Embed Size (px)

Citation preview

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 1/12

R e t a i l o p p o r t u n it ie s in

Ea s t In d ia

January 7, 2011

www.pwc.com

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 2/12

January 7, 20112PwC

A g e n d a

India’s retail sector—Snapshot

Selected observations

East India – Snapshot

East India’s retail market

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 3/12

January 7, 20113PwC

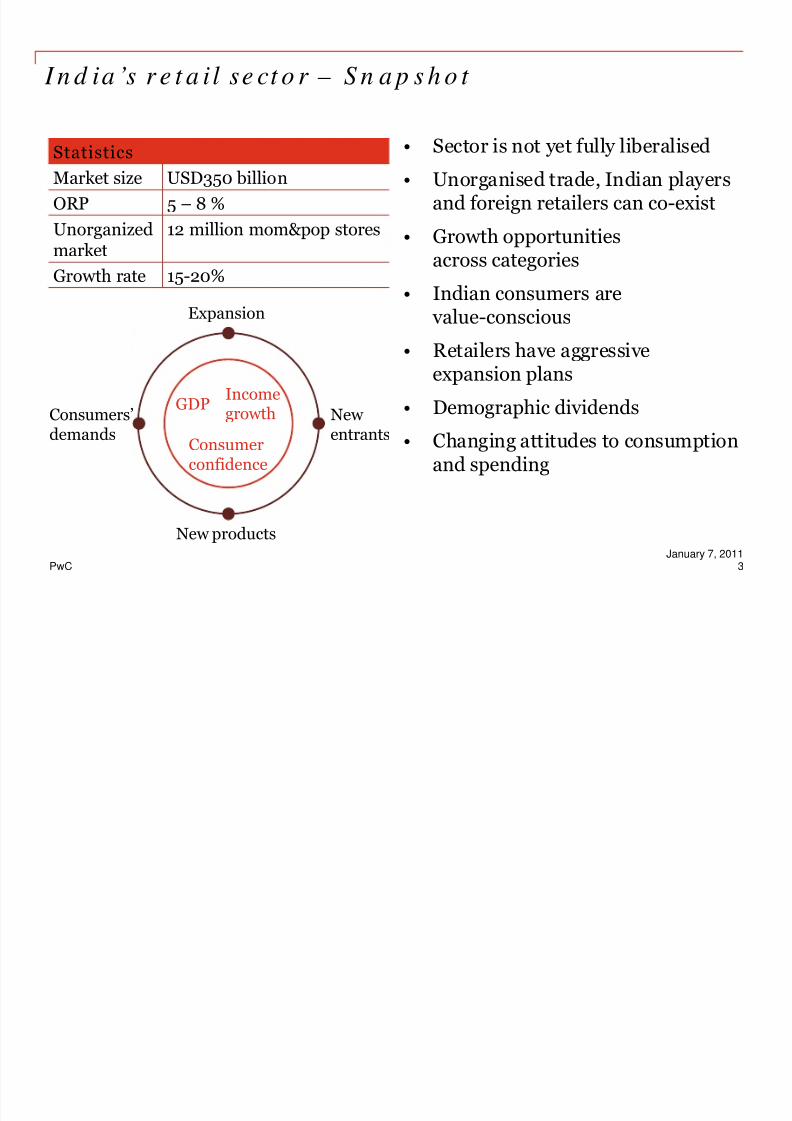

I n d ia ’s r e t a il se ct o r – S n a p s h o t

• Sector is not yet fully liberalised

• Unorganised trade, Indian playersand foreign retailers can co-exist

• Growth opportunitiesacross categories

• Indian consumers are value-conscious

• Retailers have aggressiveexpansion plans

• Demographic dividends• Changing attitudes to consumption

and spending

Statistics

Market size USD350 billion

ORP 5 – 8 %

Unorganizedmarket

12 million mom&pop stores

Growth rate 15-20%

GDPIncome

growth

Consumerconfidence

Expansion

New entrants

Consumers’demands

New products

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 4/12

January 7, 20114PwC

