Embed Size (px)

Citation preview

WORKING PAPER 220

Andrej Cupak, Pirmin Fessler, Maria Silgoner, Elisabeth Ulbrich

Exploring differences in financial literacy across countries: the role of individual characteristics and institutions

The Working Paper series of the Oesterreichische Nationalbank is designed to disseminate and to provide a platform for Working Paper series of the Oesterreichische Nationalbank is designed to disseminate and to provide a platform for Working Paper series of the Oesterreichische Nationalbankdiscussion of either work of the staff of the OeNB economists or outside contributors on topics which are of special interest to the OeNB. To ensure the high quality of their content, the contributions are subjected to an international refereeing process. The opinions are strictly those of the authors and do in no way commit the OeNB.

The Working Papers are also available on our website (http://www.oenb.at) and they are indexed in RePEc (http://repec.org/).

Publisher and editor Oesterreichische Nationalbank Otto-Wagner-Platz 3, 1090 Vienna, AustriaPO Box 61, 1011 Vienna, [email protected] (+43-1) 40420-6666Fax (+43-1) 40420-046698

Editorial Board Doris Ritzberger-Grünwald, Ernest Gnan, Martin Summerof the Working Papers

Coordinating editor Coordinating editor Coordinating editor Martin Summer

Design Communications and Publications Division

DVR 0031577

ISSN 2310-5321 (Print)ISSN 2310-533X (Online)

© Oesterreichische Nationalbank, 2018. All rights reserved.

Exploring differences in financial literacy

across countries: the role of individual

characteristics and institutions*

Andrej Cupak�, Pirmin Fessler�, Maria Silgoner�, Elisabeth Ulbrich¶

February 2018

Abstract

We examine recently compiled microdata from the OECD/INFE survey covering in-

formation on the �nancial literacy of adult individuals from twelve countries around the

globe. We �nd large di�erences in �nancial literacy across countries and decompose them

into those explainable by di�erences in individual characteristics and those that cannot be

explained by such di�erences. We show that individual characteristics matter with regard

to di�erences in average �nancial literacy, but do not fully explain the observed di�er-

ences. We further relate the unexplained di�erences in our microeconometric analysis to

institutional di�erences across countries. We �nd strong relationships between the di�er-

ences in �nancial literacy not explained by individual characteristics and life expectancy,

social contribution rate, PISA math scores, internet usage, and to a lesser degree by GDP

per capita, the gross enrolment ratio and stock market capitalization. Our results suggest

that there is room for harmonization of economic environments across countries regarding

decreasing inequality in the population's �nancial literacy.

JEL Classi�cations: D14, D91, I20

Key Words: �nancial literacy gaps, inequality, decomposition analysis, counterfactual meth-

ods, personal �nance, survey data

*We are grateful to the OECD/INFE working group for granting access to the individual-level data. Wewould like to thank Alyssa Schneebaum and an anonymous referee for helpful comments and suggestions.We are also grateful to audiences at the following seminars and conferences: Oesterreichische Nationalbankresearch seminar (Vienna, 2017); National Bank of Slovakia research seminar (Bratislava, 2017); HFCS networkmeeting at the ECB (Frankfurt, 2017); Joint ECB and Banque de France conference on household �nance andconsumption (Paris, 2017); and Slovak Economic Association annual conference (Kosice, 2017). The viewsexpressed in the paper do not necessarily re�ect the views of the Oesterreichische Nationalbank, the NationalBank of Slovakia, the Eurosystem, or the LIS: Cross-National Data Center in Luxembourg. Andrej Cupak wasa visiting researcher at the Oesterreichische Nationalbank when he started this research project.

�Research Department, National Bank of Slovakia; and LIS: Cross-National Data Center in Luxembourg,[email protected].

�Economic Analysis and Research Department, Oesterreichische Nationalbank, [email protected].�Foreign Research Division, Oesterreichische Nationalbank, [email protected].¶Financial Education Unit, Oesterreichische Nationalbank, [email protected].

Non-technical summary

Modern life is full of �nancial choices. These vary from basic day-to-day decisions such as

organizing budgets to more complex ones such as taking a loan, participating in private pension

savings schemes, or investing in sophisticated �nancial instruments. Recent literature has

shown that along with standard socio-economic characteristics that vary across individuals,

�nancial literacy is a relevant ingredient for making sound �nancial decisions. Being �nancially

literate is not only important for the wellbeing of consumers themselves, but also for the

�nancial system as a whole. Consumers' informed and sound �nancial choices are important

for �nancial stability. If better �nancial literacy also leads to more sound �nancial behavior,

we can expect fewer �nancial problems and ultimately fewer shortfalls in �nancial payments.

Generally, the risk-bearing capacity of households and the �nancial system as a whole would

increase with greater �nancial literacy.

Average �nancial literacy di�ers markedly across countries. What was missing in the literature

until now, though, has been an understanding of why there are these observed di�erences. Is

�nancial literacy higher in one country because its population has certain characteristics (such

as higher education), or is there something else at play? In this study, we estimate which

di�erences in the gap are explainable by individual characteristics (age, education, household

size, working status, and others) and which remain attributable to factors we cannot observe.

Learning what is behind the gap in �nancial literacy across countries is important because

the �ndings might suggest di�erent policy conclusions. Imagine a gap in observed �nancial

literacy between two countries. On the one hand, this gap may exist even within education

groups; this would be the case if �nancial literacy di�ered among the highly educated across

the two countries. On the other hand, the gap could exist across countries even if the �nancial

literacy within education groups across countries were the same; this could be the case if

the share of highly educated individuals is higher in one country. From a policy perspective,

these two cases need to be dealt with di�erently. Whereas the �rst raises the question of why

similarly educated groups have di�erent �nancial literacy across countries, the second case can

be addressed by increasing educational attainment.

Our results show that di�erences in individual characteristics matter considerably. We also

show that di�erent socioeconomic environments across countries might play a role in explaining

varying levels of �nancial literacy. We conclude that individual characteristics should be taken

into account when comparing �nancial literacy across countries, speci�cally when the countries

are ranked based on their populations' level of �nancial literacy, as in the OECD/INFE (e.g.

OECD, 2016) report. It is rather important to have an �apples to apples� comparison to design

policies in an informed way.

1 Introduction

The importance of �nancial literacy as a main ingredient of informed choices and sound �nan-

cial behavior of consumers has recently been recognized in the literature (see e.g. Campbell,

2006; Jappelli, 2010; Hastings et al., 2013; Fernandes et al., 2014; Lusardi and Mitchell, 2014).

Moreover, the literature shows that poor outcomes in household �nance and questionable in-

vestment decisions mostly occur for households with low levels of income and �nancial literacy

(Campbell, 2006; Badarinza et al., 2016).

We observe large di�erences in average �nancial literacy across countries (Lusardi and

Mitchell, 2014; Standard and Poor's, 2014). The policy implications of this �nding are, how-

ever, unclear since this depends on the homogeneity of the populations. It remains unknown

how much of the observed di�erence is country-speci�c and how much is driven by di�erences

in the individual characteristics of the (sampled) population. We deliver estimates of how

much of this di�erence is due to di�erences in the characteristics of the population.

We seek to answer the following research questions in this paper: How large are �nancial

literacy gaps across countries? Are the observed di�erences in �nancial literacy mainly due

to di�erences in observable individual characteristics? Do institutional factors play a role in

explaining �nancial literacy gaps across countries?

These fundamental questions are relevant for potential policies aimed at increasing �nan-

cial awareness. To illustrate why it is important to not only use unconditional comparisons

such as those presented in the existing literature on di�erences in �nancial literacy across

countries (e.g. OECD, 2016), we point to an example with regard to educational attainment.

On the one hand, a gap in average �nancial literacy may exist across countries within edu-

cation groups; this would be the case if �nancial literacy di�ered among the highly educated

in country A versus country B. On the other hand, a gap could exist across countries even if

the �nancial literacy within education groups is the same across countries if the share of, say,

highly educated individuals is higher in country A than in country B. From a policy perspec-

tive these gaps need to be dealt with di�erently. Whereas the �rst raises the question of why

similarly educated groups have di�erent �nancial literacy across countries, the second case can

be addressed by increasing educational attainment.

Furthermore, we investigate whether the links between individual characteristics and �-

nancial literacy di�er for individuals with low (basic) and high (advanced) levels of �nancial

literacy. Whereas educational attainment might be key to basic �nancial literacy, its relevance

might be less in the case of more advanced �nancial literacy.

1

Finally, we ask which di�erences in institutions are correlated with cross-country di�er-

ences in �nancial literacy that cannot be explained by individual characteristics. Character-

istics might explain part of the gap, but their interplay with di�erent environments across

countries is potentially relevant when explaining �nancial literacy gaps. One potentially rele-

vant institutional di�erence related to �nancial literacy may be di�erent welfare state regimes.

In some countries (such as Brazil, Russia, or the UK), investing privately for old age provision

or other precautionary motives is more important than in others (such as Austria, Finland,

or Germany). Moreover, the supply of �nancial services is di�erent in di�erent countries. In

some countries, the intermediation of banks is stronger (such as in continental Europe) than

in others (such as the UK).

