Embed Size (px)

Citation preview

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

FROM EQUITY RESEARCH

HMSP: Renewed growth

(HMSP IJ. IDR3,660. BUY. TP IDR4,100)

With purchasing power expected to pick up in 2H17, sales should also improve. Going into 2018, sales should benefit from the

government’s pro poor program as well as the less-aggressive excise tax revenues target, allowing earnings to grow by 7% yoy. Upgrade

to BUY.

To see the full version of this report, please click here

MARKET NEWS

Sector

▪ Infrastructure: 18 toll roads to commence operation in the next four months

Corporate ▪ Lulu Group: To expand its department stores and hypermarkets

▪ Bukit Asam: Plans to develop coal gasification with TPIA ▪ Adhi Karya: Entering the water treatment business

▪ Waskita Karya: Plans to issue IDR3.0tn of bonds as part of

IDR10.0tn self-registered bonds ▪ Waskita Beton Precast: New contracts in 8M17 reached 57% of

the target

KEY INDEX

Close

Chg Ytd Vol

(%) (%) (US$ m)

Asean - 5

Indonesia 5,824 (0.1) 10.0 353

Thailand 1,621 0.1 5.1 1,478

Philippines 7,984 (0.8) 16.7 128

Malaysia 1,772 0.2 8.0 516

Singapore 3,232 (0.6) 12.2 831

Regional

China 3,385 0.0 9.1 48,699

Hong Kong 27,614 (0.5) 25.5 11,497

Japan 19,456 0.5 1.8 1,076

Korea 2,337 0.7 15.3 4,716

Taiwan 10,548 (0.7) 14.0 4,016

India 31,662 (0.5) 18.9 524

NASDAQ 6,393 0.3 18.8 79,440

Dow Jones 21,808 0.2 10.3 8,800

CURRENCY AND INTEREST RATE

Rate

w-w m-m ytd

(%) (%) (%)

Rupiah Rp/1US$ 13,333 0.1 (0.1) 1.0

SBI rate % 5.90 - - (1.3)

10y Gov Indo bond 6.57 (0.1) (0.3) (1.4)

HARD COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Coal US$/ton 98 0.1 2.7 10.7

Gold US$/toz 1,334 0.0 6.1 15.8

Nickel US$/mt.ton 12,102 0.7 18.5 21.5

Tin US$/mt.ton 20,920 0.1 1.4 (1.3)

SOFT COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Cocoa US$/mt.ton 1,988 0.1 (3.0) (7.5)

Corn US$/mt.ton 126 0.6 (3.0) (2.4)

Oil (WTI) US$/barrel 49 (0.1) (0.6) (8.6)

Oil (Brent) US$/barrel 54 (0.3) 3.2 (4.9)

Palm oil MYR/mt.ton 2,726 1.7 4.8 (14.8)

Rubber USd/kg 171 (0.1) 12.5 (11.9)

Pulp US$/tonne 896 N/A 0.5 10.7

Coffee US$/60kgbag 126 (0.7) (4.2) (18.2)

Sugar US$/MT 381 0.8 (1.6) (27.4)

Wheat US$/ton 121 0.1 (9.1) (4.1)

Source: Bloomberg

www.danareksa.com See important disclosure at the back of this report 1

Equity Research Company Update

Thursday,07 September 2017

HM SAMPOERNA (HMSP IJ) BUY

UPGRADE Renewed growth

With purchasing power expected to pick up in 2H17, sales should also improve. Going into 2018, sales should benefit from the government’s pro poor program as well as the less-aggressive excise tax revenues target, allowing earnings to grow by 7% yoy. Upgrade to BUY. Expect better sales in 2H17. Going into 2H17, purchasing power should improve on the back of easing cost pressures given the government’s plans to: 1) delay the lifting of electricity tariff subsidies on 450 VA households, 2) allocate subsidies to 900 VA households which deserve to receive subsidies (IDR1.7tn) and 3) postpone LPG retail price hikes. Higher government spending toward the end of the year should also help bolster purchasing power in 2H17. Against this backdrop, sales should show better performance in 2H17 supported by new product offerings. Solid FY18F earnings growth. Based on our calculation, the net revenues margin for A Mild and Dji Sam Soe is down by 5% and 3%, respectively, in June 2017 since September 2015. The limited room for ASP adjustments and negative sales volume will filter through to a flat FY17 bottom line. For 2018, we estimate stronger revenues growth of 9.2% yoy with flattish sales volume. Given this and a manageable increase in excise tax (we estimate a 9.2% yoy increase for SKT and 9.7% yoy increase for SKM. For SPM, we assume 12% yoy, a similar increase like 2017), we expect HMSP to book solid FY18 earnings growth of 7.1% yoy. Upgrade to BUY with a higher TP. Going into 2018, we see more catalysts for higher sales volume, stemming from: (1) the possibility of a less aggressive excise tax revenues target, (2) higher energy subsidies and the expectation of more pro-poor government programs through direct cash assistance. With brisker sales, the earnings of cigarette companies should improve as well, we believe. We roll over our valuation and upgrade our recommendation to BUY with a higher TP of IDR4,100 – based on the median value of the DCF valuation (WACC 9%, TG 4%) and +1SD average 3-year PE of 36.5x.

