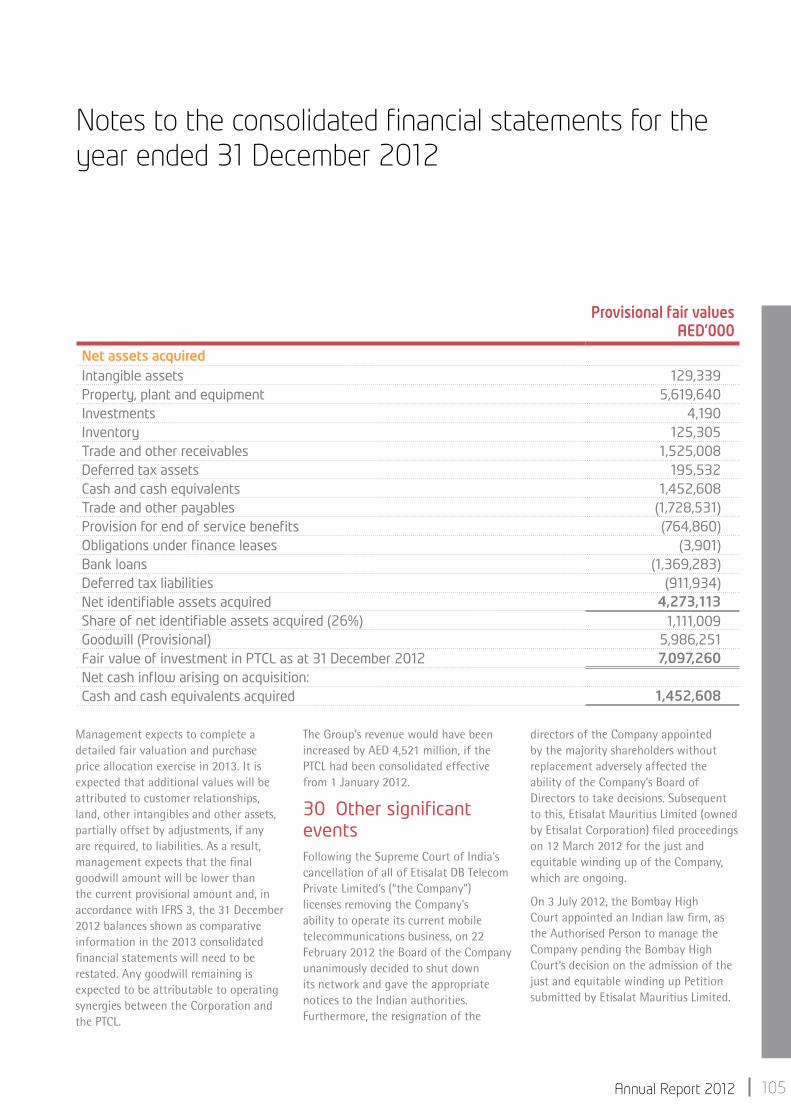

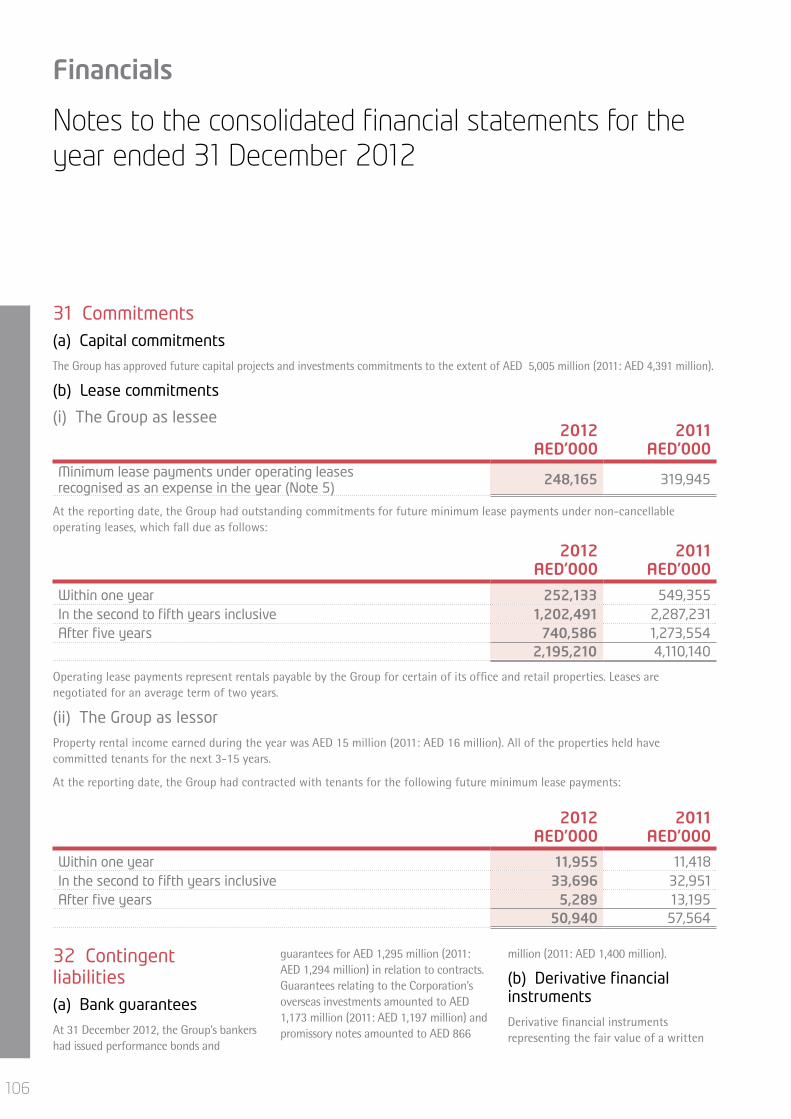

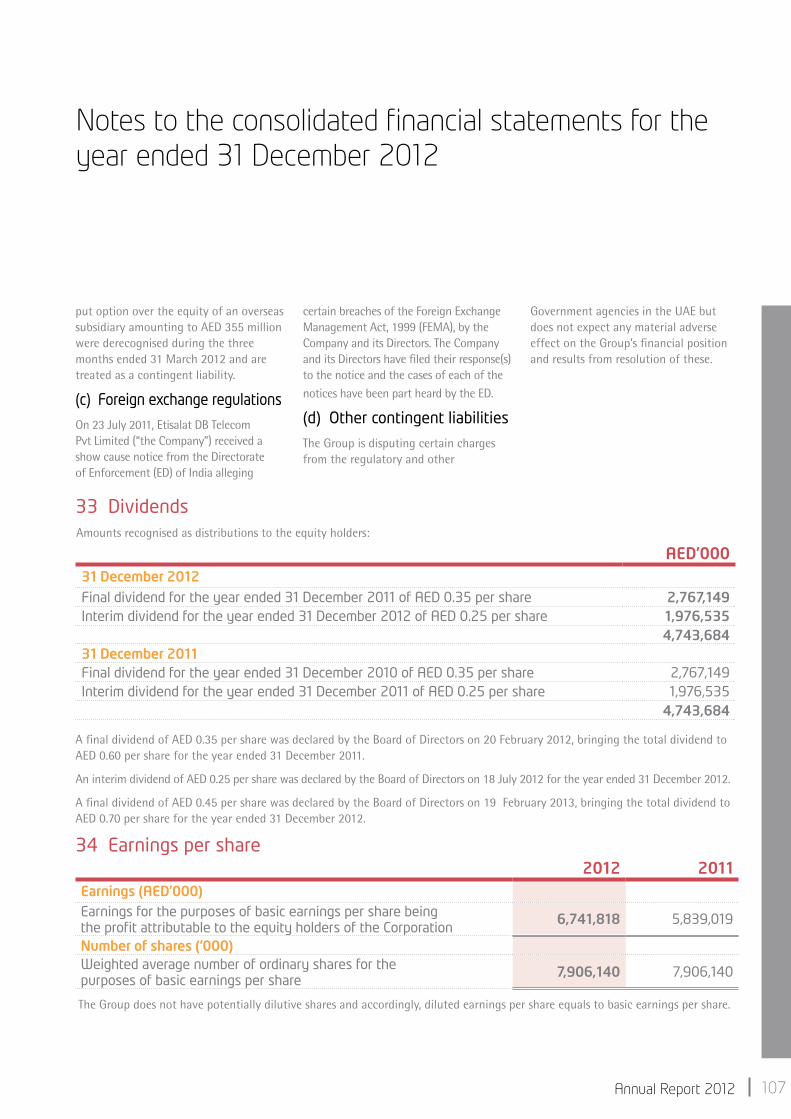

Embed Size (px)

DESCRIPTION

Etisalat annual report

Citation preview

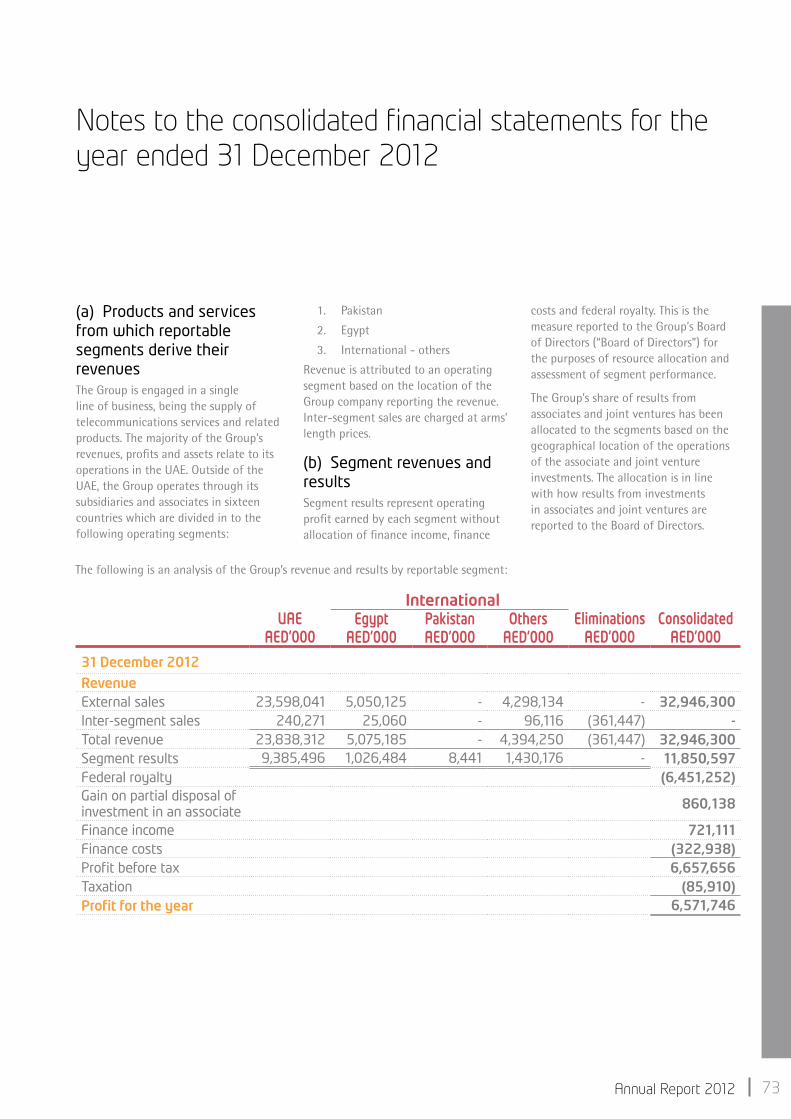

Annual Report 2012

Head Office:

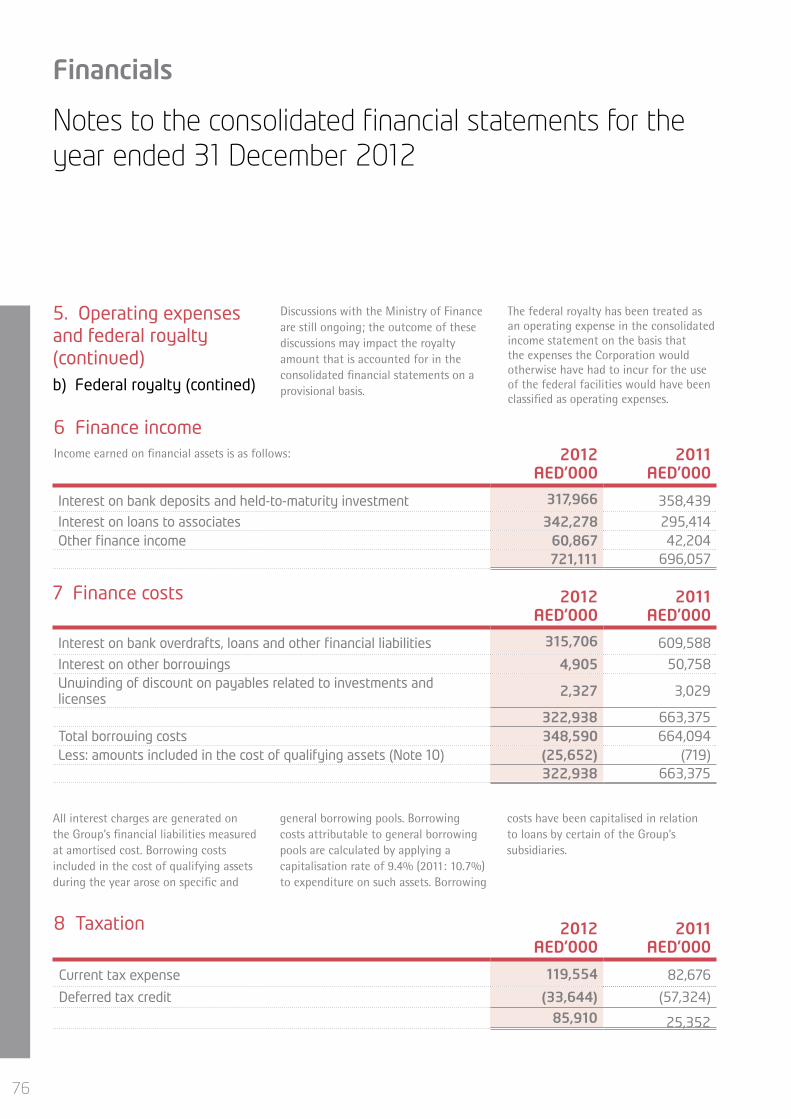

Etisalat BuildingIntersection of Zayed The 1st Street andSheikh Rashid Bin Saeed Al Maktoum StreetP.O. Box 3838Abu Dhabi, UAE