In the previous literature, researchers have analyzed di�erences in �nancial literacy across

countries and groups of individuals primarily in a descriptive way. For example, according to

the Standard and Poor's (2014) survey, the average percentage of adults that answered three

out of four �nancial literacy questions correctly is 56% in the old EU member states; 63% in

Australia, the USA, and Canada; and 45% in the Central and Eastern European (CEE) new

EU member states. Likewise, results of the OECD PISA survey show worse results for high-

school students from CEE countries compared to other Western European countries (OECD,

2013). Recently, the OECD (2016) showed substantial di�erences in the �nancial literacy of

the adult population across the world as well as across European countries. Other examples of

descriptive studies on cross-country �nancial literacy gaps include Atkinson and Messy (2011)

and Lusardi and Mitchell (2011). An exception is a study by Jappelli (2010), who analyzes

the relationship between macroeconomic variables and economic literacy using international

panel data on 44 countries over the period 1998-2008. Despite the identi�cation of important

factors driving di�erences in economic literacy across countries, the main shortcoming of Jap-

pelli (2010)'s study is that the level of economic literacy of the particular country is proxied

by the economic literacy of business leaders, hence o�ering a potentially biased picture.

Thus, until now, the di�erences in the observed distribution of �nancial literacy across

households and individuals have not been studied in a cross-country framework using compa-

rable individual-level survey data. We deliver such an analysis by answering the question of

what (possibly) determines the observed di�erences in �nancial literacy of individuals between

countries by employing microeconometric tools from the policy-evaluation and decomposition

literature.

Our study makes several contributions to the empirical literature on �nancial literacy and

household �nances. To our knowledge, we are the �rst to do a detailed analysis of the newest

2

wave of the OECD/INFE database on �nancial competencies of individuals. These data were

made available for research in the summer of 2017. The advantage of this database is its broad

set of questions, focusing on an extended set of �nancial knowledge questions as well as aspects

of �nancial attitudes and behavior. We are also the �rst to employ counterfactual decompo-

sition techniques to analyze the observed di�erences in �nancial literacy in a cross-country

perspective. In our framework, we consider individuals from Finland as a benchmark (refer-

ence) for �nancial literacy of individuals from other countries available in our dataset (namely

Austria, Brazil, Canada, Croatia, Hong Kong, Hungary, Germany, Jordan, The Netherlands,

Russia, and the UK).1 Our �ndings help to better understand the potential determinants of

gaps in �nancial literacy between countries, which are sometimes substantial � nearly 20%

in some cases (e.g. Finland vs. Croatia or Russia). We devise a two-step empirical strategy

to �rst decompose the di�erences into those due purely to di�erent individual characteristics

across countries and the remainder. Then, we use these remaining parts to analyze the poten-

tial linkage to institutions and a country's macroeconomic environment. Our methodological

framework builds on the existing literature of Christelis et al. (2013) and Bover et al. (2016).

The rest of this paper is structured as follows. Section 2 introduces the data. Section 3

includes the empirical strategy. Section 4 presents empirical results. Section 5 concludes.

2 Data

The data used for the analysis of �nancial literacy gaps across countries come from the

OECD/INFE (International Network for Financial Education) survey of adult �nancial lit-

eracy competencies. While the survey was conducted in more than 30 countries around the

world, only a few countries made the data available for research purposes. Hence, we have man-

aged to access individual-level data from Austria, Brazil, Canada, Croatia, Finland, Germany,

Hong Kong, Hungary, Jordan, The Netherlands, Russia, and the UK accounting together for

more than 15,000 observations. A unique feature of this survey is that the questions are asked

in a harmonized way across countries, making the results comparable, a major advantage as

compared to previous surveys on �nancial literacy. Also, the set of �nancial literacy questions

is much broader than in previous studies. In the earlier surveys, usually three/four basic �-

nancial literacy questions on interest rates, in�ation and diversi�cation/riskiness were asked

(Lusardi and Mitchell, 2014). In the OECD/INFE survey, questions include concepts such as

time value of money, interest paid on loans, interest and principal, compound interest, risk

1The choice of Finland as a reference category is reasonable not only for the data availability, but also forother reasons. For example, the Finnish population (both adults and high-school students) rank among thebest in di�erent �nancial literacy surveys (e.g. OECD, 2013, 2016) compared to the population from otherEuropean countries. Furthermore, Finnish households show an intense interaction with �nancial markets, asnearly 39% of households hold risky �nancial assets in their portfolios (Bover et al., 2016).

3

and return, in�ation, and risk diversi�cation. The data also contains standard socio-economic

characteristics.

Table 1 shows basic information with regard to the data collection in the countries were data

is already accessible. In 8 of the 12 countries face-to-face personal computer assisted interviews

were conducted. In one of them (Russia) some interviews were also conducted via telephone.

Two other countries used purely telephone interviews (Canada and Germany) whereas two

gathered the data via online interviews (The Netherlands and the United Kingdom). The

sample size ranges from 1,000 (Hong Kong and the United Kingdom) to 2,002 (Brazil). In many

countries the national central banks were responsible for gathering the data and delivering it

to the OECD/INFE. In others also universities, ministries or other governmental institutions

also conducted the harmonized survey developed by the OECD/INFE.

[Enter Table 1 here]

For our analysis we use a set of variables which is fully harmonized in all countries shown

in Table 2. It consists of our main variable of interest, the �nancial literacy score, which is

itself calculated from the answers given to a set of seven questions examining the �nancial

literacy of respondents. They deal with the understanding of in�ation, interest, interest plus

principal, compound interest, the relationship between risk and return and diversi�cation.

The detailed questions are listed in Appendix A. The �nancial literacy score of individuals

is computed similarly to the extant literature on �nancial literacy (e.g. Lusardi and Mitchell,

2014). Hence, the �nancial literacy score (as also used by the OECD/INFE) is computed as

a sum of all (seven) correctly answered questions asked in the survey.

In our empirical analysis, we �rst use a set of exogenous socio-economic individual char-

acteristics as predictors for the stock of �nancial literacy. In Appendix B, we also include a

set of endogenous variables capturing the experience of respondents with �nancial products

and �nancial planning. As individual characteristics we use age category dummies, a gender

dummy, a dummy for marital status, a dummy for university education and dummy variables

for di�erences in employment status. Furthermore we use a variable on the income bu�er

indicating that the individual has a �nancial bu�er of at least three times the monthly net

income, which therefore is also a crude measure of �nancial wealth. To cover experience in

Appendix B we use dummies on having a budget plan, being an active saver, holding risky

assets and engaging in long-term �nancial planning.

[Enter Table 2 here]

4

Figure 1 shows the distributions of the �nancial literacy score across all countries covered

in our analysis. In most countries the majority of individuals are able to answer 5 or more

questions correctly, in some countries the distribution is more skewed than in others.

[Enter Figure 1 here]

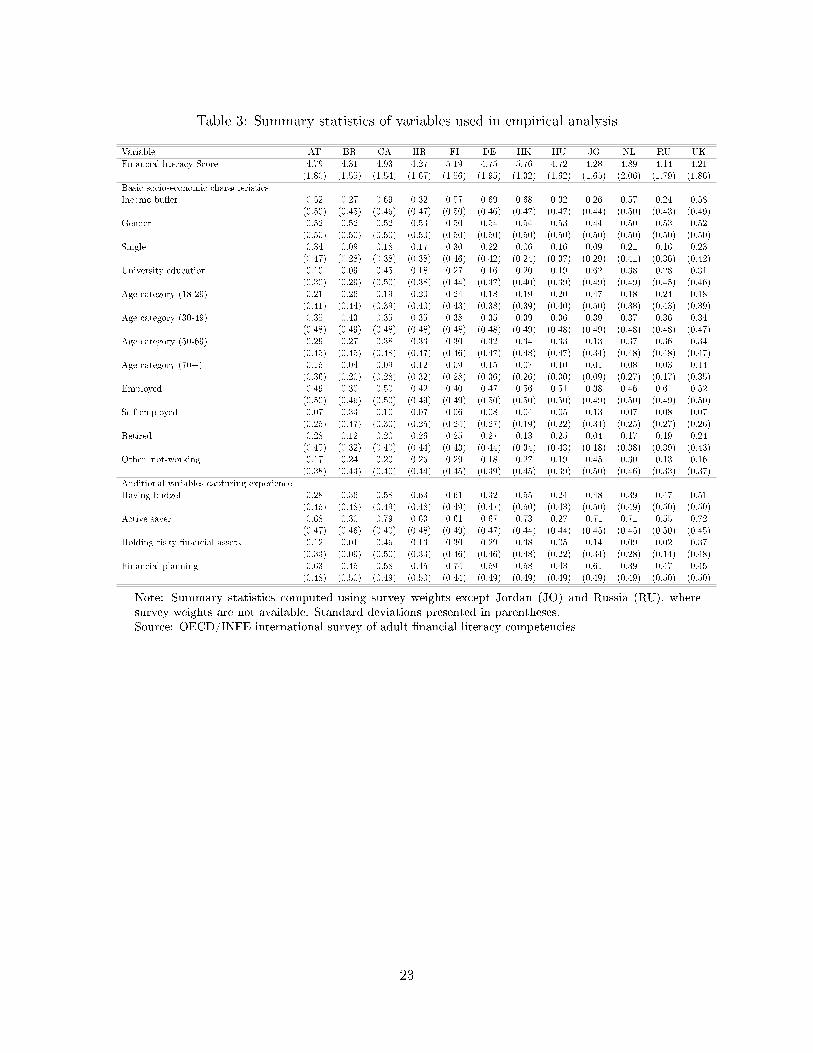

Table 3 shows descriptive statistics (means and standard deviations) for all countries and

all variables used in our empirical analysis. Note, that while the mean �nancial literacy score

varies substantially across countries, it still lies above 4.1 and below 5.2 (out of 7) correctly

answered questions in all countries. Also individual characteristics X vary substantially. In

some countries (Brazil) less than 10% of the population have university degrees while in others

(Canada, Jordan, The Netherlands and the UK) the share is above 30%. Also the proxy for

�nancial wealth, i.e. the income bu�er variable identifying individuals with at least 3 month

of their monthly income in �nancial assets, varies substantially. While in Russia only 24%

report having such a �nancial bu�er, 69% of Canadians do so. Also shares of singles and

employment status show remarkable di�erences. Regarding the individual characteristics we

use to capture experience in Appendix B, we �nd that the shares of individuals holding risky

assets is rather di�erent across countries. But also the softer measures of having a budget,

being an active saver as well as �nancial planning reveal substantial di�erences which might

potentially explain di�erences in �nancial literacy scores.