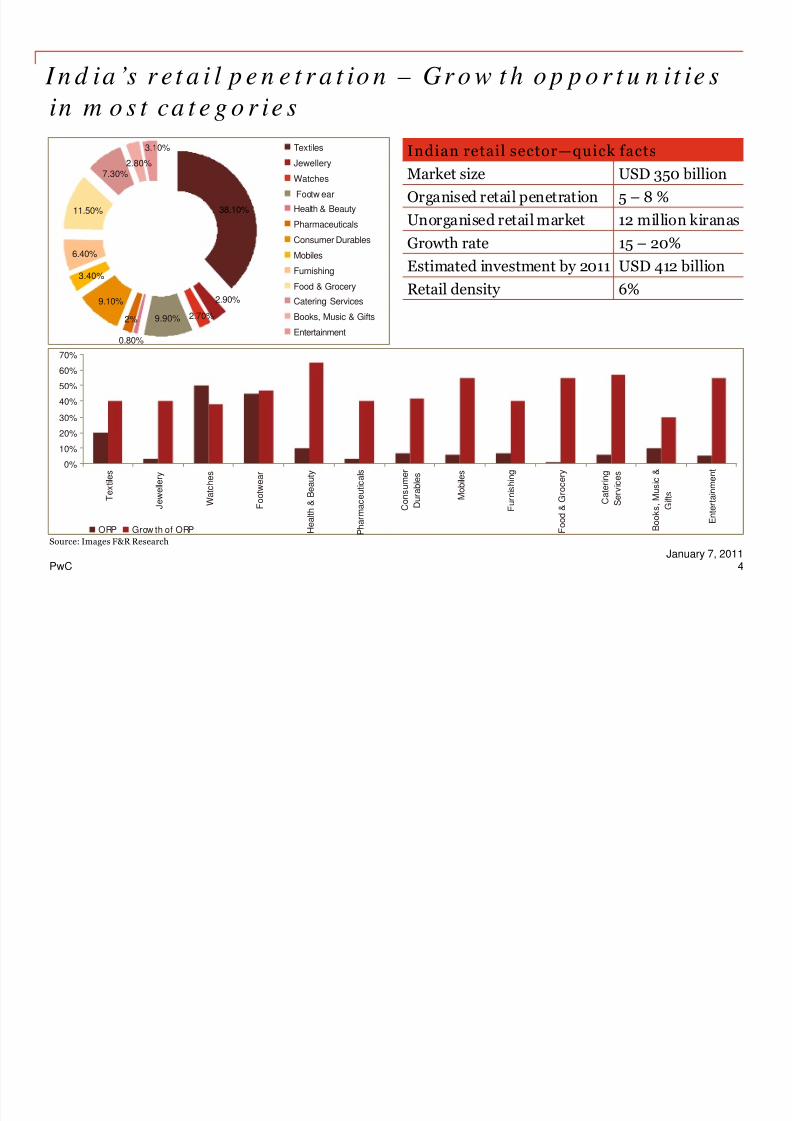

I n d ia ’s r et a i l p e n e t r a t io n – Gr o w t h o p p o r t u n it ie s

in m o s t ca t e g o r ie s

Indian retail sector—quick facts

Market size USD 350 billion

Organised retail penetration 5 – 8 %

Unorganised retail market 12 million kiranas

Growth rate 15 – 20%

Estimated investment by 2011 USD 412 billion

Retail density 6%

9.90%

9.10%

3.40%

6.40%

11.50%

7.30%2.80%

38.10%

2.90%

2.70%

0.80%

2%

3.10% Textiles

Jewellery

Watches

Footw ear

Health & Beauty

Pharmaceuticals

Consumer Durables

Mobiles

Furnishing

Food & Grocery

Catering Services

Books, Music & Gifts

Entertainment

0%

10%

20%

30%

40%

50%

60%

70%

T e x t i l e s

J e w e l l e r y

W a t c h e s

F o o t w e a r

H e a l t h & B e a u t y

P h a r m a c e u t i c a l s

C o n s u m e r

D u r a b l e s

M o b i l e s

F u r n i s h i n g

F o o d & G r o c e r y

C a t e r i n g

S e r v i c e s

B o o k s ,

M u s i c &

G i f t s

E n t e r t a i n m e n t

ORP Grow th of ORP

Source: Images F&R Research

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 5/12

January 7, 20115PwC

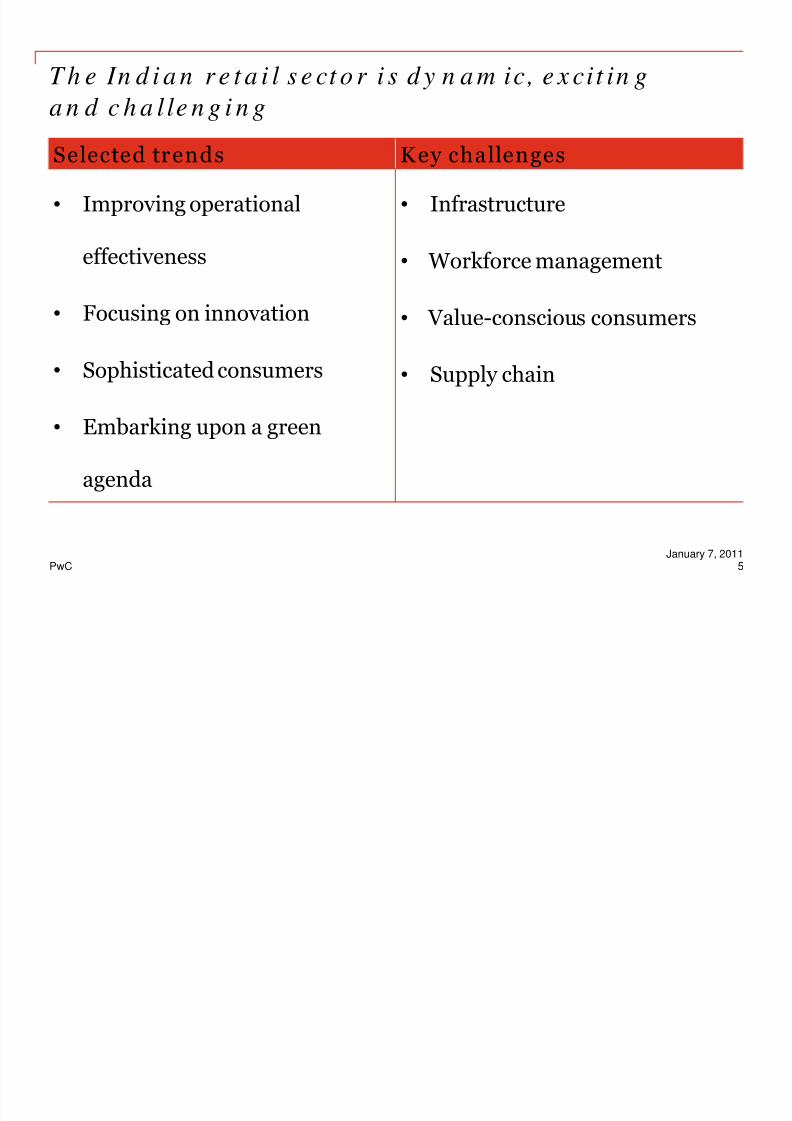

T h e In d i a n r e t a i l s e ct o r i s d y n a m ic, e x cit in g

a n d c h a l le n g i n g

Selected trends Key challenges

• Improving operational

effectiveness

• Focusing on innovation

• Sophisticated consumers

• Embarking upon a green

agenda

• Infrastructure

• Workforce management

• Value-conscious consumers

• Supply chain

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 6/12

January 7, 20118PwC

N e t w o r k r e d e sig n t o r e a p b e n e f it s o f Go o d s a n d

S e rv ic es Ta x ( GS T)

The GST regime is scheduled to beimplemented in April 2010 (although itmight be delayed). With the simplificationof the indirect tax structure, there is anopportunity to realign supply chainmanagement purely on business needs.

Selected benefits that retailers canavail include

• In the GST regime the tax paid by thelogistics company can be offset later onin the chain, reducing the cost of outsourcing and providing an impetus

to thirdparty logistics players.• Tax efficiency considerations will not

overwhelm other factors in warehouselocation decisions. This will allow rationalisation of the locations toimprove supply service levels tothe stores.