Regional Offices:Abu Dhabi, Dubai, Northern Emirates

01Annual Report 2012

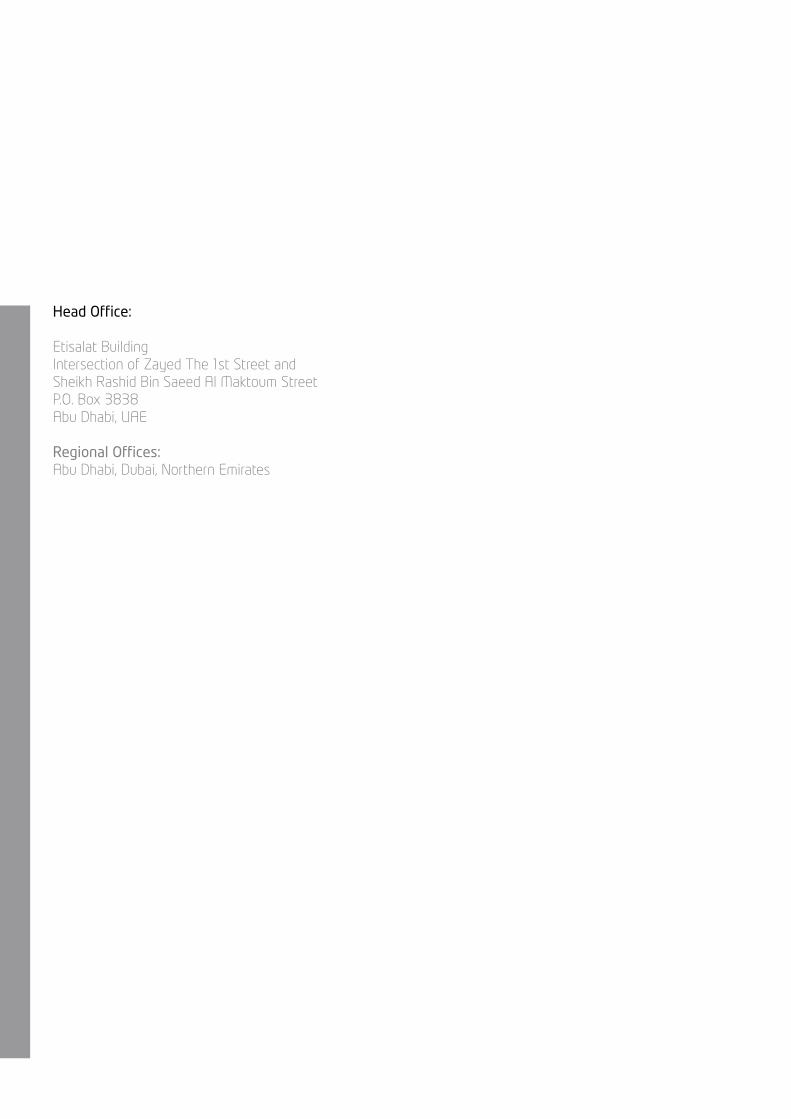

Table of contents

Key Highlights of 2012 02

Business Snapshot 04

Timeline 06

Chairman’s Statement 08

Board of Director’s 10

Chief Executive Officer’s Statement 12

Management Team 16

Etisalat Group Strategy 20

Awards 22

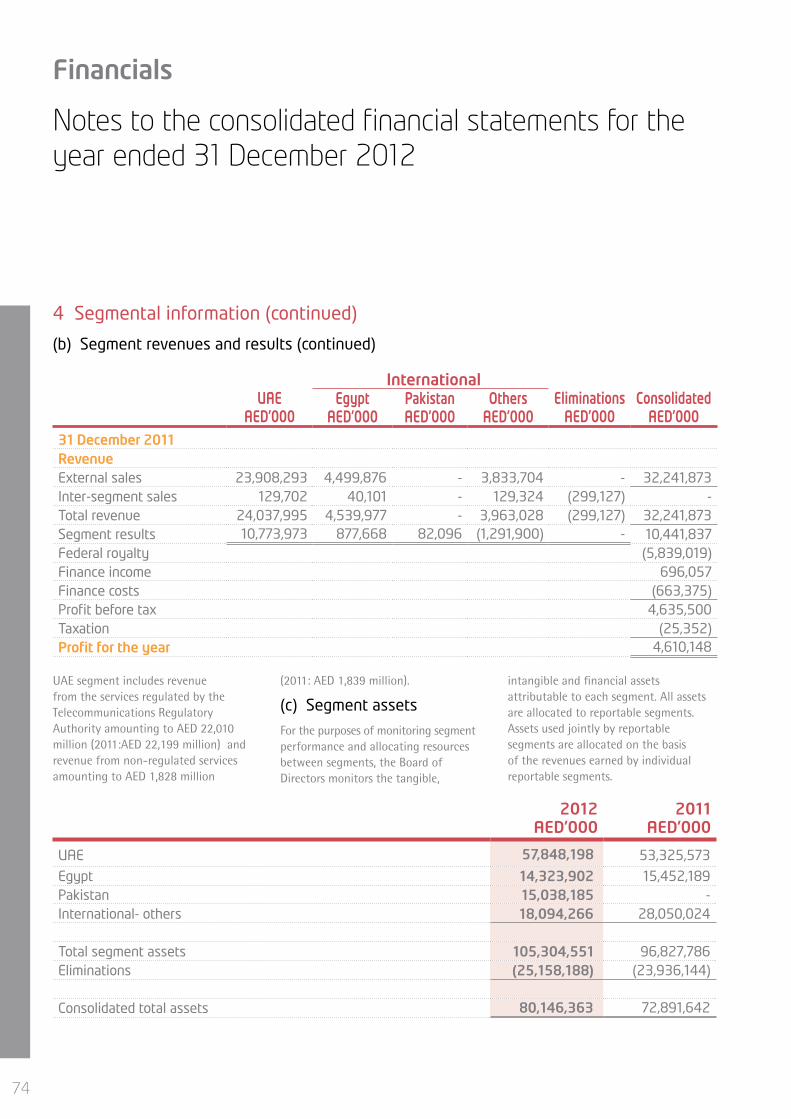

Operational Highlights 24

Management Review

• Middle East 28

• Africa 34

• Asia 37

• Etisalat Services Holding 40

• Our International Presence 42

• Human Capital 44

• Corporate Social Responsibility 46

• Corporate Governance 48

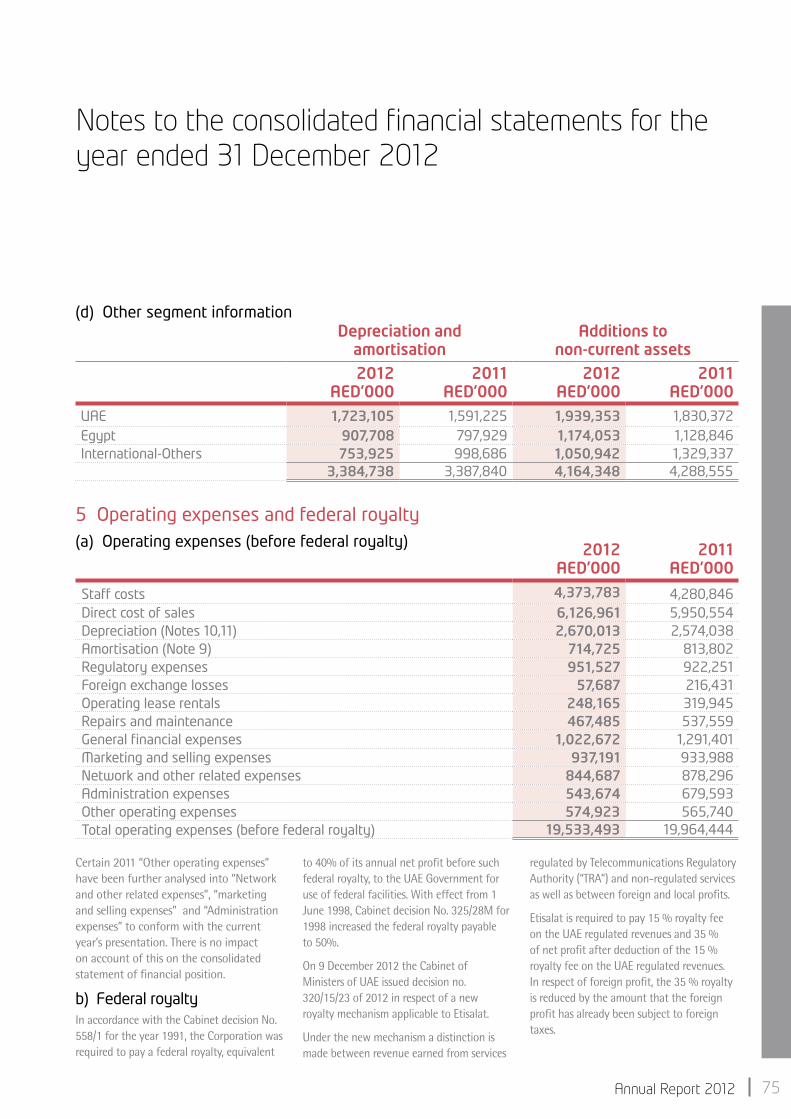

Independent Auditors Report to the Shareholders 50

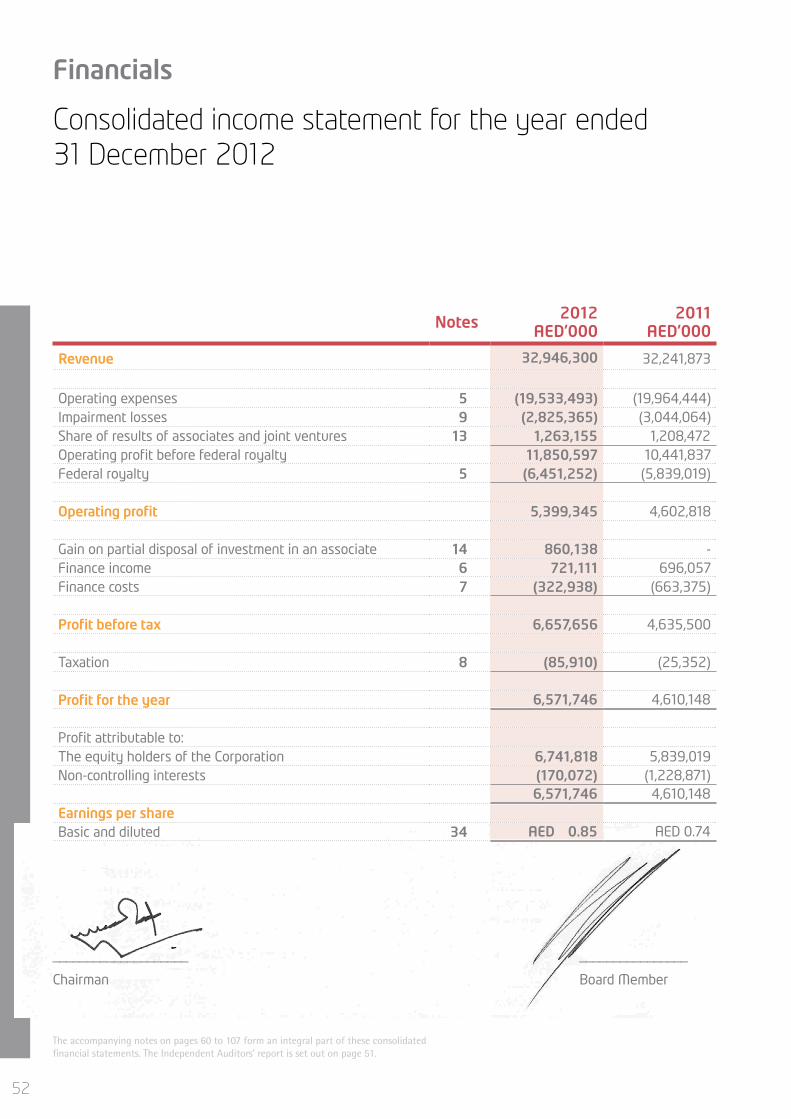

Consolidated Income Statement 52

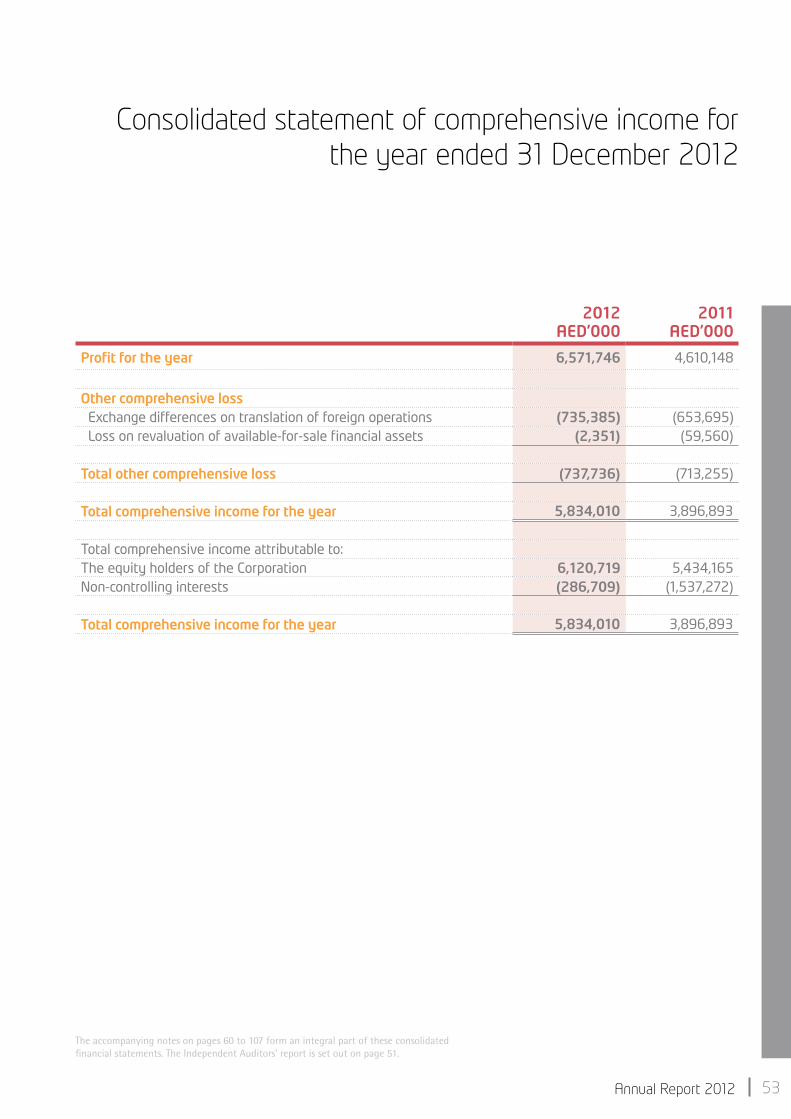

Consolidated Statement of Comprehensive Income 53

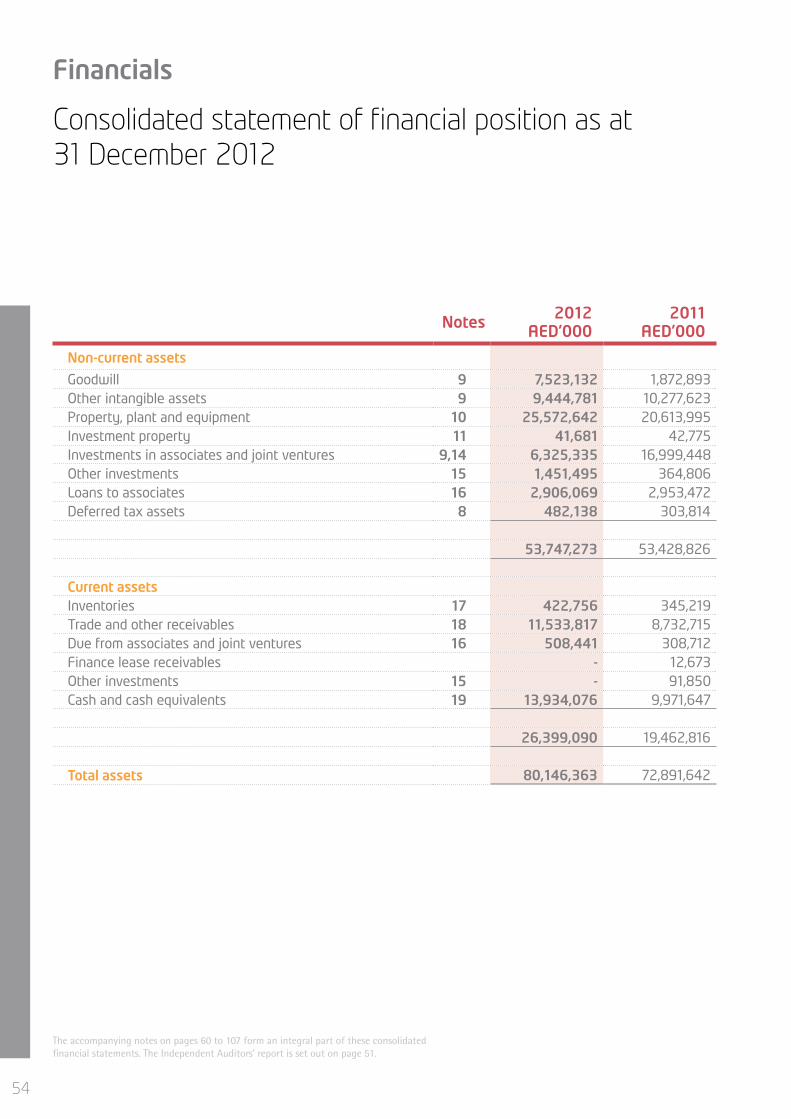

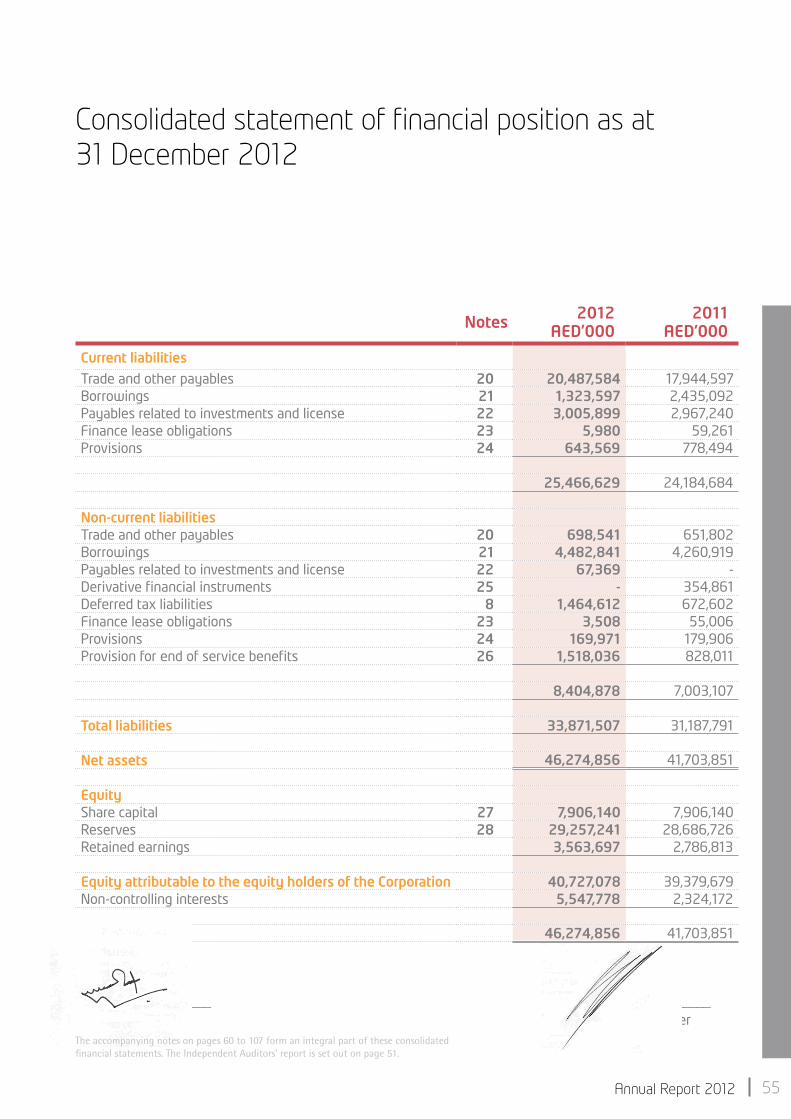

Consolidated Statement of Financial Position 54

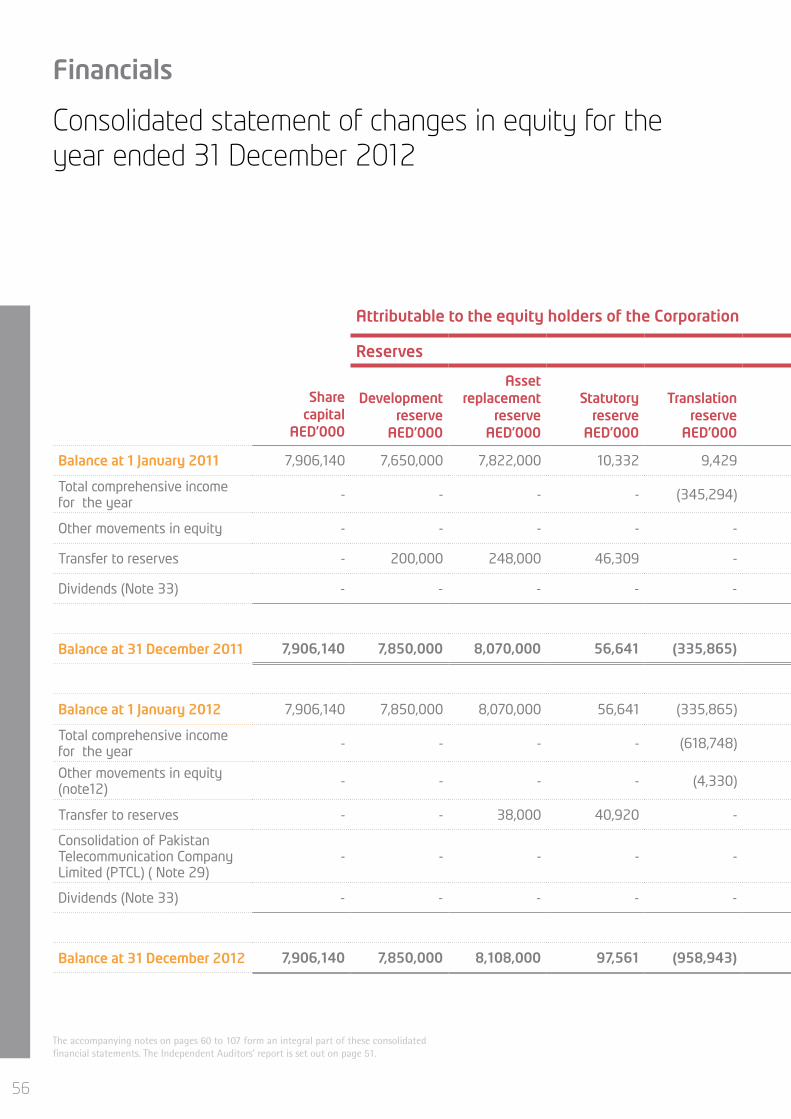

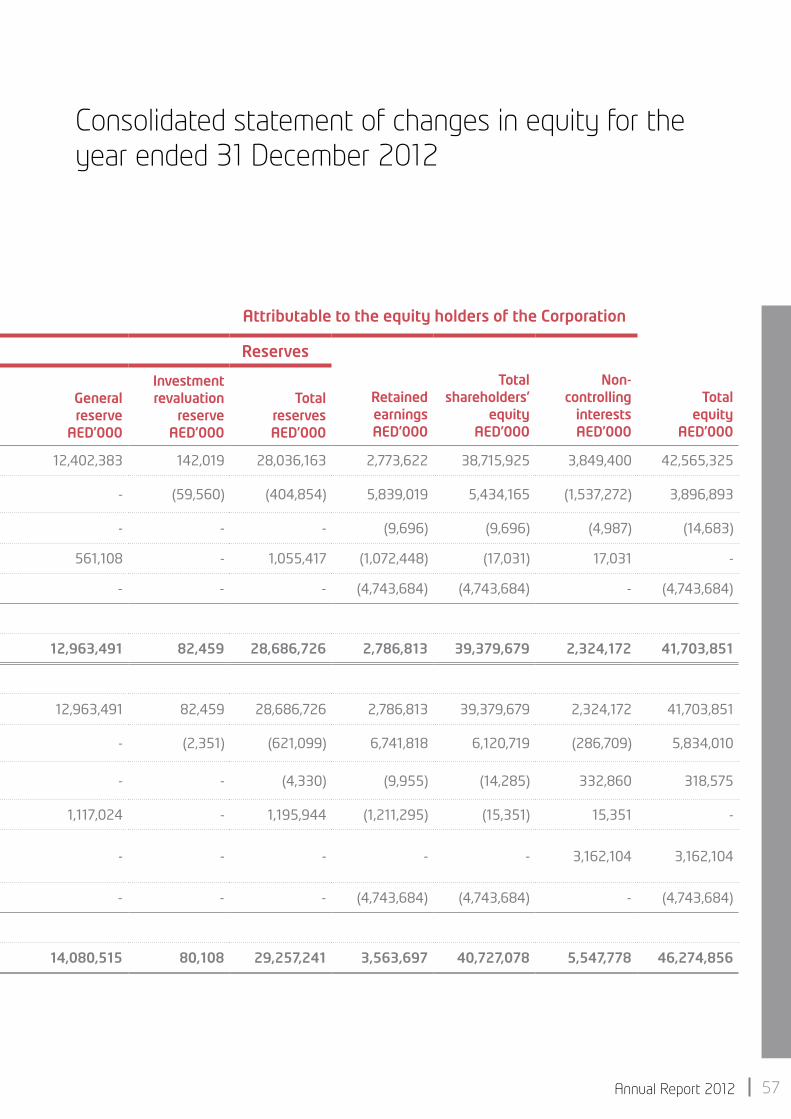

Consolidated Statement of Changes in Equity 56

Consolidated Statement of Cash Flows 58

Notes to the Consolidated Financial Statements 60

Notice of General Annual Shareholders Meeting 108

139 millionAggregate Subscribers

32.9 AED

billionRevenue

16.9 AED

billionEBITDA

6.7 AED

billionNet Profit

4.2AED

billionCAPEX

70 Fils

Dividendper share

Key highlights of 2012

04

Business snapshot

Annual Report 2012 05Annual Report 2012

Since its inception in 1976, Etisalat has been at the forefront of the Middle East’s technological revolution. Over the last forty years, it has developed and grown to become one of the world’s leading telecommunications companies.

Etisalat focuses on delivering innovative solutions to transform the communities in which it operates and accelerate social development and economic growth. This has been underpinned by its commitment to actively develop and engineer platforms for growth within the local markets in which it operates.

Etisalat’s international acquisition programme began in earnest in 2004 by winning the second mobile license, and the first 3G license in Saudi Arabia. Since then the company has witnessed rapid expansion, positioning Etisalat as one of the world’s fastest growing operators, with its subscriber numbers rocketing from 4 million in 2004 to over 139 million at the end of 2012. Etisalat now has access to a population of about seven hundred million people, and its satellite network provides services to over two thirds of the planet’s surface.

For nearly 40 years, Etisalat has helped the UAE sustain its position as the region’s hub for business, trade and foreign investment by providing reliable and high quality services. It is one of the global telecommunication industry’s innovation pacesetters - powering its home country into the Top 10 nations list by providing the latest technologies first.

Etisalat is a pioneer in next-generation

networks for both fixed line and wireless connections. The company deployed a nationwide fibre optic network in the UAE, which led to Abu Dhabi being the world’s first city to be covered by a powerful, high-speed fibre network.

Etisalat also launched 4G mobile services in the UAE, and today operates the Middle East’s largest LTE network where population coverage exceeds 82 per cent. Presently Etisalat offers both the Middle East’s fastest fixed line broadband service with speeds of up to 100Mbps to the home, and the highest speed mobile broadband connectivity. In 2012, Etisalat succeeded in completing the highest 4G LTE speed test in the world, reaching 300 Mbps. This lightning-fast speed is a breakthrough for the international telecommunications industry and establishes Etisalat as a global leader in mobile broadband.

