Embed Size (px)

Citation preview

Dynamic Revenue Management for Online DisplayAdvertising

Guillaume RoelsUCLA Anderson School of Management, UCLA, 110 Westwood Plaza, Los Angeles, CA 90095, USA, [email protected]

Kristin FridgeirsdottirManagement Science and Operations, London Business School, Regent’s Park, London, NW1 4SA, United Kingdom,

In this paper, we propose an dynamic optimization model to maximize a web publisher’s online display

advertising revenues. Specifically, our model dynamically selects which advertising requests to accept and

dynamically delivers the promised advertising impressions to viewers so as to maximize revenue, accounting

for uncertainty in advertising requests and website traffic. After characterizing the structural properties of

our model, we propose a Certainty Equivalent Control heuristic and then show with a real case study that

our optimization-based method typically outperforms common practices. Our analysis thus highlights the

importance of integrating the sales function with the advertisement delivery function in web publishing

companies for globally maximizing revenues.

Key words : Revenue Management, Online Advertising, Dynamic Programming, Linear Programming

1

Dynamic Revenue Management for Online Display Advertising2

1. Introduction

Online advertising has grown at a fast pace over the past decade, reaching a revenue of $21.2 billion

in 2007 (IAB (2007)), and the growth is not expected to slow down in the near future as users

spend more time online, rich media technology increases user interaction, and online publishers

start discovering ways to monetize their remnant inventory (Hof (2008)).

The value proposition of digital marketing is to provide real-time feedback on customer behavior

and closely monitor the performance of advertising campaigns. Online advertising has changed

the nature of marketing, requiring more quantitative approaches with sophisticated tools and

algorithms (Booz Allen Hamilton (2007)) as well as dynamic adjustment of spending, in contrast to

the traditional up-front spending in broadcast advertising (Araman and Popescu (2007)). Hence,

different approaches are needed.

The online advertising space can be divided into two parts: Search word advertising and display

advertising. Search word advertising is done by search engine websites that post advertisements

along with search word results. Display advertising, on the other hand, is done by web publishers

who post advertisement banners across the top or along the side of their website pages.

In this paper, we consider a web publisher that seeks to maximize its advertising revenues by

delivering display advertisements (ads) on its website. Taking into account traffic uncertainty, the

publisher needs to decide which advertising contracts to accept or reject and how to fulfill them.

In practice, contract negotiation and advertisement delivery are often done independently by the

sales team and delivery engines (e.g. Dart by DoubleClick) respectively, with little coordination

between the two functions.

We propose a unified approach where the web publisher dynamically decides to accept or reject

advertising requests and dynamically delivers the promised advertising contract to the viewers,

so as to maximize its revenues over a finite horizon. We formulate the problem as a dynamic

program and characterize its structural properties. We then propose a Certainty Equivalent Control

heuristic, similar to Bertsimas and Popescu (2003). Using a real case study, we show that our

heuristic typically outperforms other approaches that are commonly used in practice.

Dynamic Revenue Management for Online Display Advertising3

The paper is organized as follows. In Section 2 we review the related literature. We model the

problem as a dynamic program in Section 3 and characterize its structural properties in Section

4. We then propose the Certainty Equivalent Control heuristic in Section 5 and illustrate its

performance on a real case study in Section 6. Finally, we conclude in Section 7.

2. Literature Review

The marketing literature on online advertising is abundant (see Prasad et al. (2003) and references

therein). In contrast, there exist few guidelines for effectively managing online advertising inventory,

despite the importance of that problem (Bain & Company (2008)).

Araman and Popescu (2007) and Kimms and Muller-Bungart (2007) study revenue management

for broadcast advertising. In contrast to broadcast media, where a big part of the advertising

capacity is allocated at the beginning of the season, online advertising requests arise at any point

in time during the season. Moreover, the delivery of online media advertising can be targeted to

specific users’ demographics and behaviors. Hence, different approaches are needed.

Araman and Fridgeirsdottir (2008) develop a pricing framework for web publishers facing uncer-

tain demand and uncertain advertising inventory. Using a novel steady-state queuing model,

they determine the optimal prices to quote to heterogeneous advertisers. Building on their work,

Fridgeirsdottir and Najafi-Asadolahi (2008a) characterize the optimal pricing strategy when adver-

tisers are impatient, which results in new types of queueing models. In contrast, our model optimizes

the contract acceptance/rejection decisions over a finite time horizon with exogenous prices.

Our model also optimizes the advertisement scheduling. Ad scheduling can typically be formu-

lated as a linear optimization problem (Chickering and Heckerman (2003)) but becomes NP-Hard

when the geometrical features of the website are modeled (Kumar et al. (2006)). Similar to ad

scheduling on websites, Turner et al. (2008) model ad scheduling in video games and develop a

dynamic scheduling algorithm.

Although the cost-per-impression (CPM) pricing scheme is prominent in online display adver-

tising, there exist other pricing schemes, such as cost-per-click (CPC) and cost-per-action (CPA),

Dynamic Revenue Management for Online Display Advertising4

if the advertiser’s objective is to generate traffic or sales rather than brand awareness. The attrac-

tiveness of one pricing scheme over the other is studied by Fridgeirsdottir and Najafi-Asadolahi

(2008b) and Mangani (2004). The pricing model of search word advertising is primarily based on

clicks (CPC). Because the ad click-through rates are unknown a priori, scheduling search word ads

must balance exploration with exploitation, see Rusmevichientong and Williamson (2006).

Some web publishers not only generate revenues from advertising but also from subscriptions.

Prasad et al. (2003) suggest that websites can increase their revenues by offering a menu of con-

tracts, where high subscription fees are associated with a small number of ads and vice versa. Using

an optimal control model, Kumar and Sethi (2008) dynamically determine the optimal subscrip-

tion fee and the amount of advertising on a website. However, Baye and Morgan (2000) argue that

competition mitigates the attractiveness of subscription fees.

In this paper, we develop an integrative approach that simultaneously optimizes contract nego-

tiation and advertisement delivery. Our model draws on traditional network revenue management

models (Talluri and van Ryzin (2004)) and in particular on the solution technique developed by

Bertsimas and Popescu (2003).