Supply chain costs

C u s t o m

e r s e r v i c e

High

Low

High

Low

T

Current cost/serviceperformance curve incurrent fiscal regime

T

Cost/serviceperformance curvein Post GST regime

Supply chain exchangecurve (Illustrative)

currentperformance

Better service,same cost

Better service, better cost

Better service,lower cost

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 7/12

January 7, 20119PwC

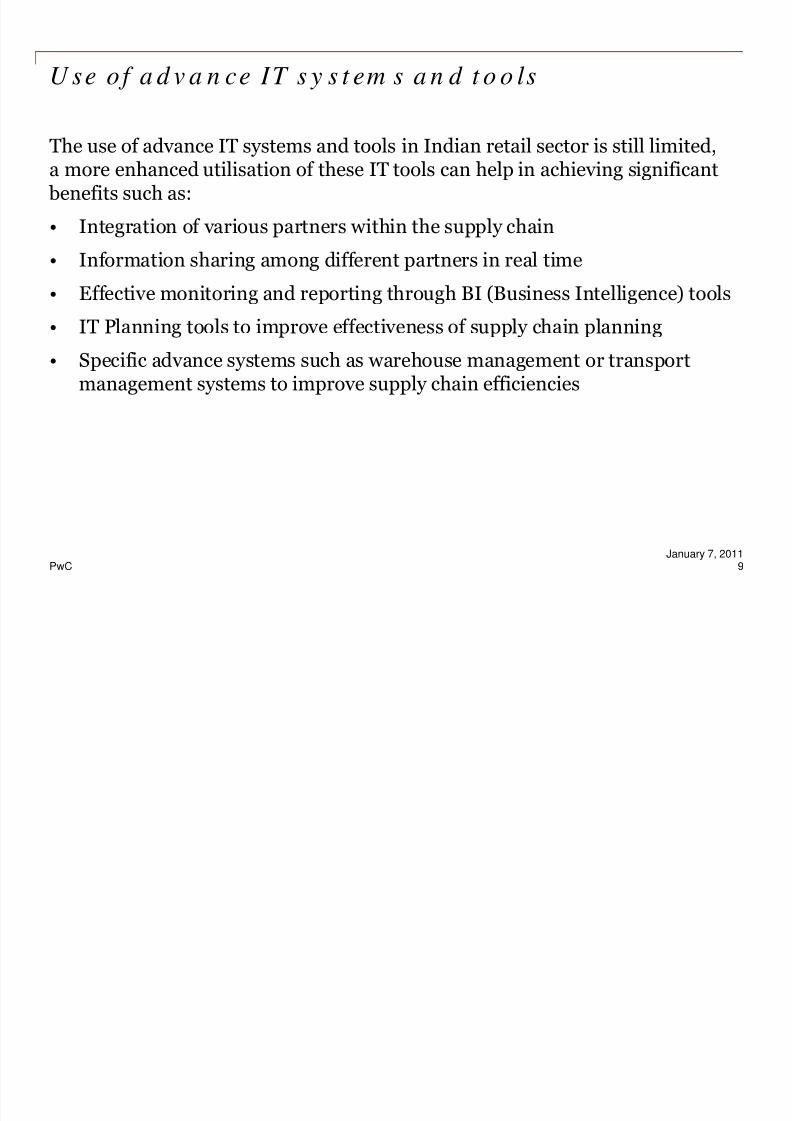

U se of a d v a n ce IT s y s t em s a n d t o o ls

The use of advance IT systems and tools in Indian retail sector is still limited,a more enhanced utilisation of these IT tools can help in achieving significant benefits such as:

• Integration of various partners within the supply chain

• Information sharing among different partners in real time

• Effective monitoring and reporting through BI (Business Intelligence) tools

• IT Planning tools to improve effectiveness of supply chain planning

• Specific advance systems such as warehouse management or transportmanagement systems to improve supply chain efficiencies

