Embed Size (px)

Citation preview

AGM2014Wacker Neuson SEMunich, May 27, 2014

Executive Board Report

Cem Peksaglam (CEO)Martin Lehner (CTO)Günther Binder (CFO)

1

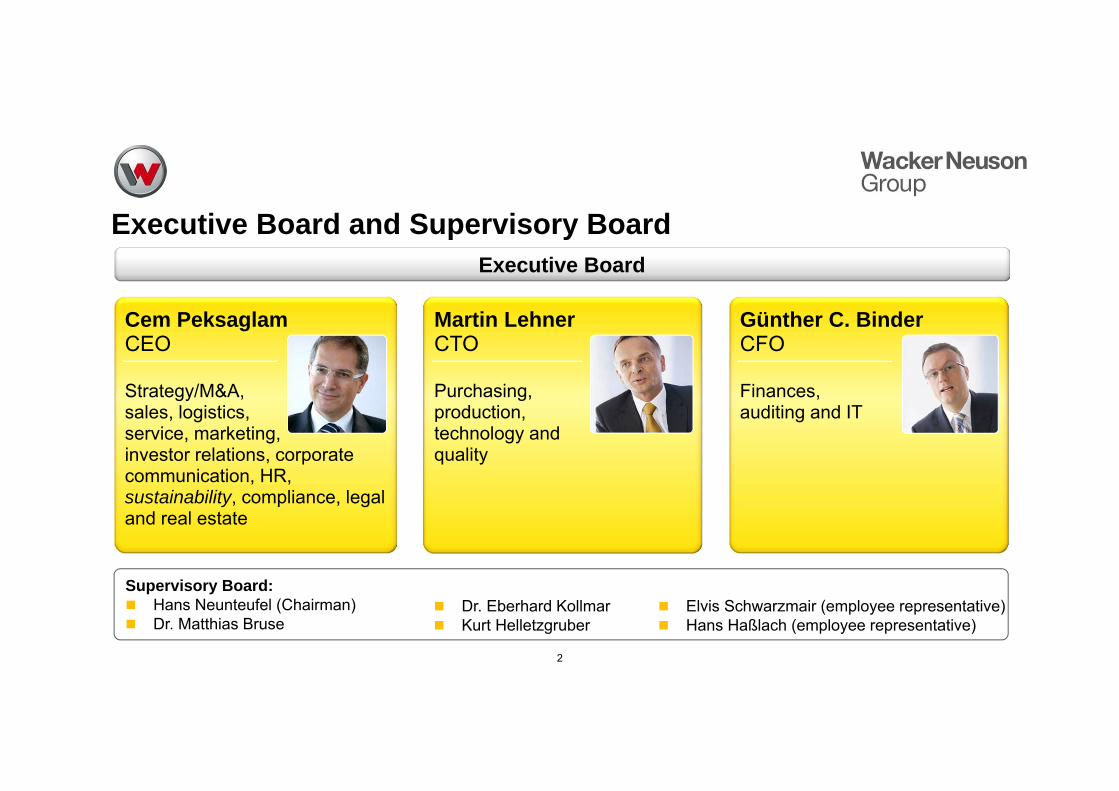

Executive Board and Supervisory Board

2

Executive Board

Supervisory Board: Hans Neunteufel (Chairman) Dr. Matthias Bruse

Dr. Eberhard Kollmar Kurt Helletzgruber

Elvis Schwarzmair (employee representative) Hans Haßlach (employee representative)

Cem PeksaglamCEO

Strategy/M&A,sales, logistics,service, marketing,investor relations, corporate communication, HR,sustainability, compliance, legal and real estate

Günther C. Binder CFO

Finances,auditing and IT

Martin LehnerCTO

Purchasing,production,technology andquality

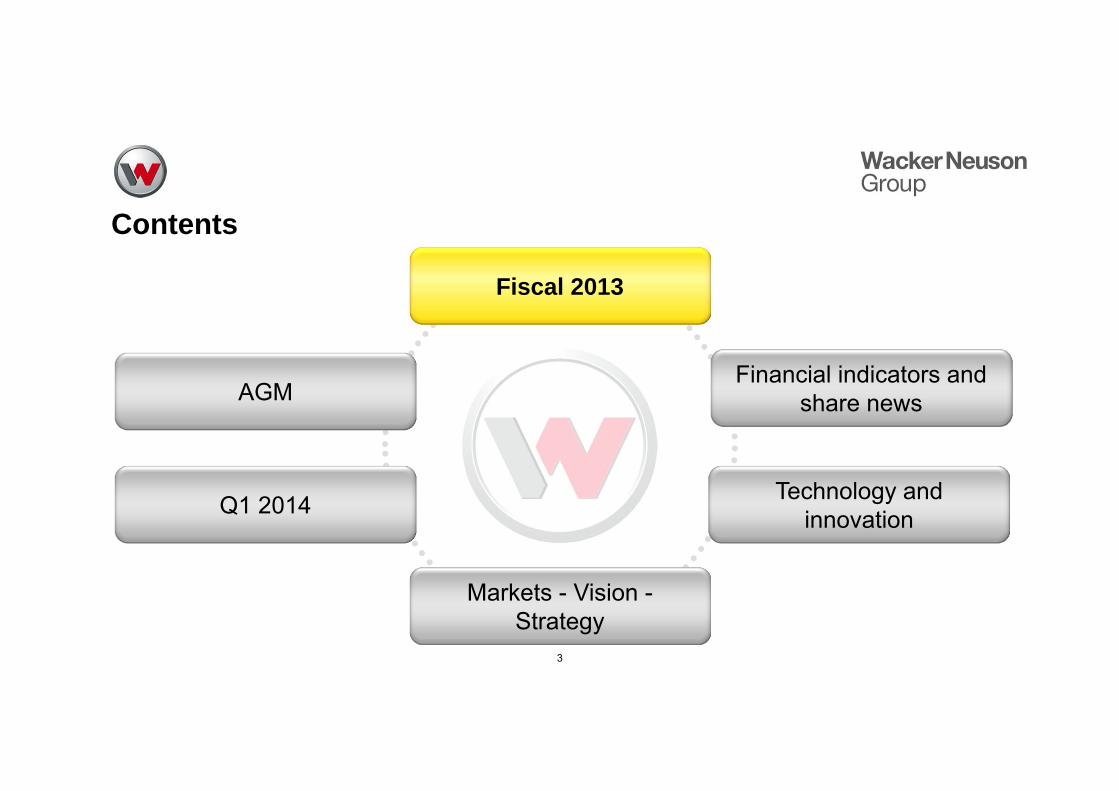

Contents

3

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

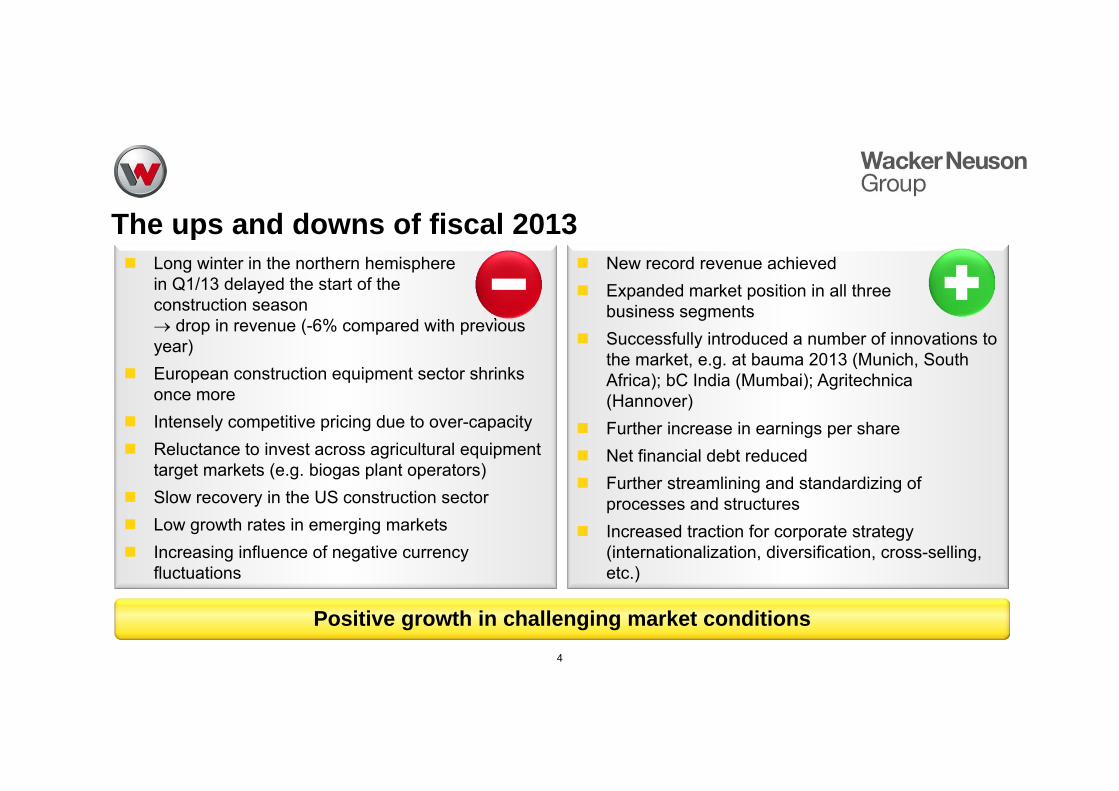

The ups and downs of fiscal 2013

4

Long winter in the northern hemispherein Q1/13 delayed the start of the construction season drop in revenue (-6% compared with previous year)

European construction equipment sector shrinks once more

Intensely competitive pricing due to over-capacity Reluctance to invest across agricultural equipment

target markets (e.g. biogas plant operators) Slow recovery in the US construction sector Low growth rates in emerging markets Increasing influence of negative currency

fluctuations

Positive growth in challenging market conditions

New record revenue achieved Expanded market position in all three

business segments Successfully introduced a number of innovations to

the market, e.g. at bauma 2013 (Munich, South Africa); bC India (Mumbai); Agritechnica(Hannover)

Further increase in earnings per share Net financial debt reduced Further streamlining and standardizing of

processes and structures Increased traction for corporate strategy

(internationalization, diversification, cross-selling, etc.)

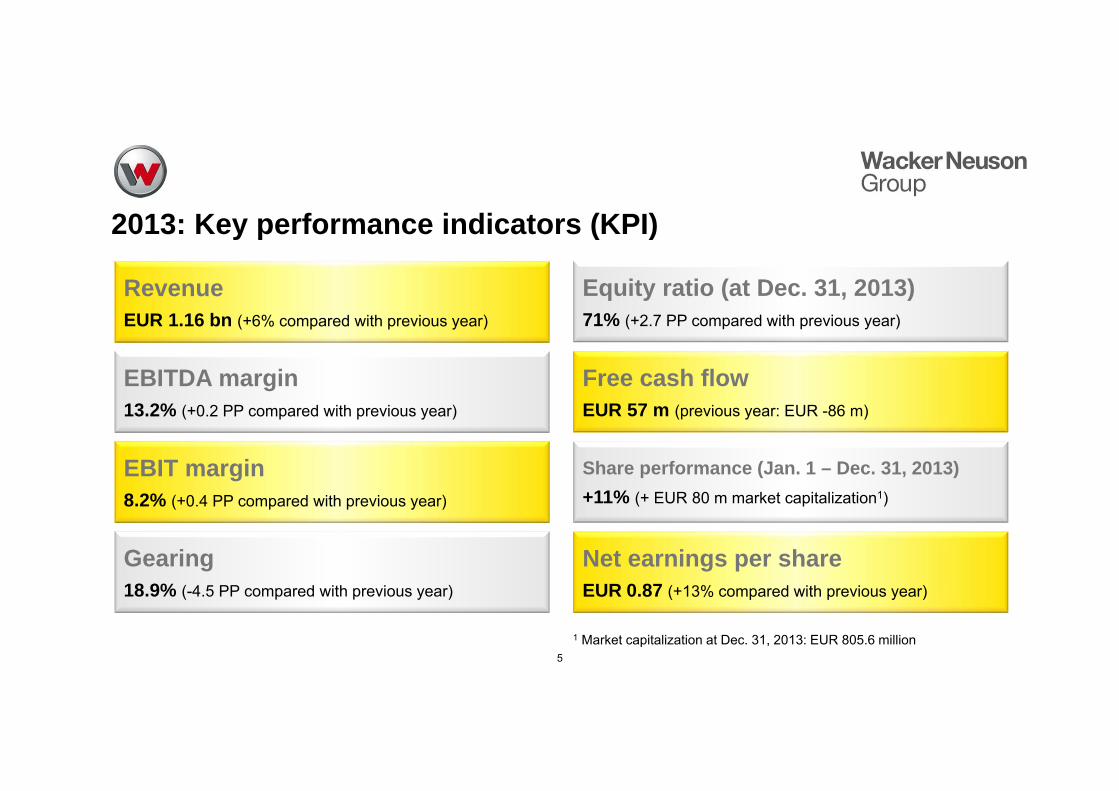

2013: Key performance indicators (KPI)

5

RevenueEUR 1.16 bn (+6% compared with previous year)

EBITDA margin13.2% (+0.2 PP compared with previous year)

EBIT margin8.2% (+0.4 PP compared with previous year)

Equity ratio (at Dec. 31, 2013)71% (+2.7 PP compared with previous year)

Free cash flowEUR 57 m (previous year: EUR -86 m)

Share performance (Jan. 1 – Dec. 31, 2013)+11% (+ EUR 80 m market capitalization1)

Gearing18.9% (-4.5 PP compared with previous year)

Net earnings per shareEUR 0.87 (+13% compared with previous year)