3. Model

We consider an online content publisher who seeks to maximize its revenue from display ads over a

time window [0, T ] (e.g., a quarter, a fiscal year), by (i) accepting or rejecting advertising requests

and (ii) dynamically delivering the advertisement impressions to the website viewers.

The publisher’s objective is thus to match supply (advertising inventory) with demand (adver-

tising requests) so as to maximize its revenues. In the following, we first formalize these concepts of

supply and demand and detail the sequence of events. We will decompose the time window [0, T ]

into subintervals, which will lead to a dynamic programming formulation for solving the publisher’s

problem.

Dynamic Revenue Management for Online Display Advertising5

3.1. Supply

Advertising impressions are uniquely characterized by combination of page and banner location,

delivery time, and viewer type. For instance, an ad impression could be “a top banner on the website

homepage during the first week of the second quarter, viewed by an 18-34-old male originating

from California.” Let P be the set of potential pages and banner locations on the website and U

be the set of viewer types. For simplicity, we consider discrete time periods and define T as the set

of delivery time windows. As a result, the set of possible types of ad impressions can be defined as

the cross-product set, i.e., W =P ×U ×T .

In any period t ∈ T , let Wt denote the set of possible ad impressions in period t, i.e., Wt =

P ×U ×{t}. The number of ad impressions, also known as the ad inventory, is however uncertain

at the time the advertising requests must be accepted or rejected because they are generated by

the web traffic. We denote by [Ik]k∈Wt the (random) ad inventory (in thousand units) available

to the publisher in period t ∈ T of each type k ∈Wt. If only one ad is delivered per page view,

∑k∈Wt Ik exactly corresponds to the website traffic in period t. In general, however, our model

allows for multiple ads to be displayed on the same page.

To simplify the analysis, we make the following standard assumption:

Assumption 1. The number of advertising impressions [Ik]k∈Wt in any period t ∈ T follows a

Markov process.

Although web traffic could in principle be correlated over time, there is empirical evidence that

a Poisson process is a reasonable approximation for web traffic (Cao et. al (2002)), which makes

Assumption 1 reasonable.

3.2. Demand

Advertisers submit their advertising requests to the publisher either directly or through the inter-

mediary of an advertising agency. Let C denote the potential set of contracts. Each contract i ∈ C

requests a number of impressions ni (in thousands) to be delivered on a particular set of pages to

Dynamic Revenue Management for Online Display Advertising6

a particular set of viewers in a particular time window (also known as flight), denoted by Wi ⊆W.

Each ad impression generates a unit revenue ri (also known as Cost-per-Thousand, or CPM) to

the publisher. If the advertising contract specifies a cost-per-click (CPC) or cost-per-action (CPA),

instead of a cost per impression, ri is the expected revenue per impression, obtained by multi-

plying the CPC or the CPA by the probability that a user will click or take the specified action.

(This approach is an aggregated way to incorporate these performance based payments schemes.

For more details see Fridgeirsdottir and Najafi-Asadolahi (2008b).) Whenever a publisher does not

fulfill a contract, it incurs a goodwill penalty πi per under-delivered impression. (Traditionally,

advertisers have requested “make-goods” in case of underdelivery, typically amounting to 10%-50%

of the average CPM of the shortfall.) To summarize, a contract i ∈ C specifies four parameters:

the number of impressions ni, the set of pages/viewers/dates Wi, the CPM ri, and the goodwill

penalty πi. In addition, we assume that the null contract (i.e., no request), denoted by the index

0, also belongs to C.

When publishers do not have enough advertisement contracts to fill their advertising slots, they

usually have recourse to advertising networks. Advertising networks (also known as “ad networks”)

offer significantly lower rates than regular advertisers (typically ten times lower) and do not require

any specific impression guarantee. As a result, ad networks are typically utilized for filling up

the remnant inventory. We model ad networks as an additional contract, say contract a, already

accepted in period 0, with an infinite number of requested impressions but no underdelivery penalty,

i.e., (na,Wa, ra, πa) = (∞,W, ra,0) where ra ¿ ri for all i∈ C \ {0}.

In general, an advertising contract consists of a bundle of contracts (ni,Wi, ri, πi). A bundle

must be accepted in full or rejected. Let B bet the potential set of bundles, including the null

contract (i.e., no request) and the ad network contract. For any bundle j ∈B, let Cj ⊆C be the set

of contracts bundled together.

Arrivals of advertising requests are assumed to be uncertain at time 0. For any bundle j ∈B, let

pjt be the probability that bundle j will be requested in period t. We also assume that the time

Dynamic Revenue Management for Online Display Advertising7

intervals are so small that the arrival probability of two simultaneous requests is negligible. That

is, in each period t, at most one bundle will be requested. Therefore, for any t∈ T ,∑

j∈B pjt = 1.

To simplify the analysis, we make the following standard assumption (see, e.g., Talluri and van

Ryzin 2004):

Assumption 2. The arrivals of advertising requests follow a Markov process.

3.3. Sequence of Events

In each time period the publisher faces two decisions. First he needs to determine which advertising

requests to accept, balancing the high CPMs against the underdelivery penalties. Then he needs

to decide which ad impressions to deliver on its website in any period t∈ T , balancing immediate

revenues against potential future profits.

In contrast to broadcast networks, online publishers can observe their traffic in real time and

dynamically adjust their advertisement delivery strategy. To model this flexibility in a discrete-time

framework, we make the following assumption.

Assumption 3. In each period t, the publisher observes the traffic on its website before delivering

the ads.

Note that this last assumption is not restrictive if the time intervals are small. Moreover, with

the current internet technology, publishers are able to first observe the characteristics of the viewers

before deciding which ads to serve. Under these three assumptions, the following sequence of

events/actions takes place in every period t:

1. Advertisers request a bundle i∈B.

2. The publisher decides to accept, or reject, the request.

3. The publisher observes the traffic on its web pages, i.e., how much advertising inventory of

each type (page/viewer) is available in period t.

4. The publisher decides which impressions to deliver, from the pool of advertising contracts it

has accepted.

Dynamic Revenue Management for Online Display Advertising8

5. The publisher delivers impressions and collects revenues. For every contract that reaches the

end of its flight, the publisher incurs goodwill penalties in case of under-delivery.