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 8/12

January 7, 201110PwC

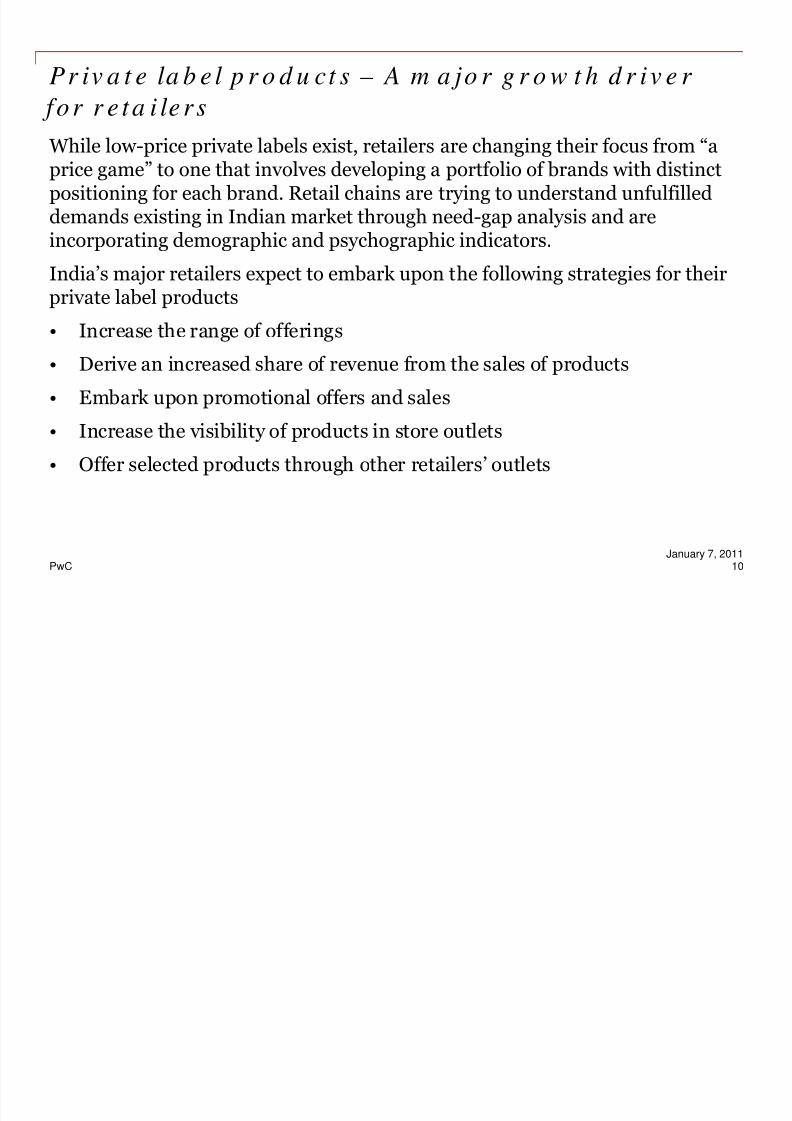

Pr iv a t e la b e l p r o d u ct s – A m a jo r g r o w t h d r iv e r

for r e ta i lers

While low-price private labels exist, retailers are changing their focus from “aprice game” to one that involves developing a portfolio of brands with distinctpositioning for each brand. Retail chains are trying to understand unfulfilleddemands existing in Indian market through need-gap analysis and areincorporating demographic and psychographic indicators.

India’s major retailers expect to embark upon the following strategies for theirprivate label products