1 Market capitalization at Dec. 31, 2013: EUR 805.6 million

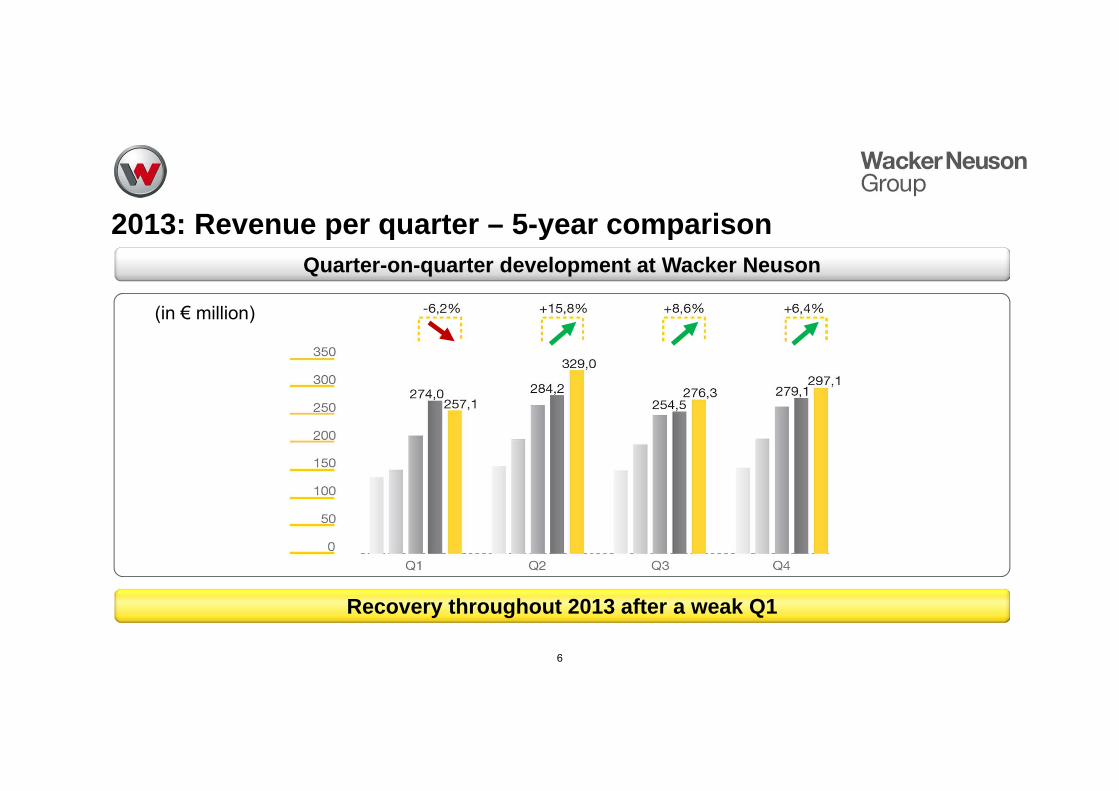

2013: Revenue per quarter – 5-year comparison

6

(in € million)

Quarter-on-quarter development at Wacker Neuson

Recovery throughout 2013 after a weak Q1

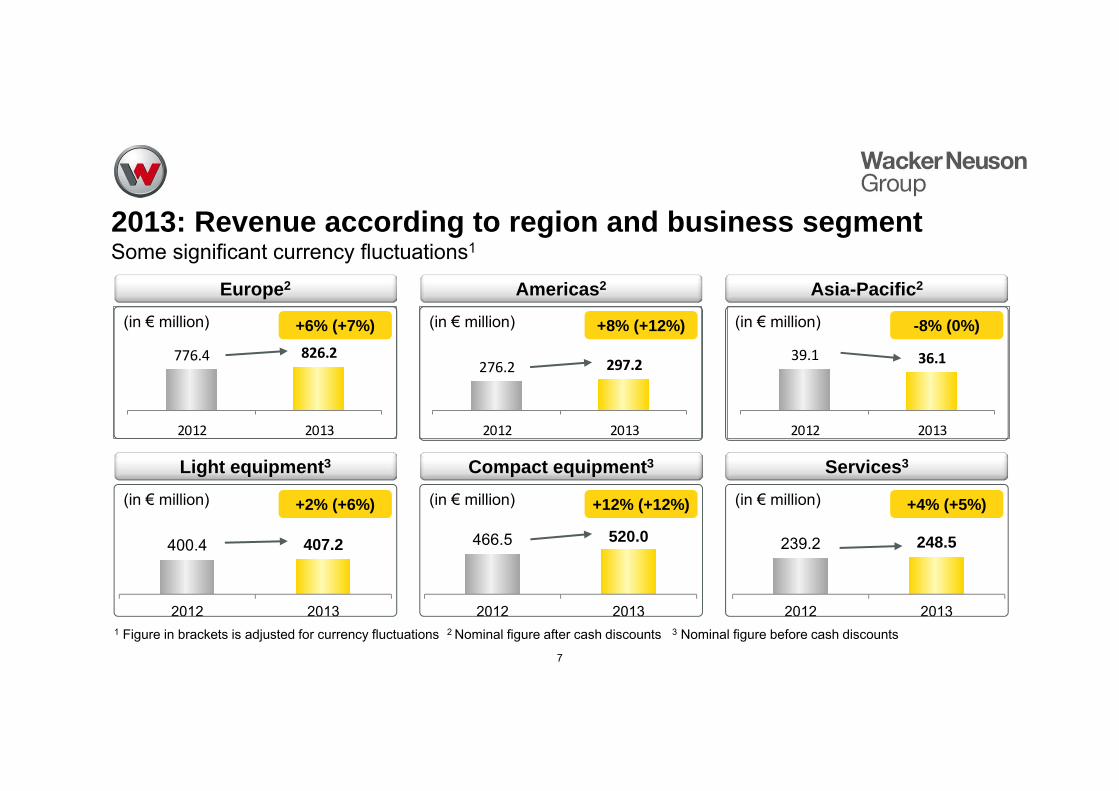

776.4 826.2

2012 2013

276.2 297.2

2012 2013

39.1 36.1

2012 2013

400.4 407.2

2012 2013

466.5 520.0

2012 2013

239.2 248.5

2012 2013

Europe2

(in € million)

Americas2

(in € million)

Asia-Pacific2

(in € million)

Light equipment3 Compact equipment3

(in € million)

Services3

(in € million)(in € million)

2013: Revenue according to region and business segmentSome significant currency fluctuations1

7

1 Figure in brackets is adjusted for currency fluctuations

-8% (0%)+6% (+7%) +8% (+12%)

+2% (+6%) +12% (+12%) +4% (+5%)

2 Nominal figure after cash discounts 3 Nominal figure before cash discounts

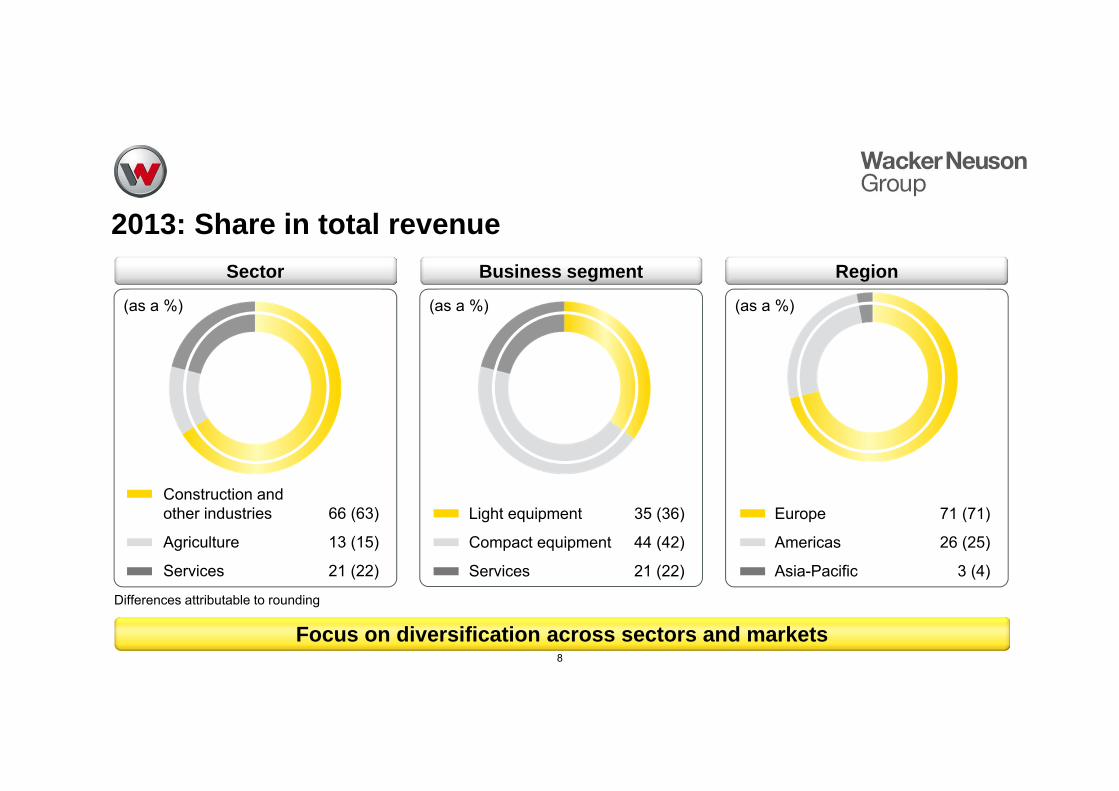

2013: Share in total revenue

8

Focus on diversification across sectors and markets

Sector Business segment Region

Differences attributable to rounding

(as a %)

Construction and other industries 66 (63)

Agriculture 13 (15)

Services 21 (22)

(as a %) (as a %)

Light equipment 35 (36)

Compact equipment 44 (42)

Services 21 (22)

Europe 71 (71)

Americas 26 (25)

Asia-Pacific 3 (4)

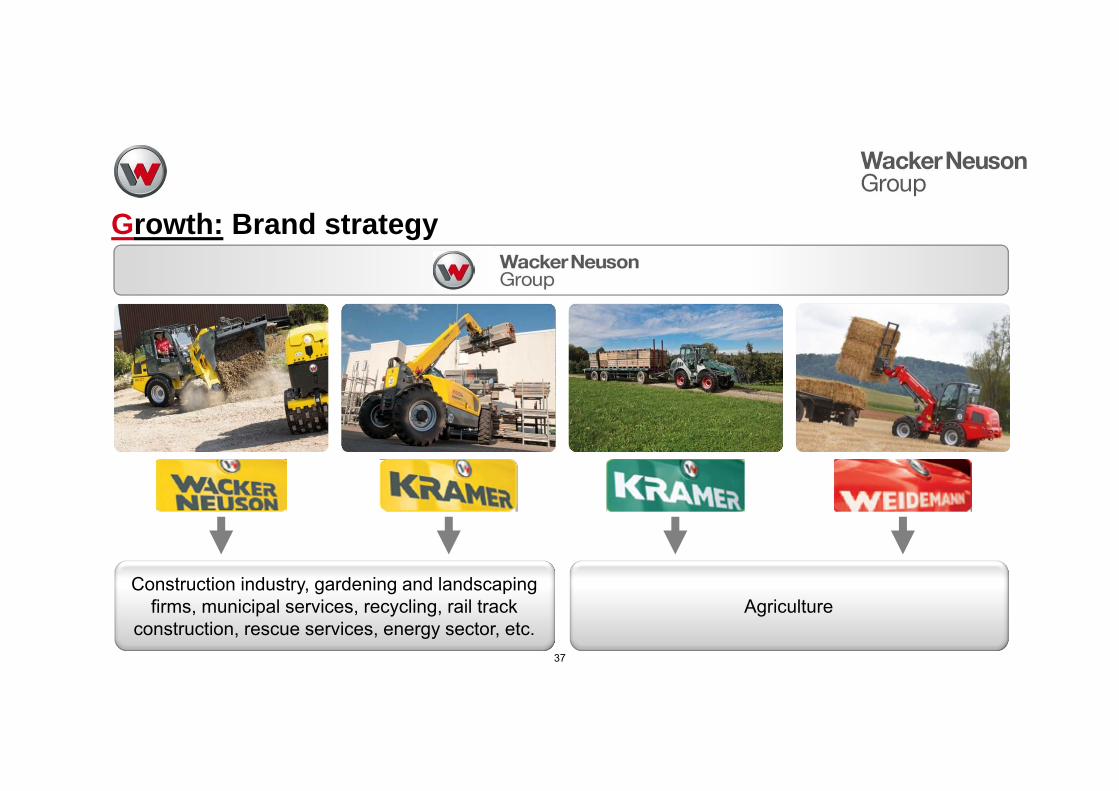

Diversifying in target markets (Wacker Neuson)

9

Gardening and landscaping

Logistics Renovation/demolition Events

Underground construction / infrastructureEnergy

Diversifying in target markets (Kramer and Weidemann)

10

Overground construction Industry

Barn or indoor work Riding stables Organic farms

Recycling

Contents

11

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

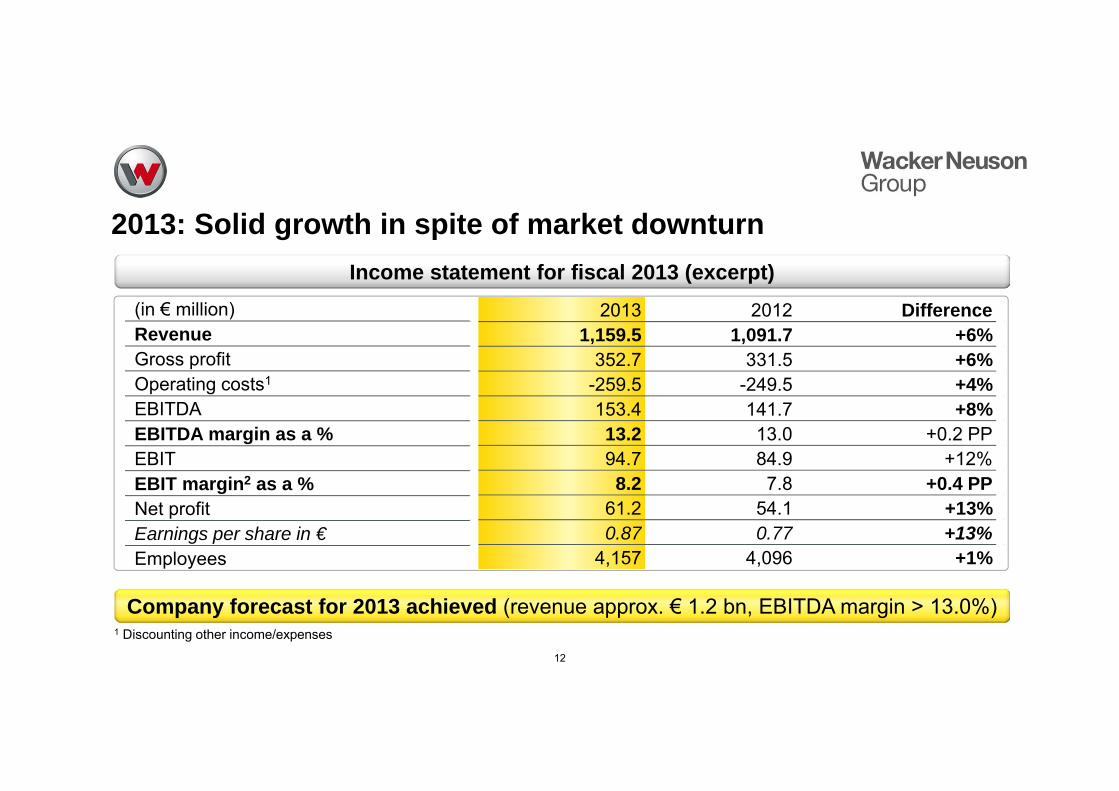

2013: Solid growth in spite of market downturn

(in € million)RevenueGross profitOperating costs1

EBITDAEBITDA margin as a %EBITEBIT margin2 as a %Net profitEarnings per share in €Employees

