Embed Size (px)

DESCRIPTION

FutureSafe is the UKS leading independent will writing company and estate planning experts they have produced this book to enable the general public to gain knowledge and advice on this most ignored subject

Citation preview

W i l l I n f o r m a t i o n P a c kFuture Safe

P e a c e o f m i n d

The vast majority of people put o� making a Willfor a variety of reasons, either believing that the people they would wish to inherit will automatically do so, or because they don’t think it is relevant tothem at this particular time.

The reality is that you can put o� making a Will untilit’s too late, and this poses all sorts of problemsfor the people left behind and could mean that someor all of your inheritance either goes to the wrongpeople or to the state.

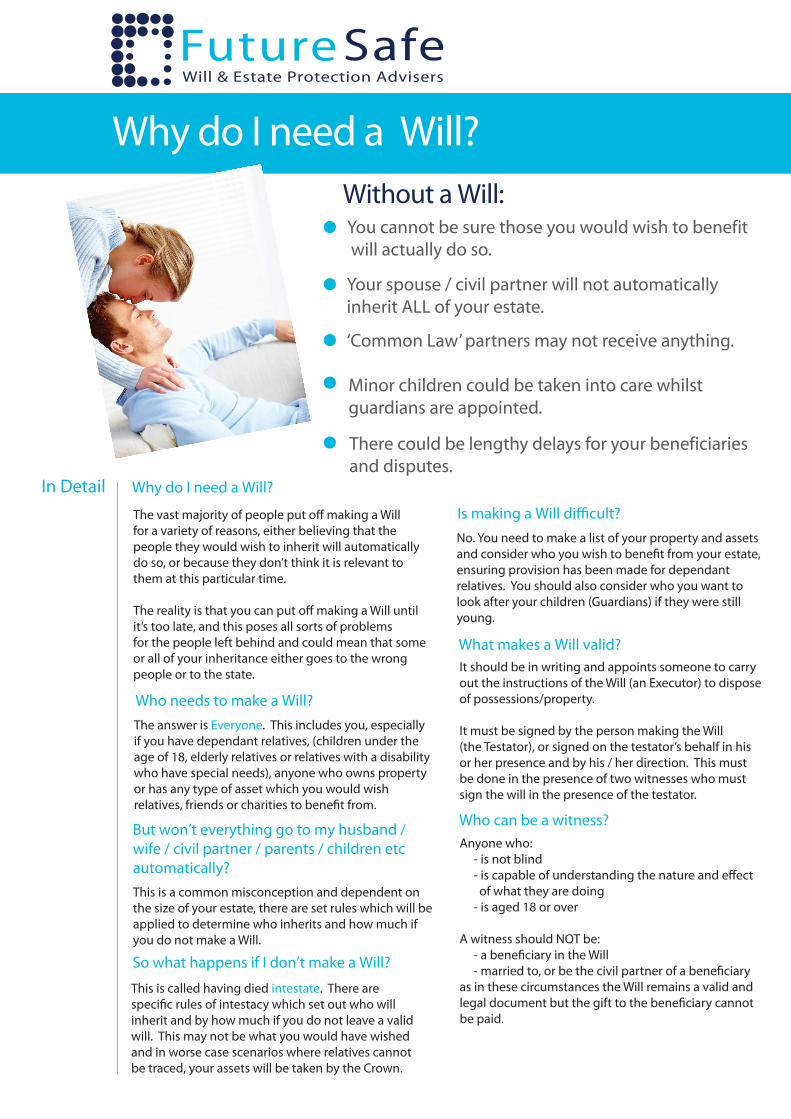

No. You need to make a list of your property and assetsand consider who you wish to bene�t from your estate,ensuring provision has been made for dependant relatives. You should also consider who you want tolook after your children (Guardians) if they were stillyoung.

It should be in writing and appoints someone to carry out the instructions of the Will (an Executor) to dispose of possessions/property.

It must be signed by the person making the Will (the Testator), or signed on the testator’s behalf in his or her presence and by his / her direction. This must be done in the presence of two witnesses who must sign the will in the presence of the testator.