Last price (IDR) 3,660

Target Price (IDR) 4,100

Upside/Downside +12.0%

Previous Target Price (IDR) 3,850

Stock Statistics

Sector CIGARETTE

Bloomberg Ticker HMSP IJ

No of Shrs (mn) 116,318

Mkt. Cap (IDR bn/USDmn) 425,724/31,930

Avg. daily T/O (IDR bn/USDmn) 73.8/5.5

Major shareholders

PHILIP MORRIS INDONESIA 92.5%

VONTOBEL HOLDING AG 0.4%

Estimated free float (%) 7.5

EPS Consensus(IDR)

2017F 2018F 2019F

Danareksa 109.0 116.8 130.7

Consensus 114.4 125.4 138.3

Danareksa/Cons (4.8) (6.9) (5.6)

HMSP relative to JCI Index

Source : Bloomberg

Natalia Sutanto

(62-21) 29 555 888 ext.3508

Key Financials Year to 31 Dec 2015A 2016A 2017F 2018F 2019F

Revenue, (IDRbn) 89,069 95,467 97,717 106,735 120,116 EBITDA, (IDRbn) 14,703 16,745 16,721 18,276 20,427 EBITDA Growth, (%) 2.3 13.9 (0.1) 9.3 11.8 Net profit (IDRbn) 10,363 12,762 12,677 13,581 15,198 EPS (IDR) 89.1 109.7 109.0 116.8 130.7 EPS growth (%) 1.8 23.1 (0.7) 7.1 11.9 BVPS, (IDR) 275.2 293.8 295.1 304.9 320.9 DPS, (IDR) 105.3 89.0 107.7 107.0 114.6 PER (x) 41.1 33.4 33.6 31.3 28.0 PBV (x) 13.3 12.5 12.4 12.0 11.4 Dividend yield (%) 2.9 2.4 2.9 2.9 3.1 EV/EBITDA (x) 28.8 25.1 25.2 23.0 20.5

Source : HMSP, Danareksa Estimates

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

SECTOR

Infrastructure: 18 toll roads to commence operation in the next four months

According to the Indonesian Toll Road Authority (BPJT), there will be 18 toll road segments covering 359km that will commence operation in the next four months. As such, 21 toll roads will have commenced operation this year

(earlier this year, 3 toll road sections – the 7km Gempol-Pasuruan section 1, the 8km Tanjung Priok toll road, and the 6.9km Gempol-Pasuruan section A1 - have started to be operated. Last year, 176km of toll roads started to be

operated.

All in all, 35 toll roads are under construction and 11 toll roads are prepared to be developed. In addition, BPJT is

also exploring proposals for the development of 30 other toll roads. (Bisnis Indonesia)

Commence operation Toll road segment Length (km)

September 2017 Semarang-Solo (Bawen-Salatiga segment) 17.6km

Kertosono-Mojokerto section 2 19.9km

Palembang-Indralaya section 1 7.75km

Medan Kualanamu-Tebing Tinggi 41.6km

Medan -Binjai section 2 and 3 (Helvetia-Binjai) 10.5km

October 2017 Bekasi Cawang Kampung Melayu section 1B and

1C – Pangkalan Jati and Jakasampurna

8.24km

Surabaya-Mojokerto section 1B III (Sepanjang-Krian)

15.5km

November 2017 Soreang-Pasirkoja section 1 and 2 8.15km

Bakauheni-Terbanggi Besar section 1C

(Pelabuhan Bakauheni – Bakauheni)

8.90km

December 2017 Bakauheni-Terbanggi Besar section 2

(Kotabaru-Lematang)

5.03km

Solo-Mantingan-Ngawi 87.9km

Pejagan-Pemalang section 3 and 4 (East Brebes – Pemalang)

37.3km

Ngawi-Kertosono section 1-3 (Ngawi-Wilangan) 52.57km

Batang-Semarang section 1 (Batang-East Batang)