2013 2012 Difference1,159.5 1,091.7 +6%

352.7 331.5 +6%-259.5 -249.5 +4%153.4 141.7 +8%13.2 13.0 +0.2 PP94.7 84.9 +12%

8.2 7.8 +0.4 PP61.2 54.1 +13%0.87 0.77 +13%

4,157 4,096 +1%

12

1 Discounting other income/expenses

Income statement for fiscal 2013 (excerpt)

Company forecast for 2013 achieved (revenue approx. € 1.2 bn, EBITDA margin > 13.0%)

0%5%10%15%20%25%30%35%40%

0

50

100

150

200

250

300

2009 2010 2011 2012 2013

Cost of sales, R&Dand administration

as a % of revenue

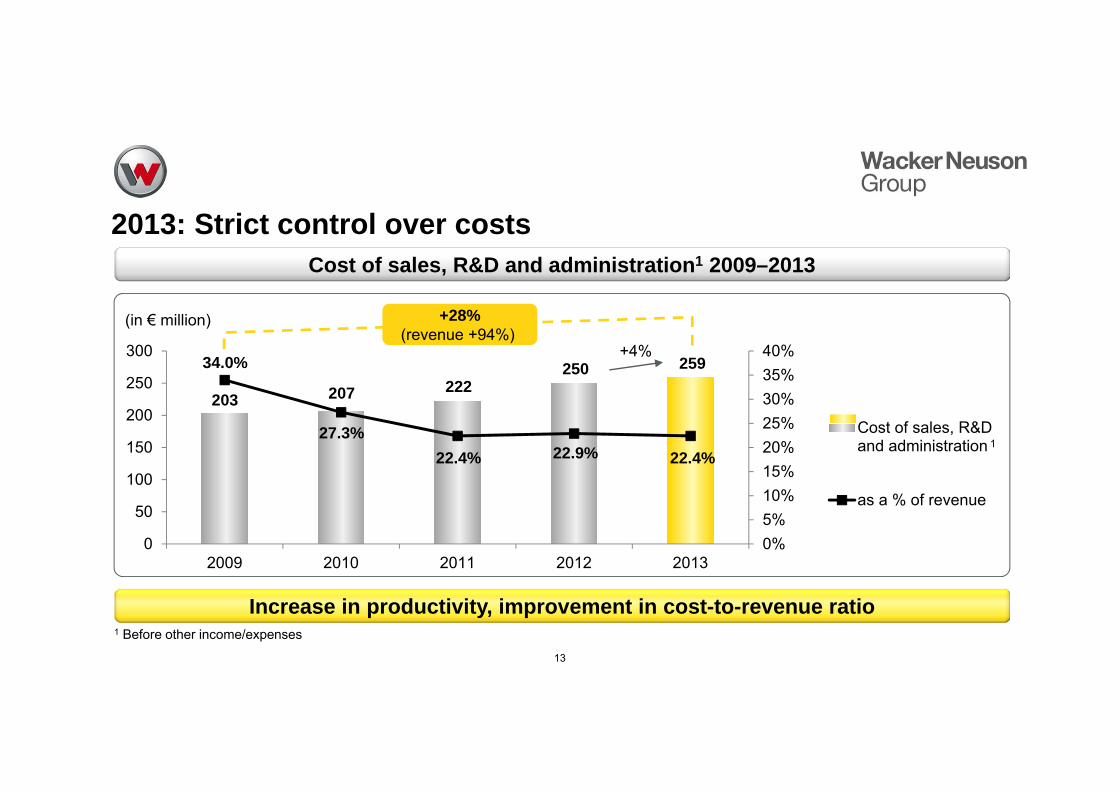

2013: Strict control over costs

34.0%

27.3%

(in € million)

22.9%

203 207 222250

+28%(revenue +94%)

259

22.4%

+4%

22.4%

13

1

1 Before other income/expenses

Cost of sales, R&D and administration1 2009–2013

Increase in productivity, improvement in cost-to-revenue ratio

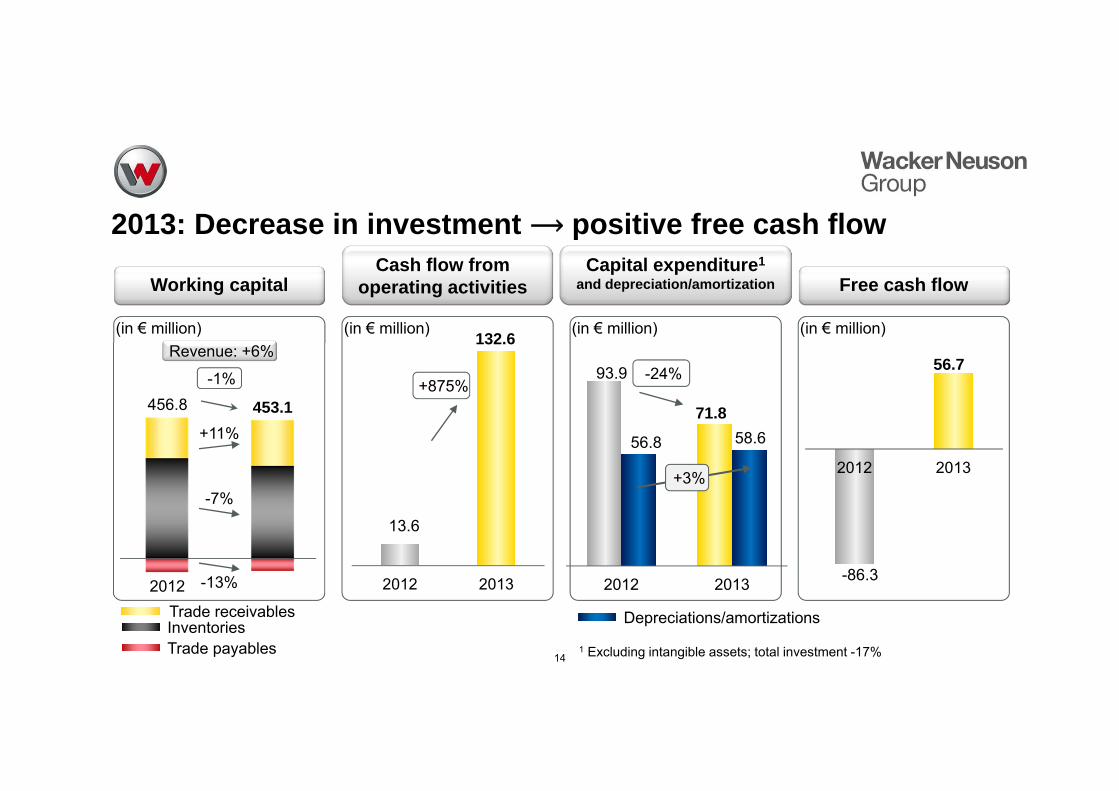

Capital expenditure1

and depreciation/amortization

2013: Decrease in investment ⟶ positive free cash flow

14

Working capitalCash flow from

operating activities Free cash flow

Trade receivablesInventoriesTrade payables 1 Excluding intangible assets; total investment -17%

(in € million)

456.8 453.1

-1%

+11%

-7%

-13%2012

Revenue: +6%

2012 2013 2012 2013

2012 2013

71.8

93.9 -24%

132.6

13.6

+875%56.7

-86.3

(in € million) (in € million) (in € million)

+3%

56.8 58.6

Depreciations/amortizations

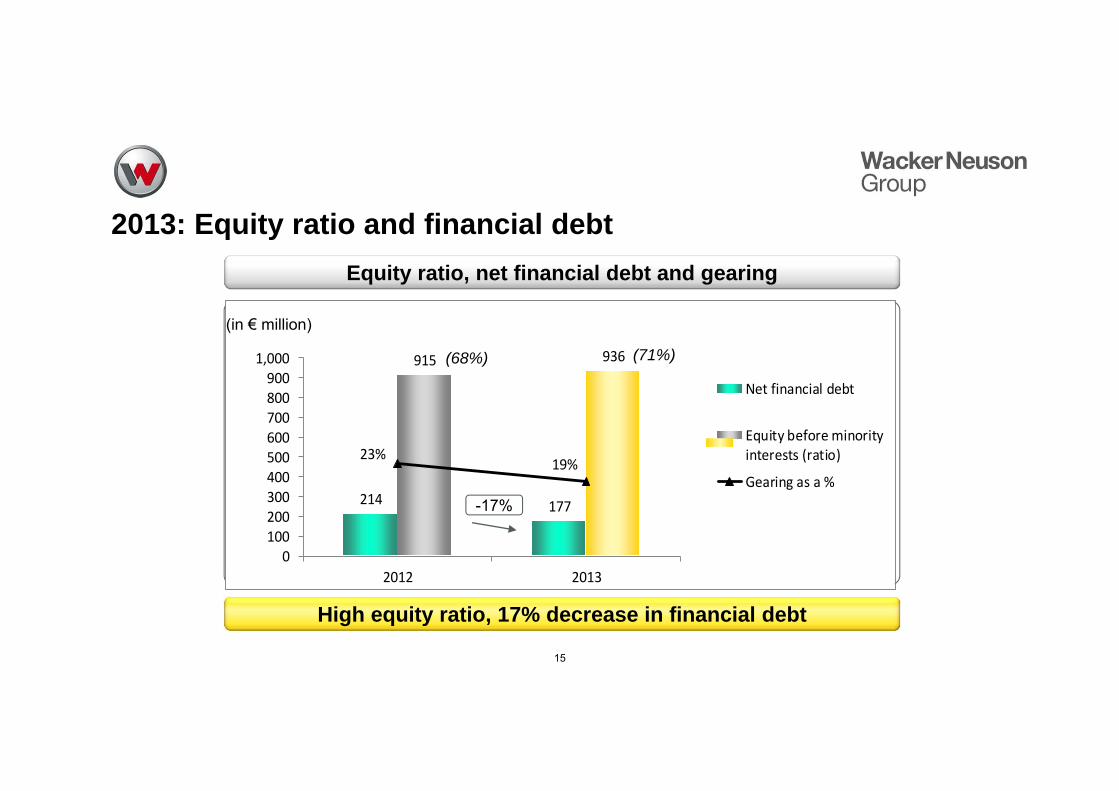

2013: Equity ratio and financial debt

15

Equity ratio, net financial debt and gearing

High equity ratio, 17% decrease in financial debt

214 177

915 936

23%19%

0.0%5.0%10.0%15.0%20.0%25.0%30.0%35.0%40.0%45.0%50.0%

0100200300400500600700800900

1,000

2012 2013

Net financial debt

Equity before minorityinterests (ratio)

Gearing as a %

(68%)

-17%

(71%)

(in € million)

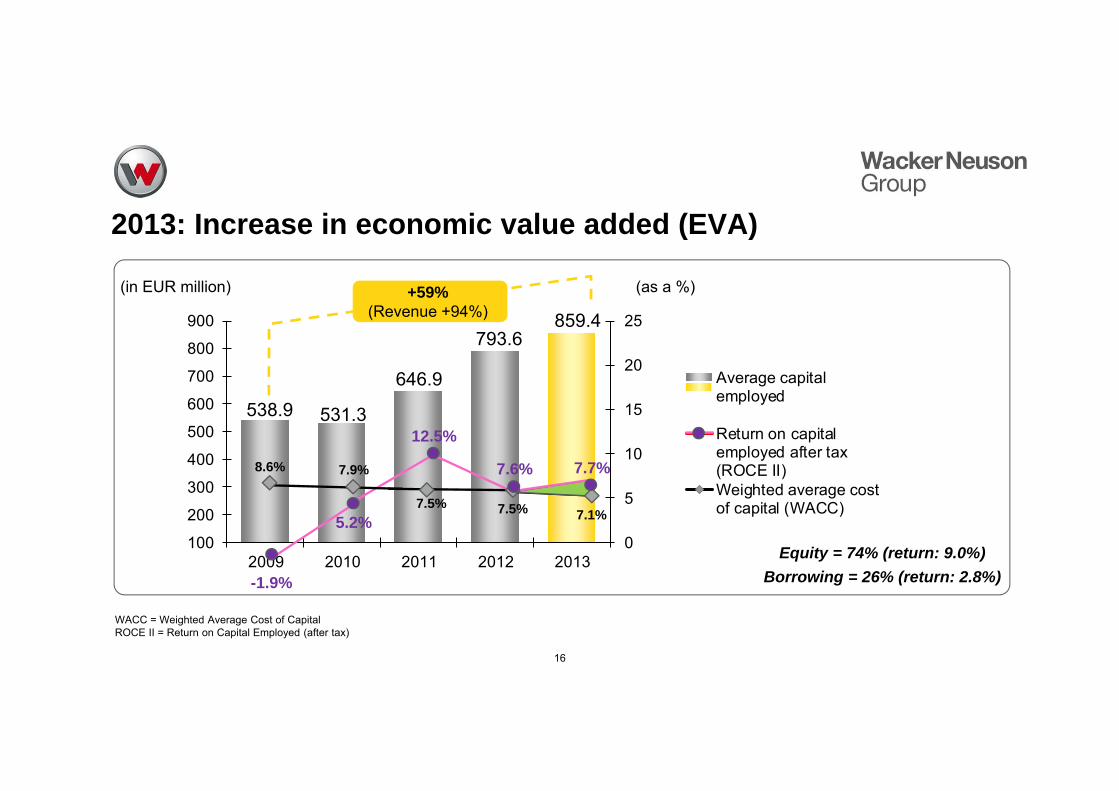

2013: Increase in economic value added (EVA)

0

5

10

15

20

25

100

200

300

400

500

600

700

800

900

2009 2010 2011 2012 2013

Average capitalemployed

Return on capitalemployed after tax(ROCE II)Weighted average costof capital (WACC)

(in EUR million) (as a %)

646.9

531.3538.9

WACC = Weighted Average Cost of CapitalROCE II = Return on Capital Employed (after tax)

-1.9%

12.5%

8.6% 7.9%

7.5%

793.6859.4

5.2%

7.6%

7.5%

7.7%

7.1%

16

Equity = 74% (return: 9.0%)Borrowing = 26% (return: 2.8%)

