedbasis the structuring and administration of the RESB process. Some of theunderlying factors are the resource constraints presently experienced in the