3.2km

Palembang-Indralaya section 2 and 3

(Pamulatan-Simpang Indralaya)

13.80km

Cinere-Jagorawi section 2 (Jalan Raya Bogor –

Kukusan)

5.5km

Ciawi Sukabumi section 1 (Ciawi, Caringin) 7.3km

Pemalang-Batang section 1C (Sewaka –

Pemalang)

6km

CORPORATE

Lulu Group: To expand its department stores and hypermarkets Despite weak purchasing power, Lulu Group remains optimistic on the Indonesian market and will continue to

expand its department stores and hypermarket business in the future. Recently, the company opened one new Lulu

Hypermart and Department Store in QBIG BSD City, Tangerang - the second Lulu store in Indonesia. The store targets mid-income consumers. (Kontan)

MARKET NEWS

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

Bukit Asam: Plans to develop coal gasification with TPIA

Bukit Asam (PTBA) plans to explore new business lines by developing coal products through coal gasification in

cooperation with Chandra Asri Petrochemical (TPIA). Coal gasification, which is known as synthetic gas or syngas can be extracted into raw materials for chemical products, such as methanol and ethylene and for fertilizer products,

such as ammonia and synthetic natural gas. (Bisnis Indonesia)

Adhi Karya: Entering the water treatment business

Adhi Karya (ADHI) is preparing IDR200bn for entering the water treatment business in Lampung, Sumatera. The project is still in the tender offer stage. ADHI is competing with two other investors. ADHI has formed a partnership

with Adaro Tirta Mandiri (ATM), a subsidiary of Adaro Energy (ADRO). ADHI owns a 50% stake in this partnership. The investment needed in this project has reached IDR700bn to build a water treatment plant with a capacity of

750 liters per second. This project is included in the government’s strategic projects under Presidential Regulation No.3/2016. Furthermore, ADHI is looking at strategic partners for a water treatment project in Banten, with an

investment needed of approximately IDR4.0-5.0tn. (Bisnis Indonesia)

Waskita Karya: Plans to issue IDR3.0tn of bonds as part of IDR10.0tn self-registered bonds

Waskita Karya (WSKT) plans to issue self-registered bonds with a total value of IDR10.0tn. In the first stage, WSKT plans to issue IDR3.0tn of bonds consisting of 2 series: A series, with a three-year tenor and coupon rate in the

range of 8.0% to 8.75% and B series, with a 5 year tenor and coupon rate in the range of 8.5% to 9.25%. In the

second stage of the bonds issuance, IDR5.0tn of bonds are scheduled to be issued next year. WSKT has received A- ratings for these bonds. Around 80% of the proceeds will be used for working capital and the remaining 20% for

investments in subsidiaries. (Kontan)

Waskita Beton Precast: New contracts in 8M17 reached 57% of the target Waskita Beton Precast (WSBP) booked new contracts of IDR7.0tn as of Aug 17. This is 56.6% of the management’s

full year target of IDR12.4tn. As a result, the order book as of Aug17 reached IDR17.2tn, supported by IDR10.2tn

of carry over contracts. Around 85% of the contracts were derived from the Waskita Group. WSBP is optimistic that it can achieve the remaining IDR5.4tn in the rest of the year. WSBP is waiting for announcements of the winners of

several tenders: the Cibitung – Cilincing toll road worth IDR2.0tn, the Kualanamu Parapat toll road worth IDR500bn, the Legundi – Bunder toll road worth IDR1.3tn, the IDR2.5tn Probolinggo – Banyuwangi toll road, and the IDR750bn

Penajam – Balikpapan toll road. WSBP currently operates 11 plants with capacity of 3.25mn tons/year. Kontan