This sequence of events naturally gives rise to a dynamic programming formulating for solving

the publisher’s problem, which we present next.

3.4. Dynamic Programming Formulation.

Suppose that at time t, the web publisher has a set S ⊆ C of contracts in progress. Let Vt

({i, yi}i∈S)

be its expected profit-to-go from t onwards, before any request arises in t, given that yi thousand

impressions remain to be delivered, for each contract i∈ S.

We denote by V t

({i, yi}i∈S ∪{i, ni}i∈Cj

)the expected profit-to-go if bundle j ∈ B has been

accepted, consisting of the contracts i ∈ Cj with a request for ni impressions each. Similarly, we

denote by V t

({i, yi}i∈S)

the expected profit-to-go from t onwards if no contract is accepted in

period t. Accordingly, for t < T , the decision of accepting or rejecting an incoming request can be

modeled as follows:

Vt

({i, yi}i∈S)=

∑j∈B

pjt max{V t

({i, yi}i∈S), V t

({i, yi}i∈S ∪{i, yi}i∈Cj

)}. (1)

Without loss of generality, we assume that the goodwill penalty fees are incurred at the end of

the horizon. That is, if yi impressions, i∈ S, have not been delivered by the end of the horizon T ,

the publisher’s profit equals

VT

({i, yi}i∈S)=−

∑i∈S

πiyi.

For the contracts that end at or before T , the loss of goodwill parameter πi will be positive. In

contrast, for contracts which flight extends beyond T , the parameter πi may represent the salvage

value associated with these contracts, and may therefore be negative; it will however never be

smaller than −ri.

According to Assumption 3, the publisher observes the web traffic before delivering the ad

impressions. Let Vt

({i, yi}i∈S , [Ik]k∈Wt

)be the profit-to-go in period t after having observed the

amount of available ad inventory [Ik]k∈Wt . Accordingly,

V t

({i, yi}i∈S)=E

[Vt

({i, yi}i∈S , [Ik]k∈Wt

)], (2)

Dynamic Revenue Management for Online Display Advertising9

in which the expectation is taken with respect to the amount of advertising inventory of each type

(or equivalently, to the web traffic) in period t.

After observing the amount of available ad inventory, the publisher decides which ad impressions

to deliver from its pool of contracts. Let xik, i ∈ S, k ∈Wi, be the number of impressions of ads

from contract i delivered on a page/viewer/time k. Let also Wti =Wi ∩Wt be the set of page and

viewer types that are available in period t for delivering ad impressions for contract i ∈ S. The

publisher’s problem can therefore be formulated as the following recursion:

Vt

({i, yi}i∈S , [Ik]k∈Wt

)= max{xik}i∈S,k∈Wt

i

∑i∈S

ri

∑

k∈Wti

xik +Vt+1

i, yi−

∑

k∈Wti

xik

i∈S

s.t.∑

i∈S:k∈Wti

xik ≤ Ik k ∈Wt,

∑

k∈Wti

xik ≤ yi i∈ S, (3)

xik ≥ 0 i∈ S, k ∈Wti .

The objective function balances the immediate revenues against the potential future profits.

The number of impressions to be delivered in the future is equal to the number of impressions

to be delivered at the beginning of period t, yi, minus the number of impressions that have been

delivered in period t,∑

k∈Wtixik. The first constraint imposes that the number of impressions

delivered on a particular page to a particular viewer type cannot exceed the available ad inventory.

If the publisher has access to advertising networks, this first constraint will always be tight because

the publisher can always sell its remnant inventory at lower rates through the ad network. The

second constraint restricts the number of deliveries to be no greater than the requested number of

impressions specified by the contract. The last constraint requires nonnegativity of the delivered

impressions.

In addition, we have Vt+1

({yi}i∈S)≤ Vt

({yi}i∈S), for all t, because setting xik = 0 for all i ∈ S,

k ∈Wti is a feasible solution for the assignment problem (3) in period t. Moreover, for any j ∈ S,

the marginal value of an impression Vt

({yi}i∈S\{j} ∪{yj +1}

)−Vt

({yi}i∈S)≤ rj because the CPM

does not change over time. With these two results, one can show that it is never optimal to delay

the delivery of an ad impression in the hope of selling it at a larger rate in the future.

Dynamic Revenue Management for Online Display Advertising10

4. Structural Properties

In general, the objective function may not be concave, if bundles of contracts are required to be

either accepted in full or rejected. (Similarly, in the classic dynamic revenue management problem,

the value function may not be concave with batch arrivals.) In practice, however, contracts are

negotiated and the publisher may have some flexibility in choosing the number of impressions to

accept. Relaxing Equation (1) to allow for the publisher to choose less number of impressions than

requested, i.e.,

Vt

({yi}i∈S)=

∑j∈B

pjt max0≤yi≤ni,∀i∈Cj

{V t

({i, yi}i∈S ∪{i, yi}i∈Cj

)}, (4)

makes the problem concave, as we show next.

Proposition 1. If contracts can be partially accepted, as in (4), then for any i∈ S, Vt

({i, yi}i∈S)

is jointly concave in yi, i∈ S.

Proof The proof is by induction. The function VT

({i, yi}i∈S)

is linear, and therefore jointly

concave in {yi}i∈S . For any t, suppose that the function Vt+1

({i, yi}i∈S)

is jointly concave in

{yi}i∈S . Because concavity is preserved under affine transformations, Vt+1

({i, yi−

∑k∈Wt

ixik

}i∈S

)

is jointly concave in xik and yi, for all i∈ S and k ∈Wti . Therefore, the objective function and the

constraint set in Problem (3) are respectively jointly concave and jointly convex in {xik}i∈S,k∈Wti

and {yi}i∈S . Because partial maximization of a jointly concave function over a convex set preserves

concavity (Boyd and Vandenberghe (2004)), Vt

({i, yi}i∈S , [Ik]k∈Wt

)is jointly concave in {yi}i∈S , for

any [Ik]k∈Wt . Taking the expectation with respect to [Ik]k∈Wt preserves concavity, so V t

({i, yi}i∈S)

is also concave in {yi}i∈S . For any j ∈ S, maximizing V t

({i, yi}i∈S)

with respect to yj over the

convex set [0, nj] in (4) preserves concavity based on the partial maximization argument above,

so does taking a nonnegative weighted sum of concave functions. Therefore, Vt

({i, yi}i∈S)

is also

concave in {yi}i∈S , completing the induction step. ¤

Because Problem (4) is a concave maximization problem over a convex set, the optimal number

of impressions to accept may not necessarily be at the boundary of the interval. As a result, large

contracts will typically tend to be renegotiated, especially if the web traffic forecasts are low.