Anyone who: - is not blind - is capable of understanding the nature and e�ect of what they are doing - is aged 18 or over

A witness should NOT be: - a bene�ciary in the Will - married to, or be the civil partner of a bene�ciaryas in these circumstances the Will remains a valid andlegal document but the gift to the bene�ciary cannotbe paid.

The answer is Everyone. This includes you, especially if you have dependant relatives, (children under theage of 18, elderly relatives or relatives with a disability who have special needs), anyone who owns property or has any type of asset which you would wishrelatives, friends or charities to bene�t from.

This is a common misconception and dependent onthe size of your estate, there are set rules which will beapplied to determine who inherits and how much ifyou do not make a Will.

Why do I need a Will?

Who needs to make a Will?

But won’t everything go to my husband /wife / civil partner / parents / children etcautomatically?

Who can be a witness?

So what happens if I don’t make a Will?

Is making a Will di�cult?

What makes a Will valid?

In Detail

Why do I need a Will?Will & Estate Protection Advisers

Future Safe

!Without a Will:

Your spouse / civil partner will not automatically inherit ALL of your estate.

‘Common Law’ partners may not receive anything.

There could be lengthy delays for your beneficiariesand disputes.

You cannot be sure those you would wish to benefit will actually do so.

Minor children could be taken into care whilstguardians are appointed.

This is called having died intestate. There arespeci�c rules of intestacy which set out who willinherit and by how much if you do not leave a validwill. This may not be what you would have wishedand in worse case scenarios where relatives cannotbe traced, your assets will be taken by the Crown.

Or contact us on 029 2025 4088

Visit our website for more information:www.future-safe.co.uk

Future Safe

!

A Will is probably the most important documentwe will ever own and something which around70% of us never get around to.Every day 2000 people die in this country and most of them leave their families with all the problems of Intestacy – this means dying without having a legally valid Will.

Most people assume that all their possessions will automatically pass on to their husband or wife, or other members of the family.

Unfortunately, many families often face immediate �nancial hardship, and sometimes they even have to sell the family home simply because no Will had been written.

The rules of intestacy mean that the state e�ectively writes a Will for them, and their money and possessions are distributed according to these rules.

Without a Will, you miss the chance of having people know your wishes, and saying who you would like to carry out your plans. This is especially important if you have children, as you are bound to have ideas about who you would most like to care for them if the need arose. You can leave instructions so that your relatives, friends and perhaps favourite charities will receive particular gifts in the manner that you want, not one imposed by Intestacy.

Your Will is in safe hands

As one of the leading independent Will writing companies in Wales we have helped thousands of people �nd security, reassurance and peace of mind as they plan for the future.

Expert advice in the comfort of your own home

Many of us �nd it di�cult or inconvenient to arrange to visit a solicitor – it often takes two appointments and usually during the working week. Making a Will with FutureSafe is easy, simply make an appointment at your convenience and we will come to you.

We can arrange to visit you at home and at a time that suits you. Our adviser will explain all the points that need to be considered – together you can discuss how your wishes can be included in your Will simply and conveniently.

Where there is no Will or only a basic Will in place your assets are exposed to the following risks:

A regular review of your current Will arrangements is a vital part of your �nancial plan.

You can easily add simple requests to your Will. If you have recently married or divorced, or you are sharing property with a new partner, then it is essential that you update your Will.

Everyone’s circumstances change as time goes on and we recommend reviewing your Will at least every �ve years, and more frequently if there is a major change in your situation.

By making a Will you can ensure that your loved ones are fully protected, and your assets, which have taken you a lifetime to acquire, are distributed in accordance with your wishes and protected for future generations.

Marriage after death - On �rst death all the assets become solely owned by the surviving spouse. What if the surviving spouse re-marries? The inherited estate could be lost to the new spouse, possibly disinheriting your children.

Care Costs - If the surviving spouse needs nursing care then the whole estate could be susceptible to the cost of that care. O�cial government statistics show that some 69,000 homes are seized and sold each year to fund long term care.

Inheritance Tax - Do you know if your family will have to pay Inheritance Tax - do you know how this can be reduced or even avoided?

Time to change a Will?

A properly constructed Will and some simple planning can ensure that those you would wish to bene�t receive their full inheritance and that these assets remain protected.