Danareksa Sekuritas – Equity SNAPSHOT

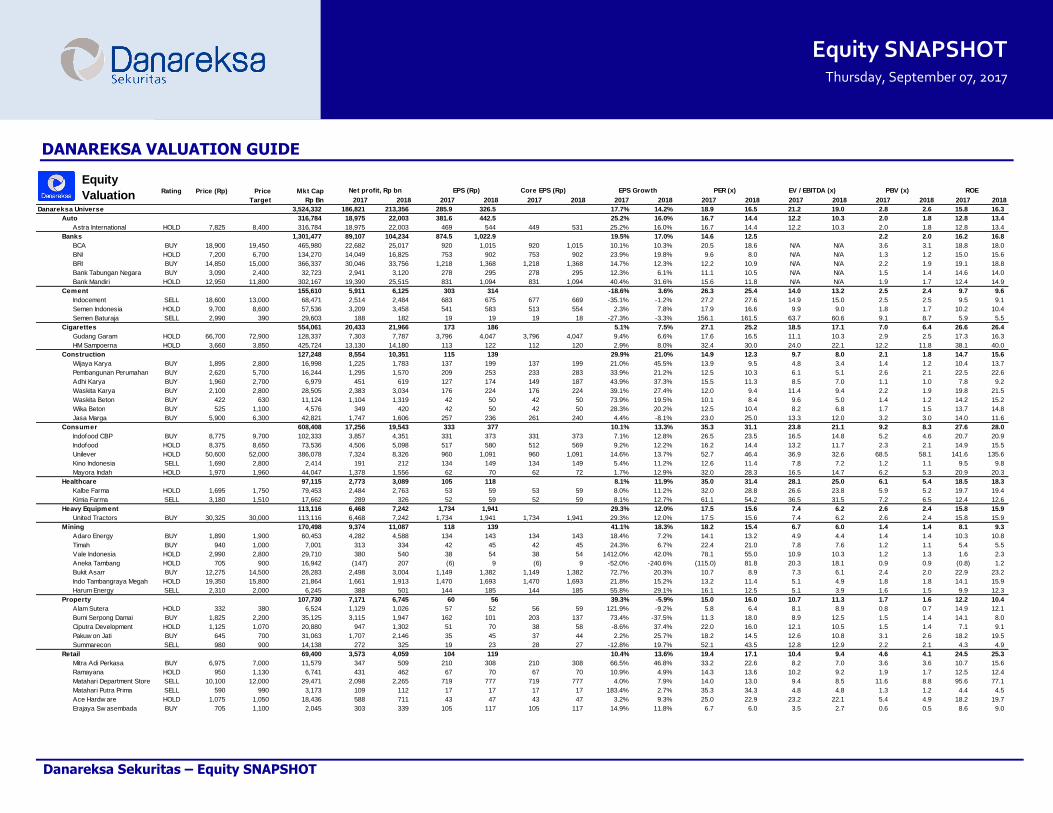

DANAREKSA VALUATION GUIDE

Rating Price (Rp) Price Mkt Cap

Target Rp Bn 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018 2017 2018

Danareksa Universe 3,524,332 186,821 213,356 285.9 326.5 17.7% 14.2% 18.9 16.5 21.2 19.0 2.8 2.6 15.8 16.3

Auto 316,784 18,975 22,003 381.6 442.5 25.2% 16.0% 16.7 14.4 12.2 10.3 2.0 1.8 12.8 13.4

Astra International HOLD 7,825 8,400 316,784 18,975 22,003 469 544 449 531 25.2% 16.0% 16.7 14.4 12.2 10.3 2.0 1.8 12.8 13.4

Banks 1,301,477 89,107 104,234 874.5 1,022.9 19.5% 17.0% 14.6 12.5 2.2 2.0 16.2 16.8

BCA BUY 18,900 19,450 465,980 22,682 25,017 920 1,015 920 1,015 10.1% 10.3% 20.5 18.6 N/A N/A 3.6 3.1 18.8 18.0

BNI HOLD 7,200 6,700 134,270 14,049 16,825 753 902 753 902 23.9% 19.8% 9.6 8.0 N/A N/A 1.3 1.2 15.0 15.6

BRI BUY 14,850 15,000 366,337 30,046 33,756 1,218 1,368 1,218 1,368 14.7% 12.3% 12.2 10.9 N/A N/A 2.2 1.9 19.1 18.8

Bank Tabungan Negara BUY 3,090 2,400 32,723 2,941 3,120 278 295 278 295 12.3% 6.1% 11.1 10.5 N/A N/A 1.5 1.4 14.6 14.0

Bank Mandiri HOLD 12,950 11,800 302,167 19,390 25,515 831 1,094 831 1,094 40.4% 31.6% 15.6 11.8 N/A N/A 1.9 1.7 12.4 14.9

Cement 155,610 5,911 6,125 303 314 -18.6% 3.6% 26.3 25.4 14.0 13.2 2.5 2.4 9.7 9.6

Indocement SELL 18,600 13,000 68,471 2,514 2,484 683 675 677 669 -35.1% -1.2% 27.2 27.6 14.9 15.0 2.5 2.5 9.5 9.1

Semen Indonesia HOLD 9,700 8,600 57,536 3,209 3,458 541 583 513 554 2.3% 7.8% 17.9 16.6 9.9 9.0 1.8 1.7 10.2 10.4