Dynamic Revenue Management for Online Display Advertising11

We next investigate the sensitivity of the publisher’s value function to the problem parameters.

For convenience, let us denote by Vt(({i, yi}i∈S ;θ

)the value function at time t when some parameter

takes on a value θ. The next proposition shows that the value function is convexly increasing

with the CPM and convexly decreasing with the penalty πi. In addition, if partial contracts are

acceptable, the publisher benefits from larger number of impressions requested, but with decreasing

marginal returns, which is in line with the findings in Araman and Fridgeirsdottir (2008) and

Fridgeirsdottir and Najafi-Asadolahi (2008a).

Proposition 2. For any j ∈ S, Vt

({i, yi}i∈S ;πj

)is convex decreasing in πj and Vt

({yi}i∈S ; rj

)

is convex increasing in rj. If the contracts can be partially accepted, as in (4), then for any j ∈ S,

Vt

({i, yi}i∈S ;nj

)is concave increasing in nj.

Proof For each {yi}i∈S , the function VT

({i, yi}i∈S ;πj

)is linear, and therefore convex, decreasing

in πj. Because the successive pointwise maximizations in (3), as well as in (1) or (4), and the

expectations in (2), preserve convexity, the value function Vt

({i, yi}i∈S ;πj

)is convex decreasing

in πj, for any t.

Let t∗ be the last period of the duration of contract i, i.e., t∗ = max{t :Wi ∩Wt 6= ∅}. For each

{yi}i∈S , the function Vt∗({i, yi}i∈S ; rj

)is convex increasing in rj, because it is the pointwise maxi-

mum of linear functions of rj in (3). Because the successive pointwise maximizations in (3) as well

as in (1) or (4), and the expectations in (2), preserve convexity, the value function Vt

({i, yi}i∈S ; rj

)

is convex increasing in rj, for any t≤ t∗.

Let t∗ be the first period of the duration of contract j, i.e., t∗ = min{t :Wj ∩Wt 6= ∅}. Because

nj is the right-hand side of the constraint in (4), Vt∗({i, yi}i∈S ;nj

)is increasing in nj, and jointly

concave in nj and {yi}i∈S . Because the successive partial maximizations, over convex sets, in (3)

and (4), and the expectations in (2), preserve concavity, the value function Vt

({i, yi}i∈S ;nj

)is

concave increasing in nj, for any t≤ t∗. ¤

The function Vt

({i, yi}i∈S , [Ik]k∈Wt

)is also concave increasing with Ik. Thus, smaller profits will

be obtained under second-order stochastically larger random variables. In particular, if the number

Dynamic Revenue Management for Online Display Advertising12

of page views is normally (or log-normally) distributed, the publisher’s profit will be decreasing

with the variance of the distribution (Levy (1992)).

The state space of the dynamic program can however be very large, leading to the so-called

curse of dimensionality and limiting the practicality of the approach. In the next two sections, we

show that, even if the dynamic program is solved approximately, it stills yield many benefits over

alternative, myopic approaches.

5. Certainty Equivalent Approximation

Following Bertsimas and Popescu (2003), we propose a Certainty Equivalent Control (CEC) heuris-

tic. Specifically, we assume that the ad inventory of each type (determined by the web traffic)

is known in advance and equal to its expectation. We also assume perfect knowledge about the

number and characteristics of future requests. In the dynamic optimization formulation, the occur-

rence of any request j ∈B, consisting of the contracts in Cj with characteristics (ni,Wi, ri, πi)i∈Cj,

has a binary nature: either request j is made in period t, with some probability pjt, or it is not.

Instead, we assume that, for all i ∈ Cj, a request for contract i will be introduced in period t,

deterministically, with only nipjt requests for impressions.

Given the good performance of the CEC heuristic in network revenue management (Bertsimas

and Popescu (2003)) and that controls based on the CEC are asymptotically optimal for the

stochastic network revenue management problem (Talluri and van Ryzin (2004)), one expects these

restrictions not to be too stringent in our setting.

Analogous to V t

({i, yi}i∈S), we denote by V

d

t

({i, yi}i∈S)

the maximum profit-to-go in period t

when there is no uncertainty (the superscript d refers to deterministic). Let S be the set of contracts

that have been accepted at time t and let Bt be the set of future bundle requests. Because both the

ad inventory and the future requests are assumed to be known at time t, the dynamic optimization

problem is now deterministic and an open-loop control is optimal. In particular, let the binary

variable δj equal 1 if bundle j ∈Bt is planned to be accepted and equal 0 otherwise. Similarly, let

xi,k,s denote the number of ad impressions from contract i∈ S ∪ (∪j∈BtCj) planned to be delivered

Dynamic Revenue Management for Online Display Advertising13

in period s = t, ..., T to the page/viewer type k ∈Wsi . Accordingly, the publisher’s problem at time

t can be formulated as the following mixed-integer optimization problem:

Vd

t

({i, yi}i∈S)= max

∑

i∈S∪(∪j∈BtCj)

T∑s=t

∑k∈Ws

i

rixi,k,s−∑i∈S

πi

yi−

T∑s=t

∑k∈Ws

i

xi,k,s

−∑j∈Bt

∑i∈Cj

πi

δjpini−

T∑s=t

∑k∈Ws

i

xi,k,s

s.t.∑

i∈S∪(∪j∈BtCj):k∈Ws

i

xi,k,s ≤E[Ik] k ∈Ws, s = t+1, ..., T,

T∑s=t

∑k∈Ws

i

xi,k,s ≤ yi i∈ S, (5)

T∑s=t

∑k∈Ws

i

xi,k,s ≤ piniδj i∈ (∪j∈BtCj) , j ∈Bt

xi,k,s ≥ 0 i∈ S ∪ (∪j∈BtCj) , k ∈Wsi , s = t, ..., T,

δj ∈ [0,1] j ∈Bt.