[Enter Table 3 here]

3 Empirical strategy

To study di�erences in �nancial literacy we employ di�erent empirical tools. In this section we

lay out our empirical approach. First, we present means of �nancial literacy across di�erent

socioeconomic groups across countries in subsection 3.1. Second, we estimate a conditional ex-

pectation function of �nancial literacy, controlling for country level �xed e�ects in subsection

3.2. Third, we decompose observed di�erences in �nancial literacy across countries and types

of individuals by employing standard counterfactual decomposition techniques (Blinder, 1973;

Oaxaca, 1973) in subsection 3.3. This step also includes use of the framework of unconditional

quantile regressions (Firpo et al., 2007, 2009) to extend our approach beyond the mean in

subsection 3.4. Finally, we correlate the unexplained parts of the gaps in �nancial literacy

with selected aggregate macroeconomic indicators which have been shown to in�uence �nan-

cial literacy at the country-level in subsection 3.5. The last step of our empirical framework

builds on the previous studies of Jappelli (2010), Christelis et al. (2013), and Bover et al.

5

(2016).

3.1 Average �nancial literacy across socioeconomic characteristics and coun-

tries

Formally, we observe a cross section of draws from country distribution functions F c of coun-

tries c ∈ C, of the matrix (L,X), where L denotes �nancial literacy and X a vector of individ-

ual characteristics such as education and age or indicators denoting experiences with �nancial

products. Let us think of �nancial literacy as an outcome variable and individual character-

istics as covariates. We calculate simple (conditional) means across di�erent subgroups and

countries. These descriptive results are discussed in subsection 4.1.

3.2 Estimation of the conditional expectation function

As a preliminary step to our empirical framework, we estimate the population conditional

expectation function (CEF) E(L∣X). If the CEF is linear, than the population regression

function is the population CEF. But even if it is not linear, the population regression function

is the best linear predictor of the population CEF in a minimum mean squared error sense.

Therefore we use a weighted linear regression to estimate the population CEF:

L = α + β′X + γI + ε, (1)

where α denotes a constant, X contains the predictors, β the slope parameters, I includes

country �xed e�ects with parameter vector γ and ε is the error term. The estimates for the

predictive e�ects β of di�erent socioeconomic characteristics on �nancial literacy are discussed

in subsection 4.2.

3.3 Decomposition analysis

As we are interested in explaining the di�erences in observed �nancial literacy across coun-

tries, we decompose them by means of the Blinder-Oaxaca (B-O) framework (Blinder, 1973;

Oaxaca, 1973). The B-O decomposition technique has been predominantly used in the labor

economics literature to study gaps in wages and employment. Recently, this method has also

been applied in the �eld of household �nance to study di�erences in stock-holdings between US

and euro-area households (Christelis et al., 2013), wealth di�erences across euro-area countries

(Mathä et al., 2017), or to study �nancial literacy gaps between male and female populations

in the US (Fonseca et al., 2012).

6

In our case, the B-O decomposition de�nes the mean di�erence in �nancial literacy scores

of individuals from the particular country studied and individuals from the reference group,

Finland. The mean di�erence is divided into two main parts � one explained by group di�er-

ences in observable individual characteristics under consideration, and another that cannot be

accounted for by di�erences in observed individual characteristics � i.e. di�erences in coe�-

cients, or how literacy is �produced� in the particular country.

Formally, we want to answer the question of how much of the mean di�erence in �nancial

literacy is accounted for by di�erences in characteristics of individuals between a benchmark

country c = j (Finland) and countries c ∈ C. The mean di�erence can be written as

△ µLc = E(Lc=j) −E(Lc). (2)

We can rewrite this di�erence based on regression parameters and decompose it into a part

explained by di�erences in characteristics X and an unexplained part,

△ µLc = [E(Xc=j) −E(Xc)]′ βc=j + [E(Xc)

′(βc=j − βc)] , (3)

where βc=j and βc are coe�cient vectors from regressions including only individuals of the

reference country c = j and country c, respectively. The �rst part [E(Xc=j) −E(Xc)]′ βc=j is

then the part of the di�erence that is due to di�erences in the individual characteristics X.

ˆ△µLc can then be estimated as,

ˆ△µLc = (X̄c=j − X̄c)′β̂c=j

´¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¸¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¶

explained

+ X̄ ′c(β̂c=j − β̂c)´¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¸¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¹¶

unexplained

, (4)

where X̄c=j and X̄c are covariate group means of the reference country c = j and country

c, respectively. Finally, we denote the estimate of the unexplained part for each country c,

E(Xc)′(βc=j − βc), which we use in a further step of our analysis by

χc = X̄′

c(β̂c=j − β̂c). (5)

We discuss the results of our decomposition in subsection 4.3.

3.4 Decomposition beyond the mean

The reasons for di�erences in average �nancial literacy might be di�erent for those in the lower

or higher parts of the distribution. Whereas in the lower part it is mostly about very basic

math (cognitive) skills (e.g. interest calculation), it is rather knowledge about the functioning

of certain sophisticated �nancial products at the top of the distribution. Basic schooling might

7

be important in the lower, but not important at all in the upper part. Therefore, to examine

whether the result of our decomposition holds also beyond the mean, we employ recently de-

veloped tools from the microeconometric decomposition literature.

We decompose distributions in the �nancial literacy scores between individuals from the

benchmark country c = j and country c by using recentered in�uence function (RIF) regres-

sions along with the B-O technique (Firpo et al., 2007, 2009).2 To do so we basically replace

the country level regressions underlying our approach with RIF-regressions. An RIF-regression

is similar to a standard regression, except that the dependent variable is replaced by the re-

centered in�uence function of the statistic of interest (see Firpo et al., 2009).

For the readers' convenience we summarize the basic approach. For our case of quantiles

of �nancial literacy scores L, the IF (L,Qτ) is given as (τ − 1{L ≤ Qτ}/fL(Qτ), where 1{⋅}

is an indicator function, fL(⋅) is the density of the marginal distribution of L, and Qτ is the

population τ -quantile of the unconditional distribution of L. The RIF (L;Qτ) is then equal

to Qτ + IF (L,Qτ), and can be written as

RIF (l;Qτ) = Qτ +τ − 1{l ≤ Qτ}

fL(Qτ)= c1,τ ⋅ 1{l > Qτ} + c2,τ , (6)

where c1,τ = 1/fL(Qτ) and c2,τ = Qτ − c1,τ ⋅ (1 − τ). As E[1{l > Qτ}] = Pr(L > Qτ) = 1 − τ , it

follows that E[RIF (l;Qτ)] = c1,τPr(L > Qτ)+ c2,τ = Qτ . By the law of iterated expectations,

we have

E[RIF (l;Qτ)] = EX{E[RIF (l;Qτ)]∣X}, (7)

which justi�es running a linear regression of the binary outcome variable 1{l > Qτ} on X (see

Fortin et al. (2011) and Firpo et al. (2009) for details). We run RIF-regressions for the 10th

(τ = 0.1) and 90th (τ = 0.9) percentiles Qτ as well as the median (τ = 0.5). This decomposition

at di�erent points of the distribution of �nancial literacy score allows us to investigate whether

individual characteristics and institutions matter in di�erent ways across the �nancial literacy

distribution. See subsections 4.3 and 4.4 for a discussion of results.

3.5 Coe�cient e�ects and institutions

In this stage of our framework, we correlate the unexplained parts of the gaps, estimated

from the B-O analysis χc, with selected macroeconomic indicators that have been shown to be

relevant for the �nancial literacy at the country-level (Jappelli, 2010). Our chosen aggregate

2An alternative way to perform a quantile decomposition analysis, which has been applied in severalempirical papers, is the approach suggested by Machado and Mata (2005).

8

indicators include GDP per capita, share of internet users, life expectancy, (gross) enrolment

ratio to secondary school, stock market capitalization, PISA match test score, and social

contributions rate (a proxy for welfare state). For a detailed description, see Table 4. Formally,

we can write this country-level relationship as a regression of our estimated unexplained parts

on macroeconomic indicators,

χ = α + φz + ε, ∀z ∈ Z, (8)

where α is a constant, z refers to one country level macroeconomic indicator of indicators Z,

and φ is the according slope parameter. φ̂ is then our estimate of the relationship between

unexplained parts χ and macroeconomic variable z ∈ Z. See subsection 4.4 for results and

discussion of this step.

[Enter Table 4 here]

4 Results

In this section we �rst discuss average �nancial literacy across countries and socioeconomic

characteristics in subsection 4.1. We then present our estimates of the conditional expecta-

tion function of �nancial literacy, controlling for country level �xed e�ects in subsection 4.2.

Subsection 4.3 includes the core of our analysis, the decomposition of cross-country di�erences

in �nancial literacy into parts explainable by individual characteristics and an unexplained

part. We also decompose beyond the mean at the 10th and 90th percentile of the �nancial

literacy distribution and the median. We employ the unexplained parts to correlate them with

macroeconomic and institutional variables to shed further light on potential drivers of di�er-

ences in �nancial literacy in subsection 4.4. In Appendix B we deliver a robustness check, in

which we add the potentially endogenous variables capturing experience presented in section

2 to the analyses.