Semen Baturaja SELL 2,990 390 29,603 188 182 19 19 19 18 -27.3% -3.3% 156.1 161.5 63.7 60.6 9.1 8.7 5.9 5.5

Cigarettes 554,061 20,433 21,966 173 186 5.1% 7.5% 27.1 25.2 18.5 17.1 7.0 6.4 26.6 26.4

Gudang Garam HOLD 66,700 72,900 128,337 7,303 7,787 3,796 4,047 3,796 4,047 9.4% 6.6% 17.6 16.5 11.1 10.3 2.9 2.5 17.3 16.3

HM Sampoerna HOLD 3,660 3,850 425,724 13,130 14,180 113 122 112 120 2.9% 8.0% 32.4 30.0 24.0 22.1 12.2 11.8 38.1 40.0

Construction 127,248 8,554 10,351 115 139 29.9% 21.0% 14.9 12.3 9.7 8.0 2.1 1.8 14.7 15.6

Wijaya Karya BUY 1,895 2,800 16,998 1,225 1,783 137 199 137 199 21.0% 45.5% 13.9 9.5 4.8 3.4 1.4 1.2 10.4 13.7

Pembangunan Perumahan BUY 2,620 5,700 16,244 1,295 1,570 209 253 233 283 33.9% 21.2% 12.5 10.3 6.1 5.1 2.6 2.1 22.5 22.6

Adhi Karya BUY 1,960 2,700 6,979 451 619 127 174 149 187 43.9% 37.3% 15.5 11.3 8.5 7.0 1.1 1.0 7.8 9.2

Waskita Karya BUY 2,100 2,800 28,505 2,383 3,034 176 224 176 224 39.1% 27.4% 12.0 9.4 11.4 9.4 2.2 1.9 19.8 21.5

Waskita Beton BUY 422 630 11,124 1,104 1,319 42 50 42 50 73.9% 19.5% 10.1 8.4 9.6 5.0 1.4 1.2 14.2 15.2

Wika Beton BUY 525 1,100 4,576 349 420 42 50 42 50 28.3% 20.2% 12.5 10.4 8.2 6.8 1.7 1.5 13.7 14.8

Jasa Marga BUY 5,900 6,300 42,821 1,747 1,606 257 236 261 240 4.4% -8.1% 23.0 25.0 13.3 12.0 3.2 3.0 14.0 11.6

Consumer 608,408 17,256 19,543 333 377 10.1% 13.3% 35.3 31.1 23.8 21.1 9.2 8.3 27.6 28.0

Indofood CBP BUY 8,775 9,700 102,333 3,857 4,351 331 373 331 373 7.1% 12.8% 26.5 23.5 16.5 14.8 5.2 4.6 20.7 20.9

Indofood HOLD 8,375 8,650 73,536 4,506 5,098 517 580 512 569 9.2% 12.2% 16.2 14.4 13.2 11.7 2.3 2.1 14.9 15.5

Unilever HOLD 50,600 52,000 386,078 7,324 8,326 960 1,091 960 1,091 14.6% 13.7% 52.7 46.4 36.9 32.6 68.5 58.1 141.6 135.6

Kino Indonesia SELL 1,690 2,800 2,414 191 212 134 149 134 149 5.4% 11.2% 12.6 11.4 7.8 7.2 1.2 1.1 9.5 9.8

Mayora Indah HOLD 1,970 1,960 44,047 1,378 1,556 62 70 62 72 1.7% 12.9% 32.0 28.3 16.5 14.7 6.2 5.3 20.9 20.3

Healthcare 97,115 2,773 3,089 105 118 8.1% 11.9% 35.0 31.4 28.1 25.0 6.1 5.4 18.5 18.3

Kalbe Farma HOLD 1,695 1,750 79,453 2,484 2,763 53 59 53 59 8.0% 11.2% 32.0 28.8 26.6 23.8 5.9 5.2 19.7 19.4

Kimia Farma SELL 3,180 1,510 17,662 289 326 52 59 52 59 8.1% 12.7% 61.1 54.2 36.5 31.5 7.2 6.5 12.4 12.6

Heavy Equipment 113,116 6,468 7,242 1,734 1,941 29.3% 12.0% 17.5 15.6 7.4 6.2 2.6 2.4 15.8 15.9

United Tractors BUY 30,325 30,000 113,116 6,468 7,242 1,734 1,941 1,734 1,941 29.3% 12.0% 17.5 15.6 7.4 6.2 2.6 2.4 15.8 15.9

Mining 170,498 9,374 11,087 118 139 41.1% 18.3% 18.2 15.4 6.7 6.0 1.4 1.4 8.1 9.3