The objective function in (5) consists of three terms: the total advertising revenue, summed over

all contracts and future time periods, the underdelivery penalty associated with the contracts that

have already been accepted at time t, and the underdelivery penalty associated with the future

contracts, if they are to be accepted (i.e., if δj = 1 for any j ∈Bt). Similar to (3), the first constraint

ensures that the number of ad impressions does not exceed the expected ad inventory, for all future

periods. The second and third constraints guarantee that the delivered impressions do not exceed

the number of impressions requested by the contracts, respectively for the contracts that have

already been accepted in period t and for the future contracts. Finally, ad impressions are required

to be nonnegative and future contracts can be either accepted in full or rejected.

Analogous to (3), we define V dt

({i, yi}i∈S , [Ik]k∈Wt

)in the same way as V

d

t

({i, yi}i∈S), where the

right-hand side of the first set of constraints in (5) associated with period t, i.e., E[Ik], are replaced

with the actual ad inventory Ik for all k ∈Wt.

Let us define At the set of future bundles that are planned to be accepted, that is At = {j ∈

Bt : δj = 1}. Moreover, let us denote by Vd

t

({i, yi}i∈S ;At

)the optimal revenue of the deterministic

Dynamic Revenue Management for Online Display Advertising14

problem if the set of future contracts that are accepted corresponds to At. For a given set of

contracts At, the optimization problem (5) reduces to a simple transportation problem. The next

proposition characterizes the sensitivity of the revenue with respect to the problem parameters

for a given set of contracts At. Similar to Proposition 2, we denote by Vd

t

({i, yi}i∈S ;At;θ)

the

optimal value of (5) when some parameter takes on the value θ. As in Proposition 2, we find

that the optimal revenue of the deterministic problem is convex increasing with the CPM, convex

decreasing with the goodwill penalty, and concave increasing in the number of impressions, when

the set of future contracts is given. We also find that broader targets (in terms of page types or

banner locations, viewer types, and flights) are beneficial to the publisher, because they give more

flexibility, but exhibit decreasing differences.

Proposition 3. Suppose the set of future contracts to be accepted is given by At. Then, for any

i ∈ S, Vd

t

({i, yi}i∈S ;At;yi

)is concave increasing in yi; for any i ∈ At, V

d

t

({i, yi}i∈S ;At;ni

)is

concave increasing in ni. For any i ∈ S ∪ At, Vd

t

({i, yi}i∈S ;At; ri

)is convex increasing in ri,

Vd

t

({i, yi}i∈S ;At;πi

)is convex decreasing in πi, and V

d

t

({i, yi}i∈S ;At;Wi

)is submodular increas-

ing on W. For any k ∈W, Vd

t

({i, yi}i∈S ;At;E[Ik])

is concave increasing in E[Ik].

Proof All results follow form standard linear programming theory (see Bertsimas and Tsitsiklis

(1997)). The submodularity of Vd

t

({i, yi}i∈S ;At;Wi

)follows from Theorem 4 in Wolsey (1989). ¤

Because Problem (5) reduces to a linear optimization problem when the set At is fixed, the

opportunity costs of the advertising space can be obtained as a byproduct of the optimization and

be used in the negotiation process. For instance, some advertisers request the exclusive use of the

homepage over a certain time window in exchange for a flat fee. Using the optimal shadow prices

from (5) could help publishers set their fees, to account for the marginal opportunity cost of the

advertising impressions. On the other hand, it may help an advertiser adjust its advertising time

window to benefit from lower rates whenever the advertisement inventory exceeds the demand.

When the set At needs to be chosen, (5) is a capacitated facility location problem, which is

known to be NP-Hard. Thus, if the number of potential contracts is large, the problem may not

Dynamic Revenue Management for Online Display Advertising15

be solvable in reasonable time. However, as demonstrated in Proposition 3.4 in Nemhauser et al.

(1978), V dt

({i, yi}i∈S ;At

)is submodular on St and simple greedy or search algorithms that select

the most promising contracts are associated with reasonable performance guarantees (see, e.g.,

Nemhauser et al. (1978)).

If there is no uncertainty about the request arrivals (as in the case study we examine in the

next section), Vd

t

({i, yi}i∈S) ≥ V t

({i, yi}i∈S)

for all t and all S ⊆ C. To see this, observe that,

for any given acceptance/rejection policy, V t

({i, yi}i∈S)

can be bounded from above by replacing

the distribution of the number of advertising impressions [Ik]k∈Wt , for all t ∈ T , by its mean,

using Jensen’s inequality. Maximizing then the upper bound over all policies exactly leads to

Vd

t

({i, yi}i∈S).

The implementation of the CEC follows the following sequence. In every period t,

1. An advertising request j ∈Bt arises.

2. Request j is accepted if Vd

t

({i, yi}i∈S ∪{i, yi}i∈Cj

)≥ V

d

t

({i, yi}i∈S). If the request is accepted,

update S ←S ∪Cj and Bt ←Bt \ {j}.

3. The publisher observes the available ad inventory in period t, i.e., [Ik], k ∈Wt.

4. Compute V dt

({i, yi}i∈S , [Ik]k∈Wt

). Let {xi,k,s}i∈S,k∈W,s=t,...,T be the optimal solution of the

associated capacitated facility location problem.

5. For all i∈ S, k ∈Wt, deliver xi,k,t ad impressions from contract i to the page/viewer type k.

Even though the number of contracts and the ad inventories are assumed to be known with

certainty in (5), the policy is adaptable to changes in contract offers or demand because it is re-

optimized on a folding horizon basis. If the number of future contracts is relatively small (i.e., less

than a few hundreds), Problem (5) can easily be solved to optimality in a reasonable amount of

time, making the approach appealing for practical applications.

6. Case Study

In this section, we evaluate the performance of our optimization-based approach on a real problem

instance, detailed in Roels and Skowrup (2008), and compare it to common practices.

Dynamic Revenue Management for Online Display Advertising16

6.1. Case Description

An online content publisher, Break.com, seeks to determine which display advertising contracts to

accept and which ad impressions to deliver over the course of the second quarter of 2008. Founded

in 2005 as a “cross between YouTube and Spike TV,” Break.com quickly built a loyal audience

around its ability to find and purchase funny, user-generated video content and games that appeal

to young males. In 2005, the company made less than $1.4 million in display ad revenue; but by

2007, with nine million monthly unique visitors, the company wanted to achieve a ten-fold growth

in advertising revenues.