4.1 Socioeconomic characteristics

Table 5 shows average �nancial literacy by socioeconomic characteristics and countries. In all

countries men � on average � obtained higher �nancial literacy scores than women. Higher

education goes along with higher �nancial literacy scores in all countries as well. Financial

literacy seems to increase initially with age and to decrease again for the elderly. However,

this pattern does not prevail in all countries (Brazil and Jordan). Regarding employment, in

many countries (8 out of 12) the self-employed have marginally higher �nancial literacy than

the employed.

9

[Enter table 5 here]

4.2 Determinants of �nancial literacy

Table 6 shows di�erent estimates of the conditional expectation function (CEF) of �nancial

literacy. It can be interpreted as a predictive production function of �nancial literacy. We

estimate two speci�cations with basic socio-economic characteristics (see Table 3) as explana-

tory variables: (1) without country �xed e�ects, (2) with country �xed e�ects. Note, that

due to missing values in some of the explanatory variables our sample reduces from 15,388

observations to 12,298.

The results with regard to the predictive e�ects of individual characteristics are robust to

adding country �xed e�ects. The income bu�er dummy, which is a raw measure of �nancial

wealth is positively related to �nancial literacy and translates to about 0.3 to 0.6 (depending

on speci�cation) correct answers (out of the 7) more for households with a �nancial bu�er of

3 monthly incomes or more. The gender gap usually found in work on �nancial literacy is

clearly visible. Women score on average about 0.4 points less. Singles also tend to have slightly

lower scores. However, the coe�cients are not always statistically and more importantly never

economically signi�cant. Individuals with university degrees score about 0.4 to 0.7 questions

better. The hump shaped age pattern we found in the descriptive tables is con�rmed in the

estimation of the CEF. The lowest age category scores lower than the oldest, but the age

category between 50-69 scores even higher. Whereas the employed score signi�cantly higher

than people not working this is less clear for the self-employed and the retired. However, the

coe�cients of employed and self-employed are not signi�cantly di�erent from each other.

[Enter Table 6 here]

4.3 Decomposition analysis

Results from the Blinder-Oaxaca (B-O) decomposition analysis are shown in Table 7.3 As

outlined in section 3, we use Finland as a reference country. The largest gaps (larger than

3Note that the means of �nancial literacy are slightly di�erent from the unconditional means due to themissing information on individual characteristics and experience. However, given the fact that the total samplesize is still 12,298 observations in the case of individual characteristics and 10,810 observations in the case ofindividual characteristics and experience (see Appendix B), the missing pattern is not highly correlated withour covariate set and our covariate set contains exclusively dummy variables, which means that we do not have alarge amount of linear extrapolation but rather look at a set of conditional group speci�c means of combinationsof dummies, and we are con�dent using the standard listwise deletion approach. Our RIF-regression basedapproach for the median serves as a robustness check as the median is a robust statistic in the sense that ithas a bounded in�uence function, which means that it is less exposed to missing observations.

10

15%) are observed in Croatia, Russia, Jordan and Brazil. But also the UK and Hungary show

relatively large gaps compared to Finland (larger than 10%). Austria and Canada still show

gaps above 5%, whereas Germany and the Netherlands hardly show relevant deviations. Hong

Kong exceeds average �nancial literacy in Finland.

In some countries di�erences in observable individual characteristics with Finland signif-

icantly dampen the gap (Canada, Jordan, The Netherlands and the UK), while for other

countries the gap is signi�cantly larger because of di�erences in individual characteristics

(Austria, Brazil, Croatia, Hungary and Russia). In the case of these countries between about

11% (Russia) and 60% (Austria) is explained by di�erences in individual characteristics. That

means that if di�erences due to di�erences in the share of characteristics in the population

are �ltered out and only within characteristic di�erences are considered, the gap reduces by

this amount. In the same way the gap widens for countries where characteristics dampen

the unconditional observed di�erences. In Germany the gap is not signi�cantly di�erent from

Finland, whereas in Hong Kong individual characteristics do not signi�cantly explain part of

the higher score in Hong Kong.

All in all, it is rather obvious that individual characteristics matter when comparing �nan-

cial literacy across countries. It is rather important to have �apples to apples� comparison to

design policies in an informed way. In the case of di�erences in educational attainment this is

rather obvious. On the one hand, a gap in average �nancial literacy may exist across countries

within education groups; this would be the case if �nancial literacy di�ered among the highly

educated in country A versus country B. On the other hand, a gap could also exist across

countries even if the �nancial literacy within education groups is the same across countries.

This could be the case if the share of, say, highly educated individuals is higher in country

A than in country B. From a policy perspective these gaps need to be dealt with di�erently.

Whereas the �rst raises the question of why similarly educated groups have di�erent �nancial

literacy, given the second �nancial literacy might just be increased by increasing educational

attainment.

[Enter Table 7 here]

Given the di�erent distributions of the �nancial literacy score across countries (Figure 1),

we decompose these distributions by means of RIF-regressions as outlined in subsection 3.5.

Results of the RIF-regression based B-O quantile decomposition analysis (for the 10th, 50th,

and 90th percentile) are presented in Table 8. The RIF-regression based approach for the

median serves also as a robustness check for the standard B-0 decomposition at the mean, as

11

the median is a robust statistic in the sense that it has a bounded in�uence function, which

means that it is less exposed to missing observations.

[Enter Table 8 here]

The B-O decomposition analysis at the median of �nancial literacy (Table 8) con�rms

the results of the decomposition at the mean (Table 7). However, results di�er substantially

for the upper (90th percentile) and lower (10th percentile) part of the distributions of the

�nancial literacy score, pointing towards di�erent mechanisms in place at di�erent points of

the distribution. Gaps in percentage are larger and individual characteristics can explain fewer

of these observed gaps at the bottom (p10) than at the top (p90). Especially interesting is

the fact that the additional explanatory power of experience tends to explain relatively more

of the gap at higher levels of �nancial literacy and especially for countries which lag behind

literacy levels of Finland (see tables B.2 and B.3).

4.4 Unexplained gaps of �nancial literacy and the role of institutions

In this section we examine the role of institutions in explaining the unexplained parts (neither

by individual characteristics nor by experience) of the gaps in �nancial literacy score across

the countries compared. Following Christelis et al. (2013), we correlate the unexplained parts

(coe�cient e�ects) obtained from the mean and quantile B-O decomposition analysis with the

selected macroeconomic variables in�uencing populations' �nancial literacy. We consider a set

of aggregate indicators which have been shown as important determinants of �nancial literacy

at country-level. Following Jappelli (2010), we consider GDP per capita, share of internet

users, (gross) enrolment ratio to secondary school, life expectancy, PISA math test scores,

stock market capitalization, and social contributions rate.

Similarly to Christelis et al. (2013), we argue that the unexplained component of the gap

in �nancial literacy might be attributed to di�erent economic environments of countries. As

an example, one could think of the education system's quality in the particular country which

can have important implications for the population's �nancial literacy, which we proxy by an

indicator on the PISA math test. According to Ciaian and Pokriv£ák (2005), crucial sectors

for economic development and human capital accumulation including the development of ed-

ucation systems in many transition countries have been lagging behind compared to Western

European countries during the transition from a centrally-planned to a market economy. The

unexplained part could also be interpreted as impacts of historic (behavioral) experiences of

the market economy which in turn could in�uence the �nancial literacy of individuals � prox-

ied by an indicator on the stock market capitalization (e.g. Jappelli, 2010).

12

Having a glance at Figure 2 one can infer the main �nding from the distributional analy-

sis (see subsection 4.3) and its relation to institutional di�erences. Overall, the unexplained

part of the gaps estimated from the B-O analysis at the mean decreases with countries being

institutionally closer to our benchmark category, Finland. This �nding holds for the whole

distribution of the �nancial literacy score, the 10th, 50th, and 90th percentile (see �gures B.1

and B.2 in Appendix B). For a detailed discussion on how experience might matter di�erently

across the distribution of �nancial literacy see Appendix B.

[Enter Figure 2 here]

As the last step of our empirical analysis, we examine which institutions matter the most

for explaining the coe�cient e�ects (the unexplained part of the gaps) estimated from the

B-O analysis. To do so, we regress the unexplained part of the gaps estimated from the mean

and quantile decomposition analysis, on a set of macroeconomic indicators whose values have

been standardized (i.e. de-meaned and divided by their standard deviations).

A ranking of the importance of di�erent institutions with regards to explaining the coef-

�cient e�ects is presented in Table 9. Overall, we can see that all the macroeconomic and

institutional variables under consideration are negatively correlated with unexplained di�er-

ences in �nancial literacy. The higher the GDP per capita, enrolment to secondary school

ratio, share of internet users, life expectancy, social contributions, PISA math results, and

stock market capitalization, the lower the unexplained di�erences with Finland. As Finland

also ranks among the highest in all these country level indicators, one can also interpret this

result as unexplained di�erences in �nancial literacy being lower if institutional di�erences are

smaller (results including experience presented in Appendix B , Table B.4).

[Enter Table 9 here]

Life expectancy shows the largest correlation with the unexplained part of the �nancial

literacy gaps. Life expectancy, as well as GDP per capita, can be considered as indicators

for the general level of development. Also the share of internet users is predictive for the size

of the unexplained gaps. The PISA math test score � an indicator which proxies the quality

of education system in the particular country � also turns out to be highly important for

explaining �nancial literacy gaps.

