Embed Size (px)

DESCRIPTION

The Electricity Industry Superannuation Scheme's Annual Report for Financial Year 2010-2011

Citation preview

ANNUAL REPORT 2010 // 2011

2

EISS at a glance…

•Lowadministrationfees

•DirectaccesstopersonalisedservicefromEISSstaff

•Financialadviceoverthephone,orreferralstoprofessionalfinancialplanningservices

•Rangeofinvestmentoptionsandinsurancebenefits

•YoucanstaywiththeSchemewhenyouretire

•Anot-for-profitfund

•Morethan$700minfundsundermanagementat30June2011

•On-lineaccesstoup-to-dateinformationonyourbenefits,insuranceandinvestmentoptions

•Worksitevisitsandretirementplanningseminars-wecometoyou!

2

3

Welcome to EISS’s 2011 Annual Report

Who looks after your money?

As at the 30 June 2011, the Board members were:

Who else works for your retirement?

Statistics

Investments

What more do you need to know?

4

5

7

10

11

13

21

3

TheElectricityIndustrySuperannuationScheme(EISS)isthesuperfundforpeoplewhosupplyelectricitytoSouthAustralia.Thisannualreportletsourmembersknowwhatwehavebeenuptoontheirbehalfinthe2010/2011financialyear.Thisisaformaldocumentanditiswritteninaformalway.Ifyouhaveanyquestionsaboutanythingyoureadhere,giveusaringandwe’lltrytoanswerthem.

Members of this super fund continue to receive fantastic benefits that members of most funds can only dream about, such as:

•DefinedBenefitmembershavebenefitslinkedto their salary, and are protected against poor investment returns.

•Accumulationmembersgettheiradministrationfees paid by their employer, and have a great choice of insurance benefits and investment options.

•Allmembershaveaccesstopersonalisedservice from the EISS staff, financial advice over the phone, referrals to professional financial planning advice, seminars delivered to your workplace,incomestreamsinretirement,theoption to voluntarily increase their super, and Trusteeswhoworkforyou.

TheEISSisoverseenbyaBoard,whoarerequiredbylawtoworkintheinterestsofmembers(withinthe rules of the EISS). The EISS office manages the fundonbehalfoftheBoard,andisalwaysavailabletoanswerquestionsthatyoumighthaveonyoursuper.ThereismoreinfoontheBoardandtheofficestaff elsewhere in the report.

AlotoforganisationsworkwiththeEISStolookafter your money. These include your employer, the fund administrator, investment managers, auditors, lawyers, accountants, doctors, insurers, financial planners.Alotofexpertiseiscalledontomakesurethatyourretirementislookedafterproperly.

Welcome to EISS’s 2011 Annual Report

What do you do if you have questions or concerns?

Contact us. We can’t answer or fix what we don’t know about.

Phone 1300 307 844

Fax (08) 8100 9974

Email [email protected]

Web www.eiss.superfacts.com

Address Level 2, 157 Grenfell St, Adelaide SA 5000

Postal Address GPO Box 4303, Melbourne VIC 3001

Please note that the EISS office is unattended at times. If you wish to discuss something with us, please ring first.

We may be able to sort it out over the phone. If not, we can make an appointment for a face-to-face chat. We can organise workplace or home visits if needed.

4

Report from the Chairman and Executive Officer

As we put the annual report together, financial markets are going through a difficult time. It is always interesting that as a result of financial market stress, we can get to the stage where the share price of companies can routinely change by 3-4% overnight. This sort of volatility is an obvious over reaction, but it shows the skittishness of investors at the moment.

Lookingpastthis,theconservatismoftheElectricityIndustrySuperannuationScheme(EISS)Boardandmanagementhasonceagainprovento be well founded. The investment returns to EISS members are never going to be top of the surveys,butneitherarewelikelytobebottom.Our investment strategy is based on providing members and employers with balanced returns from a diverse range of investments. The return for the year to 30 June 2011 highlights this. 90%ofmembersarewiththedefaultBalancedGrowth Investment option and the return after feesandtaxwas8.10%againsttheindustryaverage(benchmark)of8.20%.AlthoughmarginalIybehindthebenchmarkfortheyear,in light of the enormous volatility in financial marketswearecomfortablewiththisresultanditreflectsthequalityofourfinancialadvisorsandworkundertakenbythescheme’sInvestmentCommittee.

Superannuation Policy

The Government has been consulting widely on its plansforAustraliansuperfunds,andaregulatedlow-cost option that members can access. This process has been somewhat convoluted, and we are currently waiting on the outcomes of the consultation to establish how best to consider responding to recommendations. Atthistime,superfundsarenotrequiredtoofferalow-costoption,andasalways,theBoardwillneed to consider what is in the best interests of members.Ofcourse,Division5memberspaynoadministration fees at all at the moment, so you can’tgetmuchlowercostthanthat.