Adaro Energy BUY 1,890 1,900 60,453 4,282 4,588 134 143 134 143 18.4% 7.2% 14.1 13.2 4.9 4.4 1.4 1.4 10.3 10.8

Timah BUY 940 1,000 7,001 313 334 42 45 42 45 24.3% 6.7% 22.4 21.0 7.8 7.6 1.2 1.1 5.4 5.5

Vale Indonesia HOLD 2,990 2,800 29,710 380 540 38 54 38 54 1412.0% 42.0% 78.1 55.0 10.9 10.3 1.2 1.3 1.6 2.3

Aneka Tambang HOLD 705 900 16,942 (147) 207 (6) 9 (6) 9 -52.0% -240.6% (115.0) 81.8 20.3 18.1 0.9 0.9 (0.8) 1.2

Bukit Asam BUY 12,275 14,500 28,283 2,498 3,004 1,149 1,382 1,149 1,382 72.7% 20.3% 10.7 8.9 7.3 6.1 2.4 2.0 22.9 23.2

Indo Tambangraya Megah HOLD 19,350 15,800 21,864 1,661 1,913 1,470 1,693 1,470 1,693 21.8% 15.2% 13.2 11.4 5.1 4.9 1.8 1.8 14.1 15.9

Harum Energy SELL 2,310 2,000 6,245 388 501 144 185 144 185 55.8% 29.1% 16.1 12.5 5.1 3.9 1.6 1.5 9.9 12.3

Property 107,730 7,171 6,745 60 56 39.3% -5.9% 15.0 16.0 10.7 11.3 1.7 1.6 12.2 10.4

Alam Sutera HOLD 332 380 6,524 1,129 1,026 57 52 56 59 121.9% -9.2% 5.8 6.4 8.1 8.9 0.8 0.7 14.9 12.1

Bumi Serpong Damai BUY 1,825 2,200 35,125 3,115 1,947 162 101 203 137 73.4% -37.5% 11.3 18.0 8.9 12.5 1.5 1.4 14.1 8.0

Ciputra Development HOLD 1,125 1,070 20,880 947 1,302 51 70 38 58 -8.6% 37.4% 22.0 16.0 12.1 10.5 1.5 1.4 7.1 9.1

Pakuw on Jati BUY 645 700 31,063 1,707 2,146 35 45 37 44 2.2% 25.7% 18.2 14.5 12.6 10.8 3.1 2.6 18.2 19.5

Summarecon SELL 980 900 14,138 272 325 19 23 28 27 -12.8% 19.7% 52.1 43.5 12.8 12.9 2.2 2.1 4.3 4.9

Retail 69,400 3,573 4,059 104 119 10.4% 13.6% 19.4 17.1 10.4 9.4 4.6 4.1 24.5 25.3

Mitra Adi Perkasa BUY 6,975 7,000 11,579 347 509 210 308 210 308 66.5% 46.8% 33.2 22.6 8.2 7.0 3.6 3.6 10.7 15.6

Ramayana HOLD 950 1,130 6,741 431 462 67 70 67 70 10.9% 4.9% 14.3 13.6 10.2 9.2 1.9 1.7 12.5 12.4

Matahari Department Store SELL 10,100 12,000 29,471 2,098 2,265 719 777 719 777 4.0% 7.9% 14.0 13.0 9.4 8.5 11.6 8.8 95.6 77.1

Matahari Putra Prima SELL 590 990 3,173 109 112 17 17 17 17 183.4% 2.7% 35.3 34.3 4.8 4.8 1.3 1.2 4.4 4.5

Ace Hardw are HOLD 1,075 1,050 18,436 588 711 43 47 43 47 3.2% 9.3% 25.0 22.9 23.2 22.1 5.4 4.9 18.2 19.7

Erajaya Sw asembada BUY 705 1,100 2,045 303 339 105 117 105 117 14.9% 11.8% 6.7 6.0 3.5 2.7 0.6 0.5 8.6 9.0

PER (x)

Equity

Valuation Net profit, Rp bn EPS (Rp) Core EPS (Rp) EPS Growth ROE EV / EBITDA (x) PBV (x)