Supply. Break.com serves display ads on its homepage, on the video page, on the game page, as

well as on any page of the website (which is referred to “Run-of-Site”). Advertisements are targeted

to only one type of viewers, namely the 18-34 males, which constitute the website main audience.

Finally, the second quarter is divided in weeks, from week 14 to week 27. As a result, the set of

types of advertising slots W, defined as the cross-product P ×U ×T , consists of 56 elements.

The amount of advertising inventory is unknown at the beginning of the quarter because it

depends on the web traffic. A manager of the company estimated the daily mean number of page

views for each targeted page (homepage, videos, games, others), as well as a low and high estimates

respectively equal to 50% and 150% of the baseline estimate (see Exhibit 4 in Skowrup and Roels

2008). Due to the high traffic on the website, we modeled the number of visitors with a normal

distribution, as a limiting approximation to the Poisson distribution of web traffic. We assumed

that the low-high estimate range corresponded to the 95%-confidence interval about the mean,

leading to an estimated daily standard deviation of one fourth the mean. Without correlation,

the coefficient of variation of the weekly demand thus equals 1/(4√

7). Finally, we assumed that

the number of ad impressions was equal to the number of page views, i.e., only one banner was

displayed per page.

Demand. The publisher has already accepted 24 bundle contracts and expects to receive 11

additional requests. Hence, the number of requests is known deterministically, in contrast to the

Dynamic Revenue Management for Online Display Advertising17

dynamic programming formulation presented in Section 3. A bundle typically consists of two to

four contracts, depending on the number of page types covered. Each contract specifies a targeted

page type, a delivery time window (which we rounded to full weeks), a CPM, and a requested

number of impressions (see Exhibits 5-6 in Skowrup and Roels 2008). We considered a constant

goodwill penalty rate of 10% of the contract CPM, per underdelivered impression. We also assumed

that the company had recourse to ad networks, offering a constant CPM of $0.30 per impression.

CEC Heuristic. Because of the large number of bundles, together with the large number of types

of advertising inventory, an exact optimization approach as proposed in Section 3 would have been

computationally prohibitive. Instead, we considered the CEC approach presented in Section 5,

re-solved at the beginning of each period. The CEC heuristic involves the solution of two mixed-

integer optimization problems (5) per period, to sequentially decide (i) which bundles to accept

and (ii) how to deliver the requested impressions to the website viewers.

Benchmarks. As argued in the previous sections, Vd

0

({yi, i}i∈S), where S corresponds to the

set of 24 bundle contracts that have already been accepted at time 0, is an upper bound on the

optimal profit-to-go, and consequently, on the profit generated with the CEC approach, if there is

no uncertainty about the request arrivals. We refer to this upper bound as DET, for deterministic.

Currently, the company is using a threshold policy to determine which requests to accept or

reject, based on their average CPM. That is, a contract is accepted if and only if its CPM is larger

than a certain threshold price, which was preliminarily determined based on a yearly sales goal. In

our implementation, we considered several threshold values, ranging from $3 to $4.5, where a $3

CPM is among the lowest CPMs that were requested and $4.5 is among the highest CPMs that

were requested. Using the threshold policy, the acceptance/rejection decisions of the bundles can

be made at the beginning of the quarter, because it does not depend on capacity usage information.

Based on the threshold policy, we consider the following two heuristics. First, we consider the

threshold policy, for deciding which requests to accept, in conjunction with (5) for deciding which

impressions to deliver. Because (5) reduces to a linear optimization problem once contracts have

been selected, we refer to this heuristic as TH-LP, for threshold-linear program.

Dynamic Revenue Management for Online Display Advertising18

The second heuristic is based on the common industry practice of uniformly delivering impres-

sions over time. Specifically, in each period, we consider all contracts that remain to be completed

and define the current load as the total number of impressions remaining to be delivered, divided

by the total number of periods until the end of the flight. We then solve a one-period version of

(5) so as to match the current loads to the available ad inventory. We refer to this second heuristic

as TH-UNI, for threshold-uniform allocation.

6.2. Results.

Base Case. We simulated the performance of our CEC against TH-LP and TH-UNI over 100

runs. The optimization of (5) was implemented in CPLEX 10.0 and took less than a second. Table

1 compares the expected profit (advertising revenue + ad network advertising revenue - goodwill

penalties) of all policies for different values of demand coefficient of variation.

Table 1 Expected Revenues as a Function of the Coefficient of Variation.

Policy Threshold Coefficient of Variation1/(4

√7) 1/(2

√7) 1/(

√7) 2/(

√7)

DET 1,906,900 1,906,900 1,906,900 1,906,900CEC 1,898,200 1,886,000 1,847,400 1,791,900

TH-LP

$3.0 1,885,000 1,870,800 1,832,400 1,778,200$3.5 1,853,500 1,840,400 1,805,000 1,791,900$4.0 1,811,600 1,800,300 1,768,100 1,711,500$4.5 1,784,700 1,778,600 1,752,600 1,697,000

TH-UNI

$3.0 1,568,700 1,562,900 1,543,500 1,502,600$3.5 1,557,600 1,554,200 1,535,100 1,493,000$4.0 1,524,500 1,518,300 1,497,900 1,455,400$4.5 1,507,100 1,503,100 1,486,200 1,445,900

Table 1 shows that the CEC is near-optimal in the base case (Coefficient of Variation equal to

1/(4√

7)). The optimality gap, relative to DET, slightly deteriorates as the coefficient of variation

increases, but so does also the revenue under the optimal DP policy because it is smaller under

second-order larger distributions. We therefore expect the CEC policy to be near-optimal under

all web traffic scenarios.

In addition, the CEC heuristic always dominates the threshold policies. Moreover, comparing

the performance of TH-LP with TH-UNI reveals that adopting an optimization-based approach for

Dynamic Revenue Management for Online Display Advertising19

delivering impressions, rather than distributing them evenly over the flight duration, can generate

15-20% more profits. Optimization-based approaches can therefore lead to significant additional

gains in managing advertising contracts.