This technological expertise has helped Etisalat capture significant market share as it expands across the region, most notably in Egypt and Saudi Arabia, where the introduction of mobile broadband services, including video call and mobile TV, has changed market dynamics and provided affordable internet access for millions.

Etisalat is pioneering several advanced ‘green’ technologies and is a regional leader in providing environmentally friendly information and communication solutions. This includes smart building technologies, the latest Machine-to-Machine (M2M) solutions and the deployment of alternative power within

its regional networks. Etisalat is also ensuring that its infrastructure meets the highest international standards; its fibre optic network in the UAE is expected to reduce carbon emissions and energy consumption by over 80 per cent and 70 per cent respectively.

Etisalat is committed to the principles of corporate social responsibility and is partnering with many governments and non-government organisations to increase access to education and health care via technology.

Etisalat’s innovative services have received over 60 regional and international accolades since 2008 including an unprecedented three GSMA Global Mobile Awards at Mobile World Congress in March 2012 for two of its transformational initiatives: The Mobile Commerce cashless payment system using Near Field Communications (NFC) technology, and The Mobile Baby mHealth platform, a remarkable pre-natal application deployed in sub-Saharan Africa that allows medical practitioners to send ultrasound images, video clips and 3D scans from ultrasound machines for remote medical analysis via mobile broadband. Moreover, Etisalat has been named ‘Best Overall Operator’ in the Middle East 10 times since 2006, and was named Best International Carrier at the World Communications Awards in 2008.

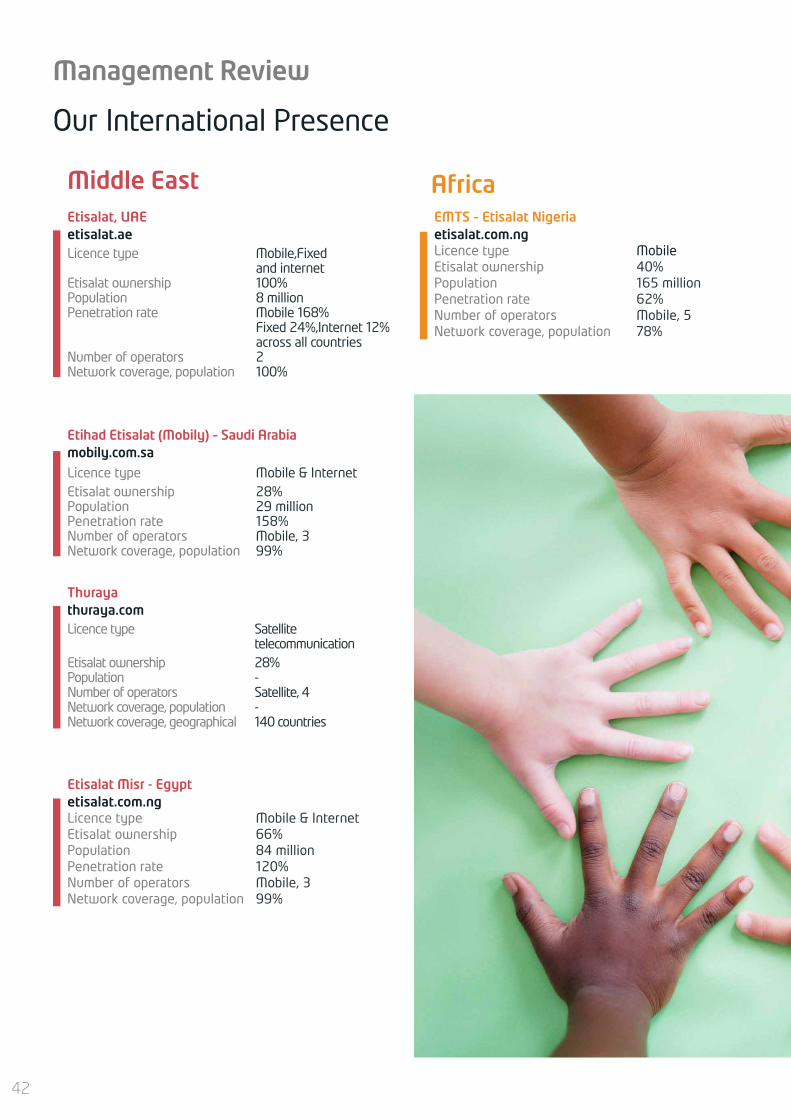

Etisalat is a multinational, blue-chip organisation with operations in 15 countries across the

Middle East, Africa and Asia.

2012

Etisalat won 3G license in Afghanistan and Ivory Coast and launched the first 3G services in history of Afghanistan. Etisalat won three GSMA awards in the ‘Best Mobile Health Innovation’ and ‘mWomen Best Mobile Product’ categories for its mobile health innovation Etisalat Mobile Baby, as well as the ‘Best Mobile Money Innovation’ award. Etisalat UAE successfully completed the highest 4G LTE speed test in the world, reaching speeds of 300 Mbps.Etisalat suspends its operation in India post Supreme Court decision of India cancellation of 122 2G licenses issued in 2008.

2011Etisalat introduces the first real 4G (LTE) experience to its customers in the UAE

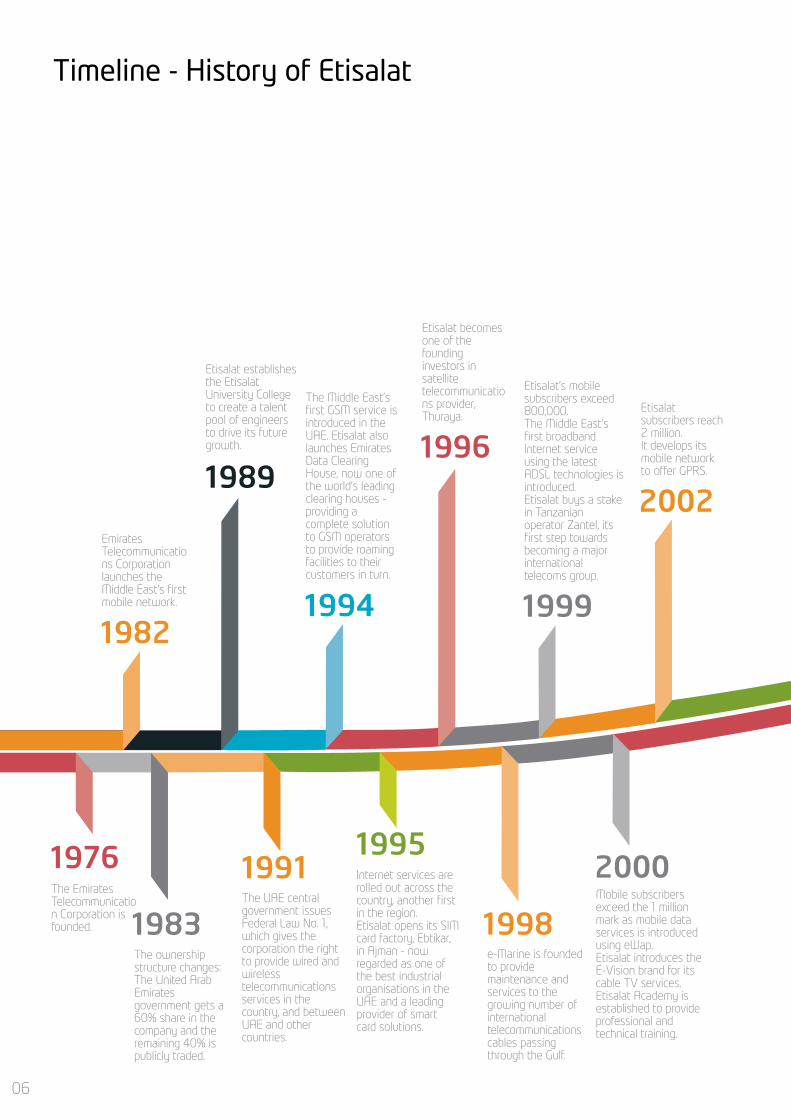

Etisalat wins the third mobile license in Egypt and plans to introduce the country’s first 3G network. It is also awarded a license to provide mobile services in Afghanistan. In the UAE, Etisalat begins offering BlackBerry®services.Etisalat Services Holding is formed to manage eight business units that offer mission-critical telecoms related services to the industry. This includes EDCH, e-Marine, Ebtikar, Etisalat Academy, E-Facility Management, e-Real Estate, Etisalat Directory Services and Tamdeed.