Equity SNAPSHOT Thursday, September 07, 2017

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

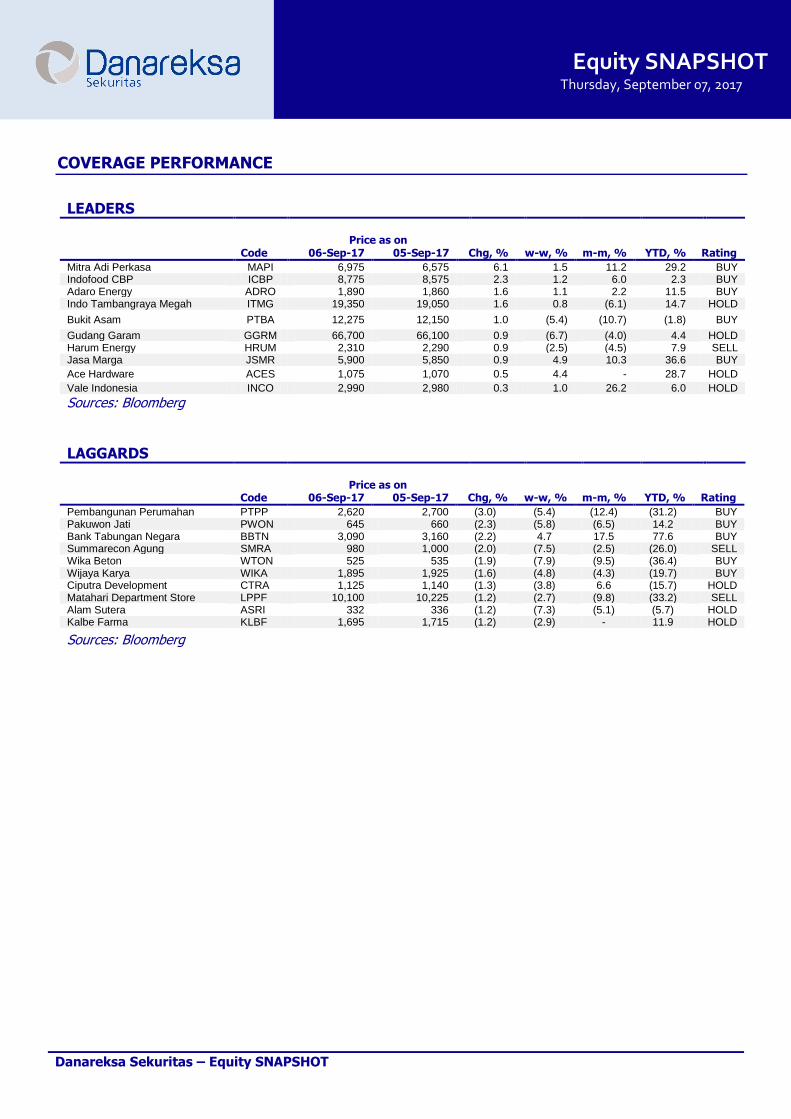

LEADERS Price as on Code 06-Sep-17 05-Sep-17 Chg, % w-w, % m-m, % YTD, % Rating

Mitra Adi Perkasa MAPI 6,975 6,575 6.1 1.5 11.2 29.2 BUY Indofood CBP ICBP 8,775 8,575 2.3 1.2 6.0 2.3 BUY Adaro Energy ADRO 1,890 1,860 1.6 1.1 2.2 11.5 BUY Indo Tambangraya Megah ITMG 19,350 19,050 1.6 0.8 (6.1) 14.7 HOLD

Bukit Asam PTBA 12,275 12,150 1.0 (5.4) (10.7) (1.8) BUY

Gudang Garam GGRM 66,700 66,100 0.9 (6.7) (4.0) 4.4 HOLD Harum Energy HRUM 2,310 2,290 0.9 (2.5) (4.5) 7.9 SELL Jasa Marga JSMR 5,900 5,850 0.9 4.9 10.3 36.6 BUY

Ace Hardware ACES 1,075 1,070 0.5 4.4 - 28.7 HOLD

Vale Indonesia INCO 2,990 2,980 0.3 1.0 26.2 6.0 HOLD

Sources: Bloomberg

LAGGARDS Price as on Code 06-Sep-17 05-Sep-17 Chg, % w-w, % m-m, % YTD, % Rating

Pembangunan Perumahan PTPP 2,620 2,700 (3.0) (5.4) (12.4) (31.2) BUY Pakuwon Jati PWON 645 660 (2.3) (5.8) (6.5) 14.2 BUY Bank Tabungan Negara BBTN 3,090 3,160 (2.2) 4.7 17.5 77.6 BUY Summarecon Agung SMRA 980 1,000 (2.0) (7.5) (2.5) (26.0) SELL Wika Beton WTON 525 535 (1.9) (7.9) (9.5) (36.4) BUY Wijaya Karya WIKA 1,895 1,925 (1.6) (4.8) (4.3) (19.7) BUY Ciputra Development CTRA 1,125 1,140 (1.3) (3.8) 6.6 (15.7) HOLD Matahari Department Store LPPF 10,100 10,225 (1.2) (2.7) (9.8) (33.2) SELL Alam Sutera ASRI 332 336 (1.2) (7.3) (5.1) (5.7) HOLD Kalbe Farma KLBF 1,695 1,715 (1.2) (2.9) - 11.9 HOLD