All in all, these results point to the importance of the environment when discussing cross-

country di�erences in �nancial literacy. Environment not only matters in a direct way, by

13

in�uencing �nancial literacy or creating more need � in the case of a smaller welfare state �

for �nancial literacy, but also indirectly, by allowing individual characteristics to translate in

di�erent ways to �nancial literacy. As an example one can imagine that an individual with

higher educational attainment might be able to acquire �nancial literacy at lower cost with

internet access rather than without. Or as another example, the need to engage in �nancial

markets might be higher in a country where the need for private pension savings is higher.

14

5 Conclusion

The literature observes large di�erences in average �nancial literacy across countries (Lusardi

and Mitchell, 2014; Standard and Poor's, 2014). While these observed di�erences arguably

in�uence policies, the populations in the di�erent countries are not homogenous. So far, it

had been unknown to what extent the observed di�erences are country-speci�c or driven by

di�erences in the individual characteristics of the (sampled) population. To design the right

policies, it is of the utmost importance to understand the reasons for observed di�erences of

cross-country �nancial literacy gaps.

By examining recently compiled harmonized OECD/INFE microdata on the �nancial lit-

eracy of individuals in 12 countries along with country level indicators, we delivered estimates

of how much of these observed di�erences are due to di�erences in the characteristics of the

population.

Results indicate that di�erences in individual characteristics matter considerably. In some

countries, di�erences in observable individual characteristics dampen much of the gap com-

pared to Finland (in particular, Canada, Jordan, The Netherlands, and the UK). For other

countries, the gap is signi�cantly larger because of di�erences in individual characteristics (in

this case, Finland versus Austria, Brazil, Croatia, Hungary, and Russia). In the latter set of

countries, between about 11% (Russia) and 60% (Austria) of the gap is explained by di�er-

ences in individual characteristics. That means that if di�erences in �nancial literacy due to

di�erences in the population's characteristics were �ltered out and only within-characteristic

di�erences were considered, the gap would be reduced by this amount. We conclude that

individual characteristics should be taken into account when countries are compared and

speci�cally when they are ranked as in the OECD/INFE report. It is rather important to

have an �apples to apples� comparison to design policies in an informed way.

A variety of robustness checks including extensions of the set of controls by potentially

endogenous variables covering experience as well as analyses beyond the mean for di�erent

points of the distribution of �nancial literacy con�rmed our results.

In the second stage of the analysis, we correlated the unexplained parts of the �nancial

literacy gaps (not explained by varying individual characteristics) obtained from decomposi-

tion analysis with macroeconomic and institutional country-level indicators. Following Jap-

pelli (2010), we considered a set of indicators such as GDP per capita, share of internet users,

(gross) enrolment ratio to secondary school, life expectancy, stock market capitalization, PISA

math test score, and social contributions rate (proxy for welfare state). Con�rming the �nd-

15

ings of Jappelli (2010), our results point to the importance of a country's institutional context

when discussing cross-country di�erences in �nancial literacy. However, while Jappelli (2010)

based his analysis on a subset of individuals (working in management), our analysis is based

on representative samples of individuals. That allows us to show that the importance of

institutions is di�erent for individuals with di�erent levels of �nancial literacy. Those with

lower �nancial literacy are generally not engaged with more complex �nancial products such

as stocks and have less need to make sophisticated �nancial decisions. For them, �nancial

decisions are instead related to taking loans and making basic day-to-day decisions. Other

individuals with higher �nancial literacy might more likely hold substantial amounts of their

wealth in more complex �nancial products. Targeted policies might di�er for these two groups.

It is important to emphasize that the country-level results obtained from the decomposition

analysis and consequent linking to di�erent economic environments do not necessarily imply

causality. Despite having this caveat in mind, our results o�er interesting policy implications.

Besides investing in individual-level factors important for human capital development (e.g.

education, basic training in �nance) it seems that there is room for harmonizing the economic

and institutional environment across countries to decrease inequality in �nancial literacy.

We conclude that taking di�erences in population characteristics into account when com-

paring �nancial literacy across countries is important. If this is not done, it is di�cult to

draw useful policy conclusions, as it is impossible to disentangle di�erences based on country-

speci�c variation from those based on variation in individual-level characteristics. Country

rankings such as those presented in the OECD/INFE report are not very meaningful with re-

gard to policy conclusions if di�erences stemming from basic individual characteristics cannot

be identi�ed.

16

References

Atkinson, Adele and Flore-Anne Messy, �Assessing �nancial literacy in 12 countries:

an OECD/INFE international pilot exercise,� Journal of Pension Economics and Finance,

2011, 10 (04), 657�665.

Badarinza, Cristian, John Y Campbell, and Tarun Ramadorai, �International com-

parative household �nance,� Annual Review of Economics, 2016, 8, 111�144.

Blinder, Alan S, �Wage discrimination: reduced form and structural estimates,� Journal of

Human Resources, 1973, 8 (4), 436�455.

Bover, Olympia, Martin Schürz, Jiri Slacalek, and Federica Teppa, �Eurosystem

Household Finance and Consumption Survey: Main Results on Assets, Debt, and Saving,�

International Journal of Central Banking, 2016, 12 (2), 1�13.

Campbell, John Y, �Household �nance,� The Journal of Finance, 2006, 61 (4), 1553�1604.

Christelis, Dimitris, Dimitris Georgarakos, and Michael Haliassos, �Di�erences in

portfolios across countries: Economic environment versus household characteristics,� Review

of Economics and Statistics, 2013, 95 (1), 220�236.

Ciaian, Pavel and Ján Pokriv£ák, �Why Some Sectors of Transition Economies are less

Reformed than Others? The Case of Research and Education,� Technical Report, EERI

Research Paper Series 2005.

Fernandes, Daniel, John G Lynch Jr, and Richard G Netemeyer, �Financial literacy,

�nancial education, and downstream �nancial behaviors,� Management Science, 2014, 60

(8), 1861�1883.

Firpo, Sergio, Nicole M. Fortin, and Thomas Lemieux, �Decomposing Wage Distribu-

tions using Recentered In�uence Function Regressions,� 2007.

, , and , �Unconditional quantile regressions,� Econometrica, 2009, 77 (3), 953�973.

Fonseca, Raquel, Kathleen J Mullen, Gema Zamarro, and Julie Zissimopoulos,

�What explains the gender gap in �nancial literacy? The role of household decision making,�

Journal of Consumer A�airs, 2012, 46 (1), 90�106.

Fortin, N., T. Lemieux, and S. Firpo, �Decomposition methods in economics,� Handbook

of Labor Economics, 2011, 4, 1�102.

Hastings, Justine S, Brigitte C Madrian, and William L Skimmyhorn, �Financial

Literacy, Financial Education, and Economic Outcomes,� Annual Review of Economics,

2013, 5 (1), 347�73.

17

Jappelli, Tullio, �Economic literacy: An international comparison,� The Economic Journal,

2010, 120 (548), F429�F451.

Lusardi, Annamaria and Olivia S Mitchell, �Financial literacy around the world: an

overview,� Journal of Pension Economics and Finance, 2011, 10 (04), 497�508.

and , �The economic importance of �nancial literacy: Theory and evidence,� Journal of

Economic Literature, 2014, 52 (1), 5�44.

Machado, José AF and José Mata, �Counterfactual decomposition of changes in wage

distributions using quantile regression,� Journal of Applied Econometrics, 2005, 20 (4),

445�465.

Mathä, Thomas Y, Alessandro Porpiglia, and Michael Ziegelmeyer, �Household

wealth in the euro area: The importance of intergenerational transfers, homeownership and

house price dynamics,� Journal of Housing Economics, 2017, 35, 1�12.

Oaxaca, Ronald, �Male-female wage di�erentials in urban labor markets,� International

Economic Review, 1973, 14 (3), 693�709.

OECD, �Results: Students and Money: Financial Literacy Skills for the 21st Century (Volume

VI), PISA,� 2013.

, OECD/INFE International Survey of Adult Financial Literacy Competencies, Organisation

for Economic Co-operation and Development, 2016.

Standard and Poor's, �Global Financial Literacy Survey,� 2014.

18

6 Figures and tables

Figure 1: Distribution of �nancial literacy score across countries

(a) Austria

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(b) Brazil

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(c) Canada

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(d) Croatia

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(e) Finland

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(f) Germany

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(g) Hong Kong

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(h) Hungary

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(i) Jordan

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(j) The Netherlands

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(k) Russia

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

(l) UK

0.1

.2.3

.4F

ract

ion

0 1 2 3 4 5 6 7

Source: OECD/INFE international survey of adult �nancial literacy competencies

19

Figure 2: Estimated coe�cient e�ects from the mean B-O decomposition versus selectedmacroeconomic indicators (baseline)

(a) Internet

AT

BR

CA

HR

FIDE

HK

HU

JO

NL

RU UK

-.5

0.5

1C

oeffi

cien

t effe

cts

55 65 75 85 95Internet users (% of the total pop.)

linear fit

(b) Life expectancy

AT

BR

CA

HR

FIDE

HK

HU

JO

NL

RU UK

-.5

0.5

1C

oeffi

cien

t effe

cts

70 75 80 85Life expectancy (years)

linear fit

(c) Math in PISA

AT

BR

CA

HR

FIDE

HK

HU

JO

NL

RUUK

-.5

0.5

1C

oeffi

cien

t effe

cts

375 425 475 525 575Math score in PISA

linear fit

(d) Welfare state

AT

BR

CA

HR

FIDE

HU

JO

NL

RUUK

0.2

.4.6

.81

Coe

ffici

ent e

ffect

s

0 20 40 60Social contributions (% of revenue)

linear fit

Note: Austria (AT), Brazil (BR), Canada (CA), Croatia (HR), Finland (FI), Germany (DE), Hong Kong (HK),Hungary (HU), Jordan (JO), The Netherlands (NL), Russia (RU), the United Kingdom (UK).Source: OECD/INFE international survey of adult �nancial literacy competencies, World Bank data