Because advertisers typically value uniform impressions to maximize the outreach of their cam-

paigns, many publishers have adopted this ad delivery mode as common industry practice, even

though it is not formally contracted on. However, the revenue differential between the TH-UNI

and the CEC approaches reveals that uniform delivery comes at a cost to the publisher and should

be incorporated in contract negotiations. In particular, it is paramount for publishers to assess

whether uniform delivery is really valued by their clients and to choose to offer this free service

only for advertisers with which they want to build long-term relationships.

It is interesting to note that the performance of the threshold heuristics is not very sensitive

to the actual threshold CPM. Two factors contribute to this effect. First, only 11 requests, out of

the 35 available, are subject to optimization, making the base profit, common to all approaches,

relatively high. Second, all threshold heuristics ignore capacity utilization and traffic variability

in their decision of contracts to accept and therefore exhibit the same biases, independent of the

magnitude of the threshold.

Table 2 compares the performance of the policies for different values of the goodwill rate πi/ri,

ranging from 0% to 150% of the CPM (the base case was 10%). Hence, the dominance of the CEC

approach over the threshold policies is even starker when the goodwill penalty is large. In fact, the

TH-UNI heuristic’s tendency to underdeliver impressions can even lead to a loss. Consequently,

publishers who wishes to build long-term relationships with their advertisers or advertising agencies

should consider adopting an optimization-based approach for managing their advertising contracts.

Expanded Product Set. To evaluate the impact of switching to an optimization-based approach

for managing all contracts, we now assume that the 24 initial bundles are also renegotiable. There-

fore, the publisher needs to decide which requests to accept among the pool of 35 bundles available.

Table 3 shows that, despite the increase in the number of requests, the performance of the CEC

Dynamic Revenue Management for Online Display Advertising20

Table 2 Expected Revenues as a Function of the Goodwill Penalty Rate.

Policy Threshold Goodwill Penalty Rate0% 50% 100% 150%

DET 1,914,500 1,877,800 1,860,000 1,847,900CEC 1,904,800 1,865,400 1,840,800 1,830,000

TH-LP

$3.0 1,891,000 1,850,600 1,790,800 1,763,400$3.5 1,857,800 1,829,300 1,790,600 1,766,100$4.0 1,814,100 1,807,800 1,796,400 1,791,100$4.5 1,786,800 1,783,900 1,779,700 1,775,600

TH-UNI

$3.0 1,698,000 1,051,300 404,600 -242,200$3.5 1,683,700 1,053,300 422,900 -207,500$4.0 1,646,400 1,036,600 426,800 -183,000$4.5 1,627,700 1,024,800 422,000 -180,900

heuristic is near optimal. Note also that the performance of the threshold policies is significantly

more sensitive to the choice of the threshold value than in our base case because all 35 contracts

are subject to selection.

Table 3 Expected Revenues with the Expanded Product Set.

Policy Threshold Expected ProfitDET 2,051,000CEC 2,037,400

TH-LP

$3.0 1,811,700$3.5 1,665,500$4.0 1,506,900$4.5 1,095,100

TH-UNI

$3.0 1,472,800$3.5 1,362,500$4.0 1,214,900$4.5 844,900

More importantly, Table 3 reveals that adopting an optimization-based approach for both the

selection of requests and the ad impressions can lead to about $200,000-$1,200,000 additional

profits per quarter, i.e., $0.8-$4.8 million per year, a significant increase for a company with a

$10-15 million sales goal.

Random Occurrences of Requests. We have assumed so far that all requests were known in

advance. We now relax this assumption by associating a 50% probability of occurrence with each

request, realized at the beginning of the flight of the request.

Dynamic Revenue Management for Online Display Advertising21

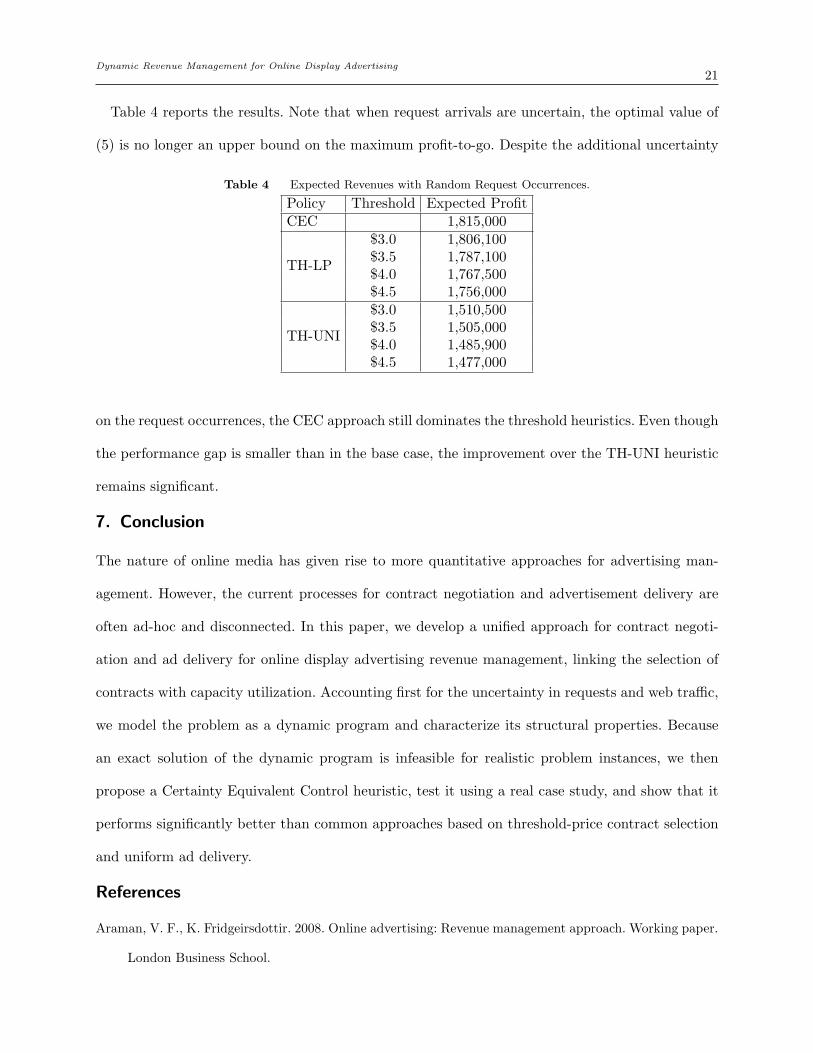

Table 4 reports the results. Note that when request arrivals are uncertain, the optimal value of

(5) is no longer an upper bound on the maximum profit-to-go. Despite the additional uncertainty

Table 4 Expected Revenues with Random Request Occurrences.