Peace of mind

It is usual (but not essential) that the same persons are appointed guardians of all of the testator’s minorchildren. When guardians are to act only after thedeath of the surviving parent it is desirable that each parent should appoint the same persons toact as guardian. It is of course, important that the testator should obtain the consent of the proposed guardian before making the appointment.

Who should act as guardians?

Guardians

In Detail

Who cannot appoint guardians?

Unmarried fathers who don’t have parental responsibilitycannot name guardians, neither will they necessarilybecome guardian should the mother die. If they wantedto ensure that they did, it would be necessary toenter into a written agreement to share responsibilitywith the mother or apply to the court. It would be possible for unmarried fathers to become guardians ifappointed by the mother or by marriage.

What is the role of a Guardian?Will & Estate Protection Advisers

Future Safe

Failing to name guardians in your Will means that the care of minor children will be decided by the courts.

You should ensure that those persons you would want to bring up your children are willing to do so.

You should make financial provision for your children to enable their guardians to raise them.

It is best to consider the age of the guardiansand to appoint two.

Guardians take on the roleof parent to your children.

The role of a guardian is a very important one ifyou have children. Should you die without making a Will or if you do not appoint guardians in your Will, your children could be placed in care until the court appoints o�cial guardians to look after them. This could take months and would obviously result in distress for your children and other members of your family. You should remember to request that the appointed guardians also make a Will themselves to further safeguard the future of your children.

You will need to consider who should be theguardians of any children under the age of 18years who may survive you. The law has certain requirements particularly where the parents are unmarried or have divorced or separated. The normal choice is to appoint family members, particularly where very young children are involved. Typically appointments can include your own brothers and sisters, or in some cases yourolder children ( where they are over 18.)

As children grow, the appointment of friends may be more appropriate as they are more likely to share your lifestyle and in these modern timeslive nearer than your family.

Although each parent can appoint di�erent guardians, it is worth remembering that all the guardians will legally act in the event of your death, so depending on who you have chosen will impact on your children's future. You canalso appoint di�erent guardians for di�erent childrenbut this may mean splitting them up. Guardians have toensure adequate contact between children is maintainedbut you may not be happy having your children dividedin any way.

Where the appointment of family members is being considered, care needs to be taken whenconsidering appointing a ‘committee’ of relatives.The obvious disadvantages with a committee is thatthe wellbeing of your children may be overlookedand a committee can be di�cult to manage. It isbest to limit the maximum number of guardiansto two and it is preferable that they share a home aspartners. Thus your children will become part of a familiar and stable environment at probably the most di�cult time of their lives. By all means appoint substitute guardians as this will ensure continuity if circumstances change.

The duties of the guardian are essentially the same as those of a parent. They are responsible for the day to day upbringing of your child including holidays, birthday presents and all the everyday things that we take for granted. The terms of the Will should besuch that executors and subsequently trustees can do all that is necessary to assist in �nancial terms.

The role of the guardian is a very responsible oneand should not be entered into lightly. There will be �nancial, social and emotional implications taking on such a vast role and the matter should be discussedbetween the testator and the appointed guardians.

Although it is a sensitive subject, parents shouldconsider the �nancial position of their chosen guardians, and consider how they would provide �nancial support for them to take on the role being asked of them. Guardians may be able to claim child bene�t and receive a guardian’s allowance in the event that both parents are deceased. Where one parent is alive and a guardian is still called upon to act, the situation will obviously be more complicated.

There could well be circumstances when guardians are called upon even when there is a living parent, for example when:

A surviving parent is unable to perform their role because they are overseas, in the army, in prison, disabled, or mentally incapicitated, or they just refuseresponsibility, or a couple are separated or divorced.The guardian will act with the surviving parent, and should disputes arise they will have to be settled by the court. The surviving parent is still considered the statutory guardian.

It is normal for the �nancial management to be separated from the day to day upbringing ofchildren. Whilst the guardians have the daily resonsibility it is better for the �nancial control to be handled by someone di�erent, normallythe trustees of your estate. The two tasks demand di�erent skills that may not always befound in the same person. It also means that the trustees, the guardians and when they are old enough, your children, can share what can bedi�cult decisions.