Sources: Bloomberg

COVERAGE PERFORMANCE

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

PREVIOUS REPORTS

Adaro Energy: 2Q17: Boosted by higher sales and a lower stripping ratio Snapshot20170829

Plantation: Key Takeaways From Palm Oil Internet Seminar, DILD: Successful launch of Fifty Seven Snapshot20170828

Agung Podomoro Land: At a hefty discount for a reason, United Tractors: Sales volume from Mining sector remained strong in July 2017 Snapshot20170824

Property: 7 days repo rate cut to create positive sentiment, Plantations: US proposes duties on biodiesel imports

from Indonesia and Argentina Snapshot20170823 Automotive: Recovery in monthly car and motorcycle sales Snapshot20170822

UNVR: Bright earnings outlook Snapshot20170821 Automotive: GIIAS 2017: More low-end MPV cars launched, INTP: Key takeaways from conference call

Snapshot20170816

MYOR: Better performance on the cards Snapshot20170815

Equity SNAPSHOT Thursday, September 07, 2017

Danareksa Sekuritas – Equity SNAPSHOT

Adeline Solaiman

[email protected] (62-21) 2955 888 ext. 3503 Retail

PT Danareksa Sekuritas

Jl. Medan Merdeka Selatan No. 14 Jakarta 10110 Indonesia Tel (62 21) 29 555 888 Fax (62 21) 350 1709

Equity Research Team

Sales team

Disclaimer

The information contained in this report has been taken from sources which we deem reliable. However, none of P.T. Danareksa Sekuritas and/or its affiliated companies and/or their respective employees and/or agents makes any representation or warranty (express or implied) or accepts any responsibility or liability as to, or in relation

to, the accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information or opinions remaining unchanged after the issue thereof.

We expressly disclaim any responsibility or liability (express or implied) of P.T. Danareksa Sekuritas, its affiliated companies and their respective employees and agents whatsoever and howsoever arising (including, without limitation for any claims, proceedings, action , suits, losses, expenses, damages or costs) which may be brought against or suffered by any person as a results of acting in reliance upon the whole or any part of the contents of this report and neither P.T. Danareksa Sekuritas, its

affiliated companies or their respective employees or agents accepts liability for any errors, omissions or misstatements, negligent or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission there from which might otherwise arise is hereby expresses disclaimed.

The information contained in this report is not be taken as any recommendation made by P.T. Danareksa Sekuritas or any other person to enter into any agreement with regard to any investment mentioned in this document. This report is prepared for general circulation. It does not have regards to the specific person who may receive this

report. In considering any investments you should make your own independent assessment and seek your own professional financial and legal advice.

Novrita E. Putrianti

[email protected] (62-21) 29555 888 ext. 3128

Ehrliech Suhartono

[email protected] (62-21) 29555 888 ext. 3132

Maria Renata

[email protected] (62-21) 29555 888 ext.3513 Construction

Lucky Bayu Purnomo

[email protected] (62-21) 29555 888 ext.3512 Technical Analyst

Laksmita Armandani

[email protected] (62-21) 29555 888 ext. 3125

Antonia Febe Hartono, CFA

[email protected] (62-21) 29555 888 ext.3504 Cement, Property

Tuty Sutopo

[email protected] (62-21) 29555 888 ext. 3121

Upik Yuzarni

[email protected] (62-21) 29555 888 ext. 3137

Kevin Giarto

[email protected] (62-21) 29555 888 ext. 3139

Stefanus Darmagiri

[email protected] (62-21) 2955 888 ext. 3530 Auto, Coal, Heavy Equip, Metal, Cement

Natalia Sutanto

[email protected] (62-21) 29555 888 ext.3508 Consumer, Tobacco, Property

Yudha Gautama

[email protected] (62-21) 29555 888 ext.3509 Plantation

See important disclosure at the back of this report www.danareksa.com

![Equity & Excellence in Maine Schools · [District àFinance Section àTake Snapshot] Finance –Per Pupil Expenditure [Finance Section àClick Regular Instruction àTake Snapshot]](https://img.pdfslide.net/doc/110x75/5fd03a6d09799b1d91116a5b/equity-excellence-in-maine-schools-district-finance-section-take-snapshot.jpg)