20

Table 1: Survey details

Country Institution Date of survey Type of survey Sampling method Sample size

AustriaOesterreichische National-bank

2014 Face-to-face Strati�ed sampling 1,994

Brazil Banco Central do Brasil 2015 Face-to-face Strati�ed cluster sampling 2,002

CanadaFinancial ConsumerAgency of Canada

2015 Telephone interviewsNested quotas using ran-dom digit dialing

1,002

CroatiaCroatian National Bankand Croatian FinancialServices Agency

2015 Face-to-face Strati�ed sampling 1,049

FinlandUniversity of Tampere andUniversity of Vaasa

2014 Face-to-face Strati�ed cluster sampling 1,533

Germany Deutsche Bundesbank 2016 Telephone interviews Strati�ed sampling 1,001

Hong Kong Investor Education Center 2015 Face-to-face Strati�ed sampling 1,000

Hungary Magyar Nemzeti Bank 2015 Face-to-faceQuota sample from strat-i�ed probability startingpoint

1,000

Jordan INJAZ 2016 Face-to-face Strati�ed sampling 1,140

The Netherlands Money Wise 2015 Online interviews N.A. 1,018

RussiaMinistry of Finance of theRussian Federation

2015 Face-to-face Strati�ed sampling 1,649

UK Money Advice Service 201530% telephone, 70% onlineinterviews

Strati�ed random sampling 1,000

15,388

Source: OECD/INFE international survey of adult �nancial literacy competencies

21

Table 2: Description of variables used in empirical analysis

Variable Description

Financial literacy scoreNumber of correctly answered �nancial literacy questions (see AppendixA for details); score ranging from 0 to 7

Income bu�erDummy variable: 1 if an individual has a �nancial bu�er for at leastthree months in case he/she loses his/her job (a proxy for wellbeing)

Gender Dummy variable: 1 if female and 0 otherwise

Single Dummy variable: 1 if an individual lives alone and 0 otherwise

University educationDummy variable: 1 if university education is the highest attained doneand 0 otherwise

Age category (18-29) Dummy variable: 1 if an individual aged from 18 to 29 and 0 otherwise

Age category (30-49) Dummy variable: 1 if an individual aged from 30 to 49 and 0 otherwise

Age category (50-69) Dummy variable: 1 if an individual aged from 50 to 69 and 0 otherwise

Age category (70+) Dummy variable: 1 if an individual aged 70+ and 0 otherwise

EmployedDummy variable: 1 if paid employment (working for someone else) and0 otherwise

Self-employedDummy variable: 1 if self employed (working for him/herself) and 0otherwise

Retired Dummy variable: 1 if retired and 0 otherwise

Other, not-workingDummy variable: 1 if unemployed or not-working (e.g. apprentice, look-ing for work, looking after home, unable to work due to sickness, student)and 0 otherwise

Having budgetDummy variable: 1 if an individual is responsible for budget and has abudget and 0 otherwise

Active saverDummy variable: 1 if an individual actively saves in one of the followingschemes (cash at home, savings account, informal savings club, invest-ment products) and 0 otherwise

Holding risky �nancial assetsDummy variable: 1 if an individual holds shares or bonds in his/her�nancial portfolio and 0 otherwise

Financial planningDummy variable: 1 if an individual sets long-term �nancial goals and 0otherwise

Source: OECD/INFE international survey of adult �nancial literacy competencies

22

Table 3: Summary statistics of variables used in empirical analysis

Variable AT BR CA HR FI DE HK HU JO NL RU UK

Financial literacy Score 4.79 4.31 4.93 4.27 5.19 4.75 5.76 4.72 4.28 4.89 4.14 4.21(1.80) (1.55) (1.54) (1.67) (1.56) (1.95) (1.32) (1.62) (1.65) (2.06) (1.79) (1.86)

Basic socio-economic characteristicsIncome bu�er 0.52 0.27 0.69 0.32 0.57 0.69 0.68 0.32 0.26 0.57 0.24 0.58

(0.50) (0.45) (0.46) (0.47) (0.50) (0.46) (0.47) (0.47) (0.44) (0.50) (0.43) (0.49)

Gender 0.52 0.52 0.52 0.53 0.50 0.54 0.54 0.53 0.44 0.50 0.53 0.52(0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50) (0.50)

Single 0.34 0.09 0.18 0.17 0.30 0.22 0.06 0.16 0.09 0.21 0.16 0.23(0.47) (0.28) (0.38) (0.38) (0.46) (0.42) (0.24) (0.37) (0.29) (0.41) (0.36) (0.42)

University education 0.10 0.09 0.45 0.18 0.27 0.16 0.20 0.19 0.62 0.38 0.28 0.31(0.30) (0.29) (0.50) (0.38) (0.44) (0.37) (0.40) (0.39) (0.49) (0.49) (0.45) (0.46)

Age category (18-29) 0.21 0.26 0.19 0.20 0.24 0.18 0.19 0.20 0.47 0.18 0.24 0.18(0.41) (0.44) (0.39) (0.40) (0.43) (0.38) (0.39) (0.40) (0.50) (0.38) (0.43) (0.39)

Age category (30-49) 0.35 0.43 0.35 0.35 0.38 0.35 0.39 0.36 0.39 0.37 0.36 0.34(0.48) (0.49) (0.48) (0.48) (0.48) (0.48) (0.49) (0.48) (0.49) (0.48) (0.48) (0.47)

Age category (50-69) 0.29 0.27 0.38 0.33 0.30 0.32 0.34 0.33 0.13 0.37 0.36 0.34(0.45) (0.45) (0.48) (0.47) (0.46) (0.47) (0.48) (0.47) (0.34) (0.48) (0.48) (0.47)

Age category (70+) 0.15 0.04 0.09 0.12 0.09 0.15 0.07 0.10 0.01 0.08 0.03 0.14(0.36) (0.20) (0.28) (0.32) (0.28) (0.36) (0.26) (0.30) (0.09) (0.27) (0.17) (0.35)

Employed 0.49 0.30 0.50 0.42 0.40 0.47 0.56 0.51 0.38 0.46 0.61 0.52(0.50) (0.46) (0.50) (0.49) (0.49) (0.50) (0.50) (0.50) (0.49) (0.50) (0.49) (0.50)

Self-employed 0.07 0.33 0.10 0.07 0.06 0.08 0.04 0.05 0.13 0.07 0.08 0.07(0.25) (0.47) (0.30) (0.25) (0.24) (0.27) (0.19) (0.22) (0.34) (0.25) (0.27) (0.26)

Retired 0.28 0.12 0.20 0.26 0.25 0.27 0.13 0.25 0.04 0.17 0.19 0.24(0.45) (0.32) (0.40) (0.44) (0.43) (0.44) (0.34) (0.43) (0.18) (0.38) (0.39) (0.43)

Other, not-working 0.17 0.24 0.20 0.26 0.29 0.18 0.27 0.19 0.45 0.30 0.13 0.16(0.38) (0.43) (0.40) (0.44) (0.45) (0.39) (0.45) (0.39) (0.50) (0.46) (0.33) (0.37)

Additional variables capturing experienceHaving budget 0.28 0.36 0.58 0.63 0.61 0.32 0.55 0.24 0.48 0.39 0.47 0.51

(0.45) (0.48) (0.49) (0.48) (0.49) (0.47) (0.50) (0.43) (0.50) (0.49) (0.50) (0.50)

Active saver 0.68 0.30 0.79 0.63 0.61 0.67 0.73 0.27 0.71 0.71 0.55 0.72(0.47) (0.46) (0.40) (0.48) (0.49) (0.47) (0.44) (0.44) (0.45) (0.45) (0.50) (0.45)

Holding risky �nancial assets 0.12 0.01 0.46 0.13 0.30 0.29 0.38 0.05 0.14 0.09 0.02 0.37(0.33) (0.09) (0.50) (0.33) (0.46) (0.46) (0.48) (0.22) (0.34) (0.28) (0.14) (0.48)

Financial planning 0.63 0.45 0.58 0.45 0.74 0.59 0.58 0.43 0.61 0.39 0.47 0.45(0.48) (0.50) (0.49) (0.50) (0.44) (0.49) (0.49) (0.49) (0.49) (0.49) (0.50) (0.50)

Note: Summary statistics computed using survey weights except Jordan (JO) and Russia (RU), wheresurvey weights are not available. Standard deviations presented in parentheses.Source: OECD/INFE international survey of adult �nancial literacy competencies

23

Table 4: Selected country-level indicators relevant for �nancial literacy

CountryGDP per

capita (current$USD)

Internet users(% of thepopulation)

Lifeexpectancy(years)

Enrolmentratio, uppersecondary (%)

Stock markettotal value toGDP (%)

Socialcontributions(% of revenue)

Math score inthe PISAsurvey

Austria 43,665 83.93 81.84 95.75 7.33 32.33 497

Brazil 8,757 59.08 74.68 90.97 31.19 31.68 377

Canada 43,316 88.47 82.14 119.30 77.59 23.70 516

Croatia 11,580 69.80 77.28 97.66 1.25 35.32 464

Finland 42,405 92.65 81.39 115.23 56.61 33.67 511

Germany 41,177 87.59 81.09 106.68 38.25 54.61 506

Hong Kong 42,351 84.95 84.28 113.22 478.70 N.A. 548

Hungary 12,366 72.83 75.96 102.67 10.00 30.10 477

Jordan 4,096 53.40 74.20 77.88 10.73 0.27 380

The Netherlands 44,293 93.10 81.70 124.47 54.45 36.69 512

Russia 9,329 70.10 70.91 98.77 20.26 21.00 494

UK 43,930 92.00 81.60 83.20 103.06 21.23 492

Source: World Bank indicators; OECD PISA data

24

Table 5: Distribution of �nancial literacy score across selected socio-economic characteristics(by country)