Board strategy

Inearly2010,theBoardconsideredarangeofdirections for the scheme. The outcome was that itwashighlyunlikelythattheschemewouldeverseektoopenitselftothepublic.Norwasitlikelyin the short term to find another fund to join with that would satisfy the needs of the members to theextentthattheEISSboardandmanagementdoes. So the outcome was to continue on as normal with an emphasis on ensuring that:

•membersfundsweremanagedaseffectively as possible

•employercontributionsweresecureand

•memberswereproperlypreparedforretirement.

To that end, we have been concentrating on educationandadviceformembers.Asanexample,duringlate2010andearly2011,wesetaboutringingupeverymemberover50(about1,000orso)tomakesurethattheyhadstartedplanningforretirement.Somehad,somehadn’t,but all appreciated the reminder that there were decisions ahead that needed to be made.

Who looks after your money?

5

We have also continued to build on our relationship with our two financial planning advice firms.Manyfinancialplannersdon’tunderstandcomplexfundslikeEISS.WeencouragememberstouseeitherMercerorTynanMackenziebecausethey have both built up this understanding through previousworkwithfundmembers.Ifmembersdon’talreadyhaveafinancialadviserthattheyarecomfortable with, then we can refer them to either firmtoseekprofessionalfinancialadvice.

EISSstaffarealsovisitingworksiteswhereverthiscanfitinwithemployersituations.Naturallyifyouwantavisittoyourworksite,pleasecontactthefund and we will try to arrange it.

Administration

Mercer has been with the scheme for many years and continues to grow and develop to be a very professional company that has been doing good workformembers.

Board and Staff

JulieOakleyresignedasanemployerappointedtrusteefollowingstaffchangesatAlintaEnergy.WewouldliketothankJuliaforherworkduringhertimeontheBoard,andwewelcomeRachelSalkeldofAlintaasherreplacement.

Asalways,theBoardandstaffputinalotofworkfor the EISS and the members. The Scheme is run byagroupofthoughtfulhardworkingpeople,andwewouldliketothankthemformakingourjobseasier.

MarkDayChairman of the board

JonHolbrookExecutive Officer

6

As at the 30 June 2011, the Board members were:

Appointed by SA Unions Appointed by members

BobDonnelly Eric LinderDarrylPayne JanetteBettcher

Independent Chairman

Appointed by the Employers

PatrickMakinson Kevin TaylorMarkDay RachelSalkeldPaulWight

7

AllBoardmembersarerequiredbylawtofollowtherulesoftheEISS,aswellasanylawsthatapply.IftheBoardhasanydiscretionundertherules,thenithastoconsiderthebestinterestsofmemberswhenapplyingthatdiscretion.

This is regardless of how they are appointed to theBoard,soemployer-appointedBoardmembershave the same obligations as member-elected Boardmembers.AdecisionoftheBoardrequirestwo-thirdsoftheBoardmemberstobeinfavour.

Training

AllBoardmembersandstaffundertaketrainingtoimprovetheirknowledgeandskillsinareasthatwill be of benefit to the Scheme. The cost of this training is met by the Scheme.

Someexamplesofthetrainingthathasbeentakenare:

•attendingthenationalconferenceoftheAssociationofSuperannuationFundsofAustralia(ASFA)

•ASFAworkshopsandlunches

•Aonedaycourseonthedutiesandresponsibilities of super fund trustees

•theCompanyDirectors’CourserunbytheAustralianInstituteofCompanyDirectors

•Onedayconferencesoninvestments,superannuationissuesandPublicSectorsuperannuation funds

Board meeting attendance

Board Member

Number of meetings held

Number of meetings attended

Mark Day 9 9

Janette Bettcher 9 7

Bob Donnelly 8 6+2Alternate

Eric Lindner 9 7

Patrick Makinson 9 8

Julia Oakley 7 7

Darryl Payne 9 8

Rachel Salkeld 2 2

Kevin Taylor 9 9

Paul Wight 9 8

Aquorumof6BoardmemberswasachievedatallBoardmeetings.

8

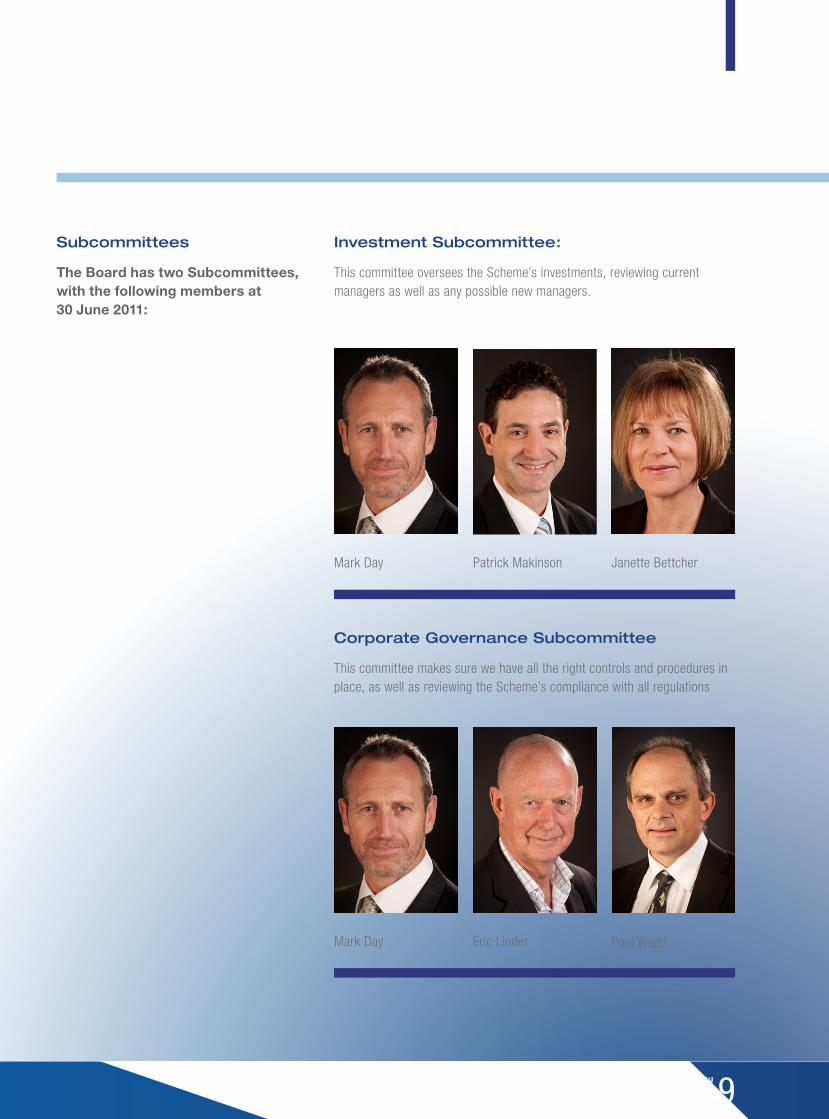

Subcommittees

TheBoardhastwoSubcommittees,withthefollowingmembersat30June2011:

MarkDay Eric Linder

PatrickMakinson JanetteBettcherMarkDay

Investment Subcommittee:

ThiscommitteeoverseestheScheme’sinvestments,reviewingcurrentmanagers as well as any possible new managers.

Corporate Governance Subcommittee

Thiscommitteemakessurewehavealltherightcontrolsandproceduresinplace,aswellasreviewingtheScheme’scompliancewithallregulations

PaulWight

9

MarkElliott DeputyExecutiveOfficer

Lyndall Carpenter Operations Manager

KarenDavey ProjectOfficer

JonHolbrook ExecutiveOfficer

Who else works for your retirement?

Jon,Mark,LyndallandKarenworkfortheBoard,andmakesurethattheSchemeisruninlinewiththeBoard’sdecisionsandpolicies.

Service providers

TheBoardobtainsspecialisthelpandadvicefromthefollowingcompaniesandpeople:

Actuary & Administrator:MercerHumanResourceConsultingPtyLtd

Accountant: SharynLongCharteredAccountants

Investment adviser: JANAInvestmentAdvisersPtyLtd

Legal advisers: DMAWLawyers|MercerLegalPtyLimited

Taxation adviser: KPMG

Auditor: Auditor-General

Insurer: MetLife

Medical advisers:DrGaryHopkinsandDrGrantTschirn

10

Statistics

Membership Statistics

Duringtheyear,themembershipincreased:

Division 2 3 4 5 Total

Members at 30 June 2010

762 295 200 1,899 3,156

Entrants during the year

204 204

Exits during the year

14 17 13 124 168

Members at 30 June 2011

748 278 187 1,979 3,192

Thisincludesmemberswhohavelefttheirjobs,buthavekepttheirsuperintheEISS.Thisisafairlytypicalyear,withthegrowthinDivision5membersoutweighing the retirements among the older defined benefit members.

TheEISSalsopaidpensionsto150members,whohaveretiredandarereceivingaregularincomefromtheScheme.Apensionoptionisavailabletoall members.

Contributions

TheEISSreceivescontributionsfrommembers(frombothaftertaxsalaryandbysalarysacrifice)andfromemployers.Thetotalcontributionsreceivedduringtheyearwere:

Employer $56.8m

Salary Sacrifice member $14.5m

Post tax member $2.3m

TOTAL $73.6m

The employers are paying all the contributions thattheBoardasksfor.TheBoardhastoaimto have enough money in the EISS to pay all benefits. This money is invested separately to the employers,andisheldbytheBoardtopayforyour retirement.

There was also $3.7m rolled into the Scheme from other super funds. You can save money by combining your super, especially as you pay very little in administration fees in EISS.

Statistics

11

Benefits

The Scheme also paid out a lot of benefits during the year, both as lump sums and pensions. The amounts were:

Lump sum benefits $17.2m

Disability pensions $0.2m

Retirement pensions $6.0m

TOTAL $23.4m

Bywayofcomparison,duringthe2009/2010year, benefits totalling $13.1m were paid.

Member Queries

PhonequeriesfrommembersarehandledbytheHelpline(runbyouradministrator),andtheScheme office. The Helpline can help you on all matters, as well as provide financial advice on simple matters over the phone. They have access to the EISS administration data and can resolve mostquestionsveryquickly.TheHelplinetakesabout80%ofallqueries,andanswers90%ofthem on the spot.

They will get help from the EISS office or the administrators(whoknowtheEISSreallywell)ifneedbe.However,ifyouwanttotalktoJon,Mark,LyndallorKarenjustask.

You are also welcome to send us an email at [email protected] answer it within two days, though we may needmoretimeifitisacomplicatedquestion.

Over the year, the Scheme office and the Helpline received3,187queries.

This means that, on average, every EISS member(ortheirfinancialadviser)rang,oremailed, or wrote in about their super. This doesn’tinclude:

•contributions(over100,000separateamounts were recorded)

•benefitpayments(168exitsfromtheScheme)

•outgoingcallsmadeandlettersandemailswritten

Thisaddsuptoalotofactivitytokeepyoursupertickingover.

12

Investments

Summary

TheBoardaimstogetthebestreturnthatitcan,whilekeepingtrackoftheriskthatisbeingtaken.

TheBoardsetsinvestmentobjectivesandastrategy with a long-term view in mind. This strategyinvolvesusing‘growth’assetslikesharesandpropertyaswellas‘defensive’assetssuchasfixedinterestandcash.

The value of investments can move up and down withinvestmentmarkets.Wetrytoreducethemovements as much as we can, but we can and do get negative returns sometimes.

TheBoardselectsprofessionalfundmanagerstoinvest the assets of the Scheme. Each manager is a specialist in the relevant investment sectors, forexampleAustralianshares,andisselectedaftertakingintoaccountadvicereceivedfromtheScheme’sinvestmentadviser.

Investment Philosophy

Background

ItisultimatelytheBoard’sresponsibilitytomakealldecisionsrelatingtotheinvestmentsofthescheme.

TheSchemehasamixofdefinedbenefitandaccumulation liabilities.

Foraccumulationliabilities,theinvestmentriskiscarriedbythemember.Thismeansthatifinvestmentreturnsarepoor,themember’sbalance is directly affected. The Scheme provides amixofinvestmentoptionstoallowmemberstochoosetheriskprofilethatbestsuitstheircircumstances.

However, for defined benefit liabilities, the investmentriskiscarriedbytheemployers.Ifreturns are poor, then the employers have to contribute more to pay for the benefits. The Boardhassoughttheemployers’viewsontheinvestmentriskprofilefortheassetsbackingthedefinedbenefitliabilitiesandwillseekreaffirmation of employer views every five years.

Currently the majority of the liabilities are defined benefit. The sections of the Scheme providing defined benefits are closed to new members, and hence the timeframe over which these benefits will be paid is shortening.

13

Board philosophy - Default and Defined Benefit Investment Pool

In light of its role as custodian for assets supporting benefitsformembers,theBoardconsidersitappropriatetotakeanapproachtoinvestingthescheme’sassetsaimedatloweringinvestmentvolatilitywhilemaintaininganexposuretogrowthassets.

TheBoardwilldiversifyinvestments,bothacrossasset classes and managers, within any constraints imposedbytheassetsizeoftheScheme.

Manager Configuration

TheBoardhasnodeliberatebiastowardsany style of investment management, but will select managers on their perceived ability to add investment value. Manager configuration is determined within, rather than across asset classes, having regard to:

•anydecisionreachedonactivevspassivemanagement

•themeritsofusingaparticularmanager

•theneedforadequatemanagerdiversification

•themanagers’particularskillsintheassetclassinquestion

•theabilitytomonitormanagerseffectivelyandefficiently

Use of derivatives

TheBoarddoesuseforeignexchangeinstrumentstomanagetheriskoffluctuationsintheAustraliandollarforthescheme’soverseasinvestments.Inaddition Investment managers employed by the scheme are permitted to use futures, options and other derivative instruments in accordance with theirparticularRiskManagementStatements.TheBoardexpectsthatoverthelongertermtheuseoftheseinstrumentswillenhancethereturnsand/orreducetheriskoftheScheme.

Use of gearing

TheBoardmayinvestinfundsthatusegearingandleverage,whereappropriate.

Asset Allocation

TheassetallocationsfortheBalancedGrowthoption(whichisalsowherethe assets supporting the defined benefits are invested) at 30 June 2010 and 30 June 2011 were

Asset class Benchmark (%)

Asset Allocation at

30 June 2010 (%)

Asset Allocation at

30 June 2011 (%)

Australian Shares

30.00% 28.7% 29.0%

Overseas Shares

21.00% 18.7% 20.0%

Property 13.00% 12.6% 12.1%

Total Growth Assets

64.00% 60.0% 61.1%

Alternatives 16.00% 17.7% 16.3%

Australian and Overseas Fixed Interest

15.00% 15.4% 15.1%

Cash 5.00% 6.9% 7.5%

Total Defensive Assets

36.00% 40.0% 38.9%

The changes in the asset allocation during the year were due to:

•differentreturnsfromthedifferentassetclasses(forexample,shareshada good year, and property not so good)

•investmentofcontributionsintosharesandalternatives

•reclassificationofacoupleofinvestmentsfromfixedinteresttoalternatives

14

Objectives

TheinvestmentstrategyhasthreeobjectivesagainstwhichtheBalancedGrowthPortfolio’sinvestmentperformance is measured. The objectives and the results are as follows:

Objective Balanced Growth Portfolio Return

Objective return

Exceed the Consumer Price Index by 3% pa over rolling 5-year periods.

3.1% pa 5.9%pa Notmet

Exceed median return in the Super ratings survey over rolling 3-year periods.

1.5%pa 1.0% pa Met

Exceed indexed benchmark portfolio over rolling 3-year periods (before tax).

1.6% pa 2.2% pa Notmet

The EISS did not meet two of its three objectives to 30 June 2011. The last 3 years have been an unusuallydifficulttimeoninvestmentmarkets,withtheglobalfinancialcrisisaffectingallassets.Unfortunately we were not immune from this, though the EISS returns have been more stable than many other funds.

Recent Returns

ThereturnsfromtheBalancedGrowthoptionoverthelast4yearstellthestoryofhowreturnshavebeenaffectedbythepoorreturnsin2008and2009,despitetherecoveryintheAustralianmarket this year:

Year 07/08 08/09 09/10 10/11Over Last

5 YearsOver Last 10 Years

Australian Shares (before tax)

-13.7% -20.3% 13.1% 11.9% 2.4% 7.2%

Overseas Shares (in $A, before tax)

-20.8% -15.7% 7.3% 3.2% -4.6% -3.2%

EISS Balanced Growth option (after tax)

-3.8% -11.8% 9.7% 8.2% 3.3% 4.9%

The investment earnings that are allocated to your account will depend on the division of the Scheme thatyouarein,whichaccountyouarelookingatandinsomecases,whenyoujoinedtheScheme.Thisis because each division has different rules about what is deducted from the declared rates in terms of administrationfeesandtax.Thedeclaredratesthatapplytoyouareshownonyourstatement.

15

2010/11 Financial Year – The Year in Review

Thelastfinancialyearwascharacterisedbyalargeamountofvolatility,witheconomicconditionsgenerallyontheweaksideindevelopedmarketeconomies(DM),contrastingwithmostoftheemergingeconomies(EM)whereconditionswereonthewholemuchstronger.Inflationhasalsobeguntosurgeonthebackofhigherfoodandenergyprices,withtheUSquantitativeeasingprogramfeedingthroughtohigherassetpricesandaggriavatinginflationinthealreadystrongEM.AsaconsequencemanyoftheEMcountrieshavebeenraisinginterestratesasacounter-measure,whiletheDMcentralbankshaveheldratesatrecordlowlevelsthroughmostoftheyearwiththeexpectationthatthepoorstateoftheeconomywilloffsetfoodandenergyandkeepinflationundercontrol.

Sentimentinbondmarketshasfluctuatedwildlyat times, with temporary signs of recovery causing bond yields to sell-off, followed by renewed buying of safe harbour bonds, while the bonds of debt ladenperipheralEuropeanmarkets(includingGreece,PortugalandIreland)havebeenconsistently sold through the year as European authorities dithered about the best means to support them. The big fear is that defaults by these countries will force a crisis for the European bankingsystemwhichisaholderoflargevolumesofthesecountries’sovereigndebt.Theratingsagencies have reacted by downgrading these to below investment grade, and in the case of Greece the current rating of CCC is only one notch above‘default’.

Outside of Europe economic conditions have alsobeentough,withtheearthquake,tsunamiand nuclear plant triple whammy causing the Japanese economy to shift into reverse in the first quarterof2011,whileAustraliawasbesetbythemassivefloodsinQueenslandandVictoria.BothoftheseeventshaveresultedinnegativeGDPgrowthratesforthefirstquarter,andexpectationsofaslowrecoveryinthesecondquarter.TheAustralianeconomycurrentlyenjoysalowrateofunemploymentcomparedtomostotherDMeconomies, but despite this consumer confidence remains at very low levels with an emphasis on reducingdebtlevelsattheexpenseofspending.This trend has led to a two paced economy, withtheminingstatesofWesternAustraliaandQueensland growing strongly, while the non-mining states have been lagging.

Inthemarkets,Australiansharesfinishedtheyear up 11.9%, whilst Global shares also ended theyearinpositiveterritory.Globalsharemarketsin local currency terms rose by nearly 27%. Overthe12months,theAustraliandollarroseagainst all currencies to record post-float highs, boosted by high interest rates, high commodity prices, and a much improved balance of trade. This currency strength offset a large part of the gains,andresultedinunhedgedglobalequityinvestorsreturningonly3.2%fortheyear.Despiteeconomic conditions deteriorating through the year, share earnings were solid especially in the USAandGermanywhereincreasedexportstoemerging countries supported sales. However domestic based securities did not fare as well with high levels of unemployment weighing on consumer sentiment as well as their desire to spend.Resourcestockscontinuedtobenefitfromthe high growth rates in China and prices rose by 18.2%overtheyearcomparedtoIndustrialstockswhich rose by 9.2%.

16

Despite12monthshavingpassedsincethelastannual comments were made, surprisingIy little haschanged.Equitymarketsareconsideredtobe cheap based on forward earnings, and once againthemoodinthemarketshasbeencautious,withtherecoveryinthedevelopedmarketsseemingly stalled, and with the authorities in a numberofkeyemergingmarketssuchasChina,BrazilandIndiatryingtoslowtherateofgrowthand reduce inflation which has been rising at anuncomfortablerate.Additionalgovernmentregulatory change and financial reform is also of concern. There is also focus on the ability of governments in debt laden economies in Southern Europe to implement appropriate austerity measures, The most recent measures to aid some of the countries under most stress may defuse some of the concern as these allow for a faster response by European authorities to future debt crises. Hopefully these may help soothe investor nervousness.

InthePropertysectorListedPropertyTrusts(LPTs)againunderperformedUnlistedPropertyTrusts.ListedPropertyTrustsreturned5.8%overtheyear,whilstUnlistedPropertydelivereda more stable return, adding 9.1% over the year, with stable capitalisation rates, and valuations increasingonlyonthebackofrentalincreases.

Hedged Global bonds returned 6.9% over the year,whilstAustralianbondsreturned5.6%.Australiangovernmentbondsunderperformedglobalbonds,astheRBAraisedratesfurthertocombat incipient inflation. Global bonds returns werealsoboostedbythe‘carry’asAustralianmoneymarketratesremainsubstantiallyhigherthanglobalmoneymarketrates.Theoutlookfornon-governmentbonds(credit)continuedto improve with very low defaults, and spreads contracted further in the first half of the year, before reversing course in 2011 under the influenceofnervousnessregardingtheGreekdebtcrisis,aswellasweakereconomicdata.These issues also contributed to a strong rally in the price of government bonds that rallied to exceptionallylowlevelsasinvestorssoughtthesafetyandliquidityofUsandGermangovernmentbonds.

17

Investment Managers

The Scheme used the following investment managers during the year, each of which is invested in a particular investment sector. The figures shown are the percentages of total assets invested with each manager at 30 June.

Australian Shares: 2011 2010

Concord Capital 5.4% 5.8%

Cooper Investors 9.7% 9.5%

DimensionalFundAdvisors 2.5%

Mellon 3.8%

Solaris 9.2% 9.2%

TribecaInvestmentPartners 2.3%

Overseas Shares:

Marathon 3.1% 3.1%

JANA 14.7% 15.3%

Wellington 2.1%

Direct Property:

AMP 4.5% 4.7%

Dexus 4.5% 4.5%

Lend Lease 3.1% 3.3%

Alternatives:

AuroraInvestmentManagement 2.7%

Bentham 4.4% 4.3%

GMO 2.5% 2.7%

Macquarie 1.1% 3.7%

Aurora 2.8%

Fauchier 2.9% 2.5%

JANA 2.8% 1.6%

Wellington 2.4%

Australian & Overseas Bonds:

AFIF 4.4% 3.1%

ColonialFirstState 4.3% 2.9%

JANA 6.4% 6.7%

Cash:

BankDeposits 0.7% 1.7%

ING 5.0%

Perennial 5.5%

Macquarie 1.2% 1.3%

18

Defensive

GrowthInvestment options

These are the options that your accounts can be invested in. Thesearen’tgenerallyavailable for your employer defined benefit.

Defensive

Conservative Growth

Objective

Thisoptionaimstoexceedtheconsumerpriceindexby2%paoverthreeyears,andtoexceedthereturnonitsbenchmarkportfolioover3years.

Strategy

This option is around 30% invested in growth investments, and hence has a moderately conservativeinvestmentriskprofile.

Investment Risk

Conservativeinvestmentstrategywithexpectedstable, but low returns.

Investment Timeframe:

1-3 years.

Risk Profile

Low; the chance of a negative return is 2 in 20 yearsandreturnsarenotexpectedtoshowlargeswings.

This option is most suited to

Members who prefer stable but moderate returns over the short to medium term.

Management Fees

0.4%(deductedfromthereturnscreditedtoyouraccount).

Cash

Objective

Thisoptionaimstoexceedtheconsumerpriceindexandsimilarlyinvestedfundsoverrollingannual periods.

Strategy

Thisoptionisfullyinvestedinshorttermfixedinterest investments, and has a very conservative investmentriskprofile.

Investment Risk

Generally a secure way to invest. However cash investments tend to earn the lowest rate of return in the longer term.

Investment Timeframe:

Nominimumtimeframe.

Risk Profile

Verylow;notlikelytohaveanegativereturn.

This option is most suited to

Membersseekingtominimisetheirinvestmentriskovertheshortterm.

Management Fees

0.2%(deductedfromthereturnscreditedtoyouraccount).

19

High Growth

Defensive

Growth

Balanced Growth

Objective

Thisoptionaimstoexceedtheconsumerpriceindexby3%paoverfiveyears,andtoexceedthereturnonitsbenchmarkportfoliooverthreeyears.

Strategy

This option is around 70% invested in Growth assets, and hence has a moderately aggressive investmentriskprofile.

Investment Risk

This option follows an investment strategy which hasabalanceofriskandreturn.

Investment Timeframe:

5years(minimum)

Risk Profile

High;thechanceofanegativereturnis5in20years and returns may show large swings in the short term.

This option is most suited to

Members who want reasonable medium term returns and can put up with large variations in the short term.

Management Fees

0.8%(deductedfromthereturnscreditedtoyouraccount)

High Growth

Objective

Thisoptionaimstoexceedtheconsumerpriceindexby4%paoverfiveyears,andtoexceedthereturnonitsbenchmarkportfoliooverfiveyears.

Strategy

This option is fully invested in growth investments, andhasaveryaggressiveinvestmentriskprofile.

Investment Risk

ThisoptionhasmorevolatilitythantheBalancedGrowth option and is designed to produce higher return over the long run. However the increased variationinreturnsisalsolikelytoproducetheoccasional negative return.

Investment Timeframe:

5to7years(ormore).

Risk Profile

High; the chance of a negative return is 6 in 20 years and returns may show large swings in the short term.

This option is most suited to

Members who want higher returns in the long term and can put up with large variations in the short term.

Management Fees

0.9%(deductedfromthereturnscreditedtoyouraccount).

20

Account-based Pensions

Lump sum benefits can be transferred to an account-based pension on retirement.

Insurance Benefits

Allmembersareeligibleforbenefitsondeathordisability, that can help you or your dependants if anything goes wrong. The Scheme office can help ifyouhaveanyquestions.Moreinformationcanbefoundinyourmemberbooklet.

What do members contribute?

Thelevelofmembercontributionsisflexible.Generally,memberscanchooseanymultipleof1.5%ofsalary.Memberscanalsochoosetotemporarilystopcontributing.

FullbenefitsfromDivisions2,3and4areachieved by contributing, on average, the standard contribution rate. This is, generally, 6% of salary, butcanbebetween5%and6%inDivision3.Anyvoluntarycontributions(AVCs)arereturnedtoyouwith interest in addition to the other benefits.

Division5membersarenotrequiredtocontribute,butmaymakecontributionsiftheywish.

Contributionsaredeductedfrommembers’salaries each pay day.

The Scheme is also able to accept salary-sacrifice member contributions. These contributions are madefrommembers’salariesbeforeincometaxispaid.However,notallemploymentarrangements allow salary-sacrifice - members needtocheckwiththeiremployer.

Contributionscanalsobemadeforamember’sspouse,whichmayhavetaxadvantages.

What are the benefits?

Scheme members belong to one of five sub-Schemes.

Open to new members

The Accumulation Scheme (Division 5)

Providesbenefitsbasedoncontributionsplusinvestment earnings. Members can choose the level of their insurance cover.

Closed sub-Schemes

The Lump Sum Scheme (Division 2)

Provideslumpsumbenefitsbasedonbothinvestment earnings and salary levels.

The Pension Scheme (Division 3)

ProvideslifetimepensionsbasedonfinalsalaryandindexedwithCPI.Alumpsummaybepaidonvoluntaryseparationorretrenchment.ProvidentAccountA(alsopartofDivision3)provideslumpsum benefits based on investment earnings.

The RG Scheme (Division 4)

Provideslumpsumbenefitsbasedonbothinvestment earnings and salary levels.

What more do you need to know?

21

How are the benefits paid for?

Themoneytopayforbenefitscomesfrommembercontributions,employercontributionsandinvestmentearnings.

Member contributions are set by the member according to their wishes.

EmployercontributionsaresetbytheBoardafterreceivingadviceontheamountsrequiredtopayforthebenefits.EmployersarerequiredtopaycontributionsundertheRulesoftheEISS.Thesecontributions are monitored by an independent actuary(anexpertinthesematters).Theactuaryprojectsthelikelybenefitpayments,salarygrowthand investment returns to estimate employer contributions, and reviews this annually or as required.

What insurance does the Scheme have?

TheBoardtakesoutinsuranceagainstthedeathand invalidity of Scheme members to protect the Schemeagainstthoserisks.AlsotheSchemepaysforinsurancetoprotecttheBoardandthe Scheme against the financial effects of any “honestmistakes”thatmightoccurintherunningof the Scheme.

How is personal information handled?

The Scheme holds personal information about members, such as name, address, date of birth,salary,taxfilenumberandsooninorderto provide member super benefits. Members should realise that this personal information may be disclosed, when necessary, to the Scheme Administratorandprofessionaladvisers,insurers,Government bodies, employers and other parties.

TheBoardhasadoptedaPrivacyPolicythatsetsoutinmoredetailthewaymembers’personal

informationishandled.ForacopyofthePrivacyPolicypleasecontacttheScheme’sPrivacyOfficeron1300307844orfax(08)[email protected].

Minimum Benefits

AllbenefitspaidfromtheSchemearecheckedtomakesurethattheyareatleastequaltotheminimumrequiredundertheSuperannuationGuarantee legislation. Members will always receive their mandatory 9%. However, this is a minimum, not in addition to other benefits. GenerallyinDivision2,3and4benefitsarewortha lot more than 9% of salary.

What Information Is available To Members?

The first stop for information on the Scheme should be the website at www.eiss.superfacts.com

Current information available to members includes:

• AnnualMemberStatements • AnnualReportstoMembers • Member’sBooklets.

Members are also entitled to access the Scheme Rules,theAnnualReporttotheTreasurer(whichincludes the full statistics, financial statements andtheauditor’sreports),theactuary’sreportsand the investment policy statement.

Information sheets and brochures are available onanumberofsubjects.TheBoardiscurrentlyupdatingboththeMemberBookletsandtheinformation sheets.

TheBoardalsoissuesnewsletterstokeepmembers up-to-date.

Ifmemberswouldliketoreceiveanyofthesedocuments, or need more information about the Schemeorbenefits,pleaserefertotheScheme’swebsite.Ifyoucan’tfindwhatyouneedthere,please contact the Scheme Office.

What do you do if you have questions or concerns?

Contact us. We can’t answer or fix what we don’t know about.

Phone 1300 307 844

Fax (08) 8100 9974

Email [email protected]

Web www.eiss.superfacts.com

Address Level 2, 157 Grenfell St, Adelaide SA 5000

Postal Address GPO Box 4303, Melbourne VIC 3001

Please note that the EISS office is unattended at times. If you wish to discuss something with us, please ring first.

We may be able to sort it out over the phone. If not, we can make an appointment for a face-to-face chat. We can organise workplace or home visits if needed.

22

How Do You Make A Complaint?

Mostqueriesandproblemscanbesortedoutoverthephone.Weaimtogetbacktoyouwithin2workingdays(thoughitmaybetoaskformoretime). We are happy to provide a written response if you want one via email or letter.

If you are not satisfied with the response to a queryyouhavemadetotheScheme,youneedtosendcomplaints(inwriting)to:

The Complaints Officer

Electricity Industry Superannuation Scheme

Level2,157GrenfellStreet,

ADELAIDESA5000

TheBoardwillexamineallwrittencomplaintswithin5weeksofreceiptandmakeadecisionwithin90days.PleasebeassuredthatallwrittencomplaintswillbepassedtotheBoard.

Complaints not dealt with to your satisfaction can be referred to the Superannuation Complaints Tribunal(SCT).TheSCTisthegovernmentbodycreated to resolve disputes in the superannuation industry,andcanbecontactedon1300780808.

Financial Details

ThetablesbelowsummarisetheScheme’smainfinancialtransactionsfortheyearended30June2011.TheauditoftheSchemeisexpectedtobecompletedinOctober2011andnoqualificationsareexpectedtobeimposedbytheauditor.

23

Change In Net Assets Over The Year

$'000

Net market value of assets available to pay benefits as at 1 July 2010 640,878

PLUS

Income

Member contributions 2,358

Employer contributions 71,189

Transfers from other funds 3,708

Netinvestmentincome 56,684

Other income 441

TOTAL 134,380

LESS

Expenditure

Benefitspaid,etc 22,992

Insurance premiums 721

Otherexpenses 1,948

Taxation 10,449

TOTAL 36,110

EQUALS

Net market value of assets available to pay benefits as at 30 June 2011 739,148

Balance Sheet

Assets

Investments 737,901

Other assets 3,404

TOTAL 741,305

LESS

Current Liabilities

Benefitspayable 0

Other liabilities 2,157

TOTAL 2,157

EQUALS

Accumulated funds as at 30 June 2011 739,148

24

contacting the scheme

stre

eta

ddre

ss//

Level2,157GrenfellStreet,AdelaideSA5000

post

ala

ddre

ss//

GPOBox4303,MelbourneVIC3001

phon

e//1300307844

fax//0881009974

emai

web//

ww

w.e

iss.

supe

rfac

ts.c

om