1976The Emirates Telecommunication Corporation is founded.

1982

Emirates Telecommunications Corporation launches the Middle East’s first mobile network.

1983The ownership structure changes: The United Arab Emirates government gets a 60% share in the company and the remaining 40% is publicly traded.

1991The UAE central government issues Federal Law No. 1, which gives the corporation the right to provide wired and wireless telecommunications services in the country, and between UAE and other countries.

1995Internet services are rolled out across the country, another first in the region. Etisalat opens its SIM card factory, Ebtikar, in Ajman - now regarded as one of the best industrial organisations in the UAE and a leading provider of smart card solutions.

1998e-Marine is founded to provide maintenance and services to the growing number of international telecommunications cables passing through the Gulf.

2000Mobile subscribers exceed the 1 million mark as mobile data services is introduced using eWap.Etisalat introduces the E-Vision brand for its cable TV services. Etisalat Academy is established to provide professional and technical training.

1989

Etisalat establishes the Etisalat University College to create a talent pool of engineers to drive its future growth. 1996

Etisalat becomes one of the founding investors in satellite telecommunications provider, Thuraya.

1994

The Middle East’s first GSM service is introduced in the UAE. Etisalat also launches Emirates Data Clearing House, now one of the world’s leading clearing houses - providing a complete solution to GSM operators to provide roaming facilities to their customers in turn.

2004

Etisalat wins the second license to operate in Saudi Arabia thereby introducing Etihad Etisalat – Mobily. It also buys a stake in Canar, a new fixed line operator in Sudan.

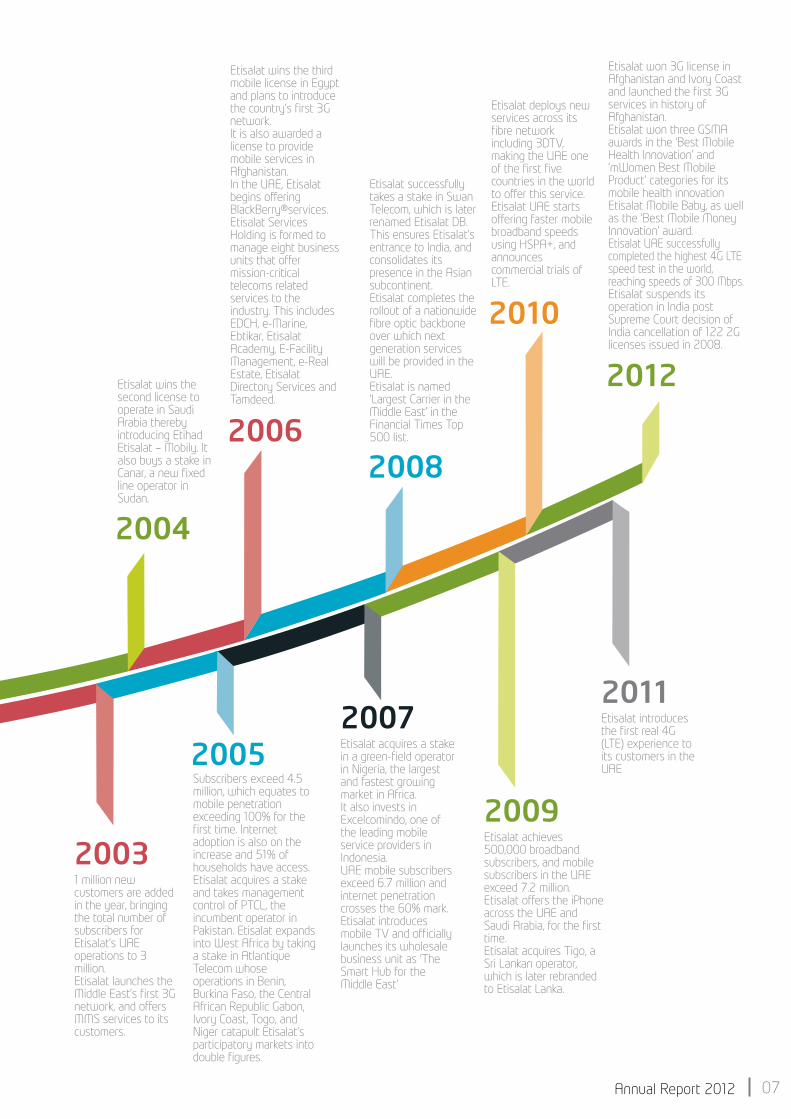

2008

Etisalat successfully takes a stake in Swan Telecom, which is later renamed Etisalat DB. This ensures Etisalat’s entrance to India, and consolidates its presence in the Asian subcontinent. Etisalat completes the rollout of a nationwide fibre optic backbone over which next generation services will be provided in the UAE. Etisalat is named ‘Largest Carrier in the Middle East’ in the Financial Times Top 500 list.

2010

Etisalat deploys new services across its fibre network including 3DTV, making the UAE one of the first five countries in the world to offer this service. Etisalat UAE starts offering faster mobile broadband speeds using HSPA+, and announces commercial trials of LTE.

1999

Etisalat’s mobile subscribers exceed 800,000.The Middle East’s first broadband Internet service using the latest ADSL technologies is introduced. Etisalat buys a stake in Tanzanian operator Zantel, its first step towards becoming a major international telecoms group.

2002

Etisalat subscribers reach 2 million.It develops its mobile network to offer GPRS.

20031 million new customers are added in the year, bringing the total number of subscribers for Etisalat’s UAE operations to 3 million. Etisalat launches the Middle East’s first 3G network, and offers MMS services to its customers.

2007Etisalat acquires a stake in a green-field operator in Nigeria, the largest and fastest growing market in Africa. It also invests in Excelcomindo, one of the leading mobile service providers in Indonesia. UAE mobile subscribers exceed 6.7 million and internet penetration crosses the 60% mark. Etisalat introduces mobile TV and officially launches its wholesale business unit as ‘The Smart Hub for the Middle East’

2009Etisalat achieves 500,000 broadband subscribers, and mobile subscribers in the UAE exceed 7.2 million. Etisalat offers the iPhone across the UAE and Saudi Arabia, for the first time.Etisalat acquires Tigo, a Sri Lankan operator, which is later rebranded to Etisalat Lanka.

2005

2006

Subscribers exceed 4.5 million, which equates to mobile penetration exceeding 100% for the first time. Internet adoption is also on the increase and 51% of households have access. Etisalat acquires a stake and takes management control of PTCL, the incumbent operator in Pakistan. Etisalat expands into West Africa by taking a stake in Atlantique Telecom whose operations in Benin, Burkina Faso, the Central African Republic Gabon, Ivory Coast, Togo, and Niger catapult Etisalat’s participatory markets into double figures.

06

Timeline - History of Etisalat

2012

Etisalat won 3G license in Afghanistan and Ivory Coast and launched the first 3G services in history of Afghanistan. Etisalat won three GSMA awards in the ‘Best Mobile Health Innovation’ and ‘mWomen Best Mobile Product’ categories for its mobile health innovation Etisalat Mobile Baby, as well as the ‘Best Mobile Money Innovation’ award. Etisalat UAE successfully completed the highest 4G LTE speed test in the world, reaching speeds of 300 Mbps.Etisalat suspends its operation in India post Supreme Court decision of India cancellation of 122 2G licenses issued in 2008.

2011Etisalat introduces the first real 4G (LTE) experience to its customers in the UAE

Etisalat wins the third mobile license in Egypt and plans to introduce the country’s first 3G network. It is also awarded a license to provide mobile services in Afghanistan. In the UAE, Etisalat begins offering BlackBerry®services.Etisalat Services Holding is formed to manage eight business units that offer mission-critical telecoms related services to the industry. This includes EDCH, e-Marine, Ebtikar, Etisalat Academy, E-Facility Management, e-Real Estate, Etisalat Directory Services and Tamdeed.

1976The Emirates Telecommunication Corporation is founded.

1982

Emirates Telecommunications Corporation launches the Middle East’s first mobile network.

1983The ownership structure changes: The United Arab Emirates government gets a 60% share in the company and the remaining 40% is publicly traded.

1991The UAE central government issues Federal Law No. 1, which gives the corporation the right to provide wired and wireless telecommunications services in the country, and between UAE and other countries.

1995Internet services are rolled out across the country, another first in the region. Etisalat opens its SIM card factory, Ebtikar, in Ajman - now regarded as one of the best industrial organisations in the UAE and a leading provider of smart card solutions.

1998e-Marine is founded to provide maintenance and services to the growing number of international telecommunications cables passing through the Gulf.

2000Mobile subscribers exceed the 1 million mark as mobile data services is introduced using eWap.Etisalat introduces the E-Vision brand for its cable TV services. Etisalat Academy is established to provide professional and technical training.

1989

Etisalat establishes the Etisalat University College to create a talent pool of engineers to drive its future growth. 1996

Etisalat becomes one of the founding investors in satellite telecommunications provider, Thuraya.

1994

The Middle East’s first GSM service is introduced in the UAE. Etisalat also launches Emirates Data Clearing House, now one of the world’s leading clearing houses - providing a complete solution to GSM operators to provide roaming facilities to their customers in turn.

2004

Etisalat wins the second license to operate in Saudi Arabia thereby introducing Etihad Etisalat – Mobily. It also buys a stake in Canar, a new fixed line operator in Sudan.

2008

Etisalat successfully takes a stake in Swan Telecom, which is later renamed Etisalat DB. This ensures Etisalat’s entrance to India, and consolidates its presence in the Asian subcontinent. Etisalat completes the rollout of a nationwide fibre optic backbone over which next generation services will be provided in the UAE. Etisalat is named ‘Largest Carrier in the Middle East’ in the Financial Times Top 500 list.

2010

Etisalat deploys new services across its fibre network including 3DTV, making the UAE one of the first five countries in the world to offer this service. Etisalat UAE starts offering faster mobile broadband speeds using HSPA+, and announces commercial trials of LTE.

1999

Etisalat’s mobile subscribers exceed 800,000.The Middle East’s first broadband Internet service using the latest ADSL technologies is introduced. Etisalat buys a stake in Tanzanian operator Zantel, its first step towards becoming a major international telecoms group.

2002

Etisalat subscribers reach 2 million.It develops its mobile network to offer GPRS.

20031 million new customers are added in the year, bringing the total number of subscribers for Etisalat’s UAE operations to 3 million. Etisalat launches the Middle East’s first 3G network, and offers MMS services to its customers.

2007Etisalat acquires a stake in a green-field operator in Nigeria, the largest and fastest growing market in Africa. It also invests in Excelcomindo, one of the leading mobile service providers in Indonesia. UAE mobile subscribers exceed 6.7 million and internet penetration crosses the 60% mark. Etisalat introduces mobile TV and officially launches its wholesale business unit as ‘The Smart Hub for the Middle East’

2009Etisalat achieves 500,000 broadband subscribers, and mobile subscribers in the UAE exceed 7.2 million. Etisalat offers the iPhone across the UAE and Saudi Arabia, for the first time.Etisalat acquires Tigo, a Sri Lankan operator, which is later rebranded to Etisalat Lanka.

2005

2006

Subscribers exceed 4.5 million, which equates to mobile penetration exceeding 100% for the first time. Internet adoption is also on the increase and 51% of households have access. Etisalat acquires a stake and takes management control of PTCL, the incumbent operator in Pakistan. Etisalat expands into West Africa by taking a stake in Atlantique Telecom whose operations in Benin, Burkina Faso, the Central African Republic Gabon, Ivory Coast, Togo, and Niger catapult Etisalat’s participatory markets into double figures.

07Annual Report 2012

08

The strides taken by Etisalat in 2012 will have a positive impact on the Company’s future growth, and its vision of becoming one of the most admirable telecommunications companies in the world

09Annual Report 2012

Chairman’s Statement

As the global telecommunications industry continues to transform, as it has for decades, Etisalat Group’s commitment to ensure that investment decisions are based on several key criteria, including the real value they add to the social development and economic growth of a country, will allow Etisalat to manage risk while growing its foundation in 2013.

Etisalat knows that the telecommunications business is no longer just about a voice call or carrier signal – It is about data and, specifically, delivering innovative services that drive social development and accelerate economic growth. Our job is to ensure that we deliver those innovative services across robust networks and offer the best customer experience to help maximise revenues from the growing data pipeline.

Our commitment to providing cutting edge services across our markets remains unwavering. This year, we announced the successful trial of the world’s fastest mobile network, providing speeds of up to 300Mbps. We also announced that we have deployed over three million kilometres of fibre optic cables across the UAE, making the UAE one of the most connected nations in the world in Fibre-To-The-Home (FTTH). We are also continuing to roll out innovative services such as near field communication (NFC), money transfer facilities and machine-to-machine (M2M) solutions across our markets – solutions that provide value to our customers and position Etisalat Group as a leader in innovation.

Etisalat Group also recognizes the potential that emerging markets, including Pakistan and Nigeria, offer to Etisalat and its shareholders. Our global footprint, which includes operations in 15 markets, positions Etisalat Group well to capitalize on the benefits associated with broadband growth. Nigeria, for example, represents tremendous growth potential for Etisalat Group. As one of the strongest and most rapidly growing economies in Africa, and with

Internet penetration at approximately 28 per cent, Nigeria represents a real opportunity for 3G operators like Etisalat Group.

We do believe that our assets in high-population, high-growth markets present real growth opportunities, especially if we focus on three key areas: networks, innovation and partnerships. For example, Etisalat Group has invested in state-of-the-art Next Generation Networks to ensure that we can manage the influx in data. And, our development of innovative digital services, specifically in the fields of mobile health (mHealth) and mobile commerce (mCommerce) has already positioned us ahead of our competitors and established our strong track record in developing services that contribute to social development and economic growth. Finally, our partnerships with key network vendors, device manufacturers and content providers will allow Etisalat Group to grow and better connect customers with services that they want and need in our growing markets.

The telecoms industry is redefining itself once more and becoming increasingly reliant on new sources of revenue including data, which is expanding globally at a rapid pace.

In the years to come, Etisalat believes that tele-media, which brings together a new technology ecosystem of inter-connected business models that involves telcos and operators with content providers and third parties, will begin to transform the customer experience, increasing availability, content and broadband uptake and adding new revenue models for the company, allowing Etisalat to maintain a position of leadership.

In 2013, our CEO will be taking on an additional leadership role within our industry. Not only will this new opportunity allow Etisalat to contribute to the growth of the Etisalat Group, but it will position Etisalat to help grow

the industry as a whole. I am proud to announce that Etisalat Group’s CEO will be joining the GSMA Board alongside 24 other CEOs and senior executives from our peers across the global telecommunications industry to work together to develop policies and tactics that will benefit individuals, organizations and governments throughout the world.

Etisalat Group now has an outstanding senior management team that is strongly committed to the growth of the organization and its contribution to its shareholders, the UAE and the markets we operate in. The senior management team is also supported by thousands of dedicated employees around the globe whose commitment to excellence allows Etisalat to achieve its goals of creating and delivering better services that positively impact people’s lives, and I would like to thank them for their unwavering dedication.

Our achievements in 2012 would not have been achieved without the support of H.H. the President of the UAE, H.H. the Prime Minister, H.H. the Crown Prince of Abu Dhabi and the UAE government’s continued support for Etisalat. I’d also like to acknowledge the support of the governments and regulators in all of our operating countries and thank our customers for their loyalty throughout the year.

It has been an honour to lead such a strong team in 2012, and I look forward to another year of growth and prosperity in 2013, through delivering new and innovative technologies and services to our clients across our markets of operation.

Respectfully yours,

Eissa Mohamed Al SuwaidiChairman

10

Mohamed Hadi Ahmed Abdulla Al Hussaini

MemberInvestment & Finance Committee

Abdulla Mohamed Saeed Ghobash Al MarriMemberInvestment & Finance Committee

Shoaib Mir Hashim KhooryMemberNomination & Remuneration Committee

Abdelmonem Bin Eisa Bin Nasser Alserkal

MemberNomination & Remuneration

Committee

Board of Directors

Sheikh Ahmed Mohamed Sultan Bin Suroor Al DhaheriMemberAudit Committee

Eissa Mohamed Al SuwaidiChairman

Investment & Finance Committee

11Annual Report 2012

Abdulla Salem Al DhaheriMemberChairman-Nomination & Remuneration Committee

Mana Mohamed Saeed Al MullaMemberAudit Committee

Mubarak Rashed Al MansouriMember

Nomination & Remuneration Committee

Hasan Al HosaniCorporate Secretary

Essa Abdulfattah KazimMember

Chairman-Audit Committee

Khalaf Bin Ahmed Al OtaibaVice Chairman

Member-Investment & Finance Committee

12

Etisalat’s long-term strategy guided us through the opportunities and challenges presented by market forces

13Annual Report 2012

Chief Executive Officer’s Statement

In 2012, the company’s long-term strategy guided us through the opportunities and challenges presented by market forces, and this is reflected in our strong performance. Our long-term strategy also guided us through growth in international emerging markets – and will continue to set the tone as we introduce new services to customers around the globe and expand our portfolio.

Over the course of 2012, Etisalat Group operations demonstrated growth in terms of both size and revenue, retaining and acquiring more customers and attracting higher revenues across our international operations. The aggregate number of subscribers, including subsidiaries and associates, reached over 139 million. Group revenues increased by 2% to reach AED 32.9 billion, driven by growth in our international operations that now contribute 29% of our consolidated revenue.

Etisalat Group’s overall financial results show a steadily increasing revenue base from our diverse portfolio of operations. Operating profits before federal royalty increased by 13% from last year. Etisalat achieved a net profit before Federal Royalty of AED 13.2 billion. Net profit after Federal Royalty amounted to AED 6.7 billion and EPS of 85 fils, compared to AED 5.8 billion and 74 fils in 2011. Meanwhile, capital expenditure decreased by 3% to reach AED 4.2 billion, representing 13% of the current year’s revenues.

In late 2012, the Cabinet of Ministers of UAE issued decision in respect of a new royalty mechanism applicable to

Etisalat. Under the new mechanism a distinction is made between revenue earned from services regulated by Telecommunications Regulatory Authority (“TRA”) and non-regulated services as well as between foreign and local profits.

Etisalat is required to pay 15 % royalty fee on the UAE regulated revenues and 35 % of net profit after deduction of the 15 % royalty fee on the UAE regulated revenues. In respect of foreign profit, the 35 % royalty is reduced by the amount that the foreign profit has already been subject to foreign taxes.

In 2012, our strategy enabled cash liquidity and wise investments for sustainable growth for both the Group and our investors. Reported earnings for the year were positively impacted by the sale of a 9.1% stake in PT XL Axiata Tbk (“XL”). The sale of 775 million shares to institutional investors capitalized on a rally in XL Axiata’s stock price and resulted in gross proceeds of AED 1,870 million to Etisalat Group.

In addition, we maintained our historically strong cash position, allowing us to reaffirm our investment-grade credit ratings in the annual review. Etisalat Group has been rated AA- by S&P, A+ by Fitch and Aa3 by Moody’s, making it the highest overall rated telecommunications company in the GCC and the fourth-highest rated telecommunications company in the world. In light of these results, and in line with what has occurred in previous years, the board has proposed dividends of 70 fils per

14

share, a pay-out of 82% of earnings per share.

On a global level, our international operations witnessed strong growth, achieving AED 9.5 billion in revenues during 2012, registering a healthy growth of 11%. International revenues for the year accounted for 29% of consolidated Group revenues, led by the solid performance of Etisalat Misr in Egypt. On the operating profit level, international operations have increased their contribution to Group results.

In the UAE, our operations have witnessed further competitive pressure, especially in the mobile segment. In 2012, we were able to maintain our market share in the UAE market, and we were also able to retain a dominant share of revenues due in large part to customer loyalty linked to superior services and quality of the network. We were also notably able to achieve a healthy gain in our mobile subscriber base throughout the year, thanks to our continuing efforts to revamp of our sales channels and a focus on value proposition in our latest mobile offerings.

Over the past decade, the telecoms industry has seen noticeable growth in the data and Internet segments. To capitalize on this trend, the Corporation spent in the UAE AED 1.8 billion during the year on infrastructure, mainly to enhance the fiber-optic network and develop the LTE core and access network.

Those investments are paying

dividends, underlined by the achievement of the highest 4G LTE speed test in the world, reaching speeds of 300 Mbps. Etisalat Group has now deployed over three million kilometres of fibre optic across the UAE – a significant accomplishment. The UAE is now one of the most “fibre-to-the-home” connected nations in the world.

Over the past year, Etisalat Group’s performance and innovative offerings have been recognized with several international awards, including three GSMA awards for ‘Best Mobile Health Innovation’, ‘mWomen Best Mobile Product’ and ‘Best Mobile Money Innovation’, as well as three International Business Awards for Most Innovative Company of the Year in the Middle East and Africa, Best New Product or Service of the Year - Health & Pharmaceuticals Service and Corporate Social Responsibility Program of the Year, in addition to myriad other awards from the World Communication Awards, the Nigerian Communications Commission (NCC), CSR Business Excellence, Forbes Middle East, the Connected World Awards and Telecom Review.

In 2012, Etisalat Group continued its policy of supporting and engaging across international industry platforms. The United Arab Emirates hosted significant International Telecommunication Union (ICT) events in 2012 including ITU Telecom World 2012, the World Telecommunication Standardization Assembly (WTSA-12) and the World Conference on

International Telecommunications (WCIT-12). The ITU events gave us a platform and a significant opportunity to positively influence and shape a new era for the telecommunications sector, and its vision for the future of ICT regulations and the importance of developing policies that enables the creation of a competitive business environment both on a local and global scale. They allowed Etisalat Group to address the challenges to standardisation in the ICT and telecommunications industries, the opportunities that cooperation can deliver in areas including healthcare, transportation and utilities, and strategies for bridging the gaps in establishing standards across regions and markets.

Etisalat Group also made a significant contribution to the shape of the industry’s future at 2012’s Mobile World Congress leadership Summit in Barcelona with top group executives presenting our vision to delegates from around the globe. And, in December 2012, Etisalat being elected to the Board of GSMA, among top Global executives from the industry.

One key focus for 2013 is the delivery of innovative solutions through applied technology – such as mHealth and mCommerce, M2M and cloud networking – and how they are helping to shape the future of the way we live and work and accelerate social development and economic growth. Digital services are set to grow from $57billion to $213billion by 2015. This year, like 2012, will see Etisalat Group

15Annual Report 2012

introducing a number of innovative solutions across our markets that will benefit our consumers and society as a whole.

Recognising the potential revenues in digital services, Etisalat Group continued its progress on restructuring with the introduction of the Digital Services Unit in 2012. The new division, which will focus on various industry verticals such as Machine-to-Machine (M2M), cloud services, commerce, digital advertisement, advanced communications, digital entertainment, and video services, aims to boost the Group’s position in the digital eco-system and drive innovation and advanced services to Group customers across all areas of operation. As part of its development in M2M technology, Etisalat Group signed an agreement with Pacific Controls to jointly work towards offering M2M applications and support to clients across the Group’s footprint.

As we look forward to the opportunities 2013 will present to us, I’d like to reflect on the contributions our employees and management team made towards the success we achieved in 2012. Our results were strong; we received international recognition regarding innovation and our contributions towards transforming communities and economies; and, we debated shoulder-to-shoulder with our peers at global industry events. Our achievements are the result of the dedication, hard work and professionalism of our employees, and I wish to take this opportunity to recognise their efforts and applaud their successes.

It has been an honour to lead the Company over the past year, and I look forward to leading our dedicated team into the opportunities and challenges that 2013 will bring.

Few global telecommunications corporations have had the year-over-

year success that Etisalat Group has had.

Our success is tied to our strategy to enrich customer experience, nurture advanced technologies, govern decisively, achieve broadband leadership, grow with a sustainable portfolio and excel in execution – and our commitment to providing value to our shareholders.

Connectivity matters to all of us. Across the UAE, and around the globe, in 2013, and in the years to come, Etisalat Group will continue to provide customers with the solutions and services they need, with the highest levels of integrity and reliability.

Respectfully yours,

Ahmad Abdulkarim JulfarChief Executive Officer

16

Ahmad Abdulkarim JulfarChief Executive Officer- Etisalat Group

Mr. Julfar was appointed as the CEO of the Etisalat Group in August 2011. Prior to this appointment, he was the Chief Operating Officer of EG. Mr. Julfar has more than 25 years’ experience in the telecommunication sector and has served in various management positions including General Manager of eCompany, ComTrust and Etisalat’s Dubai region. In addition, Mr. Julfar serves on the boards of Mobily, where he is the Chairman of the Risk Management committee, Etisalat Misr and Etisalat Services Holding. Mr. Julfar holds Bachelor’s Degrees in Civil Engineering and Computer Science from the USA.

Essa Al HaddadChief Regional Officer /Africa, Etisalat Group

Essa Al Haddad was appointed as the Chief Regional Officer, Africa, of the Etisalat Group in January 2013. Prior to this appointment, he was the Chief Commercial Officer of EG. In his 34 years of experience, Mr. Al Haddad has served in various senior leadership positions including Executive Vice President of Engineering of Etisalat UAE, Chief Marketing Officer Etisalat UAE and Chief Marketing Officer of EG. Mr. Al Haddad is Chairman of Zantel, Vice Chairman of Etisalat Nigeria and board member of Atlantique Telecom, Mobily and Canar. He holds a higher diploma in Telecom Engineering and an MBA from the UK.

Serkan OkandanChief Financial Officer, Etisalat Group

Mr. Okandan joined Etisalat in January 2012 as Chief Financial Officer of the Etisalat Group. Prior to his appointment, he was the Group Chief Financial Officer of Turkcell. Mr. Okandan started his professional career at PricewaterhouseCoopers in 1992, and worked for DHL and Frito Lay as a Financial Controller before joining Turkcell. Mr. Okandan is a board member and Chairman of the audit committee of Etisalat Nigeria, PTCL, Ufone and a board member of Etisalat Services Holding. Mr. Okandan graduated from Bosphorus University with a degree in Economics.

Dr. Daniel Ritz, Ph.DChief Strategy Officer, Etisalat Group

Daniel Ritz was appointed as Chief Strategy Officer for EG in February 2012. Prior to this appointment, he was the CSO at Swisscom Group where he held various positions including Board member of each of the Group’s Executive Board, Fastweb, Belgacom and Swisscom IT Services. He also served as Chairman of Swisscom’s Hospitality Services and as CEO of Swisscom (Central & Eastern Europe). Prior to joining Swisscom, he was a partner at BCG. Dr. Ritz also serves on the Board of Atlantique Telecom, Thuraya, PTCL and Ufone. Dr. Ritz holds a Ph.D from the Hochschule St. Gallen in Switzerland.

Management Team

17Annual Report 2012

Saleh Al Abdooli Chief Executive Officer, Etisalat UAE

Engineer Saleh Al Abdooli was appointed as Chief Executive Officer of Etisalat UAE in April 2012. A strong and charismatic leader, Saleh rose to international fame after his resounding success in Egypt as the CEO of Etisalat Misr. He built and launched the first 3G operator in Egypt in 7 months. In less than five years, he achieved 27% of revenue share, 28% market share, 36% of EBITDA margin, and 99% 2G/3G coverage. Al Abdooli holds Bachelor’s and Master’s in Electrical Eng. and Telecom from University of Colorado at Boulder, USA.

Saeed Al Hamli Chief Executive Officer, Etisalat Misr

Mr. Al Hamli was appointed as Chief Executive Officer of Etisalat Misr in April 2012. Prior to this role, he was the Chief Executive Officer of Etisalat Afghanistan since 2007. Mr. Al Hamli has more than 20 years of experience at Etisalat and Thuraya where he was the Chief Commercial Officer before moving to Afghanistan. Mr. Al Hamli also serves on the board of Etisalat Misr. Mr. Saeed holds a Bachelor’s of Science degree in Electrical Engineering from USA and Executive Master’s of Business Administration degree from the American University of Sharjah.

Jamal AljarwanChief Regional Officer/ Asia, Etisalat Group

Jamal Al Jarwan was appointed as the Chief Regional Officer of the Asian cluster of EG in October 2011. Prior to this position, he was the Chief International Investments Officer of EG. Mr. Al Jarwan started his career at Etisalat in 1988 and held various positions including Chief Commercial Officer at Thuraya. Mr. Al Jarwan is a member of the Board of Etisalat Afghanistan, Etisalat Sri Lanka, PTCL and Ufone. He holds a Bachelor’s degree in Business from Dayton University in the United States and an MBA in International Management Development from Lausanne University, Switzerland.

Abdulaziz Al SawalehChief Human Resources Officer, Etisalat Group

Mr. Al Sawaleh is the Chief Human Resources Officer (CHRO) of the Etisalat Group. Prior to this position, he was the CHRO of Etisalat UAE. Mr. Al Sawaleh has more than 25 years’ experience in various leadership positions. He is responsible for leading the global Human Capital strategies including the areas of talent development, organization effectiveness, compensation & benefits and Performance Management. He is a board member of Atlantique Telecom and Etisalat Services Holding. Mr. Al Sawaleh holds an MBA degree in Global Leadership Management from UAE University and a BBA degree from the USA.

Khalid Al KafManaging Director and Chief Executive Officer, Etihad Etisalat (Mobily)

Khalid Al Kaf was appointed as Chief Executive Officer and Managing Director of Etihad Etisalat (Mobily) in July 2005. Prior to this appointment, Mr. Al Kaf worked for over 19 years with Etisalat in various capacities. He was the General Manager of Etisalat’s Network Services division before being appointed as the start up project manager and later CEO for Mobily. Mr. Al Kaf is the Chairman of the Board of Directors of Etisalat Sri Lanka and is a board member of Mobily. Mr. Al Kaf holds a Bachelor of Science degree from George Washington University, USA.

18

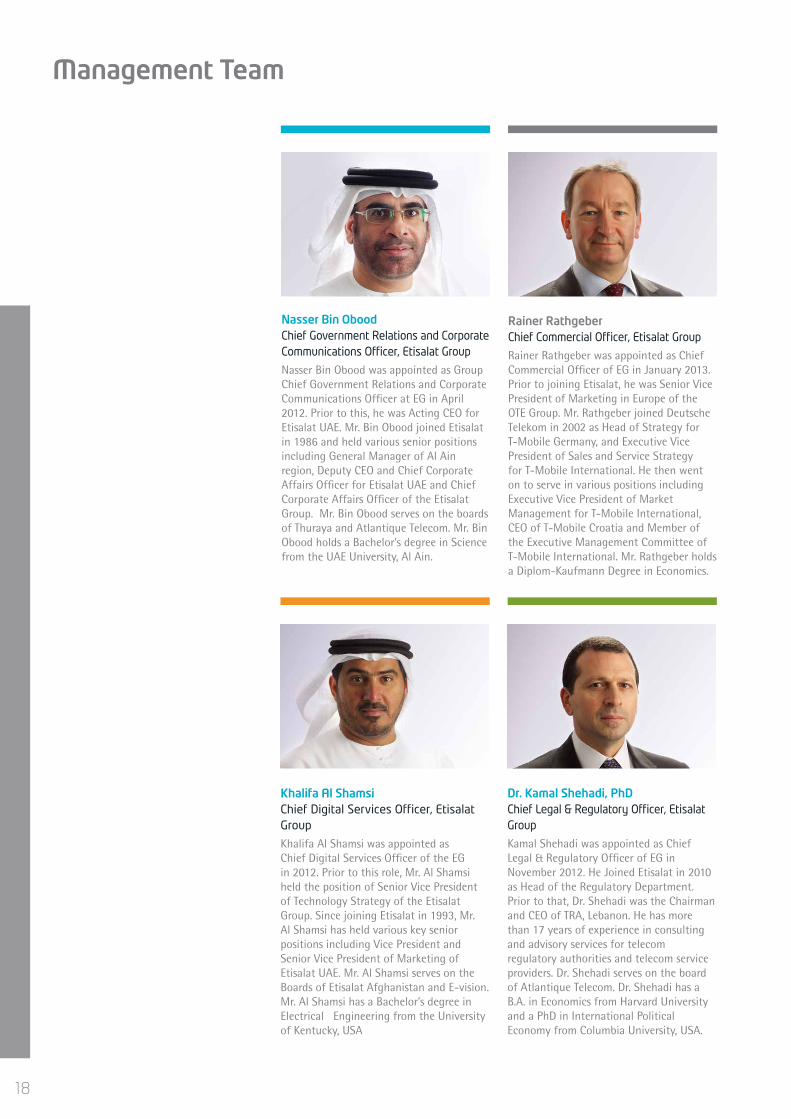

Khalifa Al ShamsiChief Digital Services Officer, Etisalat Group

Khalifa Al Shamsi was appointed as Chief Digital Services Officer of the EG in 2012. Prior to this role, Mr. Al Shamsi held the position of Senior Vice President of Technology Strategy of the Etisalat Group. Since joining Etisalat in 1993, Mr. Al Shamsi has held various key senior positions including Vice President and Senior Vice President of Marketing of Etisalat UAE. Mr. Al Shamsi serves on the Boards of Etisalat Afghanistan and E-vision. Mr. Al Shamsi has a Bachelor’s degree in Electrical Engineering from the University of Kentucky, USA

Rainer RathgeberChief Commercial Officer, Etisalat Group

Rainer Rathgeber was appointed as Chief Commercial Officer of EG in January 2013. Prior to joining Etisalat, he was Senior Vice President of Marketing in Europe of the OTE Group. Mr. Rathgeber joined Deutsche Telekom in 2002 as Head of Strategy for T-Mobile Germany, and Executive Vice President of Sales and Service Strategy for T-Mobile International. He then went on to serve in various positions including Executive Vice President of Market Management for T-Mobile International, CEO of T-Mobile Croatia and Member of the Executive Management Committee of T-Mobile International. Mr. Rathgeber holds a Diplom-Kaufmann Degree in Economics.

Dr. Kamal Shehadi, PhDChief Legal & Regulatory Officer, Etisalat Group

Kamal Shehadi was appointed as Chief Legal & Regulatory Officer of EG in November 2012. He Joined Etisalat in 2010 as Head of the Regulatory Department. Prior to that, Dr. Shehadi was the Chairman and CEO of TRA, Lebanon. He has more than 17 years of experience in consulting and advisory services for telecom regulatory authorities and telecom service providers. Dr. Shehadi serves on the board of Atlantique Telecom. Dr. Shehadi has a B.A. in Economics from Harvard University and a PhD in International Political Economy from Columbia University, USA.

Nasser Bin Obood Chief Government Relations and Corporate Communications Officer, Etisalat Group

Nasser Bin Obood was appointed as Group Chief Government Relations and Corporate Communications Officer at EG in April 2012. Prior to this, he was Acting CEO for Etisalat UAE. Mr. Bin Obood joined Etisalat in 1986 and held various senior positions including General Manager of Al Ain region, Deputy CEO and Chief Corporate Affairs Officer for Etisalat UAE and Chief Corporate Affairs Officer of the Etisalat Group. Mr. Bin Obood serves on the boards of Thuraya and Atlantique Telecom. Mr. Bin Obood holds a Bachelor’s degree in Science from the UAE University, Al Ain.

Management Team

19Annual Report 2012

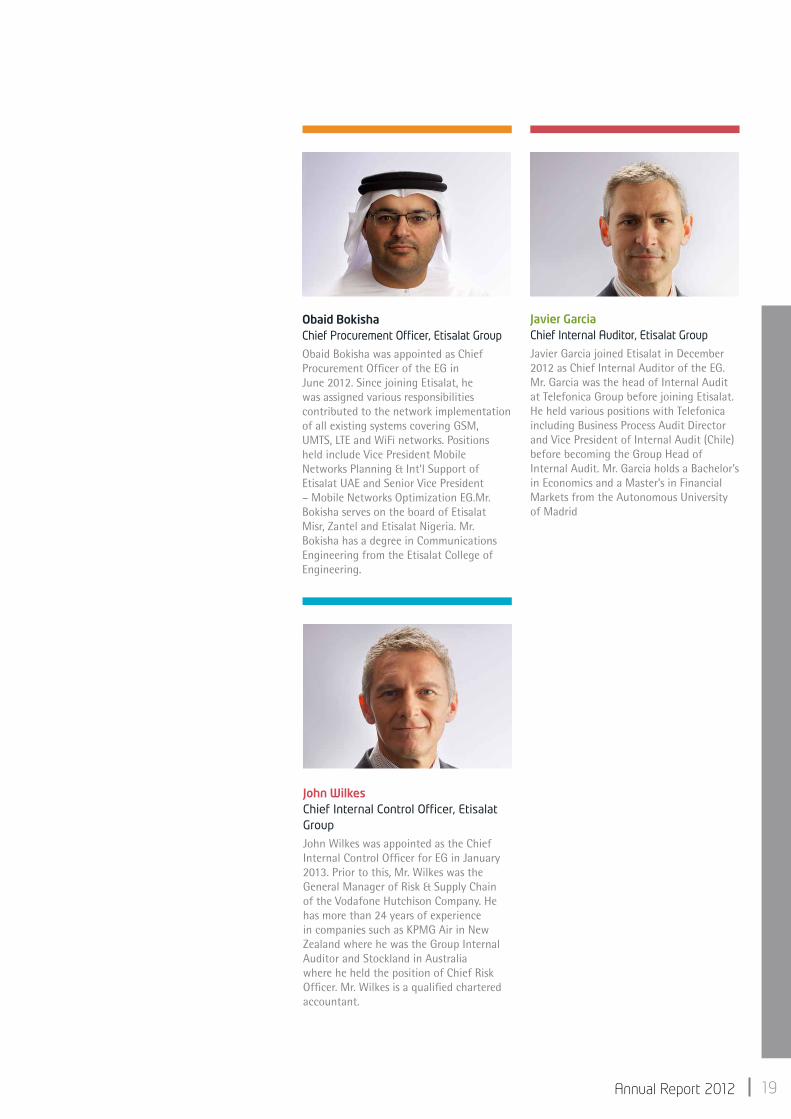

Obaid Bokisha Chief Procurement Officer, Etisalat Group

Obaid Bokisha was appointed as Chief Procurement Officer of the EG in June 2012. Since joining Etisalat, he was assigned various responsibilities contributed to the network implementation of all existing systems covering GSM, UMTS, LTE and WiFi networks. Positions held include Vice President Mobile Networks Planning & Int’l Support of Etisalat UAE and Senior Vice President – Mobile Networks Optimization EG.Mr. Bokisha serves on the board of Etisalat Misr, Zantel and Etisalat Nigeria. Mr. Bokisha has a degree in Communications Engineering from the Etisalat College of Engineering.

Javier GarciaChief Internal Auditor, Etisalat Group

Javier Garcia joined Etisalat in December 2012 as Chief Internal Auditor of the EG. Mr. Garcia was the head of Internal Audit at Telefonica Group before joining Etisalat. He held various positions with Telefonica including Business Process Audit Director and Vice President of Internal Audit (Chile) before becoming the Group Head of Internal Audit. Mr. Garcia holds a Bachelor’s in Economics and a Master’s in Financial Markets from the Autonomous University of Madrid

John WilkesChief Internal Control Officer, Etisalat Group

John Wilkes was appointed as the Chief Internal Control Officer for EG in January 2013. Prior to this, Mr. Wilkes was the General Manager of Risk & Supply Chain of the Vodafone Hutchison Company. He has more than 24 years of experience in companies such as KPMG Air in New Zealand where he was the Group Internal Auditor and Stockland in Australia where he held the position of Chief Risk Officer. Mr. Wilkes is a qualified chartered accountant.

20

In recent years, the Etisalat Group (EG) has been successfully engaged in a strategy of growing its international operations at record rates, while also maintaining the core strength of its domestic business in the UAE. In 2012, the group updated its corporate strategy from the ENGAGE pillars that were presented in the past to a newer, fresher outlook that sets Etisalat at the heart of a rapidly evolving telecoms industry.

Etisalat’s refreshed corporate strategy aims to enhance the company’s focus and attention towards the most critical internal and external factors, which will shape its long-term aspirations. Etisalat Group recognises that within the global telecoms industry it is facing new and exciting opportunities; the sector is transforming rapidly due to changes in consumption patterns and strong innovations in technology, and the company believes that telecom operators will remain the key enablers of the “Connected Society” of the future. Operators, like EG, will play a vital role in enhancing the customer’s experience by leveraging their in-depth knowledge of the customer, deploying enabling platforms for the overall industry and providing the much needed access infrastructure. With the increased complexity in the market comes further emphasis on operators to engage collaboratively with newer entrants in the digital world, which Etisalat is embracing through a wide range of international partnerships.

Looking forward, the worldwide telecommunications industry – with revenues of approximately USD1.7 trillion at the end of 2011 – will continue to represent a sizeable and attractive industry. In the coming years, the sector’s growth potential will be driven largely by emerging markets,

where Etisalat Group will continue to play an active role. In Etisalat’s current footprint alone, it is envisaged that there will be significant growth potential in the telecommunications industry, providing EG ample room for further growth. This growth will be driven primarily by broadband, as well as voice in some markets, and new revenue streams across the company’s footprint. The potential opportunities from the enterprise segment, as well as the fixed line business, also remain significant in selected markets. Etisalat fully intends to be one of the leaders of this growth and the company’s new ‘six pillars’ strategy captures its plans to achieve that ambition.

Etisalat Group’s 2017 vision and mission have been established with these thoughts in mind. The new strategy also has several principal pillars designed to deliver the objectives of the organisation. Etisalat Group believes that the pillars of Service Offering, Customer Experience, Operational Excellence, Portfolio, One Company and People & Culture are the cornerstones of the organisation’s five-year strategy.

Service OfferingEtisalat will provide differentiation and innovation in services based on the dynamics of each market in which it operates. EG will enhance its customised and innovative products and services through a wide range of strategic partnerships, which will be supported by its state-of-the-art broadband infrastructure. In particular, new digital services such as Commerce, M2M and Cloud solutions will be spearheaded by the company’s newly created Digital Services Unit, which is supporting the rollout of relevant services across Etisalat Group’s international footprint. New

enterprise services will solve customer needs to ensure strengthening of the company’s position in all relevant business segments.

Customer ExperienceEtisalat works continuously on customer insight-based and focused propositions, and the enhancement of positive customer experience across all touchpoints. Knowing its customers and ensuring positive interactions with them throughout their lifecycle is a core competence to compete in Etisalat Group’s regions. On the technology front, Etisalat Group aims to reinforce its positioning as the most trustworthy and reliable operator through superior network and services quality.

Operational ExcellenceBoasting one of the highest margins in the business, Etisalat Group has firmly put in place several strategic initiatives to maintain strong profitability. Important efficiency improvement targets have been set across the organisation which will be implemented in the future through procurement measures, operational efficiencies, commercial synergies, and capital structure optimisation across the Group.

PortfolioRecognising the strong relevance of the three areas where Etisalat operates today (MENA, Africa and Asia), Etisalat Group’s investment strategy has been built around a continued focus on these regions. The strategy also includes a clear decision to position Etisalat Group as a strategic rather than financial investor and to focus on investments which provide Etisalat Group with operational influence over its assets. Etisalat Group’s future portfolio will therefore consist

Etisalat Group Strategy

To be the leading and most admired emerging markets telecom group

21Annual Report 2012

of strategic assets that will reinforce its presence in core markets and regions internationally.

One CompanyWith a strong footprint across 15 markets, Etisalat has the scale to deliver exceptional returns. The organisation is reinforcing a strategy which leverages this scale by enabling a common set of brand values, enhancing Etisalat’s integrated systems and processes, and ensuring robust and consistent governance, as well as maximised economies of scale across the Group.

People & CultureEtisalat’s people and corporate culture are at the heart of its strategy. Having the right talent and processes in place will continue to enable Etisalat Group to successfully execute its strategic pillars. For this reason, the company’s objectives are twofold: firstly, to attract, nurture and retain top talent within the organisation through succession planning, management reinforcement, and rewarding long-term performance, and secondly to streamline processes through delegation and accountability measures. Not compromising on these

areas, Etisalat views both its people and culture as a key priority for achieving success.

As Etisalat grows over the next five years, it aims to deliver exceptional customer service and an innovative and dynamic range of services across an optimised and efficient portfolio. With these key principles in place, Etisalat will be well positioned to achieve its vision of becoming the leading and most admired emerging markets telecom group.

Vision To be the leading and most admired emerging markets telecom group

Mission• Provide best in class total customer experience for retail and business• Deliver attractive returns to shareholders while investing in the company’s long term future• Support economic development and job creation through ICT & socially responsible behavior

Strategic Pillars

Service offering

Customer Experience

Operational Excellence Portfolio One Company People &

culture

22

Awards

Awards - Corporate

Awards - Innovation and Engineering

Corporate Social Responsibility Program of the Year

International Business Awards

Best Multinational Company Middle East & Africa

International Business Awards

SAMENA TelecommunicationsCouncilBest Telecom Company MENASA

International Leaderin Telecommunications Sector – Asia & Africa

Telecom World Middle East Awards

Middle East BusinessLeaders Summit

Best Operator

2011

Leader in Telecoms

Arab Achievement Awards

International Business AwardsMost Innovative Company

Training Excellence

Technical Leadership

African Investor of the Year

Asia BrandEmployer Awards

SAMENA Awards

Africa Business Awards

First Runner-Up in NGO-partnership

Arabia CSR Awards

Most powerful company in the UAE

Forbes Middle East

2010 2012

2010

Best FMC Operator of the Year

Best Customer Experience Provider of the Year

SAMENA

COMMS MEA

Fixed Line Operator of the year

Best Mobile Health InnovationBest Mobile Money Innovation

GSMA Global Mobile Awards

International Business Awards

Most Innovative Company in the Middle East and Africa

Video Services

Global Telecom Business Innovation Awards

TMT Finance Middle EastBest Broadband Provider

Best Fixed Line Provider

COMMS MEA

2011 2012

23Annual Report 2012

Awards - Marketing and Customer Care

Awards - Management

Best CEO

International Business Awards

Honorable mentionGreen Company

Middle East Business Leaders SummitLeadership in Corporate Social Responsibility

CMO Asia AwardsBest Telecoms Brand

2011International Business Awards

International Business Awards International

Business Awards

Asian Brand Employer Awards

Best Customer Care

Honourable MentionGreen ProgrammeHonourable MentionCSR Programme

Asia’s Most Preferred Brand

2010 2012

Best Mobile Product and Service for Women in Emerging Markets

GSMA Global Mobile Awards

Best New Product or Service of the Year Health

Best Telecom Operator Leader Award

CEO of the Year IT & Telecoms

SAMENA

Lifetime Achievement Award

Best Chairman Best Chairman

Best Executive of the Year in Telecommunications

Honorable Mention Best CFOHonorable MentionBest Executive

Middle East Excellence Awards Institute

Middle East Business Leaders Summit

2011

2012

International Business Awards

International Business Awards

International Business Awards

World Communications Awards

2010

24

Operational Highlights

Global Subscribers (m)

117

2011(1) 2012

139

Revenue (AED b)2011 2012

32.2 32.9

Subscribers(1)

Etisalat Group aggregate subscriber base grew to 139 million by end of December 2012 representing year-over-year growth of 18%. The Group reported strong net additions of 21 million subscribers as a result of growth across all of our operations. In the UAE active subscriber base grew to 9.0 million subscribers representing year-over-year growth of 8%. Mobile subscribers grew to 7 million representing a year over year growth of 12%. Fixed line subscribers reached 1.1 million representing year over year decline of 6%. However, this decline is due to the successful migration of customers to eLife segment (double play and triple play) that grew by 46% surpassing half million subscribers. Fixed broadband subscribers grew by 8% to 0.8 million. Africa cluster consolidated subscriber base grew by 29% to 12 million at the end of December 2012. While Asia cluster consolidated subscriber base reached 8.2 million declining year over year by 9% as year 2011 included the subscriber numbers of the Indian operation that was deconsolidated in March 2012.

RevenuesFor full year 2012, Etisalat Group consolidated revenues totaled AED 32.9 billion, increasing by 2% in comparison to last year. Etisalat UAE revenues of AED 22.7 billion for the year were 1% lower than revenues of prior year. The decline in revenues is mainly attributed to decrease in voice revenues in both mobile and fixed segments that were mostly compensated by growth in the internet and data segments. Revenues from international operations grew by 11% to AED 9.5 billion, representing 29% of group consolidated revenues. This growth in revenues is across all clusters. In Egypt, revenues of AED 5.1 billion, up 13% compared to the reported results of the last year. Revenue growth was mainly driven by customer acquisition and growth in mobile data segment. Africa cluster consolidated revenues grew to AED 2.8 billion representing an increase of 9% in comparison to the same period of last year. This revenues growth is mainly attributed to the operations in Benin, Togo and Canar. In Asia cluster, consolidated revenues grew to AED 1.6 billion representing a growth of 11% in comparison to the same period of last year. Growth is mainly driven by subscriber uptake in both Etisalat Afghanistan and Sri Lanka and launch of 3G services in Afghanistan.

(1) Subscriber number reported in FY 2011 had been adjusted to exclude XL Axiata operations due to reclassification of XL Axiata investment as “other investment available for sale” effective September 1, 2012.

25Annual Report 2012

2011 2012

EBITDA (AED b)

15.916.9

Net Profit (AED b) EPS(Fils)

2011

7485

5.8

6.7

2012

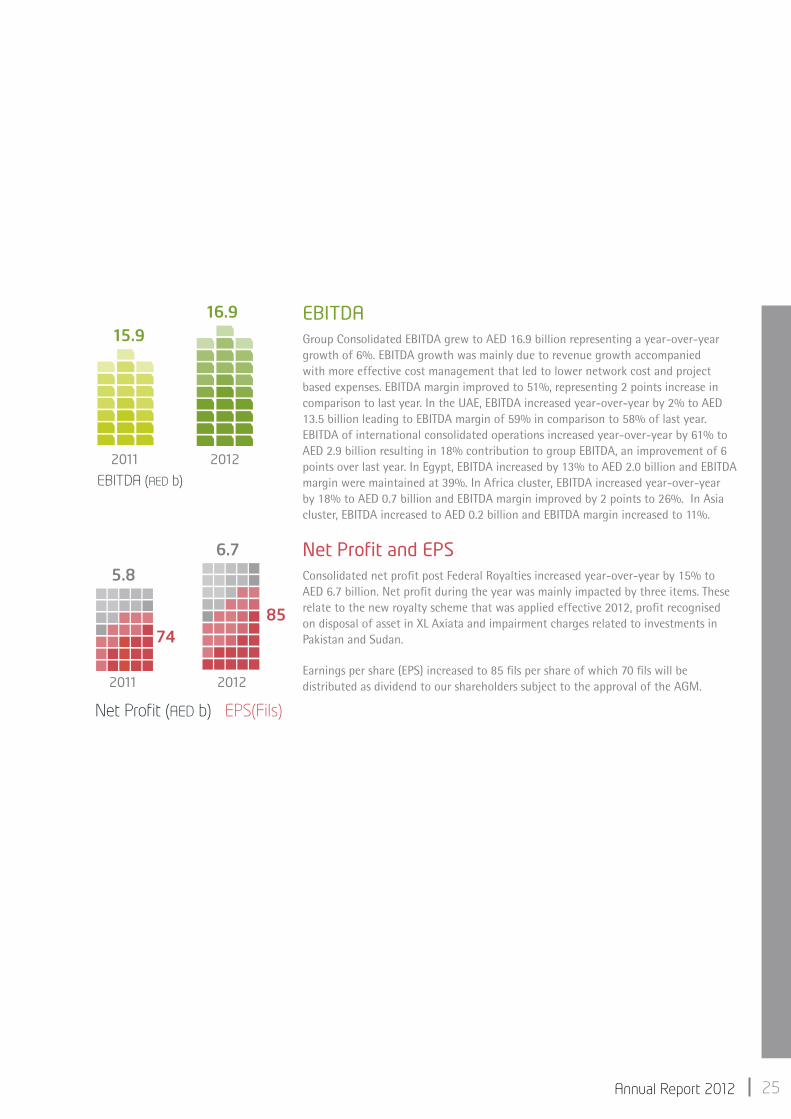

EBITDAGroup Consolidated EBITDA grew to AED 16.9 billion representing a year-over-year growth of 6%. EBITDA growth was mainly due to revenue growth accompanied with more effective cost management that led to lower network cost and project based expenses. EBITDA margin improved to 51%, representing 2 points increase in comparison to last year. In the UAE, EBITDA increased year-over-year by 2% to AED 13.5 billion leading to EBITDA margin of 59% in comparison to 58% of last year. EBITDA of international consolidated operations increased year-over-year by 61% to AED 2.9 billion resulting in 18% contribution to group EBITDA, an improvement of 6 points over last year. In Egypt, EBITDA increased by 13% to AED 2.0 billion and EBITDA margin were maintained at 39%. In Africa cluster, EBITDA increased year-over-year by 18% to AED 0.7 billion and EBITDA margin improved by 2 points to 26%. In Asia cluster, EBITDA increased to AED 0.2 billion and EBITDA margin increased to 11%.

Net Profit and EPSConsolidated net profit post Federal Royalties increased year-over-year by 15% to AED 6.7 billion. Net profit during the year was mainly impacted by three items. These relate to the new royalty scheme that was applied effective 2012, profit recognised on disposal of asset in XL Axiata and impairment charges related to investments in Pakistan and Sudan.

Earnings per share (EPS) increased to 85 fils per share of which 70 fils will be distributed as dividend to our shareholders subject to the approval of the AGM.

26

2011 2012

CAPEX (AED b)

4.34.2 CAPEX

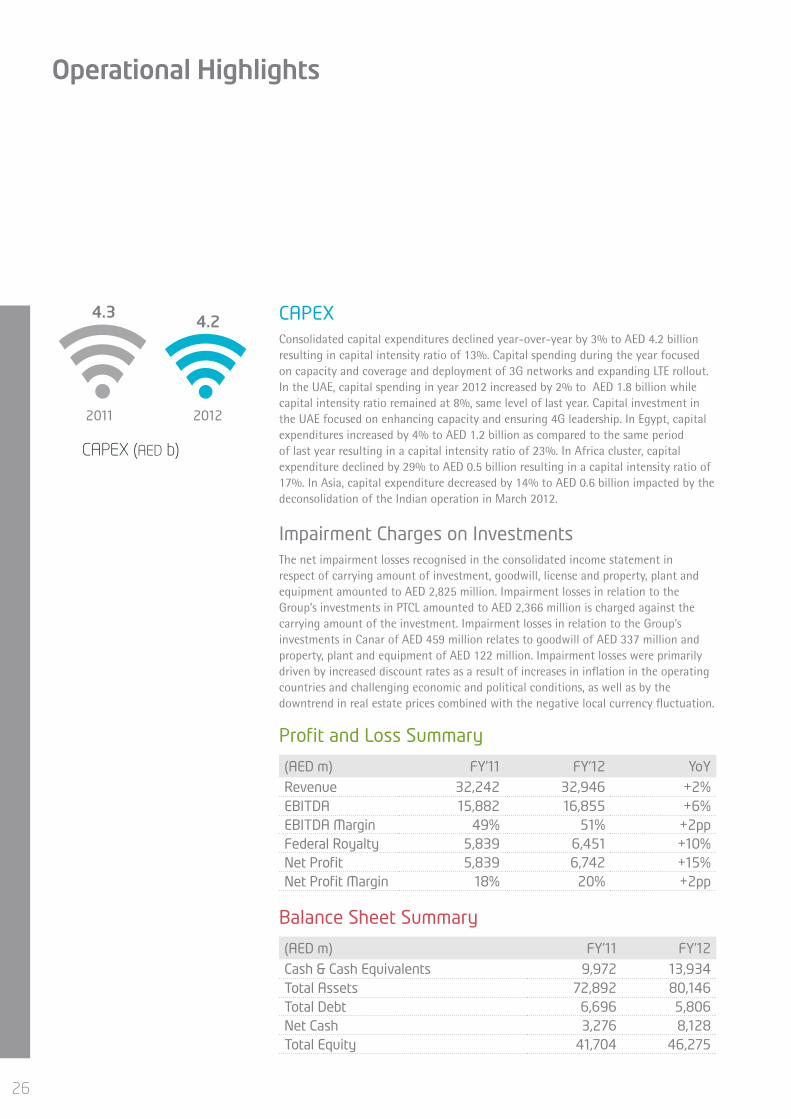

Consolidated capital expenditures declined year-over-year by 3% to AED 4.2 billion resulting in capital intensity ratio of 13%. Capital spending during the year focused on capacity and coverage and deployment of 3G networks and expanding LTE rollout. In the UAE, capital spending in year 2012 increased by 2% to AED 1.8 billion while capital intensity ratio remained at 8%, same level of last year. Capital investment in the UAE focused on enhancing capacity and ensuring 4G leadership. In Egypt, capital expenditures increased by 4% to AED 1.2 billion as compared to the same period of last year resulting in a capital intensity ratio of 23%. In Africa cluster, capital expenditure declined by 29% to AED 0.5 billion resulting in a capital intensity ratio of 17%. In Asia, capital expenditure decreased by 14% to AED 0.6 billion impacted by the deconsolidation of the Indian operation in March 2012.

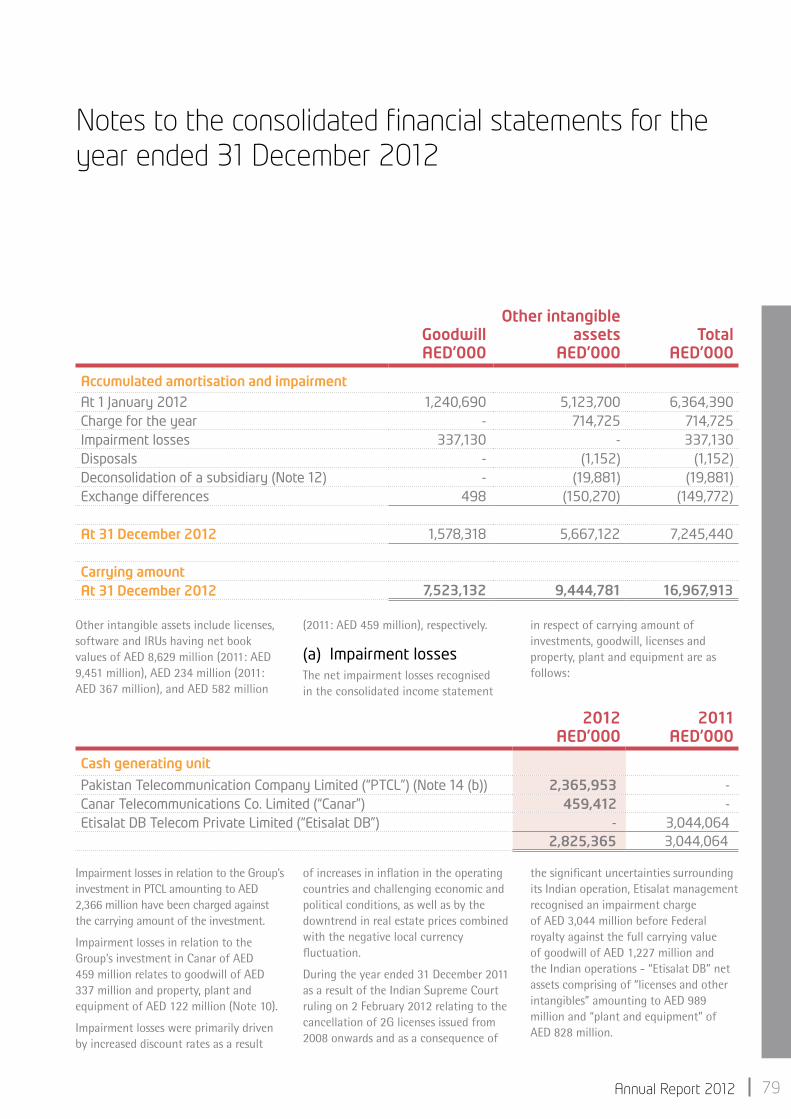

Impairment Charges on InvestmentsThe net impairment losses recognised in the consolidated income statement in respect of carrying amount of investment, goodwill, license and property, plant and equipment amounted to AED 2,825 million. Impairment losses in relation to the Group’s investments in PTCL amounted to AED 2,366 million is charged against the carrying amount of the investment. Impairment losses in relation to the Group’s investments in Canar of AED 459 million relates to goodwill of AED 337 million and property, plant and equipment of AED 122 million. Impairment losses were primarily driven by increased discount rates as a result of increases in inflation in the operating countries and challenging economic and political conditions, as well as by the downtrend in real estate prices combined with the negative local currency fluctuation.

Operational Highlights

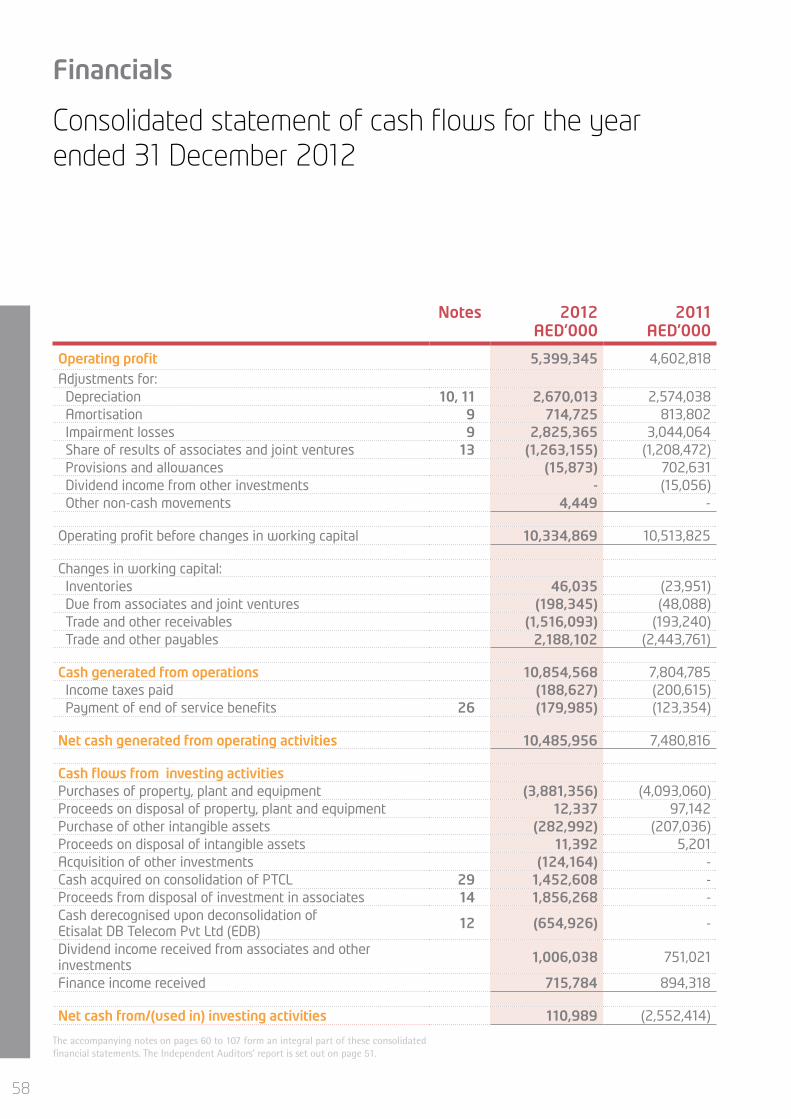

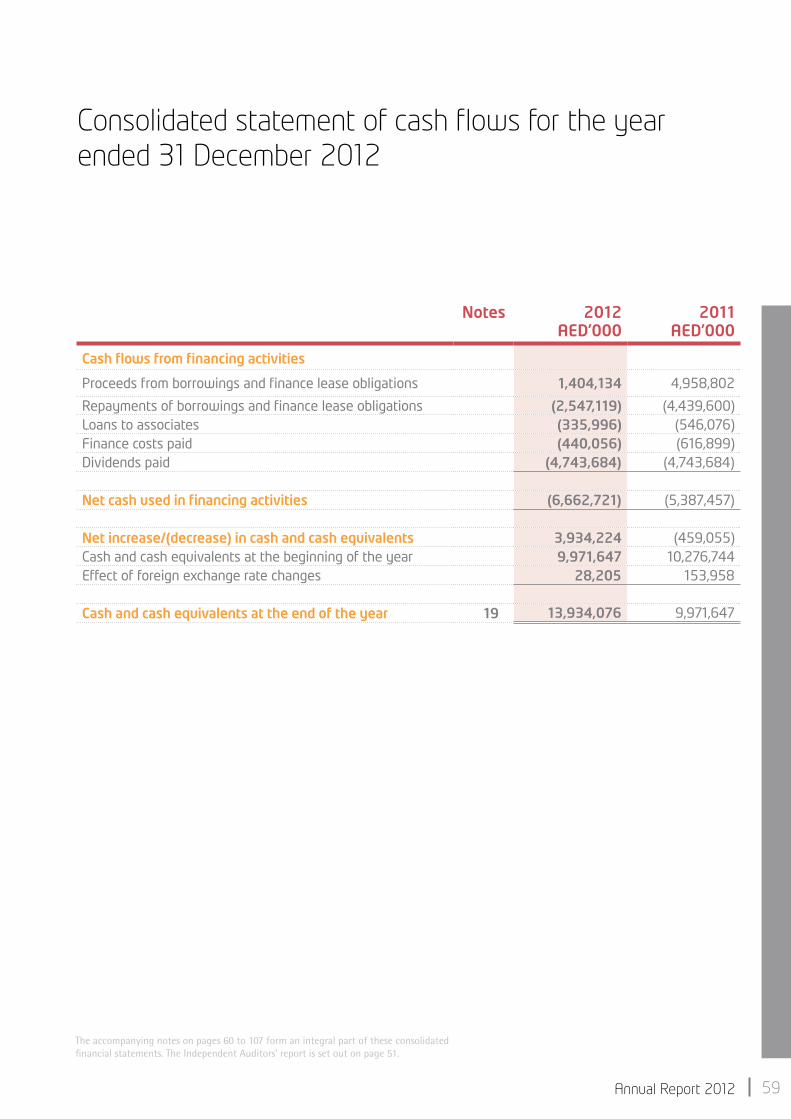

Profit and Loss Summary

(AED m) FY’11 FY’12 YoYRevenue 32,242 32,946 +2%EBITDA 15,882 16,855 +6% EBITDA Margin 49% 51% +2pp Federal Royalty 5,839 6,451 +10%Net Profit 5,839 6,742 +15%Net Profit Margin 18% 20% +2pp

Balance Sheet Summary

(AED m) FY’11 FY’12Cash & Cash Equivalents 9,972 13,934Total Assets 72,892 80,146Total Debt 6,696 5,806Net Cash 3,276 8,128Total Equity 41,704 46,275

27Annual Report 2012

Cash flow Summary

(AED m) FY’11 FY’12Operating 7,481 10,486Investing (2,552) 111Financing (5,387) (6,663)Net change in cash (459) 3,934Effect of FX rate changes 154 28Ending cash balance 9,972 13,934

Reconciliation of Non-IFRS Financial MeasurementsWe believe that EBITDA is a measurement commonly used by companies, analysts and investors in the telecommunications industry, which enhances the understanding of our cash generation ability and liquidity position, and assists in the evaluation of our capacity to meet our financial obligations. We also use EBITDA as an internal measurement tool and, accordingly, we believe that the presentation of EBITDA provides useful and relevant information to analysts and investors.

Our EBITDA definition includes revenue, staff costs, direct cost of sales, regulatory expenses, operating lease rentals, repairs and maintenance, general financial expenses, and other operating expenses.

EBITDA is not a measure of financial performance under IFRS, and should not be construed as a substitute for net earnings (loss) as a measure of performance or cash flow from operations as a measure of liquidity. The following table provides a reconciliation of EBITDA, which is a non-IFRS financial measurement, to Operating Profit before Federal Royalty, which we believe is the most directly comparable financial measurement calculated and presented in accordance with IFRS.

(AED m) FY’11 FY’12EBITDA 15,882 16,855Depreciation & Amortization (3,388) (3,385)Exchange gain/(loss) (216) (58)Share of results of associates and Joint ventures 1,208 1,263Impairment losses (3,044) (2,825)Operating Profit Before Federal Royalty 10,442 11,851

28

Etisalat UAE continues to introduce innovative services across the country creating value for its customers

Middle East - Etisalat UAE

Management Review

In 2012, Etisalat UAE focused on several strategic fronts to support its market leadership and future prospects. This included improving the quality of service, enhancing governance and processes, building capabilities, and automating systems and tools, while maintaining a focus on key commercial imperatives to improve its competitive advantage.

The company managed to further establish its leadership in the mobile segment by introducing innovative solutions and products to the market and launching aggressive promotions. Etisalat was the first to introduce a “Rollover Minutes” option for all postpaid customers, which allows them to keep their unused monthly minutes until the following month. This offer extends the validity of local or international unused minutes included in all bundled plans.

Given its aspiration to achieve mobile broadband leadership, the company revamped its offerings to become simpler, more affordable, and more tailored to customer needs of various segments. Mobile data usage was maximised with the 4G LTE Mobile Wi-Fi. Additionally, several smart handsets were launched (iPhone 5, Samsung Galaxy SIII, HTC 1X, Blackberry Curve 9320) and value for money competitive data packages were introduced. As a result of these efforts, the company’s broadband customer base witnessed a steady increase, positioning Etisalat as the No 1 operator in the Middle East for broadband growth.

Another key focus of 2012 was monetising the fiber investment by migrating fixed line subscribers to double play and triple play eLife services. The look and feel of eLife TV was enhanced with added interactive features for triple

play users with over 350 TV channels. As a result, the eLife segment grew significantly by 46 per cent to over 500,000 subscribers.

In 2012, Etisalat UAE continued to introduce innovative services across the country in order to create value for its customers. As leaders in home entertainment, Etisalat was the first in the UAE and the region to bring 3D to its customers with the broadcast of the 2010 FIFA World Cup. In 2012, the company once again introduced a first by launching a dedicated 3D entertainment and lifestyle channel, which substantiates its commitment to offering the best-in-class TV service to its viewers.

Etisalat has started SIM card registrations for its customers in line with the ‘My Number, My Identity’ campaign launched by the UAE’s Telecom Regulatory Authority (TRA). The process has taken off smoothly as planned. Trained and professional teams at Etisalat’s Business Centers and Outlets in the UAE ensured quick and easy registration for its customers. All channels and points of sales have been provided with new equipment and systems to handle the process.

In addition, Etisalat expanded its roaming agreements to over 721 operators worldwide, which allowed the corporation to increase inbound roaming traffic and enhance voice roaming aspects, thereby enhancing its customer experience.As for network investments, the focus in 2012 was on enhancing customer experience by ensuring capacity, expanding coverage and improving the network quality. As a result, Etisalat expanded the LTE network coverage

to over 82 per cent of the population. FTTH roll out progressed to reach 1.5 million home pass. In addition, Etisalat completed the highest 4G LTE speed test in the world, which reached 300 Mbps. This lightning-fast speed is a breakthrough for the international telecommunications industry and establishes Etisalat as a global leader in mobile broadband.

In 2012, Etisalat ICT solutions, in partnership with Attinad Software, developed a tablet and smartphone based patient management solution for the Friends Of Cancer Patients Association (FOCP). The new Mobile Health Patient Management Solution has been developed in line with the company’s strategy to leverage on the advancements of mobile technology to improve the quality of healthcare through real time, collaborative clinical information sharing. It will enable easy patient registration, examination, and record management and help FOCP to conduct dynamic surveys using the application, then analyse the survey response through graphical dashboards.

In 2012, Etisalat continued to look at ways in which to further enhance the high level of customer service that it offers to its customers. With the launch of the Unified Complaint Management System (UCMS), Etisalat is now equipped to handle and accelerate the resolution of complaints from all customers – both consumer and business, with increased efficiency and accuracy. UCMS elevates Etisalat’s complaint management capabilities to international standards through a number of major changes.

It also launched the ‘Prestige Programme 2012,’ which is designed to ensure that the company’s most valued customers

29Annual Report 2012

consistently receive the very best of service and privileges. The features of the programme include priority handling by a dedicated team when calling customer care, free mobile back up service, concierge services and medical advice.

In November 2012, Etisalat introduced a new per second billing plan in the UAE, which offers its discerning Wasel prepaid customers higher savings on both local and international calls. This simplifies the billing process and maximises savings for the customer, making it easy to calculate the cost of each local or international call.

Etisalat’s employees continued to be one of the company’s main assets. In 2012, career development and specialised training opportunities were offered to its UAE national employees as part of the company’s ongoing commitment to

developing future leaders and nurturing national talent.

As part of its ongoing CSR activities, Etisalat UAE supported, and contributed to, many different initiatives through sponsorships and donations for sports, educational, health, community and charitable events held across the country and on an international level.

Etisalat is very aware of the need to reduce energy consumption. This not only cuts power costs for businesses but also lowers the UAE’s carbon footprint. Accordingly, its commitment to finding solutions to reduce energy consumption and achieve cost savings is already achieving results through its recent MOU with Sheikh Khalifa Medical City, which is managed by Cleveland Clinic in Abu Dhabi.

Etisalat is dedicated to supporting initiatives that engage and encourage all members of UAE society to progress, particularly in sports, where they are represented on an international level. Etisalat recognises the special efforts of all athletes to overcome obstacles to achieve success and represent the UAE with pride and honor. Therefore, Etisalat extended their support to the UAE National Paralympics Team, which represented the UAE at the London 2012 Paralympics Games.

30

Management Review

31Annual Report 2012

Mobily is a regional leader in innovation. Its reputation has been built on its strong technical capabilities,

collaborative partnerships, and an increasing emphasis on the generation and nurture of new ideas

Middle East - Mobily

Of the many market innovations in 2012, a service that was launched to allow Hajj and Omrah returnees to donate their unused credit to charities in Saudi Arabia was one of the most noteworthy. Additionally, an i-Bill feature was offered to subscribers so that they can benefit from detailed and timely billing. Mobily, in collaboration with IBG Star, also launched the m-health product suite, which allows customers to monitor their blood glucose levels on the go for seamless diabetes management.

In 2012, Mobily established a partnership agreement with IBM Global, through which the company will provide comprehensive IT solutions. In addition, partnerships were established with Korea Telecom (KT) and global healthcare leader Sanofi, to facilitate joint projects and new product development through collaborative innovation.

In keeping with the company’s ethos of excellence in customer service, Mobily implemented The Customer Experience (CEX) programme, which was designed to improve overall customer service across all touch points. Through this

programme, a number of milestones were achieved, including a reduced average waiting time in retail stores by 11 per cent and increased call handling within the call centre by 19 per cent.

In order to maintain its leadership in the mobile data segment, Mobily continued to expand its network infrastructure with the latest and most advanced technologies. The advanced 4G network now covers more than 4,500 new sites. This highly developed network will further enhance the performance efficiency of the Mobily network.

Finally, in 2012 Mobily launched a new platform for its employees to propose ideas in response to business challenges. The “innovate Mobily” platform helped generate over 650 ideas and led to an increase in employee engagement.

32

Management Review

Middle East - Etisalat Egypt

Egypt’s mobile market continued to witness impressive growth in 2012. It was estimated that by the end of 2012 Egypt had 99 million mobile subscribers; industry experts expect this figure to double by 2018

Etisalat Misr offered competitive products to its subscribers during 2012 in order to capitalise on the country’s growth potential, and the introduction of various roaming packages was a prominent trend. One promotion offered subscribers the opportunity to roam on local data rates when visiting Saudi Arabia or the UAE, while during Ramadan customers received lower rates when using their roaming service in Saudi Arabia. In addition, Etisalat Misr leveraged its relation with the Etisalat Group to benefit from its agreement with iPass, which owns more than 1 million hotspots worldwide. This offers Etisalat Misr’s customers a more feasible solution when roaming abroad.

As per trends in more advanced markets, it is predicted that a strong broadband uptake is expected in Egypt. Etisalat is well positioned to benefit from this opportunity given its advanced network.

It will commercially launch a 42 Mbps HSPA+ after completing field testing. It is also the first company in the MENA region and the second worldwide to trial an 84 Mbps HSPA+ connection, extending its market leadership position on the technological front.

The company launched a fully-fledged, self-care account management system called Saytar. The application is the first of its kind in Egypt and enables customers to view their bills, submit customer complaints, report network issues and locate payment spots, among other features. The company also recognised the need to address Egypt’s shortage in low value coins, and introduced new recharge cards of the low denominational values of EGP 0.5, 1 and 1.5. Etisalat Misr further expanded its extensive CSR activities through the implementation of Origin – the largest water-related CSR initiative in Egypt, which aims to provide clean water to more than 100,000 Egyptian homes in a very short space of time. In 2012, the award-winning programme succeeded in providing 3,000 water connections to 30,000 people, nine water purifications stations to serve 50,000 people, 6,500

metres of irrigation channels to serve 15,000 people, seven kidney dialysis purification units to increase the efficiency of 70 kidney dialysis machines by 33 per cent, and 12 kidney dialysis machines to help 4,100 patients every month.

Etisalat Misr also continued to encourage its own employees to participate in philanthropic causes. Members of staff were asked to volunteer to donate part of their income in an initiative named Giving Back – Proud to Help Egypt. The proceedings were then donated to Egyptians living below the poverty line in order to address issues such as medical treatment and the provision of food.

The company also made major contributions to help Egypt become more energy efficient. Etisalat Misr adopted a Go Green initiative, through which it built 40 sites powered by renewable energy sources, and plans to deploy 100 solar energy sites and 100 hybrid sites by Q1 of 2013.

Etisalat Misr continued to develop innovative, customer-centric solutions that help make life easier for its subscribers.

33Annual Report 2012

In October 2012, Thuraya launched the Thuraya XT-Hotspot, which is the world’s fastest handheld hotspot. Building upon the success of its Thuraya XT handheld, the industry’s most popular and toughest satellite phone, Thuraya launched the XT-Hotspot, which is a pocket-sized router that creates a Wi-Fi zone for multiple users to connect smartphones, laptops, and tablets to the internet over Thuraya’s mobile satellite network. The XT-Hotspot is the only Wi-Fi router on the market offering a plug and play solution, enabling easy and affordable internet access with the fastest satellite data speeds on a handheld of up to 60 kbps in the most remote of areas.

In early 2012, Thuraya launched its Thuraya XT-DUAL which is the world’s first ever GSM/Satellite dual mode mobile satellite phone. It is the most advanced dual mode handheld phone featuring both GSM and satellite capabilities. The introduction of this innovative device uniquely positions Thuraya as the only satellite operator to offer seamless communications. The phone provides users with the flexibility and freedom to switch between GSM and satellite modes. With a growing subscriber base of voice consumers, one of the world’s most powerful networks, and a robust reputation for high-performance and compact

handhelds, Thuraya continues to present an unprecedented consumer experience through the new, state-of-the-art XT-DUAL phone.In July, Thuraya established a Point Of Presence (POP) and Meet Me Point (MMP) in Singapore, further enhancing the performance of its high-speed broadband terminal, Thuraya IP, in the region. Thuraya deployed the infrastructure to allow users in Asia to streamline and relay encrypted data to end destinations with guaranteed service quality. In addition, Thuraya strengthened the sales distribution network in Africa and Asia by partnering with new service providers in these regions.

Thuraya launched its roaming service in the US in partnership with the mobile operator T-Mobile. The new roaming service allows Thuraya subscribers to roam seamlessly with their Thuraya mobile numbers across the T-Mobile network, which reaches 96 percent of the US. Thuraya customers in the region can now make and receive calls, and also send and receive text messages. The company’s GmPRS roaming service will be enabled afterwards on the T-Mobile network. With more than 350 roaming partners worldwide, Thuraya is the only mobile satellite operator offering roaming services over GSM networks.

This facility is particularly beneficial to travellers who want to remain connected all the time. In a partnership with GTNT, Thuraya now provides uninterrupted satellite communications services across Russia to federal, departmental and corporate users in energy, petrochemical, construction, logistics, forestry, relief and media sectors. GTNT is Thuraya’s exclusive Service Partner in Russia, authorised to distribute company products, solutions and services across the country.In October, Thuraya was awarded the first ever ITU Humanitarian Award at the ITU TELECOMS World Conference in Dubai for the company’s contribution to providing mobile satellite communication services in times of emergency and disaster relief operations. Thuraya provides Thuraya handhelds and broadband terminals free of charge along with subsidised tariffs to the ITU to deploy to countries in need of emergency communications support. Once Thuraya learns of a disaster, it proactively contacts local governments and the ITU to offer support vis-à-vis by supplying the company’s mobile satellite handhelds and in some instances Dynamic spot beam reallocation.

Thuraya Despite a general slowing down of the overall mobile

satellite services market, Thuraya has bucked the trend and achieved a healthy year-on-year growth

3434

Atlantique Telecom continued to offer innovative products throughout 2012

Africa - Atlantique Telecom

Management Review

Following the successful launch of the Moovpassport in 2010, which allowed customers to roam at special rates across West and Central Africa, new offers were designed to address specific subscriber needs. Moov Hadj Roaming was launched to enable customers to enjoy low flat rates for both calls and SMS while travelling to Mecca.

In 2012, Atlantique Telecom acquired the 3G license in Ivory Coast – a major achievement that will enable faster mobile broadband connections to be launched, as well as a broader range of products and services. The company made a major network roll out during the year and aims to begin offering the services at the beginning of 2013.