In your Will, where your children are under ageand are to bene�t from the estate, you shouldnominate them as bene�ciaries. In no circumstances should you nominate the guardians; as mentioned above, the moneywill be held in trust, and will be controlled by the trustees for the bene�t of the children.

The appointment of guardians for children allows you to decide who should be responsible for your children’s welfare, maintenance and education, and how these should be funded if both your deaths occur whilst any child is under 18 years of age.

There is no legal reason why you cannot appoint the same people as executors, trustees and guardians if you wish, but you should be aware that there is a potential con�ict of interest in that trustees are responsible for advancing sums of money held in trust to the guardians to help with guardianship duties. However, if you have absolute trust in the people appointed then do not allowthis to concern you.

Do consider factors such as the age of your guardians, where they live in relation to you, (would the children have to move school etc.,) how close is therelationship between your children and the guardiansnow, and do your guardians know and share your views on how the children should be raised and educated etc.

How many Guardians? Financial considerations

The Guardian’s duties

The implications

Contact Us Call our Cardi� o�ce on 029 2025 4088

Visit our website for more information:www.future-safe.co.uk

Safe Will & Estate Protection Advisers

Future 1 Caspian Point | Pierhead Street | Cardi� | CF10 4DQ | Registered in England & Wales - Company No. 6624898

Don’t lose your home to care costs

Will & Estate Protection Advisers

Future Safe

Your home may have to be sold to pay for long term care costs

Your savings and investments could be wiped out

Any income would be assessed and used towards the cost ofyour care

Your children and grandchildren could lose their entire inheritance

If you fail to act now -

Unfortunately, the costs involved in moving into a

care home can literally wipe out your entire savings

and your home may have to be sold to pay for care

fees. This could mean that your loved ones

receive very little, or even nothing at all of what

you originally intended them to have.

When someone enters care they are automatically

“means tested” and ALL of their assets, including

their home are taken into account.

More and more homes are beingsold each year to pay for care

Most of us work very hard over the years to buy

our own homes and build up our savings for

our retirement and would like to leave a “little

something” for our children and grandchildren

after we are gone.

How do I protect my home and assets from care costs?

In Detail

Statistics show that more than 20,000 pensioners were forced to sell their homes to pay for residential care in 2009. The number of people

selling up has soared by 17 per cent since 2005 and experts say the �gure is likely to continue rising due to local authority budget cuts, meaning fewer people will get the help they need to stay in their own home.

If your assets are worth more than £23,500 (the upper limit) including your house, you will be expected to fund the full cost of your care fees. You would not be able to receive any �nancial help from your local council.

If you own less than the upper limit, the council will assess your ability to pay based on both your capital and income.

You are most at risk of losing your home to care costs when you enter care after owning your home jointly with a spouse. Upon �rst death you become the sole owner and as such you will be assessed on the property’s full value along with any formerly joint held assets, such as savings.

When would I have to pay forcare?

What can be done?

Let us help

A Protective Property Trust

So I can protect my property, but what about my other assets?

Assets such as cash, stocks and shares, bank and building society accounts, PEPS and ISAs etc will be determined as liquid assets, and in addition to any income received will be assessed for care.

Changing the way your assets are both held and invested will ensure that they are not assessed for care costs.

Councils are advised that investment bonds, written as one or more life insurance policies that have partial surrender options, are disregarded as capital assets in the �nancial assessment for residential accommodation. In contrast, the surrendervalue of non-life assurance bonds are taken into account.

Income from investment bonds, with or without life assurance, is taken into account in the �nancial assessment for residential accommodation as may be payments of capital by period instalments.

As stated under the Department of Health CRAG

regulations Section 6.002B.

Contact Us Call our Cardi� of�ce on 029 2025 4088

Safe Will & Estate Protection Advisers

Future 1 Caspian Point | Pierhead Street | Cardi� | CF10 4DQ | Registered in England & Wales - Company No. 6624898

Firstly it ‘s important to safeguard your home, and

the �rst step is to look at the way you currently

own your property.

The majority of people own their homes jointly,

which means that on the �rst death the survivor

owns 100% of the full property value, and this is

when the home becomes vulnerable to attack

from care costs.

By simply changing the way you own your home

to what is known as tenants in common,

combined with the correct trust plannning, you

can protect yourselves.

At FutureSafe our team of fully quali�ed advisers

are able to advise on all aspects of care planing

and provide you with the correct strategy to

ensure that your assets are protected.

For more information please refer to our website

www.future-safe.co.uk or the Charging for

Residential Accommodation Guide - Department

of Health - C.R.A.G Regulations section 7.014 of

the Social Securites Act 1970.

Firstly you would need to sever the joint

tenancy and change the ownership to tenants

in common. At this point each of you would

own 50% of the property value (percentages

can vary.) The next step is to set up mirror wills,

each bequeathing your share of the property to

a third party, usually the children, and giving

the surviving spouse the right to reside in the

property for the rest of their life.

When the �rst of you dies, that share of the

property is left to the trust, whose bene�ciaries

will either be the children, grandchildren or

other named bene�ciaries. Whilst the surviving

partner continues to reside in the property

there are no issues, but if the survivor goes into

care, that is when the property and other assets

would be assessed for care costs.

By converting the ownership of your property

into tenants in common and including a

Protective Property Trust in your Will, only

your share in the property can be taken into

account by the local authority when assessing

your ability to pay for care, and not the

percentage owned by the bene�ciaries named

in the deceased person’s Will.

How do Property Trusts work?

Can I move or will I be stuck in the same property?

In Detail

A Protective Property Trust Will

Will & Estate Protection Advisers

Future Safe

! A Protective Property Trust Will is a

good way to ensure that at least your share of the family home will pass to your children or other chosen bene�ciaries, whilst making sure that your spouse or partner has security to live in their home, and be given the option to move should they wish to do so.

Essential to the working of Property Trust Wills is the way in which you own your property. Most couples own their property as joint tenants. This means that when one of them dies, the property will automatically pass to the survivor. Should the survivor then have to go into care, the whole of the property may be sold to pay for care fees. It is possible to sever the joint tenancy, so that the property is owned as tenants in common. This means that you each own an identi�able share in the property. You can then either give your share away in your lifetime, or put it into trust for the next generation, or dispose of it by your Will – the Protective Property Trust Will. This would have an important advantage in that should the surviving co-owner need to go into care, the local authorities could only take into account that person’s one half share of the property, and not the whole. In addition to the above is the issue of re-marriage. Should your partner re-marry after your death, this could have a dramatic e�ect on where your property ends up. This is because the act of re-marriage cancels any Will your partner made whilst you were both alive, and the new husband/wife would then become his/her next of kin. Your children for example, would be no legal relative to this person and your estate

could pass outside the family to someone you have never even met. However, if you have a Property Trust Will, once again, your half of the house is protected by the trust and will not pass outside your immediate family.

You can move. The terms of the trust are �exible and ensure that the person living in the property has the option to move to a new property if he or she wishes. Perhaps the home would be too large and there would be a wish to move to a smaller property. This is what would happen: Suppose Mr and Mrs Jones own a house valued at £200,000. They have a Property Trust Will and then Mr Jones dies. Mrs Jones then wants to move to a property valued at £100,000. She can sell the house and use Mr Jones’ trust of £100,000 to buy the new home. Mrs Jones can then do as she wishes with her £100,000.

The Trustees of Mr Jones’ estate would own the new home but Mrs Jones could live there for life.

Furthermore, if the new house is priced at £125,000, Mrs Jones could again use Mr Jones’ £100,000 trust and add £25,000 herself. Thus Mrs Jones would own a �fth of the property and the trustees would own four �fths.

What do I do when somebody dies?

Let Us help

In Detail

What do I do when somebody dies?

Will & Estate Protection Advisers

Future Safe

Make an exhaustive list of all the assets and debts including utility bills.

Settle all the deceased’s debts and pay any inheritance tax necessary.

Payment of tax becomes the executor’s personal responsibilityand may leave them open to personal liability or penalties.

Arrange for the care of any minor children and pets.

Applying for probate can be both daunting and time consuming.

An Executor will need to:-

Locate all the heirs and distribute contents of the Will.

Who do I notify �rst?

As soon as possible you should:

The loss of a friend or loved one can be a verystressful time with many people needing to be noti�ed in the �rst few days. In addition to the immediate tasks that need to be attended to,such as arranging the funeral, there is a lot ofpaperwork to be dealt with and o�cial documents which need to be completed over the next few weeks.

One of the duties you may have to undertake isapplying for probate. This can often be a complex and extremely time consuming process and needs attending to at a time when you may not feel able to perform this task.

FutureSafe Will & Estate Protection Adviserscan help as we o�er a �xed fee probate servicevia our panel of solicitors. All fees are quoted inadvance of any work being undertaken which means a considerable saving on the fees you would typically need to pay a high street solicitoror bank.

In the �rst �ve days it is important that you dothe following:- Notify the deceased’s family doctor.- Contact a funeral director to commence funeralarrangements (you will need to check the Will forany special requests or pre-paid funeral arrangements which may have already been made.)- Register the death at the Registry O�ce.- Advise any departments who may have beenmaking payments to the deceased, such as taxcredits, bene�ts, pensions, etc.- You will also need to contact relatives and peopleclose to the deceased.

- Contact the executors of the Will to enable themto start the process of obtaining probate.- If there is no Will then you should decide who willapply to sort out the deceased’s a�airs and apply forLetters of Administration.

If the person who has died leaves a Will

What if the person who has died

Checking whether a Will is valid

hasn’t left a Will – (Intestacy)

When a grant is needed

Visit our website for more information:www.future-safe.co.uk

Contact Us

Call our Cardi� of�ce on 029 2025 4088

Safe Will & Estate Protection Advisers

Future 1 Caspian Point | Pierhead Street | Cardi� | CF10 4DQ | Registered in England & Wales - Company No. 6624898

In this case one or more executors may be namedin the Will to deal with the person’s a�airs aftertheir death. The executor applies for a ‘grant ofprobate’ from a section of the court known as theProbate Registry. The grant is a legal documentwhich con�rms that the executor has the authorityto deal with the deceased person’s assets (property,money and possessions.) They can use it to showthey have the right to access funds, sort out �nancesand collect and share out the deceased person’s assets.

A Will must be valid in order to obtain the grant of probate. The following list may be used to help youdetermine if a Will is likely to be valid or not:

- The Will must be an original document not a photocopy.

- The Will must be signed and dated by the testator (i.e. the person whose Will it is).

- The Will must be signed and witnessed by two witnesses who do not stand to bene�t from the Will.

- The Will must appoint executors to administer the estate, otherwise partial intestacy rules will apply.

- The Will must dispose of the whole estate. If bene�ciaries have died before the deceased and no substitute provision has been made in the Will for this event, then the Will is not e�ective for the entire estate; this is called partial intestacy.

- The Will must not be tampered with, altered, or in any way damaged or defaced.

If there is no Will, a close relative of the deceasedcan apply to the Probate Registry to deal with theestate. In this case they apply for a ‘grant of lettersof administration.’ If the grant is given, they areknown as ‘administrators’ of the estate. Like thegrant of probate, the grant of letters of administration is a legal document which con�rmsthe administrator’s authority to deal with the deceased person’s assets. When someone dieswithout leaving a Will, dealing with their estate can be complicated. It can also take a long time -months or even years in some very complex cases.

A grant is almost always needed when the personwho dies leaves one or more of the following:

- £5,000

- Stocks or shares

- Certain insurance policies

- Property or land held in their own name or as‘tenants in common’

In most cases, the bank or relevant institutionwill need to see the grant before transferringcontrol of the assets.

However if the estate is small, some organisationsmay release the money to you at their discretion.To establish whether the assets can be obtained without a grant, the executor or administrator would need to write to each institution informing them of the death and enclosing a photocopy of the death certi�cate (and Will if there is one). The personal representative won’t be granted probate until some or all of any inheritance tax that is due on the estate has been paid.

The above applies to England and Wales. If the person who has died lived in Scotland, the representative must apply for a ‘grant of con�rmation.’