+59% (Revenue +94%)

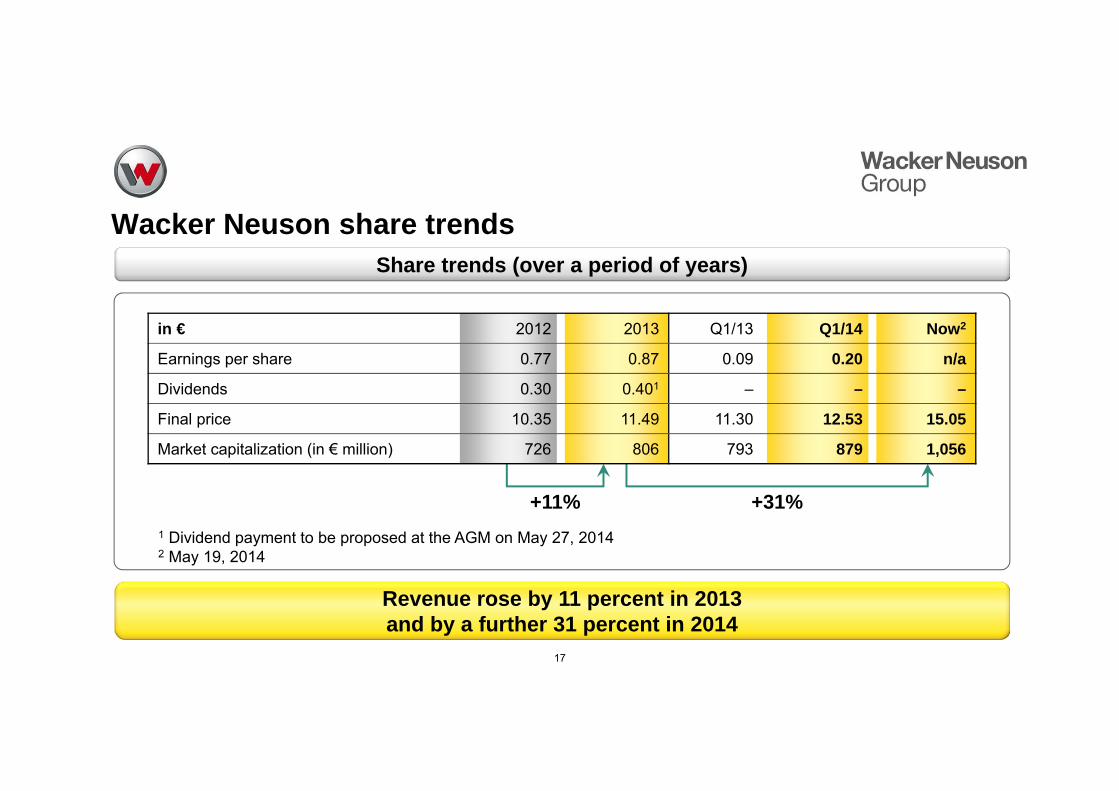

Wacker Neuson share trends

in € 2012 2013 Q1/13 Q1/14 Now2

Earnings per share 0.77 0.87 0.09 0.20 n/a

Dividends 0.30 0.401 – – –

Final price 10.35 11.49 11.30 12.53 15.05

Market capitalization (in € million) 726 806 793 879 1,056

1 Dividend payment to be proposed at the AGM on May 27, 20142 May 19, 2014

17

+31%+11%

Share trends (over a period of years)

Revenue rose by 11 percent in 2013and by a further 31 percent in 2014

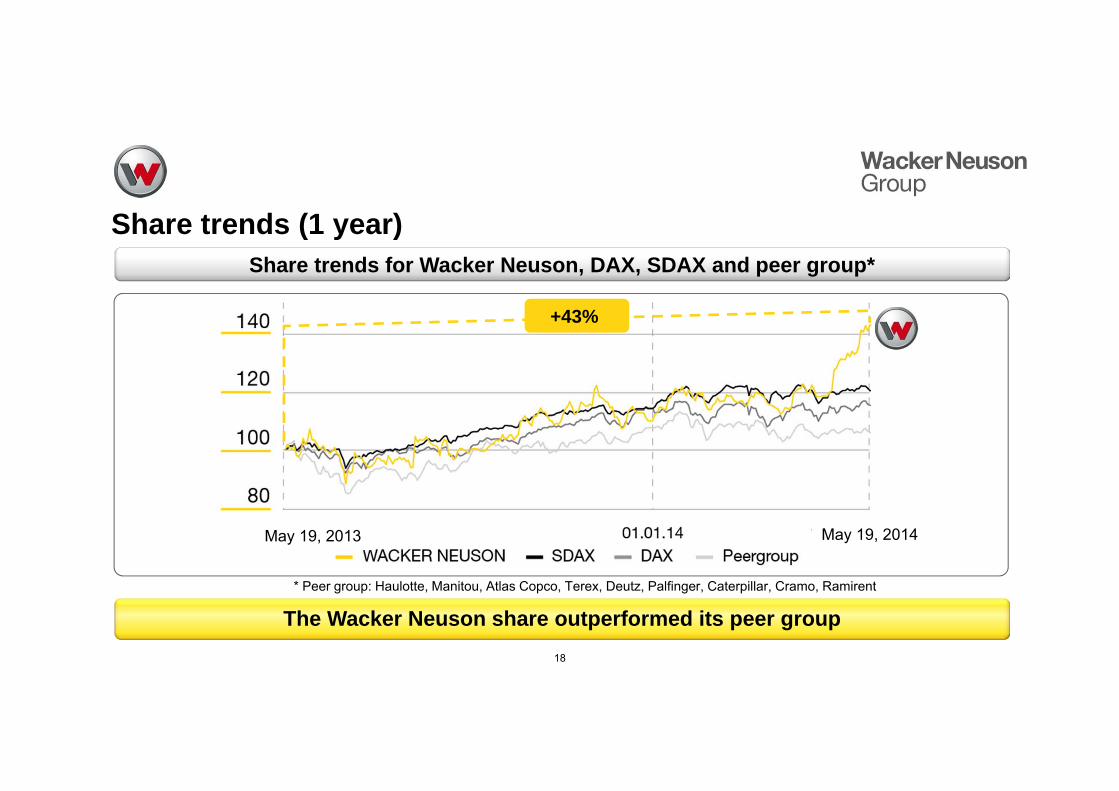

Share trends (1 year)

18

Share trends for Wacker Neuson, DAX, SDAX and peer group*

The Wacker Neuson share outperformed its peer group

+43%

May 19, 2014May 19, 2013

* Peer group: Haulotte, Manitou, Atlas Copco, Terex, Deutz, Palfinger, Caterpillar, Cramo, Ramirent

Contents

19

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

Reference (apr02) 20

Technology

21

We strive for excellence in everything we do.

RESEARCH AND DEVELOPMENT

New team set up: Corporate Technology, Standardization & Design Intensive technology-focused knowledge sharing across sites

Standardization of processes, workflows and tools

Uniform part and platform strategy

Group-wide technology and supplier strategy

Technology

22

We strive for excellence in everything we do.

PURCHASING

New team set up: Corporate Purchasing Group-wide and international strategic procurement unit

Utilization of synergies within the Group to gain worldwide access to the best suppliers

Standardization of processes and workflows

Reduction in the number of suppliers in line with TCO criteria→ innovation, quality, price and performance

Technology

23

QUALITY

New team set up: Corporate Quality Quality planning is an integral part of our product development process

Continuous improvement in quality and cost

Standardization of processes and workflows

Steering and benchmarking of plants and suppliers using Group-wide KPIs

Preemptive qualification of suppliers and targeted focus on strategic suppliers

We strive for excellence in everything we do.

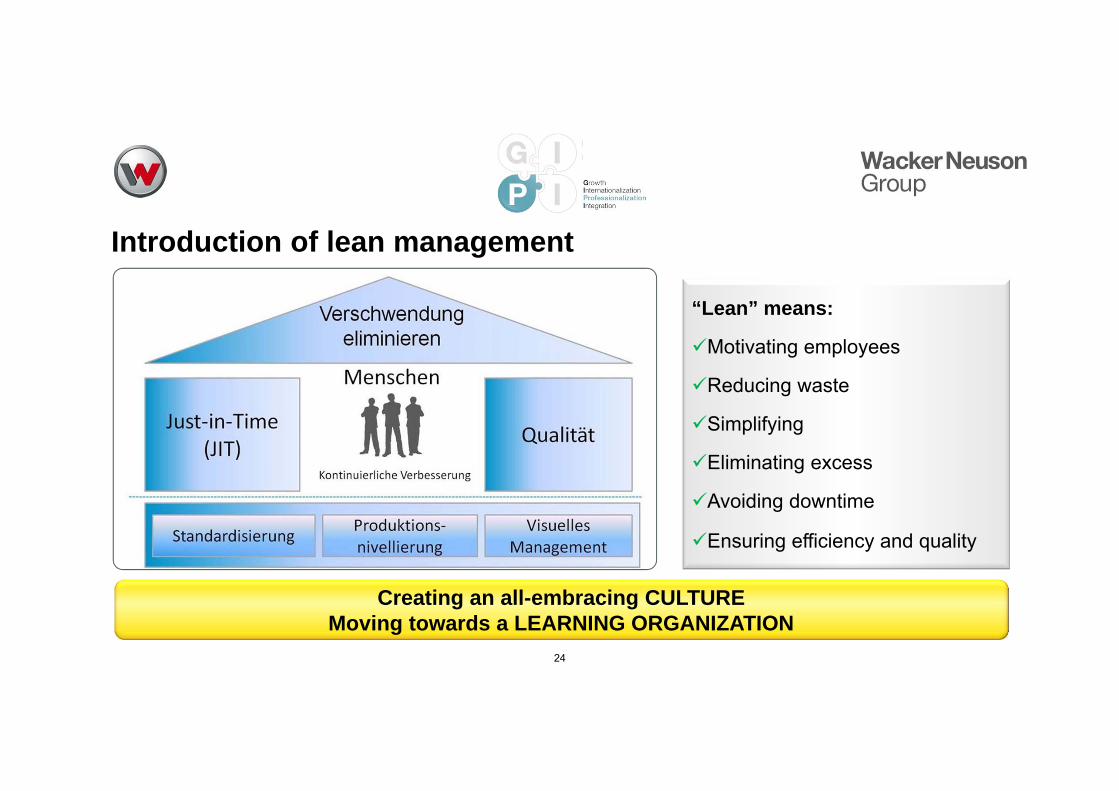

Introduction of lean management

24

“Lean” means:

Motivating employees

Reducing waste

Simplifying

Eliminating excess

Avoiding downtime

Ensuring efficiency and quality

Creating an all-embracing CULTURE Moving towards a LEARNING ORGANIZATION

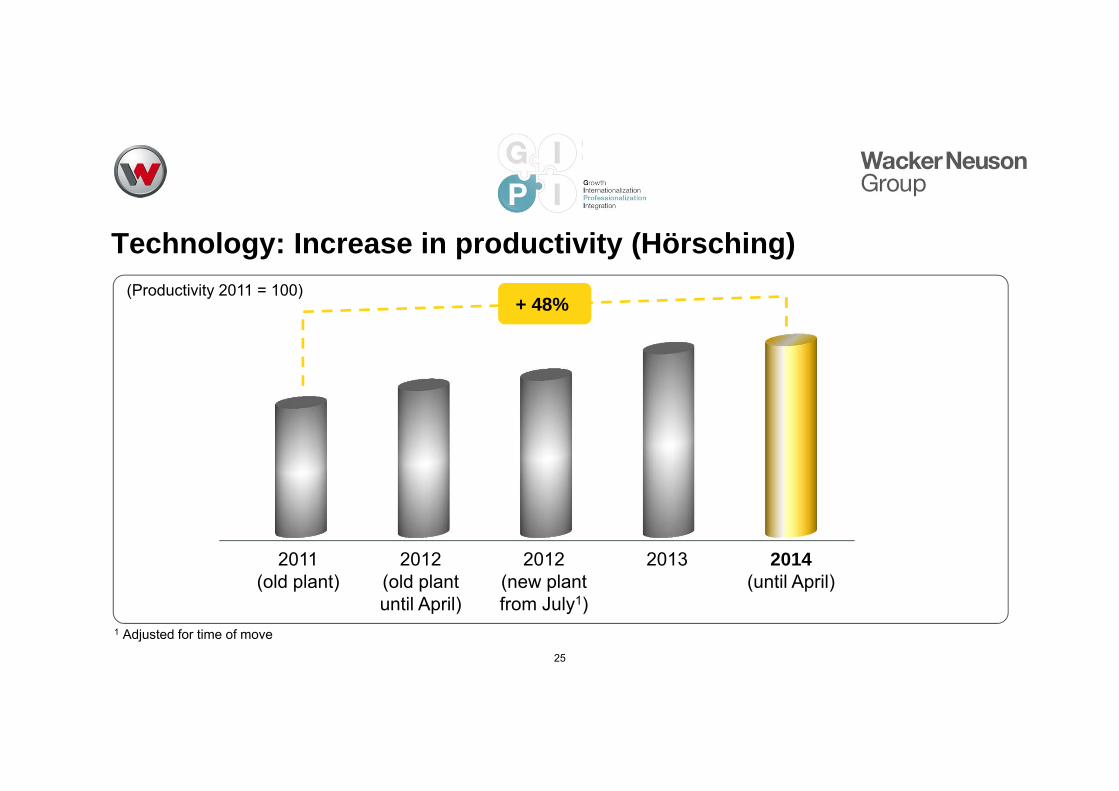

Technology: Increase in productivity (Hörsching)

25

Datenbasis BW

(Productivity 2011 = 100)

2011 (old plant)

2012 (old plant until April)

2012 (new plant from July1)

2013 2014(until April)

+ 48%

1 Adjusted for time of move

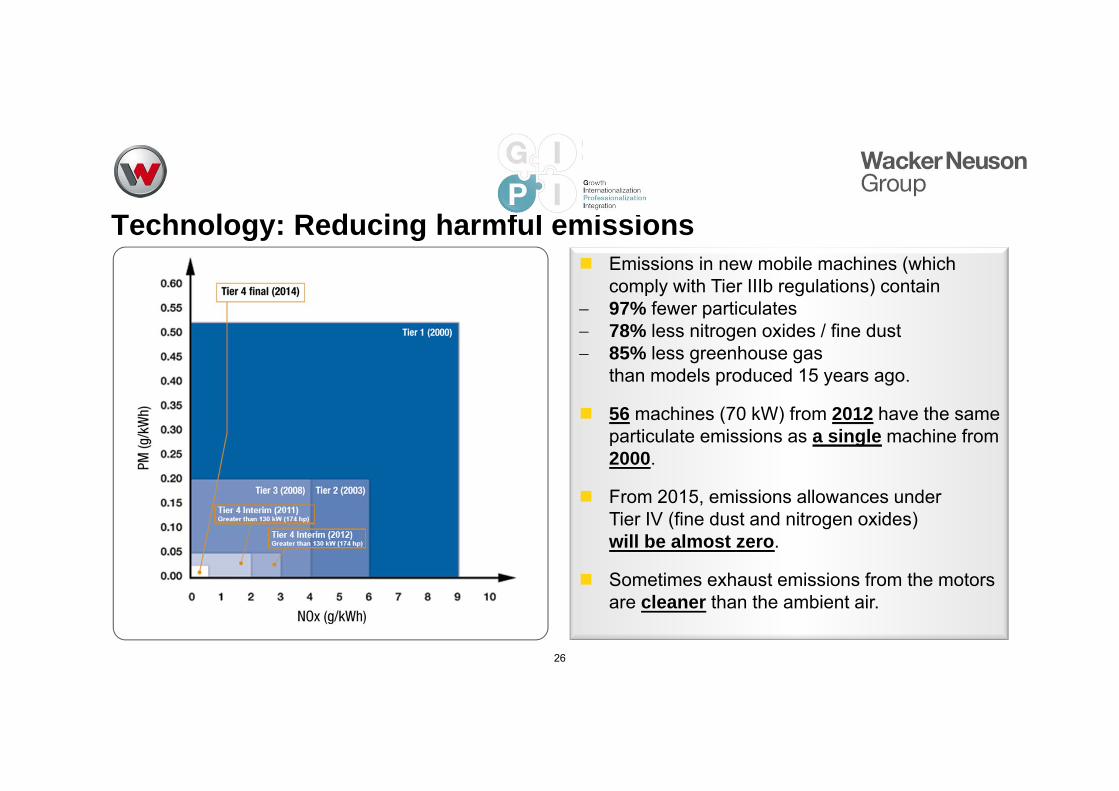

Technology: Reducing harmful emissions

26

Emissions in new mobile machines (which comply with Tier IIIb regulations) contain

97% fewer particulates 78% less nitrogen oxides / fine dust 85% less greenhouse gas

than models produced 15 years ago.

56 machines (70 kW) from 2012 have the same particulate emissions as a single machine from 2000.

From 2015, emissions allowances underTier IV (fine dust and nitrogen oxides)will be almost zero.

Sometimes exhaust emissions from the motors are cleaner than the ambient air.

Introduction of green ECO seal

27

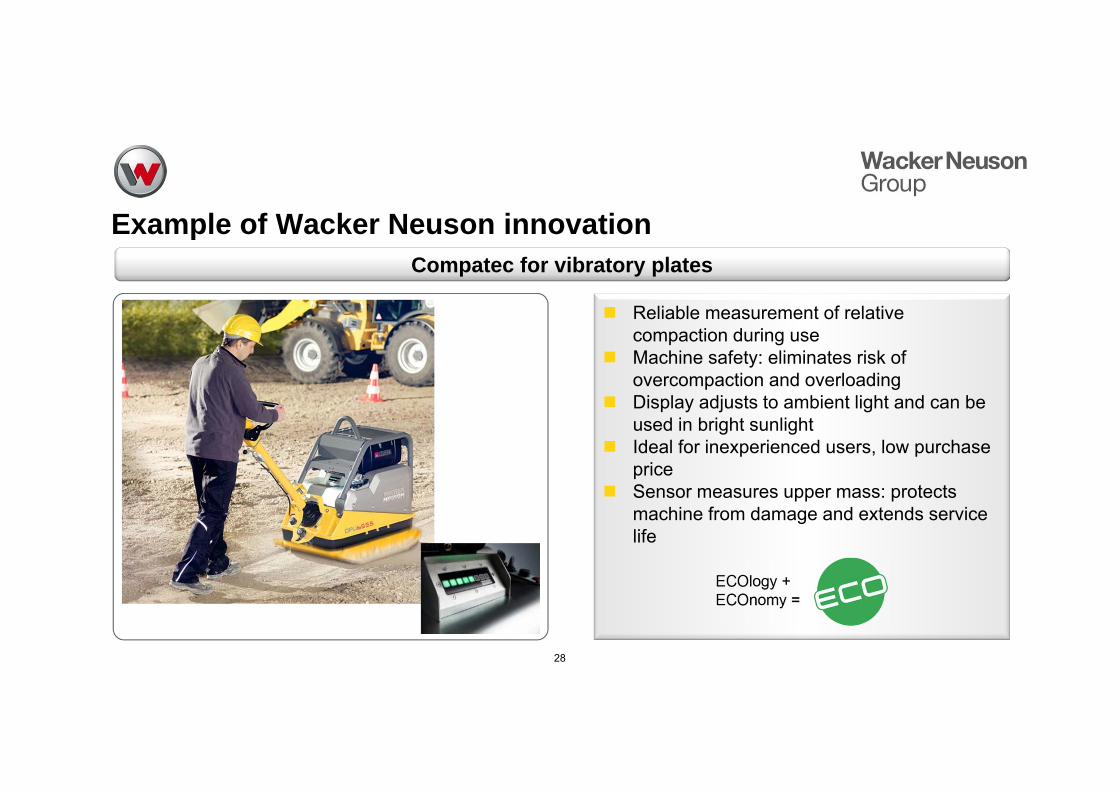

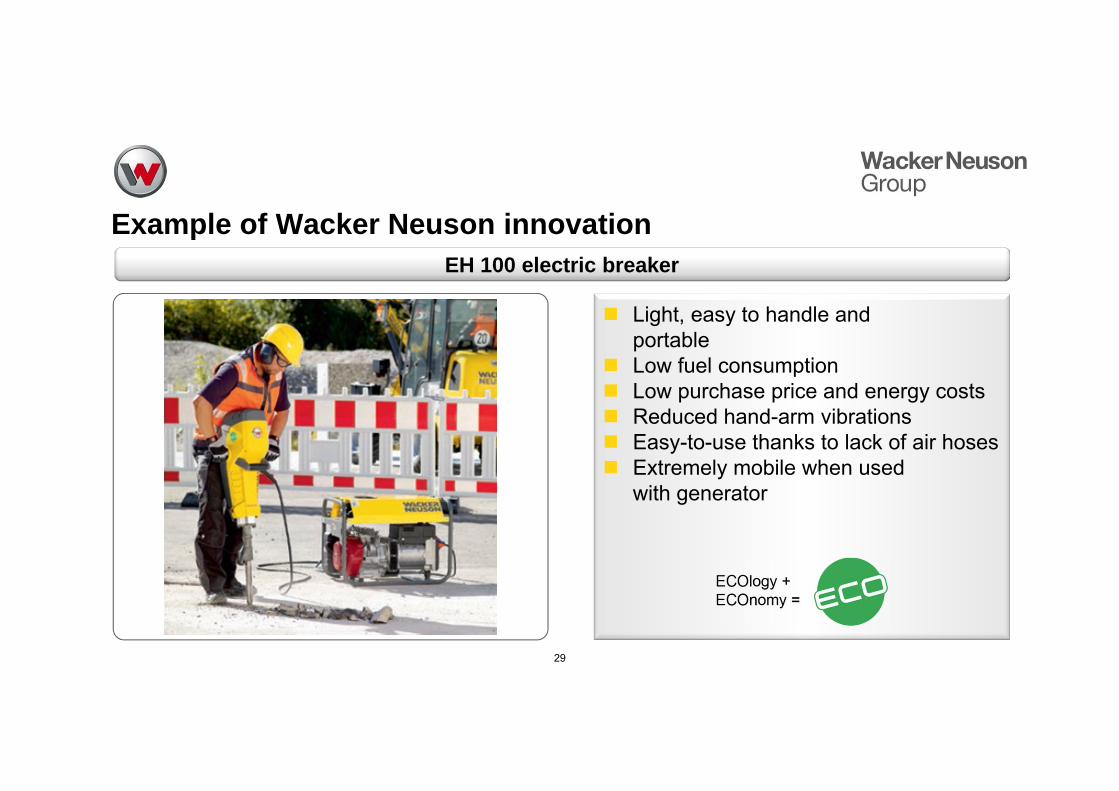

Example of Wacker Neuson innovation

28

Compatec for vibratory plates

Reliable measurement of relative compaction during use

Machine safety: eliminates risk of overcompaction and overloading

Display adjusts to ambient light and can be used in bright sunlight

Ideal for inexperienced users, low purchase price

Sensor measures upper mass: protects machine from damage and extends service life

Light, easy to handle andportable

Low fuel consumption Low purchase price and energy costs Reduced hand-arm vibrations Easy-to-use thanks to lack of air hoses Extremely mobile when used

with generator

Example of Wacker Neuson innovation

29

EH 100 electric breaker

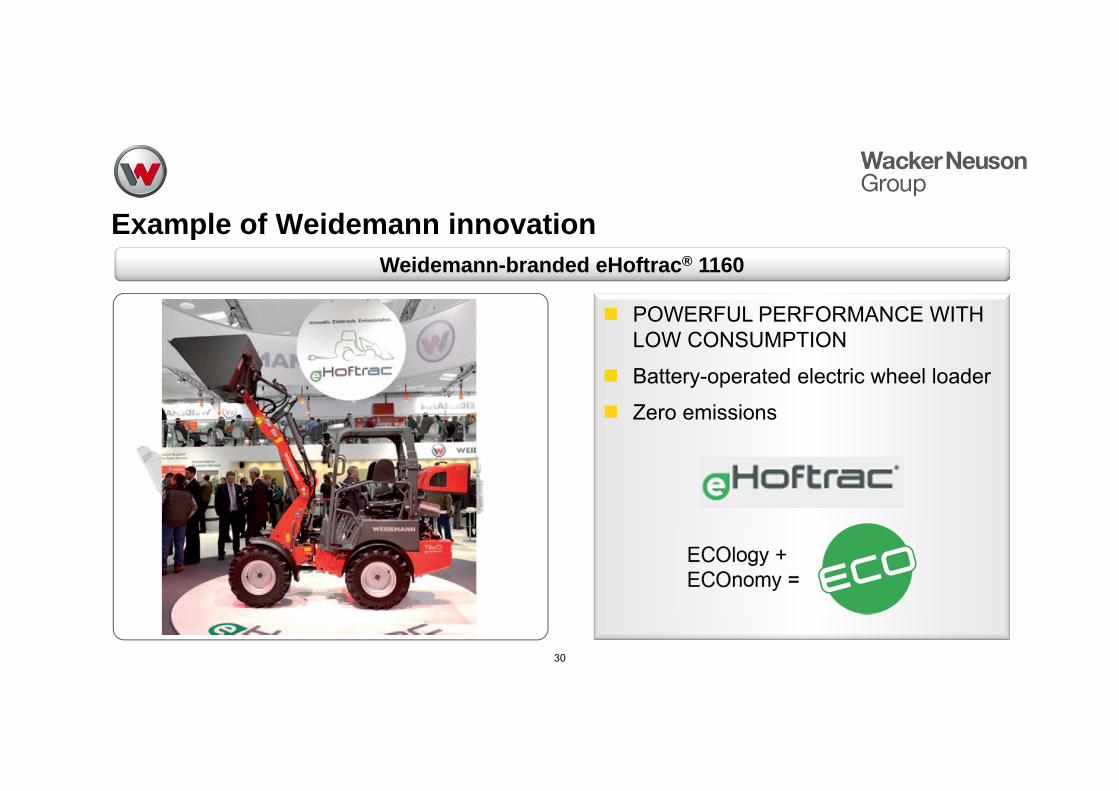

POWERFUL PERFORMANCE WITH LOW CONSUMPTION

Battery-operated electric wheel loader

Zero emissions

Example of Weidemann innovation

30

Weidemann-branded eHoftrac® 1160

Example of Wacker Neuson innovation

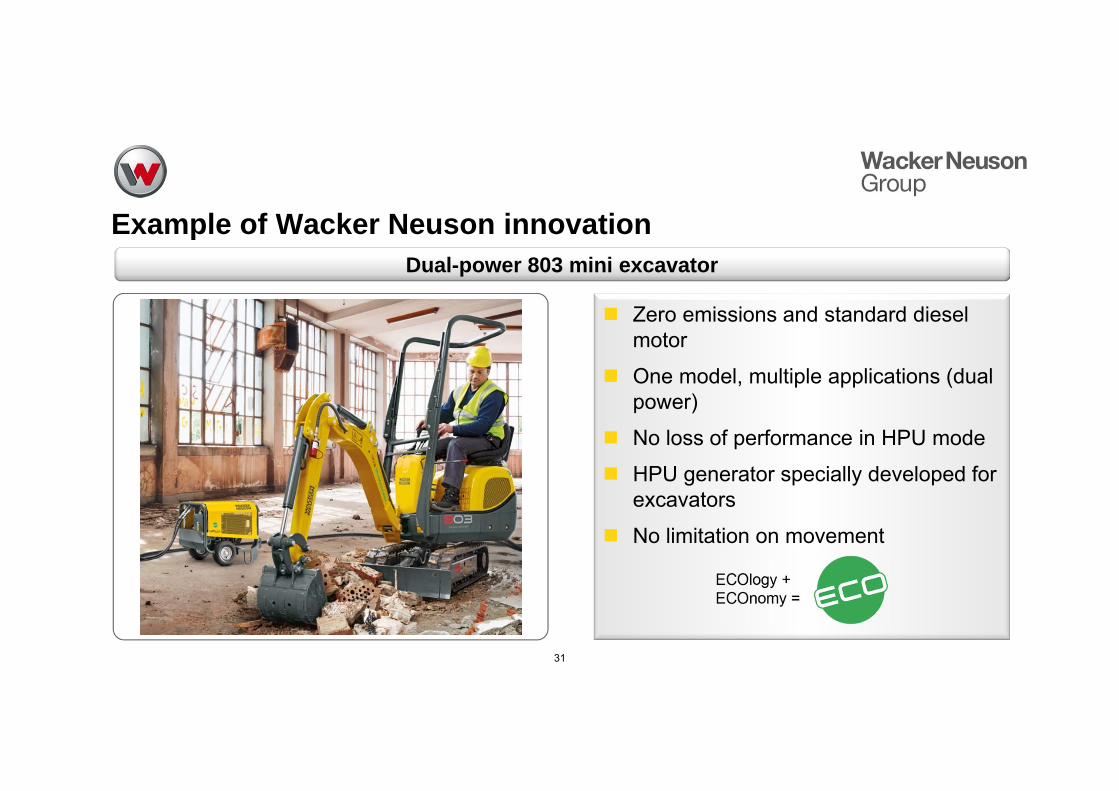

31

Dual-power 803 mini excavator

Zero emissions and standard diesel motor

One model, multiple applications (dual power)

No loss of performance in HPU mode

HPU generator specially developed for excavators

No limitation on movement

Contents

32

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

33

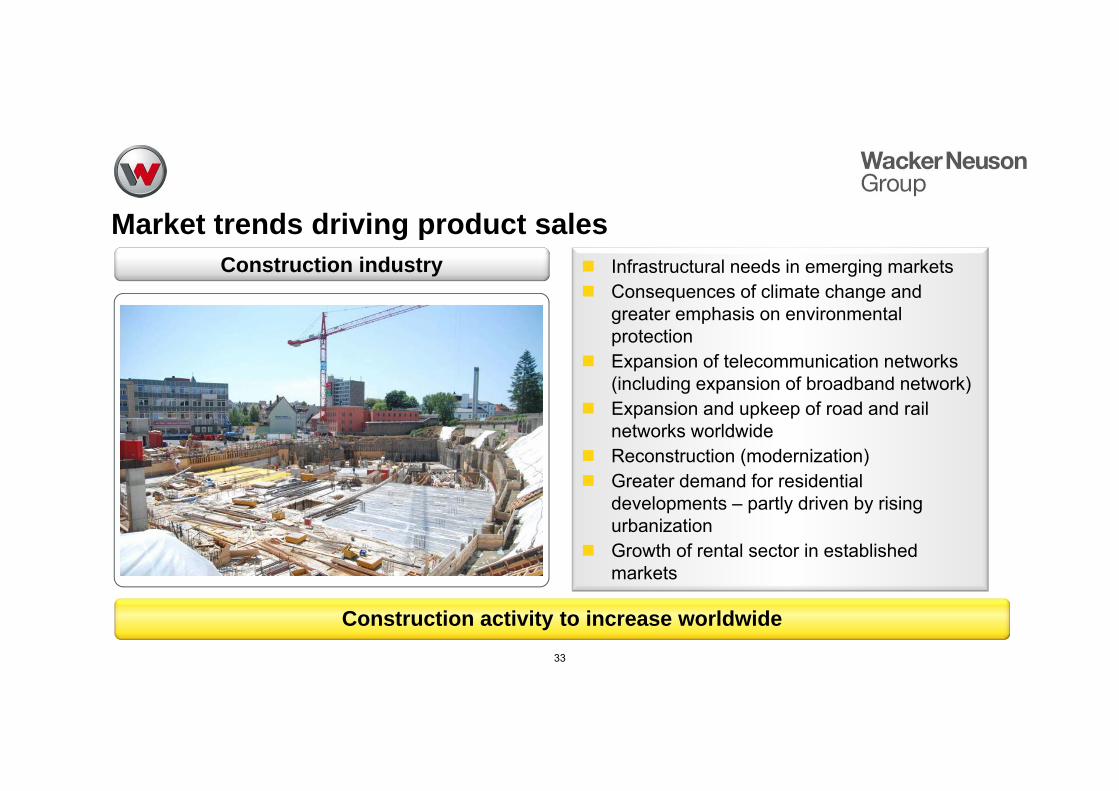

Market trends driving product sales

Construction activity to increase worldwide

Construction industry Infrastructural needs in emerging markets Consequences of climate change and

greater emphasis on environmental protection

Expansion of telecommunication networks (including expansion of broadband network)

Expansion and upkeep of road and rail networks worldwide

Reconstruction (modernization) Greater demand for residential

developments – partly driven by rising urbanization

Growth of rental sector in established markets

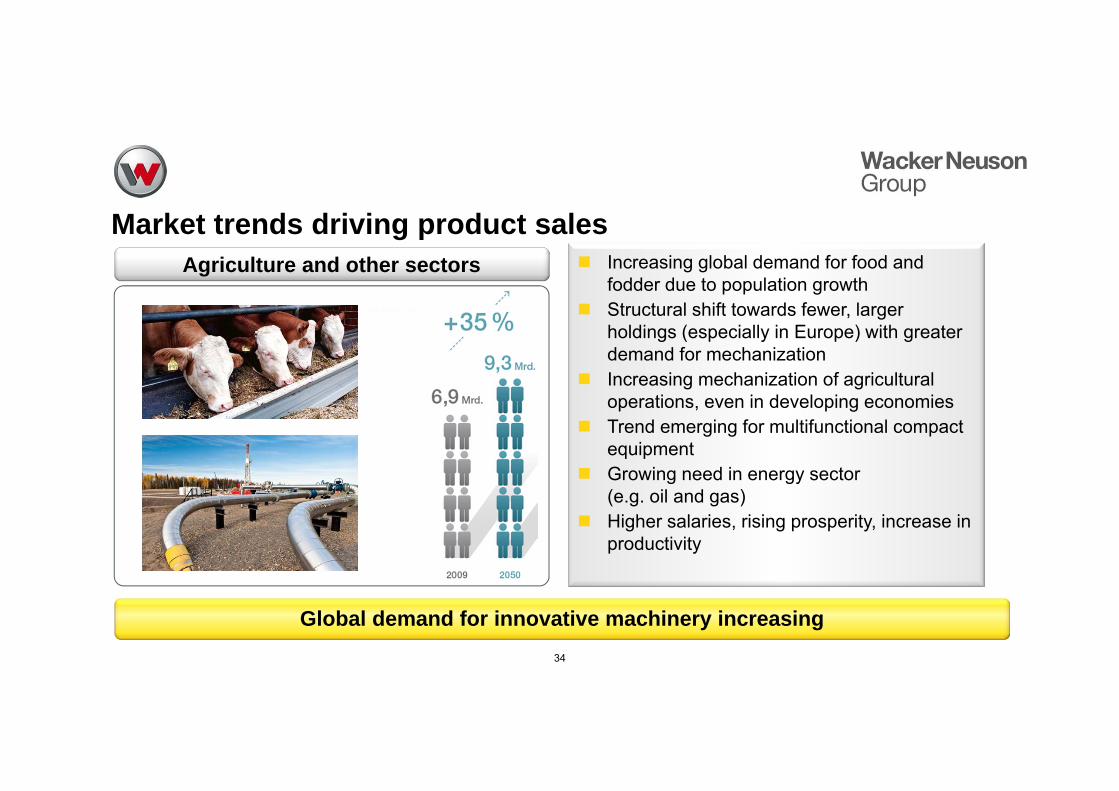

Market trends driving product sales

34

Global demand for innovative machinery increasing

Agriculture and other sectors Increasing global demand for food and fodder due to population growth

Structural shift towards fewer, larger holdings (especially in Europe) with greater demand for mechanization

Increasing mechanization of agricultural operations, even in developing economies

Trend emerging for multifunctional compact equipment

Growing need in energy sector(e.g. oil and gas)

Higher salaries, rising prosperity, increase in productivity

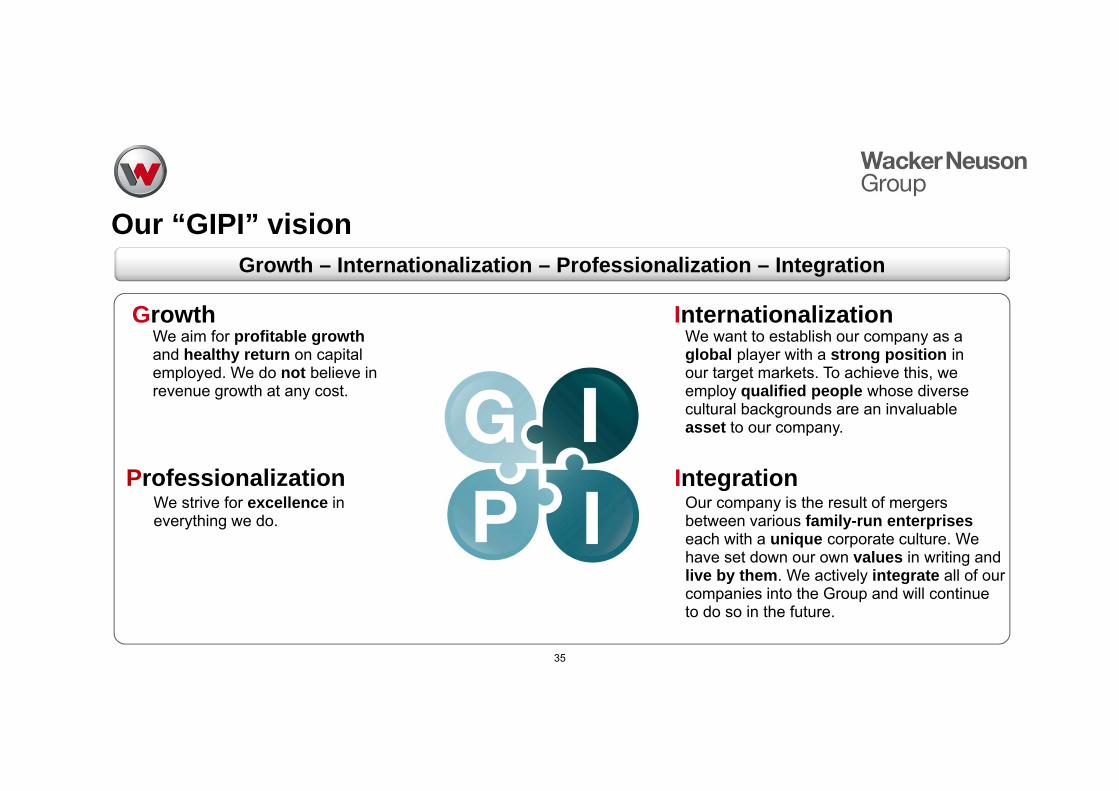

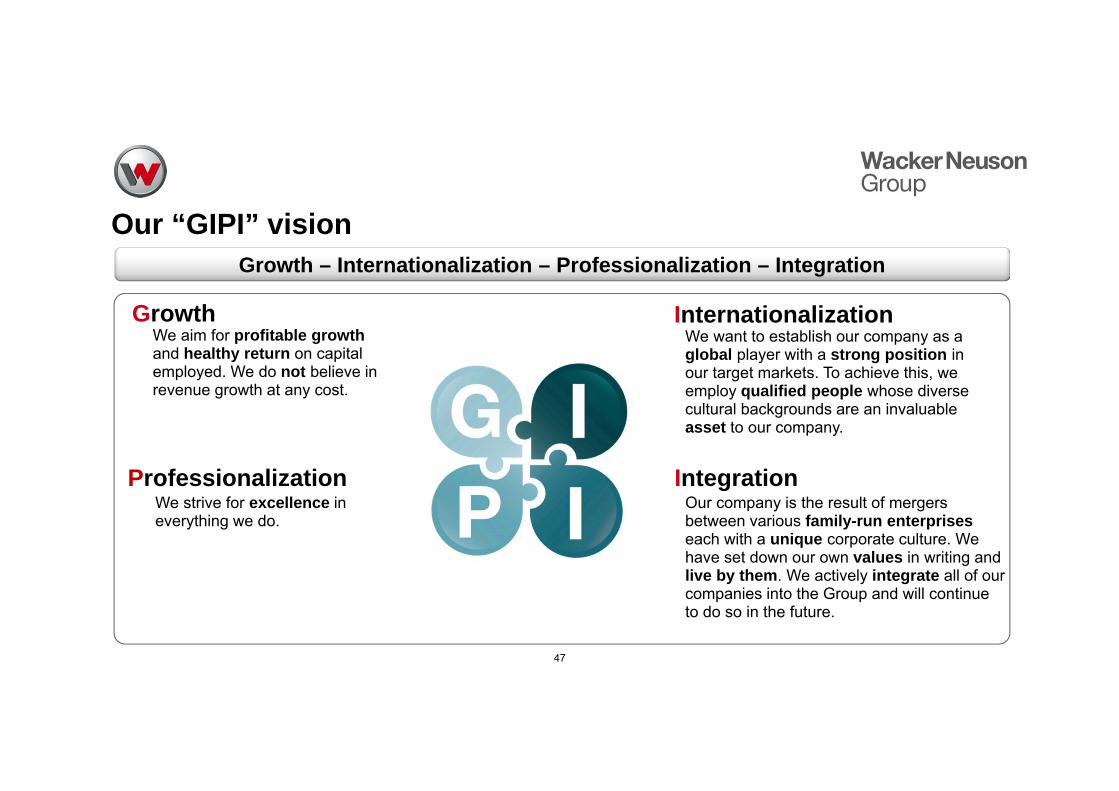

Our “GIPI” vision

35

Growth – Internationalization – Professionalization – Integration

Our company is the result of mergers between various family-run enterpriseseach with a unique corporate culture. We have set down our own values in writing and live by them. We actively integrate all of our companies into the Group and will continue to do so in the future.

Integration

We want to establish our company as a global player with a strong position in our target markets. To achieve this, we employ qualified people whose diverse cultural backgrounds are an invaluable asset to our company.

InternationalizationGrowthWe aim for profitable growthand healthy return on capital employed. We do not believe in revenue growth at any cost.

ProfessionalizationWe strive for excellence in everything we do.

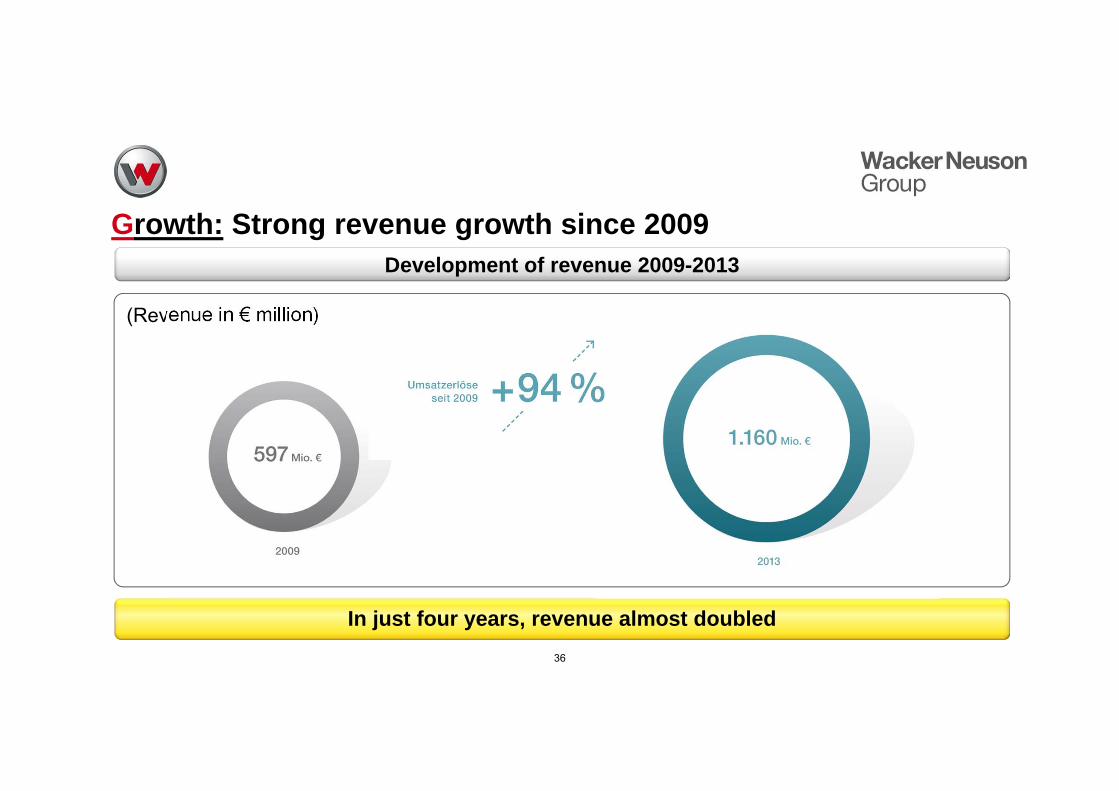

Growth: Strong revenue growth since 2009

36

(Revenue in € million)

Development of revenue 2009-2013

In just four years, revenue almost doubled

Construction industry, gardening and landscaping firms, municipal services, recycling, rail track

construction, rescue services, energy sector, etc.Agriculture

Growth: Brand strategy

37

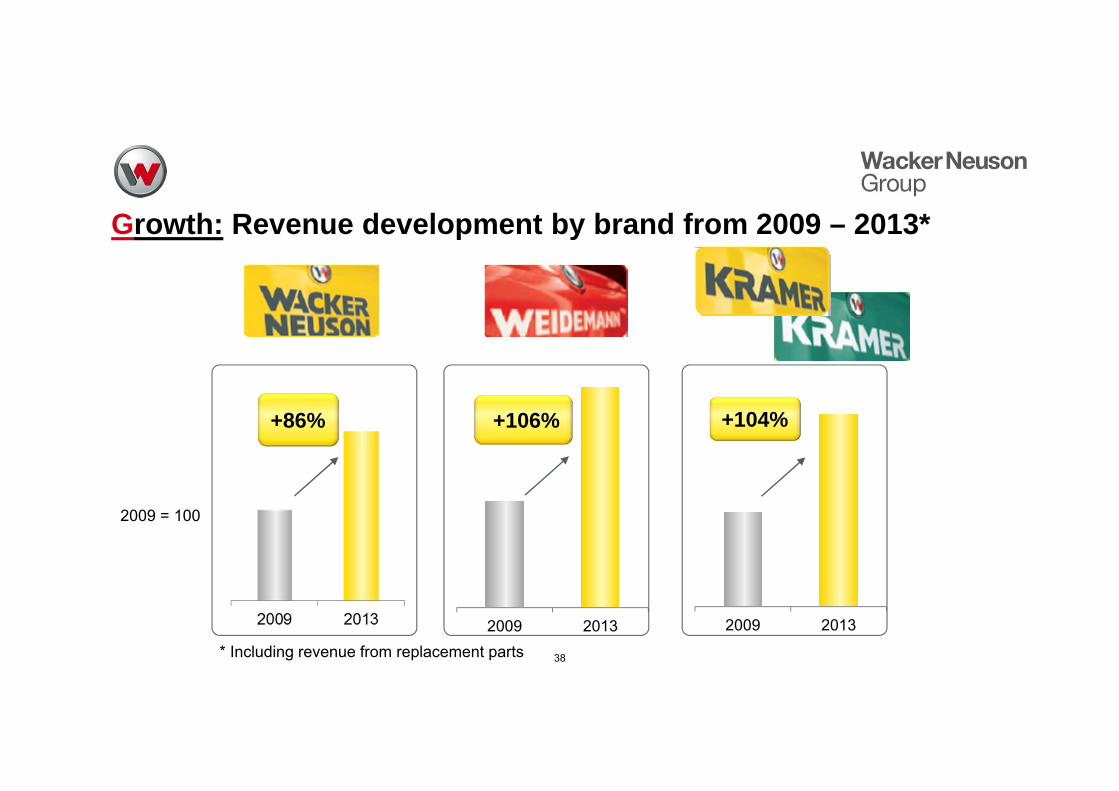

Growth: Revenue development by brand from 2009 – 2013*

38

+86%

2009 2013

+106%

2009 2013

+104%

* Including revenue from replacement parts

2009 = 100

Growth: Strategic alliances

39

Agriculture Construction industry

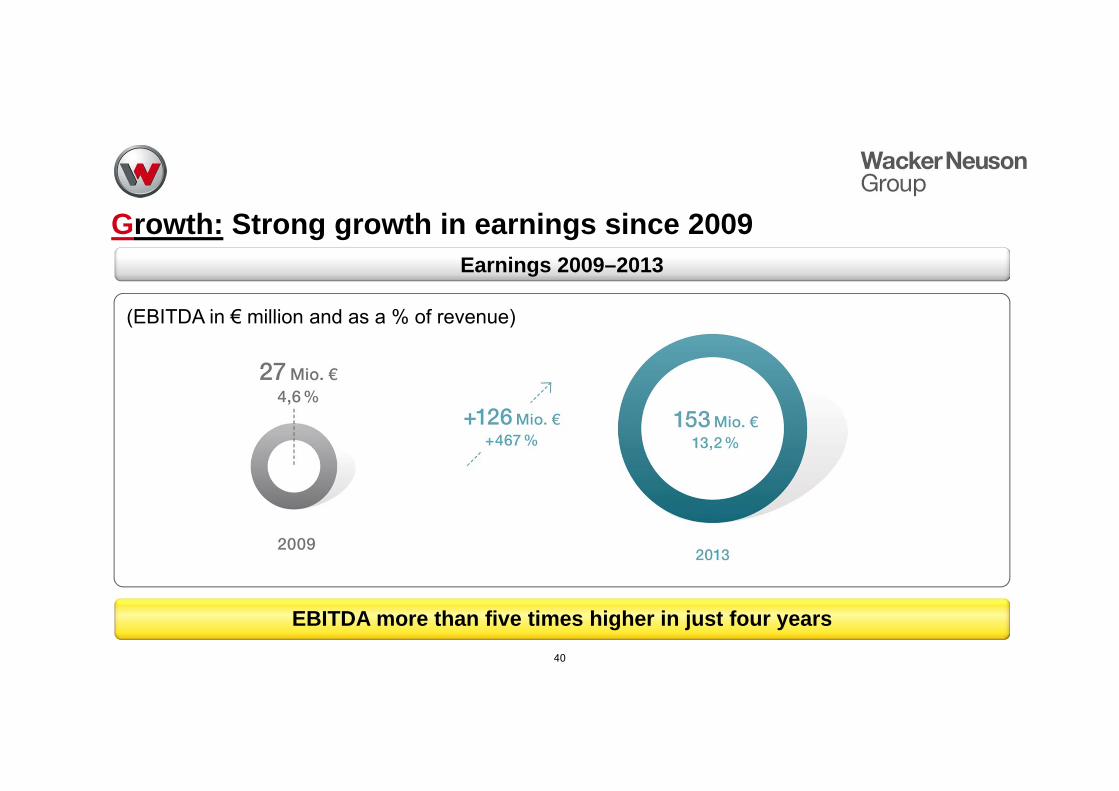

Growth: Strong growth in earnings since 2009

40

Earnings 2009–2013

EBITDA more than five times higher in just four years

(EBITDA in € million and as a % of revenue)

41

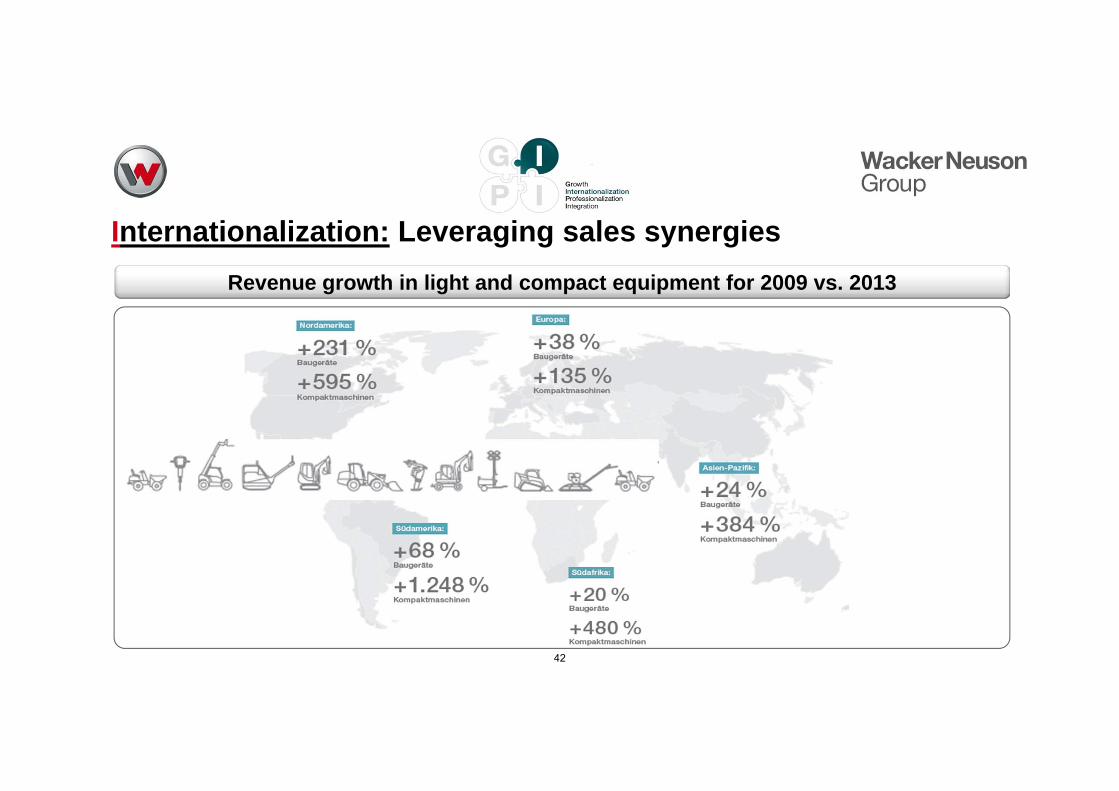

Internationalization: Leveraging sales synergies

42

Revenue growth in light and compact equipment for 2009 vs. 2013

43

Sustainability brochureProfessionalization: Sustainability management

44

Stepping up to our responsibilities to the environment and society as a whole

2013 Annual Report

45

Integration: Annual management meeting

46

Global Leader Summit: strategy – discussion – workshops

We can only achieve our goals if we work together with all our employees around the world

We want to establish our company as a global player with a strong position in our target markets. To achieve this, we employ qualified people whose diverse cultural backgrounds are an invaluable asset to our company.

InternationalizationGrowthWe aim for profitable growthand healthy return on capital employed. We do not believe in revenue growth at any cost.

Our company is the result of mergers between various family-run enterpriseseach with a unique corporate culture. We have set down our own values in writing and live by them. We actively integrate all of our companies into the Group and will continue to do so in the future.

IntegrationProfessionalizationWe strive for excellence in everything we do.

Our “GIPI” vision

47

Growth – Internationalization – Professionalization – Integration

Contents

48

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

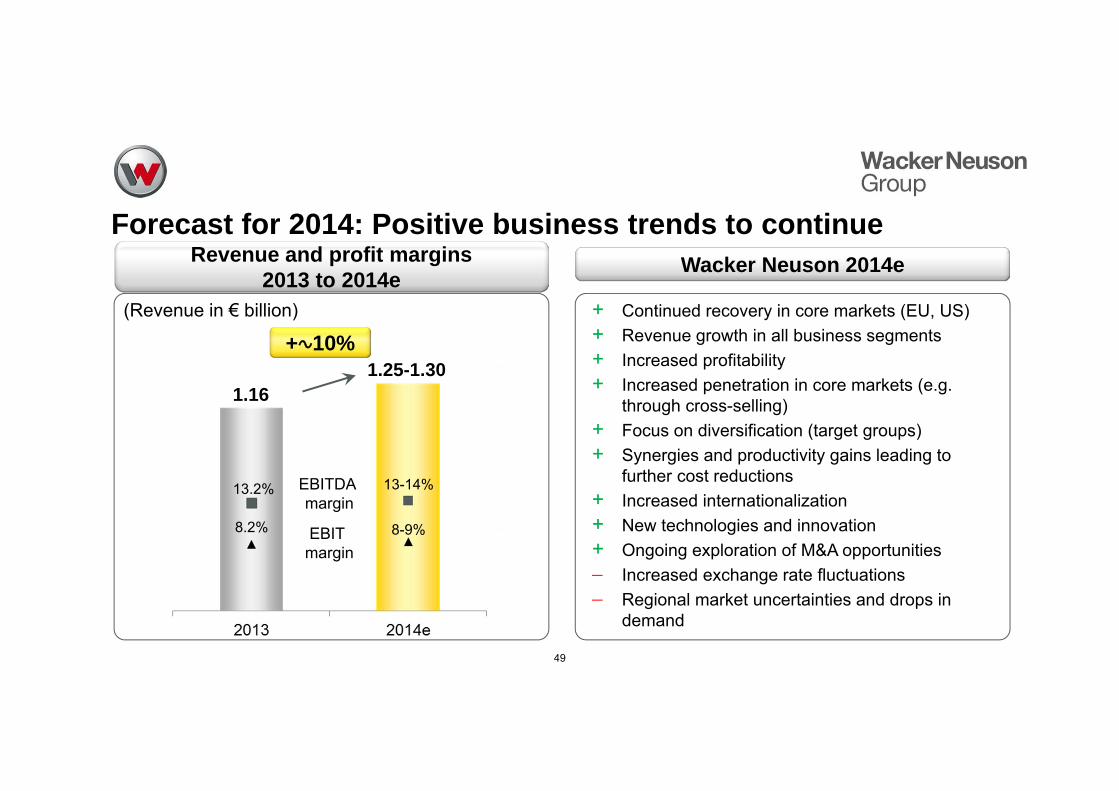

Forecast for 2014: Positive business trends to continue

(Revenue in € billion)

1.16

13-14%13.2%

+∿10%1.25-1.30

8-9%8.2%

49

Revenue and profit margins 2013 to 2014e

Wacker Neuson 2014e

EBITDA margin

EBIT margin

+ Continued recovery in core markets (EU, US)+ Revenue growth in all business segments+ Increased profitability+ Increased penetration in core markets (e.g.

through cross-selling)+ Focus on diversification (target groups)+ Synergies and productivity gains leading to

further cost reductions+ Increased internationalization+ New technologies and innovation+ Ongoing exploration of M&A opportunities Increased exchange rate fluctuations Regional market uncertainties and drops in

demand

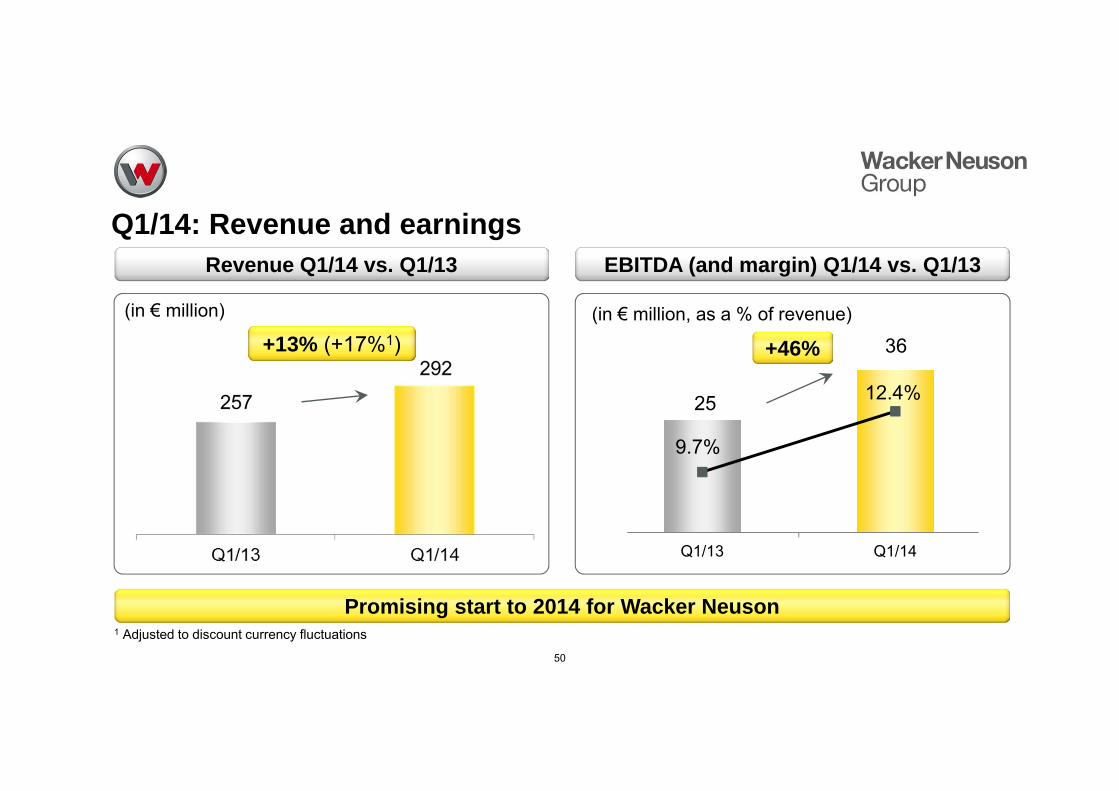

25

36

9.7%

12.4%

789101112131415

05

10152025303540

Q1/13 Q1/14

Q1/14: Revenue and earnings

50

(in € million) (in € million, as a % of revenue)

+13% (+17%1) +46%

Revenue Q1/14 vs. Q1/13 EBITDA (and margin) Q1/14 vs. Q1/13

1 Adjusted to discount currency fluctuations

Promising start to 2014 for Wacker Neuson

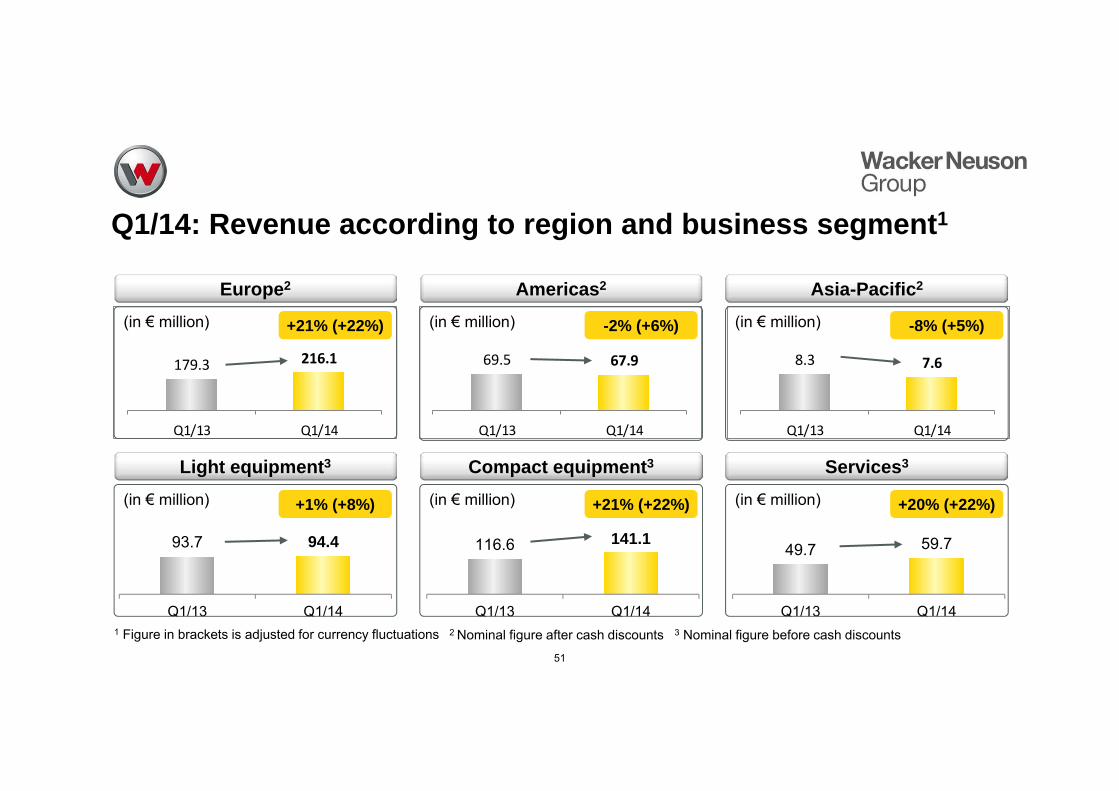

179.3 216.1

Q1/13 Q1/14

69.5 67.9

Q1/13 Q1/14

8.3 7.6

Q1/13 Q1/14

93.7 94.4

Q1/13 Q1/14

116.6 141.1

Q1/13 Q1/14

49.7 59.7

Q1/13 Q1/14

-8% (+5%)

Europe2

(in € million)

Americas2

(in € million)

Asia-Pacific2

(in € million)

Light equipment3 Compact equipment3

(in € million)

Services3

+21% (+22%) -2% (+6%)

(in € million)+1% (+8%) +21% (+22%) +20% (+22%)(in € million)

Q1/14: Revenue according to region and business segment1

51

1 Figure in brackets is adjusted for currency fluctuations 2 Nominal figure after cash discounts 3 Nominal figure before cash discounts

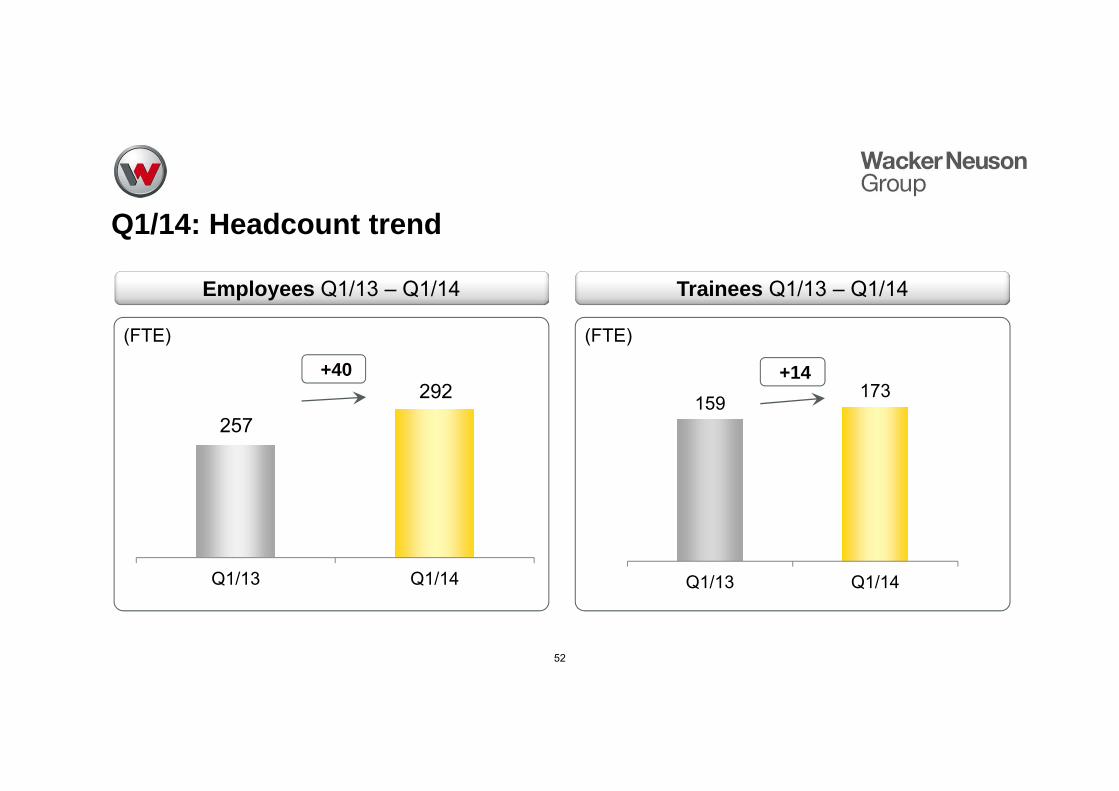

Q1/14: Headcount trend

52

(FTE)

+40

159173

Q1/13 Q1/14

(FTE)

+14

Employees Q1/13 – Q1/14 Trainees Q1/13 – Q1/14

257

292

Q1/13 Q1/14

Contents

53

Fiscal 2013

AGM

Markets - Vision -Strategy

Financial indicators and share news

Q1 2014 Technology and innovation

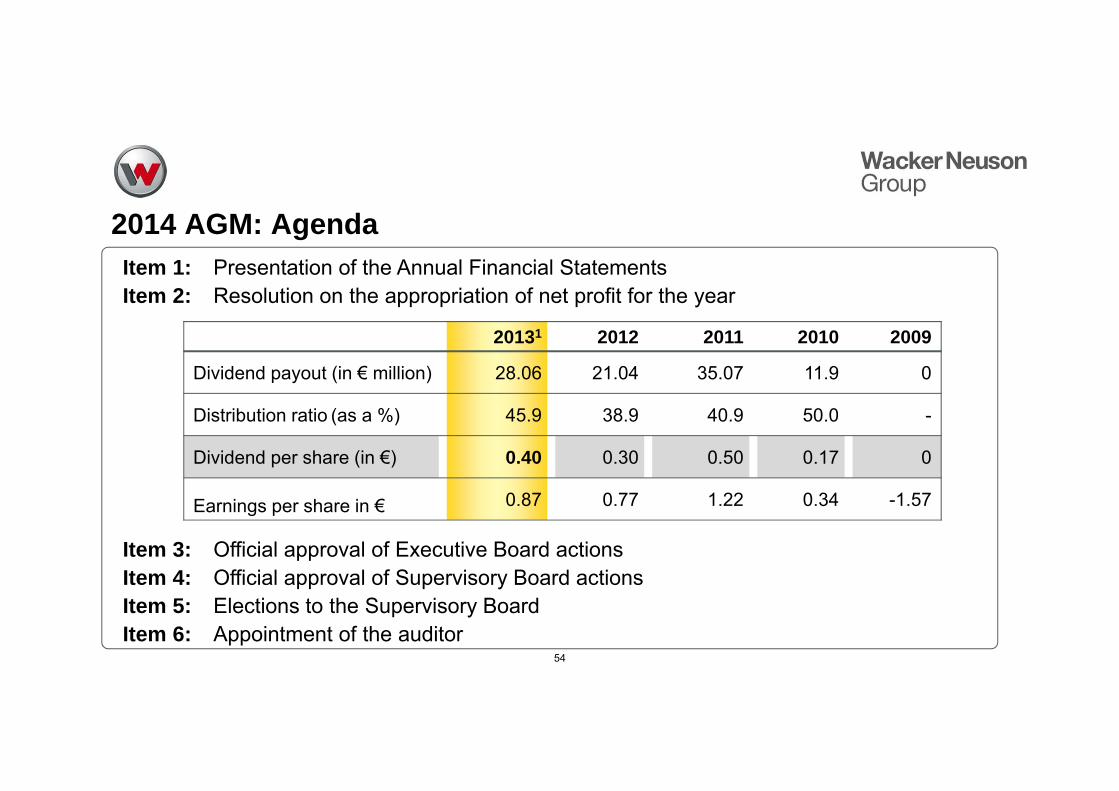

2014 AGM: AgendaItem 1: Presentation of the Annual Financial StatementsItem 2: Resolution on the appropriation of net profit for the year

Item 3: Official approval of Executive Board actionsItem 4: Official approval of Supervisory Board actionsItem 5: Elections to the Supervisory BoardItem 6: Appointment of the auditor

54

20131 2012 2011 2010 2009

Dividend payout (in € million) 28.06 21.04 35.07 11.9 0

Distribution ratio (as a %) 45.9 38.9 40.9 50.0 -

Dividend per share (in €) 0.40 0.30 0.50 0.17 0

Earnings per share in € 0.87 0.77 1.22 0.34 -1.57

AGM2014Wacker Neuson SEMunich, May 27, 2014

Executive Board Report

Cem Peksaglam (CEO)Martin Lehner (CTO)Günther Binder (CFO)

55

![Download [1.16 MB]](https://img.pdfslide.net/doc/110x75/586689df1a28ab20408b6d59/download-116-mb.jpg)