AT BR CA HR FI DE HK HU JO NL RU UK

Overall 4.8 4.3 4.9 4.3 5.2 4.8 5.8 4.7 4.3 4.9 4.1 4.2

GenderMale 5.1 4.4 5.4 4.3 5.4 5.3 6.0 4.8 4.7 5.5 4.2 4.6

Female 4.5 4.2 4.5 4.2 4.9 4.3 5.6 4.6 3.8 4.3 4.1 3.8

EducationPrimary 3.8 3.9 3.8 3.9 N.A. 4.1 4.6 4.3 3.4 4.0 3.4 3.1

Secondary 4.9 4.5 4.6 4.3 5.0 5.0 5.9 4.7 3.9 4.5 4.1 4.0

Tertiary 5.6 5.2 5.4 4.8 5.8 5.7 6.1 5.4 4.6 5.6 4.5 5.0

Age category18-29 years 4.6 4.4 4.5 4.1 5.0 4.4 5.5 4.7 3.5 4.3 3.8 3.7

30-49 years 4.8 4.4 5.0 4.4 5.4 4.7 5.9 4.8 4.1 4.9 4.2 4.6

50-69 years 5.0 4.2 5.1 4.4 5.2 5.0 5.8 4.7 4.6 5.2 4.3 4.4

70+ years 4.6 4.1 4.7 3.7 4.9 4.5 5.2 4.5 4.7 5.0 4.2 3.4

Employment statusEmployed 4.9 4.6 5.0 4.4 5.4 5.1 6.0 4.8 4.8 5.1 4.3 4.5

Self-employed 5.1 4.3 5.4 4.6 5.6 5.6 5.7 5.2 4.8 5.6 4.2 4.6

Retired 4.8 4.0 5.1 4.0 4.9 4.7 5.4 4.4 4.6 5.2 3.8 3.9

Other not working 4.3 4.2 4.3 4.2 5.2 4.1 5.5 4.8 3.8 4.5 4.0 3.5

Note: Means are presented based on the sample of adult individuals aged 18-79. Weighted �gures exceptJordan (JO) and Russia (RU), where survey weights are not available.Source: OECD/INFE international survey of adult �nancial literacy competencies

25

Table 6: Baseline OLS estimates of determinants of �nancial literacy

(1) (2)

Income bu�er 0.621∗∗∗ 0.439∗∗∗

(0.030) (0.031)Gender -0.429∗∗∗ -0.452∗∗∗

(0.029) (0.028)Single -0.078∗∗ -0.131∗∗∗

(0.039) (0.039)University education 0.543∗∗∗ 0.655∗∗∗

(0.031) (0.033)Age category (18-29) -0.148∗∗ -0.015

(0.074) (0.074)Age category (30-49) 0.067 0.135∗

(0.070) (0.069)Age category (50-69) 0.247∗∗∗ 0.288∗∗∗

(0.061) (0.059)Employed 0.217∗∗∗ 0.239∗∗∗

(0.042) (0.041)Self-employed 0.088 0.188∗∗∗

(0.055) (0.056)Retired -0.048 0.023

(0.059) (0.058)Constant 4.507∗∗∗ 4.878∗∗∗

(0.079) (0.089)

Country �xed e�ects No Yes

Adjusted R2 0.099 0.144Observations 12,298 12,298

Note: Robust standard errors presented in parentheses. Dummy variables for Age category (70+), Not-working, and Finland are the baseline categories for the respective dummy sets. ∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗

p < 0.01.Source: OECD/INFE international survey of adult �nancial literacy competencies

26

Table 7: Blinder-Oaxaca decomposition at mean (baseline)

AT BR CA HR DE HK HU JO NL RU UK

I. Di�erentialBenchmark (Finland) 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗ 5.270∗∗∗

(0.042) (0.042) (0.042) (0.042) (0.042) (0.042) (0.042) (0.042) (0.042) (0.042) (0.042)

Compared country 4.968∗∗∗ 4.510∗∗∗ 4.978∗∗∗ 4.371∗∗∗ 5.247∗∗∗ 5.778∗∗∗ 4.764∗∗∗ 4.483∗∗∗ 5.309∗∗∗ 4.430∗∗∗ 4.602∗∗∗

(0.040) (0.045) (0.044) (0.052) (0.053) (0.040) (0.050) (0.048) (0.055) (0.054) (0.054)

Di�erence (raw) 0.302∗∗∗ 0.759∗∗∗ 0.292∗∗∗ 0.899∗∗∗ 0.023 -0.509∗∗∗ 0.506∗∗∗ 0.787∗∗∗ -0.040 0.839∗∗∗ 0.667∗∗∗

(0.058) (0.061) (0.061) (0.067) (0.067) (0.058) (0.065) (0.064) (0.069) (0.068) (0.068)

Di�erence (%) 5.9% 15.5% 5.7% 18.6% 0.5% -9.2% 10.1% 16.1% -0.7% 17.3% 13.5

II. DecompositionExplained 0.179∗∗∗ 0.115∗∗ -0.207∗∗∗ 0.161∗∗∗ -0.036 -0.066 0.175∗∗∗ -0.289∗∗∗ -0.167∗∗∗ 0.094∗∗ -0.091∗∗∗

(0.032) (0.048) (0.037) (0.035) (0.035) (0.046) (0.042) (0.066) (0.050) (0.048) (0.033)

Unexplained 0.123∗ 0.644∗∗∗ 0.499∗∗∗ 0.738∗∗∗ 0.059 -0.443∗∗∗ 0.331∗∗∗ 1.076∗∗∗ 0.127 0.745∗∗∗ 0.758∗∗∗

(0.068) (0.080) (0.069) (0.078) (0.075) (0.074) (0.080) (0.091) (0.084) (0.085) (0.075)

Note: Only basic socio-economic characteristics (i.e. income bu�er, gender, age, education, and working status) used as explanatory variables in theunderlying regressions. Robust standard errors presented in parentheses. ∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01.Source: OECD/INFE international survey of adult �nancial literacy competencies

27

Table 8: RIF Blinder-Oaxaca quantile decomposition (baseline)

AT BR CA HR DE HK HU JO NL RU UK

RIF B-O decomposition for 10th percentileI. Di�erentialBenchmark (Finland) 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗ 3.407∗∗∗

(0.054) (0.054) (0.054) (0.054) (0.054) (0.054) (0.054) (0.054) (0.054) (0.054) (0.054)

Compared country 2.644∗∗∗ 2.438∗∗∗ 3.308∗∗∗ 2.508∗∗∗ 3.124∗∗∗ 4.203∗∗∗ 2.811∗∗∗ 2.696∗∗∗ 2.837∗∗∗ 2.344∗∗∗ 2.356∗∗∗

(0.062) (0.037) (0.049) (0.067) (0.092) (0.075) (0.070) (0.048) (0.124) (0.058) (0.091)

Di�erence (raw) 0.763∗∗∗ 0.969∗∗∗ 0.099 0.899∗∗∗ 0.283∗∗∗ -0.796∗∗∗ 0.595∗∗∗ 0.711∗∗∗ 0.570∗∗∗ 1.063∗∗∗ 1.051∗∗∗

(0.082) (0.066) (0.074) (0.086) (0.107) (0.093) (0.089) (0.072) (0.135) (0.080) (0.106)

Di�erence (%) 25.2% 33.2% 2.9% 30.4% 8.7% -20.9% 19.2% 20.3% 18.3% 37.0% 36.5%

II. DecompositionExplained 0.075∗ 0.093∗ -0.098∗∗ 0.084∗∗ -0.054 -0.052 0.103∗∗ -0.022 -0.109∗ 0.141∗∗ -0.030

(0.040) (0.052) (0.046) (0.042) (0.044) (0.058) (0.050) (0.086) (0.065) (0.060) (0.041)

Unexplained 0.688∗∗∗ 0.877∗∗∗ 0.197∗∗ 0.815∗∗∗ 0.337∗∗∗ -0.744∗∗∗ 0.492∗∗∗ 0.733∗∗∗ 0.679∗∗∗ 0.922∗∗∗ 1.081∗∗∗

(0.097) (0.091) (0.079) (0.102) (0.113) (0.107) (0.109) (0.111) (0.145) (0.109) (0.112)

RIF B-O decomposition for 50th percentileI. Di�erentialBenchmark (Finland) 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗ 6.035∗∗∗

(0.045) (0.045) (0.045) (0.045) (0.045) (0.045) (0.045) (0.045) (0.045) (0.045) (0.045)

Compared country 5.520∗∗∗ 4.840∗∗∗ 5.425∗∗∗ 4.782∗∗∗ 6.100∗∗∗ 6.422∗∗∗ 5.343∗∗∗ 4.825∗∗∗ 6.333∗∗∗ 4.999∗∗∗ 5.317∗∗∗

(0.031) (0.041) (0.055) (0.064) (0.078) (0.035) (0.052) (0.051) (0.074) (0.067) (0.084)

Di�erence (raw) 0.515∗∗∗ 1.195∗∗∗ 0.610∗∗∗ 1.253∗∗∗ -0.065 -0.387∗∗∗ 0.692∗∗∗ 1.210∗∗∗ -0.298∗∗∗ 1.036∗∗∗ 0.718∗∗∗