• Increase the range of offerings

• Derive an increased share of revenue from the sales of products

• Embark upon promotional offers and sales

• Increase the visibility of products in store outlets

• Offer selected products through other retailers’ outlets

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 9/12

January 7, 201111PwC

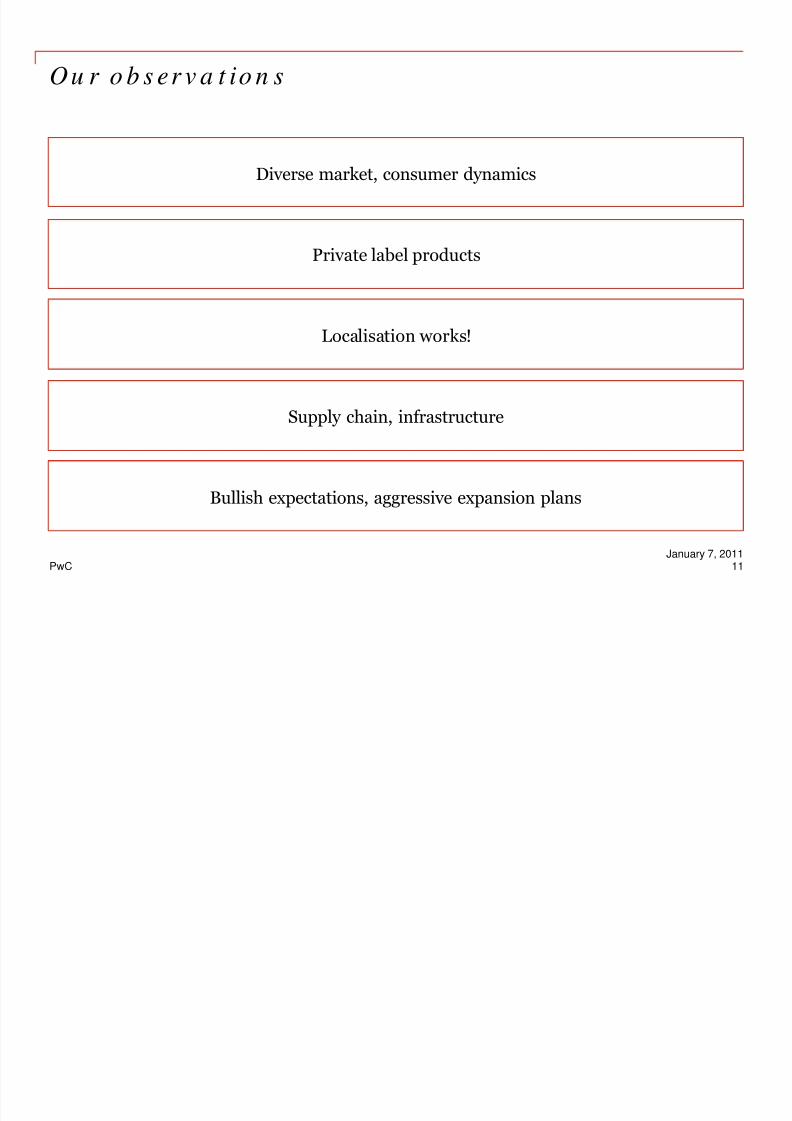

Ou r o b s er v a t io n s

Diverse market, consumer dynamics

Private label products

Supply chain, infrastructure

Bullish expectations, aggressive expansion plans

Localisation works!

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 10/12

January 7, 201112PwC

Ea s t I n d ia – A t -a -g la n ce

Opportun ity in a relatively untapped m ark et

Educational centersof excellence

Strong base forindustrial activities

Development of the ITand real estate sectors

At this time, Kolkata isthe main economic hub

Emerging hubs of economic activity

Aspirational anddemanding consumers

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 11/12

January 7, 201113PwC

E a s t I n d ia ’s r e t a il m a rk e t

Untapped retail mar ket

Aspirational consumer s

Better retail real estate ren tals

Franchising oppor tunities

Expansion plans

En t e r ing Eas t

I n d ia ena ble s

re ta i le r s to—

Drive sales

Grow theirpan-Indiafootprint

Serve new consumers

8/4/2019 DP115_v1.0

http://slidepdf.com/reader/full/dp115v10 12/12

T h a n k y o u

d e b d a s . s e n @i n .p w c .c o m

This publication has been prepared for general guidance on matters of interest only, and does notconstitute professional advice. You should not act upon the information contained in this publicationwithout obtaining specific professional advice. No representation or warranty (express or implied) isgiven as to the accuracy or completeness of the information contained in this publication, and, to theextent permitted by law, PwC, its members, employees and agents do not accept or assume any liability,responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, inreliance on the information contained in this publication or for any decision based on it.

© 2011 PricewaterhouseCoopers Private Limited. All rights reserved. In this document, “PwC” refers to

PricewaterhouseCoopers Private Limited (a limited liability company in India), which is a member firmof PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity.