Embed Size (px)

Citation preview

- CA Ravi Kumar Somani

Review of Audited FinancialStatements, Year End adjustment

entries

1

2

Coverage

Balance SheetIncome &Expense

statement

Systems &Controls

TransitionalAspects ProceduralReporting

3

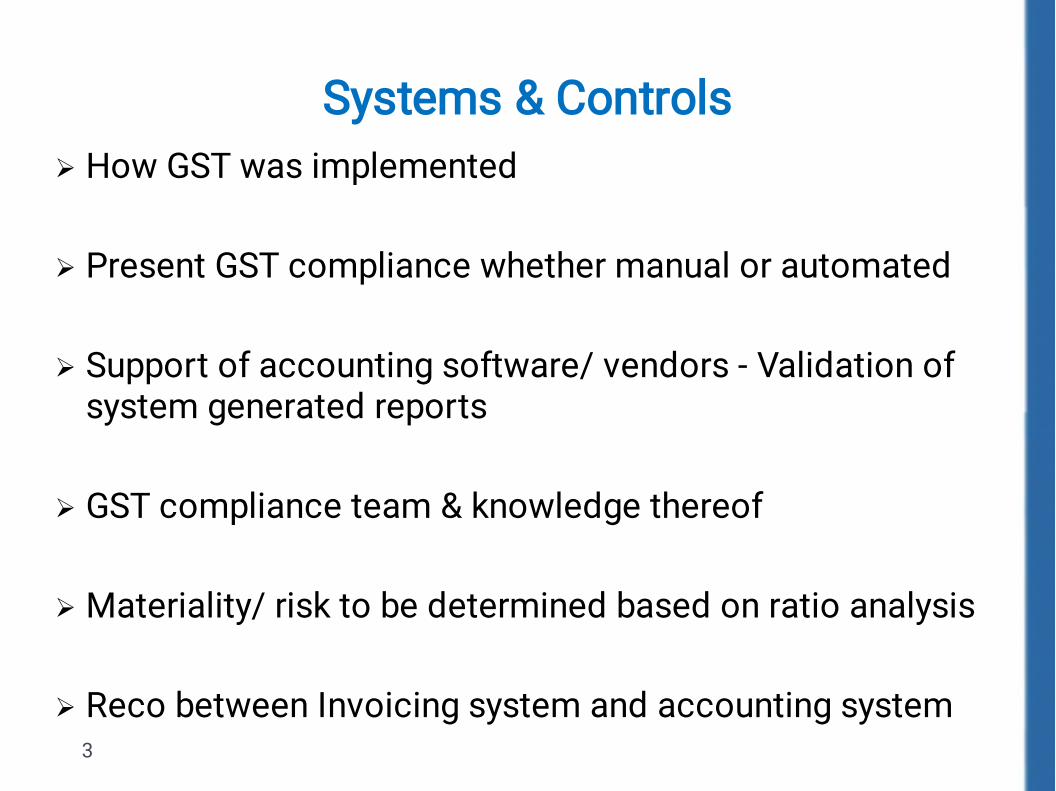

Systems & Controls

How GST was implemented Present GST compliance whether manual or automated Support of accounting software/ vendors - Validation ofsystem generated reports GST compliance team & knowledge thereof Materiality/ risk to be determined based on ratio analysis Reco between Invoicing system and accounting system

Balance Sheet

4

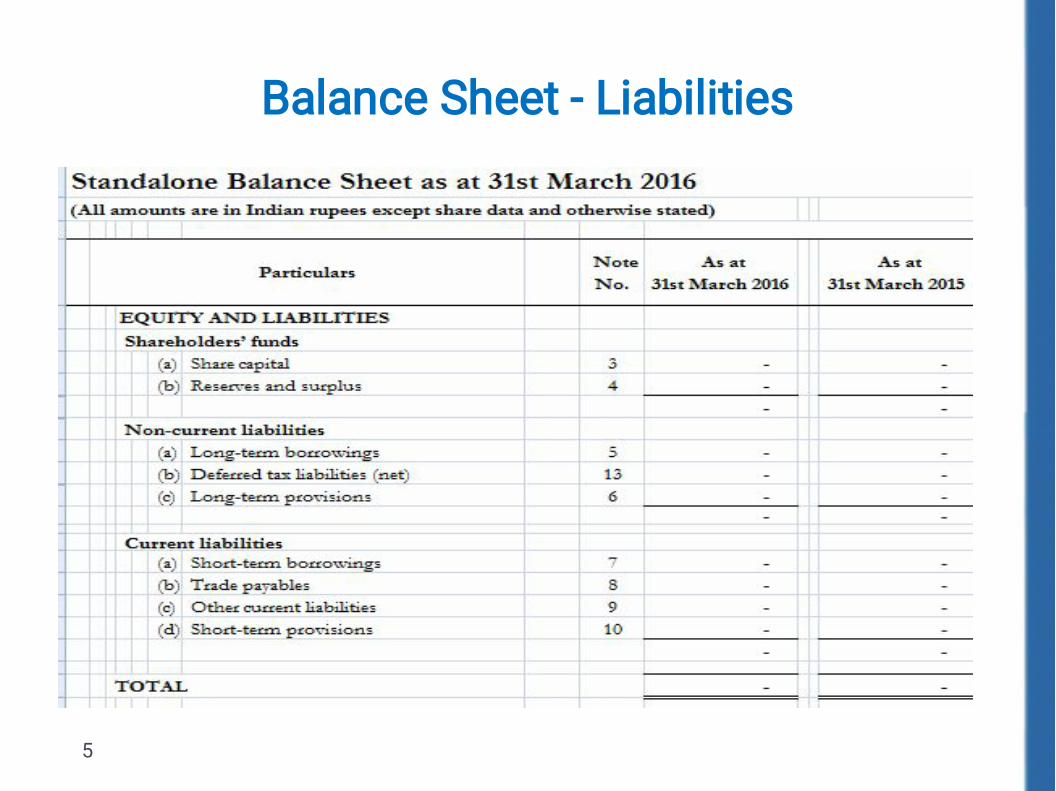

Balance Sheet - Liabilities

5

Impact on Equity

6

Transactions purely in money do not have impact on GST; Implication due to change in equity (Mergers &Acquisitions) Notes to share capital provide details of the shareholderswith more than 5%; Related Party transactions and its implications thereof. Unsecured loans vis-à-vis taxation on advances

Impact on Liabilities

7

•

•

•

•

•

Other long term liabilities:Security deposits are to be included in taxable value ifadjusted against consideration. Mobilization advances whether in the nature ofdeposits – For goods/ services

Trade Payables:GST Reversal on long dues.Working capital blockage on long advances.Tax implication due to vendor non-compliances.

Impact on Liabilities

8

•

•

•

•

Other Current Liabilities:Customer Advances - Early payment of GST &adjustment at the time of invoicing.Employees, debtors, creditors adjustment accountsReimbursements not in the nature of pure agentknocked off in the balance sheetTDS Payable

Review of Liabilities

9

•

•

•

•

•

•

Duties and Taxes:Whether present accounting system allows toextract reports for each registration separatelyMatching of GST accounting CGST records withSGSTReview of tax utilization entries passed in books ofaccounts vis a vis Electronic liability ledgerAccounting of RCM entriesBlocking/removal of redundant tax codes.Entry for advance received / paid

Review of Liabilities

10

•

•

•

•

Key Ratio’s:Non-compliance vendors / Total vendorsTax paid in cash / Total tax liability;Tax liability/ Turnover;Total Tax/ Total taxable value;

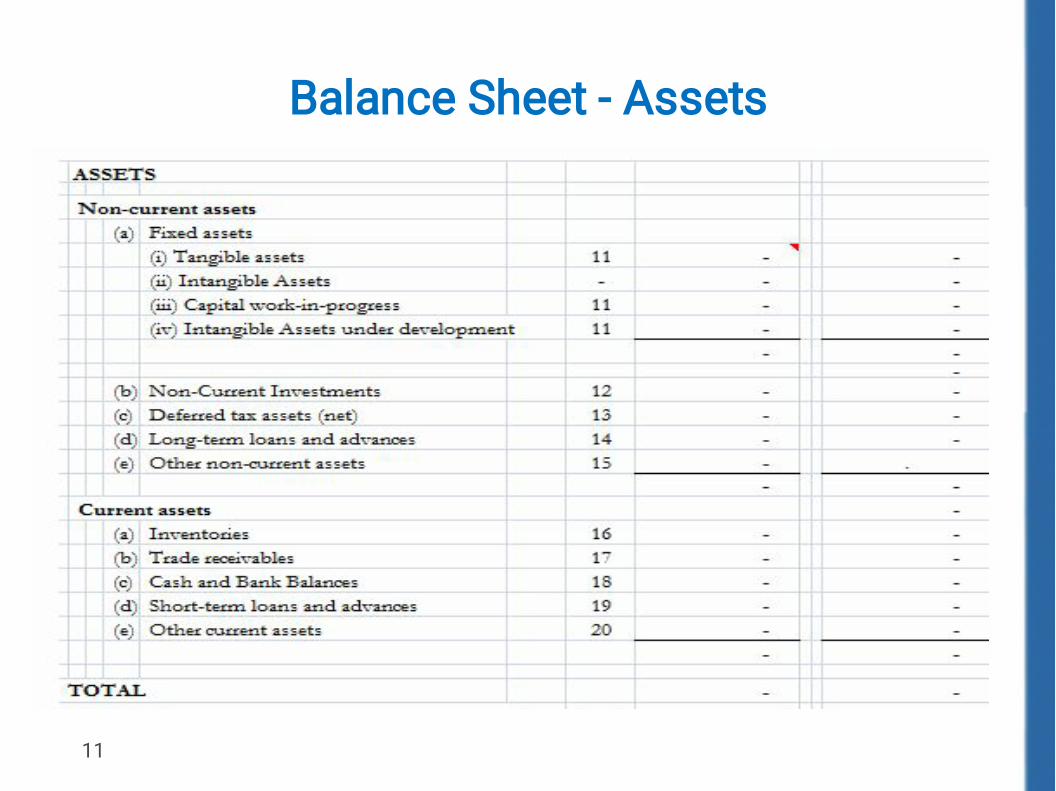

Balance Sheet - Assets

11

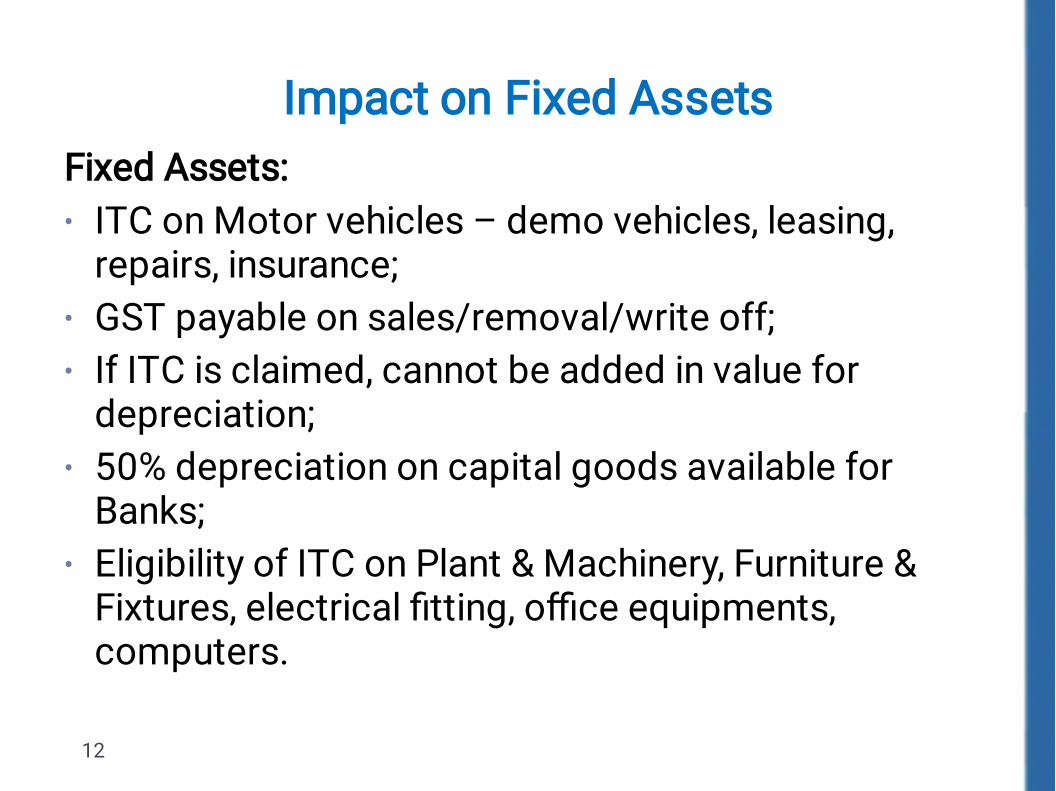

Impact on Fixed Assets

12

•

•

•

•

•

Fixed Assets:ITC on Motor vehicles – demo vehicles, leasing,repairs, insurance;GST payable on sales/removal/write off;If ITC is claimed, cannot be added in value fordepreciation;50% depreciation on capital goods available forBanks;Eligibility of ITC on Plant & Machinery, Furniture &Fixtures, electrical fitting, office equipments,computers.

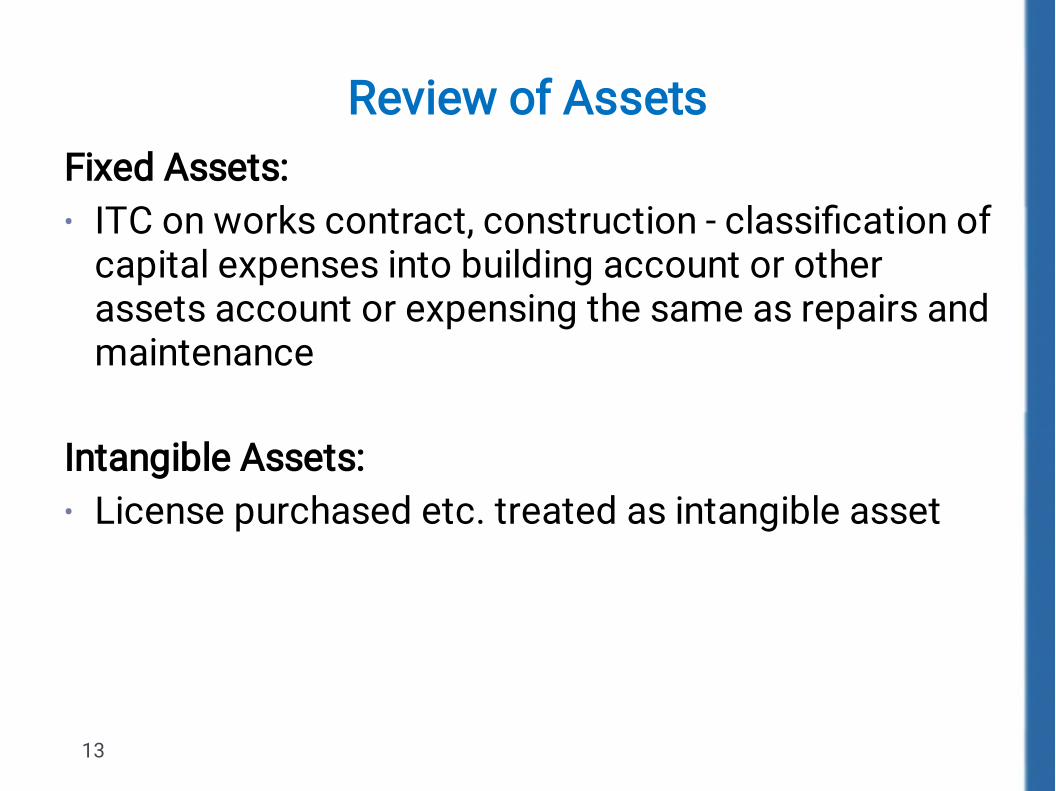

Review of Assets

13

•

•

Fixed Assets:ITC on works contract, construction - classification ofcapital expenses into building account or otherassets account or expensing the same as repairs andmaintenance

Intangible Assets:License purchased etc. treated as intangible asset

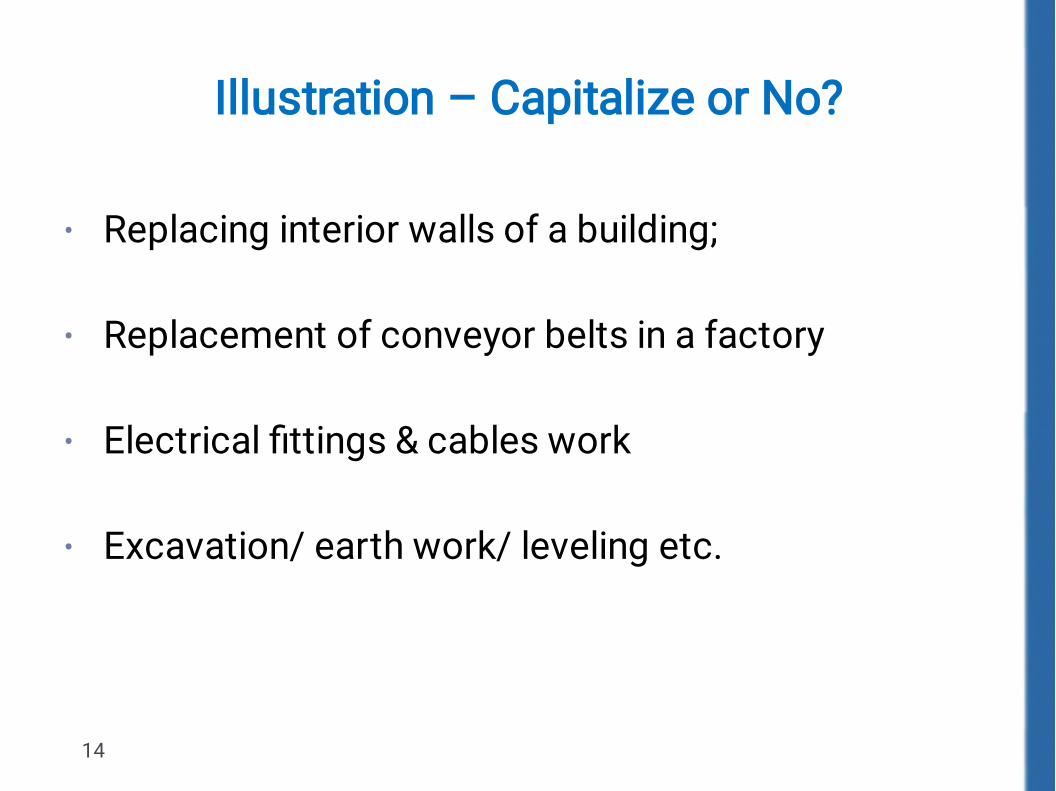

Illustration – Capitalize or No?

14

•

•

•

•

Replacing interior walls of a building; Replacement of conveyor belts in a factory Electrical fittings & cables work Excavation/ earth work/ leveling etc.

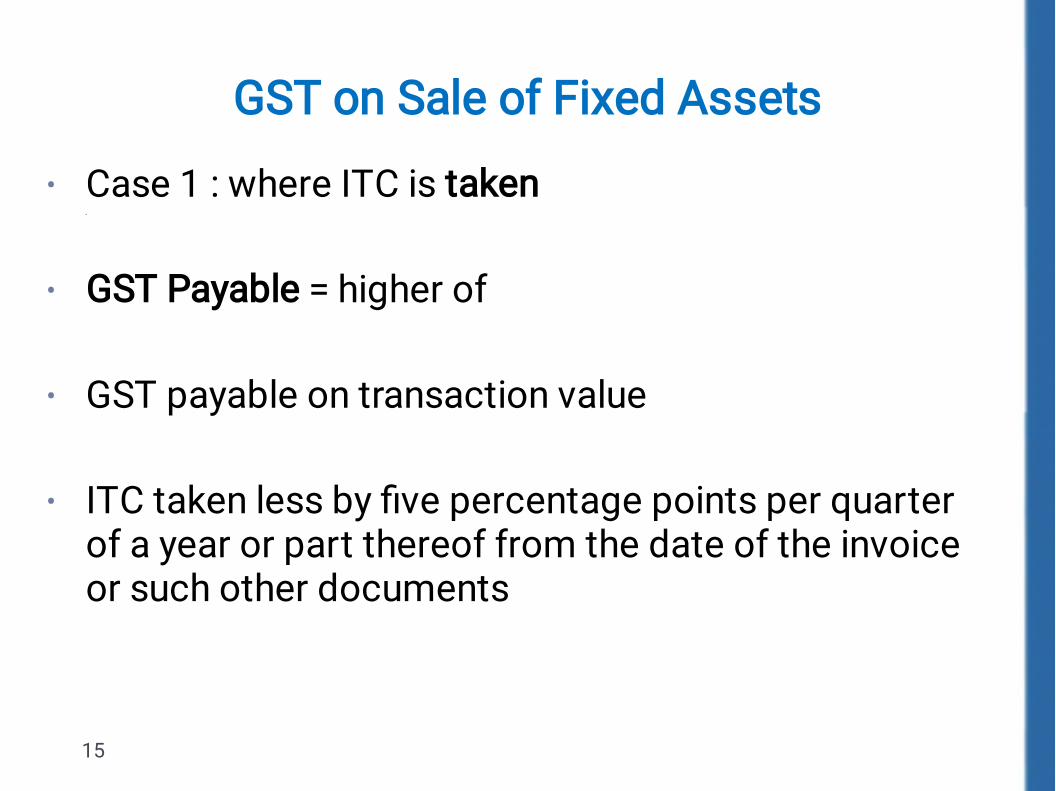

GST on Sale of Fixed Assets

15

•

•

•

•

Case 1 : where ITC is taken GST Payable = higher of GST payable on transaction value ITC taken less by five percentage points per quarterof a year or part thereof from the date of the invoiceor such other documents

GST on Sale of Vehicles

16

•

•

•

No ITC is taken on purchase of vehicles – Section17 (5)

Whether it is supply? Maharashtra AAR, in case of CMS Info Systems Ltd– it is supply!

Rate of GST on Vehicles

17

•

•

•

GST = same as that of new vehicle From 13th October 2017, Not No. 37/2017-CentralTax (Rate), a relief was given to exempt 35% of theGST payable on supply of used motor vehiclesprovided:Supply is undertaken before 1st July 2017.

Registered person who has purchased the MotorVehicle prior to 1st July, 2017 and has not availedcredit of excise duty, VAT or any other taxes paidon such vehicles.

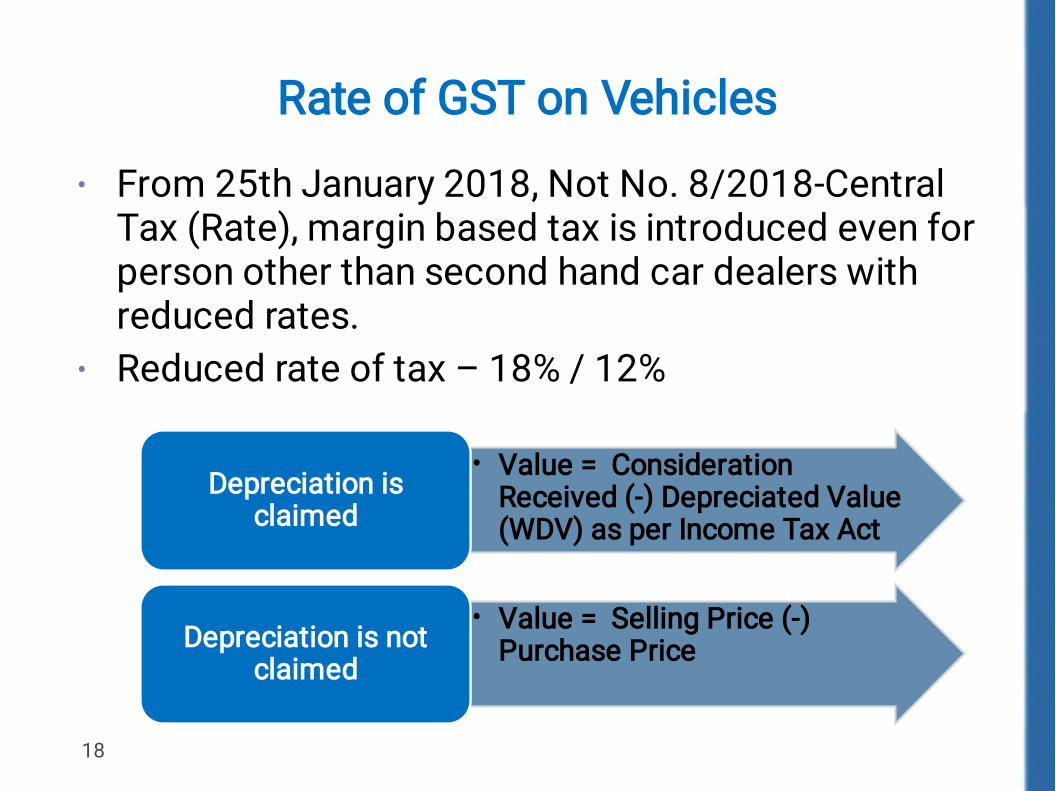

Rate of GST on Vehicles

18

•

•

From 25th January 2018, Not No. 8/2018-CentralTax (Rate), margin based tax is introduced even forperson other than second hand car dealers withreduced rates.Reduced rate of tax – 18% / 12%

• Value = Consideration

Received (-) Depreciated Value(WDV) as per Income Tax Act

Depreciation isclaimed

• Value = Selling Price (-)Purchase PriceDepreciation is not

claimed

Impact on Current Assets

19

•

••••

•••

•

Inventories:If written off/lost/stolen/gifted/removed as samples,etc. whether ITC is to be reversed – Sec. 17(5)Classification of WIP whether inputs or capital goods;Job work movement;Movement of inventory o/s the state;FOC imports

Trade Receivable:

Customer AdvancesDebtors ageing reportTax implication on customers due to GST non-compliances,Review of customer master

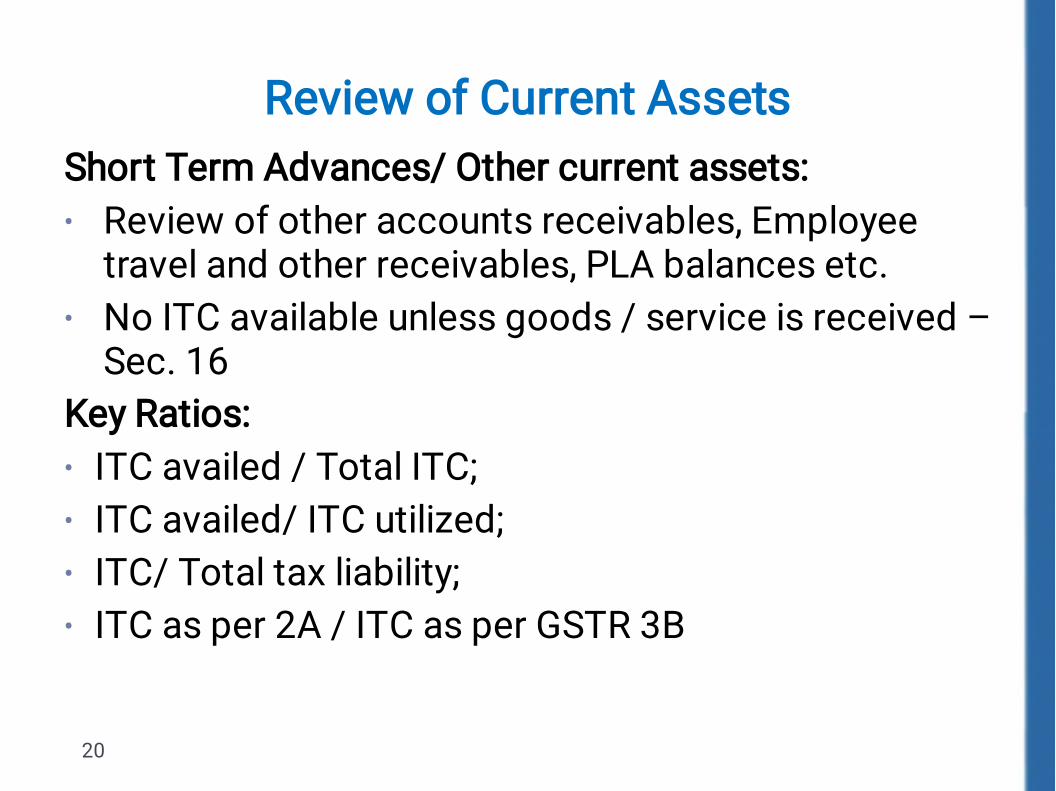

Review of Current Assets

20

•

•

•

•

•

•

Short Term Advances/ Other current assets:Review of other accounts receivables, Employeetravel and other receivables, PLA balances etc.No ITC available unless goods / service is received –Sec. 16

Key Ratios:ITC availed / Total ITC;ITC availed/ ITC utilized;ITC/ Total tax liability;ITC as per 2A / ITC as per GSTR 3B

21

Income & Expense Statement

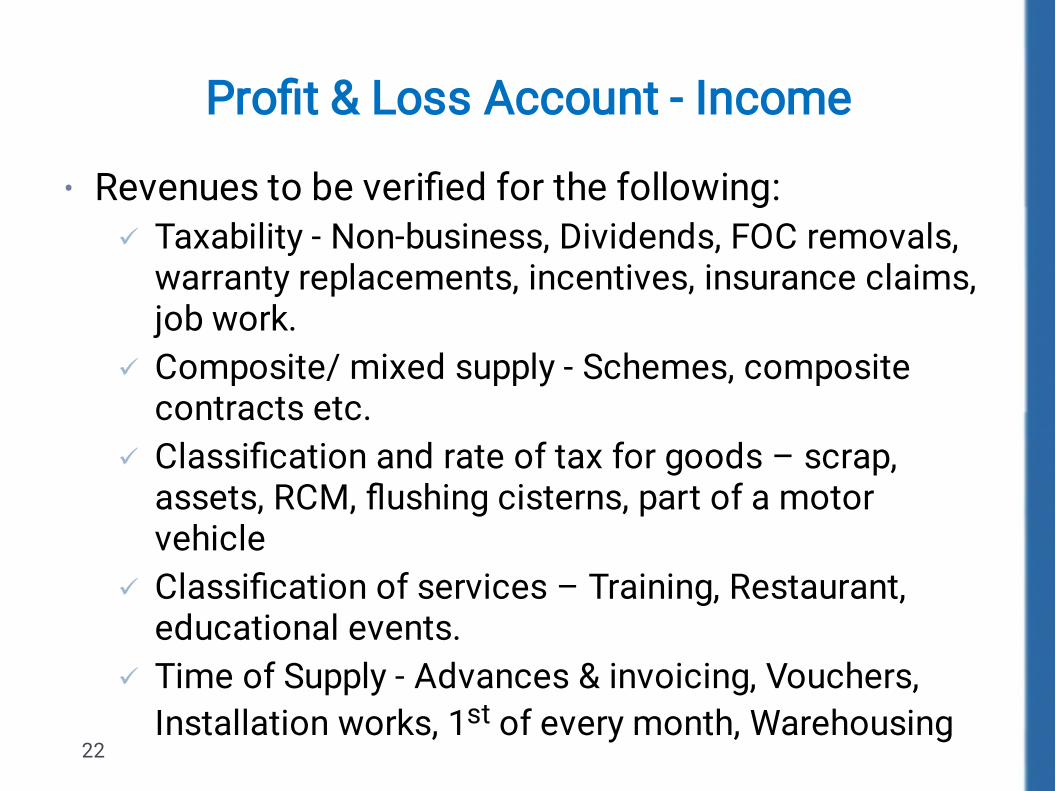

Profit & Loss Account - Income

22

•

Revenues to be verified for the following:Taxability - Non-business, Dividends, FOC removals,warranty replacements, incentives, insurance claims,job work.Composite/ mixed supply - Schemes, compositecontracts etc.Classification and rate of tax for goods – scrap,assets, RCM, flushing cisterns, part of a motorvehicleClassification of services – Training, Restaurant,educational events.Time of Supply - Advances & invoicing, Vouchers,Installation works, 1st of every month, Warehousing

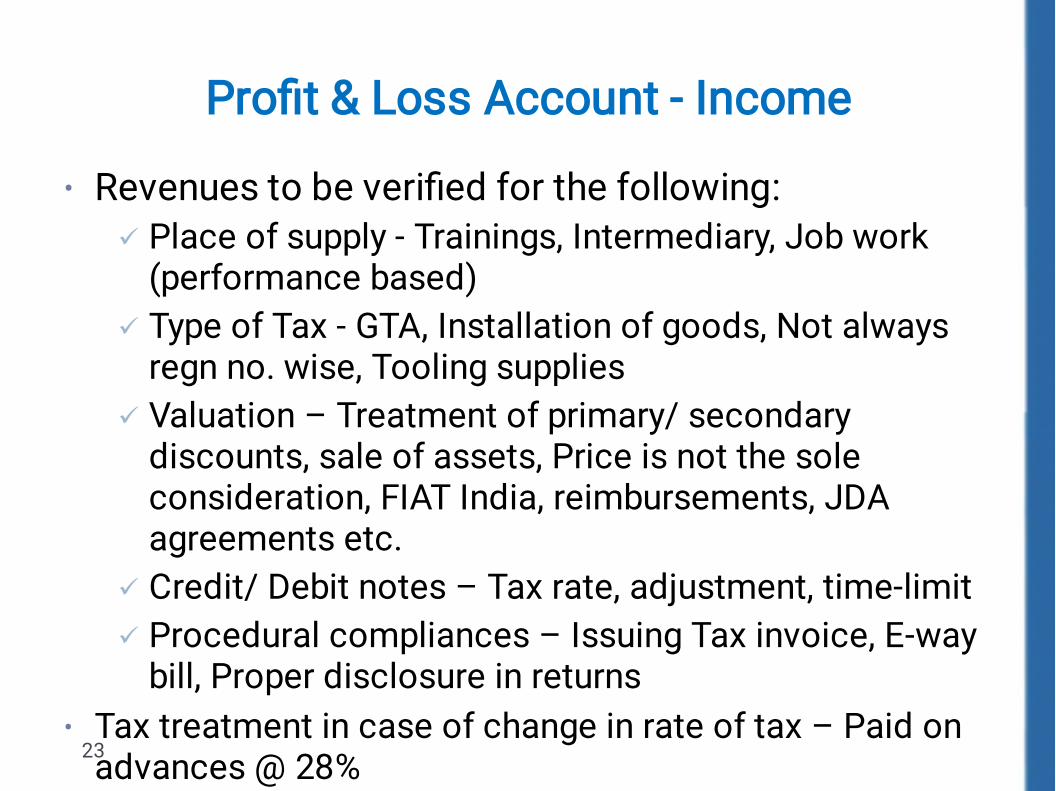

Profit & Loss Account - Income

23

•

•

Revenues to be verified for the following:Place of supply - Trainings, Intermediary, Job work(performance based)Type of Tax - GTA, Installation of goods, Not alwaysregn no. wise, Tooling suppliesValuation – Treatment of primary/ secondarydiscounts, sale of assets, Price is not the soleconsideration, FIAT India, reimbursements, JDAagreements etc.Credit/ Debit notes – Tax rate, adjustment, time-limitProcedural compliances – Issuing Tax invoice, E-waybill, Proper disclosure in returns

Tax treatment in case of change in rate of tax – Paid onadvances @ 28%

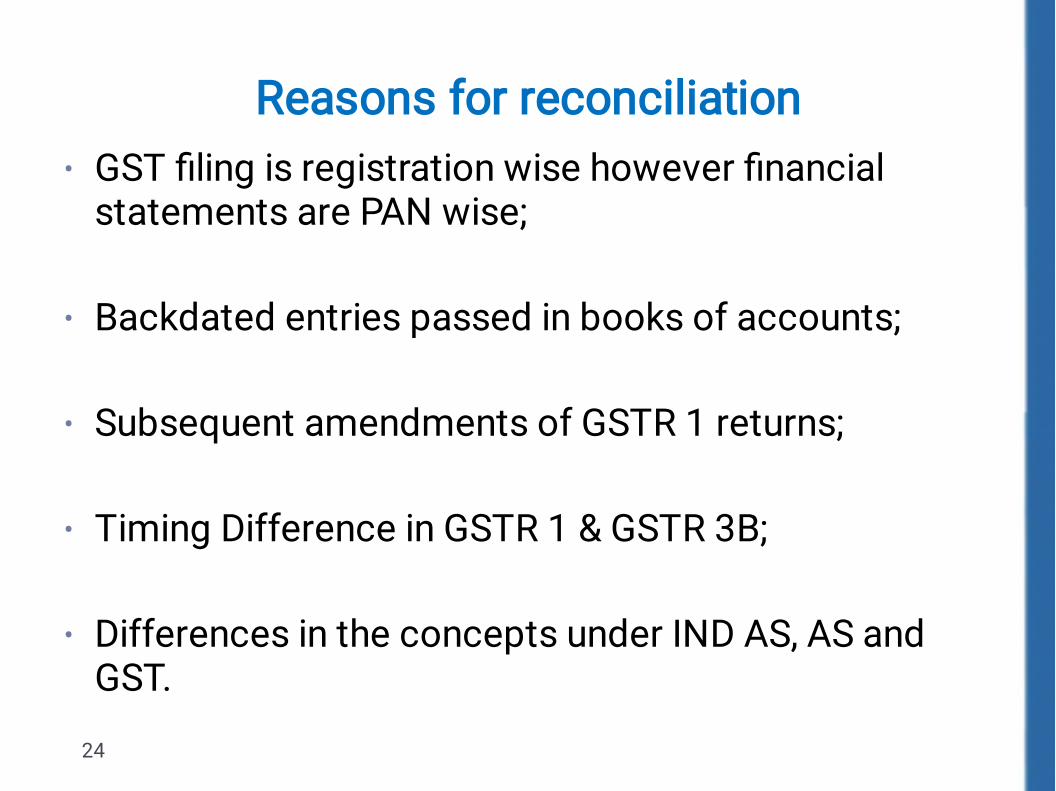

Reasons for reconciliation

24

•

•

•

•

•

GST filing is registration wise however financialstatements are PAN wise; Backdated entries passed in books of accounts; Subsequent amendments of GSTR 1 returns; Timing Difference in GSTR 1 & GSTR 3B; Differences in the concepts under IND AS, AS andGST.

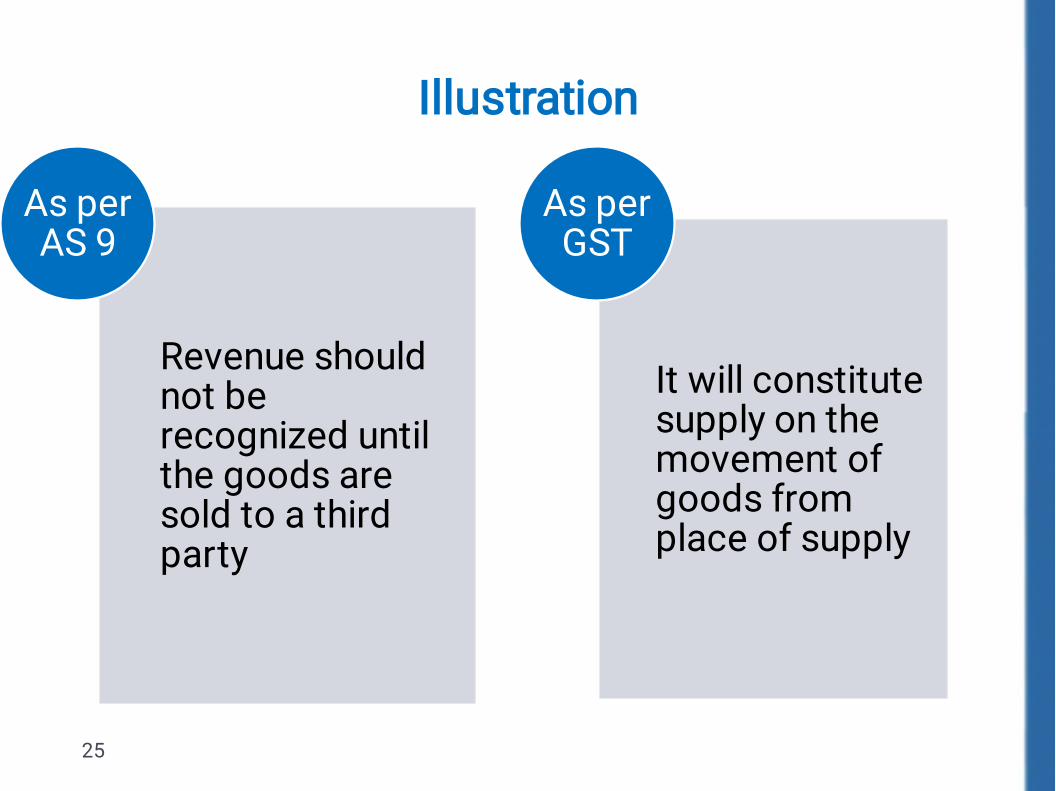

Illustration

25

Revenue shouldnot berecognized untilthe goods aresold to a thirdparty

As perAS 9

It will constitutesupply on themovement ofgoods fromplace of supply

As perGST

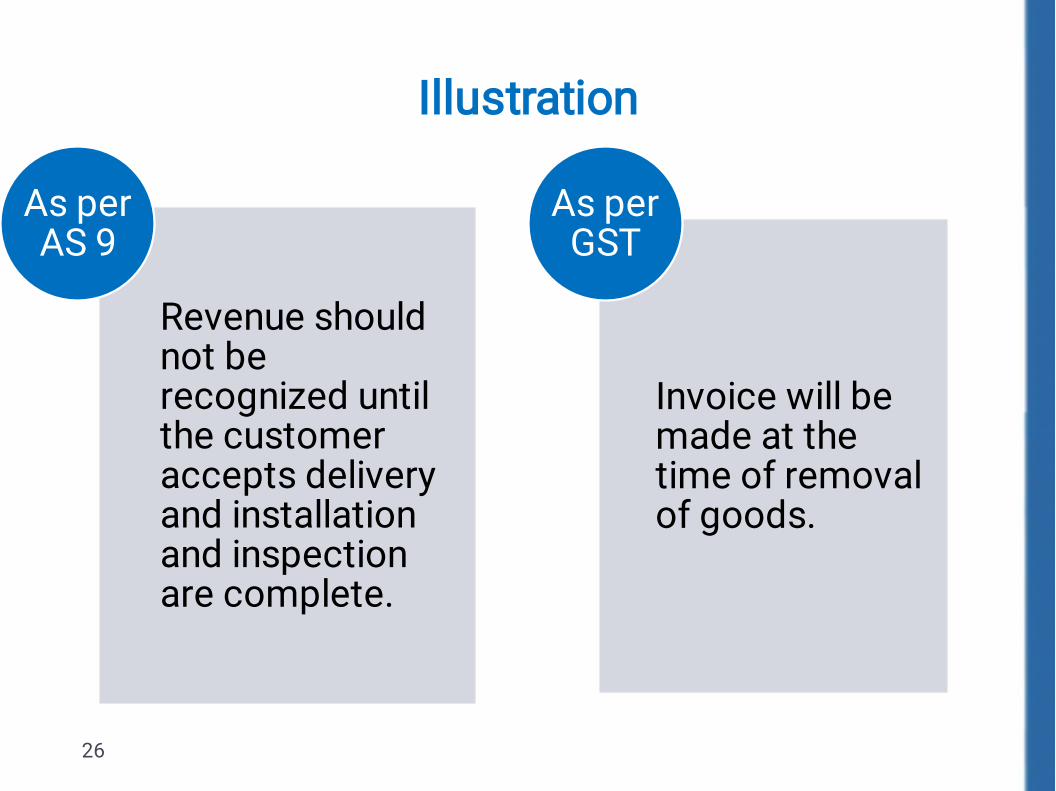

Illustration

26

Revenue shouldnot berecognized untilthe customeraccepts deliveryand installationand inspectionare complete.

As perAS 9

Invoice will bemade at thetime of removalof goods.

As perGST

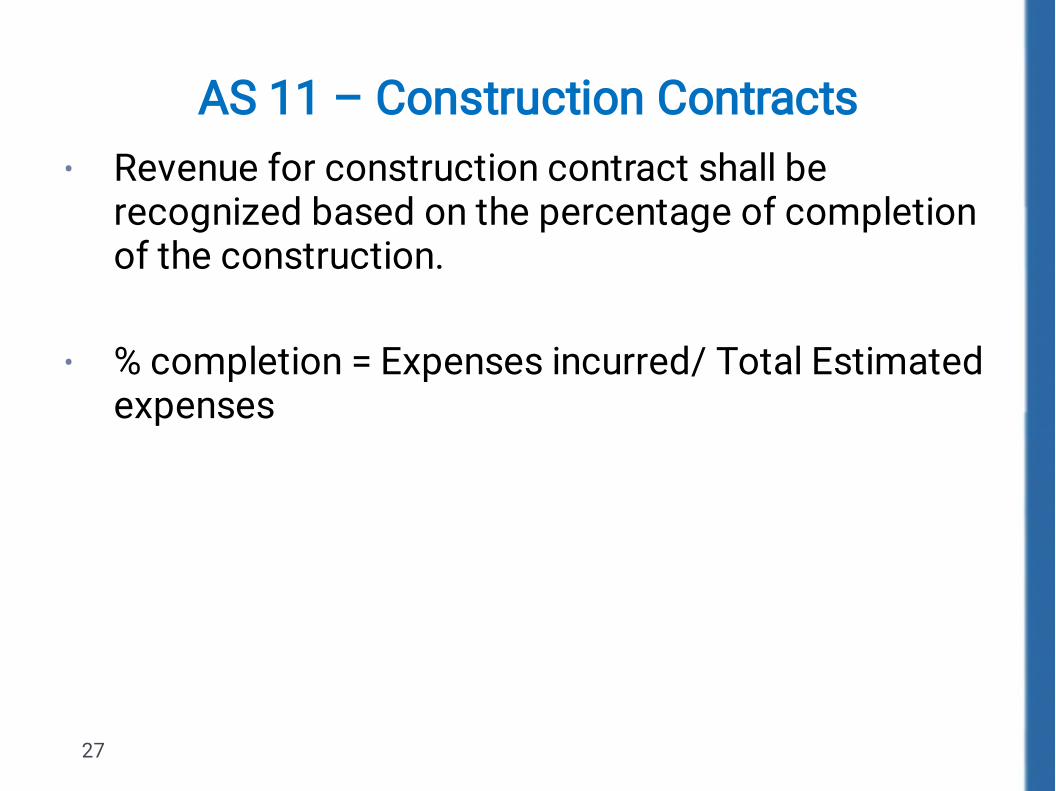

AS 11 – Construction Contracts

27

•

•

Revenue for construction contract shall berecognized based on the percentage of completionof the construction. % completion = Expenses incurred/ Total Estimatedexpenses

Profit & Loss Account - Income

28

•

•

•

•

•

Two way reconciliation from Books to returns and vice-versa - Adequate data in returns; Outward supply reconciliation - Books vs computationsheets v/s GSTR 3B; Reconciliation of outward supplies GSTR 3B and GSTR 1; Electronic cash ledger v/s Tax paid as per returns/ books Reco of ERP reports to the Books of accounts

Profit & Loss Account - Income

29

•

•

•

•

Reconciliation with E-way bill reports; Reconciliation of job work movements & its returns; Reconciliation of exports with shipping bill data; Reconciliations of refunds eligible, claimed, rejected andsanctioned.

Review of GSTR 1

30

•

•

•

•

•

Purchase return disclosed as deemed supplies;GSTR 1 gives the details of stock transfers / crossbillings on the distinct personsHSN summary gives the details of other incomessuch as sale of fixed assets, Debits/ penaltiescollected from the customers, Incomes credited tothe expenses in TB, etc..It helps identifying duplicate sales made from thedocuments and reconciliation of the sales withbooksDebtors can be cross verified from the advancesreceived.

AS 17 – Segment Reporting

31

•

•

Segment Reporting is about reporting statements ofvarious verticals. To analyse inter billing since section 25(4) –provisions of distinct persons to be checked.

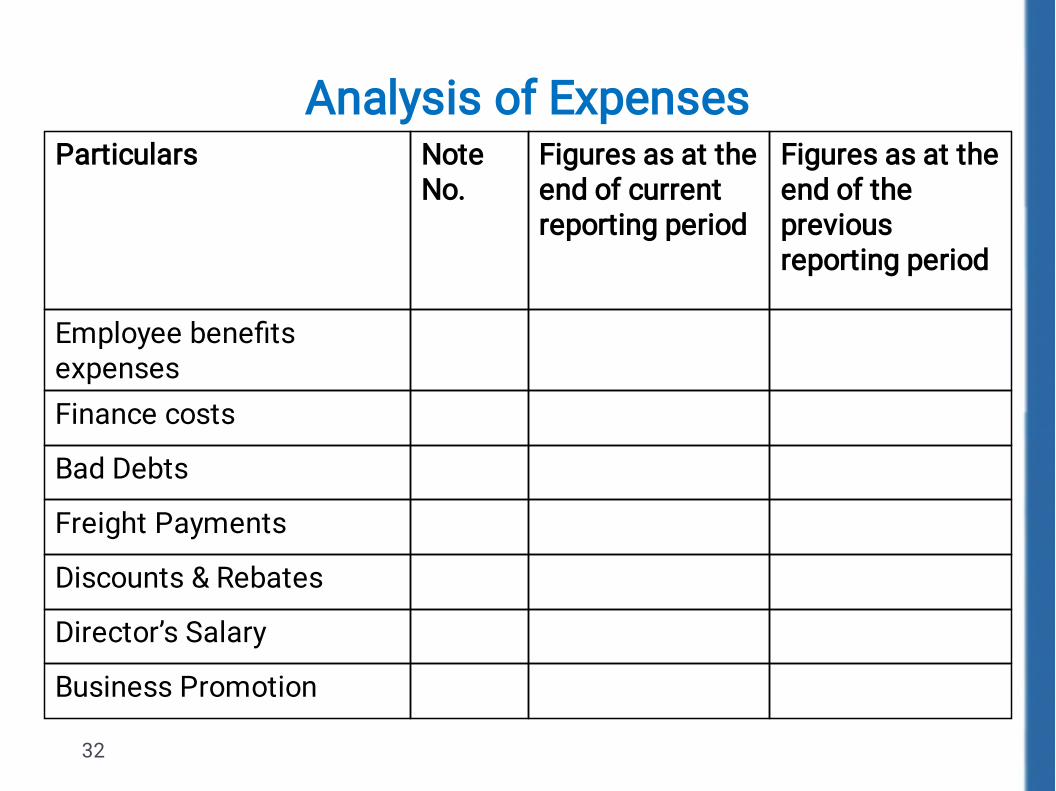

Analysis of Expenses

32

Particulars NoteNo.

Figures as at theend of currentreporting period

Figures as at theend of thepreviousreporting period

Employee benefitsexpenses

Finance costs

Bad Debts

Freight Payments

Discounts & Rebates

Director’s Salary

Business Promotion

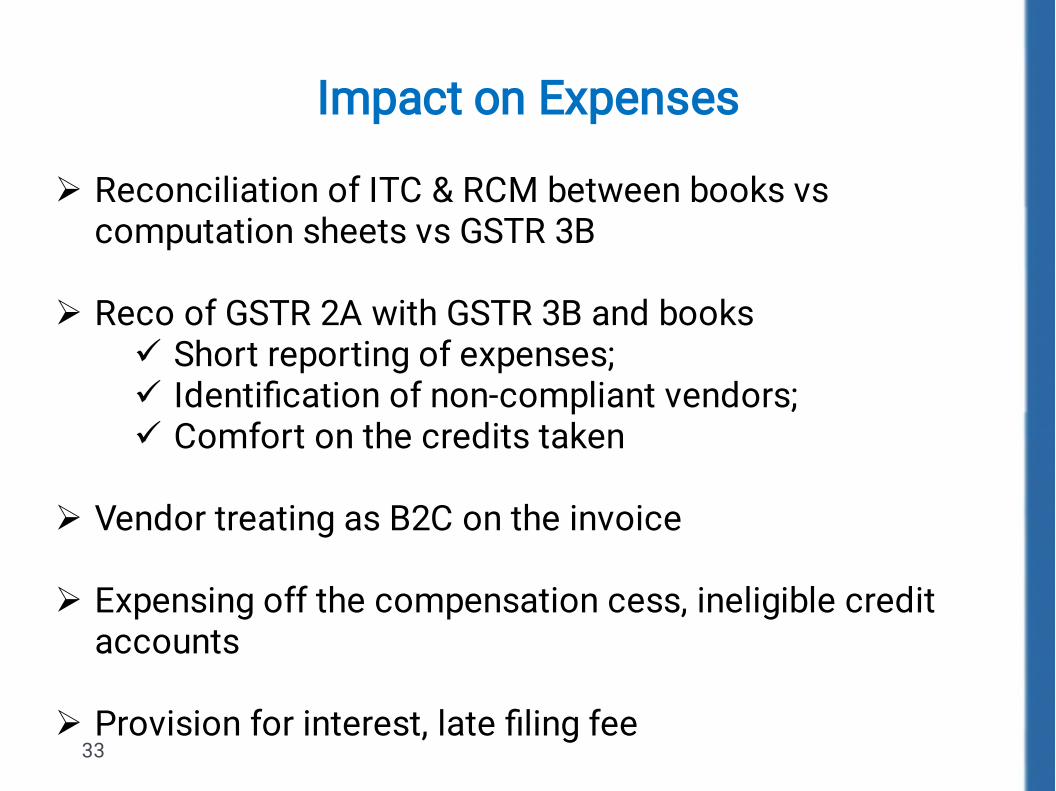

Impact on Expenses

33

Reconciliation of ITC & RCM between books vscomputation sheets vs GSTR 3B Reco of GSTR 2A with GSTR 3B and books

Short reporting of expenses;Identification of non-compliant vendors;Comfort on the credits taken

Vendor treating as B2C on the invoice Expensing off the compensation cess, ineligible creditaccounts Provision for interest, late filing fee

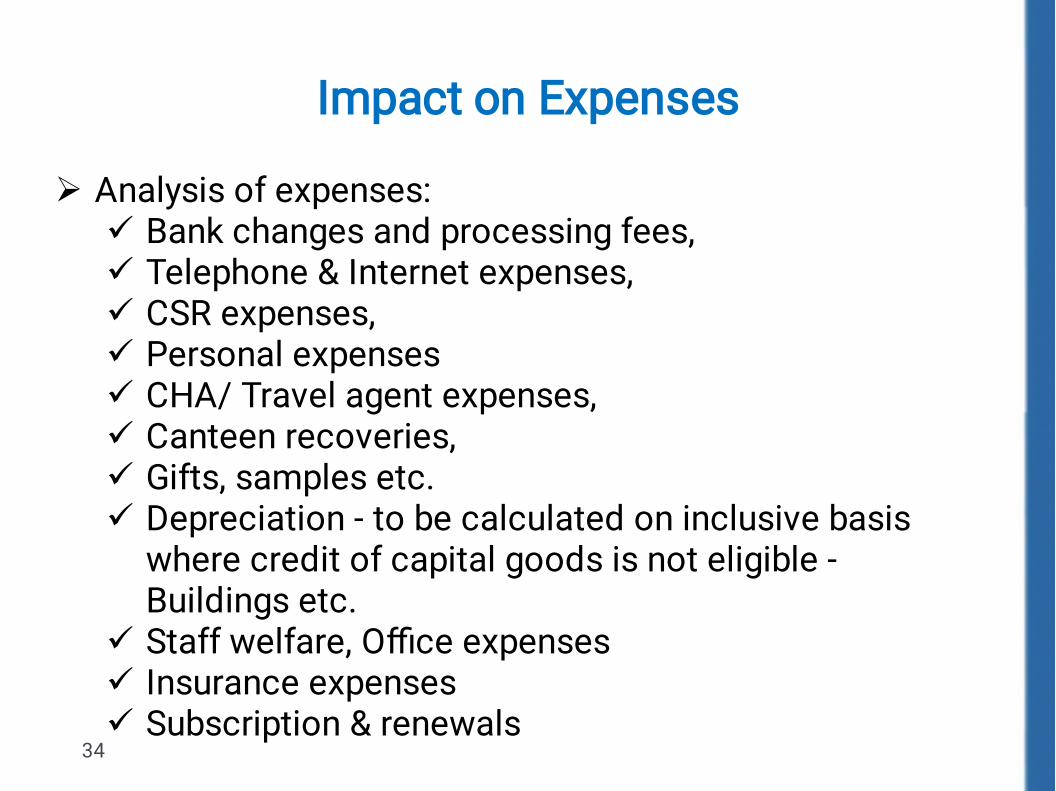

Impact on Expenses

34

Analysis of expenses:Bank changes and processing fees,Telephone & Internet expenses,CSR expenses,Personal expensesCHA/ Travel agent expenses,Canteen recoveries,Gifts, samples etc.Depreciation - to be calculated on inclusive basiswhere credit of capital goods is not eligible -Buildings etc.Staff welfare, Office expensesInsurance expensesSubscription & renewals

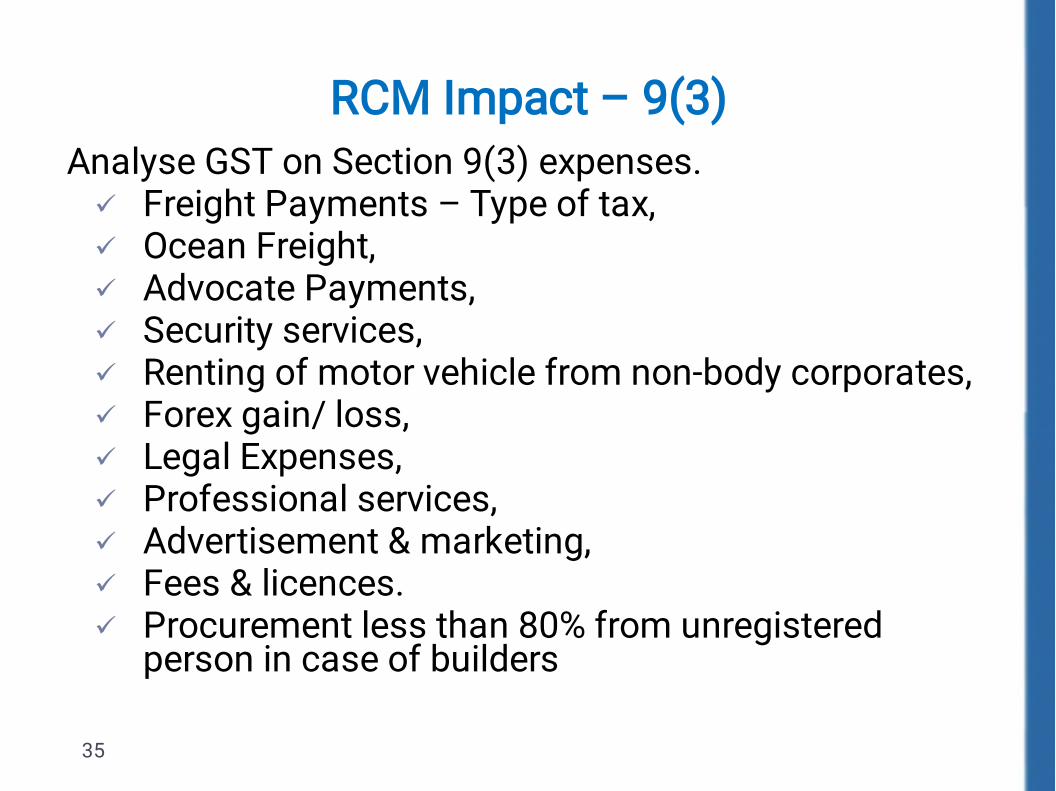

RCM Impact – 9(3)

35

Analyse GST on Section 9(3) expenses.Freight Payments – Type of tax,Ocean Freight,Advocate Payments,Security services,Renting of motor vehicle from non-body corporates,Forex gain/ loss,Legal Expenses,Professional services,Advertisement & marketing,Fees & licences.Procurement less than 80% from unregisteredperson in case of builders

Impact on expenses

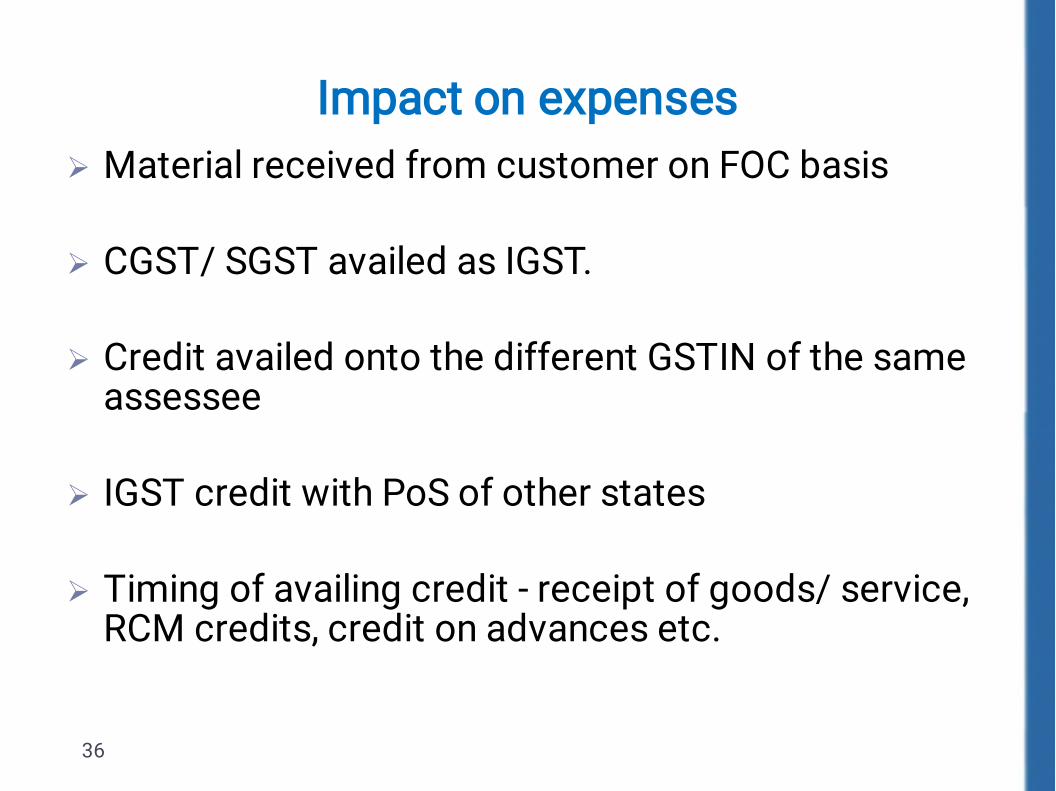

36

Material received from customer on FOC basis CGST/ SGST availed as IGST. Credit availed onto the different GSTIN of the sameassessee IGST credit with PoS of other states Timing of availing credit - receipt of goods/ service,RCM credits, credit on advances etc.

Impact on expenses

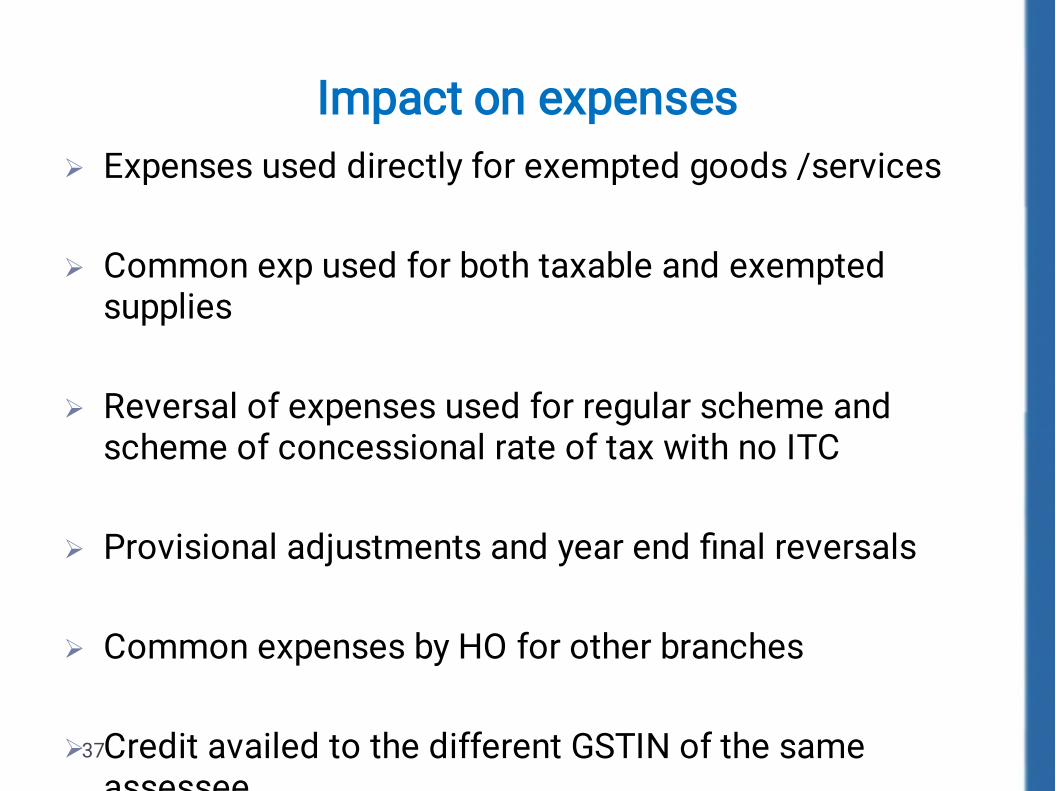

37

Expenses used directly for exempted goods /services Common exp used for both taxable and exemptedsupplies Reversal of expenses used for regular scheme andscheme of concessional rate of tax with no ITC Provisional adjustments and year end final reversals Common expenses by HO for other branches Credit availed to the different GSTIN of the sameassessee

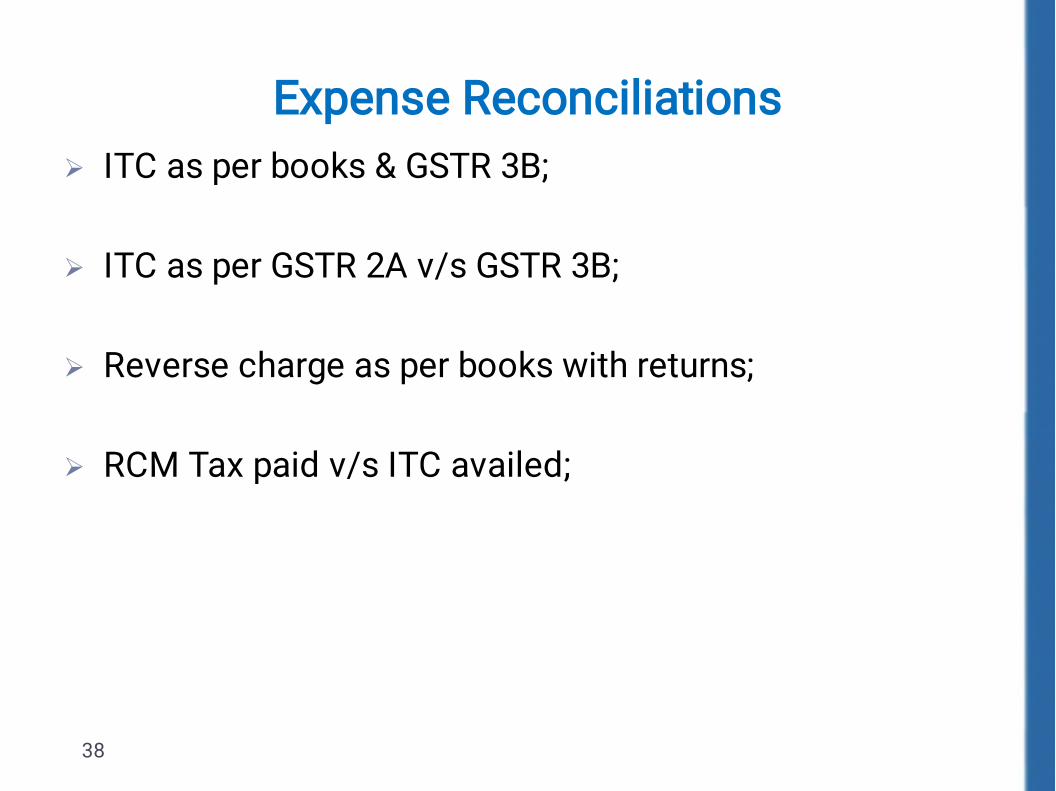

Expense Reconciliations

38

ITC as per books & GSTR 3B; ITC as per GSTR 2A v/s GSTR 3B; Reverse charge as per books with returns; RCM Tax paid v/s ITC availed;

Transitional aspects

39

40

Transitional Aspects

Filing status of TRAN 1 – Timing of availing TRAN credit Transfer of closing balance as per last returns service tax,excise, VAT returns in TRAN-1 Proper documentation, certification, stock statement forcredit taken on stocks Verification of the expenses underlying transferredcredits Tax treatment in case of Education cess, SHEC, KKC,SBC, NCCD, clean energy cess

41

Important Year end Action Points

Cross charge to related/ distinct persons; Review of ITC availed with actual vendor invoices; E-way bill compliance & reconciliation; ITC distribution under ISD; Reversal of common ITC; Various reconciliations between books, GSTR 1, GSTR 3B,E-way bill etc.

42

Important Year end Action Points

Issuance of Debit notes & credit notes; Tax entries for various adjustments made in the year endand also various adjustments made while filing annualreturns;

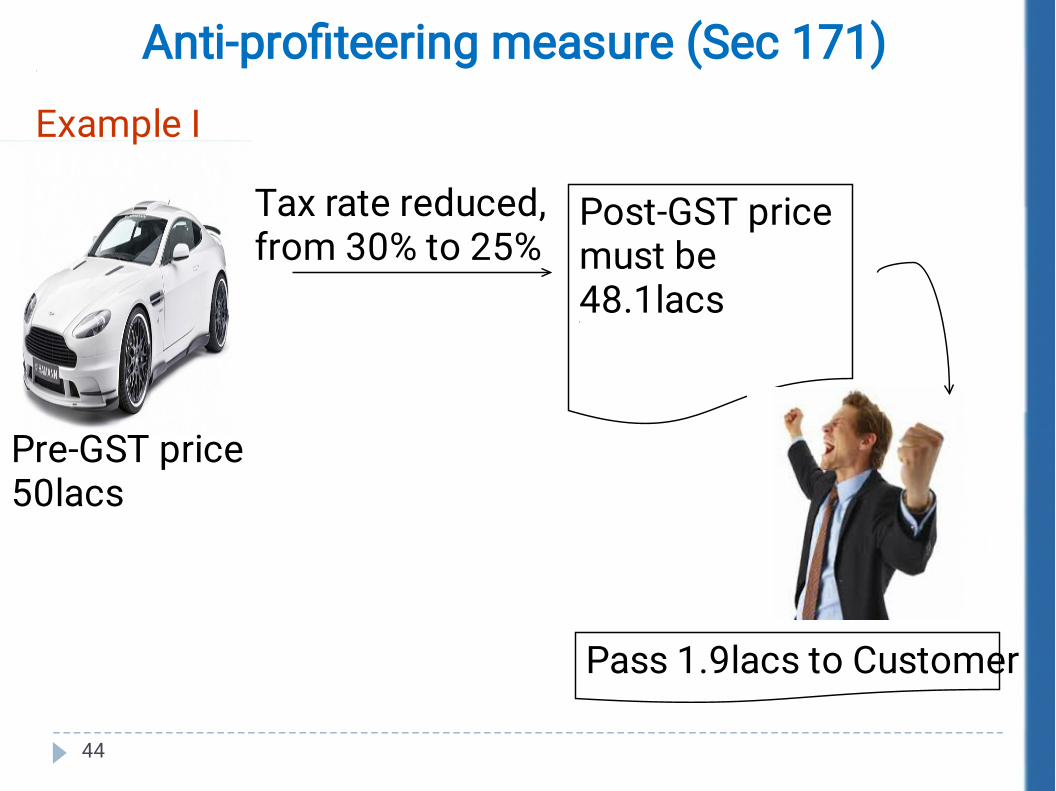

Anti-profiteering measure (Sec 171)

43

•

•

Why Anti-profiteering measure?

To protect consumers from businesses“profiteering” by way of commensurate reduction inprices andTo ensure inflation does not exceed expectations.

Benefit ofInput tax

creditReduction inthe tax rate

Reductionin Price

Example I Tax rate reduced,

from 30% to 25%

Pre-GST price50lacs

Pass 1.9lacs to Customer

Post-GST pricemust be48.1lacs

44

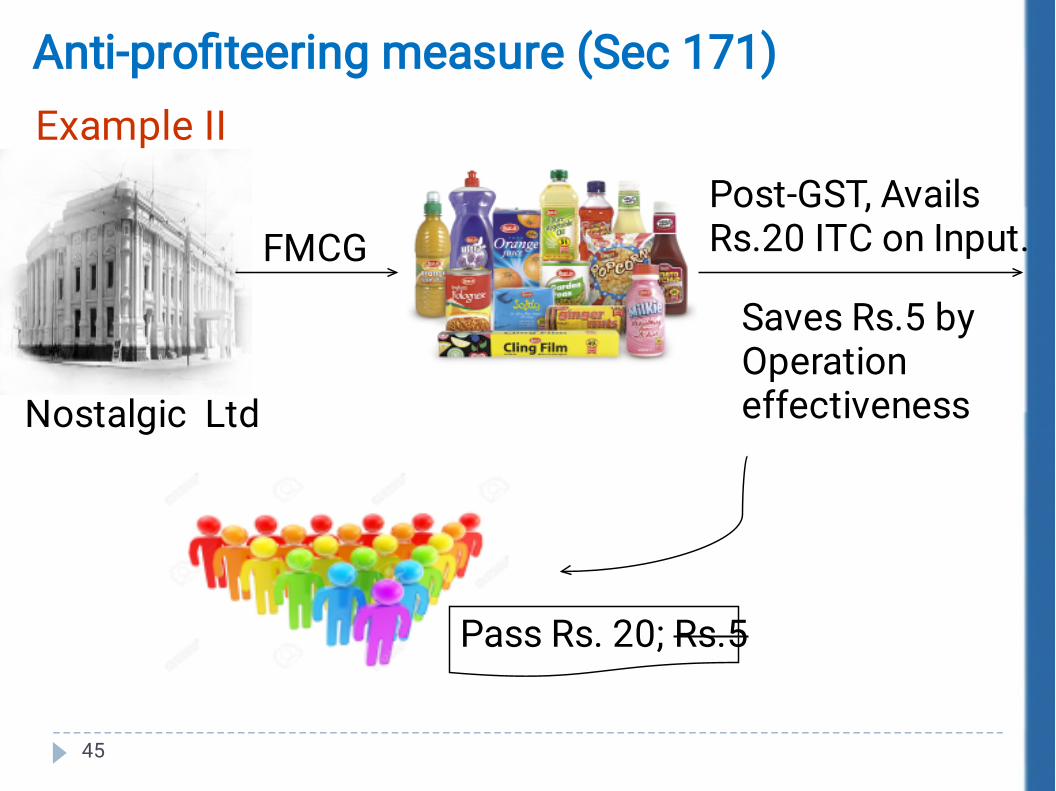

Anti-profiteering measure (Sec 171)

Anti-profiteering measure (Sec 171)Example II Post-GST, Avails

Rs.20 ITC on Input.

Nostalgic Ltd

Pass Rs. 20; Rs.5

Saves Rs.5 byOperationeffectiveness

FMCG

45

46

Reporting

47

Notes to accounts

•

•

•

•

•

Related Party Disclosures – whether GST paid. Foreign Expenses and Income Disclosures –Whether RCM paid. Contingent liability on account of Anti-profiteering. Departmental correspondence review, status ofpending cases SCNs. Status of refund applications filed

48

•

•

Disclosures on non-payment of undisputed taxliability.

Disclosures on disputed tax liabilities

CARO

49

Tax Audit Report – Form 3CD Para 4

Whether the assessee is liable to pay Indirect Tax likeExcise Duty, Service Tax, Sales Tax, Customs Duty, etc. If yes, please furnish the registration number or anyother identification number allotted for the same. Basic Details of Assessee GSTIN. In case of multipleregistration all GSTIN shall be provided by theAssessee.

50

Tax Audit Report Form 3CD Para11

Books of Accounts prescribed are maintained andexamined by the Tax Auditor? If Yes, GST Accounts & Records has been maintainedas per Sec 35 of CGST Act, 2017 r/a Rule 56 of CGSR,2017. Stock Records (Mandatory as per Sec 35 of CGST Act)

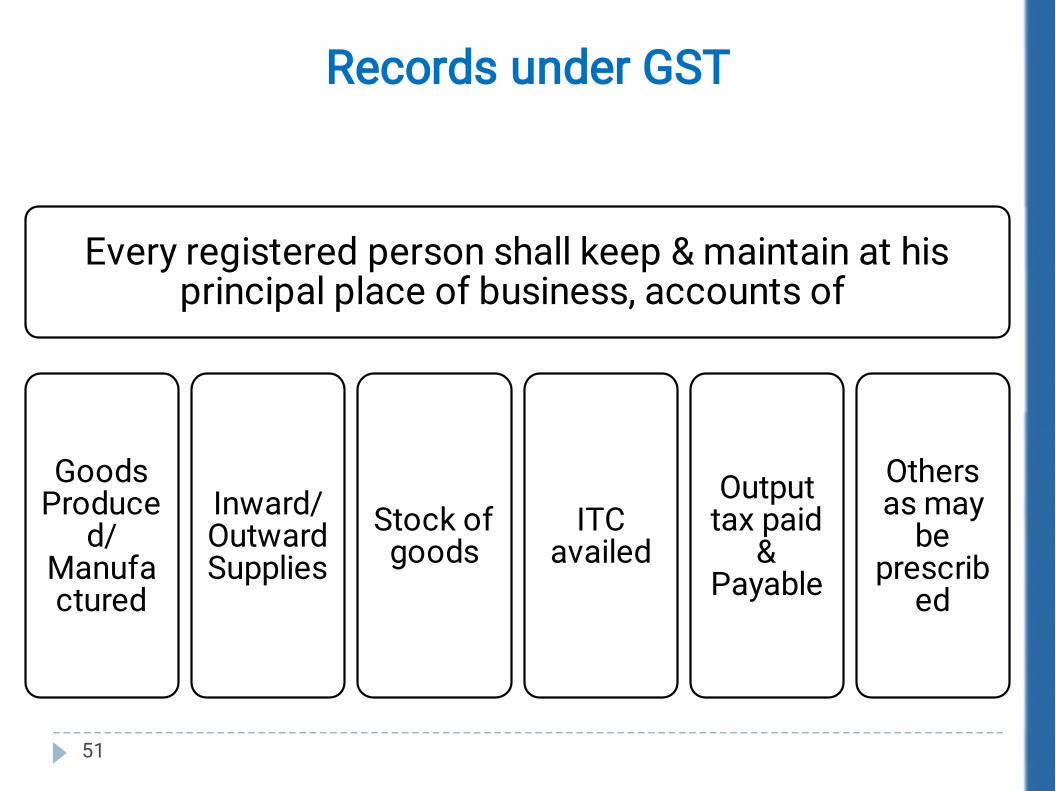

51

Records under GST

Every registered person shall keep & maintain at hisprincipal place of business, accounts of

GoodsProduce

d/Manufactured

Inward/OutwardSupplies

Stock ofgoods

ITCavailed

Outputtax paid

&Payable

Othersas may

beprescrib

ed

52

Period of retention of accounts

Every registered person shall retain books ofaccounts until the expiry of SEVENTY TWO MONTHSfrom the due date of furnishing of annual return forthe year pertaining to such accounts and records:

53

Tax Audit Report Form 3CD Para 21 (a)

Amount debited to Profit & Loss Account:Expenses of Capital Nature - No Difference in ITC,during further Sale.Personal Expenses – ITC on such expenses Sec 17of CGST Act.Club Expenses – ITC on such expenses Sec 17 ofCGST Act.Entrance Fee & Subscription – ITC on suchexpenses Sec 17 of CGST Act.

54

Tax Audit Report Form 3CD Para 27

••

Form 3CD Para 27(a):-Amount of Central Value Added Tax utilized andBalance Outstanding;

Details of ITC Availed & UtilizedCompared with E Cr. L and Books

55

Tax Audit Report Form 3CD Para 27

Form 3CD Para 27(b):-Income or Expenditure of Prior PeriodTime of Supply of Goods or Services as per Sec 12 or13 of CGST Form 3CD Para 38:-Central Excise Audit has been Conducted?If Yes, Qualifications made in such Report, if any.

56

Procedural verifications

57

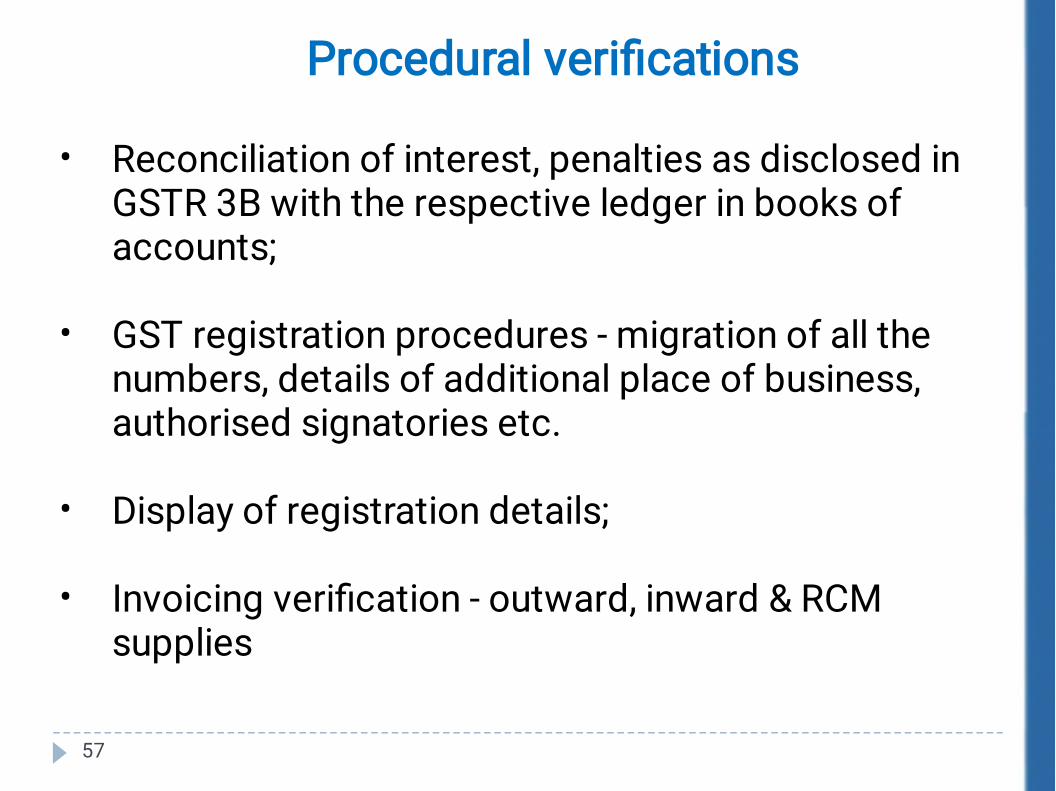

Procedural verifications

•

•

•

•

Reconciliation of interest, penalties as disclosed inGSTR 3B with the respective ledger in books ofaccounts; GST registration procedures - migration of all thenumbers, details of additional place of business,authorised signatories etc. Display of registration details; Invoicing verification - outward, inward & RCMsupplies

58

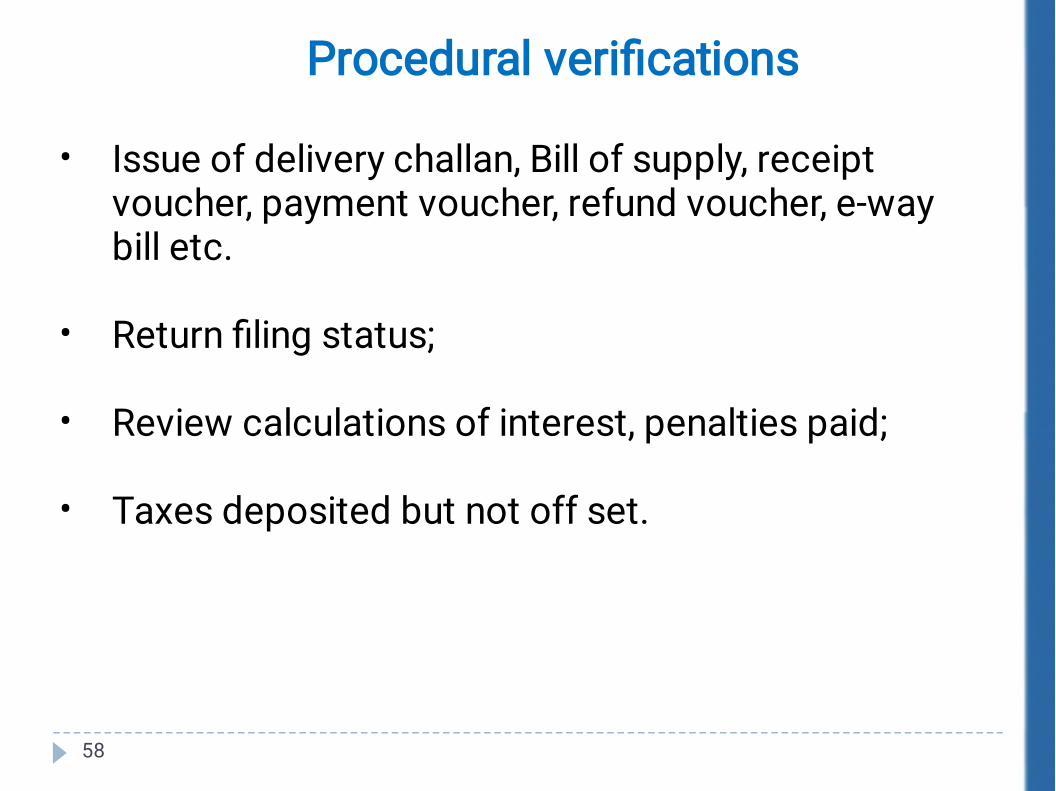

Procedural verifications

•

•

•

•

Issue of delivery challan, Bill of supply, receiptvoucher, payment voucher, refund voucher, e-waybill etc. Return filing status; Review calculations of interest, penalties paid; Taxes deposited but not off set.

59

Audit under GST

60

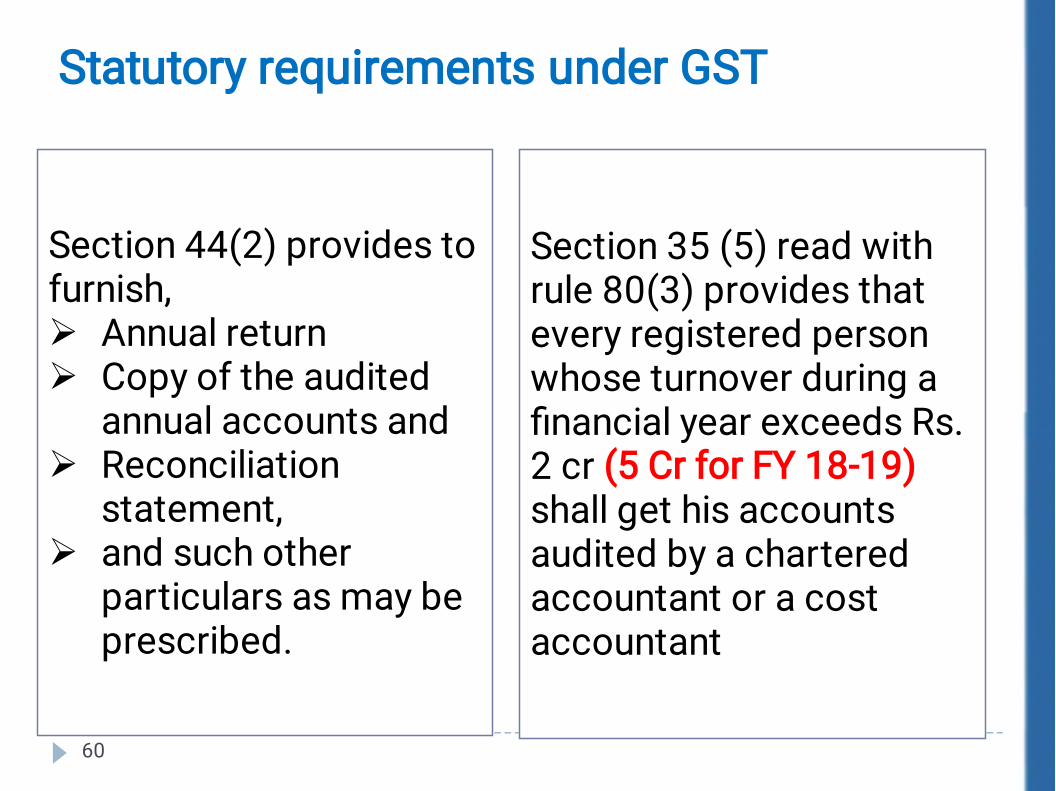

Statutory requirements under GST

Section 35 (5) read withrule 80(3) provides thatevery registered personwhose turnover during afinancial year exceeds Rs.2 cr (5 Cr for FY 18-19)shall get his accountsaudited by a charteredaccountant or a costaccountant

Section 44(2) provides tofurnish,

Annual returnCopy of the auditedannual accounts andReconciliationstatement,and such otherparticulars as may beprescribed.

61

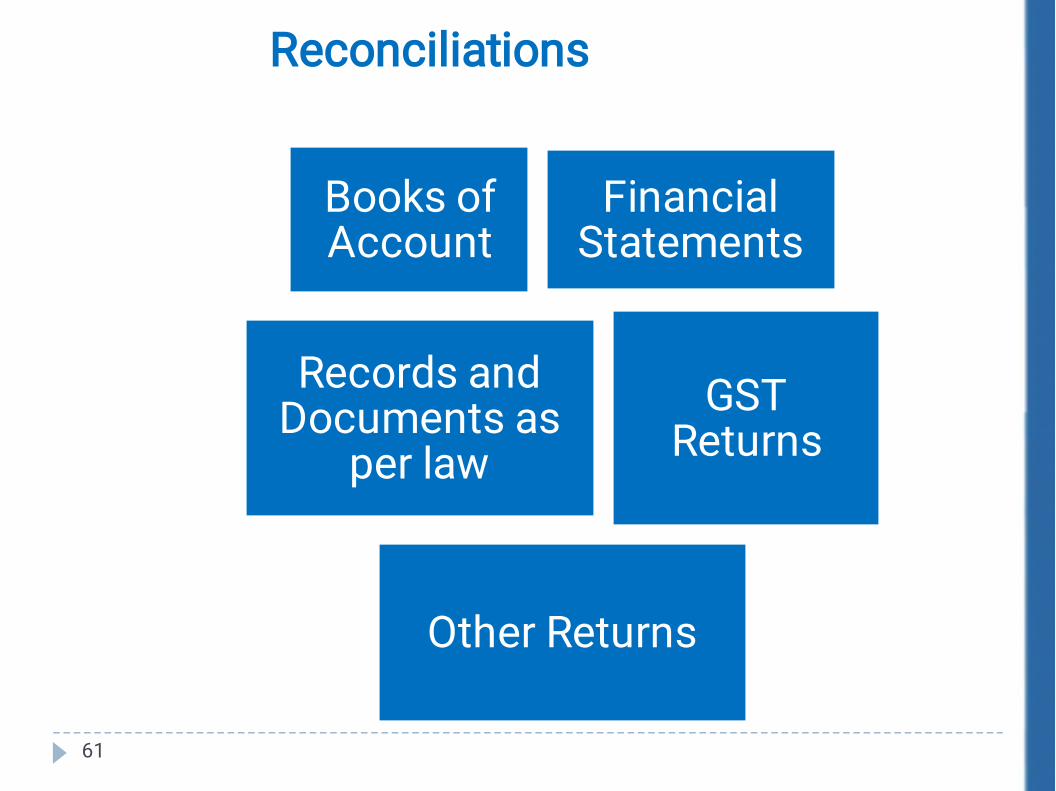

Reconciliations

Books ofAccount

FinancialStatements

Records andDocuments as

per lawGST

Returns

Other Returns