(0.054) (0.061) (0.071) (0.079) (0.090) (0.057) (0.069) (0.068) (0.087) (0.081) (0.095)

Di�erence (%) 8.9% 22.0% 10.6% 23.2% -1.1% -6.2% 12.2% 22.3% -4.8% 18.8% 12.6%

II. DecompositionExplained 0.172∗∗∗ 0.097∗ -0.175∗∗∗ 0.138∗∗∗ 0.003 -0.039 0.154∗∗∗ -0.337∗∗∗ -0.144∗∗∗ 0.045 -0.078∗∗

(0.035) (0.053) (0.038) (0.038) (0.037) (0.048) (0.044) (0.070) (0.051) (0.051) (0.034)

Unexplained 0.343∗∗∗ 1.097∗∗∗ 0.785∗∗∗ 1.114∗∗∗ -0.068 -0.348∗∗∗ 0.538∗∗∗ 1.547∗∗∗ -0.154 0.991∗∗∗ 0.796∗∗∗

(0.066) (0.082) (0.079) (0.088) (0.097) (0.074) (0.083) (0.096) (0.101) (0.095) (0.101)

RIF B-O decomposition for 90th percentileI. Di�erentialBenchmark (Finland) 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗ 7.486∗∗∗

(0.039) (0.039) (0.039) (0.039) (0.039) (0.039) (0.039) (0.039) (0.039) (0.039) (0.039)

Compared country 7.393∗∗∗ 6.825∗∗∗ 7.447∗∗∗ 7.038∗∗∗ 7.731∗∗∗ 7.549∗∗∗ 7.249∗∗∗ 6.883∗∗∗ 7.889∗∗∗ 7.050∗∗∗ 7.452∗∗∗

(0.036) (0.061) (0.050) (0.088) (0.049) (0.031) (0.065) (0.076) (0.050) (0.081) (0.073)

Di�erence (raw) 0.093∗ 0.660∗∗∗ 0.038 0.448∗∗∗ -0.245∗∗∗ -0.063 0.237∗∗∗ 0.602∗∗∗ -0.403∗∗∗ 0.435∗∗∗ 0.033(0.053) (0.072) (0.064) (0.097) (0.062) (0.050) (0.076) (0.086) (0.064) (0.090) (0.083)

Di�erence (%) 1.3% 9.2% 0.5% 6.2% -3.2% -0.8% 3.2% 8.4% -5.2% 6.0% 0.5%

II. DecompositionExplained 0.176∗∗∗ 0.063 -0.158∗∗∗ 0.116∗∗∗ 0.012 -0.048 0.131∗∗∗ -0.323∗∗∗ -0.118∗∗ 0.019 -0.065∗∗

(0.033) (0.047) (0.036) (0.034) (0.033) (0.043) (0.040) (0.060) (0.047) (0.044) (0.032)

Unexplained -0.083 0.598∗∗∗ 0.197∗∗∗ 0.332∗∗∗ -0.257∗∗∗ -0.015 0.106 0.926∗∗∗ -0.285∗∗∗ 0.416∗∗∗ 0.099(0.060) (0.086) (0.076) (0.101) (0.071) (0.067) (0.085) (0.107) (0.081) (0.100) (0.090)

Note: Only basic socio-economic characteristics (i.e. income bu�er, gender, age, education, and working status) used as explanatory variables in theunderlying regressions. Robust standard errors presented in parentheses. ∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗ p < 0.01.Source: OECD/INFE international survey of adult �nancial literacy competencies

28

Table 9: Which institutions matter the most? (baseline)

Mean 10th percentile 90th percentileIndicator Standardized e�ect Rank Standardized e�ect Rank Standardized e�ect Rank

GDP per capita -0.289∗∗ 6 -0.222 5 -0.288∗∗∗ 4Gross enrolment ratio -0.293∗∗∗ 5 -0.292∗ 3 -0.233∗∗ 6Internet users -0.297∗∗∗ 4 -0.200 6 -0.338∗∗∗ 2Life expectancy -0.514∗∗ 1 -0.489∗ 1 -0.440∗∗ 1Math score in PISA -0.301∗∗∗ 3 -0.273∗ 4 -0.283∗∗∗ 5Social contributions rate -0.301∗∗∗ 2 -0.121∗ 7 -0.307∗∗∗ 3Stock market capitalization -0.247∗∗∗ 7 -0.368∗∗∗ 2 -0.078 7

Note: Country-level regressions of the unexplained parts of the gap (coe�cient e�ects) estimated from themean and quantile decomposition analysis on a set of aggregate indicators (one by one) which have beenstandardized (i.e. values demeaned and divided by their standard deviations). ∗ p < 0.10, ∗∗ p < 0.05, ∗∗∗

p < 0.01.Source: OECD/INFE international survey of adult �nancial literacy competencies; World Bank data

29

Appendix

A Financial literacy questions in the OECD/INFE survey

Below we provide the list of �nancial literacy knowledge questions (KQ) asked in the OECD/INFE

survey on �nancial literacy of adult individuals that were used for the calculation of the overall

�nancial knowledge score. For sake of space-saving, answer options such as �Don't know� or

�Refused to answer� are omitted.

� KQ1 Time-value of money: Imagine that �ve brothers are given a gift of EUR 1,000

and have to share the money equally. The brothers have to wait for one year to get their

share of the EUR 1,000 and in�ation stays at 2%. In one year's time, will they be able

to buy (a) more with their share of the money than they could today, (b) as much as

today, or (c) less than they could buy today? (correct answer: c)

� KQ2 Interest paid on a loan: You lend EUR 25 to a friend one evening and he gives

you EUR 25 back the next day. How much interest has he paid on this loan? (correct

answer: 0)

� KQ3 Interest plus principal: Suppose you put EUR 100 into a no-fee savings account

with a guaranteed interest rate of 2% per year. You do not make any further payments

into this account and you do not withdraw any money. How much would be in the

account at the end of the �rst year, once the interest payment is made? (correct answer:

102 EUR)

� KQ4 Compound interest: And how much would be in the account at the end of �ve

years? (a) More than EUR 110, (b) exactly EUR 110, (c) less than EUR 110, (d) It is

impossible to tell from the information given. (correct answer: a)

� KQ5 Risk and return: Is the following statement (a) true or (b) false? An investment

with a high return is likely to be high risk. (correct answer: a)

� KQ6 De�nition of in�ation: Is the following statement (a) true or (b) false? High

in�ation means that the cost of living is increasing rapidly. (correct answer: a)

� KQ7 Diversi�cation: Is the following statement (a) true or (b) false? It is usually

possible to reduce the risk of investing in the stock market by buying a wide range of

stocks and shares. (correct answer: a)

30

B The importance of experience for �nancial literacy

As a robustness check, we extend our multivariate and decomposition analysis by considering

a set of variables capturing experience with �nance (see Table 2, for exact de�nition). The in-

clusion of these endogenous variables to better explain �nancial literacy gaps across countries

is justi�ed by the prior literature studying the reverse causality between �nancial knowledge

and �nancial outcomes of households and individuals (e.g. Fernandes et al., 2014).

B.1 Production function

The results on experience variables (presented in Table B.1) are remarkable in two dimensions.

First, with regard to having a budget. This dummy variable indicates whether an individual

is responsible for the budget, if the household has a budget at all and is used by the OECD in

their so called ��nancial behavior� score. However, it interestingly relates to marginally lower

�nancial literacy. This could be for two reasons. Either low-income, low-educated households

have a higher probability of having a budget as they have more need to do so. If so, it might

not be a good indicator for using it in a ��nancial behavior� score as it only captures a selection

issue and is a proxy for tight �nances. Or the less �nancially literate person in a household

typically is responsible for the households budget. That would be worrisome as it would lead

to less e�cient budgeting. In both cases it questions the de�nition and use in the OECD's

��nancial behavior score� in this combination of two variables, a household having a budget

and a person being responsible for that budget. Second all other experience variables are asso-

ciated with higher �nancial literacy. In particular, holding risky �nancial assets and �nancial

planning also have economically signi�cant e�ects of about 0.2 (�nancial planning) and 0.3

to 0.4 (holding risky assets). Of course these coe�cients should not be interpreted as causal

e�ects but rather as predictive e�ects or conditional correlations. We consider it likely that

individuals learn before and while they are dealing with certain �nancial products how to deal

with such products and thereby increase their �nancial knowledge which is partly covered by

our observed �nancial literacy scores.

31

Table B.1: OLS estimates of determinants of �nancial literacy (robustness check)

(1) (2) (3) (4)

Income bu�er 0.621∗∗∗ 0.439∗∗∗ 0.473∗∗∗ 0.306∗∗∗

(0.030) (0.031) (0.033) (0.034)Gender -0.429∗∗∗ -0.452∗∗∗ -0.387∗∗∗ -0.419∗∗∗

(0.029) (0.028) (0.030) (0.029)Single -0.078∗∗ -0.131∗∗∗ -0.023 -0.094∗∗

(0.039) (0.039) (0.040) (0.040)University education 0.543∗∗∗ 0.655∗∗∗ 0.452∗∗∗ 0.568∗∗∗

(0.031) (0.033) (0.032) (0.033)Age category (18-29) -0.148∗∗ -0.015 -0.236∗∗∗ -0.056

(0.074) (0.074) (0.077) (0.076)Age category (30-49) 0.067 0.135∗ -0.059 0.044

(0.070) (0.069) (0.073) (0.072)Age category (50-69) 0.247∗∗∗ 0.288∗∗∗ 0.092 0.156∗∗

(0.061) (0.059) (0.063) (0.062)Employed 0.217∗∗∗ 0.239∗∗∗ 0.133∗∗∗ 0.142∗∗∗