Policy Threshold Expected ProfitCEC 1,815,000

TH-LP

$3.0 1,806,100$3.5 1,787,100$4.0 1,767,500$4.5 1,756,000

TH-UNI

$3.0 1,510,500$3.5 1,505,000$4.0 1,485,900$4.5 1,477,000

on the request occurrences, the CEC approach still dominates the threshold heuristics. Even though

the performance gap is smaller than in the base case, the improvement over the TH-UNI heuristic

remains significant.

7. Conclusion

The nature of online media has given rise to more quantitative approaches for advertising man-

agement. However, the current processes for contract negotiation and advertisement delivery are

often ad-hoc and disconnected. In this paper, we develop a unified approach for contract negoti-

ation and ad delivery for online display advertising revenue management, linking the selection of

contracts with capacity utilization. Accounting first for the uncertainty in requests and web traffic,

we model the problem as a dynamic program and characterize its structural properties. Because

an exact solution of the dynamic program is infeasible for realistic problem instances, we then

propose a Certainty Equivalent Control heuristic, test it using a real case study, and show that it

performs significantly better than common approaches based on threshold-price contract selection

and uniform ad delivery.

References

Araman, V. F., K. Fridgeirsdottir. 2008. Online advertising: Revenue management approach. Working paper.

London Business School.

Dynamic Revenue Management for Online Display Advertising22

Araman, V. F., I. Popescu. 2007. Stochastic revenue management models for media broadcasting. Working

paper.

Bain and Company. 2008. Bain/IAB Digital Pricing Research, www.iab.net.

Baye M. R., J. Morgan. 2000. A simple model of advertising and subscription fees. Economics Letters 69

345-351.

Baye M. R., J. Morgan. 2003. The value of information in an online consumer electronics market. Journal

of Public Policy and Marketing 22 17-25.

Bertsimas D., I. Popescu. 2003. Revenue management in a dynamic network environment. Transportation

Science 37 257-277.

Bertsimas, D., J. N. Tsitsiklis. 1997. Introduction to Linear Optimization, Athena Scientific, Belmont, MA.

Bollapragada, S., H. Cheng, M. Phillips, M. Garbiras, M. Scholes, T. Gibbs, M. Humphreville. 2002. NBC’s

optimization systems increase revenues and productivity. Interfaces 32 (1) 47-60.

Booz Allen Hamilton. 2007. HD Marketing 2010: Sharpening the conversations, www.boozallen.com.

Boyd, S., L. Vandenberghe. 2004. Convex Optimization. Cambridge University Press, UK.

Cao, J., W. S. Cleveland, D. Lin, D. X. Sun. 2002. Internet traffic tends toward Poisson and independent as

the load increases. Nonlinear estimation and classification, eds. C. Holmes, D. Denison, M. Hansen, B.

Yu, B. Mallick, Springer, New York.

Chickering, D.M., Heckerman, D. 2003. Targeted advertising on the web with inventory management. Inter-

faces 33 (5) 71-77.

Fridgeirsdottir, K., S. Najafi Asadolahi. 2008. Revenue management for online advertising: Impatient adver-

tisers. Working paper. London Business School.

Fridgeirsdottir, K., S. Najafi Asadolahi. 2008. Revenue management for online advertising: Pay-per-click

pricing. Working paper. London Business School.

Hof, R. D. 2008. Yahoo is counting on Apex. Business Week September 18, 2008.

IAB Internet Advertising Revenue Report. 2007. Interactive Advertising Bureau, www.iab.net.

Kimms, A., M. Muller-Bungart. 2007. Revenue management for broadcasting commercials: The channel’s

problem of selecting and scheduling the advertisements to be aired. International Journal of Revenue

Management 1(1) 28-44.

Dynamic Revenue Management for Online Display Advertising23

Kumar, S., S. P. Sethi. 2008. Dynamic pricing and advertising for web content providers. To appear in

European Journal of Operational Research.

Kumar, S., V.S. Jacob, C. Srikandarajah. 2006. Scheduling advertisements on a web page to maximize

revenue. European Journal of Operational Research. 173 1067-1089.

Levy, H. 1992. Stochastic dominance and expected utility: survey and analysis. Management Science 38(4)

555-593.

Mangani, A. 2004 Online advertising: Pay-per-view versus pay-per-click. Journal of Pricing and Revenue

Management 4 (1) 295-302.

Nemhauser, G. L., L. A. Wolsey, M. L. Fisher. 1978. An analysis of approximations for maximizing submod-

ular set functions – I. Mathematical Programming 14 265-294.

Prasad, A., V. Mahajan, B. Bronnenberg. 2003. Advertising versus pay-per-view in electronic media. Inter-

national Journal of Research in Marketing 20 13-30.

Roels, G., T. Skowrup. 2008. Break.com. UCLA Anderson School of Management Case Study, http://www.

anderson.ucla.edu/x15450.xml.

The Rubicon Project. 2008. 2008 Online advertising market report: Q1: Ad network landscape, trends and

outlook, www.rubiconproject.com.

Rusmevichientong, P., D.P. Williamson. 2006. An adaptive algorithm for selecting profitable keywords for

search-based advertising services. in Proceedings of the Seventh ACM Conference on Electronic Com-

merce. 260-269.

Talluri, K.T., G.J. van Ryzin. 2004. The Theory and Practice of Revenue Management. Kluwer Academic

Press, Norwell, MA.

Turner, J., A. A. Scheller-Wolf, S. R. Tayur. 2008. Scheduling of dynamic in-game advertising. Working

paper. Carnegie Mellon.

Wolsey, L. A. 1998. Submodularity and valid inequalities in capacitated fixed charge networks. Operations

Research Letters 8 119-124.